meeting the co challenge - automotivebusiness.com.br · © pa knowledge limited | confidential...

TRANSCRIPT

1© PA Knowledge Limited | Confidential between PA and intended recipient

MEETING THE CO2

CHALLENGEIMPLICATIONS FOR THE AUTOMOTIVE INDUSTRY

Discussion paper

PA CONSULTING GROUP

JUNE 2018

2© PA Knowledge Limited | Confidential between PA and intended recipient

2017 2025

Pri

ori

ty

Today

low

hig

h

PRIORITY OF CURRENT MEGATRENDS IN THE AUTOMOTIVE INDUSTRY AND CHANGE IN NUMBERS GLOBALLY*

THE STRATEGIC

PRIORITISATION OF THE

MEGATRENDS TAKES PLACE

IN THOSE MAIN AREAS:

▪ Resources & invest

▪ Return

▪ Time-to-Impact

THE FOLLOWING

DEVELOPMENT CAN BE

OBSERVED:

▪ Autonomous driving after

the first hype phase now

rising sharply again and

dominating in the future

▪ CO2 reduction with

increasing relevance by

tightening targets and

impending driving bans

▪ Mobility platforms currently

stagnating and in a

consolidation phase from

2020

▪ Connectivity is evolving

along ever shorter release

cycles

IMPLICATIONS

1

12

0.001

EVs, annually

L3 vehicles, annually

Connectivity

New Mobility &

Platforms

CO2 Reduction &

EVs

Autonomous

Driving

CO2 TARGET ACHIEVEMENTTOP items in the automotive agenda

1

2017 2025

15-30

8

20252017

35-40

30

2017 2025

400-600

*in million vehicles; Source: Citibank 2017, IHS Global Insight 2017, Statistica 2017, Frost & Sullivan 2016, Autofacts 2017, PA analysis 2017

2015 2020 2025

Car Sharing user

Connected vehicles, total

3© PA Knowledge Limited | Confidential between PA and intended recipient

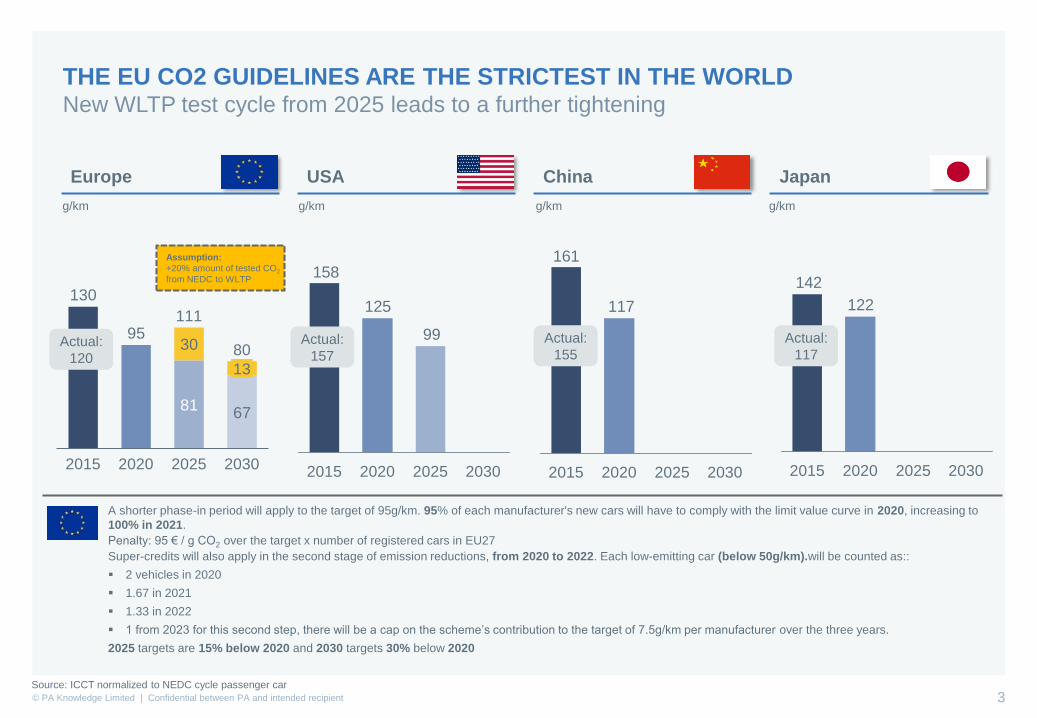

THE EU CO2 GUIDELINES ARE THE STRICTEST IN THE WORLDNew WLTP test cycle from 2025 leads to a further tightening

Europe USA China Japan

130

95

8167

30

2015 2020 2025

13

2030

111

8099

125

158

2015 2020 2025 2030

117

161

20202015 2025 2030

122

142

20202015 20302025

Assumption:

+20% amount of tested CO2

from NEDC to WLTP

A shorter phase-in period will apply to the target of 95g/km. 95% of each manufacturer's new cars will have to comply with the limit value curve in 2020, increasing to

100% in 2021.

Penalty: 95 € / g CO2 over the target x number of registered cars in EU27

Super-credits will also apply in the second stage of emission reductions, from 2020 to 2022. Each low-emitting car (below 50g/km).will be counted as::

▪ 2 vehicles in 2020

▪ 1.67 in 2021

▪ 1.33 in 2022

▪ 1 from 2023 for this second step, there will be a cap on the scheme’s contribution to the target of 7.5g/km per manufacturer over the three years.

2025 targets are 15% below 2020 and 2030 targets 30% below 2020

g/km g/km g/km g/km

Source: ICCT normalized to NEDC cycle passenger car

Actual:

155

Actual:

117Actual:

157Actual:

120

4© PA Knowledge Limited | Confidential between PA and intended recipient

THREATENING DRIVING BANS AND GOVERNMENT INCENTIVES

Pressure for action for car makers continues to grow

India 2030

China “in the near future”

California 2040

from 2030

from 2025

from 2040

from 2040

Government incentives

for BEVs & HEVs

in

discussion

Planned driving bans for combustion engines

?

Source: PA Research

Subsid

ies

at

purc

hase

Vehic

le tax

reduction

VA

T

Reduction

Fin

ancia

l

incentives

Oth

er

incentives

(lik

e fre

e

park

ing, use o

f

bus lanes)

Austria x x x x x

Belgium x x x

Denmark x x

Finland x x

France x x x x

Germany x x x x

Greece x x

Ireland x x x x x

Italy x

Netherlands x x

Norway x x x x

Portugal x x x x

Spain x x x x

Sweden x x x

Switzerland x x

United

Kingdomx x x x

5© PA Knowledge Limited | Confidential between PA and intended recipient

-

-

-

-

200

290

570

1,200

500

455

1,300

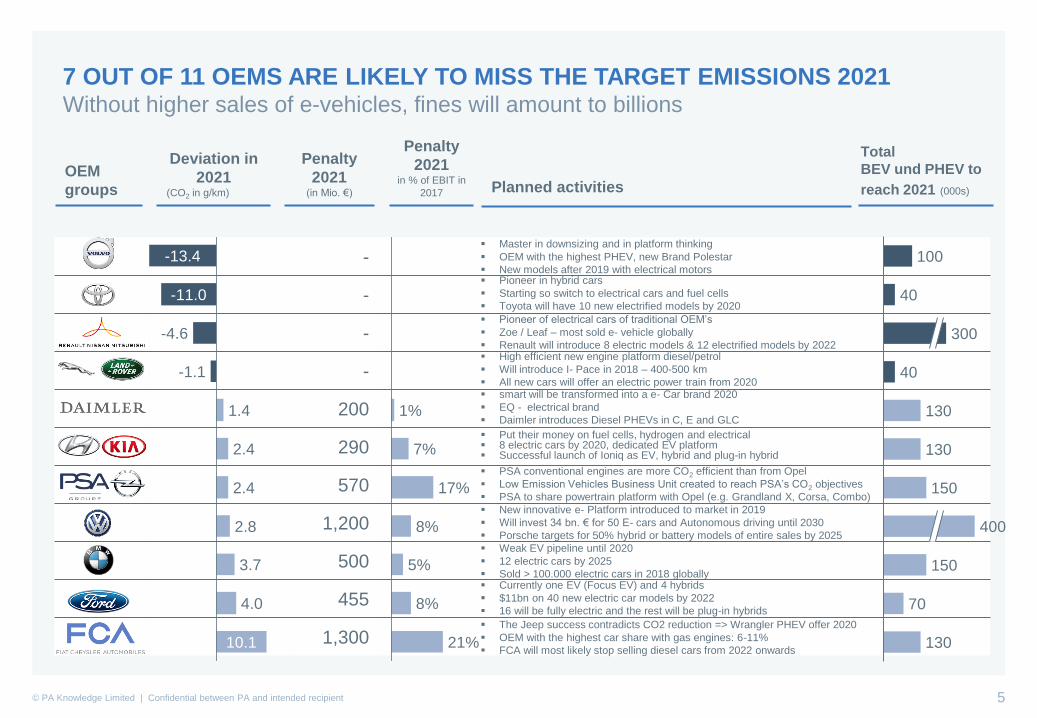

7 OUT OF 11 OEMS ARE LIKELY TO MISS THE TARGET EMISSIONS 2021 Without higher sales of e-vehicles, fines will amount to billions

Deviation in

2021(CO2 in g/km)

Penalty

2021(in Mio. €) Planned activities

Total

BEV und PHEV to

reach 2021 (000s)

OEM

groups

-11.0

-13.4

10.1

-1.1

-4.6

2.4

2.4

1.4

2.8

3.7

4.0

▪ Master in downsizing and in platform thinking

▪ OEM with the highest PHEV, new Brand Polestar

▪ New models after 2019 with electrical motors▪ Pioneer in hybrid cars

▪ Starting so switch to electrical cars and fuel cells

▪ Toyota will have 10 new electrified models by 2020

▪ Pioneer of electrical cars of traditional OEM’s

▪ Zoe / Leaf – most sold e- vehicle globally

▪ Renault will introduce 8 electric models & 12 electrified models by 2022▪ High efficient new engine platform diesel/petrol

▪ Will introduce I- Pace in 2018 – 400-500 km

▪ All new cars will offer an electric power train from 2020▪ smart will be transformed into a e- Car brand 2020

▪ EQ - electrical brand

▪ Daimler introduces Diesel PHEVs in C, E and GLC

▪ Put their money on fuel cells, hydrogen and electrical▪ 8 electric cars by 2020, dedicated EV platform▪ Successful launch of Ioniq as EV, hybrid and plug-in hybrid

▪ PSA conventional engines are more CO2 efficient than from Opel

▪ Low Emission Vehicles Business Unit created to reach PSA’s CO2 objectives

▪ PSA to share powertrain platform with Opel (e.g. Grandland X, Corsa, Combo)

▪ New innovative e- Platform introduced to market in 2019

▪ Will invest 34 bn. € for 50 E- cars and Autonomous driving until 2030

▪ Porsche targets for 50% hybrid or battery models of entire sales by 2025

▪ Weak EV pipeline until 2020

▪ 12 electric cars by 2025

▪ Sold > 100.000 electric cars in 2018 globally▪ Currently one EV (Focus EV) and 4 hybrids

▪ $11bn on 40 new electric car models by 2022

▪ 16 will be fully electric and the rest will be plug-in hybrids

▪ The Jeep success contradicts CO2 reduction => Wrangler PHEV offer 2020

▪ OEM with the highest car share with gas engines: 6-11%

▪ FCA will most likely stop selling diesel cars from 2022 onwards

100

40

40

130

130

150

150

70

130

300

400

Penalty

2021in % of EBIT in

2017

1%

21%

8%

5%

7%

17%

8%

6© PA Knowledge Limited | Confidential between PA and intended recipient

FUTURE MOBILITY

PERFORMANCE SCORE

SIX KEY FACTORS

FOR CAR MAKERS'

E-MOBILITY SUCCESS

PA CONSULTING

JUNE 2018

7© PA Knowledge Limited | Confidential between PA and intended recipient

PA‘S FUTURE MOBILITY PERFORMANCE SCORE FOR TOP 13 GLOBAL CAR MAKERS

SIX KEY FACTORS INDICATE CAR MAKER’S POTENTIAL TO SUCCEED IN E-MOBILITY

1. Technology & Strategy

▪ Model portfolio & technology

roadmap

▪ E-Branding

▪ Organisational strategy & set-up

PA’s Future Mobility Performance Score

Future MobilityPerformanceScore

6. Financial

Performance

1. Technology & Strategy

2. Battery Technology

3. Culture &

Incentives

4. Supplier

Network

5. Ecosystem

& Partners

30%

20%

10%15%

10%

15%

Key success factors

2. Battery Technology

▪ Cost position & scalability

▪ Technology maturity

▪ Value creation strategy

3. Culture & Incentives

▪ Culture & leadership

▪ Incentive system & motivation

▪ New working models (e.g. agile)

4. Supplier Network

▪ Value chain integration

▪ Make or buy

▪ Raw material supply & recycling

5. Ecosystem & Partners

▪ Charging technology & stations

▪ 3rd party services

▪ Technology standards &

interfaces

6. Financial Performance

▪ EBIT performance (E-Mobility

investment indication)

xx% weightingfactor

8© PA Knowledge Limited | Confidential between PA and intended recipient

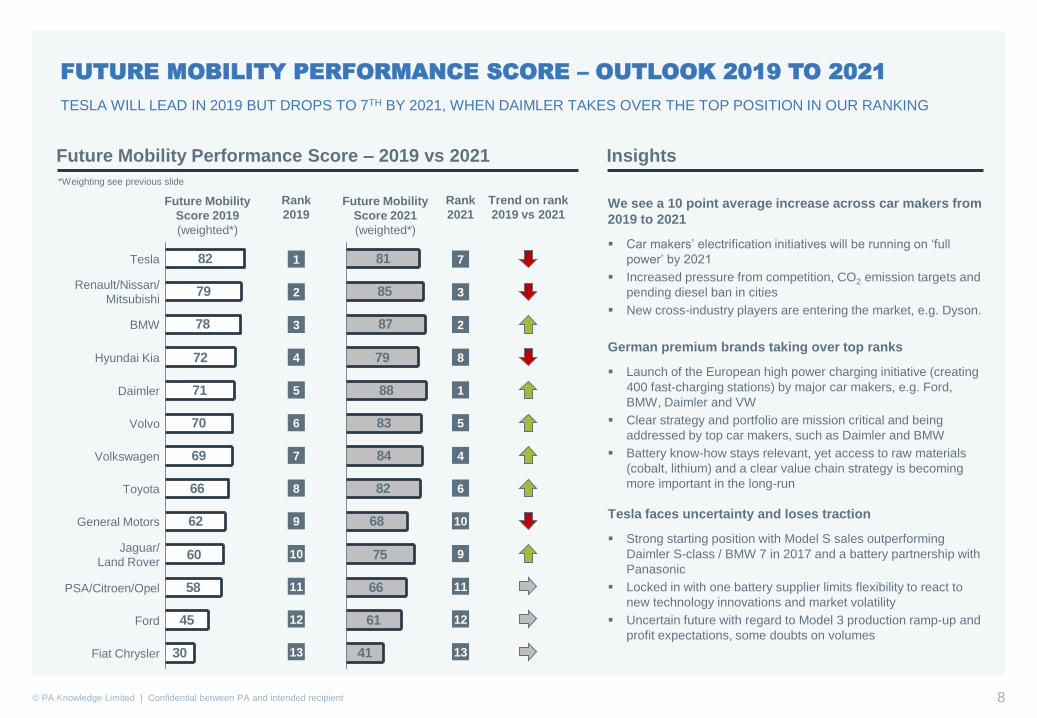

FUTURE MOBILITY PERFORMANCE SCORE – OUTLOOK 2019 TO 2021

TESLA WILL LEAD IN 2019 BUT DROPS TO 7TH BY 2021, WHEN DAIMLER TAKES OVER THE TOP POSITION IN OUR RANKING

82

79

78

72

71

70

69

66

62

60

58

45

30

BMW

General Motors

Fiat Chrysler

Renault/Nissan/

Mitsubishi

Daimler

Tesla

Jaguar/

Land Rover

Toyota

Volvo

Volkswagen

Ford

Hyundai Kia

PSA/Citroen/Opel

Future Mobility Performance Score – 2019 vs 2021

1

2

3

4

5

6

7

10

8

9

11

12

13

Rank

2019

Insights

Future Mobility

Score 2019

(weighted*)

81

85

87

79

88

83

84

82

68

75

66

61

41

Future Mobility

Score 2021

(weighted*)

7

3

2

8

1

5

4

9

6

10

11

12

13

Rank

2021

Trend on rank

2019 vs 2021We see a 10 point average increase across car makers from

2019 to 2021

▪ Car makers’ electrification initiatives will be running on ‘full

power’ by 2021

▪ Increased pressure from competition, CO2 emission targets and

pending diesel ban in cities

▪ New cross-industry players are entering the market, e.g. Dyson.

German premium brands taking over top ranks

▪ Launch of the European high power charging initiative (creating

400 fast-charging stations) by major car makers, e.g. Ford,

BMW, Daimler and VW

▪ Clear strategy and portfolio are mission critical and being

addressed by top car makers, such as Daimler and BMW

▪ Battery know-how stays relevant, yet access to raw materials

(cobalt, lithium) and a clear value chain strategy is becoming

more important in the long-run

Tesla faces uncertainty and loses traction

▪ Strong starting position with Model S sales outperforming

Daimler S-class / BMW 7 in 2017 and a battery partnership with

Panasonic

▪ Locked in with one battery supplier limits flexibility to react to

new technology innovations and market volatility

▪ Uncertain future with regard to Model 3 production ramp-up and

profit expectations, some doubts on volumes

*Weighting see previous slide

9© PA Knowledge Limited | Confidential between PA and intended recipient

FUTURE MOBILITY PERFORMANCE SCORE – SPOTLIGHT ON GERMAN CAR MAKERS

INCREASE IS DRIVEN BY A RAMP-UP AND EXTENSION OF PRODUCT PORTFOLIOS

Future Mobility Score & key success factors 2019 vs 2021 Insights

7887

20212019

95

80

7093

93

90

Technology & Strategy

Battery Technology Supplier Network Financial Performance

Culture & Incentives Ecosystem & Partners

50

65100

87

90

80

71

88

2019 2021

93

83

95

80

93

80

69

84

2019 2021

80

90

8376

80

8765

7070

80

50

67

BMW

Daimler

VW

6390

75

8060

73

▪ Strong starting point with highest total sales of EVs and

PHEVs globally (more than 100,000) and gradual

broadening of product portfolio. However, no major

innovations until iNext in 2021.

(13 PHEV/BEV models by 2018, 12 EV models by 2025)

▪ Increased focus on the EV ecosystem through a service

portfolio and charging station installation

(e.g. car sharing, European charging initiative)

▪ Strongest raw material strategy

▪ Industry leader in profit and productivity

▪ Internal alignment and commitment to EV (CASE Business

Unit, Factory 56, Brand EQ, agile development)

▪ Full-scale electrification of all Smarts by 2020

▪ Increased focus on the EV ecosystem through a service

portfolio and charging station installation – similar to BMW

▪ Limited robustness of raw material strategy

▪ Fast acceleration and huge volume potential across multiple

brands

▪ Gradual ramp-up with 48 volt mild hybrid, 14 PHEV/BEV models

(2018) and e-platform (2019)

▪ Initial plans for in-house battery production (focus on modules

with potential for cell production), raw material strategy yet to

evolve further – need to rethink

▪ Potential investment in ECU development and production

▪ Strong board level commitment for e-mobility

▪ Sales incentives models yet to be improved

Late starter

Long-term

strategist

Joint, smart &

agile driver

10© PA Knowledge Limited | Confidential between PA and intended recipient

FUTURE MOBILITY PERFORMANCE SCORE – SPOTLIGHT ON TESLA, HYUNDAI KIA

E-MOBILITY INDEX INCREASE IS DRIVEN BY A RAMP-UP AND EXTENSION OF PRODUCT PORTFOLIOS

Insights

8182

20212019

93

90

70

95

1585

Financial Performance

Ecosystem & Partners

Supplier Network

Culture & Incentives

Battery Technology

Technology & Strategy

90

65

090 95

95

Tesla

▪ Tesla is 4 years ahead of the competition in terms of

powertrain development and is catching up on the remaining

car development

▪ Tesla is working on too many projects and business units

(cars, Hyperloop, SpaceX, Solar City,…) => focus

▪ Globalisation into China and Europe requires lots of

management attention and experience

▪ Trumps tariff policy is not in favour of Telsa’s expansion e.g.

China

▪ Tesla is suffering from a severe brain drain, lot of key

management people are leaving the firm due to the culture

▪ Tesla is a great and cool brand, but will struggle to recruit

potential automotive experts because of stable stock price

▪ Auto Industry benchmark: Appr. 6 weeks until full production

from SOP and then stable production while Tesla needed 1

full year as a minimum, and still not being stable

▪ Tesla will be profitable (Source Reuters) either at Tesla or a

new owner

Industry

Shaper

75

65

50

90

40 80

9370

49

73

80

90

Hyundai Kia

Fast follower

7972

20212019

▪ Very strong pipeline and positive platform approach to share

Hybrid, PHEV and BEV technology and models

▪ Culture and incentives does not support a very agile and high

performance culture in Europe

▪ Management of battery suppliers to be revisited; high degree

dependency on LG Chen and SK Innovation

▪ Ionic battery at lower range than E-Golf, high TCO cost

compared to peers, Kia Soul EV long charging time without

wallbox – range is impacted by heating system

▪ No visible raw material access strategy in place

▪ A limited ECO System – partnering model to be improved

▪ Financial performance in last quartile compared to peers

Future Mobility Score & key success factors 2019 vs 2021

11© PA Knowledge Limited | Confidential between PA and intended recipient

Levers

ProductDevelop the right offers fast

CustomersInspire customers & increase

sales

Supply chainRealize efficient products and

services for the customer

External

factorsDefine incentives for additional

sales

Typical questions CO2 target 2021

▪ What must the future brand / model / engine portfolio look like?

▪ Which R & D competencies will be decisive in the future?

▪ Which partnerships bring additional speed?

▪ How can the development process be more agile and development cycles be

shortened?

▪ How can the multichannel approach be optimally used?

▪ How can the customer experience of e-mobility be improved significantly?

▪ What is the optimal pricing strategy?

▪ What sales approaches and competences are required for sales of e-mobility

products?

▪ How can new drive technologies be integrated into existing plant footprint?

▪ Which competences are required in the future for the supply chain?

▪ What can strategic suppliers and partners contribute?

▪ How can the procurement of specific raw materials be ensured?

▪ Which activities support the expansion of e-mobility infrastructure?

▪ How can standardisation and the introduction of technical standards be

advanced?

▪ How can acceptance and sales be further enhanced with government and

industry cooperation?

1

99.1

CO2

Target 2021

CO2 Footprint

VW 2021

96.3

-3%

-2.8 g/km

2

3

4

Example: Volkswagen AG

CO2 TARGETS CAN BE REACHED BY 4 LEVERSSpeed and reorientation in product development and supply chain as well as increased

sales through customer focus and influencing external factors

12© PA Knowledge Limited | Confidential between PA and intended recipient

SCOPE FOR ACTIONAcross the 16 brands in Europe, 267,000 employees are redundant of which 141,000 need

to be retrained

-69,400

4,300

-51,900

39,100

-37,400

-7,100

8,000 11,600

-5,700

13,10029,000

-38,100

-57,300

35,700

116,200

220,800

21,100 20,600

75,800 83,100

293,400

Overview functions Sum

Positioning in Europe BMW, Daimler, VW, Audi,

Porsche, Volvo, Opel/PSA,

Renault, Nissan, JLR, SEAT,

SKODA, FCA, Ford,

Hyundai/Kia, Toyota

R&DSales &

After Sales ProductionPurchasing

Redundancy(Factory Realignment,

Department Realignment)

Requalification &

build up new

competencies

Topic

Sum

ca. 267,000

Sum

ca. 141,000

Sum

ca. 840,000

Engines Drive Vehicles

Inland

Vehicles

Abroad

Source: PA Research; Assumptions see Back-Up

13© PA Knowledge Limited | Confidential between PA and intended recipient

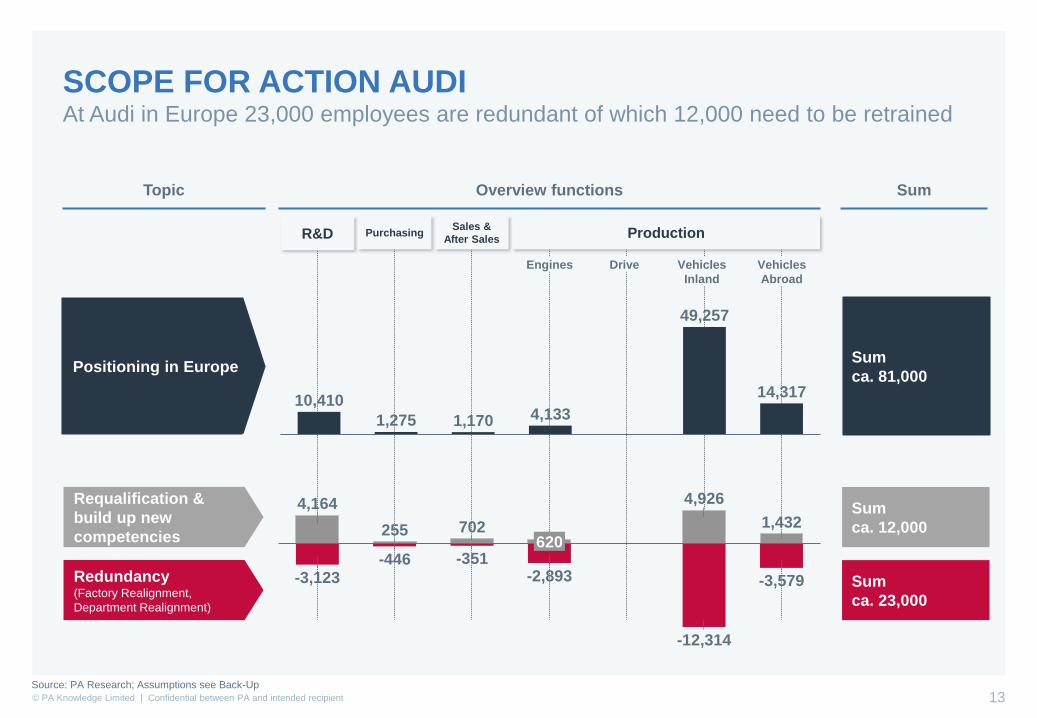

SCOPE FOR ACTION AUDIAt Audi in Europe 23,000 employees are redundant of which 12,000 need to be retrained

255 702

-446 -351620

-2,893

4,164

-3,123

4,926

-12,314

1,432

-3,579

10,410

1,1701,275 4,133

14,317

49,257

Positioning in Europe

Sum

ca. 23,000

Sum

ca. 12,000

Sum

ca. 81,000

Source: PA Research; Assumptions see Back-Up

Overview functions Sum

R&DSales &

After Sales ProductionPurchasing

Topic

Engines Drive Vehicles

Inland

Vehicles

Abroad

Redundancy(Factory Realignment,

Department Realignment)

Requalification &

build up new

competencies

14© PA Knowledge Limited | Confidential between PA and intended recipient

SCOPE FOR ACTION BMWAt BMW in Europe 21,000 employees are redundant of which 13,000 need to be retrained

450 780 480

-630 -325

-9,465

-3,300

5,2454,400

1,365

-6,435

-1,120

11,000

1,800

9,100

1,3004,800

38,100

Sum

ca. 21,000

Sum

ca. 13,000

Sum

ca. 66,000

Source: PA Research; Assumptions see Back-Up

Positioning in Europe

Overview functions Sum

R&DSales &

After Sales ProductionPurchasing

Topic

Engines Drive Vehicles

Inland

Vehicles

Abroad

Redundancy(Factory Realignment,

Department Realignment)

Requalification &

build up new

competencies

15© PA Knowledge Limited | Confidential between PA and intended recipient

SCOPE FOR ACTION DAIMLERAt Daimler AG in Europe 31,000 employees are redundant of which 17,000 need to be

retrained

300 780 470

-525 -390 -1,075

-8,250

6,520

-4,890

1,231

-4,155

4,725

-11,860

3,300

16,300

25,950

1,5004,300

1,3006,500

33,000

Sum

ca. 31,000

Sum

ca. 17,000

Sum

ca. 89,000

Source: PA Research; Assumptions see Back-Up

Positioning in Europe

Overview functions Sum

R&DSales &

After Sales ProductionPurchasing

Topic

Engines Drive Vehicles

Inland

Vehicles

Abroad

Redundancy(Factory Realignment,

Department Realignment)

Requalification &

build up new

competencies

16© PA Knowledge Limited | Confidential between PA and intended recipient

SCOPE FOR ACTION PORSCHEAt Porsche in Europe 9,000 employees are redundant of which 5,000 need to be retrained

140 200878

272

-210 -125-680

1,0502,000

-1,500

-4,095

-2,625

700 500

2,720

10,498

5,0005,850

Sum

ca. 9,000

Sum

ca. 5,000

Sum

ca. 25,000

Source: PA Research; Assumptions see Back-Up

Positioning in Europe

Overview functions Sum

R&DSales &

After Sales ProductionPurchasing

Topic

Engines Drive Vehicles

Inland

Vehicles

Abroad

Redundancy(Factory Realignment,

Department Realignment)

Requalification &

build up new

competencies

17© PA Knowledge Limited | Confidential between PA and intended recipient

SCOPE FOR ACTION VWAt VW in Europe 56,000 employees are redundant of which 30,000 need to be retrained

700

-750-4,241-4,500

-1,050

-16,681

6,0001,200 1,837

-8,573

5,147

12,647

-20,578

2,540

82,612

3,00015,000

33,700

3,50012,247 17,008

Sum

ca. 56,000

Sum

ca. 30,000

Sum

ca. 167,000

Source: PA Research; Assumptions see Back-Up

Positioning in Europe

Overview functions Sum

R&DSales &

After Sales ProductionPurchasing

Topic

Engines Drive Vehicles

Inland

Vehicles

Abroad

Redundancy(Factory Realignment,

Department Realignment)

Requalification &

build up new

competencies

18© PA Knowledge Limited | Confidential between PA and intended recipient

WALK THE TALK – E-MOBILITY TRANSFORMATION MATRIX5 ways and recommended actions for the 16 brands

CH

AN

GE

PR

ES

SU

RE

OF

TH

E O

RG

AN

IZA

TIO

N

MODEL PORTFOLIO &

PLANNING GAP

AUDI

Porsche

Ford

BMW

VW

RENAULT

VOLVO

JLR

FCA

Hyundai

Toyota

SKODA

Seat

Nissan

OPEL/PSADAIMLER

1

2

3

4

5

highlow

hig

hlo

w

Transform for Leading EdgeCar makers with ambitious electrification targets in a tight time frame currently with a

production footprint focussed to traditional drives

Way forward

Comprehensive transformation and creation of the necessary structures to cushion

redundancy and requalification needs

Maintain MomentumCar makers who are successful in the market with the first e-models and have

already built up competence and structures

Way forward

Realisation of time and knowledge advantage through know-how expansion and

scaling of today's platforms

Make or BreakCar makers whose current transformation is dominated by internal (merger) and

external drivers (Brexit)

Way forward

Linking clear electrification targets with rapid development of necessary electrification

structures and knowledge in the course of transformation

Platform AddictsCar makers whose electrification success largely depends on the transformation at

group level

Way forward

Create future-proof electrification strategy as well as group-wide connection of

structures and secure local resources

Big Sell OutCar makers who are threatened to lose their competitive position due to their

strategic orientation

Way forward

Create future-proof electrification strategy as well as group-wide connection of

structures and secure local resources

1

2

3

4

5

Source: PA Research; Assumptions see Back-Up

E-mobility Transformation Matrix

19© PA Knowledge Limited | Confidential between PA and intended recipient

DIMENSIONS: E-MOBILITY TRANSFORMATION MATRIXThe two dimensions of the E-mobility Transformation Matrix are based on a number of

selected factors

Model portfolio & planning gap

Model portfolio

&

Planning

6. Financial

Performance

1. Technology & Strategy

2. Battery Technology

3. Culture &

Incentives

4. Supplier

Network

5. Ecosystem

& Partners

30%

20%

10%15%

10%

15%

xx%weightingfactor

Change pressure of the organisation

Change pressure of the

organisation

10%10%

40%

30%

10%

1. Number of employees in

Europe

2.Redundancy

3. Requalification need

4. Avg. age ofemployees

5. Influence of unions

xx%weightingfactor

20© PA Knowledge Limited | Confidential between PA and intended recipient

ASSUMPTIONS: REDUNDANCY & REQUALIFICATION NEEDSThe two dimensions of the E-mobility Transformation Matrix are based on a number of

selected factors

Timing

Vehicles sold

Engine split /

Europe

Cost of oil

Price level / battery

Raw materials

CO2 legislation

▪ 2025-2030

▪ Increase max. 5-15%, depending

on the OEM during study scope

▪ 0-10% Diesel

▪ 30-40% BEV/PHEV

▪ 15-25% Hybrid / Mild Hybrid

▪ 3-5% CNG

▪ 20-30% petrol

▪ 1-3% fuel cell

▪ Price level / battery: from 2020 –

90-120 € / KWh (cell module,

system parts and supply chain)

▪ $60-90 / Barrel

▪ Price level 2018 after the high

increase (e.g. cobalt) at 70-100 € /

kg – assumption will be around

70-150 €/ kg during study scope

▪ Consistent until 2021; until 2025

further tightening to 81 g / km

currently in discussion (test cycle

NEDC, 67g / km in 2030)

21© PA Knowledge Limited | Confidential between PA and intended recipient

Michael Schweikl

An der Welle 3

60322 Frankfurt

+49 17155 728 42 (mobil)

YOUR CONTACT TO PA

Thomas Brand

An der Welle 3

60322 Frankfurt

+49 171 55 72 846 (mobil)