medium term debt trategy managggyement strategy period 1 period 2 period 3 period 4 period 5 overall...

TRANSCRIPT

MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGY

Maria A. OlivaSenior EconomistInternational Monetary Fundy

Note: A portion of this content appears as text within the course itself.

This training material is the property of the International Monetary Fund and is intended for use in IMF Institute for Capacity Development courses. Any reuse requires the permission of the IMF. The views expressed in this material are those of the course staff and do not necessarily represent those of the IMF or IMF policy.

Public debt managementPublic debt management

“Public debt management is the process of Public debt management is the process of establishing and implementing a strategy for managing debt to achieve the

t’ fi i i k t government’s financing, risk, cost objectives and other goals, such as developing the domestic debt market”developing the domestic debt market

Guidelines for Public Debt Management: IMF/World Bank, 2001

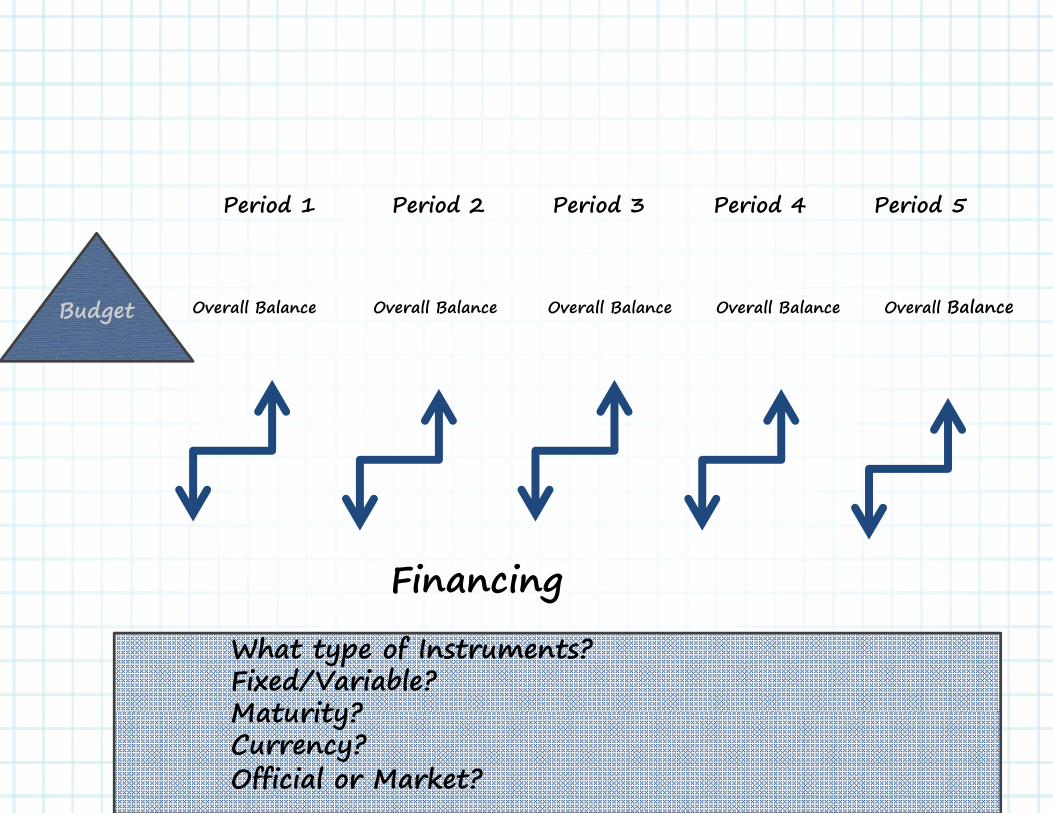

Debt Management Strategyg gy

Period 1 Period 2 Period 3 Period 4 Period 5

Overall Fiscal Overall Fiscal Overall Fiscal Overall Fiscal Overall Fiscal Overall Fiscal Overall Fiscal Overall Fiscal Overall Fiscal Overall Fiscal Balance Balance Balance Balance BalanceBudget

Financing

What type of Instruments?

Fixed/Variable? Maturity? Currency? yOfficial or Market?

• Sovereign debt management is distinct f om fiscal policy a d the DSA exe cise from fiscal policy and the DSA exercise

– Fiscal policy determines the level of public debt;

– Public debt management involves its i i i k i k

gcomposition, i.e. exposure to market risks

The Capacity to Fund the Debt Matters

2013 2014Algeria 9.8 10.2

Stock of Debt to GDP

Algeria 9.8 10.2Bahrain 35.4 39.5Djibouti 38.6 34.5Iraq 17 5 14 9

G7 2013 2014Stock of Debt to GDP

Iraq 17.5 14.9Jordan 83.8 87Kuwait 2.4 2.4

USA 106.0 107.3Japan 243.5 242.0EU 89.5 90.0

Lebanon 143.1 147.9Mauritania 98.5 83.1Qatar 33.2 30.2

Canada 87.1 85.6France 93.5 94.8Germany 80.4 78.1

Sudan 66.2 66Syria … …Tunisia 45 5 49 7

Italy 132.3 133.1UK 92.1 95.3

Tunisia 45.5 49.7West Bank & Gaza 21.7 20Yemen 48.1 50.1

Source: World Economic Outlook, http://www.imf.org/external/index.htm

Medium-term Debt Sustainability Framework (MTDS):

• Framework to design the characteristics of the sovereign debt portfolio taking into account a sovereign debt portfolio taking into account a medium-term/long-term objective.

• Framework to examine costs and risks d bl bassociated to possible borrowing strategies to

cover a financing need.

Why an Explicit Debt Management Why an Explicit Debt Management Strategy Framework??Because we need to understand

… cost-risk tradeoffs of our sovereign debt portfolio

h th iti f d bt tf li h l … how the composition of our debt portfolio can help minimize amplify the magnitude of external and domestic shocks

… how the macro affects borrowing

ff d d b… how monetary policy affects domestic debt issuance

… new risks and complexities affecting the debt portfoliop g p

The Framework: A 8 step approach

The Framework: A 8 step approachA 8-step approachA 8-step approach

Step1: Identify Objectives & Scope p fy j p

Step 2: Identify Costs & Risks of the Existing Debt

Step 3: Identify Potential Funding Sources

Step 4: Identify Baseline Projections & Risks _ fiscal, monetary & k tmarket

Step 5: Review Key Structural FactorsIF NeededIF Needed

Step 6: Identify Cost-Risk trade-offs for alternative debt management strategies

Step 7: Review Implications for macroeconomic policies and market IF NeededIF Needed

Step 8: Recommend MTDS for approval

MTDS ToolkitMTDS Toolkit

Guidance Note

Analytical tool provides generic template for quantitative analysis of costs and risks of q y f fborrowing strategies

The analytical tool is just one component of the framework.

DD MM SS DDEBTEBT MMANAGEMENTANAGEMENT SSTRATEGYTRATEGY: : TTHEHE TTOOLOOLKKITIT OOUTCOMESUTCOMES

3

Cost and Risk Indicators as of end-T0Cost a d Risk I dicators as of e d T0

Cost and Risk Indicators External debt Domestic debt Total debt

Nominal debt as % of GDP 10 4.6 14.6

Implied interest rate 1.9 3.6 2.4

Refinancing risk

ATM (years) 8.6 2.6 5.9

Debt maturing in 1yr (% of total) 4.3 75.5 36.7

ATR (years) 6.5 2.6 4.7

Debt refixing in 1yr (% of total) 30 75.5 50.7

Interest rate risk Fixed rate debt (% of total) 71.3 100 84.4

FX risk

FX debt (% of total debt) 54.5

ST FX debt (% of reserves) 7.4

R d ti P fil t TRedemption Profile at T0

Q tif i th Ch t i ti f th Quantifying the Characteristics of the Alternative Portfolios

Risk Indicators T0 As at end-T

Current S1 S2 S3 S4

N i l d b % f GDP 14 6 29 0 28 9 29 7 30 4Nominal debt as % of GDP 14.6 29.0 28.9 29.7 30.4

PV as % of GDP 12.8 21.0 24.6 24.8 31.2

Implied interest rate 2.3 2.4 2.5 3.9 5.4

Refinancing risk ATM External Portfolio (years) 12.4 18.3 14.0 17.7 16.8

ATM Domestic Portfolio (years) 4.3 3.0 3.0 2.0 3.5

ATM Total Portfolio (years) 9 7 15 8 12 2 11 7 9 8 ATM Total Portfolio (years) 9.7 15.8 12.2 11.7 9.8

Interest rate risk ATR (years) 9.6 15.6 11.6 11.6 9.7

Debt re-fixing in 1yr (% of total) 11.5 14.3 31.0 32.6 9.2

Fixed rate debt (% of total) 96.4 88.6 71.9 69.4 95.5

FX risk FX debt as % of total 66.8 83.2 83.2 61.7 46.9

ST FX debt as % of reserves 26 3 45 4 36 7 45 4 45 4 ST FX debt as % of reserves 26.3 45.4 36.7 45.4 45.4

Quantifying Refinancing Risks

Strategy 1 (S1): External borrowing accounts for 70 percent of new borrowing. Domestic b wi is stl sh t te

Strategy 2 (S2): Same external/domestic composition but less highly concessional and fixed rate loans.borrowing is mostly short-term.

800,000

1,000,000

Strategy 4

External Domestic

0

200,000

400,000

600,000

0

2017

2020

2023

2026

2029

2032

2035

2038

2041

2044

2047

2050

2053

2056

2059

2062

2065

Strategy 3 (S3): Domestic borrowing increases, especially the issuance of short-term instruments.

Strategy 4 (S4): Domestic borrowing increases, specially the issuance of 2- and 5-year fixed-rate instruments.

Quantifying Risk-Cost Trade-Offsy g

Debt/GDP (end-year T) Interest/GDP (end-year T)

PV of Public Debt to GDP Debt Service to GDPPV of Public Debt to GDP

35 37 39

Debt Service to GDP

1.2

1.4 S4

2325 27 29 31 33

Cost

(%) S4

S1

S2

0.8

1.0

1.2

Cost

(%)

S1

S2 S3

19 21 23

0.0 0.2 0.4 0.6 0.8 1.0Risk

S3

0.4

0.6

0.0 0.2 0.4 0.6 0.8 1.0Risk

h ld Y C l d ?What Would You Conclude?

• Cost-Risk trade offs vis-à-vis objectives

• The Structural Agenda

MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGYMMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGYSSTEPTEP 11

The Framework: A 8 step approach

The Framework: A 8 step approachA 8-step approachA 8-step approach

Step1: Identify Objectives & Scope Step1: Identify Objectives & Scope

KKEYEY IISSUESSSUES MMAINAIN MMESSAGESESSAGESMMAINAIN MMESSAGESESSAGES

OOBJECTIVESBJECTIVESClear about:

The main goal and intermediate goals Steps to reach the goal Steps to reach the goal.

SSCOPECOPE Choosing the “appropriate” definition of “government” matters.

f d b f l lTTHEHE CCURRENTURRENTDDEBTEBT PPORTFOLIOORTFOLIO

The characteristics of the current debt portfolio is legacy that conditions future decisions.

Medium MTDS:

Framework to design the characteristics of the sovereign debt portfolio taking into account a sovereign debt portfolio taking into account a medium-term/long-term objective.

Period 1 Period 2 Period 3 Period 4 Period 5Period 1 Period 2 Period 3 Period 4 Period 5

Overall Balance Overall Balance Overall Balance Overall Balance Overall BalanceB d t Overall Balance Overall Balance Overall Balance Overall Balance Overall BalanceBudget

Financing

What type of Instruments?Fixed/Variable? Maturity? Maturity? Currency? Official or Market?

OOBJECTIVESBJECTIVESOOBJECTIVESBJECTIVES

OBJECTIVE: GO FROM A TO E

CB “Go with h idCB the tides

and wind”

D

AA

EStart: Einitial portfolio

Final Note: plans are made subject to constraints Final destination: desired portfolio

p j(navigation skills, weather conditions and forecast, ship size, etc.)

TTHEHE SSTRATEGYTRATEGYPlan that provides direction and benchmarks for debt management

Government’s medium term goals

TTHEHE FFORMALORMAL

g

Standard goals: 1 tt i i i i k/ t OOBJECTIVEBJECTIVE 1.- attaining a given risk/cost level 2 - domestic debt market

24

2. domestic debt market development

SUBJECT TO: SUBJECT TO:

CCONSTRAINTSONSTRAINTSTTHEHE REALITYREALITY &

MT Macro-economic outlook

Stock of debt

Market development Market development

Market access

25

Legal and institutional framework

SSCOPECOPESSCOPECOPE

Liabilities: Financial claims to financial sector Non-fin Liabilities: Financial claims to financial sector, Non-fin private sector and to the rest of the world

MMARKETABLEARKETABLE DEBTDEBTOO

But …..

OOTHERSTHERSLLOANSOANS

What is the relevant coverage ? Is it feasible?

Central Government, General Government, Public Government, Public Enterprises?

Should contingencies be included? If so, which ones? How should these be valued?

Explicit/Implicit guarantees

Contingent liabilities Implicit contingencies

Financial Sector (SIFIs)Financial Sector (SIFIs)

Foreign exchange in fixed ERs

Explicit contingencies

ERs

SInFIs bail outs/SOEs

Credit guarantees Natural Disasters

A d the s State insurance schemes

Legal proceedings and

And others …

g p gdisputes

• And

Sub-national debt :

On lendingothers …

On lending

Implicit Contingent liability?

MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGY: : SSTEPTEP 22SSTEPTEP 22

The Framework: A 8 step approach

The Framework: A 8 step approachA 8-step approachA 8-step approach

Step1: Identify Objectives & Scope

Step 2: Identify Costs & Risks of the Existing DebtStep 2: Identify Costs & Risks of the Existing Debt

Period t-3 Period t-2 Period t-1 Period t…. Period t 3 Period t 2 Period t 1 Period t

BudgetOverall Fiscal Overall Fiscal Overall Fiscal Overall Fiscal Overall Fiscal

Balance Balance Balance Balance Balance

Debt OutstandingDomestic and External DebtDomestic and External Debt

The sovereign debt portfolio at time t is

1

NewDebtIssued t LegacyDebtt‐1 maturity t i*Debt t‐1 g y yPrimaryBalancet ContingentLiabilities t Valuationt

Analyzing the current portfolio implies using some matrix

800,000Baseline

600,000Domestic debt

400,000

External debt

0

200,000

0

2013

2016

2019

2022

2025

2028

2031

2034

2037

2040

2043

2046

2049

Financing of Debt:Financing of Debt:d bl ff lWhat Instruments? Fixed/Variable? Maturity? Currency? Official/

Market?

Cost characteristics

Risk characteristics:

Market riskMarket risk

Refinancing risk

External debt Domestic debt Total debtRisk Indicators External debt Domestic debt Total debtRisk IndicatorsAmount (in millions of USD)Nominal debt as % GDPNPV as % of GDPCost of debt Weighted Av. IR (%)

ATM (years)

NPV as % of GDP

Debt maturing in 1yr (% of total)ATR (years)Debt refixing in 1yr (% of total)

Refinancing risk

Fixed rate debt (% of total)FX debt (% of total debt)ST FX debt (% of reserves)FX risk

Interest rate risk

ST FX debt (% of reserves)FX risk

Debt Portfolio Debt Portfolio and

Cost Measures

Defining Cost:Defining Cost:

D bt t bj ti ll f th • Debt management objectives usually focus on the economic cost

– Measures that focus exclusively on prevailing accounting/budgetary practices may also be inadequate

• Cost can be measured in different ways– Accrual, due-for-payment, cash, p y ,– Nominal versus real value– Discounted cash-flows (Present Value) versus cash-flow measures

• Different cost measures provide different information on cost - do not rely on one cost measurecost do ot rely o o e cost easure

Cost indicators? Key indicatorsCost indicators? Key indicators

• Interest cost – key for budget preparation

• Interest / GDP– captures economic burden (liquidity)

• Debt / GDP and NPV of Debt / GDP also capture extent of debt burden – also “costs” (solvency)

• Annual interest payments + the potential impact of changes in exchange rates and other changes to the changes in exchange rates and other changes to the principal (e.g. inflation indexed debt)

D bt P tf li Debt Portfolio and

Risk Measures

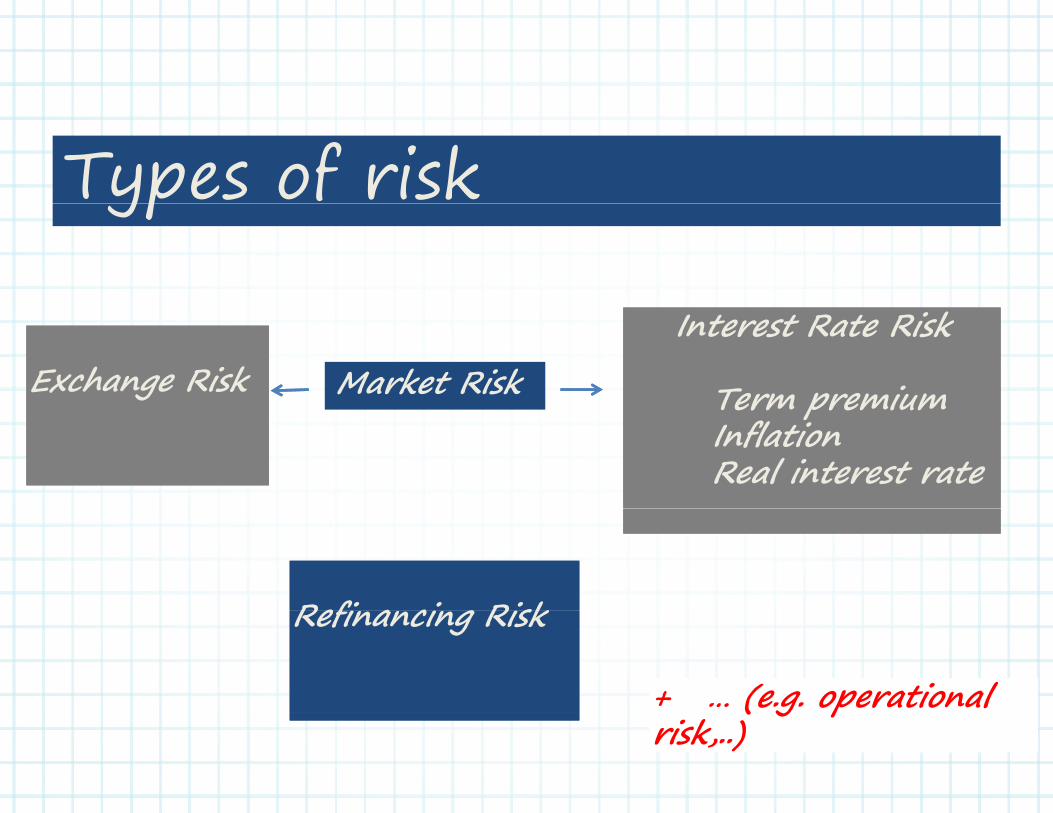

Types of riskyp

Exchange RiskExchange RiskInterest Rate Risk

Term premium

Interest Rate Risk

Term premiumMarket Risk Term premiumInflationReal interest rate

Term premiumInflationReal interest rate

Refi a ci g RiskRefi a ci g RiskRefinancing RiskRefinancing Risk

+ … (e.g. operational + … (e.g. operational ( g prisk,..)

( g prisk,..)

k i kMarket Risk

M k t i k i f ti fMarket risk is a function of

– Volatility of underlying factors (risk factors = interest and exchange rate volatility)

– Trends

Our main focus here is on downside risk

Interest rate riskInterest rate risk

Vulnerability of funding costs to higher interest rates when variable rates are reset and/or fixed rate debt needs to be refinanced

Typical measures of exposure– Fixed-Floating ratio

– Floating rate debt as a percentage of total debt

– Debt exposed to interest rate re-fixing within a specific time period • Maturing fixed rate debt to be rolled over• Maturing fixed rate debt to be rolled over• Variable rate debt (include interest rate swaps)

– Average Time to Re-fixing (ATR)

ATR = time weighted average until all principal payments in the debt portfolio become subject to a new interest rate

E h i kExchange rate risk The exposure of the portfolio to changes in the

exchange rate exchange rate

Typical measure of exposure

– Share of foreign currency debt in total debt• Can be split by specific currency (dollar risk Euro risk • Can be split by specific currency (dollar risk, Euro risk

etc.) – Currency composition

f f b– Degree of foreign currency liabilities mismatch relative to foreign currency reserves

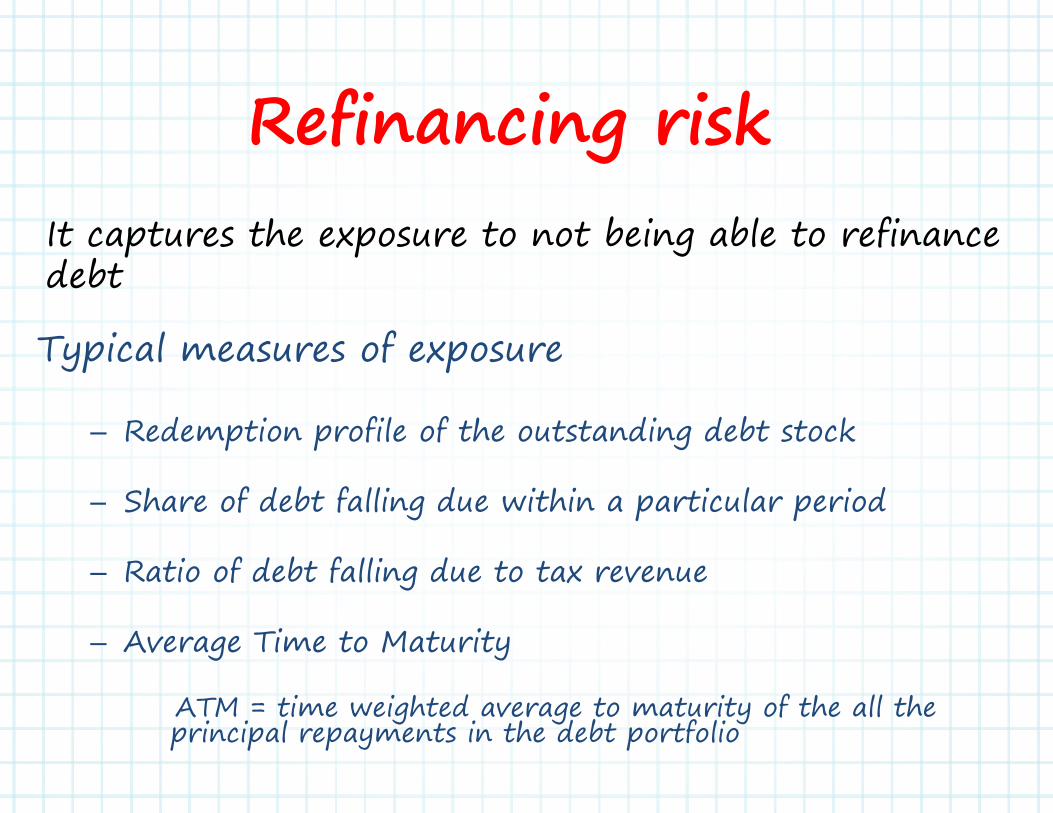

R fi i i kRefinancing riskIt captures the exposure to not being able to refinance debt

Typical measures of exposure

– Redemption profile of the outstanding debt stock

– Share of debt falling due within a particular periodShare of debt falling due within a particular period

– Ratio of debt falling due to tax revenue

– Average Time to Maturity

ATM = time weighted average to maturity of the all the ATM time weighted average to maturity of the all the principal repayments in the debt portfolio

What Can Mitigate Refinancing Risk?

Smooth debt profile Smooth debt profile

Offi i l s s s b ff f B P ds d t Official reserves as a buffer for BoP needs and to enhance confidence

bR/STD = reserves over short-term external debt

Broad creditor-base concentration

Macro-financial stability Macro-financial stability

E iExerciseLets compute the average time of maturity and refixing of the following portfolio

Principal Repayments T0 T0+1 T0+2 T0+3

Currency Indicator Type Code Years to maturity 1 2 3 4USD 1 Fix USD_1 255 100 55 60 40EUR 2 Fix EUR_2 85 40 30 10 5EUR 3 VAR EUR_3 137 25 12 80 20

Total 477 165 97 150 65

All figures are in USDg

An Indicator of Refinancing RiskAn Indicator of Refinancing RiskAverage Time to Maturity

Calculate average time to maturity

Time to maturity 1.0 2.0 3.0 4.0Principal repayments (fixed

rate only) $ 340=255+85 =100+40 =55+30 =60+10 =40+5 Principal repayments (variable

rate only) $ 137 =25+12+80+20 25 12 80 20

Total principal repayments $ 477= 340+137 165 97 150 65

0 34= 0 2= 0 31=0.34= 0.2= 0.31=

(100+40+25) / 477 (55+30+12) /477 (60+10+80) / 477

0.34= 0.41= 0.94= 0.54=

0.34*1 0.2*2 0.31*3 0.136*4

Weights of cash flow0.14= (40+5+20) /477

Weight * Time to maturity

Weighted average time to maturity (years)

2.24=

0.34+0.41+0.94+0.54

; Tt tP Pt= principal payments due

TD = total outstanding debt;0

tt TD

TD = total outstanding debtT = time to maturity

An Indicator of Interest RiskAn Indicator of Interest RiskAverage Time to Refixing Calculate average time to refixing

Time to refixing1 0 2 0 3 0 4 01.0 2.0 3.0 4.0

Principal repayments (fixed rate only) $=255+85 =100+40 =55+30 =60+10 =40+5

Principal repayments (variable rate only) $

=25+12+80+20 =25+12+80+2025 12 80 20 25 12 80 20

Total principal repayments $255+85+137 =100+40+25+12+80+20 =55+30 =60+10 =40+5

Weights of cash flow0.58=

(100+40+25+12+80+20) / 0.18= 0.146= 0.09= (40+5) / ( )(255+85+137) (55+30) / (255+85+137) (60+10) / (255+85+137)

( )(255+85+137)

Weight * Time to refixing0.58=[(100+40+25+12+80+20) /

(255+85+137)]*1

0356= [(55+30) /

(255+85+137)]*20.44 = [(60+10) / (255+85+137)]*3

0.38=[(40+5) / (255+85+137)]*4

= 1.75 Weighted average time to refixing (years)

[(100+40+25+12+80+20) / (255+85+137)]*1+[(55+30) / (255+85+137)]*2+[(60+10) / (255+85+137)]*3+[(40+5) / (255+85+137)]*4

MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGY: S: STEPTEP 33

The Framework: A 8 step approach

The Framework: A 8 step approachA 8-step approachA 8-step approach

Step1: Identify Objectives & Scope

Step 2: Identify Costs & Risks of the Existing Debt

Step 3: Potential sources of financingStep 3: Potential sources of financing

KKEYEY IISSUESSSUESKKEYEY IISSUESSSUESMMAINAIN MMESSAGESESSAGESMMAINAIN MMESSAGESESSAGES

OOPTIONSPTIONSAll types of loans carry some type of risk.IDA loans are very concessional (long maturity/low rates)

TT--SECURITIESSECURITIESNot only a source of financing but also a tool to create benchmarks

h i l h i b l h di i

benchmarks

CCOSTOST OFOF LOANSLOANSThe cost is not only the interest but also other conditions attached to them.

Potential Sources of Financing

Non-marketable

Concessional loansSemi-concessional loans Commercial loansOther non-marketable sources

MarketableMarketable

International bondi i i

51

Domestic securities

N k t bl D btNon-marketable DebtStructure Issues Cost Principal Risk

ExposureExposure

Fixed or

Size constraint; volatility and

speed of Very low cashOfficial sector loans

floating, amortizing, long-term

speed of disbursement;

may be conditions

h d

Very low cash cost; indirect

costs

FX – risk mitigated by LT

attached

Commercial Variable, bullet

Domestic,

Liquidity conditions; h lth f M k t b d

FX where l t llbank loans

,internationalShort-term

health of banking sector

(domestic)

Market based relevant; roll-over; refixing

Need efficient Uncertainty as toRetail debt Fixed or variable

Need efficient sales network.

Reliable source.

Can be competitive

Uncertainty as to quantum of

supply

Non-transparent;Other non-marketable Depends

Non transparent; hampers market

development

Cost born indirectly

Hidden costs; abuse

Marketable DebtStructure Issues Cost Principal Risk

ExposureSi l b

T-bills Discount, bullet

Simple; robust demand from banking sector

Low, except in liquidity crisis

Rollover and refinancing risk

D d

T-bondsFixed /

variable, bullet

Market development will impact demand

LT can be expensive (inflation

risk premium).

Depends on tenors achieved, may be some

rollover and refinancing Refixing ifbullet impact demand Deflation is costly. refinancing. Refixing if

variable rate.

Requires reliable index Can secure

Depends on link between inflation and

Inflation indexed

Indexation structure

index. Can secure maturity

extension. But complex

Depends on credibility of

monetary policy

between inflation and tax revenue and

likelihood of supply side shock. Reduces p

instrument. roll-over risk.

International Fixed / i bl

Large size, timing risk, Credit rating.

D d RER FX ll i kbond variable, bullet

g ,excess cash at

issuance

Depends on RER trend

FX, rollover risk

Concessional BorrowingConcessional Borrowing

L d Lenders:

Multilateral and bilateral official creditors Risk characteristicscreditors Risk characteristics

Interest rate exposure limited – typically long-term, fixed rate

Cost characteristics: Low cost –grant element 35% for multilateral rate

Exchange rate exposure –mitigated by amortizing structure

grant element 35% for multilateral

Factors that may influence the l bl structure

Rollover exposure – also mitigated by amortizing structure and nature of

amounts available

Income level Q lit f i tit ti structure, and nature of

creditor

Amount – often linked to an

Quality of institutions Access to market financingSize of multilateral balance sheet Amount often linked to an

allocation rulesheetEconomic developments

Example: Current IDA termsExample: Current IDA terms

h // ldb k /id /fi i h l55

http://www.worldbank.org/ida/financing.html

IMF Funding FacilitiesIMF Funding Facilities

IMF’s Stand By Arrangement(non-concessional)

The IMF’s Poverty Reduction and Growth Trust (concessional)

IMF loans: IMF loans: To help member countries tackle

b l f t bl balance of payments problems, stabilize their economies, and restore sustainable economic growth.

The global financial crisis

Crisis resolution role

Crisis prevention role Crisis prevention role

Detail on program conditions is publicly available:

http://www.imf.org/external/np/exr/facts/howlend.htm

Detail on program conditions is publicly available:

Semi-Concessional BorrowingSemi Concessional Borrowing

Lenders:

Multilateral and bilateral official creditors Risk characteristics:

In specific cases, these could be negotiated.Cost characteristics: at a discount to

market financing There could be Interest rate exposure - floating rate

Exchange rate exposure – mitigated by amortizing structure

market financing. There could be indirect cost [exchange rate; purchase conditions]

h i fl h by amortizing structure

Rollover exposure – similar to concessional

Factors that may influence the amounts available

F d ’ il bilit

Amount – can be linked to

Funds’ availabilityStrategic factors Economic developments

Amount can be linked to allocation rules

Commercial Bank LoansCommercial Bank Loans

Lenders:

Domestic and international banks Risk characteristics:D l

In specific cases, these could be negotiated.

Cost characteristics: At market rates (typically more expensive than

Interest rate exposure – often floating rate

Exchange rate exposure – depends

yp y pbonds, but cost of carry may be lower.)

Exchange rate exposure – depends

Rollover exposure – shorter maturityFactors that may influence the amounts available

Amount – Depends on allocated

Strategic factors Economic conditions Liquidity conditions p

credit lineLiquidity conditionsThese may be marketable –through syndication (fees increase).

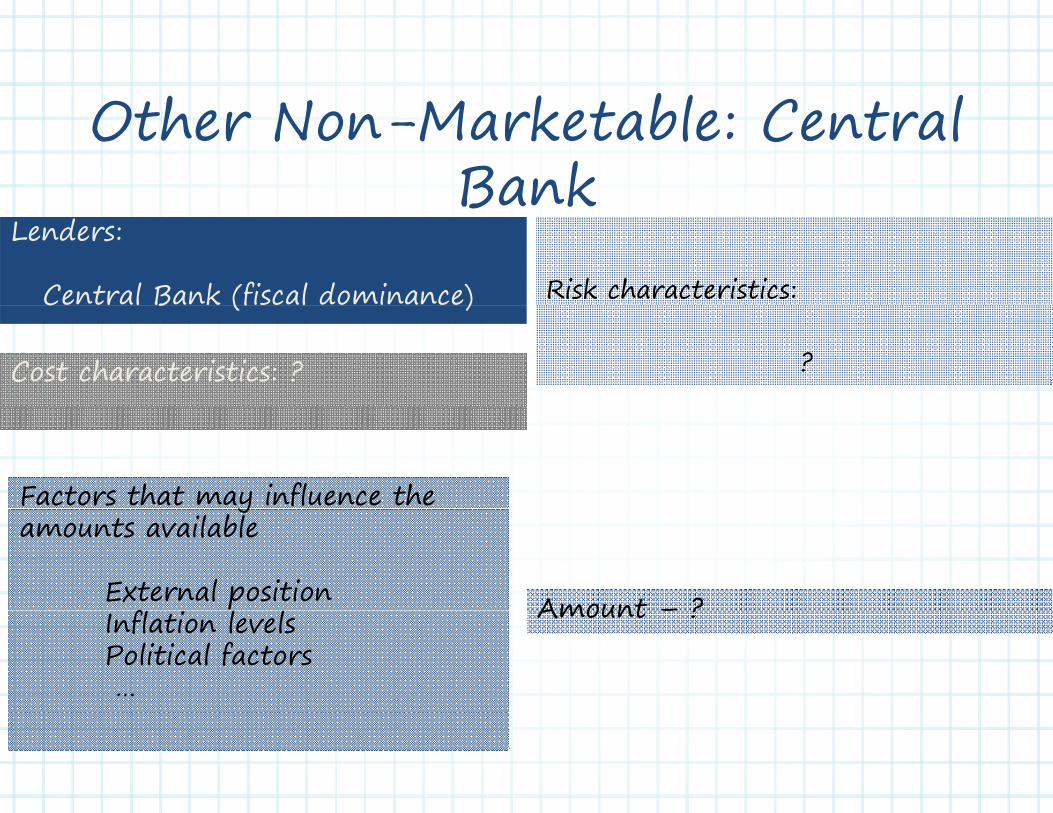

Oth N M k t bl C t l Other Non-Marketable: Central BankBank

Lenders:

Central Bank (fiscal dominance) Risk characteristics:C l B (f l )

?Cost characteristics: ?

Factors that may influence the

Amount – ?

yamounts available

External positionf Amount – ? Inflation levels

Political factors…

International Sovereign BondsInternational Sovereign Bonds

Lenders:

International and domestic institutional investors

Risk characteristics:

Rollover risk and exchange rate exposure aggravated by “bullet” investors p gg ystructure

Reflects nature of market demand

E d t “ dd t ” i

Cost characteristics:

k d i d Exposed to “sudden stops” in international capital markets

Tenors and interest rate structure ca be c stomi ed

Market determined. High transaction cost

can be customized

Possibly longer tenors than in the domestic market

Factors that may influence the amounts available

Helps diversify investor base

Amount – typically there is a

Established track record of good economic performancePositive medium-term outlookCredit rating Amount typically there is a

minimum (e.g. $200mn), maximum depends on market conditions

Credit ratingInvestors’ risk appetite/ global market conditions

Financing Environment – Debut Spreadsg p

53 500

Timeline of International Bond Issuance(in millions of US dollars)

3

4

5

2,500

3,000

3,500AfricaEastern EuropeLatin AmericaMiddle EastAsia# of issues (rhs)

1

2

3

1,000

1,500

2,000

0

1

0

500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 (Q3)Source: Dealogic and IMF staff calculations.

Maturity(in years and percent of total issuers)

5 year 6 year 7 year 10 year

42

50

44

50

4

Financing Environment – Debut Spreads

Financial Characteristics of First-time International Sovereign Issuances (2004- December 2013)

Issue size Spread at issue

8 25

Issue size (in US$ and percent of total issuers)

up to 200 mn. 201-499 mn.500-649 mn. 650-749 mn.

33

Spread at issue(in bps and percent of total issuers)

below 200 bps. 200-299 bps.300-399 bps. 400-499 bps.

58

8

50

17

33

17

Maturity(in years and percent of total issuers)

5 year 6 year7 year 10 year

Yields at issue(in bps and percent of total issuers)

Less 4% 4%-5%5.01%-6% 6.01%-7%

42

50

29

54

Source: Dealogic;and IMF staff calculations

44

17

54

Source: Dealogic; and IMF staff calculations.

Domestic Market

Domestic Securities: T-billsDomestic Securities: T bills

dLenders: Domestic (banks, pension, insurance and

mutual funds, etc) and international investors Risk characteristics

Interest rate risk: high

Rollover riskCost characteristics:

k d i dMarket determined.

Amount – ?Factors that may influence the amounts available Others:

Economic developmentsSize of banking sectorMarket development

Useful at early stages of market development

T l t t ti i Tools to meet reserve ratios, in payment systems, etc.

Often tool of monetary policy

Domestic Securities: T-bondsDomestic Securities: T bonds

Lenders: Domestic (banks, pension, insurance and

mutual funds, etc) and international investors

Types:

Fixed d fl ti te

Cost characteristics:

Fixed and floating rate bonds Zero coupon bondsIndexed bonds

Risk characteristicsMarket determined. They usually require a risk premium.

Interest rate risk –

Rollover risk –Factors that may influence the amounts available

Exchange rate exposure –

Amount – ?

Economic developmentsSize of banking sectorMarket development Amount ?Market development

MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGY MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGY: : SSTEPSTEPS 4&54&5

The Framework: A 8 step approach

The Framework: A 8 step approachA 8-step approachA 8-step approach

Step1: Identify Objectives & Scope

Step 2: Identify Costs & Risks of the Existing Debt

Step 3: Potential sources of financing

Step 4&5 : Identifying baseline projections and risks in key policy areas—fiscal, monetary, external sectors Step 4&5 : Identifying baseline projections and risks in key policy areas—fiscal, monetary, external sectors

To develop an explicit Debt Management StrategyManagement Strategy…

There is a need to understand

• … cost-risk tradeoffs of the debt… cost risk tradeoffs of the debt

• … how debt structures can dampen or amplify the it d f t l d d ti h kmagnitude of external and domestic shocks

• … how the macro affects borrowingg

• … how monetary control helps domestic debt issuance

• … constraints: institutional, market, …

• … new risks and complexities

The Economy

R l S t External Government Monetary Real Sector External Sector

Government Sector

Monetary Sector

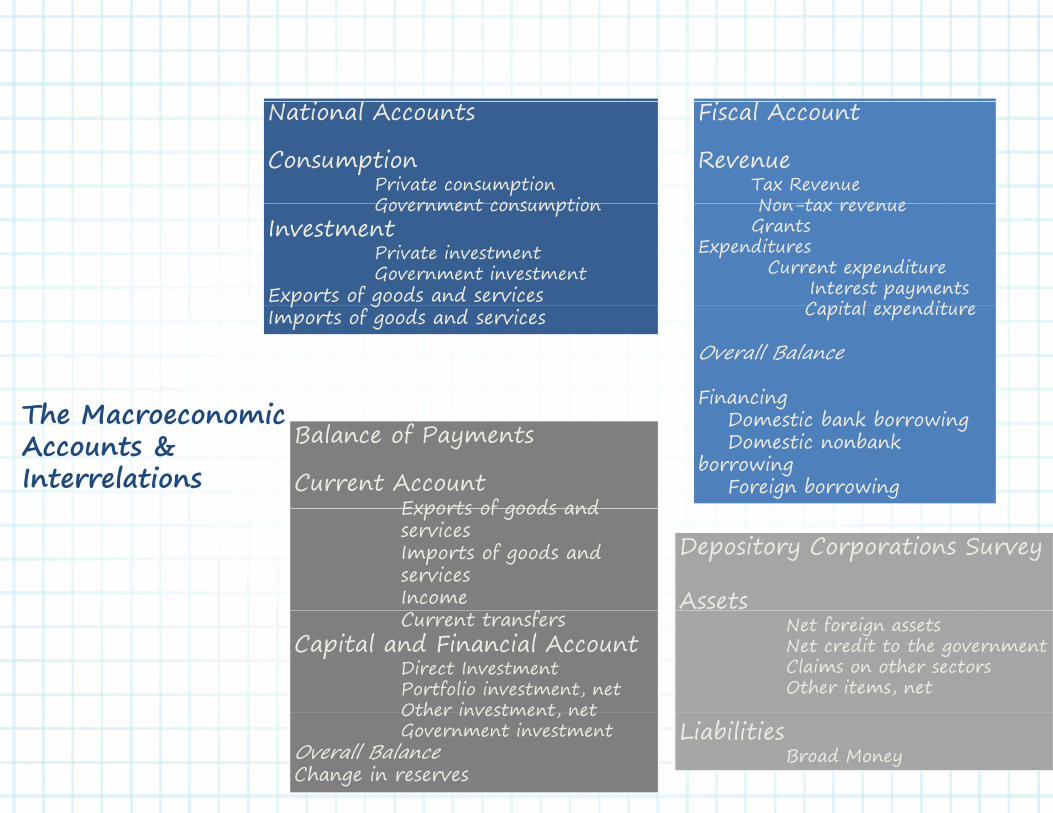

i l i lNational Accounts

ConsumptionPrivate consumptionGovernment consumption

Fiscal Account

Revenue Tax RevenueNon tax revenue Government consumption

InvestmentPrivate investmentGovernment investment

Exports of goods and services

Non-tax revenue Grants

ExpendituresCurrent expenditure

Interest paymentsC pit l xp dit

p gImports of goods and services Capital expenditure

Overall Balance

FinancingTh M i

gDomestic bank borrowingDomestic nonbank

borrowing Foreign borrowing

Balance of Payments

Current AccountExports of goods and

The MacroeconomicAccounts & Interrelations

Exports of goods and servicesImports of goods and servicesIncome

f

Depository Corporations Survey

Assets Current transfers

Capital and Financial AccountDirect Investment Portfolio investment, netOther investment net

Net foreign assets Net credit to the governmentClaims on other sectors Other items, net

Other investment, netGovernment investment

Overall Balance Change in reserves

Liabilities Broad Money

Real GDP Growth Inflation Overall fiscal Balance

(with grants)External Current

Account

(Percent)(Annual average, percent change) (Percent of GDP) (Percent of GDP)

2012 2013 (e) 2014 (p) 2012 2013 (e) 2014 (p) 2012 2013 (e) 2014 (p) 2012 2013 (e) 2014 (p)

South Sudan -47.6 24.7 43.0 45.1 2.8 7.2 -16.0 -9.0 8.1 -27.7 -14.9 8.7

Middle-income

Botswana 4.2 3.9 4.1 7.5 6.8 5.8 0.2 0.2 1.5 -4.9 -1.8 -1.2

Lesotho 4.5 4.1 5.0 5.6 6.5 6.2 5.3 2.0 2.2 -13.6 -13.6 -13.4

Namibia 5.0 4.4 4.0 6.5 6.4 6.2 -3.0 -4.2 -1.6 -2.6 -3.4 -5.2

Zambia 7.2 6.0 6.5 6.6 7.1 7.3 -3.1 -7.8 -6.6 0.0 -3.7 -3.8

Kenya 4.6 5.9 6.2 9.4 5.4 5.0 -6.3 -5.8 -4.2 -9.3 -7.8 -7.3

Malawi 1.9 5.0 6.1 21.3 26 8.4 -4.0 -2.7 -2.1 -4.4 -3.1 -5.1

Tanzania 6.9 7.0 7.2 16 8.5 5.8 -5.0 -5.3 -4.5 -15.3 -14.9 -14.1Tanzania 6.9 7.0 7.2 16 8.5 5.8 5.0 5.3 4.5 15.3 14.9 14.1

Uganda 2.8 5.6 6.5 4.4 5.2 4.8 -3.5 -1.8 -6.0 -10.5 -12.0 -13.9

Fragile countries

Zimbabwe 4.4 3.2 3.6 3.7 2.6 3.3 -0.7 -0.7 1.3 -26.2 -21.7 -16.8

Source: IMF REO (October, 2013)

180

Low Income Countries: Higher Growth Translated into Lower Debt Levels

ERI

LBR

120

140

160

DP

at t

DRC

GMBGIN

GNB

80

100

120

Deb

t to

GD

BEN BFA

BDI

KHM

CAF

TCD

COM

ETHHTI

KENKYR

MDGMWI

MLI

MOZMMR

NPLNER

RWA

SLETZA

UGA20

40

60

Aver

age

00 2 4 6 8 10 12

Average Growth Rates at t-2Average Growth Rates at t 2(In Percent)

How much (Financing Need)How much (Financing Need)Input 20132014201520162017

h

Macro

Growth rateInflation ratePrimary deficitMacro Primary deficit

DebtInterestInterest on existing debtInterest on new debt

Fiscal deficit (Net financing)( g)

DebtPrincipal repaymentPrincipal on existing debt

l d bPrincipal on new debtGross financing requirementrequirement

2013 Financing Needs (In domestic currency)2013 Financing Needs (In domestic currency)

Gross Central Government Cash Requirements 20,000

Redemptions -- Example Total Financing Need 20,000

Financing Sources 20,000

External Financing (60%) 12,000

Multilateral concessional (40%) 4 800Multilateral concessional (40%) 4,800

Bilateral concessional (30%) 3,600

Eurobonds (10%) 1,200

Commercial bank loans (20%) 2,400

MTDS

Domestic Financing (40%) 8,000

T-Bonds (60%) 4,800

T-bills (40%) 3,200

Macro-Framework

National Accounts

Consumption

Fiscal Account

Revenue ConsumptionPrivate consumptionGovernment consumption

InvestmentP i t i t t

Revenue Grants

ExpendituresCurrent expenditure

Interest paymentsCapital expenditure

MTDsPrivate investmentGovernment investment

Exports of goods and servicesImports of goods and services

Capital expenditure

Overall Balance

Financingb k b

p gDomestic bank borrowingDomestic nonbank

borrowing Foreign borrowing

Balance of Payments

Current AccountCurrent AccountExports of goods and servicesImports of goods and servicesI

Depository Corporations Survey

IncomeCurrent transfers

Capital and Financial AccountDirect Investment Portfolio investment, net

Assets Net foreign assets Net credit to the governmentClaims on other sectors

DSA

Portfolio investment, netOther investment, net

Overall Balance Change in reserves

Claims on other sectors Other items, net

Liabilities Broad Money

Key Challenges in FundingInvestor base: geographyInvestor base: geography

Local borrowingInvestor base: composition

g

I te ti l

Market borrowing

InstrumentsConditions with

Roll-over risksInternational borrowing

g

“New” bilateral official lenders

Roll-over risksFX-risk exposuresIR-risk exposures

Less concessional borrowing

IR-risk exposuresOperational risks

6

Average interest on new external

Average Yields for New External Credits Obtained by HIPCs(as percent)

38 Average Maturity of New External Debt Borrowings(in years)

4

5

gdebt commitments, official (%)

Average interest on new external debt commitments, private (%)

23

28

33

2

3

13

18 Average maturity on new external debt commitments, private (years)

Average maturity on new external debt commitments, official (years)

1

-2

3

8

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

02003 2004 2005 2006 2007 2008 2009 2010 2011

The Structural Agenda? E l f t t l Agenda?

M k t A ?

Examples of structural factors:

Market Access?

Investor Base?Structural changes in monetary policy (inflation targeting)

Pricing?

Institutional constraints?

targeting)

Domestic debt markets development Institutional constraints? development

Price of commodities trend

Real effective exchange rate and productivity

Trade liberalization reform

Why a MTDS? Mitigating Fiscal Vulnerabilities

• Choice of strategy can reduce risks and therefore, reduce the likelihood of crisis

– Longer debt maturity helps reduce fiscal vulnerabilities: reduces roll-over risk

– More domestic funding reduces foreign exchange rate risk exposurerate risk exposure

– And, reducing variable rate debt can reduce b

gbudgetary uncertainty and exposure to interest risk

Why a MTDS? Financial Markets Development

P blic debt ma a eme t ca effecti el s pp t the • Public debt management can effectively support the development of more robust financial markets, improving the functioning of the financial system

– Facilitating corporate debt markets• Providing a benchmark for the private sector• Providing scope for securitization of banks’ assetsg p f z f

– Facilitate repo market development• Improving liquidity of banks’ balance sheetsp g q y

– Facilitate development of derivatives markets• Allowing for more effective risk management within g g

the economy

Pricing and Monetary Policy

Baseline and Monetary Policy

• Key variables: Interest and Exchange Rates

• Interest rates:

–Short-term driven by monetary policy–Nominal rates driven by inflation expectations–Monetary policy stance may influence real interest rates given the Monetary policy stance may influence real interest rates given the impact of macroeconomic stability on risk premium

• Exchange Rates:• Exchange Rates:

–Influenced by interest rates (parity equation) f f f–Relationship with foreign reserves, including a policy of foreign

reserve accumulation

THE YIELD CURVE

Yield Curve or Term Structure Plots of yields to maturity of a series of bonds against their term to maturity

Crude representation of risk: return trade off of bond investment alternatives

with reasonably equivalent risk (liquidity, credit, call, premium/discount)

Determinants:

real interest rate

Term structure in one year

inflation premium risk premium

)1()1()1()1( )1( ,13

3,12

2,11 n

nn fffii

Term structure in one year

Term Structure Shapes

NormalYTM YTM

Symptoms of economic downturn, recession

Normal

Inverse

YTM YTMThe longer maturity

the higher the risk

Term to maturity (in years) Term to maturity (in years)

Flat

Humped

YTM YTM

Term to maturity (in years)Term to maturity (in years)

L ss liq id b dsLess liquid bonds

YTM Liquid bondsq

Term to maturity (in years)Term to maturity (in years)

EXCHANGE RATE POLICY EXCHANGE RATE POLICY

• Foreign currency denominated debt

• Exchange rate regimes:

–Fixed exchange rate regimes with an open capital account can aggravate liquidity risk in case of sudden stops or reversals (changes in market sentiment)

– Reducing FX debt and monetary policy, and exchange rate policy coordination.

• FX support, public debt management coordination and FX reserves

d l li i bTo develop an explicit Debt Management StrategyManagement Strategy…

There is a need to understand

• … cost-risk tradeoffs of the debt

• … how debt structures can dampen or amplify the magnitude of external and domestic shocks

• … how the macro affects borrowing

• how monetary control helps domestic debt issuance• … how monetary control helps domestic debt issuance

• … constraints: institutional, market, …

• … new risks and complexities

They got speculative grades … with few variations from Moody’s 4

Moodys: Government Bonds Ratings, a Historical View

B1 few variations from Moody s

3B2

Foreign currencyLocal currency

… and below investment grade from S&P2B3

4

S&P: Local and Foreign Currency Ratings, An Historical Perspective to Date

B+

0

1Caa1

2

3B

B-

Ma

y-98

Ap

r-03

Se

p-0

9Ju

n-1

0D

ec-1

0Ju

n-1

2

Ma

y-07

Se

p-1

3

De

c-12

Se

p-9

8Ju

l-99

Fe

b-1

3

No

v-12

Se

p-1

3

Ma

r-98

Jun

-03

Ma

y-10

Ma

r-11

No

v-12

BOL KHM DRC GHA HND KEN MOZ NIC SEN ZMB

1

B

CCC

0 No

v-05

Ma

y-0D

ec-1

0

Jul-0

6

De

c-04

Ma

y-0

No

v-05

Se

p-0

7A

ug

-10

Oct-0

8S

ep

-09

Jun

-12

Au

g-1

3M

ay-0

Jul-0

8Ju

l-04

Ap

r-06

Au

g-1

3D

ec-1

1

No

v-05

Ma

y-0M

ay-1

De

c-12

Ma

r-1

NR…and if rated by S&P and Moody’s… 5 7 0 4 6 5 7 0 8 9 2 3 4 6 3 1 5 9 0 2 1

BRB BFR CMR GHA HND MLI MOZ RWA SEN UGAZMB

y

Ri kMacro-economic risks and

implications for the debt strategy Risksimplications for the debt strategy

Risks

For the Governme

nt Implications

for the MTDSFinances

f D

Real Sector

Real Growth Inflation

Fiscal Sector Risks Implications

Fiscal receiptsPrimary Balance

Monetary Sector

Further global economic slowdown

Reduce inflows of aid and FDI ?Decline in oil and other commodityMonetary Sector

Commodity PricesInterest rate

commodityprices?

Capital flow reversalStrains in financial markets?

Homegrown risks Political instability?

MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGY MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGY: : SSTEPSTEPS 6&76&7

The Framework: A 8 step approach

The Framework: A 8 step approachA 8-step approachA 8-step approach

Step1: Identify Objectives & Scope p fy j p

Step 2: Identify Costs & Risks of the Existing Debt

Step 3: Identify Potential Funding Sources

Step 4: Identify Baseline Projections & Risks _ fiscal, monetary & k tmarket

Step 5: Review Key Structural FactorsIF NeededIF Needed

Step 6: Identify Cost-Risk trade-offs for alternative debt management strategiesStep 6: Identify Cost-Risk trade-offs for alternative debt management strategies

IF NeededIF Needed

Step 7: Review Implications for macroeconomic policies and marketStep 7: Review Implications for macroeconomic policies and market

Step 8: Recommend MTDS for approval

Setting up alternative strategies

New debt S1 S2 S3 S4% of gross borrowing - Over Projection Period

New debt S1 S2 S3 S4IDA FX 100% 0% 20% 50%AfDF FX 0% 0% 30% 0%Bilateral semi-conc FX 0% 0% 50% 0%Bilateral semi-conc FX 0% 0% 0% 0%Bilateral semi-conc DX 0% 0% 0% 0%Bilateral semi-conc DX 0% 100% 0% 0%Eurobond FX 0% 0% 0% 0%

Are these the right st t i s? Eurobond FX 0% 0% 0% 0%

Dom 1 an DX 0% 0% 0% 25%Dom 3 ans DX 0% 0% 0% 0%Dom 5 ans DX 0% 0% 0% 25%

strategies?

Dom 7 ans DX 0% 0% 0% 0%Commercial DX 0% 0% 0% 0%Arrears FX 0% 0% 0% 0%Arrears DX 0% 0% 0% 0%Arrears DX 0% 0% 0% 0%

0 FX 0% 0% 0% 0%External 100% 0% 100% 50%Domestic 0% 100% 0% 50%

100% 100% 100% 100%

Or, are these the most reasonable strategies?

New debt S1 S2 S3 S4% of gross borrowing - Over Projection Period

New debt S1 S2 S3 S4IDA FX 19% 13% 8% 15%AfDF FX 11% 8% 5% 9%Bilateral semi-conc FX 11% 8% 5% 9%Bilateral semi-conc FX 11% 8% 5% 9%Bilateral semi-conc FX 11% 8% 5% 9%Bilateral semi-conc FX 11% 8% 5% 9%Eurobond FX 0% 0% 0% 0%Dom 1 year DX 13% 0% 14% 7%Dom 3 year DX 13% 0% 28% 13%Dom 5 year DX 0% 0% 14% 10%D 7 DX 0% 50% 14% 9%Dom 7 year DX 0% 50% 14% 9%Commercial loan DX 0% 0% 0% 0%Arrears FX 0% 0% 0% 0%Arrears DX 0% 0% 0% 0%Instrument EUR Var FX 0% 0% 0% 0%External 75% 50% 30% 60%Domestic 25% 50% 70% 40%

100% 100% 100% 100%100% 100% 100% 100%

Issues: Debt Rollover?

Many economies fit under the group of

– long-term external debt holdings and long term external debt holdings and – short-term domestic debt

The question is: could the FX risk of external debt be rebalanced using domestic market instruments?

Committed but undisbursed loans?loans?

Evaluating alternative strategies

Evaluating Strategies: d i k d ffcost and risk trade-off

• Step1: Simulate range of candidate viable and li i i d ifi b lip g

realistic strategies under specific baseline

• Step 2: Have already defined the set of p yalternative strategies and alternative scenarios –the stress tests

• Step 3: Consider and compare the outcomes

k f d d i h• Step 4: Rank performance and determine the preferred strategy

Assessing performanceAssessing performance

• Need to be critical in the assessment

Consider ex ante the possible ranking / effects of stress scenarios…

Which strategy is likely to be least costly?

What risk exposures are likely to increase with each strategy?

Do expectations differ from outcomes? If so, why?

• Need to determine in advance indicators and • Need to determine in advance indicators and cost/risk levels

Recall Cost and Risk IndicatorsRecall Cost and Risk Indicators

• Cost?

– Interest– Interest / Revenues or Interest / GDP

I t t Adj t d P i i l– Interest + Adjusted Principal– Debt / GDP

hi h l f hWhich measures are relevant for the economy?

• Risk? What is the reasonable level of risk? What is the reasonable level of risk?

Measurement of riskMeasurement of risk

Cost

Risk Scenario 1Risk1,X

Baseline Scenario Cost1,X Cost baseline

TimeTime

Borrowing Strategies

80%

100%IDA AfDF

Bilateral semi-conc Bilateral semi-conc

60%

80% Bilateral semi conc Bilateral semi conc

Bilateral semi-conc Bilateral semi-conc

Eurobond Dom 1 year

40%

Eurobond Dom 1 year

Dom 3 year Dom 5 year

Dom 7 year Commercial loan

0%

20%Dom 7 year Commercial loan

Arrears Arrears

Instrument EUR Var0%Current S1 S2 S3 S4

Instrument EUR Var

Outcomes: Interest / Revenues

0 7

S2S3

S40.5

0.6

0.7

%)

S1S4

0.2

0.3

0.4

Cost

(%

-

0.1

- 0.01 0.01 0.02 0.02 0.03 0.03 Risk

N l t d ff S1 l l l t t d l t i kNo real trade-off: S1 clearly least cost and least risk

250,000Strategy 1 External Domestic

500,000Strategy 2 External Domestic

100,000

150,000

200,000

200,000

300,000

400,000

0

50,000

2018

2021

2024

2027

2030

2033

2036

2039

2042

2045

2048

2051

2054

2057

2060

2063

2066

0

100,000

2018

2021

2024

2027

2030

2033

2036

2039

2042

2045

2048

2051

2054

2057

2060

2063

2066

2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

350,000400,000450,000

Strategy 3 External Domestic

250,000

300,000Strategy 4 External Domestic

100,000150,000200,000250,000300,000

100,000

150,000

200,000

050,000

100,000

2018

2021

2024

2027

2030

2033

2036

2039

2042

2045

2048

2051

2054

2057

2060

2063

2066

0

50,00020

1820

2120

2420

2720

3020

3320

3620

3920

4220

4520

4820

5120

5420

5720

6020

6320

66

Risk Indicators 2013 As at end FY2017Current S1 S2 S3 S4

Nominal debt as % of GDP 17.6 13.3 13.9 14.0 13.6

PV as % of GDP 17.3 11.1 12.6 13.0 11.9

Implied interest rate (%) 3.6 2.6 4.2 4.4 3.3Refinancing risk ATM E t l P tf l i ( ) 7 7 16 5 15 7 15 6 16 2Refinancing risk ATM External Portfolio (years) 7.7 16.5 15.7 15.6 16.2

ATM Domestic Portfolio (years) 2.3 2.7 4.5 3.2 3.4ATM Total Portfolio (years) 3.2 14.6 10.2 8.4 12.1

Interest rate risk ATR (years) 3.2 13.2 9.4 7.8 11.0(y )Debt refixing in 1yr (% of total) 29.9 19.8 10.0 20.7 17.9Fixed rate debt (% of total) 99.8 88.3 93.5 94.9 91.0

FX risk FX debt as % of total 15.5 85.8 51.0 42.0 67.6d b % fST FX debt as % of reserves 6.9 22.1 18.9 17.0 20.3

Other relevant indicators?Other relevant indicators?

• Can compare ….

Current S1 S2 S3 S4End-Simulation Horizon (2017)

% DX in debt portfolio 1% 30% 27% 39%ATM (years) 15.6 13.0 9.3 8.3% of debt refixing within 12 months 6.2% 24.4% 23.6% 33.0%% f d bt fi i ithi 12 th 5 5% 31 4% 28 6% 34 7%% of debt refinancing within 12 months 5.5% 31.4% 28.6% 34.7%Short-term external debt / Reserves 3% 3% 3% 3%External debt / Reserves 102% 81% 91% 78%Average interest rate 2.4% 2.5% 2.6% 2.8%Average interest rate 2.4% 2.5% 2.6% 2.8%

Stress Scenarios …2013 2014 2015 2016 2017

Baseline FX depreciation USD 0.2% 0.4% 0.5% 0.4% 0.4%EUR 0.0% 0.0% 0.0% 0.0% 0.0%JPK 0.1% 0.3% 0.4% 0.3% 0.3%GBP 2 9% 3 1% 3 2% 3 2% 3 1%GBP 2.9% 3.1% 3.2% 3.2% 3.1%CNYUTP 0.0% 0.0% 0.0% 0.0% 0.0%

2013 2014 2015 2016 201730% depreciation in year 2 (stand-alone exchange rate shock)

30.00% USD 0.2% 30.4% 0.5% 0.4% 0.4%EUR 0.0% 0.0% 0.0% 0.0% 0.0%JPK 0.1% 0.3% 0.4% 0.3% 0.3%GBP 2.9% 3.1% 3.2% 3.2% 3.1%CNY 0.0% 0.0% 0.0% 0.0% 0.0%

% % % % %UTP 0.0% 0.0% 0.0% 0.0% 0.0%

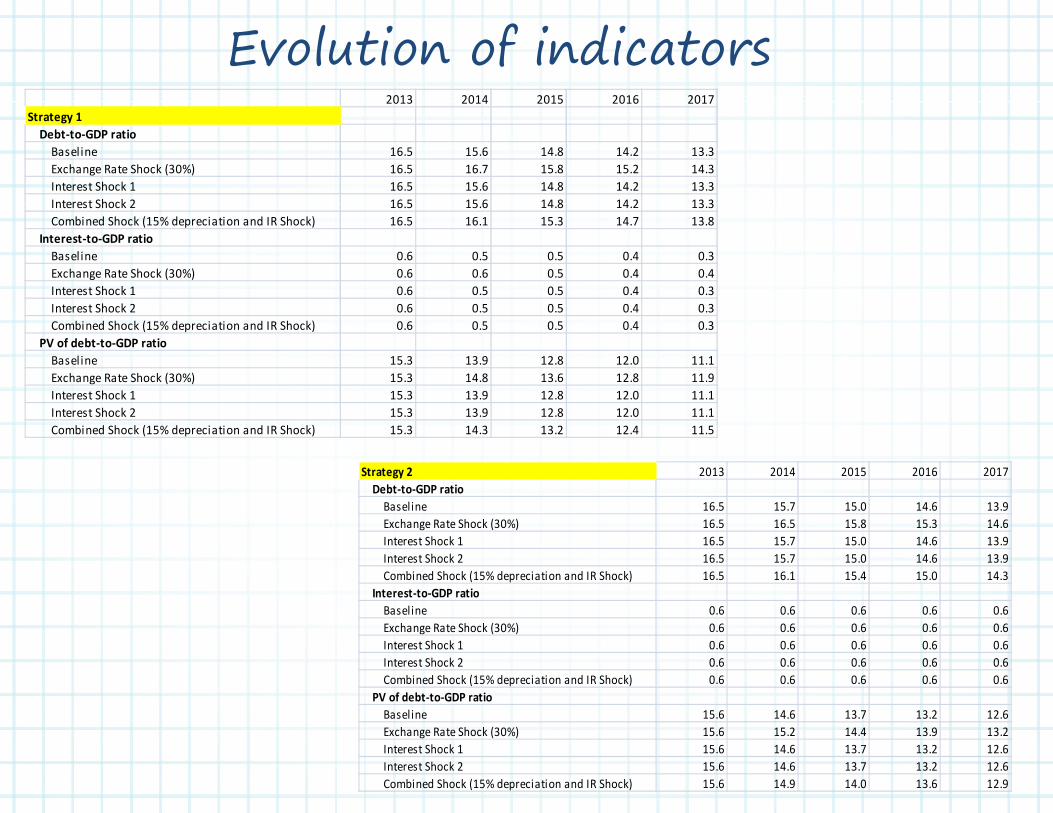

Evolution of indicators2013 2014 2015 2016 20172013 2014 2015 2016 2017

Strategy 1Debt-to-GDP ratio

Baseline 16.5 15.6 14.8 14.2 13.3Exchange Rate Shock (30%) 16.5 16.7 15.8 15.2 14.3Interest Shock 1 16.5 15.6 14.8 14.2 13.3Interest Shock 2 16 5 15 6 14 8 14 2 13 3Interest Shock 2 16.5 15.6 14.8 14.2 13.3Combined Shock (15% depreciation and IR Shock) 16.5 16.1 15.3 14.7 13.8

Interest-to-GDP ratioBaseline 0.6 0.5 0.5 0.4 0.3Exchange Rate Shock (30%) 0.6 0.6 0.5 0.4 0.4Interest Shock 1 0.6 0.5 0.5 0.4 0.3I t t Sh k 2 0 6 0 5 0 5 0 4 0 3Interest Shock 2 0.6 0.5 0.5 0.4 0.3Combined Shock (15% depreciation and IR Shock) 0.6 0.5 0.5 0.4 0.3

PV of debt-to-GDP ratioBaseline 15.3 13.9 12.8 12.0 11.1Exchange Rate Shock (30%) 15.3 14.8 13.6 12.8 11.9Interest Shock 1 15.3 13.9 12.8 12.0 11.1

Strategy 2 2013 2014 2015 2016 2017Debt-to-GDP ratio

Baseline 16 5 15 7 15 0 14 6 13 9

Interest Shock 2 15.3 13.9 12.8 12.0 11.1Combined Shock (15% depreciation and IR Shock) 15.3 14.3 13.2 12.4 11.5

Baseline 16.5 15.7 15.0 14.6 13.9Exchange Rate Shock (30%) 16.5 16.5 15.8 15.3 14.6Interest Shock 1 16.5 15.7 15.0 14.6 13.9Interest Shock 2 16.5 15.7 15.0 14.6 13.9Combined Shock (15% depreciation and IR Shock) 16.5 16.1 15.4 15.0 14.3

Interest-to-GDP ratioBaseline 0 6 0 6 0 6 0 6 0 6Baseline 0.6 0.6 0.6 0.6 0.6Exchange Rate Shock (30%) 0.6 0.6 0.6 0.6 0.6Interest Shock 1 0.6 0.6 0.6 0.6 0.6Interest Shock 2 0.6 0.6 0.6 0.6 0.6Combined Shock (15% depreciation and IR Shock) 0.6 0.6 0.6 0.6 0.6

PV of debt-to-GDP ratioB li 15 6 14 6 13 7 13 2 12 6Baseline 15.6 14.6 13.7 13.2 12.6Exchange Rate Shock (30%) 15.6 15.2 14.4 13.9 13.2Interest Shock 1 15.6 14.6 13.7 13.2 12.6Interest Shock 2 15.6 14.6 13.7 13.2 12.6Combined Shock (15% depreciation and IR Shock) 15.6 14.9 14.0 13.6 12.9

Evolution of indicatorsStrategy 3 2013 2014 2015 2016 2017Strategy 3 2013 2014 2015 2016 2017

Debt-to-GDP ratioBaseline 16.5 15.7 15.0 14.7 14.0Exchange Rate Shock (30%) 16.5 16.3 15.6 15.2 14.6Interest Shock 1 16.5 15.7 15.0 14.7 14.0Interest Shock 2 16.5 15.7 15.0 14.7 14.0Combined Shock (15% depreciation and IR Shock) 16.5 16.0 15.3 15.0 14.3( p )

Interest-to-GDP ratioBaseline 0.6 0.6 0.6 0.6 0.6Exchange Rate Shock (30%) 0.6 0.6 0.6 0.6 0.6Interest Shock 1 0.6 0.6 0.6 0.6 0.6Interest Shock 2 0.6 0.6 0.6 0.6 0.6Combined Shock (15% depreciation and IR Shock) 0.6 0.6 0.6 0.6 0.6

PV of debt-to-GDP ratioBaseline 15.9 14.9 14.1 13.6 13.0Exchange Rate Shock (30%) 15.9 15.4 14.7 14.1 13.4Interest Shock 1 15.9 14.9 14.1 13.6 13.0Interest Shock 2 15.9 14.9 14.1 13.6 13.0Combined Shock (15% depreciation and IR Shock) 15.9 15.2 14.4 13.9 13.2

Strategy 4Debt-to-GDP ratio

Baseline 16.5 15.6 14.9 14.4 13.6Exchange Rate Shock (30%) 16 5 16 6 15 8 15 2 14 4Exchange Rate Shock (30%) 16.5 16.6 15.8 15.2 14.4Interest Shock 1 16.5 15.6 14.9 14.4 13.6Interest Shock 2 16.5 15.6 14.9 14.4 13.6Combined Shock (15% depreciation and IR Shock) 16.5 16.1 15.3 14.8 14.0

Interest-to-GDP ratioBaseline 0.6 0.6 0.5 0.5 0.4Exchange Rate Shock (30%) 0.6 0.6 0.5 0.5 0.5Interest Shock 1 0.6 0.6 0.5 0.5 0.4Interest Shock 2 0.6 0.6 0.5 0.5 0.4Combined Shock (15% depreciation and IR Shock) 0.6 0.6 0.5 0.5 0.5

PV of debt-to-GDP ratioBaseline 15.5 14.3 13.3 12.6 11.9Exchange Rate Shock (30%) 15.5 15.0 14.0 13.3 12.6Interest Shock 1 15.5 14.3 13.3 12.6 11.9Interest Shock 2 15.5 14.3 13.3 12.6 11.9Combined Shock (15% depreciation and IR Shock) 15.5 14.7 13.7 13.0 12.2

Resolving a conflict between indicators?

• Consider wider set of indicators?

• Consider more closely how well the strategies meet other objectives meet other objectives

• Consider how they perform relative to identified • Consider how they perform relative to identified priorities for mitigate macro vulnerabilities

• At the end of the day … need to use judgment

Implied Issuance Patterns

Is this viable? (Average over simulation) S1 S2 S3 S4Net external borrowing 2 3% 1 3% 1 0% 1 8%

Implied net borrowing (% of GDP)

How realistic are the strategies being analyzed?

Net external borrowing 2.3% 1.3% 1.0% 1.8%Net domestic borrowing -1.9% -0.8% -0.4% -1.3%External net borrowing 2013 2014 2015 2016 2017S1 3.9% 2.8% 2.2% 1.8% 1.1%

analyzed?

What do these

S2 2.5% 1.5% 1.2% 0.8% 0.4%S3 1.5% 1.1% 0.9% 0.9% 0.6%S4 3.1% 2.1% 1.6% 1.5% 0.8%D ti t b i 2013 20 20 20 6 20 What do these

decisions imply for the rest of the economy?

Domestic net borrowing 2013 2014 2015 2016 2017S1 -3.3% -2.3% -1.7% -1.5% -0.8%S2 -2.0% -0.9% -0.6% -0.3% 0.1%S3 -0.9% -0.5% -0.2% -0.4% 0.0%

Is this compatible with the monetary policy stance?

S3 0.9% 0.5% 0.2% 0.4% 0.0%S4 -2.5% -1.5% -1.1% -1.1% -0.4%

p y

Drawing conclusionsDrawing conclusions

Q tit ti e t ls help i f decisi ki • Quantitative tools help inform decision-making process by allowing producing a ranking of candidate strategies on a consistent basisg

• However,

The quality of outputs is only as good as th lit f th i tthe quality of the inputs

Decisions need to be made in line with Decisions need to be made in line with the pre-set objectives and take constrains into account

MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGY MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGY: : SSTEPTEP 88

OUTLINEOUTLINEKKEYEY IISSUESSSUES MMAINAIN MMESSAGESESSAGESMMAINAIN MMESSAGESESSAGES

IIMPLEMENTATIONMPLEMENTATIONDefining financing plan in line with budgetary cash needs

Issuance plan

MMONITORINGONITORING

ssua e p a

Impact on key targetsMeet?

Developing/improving risk management system.

Meet?

“S“STRUCTURALTRUCTURAL” ” REFORMSREFORMS

Developing/improving risk management system. Market development objectivesInvestor base relation

Developing a consistent borrowing planDeveloping a consistent borrowing plan

After choosing a DMS….l iImplementation

• What is the annual financing plan that is consistent with the selected strategy?consistent with the selected strategy?

• Are there other portfolio management activities p gthat are needed to attain the portfolio targets? (e.g. derivatives?)

• How is the monitoring of implementation going to be applied? And if there are deviations how to be applied? And, if there are deviations, how are these going to be addressed?

The Financing Plan

H D th Fi i Pl f th How Does the Financing Plan for the Next Budgetary Cycle Look Like? g

D t i th ss b i ds f h t p • Determine the gross borrowing needs for each type of instrument to cover

expected budgetary needs roll over needs/amortization needs /

• Are these consistent with the debt strategy? gy

• Borrowing plan. What is the timing?

2013 Financing Needs (In domestic currency)

Gross Central Government Cash Requirements 20,000Redemptions --Total Financing Need 20,000

Financing Sources 20,000

External Financing (60%) 12,000

Multilateral concessional (40%) 4,800 Bilateral concessional (30%) 3,600 Eurbonds (10%) 1,200 Commercial bank loans (20%) 2,400

Domestic Financing (40%) 8,000T-Bonds (60%) 4,800 T-bills (40%) 3,200

Timing Issues and program design

The debt program needs to be consistent with the cash management program management program.

Calendar of issuances. Quarterly?

Inputs: revenue & spending (including debt service) programming

l f d b lLevel of deposits, TSA balancesProgrammed grants/loans disbursements

Ministry of Finance

Tax and spending Tax and spending data Fiscal position

forecasts il h fl

Back Office Middle Front Daily cash flowsDefines debt and cash

management policy Debt manager

Office Office

policy gBorrowing to meet medium/long term needsDeveloping secondary marketI terfaces to i vestor base a d Interfaces to investor base and creditors

Central Bank

Government’s banker

Key Relationships: Need for Prompt Updates

Manages monetary policyUpdates

Key Relationships

Ministry of Finance

Tax and spending Tax and spending data Fiscal position

forecasts il h fl

Back Office Middle Front Daily cash flowsDefines debt and cash

management policy Debt manager

Office Office

policy gBorrowing to meet medium/long term needsDeveloping secondary marketI terfaces to i vestor base a d Interfaces to investor base and creditors

Central Bank

Government’s banker

Manages monetary policy

Filling the Domestic and External Borrowing Plans: Filling the Domestic and External Borrowing Plans: Consistency

External Borrowing: Options

Official sector flowsDomestic Borrowing:

Options Official sector flows Access to market sources Financing from reserves

f

Options

Marketable debt Instruments Financing secured from FX

market Postponing spending plans

Overdraft facilities Non-marketable instruments Pre funding p p p Pre-funding

Issues Difficult to forecast the Issues Difficult to forecast the

timing of disbursements Need for sterilization, bridge

fi i

Issues Market development

objectivesfinancing?

Identifying the matching liability

j

Fiscal dominance?

Examples

Example of an Issuance Plan:• Target balance on TSA?

• Target bond financing: 4,500Target bond financing: 4,500

• Market development considerations

–Regular issuance: Bonds are auctioned on a Friday.

–Standard amounts: Minimum size of an auction is 150, Standard amounts: Minimum size of an auction is 150, maximum is 400, increments of 25

– Frequency: Maximum frequency of every two weeksq y q y y

– Seasonal factors: No auctions are scheduled in August or December

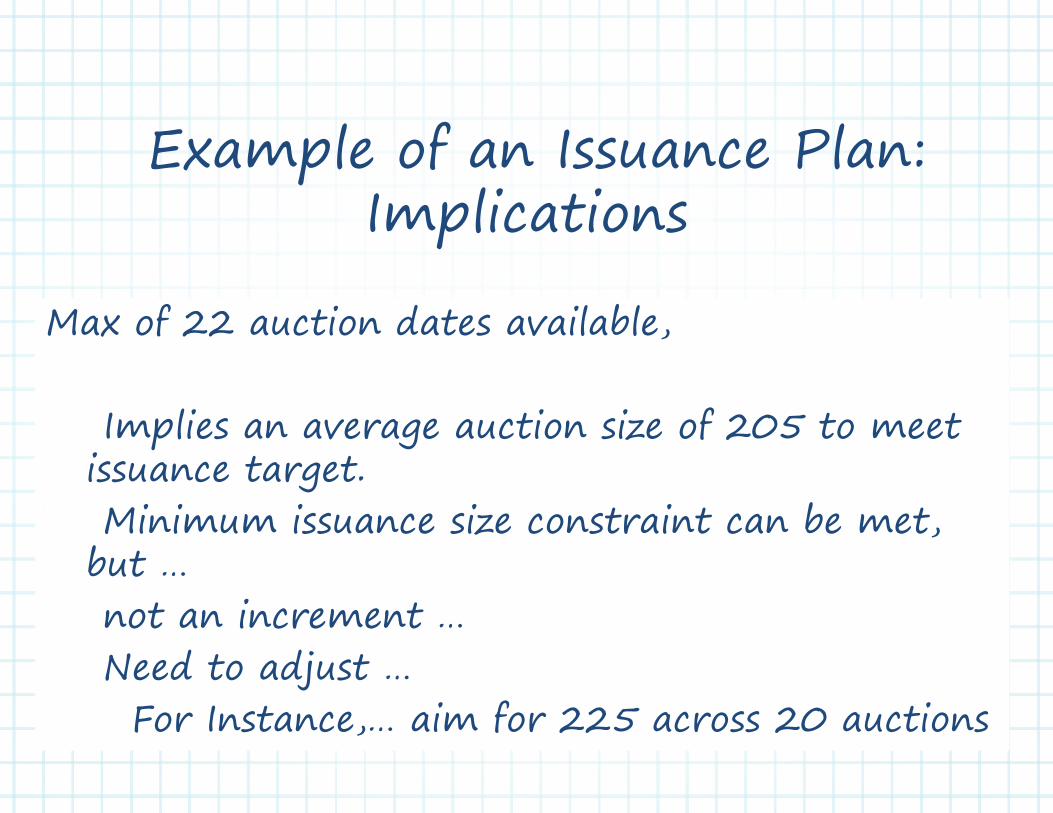

Example of an Issuance Plan: Implicatio sImplications

f d l blMax of 22 auction dates available,

Implies an average auction size of 205 to meet issuance target. Mi i i i t i t b t Minimum issuance size constraint can be met,

but …not an increment not an increment … Need to adjust … F I sta ce ai f 225 ac ss 20 a cti sFor Instance,… aim for 225 across 20 auctions

Example:

The French Calendar

for Domestic Debt for Do estic Debt

Issuances

http://www.aft.gouv.fr/articles/monthly-auction-calendar_669.html

26W T BILLS 13W T BILLS

LATEST T-BILLS AUCTION RESULTS

26W T-BILLS 13W T-BILLS

AUCTION DATE 5-Nov-13 12-Νov-13ISSUE DATE 8-Nov-13 15-Nov-13

MATURITY DATE 9 M 14 14 F b 14MATURITY DATE 9-May-14 14-Feb-14

AMOUNT AUCTIONED 1,000,000,000 1,000,000,000

TOTAL BIDS 1,860,000,000 2,025,000,000

b l

COMPETITIVE BIDS 1,560,000,000 1,725,000,000

NON-COMP. BIDS 300,000,000 300,000,000

COVERAGE RATIO 1.86 2.03

Greece: November 2013 ResultsTOTAL ACCEPT. AMNT 1,300,000,000 1,300,000,000

UNIFORM YIELD 4.15% 3.90%

CUT-OFF PRICE 97.945 99.024CUT OFF PRICE 97.945 99.024

CUT-OFF RATIO 71.60% 90.90%

SECOND DAY BIDS

AUTHORIZED AMNT 300 MLN EURO 300 MLN EURO

EXERCISED AMNT 300 MLN EURO 300 MLN EURO

http://www.pdma.gr/index.php/en/

Spain Tesoro Público funding in 2011 Forecast(in Bn Euros) Forecast 2 0 1 0 Forecast 2 0 1 1 2012

Jan-10 Close Jan-11 Close Strategy

Funding requirement (=Net Issuance) 76 8 62 1 47 2 48 2 36 8Funding requirement (=Net Issuance) 76.8 62.1 47.2 48.2 36.8Redemptions of long-term bonds and loans* -35.4 -35.8 -46.6 -47.1 -50.1Net issuance of long-term bonds and loans* 61.6 58.7 47.2 48.6 35.8Gross issuance of long-term bonds and loans* 97 94.5 93.8 95.6 85.9Net increase in Letras del Tesoro outstanding 15.2 3.4 0 -0.4 1Net change in outstanding Central Government Debt** 78.3 65.2 47.2 51.5 36.8Central Government Debt outstanding at year-end** 553.5 540.6 588 592.1 628.9

*Including foreign-currency debt, medium- and long-term bonds and assumed debt**In nominal terms

i i i d iSpain: 2012 Financing Needs Programming

Spain

http://www tesoro es/en/deuda/index deuda asp

Auction Calendar for Spain

http://www.tesoro.es/en/deuda/index_deuda.asp

Debt Issuance Strategy for Spain

http://www.tesoro.es/en/home/estrategia.asp

Mi i M iIndicators 2011

Limits for 2012

Minimum Maximun

Stock of FDP (R$ billions)

1,866.4 1,950.0 2,050.0 , , ,

Profile (%)

Fixed Rate 37.2 37.0 41.0

Inflation Linked 28.3 30.0 34.0

Floating Rate 30.1 22.0 26.0

E h R t 4 4 3 0 5 0Exchange Rate 4.4 3.0 5.0

Maturity Structure

Average maturity (years) 3.6 3.6 3.8g y (y )

% Maturing in 12 months 21.9 22.0 26.0

www tesouro fazenda gov brwww.tesouro.fazenda.gov.br

http://www.tesouro.fazenda.gov.br/english/hp/public_debt_report.asp.

Turkey

http://www.tukuphane.tcmb.gov.tr

Canada

http://www.fin.gc.ca/treas/frame/tmrf08_1-eng.asp

MMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGYMMEDIUMEDIUM TTERMERM DDEBTEBT SSTRATEGYTRATEGYSSTEPTEP 88

The Framework: A 8 step approach

The Framework: A 8 step approachA 8-step approachA 8-step approach

Step8: Recommend MTDS for approval Step8: Recommend MTDS for approval Step8: Recommend MTDS for approval Step8: Recommend MTDS for approval

Not only developed but also a number of developing countries have y p p gpublished their MTDS document and got Parliaments’ approval.

Reports published include:

Kenya (2009, 2010, 2011)Ghana 2010Ta a ia 2011 2012Tanzania 2011, 2012Malawi 2011Moldova 2011Bangladesh Bangladesh Kyrgyz Republic

Tool that permits

Improved policy coordination p p yEnhanced transparency Better communication also with investorsCommitment to a medium-term debt funding strategy