medicaid eligibility handbook (meh) release 12-02 · medicaid eligibility handbook (meh) release...

TRANSCRIPT

Medicaid Eligibility Handbook (MEH) Release 12-02

ii

Table Of Contents

1. Introduction (Ch 1) ___________________________________________________________________________ 1

2. 1.1 Introduction to Medicaid ___________________________________________________________________ 1 1.1.1 Introduction 1 1.1.2 Subprograms of Medicaid 1 1.1.3 Financial Introduction 2

1.1.3.1 Assets 2 1.1.3.2 EBD Fiscal Group 2 1.1.3.3 Disabled Minors 3 1.1.3.4 Income 3

1.1.4 Health Care Choice 3 1.1.5 How to Apply 4

3. Apps and Reviews (Chs. 2-3) ___________________________________________________________________ 6 2 Applications 6

4. 2.1 Applications Introduction __________________________________________________________________ 6 2.1.1 Affirmative Action and Civil Rights 7

5. 2.2 Application Types/Methods _________________________________________________________________ 8

6. 2.3 Where to Apply ___________________________________________________________________________ 8 2.3.1 Where To Apply Introduction 9 2.3.2 Intercounty Placements 9 2.3.3 Applications Outside Wisconsin 10

7. 2.4 Valid Application _________________________________________________________________________ 12

8. 2.5 Valid Signature __________________________________________________________________________ 12 2.5.1 Valid Signature Introduction 13 2.5.2 Witnessing the Signature 15 2.5.3 Spousal Impoverishment MA Signatures 15

9. 2.6 Filing Date ______________________________________________________________________________ 17 2.6.1 In Person 17 2.6.2 By Mail or Fax 17 2.6.3 By Phone 17 2.6.4 By ACCESS 17 2.6.5 Low Income Subsidy (LIS) Program of Medicare Savings Programs (MSPs) 18

10. 2.7 Timeframes _____________________________________________________________________________ 18 2.7.1 Timeframes Introduction 18 2.7.2 Changes 19

11. 2.8 Begin Dates _____________________________________________________________________________ 21 2.8.1 Begin Dates Introduction 21 2.8.2 Backdated Eligibility 22

Table Of Contents

iii

12. 2.9 Denials and Terminations _________________________________________________________________ 23 2.9.1 Termination 24 2.9.2 Denial 24

3 Reviews 25

13. 3.1 Reviews ________________________________________________________________________________ 25 3.1.1 Reviews Introduction 26 3.1.2 Choice of Review 26 3.1.3 Review Processing 27 3.1.4 Signature at Review 27 3.1.5 Administrative Renewals 27

14. Nonfinancial (Chs. 4 - 14) _____________________________________________________________________ 31 4 Who is Nonfinancially Eligible for Medicaid? 31 4.1 Who is NonFinancially eligible for Medicaid? 31 5 Elderly, Blind, or Disabled (EBD) 31

15. 5.1 Elderly _________________________________________________________________________________ 31 5.2 Determination of Disability 32

16. 5.3 Disability Application Process _____________________________________________________________ 32 5.3.1 Application Form 33

5.3.1.1 Claims filed on behalf of Deceased Applicants 33 5.3.2 Agency Form Processing 34 5.3.3 Release Form 34 5.3.4 Medical Report 35 5.3.5 SSI Application Date 35 5.3.6 Routine SSI-MA Extension 36

5.3.6.1 Case Processing 36 5.3.7 Other SSI-MA Extensions 38

17. 5.4 DDB Action _____________________________________________________________________________ 39 5.4.1 DDB Action Introduction 39 5.4.2 Diary Date 39 5.4.3 Allowances 40 5.4.4 Denials 40

18. 5.5 Reconsideration / hearing _________________________________________________________________ 41 5.5.1 Reconsideration/ Hearing Introduction 41 5.5.2 Reversed Disability Denial Decision 42 5.5.3 CARES Processing 43

19. 5.6 Medical Exam Cost _______________________________________________________________________ 44

20. 5.7 Redetermination _________________________________________________________________________ 44 5.7.1 Redetermination Introduction 45

5.7.1.1 Example of Medicaid Disability Cessation Case Notice Text 47 5.7.2 Recipients Exceeding the Substantial Gainful Activity Level 48

Medicaid Eligibility Handbook (MEH) Release 12-02

iv

21. 5.8 Conflicting Claims _______________________________________________________________________ 49

22. 5.9 Presumptive Disability (PD) ________________________________________________________________ 49 5.9.1 Presumptive Disability Introduction 50 5.9.2 PD Determined By The IM Workers 50

5.9.2.1 Definition of Urgent Need 51 5.9.2.2 Impairments 51 5.9.2.3 PD Certification Process 52

5.9.3 PD Determined By DDB 54 5.9.4 Deceased Applicants 54 5.9.5 Eligibility 55 5.9.6 Disability Application Denials 55

5.9.6.1 DDB Returns a Negative Presumptive Disability Decision 55 5.9.6.2 Recipient Ineligible for Non-Medical Reasons 56 5.9.6.3 DDB Reverses PD Decision Made by DDB or by the IM Worker 56

23. 5.10 MAPP (Medicaid Purchase Plan) Disability __________________________________________________ 57 5.10.1 MAPP Introduction 57 5.10.2 MAPP recipients over age 65 57

6 Residency 58

24. 6.1 Residency Eligibility ______________________________________________________________________ 58 6.1.1 Residency Eligibility Introduction 59 6.1.2 Migrant Farm Worker 59

25. 6.2 Intent to Reside __________________________________________________________________________ 60

26. 6.3 Determining Residence ___________________________________________________________________ 61 6.3.1 Under Age 21 61

6.3.1.1 In an institution 61 6.3.1.2 Not in institution 61

6.3.2 Age 21 and Over 62 6.3.2.1 In an institution 62

27. 6.4 Special Situations ________________________________________________________________________ 63 6.4.1 SSP Payment 63 6.4.2 Homeless Persons 63

28. 6.5 Absence ________________________________________________________________________________ 64 6.5.1 Absence Introduction 64 6.5.2 Temporary Absence 64

29. 6.6 Effective Date of Medicaid for SSI Recipients _________________________________________________ 65

30. 6.7 Wisconsin Veterans Home _________________________________________________________________ 65

31. 6.8 Interstate Placements _____________________________________________________________________ 65 6.8.1 Interstate Placements Introduction 66 6.8.2 Reciprocal Agreement 67 6.8.3 Disputes 68

Table Of Contents

v

32. 6.9 Inmates ________________________________________________________________________________ 69 6.9.1 Definitions 69 6.9.2 Inmates Introduction 69 6.9.3 Inmates of State Correctional Institutions 70 6.9.4 State Correctional Institutions 72

7 U.S. Citizen or Qualifying Immigrant 76

33. 7.1 US Citizens and nationals _________________________________________________________________ 76 7.1.1 US Citizens and Nationals Introduction 76 7.1.2 Child Citizenship Act of 2000 76 7.1.3 Compact of Free Association States 78

34. 7.2 Documenting Citizenship and Identity _______________________________________________________ 78 7.2.1 Documenting Citizenship and Identity Introduction 79

7.2.1.1 Covered Programs 81 7.2.1.2 Exempt Populations 81

7.2.2 Reserved 82 7.2.3 Reserved 82 7.2.4 Hierarchy of Documentation 82 7.2.4.1 Levels of Documentation 83

7.2.4.2 Naturalized Citizens 84 7.2.4.3 Agencies Paying For Documentation 84 7.2.4.4 Tribes With An International Border 85

7.2.5 Policy for Special Populations 85 7.2.6 Situations Which Require Special Documentation Processing 89

7.2.6.1 Person Add 89 7.2.6.2 Individuals Without Verification and Affect on Household Eligibility 89 7.2.6.3 Individuals Gaining Citizenship Through The Child Citizenship Act of 2000 89 7.2.6.4 Non-citizens 89

7.2.6.5 Individuals in Institutional Care Facilities 90

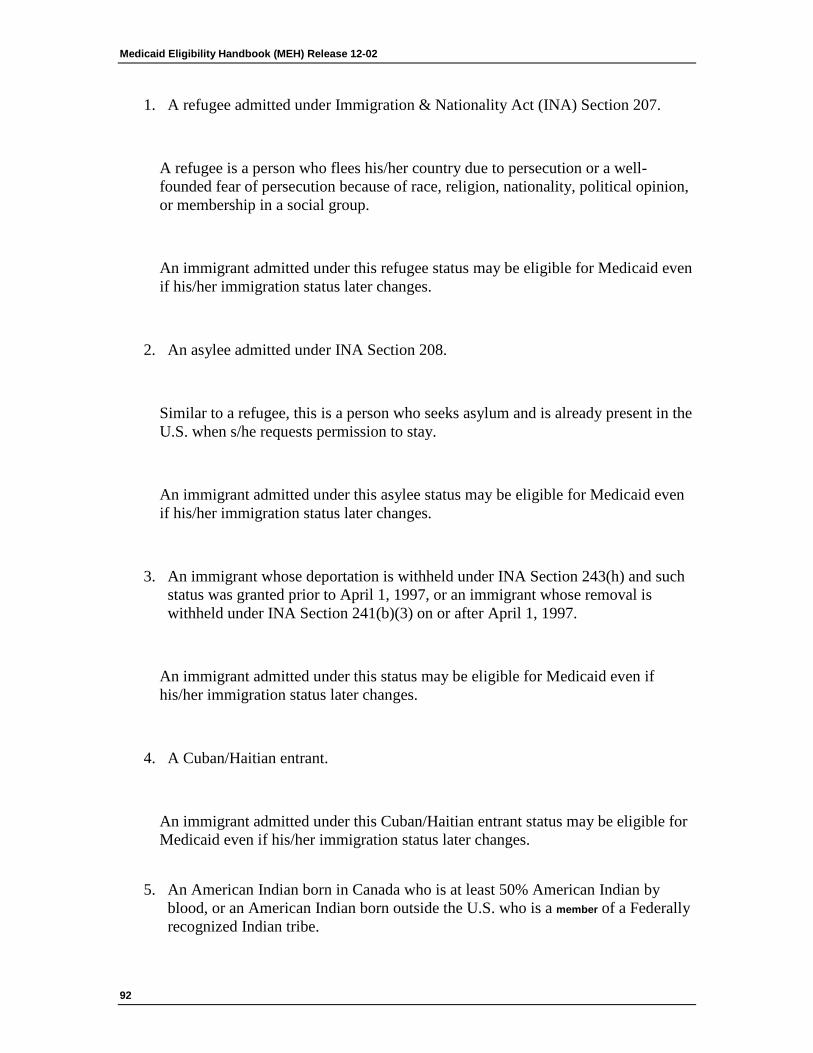

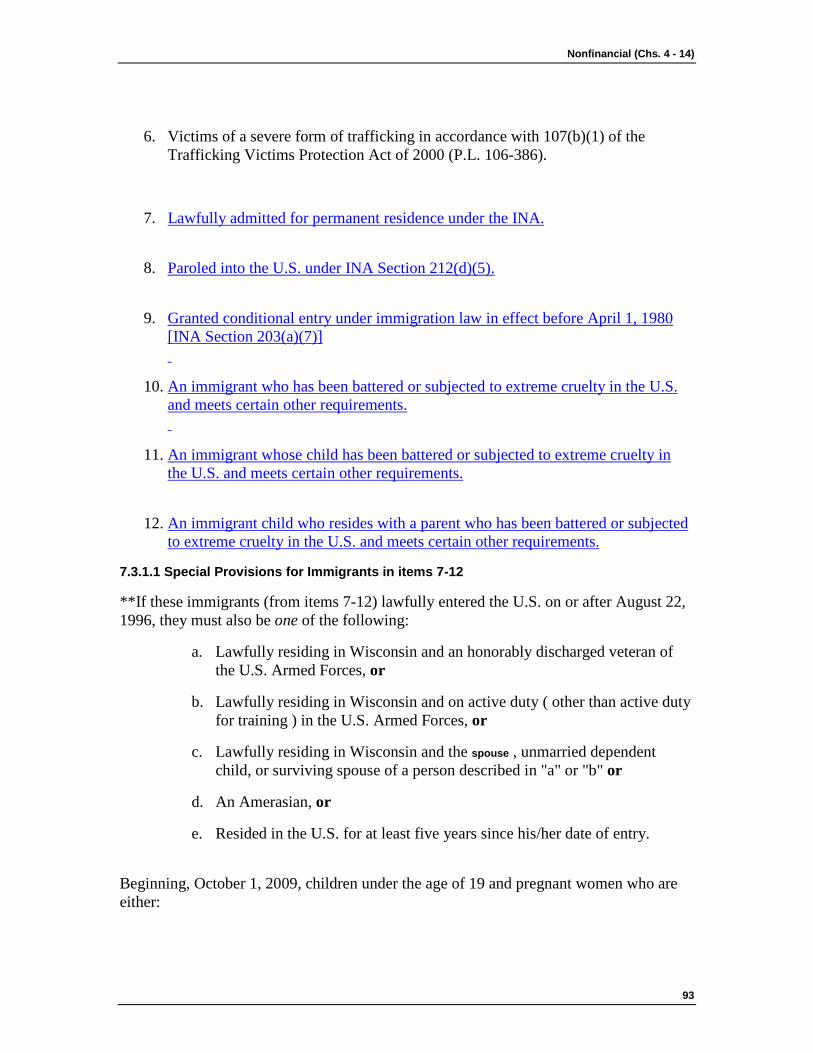

35. 7.3 Immigrants______________________________________________________________________________ 91 7.3.1 Immigrants Introduction 91

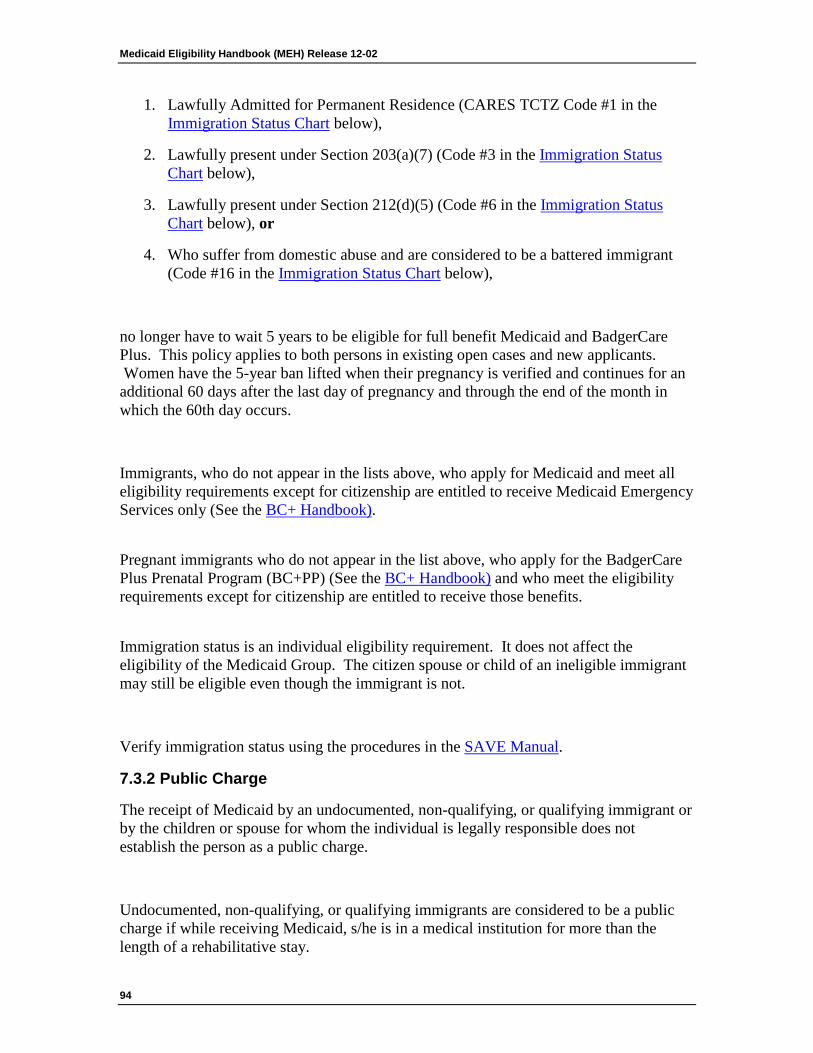

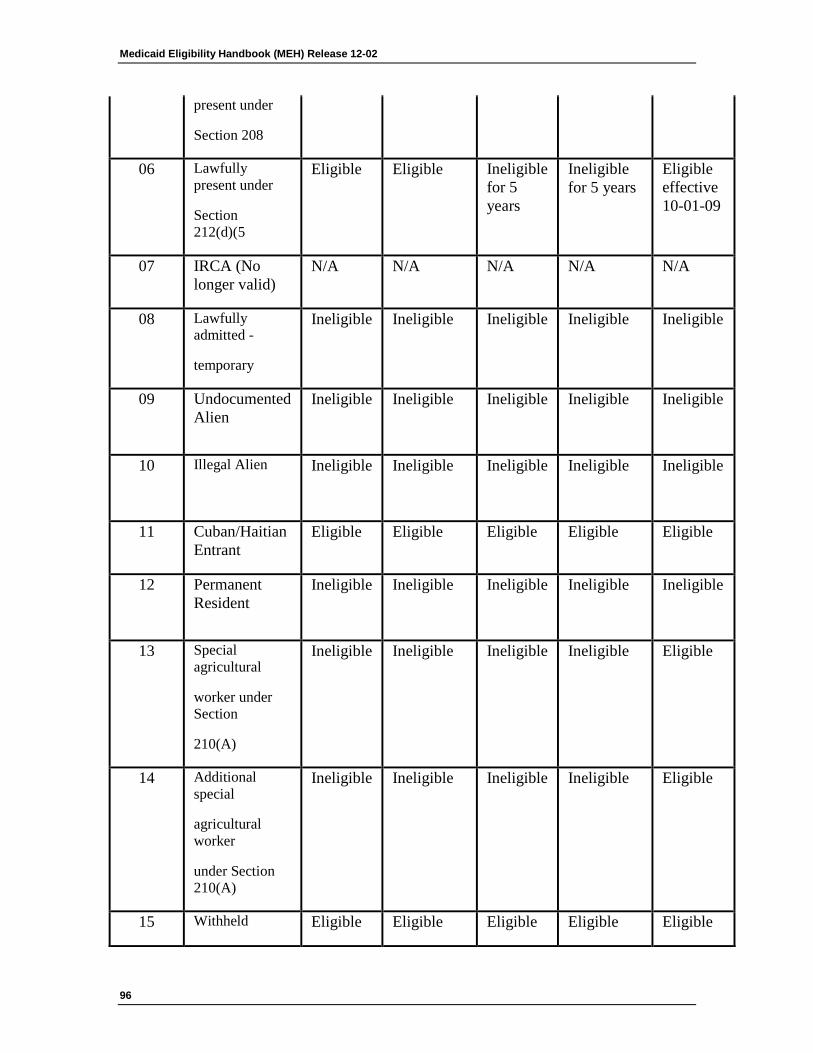

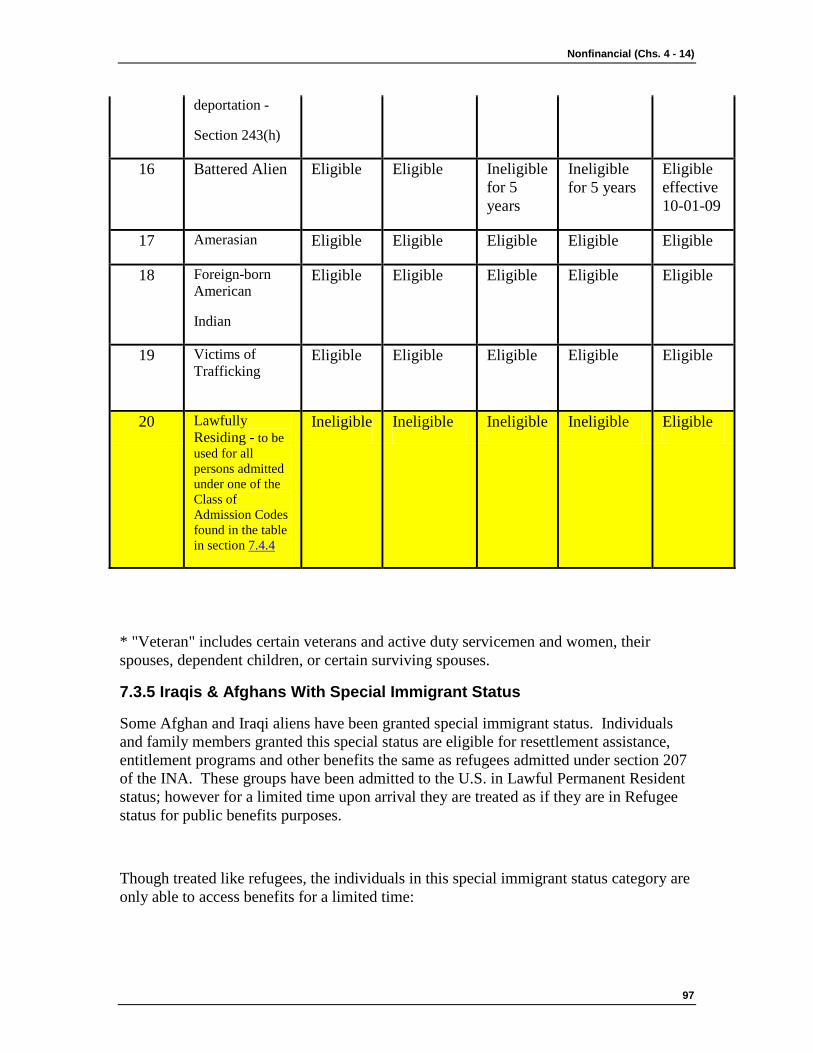

7.3.1.1 Special Provisions for Immigrants in items 7-12 93 7.3.2 Public Charge 94 7.3.3 INS Reporting 95 7.3.4 Immigration Status Chart 95 7.3.5 Iraqis & Afghans With Special Immigrant Status 97

7.3.5.1 End of Temporary Benefit Period 98 7.3.5.2 Counting Refugee Related Income 99 7.3.5.3 Refugee Medical Assistance 99

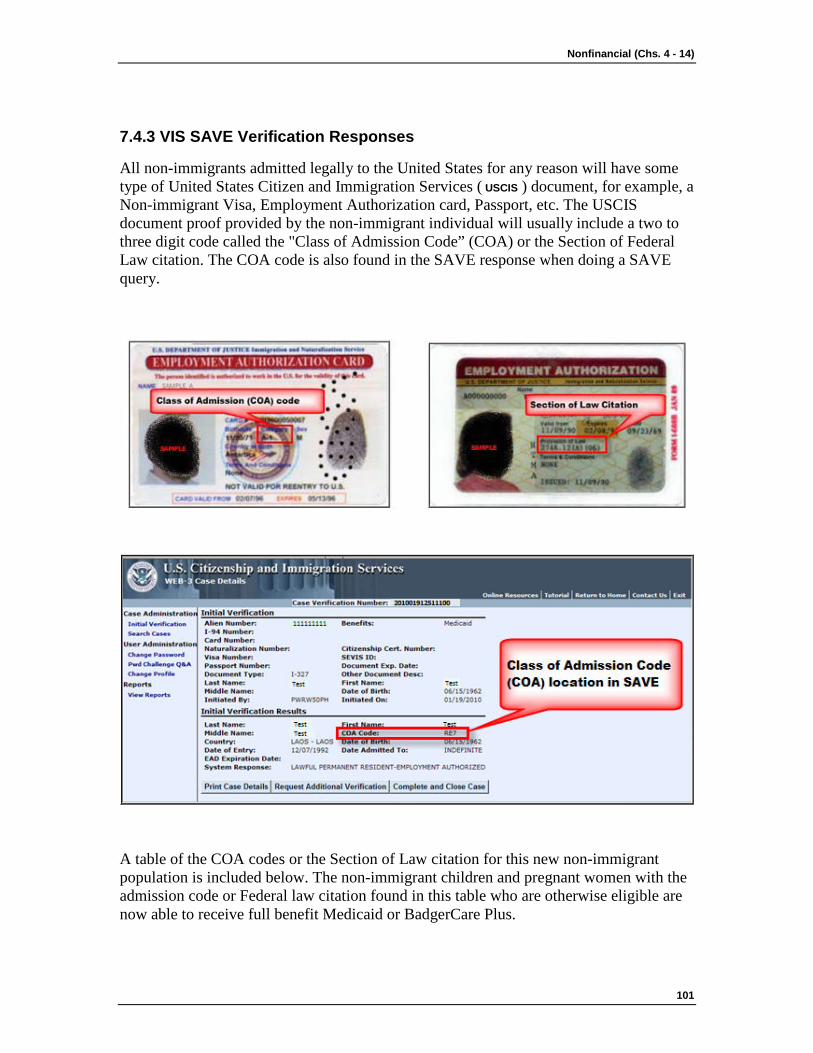

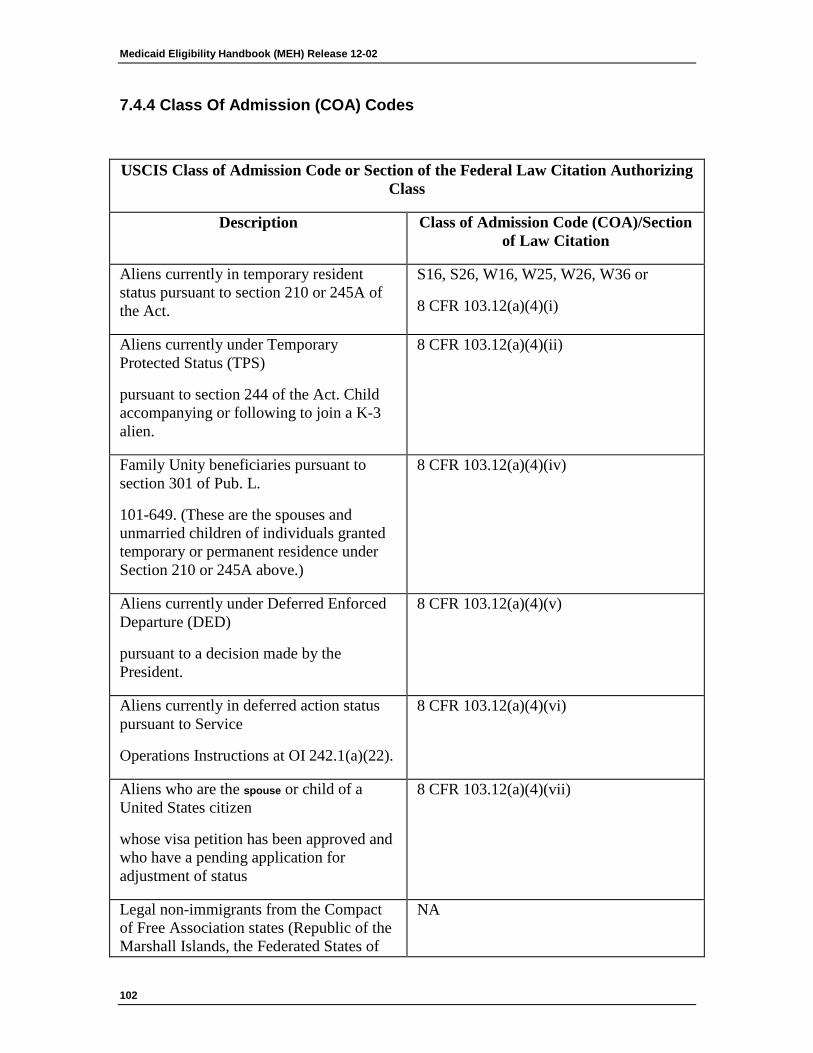

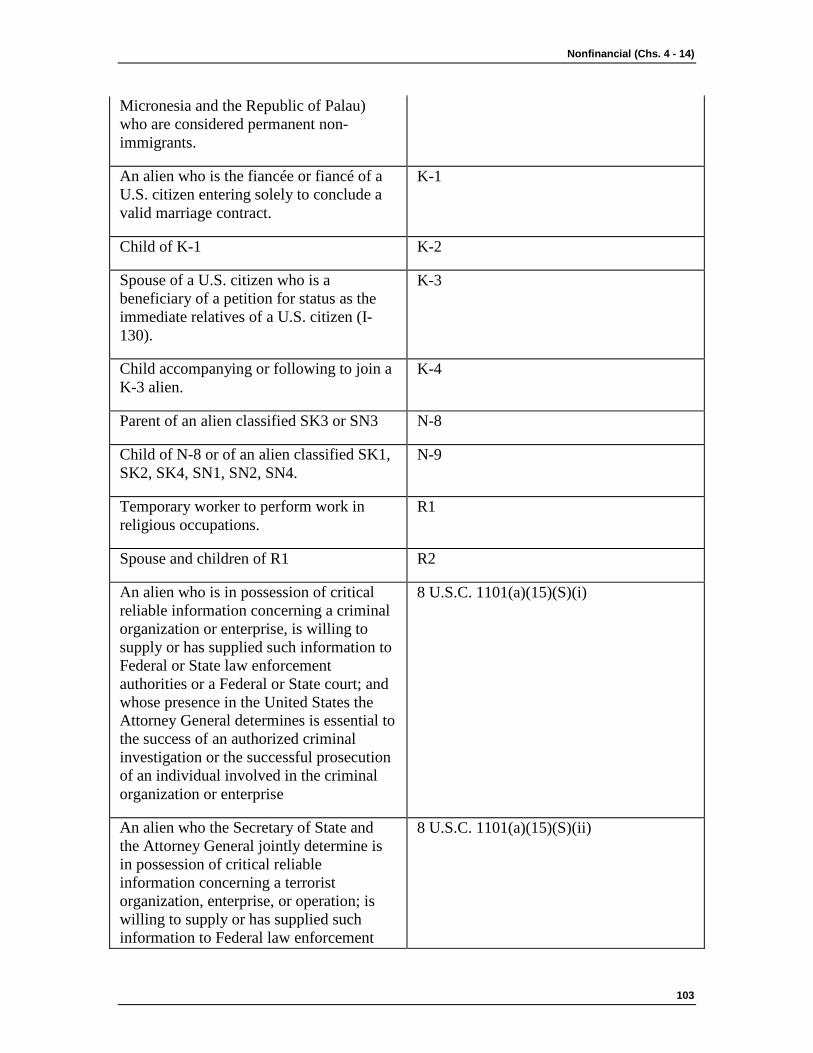

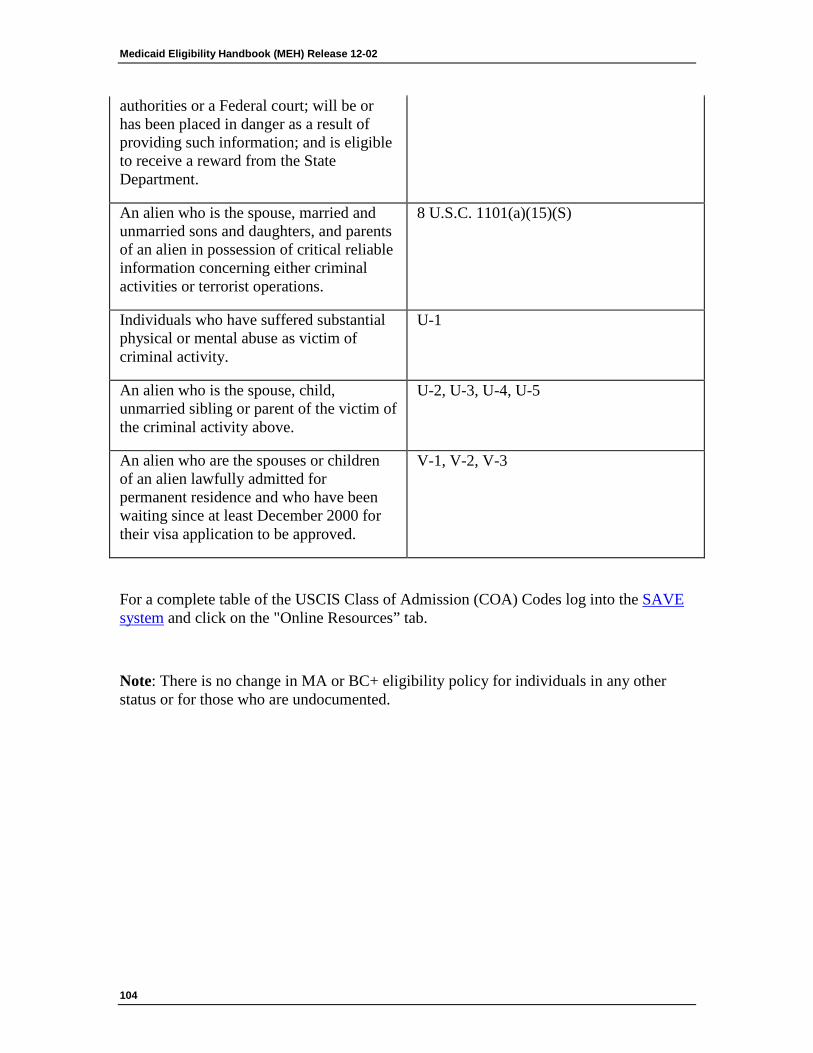

36. 7.4 Non-Immigrant, Non-Citizens _____________________________________________________________ 100 7.4.1 Introduction 100 7.4.2 New Age Group 100 7.4.3 VIS SAVE Verification Responses 101 7.4.4 Class Of Admission (COA) Codes 102

8 Medical Support 105

37. 8.1 Medical Support ________________________________________________________________________ 105 8.1.1 Medical Support Introduction 105 8.1.2 Recovery of Birth Costs 105 8.1.3 Referral to CSA 105

Medicaid Eligibility Handbook (MEH) Release 12-02

vi

38. 8.2 Medical Support/ CSA Cooperation ________________________________________________________ 107 8.2.1 Medical Support / Child Support Agency (CSA) Cooperation 107 8.2.2 Failure to Cooperate 108

39. 8.3 Claiming Good Cause ___________________________________________________________________ 110 8.3.1 Claiming Good Cause Introduction 110 8.3.2 Notice 110 8.3.3 Good Cause Claim 111 8.3.4 Circumstances 111 8.3.5 Evidence 112 8.3.6 Investigation 114 8.3.7 Determination 115 8.3.8 Good Cause Found 115 8.3.9 Good Cause Not Found 116 8.3.10 Review 116

40. 8.4 Cooperation Between IM & CSA ___________________________________________________________ 119 8.4.1 Information 119 8.4.2 Medicaid Discontinued 119 8.4.3 Fraud 119

9 Third Party Liability (TPL) 121

41. 9.1 Third Party Liability (TPL) ________________________________________________________________ 121 9.1.1 Third Party Liability Introduction 121 9.1.2 TPL Cooperation 121 9.1.3 TPL Cooperation Requirements 121 9.1.4 TPL Good Cause Claim 122 9.1.5 Assignment Process 122

42. 9.2 Nursing Home and Hospital Insurance ______________________________________________________ 123 9.2.1 Nursing Home and Hospital Insurance Introduction 123 9.2.2 Assignment 124 9.2.3 Recovery of Payments 124

43. 9.3 Health Insurance Risk Sharing Plan (HIRSP) _________________________________________________ 126

44. 9.4 Health Insurance Premium Payment (HIPP) __________________________________________________ 127 9.4.1 Cost-Effective 127 9.4.2 Participation in HIPP 127 9.4.3 Cooperation 127 9.4.4 Exceptions 128 9.4.5 Not Cost-Effective 128

45. 9.5 Casualty Claim Process (Subrogation) _____________________________________________________ 130 9.5.1 Casualty Claims (Subrogation) Introduction 130 9.5.2 Reporting Accident or Injury Claims 130

46. 9.6 Other Health Insurance __________________________________________________________________ 132 9.6.1 Other Health Insurance Introduction 132 9.6.2 Policies Not To Report 132

Table Of Contents

vii

47. 9.7 Third Party Liability (TPL) Ending __________________________________________________________ 133

48. 9.8 Double Payment ________________________________________________________________________ 134

49. 9.9 Health Insurance Form ___________________________________________________________________ 135 9.9.1 Health Insurance Information Form Introduction 135 9.9.2 Section A 136 9.9.3 Section B 137 9.9.4 Section C 137 9.9.5 Section D 137 9.9.6 Where to Send 137

10 SSN 138

50. 10.1 SSN Requirements _____________________________________________________________________ 138 10.1.1 SSN Requirements Introduction 139 10.1.2 Emergency Services 139 10.1.3 SSN Mismatches 139 10.1.4 SSN Fraud 139 10.1.5 Failure to Provide SSN 139

11 Premium or Cost Share 141 11.1 Premium or Cost Share 141 12 Change Reporting 141

51. 12.1 Change Reporting Introduction ___________________________________________________________ 141 13-14 Reserved 142

52. 13 - 14 Reserved ___________________________________________________________________________ 142

53. Financial (Chs. 15 - 19) ______________________________________________________________________ 143 15 Income 143

54. 15.1 Income Introduction ____________________________________________________________________ 143 15.1.1 EBD Fiscal Group 143 15.1.2 Special Financial Tests for Disabled Minors 144 15.1.3 Income 147 15.1.4 EBD Related Test 148 15.1.5 Availability 148 15.1.6 Countable Income 150

15.1.6.1 Migrant Workers 150

55. 15.2 Prospective Income ____________________________________________________________________ 151 15.2.1 Prospective Budgeting 151 15.2.2 Prorating Income 151 15.2.3 Fluctuating Income 153

56. 15.3 Exempt/Disregarded Income _____________________________________________________________ 153 15.3.1 Adoption Assistance 155 15.3.2 Agent Orange Settlement Fund 155 15.3.3 Combat Pay 155 15.3.4 Crime Victim Restitution Program 156 15.3.5 Disaster and Emergency Assistance 156 15.3.6 Dottie Moore Payments 156

Medicaid Eligibility Handbook (MEH) Release 12-02

viii

15.3.7 Foster Care 156 15.3.8 General Income Disregard 156 15.3.9 Individual Development Account (IDA) Payments 156 15.3.10 Inconsequential 156 15.3.11 Kinship Care 157 15.3.12 Life Insurance 157 15.3.13 Nutrition Benefits 157 15.3.14 Payments to Native Americans 158 15.3.15 Payments to Nazi Victims 159 15.3.16 Radiation Exposure Compensation Act 159 15.3.17 Refugee Cash Assistance (RCA) 159 15.3.18 Refugee "Reception and Placement" (R&P) payments 159 15.3.19 Reimbursements 160 15.3.20 Relocation Payments 160 15.3.21 Repayments 161 15.3.22 Special Programs 161 15.3.23 Spina Bifida Child 162 15.3.24 Susan Walker Payments 162 15.3.25 Travel Tickets 162 15.3.26 VA Allowances 163

15.3.26.1 Residents of a State Veterans Home 164 15.3.27 Wartime Relocation of Citizens 165 15.3.28 W2 Payments 165 15.3.29 The American Recovery and Reinvestment Act (ARRA) of 2009 165 15.3.30 Subsidized Guardianship Payments. 165

57. 15.4 Unearned Income ______________________________________________________________________ 167 15.4.1 Income from Trusts 168 15.4.2 Sick Benefits 169 15.4.3 Unemployment Compensation ( UC ) 169 15.4.4 Retirement Benefits 169 15.4.5 General Relief and Charity 170 15.4.6 Gifts 170 15.4.7 Land Contract 171 15.4.8 Loans 171 15.4.9 Interest/Dividend Income 172

15.4.9.1 EBD Interest/Dividend Income 172 15.4.9.1.1 Excluded Sources of Interest or Dividend Income 172 15.4.9.1.2 Interest and Dividends Income not excluded for EBD 173

15.4.10 Social Security Benefits 174 15.4.11 Property Settlement 174 15.4.12 Lump Sum Payments 175 15.4.13 Money for School 175

15.4.13.1 Total Disregards 175 15.4.13.2 Partial Disregards 176 15.4.13.3 Workforce Investment Act (WIA) 176

15.4.14 Child Support 177 15.4.15 Profit Sharing 178 15.4.16 Income Received by Members of a Religious Order 178 15.4.17 Federal Match Grants for Refugees 178 15.4.18 Gambling winnings 178 15.4.19 Payments to Native Americans 178 15.4.20 First Time Home Buyer Tax Credits 179 15.4.21 Alimony, Maintenance, and Other Spousal Support Payments 179

Table Of Contents

ix

58. 15.5 earned Income ________________________________________________________________________ 180 15.5.1 Income In-Kind 181 15.5.2 Contractual Income 181 15.5.3 Rental Income 182 15.5.4 Jury Duty Payments 183 15.5.5 Wage Advances 183 15.5.6 Worker's Compensation 183 15.5.7 Governor's Central City Initiative 183 15.5.8 Income Tax Refunds 183 15.5.9 Student Income 183 15.5.10 AmeriCorps 184 15.5.11 Census 2010 184 15.5.12 Severance Pay 184 15.5.13 Income Received by Members of a Religious Order 184 15.5.14 Title V - Older Americans Act of 1965 184 15.5.15 Room and Board Income 185 15.5.16 Earned Income Tax Credit (EITC) 185 15.5.17 Make Work Pay Credit 185 15.5.18 Special Tax Credit for Certain Government Retirees 185

59. 15.6 Self Employment Income ________________________________________________________________ 186 15.6.1 Definitions 187

15.6.1.1 Income 187 15.6.1.2 Business 187 15.6.1.3 Operating 188 15.6.1.4 IM Income 188 15.6.1.5 Real Property 188 15.6.1.6 Non-real Property 188

15.6.2 Ways to Identify 188 15.6.2.1 By Organization 188 15.6.2.2 By IRS Tax Forms 189 15.6.2.3 Employee Status 189

15.6.3 Self Employment Income Assets 190 15.6.3.1 Business Assets 191 15.6.3.2 Bank Accounts 192 15.6.3.3 Disallowed Expenses 192

15.6.4 Self-Employed Income Sources 192 15.6.5 Calculating IM Income 194

15.6.5.1 IRS Tax Forms 195 15.6.5.2 Worksheets 195 15.6.5.2.1 Depreciation 196 15.6.5.3 Anticipated Earnings 196

15.6.6 Verification 199 15.6.7 Self-Employment Hours 200

60. 15.7 Income Deductions ____________________________________________________________________ 201 15.7.1 Maintaining Home or Apartment 201 15.7.2 Special Exempt Income 202

15.7.2.1 Support Payments 203 15.7.2.1.1 Court-Ordered 203 15.7.2.1.2 Non-court-Ordered 203 15.7.2.2 Self-Support Plan 204 15.7.2.3 Fees to Guardians or Attorneys 204 15.7.2.3.1 Countable 204 15.7.2.3.2 Not Countable 205

15.7.3 Medical/Remedial Expenses ( MRE ) 205

Medicaid Eligibility Handbook (MEH) Release 12-02

x

15.7.4 Impairment Related Work Expenses ( IRWE ) 206 15.7.5 $65 and ½ Earned Income Deduction 208

16 Assets 210

61. 16.1 Assets Introduction ____________________________________________________________________ 210

62. 16.2 Assets Availability______________________________________________________________________ 211 16.2.1 Assets Availability Introduction 212 16.2.2 Real Property 212

63. 16.3 Separate and Mixed Assets ______________________________________________________________ 214

64. 16.4 Accounts _____________________________________________________________________________ 215 16.4.1 Joint Accounts 215

16.4.1.1 EBD Medicaid Applicant/Recipient EBD co-owner 215 16.4.1.2 EBD Medicaid Applicant/Recipient Non EBD Co-Owner 216 16.4.1.3 Exception to Joint Accounts policy 216

16.4.2 Jointly Held Real Property 217

65. 16.5 Burial Assets __________________________________________________________________________ 218 16.5.1 Burial Trusts 219 16.5.2 Burial Insurance 219 16.5.3 Life Insurance Funded Burial Contracts (LIFBC) 220

16.5.3.1 Irrevocable Assignment of LIFBC 220 16.5.3.2 Revocable Assignment of LIFBC 222

16.5.4 Spaces 223 16.5.5 Burial Funds 224 16.5.6 Wisconsin Pre-Need Funeral Trust Program 226

16.5.6.1 Statement of Funeral Goods & Services 228 16.5.6.2 Cash Advances 228

66. 16.6 Non-Burial Trusts ______________________________________________________________________ 229 16.6.1 Non-Burial Trusts Introduction 230 16.6.2 Trust Principal 231 16.6.3 Revocable Trusts 231 16.6.4 Irrevocable Trusts 231

16.6.4.1 Trust Established With Resources of a Third Party 231 16.6.4.2 Trust Established With Resources of the Individual or Spouse 231

16.6.5 Special Needs Trust 233 16.6.6 Pooled Trusts 233

Note: The assets that have been placed in a potential pooled trust pending a disability determination are unavailable assets until the disability determination has been made. If the individual has been determined disabled by DDB, the pooled trust is an exempt asset as of the disability onset date. If the individual is not determined disabled, the assets are counted. 235

16.6.7 Ho-Chunk Tribal Trusts 235

67. 16.7 Liquid Assets _________________________________________________________________________ 235 16.7.1 Personal Property 237

16.7.1.1 Household Goods 237 16.7.1.2 Personal Effects 238 16.7.1.3 Other Personal Property 238

16.7.2 Loans 239 16.7.2.1 Reverse Mortgage 239

16.7.3 HUD Payments 240

Table Of Contents

xi

16.7.4 Annuities 240 16.7.4.1 Annuities Purchased After March 1, 2004 240 16.7.4.1.1 Annuities That Can Be Surrendered: 240 16.7.4.1.2 Annuities That Cannot Be Surrendered (this subsection effective 03-01-09) 241 16.7.4.2 Annuities Purchased before March 1, 2004 242

16.7.5 Life Insurance 242 16.7.6 Treatment Of Continuing Care Retirement Community Entrance Fees 243 16.7.7 Income Tax Refunds 244 16.7.8 Earned Income Tax Credit (EITC) 244 16.7.9 Vehicles (Automobiles) 245

16.7.9.1 Determining Equity Value 245 16.7.9.2 When to Count, When to Exempt 245

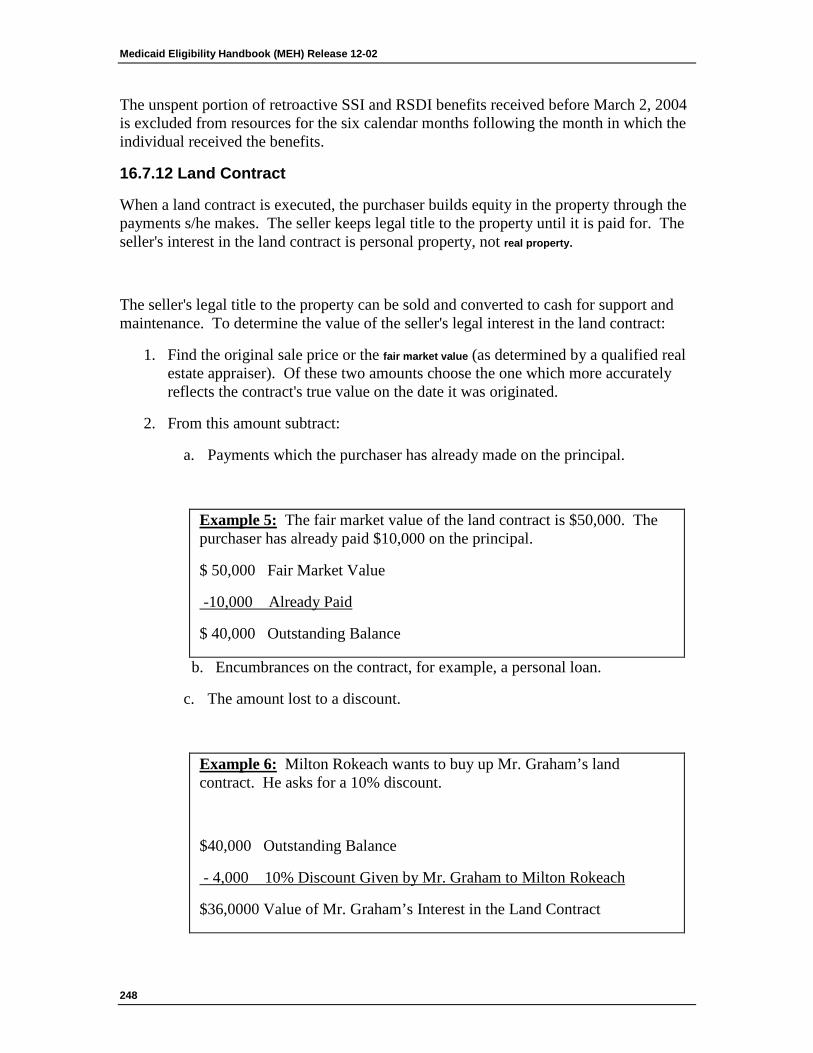

16.7.10 Property Settlement 247 16.7.11 Lump Sums Payments 247

16.7.11.1 Retroactive SS Payments 247 16.7.12 Land Contract 248 16.7.13 Mortgage 249 16.7.14 Wisconsin Higher Education Bonds 249 16.7.15 Wartime Relocation of citizens 250 16.7.16 Agent Orange Settlement Fund 250 16.7.17 Radiation Exposure Compensation Act 250 16.7.18 Institutionalized Person’s Assets 250 16.7.19 Blind/Disabled Set-Aside 251 16.7.20 Replacing and Repairing Exempt Assets 251 16.7.21 Retirement Benefits 251 16.7.22 Gifts 253 16.7.23 U.S. Savings Bonds 253 16.7.24 Make Work Pay 253 16.7.25 Indian Judgment Fund Purchases 253 16.7.26 Payments to Nazi Victims 253 16.7.27 Spina Bifida Child 253 16.7.28 Uniform Gifts to Minors Act 254 16.7.29 Individual Development Accounts ( IDA ) Programs 254 16.7.30 Crime Victim Restitution Program 254 16.7.31 The American Recovery and Reinvestment Act (ARRA) of 2009 254 16.7.32 First Time Home Buyer’s Tax Credit 254 16.7.33 Special Tax Credit for Certain Government Retirees 254

68. 16.8 Real Property _________________________________________________________________________ 255 16.8.1 Home/Homestead Property 256

16.8.1.1 Multi-unit Dwelling 256 16.8.1.2 Non-Motorized Trailer Homes 256 16.8.1.3 Exempt Home Property 257

16.8.1.4 Home Equity over $750,000.00 258 16.8.1.5 Sale of Home Property 259 16.8.1.6 Life Estate 260

69. 16.9 Non-Home Property Exclusions __________________________________________________________ 261

70. 16.10 Indian Lands _________________________________________________________________________ 262 17 Divestment 263

Medicaid Eligibility Handbook (MEH) Release 12-02

xii

71. 17.1 Divestment Introduction ________________________________________________________________ 263

72. 17.2 Divestment Definitions __________________________________________________________________ 263 17.2.1 Divestment 264 17.2.2 Transfer 265

17.2.2.1 Date of Transfer 265 17.2.3 Nonexempt Assets 266

17.2.3.1 Homestead Property 266 17.2.4 Institutionalized Person 266 17.2.5 Community Spouse 266 17.2.6 Fair Market Value 266 17.2.7 Divested Amount 266 17.2.8 Net Market Value 266 17.2.9 Value Received 267 17.2.10 Unavailability 267

73. 17.3 Look Back Period ______________________________________________________________________ 268 17.3.1 Look Back Period Introduction 268 17.3.2 Divestments Prior To January 1, 2009 269 17.3.3 Divestments On or After January 1, 2009 269

74. 17.4 Exceptions ____________________________________________________________________________ 270

75. 17.5 Penalty Period _________________________________________________________________________ 277 17.5.1 Penalty Period Introduction 278 17.5.2 Calculating the Penalty Period 278

17.5.2.1 Penalty Period for Divestments prior to January 1, 2009 278 17.5.2.2 Penalty Period for divestments on or after January 1, 2009 279

17.5.3 Penalty Period Begin Date For Applicants 279 17.5.3.1 Divestments That Occurred Prior to January 1, 2009 279 17.5.3.2 Divestments That Occurred On or After January 1, 2009 280

17.5.4 Penalty Period Begin Date For Recipients 281 17.5.5 Recalculation of Penalty Periods 282

17.5.5.1 Full Refund 282 17.5.5.2 Partial Refund 283 17.5.5.3 Divestments During a Penalty Period 284

76. 17.6 Multiple Divestments ___________________________________________________________________ 286

77. 17.7 Jointly Held Assets _____________________________________________________________________ 288

78. 17.8 Divesting by Paying Relatives ____________________________________________________________ 289 17.8.1 Divesting by Paying Relatives Introduction 290 17.8.2 Room & Board 291

79. 17.9 Income Divestment _____________________________________________________________________ 292

80. 17.10 Life Estates __________________________________________________________________________ 293 17.10.1 Life Estates Introduction 294 17.10.2 Joint Owners 296 17.10.3 Purchase of a Life Estate in the Home of Another Person 297

Table Of Contents

xiii

81. 17.11 Annuities ____________________________________________________________________________ 300 17.11.1 Annuities Purchased Prior to 1/1/09 300 17.11.2 Annuities Purchased On Or After 01/01/09 Or Had Transactions To Them On Or After 01/01/09 302

17.11.2.1 Disclosure 302 17.11.2.2 Remainder Beneficiary Designation 303 17.11.2.3 Additional Divestment Criteria For Unavailable Annuities Owned By The Institutionalized Applicant/ Member 305

82. 17.12 Promissory Notes _____________________________________________________________________ 307 17.12.1 Promissory Notes Prior to 01/01/09 308 17.12.2 Promissory Notes On or After 01/01/09 308

83. 17.13 Trusts _______________________________________________________________________________ 310 17.13.1 Trusts Introduction 310 17.13.2 Revocable Trusts 311 17.13.3 Irrevocable Trusts 311 17.13.4 Exceptions 312

84. 17.14 Both Spouses Institutionalized __________________________________________________________ 315

85. 17.15 Medicaid Card Services ________________________________________________________________ 317 17.15.1 Nursing Home 317 17.15.2 Community Waivers 317

86. 17.16 Gambling ____________________________________________________________________________ 319

87. 17.17 Undue Hardship ______________________________________________________________________ 319 17.17.1 Introduction 320 17.17.2 Hardship Waiver Request Process 320 17.17.3 Valid Request 320 17.17.4 Effective Date of Approved Hardship Waivers 321

17.17.4.1 Timely Request- Received Within 20 days After Notification Is Mailed 321 17.17.4.2 Untimely Request- Received Later Than 20 days After Notification Is Mailed 321

17.17.5 Required Documentation 321 17.17.6 Determination Process Timeframe 322 17.17.7 Bed Hold Payments and Notification 323 17.17.8 Fair Hearing Rights 323 17.17.9 Referral 324

18 Spousal Impoverishment 325

88. 18.1 Spousal Impoverishment Introduction _____________________________________________________ 325

89. 18.2 Spousal Impoverishment Useful Terms ____________________________________________________ 326 18.2.1 Community Spouse 326 18.2.2 Community Spouse Asset Share 326 18.2.3 Institutionalized 326

90. 18.3 Spousal Impoverishment Requirements ___________________________________________________ 327

91. 18.4 Spousal Impoverishment Assets _________________________________________________________ 328 18.4.1 Spousal Impoverishment Assets Introduction 329 18.4.2 Asset Assessment 330

Medicaid Eligibility Handbook (MEH) Release 12-02

xiv

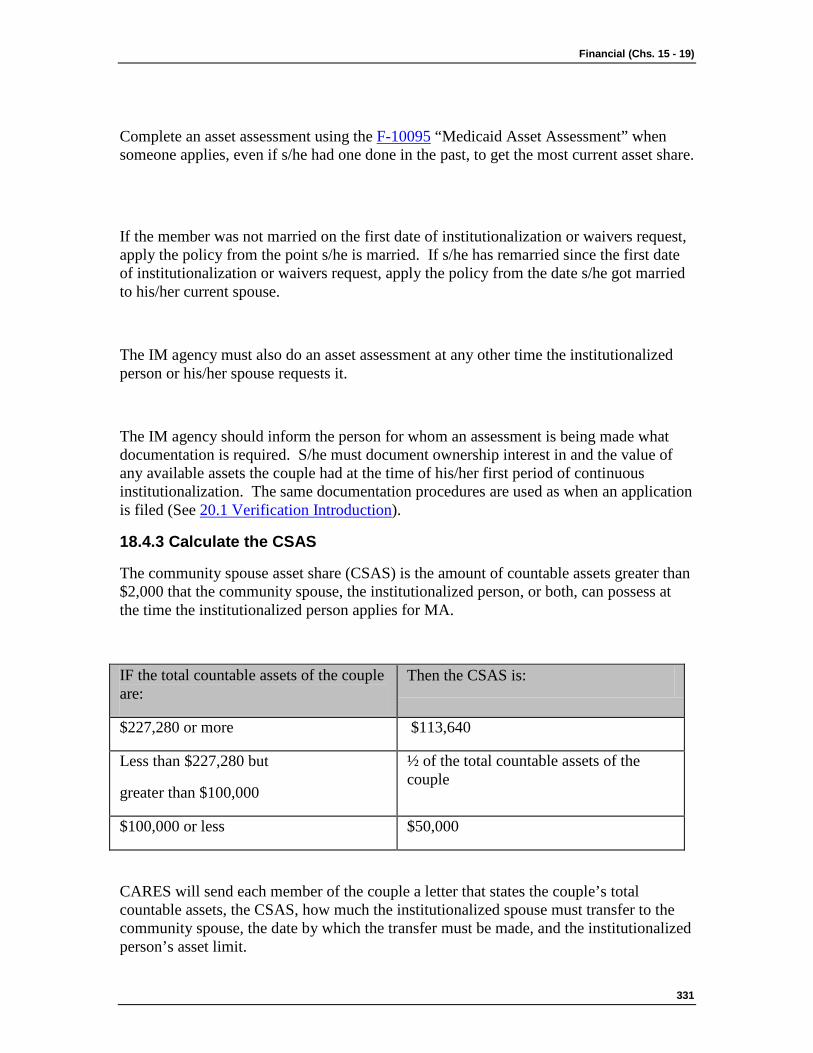

18.4.3 Calculate the CSAS 331 18.4.4 Asset Test 332 18.4.5 Undue Hardship 332 18.4.6 Asset Transfer 332

18.4.6.1 Asset Transfer Period 332 18.4.6.1.1 Leaves Institution or becomes ineligible during the 12 month transfer period. 333 18.4.6.2 Institutionalized Spouse is Eligible after the 12 month transfer period 333 18.4.6.2.1 Leaves Institution for 30 or more days then Re-institutionalized 333 18.4.6.2.2 Loses Medicaid Eligibility But Remains Institutionalized 334 If the institutionalized person reapplies for Medicaid, her/his asset limit would be $2000 and the spouse's assets would not be counted. 334

92. 18.5 Spousal Impoverishment Income _________________________________________________________ 335 18.5.1 Nontrust Income 335 18.5.2 Trust Income 336

93. 18.6 Spousal Impoverishment Income Allocation ________________________________________________ 336 18.6.1 Spousal Impoverishment Income Allocation Introduction 337 18.6.2 Worksheet 7 Section A -- Community Spouse Income Allocation 338 18.6.3 Worksheet 7 Section B -- Family Member Income Allowance 340 18.6.4 Section C -- Cost of Care 340

94. 18.7 Spousal Impoverishment Effective Date ___________________________________________________ 343

95. 18.8 Spousal Impoverishment Notices _________________________________________________________ 344

96. 18.9 Community Spouse's Medicaid Application ________________________________________________ 345 19 Reserved 345

97. Ch. 19 Reserved ___________________________________________________________________________ 345

98. Program Admin. (Chs. 20 - 23)________________________________________________________________ 346 20 Verification 346

99. 20.1 Verification Introduction ________________________________________________________________ 346 20.1.1 Verification Definition 346 20.1.2 Documentation 346 20.1.3 Verification Receipt Date 346

100. ___________________________________________________________________ 20.2 General Rules _________________________________________________________________________ 348

101. ___________________________________________________________________ 20.3 Mandatory Verification Items _____________________________________________________________ 349 20.3.1 Mandatory Verification Items Introduction 350 20.3.2 Social Security Number 350

20.3.2.1 Emergency Services 351 20.3.3 Alien Status 351 20.3.4 Disability 352 20.3.5 Assets 352

20.3.5.1 Divestment 353 20.3.6 Medical Expenses 353 20.3.7 Power of Attorney and Guardianship 353

Table Of Contents

xv

20.3.8 Income 353

102. ___________________________________________________________________ 20.4 Questionable Items _____________________________________________________________________ 355 20.4.1 Questionable Items Introduction 355 20.4.2 Tuberculosis 356 20.4.3 Farm and Self-employment Income 356

103. ___________________________________________________________________ 20.5 Member Responsibility _________________________________________________________________ 357

104. ___________________________________________________________________ 20.6 Front End Verification __________________________________________________________________ 358

105. ___________________________________________________________________ 20.7 When To Verify ________________________________________________________________________ 359 20.7.1 Application and Review 359

20.7.1.1 Application 359 20.7.1.2 Eligibility Reviews 360

20.7.2 Changes 360

106. ___________________________________________________________________ 20.8 Actions _______________________________________________________________________________ 361 20.8.1 Positive Actions 361 20.8.2 Delay 362 20.8.3 Negative Actions 362

107. ___________________________________________________________________ 20.9 Release of Information __________________________________________________________________ 363

108. ___________________________________________________________________ 20.10 Verification Resources _________________________________________________________________ 364

21 Benefits 365

109. ___________________________________________________________________ 21.1 Benefits Introduction ___________________________________________________________________ 365

110. ___________________________________________________________________ 21.2 Full-Benefit Medicaid ___________________________________________________________________ 366

111. ___________________________________________________________________ 21.3 Limited Benefit Medicaid ________________________________________________________________ 366

112. ___________________________________________________________________ 21.4 Covered Services ______________________________________________________________________ 367 21.4.1 Covered Services Introduction 367 21.4.2 Transportation 370

21.4.2.1 Ambulance 370 21.4.2.2 Specialized Medical Vehicle (SMV) 370 21.4.2.3 Common Carrier 371 21.4.2.3.1 Transportation to Out-of-State Providers 371 21.4.2.3.2 Transportation Administration 372 21.4.2.3.3 Reimbursement 372 21.4.2.3.4Transportation Waiver 377

Medicaid Eligibility Handbook (MEH) Release 12-02

xvi

113. ___________________________________________________________________ 21.5 Co-Payment ___________________________________________________________________________ 378

114. ___________________________________________________________________ 21.6 HMO Enrollment _______________________________________________________________________ 379 21.6.1 HMO Enrollment Introduction 380 21.6.2 Exemptions 380 21.6.3 Change of Circumstances 381 21.6.4 Disenrollment 381 21.6.5 HP Enterprise Services Ombuds 381

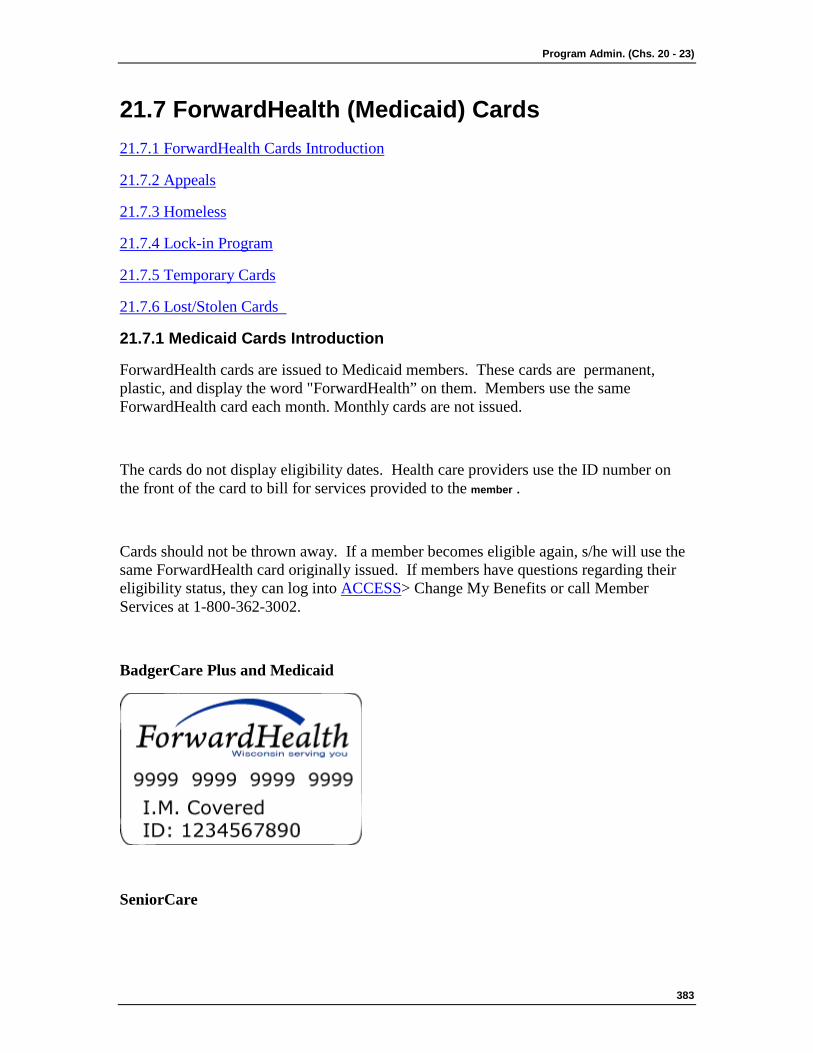

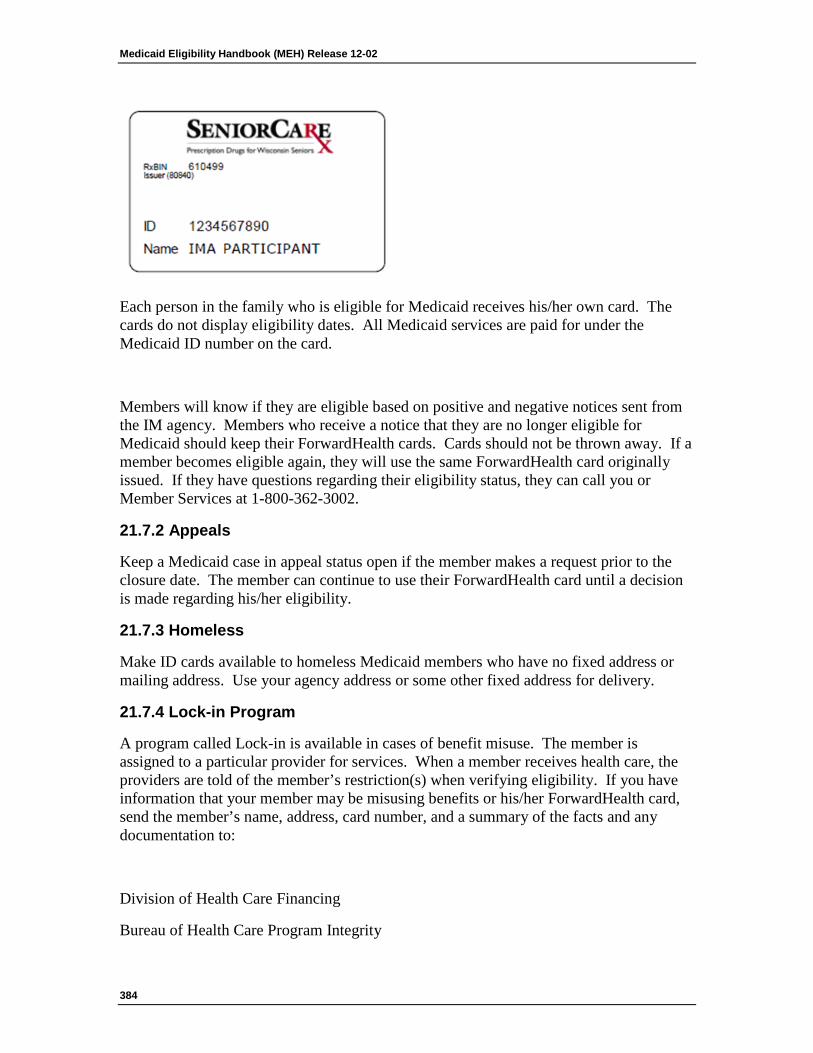

115. ___________________________________________________________________ 21.7 ForwardHealth (Medicaid) Cards __________________________________________________________ 383 21.7.1 Medicaid Cards Introduction 383 21.7.2 Appeals 384 21.7.3 Homeless 384 21.7.4 Lock-in Program 384 21.7.5 Temporary Cards 385 21.7.6 Lost/Stolen Cards 385

116. ___________________________________________________________________ 21.8 Waiver of Medicaid BEnefit Limitations ____________________________________________________ 387

117. ___________________________________________________________________ 21.9 Third Party Coverage ___________________________________________________________________ 387

118. ___________________________________________________________________ 21.10 Good Faith Claims ____________________________________________________________________ 387 21.10.1 Definition of Good Faith Claims 388 21.10.2 Denials 388 21.10.3 Causes and Resolutions 388 21.10.4 Process 390 21.10.5 Instructions 390

22 Administration 394 22.1 Estate Recovery 394

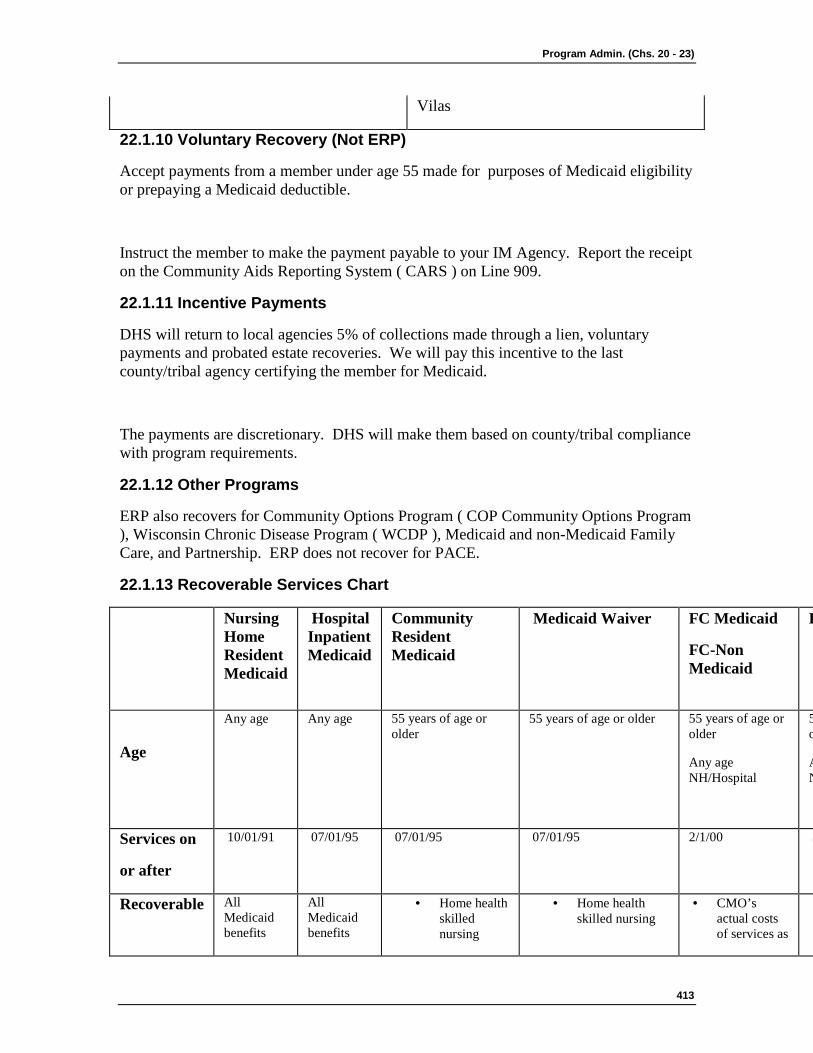

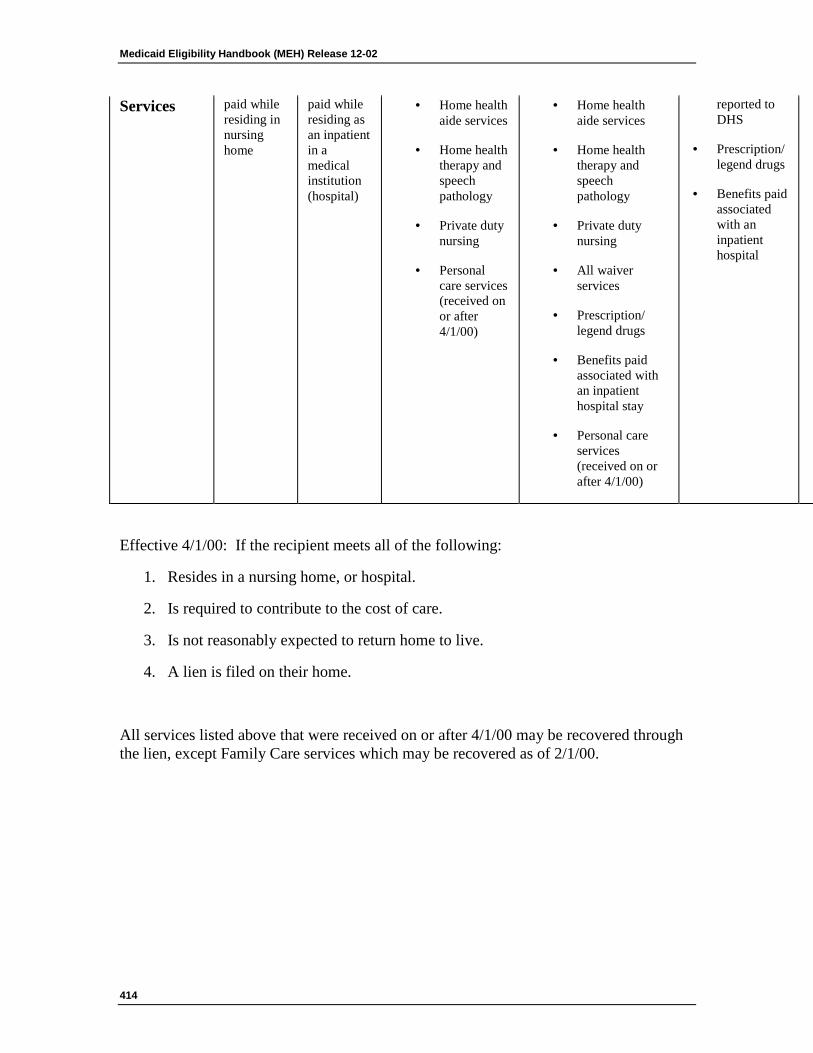

22.1.1 Estate Recovery Program Definition 395 22.1.2 Recoverable Services 395

22.1.2.1 QMB 396 22.1.3 Nursing Home Definition 397 22.1.4 Liens 397

22.1.4.1 Notice of Intent to File a Lien 399 22.1.4.2 Out of State Property 400 22.1.4.3 Returns Home to Live 400 22.1.4.4 Change in Circumstances 401 22.1.4.5 Special Cases 401 22.1.4.6 Adjustment for Burial Trust 401 22.1.4.7 Administrative Hearing: Liens 401 22.1.4.8 Homes Placed in Revocable Trusts 402

22.1.5 Estate Claims 402 22.1.5.1 Waiver of Estate Claim 403 22.1.5.2 Notice of Hardship Waiver Rights 404 22.1.5.3 Administrative Hearings: Hardship Waivers 404 22.1.5.4 Personal Representative’s Report 405 22.1.5.5 Home as Part of the Estate 405 22.1.5.6 Affidavits in Small Sum Estates 407 22.1.5.7 Patient Fund Account 408

Table Of Contents

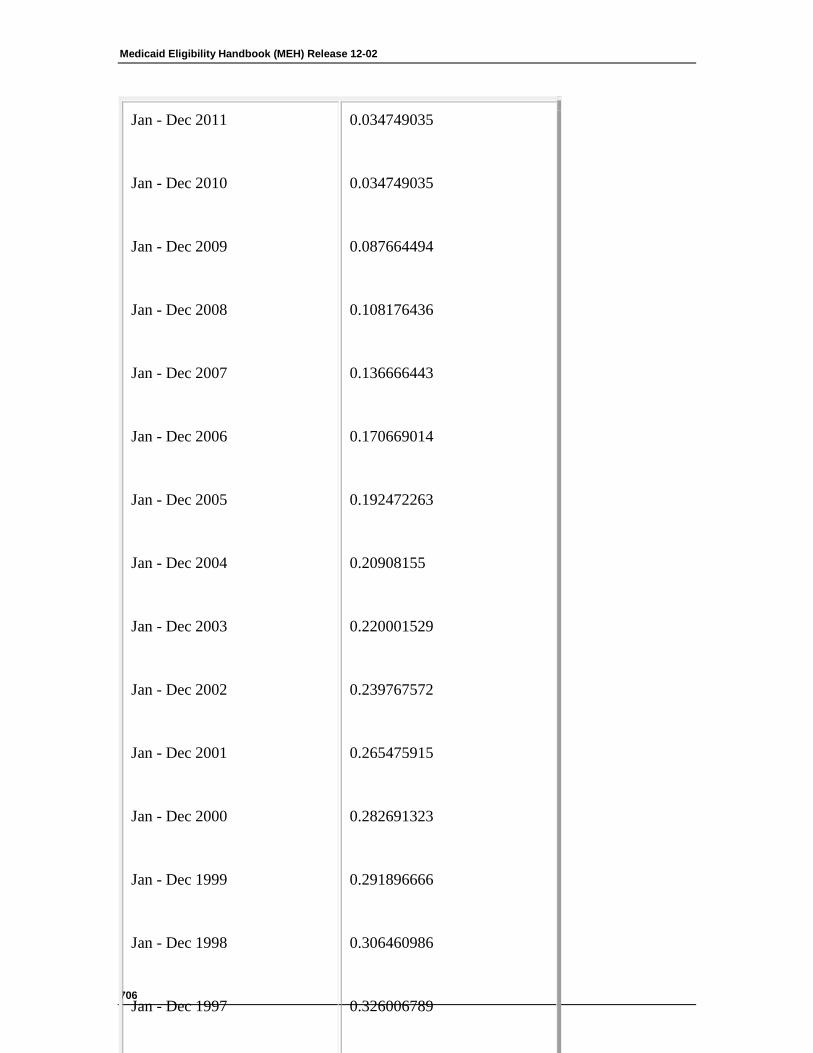

xvii

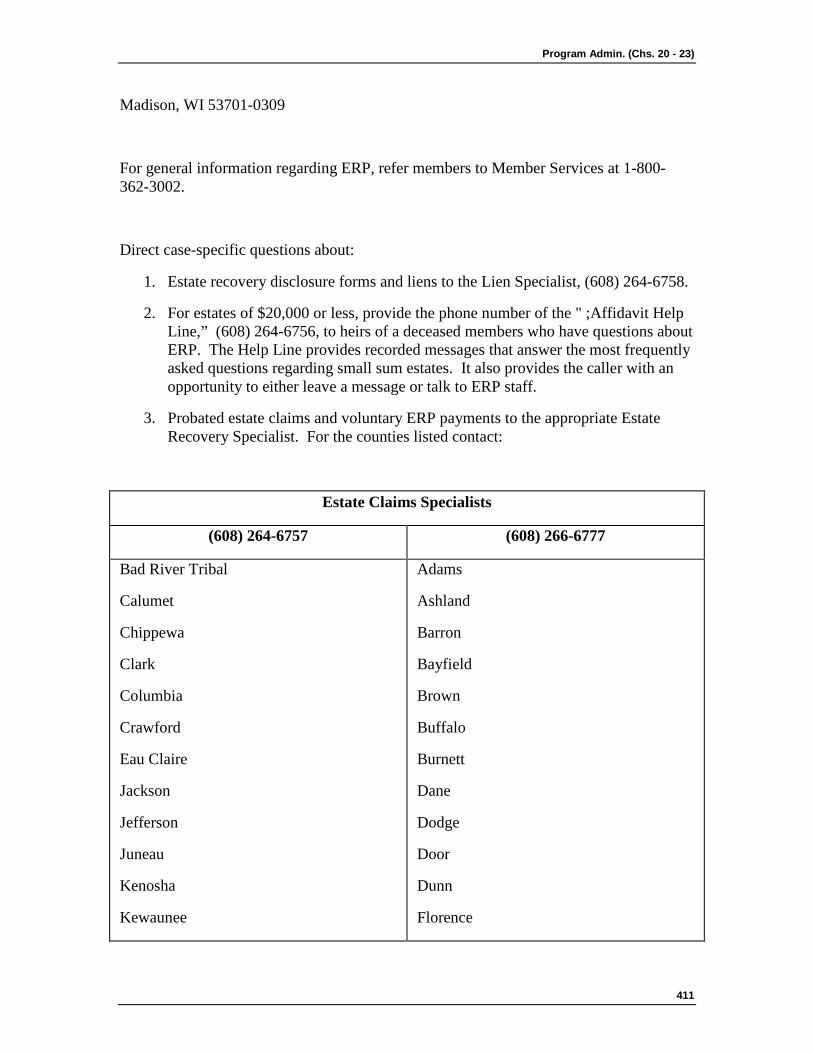

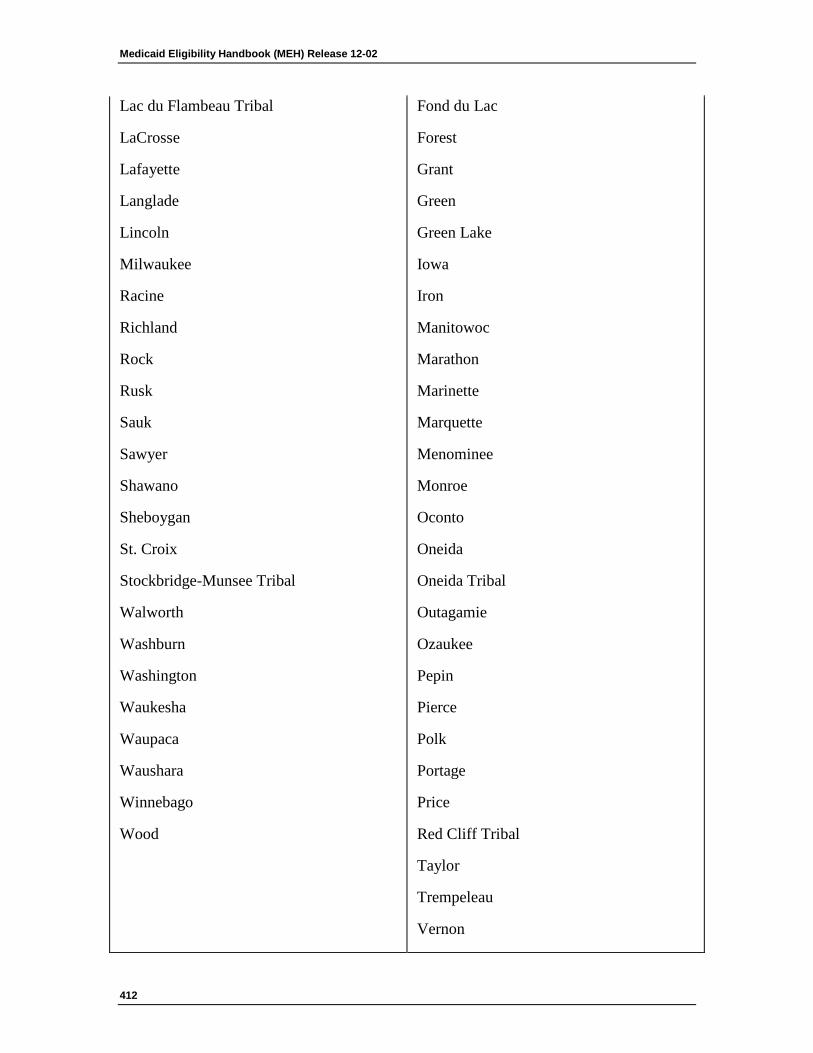

22.1.5.8 Voluntary Recovery (ERP) 408 22.1.6 Match System 409 22.1.7 Notify Members 409 22.1.8 Disclosure Form 409 22.1.9 Estate Recovery Program (ERP) Contacts 410 22.1.10 Voluntary Recovery (Not ERP) 413 22.1.11 Incentive Payments 413 22.1.12 Other Programs 413 22.1.13 Recoverable Services Chart 413

119. ___________________________________________________________________ 22.2 Corrective Action ______________________________________________________________________ 415 22.2.1 Overpayments 416 22.2.1.1 Recoverable Overpayments 416 22.2.1.2 Non-Recoverable Overpayments 419 22.2.2 Overpayment Calculation 420

22.2.2.1 Overpayment Period 420 22.2.2.2 Overpayment Amount 421 22.2.2.2.1 Institutional Overpayments 421 22.2.2.2.1.1 Overpayment as a Result of Misstatement or Omission of Fact 422 22.2.2.3 Deductible 423 22.2.2.4 Premiums 423 22.2.2.4.1 Overpayments for Individuals Eligible for FPW Benefits 424 22.2.2.4.2 Overpayments for QMB cases 424 22.2.2.5 Determining Liable Individual 425

22.2.3 Overpayment Process 425 22.2.3.1 Overpayment Process Introduction 425 22.2.3.2 Member Notice 426

22.2.4 Refer to District Attorney (DA) 426 22.2.5 Fair Hearing 426 22.2.6 Agency Retention 426 22.2.7 Restoration of Benefits 426 22.2.8 Incorrect Member Contribution 427

22.2.8.1 Premiums 427 22.2.8.1.1 BadgerCare 428 22.2.8.1.2 Medicaid Purchase Plan (MAPP) 428

120. ___________________________________________________________________ 22.3 Interagency Case Transfer _______________________________________________________________ 429

23 Reserved 430

121. ___________________________________________________________________ Ch. 19 Reserved ___________________________________________________________________________ 430

122. ___________________________________________________________________ Subprograms (Chs. 24- 38) __________________________________________________________________ 431

24 SSI Related Medicaid and Deductibles 431

Medicaid Eligibility Handbook (MEH) Release 12-02

xviii

123. ___________________________________________________________________ 24.1 SSI Related Medicaid Introduction ________________________________________________________ 431

124. ___________________________________________________________________ 24.2 Medicaid Deductible Introduction _________________________________________________________ 432

125. ___________________________________________________________________ 24.3 Deductible Period ______________________________________________________________________ 433

126. ___________________________________________________________________ 24.4 Choosing Not to Have a Deductible _______________________________________________________ 435

127. ___________________________________________________________________ 24.5 Calculating the Deductible _______________________________________________________________ 437 24.5.1 Fiscal Test Groups 437 24.5.2 Institution Cases 438

24.5.2.1 Backdating 438 24.5.2.2 Deductible 438

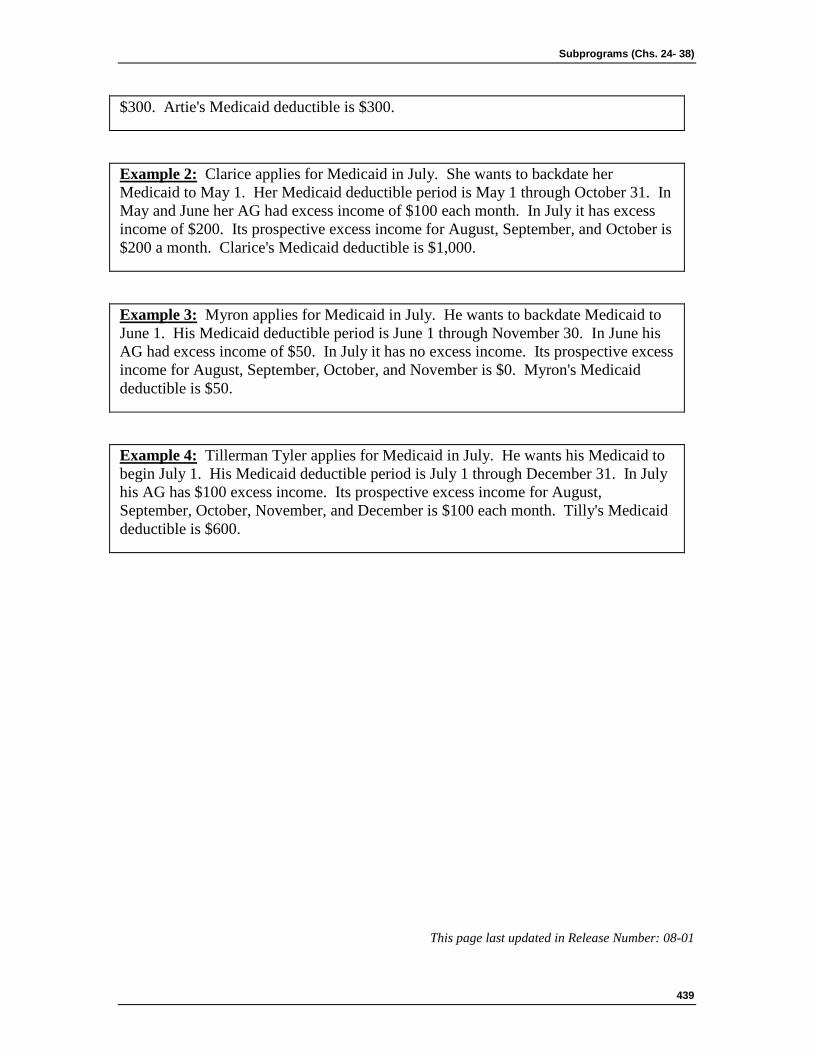

24.5.3 Deductible Examples 438

128. ___________________________________________________________________ 24.6 Changes During the Deductible Period ____________________________________________________ 440 24.6.1 Income Changes 440 24.6.2 Group Size Changes 441 24.6.3 Asset Changes 442 24.6.4 Non-Financial Changes 442

129. ___________________________________________________________________ 24.7 Meeting the Deductible _________________________________________________________________ 443 24.7.1 Countable Costs 443

24.7.1.1 Countable Expenses 446 24.7.2 Noncountable Costs 450 24.7.3 Prepaying a Deductible 451

24.7.3.1 Payment of Entire Deductible Amount 452 24.7.3.2 Combination of Payment and Incurred Expenses 452 24.7.3.3 Combination of Payment and Outstanding Expenses 453 24.7.3.4 Calculation Errors 453 24.7.3.5 Insufficient Funds 453

130. ___________________________________________________________________ 24.8 Order of Bill Deduction _________________________________________________________________ 454 24.8.1 Hospital Bills 455 24.8.2 Pregnancy Fees 455

Table Of Contents

xix

131. ___________________________________________________________________ 24.9 Notice to Fiscal Agent __________________________________________________________________ 456

132. ___________________________________________________________________ 24.10 Late Reporting of Deductible Information _________________________________________________ 457

133. ___________________________________________________________________ 24.11 Deductibles and Inter-Agency Transfers __________________________________________________ 457

134. ___________________________________________________________________ 24.12 Changes After Meeting a Deductible _____________________________________________________ 458 24.12.1 Changes After Meeting a Deductible Introduction 458 24.12.2 Income Changes 458 24.12.3 Asset Changes 458 24.12.4 Non-Financial Changes 458

135. ___________________________________________________________________ 24.13 Death During a Deductible Period ________________________________________________________ 459 24.13.1 Death During a Deductible Period Introduction 460 24.13.2 Prepaid Deductible 460

136. ___________________________________________________________________ 24.14 Medicaid Deductible, Cost of Care _______________________________________________________ 461

25 Special Status Medicaid 461

137. ___________________________________________________________________ 25.1"503" Eligibility ________________________________________________________________________ 461 25.1.1 503 Introduction 461 25.1.2 Identifying a "503" AG 462 25.1.3 Calculating the COLA Disregard 463

138. ___________________________________________________________________ 25.2 Disabled Adult Child (DAC) ______________________________________________________________ 464 25.2.1 DAC Introduction 465 25.2.2 DAC Payment Disregard 465 25.2.3 COLA Disregard 466 25.2.4 Disregards For Individuals Who Lose SSI Eligibility As A Result of Initial Receipt Or An Increase In DAC Benefits 466

139. ___________________________________________________________________ 25.3 Widows & Widowers ____________________________________________________________________ 468

140. ___________________________________________________________________ 25.4 Medicaid Deductible, Cost of Care ________________________________________________________ 469

141. ___________________________________________________________________ 25.5 1619 Cases ___________________________________________________________________________ 469

142. ___________________________________________________________________ 25.6 Katie Beckett __________________________________________________________________________ 470

143. ___________________________________________________________________ 25.7 Tuberculosis __________________________________________________________________________ 471 25.7.1 Non-Financial Requirements 471 25.7.2 Financial Tests 472

Medicaid Eligibility Handbook (MEH) Release 12-02

xx

25.7.3 TB-Related Services 473 25.7.4 QMB, SLMB and QDWI 474 25.7.5 Aliens 474 25.7.6 Processing 474

144. ___________________________________________________________________ 25.8 Migrant workers _______________________________________________________________________ 475 25.8.1 Migrant Workers Introduction 476 25.8.2 Simplified Application 476 25.8.3 Regular Application 478 25.8.4 Reviews 478

25.8.4.1 Simplified Application 478 25.8.4.2 Regular Application 478

26 Medicaid Purchase Plan (MAPP) 479

145. ___________________________________________________________________ 26.1 Medicaid Purchase Plan (MAPP) Introduction _______________________________________________ 479

146. ___________________________________________________________________ 26.2 MAPP Application ______________________________________________________________________ 481 26.2.1 Begin Month 481 26.2.2 Fiscal Test Group ( FTG ) 481

147. ___________________________________________________________________ 26.3 MAPP Non-Financial Requirements _______________________________________________________ 482 26.3.1 MAPP Nonfinancial Requirements Introduction 483 26.3.2 Disability 483 26.3.3 Work Requirement 484

26.3.3.1 Self-Employment 484 26.3.3.2 Contractual Employment 484 26.3.3.3 Employment Ending 484 26.3.3.4 Temporary Employment 484

26.3.4 Work Requirement Exemption 485 26.3.5 Health and Employment Counseling Program ( HEC ) 485

26.3.5.1 HEC Processing 486 Beginning January 1, 2012 there will be no HEC specialists around the state. Individuals wishing to enroll in HEC will be required to fill out the MAPP Employment Plan form (http://www.dhs.wisconsin.gov/forms/F0/f00004.doc) and send it to the Department of Health Services MAPP Unit at the address below. A final approval/disapproval decision will be made by that unit within 10 working days. 486 26.3.5.2 HEC Extension 487 26.3.5.3 HEC Participation Changes 487

26.3.6 Health Insurance Premium Payment (HIPP) 487 26.3.7 Spousal Impoverishment 487 26.3.8 Institutionalization 487 26.3.9 Community Waivers 487

26.3.9.1 Special Managed Care Programs 488

148. ___________________________________________________________________ 26.4 MAPP Financial Requirements ___________________________________________________________ 489 26.4.1 Assets 489

26.4.1.1 Independence Accounts 489 26.4.1.2 Independence Account Exemption Status 490 26.4.1.3 Pension or Retirement Accounts 491

26.4.2 Income 491

Table Of Contents

xxi

149. ___________________________________________________________________ 26.5 MAPP Premiums _______________________________________________________________________ 492 26.5.1 Calculation 493

26.5.1.1 Penalty 494 26.5.2 Initial Premium 495 26.5.3 Payment Information 496

26.5.3.1 Payment Methods 496 26.5.3.2 Advance Payments 496 26.5.3.3 Refunds 496

26.5.4 Ongoing Cases 497 26.5.5 Late Payments 497

26.5.5.1 Between Due Date and Adverse Action of the Benefit Month 497 26.5.5.2 Between Adverse Action of the Benefit Month and the Last Day of Benefit Month 497 26.5.5.3 Anytime in Month After the Benefit Month 498 26.5.5.4 Two Months After the Benefit Month 498

26.5.6 Non-Payment 498 26.5.6.1 Insufficient Funds 498

26.5.7 Opting Out 499

150. ___________________________________________________________________ 26.6 MAPP Restrictive Re-enrollment Period (RRP) ______________________________________________ 500 26.6.1 MAPP RRP Introduction 500 26.6.2 Good Cause 501

151. ___________________________________________________________________ 26.7 MAPP Changes ________________________________________________________________________ 501 26.7.1 MAPP Changes Introduction 502 26.7.2 Reduced Premiums or No Premiums 502

152. ___________________________________________________________________ 26.8 MAPP Prepaid Deductibles ______________________________________________________________ 503

153. ___________________________________________________________________ 26.9 MAPP Notices _________________________________________________________________________ 503

154. ___________________________________________________________________ 26.10 MAPP / Health and Employment Counseling Program (HEC) Specialists _______________________ 504

27 Institutional Long Term Care (ILTC) 505

155. ___________________________________________________________________ 27.1 Institutions ___________________________________________________________________________ 505 27.1.1 Institutions Introduction 505 27.1.2 Institutions for Mental Disease 506

27.1.2.1 Eligible Age 506 27.1.2.2 Temporary Leave 506 27.1.2.3 Minors in IMD 507

27.1.3 Hospitals 507

Medicaid Eligibility Handbook (MEH) Release 12-02

xxii

156. ___________________________________________________________________ 27.2 ILTC Licensing and Certification __________________________________________________________ 508

157. ___________________________________________________________________ 27.3 Facilities Not Medicaid Certified __________________________________________________________ 509

158. ___________________________________________________________________ 27.4 ILTC Definitions________________________________________________________________________ 509 27.4.1 Institutionalized Person 509 27.4.2 Community Spouse 509 27.4.3 SSI Recipient and Institutional Medicaid application 510

159. ___________________________________________________________________ 27.5 ILTC Financial _________________________________________________________________________ 511 27.5.1 ILTC Assets 511 27.5.2 ILTC Income 512 27.5.3 Divestment 512 27.5.4 Instructions for Manual Eligibility Determinations 512

160. ___________________________________________________________________ 27.6 ILTC Monthly Need _____________________________________________________________________ 514 27.6.1 ILTC Monthly Need Introduction 515 27.6.2 Hospitalized Persons 515 27.6.3 Both Spouses Institutionalized 515 27.6.4 Health Insurance 515

27.6.4.1 Nursing Home and Hospital Insurance 516 27.6.4.2 Assignment of Nursing Home and Hospital Insurance Payments 516

27.6.5 Support Payments 516 27.6.6 Fees to Guardians or Attorneys 516

161. ___________________________________________________________________ 27.7 ILTC Cost of Care Calculation ____________________________________________________________ 517 27.7.1 ILTC Cost of Care Calculation Introduction 518 27.7.2 Hospitalized Persons 519 27.7.3 Managed Care Programs 519 27.7.4 Partial Months 519

27.7.4.1 Death 520 27.7.4.2 Community and Nursing Home 520

27.7.5 Transfers Between Institutions 520 27.7.6 Retroactive Cost of Care 521 27.7.7 Personal Needs Allowance 521 27.7.8 Medical/Remedial Expenses and Payments for Non-Covered Services 521 27.7.8.1 Introduction 521 27.7.8.2 Disallowed Expenses 523

Table Of Contents

xxiii

162. ___________________________________________________________________ 27.8 ILTC Nursing Home Contracts ____________________________________________________________ 525

163. ___________________________________________________________________ 27.9 ILTC Nursing Home Refunds _____________________________________________________________ 527

164. ___________________________________________________________________ 27.10 ILTC Liability Effective Dates ____________________________________________________________ 527

165. ___________________________________________________________________ 27.11 Institutions for Mental Disease (IMDs) ____________________________________________________ 528

28 Home and Community Based Waivers Long Term Care (HCBWLTC) 530

166. ___________________________________________________________________ 28.1 Home and Community Based Waivers Long Term Care (HCBWLTC) Introduction _________________ 530

167. ___________________________________________________________________ 28.2 Home and Community Based Waivers Long Term Care (HCBWLTC) Application __________________ 532 28.2.1 Case Manager 532 28.2.2 Spousal Impoverishment 532 28.2.3 Minors 532 28.2.4 Tentative Approval 533

168. ___________________________________________________________________ 28.3 Home and Community Based Waivers Long Term Care (HCBWLTC) Fiscal test group _____________ 534

169. ___________________________________________________________________ 28.4 Home and Community Based Waivers Long Term Care (HCBWLTC) Divestment __________________ 534

Note: Effective 10/01/09, assets are no longer counted for disabled or institutionalized children. Since assets are disregarded, there can be no divestment in a Medicaid case for a child. 535

170. ___________________________________________________________________ 28.5 Home and Community Based Waivers Long Term Care (HCBWLTC) Cost Sharing ________________ 535 28.5.1 HCBWLTC Cost Sharing Introduction 535 28.5.2 Spenddown 535

171. ___________________________________________________________________ 28.6 Home and Community Based Waivers Long Term Care (HCBWLTC) Uniform Fee System __________ 536

172. ___________________________________________________________________ 28.7 Home and Community Based Waivers Long Term Care (HCBWLTC) Effective Date ________________ 537

173. ___________________________________________________________________ 28.8 Home and Community Based Waivers Long Term Care (HCBWLTC) Instructions _________________ 537 28.8.1 HCBWLTC Instructions Introduction 538 28.8.2 Group A 539 28.8.3 Group B 539

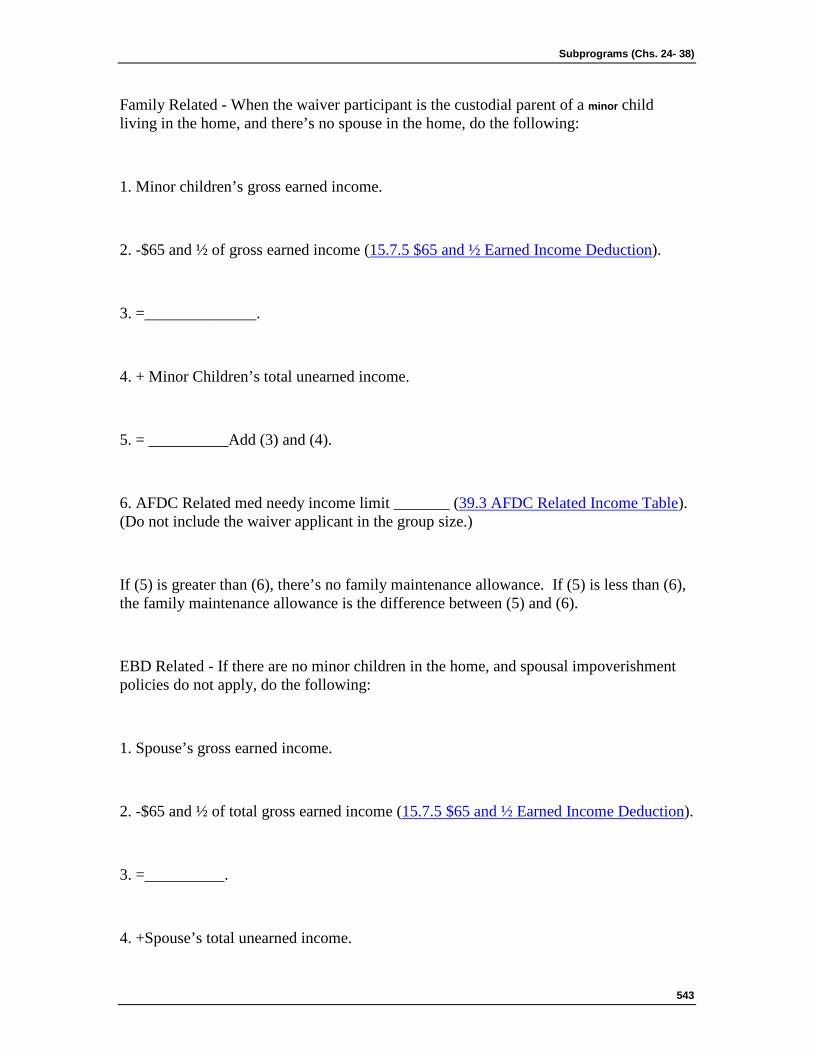

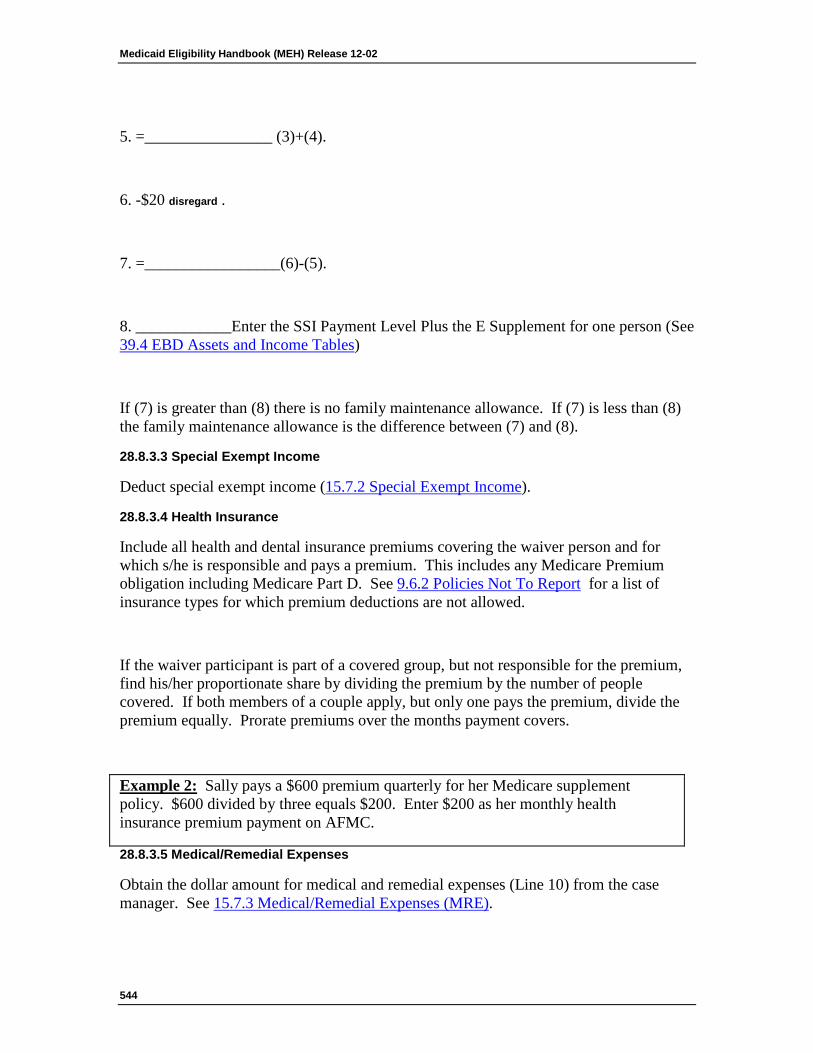

28.8.3.1 Personal Maintenance Allowance 539 28.8.3.2 Family Maintenance Allowance 542 28.8.3.3 Special Exempt Income 544 28.8.3.4 Health Insurance 544 28.8.3.5 Medical/Remedial Expenses 544 28.8.3.6 Cost Share Amount 545

28.8.4 Group C 545

Medicaid Eligibility Handbook (MEH) Release 12-02

xxiv

174. ___________________________________________________________________ 28.9 Home and Community Based Waivers Long Term Care (HCBWLTC) Medical Codes _______________ 546

175. ___________________________________________________________________ 28.10 Home and Community Based Waivers Long Term Care (HCBWLTC) Review ____________________ 546

176. ___________________________________________________________________ 28.11 Home and Community Based Waivers Long Term Care (HCBWLTC) Community Spouse's Medicaid Application _______________________________________________________________________________ 547

177. ___________________________________________________________________ 28.12 Home and Community Based Waivers Long Term Care (HCBWLTC) Notices ____________________ 547

178. ___________________________________________________________________ 28.13 Home and Community Based Waivers Long Term Care (HCBWLTC) Transfers __________________ 548

179. ___________________________________________________________________ 28.14 Home and Community Based Waivers Long Term Care (HCBWLTC) Children's Long Term Care (CLTC)548 28.14.1 CLTC Introduction 548 28.14.2 CLTC CARES Processing 549

29 Family Care Long Term Care (FCLTC) 551

180. ___________________________________________________________________ 29.1 Family Care Long Term Care (FCLTC) Introduction __________________________________________ 551

181. ___________________________________________________________________ 29.2 FCLTC Administration __________________________________________________________________ 551

182. ___________________________________________________________________ 29.3 FCLTC Medicaid and Non-Medicaid _______________________________________________________ 552 29.3.1 Family Care Medicaid 552 29.3.2 Family Care Non-Medicaid (MA) 554

183. ___________________________________________________________________ 29.4 FCLTC Functional Eligibility _____________________________________________________________ 555

184. ___________________________________________________________________ 29.5 FCLTC Enrollment/Disenrollment and Intercounty Moves _____________________________________ 556 29.5.1 Enrollments 556

29.5.1.1 Urgent Services 556 29.5.1.2 SSI Recipients 557

29.5.2 Disenrollment 557 29.5.2.1 ADRC Approved Disenrollments 557 29.5.2.2 Adverse Action Disenrollment 559 29.5.2.3 Death Of A Family Care Participant & Disenrollment 559 29.5.2.4 Non-Payment Of Cost Share & Disenrollment 559

29.5.3 Re-enrollment in Family Care 560 29.5.4 Inter-county Moves 562

185. ___________________________________________________________________ 29.6 FCLTC Closures _______________________________________________________________________ 563

186. ___________________________________________________________________ 29.7 FCLTC Enrollment and Cost Share Reports ________________________________________________ 564 29.7.1 Enrollment Reports 564

Table Of Contents

xxv

29.7.1.1 Initial Enrollment Report 564 29.7.1.2 Final Enrollment Report 565 29.7.1.3 When the IM Agency Should Contact the MCO/ Enrollment Reports 565

29.7.2 Cost Share Report 566 29.7.2.1 When Agencies Should Contact the MCO/Cost Share Report 566

30 Partnership Long Term Care 567

187. ___________________________________________________________________ 30.1 Partnership Long Term Care _____________________________________________________________ 567

188. ___________________________________________________________________ 30.2 Partnership Administration ______________________________________________________________ 568

189. ___________________________________________________________________ 30.3 Partnership Medicaid Eligibility __________________________________________________________ 569 30.3.1 Partnership Medicaid Eligibility Introduction 569 30.3.2 Non-Institutional Cases 570 30.3.3 Institutional Cases 570

190. ___________________________________________________________________ 30.4 Partnership Functional Eligibility _________________________________________________________ 571

191. ___________________________________________________________________ 30.5 Partnership Enrollment/Disenrollment and Intercounty Moves _________________________________ 572 30.5.1 Enrollments 572

30.5.1.1 SSI Recipients 572 30.5.2 Disenrollment 573

30.5.2.1 ADRC Approved Disenrollments 573 30.5.2.2 Adverse Action Disenrollment 575 30.5.2.3 Death Of A Partnership Participant & Disenrollment 576 30.5.2.4 Non-Payment Of Cost Share & Disenrollment 576 30.5.3 Re-enrollment In Partnership 576 30.5.3.1 Request For Retroactive Enrollment 578

30.5.4 InterCounty Moves 578

192. ___________________________________________________________________ 30.6 Partnership Closures ___________________________________________________________________ 580

193. ___________________________________________________________________ 30.7 Partnership Enrollment and Cost Share Reports ____________________________________________ 581 30.7.1 Enrollment Reports 581

30.7.1.1 Initial Enrollment Report 581 30.7.1.2 Final Enrollment Report 582 30.7.1.3 When the IM Agency Should Contact the MCO/ Enrollment Reports 582 30.7.2 Cost Share Report 583 30.7.2.1 When Agencies Should Contact the MCO/Cost Share Report 583

31 PACE (Program of All-Inclusive Care for the Elderly) 585

194. ___________________________________________________________________ 31 PACE (Program of All-Inclusive Care for the Elderly) __________________________________________ 585

32 Medicare Savings Programs (MSP) 586

195. ___________________________________________________________________ 32.1 Medicare Savings Programs (MSP) _______________________________________________________ 586 32.1.1 Medicare Savings Programs (MSP) Introduction 586

Medicaid Eligibility Handbook (MEH) Release 12-02

xxvi

32.1.2 MSP Fiscal Test Group 587 32.1.3 MSP Benefits 587 32.1.4 LIS Requests 587 32.1.5 Part B Enrollment Via The MSP Buy-In Program 588

196. ___________________________________________________________________ 32.2 QMB (Qualified Medicare Beneficiary) _____________________________________________________ 589 32.2.1 QMB Introduction 589 32.2.2 Entitled to Medicare 590 32.2.3 QMB Income Limit 591

197. ___________________________________________________________________ 32.3 Specified Low-Income Medicare Beneficiary (SLMB) _________________________________________ 594 32.3.1 SLMB Introduction 594 32.3.2 SLMB Income Limit 595

198. ___________________________________________________________________ 32.4 Specified Low-Income Medicare Beneficiary Plus (SLMB+) ___________________________________ 596 32.4.1 SLMB+ Introduction 596 32.4.2 SLMB+ Income Limit 596

199. ___________________________________________________________________ 32.5 Qualified Disabled and Working Individual (QDWI) ___________________________________________ 597 32.5.1 QDWI Introduction 597 32.5.2 QDWI Income Limit 597

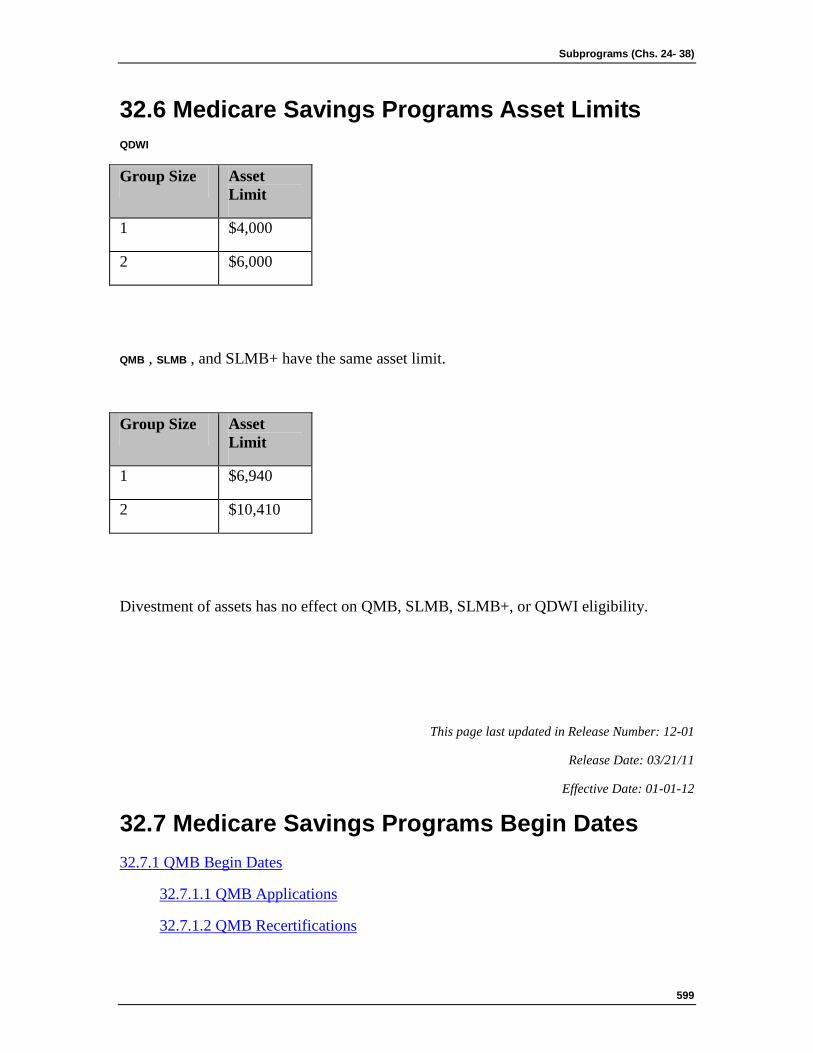

200. ___________________________________________________________________ 32.6 Medicare Savings Programs Asset Limits __________________________________________________ 599

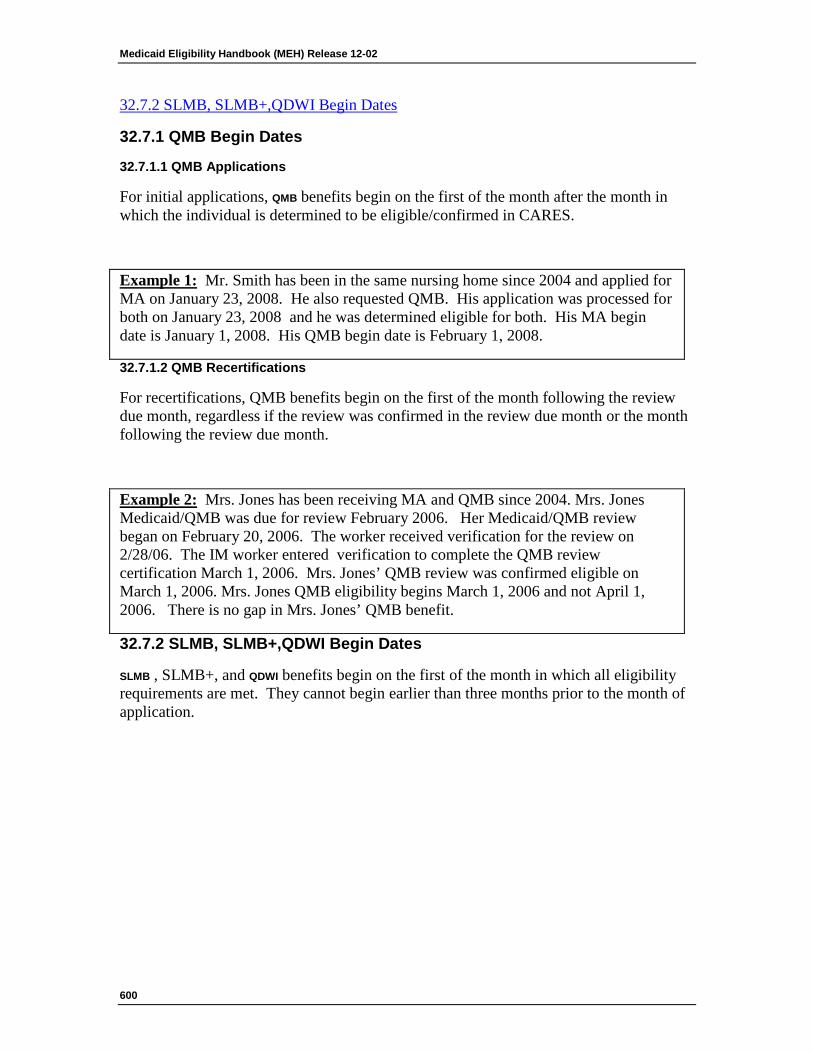

201. ___________________________________________________________________ 32.7 Medicare Savings Programs Begin Dates __________________________________________________ 599 32.7.1 QMB Begin Dates 600

32.7.1.1 QMB Applications 600 32.7.1.2 QMB Recertifications 600

32.7.2 SLMB, SLMB+,QDWI Begin Dates 600

202. ___________________________________________________________________ 32.8 Medicare Savings Programs Backdating ___________________________________________________ 601 32.8.1 QMB Backdating 602 32.8.2 SLMB, SLMB+, QDWI Backdating 602

203. ___________________________________________________________________ 32.9 Medicare Savings Programs No Deductible ________________________________________________ 603

204. ___________________________________________________________________ 32.10 Medicare Savings Programs Reviews ____________________________________________________ 604

205. ___________________________________________________________________ 32.11 Potential Adverse Effect of MSP Participation ______________________________________________ 605

33 SeniorCare (SC) 606

Table Of Contents

xxvii

206. ___________________________________________________________________ 33.1 SeniorCare (SC) Introduction ____________________________________________________________ 606

207. ___________________________________________________________________ 33.2 SC Application ________________________________________________________________________ 608 33.2.1 SC Application Introduction 608 33.2.2 Application Processing 609 33.2.3 Signing the Application 610

33.2.3.1 Witnessing the Signature 610 33.2.4 Authorized Representative 610 33.2.5 Guardian and Power of Attorney 611

208. ___________________________________________________________________ 33.3 SC Nonfinancial Requirements ___________________________________________________________ 611 33.3.1 SC Nonfinancial Requirements Introduction 612 33.3.2 Enrollment Fee 614

33.3.2.1 Refunds 614 33.3.2.2 Refunds to Deceased Participants 616 33.3.2.3 Opt In 616

33.3.3 Age Limitation 616 33.3.4 Other Insurance 617

209. ___________________________________________________________________ 33.4 SC Fiscal Test Group (FTG) ______________________________________________________________ 618

210. ___________________________________________________________________ 33.5 SC Benefit Period ______________________________________________________________________ 618 33.5.1 SC Benefit Period Introduction 619 33.5.2 ID Cards 619 33.5.3 Eligibility Begin Date 619

211. ___________________________________________________________________ 33.6 SC Financial Requirements ______________________________________________________________ 621 33.6.1 Assets 622 33.6.2 Income 622 33.6.3 Gross Social Security 623 33.6.4 Gross Earnings 623 33.6.5 Interest and Dividends 624

33.6.5.1 Capital Gains 625 33.6.5.2 Trusts 625 33.6.5.3 Joint Savings 625

33.6.6 Self-Employment Earnings 625 33.6.6.1 Rental Income 626

33.6.7 Gross Pension 626 33.6.7.1 Retirement Benefits 626

33.6.8 Other Income 627 33.6.8.1 Allocated Income from a Medicaid Recipient’s Spouse 628 33.6.8.2 Farm Subsidy 628 33.6.8.3 Rental Income 628 33.6.8.4 Veterans Disability 628

33.6.9 Disregarded Income 629

212. ___________________________________________________________________ 33.7 SC Participation Levels _________________________________________________________________ 632

See 39.11 SeniorCare Income Limits 632

Medicaid Eligibility Handbook (MEH) Release 12-02

xxviii

213. ___________________________________________________________________ 33.8 SC Countable Costs ____________________________________________________________________ 632 33.8.1 SC Countable Costs Introduction 632 33.8.2 Carryover 633 33.8.3 Date of Purchase 634

214. ___________________________________________________________________ 33.9 SC Addition of a Spouse ________________________________________________________________ 635 33.9.1 SC Addition of a Spouse Introduction 635 33.9.2 Adding a Spouse No Change in FTG 637

33.9.2.1 Adding A Spouse, No FTG Change, At Levels 2a and 2b 637 33.9.2.2 Adding A Spouse, No FTG Change, At level 3 638 33.9.2.2.1 Unmet Spenddown 638 33.9.2.2.2 Met Spenddown 640

33.9.3 FTG Changes 641 33.9.3.1 FTG Changes at Level 2a and 2b 642 33.9.3.2 FTG Changes At Level 3 642

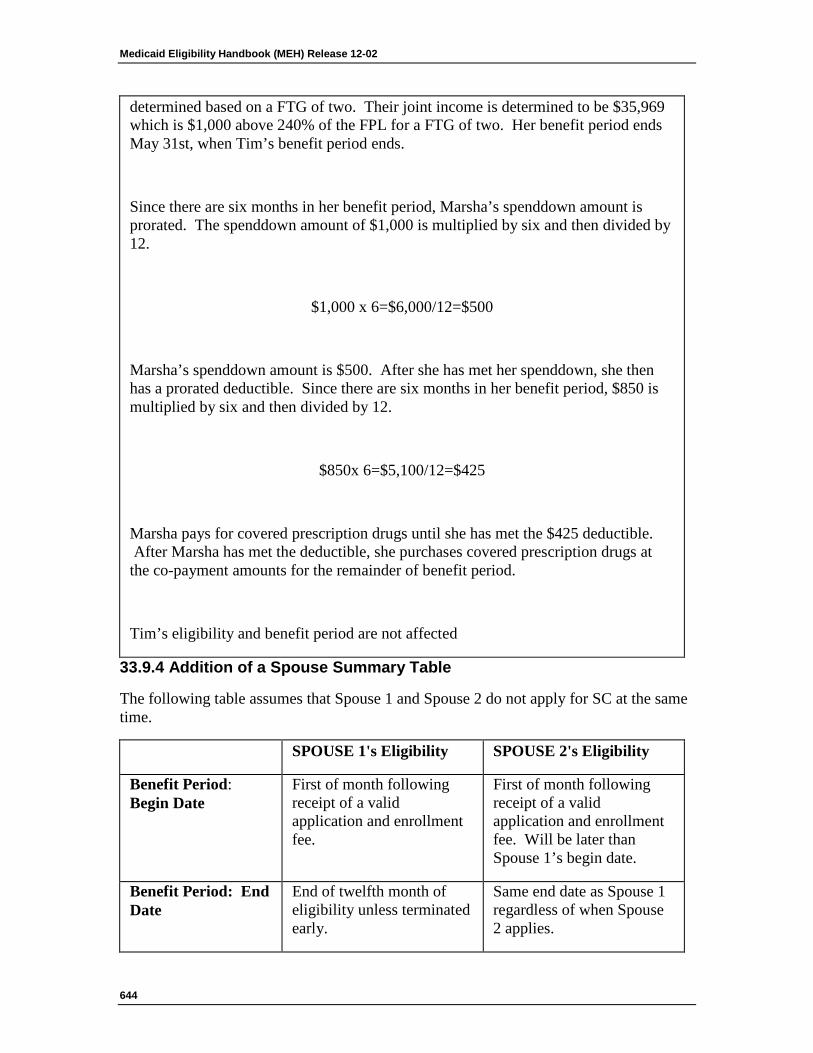

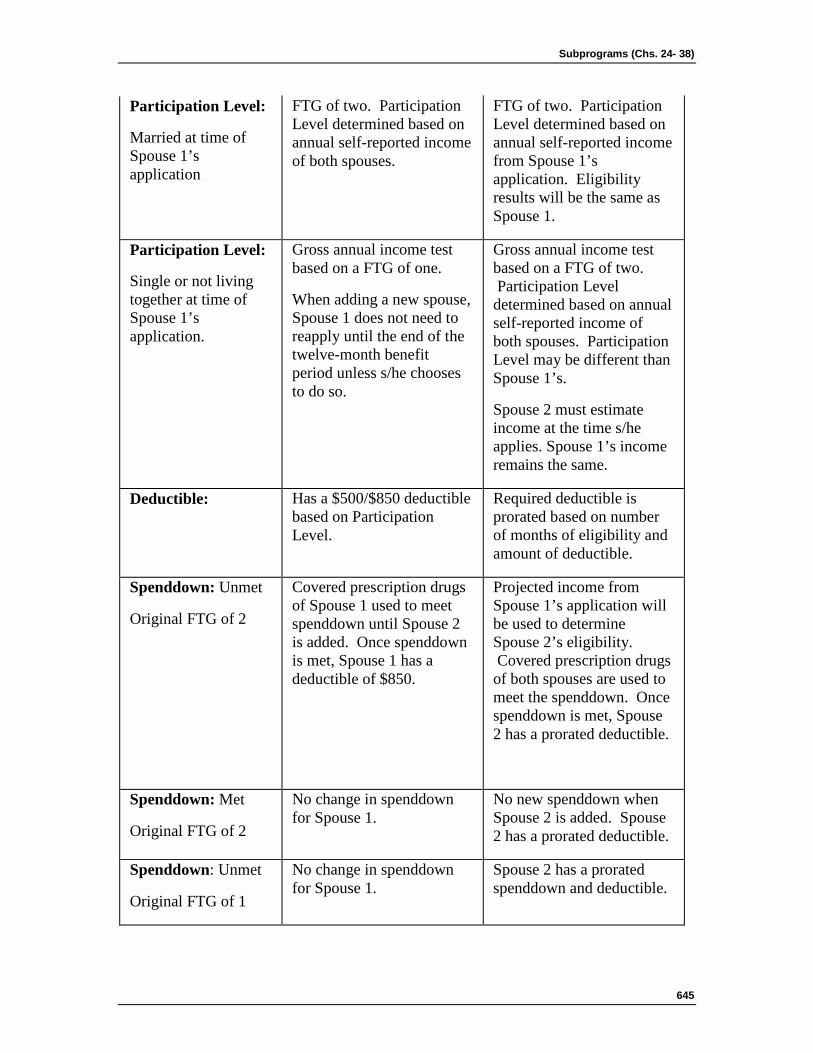

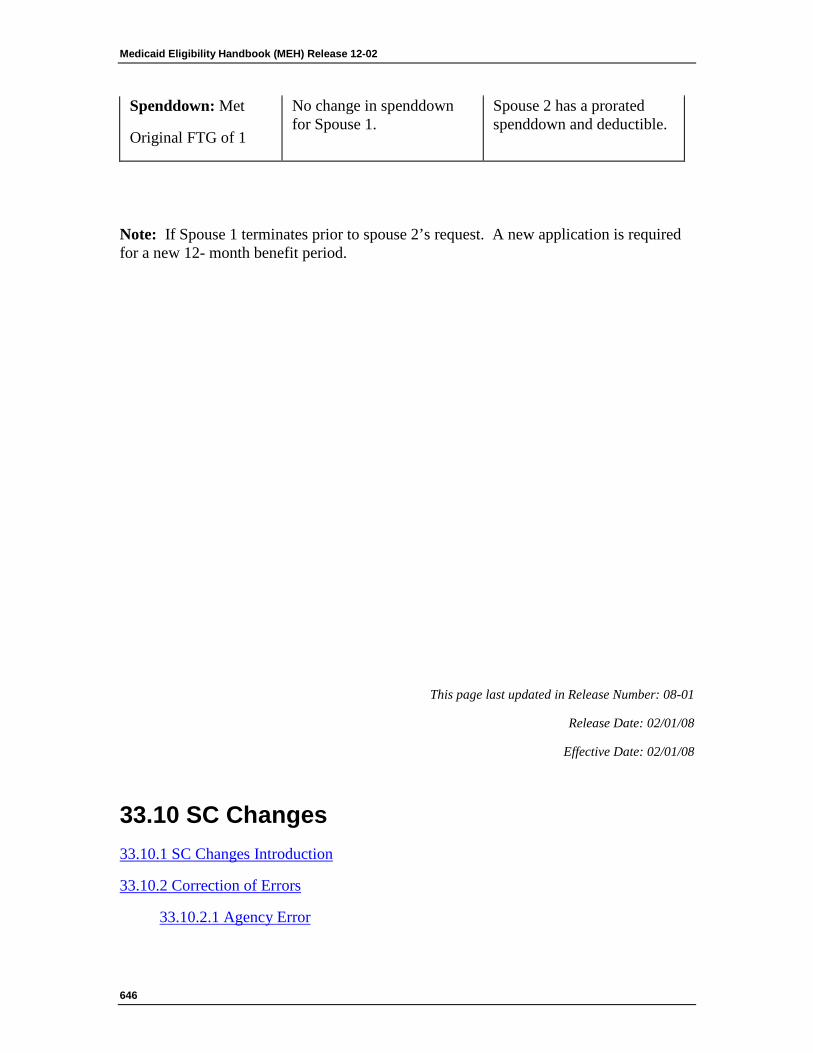

33.9.4 Addition of a Spouse Summary Table 644

215. ___________________________________________________________________ 33.10 SC Changes __________________________________________________________________________ 646 33.10.1 SC Changes Introduction 647 33.10.2 Correction of Errors 649

33.10.2.1 Agency Error 650 33.10.2.2 Applicant/Participant Error 650

33.10.3 Fraud 652

216. ___________________________________________________________________ 33.11 SC Re-Application _____________________________________________________________________ 653

217. ___________________________________________________________________ 33.12 SC Early Termination __________________________________________________________________ 654 33.12.1 SC Early Termination 654 33.12.2 Withdrawal 655

218. ___________________________________________________________________ 33.13 SC Notice of Decision _________________________________________________________________ 657

219. ___________________________________________________________________ 33.14 SC Appeals __________________________________________________________________________ 658 33.14.1 SC Appeals Introduction 658 33.14.2 Requesting a Hearing 659 33.14.3 Hearing 659

220. ___________________________________________________________________ 33.15 SC Annual Eligibility Review ____________________________________________________________ 660

221. ___________________________________________________________________ 33.16 SC Benefits __________________________________________________________________________ 661 33.16.1 SC Benefits Introduction 661 33.16.2 Discount Pricing 662 33.16.3 Early Refills 662 33.16.4 Out-of-state Pharmacies 662

34 Emergency Services 664

Table Of Contents

xxix

222. ___________________________________________________________________ 34.1 Emergency Services ____________________________________________________________________ 664 34.1.1 Emergency Services Eligibility Introduction 664 34.1.2 Determination of Emergency Services Eligibility 665

34.1.2.1 Medicaid Deductible 666 34.1.3 Certification of Emergency Services Eligibility 666 34.1.4 BC+ Emergency Services 667

35 Long Term Care Insurance Partnership (LTCIP) 668

223. ___________________________________________________________________ 35.1 Long Term Care Insurance Partnership (LTCIP) _____________________________________________ 668 35.1.1 LTCIP Introduction 669 35.1.2 LTCIP Asset Disregard 669 35.1.3 Verification 669

35.1.3.1 Verification of the Qualified LTCIP Policy 670 35.1.3.2 Reciprocity Standards 670 35.1.3.3 Verification of Benefits Paid 670 35.1.4 Examples 671 35.1.5 Process Help 673

36 Well Woman Medicaid (WWMA) 674

224. ___________________________________________________________________ 36.1 Wisconsin Well Woman Medicaid (WWMA) Introduction ______________________________________ 674

225. ___________________________________________________________________ 36.2 Well Woman Medicaid (WWMA) Enrollment ________________________________________________ 675 36.2.1 EM CAPO Administrating Enrollment for WWMA 676 36.2.2 Enrollment Through The Wisconsin Well Woman Program (WWWP) 676

36.2.2.1 Temporary Enrollment / Presumptive Eligibility (TE) Available Only To Women Enrolling Through WWWP677 36.2.3 WWWP Clients Enrolling For Continuous WWMA 678

36.2.3.1 Applications For WWMA Through Well Woman Program (WWWP) 678 36.2.4 Enrollment For Family Planning Waiver (FPW), BadgerCare Plus CORE and Benchmark Members 682

36.2.4.1 Applications For Wisconsin Well Woman Medicaid Through the Family Planning Waiver (FPW), BadgerCare Plus CORE or Benchmark Plans 682

226. ___________________________________________________________________ 36.3 Wisconsin Well Woman Medicaid (WWMA) Nonfinancial Requirement __________________________ 684 36.3.1 WWMA Introduction 684 36.3.2 Disqualifying Insurance Coverage 684 36.3.3 Non-Disqualifying Insurance Coverage 685

227. ___________________________________________________________________ 36.4 Wisconsin Well Woman Medicaid (WWMA) financial Requirement ______________________________ 687

228. ___________________________________________________________________ 36.5 Wisconsin Well Woman Medicaid (WWMA) Changes and Transfers ____________________________ 687 36.5.1 Member Loses Eligibility 687 36.5.2 WWMA InterAgency Case Transfers 688

229. ___________________________________________________________________ 36.6 Wisconsin Well Woman Medicaid (WWMA) Reviews /Recertifications ___________________________ 689

37 IRIS 691

230. ___________________________________________________________________ 37.1 IRIS (Include, Respect, I Self-Direct) _______________________________________________________ 691 37.1.1 Introduction 691

Medicaid Eligibility Handbook (MEH) Release 12-02

xxx

37.1.2 Role of the Aging and Disability Resource Center 691 37.1.3 IRIS Eligibility 692 37.1.4 IRIS In CARES 692

38 Reserved 693

231. ___________________________________________________________________ Ch. 35-38 Reserved _________________________________________________________________________ 693

232. ___________________________________________________________________ Appendix (Chs. 39-40) ______________________________________________________________________ 694

39 Tables 694

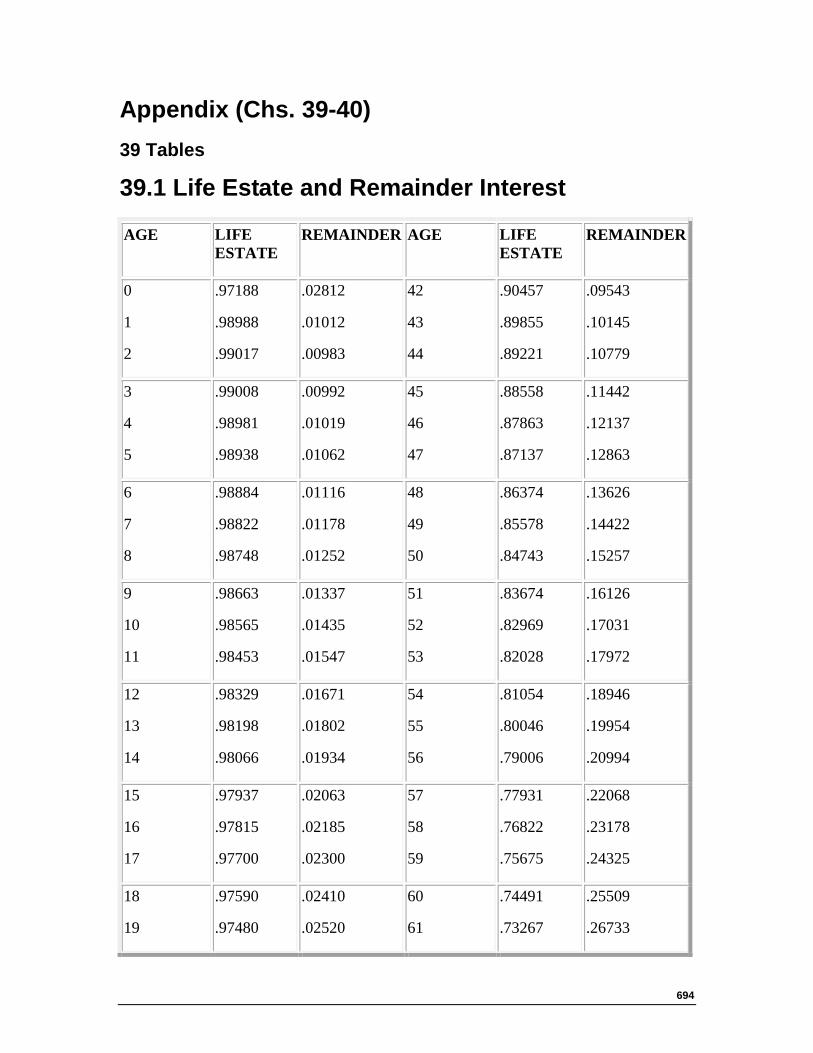

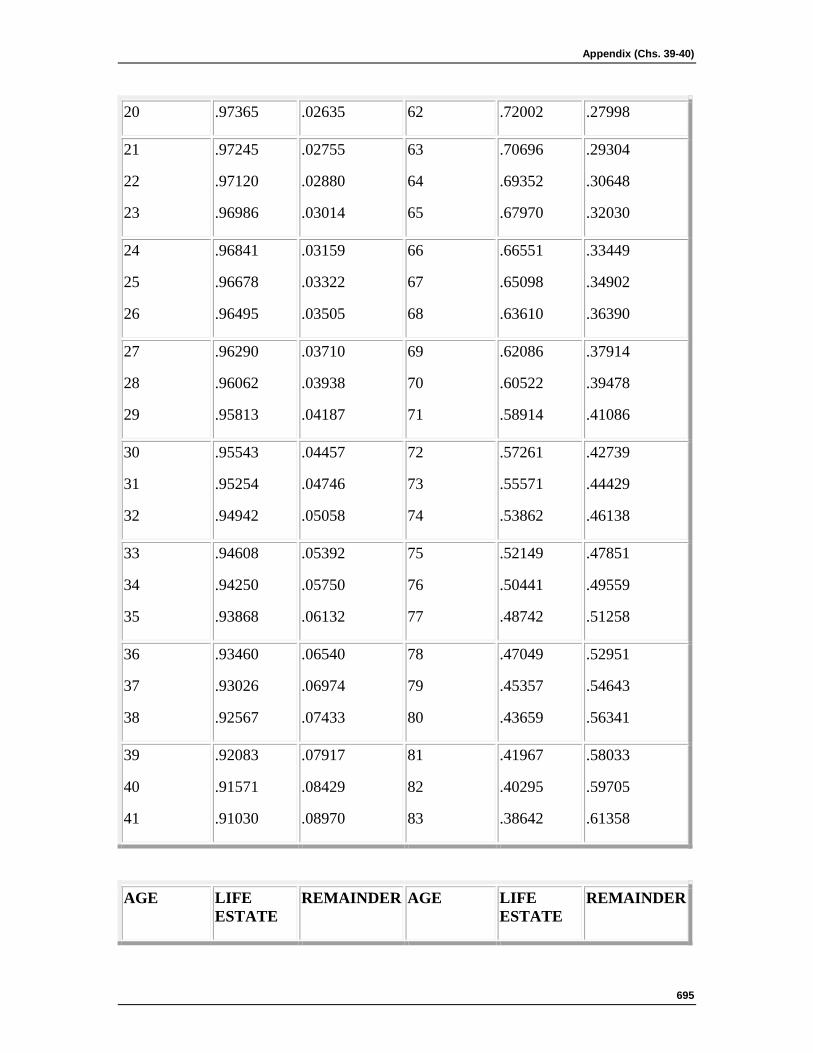

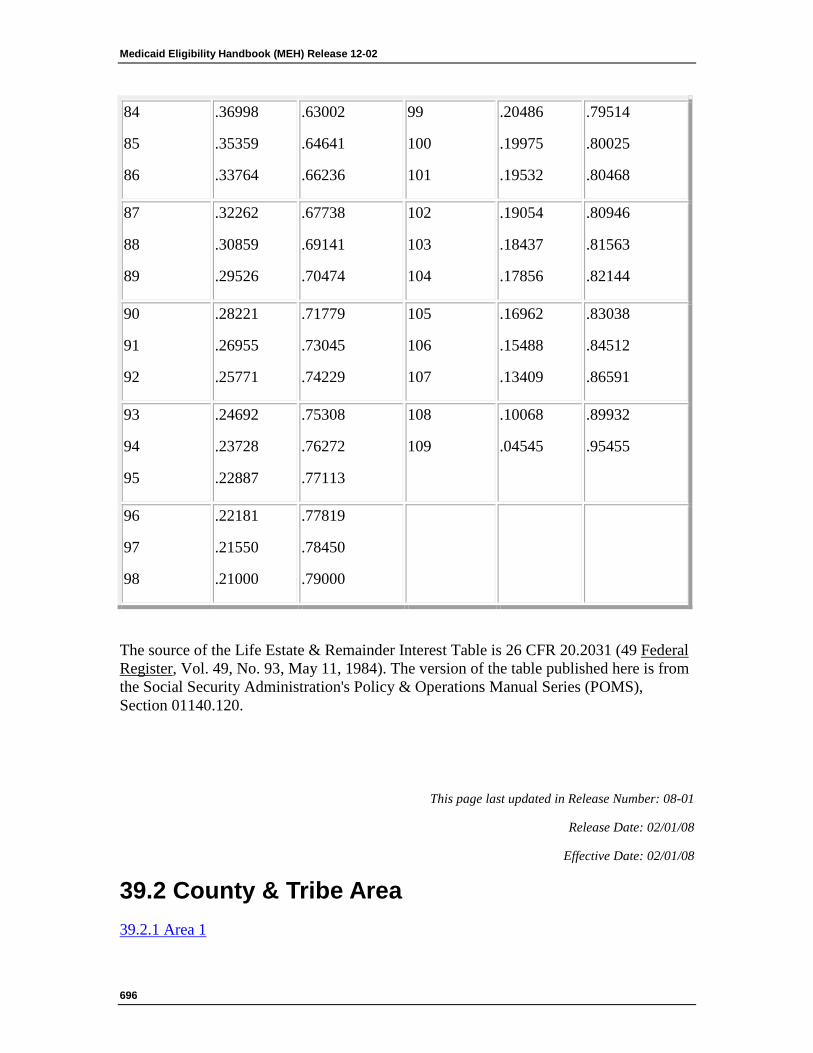

233. ___________________________________________________________________ 39.1 Life Estate and Remainder Interest ________________________________________________________ 694

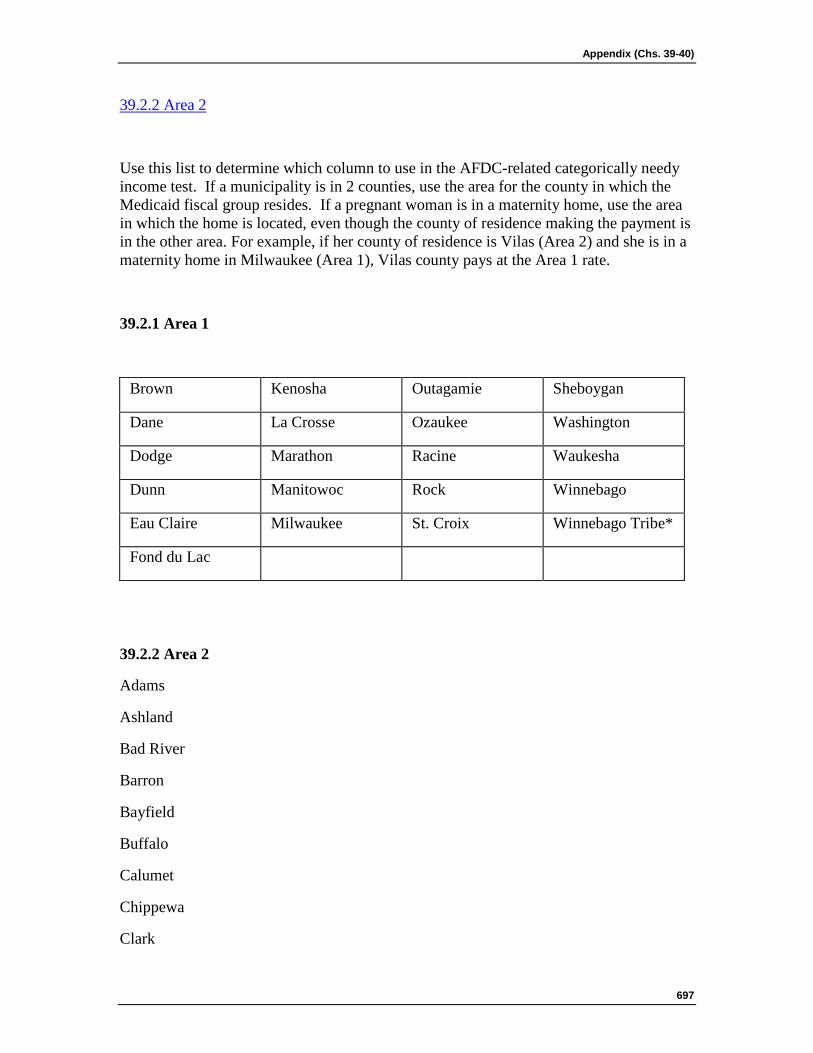

234. ___________________________________________________________________ 39.2 County & Tribe Area ____________________________________________________________________ 696

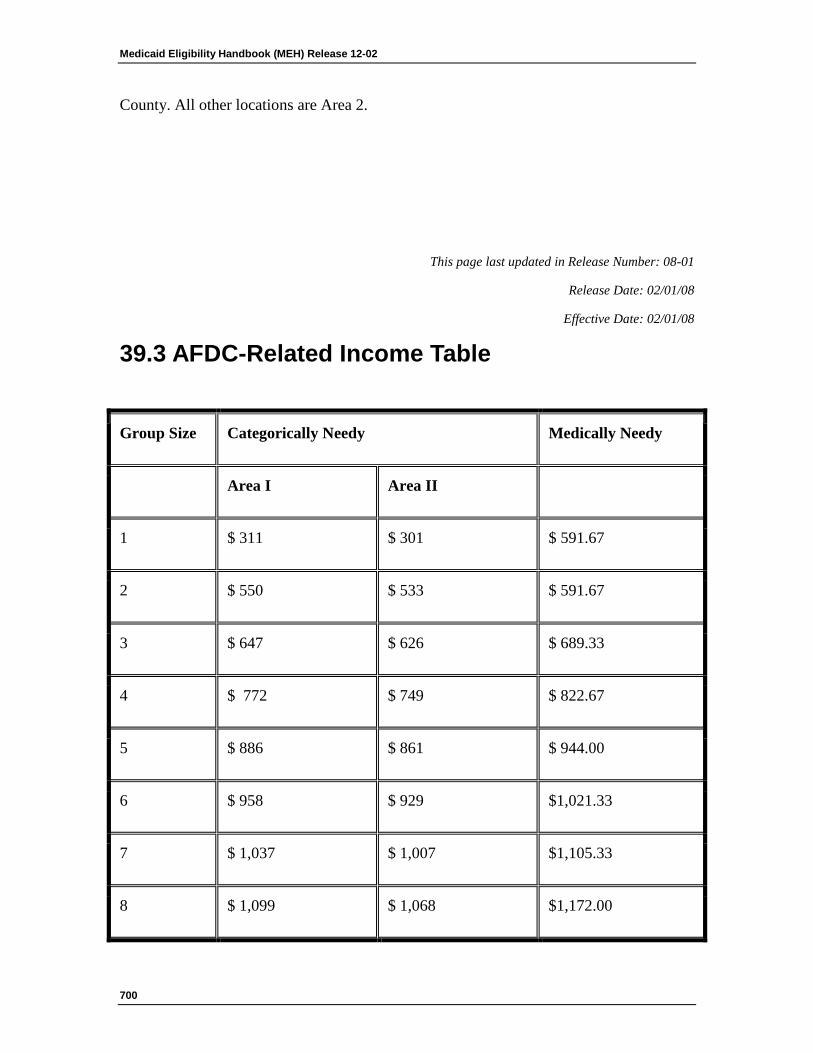

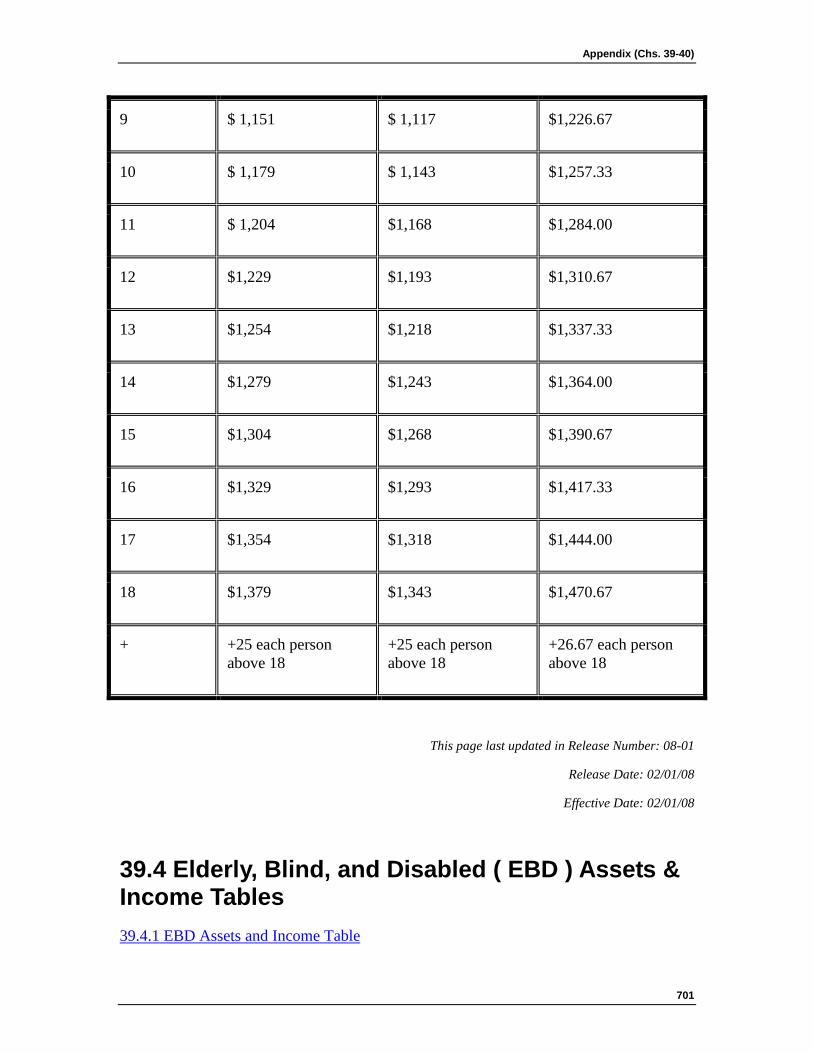

235. ___________________________________________________________________ 39.3 AFDC-Related Income Table _____________________________________________________________ 700

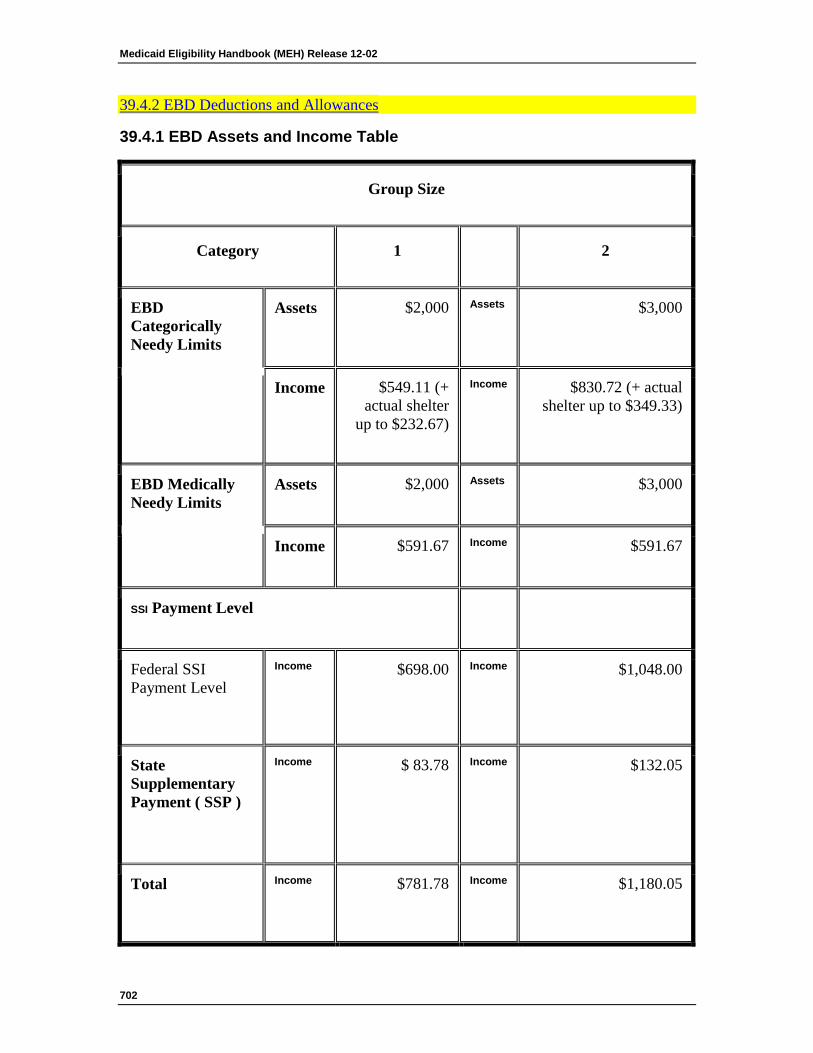

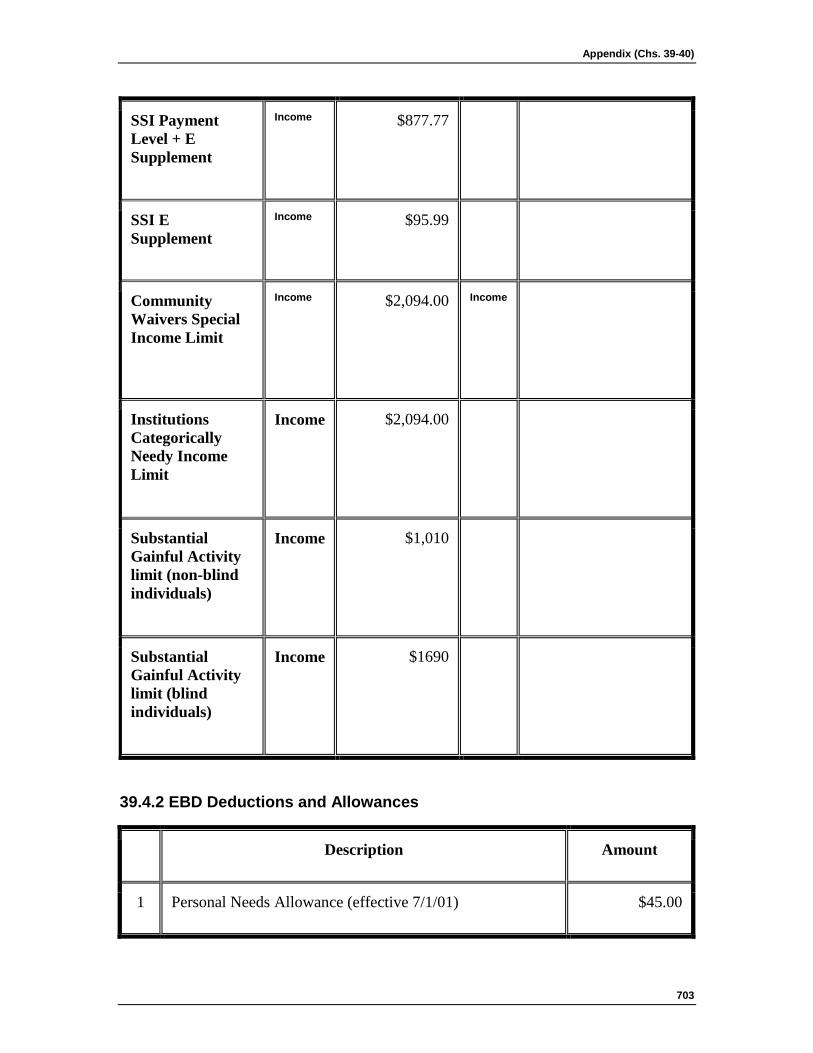

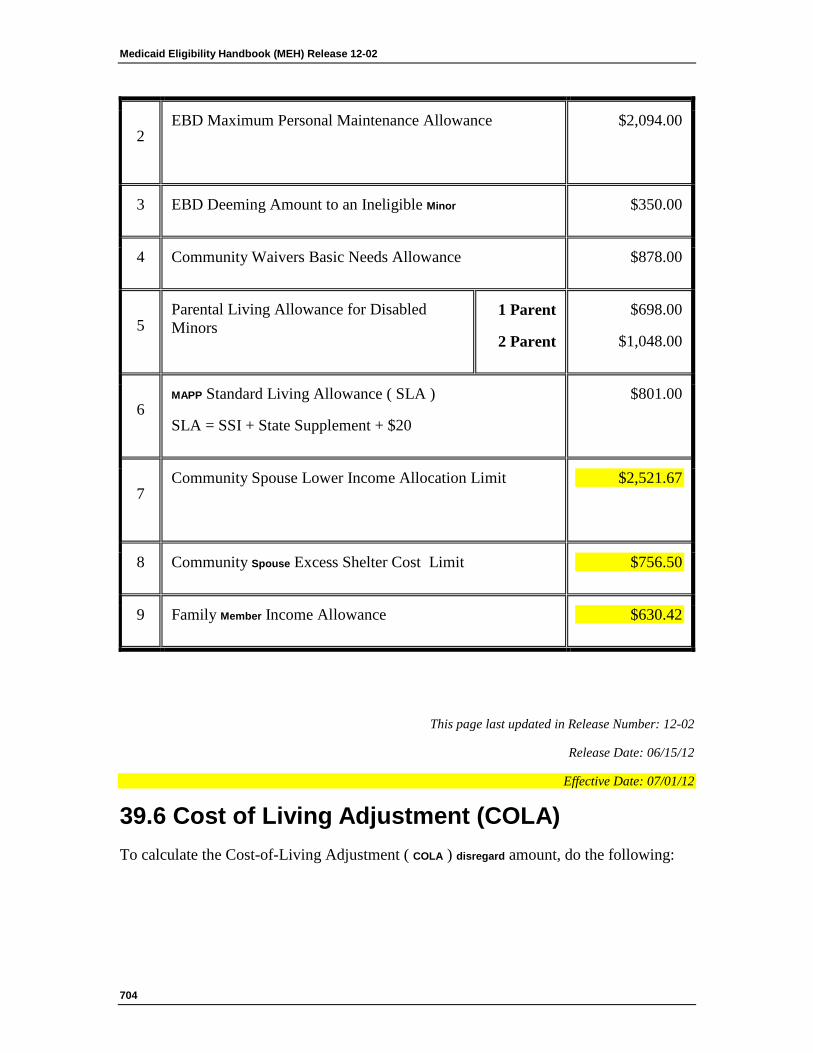

236. ___________________________________________________________________ 39.4 Elderly, Blind, and Disabled ( EBD ) Assets & Income Tables __________________________________ 701 39.4.1 EBD Assets and Income Table 702 39.4.2 EBD Deductions and Allowances 703

237. ___________________________________________________________________ 39.6 Cost of Living Adjustment (COLA) ________________________________________________________ 704

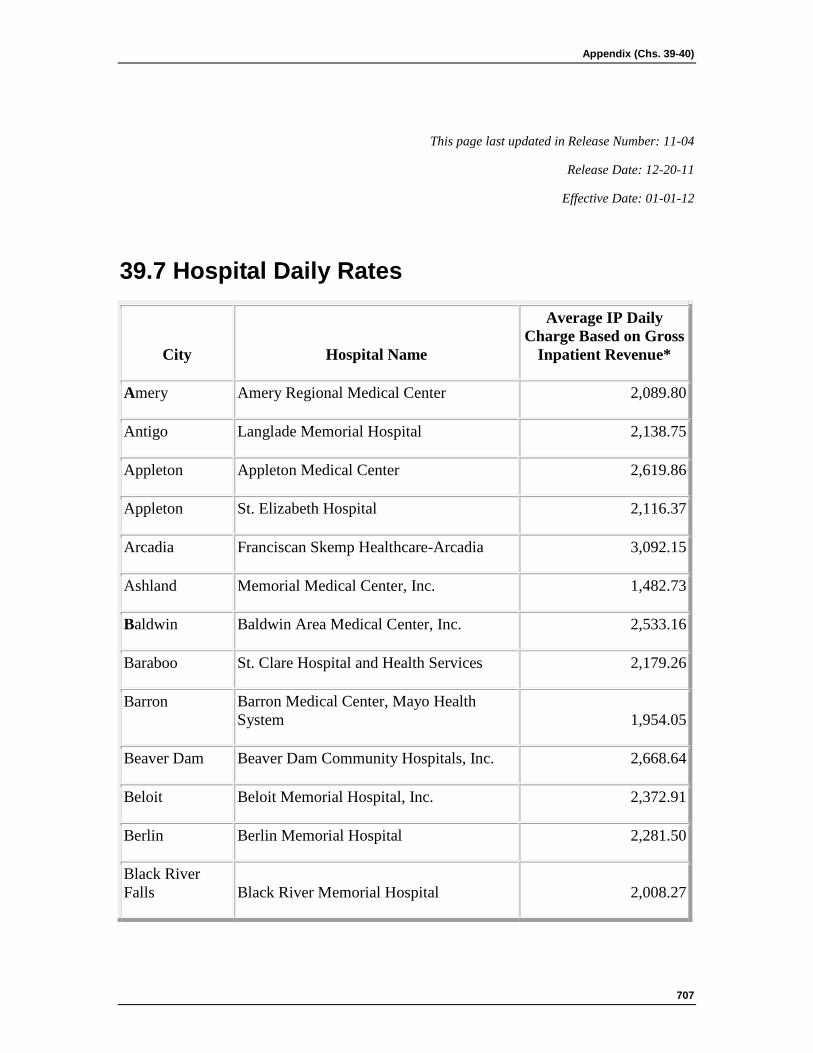

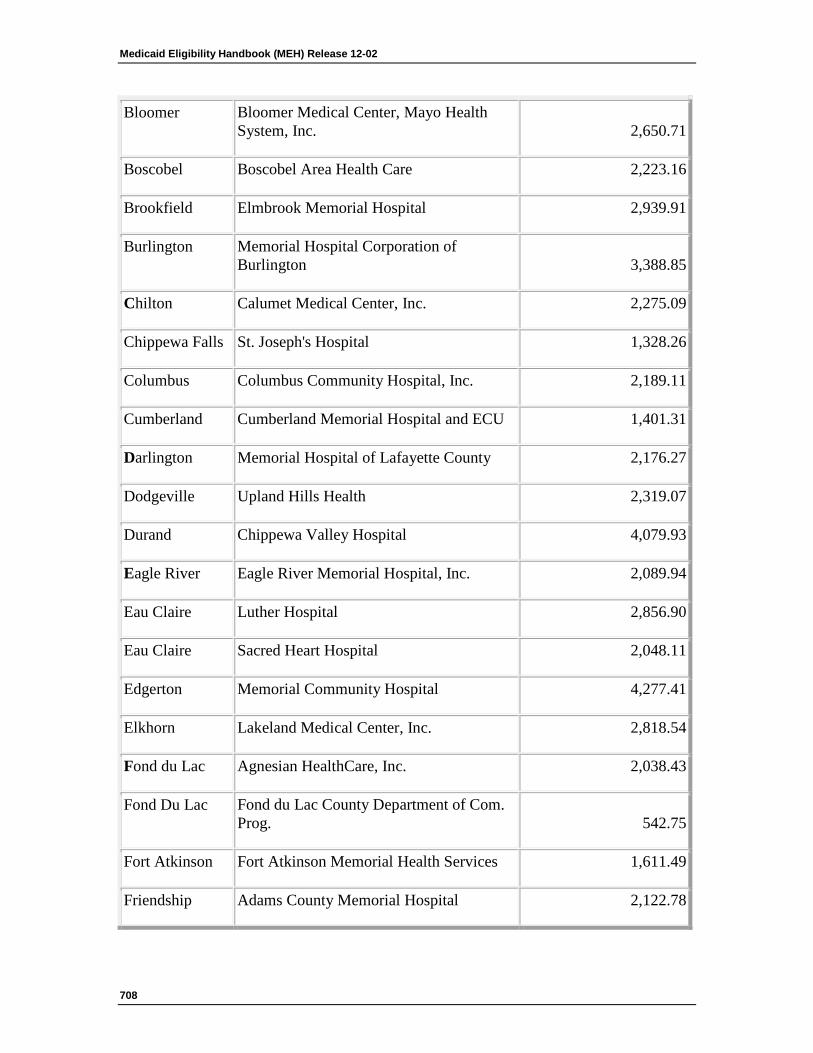

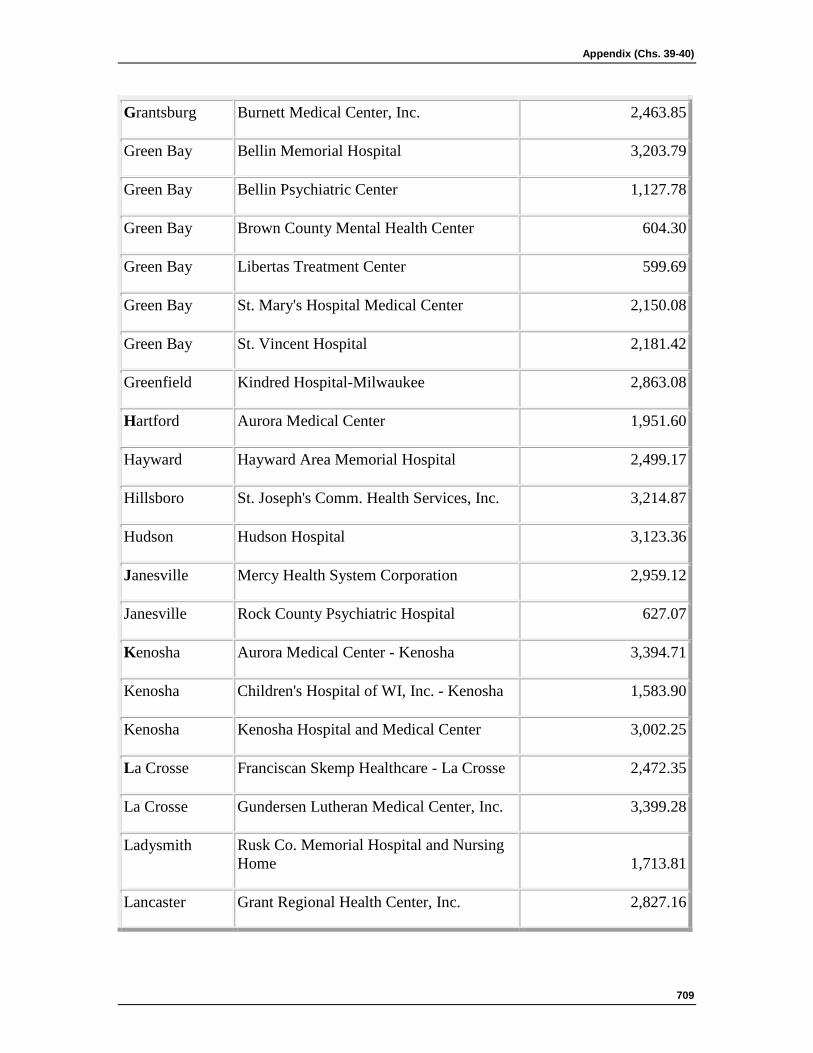

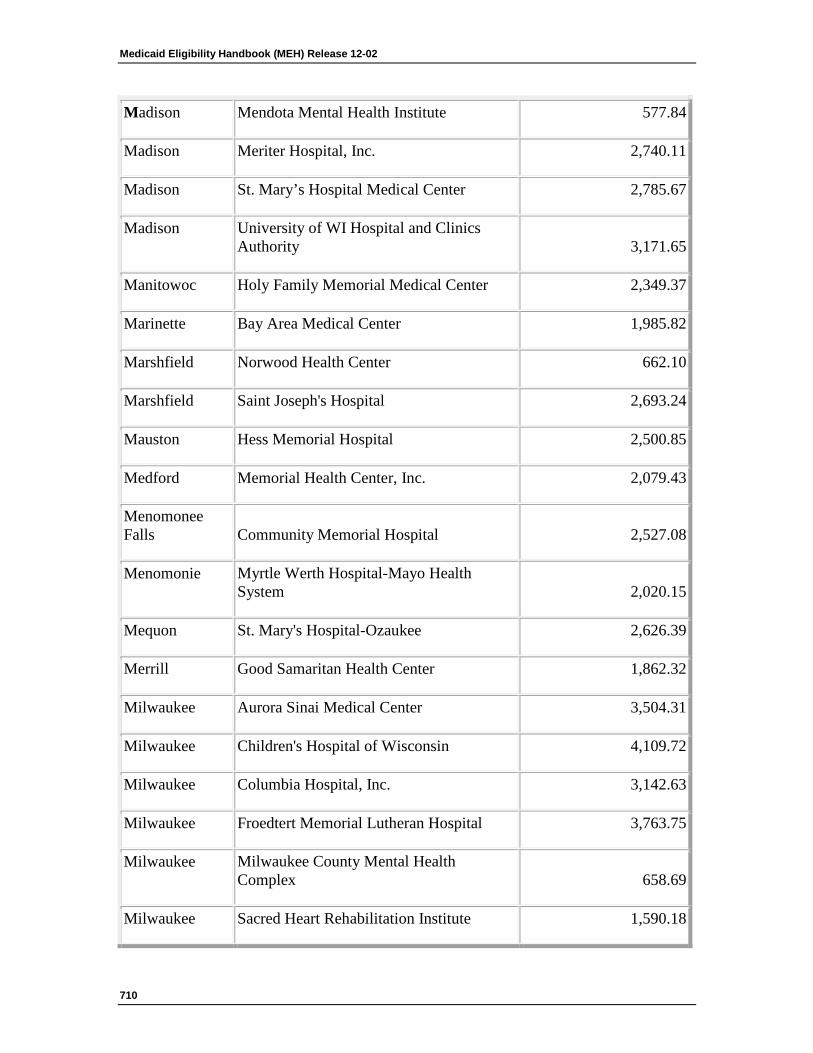

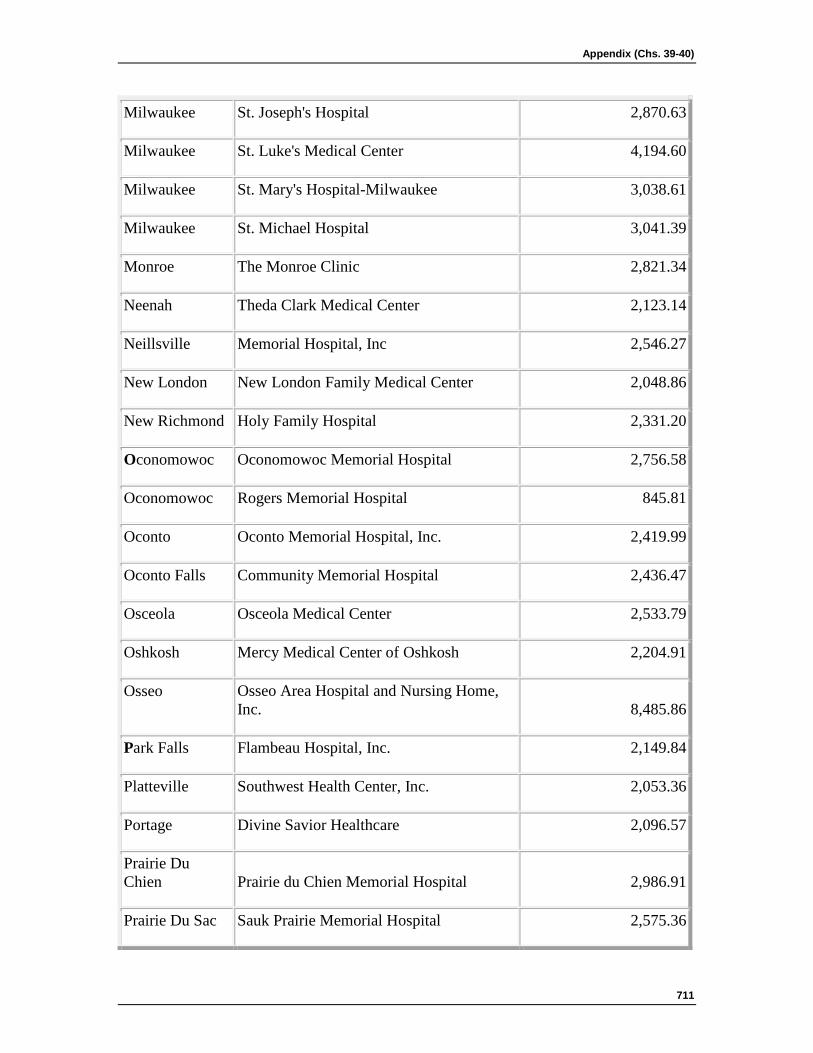

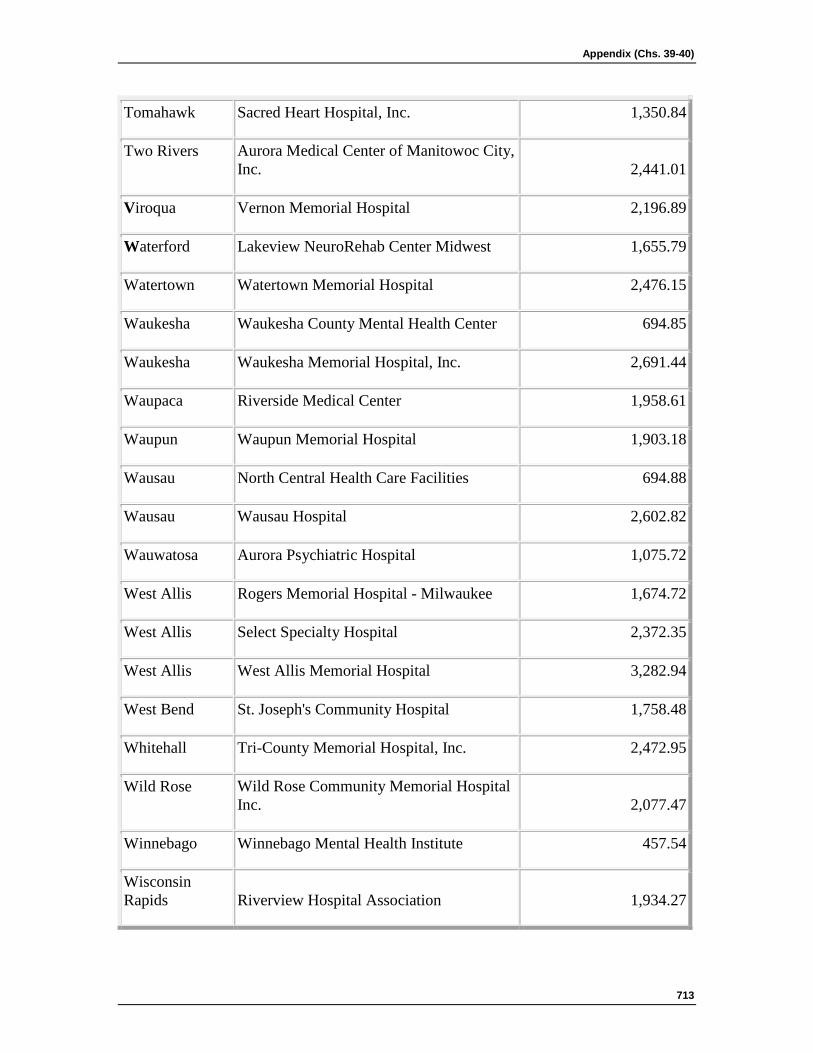

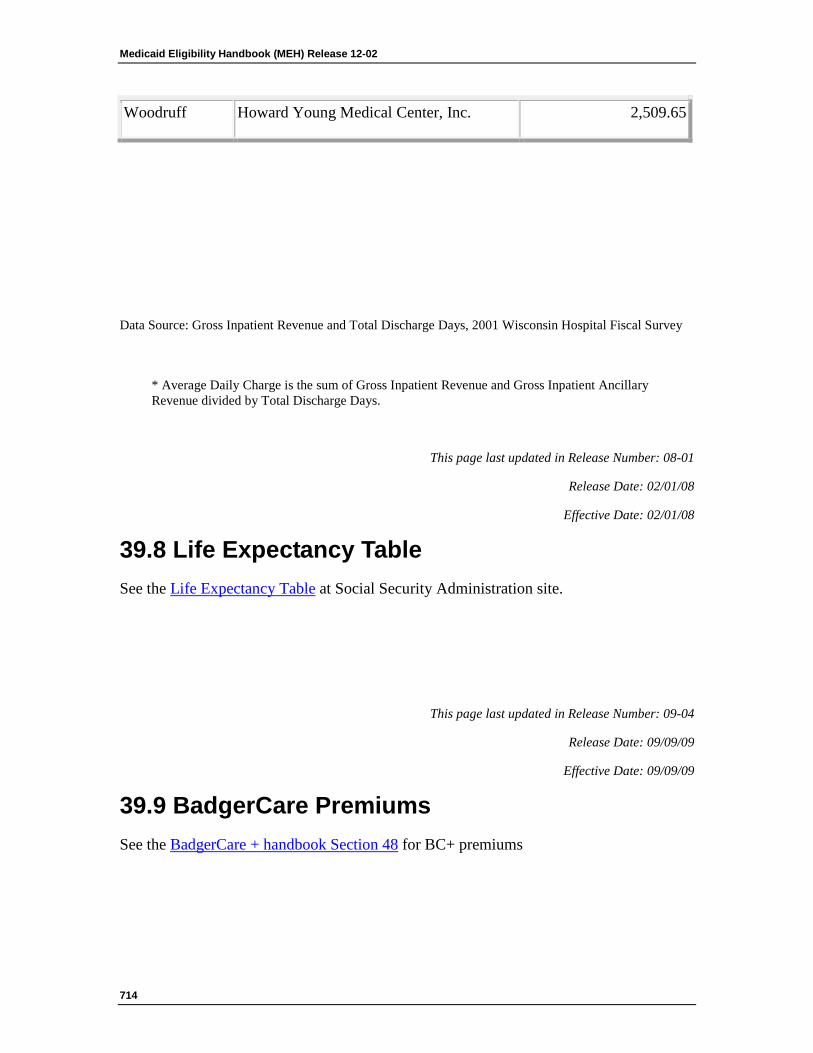

238. ___________________________________________________________________ 39.7 Hospital Daily Rates ____________________________________________________________________ 707

239. ___________________________________________________________________ 39.8 Life Expectancy Table __________________________________________________________________ 714

240. ___________________________________________________________________ 39.9 BadgerCare Premiums __________________________________________________________________ 714

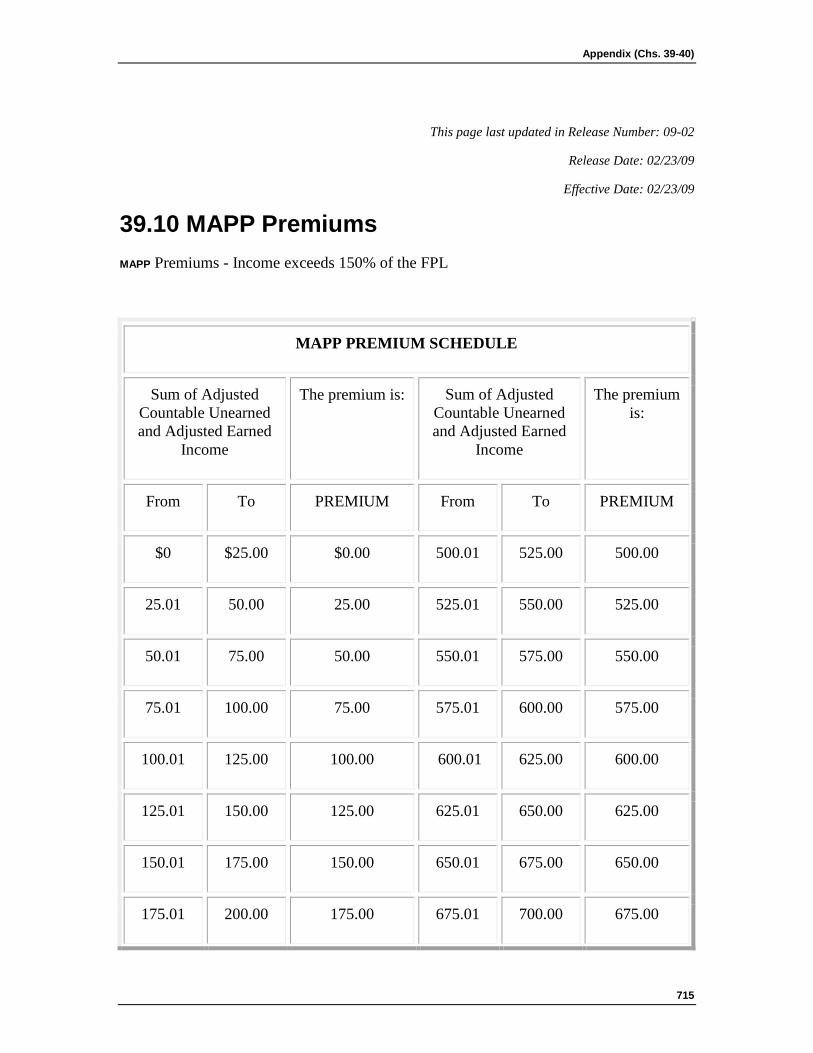

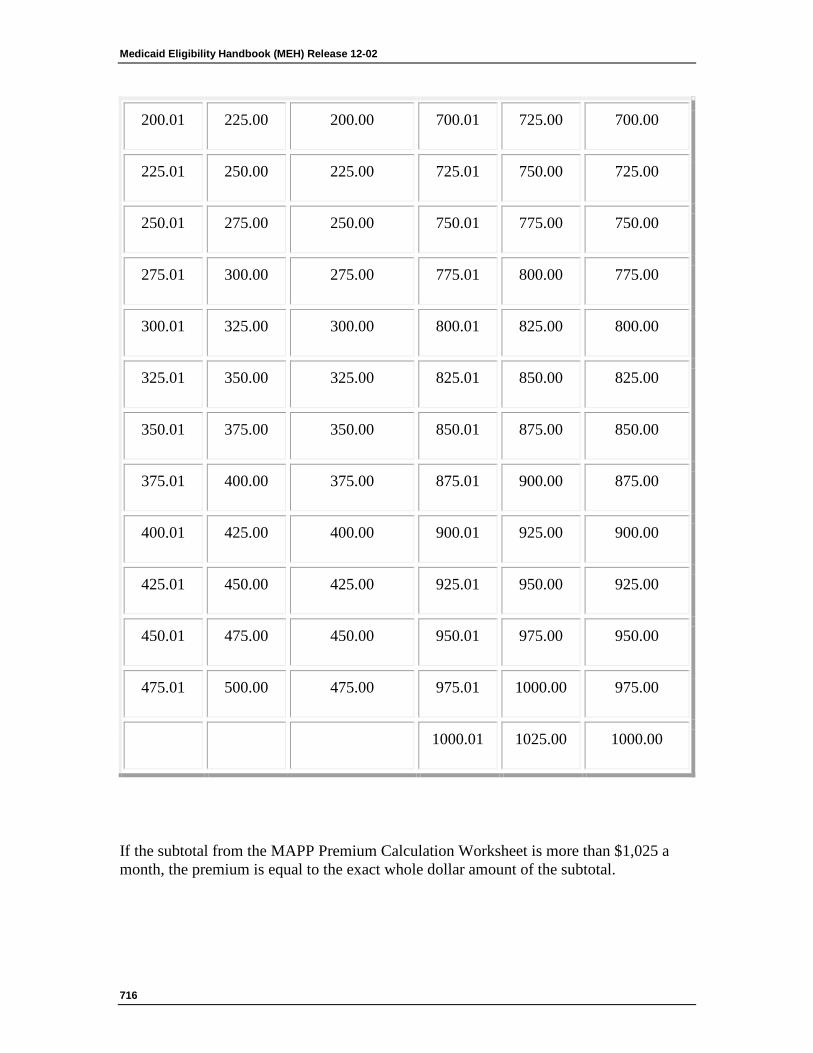

241. ___________________________________________________________________ 39.10 MAPP Premiums ______________________________________________________________________ 715

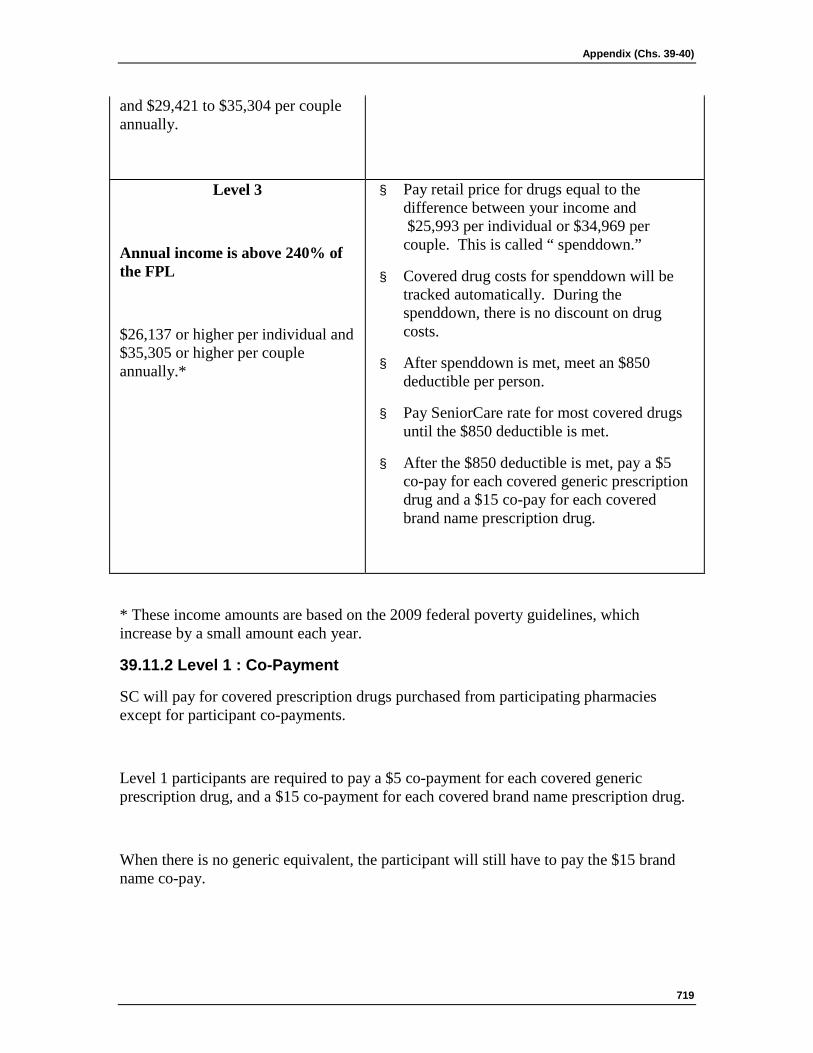

242. ___________________________________________________________________ 39.11 seniorcare income limits and Participation Levels __________________________________________ 717 39.11.1 SC Income Limits Introduction 717 39.11.2 Level 1 : Co-Payment 719 39.11.3 Level 2a: Deductible 720 39.11.4 Level 2b: Deductible 720 39.11.5 Level 3: Spenddown 721

39.11.5.1 Level 3: FTG of One 721 39.11.5.2 Level 3: FTG of Two 722

40 Worksheets 725

243. ___________________________________________________________________ 40.1 Worksheets table of contents ____________________________________________________________ 725

1

Introduction (Ch 1)

1.1 Introduction to Medicaid 1.1.1 Introduction

1.1.2 Subprograms of Medicaid

1.1.3 Financial Introduction

1.1.3.1 Assets

1.1.3.2 EBD Fiscal Group

1.1.3.3 Disabled Minors

1.1.3.4 Income

1.1.4 Health Care Choice

1.1.5 How to Apply

1.1.1 Introduction

'Medicaid’ is a state/federal program that provides health coverage for Wisconsin residents that are elderly, blind, or disabled (EBD) or receive Wisconsin Well Woman Medicaid. Medicaid is also known as Medical Assistance, MA, and Title 19.

1.1.2 Subprograms of Medicaid

There are different subprograms of Medicaid:

· SSI -related Medicaid

· MAPP

· Institutional Long Term Care

· Home and Community Based Waivers Long Term Care

· Family Care Long Term Care

· Partnership Long Term Care

· Program of All-Inclusive Care for the Elderly (PACE)

· Katie Beckett

· Tuberculosis ( TB ) -related

· Medicare Premium Assistance ( MPA ): QMB , SLMB , SLMB+, QDWI ;

Medicaid Eligibility Handbook (MEH) Release 12-02

2

· Emergency Medicaid

· SeniorCare

· Wisconsin Well Woman Medicaid (WWWMA)

A person may fit into one (or more) of the above subprograms based on non-financial factors. A person is eligible if s/he meets all Medicaid non-financial and financial requirements. Individuals who are not elderly, blind or disabled (EBD) may be eligible for BadgerCare+ (BC+). See the BC+ Handbook for more information.

1.1.3 Financial Introduction

See 39.4 for EBD asset limits. See 25.7.2 for TB-Related asset limits. See 1.1.3.3

to determine Medicaid eligibility for disabled minors that fail BadgerCare Plus financial

tests.

1.1.3.1 Assets

Use the EBD Related Determination worksheet when doing manual eligibility determinations for non institutionalized EBD Medicaid applicants and recipients. The EBD fiscal group’s assets must be within the appropriate categorically needy or medically needy asset limit before any member of that group can qualify for Medicaid. EBD fiscal groups who have assets in excess of the appropriate EBD medically needy asset limit are ineligible for Medicaid.

1.1.3.2 EBD Fiscal Group

An EBD fiscal group includes the individual who is non financially eligible for Medicaid and anyone who lives with them, who is legally responsible for them. Spouses who live together are in each other’s fiscal group. This means that the income and assets of both spouses are counted when determining Medicaid eligibility for either or both spouses. The fiscal group size for this situation/living arrangement is two.

There are some exceptions to this concept. A blind or disabled minor living with their parents would be a one person fiscal group. Special instructions for deeming parental income and assets to the disabled minor are described in 24.1 SSI Related Medicaid Introduction.

Introduction (Ch 1)

3

Another exception to the fiscal group policy involves SSI recipients. If one spouse is applying for EBD Medicaid and the other spouse is an SSI recipient, the SSI recipient spouse is not included in the other spouse’s fiscal group. For this situation you would again have a one person fiscal group when determining the Medicaid eligibility of the non-SSI spouse.

An individual living in a medical institution for 30 or more consecutive days would be a one person fiscal group. If the institutionalized person is married, refer to 18.1 Spousal Impoverishment Introduction for special instructions regarding spousal impoverishment procedures.

1.1.3.3 Disabled Minors

A blind or disabled minor (or dependent 18 year old) can have their Medicaid eligibility determined according to special procedures when the disabled minor fails BadgerCare Plus eligibility test or when the parent chooses to decline BC+ for their child and have their child receive EBD Medicaid if eligible. See section 15.1.2 Special Financial Tests for Disabled Minors.

1.1.3.4 Income

See 39.4 EBD Assets and Income Tables for EBD income limits. See 39.5 FPL Table for all other MA income limits. Chapters for each type of MA explain how to determine the income that you compare to the income limits.

See 39.4.2 EBD Deductions and Allowances for TB-Related income limits.

1.1.4 Health Care Choice

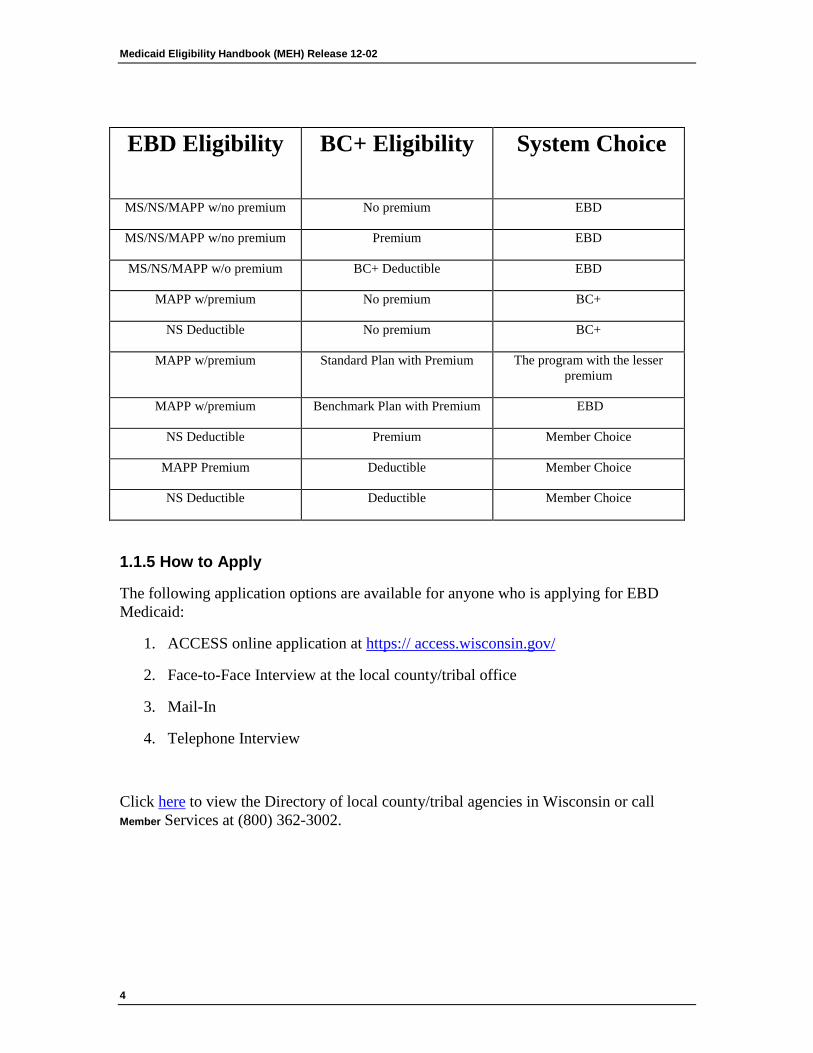

It is possible for individuals to qualify for both BC+ and Elderly, Blind and Disabled Medicaid (EBD MA). In some circumstances, CARES will automatically enroll the individual in the program with the best benefit plan and lowest cost share. The individual has the right to request coverage under the program not chosen by CARES. See table below. The change is effective in the next possible payment following Adverse Action , unless the member requests the change be effective in the month the request to change the health plan was made.

When CARES is unable to make an automatic choice between BC+ and EBD MA, a notice requesting the individual to make a choice will be generated. Once the member has made a choice the decision remains in effect until:

1. The member requests a change, or

2. The member’s benefit under the health plan of his or her choice ends. (This includes being placed into an unmet deductible assistance group.)

Medicaid Eligibility Handbook (MEH) Release 12-02

4

EBD Eligibility BC+ Eligibility

System Choice

MS/NS/MAPP w/no premium No premium EBD

MS/NS/MAPP w/no premium Premium EBD

MS/NS/MAPP w/o premium BC+ Deductible EBD

MAPP w/premium No premium BC+

NS Deductible No premium BC+

MAPP w/premium Standard Plan with Premium The program with the lesser premium

MAPP w/premium Benchmark Plan with Premium EBD

NS Deductible Premium Member Choice

MAPP Premium Deductible Member Choice

NS Deductible Deductible Member Choice

1.1.5 How to Apply

The following application options are available for anyone who is applying for EBD Medicaid:

1. ACCESS online application at https:// access.wisconsin.gov/

2. Face-to-Face Interview at the local county/tribal office

3. Mail-In

4. Telephone Interview

Click here to view the Directory of local county/tribal agencies in Wisconsin or call Member Services at (800) 362-3002.

Introduction (Ch 1)

5

This page last updated in Release Number: 11-01

Release Date: 04/04/11

Effective Date: 04/04/11

6

Apps and Reviews (Chs. 2-3) 2 Applications

2.1 Applications Introduction 2.1.1 Affirmative Action and Civil Rights

Anyone has the right to apply for Medicaid. However, individuals under 18 years of age must have a parent or a legal guardian apply for Medicaid on their behalf unless living independently.

They may be assisted by any person s/he chooses in completing an application.

Encourage anyone who expresses interest in applying to file an application as soon as possible. When an application is requested:

1. Suggest the applicant use the ACCESS online application at the following site http://access.wisconsin.gov ; or

2. Mail-In using the Wisconsin Medicaid for the Elderly , Blind,and Disabled Application Packet (F 10101).

3. Schedule a telephone or face-to-face interview.

Provide any information, instruction and/or materials needed to complete the application process. Provide a Notice of Assignment: Child Support, Family Support, Maintenance and Medical Support form (DWSP 2477) and Good Cause Notice (DWSP 2018) to each applicant with children applying for Medicaid or to anyone that requests either of these.

Refer requests for applications and other outreach materials from groups and persons involved in outreach efforts to:

http://dhs.wisconsin.gov/forms/ paperfpc.htm

Apps and Reviews (Chs. 2-3)

7

Note: An application can be filed on behalf of a deceased person. If the application is filed within the same calendar month as the date of death or within the 3 months after the date of death, the application should be processed as if the applicant were alive. If the application is filed more than 4 months after the date of death, s/he is not eligible.

2.1.1 Affirmative Action and Civil Rights