mechanisms to reduce emissions uncertainty …2018/04/17 · mechanisms to reduce emissions...

TRANSCRIPT

Mechanisms to Reduce Emissions Uncertaintyunder a Carbon Tax

Marc HafsteadResources for the Future

Roberton C. Williams IIIUniversity of Maryland, Resources for the Future, and NBER

April 17, 2018

Hafstead and Williams (2018) Emissions Certainty Mechanisms

Carbon Taxes and Emissions Uncertainty

In the US, some right-leaning think tanks and parts of thebusiness community have joined the carbon tax coalition

But environmentalist groups are either

hostile to emissions pricingor want assurances emissions targets can me met.

An additional issue for a carbon tax: international agreementsare defined in quantitiesIf we care about emissions levels, why not just implement acap-and-trade?

US federal cap-and-trade is (currently) politically unviable

Some policymakers are considering a hybrid carbon tax policysolution

Hafstead and Williams (2018) Emissions Certainty Mechanisms 1 / 42

Carbon Taxes and Emissions Uncertainty

In the US, some right-leaning think tanks and parts of thebusiness community have joined the carbon tax coalitionBut environmentalist groups are either

hostile to emissions pricingor want assurances emissions targets can me met.

An additional issue for a carbon tax: international agreementsare defined in quantitiesIf we care about emissions levels, why not just implement acap-and-trade?

US federal cap-and-trade is (currently) politically unviable

Some policymakers are considering a hybrid carbon tax policysolution

Hafstead and Williams (2018) Emissions Certainty Mechanisms 1 / 42

Carbon Taxes and Emissions Uncertainty

In the US, some right-leaning think tanks and parts of thebusiness community have joined the carbon tax coalitionBut environmentalist groups are either

hostile to emissions pricing

or want assurances emissions targets can me met.

An additional issue for a carbon tax: international agreementsare defined in quantitiesIf we care about emissions levels, why not just implement acap-and-trade?

US federal cap-and-trade is (currently) politically unviable

Some policymakers are considering a hybrid carbon tax policysolution

Hafstead and Williams (2018) Emissions Certainty Mechanisms 1 / 42

Carbon Taxes and Emissions Uncertainty

In the US, some right-leaning think tanks and parts of thebusiness community have joined the carbon tax coalitionBut environmentalist groups are either

hostile to emissions pricingor want assurances emissions targets can me met.

An additional issue for a carbon tax: international agreementsare defined in quantitiesIf we care about emissions levels, why not just implement acap-and-trade?

US federal cap-and-trade is (currently) politically unviable

Some policymakers are considering a hybrid carbon tax policysolution

Hafstead and Williams (2018) Emissions Certainty Mechanisms 1 / 42

Carbon Taxes and Emissions Uncertainty

In the US, some right-leaning think tanks and parts of thebusiness community have joined the carbon tax coalitionBut environmentalist groups are either

hostile to emissions pricingor want assurances emissions targets can me met.

An additional issue for a carbon tax: international agreementsare defined in quantities

If we care about emissions levels, why not just implement acap-and-trade?

US federal cap-and-trade is (currently) politically unviable

Some policymakers are considering a hybrid carbon tax policysolution

Hafstead and Williams (2018) Emissions Certainty Mechanisms 1 / 42

Carbon Taxes and Emissions Uncertainty

In the US, some right-leaning think tanks and parts of thebusiness community have joined the carbon tax coalitionBut environmentalist groups are either

hostile to emissions pricingor want assurances emissions targets can me met.

An additional issue for a carbon tax: international agreementsare defined in quantitiesIf we care about emissions levels, why not just implement acap-and-trade?

US federal cap-and-trade is (currently) politically unviable

Some policymakers are considering a hybrid carbon tax policysolution

Hafstead and Williams (2018) Emissions Certainty Mechanisms 1 / 42

Carbon Taxes and Emissions Uncertainty

In the US, some right-leaning think tanks and parts of thebusiness community have joined the carbon tax coalitionBut environmentalist groups are either

hostile to emissions pricingor want assurances emissions targets can me met.

An additional issue for a carbon tax: international agreementsare defined in quantitiesIf we care about emissions levels, why not just implement acap-and-trade?

US federal cap-and-trade is (currently) politically unviable

Some policymakers are considering a hybrid carbon tax policysolution

Hafstead and Williams (2018) Emissions Certainty Mechanisms 1 / 42

Carbon Taxes and Emissions Uncertainty

In the US, some right-leaning think tanks and parts of thebusiness community have joined the carbon tax coalitionBut environmentalist groups are either

hostile to emissions pricingor want assurances emissions targets can me met.

An additional issue for a carbon tax: international agreementsare defined in quantitiesIf we care about emissions levels, why not just implement acap-and-trade?

US federal cap-and-trade is (currently) politically unviable

Some policymakers are considering a hybrid carbon tax policysolution

Hafstead and Williams (2018) Emissions Certainty Mechanisms 1 / 42

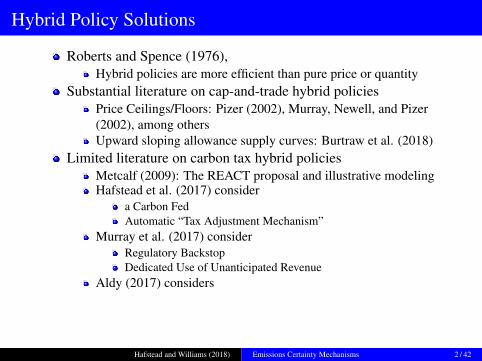

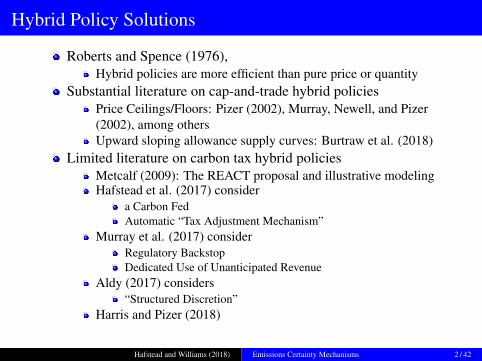

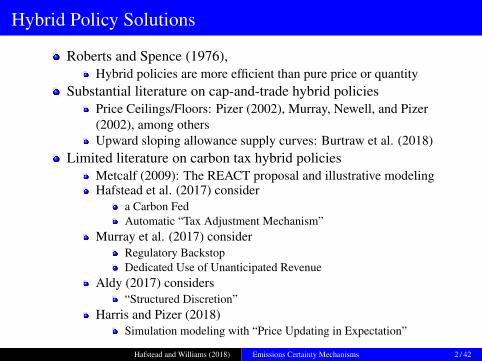

Hybrid Policy Solutions

Roberts and Spence (1976),

Hybrid policies are more efficient than pure price or quantitySubstantial literature on cap-and-trade hybrid policies

Price Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policies

Metcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policies

Price Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policies

Metcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policies

Price Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policies

Metcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among others

Upward sloping allowance supply curves: Burtraw et al. (2018)Limited literature on carbon tax hybrid policies

Metcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policies

Metcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policies

Metcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modeling

Hafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon Fed

Automatic “Tax Adjustment Mechanism”Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) consider

Regulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) considerRegulatory Backstop

Dedicated Use of Unanticipated RevenueAldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) considerRegulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) considerRegulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers

“Structured Discretion”Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) considerRegulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) considerRegulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers“Structured Discretion”

Harris and Pizer (2018)

Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Hybrid Policy Solutions

Roberts and Spence (1976),Hybrid policies are more efficient than pure price or quantity

Substantial literature on cap-and-trade hybrid policiesPrice Ceilings/Floors: Pizer (2002), Murray, Newell, and Pizer(2002), among othersUpward sloping allowance supply curves: Burtraw et al. (2018)

Limited literature on carbon tax hybrid policiesMetcalf (2009): The REACT proposal and illustrative modelingHafstead et al. (2017) consider

a Carbon FedAutomatic “Tax Adjustment Mechanism”

Murray et al. (2017) considerRegulatory BackstopDedicated Use of Unanticipated Revenue

Aldy (2017) considers“Structured Discretion”

Harris and Pizer (2018)Simulation modeling with “Price Updating in Expectation”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 2 / 42

Key Research Questions

How uncertain are emissions under a carbon tax?What are the drivers of emissions uncertainty?

What are the costs of providing emissions certainty under acarbon tax?

How do the costs vary by mechanism design?What are the trade-offs across different designs?

Hafstead and Williams (2018) Emissions Certainty Mechanisms 3 / 42

Key Research Questions

How uncertain are emissions under a carbon tax?What are the drivers of emissions uncertainty?

What are the costs of providing emissions certainty under acarbon tax?

How do the costs vary by mechanism design?What are the trade-offs across different designs?

Hafstead and Williams (2018) Emissions Certainty Mechanisms 3 / 42

Preview of Results

How uncertain are emissions under a carbon tax?The confidence interval for cumulative emissions is quite large

+/− 24 percent of expected cumulative emissions

Uncertainty in the price elasticity drives emissions uncertaintyWhat are the additional expected costs of providing emissionscertainty under a carbon tax?

Depends on how we define certaintyDepends on key design choices

5 - 80% of primary cost

Hafstead and Williams (2018) Emissions Certainty Mechanisms 4 / 42

Outline

Intro

Emissions Certainty Mechanisms Examples

Reduced-Form Model of Emissions with Uncertainty

Quantifying Emissions Uncertainty

Defining Emissions Certainty

Comparing Tax Adjustment Mechanisms

Hafstead and Williams (2018) Emissions Certainty Mechanisms 5 / 42

Outline

Intro

Emissions Certainty Mechanisms Examples

Reduced-Form Model of Emissions with Uncertainty

Quantifying Emissions Uncertainty

Defining Emissions Certainty

Comparing Tax Adjustment Mechanisms

Hafstead and Williams (2018) Emissions Certainty Mechanisms 5 / 42

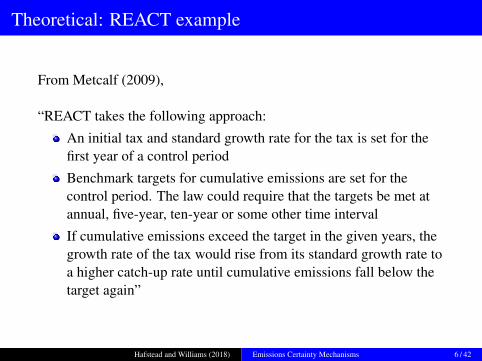

Theoretical: REACT example

From Metcalf (2009),

“REACT takes the following approach:

An initial tax and standard growth rate for the tax is set for thefirst year of a control period

Benchmark targets for cumulative emissions are set for thecontrol period. The law could require that the targets be met atannual, five-year, ten-year or some other time interval

If cumulative emissions exceed the target in the given years, thegrowth rate of the tax would rise from its standard growth rate toa higher catch-up rate until cumulative emissions fall below thetarget again”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 6 / 42

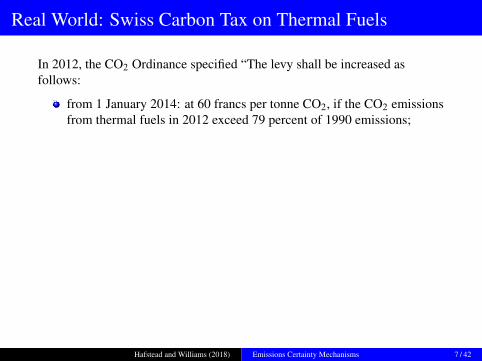

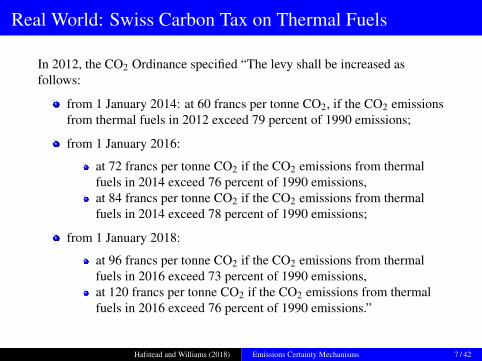

Real World: Swiss Carbon Tax on Thermal Fuels

In 2012, the CO2 Ordinance specified “The levy shall be increased asfollows:

from 1 January 2014: at 60 francs per tonne CO2, if the CO2 emissionsfrom thermal fuels in 2012 exceed 79 percent of 1990 emissions;

from 1 January 2016:

at 72 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2014 exceed 76 percent of 1990 emissions,at 84 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2014 exceed 78 percent of 1990 emissions;

from 1 January 2018:

at 96 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2016 exceed 73 percent of 1990 emissions,at 120 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2016 exceed 76 percent of 1990 emissions.”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 7 / 42

Real World: Swiss Carbon Tax on Thermal Fuels

In 2012, the CO2 Ordinance specified “The levy shall be increased asfollows:

from 1 January 2014: at 60 francs per tonne CO2, if the CO2 emissionsfrom thermal fuels in 2012 exceed 79 percent of 1990 emissions;

from 1 January 2016:

at 72 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2014 exceed 76 percent of 1990 emissions,at 84 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2014 exceed 78 percent of 1990 emissions;

from 1 January 2018:

at 96 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2016 exceed 73 percent of 1990 emissions,at 120 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2016 exceed 76 percent of 1990 emissions.”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 7 / 42

Real World: Swiss Carbon Tax on Thermal Fuels

In 2012, the CO2 Ordinance specified “The levy shall be increased asfollows:

from 1 January 2014: at 60 francs per tonne CO2, if the CO2 emissionsfrom thermal fuels in 2012 exceed 79 percent of 1990 emissions;

from 1 January 2016:

at 72 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2014 exceed 76 percent of 1990 emissions,at 84 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2014 exceed 78 percent of 1990 emissions;

from 1 January 2018:

at 96 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2016 exceed 73 percent of 1990 emissions,at 120 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2016 exceed 76 percent of 1990 emissions.”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 7 / 42

Real World: Swiss Carbon Tax on Thermal Fuels

In 2012, the CO2 Ordinance specified “The levy shall be increased asfollows:

from 1 January 2014: at 60 francs per tonne CO2, if the CO2 emissionsfrom thermal fuels in 2012 exceed 79 percent of 1990 emissions;

from 1 January 2016:

at 72 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2014 exceed 76 percent of 1990 emissions,at 84 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2014 exceed 78 percent of 1990 emissions;

from 1 January 2018:

at 96 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2016 exceed 73 percent of 1990 emissions,at 120 francs per tonne CO2 if the CO2 emissions from thermalfuels in 2016 exceed 76 percent of 1990 emissions.”

Hafstead and Williams (2018) Emissions Certainty Mechanisms 7 / 42

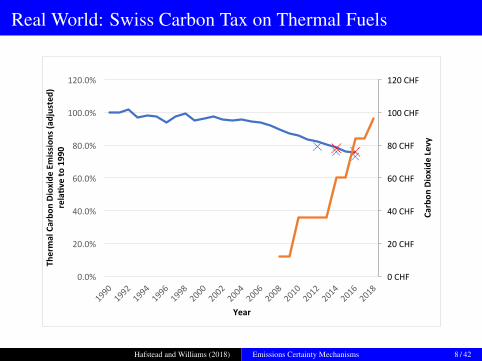

Real World: Swiss Carbon Tax on Thermal Fuels

0CHF

20CHF

40CHF

60CHF

80CHF

100CHF

120CHF

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

199019921994199619982000200220042006200820102012201420162018

Carbon

Dioxide

Levy

ThermalCarbo

nDioxideEm

ission

s(ad

justed

)rela;v

eto1990

Year

Hafstead and Williams (2018) Emissions Certainty Mechanisms 8 / 42

Outline

Intro

Emissions Certainty Mechanisms

Reduced-Form Model of Emissions with Uncertainty

Quantifying Emissions Uncertainty

Defining Emissions Certainty

Comparing Tax Adjustment Mechanisms

Hafstead and Williams (2018) Emissions Certainty Mechanisms 9 / 42

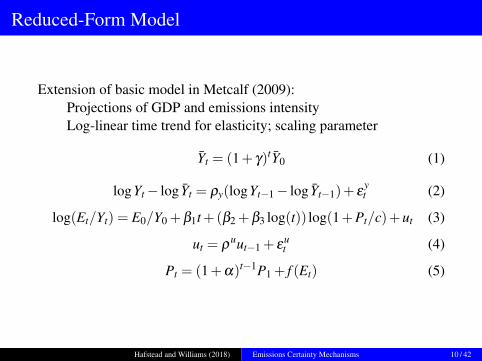

Reduced-Form Model

Extension of basic model in Metcalf (2009):Projections of GDP and emissions intensityLog-linear time trend for elasticity; scaling parameter

Yt = (1+ γ)tY0 (1)

logYt − log Yt = ρy(logYt−1 − log Yt−1)+ εyt (2)

log(Et/Yt) = E0/Y0 +β1t+(β2 +β3 log(t)) log(1+Pt/c)+ut (3)

ut = ρuut−1 + ε

ut (4)

Pt = (1+α)t−1P1 + f (Et) (5)

Hafstead and Williams (2018) Emissions Certainty Mechanisms 10 / 42

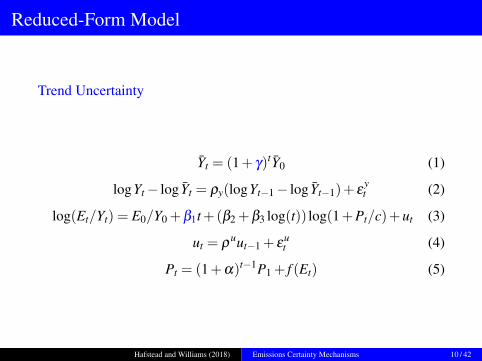

Reduced-Form Model

Trend Uncertainty

Yt = (1+ γ)tY0 (1)

logYt − log Yt = ρy(logYt−1 − log Yt−1)+ εyt (2)

log(Et/Yt) = E0/Y0 +β1t+(β2 +β3 log(t)) log(1+Pt/c)+ut (3)

ut = ρuut−1 + ε

ut (4)

Pt = (1+α)t−1P1 + f (Et) (5)

Hafstead and Williams (2018) Emissions Certainty Mechanisms 10 / 42

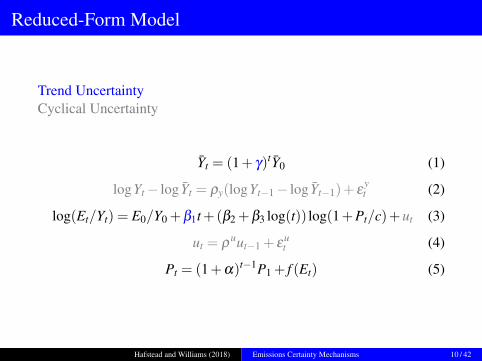

Reduced-Form Model

Trend UncertaintyCyclical Uncertainty

Yt = (1+ γ)tY0 (1)

logYt − log Yt = ρy(logYt−1 − log Yt−1)+ εyt (2)

log(Et/Yt) = E0/Y0 +β1t+(β2 +β3 log(t)) log(1+Pt/c)+ut (3)

ut = ρuut−1 + ε

ut (4)

Pt = (1+α)t−1P1 + f (Et) (5)

Hafstead and Williams (2018) Emissions Certainty Mechanisms 10 / 42

Reduced-Form Model

Trend UncertaintyCyclical UncertaintyPrice Elasticity Uncertainty

Yt = (1+ γ)tY0 (1)

logYt − log Yt = ρy(logYt−1 − log Yt−1)+ εyt (2)

log(Et/Yt) = E0/Y0 +β1t+(β2 +β3 log(t)) log(1+Pt/c)+ut (3)

ut = ρuut−1 + ε

ut (4)

Pt = (1+α)t−1P1 + f (Et) (5)

Hafstead and Williams (2018) Emissions Certainty Mechanisms 10 / 42

Reduced-Form Model: Central-Case Calibration

Trend parameters β1 and γ

EIA AEO 2017 estimates for 2017-2050Price elasticities β2 and β3 and constant term c

Fit long-run elasticity and constant term to steady-state outputfrom E3 CGE modelFit short-run elasticity, holding constant term fixed, to transitionoutput from Goulder-Hafstead E3 CGE model

Hafstead and Williams (2018) Emissions Certainty Mechanisms 11 / 42

Reduced-Form Model: Evaluating Price Elasticity Fit

-9.6

-9.4

-9.2

-9

-8.8

-8.6

-8.4

-8.2

-8

$0 $25 $50 $75 $100$125$150$175$200$225$250$275$300$325$350$375$400$425$450$475

log(Em

ission

sInten

sity)

CarbonPrice

E3 FiDedReduced-Form Non-FiDedReducedForm

Hafstead and Williams (2018) Emissions Certainty Mechanisms 12 / 42

Reduced-Form Model: Evaluating Price Elasticity Fit

0

1

2

3

4

5

2018 2022 2026 2030 2034 2038 2042 2046 2050

Energy-Related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

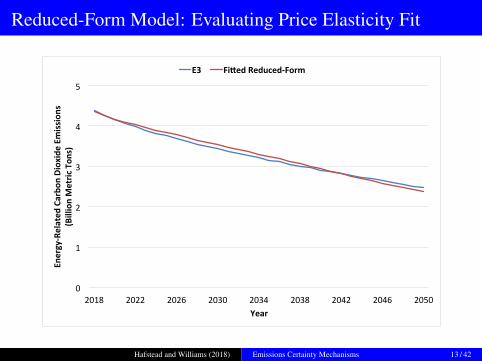

E3 Fi?edReduced-Form

Hafstead and Williams (2018) Emissions Certainty Mechanisms 13 / 42

Reduced-Form Model: Calibrating Uncertainty

Trend UncertaintyNormal distributionChoose std. dev. such that confidence interval matches AEOconfidence intervals

Cyclical UncertaintyCalibrate to match historical ()1973-2017) fluctuations

Price Elasticity UncertaintyLog-normal distribution (β2 and β3)Choose std. dev. to generate plausible confidence intervalsAlternatives include: Abrell and Rausch (2017), EMF32, others?

Hafstead and Williams (2018) Emissions Certainty Mechanisms 14 / 42

Outline

Intro

Emissions Certainty Mechanisms

Reduced-Form Model of Emissions with Uncertainty

Quantifying Emissions Uncertainty

Defining Emissions Certainty

Comparing Tax Adjustment Mechanisms

Hafstead and Williams (2018) Emissions Certainty Mechanisms 15 / 42

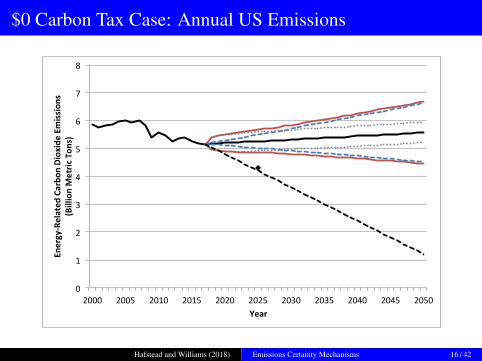

$0 Carbon Tax Case: Annual US Emissions

0

1

2

3

4

5

6

7

8

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Energy-Related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

Hafstead and Williams (2018) Emissions Certainty Mechanisms 16 / 42

$0 Carbon Tax Case: Cumulative US Emissions

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

108 116 124 132 140 148 156 164 172 180 188 196 204 212 220

Density

Cumula.veEmissions2017-2050,BillionMetricTons

FullUncertainty TrendUncertainty CyclicalUncertainty

Hafstead and Williams (2018) Emissions Certainty Mechanisms 17 / 42

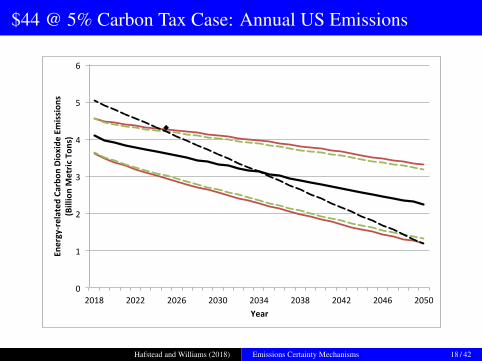

$44 @ 5% Carbon Tax Case: Annual US Emissions

0

1

2

3

4

5

6

2018 2022 2026 2030 2034 2038 2042 2046 2050

Energy-related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

Hafstead and Williams (2018) Emissions Certainty Mechanisms 18 / 42

$44 @ 5% Carbon Tax Case: Cumulative US Emissions

0

0.05

0.1

0.15

0.2

0.25

50 58 66 74 82 90 98 106 114 122 130 138 146 154 162

Density

Cumula.veEmissions2017-2050,BillionMetricTons

FullUncertainty TrendUncertainty CyclicalUncertainty Elas.cityUncertainty

Hafstead and Williams (2018) Emissions Certainty Mechanisms 19 / 42

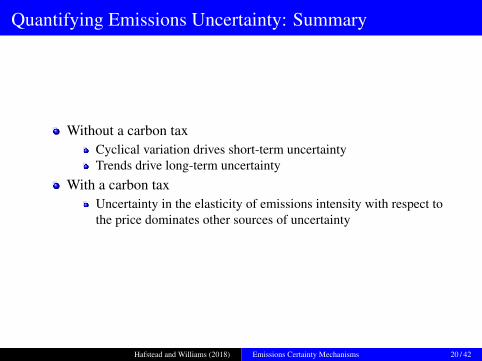

Quantifying Emissions Uncertainty: Summary

Without a carbon taxCyclical variation drives short-term uncertaintyTrends drive long-term uncertainty

With a carbon taxUncertainty in the elasticity of emissions intensity with respect tothe price dominates other sources of uncertainty

Hafstead and Williams (2018) Emissions Certainty Mechanisms 20 / 42

Outline

Intro

Emissions Certainty Mechanisms Examples

Reduced-Form Model of Emissions with Uncertainty

Quantifying Emissions Uncertainty

Defining Emissions Certainty

Comparing Tax Adjustment Mechanisms

Hafstead and Williams (2018) Emissions Certainty Mechanisms 21 / 42

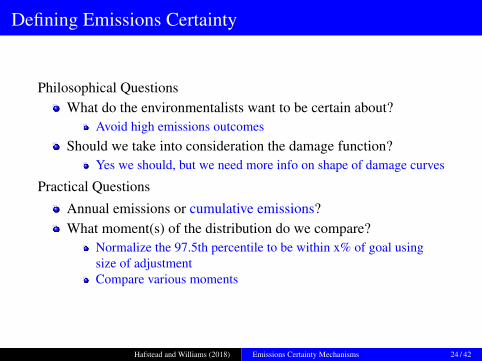

Defining Emissions Certainty

Philosophical Questions

What do the environmentalists want to be certain about?

Should we take into consideration the damage function?

Practical Questions

Annual emissions or cumulative emissions?

What moment(s) of the distribution do we compare?

Hafstead and Williams (2018) Emissions Certainty Mechanisms 22 / 42

Cumulative Emissions Distribution: Examples

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

50 58 66 74 82 90 98 106 114 122 130 138 146 154 162

Dens

ity

Cumulative Emissions 2017-2050, Billion Metric Tons

Hafstead and Williams (2018) Emissions Certainty Mechanisms 23 / 42

Cumulative Emissions Distribution: Examples

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

50 58 66 74 82 90 98 106 114 122 130 138 146 154 162

Dens

ity

Cumulative Emissions 2017-2050, Billion Metric Tons

Hafstead and Williams (2018) Emissions Certainty Mechanisms 23 / 42

Cumulative Emissions Distribution: Examples

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

50 58 66 74 82 90 98 106 114 122 130 138 146 154 162

Dens

ity

Cumulative Emissions 2017-2050, Billion Metric Tons

Hafstead and Williams (2018) Emissions Certainty Mechanisms 23 / 42

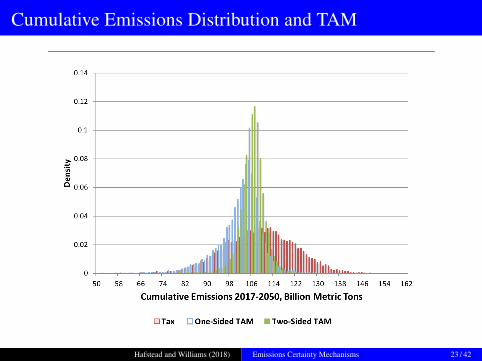

Cumulative Emissions Distribution and TAM

Hafstead and Williams (2018) Emissions Certainty Mechanisms 23 / 42

Cumulative Emissions Distribution and TAM

Hafstead and Williams (2018) Emissions Certainty Mechanisms 23 / 42

Defining Emissions Certainty

Philosophical QuestionsWhat do the environmentalists want to be certain about?

Avoid high emissions outcomesShould we take into consideration the damage function?

Yes we should, but we need more info on shape of damage curves

Practical Questions

Annual emissions or cumulative emissions?What moment(s) of the distribution do we compare?

Normalize the 97.5th percentile to be within x% of goal usingsize of adjustmentCompare various moments

Hafstead and Williams (2018) Emissions Certainty Mechanisms 24 / 42

Outline

Intro

Emissions Certainty Mechanisms Examples

Reduced-Form Model of Emissions with Uncertainty

Quantifying Emissions Uncertainty

Defining Emissions Certainty

Comparing Tax Adjustment Mechanisms

Hafstead and Williams (2018) Emissions Certainty Mechanisms 25 / 42

Comparing Tax Adjustment Mechanisms

Alternative mechanism design

Examples of TAM’s in practice

Comparison across mechanisms: A Monte Carlo experiment

Hafstead and Williams (2018) Emissions Certainty Mechanisms 26 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period

Targets and Benchmarks

Types of Adjustments

Frequency and Size of Adjustments

Adjustment Trigger

Hafstead and Williams (2018) Emissions Certainty Mechanisms 27 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of Adjustments

DiscreteGrowth rate “penalty”

Frequency and Size of Adjustments

2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050

Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of Adjustments

DiscreteGrowth rate “penalty”

Frequency and Size of Adjustments

2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of Adjustments

DiscreteGrowth rate “penalty”

Frequency and Size of Adjustments

2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative Emissions

Alternative benchmark pathsTypes of Adjustments

DiscreteGrowth rate “penalty”

Frequency and Size of Adjustments

2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of Adjustments

DiscreteGrowth rate “penalty”

Frequency and Size of Adjustments

2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of Adjustments

DiscreteGrowth rate “penalty”

Frequency and Size of Adjustments

2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of AdjustmentsDiscrete

Growth rate “penalty”Frequency and Size of Adjustments

2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of AdjustmentsDiscreteGrowth rate “penalty”

Frequency and Size of Adjustments

2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of AdjustmentsDiscreteGrowth rate “penalty”

Frequency and Size of Adjustments

2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of AdjustmentsDiscreteGrowth rate “penalty”

Frequency and Size of Adjustments2 or 5 years

Define stringency with size of adjustmentsAdjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of AdjustmentsDiscreteGrowth rate “penalty”

Frequency and Size of Adjustments2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of AdjustmentsDiscreteGrowth rate “penalty”

Frequency and Size of Adjustments2 or 5 yearsDefine stringency with size of adjustments

Adjustment Trigger

One Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of AdjustmentsDiscreteGrowth rate “penalty”

Frequency and Size of Adjustments2 or 5 yearsDefine stringency with size of adjustments

Adjustment TriggerOne Sided vs. Two Sided

Alternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Alternative Mechanism Design from Hafstead et al.

Rules vs. Discretion

Control Period 2018-2050Targets and Benchmarks

Cumulative EmissionsAlternative benchmark paths

Types of AdjustmentsDiscreteGrowth rate “penalty”

Frequency and Size of Adjustments2 or 5 yearsDefine stringency with size of adjustments

Adjustment TriggerOne Sided vs. Two SidedAlternative Thresholds

Hafstead and Williams (2018) Emissions Certainty Mechanisms 28 / 42

Example: $44 @ 5% Carbon Tax, No TAM

0

1

2

3

4

5

6

2018 2022 2026 2030 2034 2038 2042 2046 2050

Energy-Related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

(a) Emissions

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2018 2022 2026 2030 2034 2038 2042 2046 2050

Pricepe

rMetric

Ton

Year

(b) Price

Bad DrawGood Draw

Hafstead and Williams (2018) Emissions Certainty Mechanisms 29 / 42

Example: $44 @ 5% Carbon Tax, TAM

Central case benchmark path (annual emissions), growth rate penalty(5%), 5 years, One-Sided

0

1

2

3

4

5

6

2018 2022 2026 2030 2034 2038 2042 2046 2050

Energy-Related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

(a) Emissions

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2018 2022 2026 2030 2034 2038 2042 2046 2050

Pricepe

rMetric

Ton

Year

(b) Price

Bad DrawGood Draw

Hafstead and Williams (2018) Emissions Certainty Mechanisms 29 / 42

Example: $44 @ 5% Carbon Tax, TAM

Central case benchmark path (annual emissions), growth rate penalty(5%), 5 years, Two-Sided

0

1

2

3

4

5

6

2018 2022 2026 2030 2034 2038 2042 2046 2050

Energy-Related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

(a) Emissions

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2018 2022 2026 2030 2034 2038 2042 2046 2050

Pricepe

rMetric

Ton

Year

(b) Price

Bad DrawGood Draw

Hafstead and Williams (2018) Emissions Certainty Mechanisms 29 / 42

Example: $44 @ 5% Carbon Tax, TAM

Straight-line benchmark path (annual emissions), growth rate penalty(5%), 5 years, One-Sided

0

1

2

3

4

5

6

2018 2022 2026 2030 2034 2038 2042 2046 2050

Energy-Related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

(a) Emissions

$0

$100

$200

$300

$400

$500

$600

2018 2022 2026 2030 2034 2038 2042 2046 2050

Energy-Related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

(b) Price

Bad DrawGood Draw

Hafstead and Williams (2018) Emissions Certainty Mechanisms 29 / 42

Example: $44 @ 5% Carbon Tax, TAM

Straight-line benchmark path (annual emissions), growth rate penalty(5%), 5 years, Two-Sided

0

1

2

3

4

5

6

2018 2022 2026 2030 2034 2038 2042 2046 2050

Energy-Related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

(a) Emissions

$0

$100

$200

$300

$400

$500

$600

2018 2022 2026 2030 2034 2038 2042 2046 2050

Energy-Related

Carbo

nDioxideEm

ission

s(BillionMetric

Ton

s)

Year

(b) Price

Bad DrawGood Draw

Hafstead and Williams (2018) Emissions Certainty Mechanisms 29 / 42

Mechanism Comparison

Key questions

How do the additional expected costs vary across mechanisms?

What are the trade-offs across mechanisms?

Do some mechanisms Pareto dominate others?

Hafstead and Williams (2018) Emissions Certainty Mechanisms 30 / 42

Cost vs Emissions (97.5th percentile)

Hafstead and Williams (2018) Emissions Certainty Mechanisms 31 / 42

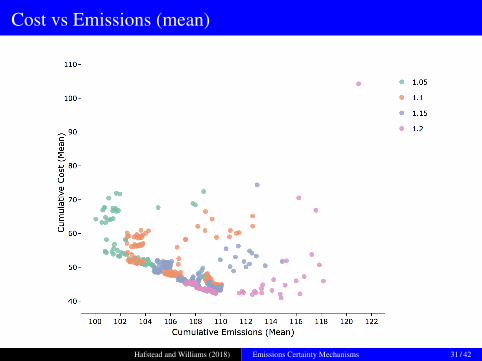

Cost vs Emissions (mean)

Hafstead and Williams (2018) Emissions Certainty Mechanisms 31 / 42

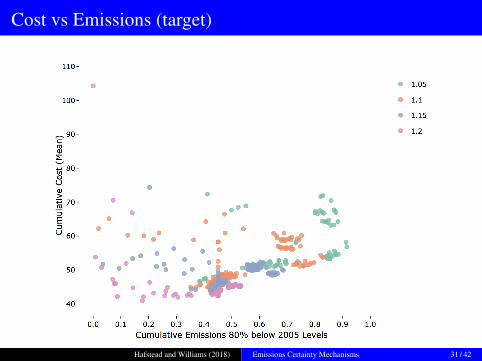

Cost vs Emissions (target)

Hafstead and Williams (2018) Emissions Certainty Mechanisms 31 / 42

Mechanism Comparison

Key questionsHow do the additional expected costs vary across mechanisms?

ConsiderablyWhat are the trade-offs across mechanisms?

Mechanisms that are more costly at reducing “right-side” riskmay have lower average emissions (or higher probability ofmeeting projected cumulative emissions goal)

Do some mechanisms Pareto dominate others?

Hafstead and Williams (2018) Emissions Certainty Mechanisms 32 / 42

Mechanism Comparison: Details

Alternative benchmark paths

Type of Adjustment

Frequency of Adjustment

One-side vs Two-sided

Hafstead and Williams (2018) Emissions Certainty Mechanisms 33 / 42

Cost vs Emissions (97.5th percentile): Adj. Path

Hafstead and Williams (2018) Emissions Certainty Mechanisms 34 / 42

Cost vs Emissions (mean): Adj. Path

Hafstead and Williams (2018) Emissions Certainty Mechanisms 34 / 42

Cost vs Emissions (target): Adj. Path

Hafstead and Williams (2018) Emissions Certainty Mechanisms 34 / 42

Mechanism Comparison: Details

Alternative benchmark pathsCentral case path Pareto dominates straight-line path

Type of Adjustment

Frequency of Adjustment

One-side vs Two-sided

Hafstead and Williams (2018) Emissions Certainty Mechanisms 35 / 42

Cost vs Emissions (97.5th percentile): Type of Adj.

Hafstead and Williams (2018) Emissions Certainty Mechanisms 36 / 42

Cost vs Emissions (mean): Type of Adj.

Hafstead and Williams (2018) Emissions Certainty Mechanisms 36 / 42

Cost vs Emissions (target): Type of Adj.

Hafstead and Williams (2018) Emissions Certainty Mechanisms 36 / 42

Mechanism Comparison: Details

Alternative benchmark pathsCentral case path Pareto dominates straight-line path

Type of AdjustmentDiscrete adjustments seem to dominate growth rate penalties

Frequency of Adjustment

One-side vs Two-sided

Hafstead and Williams (2018) Emissions Certainty Mechanisms 37 / 42

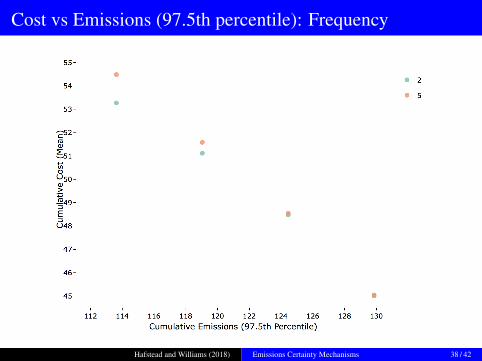

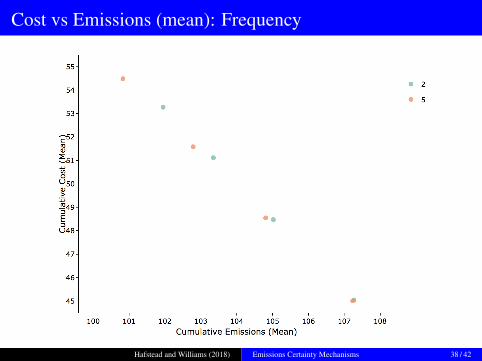

Cost vs Emissions (97.5th percentile): Frequency

Hafstead and Williams (2018) Emissions Certainty Mechanisms 38 / 42

Cost vs Emissions (mean): Frequency

Hafstead and Williams (2018) Emissions Certainty Mechanisms 38 / 42

Cost vs Emissions (target): Frequency

Hafstead and Williams (2018) Emissions Certainty Mechanisms 38 / 42

Mechanism Comparison: Details

Alternative benchmark pathsCentral case path Pareto dominates straight-line path

Type of AdjustmentDiscrete adjustments seem to Pareto dominate growth ratepenalties

Frequency of AdjustmentMore frequent adjustments are more cost-effective given 97.5percentile targetLess frequent adjustments may lead to lower emissionsUnclear if there is Pareto dominance

One-side vs Two-sided

Hafstead and Williams (2018) Emissions Certainty Mechanisms 39 / 42

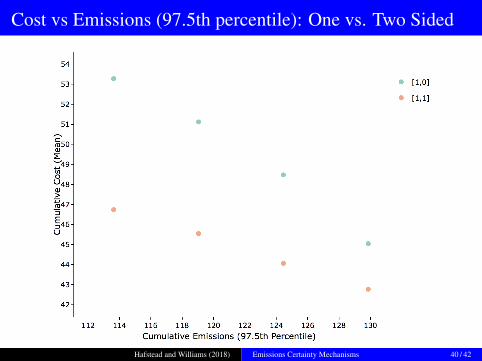

Cost vs Emissions (97.5th percentile): One vs. Two Sided

Hafstead and Williams (2018) Emissions Certainty Mechanisms 40 / 42

Cost vs Emissions (mean): One vs Two Sided

Hafstead and Williams (2018) Emissions Certainty Mechanisms 40 / 42

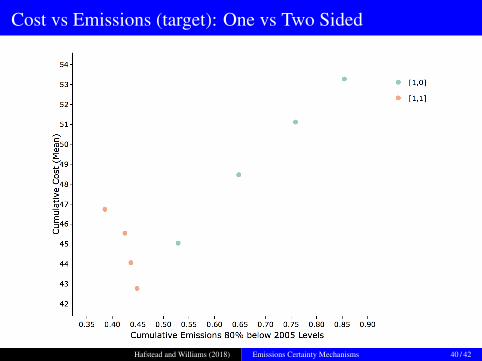

Cost vs Emissions (target): One vs Two Sided

Hafstead and Williams (2018) Emissions Certainty Mechanisms 40 / 42

Mechanism Comparison: Details

Alternative benchmark pathsCentral case path Pareto dominates straight-line path

Type of AdjustmentDiscrete adjustments seem to Pareto dominate growth ratepenalties

Frequency of AdjustmentMore frequent adjustments are more cost-effective given 97.5percentile targetLess frequent adjustments may lead to lower emissionsUnclear if there is Pareto dominance

One-side vs Two-sidedTwo-sided adjustments are far more cost-effective given 97.5percentile targetTwo-sided adjustments are much less likely to hit projectedemissions target

Hafstead and Williams (2018) Emissions Certainty Mechanisms 41 / 42

Conclusion

Using a new reduced-form model, we

quantify emissions uncertainty under a carbon tax

perform a comprehensive quantitative analysis of tax adjustmentmechanisms

We find

emissions uncertainty is potentially large

tax adjustment mechanisms can reduce right-side risk at amoderate expected cost

trade-offs exist across mechanisms

Hafstead and Williams (2018) Emissions Certainty Mechanisms 42 / 42