measuring economic impacts of b2b e-business basic modelling considerations

TRANSCRIPT

RCSResearch onCom petitive Strategies

Measuring Economic Impacts of B2Be-Business

Basic Modelling Considerations

OverviewOverview

Theoretical assumptions on impacts

Our approach of measurement

How to modify the initial model?

What is e-Business

Results

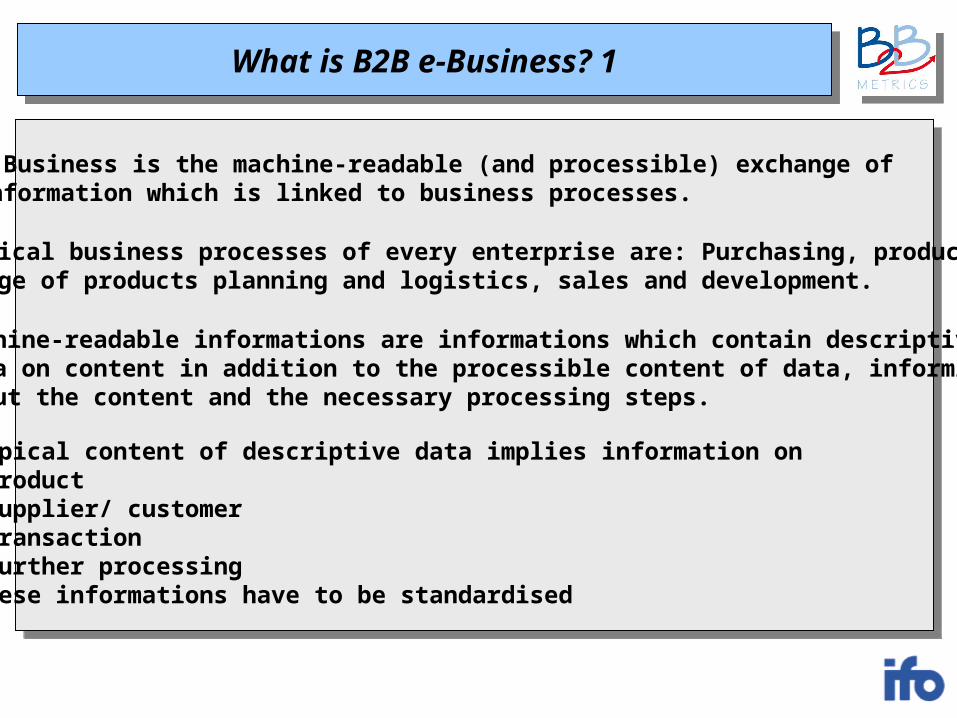

What is B2B e-Business? 1What is B2B e-Business? 1

E-Business is the machine-readable (and processible) exchange of information which is linked to business processes.

Typical content of descriptive data implies information on•Product•Supplier/ customer•Transaction•Further processingThese informations have to be standardised

Typical business processes of every enterprise are: Purchasing, production/range of products planning and logistics, sales and development.

Machine-readable informations are informations which contain descriptivedata on content in addition to the processible content of data, informing about the content and the necessary processing steps.

What is B2B e-Business? 2What is B2B e-Business? 2

E-Business therefore is the standardised exchange of information related to business processes which needs standards on several levels:

Product/ supplier/ customer standardCatalogue format standardTransmission standard andIntegration standard

The aim is not only the automation of processes but the integration of information into all relevant process chains

within the enterprise and with all partners in the value chain

in order to increase transparency and throughput speed and to savetransaction, capital and handling cost.

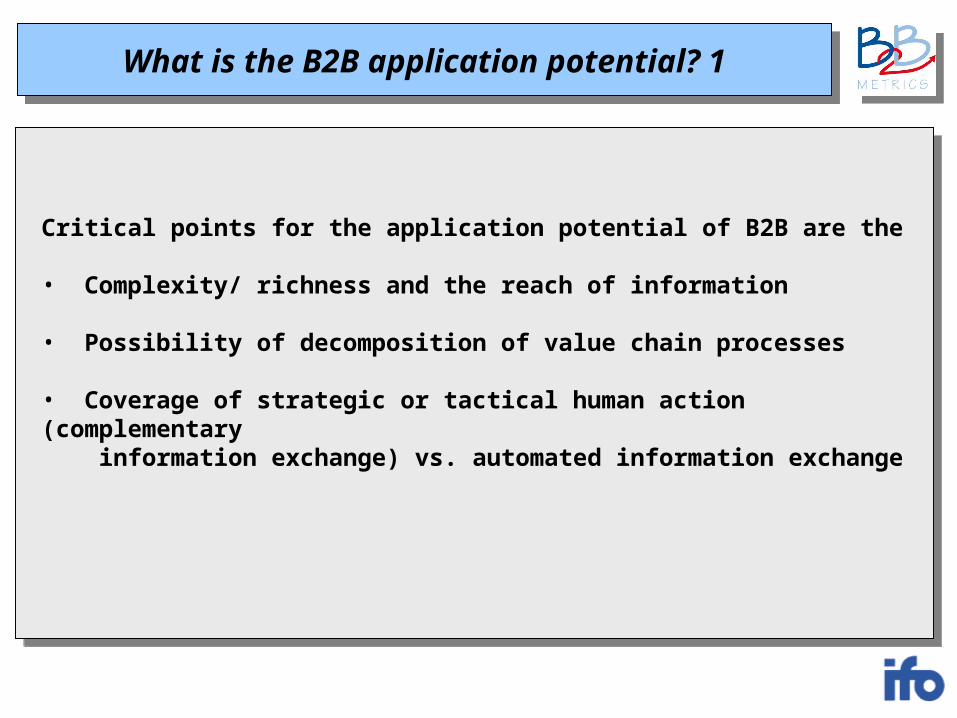

What is the B2B application potential? 1What is the B2B application potential? 1

Critical points for the application potential of B2B are the

• Complexity/ richness and the reach of information

• Possibility of decomposition of value chain processes

• Coverage of strategic or tactical human action (complementary information exchange) vs. automated information exchange

What is the B2B application potential? 2What is the B2B application potential? 2

Complementary informationexchange for strategic and tactical

human action

B2B informationexchange

Very richinformation

Informationwith potentially wide reach

Types of Business InformationTypes of Business Information

complementary communicationcomplementary communication

feasible & measurable as B2B

simple information

very rich

information

Batch EDI interchange structureBatch EDI interchange structure

Name Tag Status

Service String Advice UNA ConditionalInterchange Header UNB MandatoryGroup Header UNG ConditionalMessage Header UNH Mandatory

Message Body

Message Trailer UNT MandatoryGroup Trailer UNE ConditionalInterchange Trailer UNZ Mandatory

Interactive EDI interchange structureInteractive EDI interchange structure

Name Tag StatusService String Advice UNA Conditional

Interactive Interchange Header UIB MandatoryInteractive Message Header UIH Mandatory

Message Body

Interactive Message Trailer UIT MandatoryInteractive Interchange Trailer UIZ Mandatory

Example message segment tableExample message segment table

-----------------------------------------------------------------------------POS TAG Name S R Notes0010 Uxx Message header M 10020 AAA Segment AAA name M 10030 BBB Segment BBB name C 90040 CCC Segment CCC name C 90050 ---------- Segment group 1 ------------------ C 999 -------+ 10060 DDD Segment DDD name M 1 |0070 EEE Segment EEE name C 9 |0080 FFF Segment FFF name C 9 |0090 GGG Segment GGG name C 1 -------+0100 ---------- Segment group 2 ------------------ C 9 -------+ 10110 HHH Segment HHH name M 1 |

|0120 ---------- Segment group 3 ------------------ C 9 ------++0130 III Segment III name M 1 | |0140 JJJ Segment JJJ name C 9 | |

| |0150 ---------- Segment group 4 ------------------ C 9 -----+ | |0160 KKK Segment KKK name M 1 | | |0170 LLL Segment LLL name C 9 -----+++...nnnn Uxx Message trailer M 1DEPENDENCY NOTES:1. D3(0050, 0100) One or more-----------------------------------------------------------------------------

An example for information storage from JapanAn example for information storage from Japan

Spec information

Assemble makers

Order information

Deployment

Operation

Integrated DB

STEP: engineering dataEDI: electronic orderingSGML: technical doc.

Order

Eng. Designing

Production

Delivery

Auto parts makers

Spec information

Assemble makers

Order information

Deployment

Operation

Integrated DB

STEP: engineering dataEDI: electronic orderingSGML: technical doc.

Integrated DB

STEP: engineering dataEDI: electronic orderingSGML: technical doc.

Order

Eng. Designing

Production

Delivery

Auto parts makers

Source: Japan Automobile Manufacturing Association, Inc.Figure: An example of CALS network

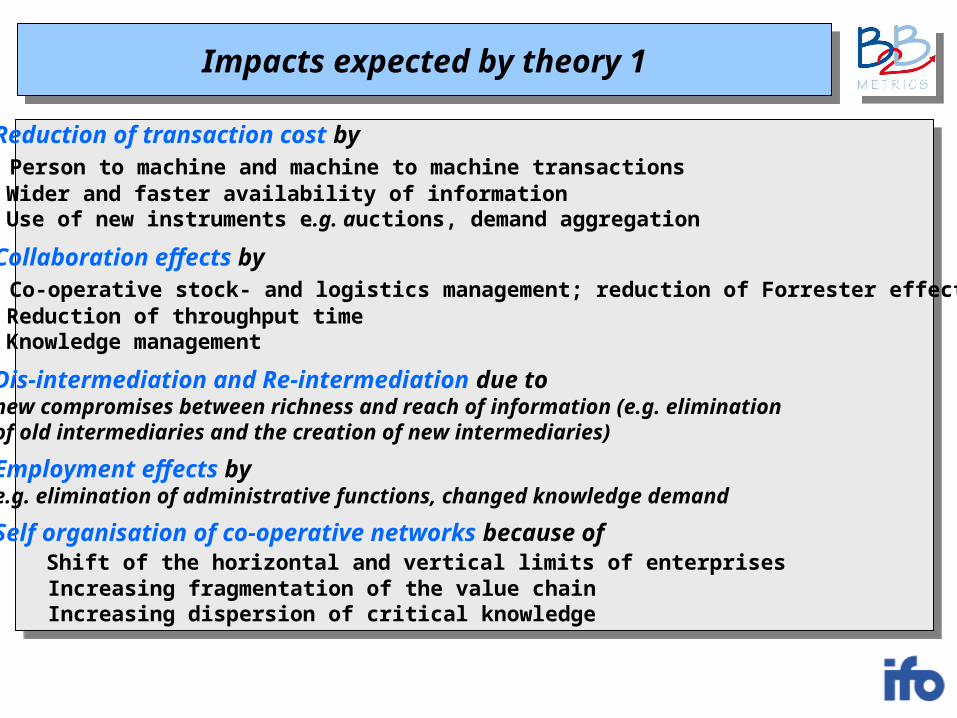

Impacts expected by theory 1Impacts expected by theory 1

Reduction of transaction cost by Person to machine and machine to machine transactions Wider and faster availability of information Use of new instruments e.g. auctions, demand aggregation

Collaboration effects by Co-operative stock- and logistics management; reduction of Forrester effects Reduction of throughput time Knowledge management

Dis-intermediation and Re-intermediation due tonew compromises between richness and reach of information (e.g. eliminationof old intermediaries and the creation of new intermediaries)

Employment effects bye.g. elimination of administrative functions, changed knowledge demand

Self organisation of co-operative networks because of Shift of the horizontal and vertical limits of enterprises Increasing fragmentation of the value chain Increasing dispersion of critical knowledge

Impacts expected by theory 2Impacts expected by theory 2

Diffusion of “General Purpose Technologies”(Helpman/ Trajtenberg)

characterised by•Pervasiveness

•continuous technol. advances•Necessity of complementary innovation

•Impacts dependent on completion of complementary innovation•“downstream” productivity gains

Typical diffusion phases(Strassman, Skinner, Millard...)

characterised by•Implementation of new technology•Internal diffusion of applications

•Definition of standards & interfaces •New process organisation•Organisational adaptation

Our approach 1Our approach 1

AimsAims

Problems /Framework conditions

Problems /Framework conditions

B2B e-Business Processes

B2B e-Business Processes ImpactsImpacts

Infrastructure / complementary

Innovation

Infrastructure / complementary

Innovation

Our approach 2Our approach 2

InfrastructureInfrastructure

UseUse

StandardisationStandardisation

Complementary Innovation

Complementary Innovation

Systems integrationSystems integration

ImpactsImpacts

“preparatory”

X

X

X

X

X

X

X

“advanced application”

X

X

X

“early application”

X

X

X

X

X

“enlarged application”

X

Our approach 3Our approach 3

Product / Service Value Chain

Enterprise Related Services /Equipment Value Chain

Tier NSuppliers

Tier NSuppliers

Tier 1Suppliers

Tier 1Suppliers

“Core” Firms

“Core” Firms

Business Customers

Business Customers

Equipment & indirect

goodsSuppliers

Equipment & indirect

goodsSuppliers

Enterprise Oriented Service

Suppliers

Enterprise Oriented Service

Suppliers

Results 1Results 1

Sample distribution by phase of developmentresponses in % (n=121)

Source: ifo distribution survey 2003

advanced34,4%

enlarged34,4%

early13,1%

not classifiable18,0%

Ergebnisse der Diffusion 1aErgebnisse der Diffusion 1a

Enterprises with network mediated collaborationSorted by number of used applications

ifo B2B survey distribution co-operations

15,8%

3,3%

3,3%2,5%

34,2%

10,8%

3,3% 8,3%

18,3%

No collaboration 75% (90)

Four applicationsThree applications

Two applications

One applicationIntegrated payment

No application

Catalogue use

Service applications Simple applications

Distributionn=121

Ergebnisse der Diffusion 2Ergebnisse der Diffusion 2

Access to EDI and other networksresponses in %

yes23,0%

no67,0%

no answer10,0%

yes17,0%

no73,0%

no answer10,0%

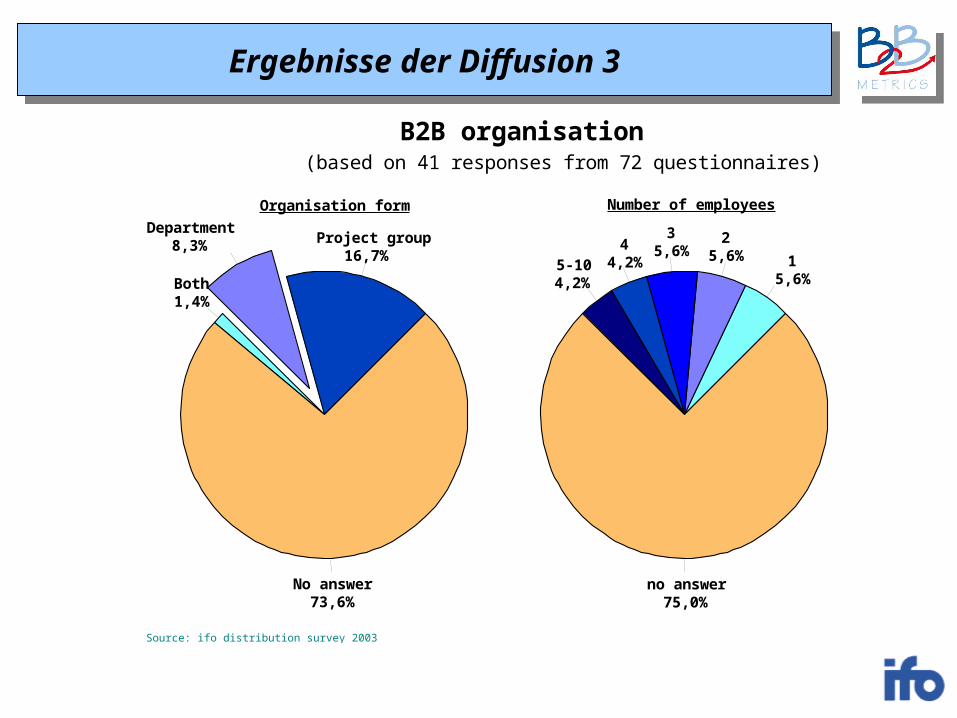

Ergebnisse der Diffusion 3Ergebnisse der Diffusion 3

B2B organisation (based on 41 responses from 72 questionnaires)

Source: ifo distribution survey 2003

Project group16,7%

Department8,3%

Both1,4%

No answer73,6%

15,6%

25,6%

35,6%4

4,2%5-104,2%

no answer75,0%

Organisation form Number of employees

Ergebnisse der Diffusion 4Ergebnisse der Diffusion 4

Use of standards for....(based on 41 responses from 72 questionnaires)

Source: ifo distribution survey 2003

yes29,2%

planned5,6%

no13,9%

no answer51,4%

yes29,2%

planned9,7%

no12,5%

no answer48,6%

yes36,1%planned

8,3%

no6,9%

no answer48,6%

yes11,1%

planned5,6%

no19,4%

no answer63,9%

Product/ supplier classification

Catalogdataexchange

Data transmission

Dataintegration

Ergebnisse der Diffusion 5Ergebnisse der Diffusion 5

Internal integration through...(based on 41 responses from 72 questionnaires)

Independent systems1,4%

Partly integrated12,5%

Integrated systems4,2%

Integration not specif15,3%

No system19,4%

No answer47,2%

mostly20,8%

partially11,1%

no18,1%

does not make sense4,2%

no answer45,8%

use of ERPsystems

Integrationof processes andoperational accounting

Ergebnisse der Diffusion 6Ergebnisse der Diffusion 6

External integration with suppliers and B-customers(based on 41 responses from 72 questionnaires)

mostly2,8%

partially44,4%

no5,6%

no answer47,2%

mostly9,7%

partially23,6%

no15,3%

does not make sense2,8%

no answer48,6%

Suppliers B-customers

Ergebnisse der Diffusion 7Ergebnisse der Diffusion 7

Planning data exchange with...(based on 41 responses from 72 questionnaires)

Source: ifo distribution survey 2003

yes4,2%

planned6,9%

no43,1%

no answer45,8%

yes2,8%

in part15,3%

planned1,4%no

31,9%

no answer48,6%

Suppliers B-customers

Ergebnisse der Diffusion 8Ergebnisse der Diffusion 8

Main problems of integration(based on 41 responses from 72 questionnaires)

Source: ifo distribution survey 2003

Very high cost

Multitude of external standards

Lacking willingness to share data

Missing Interfaces

Missing standardisation

Problems in updating

No trained employees

Data security

Several decentralised solutions

0% 20% 40% 60% 80% 100%

internally

externally

both

no answer

Nutzung neuer Techniken 1Nutzung neuer Techniken 1

Bundling of purchasing of indirect goods(based on 41 responses from 72 questionnaires)

Source: ifo distribution survey 2003

in our enterprise23,6%

with external partners6,9%

both1,4%

no answer68,1%

Nutzung neuer Techniken 2Nutzung neuer Techniken 2

Use of marketplaces in purchasing (supplier/ own/ independent)(based on 41 responses from 72 selected firms)

Source: ifo distribution survey 2003

raw/ intermediate products

indirect goods

Services

investment goods

0 10 20 30 40 50 60 70

supplier portal own portal

exchange neither

Nutzung neuer Techniken 3Nutzung neuer Techniken 3

Use of marketplaces in sales (supplier/ own/ independent)(based on 41 responses from 72 selected firms)

Source: ifo distribution survey 2003

final products

parts/ accessories

0 10 20 30 40 50 60

supplier portal own portal

exchange neither

Wirkungen 1Wirkungen 1

Procurement

Reduced personnel cost

Reduction of stocks, interest paid

Reduced procurement prices

Process time reduction

Reduction in number of suppliers

0% 20% 40% 60% 80% 100%

clearly measurable

not measurable

increase

no answer

Wirkungen 2Wirkungen 2

Production planning, logistics

Reduced personnel cost

Reduction of stocks, interest paid

Process time reduction

0% 20% 40% 60% 80% 100%

clearly measurable

not measurable

increase

no answer

Impacts

Wirkungen 3Wirkungen 3

Impacts of sales and marketing applications(based on 41 responses from 72 questionnaires)

Sorce: ifo distribution survey 2003

Reduced personnel cost

Reduction of stocks, interest paid

Process time reduction

0% 20% 40% 60% 80% 100%

clearly measurable

not measurable

increase

no answer

Wirkungen 4Wirkungen 4

Sample distribution by phase of developmentresponses in % (n=224)

Source: ifo automotive survey 2003

advanced72,3%

enlarged19,6%

early7,1%

not classifiable0,9%

Zum Vergleich: Handelskooperationen 34%

Wirkungen 5Wirkungen 5

Enterprises with network mediated collaborationSorted by number of used applications

ifo B2B survey automotive industry 2003

16,1%

21,9%

12,5%

10,3%

3,1%1,8%

17,4%

9,8%

2,2%

4,0%

0,9%

No collaboration 34,4% (77)

Four applications

Three applications

Two applications

One application

Integrated payment

No application

Catalogue use

Service applications

Simple applications

Automotiven=224

Five applications

Six applications

Automobilindustrie 65%Zum Vergleich: Handelskooperationen 25%

How to modify the initial model?How to modify the initial model?

Important, not included framework conditions

Existence of enterprises with formative power

Fragmentation of the value chain

Concentration of management, product- and process knowledge

Possibility to standardise processes

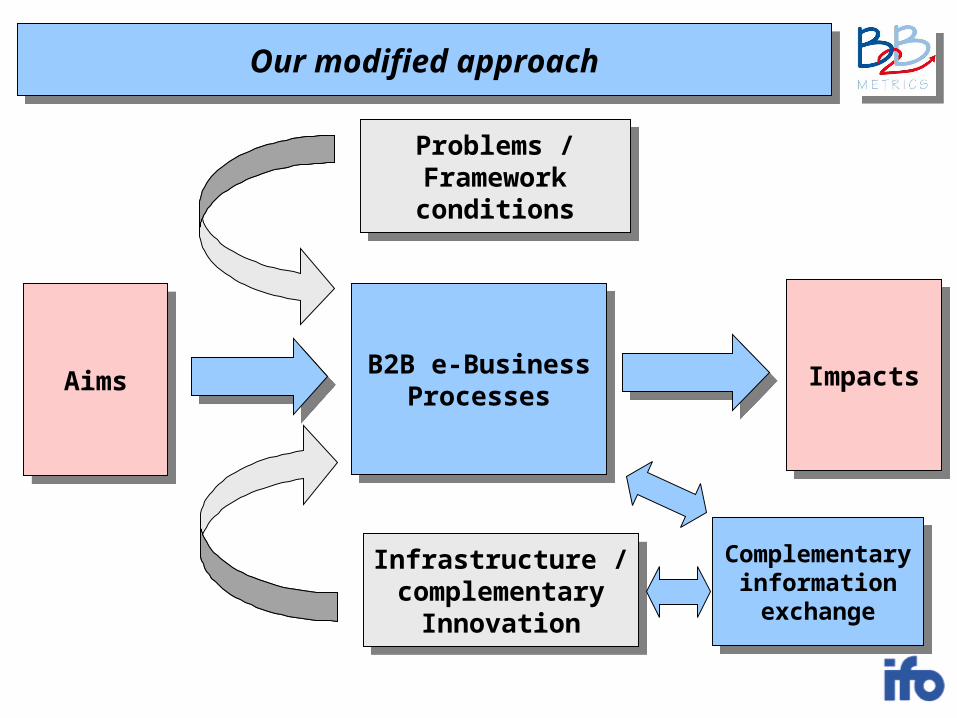

Our modified approachOur modified approach

AimsAims

Problems /Framework conditions

Problems /Framework conditions

B2B e-Business Processes

B2B e-Business Processes ImpactsImpacts

Infrastructure / complementary

Innovation

Infrastructure / complementary

Innovation

Complementary information exchange

Complementary information exchange