measuring and forecasting financial wellness · 2017-04-26 · measuring and forecasting financial...

TRANSCRIPT

PAGE 1

Measuring and Forecasting

Financial Wellness

PAGE 2

What does financial wellness have to do with the weather? In both, the ability to measure, track, and

forecast its impact leads people to be better prepared. But, unlike the weather, there has not historically been a clear way to measure, track, and forecast a person’s financial state. With this in mind, our new research has helped us:

Define financial wellnessCreate the Fidelity Financial Wellness Score to measure itEstimate the wellness level of a workforce

These insights will help employers better understand the financial state of their employees, pinpoint the areas where workers need help, and provide solutions to ultimately drive improved outcomes.

PAGE 3

Being well ... and feeling wellWe believe being financially well is about more than just dollars and cents. It’s also about how people feel. The two don’t always line up.

51% 30%62% 40%57%48%have less than

3 months’ salary saved for an emergency1

feel anxious, worried, or sick

about their finances2

can’t be happy unless they feel

financially secure2

have credit card debt2

either just break even or spend more than they

earn each month1

feel they have too

much debt2

H O W P E O P L E A R E D O I N G H O W T H E Y ’ R E F E E L I N G

PAGE 3

PAGE 4

28%

54%24%

of workers are less committed at work after periods of stress4

are distracted at work by finances3 avoid medical treatment

due to cost5

Many bring stress to work Reducing financial stress can decrease absenteeism, increase productivity, and improve health—benefiting employers and employees alike.

PAGE 4

PAGE 5

BUDGET (25%)• Calculation of monthly

essential spending compared to take-home pay

• How they feel about their spending

• Household income• Retirement savings rate• Pension income• How they feel about their

ability to save• Likelihood they are on

track to meet goals

DEBT (25%)• Monthly debt payments

compared to gross income• Credit score• Types of debt• How they feel about their

debt

• Ability to cover emergency expenses

• Appropriate insurance• Feeling that they have

adequate protection• Time horizon they are

planning for

The basis for measuring financial wellness We believe financial wellness is based on four things: Budget, savings, debt, and protection, each with underlying components that create a holistic financial picture. In building a financial wellness score, we started by giving each domain equal weight (25%).

SAVINGS (25%)

PROTECTION (25%)

PAGE 6

70%“How they’re doing” Objective measures include income, savings, real spending, debt, and insurance coverage. These things are indicative of the behaviors people exhibit.

30%“How they’re

feeling” Subjective measures focus on

how a person feels about their spending, debt, savings, and

insurance. This is important because emotions also drive behaviors, but this does not

carry the same weight as objective measures.

The balance of being well and feeling well Within each of the four domains of financial wellness—budget, debt, savings, and protection—there are both objective and subjective measures. While each domain carries equal weight in building a score, the objective measures of “how they’re doing” outweigh “how they’re feeling.”

Budget25%

Debt25%

Savings25%

Protection25%

PAGE 7

This score provides a framework to measure overall wellness and help individuals understand where they

may need to improve. To build the score, we collected in-depth financial data from more than 6,000 people.2 Their responses, along with Fidelity’s definition of financial wellness and points of view on personal finance, allowed us to score respondents in each of the four domains of financial wellness, as well as give them an overall score.

FIDELITY FINANCIAL WELLNESS SCORE

Objective “How they’re doing”

Subjective“How they’re feeling” Total

Budget

Debt

Savings

Protection

Financial Wellness Score

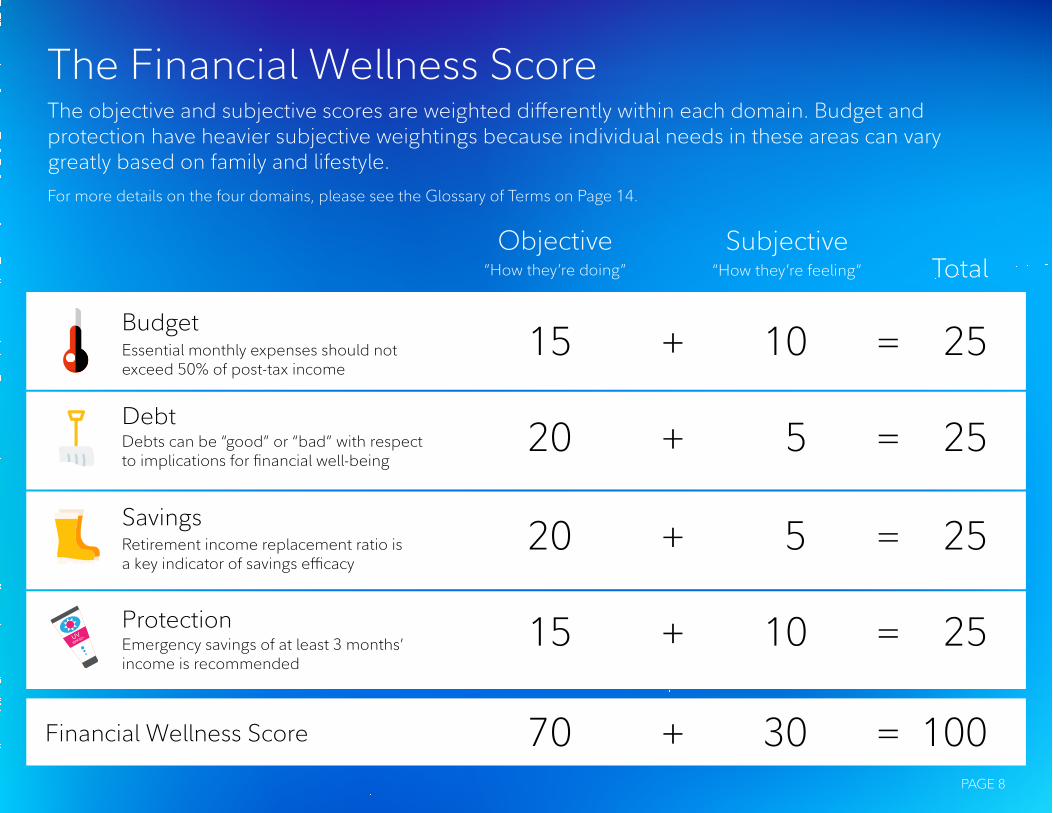

15 + 10 = 25

20 + 5 = 25

20 + 5 = 25

15 + 10 = 25

70 + 30 = 100

Essential monthly expenses should not exceed 50% of post-tax income

Debts can be “good” or “bad” with respect to implications for financial well-being

Retirement income replacement ratio is a key indicator of savings e�cacy

Emergency savings of at least 3 months’ income is recommended

The Financial Wellness ScoreThe objective and subjective scores are weighted differently within each domain. Budget and protection have heavier subjective weightings because individual needs in these areas can vary greatly based on family and lifestyle. For more details on the four domains, please see the Glossary of Terms on Page 14.

PAGE 8

PAGE 9

What’s today’s report?

14% 37% 33%

81–100 61–80 41–60

16%

0–40Excellent Good Fair At risk

How our survey respondents scored:

We applied our research to divide survey respondents into four categories. The scoring also helped drive a deeper

understanding of the financial behaviors of employees and the challenges they face.

For greater insight, read our white paper. See “About Fidelity’s Financial Score” on page 15 for methodology details. PAGE 9

PAGE 10

14% 37% 33% 16%24% 35% 42% 58%

7% 14% 19% 27%

18% 13% 8% 5%

1 2 3 4

10+ years 5–10 years 1 year Next few weeks

$150,000 $120,000 $85,000 $58,000

Excellent Good Fair At risk

% of take-home pay spent on essentials

Monthly debt payments as a % of pretax income

Retirement savings rate

Plan ahead time frame

Number of debts

Household income

The detailed reportWhen applying the score to the individuals surveyed, we see significant differences in the financial behaviors of those who fell into the Excellent category compared with those in other categories.

All numbers reported here are medians. PAGE 10

PAGE 11

PAGE 10

Like a weather forecast, financial modeling becomes more accurate when we have access to robust data. Our

survey population provided detailed financial information, which gave us the ability to create an accurate Financial Wellness Score by simply applying our methodology. We analyzed their retirement plan behaviors and found direct correlations between their actual level of financial wellness and their savings rate, balance, loan activity, and asset allocation in their DC plan. Our analysis of this data is the foundation for our Financial Wellness Model, which uses DC plan data alone to group participants into two categories: Financially well and needs attention.

See “About Fidelity’s Financial Model” on page 15 for methodology details.

PREDICTING FINANCIAL WELLNESS

PAGE 12

Based on DC plan behaviors alone, we can group your plan participants into two levels of financial wellness and see where they may need the most help.

54% 46%

Creating your forecast

Here’s an example of the results you can expect to see:

55%need help with savings 38%

Debt

32%Protection

40%Budget

Financially Well

Needs attention

See “About Fidelity’s Financial Model” on page 15 for methodology details. PAGE 12

PAGE 13

Preparing for tomorrow

The ability to define and measure Financial Wellness helps us better understand where employees might be struggling financially. Employers interested in improving the financial wellness of their employees should continue promoting resources focused on these key areas:

SPENDING HABITSMany are surprised by their monthly spending because they haven’t taken the time to create or review a budget.

LACK OF EMERGENCY SAVINGSBeing prepared for the unexpected can help avoid taking on debt or having to tap into long-term savings too early.

STUDENT LOAN DEBTAs the cost of education increases so does the burden on employees, which may keep them from being able to save for other future priorities.

NEED FOR PROTECTIONMany people need help understanding how to use estate planning, life insurance, and more to protect the assets they have worked so hard to accumulate.

PAGE 13

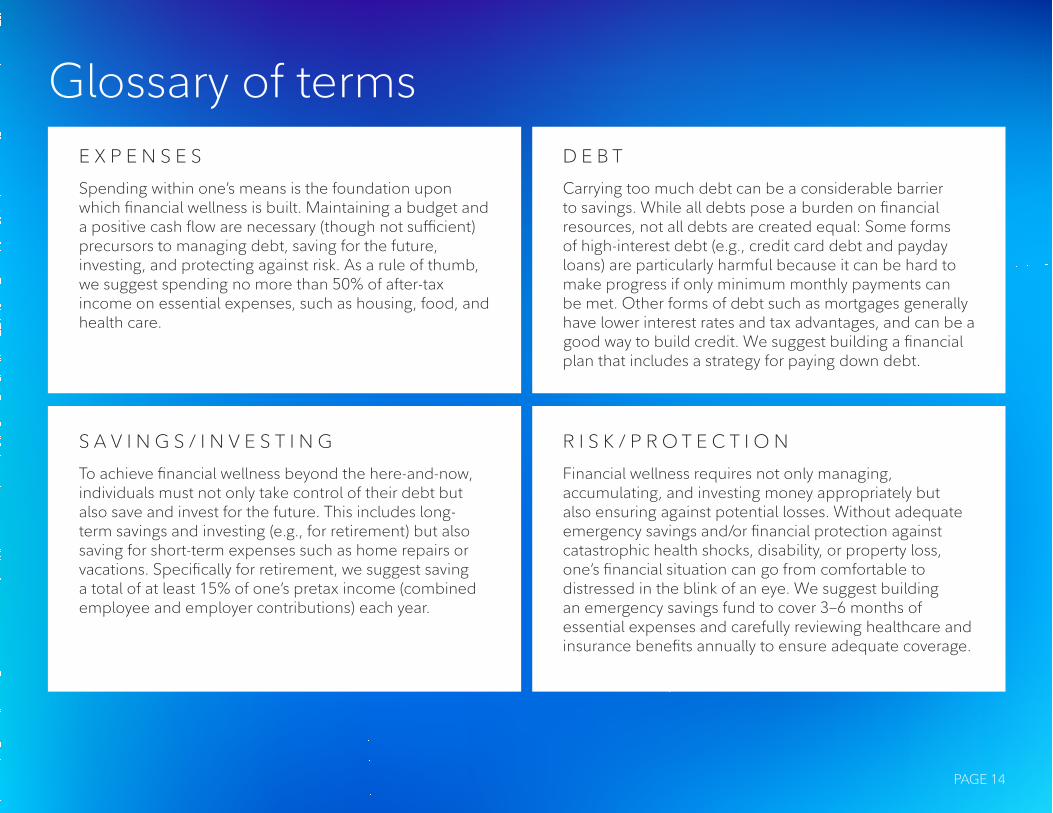

Glossary of termsE X P E N S E S

Spending within one’s means is the foundation upon which financial wellness is built. Maintaining a budget and a positive cash flow are necessary (though not sufficient) precursors to managing debt, saving for the future, investing, and protecting against risk. As a rule of thumb, we suggest spending no more than 50% of after-tax income on essential expenses, such as housing, food, and health care.

D E B T

Carrying too much debt can be a considerable barrier to savings. While all debts pose a burden on financial resources, not all debts are created equal: Some forms of high-interest debt (e.g., credit card debt and payday loans) are particularly harmful because it can be hard to make progress if only minimum monthly payments can be met. Other forms of debt such as mortgages generally have lower interest rates and tax advantages, and can be a good way to build credit. We suggest building a financial plan that includes a strategy for paying down debt.

S A V I N G S / I N V E S T I N G

To achieve financial wellness beyond the here-and-now, individuals must not only take control of their debt but also save and invest for the future. This includes long-term savings and investing (e.g., for retirement) but also saving for short-term expenses such as home repairs or vacations. Specifically for retirement, we suggest saving a total of at least 15% of one’s pretax income (combined employee and employer contributions) each year.

R I S K / P R O T E C T I O N

Financial wellness requires not only managing, accumulating, and investing money appropriately but also ensuring against potential losses. Without adequate emergency savings and/or financial protection against catastrophic health shocks, disability, or property loss, one’s financial situation can go from comfortable to distressed in the blink of an eye. We suggest building an emergency savings fund to cover 3–6 months of essential expenses and carefully reviewing healthcare and insurance benefits annually to ensure adequate coverage.

PAGE 14

1 Based on 296,700 responses from Fidelity Investments Financial Wellness Money Check-up from June-January 2016.2 Fidelity Markers of Financial Wellness Survey of more than 6,000 active Defined Contribution plan participants recordkept by Fidelity, who have input into household financial decisions. Conducted by CMI Research, an independent third-party research firm. July 2016.3 Pwc Employee Financial Wellness Survey, April 2016.4 Fidelity Investments Life Decisions Research online survey of more than 9,000 defined contribution plan participants recordkept by Fidelity and who are employed full time (more than 30 hours per week). The research was completed in October 2016 by Greenwald & Associates, Inc., an independent third-party research firm. Fidelity also worked in collaboration with the Stanford Center on Longevity on the study.

5 Gallup poll: telephone interviews conducted Nov. 4-8, 2015, with a random sample of 1,021 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia.

For Plan Sponsor and investment professional use only. Not for use with plan participants.

Approved for use in the advisor and 401(k) markets. Firm review may apply.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917

© 2017 FMR LLC. All rights reserved.

796962.1.0

About Fidelity’s Financial Wellness Score

These findings are the culmination of a yearlong research project with Strategic Advisers, Inc., a registered investment adviser and a Fidelity Investments company, which analyzed the overall financial wellness of 6,300 active retirement plan participants based on data collected through the Fidelity Financial Wellness Markers Survey, July 2016. Survey questions assessed objective and subjective indicators in four domains of personal finance (budget, debt, savings/investment, and protection) as well as general feelings and demographic characteristics. All four domains contribute 25% each to the overall score, for a total of 100%. Overall, the objective factors are assigned a total weight of 70% and overall subjective factors are weighted at 30%. However, the objective and subjective subscores are weighted differently across domains to reflect the fact that some domains are inherently more objective than others. For example, measures of debt and savings/investment are relatively clear-cut and straightforward (e.g., debt-to-income ratio and projected retirement replacement rate). By contrast, the objective aspects of budget and protection are relatively more difficult to quantify (e.g., whether an individual’s health insurance plan is optimal) and the subjective factors may play a greater role (e.g., whether an individual is comfortable with his/her level of protection). As a consequence, the objective subscores are weighted higher for the debt and savings/investment (20%) versus the budgeting and protection (15%), as shown in Figure 2. The subjective subscore for each domain is the complement of the 25% domain score (5% or 10%, respectively). This scoring approach affords great flexibility in breaking down the Fidelity Financial Wellness Score in ways that provide deep insights into personal financial wellbeing. The sum of all four domains yields a total score from 0 to 100, where 0 represents extreme financial distress and 100 indicates the maximum level of financial wellness. Data collection was completed by CMI Research. Fidelity Investments was not identified as the survey sponsor. CMI Research is an independent research firm not affiliated with Fidelity Investments.

About Fidelity’s Financial Wellness Model

The Financial Wellness predictive model was created using a combination of survey data and Fidelity recordkeeping data representing different aspects of participant’s financial behavior and Defined Contribution (DC) plan activity. It uses data from 6,000 participants who responded to the 2016 Financial Wellness survey, including their DC plan activity and the financial wellness score developed by Strategic Advisors. Behaviors within the DC plan are used to infer if a participant is well or unwell (based on SAI score) using a Random Forest model. Each component of wellness (Savings, Budget, Debt, Protection, and Overall) uses a separate model and has its own accuracy scores. Accuracy is calculated as the percent of correct classifications in the hold out sample, which is a random subset of the 6,000 survey respondents. For each model, accuracy is as follows: Overall Financial Wellness Model = 75% accuracy; Savings Model = 60% accuracy; Budget Model = 63% accuracy; Debt Model = 75% accuracy; and Protection Model = 71% accuracy.