measurement error 1 in this sequence we will investigate the consequences of measurement errors in...

TRANSCRIPT

MEASUREMENT ERROR

1

In this sequence we will investigate the consequences of measurement errors in the variables in a regression model. To keep the analysis simple, we will confine it to the simple regression model.

vZY 21 wZX

2

We will start with measurement errors in the explanatory variable. Suppose that Y is determined by a variable Z, but Z is subject to measurement error, w. We will denote the measured explanatory variable X.

MEASUREMENT ERROR

vZY 21 wZX

uX

wvX

vwXY

21

221

21 )(

vZY 21 wZX

3

Substituting for Z from the second equation, we can rewrite the model as shown.

MEASUREMENT ERROR

uX

wvX

vwXY

21

221

21 )(

vZY 21 wZX

4

We are thus able to express Y as a linear function of the observable variable X, with the disturbance term being a compound of the disturbance term in the original model and the measurement error.

wvu 2

MEASUREMENT ERROR

uX

wvX

vwXY

21

221

21 )(

w w

vZY 21 wZX

5

However if we fit this model using OLS, Assumption B.7 will be violated. X has a random component, the measurement error w.

MEASUREMENT ERROR

6

And w is also one of the components of the compound disturbance term. Hence u is not distributed independently of X.

uX

wvX

vwXY

21

221

21 )(

w w

MEASUREMENT ERROR

vZY 21 wZX

7

We will demonstrate that the OLS estimator of the slope coefficient is inconsistent and that in large samples it is biased downwards if 2 is positive, and upwards if 2 is negative.

vZY 21 wZX

uXY 21 wvu 2

MEASUREMENT ERROR

2222

22121

22

XX

uuXX

XX

uuXXXX

XX

uXuXXX

XX

YYXXb

i

ii

i

iii

i

iii

i

ii

8

We begin by writing down the OLS estimator and substituting for Y from the true model. In this case there are alternative versions of the true model. The analysis is simpler if you use the equation relating Y to X.

MEASUREMENT ERROR

2222

22121

22

XX

uuXX

XX

uuXXXX

XX

uXuXXX

XX

YYXXb

i

ii

i

iii

i

iii

i

ii

vZY 21 wZX

uXY 21 wvu 2

9

Simplifying, we decompose the slope coefficient into the true value and an error term as usual.

2222

22121

22

XX

uuXX

XX

uuXXXX

XX

uXuXXX

XX

YYXXb

i

ii

i

iii

i

iii

i

ii

MEASUREMENT ERROR

vZY 21 wZX

uXY 21 wvu 2

10

We have reached this point many times before. We would like to investigate whether b2 is biased. This means taking the expectation of the error term.

MEASUREMENT ERROR

2222

XX

uuXX

XX

YYXXb

i

ii

i

ii

vZY 21 wZX

uXY 21 wvu 2

11

However, it is not possible to obtain a closed-form expression for the expectation of the error term. Both its numerator and its denominator are functions of w and there are no expected value rules that can allow us to simplify.

MEASUREMENT ERROR

w

w

2222

XX

uuXX

XX

YYXXb

i

ii

i

ii

vZY 21 wZX

uXY 21 wvu 2

12

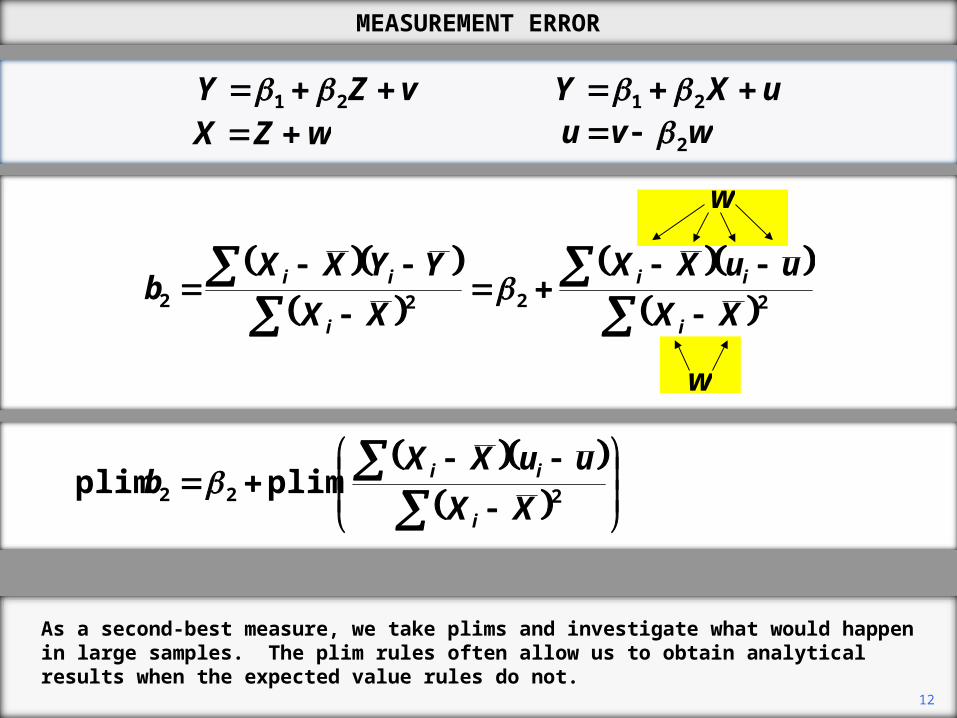

As a second-best measure, we take plims and investigate what would happen in large samples. The plim rules often allow us to obtain analytical results when the expected value rules do not.

222 plim plimXX

uuXXb

i

ii

MEASUREMENT ERROR

w

w

2222

XX

uuXX

XX

YYXXb

i

ii

i

ii

vZY 21 wZX

uXY 21 wvu 2

13

We focus on the error term. We would like to use the plim quotient rule. The plim of a quotient is the plim of the numerator divided by the plim of the denominator, provided that both of these limits exist.

MEASUREMENT ERROR

22

222

1

1

plim

plim plim

XXn

uuXXn

XX

uuXXb

i

ii

i

ii

vZY 21 wZX

uXY 21 wvu 2

BA

BA

plim plim

plim

if A and B have probability limits

and plim B is not 0.

14

However, as the expression stands, the numerator and the denominator of the error term do not have limits. The denominator increases indefinitely as the sample size increases. The nominator has no particular limit.

MEASUREMENT ERROR

22

222

1

1

plim

plim plim

XXn

uuXXn

XX

uuXXb

i

ii

i

ii

vZY 21 wZX

uXY 21 wvu 2

BA

BA

plim plim

plim

if A and B have probability limits

and plim B is not 0.

15

To deal with this problem, we divide both the numerator and the denominator by n.

22

222

1

1

plim

plim plim

XXn

uuXXn

XX

uuXXb

i

ii

i

ii

MEASUREMENT ERROR

BA

BA

plim plim

plim

if A and B have probability limits

and plim B is not 0.

vZY 21 wZX

uXY 21 wvu 2

16

It can be shown that the limit of the numerator is the covariance of X and u and the limit of the denominator is the variance of X.

uXuuXXn ii ,cov1

plim

XXXn i var1

plim 2

XuX

XXn

uuXXnb

i

ii

var,cov

1

1

plim plim2

22

MEASUREMENT ERROR

vZY 21 wZX

uXY 21 wvu 2

17

Hence the numerator and the denominator of the error term have limits and we are entitled to implement the plim quotient rule. We need var(X) to be non-zero, but this will be the case assuming that there is some variation in X.

MEASUREMENT ERROR

uXuuXXn ii ,cov1

plim

XXXn i var1

plim 2

XuX

XXn

uuXXnb

i

ii

var,cov

1

1

plim plim2

22

vZY 21 wZX

uXY 21 wvu 2

22

2

2222 )var(,cov

plimwZ

w

XuX

b

22

22

2

000

,cov,cov,cov,cov

,cov,cov

w

wwwZvwvZ

wvwZuX

vZY 21 wZX

uXY 21 wvu 2

18

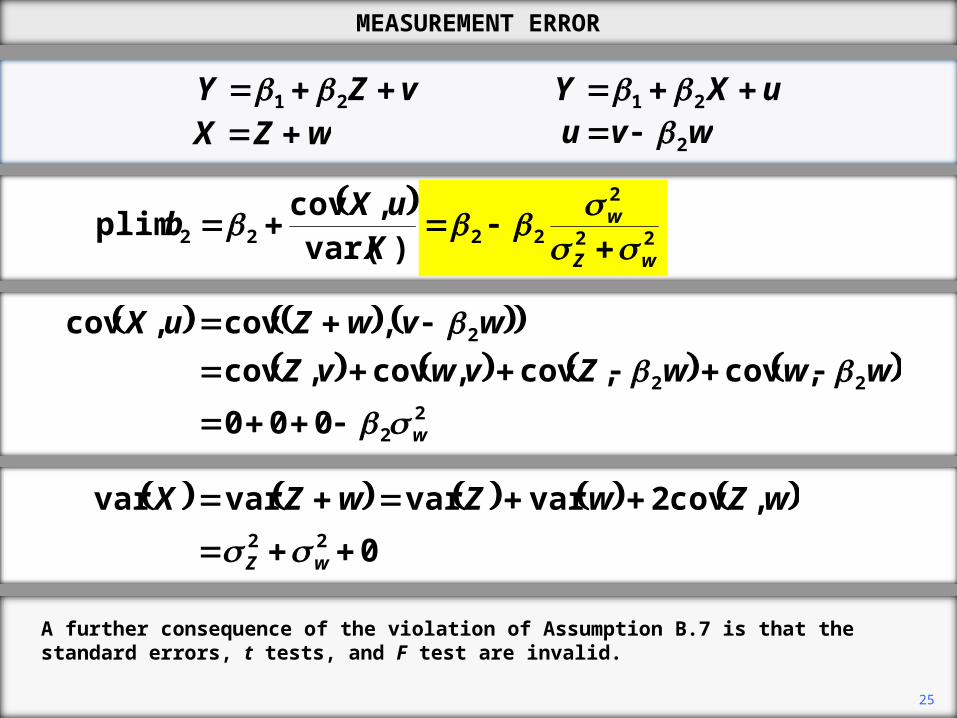

We can decompose both the numerator and the denominator of the error term. We will start by substituting for X and u in the numerator.

MEASUREMENT ERROR

22

2

2222 )var(,cov

plimwZ

w

XuX

b

22

22

2

000

,cov,cov,cov,cov

,cov,cov

w

wwwZvwvZ

wvwZuX

vZY 21 wZX

uXY 21 wvu 2

19

We expand the expression using the first covariance rule.

MEASUREMENT ERROR

20

If we assume that Z, v, and w are distributed indepndently of each other, the first 3 terms are 0. The last term gives us –2w

2.

MEASUREMENT ERROR

22

2

2222 )var(,cov

plimwZ

w

XuX

b

22

22

2

000

,cov,cov,cov,cov

,cov,cov

w

wwwZvwvZ

wvwZuX

vZY 21 wZX

uXY 21 wvu 2

22

2

2222 )var(,cov

plimwZ

w

XuX

b

22

22

2

000

,cov,cov,cov,cov

,cov,cov

w

wwwZvwvZ

wvwZuX

0

,cov2varvarvarvar22

wZ

wZwZwZX

vZY 21 wZX

uXY 21 wvu 2

21

We next expand the denominator of the error term. The first two terms are variances. The covariance is 0 if we assume w is distributed independently of Z.

MEASUREMENT ERROR

22

Thus in large samples, b2 is biased towards 0 and the size of the bias depends on the relative sizes of the variances of w and Z.

MEASUREMENT ERROR

22

2

2222 )var(,cov

plimwZ

w

XuX

b

22

22

2

000

,cov,cov,cov,cov

,cov,cov

w

wwwZvwvZ

wvwZuX

0

,cov2varvarvarvar22

wZ

wZwZwZX

vZY 21 wZX

uXY 21 wvu 2

23

Since b2 is an inconsistent estimator, it is safe to assume that it is biased in finite samples as well.

MEASUREMENT ERROR

22

2

2222 )var(,cov

plimwZ

w

XuX

b

22

22

2

000

,cov,cov,cov,cov

,cov,cov

w

wwwZvwvZ

wvwZuX

0

,cov2varvarvarvar22

wZ

wZwZwZX

vZY 21 wZX

uXY 21 wvu 2

24

If our assumptions concerning Z, v, and w are incorrect, b2 would almost certainly still be an inconsistent estimator, but the expression for the large-sample bias would be more complicated.

MEASUREMENT ERROR

22

2

2222 )var(,cov

plimwZ

w

XuX

b

22

22

2

000

,cov,cov,cov,cov

,cov,cov

w

wwwZvwvZ

wvwZuX

0

,cov2varvarvarvar22

wZ

wZwZwZX

vZY 21 wZX

uXY 21 wvu 2

25

A further consequence of the violation of Assumption B.7 is that the standard errors, t tests, and F test are invalid.

MEASUREMENT ERROR

22

2

2222 )var(,cov

plimwZ

w

XuX

b

22

22

2

000

,cov,cov,cov,cov

,cov,cov

w

wwwZvwvZ

wvwZuX

0

,cov2varvarvarvar22

wZ

wZwZwZX

vZY 21 wZX

uXY 21 wvu 2

26

The analysis will be illustrated with a simulation. The true model is Y = 2.0 + 0.8Z + u,with the values of Z drawn randomly from a normal distribution with mean 10 and variance 4, and the values of u being drawn from a normal distribution with mean 0 and variance 4.

MEASUREMENT ERROR

Simulation

uZY 8.00.2 4,10~ NZ 4,0~ Nu

22

2

2222 )var(,cov

plimwZ

w

XuX

b

vZY 21 wZX

uXY 21 wvu 2

27

X = Z + w, where w is drawn from a normal distribution with mean 0 and variance 1. With this information, we are able to determine plim b2.

MEASUREMENT ERROR

Simulation

uZY 8.00.2 4,10~ NZ 4,0~ Nu

64.014

18.08.0 plim 22

2

222

wZ

wb

wZX 1,0~ Nw

22

2

2222 )var(,cov

plimwZ

w

XuX

b

vZY 21 wZX

uXY 21 wvu 2

28

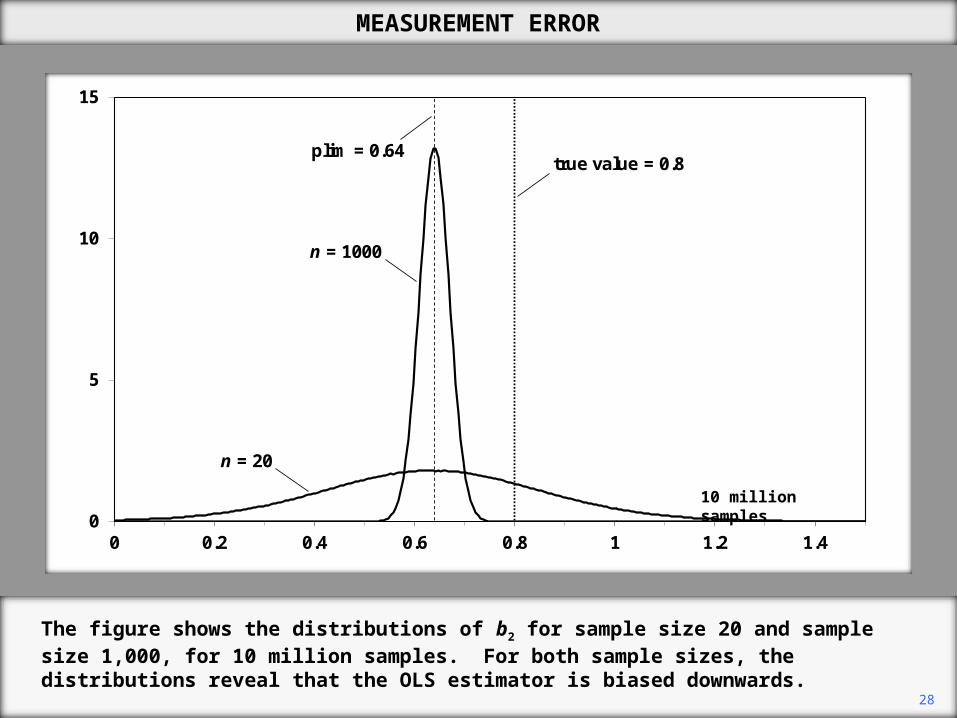

The figure shows the distributions of b2 for sample size 20 and sample size 1,000, for 10 million samples. For both sample sizes, the distributions reveal that the OLS estimator is biased downwards.

MEASUREMENT ERROR

0

5

10

15

0 0.2 0.4 0.6 0.8 1 1.2 1.4

true value = 0.8plim = 0.64

n = 1000

n = 20

10 million samples

29

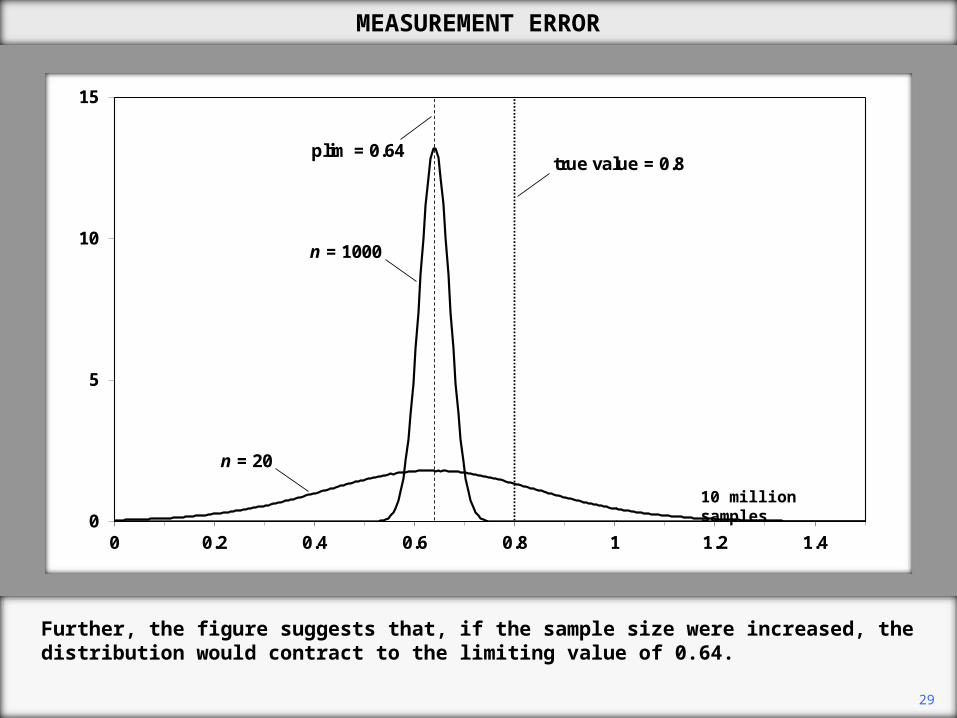

Further, the figure suggests that, if the sample size were increased, the distribution would contract to the limiting value of 0.64.

MEASUREMENT ERROR

0

5

10

15

0 0.2 0.4 0.6 0.8 1 1.2 1.4

true value = 0.8plim = 0.64

n = 1000

n = 20

10 million samples

30

There remains the question of whether the limiting value provides guidance to the mean of the distribution for a finite sample. In general, the mean will be different from the limiting value, but will approach it as the sample size increase.

MEASUREMENT ERROR

0

5

10

15

0 0.2 0.4 0.6 0.8 1 1.2 1.4

true value = 0.8plim = 0.64

n = 1000

n = 20

10 million samples

31

In the present case, however, the mean of the sample is almost exactly equal to 0.64, even for sample size 20.

MEASUREMENT ERROR

0

5

10

15

0 0.2 0.4 0.6 0.8 1 1.2 1.4

true value = 0.8plim = 0.64

n = 1000

n = 20

10 million samples

32

Measurement error in the dependent variable has less serious consequences. Suppose that the true dependent variable is Q, that the measured variable is Y, and that the measurement error is r.

MEASUREMENT ERROR

rQY vXQ 21

33

We can rewrite the model in terms of the observable variables by substituting for Q from the second equation.

MEASUREMENT ERROR

vXrY 21

rQY vXQ 21

34

In this case the presence of the measurement error does not lead to a violation of Assumption B.7. If v satisfies that assumption in the original model, u will satisfy it in the revised one, unless for some strange reason r is not distributed independently of X.

MEASUREMENT ERROR

uX

rvXY

21

21

vXrY 21

rvu

rQY vXQ 21

35

uX

rvXY

21

21

The standard errors and tests will remain valid. However the standard errors will tend to be larger than they would have been if there had been no measurement error, reflecting the fact that the variances of the coefficients are larger.

vXrY 21

2

22

2

22

2

X

rv

X

ub nn

rvu

MEASUREMENT ERROR

rQY vXQ 21

2012.11.12

Copyright Christopher Dougherty 2012.

These slideshows may be downloaded by anyone, anywhere for personal use.

Subject to respect for copyright and, where appropriate, attribution, they may be

used as a resource for teaching an econometrics course. There is no need to

refer to the author.

The content of this slideshow comes from Section 8.4 of C. Dougherty,

Introduction to Econometrics, fourth edition 2011, Oxford University Press.

Additional (free) resources for both students and instructors may be

downloaded from the OUP Online Resource Centre

http://www.oup.com/uk/orc/bin/9780199567089/.

Individuals studying econometrics on their own who feel that they might benefit

from participation in a formal course should consider the London School of

Economics summer school course

EC212 Introduction to Econometrics

http://www2.lse.ac.uk/study/summerSchools/summerSchool/Home.aspx

or the University of London International Programmes distance learning course

EC2020 Elements of Econometrics

www.londoninternational.ac.uk/lse.