mdec’s perspective on creative multimedia – the next ... · mdec’s perspective on creative...

TRANSCRIPT

1

MDEC’S PERSPECTIVE ON CREATIVE

MULTIMEDIA – THE NEXT BOOMING

INDUSTRY

Kamil Othman

Vice President, Creative Multimedia Division

Multimedia Development Corporation

6 May 2014

Penang Creative Industry Conference & Showcase (PCICS), 2014

Equatorial Hotel, Penang

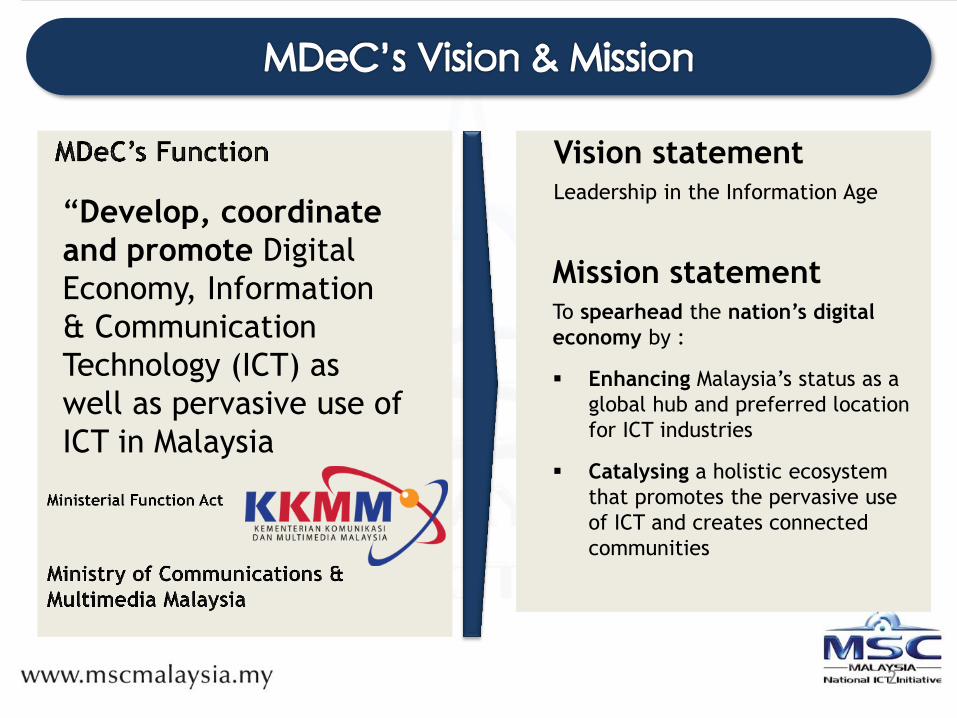

“Develop, coordinate

and promote Digital

Economy, Information

& Communication

Technology (ICT) as

well as pervasive use of

ICT in Malaysia

2

Mission statement To spearhead the nation’s digital

economy by :

Enhancing Malaysia’s status as a

global hub and preferred location

for ICT industries

Catalysing a holistic ecosystem

that promotes the pervasive use

of ICT and creates connected

communities

Vision statement Leadership in the Information Age

1,764 companies 309 companies 241 companies

4

Entertainment Medical

Tourism

Animation & VFX

Games and Digital Comics

Mobile Content and

Apps

E-Publishing &

Interactive Media

INDUSTRY CREATES PRODUCTS AND SERVICES

TECHNOLOGY ENABLES INNOVATION AND PRODUCTION OF CONTENT

Development Pre-

Production Production Post-

Production

Marketing , Distribution & Licensing

Light Stage Technology

2D / 3D/CGI 3D Stereoscopic

Motion Graphics Motion Capture Cloud Rendering

Serious Games Digital

Compression

Religion and Cultural

Design & Architecture

Education/Training

Defence

Govt Services

Oil & Gas

Construction

Virtual & Augmented

Reality

Film & TV Content

Cross-industry applications

5

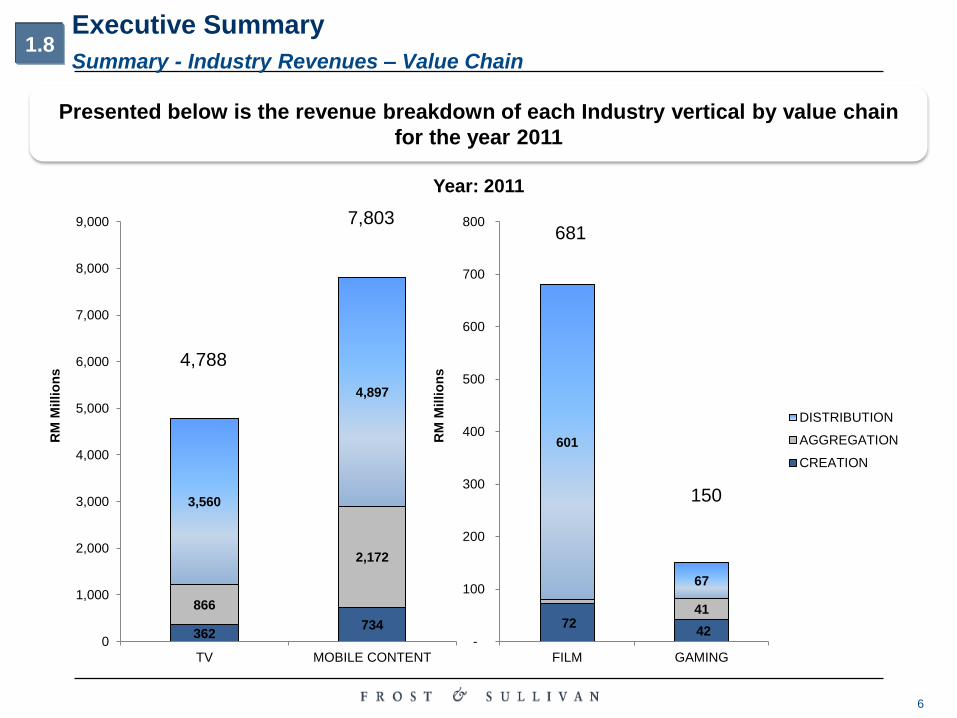

Presented below is the Revenue of total Creative Multimedia industry revenue for

2011 and Forecast for Year 2017

Summary - Industry Revenues

Executive Summary

Creative Multimedia Industry Revenues

1.8

Overall Industry Size:

RM 13.422 Billion

In 2011

Overall Industry Size:

RM 23.847 Billion

In 2017

CAGR: +10.05%

RM

Millio

n

681

150

1,714

280

-

500

1,000

1,500

2,000

2,500

3,000

FILM TV GAMING MOBILE CONTENT

6- Yr CAGR:

+11%

6- Yr CAGR:

+17%

4,788 7,803 8,030

13,823

-

5,000

10,000

15,000

2011 2017 6- Yr CAGR:

+10% 6- Yr CAGR:

+9%

6

Presented below is the revenue breakdown of each Industry vertical by value chain

for the year 2011

Summary - Industry Revenues – Value Chain

Executive Summary

72 42

41

601

67

-

100

200

300

400

500

600

700

800

FILM GAMING

RM

Millio

ns

DISTRIBUTION

AGGREGATION

CREATION

362 734

866

2,172

3,560

4,897

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

TV MOBILE CONTENT

RM

Millio

ns

Year: 2011

1.8

4,788

7,803 681

150

7

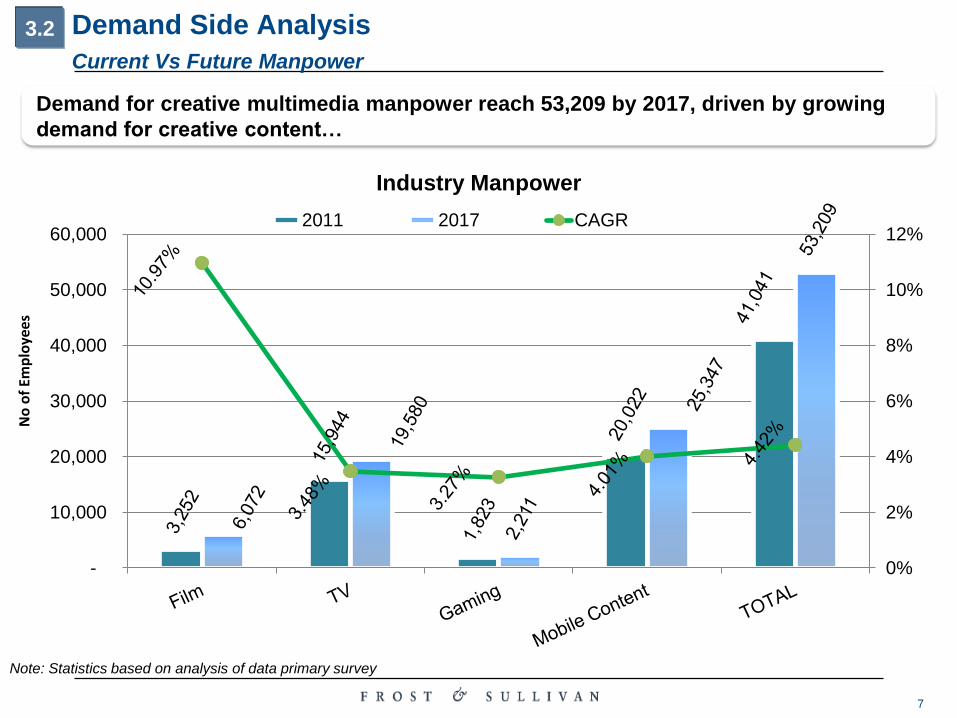

Demand Side Analysis

Current Vs Future Manpower

Demand for creative multimedia manpower reach 53,209 by 2017, driven by growing

demand for creative content…

0%

2%

4%

6%

8%

10%

12%

-

10,000

20,000

30,000

40,000

50,000

60,000

Industry Manpower

2011 2017 CAGR

No

of

Emp

loye

es

3.2

Note: Statistics based on analysis of data primary survey

8

Demand Side Analysis

Current Vs Future Manpower

Mobile content, film and TV sectors have high revenue to employee ratios due to

greater levels of automation 2

09

,31

7

30

0,2

98

82

,12

5

38

9,7

21

28

2,3

04

410,1

13

12

6,6

45

54

5,3

59

Film TV Gaming Mobile Content

Productivity

2011 2017

Note:

Efficiency measured based on revenue per employee ratio

3.2

Note: Statistics based on analysis of data primary survey

In the future, improvements in efficiency is to be driven by

a. Technological advancements, b. Skillset enhancements, c. Greater ease of distribution

Mobile content has the highest Productivity because distribution through Mobile operators is the most automated amongst the 4

Industry Verticals

Development of the Creative

Industry In MSC Malaysia

1- Policies & Legislation

2 - Funding & Incentives

3- Market Access, Distribution & Delivery

8-Enterprise Development

7-Infrastructure

5-Talent & Skills Development

9-Generate, Amass & Monetize

IP Inventory

4- IP Protection

9

6-R&D and Technology

STRENGTHEN THE INDUSTRY’S BUILDING BLOCKS

OUR SUPPORT TO INDUSTRY….

10

FACILITIES & PROGRAMMES

52 companies

Games

and

Digital

Comics

104 companies

Animation

54 companies

Mobile

Content,

Apps and

New Media

99 companies

Film, TV

and VFX

Codemasters (UK)

Games

Mobile

Smilegate (KOR) Polygon Pictures

(JPN)

Digital Frontier (JPN) Bloomberg (USA) Al Jazeera (QAT)

Animation

Animation

TV

Games

TV

Terato Tech

Games

Mobile

Lemon Sky Silver Ant

Animonsta KRU Studios MIG

Animation

Animation

Visual Effects

Games

Film

Just Mobile

Terato Tech

Rhythm & Hues

MOL Global

CiB Development

Codemasters

Kingsoft

Pinewood Studio

Kreatevee

Saladin

KRU Studios

MIG

War of the

Worlds: Goliath

BoboiBoy

Cingkus Blues

Upin & Ipin

Seefood

ddung

International Presence Animation

Games Mobile VFX

IP Creator Challenge Series

Competency & Mentorship

Programmes

Public Awareness &

Enculturation

Digital Story Telling

TBS DigiCon6

Creative Industry Lifelong

Learning (CILL)

The MSC Malaysia Creative Content Centre (MaC3) was established in June 2009 to:

1. Provide facilities and access to technology

and resources for content entrepreneurs

2. Develop talent through training and mentoring

3. Launch Malaysia as a leading provider of creative digital content

Content Accelerators

Technology Training Lab

Games Test Centre

Rendering Facilities Audio and Post Production

MAC3 is the nucleus in the

development of the creative

digital content industry in

Malaysia. It is to help and

inspire artists, scientists and

the general public in the

opportunities in content

creation and

commercialization ”

“

BoboiBoy

Mask Master

Vektor 58

Jellyfish Eyes

Some Productions

Rendered @MaC3

• The MaC3 Fund (formerly known as MaC3 Co-Pro Fund) was

launched in 2009 to fund innovative local companies develop,

produce and co-produce creative multimedia content

• Funds offered are: Development Fund, Production Fund and

Co-Production Fund

• Offered to Malaysian incorporated companies with majority

Malaysian shareholding

• Areas: Animation, Game, Digital Film with VFX components,

Beyond Entertainment), High-end Technology Deployment

and Digital Music

To date, RM 58 million has been awarded.

RM 30 million on offer in 2013.

MaC3 Fund Development | Production | Co-Production

Buzzy Bee

BBoing

Chuck

Chicken

Some MaC3 Fund Recipients

North America

South America

Africa

UK

France

Rome Qatar

Indonesia

Australia

Korea

Japan

Thailand

Singapore

India

Hong Kong

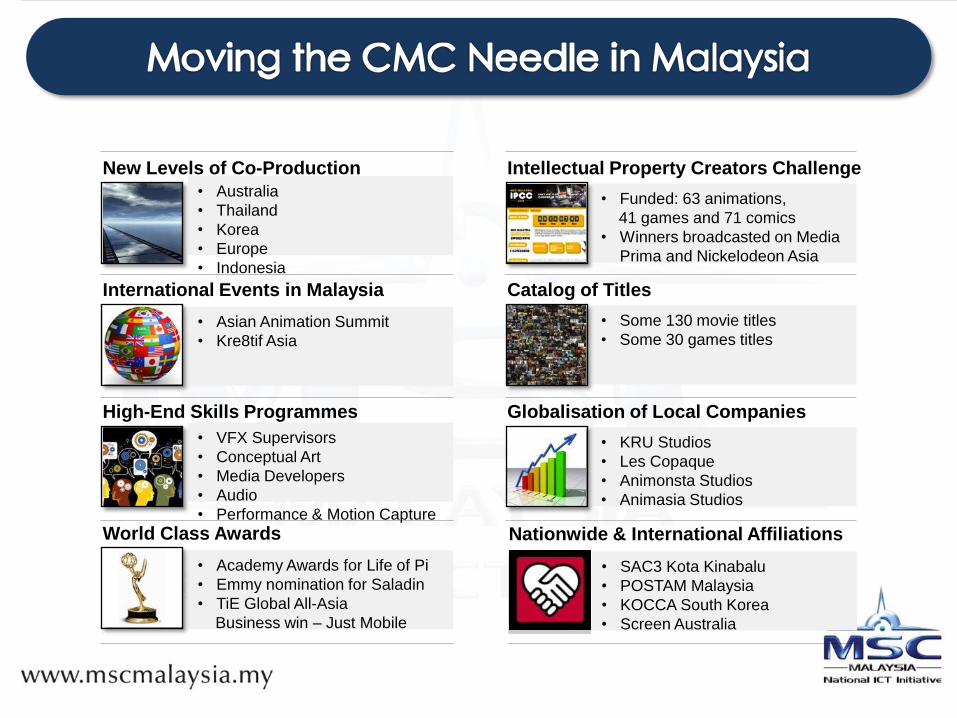

New Levels of Co-Production

• Australia

• Thailand

• Korea

• Europe

• Indonesia

International Events in Malaysia

• Asian Animation Summit

• Kre8tif Asia

High-End Skills Programmes

• VFX Supervisors

• Conceptual Art

• Media Developers

• Audio

• Performance & Motion Capture

World Class Awards

• Academy Awards for Life of Pi

• Emmy nomination for Saladin

• TiE Global All-Asia

Business win – Just Mobile

Intellectual Property Creators Challenge

• Funded: 63 animations,

41 games and 71 comics

• Winners broadcasted on Media

Prima and Nickelodeon Asia

Catalog of Titles

• Some 130 movie titles

• Some 30 games titles

Globalisation of Local Companies

• KRU Studios

• Les Copaque

• Animonsta Studios

• Animasia Studios

Nationwide & International Affiliations

• SAC3 Kota Kinabalu

• POSTAM Malaysia

• KOCCA South Korea

• Screen Australia

National Creative Industry

Policy

(NCIP/ DIKN)

National Key Economic Area

Communication, Content &

Infrastructure (NKEA/CCI)

1. Aims to enhance capacity

and capability: To create

original locally produced

content and at the same

time develop a

competency to provide

content related services to

the regional market.

2. Target in year 2020:

Incremental GNI impact –

RM35.7 billion with

additional 43,163 jobs.

1. To spur creative activities

in the country as an

economic generator

2. To promote the

development of the three

major sectors which are

the Creative Multimedia,

Arts & Culture and Cultural

Heritage

IP Funding

1.

Market

Access 2.

Strategic

Alliances 3.

Skills

Developmen

t Digital

Media

Zones

5.

4.

MSC Malaysia Bill of

Guarantees

Film In Malaysia Incentive

(FIMI)

1. 30% cash rebate on all

Qualifying Malaysian

Production Expenditure

(QMPE)

2. Applicable to Production

and/or Post Production

activities

3. For TV series and films,

both live action and

animated

1. Zero corporate income tax

for up to 10 years

2. Investment Tax Allowance

for up to 5 years

3. No restriction on foreign

ownership of the company

4. No restriction on hiring of

foreign knowledge workers

Future Focus For Malaysia’s Creative Content Industry

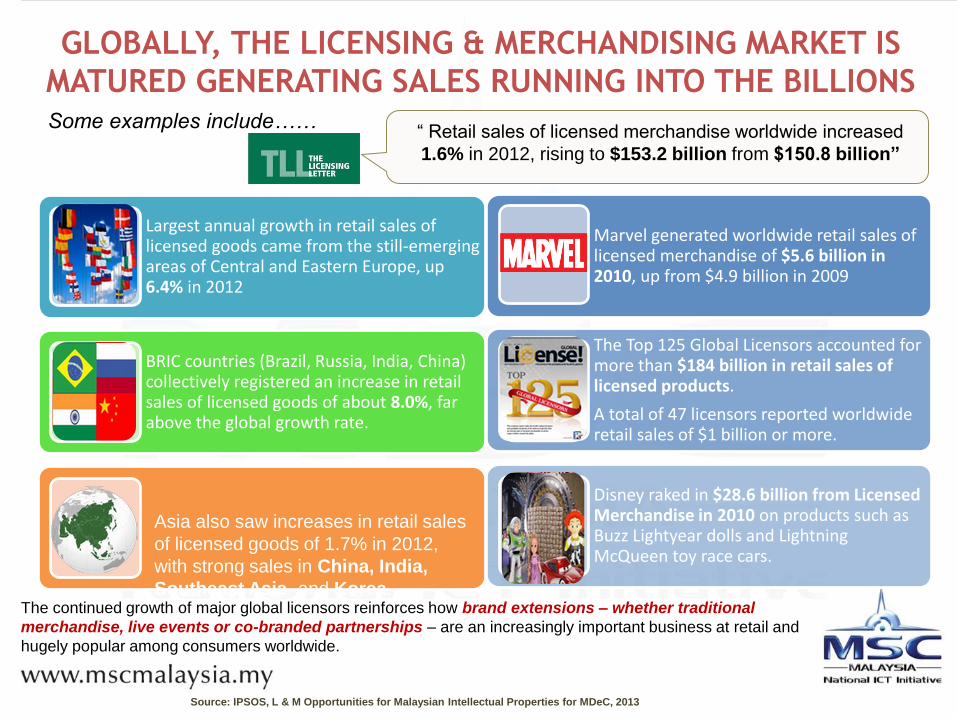

GLOBALLY, THE LICENSING & MERCHANDISING MARKET IS

MATURED GENERATING SALES RUNNING INTO THE BILLIONS Some examples include……

Largest annual growth in retail sales of licensed goods came from the still-emerging areas of Central and Eastern Europe, up 6.4% in 2012

BRIC countries (Brazil, Russia, India, China) collectively registered an increase in retail sales of licensed goods of about 8.0%, far above the global growth rate.

Marvel generated worldwide retail sales of licensed merchandise of $5.6 billion in 2010, up from $4.9 billion in 2009

The Top 125 Global Licensors accounted for more than $184 billion in retail sales of licensed products.

A total of 47 licensors reported worldwide retail sales of $1 billion or more.

Disney raked in $28.6 billion from Licensed Merchandise in 2010 on products such as Buzz Lightyear dolls and Lightning McQueen toy race cars.

The continued growth of major global licensors reinforces how brand extensions – whether traditional

merchandise, live events or co-branded partnerships – are an increasingly important business at retail and

hugely popular among consumers worldwide.

Asia also saw increases in retail sales

of licensed goods of 1.7% in 2012,

with strong sales in China, India,

Southeast Asia, and Korea.

“ Retail sales of licensed merchandise worldwide increased

1.6% in 2012, rising to $153.2 billion from $150.8 billion”

Source: IPSOS, L & M Opportunities for Malaysian Intellectual Properties for MDeC, 2013

• The traditional value chain :

L&M TRENDS: REINVENTION

Dooodolls was

produced as

characters and

merchandised.

Now moving into

the content space

of producing

digital games

Focus on characters and merchandising

these character without a content format

Marketing content for free to establish market

base for L&M

Thomas & Friends markets its

content for free to media

platforms to create a

substantial market base. Main

revenue generation from

L&M.

Reversing the value chain,

producing merchandises prior to the

release of content

Ironman 3 merchandises

were available in retail

stores even before the

movie premiered

Produce IP

Market on traditional platform:

broadcasting, publishing etc

Merchandising

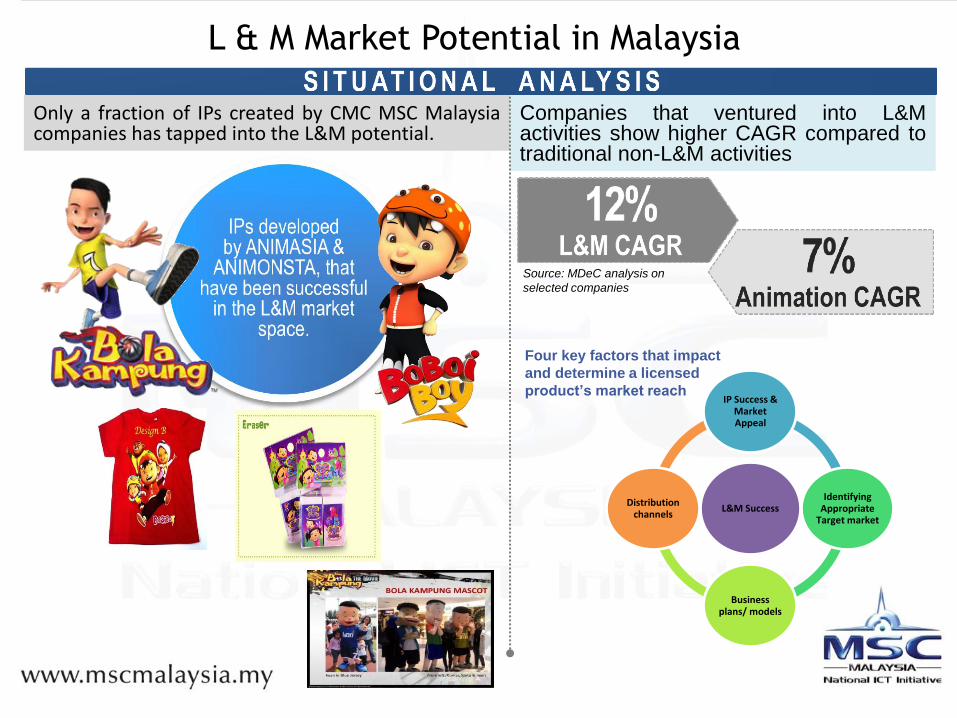

Only a fraction of IPs created by CMC MSC Malaysia companies has tapped into the L&M potential.

L & M Market Potential in Malaysia

Companies that ventured into L&M activities show higher CAGR compared to traditional non-L&M activities

L&M Success

IP Success & Market Appeal

Identifying Appropriate

Target market

Business plans/ models

Distribution channels

Four key factors that impact

and determine a licensed

product’s market reach

Source: MDeC analysis on

selected companies

Gaming industry in Malaysia is in its infancy, RM31 mil was generated from own IPs;

which constitutes to about 20% of overall gaming revenues

IP Statistics

2.3 Gaming

150

31

-

20

40

60

80

100

120

140

160

TotalRevenues

Revenuesfrom Own

IP

RM

Mil

lio

n

Revenues

22.44%

13.41%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Cost of First IP/Revenue

Cost ofSubsequent IP/

Revenue

Cost of IPs/Revenue Year: 2011

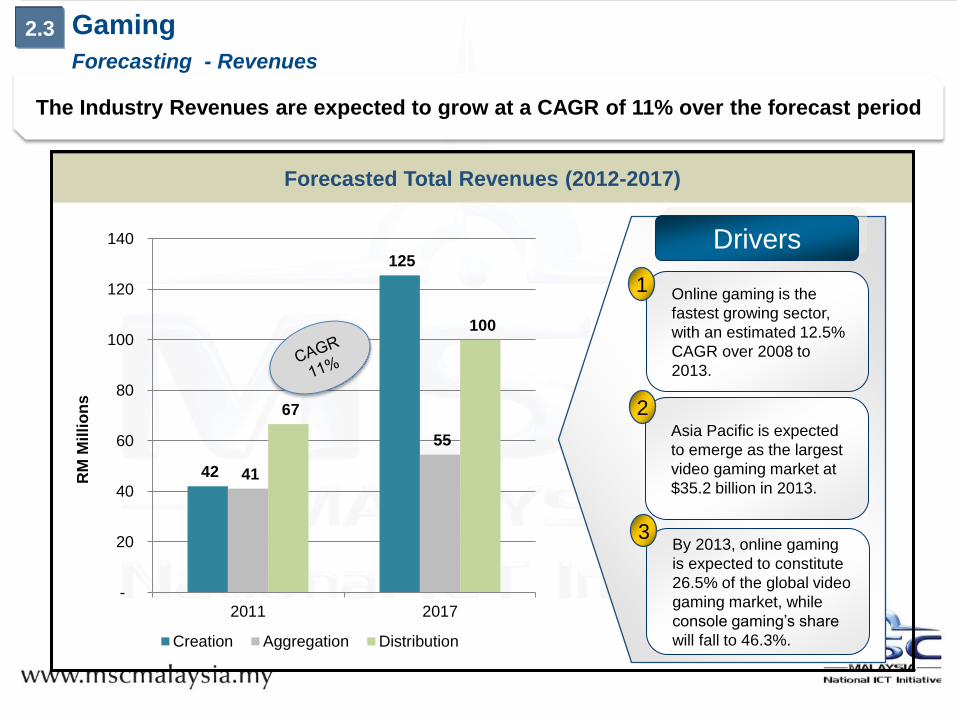

Forecasted Total Revenues (2012-2017)

The Industry Revenues are expected to grow at a CAGR of 11% over the forecast period

By 2013, online gaming

is expected to constitute

26.5% of the global video

gaming market, while

console gaming’s share

will fall to 46.3%.

3

Drivers

Asia Pacific is expected

to emerge as the largest

video gaming market at

$35.2 billion in 2013.

2

Online gaming is the

fastest growing sector,

with an estimated 12.5%

CAGR over 2008 to

2013.

1

Forecasting - Revenues

2.3 Gaming

42

125

41

55

67

100

-

20

40

60

80

100

120

140

2011 2017

RM

Milli

on

s

Creation Aggregation Distribution

Sources: Factiva, ISI Emerging Markets,

Business Insights

Asia Pacific is expected to emerge as the

largest video gaming market at $35.2

billion in 2013.

3

Trends and

Developments

Online gaming is the fastest growing

sector, with an estimated 12.5% CAGR

over 2008 to 2013.

2

Console gaming remains the largest

segment of the regional video gaming

market, with a market value of $40.7

billion.

1

2.3 Gaming

Regional Trends

A regional perspective of the Gaming industry.

Forecasted Total Revenues (2012-2017)

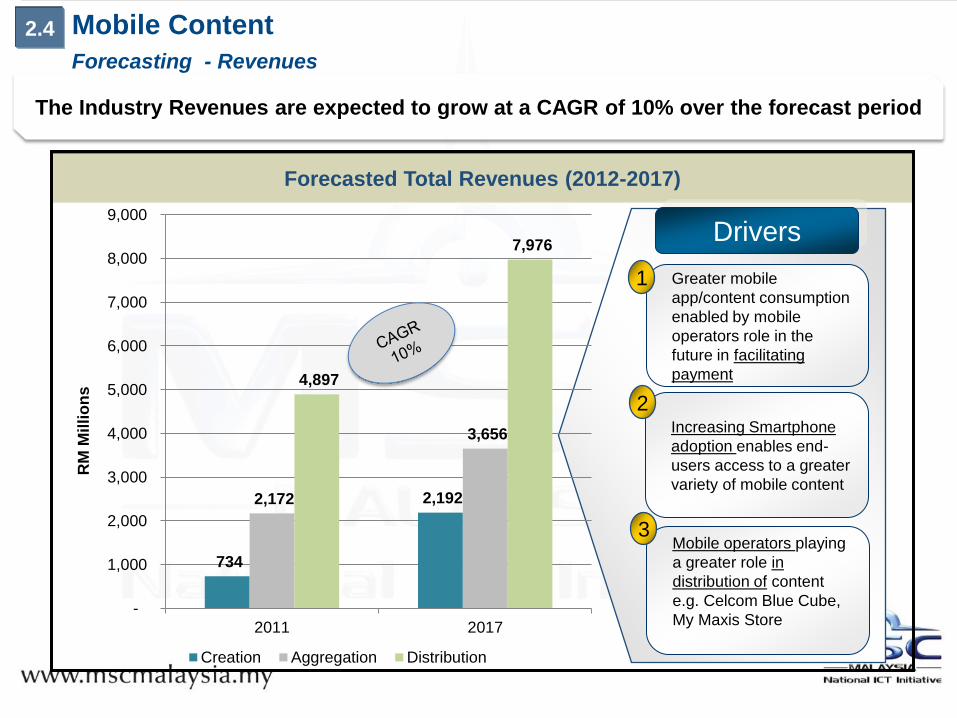

The Industry Revenues are expected to grow at a CAGR of 10% over the forecast period

Mobile operators playing

a greater role in

distribution of content

e.g. Celcom Blue Cube,

My Maxis Store

3

Drivers

Increasing Smartphone

adoption enables end-

users access to a greater

variety of mobile content

2

Greater mobile

app/content consumption

enabled by mobile

operators role in the

future in facilitating

payment

1

Forecasting - Revenues

Mobile Content 2.4

734

2,192 2,172

3,656

4,897

7,976

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2011 2017

RM

Milli

on

s

Creation Aggregation Distribution

Forecasted Total Manpower (2012-2017)

Forecasting - Manpower

2.4 Mobile Content

3,030

6,465

8,699

10,463

8,293 8,419

0

2000

4000

6000

8000

10000

12000

2011 2017

Creation Aggregation Distribution

Manpower will grow at rate of 4.01% and Revenue per employee will grow at rate of

5.76% between 2012 and 2017

Lower growth in

distribution manpower

driven by technology

efficiency and declining

role of mobile companies

in content distribution

3

Drivers

More aggregation

manpower to support the

growing content

consumption (e.g. mobile

content portals e.g. Play

Store, BBC News App)

2

Greater content creation

activities due to

technology driven growth

in demand (e.g. smart

phones enable greater

content consumption)

1

MSC Malaysia ICON Program is a

collaboration between Nokia, MSC

Malaysia and Cradle Fund which aims

to provide support to the developer

community and encourage digital

content development in Malaysia.

1

Asia is the biggest market for

applications, accounting for 37% of

global downloads although North

American users spent the most money.

3

Trends and

Developments

Data revenue in Japan will reach $43.5

billion and monthly data average

revenue per user will be $27.1 in 2014,

with data revenue surpassing voice

revenue.

2

Regional Trends

A regional perspective of the Mobile Content Industry.

Mobile Content 2.4