mcgraw-hill/irwin ©2001 the mcgraw-hill companies all rights reserved 5.0 chapter 5 discounte d...

TRANSCRIPT

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.1

Chapter

5Discounted Cash Flow Valuation

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

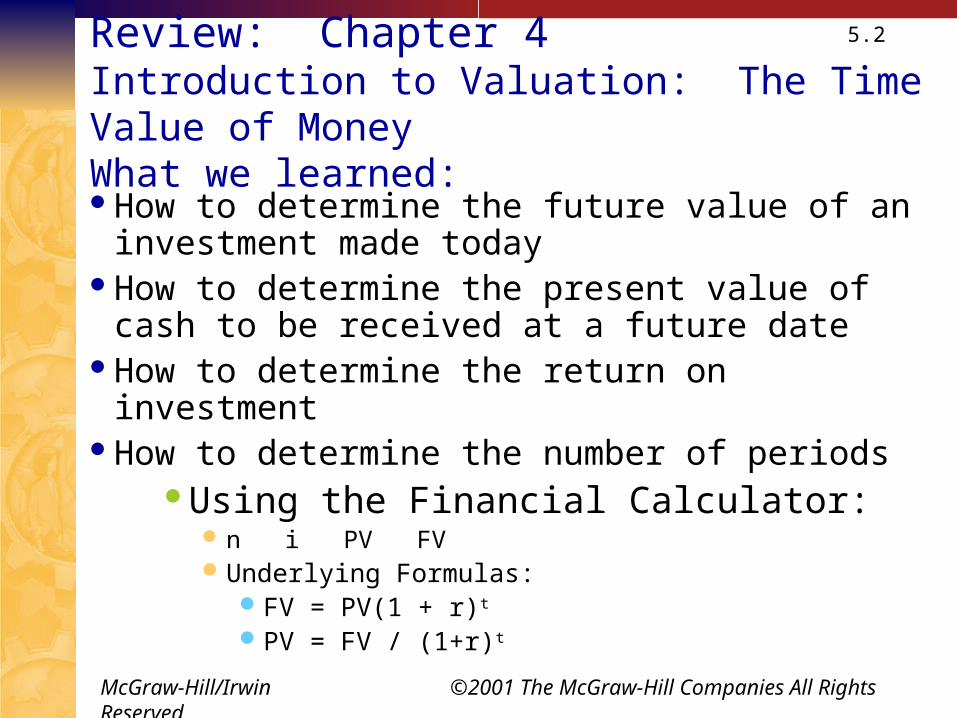

5.2Review: Chapter 4Introduction to Valuation: The Time Value of MoneyWhat we learned:How to determine the future value of an investment

made todayHow to determine the present value of cash to be

received at a future dateHow to determine the return on investmentHow to determine the number of periods

Using the Financial Calculator: n i PV FV Underlying Formulas:

FV = PV(1 + r)t

PV = FV / (1+r)t

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.3

Chapter 5 (Part 1) Outline

Future and Present Values of Multiple Cash Flows

Valuing Level Cash Flows: Annuities and Perpetuities

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.4

Note on Cash Flow Timing Pg 117

In almost all cash flow timing problems, it is implicitly assumed that the cash flows occur at the “end” of each period. Unless you are very explicitly told otherwise, you

should always assume that this is what is meant.Default settings on a financial calculator or spread

sheet assume that cash flows occur at the end of each period.

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.5

5.1 Future Value and Present Valuewith “Multiple” Cash Flows

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.6

Future Value with Multiple Cash Flows

FV = PV(1 + r)t

General FV Time Line Example:

Figure 5.4, Page 112

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.7

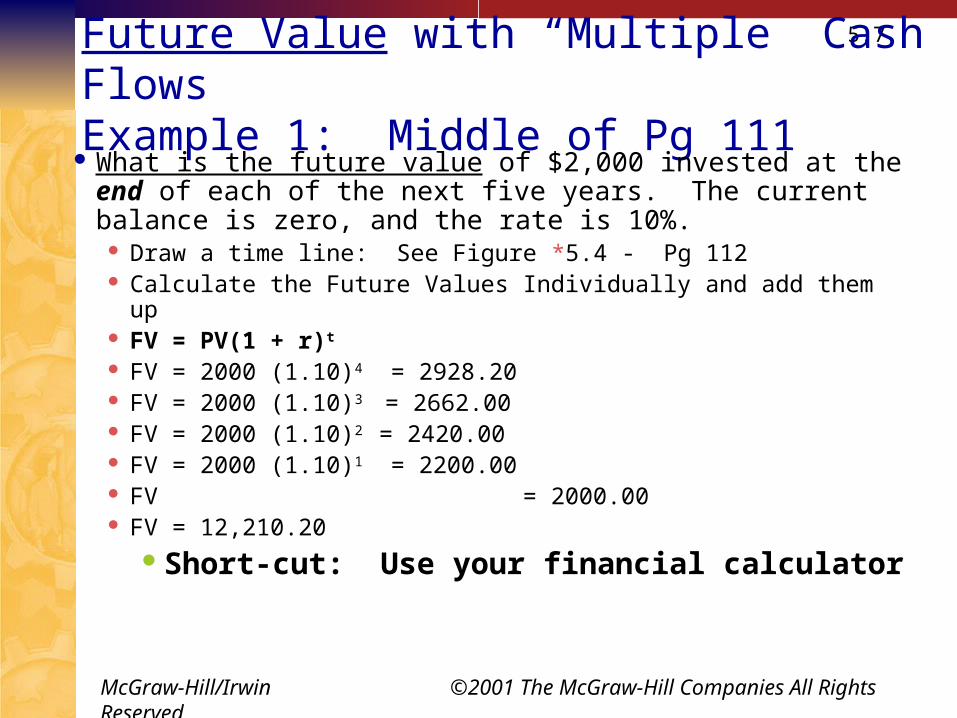

Future Value with “Multiple” Cash FlowsExample 1: Middle of Pg 111

What is the future value of $2,000 invested at the end of each of the next five years. The current balance is zero, and the rate is 10%.

Draw a time line: See Figure *5.4 - Pg 112 Calculate the Future Values Individually and add them up FV = PV(1 + r)t

FV = 2000 (1.10)4 = 2928.20 FV = 2000 (1.10)3 = 2662.00 FV = 2000 (1.10)2 = 2420.00 FV = 2000 (1.10)1 = 2200.00 FV = 2000.00 FV = 12,210.20

Short-cut: Use your financial calculator

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.8

Future Value with “Multiple” Cash Flows Example: 2

Suppose you invest $500 in a mutual fund today and $600 in one year. If the fund pays 9% annually, how much will you have in two years?

Draw a Time Line Calculate the Future Values Individually and add them up FV = PV(1 + r)t

FV = 500 (1.09)2 = 594.05 FV = 600 (1.09)1 = 654 FV = 1248.05

Short-cut: Use your financial calculator

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.9

Future Value with “Multiple” Cash Flows Example: 2 Continued

How much will you have in 5 years if you make no further deposits?

Extend the previous Time LineAnswer: 1616.26

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.10

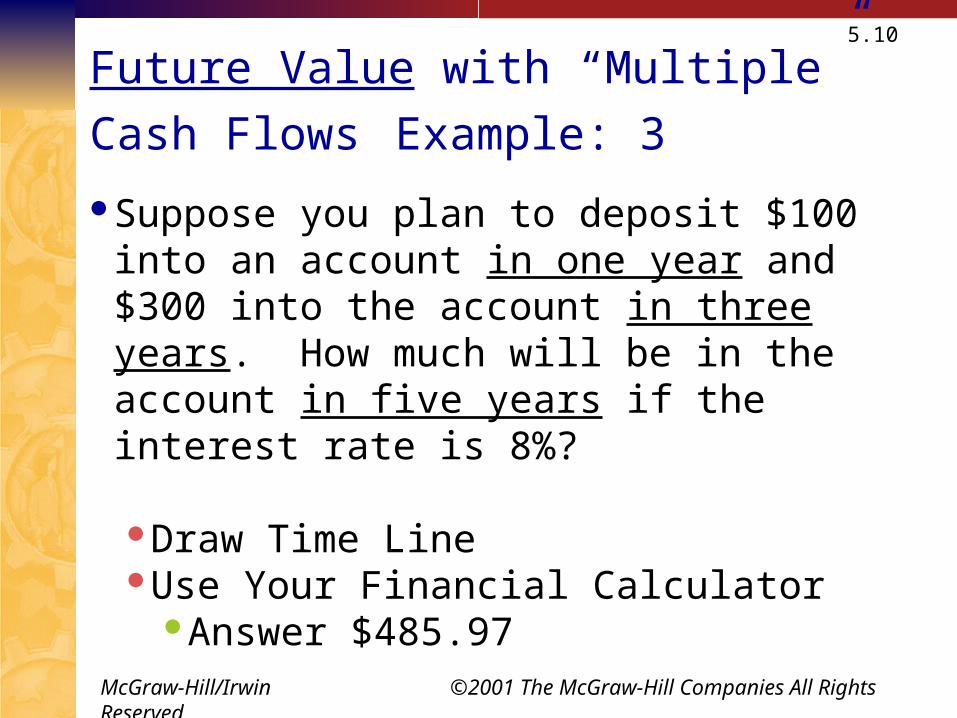

Future Value with “Multiple” Cash Flows Example: 3

Suppose you plan to deposit $100 into an account in one year and $300 into the account in three years. How much will be in the account in five years if the interest rate is 8%?

Draw Time LineUse Your Financial Calculator

Answer $485.97

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.11

Present Value with Multiple Cash Flows

PV = FV / (1+r)t

General PV Time Line Example:

Figure 5.5, Page 114

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

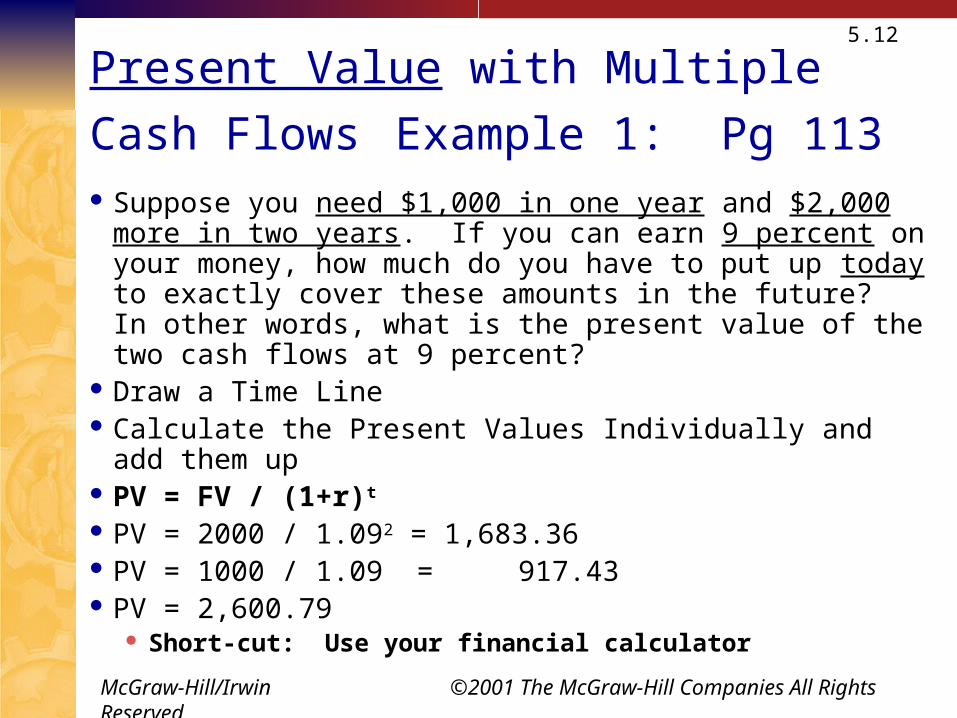

5.12

Present Value with Multiple Cash Flows Example 1: Pg 113 Suppose you need $1,000 in one year and $2,000 more in two

years. If you can earn 9 percent on your money, how much do you have to put up today to exactly cover these amounts in the future? In other words, what is the present value of the two cash flows at 9 percent?

Draw a Time Line Calculate the Present Values Individually and add them up PV = FV / (1+r)t

PV = 2000 / 1.092 = 1,683.36 PV = 1000 / 1.09 = 917.43 PV = 2,600.79

Short-cut: Use your financial calculator

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

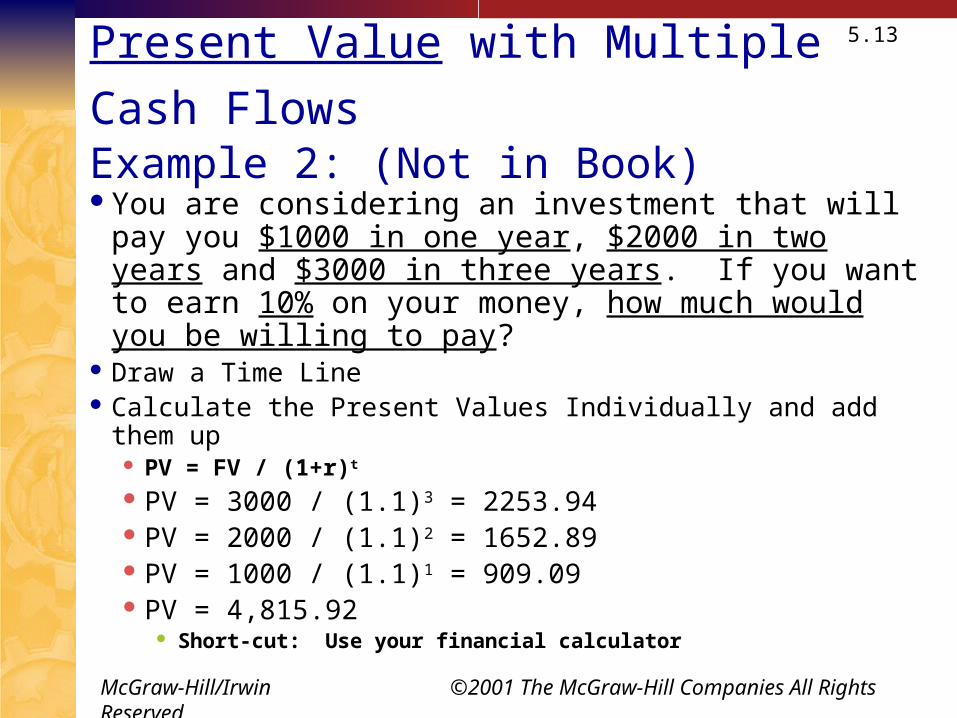

5.13

Present Value with Multiple Cash Flows Example 2: (Not in Book)

You are considering an investment that will pay you $1000 in one year, $2000 in two years and $3000 in three years. If you want to earn 10% on your money, how much would you be willing to pay?

Draw a Time Line Calculate the Present Values Individually and add them up

PV = FV / (1+r)t

PV = 3000 / (1.1)3 = 2253.94 PV = 2000 / (1.1)2 = 1652.89 PV = 1000 / (1.1)1 = 909.09 PV = 4,815.92

Short-cut: Use your financial calculator

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

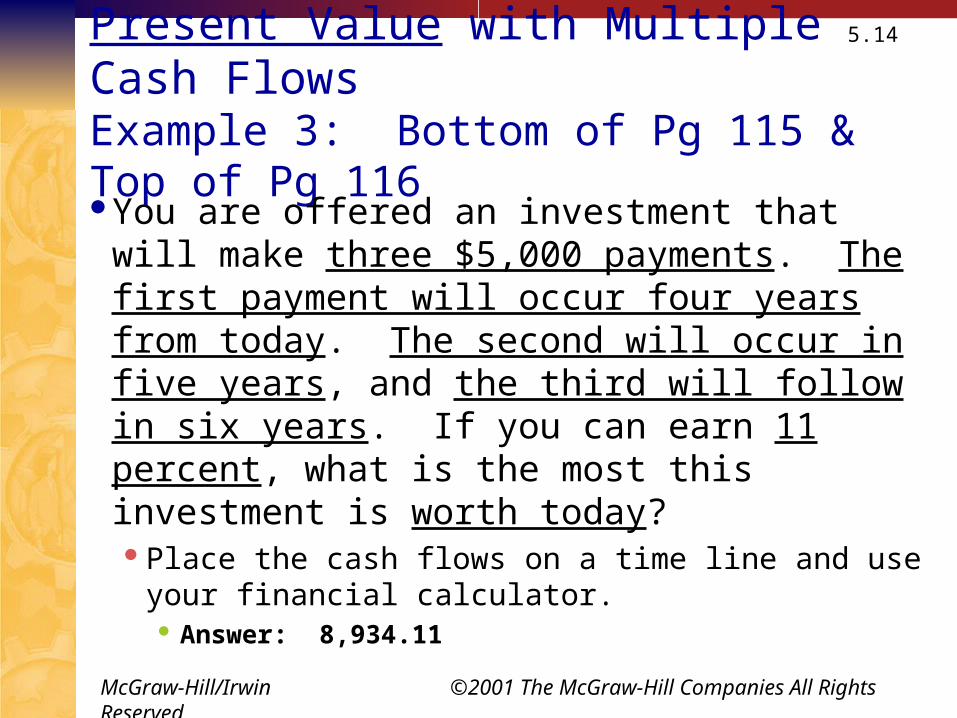

5.14

Present Value with Multiple Cash FlowsExample 3: Bottom of Pg 115 & Top of Pg 116

You are offered an investment that will make three $5,000 payments. The first payment will occur four years from today. The second will occur in five years, and the third will follow in six years. If you can earn 11 percent, what is the most this investment is worth today? Place the cash flows on a time line and use your

financial calculator. Answer: 8,934.11

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.15

5.2 Valuing Level Cash Flows:Annuities and Perpetuities

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.16

Valuing Level Cash Flows: Annuities and Perpetuities

Annuity –a level stream of cash flows (a series of equal payments) for a fixed period of timeHome MortgagesCar LoansStudent Loans

“Ordinary” Annuity – a series of equal payments for a fixed period of time that occur at the end of each period.

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

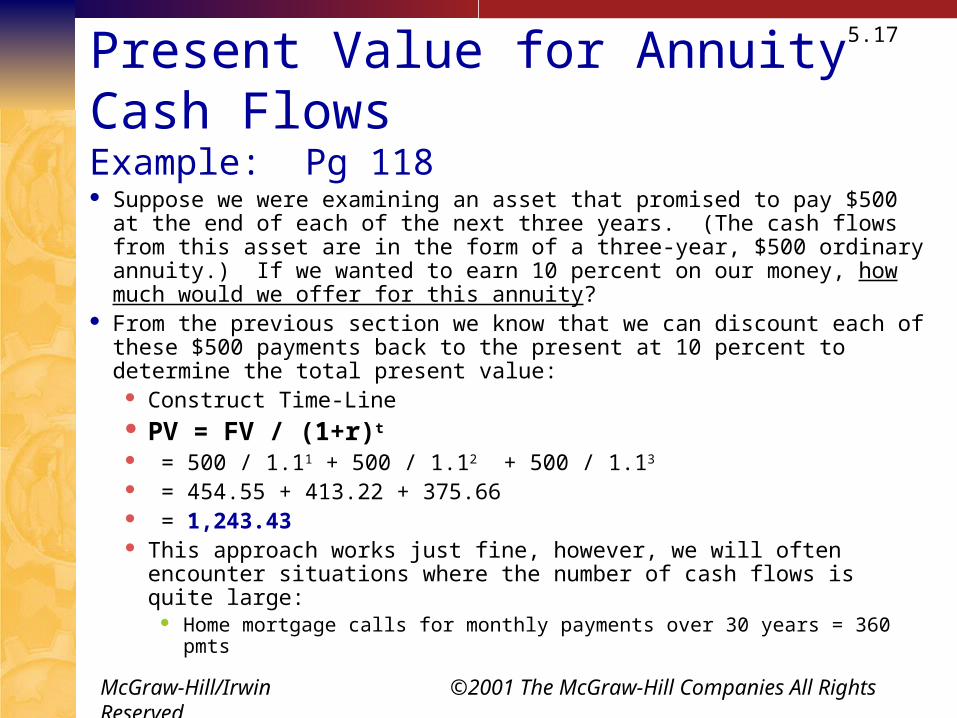

5.17

Present Value for Annuity Cash FlowsExample: Pg 118

Suppose we were examining an asset that promised to pay $500 at the end of each of the next three years. (The cash flows from this asset are in the form of a three-year, $500 ordinary annuity.) If we wanted to earn 10 percent on our money, how much would we offer for this annuity?

From the previous section we know that we can discount each of these $500 payments back to the present at 10 percent to determine the total present value:

Construct Time-Line PV = FV / (1+r)t

= 500 / 1.11 + 500 / 1.12 + 500 / 1.13

= 454.55 + 413.22 + 375.66 = 1,243.43 This approach works just fine, however, we will often encounter situations

where the number of cash flows is quite large: Home mortgage calls for monthly payments over 30 years = 360 pmts

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.18

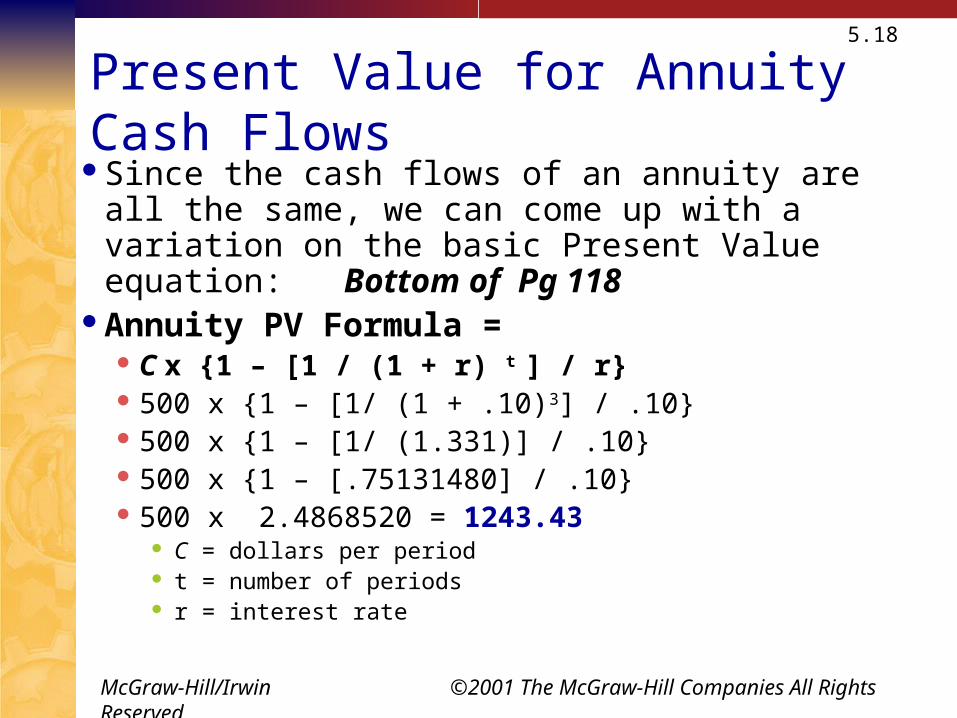

Present Value for Annuity Cash FlowsSince the cash flows of an annuity are all the same,

we can come up with a variation on the basic Present Value equation: Bottom of Pg 118

Annuity PV Formula = C x {1 – [1 / (1 + r) t ] / r} 500 x {1 – [1/ (1 + .10)3] / .10} 500 x {1 – [1/ (1.331)] / .10} 500 x {1 – [.75131480] / .10} 500 x 2.4868520 = 1243.43

C = dollars per period t = number of periods r = interest rate

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.19

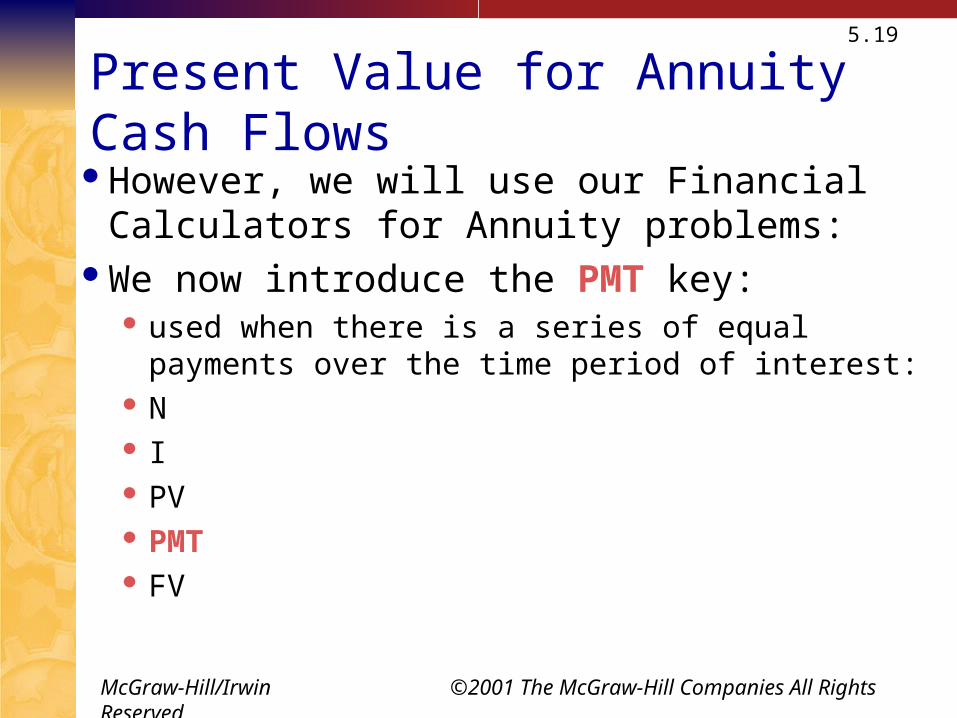

Present Value for Annuity Cash FlowsHowever, we will use our Financial Calculators for

Annuity problems:We now introduce the PMT key:

used when there is a series of equal payments over the time period of interest:

N I PV PMT FV

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.20

Present Value for Annuity Cash Flows

Once you identify that the problem is an annuity (a series of equal cash flows for a fixed time frame), you know the PMT key will be involved (either cash flows coming in or cash flows going out)

Simply enter the information you know and solve for the unknown.

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

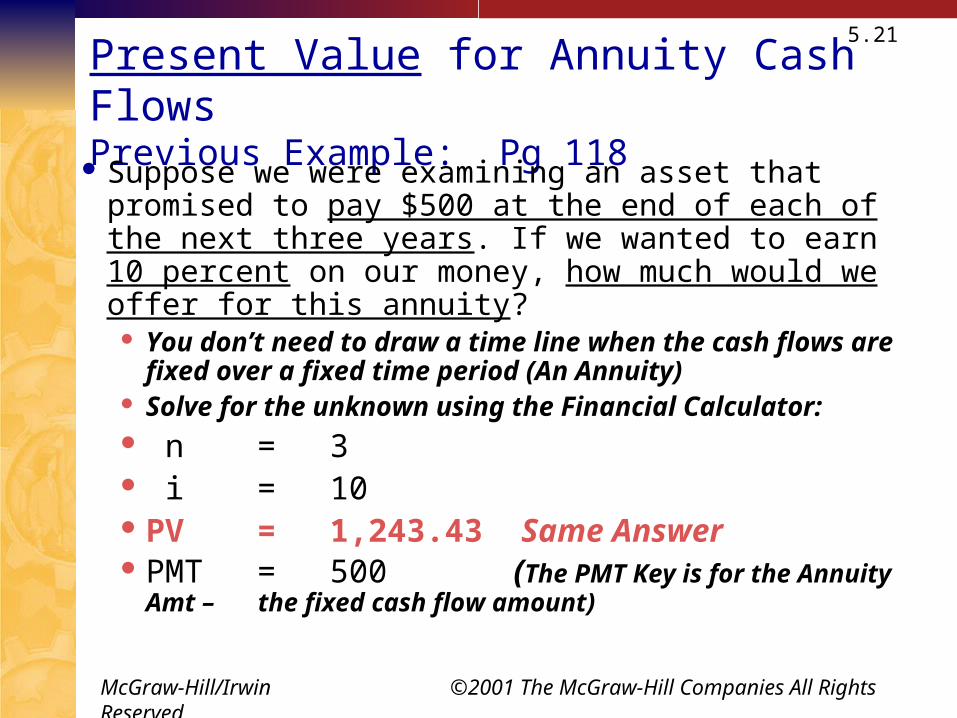

5.21

Present Value for Annuity Cash FlowsPrevious Example: Pg 118

Suppose we were examining an asset that promised to pay $500 at the end of each of the next three years. If we wanted to earn 10 percent on our money, how much would we offer for this annuity?

You don’t need to draw a time line when the cash flows are fixed over a fixed time period (An Annuity)

Solve for the unknown using the Financial Calculator: n = 3 i = 10 PV = 1,243.43 Same Answer PMT = 500 (The PMT Key is for the Annuity Amt –

the fixed cash flow amount)

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

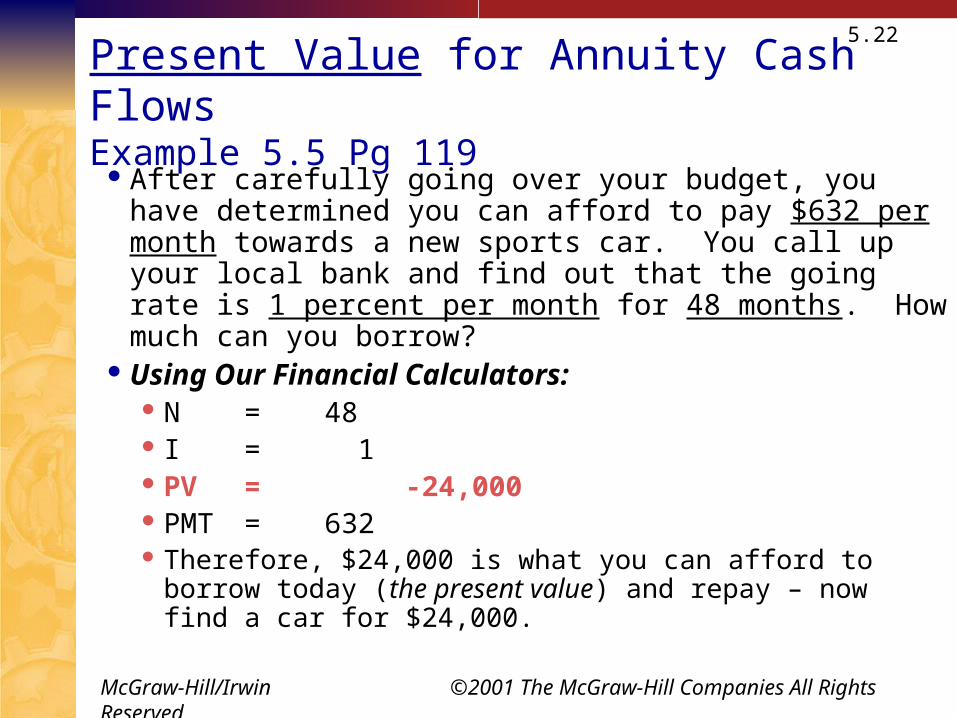

5.22

Present Value for Annuity Cash FlowsExample 5.5 Pg 119

After carefully going over your budget, you have determined you can afford to pay $632 per month towards a new sports car. You call up your local bank and find out that the going rate is 1 percent per month for 48 months. How much can you borrow?

Using Our Financial Calculators: N = 48 I = 1 PV = -24,000 PMT = 632 Therefore, $24,000 is what you can afford to borrow today

(the present value) and repay – now find a car for $24,000.

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

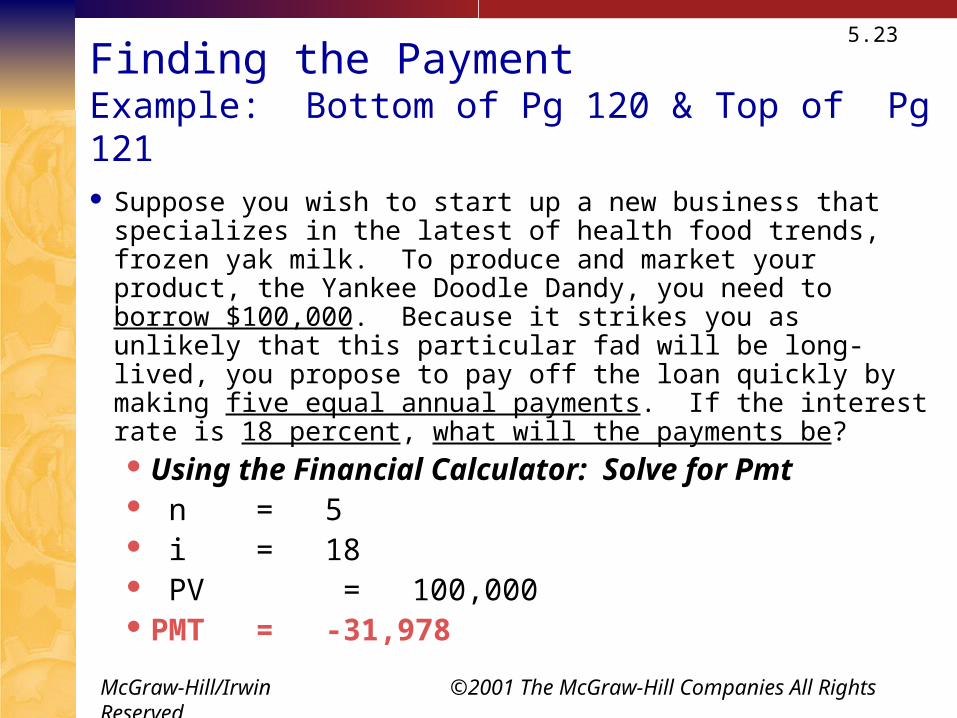

5.23

Finding the PaymentExample: Bottom of Pg 120 & Top of Pg 121

Suppose you wish to start up a new business that specializes in the latest of health food trends, frozen yak milk. To produce and market your product, the Yankee Doodle Dandy, you need to borrow $100,000. Because it strikes you as unlikely that this particular fad will be long-lived, you propose to pay off the loan quickly by making five equal annual payments. If the interest rate is 18 percent, what will the payments be? Using the Financial Calculator: Solve for Pmt n = 5 i = 18 PV = 100,000 PMT = -31,978

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

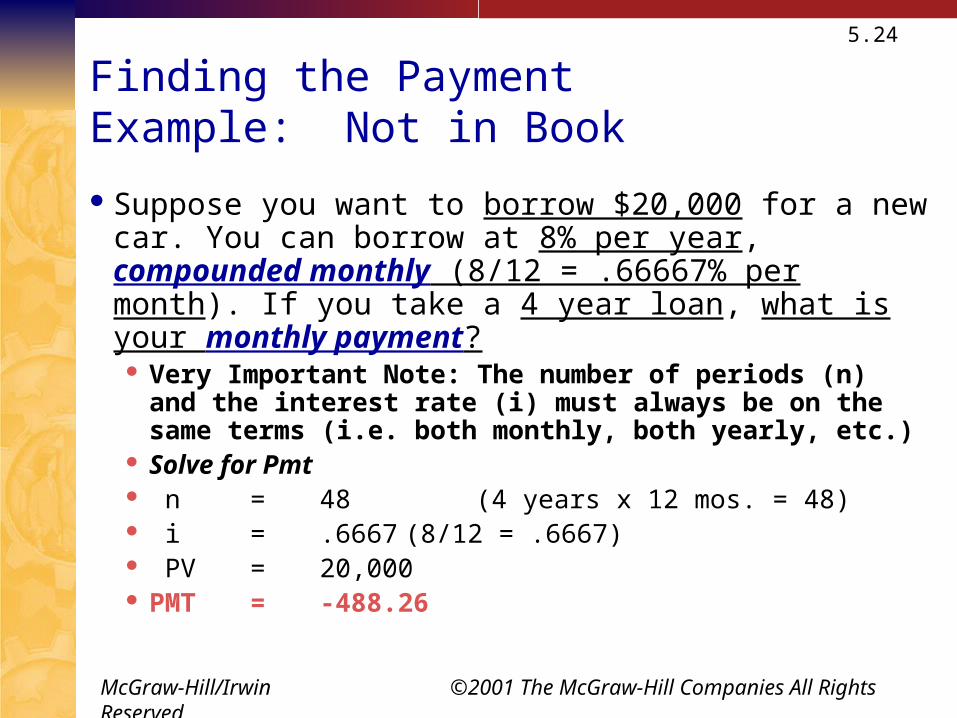

5.24

Finding the PaymentExample: Not in Book

Suppose you want to borrow $20,000 for a new car. You can borrow at 8% per year, compounded monthly (8/12 = .66667% per month). If you take a 4 year loan, what is your monthly payment?

Very Important Note: The number of periods (n) and the interest rate (i) must always be on the same terms (i.e. both monthly, both yearly, etc.)

Solve for Pmt n = 48 (4 years x 12 mos. = 48) i = .6667 (8/12 = .6667) PV = 20,000 PMT = -488.26

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.25

Finding the # of PaymentsExample: Bottom of Pg 121 122

You ran a little short on your spring break vacation, so you put $1,000 on your credit card. You can only afford to make the minimum payment of $20 per month. The interest rate on the credit card is 1.5 percent per month. How long will you need to pay off the $1,000?

Using the Financial Calculator: Solve for n n = 94 months (94 / 12 months = 7.83

years) i = 1.5

PV = 1,000 The amount you owe today

PMT = -20 Enter the PMT (cash out) as a negative (Note: book has 93.11 – the hp 12C calculator rounds up)

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

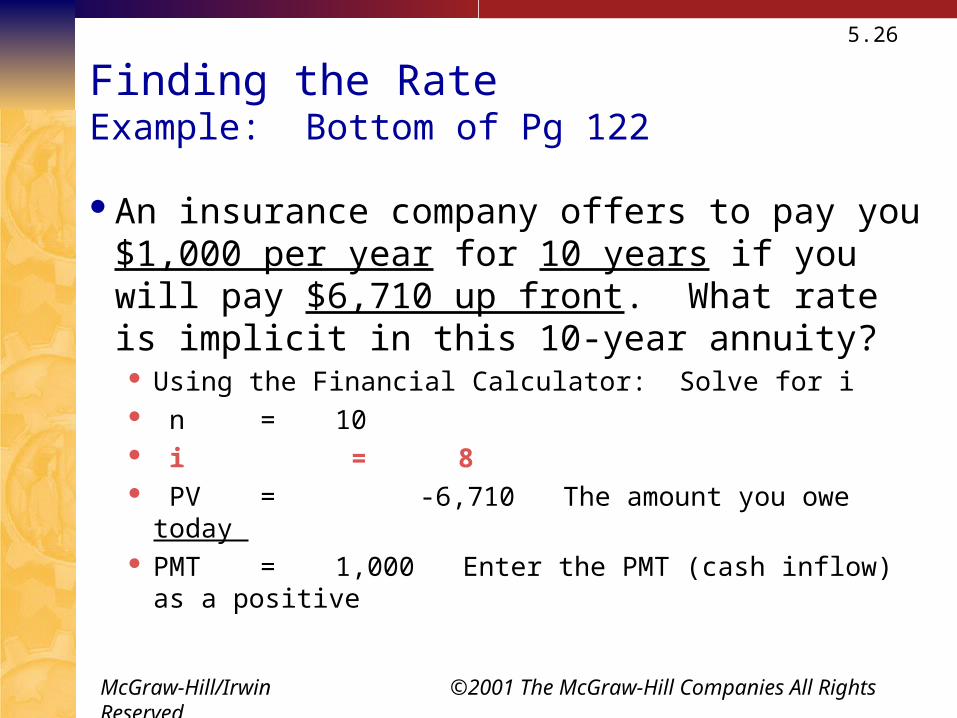

5.26

Finding the RateExample: Bottom of Pg 122

An insurance company offers to pay you $1,000 per year for 10 years if you will pay $6,710 up front. What rate is implicit in this 10-year annuity?

Using the Financial Calculator: Solve for i n = 10 i = 8 PV = -6,710 The amount you owe today

PMT = 1,000 Enter the PMT (cash inflow) as a positive

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

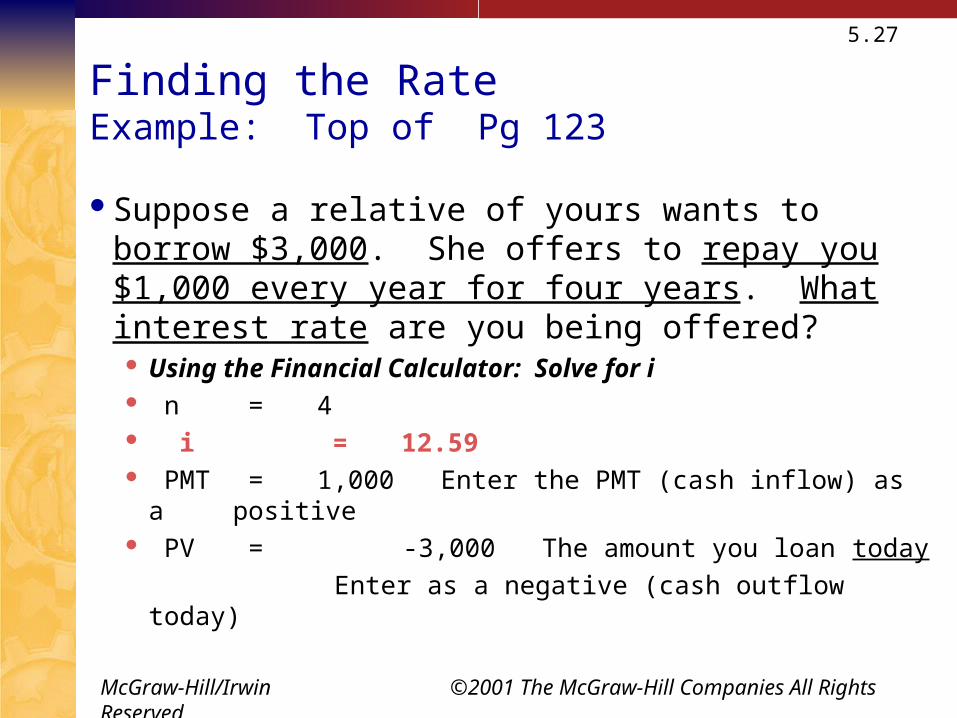

5.27

Finding the RateExample: Top of Pg 123

Suppose a relative of yours wants to borrow $3,000. She offers to repay you $1,000 every year for four years. What interest rate are you being offered?

Using the Financial Calculator: Solve for i n = 4 i = 12.59 PMT = 1,000 Enter the PMT (cash inflow) as a

positive PV = -3,000 The amount you loan today

Enter as a negative (cash outflow today)

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.28

Future Values of an Annuities Pg 124

Suppose you plan to contribute $2,000 every year into a retirement account paying 8 percent. If you retire in 30 years, how much will you have?

Using the Financial Calculator: Solve for FV

n = 30 i = 8 PMT = -2,000 Enter the PMT (cash outflow)

as a negative FV = 226,566.4 The amount you loan today

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.29

A Note on Annuities Due

So far, we have only discussed ordinary annuities (cash flows that occur at the end of each period) Example: A loan – the first loan pmt normally occurs one month “after” you

get the loan. However, when you lease an apt, the first lease pmt is usually due “immediately”.

The second pmt is due at the beginning of the second month, and so on. A lease is an example of an annuity due:

Annuity Due = An annuity for which the cash flows occur at the beginning of the period.

Almost any type of arrangement in which we have to prepay the same amount each period is an annuity due.

You would switch your Financial Calculator to “beginning” mode. For now we will concentrate on “ordinary” annuities.

End of period cash flows.

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.30

Perpetuities

Perpetuity: An annuity in which the fixed cash flows continue foreverThe cash flows are perpetual.An infinite number of cash flows

PV for a perpetuity = C / rC = the perpetual cash flow r = the interest rate

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.31

PerpetuitiesExample Page 125: An investment offers a perpetual cash flow of $500 every year. The

return you require on such an investment is 8%. What is the value of this investment?

PV for a perpetuity = C / r C = the perpetual cash flow r = the interest rate

$500/.08 = $6,250 In other words you could invest the lump sum present value

amount of $6,250 today in an investment paying 8% and receive a $500 interest pmt per year forever.

$6,250 x .08 = $500 $500 is the interest paid each year on the invested amt of $6,250

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.32

Chapter 5

We’ll cover the remaining portion of Chapter 5 in the next class and start on Chapter 6.

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

5.33

Chapter 5 (part 1) Suggested Homework Know chapter theories, concepts, and definitions

Re-read the chapter and review the Power Point Slides Review the problems worked in class Suggested Homework:

Chapter Review and Self-Test Problems: Page 134 5.1, 5.2, and 5.3

Answers are provided in the book just below the problems

Questions and Problems: Page 137 1, 3, 4, 5, 8, 9, 10, 21, 24, 28, 34, and 39

Answers are provided in your Solutions Manual Note: Use your financial calculator to work the problems.

Refer to the Solutions Manual to confirm your answers.