may 3, 2017 - mirae asset · holcim indonesia (smcb/not rated) ... semen baturaja (smbr/not rated)...

TRANSCRIPT

Mirae Asset Sekuritas Indonesia

Table 1. Summary of listed cement companies’ revenue ()

(in IDRbn) 1Q16 4Q16 1Q17 YoY QoQ

SMGR 6,021 7,052 6,399 6.3% -9.3%

INTP 3,929 4,015 3,376 -14.1% -15.9%

SMCB 2,456 2,552 2,159 -12.1% -15.4%

SMBR 297 480 328 10.2% -31.7%

Source: Company data, Mirae Asset Sekuritas Indonesia Research

Mimi Halimin +62-21-515-1140 [email protected]

To subscribe to our Daily Focus, please contact us at [email protected]

Cement: Summarizing 1Q17 earnings results

With all cement companies listed on the Indonesia Stock Exchange (IDX) having

now released their 1Q17 financial results, we provide a summary of each below:

Semen Indonesia (SMGR/Hold/TP IDR8,000)

For 1Q17, SMGR posted revenue of IDR6.4tr (+6.3% YoY, -9.3% QoQ). However,

SMGR’s main business, cement, still reported negative revenue growth (-1.2%

YoY). As for the bottom line, SMGR booked IDR746.5bn in net profit (-27.8% YoY; -

53.1% QoQ). (Please refer to our report titled SMGR’s 1Q17 review: Hard time

persists for further details).

Indocement Tunggal Prakarsa (INTP/Sell/TP IDR13,000)

INTP’s 1Q17 revenue came in at IDR3.4tr (-14.1% YoY; -15.9% QoQ). COGS came

in higher than expected, causing gross profit margin to shrink to 34.5% (from

43.2% in 1Q16 and 40.0% in 4Q16). For the bottom line, 1Q17 net profit slumped

48.7% YoY to only IDR491.6bn. (Please refer to our report titled INTP’s 1Q17

review: Weaker than expected for further details).

Holcim Indonesia (SMCB/Not rated)

For 1Q17, SMCB posted revenue of IDR2.2tr (-12.1% YoY; -15.4% QoQ). As for the

bottom line, SMCB booked a net loss of IDR116.5bn.

Semen Baturaja (SMBR/Not rated)

SMBR’s 1Q17 revenue came in at IDR327.8bn (+10.2% YoY; -31.7% QoQ) with net

profit still grew 13.2% YoY to IDR32.1bn. Although SMBR’s 1Q17 performance

was better than that of any other listed cement company on a YoY basis, its

performance weakened QoQ. In particular, we note that SMBR’s 1Q17 net profit

declined 62.0% QoQ.

Overall, we think the cement industry is still in the midst of hard times, given weak

1Q17 performances. The property market remained stagnant, limiting cement

consumption growth. Tough competition amid oversupply also persisted,

compressing cement companies’ ASP. These two components (volume and price)

compressed cement companies’ revenues. On the COGS side, rising coal prices

were an additional burden, squeezing margins. All in all, we maintain our

Underweight recommendation on the cement sector. Risks to our call are: 1) a

stronger-than-expected property market recovery, 2) cement industry

consolidation, and 3) government intervention supportive to the property and

cement industries.

May 3, 2017

Market Index

Last Trade Chg (%) MoM YoY

JCI 5,675.8 -0.2 1.4 18.1

MSCI Indonesia 26.5 0.6 2.2 13.9

MSCI EM 988.2 0.9 1.5 19.3

HANG SENG 24,696.1 0.3 1.5 19.0

KOSPI 2,205.4 0.6 1.7 11.0

FTSE 7,250.1 0.6 -1.1 16.5

DJIA 20,949.9 0.2 1.3 17.8

NASDAQ 6,095.4 0.1 3.3 27.9

Valuation

2017F P/E (x) P/B (x) ROE (%)

JCI 16.2 2.5 18.3

Key Rates

Last Trade Chg (bps) MoM YoY

BI 7-Day RR 4.75 0 0 -50*

3yr 6.60 -1 -17 -75

10yr 7.05 0 1 -64 *since introduced in Aug 2016

FX

Last Trade Chg (%) MoM YoY

USD/IDR 13,312.00 -0.1 0.0 1.3

USD/KRW 1,137.80 0.0 2.0 0.0

USD/JPY 111.99 0.1 1.0 5.1

USD/CNY 6.90 0.0 0.1 6.4

Commodities

Last Trade Chg (%) MoM YoY

WTI 47.7 -2.4 -6.0 0.9

Gold 1,256.8 0.0 0.3 -2.3

Coal 79.0 -5.8 -2.2 54.9

Palm Oil 2,730.0 0.2 -6.0 3.6

Rubber 169.5 0.0 -5.0 17.9

Nickel 9,450.0 1.2 -5.7 0.1

Copper 5,802.0 1.2 0.9 17.9

Tin 19,960.0 0.3 -1.4 15.6

JCI Index VS MSCI Emerging Markets

650

800

950

1,100

3,500

4,500

5,500

05/13 05/14 05/15 05/16 05/17

(pt) JCI MSCI EM (pt)

650

800

950

1,100

3,500

4,500

5,500

04/13 01/14 10/14 07/15 04/16

(pt) JCI MSCI EM (pt)

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Adhi Karya (ADHI IJ)

1Q17 review: On the right path

Adhi Karya (ADHI) delivered moderate earnings growth in 1Q17, an improvement from

the weak performances it exhibited last year. For the quarter, the company witnessed a

jump in each of its revenue (+69.3% YoY), gross profit (+87.6% YoY), operating profit

(+162.5% YoY), and net profit (+79.1% YoY) (see Table 1). However, these figures are

quite slow compared to the 1Q17 triple-digit growth achievements of Waskita Karya

(WSKT/Buy/TP IDR3,300) and Wijaya Karya (WIKA/Buy/TP IDR3,200) (please refer to

our WSKT 1Q17 review “Strong head start to linger” and WIKA 1Q17 review “Prizing

the overachiever”).

ADHI’s 1Q17 top and bottom lines met 11.6% and 2.6% of our full-year 2017F

estimates, respectively (see Table 2). These figures were in-line with the seasonal run-

rate of 10-13% (top line) and 2-5% (bottom line) in the first quarter. We would also like

to recap that ADHI’s soft performance in 2016 serves as a low base effect for this year

(please refer to our ADHI 4Q16 review “Disappointment leads to low base effect” for

more details). Hence, we assume this quarter’s high growth is as expected.

Solid new contract signings in the midst of weak property market

We like ADHI’s new contract signings in 1Q17 as it remained strong in the midst of soft

property market during the period (71.7% of the company’s new contracts came from

high-rise buildings; see Figure 4). In 1Q17, ADHI booked new contracts worth IDR3.7tr

(+60.9% YoY; 17.1% of its management’s FY17 target; see Figure 2 and 3). Its most

notable new contracts were Pancoran Riverside Apartment (IDR435bn), Nagrak flats

tower 6-10 North Jakarta (IDR215.4bn), Medan-Kualanamu-Tebing Tinggi Package 1A

toll road (IDR299.7bn), and Mojo sugar plant revitalization (IDR204.5bn). Given its good

start in new contract signings, we retain our forecast of IDR35.9tr worth of new

contracts (including LRT) to be signed by ADHI in FY17.

LRT project to begin its sizable recognition in 2H17

As a quick reminder, ADHI signed the contract for the 43.5-km LRT Jabodebek LRT

phase 1 project (Cawang-Cibubur, Cawang-Kuningan-D. Atas, and Cawang-Bekasi Timur)

worth IDR23.3tr in Feb 2017. The progress itself has been lingering at c.15% completion

rate (allocation since late-2015), which we think to be quite slow when compared to

WSKT’s Palembang LRT, which already reached c.40% completion rate (allocation since

mid-2016). Hence, we believe ADHI’s earnings would remain moderate in 1H17 given

that the revenue recognition from its LRT project in the period would be minimum. It is

worth noting that the funding scheme itself has not met full finalization as it still needs

to pass the House of Representatives’ approval prior to PMN (Penanaman Modal

Negara) disbursement to KAI (Kereta Api Indonesia). Hence, we retain our assumptions

that the LRT project will meet its crystal clear direction by end-1H17 and begin its

sizable revenue recognition starting in 2H17.

Construction

Company Report

May 2, 2017

(Maintain) Hold

Target Price (12M, IDR) 2,390

Share Price (5/2/17, IDR) 2,210

Expected Return 8.1%

Consensus OP (17F, IDRtr) 1.3

EPS Growth (17F, %) 134.4

P/E (17F, x) 10.7

Industry P/E (17F, x) 14.0

Benchmark P/E (17F, x) 16.2

Market Cap (IDRbn) 7,869.5

Shares Outstanding (mn) 3,560.8

Free Float (mn) 1,744.8

Institutional Ownership (%) 61.0

Beta (Adjusted, 24M) 1.0

52-Week Low (IDR) 1,830

52-Week High (IDR) 2,900

(%) 1M 6M 12M

Absolute -6.8 2.3 -15.0

Relative -8.7 -2.7 -33.0

PT. Mirae Asset Sekuritas Indonesia

Property

Franky Rivan

+62-21-515-1140 (ext. 124)

FY (Dec.) 12/13 12/14 12/15 12/16 12/17F 12/18F

Revenue (IDRbn) 9,799.6 8,653.6 9,389.6 11,063.9 19,462.9 26,629.9

Operating profit (IDRbn) 864.2 642.0 579.2 659.2 1,463.9 1,932.6

OP Margin (%) 8.8 7.4 6.2 6.0 7.5 7.3

Net profit (IDRbn) 406.0 329.1 463.7 313.5 734.6 812.4

EPS (IDR) 114.0 92.4 130.2 88.0 206.3 228.1

BPS (IDR) 410.0 460.8 1,449.7 1,528.5 2,109.2 2,285.0

P/E (x) 19.4 23.9 17.0 25.1 10.7 9.7

P/B (x) 5.4 4.8 1.5 1.4 1.0 1.0

ROE (%) 27.8 20.1 9.0 5.8 9.8 10.0

ROA (%) 4.2 3.1 2.8 1.6 2.3 2.3

Note: Net profit refers to net profit attributable to controlling interests Source: Company data, Mirae Asset Sekuritas Indonesia Research

60

80

100

120

140

5/1

6

6/1

6

7/1

6

8/1

6

9/1

6

10

/16

11

/16

12

/16

1/1

7

2/1

7

3/1

7

4/1

7

5/1

7

JCI ADHI(D-1yr=100)

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Macro update April inflation: Rising prices

April consumer prices beat consensus forecast

According to data released by the Central Bureau of Statistics (BPS), inflation for the

month of April came in at 4.17% YoY (vs. 3.61% YoY in March), beating the consensus

estimate (4.08% YoY). Consumer prices picked up 0.09% MoM in April (vs. -0.02% MoM

in March). Regarding the main contributors to monthly price inflation,

housing/water/electricity/gas/fuel prices increased 0.93% MoM (vs. +0.30% MoM in

March); clothing prices increased 0.49% MoM (vs. +0.18% MoM in March), and

transportation & communication prices increased 0.27% MoM (vs. -0.13% MoM in

March), whereas unprocessed food prices declined by 1.13% MoM (vs. -0.66% MoM in

March). Core inflation—excluding administered prices and volatile foods—came in at

3.28% YoY (vs. 3.30% YoY in March).

Electricity tariff adjustment was the main contributor to April’s inflation

According to BPS, the biggest contributor to April’s inflation was the electricity tariff

adjustment for households (900VA). The state electricity company PLN began adjusting

tariffs for 900VA household customers in 1Q17, with tariffs diverging for subsidized (i.e.,

low-income) vs. non-subsidized customers. Electricity tariff hikes (30%) are being phased

in gradually for non-subsidized customers.

Adjusting to rising price environment

We do not think inflation will overshoot going forward, as the core inflation trend

remains stable (see Figure 3). In our view, the central bank is unlikely to tighten its

monetary policy in the near term, which should keep the market liquid. However, we

believe April inflation should provide some relief for consumer names. We believe higher

inflation will provide validation for ASP hikes by consumer companies, and think

consumers are able to absorb higher prices given the continuous rise in household

income in recent years. We recommend that investors take another look at consumer

plays with strong brand awareness and pricing power. Our picks within the consumer

area are: Unilever Indonesia (UNVR/Buy/TP: IDR 52,700), Indofood CBP Sukses Makmur

(ICBP/ Under Review), Gudang Garam (GGRM/Under Review), Ramayana Lestari Sentosa

(RALS/Trading Buy/TP: IDR1,470), and Astra International (ASII/Not Rated).

Macro update

May 3, 2017

PT.Mirae Asset Sekuritas Indonesia

Economy

Taye Shim

+62-21-515-3281

Mangesti Diah Sulistiani

+62-21-515-1140 (ext. 127)

mangesti@ miraeasset.co.id

April inflation by component

Source: BPS, Mirae Asset Sekuritas Indonesia Research

2.99

5.02

4.09

2.61

3.98

2.78

3.16

3.61

3.3

2.80

4.78

5.19

2.88

3.73

2.79

5.12

4.17

3.28

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5 March

April

(YoY, %)

May 3, 2017

4

Indonesia Daily Focus

Mirae Asset Sekuritas Indonesia

Local flash

Economy: Indonesia records inflation of 0.09% in April. After seeing deflation a

month earlier owing to the harvest season, the country recorded monthly inflation of

0.09 percent in April on account of increases in the prices of most commodities.

Inflation in April brought annual inflation to 4.17 percent year-on-year (yoy), the

Central Statistics Agency (BPS) announced on Tuesday. "I think inflation at 0.09

percent in April remained in line with what the government is trying to manage

because there will be bigger challenges in May and June," said BPS head Suhariyanto.

(Jakarta Post)

MAIN: Malindo's net profit shrank by 52%. The performance of PT Malindo Feedmill

Tbk (MAIN) in the first quarter of 2017 is less encouraging. Net profit declined by 52%

year on year (yoy) to IDR24.63 billion from IDR52.16 billion. Signal weakening

performance has been seen from the sales. Based on the financial statements, Tuesday

(2/4), revenue at IDR1.27 trillion, down 2% yoy from IDR1.3 trillion in the same period

last year. (Kontan)

MAPI: Mitra Adiperkasa profits jumped by 409%. PT Mitra Adiperkasa Tbk recorded

profit attributable to owners entity of IDR57.42 billion in 1Q17, soared up to 409%

from IDR11.28 billion in the same period in the previous year. The achievement is in

line with the increase in net revenue. Revenue in the first quarter of 2017 reached

IDR3.61 trillion, up 14.2% from IDR3.16 trillion in the first quarter of 2016. (Bisnis

Indonesia)

TPIA: Shareholders approves TPIA rights issue. The General Meeting of Shareholders

of PT Chandra Asri Petrochemical (TPIA) has finally approved the addition of Capital

with Preemptive Rights (HMETD) or rights issue. This funding agenda includes

company's effort to comply the free float rule of the Indonesia Stock Exchange. "The

proceeds will be used by the Company as a capital expenditure in line with the

Company's medium-term business plan to increase its production capacity and

diversify its product portfolio," said Harry Muhammad Tamin, Head of Investor

Relations TPIA. (Kontan)

LPKR: Sluggish in property, Lippo Karawaci profit slump in 1Q17. PT Lippo Karawaci

Tbk (LPKR) posted first-quarter net profit of IDR142.66 billion, down 54.17% from

IDR311.28 billion in the first quarter of 2016. This is in line with the revenue in 1Q17

amounting to IDR2.54 trillion. This figure decreased by 2.48% compared to the first

quarter of 2016 amounting to IDR2.60 trillion. (Kontan)

ERTX: Eratex 1Q17 profit plummeted due to higher expenses. PT Eratex Djaja Tbk

only able to posted a net profit of USD319,757 in 1Q17, drop by 49% compared to the

same quarter last year which was USD604,129. In fact, ERTX achieves revenue growth

in the first quarter to USD18.9 million. Corporate Secretary of PT Eratex Djaja Tbk,

Juliarti Pudji, said this is due to the factory expansion project this year. As is known,

ERTX plans to increase its production capacity to 7.2 million pieces of clothing per year.

(Kontan)

SIDO: Sido Muncul ready for expansion into Philippine market. PT Industri Jamu &

Farmasi Sido Muncul Tbk (SIDO) is targeting revenue growth this year by 15%. This

target is driven by the addition of production capacity and the strengthening of export

sales to Philippines. Last year, SIDO managed to book IDR2.56 trillion in revenue. This

figure is up 15.4% compared to last year's IDR2.12 trillion. (Kontan)

May 3, 2017

5

Indonesia Daily Focus

Mirae Asset Sekuritas Indonesia

Technical analysis

Tasrul +62-21-515-1140 [email protected]

Jakarta Composite Index (JCI) – Consolidation

Summary

Item Data Item Data

Close (May 2, 2017) 5,675.8 (-0.2%) Normal trading range 5,654-5,707

Average index performance (%) 3.23 Target

Period 48 - Daily 5,707

r-squared 0.9045 - Weekly 5,729

Volatility (+/-, %) 0.42 - Monthly 5,806

Volatility (+/-, point) 24.1 Stop loss 5,654

Source: Mirae Asset Sekuritas Indonesia Research

Figure 1. Daily trend - Uptrend

Source: Mirae Asset Sekuritas Indonesia Research

Created w ith AmiBroker - advanced charting and technical analysis softw are. http://w w w .amibroker.com

Optimization Trading System - ©2010 Optimization Trading System - ©2010 Optimization Trading System - ©2010 Optimization Trading System - ©2010

5,707

5,670

^JKSE - Daily 5/2/2017 Open 5703.87, Hi 5714.34, Lo 5675.81, Close 5675.81 (-0.2%) Upper Band = 5,782.83, Channel_prd = 5,719.29, Lower Band = 5,655.75, VWAP = 5,673.92, VWAP = 5,654.39, VWAP

5,675.81

5,673.92

5,655.75

5,654.39

5,584.83

5,719.29

5,782.83

16 23 30 Feb 6 13 20 27 Mar 6 13 20 27 Apr 10 17 25 May Optimization Trading System - ©2010

^JKSE - Volume = 6,007,262,208.00, Avg.Volume = 6,489,360,384.00

6,007,262,208

6,489,360,384

May 3, 2017

6

Indonesia Daily Focus

Mirae Asset Sekuritas Indonesia

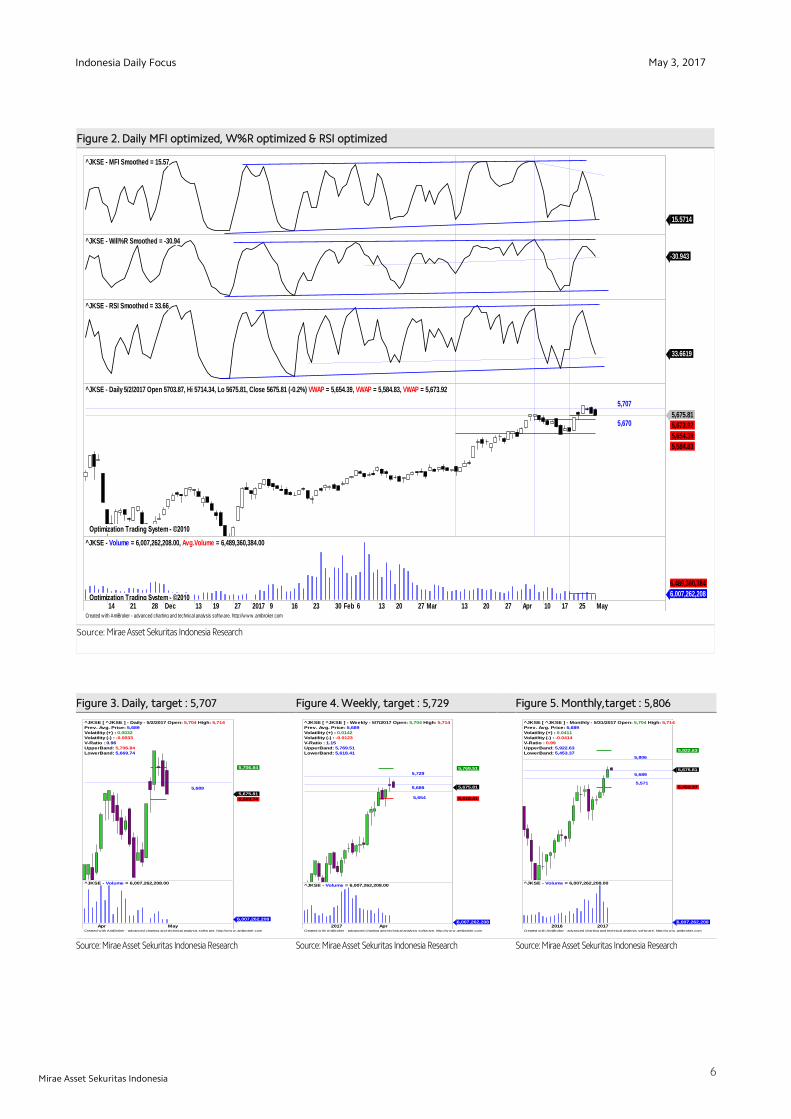

Figure 2. Daily MFI optimized, W%R optimized & RSI optimized

Source: Mirae Asset Sekuritas Indonesia Research

Figure 3. Daily, target : 5,707 Figure 4. Weekly, target : 5,729 Figure 5. Monthly,target : 5,806

x

Source: Mirae Asset Sekuritas Indonesia Research

Source: Mirae Asset Sekuritas Indonesia Research

Source: Mirae Asset Sekuritas Indonesia Research

Created w ith AmiBroker - advanced charting and technical analysis softw are. http://w w w .amibroker.com

^JKSE - MFI Smoothed = 15.57

15.5714

^JKSE - Will%R Smoothed = -30.94

-30.943

^JKSE - RSI Smoothed = 33.66

33.6619

Optimization Trading System - ©2010 Optimization Trading System - ©2010 Optimization Trading System - ©2010

5,707

5,670

^JKSE - Daily 5/2/2017 Open 5703.87, Hi 5714.34, Lo 5675.81, Close 5675.81 (-0.2%) VWAP = 5,654.39, VWAP = 5,584.83, VWAP = 5,673.92

5,675.81

5,673.92

5,654.39

5,584.83

14 21 28 Dec 13 19 27 2017 9 16 23 30 Feb 6 13 20 27 Mar 13 20 27 Apr 10 17 25 May Optimization Trading System - ©2010

^JKSE - Volume = 6,007,262,208.00, Avg.Volume = 6,489,360,384.00

6,007,262,208

6,489,360,384

Created w ith AmiBroker - advanced charting and technical analysis softw are. http://w w w .amibroker.com

5,689

^JKSE [ ^JKSE ] - Daily - 5/2/2017 Open: 5,704 High: 5,714

Prev. Avg. Price: 5,689

Volatility (+) : 0.0032

Volatility (-) : -0.0033

V-Ratio : 0.96

UpperBand: 5,706.84

LowerBand: 5,669.74

5,675.81

5,669.74

5,706.84

Apr May

^JKSE - Volume = 6,007,262,208.00

6,007,262,208

Created w ith AmiBroker - advanced charting and technical analysis softw are. http://w w w .amibroker.com

5,689

5,654

5,729

^JKSE [ ^JKSE ] - Weekly - 5/7/2017 Open: 5,704 High: 5,714

Prev. Avg. Price: 5,689

Volatility (+) : 0.0142

Volatility (-) : -0.0123

V-Ratio : 1.15

UpperBand: 5,769.51

LowerBand: 5,618.41

5,675.81

5,618.41

5,769.51

2017 Apr

^JKSE - Volume = 6,007,262,208.00

6,007,262,208

Created w ith AmiBroker - advanced charting and technical analysis softw are. http://w w w .amibroker.com

5,689

5,806

5,571

^JKSE [ ^JKSE ] - Monthly - 5/31/2017 Open: 5,704 High: 5,714

Prev. Avg. Price: 5,689

Volatility (+) : 0.0411

Volatility (-) : -0.0414

V-Ratio : 0.99

UpperBand: 5,922.63

LowerBand: 5,453.37

5,675.81

5,453.37

5,922.63

2016 2017

^JKSE - Volume = 6,007,262,208.00

6,007,262,208

May 3, 2017

7

Indonesia Daily Focus

Mirae Asset Sekuritas Indonesia

Chart 6. JCI Vs. USD/IDR Chart 7. JCI performance (absolute vs. relative)

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Note: Relative to MSCI EM Index

Source: Bloomberg, Mirae Asset Sekuritas Indonesia

Chart 8. Foreigner’s net purchase (EM) Chart 9. Energy price

Note: The latest figure for India are April 28th, 2017

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Source: Bloomberg, Mirae Asset Sekuritas Indonesia

Chart 10. Non-ferrous metal price Chart 11. Precious metal price

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Source: Bloomberg, Mirae Asset Sekuritas Indonesia

13,100

13,300

13,500

13,700

4,800

5,000

5,200

5,400

5,600

5,800

1/31 2/28 3/28 4/25

(IDR) (pt) JCI (L) USD/IDR (R)

-0.2

0.2 1.2

17.9

-1.0 -0.4 -1.2

-2.4 -4

0

4

8

12

16

20

1D 1W 1M 1Y

Absolute Relative(%, %p)

116

357

64

-6

7

-173

1,020

1,380

371

85 48

-171 -400

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

Korea Taiwan Indonesia Thailand Philippines India

1 Day 5 Days (USDmn) (USDmn) (USDmn) (USDmn)

75

80

85

90

95

100

105

110

1/31 2/28 3/28 4/25

CPO WTI Coal(D-3M=100)

80

85

90

95

100

105

110

115

1/31 2/28 3/28 4/25

(D-3M=100) Copper Nickel Tin

90

95

100

105

110

1/31 2/28 3/28 4/25

Silver Gold Platinum(D-3M=100)

May 3, 2017

8

Indonesia Daily Focus

Mirae Asset Sekuritas Indonesia

Table. Key valuation metrics

Company Name Ticker Price Market Cap Price Performance (%) P/E(X)* P/B(X)* ROE(%)*

(IDR) (IDRbn) 1D 1W 1M 1Y FY16 FY17 FY16 FY17 FY16 FY17

Jakarta Composite Index JCI 5,676 6,211,001 -0.2 0.2 1.9 17.3 16.2 14.1 2.5 2.3 18.2 19.9

FINANCIALS

Bank Central Asia BBCA 17,900 441,325 0.8 2.4 8.2 36.6 18.5 19.3 3.4 3.4 20.4 18.9

Bank Mandiri Persero BMRI 11,675 272,417 -0.2 2.4 -0.2 22.3 19.6 13.5 1.8 1.7 10.3 12.6

Bank Rakyat Indonesia Persero BBRI 13,050 321,933 1.2 1.0 0.6 27.0 10.9 11.5 1.9 2.0 20.2 18.2

Bank Negara Indonesia Persero BBNI 6,425 119,818 0.8 4.5 -0.8 43.1 9.1 9.0 1.2 1.3 13.9 14.6

Bank Tabungan Negara Persero BBTN 2,300 24,357 0.0 -1.3 1.3 30.7 13.3 12.1 1.0 1.2 7.6 10.1

CONSUMER

HM Sampoerna HMSP 3,820 444,335 0.0 -1.8 -2.1 -3.8 34.8 32.6 13.0 12.5 38.6 38.2

Gudang Garam GGRM 67,150 129,203 1.1 4.6 2.5 -6.2 18.4 17.0 3.1 2.9 17.3 17.8

Indofood CBP Sukses Makmur ICBP 8,550 99,709 -2.6 1.8 4.9 11.8 27.8 25.6 5.7 5.0 21.8 21.0

Indofood Sukses Makmur INDF 8,425 73,975 0.6 5.0 5.3 19.9 18.3 16.4 2.4 2.3 14.7 14.4

Kalbe Farma KLBF 1,515 71,016 -4.4 -4.1 -1.6 13.1 30.9 27.8 6.0 5.3 20.6 19.2

Unilever Indonesia UNVR 45,300 345,639 1.8 -0.5 4.6 4.7 46.3 48.2 62.9 62.7 134.1 137.3

AGRICULTURAL

Astra Agro Lestari AALI 14,350 27,619 -0.3 -1.0 -3.7 -7.3 14.8 14.2 1.9 1.6 14.1 11.1

PP London Sumatera Indonesia LSIP 1,395 9,518 0.0 1.8 -4.8 -6.7 20.0 12.2 1.6 1.2 7.9 9.8

Sawit Sumbermas Sarana SSMS 1,720 16,383 -1.7 3.3 3.9 -6.5 22.5 22.3 3.9 4.1 18.3 18.4

INFRASTRUCTURE

XL Axiata EXCL 3,080 32,919 -4.0 2.7 0.7 -11.3 60.8 73.2 1.2 1.5 2.1 1.6

Jasa Marga JSMR 4,620 33,531 -0.4 3.4 0.0 -15.4 15.6 17.4 2.3 2.2 15.7 13.1

Perusahaan Gas Negara PGAS 2,410 58,422 -0.8 0.0 -4.7 -4.0 15.3 10.6 1.5 1.3 9.8 12.6

Tower Bersama Infrastructure TBIG 5,900 26,735 0.9 -2.1 8.3 2.2 17.4 20.7 14.3 8.4 83.6 49.3

Telekomunikasi Indonesia TLKM 4,410 444,528 0.9 -0.2 6.8 27.8 20.3 19.4 4.7 4.6 24.3 24.0

Soechi Lines SOCI 372 2,626 -3.1 -0.5 -3.1 -20.9 8.2 5.6 0.9 N/A 15.9 10.1

Garuda Indonesia GIAA 358 9,267 -2.7 -3.2 4.7 -14.4 31.7 21.3 2.6 2.6 8.6 13.2

BASIC-INDUSTRIES

Semen Indonesia SMGR 8,800 52,197 -0.3 1.1 -2.2 -7.9 12.0 13.6 1.9 1.7 16.3 12.7

Charoen Pokphand Indonesia CPIN 3,200 52,474 0.3 -3.0 0.0 -13.7 22.6 15.6 3.6 3.1 16.5 21.1

Indocement Tunggal Prakarsa INTP 16,150 59,452 -4.7 0.9 -2.7 -15.2 14.6 17.0 2.2 2.1 15.5 12.7

Japfa Comfeed Indonesia JPFA 1,400 15,975 -4.4 -8.2 -9.4 55.6 7.7 8.4 1.9 1.6 28.6 20.2

MINING

Indo Tambangraya Megah ITMG 18,625 21,045 -2.6 -0.9 -7.8 139.5 10.4 7.7 1.5 1.6 15.0 20.1

Adaro Energy ADRO 1,720 55,016 -3.1 -6.5 -1.7 140.6 12.0 10.8 1.3 1.2 11.1 11.4

Aneka Tambang ANTM 685 16,461 -1.4 -2.1 -6.2 -9.3 298.3 59.7 1.2 0.9 0.4 2.6

Vale Indonesia INCO 2,260 22,456 1.8 5.1 -5.4 25.2 N/A 33.9 1.1 0.9 0.1 2.5

Tambang Batubara Bukit Asam PTBA 12,350 28,456 -0.3 -0.8 -6.4 75.2 13.1 9.3 2.5 2.2 20.5 24.9

TRADE

United Tractors UNTR 26,000 96,984 -3.3 -3.4 -1.9 73.3 15.8 15.1 1.9 2.2 12.7 14.9

AKR Corporindo AKRA 6,650 26,601 -1.1 0.8 6.4 4.7 23.5 21.3 3.5 3.4 15.7 16.5

Global Mediacom BMTR 540 7,667 0.9 0.0 3.8 -55.4 41.8 N/A 0.9 N/A 2.0 N/A

Matahari Department Store LPPF 14,800 43,185 1.4 11.3 12.3 -22.1 21.9 19.4 23.8 15.6 136.4 86.2

Media Nusantara Citra MNCN 1,845 26,339 1.1 3.1 -0.3 -16.1 17.7 14.6 2.7 2.4 15.4 17.0

Matahari Putra Prima MPPA 975 5,244 3.2 5.4 -11.8 -35.4 211.4 31.9 3.3 2.1 1.6 5.0

Surya Citra Media SCMA 2,830 41,379 -1.0 -1.4 4.8 -13.7 27.2 23.0 11.9 10.1 45.7 46.6

Siloam International Hospital SILO 14,200 18,469 3.6 0.5 1.4 65.4 150.3 129.1 4.5 5.7 3.5 4.6

PROPERTY

Bumi Serpong Damai BSDE 1,775 34,163 -0.8 -2.5 -5.8 0.9 18.8 14.4 1.6 1.5 9.1 10.5

Adhi Karya ADHI 2,210 7,869 -2.2 -3.5 -6.8 -15.0 23.6 13.4 1.4 1.3 5.9 10.0

Alam Sutera Realty ASRI 346 6,799 -0.6 0.0 -4.4 -13.1 13.6 8.0 1.0 0.9 7.5 11.3

Ciputra Development CTRA 1,215 22,551 -5.1 -6.5 -1.2 -1.0 19.9 16.9 2.2 1.6 9.8 11.5

Lippo Karawaci LPKR 790 18,231 0.0 1.9 9.0 -21.4 18.6 16.3 0.9 0.9 5.0 6.1

Pembangunan Perumahan PTPP 2,970 18,414 -6.6 -7.5 -10.3 -14.9 23.1 12.8 2.4 1.7 14.4 14.5

Pakuwon Jati PWON 635 30,581 1.6 4.1 3.3 25.7 16.3 15.1 3.1 2.9 21.0 19.8

Summarecon Agung SMRA 1,350 19,476 -0.7 -2.9 0.7 -9.7 61.3 42.3 3.1 2.8 5.1 7.1

Wijaya Karya WIKA 2,320 20,810 -2.1 -2.1 -3.7 -2.9 14.4 16.5 1.8 1.6 12.9 10.4

Waskita Karya WSKT 2,350 31,898 -1.7 -2.1 -0.8 -0.8 17.3 13.2 3.1 2.0 16.6 16.7

MISCELLANEOUS

Astra International ASII 9,000 364,352 1.8 -1.6 4.3 34.3 22.1 18.4 3.0 3.0 14.2 16.4

Source: Bloomberg, Mirae Asset Sekuritas Indonesia

*Note: Valuation metrics based on Bloomberg consensus estimates

May 3, 2017

9

Indonesia Daily Focus

Mirae Asset Sekuritas Indonesia

Sector performance

Top 10 market cap performance

Name Index Chg (%) Ticker Price Market Cap (IDRbn) Chg (%)

Agricultural 1,819.8 -1.1 BRAM IJ 12900 5,805 19.72

Mining 1,499.3 -1.9

INKP IJ 2360 12,912 13.46

Basic-Industry 602.4 -1.2 KREN IJ 450 8,194 5.63

Miscellaneous Industry 1,515.8 0.6 SDRA IJ 1100 5,580 4.76

Consumer Goods 2,436.9 0.1 SILO IJ 14200 18,469 3.6

Property & Construction 498.8 -1.3

MPPA IJ 975 5,244 3.17

Infrastructure 1,146.6 0.3 AISA IJ 2290 7,371 3.15

Finance 895.9 0.4 NIKL IJ 4010 10,119 2.82

Trade 915.4 -0.8 TOWR IJ 3980 40,608 2.6

Composite 5,675.8 -0.2 RALS IJ 1305 9,260 2.35 Source: Bloomberg

Top 5 leading movers Top 5 lagging movers

Name Chg (%) Close Name Chg (%) Close

UNVR IJ 1.8 45,300 SMBR IJ -10.8 3,150

TLKM IJ 0.9 4,410 UNTR IJ -3.4 26,000

BBRI IJ 1.2 13,050 KLBF IJ -4.4 1,515

BBCA IJ 0.9 17,900 INTP IJ -4.7 16,150

ASII IJ 0.6 9,000 ICBP IJ -2.6 8,550 Source: Bloomberg

Economic Calendar

Time Currency Detail Forecast Previous

5:45am NZD Employment Change q/q 0.8% 0.8%

5:45am NZD Unemployment Rate 5.1% 5.2%

5:45am NZD Labor Cost Index q/q 0.5% 0.4%

6:01am GBP BRC Shop Price Index y/y -0.8%

6:30am AUD AIG Services Index 51.7

All Day JPY Bank Holiday

2:00pm EUR Spanish Unemployment Change 21.3K -48.6K

2:55pm EUR German Unemployment Change -10K -30K

3:30pm GBP Construction PMI 52.1 52.2

4:00pm EUR Prelim Flash GDP q/q 0.5% 0.4%

4:00pm EUR PPI m/m 0.1% 0.0%

Tentative EUR German 10-y Bond Auction 0.21|1.4

7:15pm USD ADP Non-Farm Employment Change 178K 263K

8:45pm USD Final Services PMI 52.5 52.5

9:00pm USD ISM Non-Manufacturing PMI 56.1 55.2

9:30pm USD Crude Oil Inventories -3.6M

Note: Time is based on Indonesian local time

Source: Forex Factory

Disclaimers

This report is prepared strictly for private circulation only to clients of PT Mirae Asset Sekuritas Indonesia. It is purposed only to person having professional

experience in matters relating to investments. The information contained in this report has been taken from sources which we deem reliable. No warranty

(express or implied) is made to the accuracy or completeness of the information. All opinions and estimates included in this report constitute our

judgments as of this date, without regards to its fairness, and are subject to change without notice. However, none of Mirae Asset Sekuritas Indonesia

and/or its affiliated companies and/or their respective employees and/or agents makes any representation or warranty (express or implied) or accepts any

responsibility or liability as to, or in relation to, the accuracy or completeness of the information and opinions contained in this report or as to any

information contained in this report or any other such information or opinions remaining unchanged after the issue thereof. We expressly disclaim any

responsibility or liability (express or implied) of Mirae Asset Sekuritas Indonesia, its affiliated companies and their respective employees and agents

whatsoever and howsoever arising (including, without limitation for any claims, proceedings, action, suits, losses, expenses, damages or costs) which may

be brought against or suffered by any person as a results of acting in reliance upon the whole or any part of the contents of this report and neither Mirae

Asset Sekuritas Indonesia, its affiliated companies or their respective employees or agents accepts liability for any errors, omissions or misstatements,

negligent or otherwise, in the report and any liability in respect of the report or any inaccuracy therein or omission there from which might otherwise arise

is hereby expresses disclaimed.

This document is not an offer to sell or a solicitation to buy any securities. This firms and its affiliates and their officers and employees may have a position,

make markets, act as principal or engage in transaction in securities or related investments of any company mentioned herein, may perform services for or

solicit business from any company mentioned herein, and may have acted upon or used any of the recommendations herein before they have been

provided to you. © PT Mirae Asset Sekuritas Indonesia 2016.