may 19th 2012 retail renaissance - the...

TRANSCRIPT

May 19th 2012

S P E C I A L R E P O R T

I N T E R N AT I O N A L B A N K I N G

Retail renaissance

SRInternationalBankingindd 1 08052012 1643

1

IF YOUR BANK could start over this is what it would be trumpeted themarketing campaign for the launch in 1999 of Wingspan an internetbank The following year the bank was gone In September 2000 a fewmonths after the dotcom bubble burst it was absorbed by its boringAmerican bricks-and-mortar parent Bank One (now part of JPMorgan)

For all the high hopes that the internet would transform bankingmost other internet banks launched around that time met with a similarfate Citi fi an online bank started by Citigroup was folded back into itsparent in 2000 NetBank an American pioneer of internet banking sol-diered on for longer than most but was shut down by banking regulatorsin 2007 On the other side of the Atlantic Egg Britainrsquos rst stand-aloneinternet bank shook the market in 1999-2000 when it gained more than2m customers within months of starting up But within a few years it toohad in eect disappeared its customers having been sold rst to Citi-group and then to Barclays and the Yorkshire Building Society It was anignominious end to a bold experiment in online banking that had causedpalms to sweat in banking centres around the world

The promise of internet banking had seemed obvious More thanmost other industries banking was already largely digitised In most richcountries the cash that people carry in their wallets represents only a tinyfraction of their assets and is used for only a small portion of their spend-ing The rest exists only in the pattern of magnetic charges and ickeringelectronic impulses of banksrsquo data centres

Moreover banking is something few people enjoy If oered an al-ternative to queuing up in a branch to get served surely customerswould take it up avidly After all large numbers of bookshops and musicstores have already closed as people have taken to buying online eventhough browsing in such places was rather fun Going to the bank is notmuch fun All the more reason to do your banking from your armchair

Yet except in a very few rich countries there are 10-20 more bankstoday on main streets the world over than there were a decade ago In-

Retail renaissance

The internet and mobile phones are at long last turning boring old

retail banking into an exciting industry says Jonathan Rosenthal

A C K N O W L E D G M E N T S

CONTENT S

This special report beneted from

the time and insight of many people

in addition to those mentioned in

the text The author would like to

thank in particular Sebastian

Arcuri Jan Bellens Roelof Botha

Louisa Cheang Sylvia Coutinho

Douglas Flint Noel Gordon Greg

Hinston Ed McLaughlin Tim

Murphy Gloria Ortiz Portero Narciso

Perales Emmanuel Pitsilis Simon

Samuels Michael Shepherd Antonio

Simoes Tim Sloan Paul Thurston

Huw van Steenis Mark Weil and

others who wished to remain

anonymous

3 Branches

Withering away

6 Spain

Dispatches from the hothouse

7 Big data

Crunching thenumbers

10 Mobile payments

A wealth of wallets

13 Remittances

Over the sea andfar away

14 Wealth

management

Private pursuits

17 Winners and losers

World here we come

SPECIAL REPORT

INTERNATIONAL BANKING

The Economist May 19th 2012 1

A list of sources is at

Economistcomspecialreports

An audio interview with

the author is at

Economistcomaudiovideo

specialreports

2 The Economist May 19th 2012

INTERNATIONAL BANKING

SPECIAL REPORT

2 stead of superseding banks the internet has simply made them alittle more convenient Conventional banks have added internetbanking mobile banking and even video banking to their oer-ing Yet all the while they have expanded their branch networks

In retrospect the years in the run-up to the nancial crisiswere a golden age for banks Even the dullest of them could earnhigh returns by taking big risks And few really bothered to try tocut costs when their revenues were being massively boosted bya debt-fuelled bubble Since the mid-1990s Europersquos big retailbanks have managed to cut their costs relative to income by anaverage of just 03 a year reckons Simon Samuels an invest-ment analyst at Barclays Yet even that modest gure atters thebanks He calculates that costs over the period increased by anaverage of 8 a year The only thing that saved them was that rev-enues increased a little faster

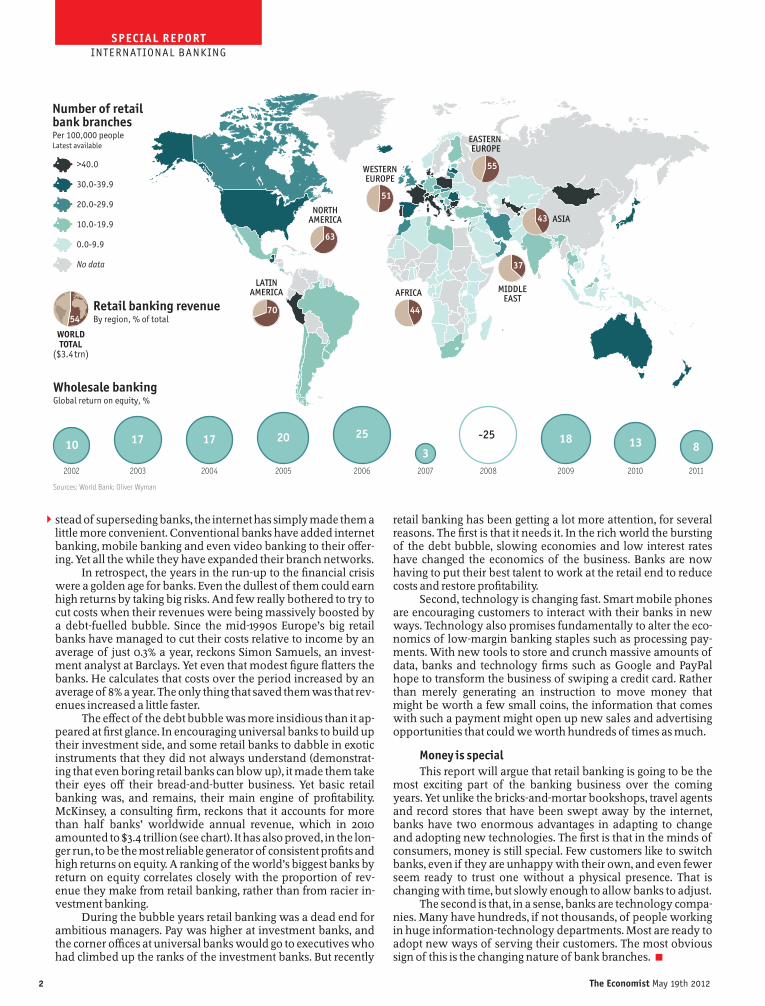

The eect of the debt bubble was more insidious than it ap-peared at rst glance In encouraging universal banks to build uptheir investment side and some retail banks to dabble in exoticinstruments that they did not always understand (demonstrat-ing that even boring retail banks can blow up) it made them taketheir eyes o their bread-and-butter business Yet basic retailbanking was and remains their main engine of protabilityMcKinsey a consulting rm reckons that it accounts for morethan half banksrsquo worldwide annual revenue which in 2010amounted to $34 trillion (see chart) It has also proved in the lon-ger run to be the most reliable generator of consistent prots andhigh returns on equity A ranking of the worldrsquos biggest banks byreturn on equity correlates closely with the proportion of rev-enue they make from retail banking rather than from racier in-vestment banking

During the bubble years retail banking was a dead end forambitious managers Pay was higher at investment banks andthe corner oces at universal banks would go to executives whohad climbed up the ranks of the investment banks But recently

retail banking has been getting a lot more attention for severalreasons The rst is that it needs it In the rich world the burstingof the debt bubble slowing economies and low interest rateshave changed the economics of the business Banks are nowhaving to put their best talent to work at the retail end to reducecosts and restore protability

Second technology is changing fast Smart mobile phonesare encouraging customers to interact with their banks in newways Technology also promises fundamentally to alter the eco-nomics of low-margin banking staples such as processing pay-ments With new tools to store and crunch massive amounts ofdata banks and technology rms such as Google and PayPalhope to transform the business of swiping a credit card Ratherthan merely generating an instruction to move money thatmight be worth a few small coins the information that comeswith such a payment might open up new sales and advertisingopportunities that could we worth hundreds of times as much

Money is special

This report will argue that retail banking is going to be themost exciting part of the banking business over the comingyears Yet unlike the bricks-and-mortar bookshops travel agentsand record stores that have been swept away by the internetbanks have two enormous advantages in adapting to changeand adopting new technologies The rst is that in the minds ofconsumers money is still special Few customers like to switchbanks even if they are unhappy with their own and even fewerseem ready to trust one without a physical presence That ischanging with time but slowly enough to allow banks to adjust

The second is that in a sense banks are technology compa-nies Many have hundreds if not thousands of people workingin huge information-technology departments Most are ready toadopt new ways of serving their customers The most obvioussign of this is the changing nature of bank branches 7

Sources World Bank Oliver Wyman

51

55

43

37

447054

63

No data

00-99

100-199

200-299

300-399

gt400

WORLDTOTAL

($34 trn)

ASIA

MIDDLEEAST

EASTERN EUROPE

WESTERNEUROPE

AFRICALATIN

AMERICA

NORTHAMERICA

Number of retailbank branchesPer 100000 peopleLatest available

Retail banking revenueBy region of total

Wholesale bankingGlobal return on equity

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

310 17 17 20 25 -25 18 13 8

The Economist May 19th 2012 3

SPECIAL REPORT

INTERNATIONAL BANKING

1

A HUGE GLOWING wall blinks blue and red at the torrentof commuters as they ow up the escalators and into the

halls of Orchard Road station one of the busiest on Singaporersquostransit system As they pass the wall it spews out useful informa-tion the weather the latest news headlines movements in themarkets Behind all this are the changing advertisements for Ci-tigrouprsquos latest deals on oer right by the concourse This is abold attempt to entice customers into a branch that looks noth-ing like a bank there are no doors to keep robbers out no coun-ters to shelter cashiers Instead there are massive touch-screentelevisions on the outside walls and gleaming white bencheswith tidy rows of Apple computers Neatly dressed assistantsbrandish iPads with smart black leather covers

With a few taps on the iPad Han Kwee Juan Citibankrsquosboss in Singapore shows how a customer spending a few thou-sand Singaporean dollars a month on a Citibank credit cardcould earn thousands a year back in rebates discounts and otherrewards How about consolidating credit-card debts into a perso-nal loan The saving could be more than S$600 a year he says

This branch is worth close examination because togetherwith its siblings along Singaporersquos transit lines it reects a radicalchange in the way that Citi (and a growing number of other bigbanks) thinks about its large network of branches For decadesthose branches were seen mainly as places where customerscame to deposit or withdraw money More recently some peopleassumed that they would be swept away by the internet and oth-er waves of innovation Ten years ago the consultants said to usthat we had to scrap our branches and go straight to the internet

says Alfredo Saacuteenz the chief executive of Santander a big Span-ish bank But I had heard those kinds of statements before withthe credit cards and ATMsIrsquom old enough to remember

Branches were seen to be under threat because they are ex-pensive They usually occupy a prominent corner in a pricey partof town and they cost a lot to man Because they get robbed ev-ery now and then even the smallest will usually have at leastfour people on site at all times even though three of them mayhave nothing much to do For most big retail banks rentingequipping and stang branches can easily account for 40-60of their total operating costs with computer systems making upmost of the rest

Despite the predictions of the death of branch banking inmost countries the number of branches has increased over thepast decade In America which is still the worldrsquos richest bank-ing market the number of branches and oces has risen by 22since 2000 to almost 90000 In Europe too the number of bankbranches has increased steadily over the decade rather toomuch so in Spain and Italy Spain for instance has some 43000

branches about half as many as the whole of America a coun-try with almost seven times as many people and a land mass 20times larger than Spainrsquos

Branches continue to thrive because people still think thatmoney is special and want reassurance that their cash is safeLocation is still the rst and most important decision-makerwhen you choose your branch says John Stumpf chairmanand chief executive of Wells Fargo an American bank Afterthat you might bank online you might not go back to visit thatbank againbut that location is where you think your moneyis Baudouin Prot the chairman of BNP Paribas a French bankreckons that most of the customers still want a branch some-where nearbyyou still need a shop around the corner AndRob Markey of Bain a consultancy thinks that people cravephysical interactions with human beings in the branch to makethem feel that their money is well looked after

Intriguingly it seems that where a bank has lots ofbranches it attracts more customers JPMorgan Chase Americarsquosbiggest bank opened more than 200 new branches last year andplans to add 150-200 annually over the next ve years Most ofthese will be in areas where it already has a big share of the mar-ket It always has been more valuable to increase your marketshare in an existing market than it is to go to a new market not-ed Jamie Dimon the bankrsquos chairman and chief executive in a

recent letter to shareholders Todd Maclinhead of consumer and business bankingreckons that each new retail branch willearn the bank an average of $1m a year

This simple rulethat the bank withthe greatest branch density in a given mar-ket will win the most customhas denedbanking for generations A study forAmericarsquos Federal Deposit Insurance Cor-poration in 2005 found that banks withbigger branch networks were more suc-cessful at increasing revenues and moreprotable than those with smaller net-works Having a dense branch networknot only helps banks gain a large share ofthe market it also allows them to charge abit more for loans or pay a slightly lowerrate of interest Until now branches havebeen expensive but highly ecient bill-boards says Peter Carroll of Oliver Wy-man a consulting rm

Despite all the innovation and newtechnology that has gone into banks in recent decades the basicdrivers of retail banking have remained much the same over thepast 100 years But that is about to change for three reasons

This time is dierent

The rst is economic Since the nancial crisis the protabil-ity of retail banking in many rich countries has plummeted be-cause of rock-bottom interest rates and tangled regulation Insome places such as America and Britain new regulations havealso slashed the fees banks can charge Banks everywhere haveto hold much more capital In America retail banks have tradi-tionally made about half their prots from gathering cheap de-posits in cheque accounts on which they pay no interest andthen lend out at a prot Yet with ocial interest rates close tozero lending rates have slumped squeezing margins

The other big sources of income were fees and charges onoverdrafts late payments on credit cards and fees charged to re-tailers when customers use their debit cards New regulations in-troduced as part of the Dodd-Frank act in America outlaw some

Branches

Withering away

Bank branches hitherto all-important will become

far less numerousand look very dierent

A simple rulethat the bank with the greatest branchdensity in a given market will win the most customhasdened banking for generations

4 The Economist May 19th 2012

INTERNATIONAL BANKING

SPECIAL REPORT

2

1

of these charges and cap others Sherief Meleis of Novantas an-other consultancy reckons that thanks to low rates banks areabout $60 billion a year worse o than in 2007 and that newrules are trimming their revenues by another $15 billion or soWith such a steep drop in income about 15 of the currentbranch network tips over into unprotability he says

In Europe too low interest rates are having a very signi-cant impact on retail banks says Pedro Rodeia of McKinsey Hereckons that on average big European retail banks are currentlylosing money on about half their customersrsquo accounts For somebanks the ratio is even higher Until now why would you closebranches There wasnrsquot the nancial imperative says MichaelPoulos of Oliver Wyman This time it really is dierentyouwill see people closing a signicant number of branches Thepotential savings are large European banks could probably cuttheir costs by some 15 billion-20 billion a year by getting cus-tomers to do more banking online according to McKinsey

Give me a buzz

As it happens customers are already turning to both the in-ternet and their phones for banking without much promptingThe widespread adoption of the smartphone is proving to be therst big innovation in banking that is actually causing people tomake fewer visits to bank branches Earlier waves of innovationsuch as ATMs and telephone banking promised to reduce thefrequency of visits but turned out merely to increase the numberof transactions by making it more convenient to withdraw mon-ey say or to check a balance

Smartphones and tablets by contrast are radically chang-ing bank customersrsquo behaviour causing them to visit theirbranch far less often but sharply to in-crease the number of transactions withtheir bank When banks rst introducedvery basic mobile-banking systems thatallowed customers to check their balanceby text message interactions went upfrom an average of nine to 20 a monthsays CeCe Morken of Intuit a maker ofpersonal-nance software used by con-sumers and banks When banks started toproduce banking applications for smart-phones with touch-screens we gotshocked because engagement went upinto the 30s says Ms Morken Whatmakes smartphones so convenient is thatthey allow customers to go online almostanywhere and at any time of day Manynow pay bills or send money to familymembers abroad over their phones whilethey are away from home perhaps com-muting to work

For banks the most immediate bene-t of smartphones is likely to be thechance to automate transactions such asdepositing cheques which are still mostlypaper-based and therefore expensiveThis is particularly important in Americawhere cheques still account for about aquarter of all non-cash payments Mostbig American banks have introduced ap-plications (apps) that let customers pho-tograph cheques as a way of depositingthem cutting down on millions of branchvisits The customers seem to love themJPMorgan says that over the past year cus-

tomers deposited 10m cheques by taking pictures of them(though that is still only a tiny proportion of the 25 billioncheques handled by American banks each year) Further aheadphones will displace cheques entirely as it will become possibleto send money from one phone to another and small businesseswill accept card payments over their mobile phones

The third big trend is that people are becoming used to do-ing complicated things such as buying airline tickets or ling taxreturns online The main drivers of this are often industries otherthan banking Sometimes it is even the state In Denmark for in-stance the government oversees the issue of digital identity cer-ticates which can be used on both government websites andfor online banking Whatever the agent of change it seems clearthat as people become more comfortable online in other areas oflife they also seem willing to do more of their banking on the in-ternet Matthew Sebag-Monteore of Oliver Wyman cites a Dan-ish banker who got an online divorce using the Danish govern-mentrsquos website When you are comfortable divorcing onlinebanking is easy says Mr Sebag-Monteore Banking in short isbecoming less special

In America transactions conducted in bank branches arenow falling by about 5 a year says Mr Meleis of Novantas InAsia the trend is even clearer McKinsey reckons that branch vis-its across the region have fallen for the rst time since it startedcollecting data 13 years ago In the Netherlands only half of allbank customers have stepped inside a branch in the past yearMore than 80 use the internet for banking

Bradesco one of Brazilrsquos biggest banks has been an enthu-siastic early adopter of new technologies It was one of the rstbanks in the world to oer internet banking starting in 1996 and

SPECIAL REPORT

INTERNATIONAL BANKING

2 it remains at the forefront of innovation Its ATM machines havebiometric sensors that can recognise customersrsquo palms to savethe need to remember PIN numbers (the machines also checkthat the blood is owing to forestall macabre robberies) Thebank also oers loans by iPhone It reckons that the cost of han-dling a customer transaction via an automated telephone sys-tem is just 6 of what it would be in a branch Some 93 of all ofits customer transactions are now self-service

Technology for us is almost everything says DomingosFigueiredo de Abreu Bradescorsquos vice-president Even so thebank has recently opened 1000 new branches many in poorerparts of the country These include a bank on a boat that travelsup and down the Amazonrsquos tributaries allowing people to openaccounts and borrow money

Coee and iPads

The conundrum facing Bradesco and most other banks theworld over is that even as their customers make less use ofbranches for everyday transactions the banks have yet to nd anequally good way of drawing in new customers and doing morelucrative business with existing ones Our goal is still to ll thebranches with customers says Lukas Gaumlhwiler who runs theSwiss banking business of UBS Every conversation (in abranch) is a potential advice and sales opportunity So insteadof doing away with branches banks are trying to reinvent themMany of their experiments seem to involve coee and iPads andthe word branch is rarely used

In the middle of Paris the ornate iron and glass doors ofBNP Paribasrsquos agship concept store look out directly onto theOpeacutera Away from the chandeliers and down a carpeted corridor

you will nd bright red green and yellow beanbags more whitebenches with iPads and rooms with couches and at-screen tele-visions Here we are in the lounge says Nathalie Martin-San-chez who oversaw the creation of the branch The customercan see an adviser while having a coeeit is designed to en-courage more proximity more interaction more personal con-tact This is a laboratory where the bank can test ideas such asgetting customers and their nancial advisers to sit side by sideor letting customers speak to specialists on a video link

Online banks meanwhile are trying to build a physical in-frastructure to supplement their online oering The new brightorange ING Direct Cafeacute near San Franciscorsquos Union Squareserves coee from Peetrsquos a speciality Californian coee roasterand freshly made snacks at reasonable prices But as well as ask-ing how you want your latte the baristas also inquire politely ifyou would like to talk about money or open a savings accountTo reinforce the sense that this is not a bank there is a rule againsttransactions If you try to deposit a cheque you will be given anenvelope to post it to a processing centre

Whereas banks in the rich world are trying to make theirbranches more like shops or cafeacutes retailers in emerging marketslook set to leapfrog them by turning shops into banks In Brazilone of the countryrsquos fastest-growing providers of small loans isMagazine Luiza Its main business is selling home appliancesand electronics through stores and online catalogues Yet it alsonances three-quarters of its customersrsquo purchases and collectspayments on their loans from its network of more than 600shops Unlike banks which want their customers to visit theirbranches as little as possible Magazine Luiza encourages its cus-tomers to come in to pay their monthly bills in cash because it

gives them an opportunity to sell more tothem I cannot really tell you if we are apure retailer or a nancial company saysFrederico Trajano-Vendas the rmrsquos salesand marketing manager We are a mix-ture of the two

But the new branches that are gettingthe most attention (and it seems custom)are Citigrouprsquos The resemblance of itsbranches to Applersquos iconic stores is morethan passing When Citigroup decided tobuild its new network in Singapore ithired Eight Inc the rm that had designedApplersquos stores The bankrsquos experiment inSingapore marked an attempt to scale upquickly in a sophisticated and competitivemarket Its 26 branches have gone up insome of the busiest parts of the island andhave won an outsized share of businessThe bank is now replicating its Singaporestrategy in Hong Kong where it hasopened a huge agship branch in a formerclothes shop in Mong Kok Wersquore ndingthat if you have one of those branches it isworth ten ordinary ones says JonathanLarsen Citigrouprsquos head of retail and busi-ness banking for Asia

Branches are unlikely to disappearbut there will be far fewer of them andthey will look quite dierent from the cur-rent model They will also be far more e-ciently run It is the worldrsquos most over-banked country Spain that oers some ofthe most interesting lessons as to how thatwill be done 7

Theconundrumfacing mostbanks theworld over is that evenas theircustomersmake lessuse ofbranchesthe bankshave yetto nd anequallygood wayof drawingin newcustomers

The Economist May 19th 2012 5

6 The Economist May 19th 2012

INTERNATIONAL BANKING

SPECIAL REPORT

BETWEEN A RANGE of arid hills and the encroaching me-tropolis of Madrid stands an oasis with hundreds of an-

cient olive trees dotted all over it A cluster of bright modernbuildings sits alongside a green golf course in a valley Overlook-ing all this is a building one oor taller than the others with abright silver dome under which the chairman has his oce Thisserene campus is home to Santander and in some ways the Goo-gleplex of banking Two huge data centreslow and built like nu-clear-bomb sheltersprovide some of the computer networks tosupport a far-ung banking empire (Brazilrsquos on this one Britainon the other says a guide) The idea behind them is that compet-itive advantage in banking comes from rig-orously standardising computer systemsand procedures around the world and re-lentlessly driving down costs Our busi-ness model is extremely consistent every-where says Mr Saacuteenz Santanderrsquos bossWe have the same systems everywhereExactly the same systems

Spainrsquos two biggest banks Santan-der and BBVA have been expanding theirretail operations abroad rapidly in recentdecades and have managed to do so prof-itably even though their own countryrsquoseconomy is melting down around themSantander which a few decades ago wasjust a small regional bank now has sub-

stantial businesses in ten countries around the world Almost90 of its prots are made outside Spain BBVA its biggest Span-ish rival has also expanded vigorously outside Spain Betweenthem the two banks manage more than 20000 bank branchesmost of them outside Spain Spainrsquos biggest export is the man-agement of bank branches quips one Spanish banker

Spain is arguably the worldrsquos most competitive bankingmarket Thanks to its ercely independent regions it has a re-markable number of banks for its size Even more remarkable isthe number of branches some 43000 which works out at onebranch for every 1000 people or about six times the number inBritain and more than twice as many as in France and AmericaWith too many players you end up overbanked because everybank wants to be everywhere says Pedro Rodeia at McKinseyThis keen competition pushed some smaller banks to lend reck-lessly causing a banking crisis that blew up the economy Yet italso forced banks to squeeze out costs which at Santander andBBVA account for less than 50 cents of every euro they earn de-spite their huge branch networks Most large retail banks in othercountries would be happy with anything below 60 cents

Spanish banks embraced modernisation relatively lateHaving been trapped in a bubble for many years during the fas-cist dictatorship once they were freed they were able to leapfrogrivals in more developed markets The most important innova-tion was the rapid and almost universal adoption by bank cus-tomers of electronic bill payments Spainrsquos banks have a hugeadvantage in not having to process cheques or handle transac-tions in their branches They have invested diligently in install-ing the latest and most eective computer systems making theirbanks enviably ecient Their rapid growth and the economictroubles at home raise some question marks Even so they havedeveloped an innovative model of banking that is being export-ed around the world It may also hold some clues about whatbanks elsewhere may soon be doing

Joined-up banking

In a branch in downtown Madrid of Banesto a bank that isowned by Santander a branch manager pulls up a series ofscreens on her computer One shows all the balances of a cus-tomer at the branch At a glance she can see whether the custom-er is protable which of her sta is responsible for looking after

him and what other banking services hemight need To non-bankers it seems in-conceivable that banks may not have acomplete overview of the business theyare doing with each of their customersYet only a handful of the worldrsquos bigbanks are able to see instantly that a cus-tomer asking for a credit card may alreadyhave a savings account with them

Spainrsquos banks go a step further Withanother few clicks of a mouse the branchmanager can see whether the branch it-self is protable She assembles her staeach morning to discuss which customersmay need to be contacted perhaps be-cause they have missed a loan repaymentor received an unusually large deposit

The Spanish model is not just aboutusing technology to drive down costs andpush up employeesrsquo productivity It alsoallows very small branches to oer so-phisticated advice and customer service

Across town Bankinter a small buttech-savvy bank takes this idea a step fur-

ther Just inside the bankrsquos entrance is a large computer screenwith a camera and a phone If customers need specialist adviceon a mortgage say and no one can see them they are connectedby video call with a free adviser in another branch As custom-ers use more channels they become more loyal buy more pro-ducts and are more satisedand that makes good businessnotes Accenture a consulting rm With a cross-sell ratio aheadof many of their Spanish peers Bankinterrsquos customer relation-ships are also more protable

The nal element of the Spanish banksrsquo formula is to con-centrate on markets where they can achieve a signicant shareThey would rather be deep in a few markets than thinly spreadover many BBVA for instance tried its hand in Brazil but found itcould not reach critical mass Santander sold its rst investmentsin the United States to raise the capital to bulk up in Brazil al-though it has since returned The Spanish model has been asmuch about banks being local in their main markets as about be-ing international Yet technology is changing the economies ofscale involved in banking particularly as banks try to prot fromthe vast amounts of data they collect on their customers 7

Spain

Dispatches from the hothouse

Lessons from the worldrsquos most competitive banking

market

Having been trapped in a bubble during the fascistdictatorship once they were freed Spanish banks wereable to leapfrog rivals in more developed markets

The Economist May 19th 2012 7

SPECIAL REPORT

INTERNATIONAL BANKING

1

A BIG BANK hires a star analyst from another rm promis-ing to pay a substantial bonus if the new hire increases rev-

enue or cuts costs In banking this happens all the time but thisdeal diers from the rest in one small detail the new hire Wat-son is an IBM computer

Watson became something of a celebrity after beating thechampion human contestants on Jeopardy an American quizshow Its skill is to be able to process millions of documentsquickly by reading and understanding ordinary written lan-guage Computers have no trouble with searching data neatlysorted in databases Watsonrsquos claim to fame is that it can do thesame with unstructured data such as those found in e-mailsnews reports books and websites IBM hopes that Watson mayin time do some of the work that human analysts do now suchas reading the nancial pages of newspapers looking at thou-sands of company results and forecasts and producing a list ofcompanies that might be takeover targets soon

Citigroup has hired Watson to help it decide what new pro-ducts and services (such as loans or credit cards) to oer its cus-tomers The bank doesnrsquot say so but Watsonrsquos rst job may wellbe to try to cut down on fraud and look for signs of customers be-coming less creditworthy If so Watson will be following othercomputers designed to deal with big data Across a slew ofnew rms in Silicon Valley and in big banks across the world arange of new ideas is being tried to crunch data Some have thepotential to change banking from the bottom up

In most nancial institutions the immediate use of big datais in containing fraud and complying with rules on money-laun-dering and sanctions Even seemingly simple tasks such aschecking the names of clients against those on a sanctions black-list become immensely complicated in the real world wherebanks may have thousands of customers with the same namesas those on the blacklist Each becomes a false positive that mayembarrass the bank and ruin a client relationship So banks havehad to turn to computers that can amass data from a variety ofdierent sources including the customerrsquos nationality and ad-

dress the names of family members and whether they havetravelled to or received money from countries on sanctions lists

When moving on to more complex tasks such as identify-ing the tiny percentage of fraudulent transactions among themillions of legitimate ones the demands become ever greaterThe problem is getting bigger because as banking has movedonto computers and mobile phones and payments have shiftedfrom cash to cards or electronic transfers the opportunities forfraud have proliferated

The danger of fraud is particularly acute in areas such ascard payments and some of the more innovative kinds of mon-ey transfers that are oering cheaper or more convenient ser-vices than those already available PayPal which dominates on-line payments barely survived its rst year in business after itcame under sustained attack from fraudsters and several of itsearly rivals were cleaned out and had to close down

PayPal came up with Igor a computer system named after aRussian thief and hacker who had opened fake accounts andtaunted the rmrsquos security team in e-mails Igor would look forpatterns such as a concentration of payments close to the toplimit and their destinations and then compare those paymentswith all the others in the system What started at PayPal soonspread to the rest of banking and beyond it

A better kind of crystal ball

The rm that has perhaps gone furthest in nding usefulconnections in disparate databases is Palantir Technologieswhich takes its name from the magical all-seeing crystal balls ofJRR Tolkienrsquos mythology It was founded by a group of PayPalalumni and backed by Peter Thiel one of PayPalrsquos co-foundersIts speciality is building systems that pull together informationfrom dierent places and try to nd connections Some of its ear-liest adopters have been spy agencies In America the CIA andthe FBI use it to connect individually innocuous activities suchas taking ying lessons and receiving money from abroad to spotpotential terrorists Its other main market is in banking wherebig rms such as JPMorgan and Citi use it for a range of activitiesfrom structuring equity derivatives to reducing loan losses

A stablemate of sorts to Palantir is Xoom a rm that spe-cialises in cross-border remittances It is backed by some of Pa-lantirrsquos investors and has swapped a senior employee with it butmore importantly it shares Palantirrsquos belief that given enoughdata even the toughest risks can be managed Xoom accepts pay-ments from bank accounts or debit cards in America then handsover cash in countries such as the Philippines or India It does nothave much time to nd out if it has been swindled on a paymentbefore it has to produce the cash So it has devised a sophisticat-ed computer system that analyses a range of data the nature ofmost of which it will not disclose

Some of these checks may seem obvious but some are noteasy to do when processing millions of transactions and movingbillions of dollars Moreover few of these pieces of informationon their own are powerful enough signals for Xoom to decline oragree to make a payment Yet when the computer looks at all ofthe payments in its system it is remarkably good at weaving to-gether the bits of information to spot fraud

It also learns as it goes When it recently noticed a string ofpayments funded by Discover credit cards and originating inNew Jersey its algorithms raised a red ag even though each pay-ment looked legitimate It saw a pattern when there shouldnrsquothave been a pattern says John Kunze Xoomrsquos chief executiveThe pattern it found turned out to have been an eort by a crimi-nal gang to defraud the rm

The other big users of fraud-ghting computers are credit-card associations such as Visa and MasterCard Their systems as

Big data

Crunching the numbers

Banks know a lot about their customers That

information may be valuable in more ways than one

Open wide

Source IDC 1 zettabyte=1 trillion gigabytes daggerForecast

Global digital information Zettabytes

0

5

10

15

20

25

30

35

2005 2010 2015 2020

Created Storage available

F O R E C A S TESTIMATE

1

2005 013

2020dagger 346

8 The Economist May 19th 2012

INTERNATIONAL BANKING

SPECIAL REPORT

2

1

well as those of big card issuers such as Capital One look at vastnumbers of transactions for unusual patterns or connectionsThis has allowed them to graduate from simple rules-basedfraud detection (such as whether a credit card has been swipedin locations a long way apart in a short space of time) to morecomplex sorts

None of these systems is cheap but they are usually a lotcheaper than falling victim to fraud Xoom puts its losses throughfraud at 035 of the sums transferred The average for credit-cardrms is about 01 and the best achieve rates of about half ofthat says Mike Gordon of FICO the company that inventedcredit-scoring and now also supplies fraud-detection softwareLosses on cashed cheques in America run to about 1 a year Forcompanies selling goods online loss rates are considerably high-er CyberSource an electronic-payment and risk-services com-pany says that online retailers in Britain reckoned on losses of18 of revenue last year

The high cost of ghting card fraud has changed the balanceof competition in banking weakening smaller banks that lackthe scale to build the necessary systems Many closed or soldtheir own credit-card businesses and instead signed their cus-tomers up to cards issued by large specialists such as MBNA orCapital One Many smaller banks now think this was a mistakedepriving them not only of an important source of revenue butalso of the opportunity to form the deeper and more lasting rela-tionship with their customers that comes from selling them sev-eral nancial products Most important of all perhaps it has de-prived them of a rich source of data on their customersrsquospending patterns

That may soon change for two reasons The rst is that card

associations such as Visa and MasterCard are getting better atspotting fraudulent transactions as they pass through the net-work relieving the burden on smaller banks says FICOrsquos MrGordon The main strength of these network-level systems isthat they are able to look at far more transactions than any singlebank could which helps them to spot fraud patterns on an inter-national scale

Second the systems used to crunch data are becomingcommoditised and their price is coming down Thomson Reu-ters reckons that last year venture rms invested a total of $247billion in companies that want to crunch big data Much of thisinvestment was in database and storage outts that are not spe-cic to banks yet the tools being developed elsewhere are quick-ly spreading Whereas a decade ago the big banks would get theirsystems custom-made at huge cost smaller banks can now buysimilar ones o the shelf at a small fraction of the price

Bankinter the tech-savvy small Spanish bank last yearstarted using a system to analyse complex loan portfolios oncomputers run by Amazon an online retailer Cloud computingenables it to hire massive number-crunching capacity wheneverit needs it These two factors are making it easier for smallerbanks the world over to keep their credit-card businesses tothemselves and lean against the powerful forces for more andmore consolidation in banking

Panning for gold

As the ability to process large amounts of data becomesubiquitous banks are discovering that it is good for far more thanghting fraud These data also contain hidden nuggets of gold

One way of using them is to try to sell customers more pro-ducts Santander sends out weekly lists toits branches of customers who it thinksmay be interested in particular oers fromthe bank such as home insurance Someof the products banks are oering are noteven nancial In Singapore Citigroupkeeps an eye on customersrsquo card transac-tions for opportunities to oer them dis-counts in stores and restaurants Citi hasmore than 250 people in Asia working ondata analysis Last year it opened a newinnovation lab in Singapore that bringstogether those data analysts with big insti-tutional customers and a large analyticscentre in Bangalore

If a customer who has signed up forthis service swipes a credit card the sys-tem can look at the time of day the loca-tion and the customerrsquos previous shop-ping or eating habits If it nds that heenjoys Italian food it is almost lunchtimeand there is a nearby trattoria it can send atext message oering a discount at the res-taurant That may give the bank a secondtransaction and a cut of the extra spend-ing What makes the system even creepieris its ability to nd out what proportion ofcustomers take up such oers so it cancontinuously learn to improve them Themodel for this is Amazonrsquos online storewhich recommends items that a customermight like based not only on what he hasbought previously but also on what simi-lar customers have bought

McKinsey reckons that some banks

INTERNATIONAL BANKING

have been able to double the share of customers that accept of-fers of loans and reduce loan losses by a quarter simply by usingdata they already have Card networks and other retailers arealso getting in on this business In America Visa has teamed upwith Gap a clothes retailer to send discount oers to cardhold-ers who swipe their cards near Gaprsquos stores Yet in peering so ob-viously into peoplersquos spending habits banks run a risk of spook-ing their customers and running foul of privacy advocatesTarget an American retailer received unwelcome attention earli-er this year when it reportedly discovered from a teenage girlrsquosshopping patterns that she was pregnant and mailed her baby-related couponsbefore she had told her father

A less controversial way of using the data banks hold is todraw on them to oer something genuinely useful to their cus-tomers Britainrsquos Lloyds Banking Group is thinking of tweakingits systems to tell customers not just how much money is in their

accounts when they ask for a balance but also how much theywill have available once all their usual bills are paid We havedeep and rich information about customers that we can use togive them better insights rather than just providing us with bet-ter insight to improve our risk management says Alison Brit-tain head of consumer banking at Lloyds

Yet even as big data are helping banks they are also throw-ing up new competitors from outside the industry One such rmis ZestCash which provides loans to people with bad or no cred-it histories It was started by Douglas Merrill a former chief infor-mation ocer and head of engineering at Google The big dier-ence between ZestCash and most banks is the sheer quantity ofdata that the rm crunches Whereas most American banks rely

on FICO credit scores thought to be based on 15-20 variablessuch as the proportion of credit that is used and whether pay-ments have been missed ZestCash looks at thousands of indica-tors If a customer calls to say he will miss a payment mostbanks would see this as a signal that he is a high risk But Zest-Cash has found that such customers are in fact more likely to re-pay in full Another useful signal is the length of time customersspend on ZestCashrsquos website before applying for a loan Everybit of data is noise but when you add enough of them togetherin a clever enough way you can make sense of the garbage MrMerrill said at a recent conference

ZestCashrsquos customers are not typical bank customers be-cause of their poor credit histories Most would normally usepayday lenders Mr Merrill says his rmrsquos interest rates are abouta third of those charged by many payday lenders (although stillan eye-popping 300 or so) and that it is achieving defaults of

well under half the payday industryrsquos av-erage of 40

Wonga a British start-up that oersloans for very short periods also looks at aplethora of dierent data sources such ase-mail-address and social-network sitesto make credit decisions on the y Anoth-

er rm Cigni digs deep into mobile-phone records crunchingvariables such as the time when calls were made their frequen-cy and the whereabouts of the callers for clues about their pro-pensity to repay loans (Disclosure Jonathan Hakim the presi-dent and CEO of Cigni used to work for this newspaper)Banks have to keep up in this arms race says Thomas Achhor-ner of the Boston Consulting Group They have to make surethey know at least as much about their own customers as anythird party could know

Tesco a large British retailer collects enormous amounts ofdata on its customersrsquo shopping habits that allow it to send pre-cisely targeted coupons When a household starts buying nap-pies signalling the arrival of a new baby Tesco usually sends dis-

Even as big data are helping banks they are alsothrowing up new competitors from outside the industry

2

The Economist May 19th 2012 9

1

SPECIAL REPORT

1

TURN LEFT OFF the main reception to PayPalrsquos oces inSan Jose open a nondescript door and you step into a

garish living room dominated by a at-screen television This is alaboratory for what PayPal calls couch commerce people sit infront of the television buying things with their mobile phones ortablet computers Next door is a make-believe shopping mallcomplete with a mock hardware store grocery and coee shopIn each consumers can order buy and pay for things using theirphones or even just their phone numbers

The virtual mall and living room are exercise grounds forthe next big battle in banking over who will control the new dig-ital wallets that will change the way in which people shop andspendand by implication the way they save and borrow

On the face of it the business of facilitating paymentsseems a particularly unpromising one for start-ups to enter Mosttransfers of money run down a few main highways that linkbanks to one another They carry huge volumes of trac and aregenerally strictly regulated They move quadrillions a day andtake just a few crumbs says Simon Bailey a payments expert atLogica a consulting rm To consumers most payments appearto be free because they are given away by banks as part of a bun-dle of banking services that some customers subsidise throughlow interest rates on deposits

Yet payments turn out to be a battleground between banksand a slew of innovators trying to disrupt the market Many ofthese rms have relatively humble ambitions Some are trying tograb thimblefuls of the huge ows of money that wash aroundthe world by concentrating on particular areas such as cross-bor-der payments (see next article) Yet they nd themselves gettingever closer to oering bank-like services without having to bebanks themselves

There has been massive growth in supplying payments ser-vices to tradesmen such as plumbers or ea-market stallholderswhich until recently could accept payment only in cash or bycheque Yet cheques are bouncy and although cash has its attrac-

Mobile payments

A wealth of wallets

Digital payments pose a serious threat to banks

The way to go

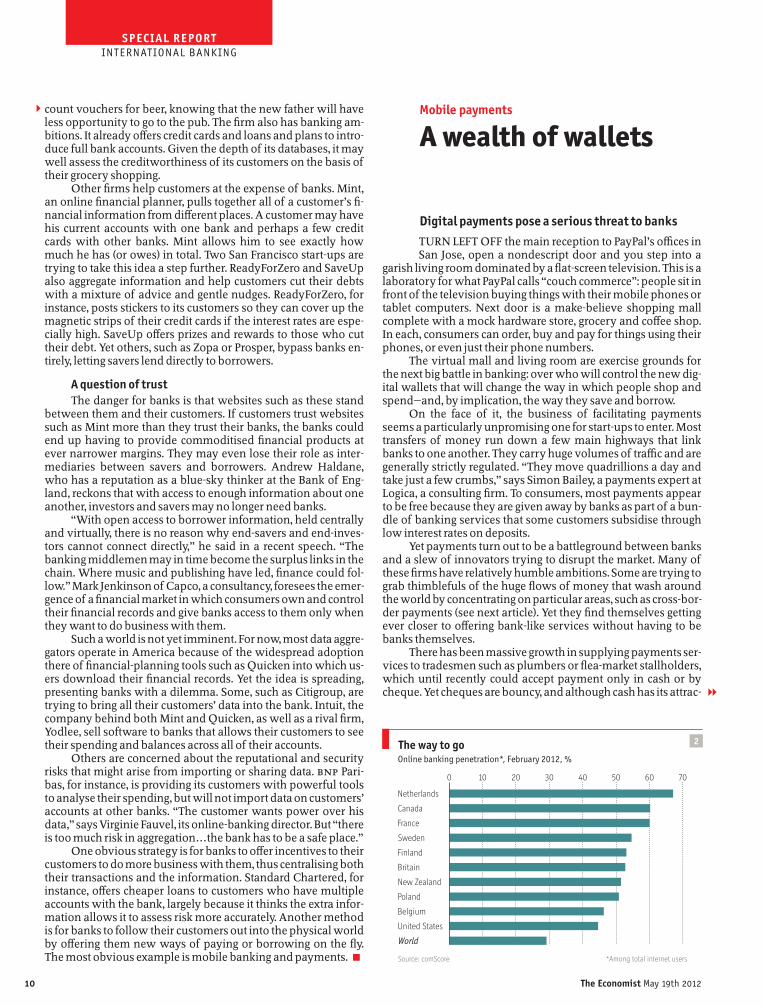

Source comScore

Online banking penetration February 2012

Among total internet users

0 10 20 30 40 50 60 70

Netherlands

Canada

France

Sweden

Finland

Britain

New Zealand

Poland

Belgium

United States

World

2

count vouchers for beer knowing that the new father will haveless opportunity to go to the pub The rm also has banking am-bitions It already oers credit cards and loans and plans to intro-duce full bank accounts Given the depth of its databases it maywell assess the creditworthiness of its customers on the basis oftheir grocery shopping

Other rms help customers at the expense of banks Mintan online nancial planner pulls together all of a customerrsquos -nancial information from dierent places A customer may havehis current accounts with one bank and perhaps a few creditcards with other banks Mint allows him to see exactly howmuch he has (or owes) in total Two San Francisco start-ups aretrying to take this idea a step further ReadyForZero and SaveUpalso aggregate information and help customers cut their debtswith a mixture of advice and gentle nudges ReadyForZero forinstance posts stickers to its customers so they can cover up themagnetic strips of their credit cards if the interest rates are espe-cially high SaveUp oers prizes and rewards to those who cuttheir debt Yet others such as Zopa or Prosper bypass banks en-tirely letting savers lend directly to borrowers

A question of trust

The danger for banks is that websites such as these standbetween them and their customers If customers trust websitessuch as Mint more than they trust their banks the banks couldend up having to provide commoditised nancial products atever narrower margins They may even lose their role as inter-mediaries between savers and borrowers Andrew Haldanewho has a reputation as a blue-sky thinker at the Bank of Eng-land reckons that with access to enough information about oneanother investors and savers may no longer need banks

With open access to borrower information held centrallyand virtually there is no reason why end-savers and end-inves-tors cannot connect directly he said in a recent speech Thebanking middlemen may in time become the surplus links in thechain Where music and publishing have led nance could fol-low Mark Jenkinson of Capco a consultancy foresees the emer-gence of a nancial market in which consumers own and controltheir nancial records and give banks access to them only whenthey want to do business with them

Such a world is not yet imminent For now most data aggre-gators operate in America because of the widespread adoptionthere of nancial-planning tools such as Quicken into which us-ers download their nancial records Yet the idea is spreadingpresenting banks with a dilemma Some such as Citigroup aretrying to bring all their customersrsquo data into the bank Intuit thecompany behind both Mint and Quicken as well as a rival rmYodlee sell software to banks that allows their customers to seetheir spending and balances across all of their accounts

Others are concerned about the reputational and securityrisks that might arise from importing or sharing data BNP Pari-bas for instance is providing its customers with powerful toolsto analyse their spending but will not import data on customersrsquoaccounts at other banks The customer wants power over hisdata says Virginie Fauvel its online-banking director But thereis too much risk in aggregationthe bank has to be a safe place

One obvious strategy is for banks to oer incentives to theircustomers to do more business with them thus centralising boththeir transactions and the information Standard Chartered forinstance oers cheaper loans to customers who have multipleaccounts with the bank largely because it thinks the extra infor-mation allows it to assess risk more accurately Another methodis for banks to follow their customers out into the physical worldby oering them new ways of paying or borrowing on the yThe most obvious example is mobile banking and payments 7

10 The Economist May 19th 2012

SPECIAL REPORT

INTERNATIONAL BANKING

2

3March of the mobile banking parlours

Sources KPCB Morgan Stanley

Device shipments units m

0

100

200

300

400

500

600

700

800

2005 06 07 08 09 10 11 12 13

Smartphones Tablets

F O R E C A S T

Estimate

tionsforemost of which is that it is easily hidden from the tax-mancarrying large amounts of it is risky and customers canspend only as much of it as they have in their wallets

In America two rms Square and Intuit lead this marketwith small devices that attach to smartphones and allow eventhe smallest business or tradesman to accept credit-card pay-ments Both rms oer free card-readers to users and then chargethem a fee of about 27 of the amount that changes hands Bothare growing at a rapid clip Square has signed up more than 1mcustomers since its launch in 2010 Among them is the SalvationArmy which last Christmas started testing the device to acceptdigital donations alongside its traditional red kettles Intuitrsquos Go-Payments which also launched three years ago says the numberof its clients increased by 1200 last year though it will not givean actual number Before this small businesses would havehad to take cheques or lose sales says Chris Hylen the head ofIntuitrsquos payments division

In little over a year Square alone has increased the numberof credit-card readers in America by about a sixth The growth ofboth rms highlights the huge pent-up demand for mobile pay-ments Both reckon that some 26m small businesses and self-employed people in America had wanted to accept card pay-ments but were put o by the cost and the paperwork A tradi-tional card-reader sells for hundreds of dollars with xedmonthly fees on top and applicants have to submit to creditchecks and provide accounts for the previous yearimpossiblefor a start-up

Some big banks sneer at these newcomers arguing that thetechnology involved in adding a card reader to a phone can beeasily replicated In fact the innovation has less to do with thedevice reader than with a business model that has made a hugedierence to costs involved in accepting credit-card payments Itis rapidly overturning a lucrative industry of merchant acquisi-tion that allowed banks to earn wide margins for agreeing toprovide credit-card readers to shops The rst Square device wasbuilt by Jack Dorsey one of the founders of Twitter who found itso simple that he wondered why no one had done it before saysKeith Rabois Squarersquos chief operating ocer They literallymade this thing work in a month he explains It took anotheryear-plus to navigate the nancial-services industry

The success of mobile payments would not have been pos-sible without the massive growth in the number of smartphonesand the falling cost of computing power both of which are low-ering the barriers to new entrants in parts of nance Smart-phones are vital to this because by providing consumers withpowerful computing devices and internet connections that arealways on they open the way to all sorts of other innovations

Square and Intuit can give away their card readers free in part be-cause all the processing power to run them is already on thephones they are plugged into It is a device that can link the on-line and oine worlds says Zilvinas Bareisis an analyst at Ce-lent a consultancy The smartphone gives such a rich experi-ence that we are playing games on it we are tracking stars so it isa natural extension to check your bank account or even make apayment Its use is also spreading fast Nielsen a research rmreckons that by the end of last year almost half of American mo-bile-phone subscribers had smartphones compared with undera fth two years earlier

The two companies whose online-payments experimentsare being watched most closely are Google and PayPal PayPalinitially set itself up as a mobile wallet that would allow peopleto beam money from one Palm Pilot (an early handheld device)to another That idea died pretty quickly when PayPal realisedthat people were not particularly interested in being able tobeam money to someone standing in front of them but that theydid want a safe way to send money over the internet to peoplewho might be complete strangers It is now arguably the worldrsquosbiggest bank with more than 100m account holders It providesa virtual wallet that can be used to pay for online purchases on acomputer at home as well as for things bought in bricks-and-mortar stores on a smartphone The wallet can even be com-pletely dematerialised In shop trials in America customerswere happy to pay at the till by typing in their phone numbersand secret code

PayPal is also padding out its virtual wallet with otherbank-like features such as loans Even after a customer hasbought and already paid for something in a shop PayPal oershim various options for funding the purchase The amountowed can be debited to his current account credit card or debitcard PayPal also oers its own line of credit to customers whowant to borrow money to pay for things they have just bought

A wizard in your pocket

Since customers can link a vast number of dierent ac-counts to their PayPal wallets the system can help them ensurethat they always pay for things in the most cost-eective way Itmight suggest they use a store card when shopping at a particularretailer to maximise the number of loyalty points they accumu-late but propose that they use a dierent card somewhere elseSuch advice poses a serious threat to the banks

Google is for the moment somewhat coy about its walletand insists it is working in partnership with the banks ratherthan trying to supplant them Its wallet allows customers to storebank-issued cards on their phones which they then swipeacross a reader when paying for something Google is interestedin payments because in rich countries more than 90 of allshopping still takes place in real stores rather than online It toothreatens to stand between banks and cardholders

In Europe where the market is more fragmented the ideaof an electronic wallet has been slower to take o iZettle aSwedish rm also oers free card readers and charges a fee simi-lar to Squarersquos and Intuitrsquos It reckons it has already expanded thenumber of merchants able to accept card payments by about 15in Sweden and has recently expanded into Denmark Finlandand Norway

Some emerging markets are leapfrogging rich ones goingstraight to mobile banking from having hardly any banks in ruralareas In Brazil and India banks are also reaching far beyond theirtraditional branch networks by using agents These are oftenshopkeepers in small villages equipped with mobile phonesand card readers Customers can make small deposits with-drawals and money transfers through these agents instead of

2

The Economist May 19th 2012 11

INTERNATIONAL BANKING

SPECIAL REPORT

1

12 The Economist May 19th 2012

INTERNATIONAL BANKING

SPECIAL REPORT

2 visiting faraway branches The poster-child of mobile banking is Kenya where some

14m people now save and send money using M-Pesa a tele-phone-based banking system It allows them to deposit with orwithdraw cash from a network of small agents Similar systemshave also been deployed in places such as Bangladesh UgandaNigeria and the Philippines but with less success

In this rapidly evolving market even relatively young rmsrun the risk of being outpaced themselves by fresh and evenmore disruptive innovations One such very new rm is Stripewhich has attracted investment from some of the original foun-ders of PayPal and is trying to muscle in on PayPalrsquos online mar-ket It wants to make online payments easier to accept for web-site owners than by using PayPal or Google

The agony of choice

There are two big and interrelated questions about howpeople will behave when they start using electronic wallets on alarge scale The rst is whether they will consolidate all theirspending into a single account or spread it even more widelythan they do now The arguments seem nely balanced Thosewho expect spending to be consolidated reckon that when peo-ple are no longer faced with a physical choice they will simplyuse whichever card or account has been set as the default Thosewho think that spending will be spread more widely point outthat phones eliminate the inconvenience of carrying around alot of dierent cards which may prompt some consumers tohave more banking relationships

The second question is whether consumers will use justone electronic wallet on their phones choosing between sayGoogle PayPal and their own bank or whether they will haveseveral Most analysts think that consumers will gravitate to-wards a single electronic wallet which will hold many cardsThis is because there may be signicant benets to be gainedfrom aggregating transactions and the data associated withthem For example PayPalrsquos wallet will allow consumers to usevarious stores of value besides money when paying for goods orservices These could include coupons loyalty points fromstores and banks and air miles from airlines PayPal stands to pro-t from steering customers into shops perhaps by remindingthem that they have unused coupons It could also tell shopkeep-ers about the tastes of their customers allowing retailers to maketargeted shopping oers (this would look great with the blackskirt you bought last week) or extend credit on the y

Google too is hoping to do far more with its wallet thanprocess payments which it sees as akin to queries typed into itssearch engine In the same way that it sells advertisements thatare precisely targeted to a userrsquos search it hopes to be able to de-liver oers matched to peoplersquos spending patterns

Innovations of this sort are forcing big banks and the credit-card networks to respond in kind either by teaming up with theinnovators or building their own competing systems Some aredoing both Citigroup is working with Google at the time ofwriting it is the only bank to have its card in the Google walletIrsquom not sure any of us will carry [physical] wallets ten yearsfrom now says Michelle Peluso the head of marketing and in-ternet banking for Citigrouprsquos consumer business

JPMorgan has built its own network to allow people tomake payments by e-mail using their phones or computers InBritain Barclays recently introduced a similar system Technol-ogy is to some extent disintermediating legacy banks says An-tony Jenkins the head of retail and business banking at BarclaysBut we also see it as a huge opportunity because with our accessto the banking system and our technology we can build these[systems] ourselves 7

The Economist May 19th 2012 13

SPECIAL REPORT

INTERNATIONAL BANKING

1

STANDING JUST INSIDE the entrance to Wells Fargorsquos headoce in San Francisco is a magnicent antique stagecoach

complete with a strongbox and a seat next to the driver for theshotgun messengers who worked for the bank It is a reminderthat in the not-too-distant past one of the main jobs of banks wasto lock money in boxes and move it around the world underguard For companies these days big global banks provide a vir-tual version of this with networks that let them sweep up cashfrom far-ung outposts every day For the biggest rms andbanks the money never stops owing It follows the rising sunnancing trade and payrolls and then moves on as night falls todo the same again in another part of the globe

For consumers who want to wire money to some far cor-ner of the world less has changed since the days of the Old WestIf you try to send a small amount of money from America to thePhilippines say or Mexico you will probably have to queue at aneighbourhood money-transfer agent and pay a fee that couldeasily reach 10 of the value of the remittance

The World Bank reckons that cross-border remittances add-ed up to $483 billion last year These are mainly small amountssent regularly by migrants to their families back home As thenumber of migrants has swelled so too have the remittances byabout 8 annually in recent years says the bank

Surprisingly most big banks have shown little interest inhelping these ows along The Organisation for Economic Co-operation and Development reckons that banks handle just5-10 of remittances between America and Latin America oneof the worldrsquos biggest payment corridors Although the marginsare fat banks largely avoid this business because the existing in-terbank transfer systems were built to move money in big lumpsrather than by the spoonful So most banks have oered small-scale cross-border transfers as an afterthought and made themso expensive and inconvenient that they are rarely used Mosttake days to process and if a payment goes awry the customergets little help A charge of $25 or more to send money to anothercountry is common and banks often load on extra fees of 2-3

when they switch currencies Many banks charge not only forsending money but also for accepting it A World Bank study in2009 found that banks charged an average of 12 for small remit-tances whereas money-transfer agents such as Western Unionaveraged 9

Western Union is the gorilla of money transfers handlingclose to $1 in every $5 that is wired around the world Last year itsent close to $80 billion working through almost half a millionagents Its next-largest global competitor is MoneyGram whichtransfers about $20 billion a year UAE Exchange is a bit biggerbut still has a strong regional focus There is also a plethora ofsmall money-transfer agents that spring up in kiosks and grocery

Remittances

Over the sea andfar away

The business of sending money across borders is

lucrative fast-growing and ripe for change

stores in areas with large migrant populationsEven though they undercut the banks money-transfer

agents earn mouth-watering margins on remittances WesternUnionrsquos were above 28 in many of its biggest markets last yearMargins are so fat because pricing is far from transparent West-ern Union for instance sets prices for individual customers de-pending on where they are and the amount they send To wire$500 to Mexico from Dallas costs $14 To send the same amountfrom New York costs $25

The nimble shall prot

Given such margins this market is attracting some interestfrom new tech rms that think it is ripe for disruption One of thebest-known of these is Xoom a San Francisco-based internetrm backed by some of the smartest money in Silicon Valley Itcharges a at fee of $5 or $6 per transaction The reason it is ableto keep it so low is that it has moved one leg of the transactiononline Most remittances are deposited in cash and withdrawnas cash but Xoom has managed to persuade almost all its cus-tomers to make their transfers from bank accounts (a few use

credit cards which are more expensive forXoom) The company is still tiny com-pared with rivalslast year it handledabout $17 billionbut it is growing fast Itsservice is very convenient Many custom-ers send money from their bank accountsusing their phones while commuting to

work This year Xoom expects to transfer about $34 billion Itreckons that even with charges this low it can achieve better op-erating margins than Western Union

If Xoom can save money by moving one leg of the transac-tion online then why not move both legs John Kunze the com-panyrsquos chief executive explains that the recipients are often incountries with undeveloped banking systems and a strong pref-erence for cash The rule we have is never ask Mom to changeher behaviour he says

For those who are willing to move onto an entirely elec-tronic platform transferring money abroad can be a lot cheaperstill CurrencyFair is a peer-to-peer marketplace that started up

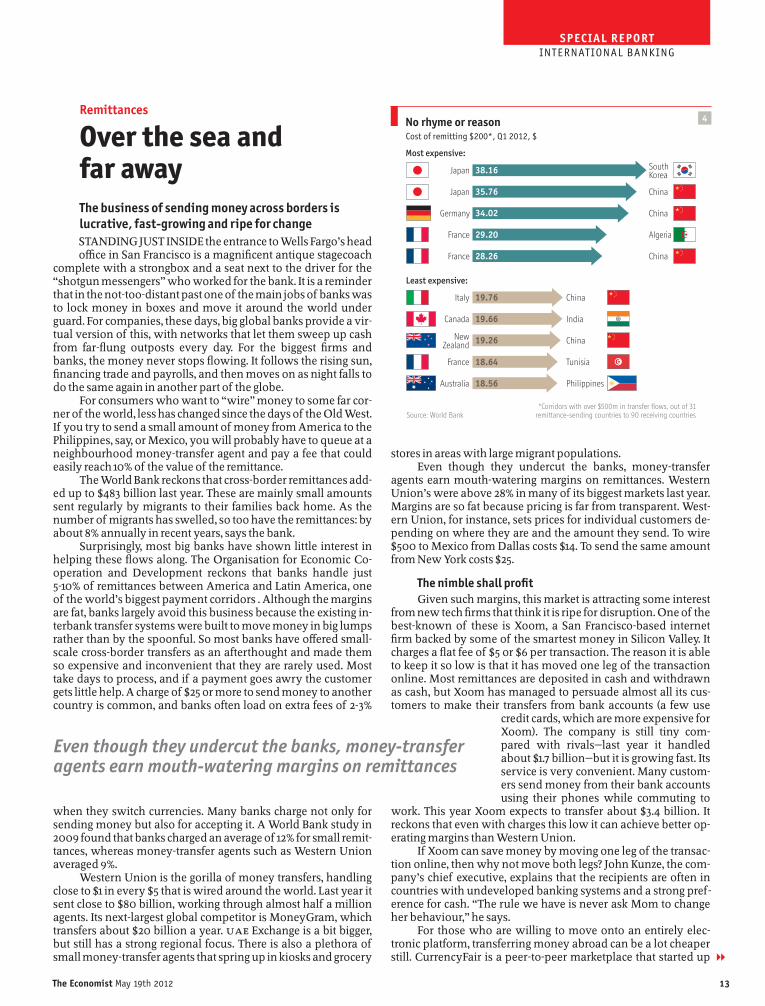

4No rhyme or reason

Source World BankCorridors with over $500m in transfer flows out of 31

remittance-sending countries to 90 receiving countries

Cost of remitting $200 Q1 2012 $

Japan

Japan

Germany

France

France

SouthKorea

China

China

Algeria

China

Italy

Canada

NewZealand

France

Australia

China

India

China

Tunisia

Philippines

Most expensive

Least expensive

3816

3576

3402

2920

2826

1976

1966

1926

1864

1856

Even though they undercut the banks money-transferagents earn mouth-watering margins on remittances

14 The Economist May 19th 2012

INTERNATIONAL BANKING

SPECIAL REPORT

2

1

just over a year ago after one of its founders Brett Meyers wascharged huge bank fees hidden in the exchange rate when trans-ferring money abroad After that he started ringing up friendsabroad to see who wanted to swap currencies The result was anonline marketplace that matches people wanting to buy and sellcurrencies In the main corridors such as that between Britainand the euro area very little money ever crosses borders Some-one wanting to sell sterling and buy euros deposits their poundswith the rm and is matched with people who have depositedeuros and want sterling Whereas most banks charge about 25through the spread between their buying and selling prices for acurrency on CurrencyFair the participants decide on the rate If atransaction is completed CurrencyFair charges 015 of its valueand a small fee to send the money to the recipientrsquos bank accountin the new currency In practice this means that for the momentpeople would generally need an account in each country or atleast a friend to whom they could send money CurrencyFairsays it is planning to add cash delivery If matching parties can-not be found CurrencyFair itself will quote a rate that it obtainsfrom wholesale markets with a fee of about 05 added on

Another option is sending money from one phone to an-other M-Via an American rm lets people in America top uptheir phones at 7-Eleven stores or other shops and then send themoney to other members Cash can be withdrawn from ATM

machines using cards linked to the accounts or the money canbe spent using a debit card

New online services are emerging for businesses too TheCurrency Cloud a London-based rm has received $4m in fund-ing from venture capitalists to build an automated foreign-ex-change system to help businesses make and receive payments in140 currencies

Boots on the ground

But good ideas on their own are not enough to overcomethe many barriers to entry in this business Perhaps the biggestone is the need for a network for taking in and handing out cashWestern Union for instance has kept increasing its share of themarket partly because it has raised the number of agents in itsnetwork nearly vefold over the past few years Branding is alsoimportant Western Union is able to charge more than some ofits competitors because its customers are willing to pay a pre-mium for a well-known name with which they feel safe

A third barrier and one that will probably become higherwith time as more transactions move online is knowledge andrisk control If you arenrsquot very good at fraud detection in thisbusiness you either end up bankrupt or in jail says Xoomrsquos MrKunze The fraudsters are reading all the books we are They arePhDs themselves

Given these barriers many of the new entrants are likely tolook for alliances and partnerships rather than try to disrupt themarket alone This has already started to happen M-Pesa theKenyan rm that allows people to send money to each otherover the phone has teamed up with Western Union to let peoplein 45 countries send money directly to M-Pesarsquos users in Kenya

New entrants to this market do not need to take a dominantshare of it to make a big dierence to the way it operates In mostof the main corridors with plenty of competition the feescharged by banks and traditional money-transfer agents are fall-ing sharply One old-school bank that is successfully making thetransition to the online world is Indiarsquos ICICI bank which be-tween 2008 and 2011 increased its share of the remittances mar-ket by well over 50 making it number four in the global rank-ings according to Aite Group a research rm Its customers areboth tech-savvy and price-conscious and they quickly took tocheaper internet transfers 7

STRATEGICALLY I THINK in terms of millionaires and bil-lionaires says Juumlrg Zeltner the head of wealth manage-

ment at UBS a Swiss bank It is a claim that many big bankswould like to make about their clients Few can With a squeezeon revenues from banking services for more down-at-heel folkmany of the worldrsquos biggest banks as well as some smaller oneshope to plump up their prot margins by serving the verywealthy Yet margins in private banking and wealth manage-ment are also being squeezed and new competitors from out-side banking stand a good chance of breaking into this market

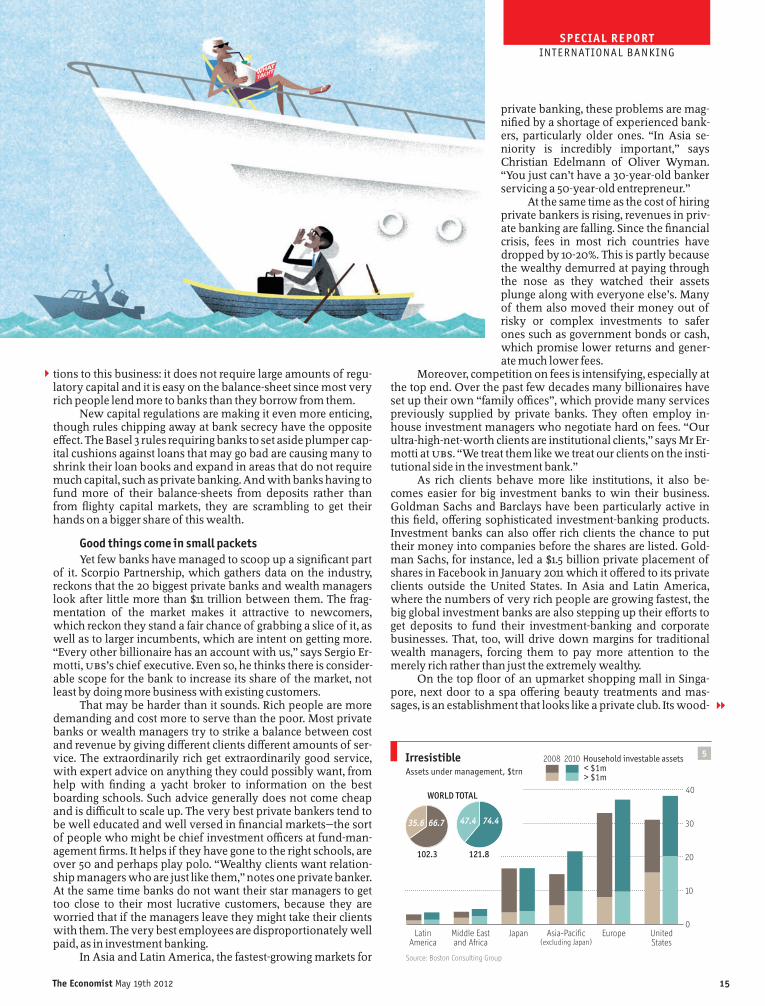

Self-evidently the big attraction for banks is that rich peo-ple have more money to invest and spend on advice than poorerones Denitions of rich customers vary from bank to bank andregion to region but there is a rough pecking order Customerswith nancial assets above $1m (not counting their homes orbusinesses) are generally classied as high-net-worth individ-uals and those with assets of $10m-30m as ultra-high-net-worthThe Boston Consulting Group puts the total investible assets ofthe worldrsquos wealthy at around $122 trillion last year almostenough to buy all the shares traded on the New York Stock Ex-change ten times over Capgemini and Merrill Lynch come upwith a more modest estimate of about $43 trillion Whichevernumber is right the market is certainly big enough to be interest-ing and everyone agrees that it is growing quickly The richworld is still home to most of the worldrsquos money about a third isin America and another third in Europe Yet the fastest growth isin Asia where the assets of the rich increased by almost a fth in2010 (see chart 5 next page)

The market is lucrative as well as large Before the 2007-08nancial crisis private banks generally earned revenues of about1 of the assets they looked after Those in oshore centressuch as Switzerland which used to be discreet to a fault tendedto ask for a bit more and those in America a bit less According toMcKinsey such fees left banks with a margin of about 035 oftheir clientsrsquo money under management There are other attrac-

Wealth management

Private pursuits

Many banks are hoping that wealth management can

restore their fortunes

The Economist May 19th 2012 15

SPECIAL REPORT

INTERNATIONAL BANKING

2

1

tions to this business it does not require large amounts of regu-latory capital and it is easy on the balance-sheet since most veryrich people lend more to banks than they borrow from them

New capital regulations are making it even more enticingthough rules chipping away at bank secrecy have the oppositeeect The Basel 3 rules requiring banks to set aside plumper cap-ital cushions against loans that may go bad are causing many toshrink their loan books and expand in areas that do not requiremuch capital such as private banking And with banks having tofund more of their balance-sheets from deposits rather thanfrom ighty capital markets they are scrambling to get theirhands on a bigger share of this wealth

Good things come in small packets

Yet few banks have managed to scoop up a signicant partof it Scorpio Partnership which gathers data on the industryreckons that the 20 biggest private banks and wealth managerslook after little more than $11 trillion between them The frag-mentation of the market makes it attractive to newcomerswhich reckon they stand a fair chance of grabbing a slice of it aswell as to larger incumbents which are intent on getting moreEvery other billionaire has an account with us says Sergio Er-motti UBSrsquos chief executive Even so he thinks there is consider-able scope for the bank to increase its share of the market notleast by doing more business with existing customers

That may be harder than it sounds Rich people are moredemanding and cost more to serve than the poor Most privatebanks or wealth managers try to strike a balance between costand revenue by giving dierent clients dierent amounts of ser-vice The extraordinarily rich get extraordinarily good servicewith expert advice on anything they could possibly want fromhelp with nding a yacht broker to information on the bestboarding schools Such advice generally does not come cheapand is dicult to scale up The very best private bankers tend tobe well educated and well versed in nancial marketsthe sortof people who might be chief investment ocers at fund-man-agement rms It helps if they have gone to the right schools areover 50 and perhaps play polo Wealthy clients want relation-ship managers who are just like them notes one private bankerAt the same time banks do not want their star managers to gettoo close to their most lucrative customers because they areworried that if the managers leave they might take their clientswith them The very best employees are disproportionately wellpaid as in investment banking

In Asia and Latin America the fastest-growing markets for

private banking these problems are mag-nied by a shortage of experienced bank-ers particularly older ones In Asia se-niority is incredibly important saysChristian Edelmann of Oliver WymanYou just canrsquot have a 30-year-old bankerservicing a 50-year-old entrepreneur

At the same time as the cost of hiringprivate bankers is rising revenues in priv-ate banking are falling Since the nancialcrisis fees in most rich countries havedropped by 10-20 This is partly becausethe wealthy demurred at paying throughthe nose as they watched their assetsplunge along with everyone elsersquos Manyof them also moved their money out ofrisky or complex investments to saferones such as government bonds or cashwhich promise lower returns and gener-ate much lower fees

Moreover competition on fees is intensifying especially atthe top end Over the past few decades many billionaires haveset up their own family oces which provide many servicespreviously supplied by private banks They often employ in-house investment managers who negotiate hard on fees Ourultra-high-net-worth clients are institutional clients says Mr Er-motti at UBS We treat them like we treat our clients on the insti-tutional side in the investment bank