matthew e mcgarvey - frontlinetechnologies.fall2011

TRANSCRIPT

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 1/32

Employee Benefit Plan Analysis

Frontline Technologies

Part 1: Loss Exposure Matrix

Part 2: Inventory of Existing Benefits

912619478

912479299

RMI 3501

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 2/32

Dr. Drennan

Fall 2011

Table of Contents

Loss Exposure Matrix………………………………………………………………………………………………………………1

Inventory of Existing Benefits…………………………………………………………………………………………………..2

Inventory of Benefits…………………………………………………………………………………………………...3

Background of the Healthcare Plan…………………………………………………………………....3

Medical Benefits………………………………………………………………………………………......……………...4Preferred Provider Organization (PPO) Plan……………………………………………….…..3-4

Dental……………………………………………………………………………………………………………4-5

Vision…………………………………………………………………………………………………………….5-6

Prescription Drug…………………………………………………………………………………………..6-7

Loss of Income Benefits………………………………………………………………………………………………..7

Basic Life, AD&D, Supplemental Life……………………………………………………………….7-8

STD, LTD……………………………………………………………………………………………………...9-10

401(k) Plan………………………………………………………………………………………………..11-12

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 3/32

Loss Exposure Matrix

Loss Exposure Covered? Benefit/Coverage Provided

Medical Expenses

Hospital and Physician Yes IBC Personal Choice PPODental Yes Guardian PPO

Vision Yes Davis Vision

Prescription Drugs Yes PBM - Millennium Drug Coverage

Retiree Health Care Yes Medicare, COBRA

Long Term Care No

Loss of Income - Death

Accidental Death Yes Basic Life Insurance, AD&D Insurance,Supplemental Life Insurance, OASDI, 401(k)

Plan

Occupational Death Yes Basic Life Insurance, Supplemental LifeInsurance, Worker’s Compensation, OASDI,

401(k) Plan

Non-Accidental Non-Occupational Death

Yes Basic Life Insurance, Supplemental LifeInsurance, OASDI, 401(k) Plan

Disability

Occupational, Short Term Yes STD, AD&D Insurance, OASDI, 401(k) Plan,Worker’s Compensation

Non-Occupational, Short Term Yes STD, AD&D Insurance, OASDI, 401(k) Plan

Occupational, Long Term Yes LTD, AD&D Insurance, 401(k) Plan, OASDI,Worker’s Compensation

Non-Occupational, Long Term Yes LTD, AD&D Insurance, 401(k) Plan, OASDI

Unemployment Yes PA State Unemployment Insurance

Retirement Yes 401(k) Plan, OASDI

Additional Exposures

Dependent Care No

Work/Life No

Educational Assistance NoProperty and Liability No

Legal Expenses No

Inventory of Existing Benefits

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 4/32

Benefit Plan A.M. Best

Rating

Funding Financing Eligibility

ConditionsPersonal Choice PPO B+

(Good)Fully

InsuredContributory Full Time

Employees &Dependents

Guardian Dental PPO A++(Superior)

FullyInsured

Contributory Full TimeEmployees &Dependents

Davis Vision A(Excellent)

FullyInsured

Contributory Full TimeEmployees &

Dependents

MillenniumAdministrators -Prescription Drug

B+(Good)

FullyInsured

Contributory Full TimeEmployees &Dependents

The Hartford Life andAccident Ins. Co. -Life Insurance

A++(Superior)

FullyInsured

Non-Contributory Full TimeEmployees &Dependents

The Hartford Life andAccident Ins. Co. -AD&D Insurance

A++(Superior)

FullyInsured

Non-Contributory Full TimeEmployees

The Hartford Life and

Accident Ins. Co. -STD & LTD Insurance

A++

(Superior)

Fully

Insured

Non-Contributory Full Time

Employees

All A.M. Best Ratings were sourced from www.ambest.com

Inventory of Benefits

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 5/32

Background of the Healthcare Plan

Frontline Technologies, a workforce management software company based out of Exton,

Pennsylvania, offers a competitively-priced benefits plan package to its employees. While

medical benefit choices are limited to one plan, the coverage available is priced well below much

of its competition and national averages. This issue will be addressed in the analysis section.

Eligibility to participate in the medical plan is defined to include full-time, active employees,

working forty hours per week, who are citizens or legal residents of the United States, its

territories and protectorates, excluding temporary, leased or seasonal employees.

Due to the fact that Frontline Technologies is a young and small sized company, with

only 80 employees, all of the firm’s available medical benefits are fully insured, contributory,

and community rated. The firm’s medical plan covers 65 total employees. In its entirety, there

are 39 family groups, 2 parent/child groups, 10 employees with legal spouse coverage and 14

single employees. When an employee enrolls in the health care plan, they are automatically

provided with coverage under the dental and prescription drug plans as well. If an employee is

covered under a spouse’s or parent’s plan, he/she may elect to opt-out of medical coverage with

the firm.

Medical Expenses

Preferred Provider Organization Plan (PPO)

Frontline’s only option for medical coverage is a high-deductible health plan through

Independence Blue Cross (IBC). The plan, which IBC calls “Personal Choice”, provides full

coverage on the first of the month after the employee’s initial hire date if he/she chooses to enroll

and participate. The monthly premium for the entire medical plan is as follows: $62 for a single

employee, $68 for employee and legal spouse coverage, $55 for an employee with one child, or

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 6/32

$92 for family coverage (married couple with any number of children). Personal Choice, like all

PPOs, allows for balance billing. The annual deductible for in-network coverage is $3,000 for

singles and $5,000 for families. Deductibles are $5,000 and $10,000, respectively, for out-of-

network costs. As far as out-of-pocket maximums are concerned, the plan caps these costs at

$5,600 for in-network single coverage and $11,200 for families. Out-of-pocket maximums for

out-of-network coverage are $11,600 for singles and $20,000 for families. Higher deductibles

and increased out-of-pocket maximums create significant incentives for employees to stay in

network. It should also be noted that, for covered services not recognized or reimbursed by

Medicare or IBC’s fee schedule, reimbursement may be available at a rate of 50% for out of

network services, compared to 100% for in-network utilization.

Dental

Frontline offers dental care through a dental PPO sponsored by Guardian. Guardian’s

A.M. Best rating is currently at A++. The employees of Frontline must fill out the enrollment

form and turn it in to receive coverage. Once this process is completed and an employee is

enrolled, coverage begins immediately. Members can choose to stay in-network, which is called

“DentalGuard Preferred”, or go out-of-network for their dental services. However, if an

employee decides to stay in-network, their out-of-pocket expenses will likely be much lower

than if they decide to visit a provider outside of the network. If members go out-of-network, they

are required to submit a claim through the plan and wait to receive reimbursement from the PPO.

There is no guarantee that they will be fully reimbursed for their expenses.

The deductible is $50, whether the Employee chooses to stay in or go out of the network

for dental care. The PPO will cover 100% of the charges for preventive care (e.g. basic

cleanings) for both in and out-of-network users. However, the PPO lowers its coinsurance

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 7/32

coverage of basic care (e.g. fillings) to 80% for both in and out-of-network users. Also, the

coinsurance limits are decreased even further for major care procedures (e.g. crowns, dentures),

at a coverage rate of 50% for both in and out-of-network users. Currently, the plan offers no

coverage for orthodontia. Under the Guardian Dental Plan, dependent age limits are currently

capped at twenty years old if the son/daughter is a non-student and twenty-six years old if he/she

is currently enrolled as a full-time student.

Vision

Frontline offers a vision plan through Independence Blue Cross, which has an A.M. Best

Rating of A. The plan is fully insured and offered on a contributory basis. The IBC vision plan

for Frontline is administered by Davis Vision and offers members benefits that include eye

exams (including refraction and glaucoma screening), frames, lenses, and contact lenses. The eye

exams, certain spectacle lenses, and frames from the Davis Collection of Frames have no charge

to the member as long as they use a provider from the Davis Vision network. Members can also

get an eye exam from a non-participating provider which will be reimbursed up to $35. Members

may also choose frames from a participating provider’s own frame collection, as opposed to the

Davis Collection of Frames. If an employee follows this route, he/she will receive a $60

allowance. If a member exceeds the $60 allowance, they are balance-billed for the remaining

excess expenses. If a member wants to select either lenses or frames from a non-participating

provider, there is a reimbursement for up to $75 available.

There are no completely cost-free contact lenses available for members. Members can

receive contact lenses which include standard, specialty, and disposable lenses, through a

participating provider with an allowance up to $75. If a member goes over that allowance, they

will also be balance-billed for the difference. If a member would rather go out of the network and

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 8/32

use a non-participating provider, they can receive up to $75 in reimbursement; however they are

not guaranteed all of the $75.

Prescription Drug Plan

Frontline’s prescription drug plan is provided through a PBM (Pharmacy Benefit

Manager), Millenium Administrators. If an eligible employee or a dependent covered under the

plan incurs expenses from a non-work related injury or sickness, and prescription drugs are

needed, a small co-payment will cover most prescription costs. As previously mentioned, an

employee is automatically enrolled in the prescription drug plan when they elect to receive

medical benefits through the firm.

The schedule for co-payments is listed below. All of these prices for retail drugs reflect a

typical 30-day supply. The prices for mail order drugs reflect a 90-day supply for prescribed

medications.

Participant’s Co-Payments

(Retail)

Participant’s Co-Payments

(Mail Order)

Generic Drugs $10 $20

Preferred Brand Drugs $20 $40

Non-Preferred Brand Drugs $35 $70

Preferred drugs are defined as drugs that have been on the market for a longer period of

time and are widely accepted, therefore they are given discounts. Non-preferred drugs are

usually newer on the market, more expensive and do not receive any other discounts under the

plan. There is also a major incentive for consumers to purchase through the mail due to the cost

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 9/32

saving potential. The plan also covers diabetic supplies, insulin, injectables, contraceptives and

other drugs deemed medically necessary by the provider.

Loss of Income Benefits

Basic Life, Accidental Death & Dismemberment Insurance, Supplemental

Life Insurance, Supplemental Dependent Life Insurance

Frontline offers basic life insurance, accidental death & dismemberment (AD&D), and

supplemental life insurance to all eligible, full-time active employees who are citizens or legal

residents of the United States, its territories and protectorates, excluding temporary, leased or

seasonal employees. This coverage is made available to help surviving dependents deal with loss

of income caused by the death of the employee. Supplemental dependent life insurance is offered

to spouses and children of full-time employees as defined above. All of these options are

sponsored by The Hartford Life and Accident Insurance Company, who has an A.M. Best Rating

of A++ (superior). Basic life insurance and AD&D are offered on a non-contributory basis and

supplemental life insurance and supplemental dependent life insurance are offered on a

contributory basis. There is an annual enrollment period with no waiting period if the employee

is working for Frontline on the policy effective date. If the employee is not employed by

Frontline at the time that the policy became effective, the employee must wait until the first day

of the month following the date they were hired.

The amount of coverage for basic life insurance is equal to the employee’s annual

earnings, subject to a maximum of $150,000, rounded to the next higher $1,000 if not already a

multiple of $1,000. In no event will the employee’s basic amount of life insurance be less than

$10,000. AD&D has a limit of 1 times the employee’s annual earnings, subject to a maximum of

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 10/32

$150,000, rounded to the next higher $1,000 if not already a multiple of $1,000. The employee’s

principal sum of AD&D will never be less than $10,000. AD&D also offers additional benefits

which include: repatriation, child education, day care, rehabilitation, spouse education, and

adaptive home and vehicle benefits.

Frontline employees may also choose supplemental life insurance. They can choose how

much they want with a guaranteed issue amount that the amount the employee elects in

increments of $10,000, subject to a maximum of $100,000. However, the maximum amount they

can receive is the amount they elect in increments of $10,000, subject to the lesser of $300,000

or three times their annual earnings. The employee will never have less than $10,000 in

Supplemental Life Insurance however. Finally, the supplemental amount of dependent life

insurance available for an employee’s spouse includes a guaranteed issue amount that the

employee elects in increments of $5,000, subject to a maximum of $100,000. The dependent

children (ages 15 days – 19 years,) are only eligible up to a maximum amount of $10,000. The

amount of spouse supplemental coverage may never exceed 50% of the supplemental amount of

life insurance in force for the employee.

There is some reduction in coverage for life insurance once the individual employee

reaches a certain age. On the date that the employee becomes 65 years old, their life insurance

and principal sum is reduced by 35%. Once the employee then reaches the age of 70, their life

insurance and principal sum will be reduced by 50% of the original amount.

Short-Term Disability Insurance & Long-Term Disability Insurance

Short-term disability and long-term disability insurance are offered by Frontline through

The Hartford Life and Accident Insurance Company, which has an A.M. Best Rating of A++.

The short-term disability (STD) policy provides Frontline employees with short-term income

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 11/32

protection if they become disabled from a covered injury, sickness, or pregnancy. The long-term

disability (LTD) insurance policy follows the same general guidelines as the STD policy except

its nature varies as it is meant for long term income protection. The STD and LTD are both

offered on a non-contributory basis. All full-time active employees who are citizens or legal

residents of the United States, its territories and protectorates, excluding temporary, leased or

seasonal employees are eligible for this coverage. Consistent with the life insurance policies,

there is no eligibility waiting period for disability coverage if the employee is working for

Frontline on the policy effective date. If the employee joined Frontline after the policy was

already in effect, they must wait until the first day of the month following their hire date.

Short-term disability benefits are available for disability resulting from non-work related

injury on the 30th consecutive day of total disability or disabled and working. For disability

caused by sickness, the benefits also commence on the 30 th consecutive day of total disability or

disabled and working. Benefits are paid weekly at a rate of 66

% of the employee’s pre-

disability earnings or $1,500, whichever is the lesser amount. This coverage level provides an

incentive to the employee to return to work as soon as he/she can to the extent that it does not

provide full compensation coverage. The maximum duration of benefits payable for STD is 9

weeks if caused by injury or sickness. Once the allotted 9 weeks of coverage has expired, STD

benefits cease completely.

For long-term disability insurance, there is a deductible, in nature, which is 90

consecutive days at the beginning of any one period of disability or 90 consecutive days from the

expiration of any employer sponsored STD benefits or salary continuation program, excluding

benefits required by state law. The maximum monthly benefit an employee can receive for LTD

is $8,000, while the minimum monthly benefit he/she can receive is the greater of $100 or 10%

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 12/32

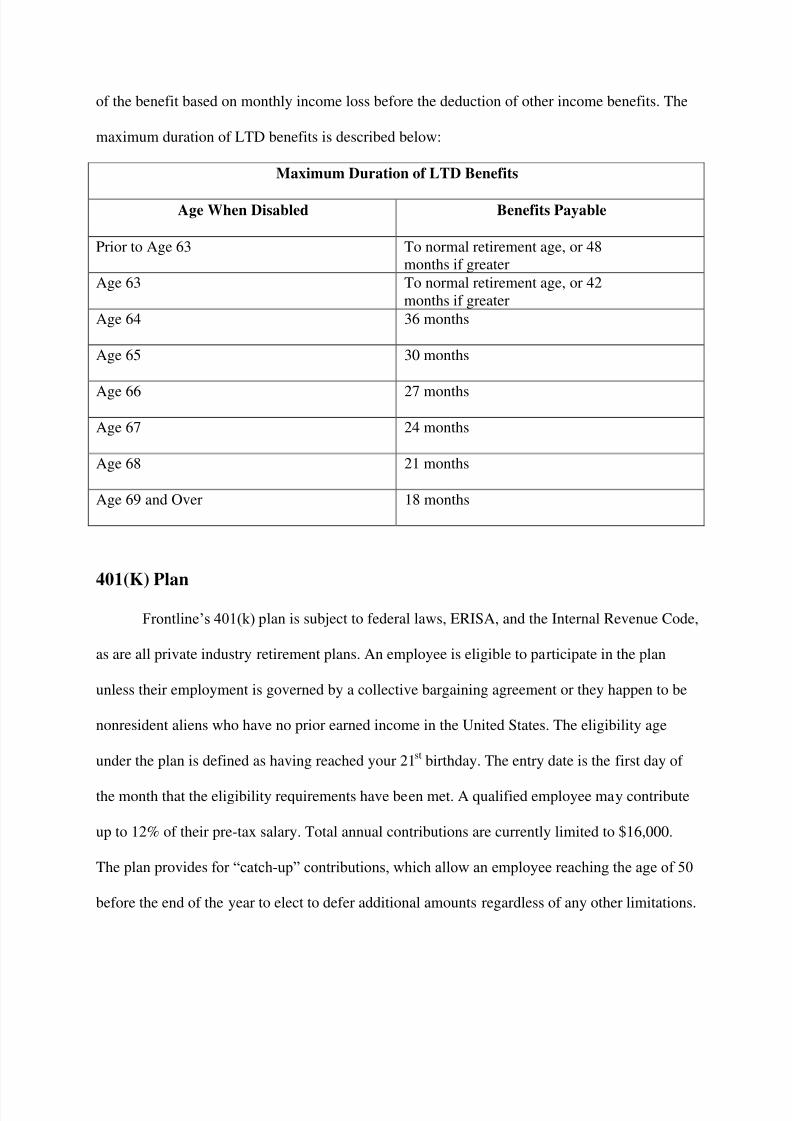

of the benefit based on monthly income loss before the deduction of other income benefits. The

maximum duration of LTD benefits is described below:

Maximum Duration of LTD Benefits

Age When Disabled Benefits Payable

Prior to Age 63 To normal retirement age, or 48months if greater

Age 63 To normal retirement age, or 42months if greater

Age 64 36 months

Age 65 30 months

Age 66 27 months

Age 67 24 months

Age 68 21 months

Age 69 and Over 18 months

401(K) Plan

Frontline’s 401(k) plan is subject to federal laws, ERISA, and the Internal Revenue Code,

as are all private industry retirement plans. An employee is eligible to participate in the plan

unless their employment is governed by a collective bargaining agreement or they happen to be

nonresident aliens who have no prior earned income in the United States. The eligibility age

under the plan is defined as having reached your 21st birthday. The entry date is the first day of

the month that the eligibility requirements have been met. A qualified employee may contribute

up to 12% of their pre-tax salary. Total annual contributions are currently limited to $16,000.

The plan provides for “catch-up” contributions, which allow an employee reaching the age of 50

before the end of the year to elect to defer additional amounts regardless of any other limitations.

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 13/32

The maximum “catch up” amount in the cur rent year is $2,000 and increases $1,000 for every

additional year with an aggregate limit of $5,000. The normal retirement age is defined as 65

years old.

As far as ownership rights are concerned, the employee is always 100% vested, or fully

vested, in the contributions they make to the plan. Employees are not permitted to withdraw from

their 401(k) accounts unless there is an event of death, disability or separation from service

within the company past a certain, pre-set date. The employer, Frontline, will match the total

amount of the salary deduction the employee elects to defer. The plan allows for “rollover” at the

discretion of the administrator from eligible IRAs or retirement plans.

The vesting schedule for employer contributions is as follows:

Years of Service Vesting Percentage

Less than 2 0%

2 20%

3 40%

4 60%

5 80%

6 100%

If an employee becomes disabled, he/she is entitled to 100% of their 401(k) account

balance. This would be paid out as if they had retired at the normal retirement age. If a plan

participant happens to pass away, the named beneficiary will naturally receive the benefits. If

there is no named beneficiary the balance will be paid to, in priority order, the surviving spouse,

the children, the surviving parents or the applicable estate.

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 14/32

To protect from discrimination, the 401(k) also provides “Top Heavy” rules. This occurs

when a retirement plan’s assets are more than 60% attributable to “key employees”. When this

occurs, a “Top Heavy Minimum Benefit” will be allotted to all eligible, non-key employees.

Employee Benefit Plan Analysis

Frontline Technologies

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 15/32

Part 3: Benefits Analysis

912619478

912479299

RMI 3501

Dr. Drennan

Fall 2011

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 16/32

Table of Contents

Company History………………………………………………………………………………………….………………………..…………1-2

Overall Design Considerations in Employee Benefits…………………………………..……………………………..2

Goals……………………………………………………………………………………………………………..2-4

Demographics………………………………………………………………………..………………………....4

Funding and Financing Considerations………………………………..…………......……………...4

Problems in the Design of Health Benefits…………………….……………………………………….…..3-4

Funding Considerations…………………………………………………………………………………4-5

Shift of Medical Plan Coverage……….………………………………………………………………….6

Health Reform Considerations………………………………………………………………………..6-7

Cost Containment………………………….………………………………………………………………….7

Problems in the Design of Other Non-Retirement Benefits………...…………………………...……..8

Communication…………………………….……………………………..…………………………….……..8

Regulatory Compliance………………………………………………………………………………………………..9

HIPAA………………………………………………………………………………………...….…………………9

COBRA………………………………………………………………………………………………….……..9-10

ERISA…………………………………………………………………………………………………….……….10

Recommendations Moving Forward………………………………………………………………………10-12

Conclusion……………………………………………………………………………………………………..................12

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 17/32

912619478 Frontline Technologies

912479299 Page 1

Company History

Frontline Technologies, based out of Exton, Pennsylvania, is a privately held workforce

management software technology company. Roland Thompson and Michael Blackstone founded

the company in 1998. Thompson is an ex-Wall Street trader and Blackstone worked for many

major banking and financial institutions over the course of his early career. Thompson and

Blackstone were both very gifted at what they did but were frustrated with the perceived poor

ethics and morals that existed in their industries. They both came to the realization that they

needed to leave the corporate world and try to make it on their own. They decided to take a very

large leap of faith in starting not one, but three, highly successful start up companies. It was

fascinating to learn that, prior to starting Frontline, one of Roland Thompson’s previous ventures

was the invention and sale of the SkyCam overhead camera technology that we all see every

weekend in the Fall at most major NFL football stadiums.

To this day religion and spirituality play a vital role in Thompson and Blackstone’s lives.

They actually attend the same church together every Sunday. During our interviews Mr.

Thompson said, “We wanted to create a company using Biblical principals - things like

character, honesty, morals, valuing family. That is what a company should be founded on.”

These principals have often been seen as taboo and are rare in corporate America because the

primary goal of many businesses is to generate profits. One of the slogans that is common within

the company is “Family before fame. People before profit. God before game.” These are but just

a few examples of how family oriented and employee-centered the company culture truly is.

Below is an excerpt from the Frontline Mission Statement:

“We will honor God in all we do. We will empower our people to innovate, to think

strategically and to be business leaders. We believe customer service is our differentiator and

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 18/32

912619478 Frontline Technologies

912479299 Page 2

we will not let it be commoditized by our competitors. We will pursue business excellence by

expecting the best from our people while delivering the best for our customers. We will grow

profitably by listening to our customers and markets, and continuously be innovating and

creating simple solutions for complex needs.”

After speaking with Roland Thompson (one of the Managing Partners), Todd Orlando

(the Chief Financial Officer), Matt Bachman (the Controller), and Colleen Dewan (the Human

Resources Manager), it was quite apparent that this biblical-based company culture is imbedded

into the minds of all of these individuals. At one point Mr. Blackstone clarified that one does not

have to believe in the Bible or God to work at the company, however the principals they instill in

their employees make for an extremely unique and productive company culture.

It is also noteworthy that there appear to be real business impacts from their approach.

While striving to maintain a strong spiritual environment, the company has also enjoyed very

solid performance results. After only 12 years they have amassed close to 3,000 customers.

Profit margins consistently exceed 70% and revenue growth has topped 20% in each of the last

three years.

Frontline’s most significant product offering is a software program branded Aesop, which

is an automated scheduling and shift fulfillment system that is in place in thousands of

institutions across the world. Aesop was first developed in 1998 and has grown rapidly ever

since. In fact, the program is in place in 20% of the school districts across the country. The

program utilizes Internet services and automated telephone communication in placing substitute

teachers in the Kindergarten through Grade 12 marketplace. The program is entirely automated

and is beginning to corner the market due to its unique capabilities. Frontline also offers other

programs that are seamlessly integrated with Aesop such as Jobulator and Veritime. Jobulator, a

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 19/32

912619478 Frontline Technologies

912479299 Page 3

desktop computer application, is an automatic job notification center for substitute teachers.

Veritime is a web-based time and attendance program that aids in the processing of time sheets,

ultimately saving tedious paperwork and reducing administrative costs. Frontline has

successfully broken into the K-12 education market, as well as the health care industry, staffing

services, manufacturing, live event staffing, and library functions. Their Aesop program has

unlimited potential applications and continues to make breakthroughs in both its technology and

in new industries.

Overall Design Considerations in Employee Benefits

Goals

Frontline is a rapidly growing software company that has had to face many plan design

changes in the past few years and will certainly be going through more radical changes in the

near future. One plan year ago, in 2010, the company offered a choice between two health plans:

a Blue Cross Personal Choice indemnity plan, or a POS-type HMO through Keystone Health (a

subsidiary of IBC). The POS-type HMO offered a Health Reimbursement Account and also a

Dependent Care Reimbursement Account. According to their broker, Kim Phelps, the growing

company would be smart to switch to the high deductible PPO offered through Independence

Blue Cross, which is what they currently offer. This recommendation is based on the fact that the

firm felt compelled to instill a sense of consumerism in the employees and also due to certain

cost shifting strategies.

Plan design, essentially, was somewhat basic due to the small size of the company but

they had to keep in mind the possibility of self-insuring within one to two years. After speaking

with Matt Bachman (Controller) and Todd Orlando (CFO), they both agreed that with the

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 20/32

912619478 Frontline Technologies

912479299 Page 4

increased growth within the firm they certainly see themselves being a fully self-insured

company within the next two to three years.

Since Frontline is a software technology company, most of their employees are highly

compensated and are accustomed to receiving highly rich benefit plans. Keeping this in mind,

Frontline has to offer a benefit plan that is comparable to its competition which includes firms

like E-School Solutions (Orlando, FL) and CRS Advanced Technology (Montoursville, PA).

Offering benefits comparable to its competition is a key decision making factor for the company.

Colleen Dewan (HR Manager) and Orlando both explained that when prospective employees are

shown the benefits package during the interview process, many of them are shocked at the

richness of the provided plan. However, they explained that their benefit package is mainly used

as a retention tool more than anything else due to the fact that a rich benefit package is quite

common in the industry.

The increased trend of offering flex benefits and wellness programs has also been

considered and will be an influential topic during the future plan design discussions. Currently,

the only wellness program Frontline offers is the on-site gym. The company, in the past, has

considered smoking cessation programs and weight management programs as well. However the

fact remains that only two employees smoke and due to the fact that a large majority of the

company are young and in good health these programs would be largely underutilized.

Demographics

The demographics of the company were not a major decision factor in the

implementation or designing of the benefit plan. The company is comprised of a large percentage

of young, single males so this factor did come into play as to the level of benefits offered. This is

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 21/32

912619478 Frontline Technologies

912479299 Page 5

one of the reasons why the monthly premium for the health care benefits is so significantly

reduced; it is currently at a surprisingly low $32/month.

Funding and Financing Considerations

Frontline will be offering a benefit plan that for the most part is fully insured with the

exception of their prescription drug and vision plans, which are self-insured. At the moment, the

company is not large enough to self-insure all benefits but this consideration will be discussed

furthermore throughout the analysis.

Problems, Issues, Concerns, and Considerations in the Design of

Health Benefits

Funding Considerations

As the company sees increased revenue quarter after quarter and as their products are

becoming wildly successful, the idea of self-funding is becoming an increasingly likely option.

In the next plan year the company will be moving to a self-funded dental plan as well as a self-

insured prescription drug plan. According to Kim Phelps, the firm has some serious incentives to

initiate a self-insured medical plan and potentially self-funding their disability coverage (long-

term and short-term) as well.

Many issues related to implementing a self-funded plan will surely arise for Frontline. As

they are approaching nearly 100 employees and hitting certain annual revenue thresholds, it is

entirely possible that they can save a substantial amount of money by offering such a plan. When

Frontline ultimately decides to self-insure they will need to be generating sufficient revenue in

order to establish loss reserves for the firm. They must be able to properly manage cash flow,

predict future earnings, sufficiently deal with shortfalls in expected income, and adapt to

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 22/32

912619478 Frontline Technologies

912479299 Page 6

changing demographics. The firm’s current accounting team is young and may be forced to grow

nearly as fast as the company itself in order to predict such figures. The issue of stop-loss

insurance also arises when considering a self-insured plan. To protect themselves from

unexpectedly high claims, stop-loss insurance is an absolute necessity. In addition, stop-loss

insurance is an additional expense due to the premium that will be paid for the appropriate

policy. Extra resources and time will be necessary in order to find the correct plan with the

necessary stop-loss limits.

A major incentive for Frontline to implement a self-insured plan other than the cost

savings would be the decreased need for regulatory compliance. Under ERISA, self-insured

plans are exempt to hundreds of state laws that regulate and set certain benefit requirements on

employer-sponsored health care plans. This fact alone may hurt them in the long run due to new

regulation of health reform. Under legislation that is waiting to be passed, PPACA may limit the

design options for employers implementing a self-insured plan. The Department of Health and

Human Services is examining the limitations it needs to put in place by analyzing self-insured

plans’ ability to offer less costly coverage.

Shift of Medical Plan Coverage

Frontline, as of their last plan year, offered a POS-type HMO through Keystone Health

with a monthly premium of roughly $125. This plan was the most popular for employees due to

its low cost and the ability to go to virtually any doctor. In addition to the POS plan, Frontline

offered a traditional indemnity plan through Blue Cross called “Personal Choice”. This plan,

referred to as a “Cadillac” plan, had a premium of roughly $325/month. This plan was offered

and chosen by only five employees, because these highly-compensated individuals either did not

want to change their doctors or had increased expected medical costs. One aspect that makes

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 23/32

912619478 Frontline Technologies

912479299 Page 7

Frontline so unique is the fact that it still has the ability to listen and coordinate with its

employees. The only reason the “Cadillac” plan was offered was due to the requests of a few

employees to offer such a plan. The firm switched to the PPO through IBC in order to broaden

the network of primary care physicians and specialists as well as force employees to act more

like traditional consumers of health care services.

Health Reform Considerations

With the array of health reform regulation that has passed legislature or is still on the

docket with the Supreme Court, health reform is the most controversial issue facing small

businesses today. Frontline, who currently fully-insures their PPO plan through IBC, will face

some increased compliance issues if the Supreme Court allows the Individual Mandate.

Currently, the program is waiting for a ruling on whether or not it is in fact constitutional and if

so it will be effective as of January 2014. From what the key decision makers of the company, as

well as the broker Kim Phelps have explained, they believe that the company will be self-funding

before the Individual Mandate is passed so that fact makes this a non-issue.

Health reform, the Individual Mandate in particular, will limit the flexibility of health

insurance policies. Any policy that is deemed qualified under future legislation will face

limitations as to the level of deductibles, maximum payouts, and copayments.

Cost Containment

As with most companies, Frontline is focused on and concerned about continuous

inflation when it comes to healthcare costs. As these costs continue to escalate, employers need

to start rethinking certain aspects of their employee benefit plans. Frontline has certainly taken

notice of these recent trends and has started to rethink their benefits packages and in certain areas

they have already taken steps to attempt to contain the costs. For example, Frontline’s most

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 24/32

912619478 Frontline Technologies

912479299 Page 8

noteworthy effort so far has been the move to a $3,000 /$6,000 High Deductible Health Plan.

This shifted more of the cost towards the employees so that Frontline won’t have to bear as much

of the overall cost. The Frontline team indicated that they are not able offer traditional co-pay

plans any longer due to cost constraints. Not only are the deductibles extremely high, but also the

co-pays were moved from $5.00 to $10.00. However, employee satisfaction didn’t change.

Ironically, the staff’s loudest complaint was that they had to switch plans, with limited concern

about the high deductible or the high co-pay.

Frontline has also been considering not offering any type of healthcare at all in the future

as a potential alternative depending on where the cost structure goes in the future. With the “Play

or Pay” law coming into effect in the future, Frontline is contemplating possibly paying the

$2,000 penalty for not “playing”, then simply giving their employees a 20% raise to help them

out with their own healthcare expenses. Frontline says that this option of paying the $2,000

penalty is a last resort option and they don’t believe it will come to fruition.

Problems, Issues, Concerns, and Considerations in the Design of

Other Non-Retirement Benefits

Communication

Frontline communicates with their employees in several different ways to inform them

about the benefits they are offered and how they work. First, Frontline sends out SPDs to all of

their employees electronically so that they can start to gain a little bit of a background as to what

is offered and how much they will have to pay and other things of that nature. Open Enrollment

is another way Frontline communicates benefits with their employees. Once a year, in March,

Frontline holds a meeting to go over the different benefits that they offer and what each of them

contains. All the employees gather together to learn more about the benefits they will be

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 25/32

912619478 Frontline Technologies

912479299 Page 9

receiving. To keep the employees engaged, there are food and beverages provided. Kim Phelps is

also there to help inform the employees and answer any questions that they might have.

Also, Frontline has completed utilization surveys in the past. These surveys go to the

employees to see what they like about their benefits and what they do not necessarily like about

them. For example, Colleen Dewan gave one to the employees two years ago regarding their

vision plan in order to determine basic participation percentages. She said she was surprised to

find out that about 85% - 90% of the employees were going to the eye doctors regularly and were

using the glasses and contact lens benefits. This and other surveys are used to help determine

how the benefits that are being offered can be altered or eliminated from the benefits package.

Regulatory Compliance

HIPAA

Most privately held companies have to worry about HIPAA and the confidentiality of

their employee documents and claims history. Kim Phelps said that this is not completely the

case for Frontline. This is all because everyone at Frontline is upfront and open with everyone

else and most of the time the employees share a lot of their health problems with other

employees anyway. “It is just how the culture is at Frontline” Kim said, “Everyone is open with

each other”. However, Colleen Dewan said that she has to be very careful about not knowing

anything that she doesn’t necessarily need to know. If something of that much importance is

brought up she will tell the employee to just go straight to the broker, Kim, to discuss any issues

they might have. There was one instance at Frontline when Colleen found out that an employee

had pneumonia and she accidently told another employee. This caused a big problem within

Frontline because the employee who was ill became very upset. From then on out, Colleen

advised the employees to go directly to Kim with their questions or concerns. The employees

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 26/32

912619478 Frontline Technologies

912479299 Page 10

also don’t have access to their spouses and children’s medical information/bills. If they are over

the age of 18, the dependents must give permission to the employee to have access to their

records even though the employee is more often than not the one who is paying the bills.

COBRA

Frontline must offer COBRA coverage due to the fact that they have over twenty

employees. If an employee does leave Frontline, they can get COBRA coverage for up to 18

months thereafter. There is also an HRA account which holds either $2,000 or $4,000 depending

on if the employee is single or married. (These numbers come from the same amounts that

Frontline helps to pay for the employee’s deductibles under their HDHP.) Frontline deals with

COBRA in house with the help of Kim Phelps also. She says that Frontline has few issues

complying with COBRA. Due to the fact that the COBRA coverage is exactly the same as the

active, full-time employee coverage, the employees who are provided COBRA only complain

about the issue of them having to pay the entire premium for the health benefits.

ERISA

Under ERISA, Frontline has a fiduciary responsibility that they must abide by. One

example of this is the switching of health care plans. Last year, Frontline offered two plans: a

Blue Cross Personal Choice indemnity plan and a POS-type HMO through Keystone Health. By

switching to their Blue Cross Personal Choice PPO, the employees now have more possible

providers because they have a broader network of doctors than before when they were either in

the indemnity plan or the POS-type HMO. Also, the switch to the PPO greatly reduced the

premium. Frontline must also communicate their benefits effectively to the employees under

ERISA. Frontline sends out SPDs to its employees electronically as well as has an annual

meeting to discuss the upcoming year’s benefits plan where Kim is also present to answer any

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 27/32

912619478 Frontline Technologies

912479299 Page 11

question the employees might have. Discrimination testing is another area of concern under

ERISA but not for Frontline. Because Frontline has fewer than 100 employees, they need not

perform any discrimination testing so that area of ERISA is not an issue for Frontline.

Recommendations Moving Forward

Frontline has overcome many obstacles in making major changes as far as their benefits

program. Switching from offering a traditional indemnity plan and a POS-type HMO to a high

deductible PPO plan was no easy decision for the executive panel. The company still has many

challenges ahead of them, resulting from health reform and other market and regulatory

pressures. It is suggested that the best course of action, strategically, for Frontline would be to

self-insure their benefits plan. This may mean considering an ASO contract due to the fact that

current administration will most likely not be able to handle and regulate the plan as required.

There are only a few key decision makers within the company, as well as a small accounting

department, that are informed as to the true cost of the benefits provided. This may be a

challenge when the company has to analyze the appropriate amount of loss reserves and correctly

predict future earnings taking into account their current product offering and competitors.

In order to keep up with competition, Frontline may also want to consider offering

wellness programs to their employees. Although weight management programs and smoking

cessation programs are not cost effective at the moment, they should keep them in mind as the

company continues to grow. Although they do have a small on-site gym, they may want to also

consider discounts on local gym memberships in order to keep the company’s employees as

happy and healthy as possible.

As far as communication is concerned, Frontline handles the enrollment process very

well. As previously mentioned, they provide summary plan descriptions for all of their

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 28/32

912619478 Frontline Technologies

912479299 Page 12

employees’ eligible plans during open enrollment. New employees are briefed as to what

benefits are offered and are encouraged to talk to the Human Resources manager, Colleen

Dewan, if they have any questions or concerns. The only recommendation related to the

communications process is related to the HIPAA privacy laws. Any employee who is responsible

for the bills of his/her adult dependents, cannot legally view said bills without written consent of

the dependent. This means a parent cannot see the bill for their child’s broken leg if he/she is

over the age of 18. This presents a problem to the employee and many are unaware of this law.

In order to improve this process, Frontline should brief all of their employees on the laws

surrounding HIPAA in order to avoid potential problems or complaints in the future.

The firm should also consider self-insuring their short-term and long-term disability

coverage as they approach one hundred employees. In order to do so they will need sufficient

data on past claims. They will also need to consider outsourcing some of the administrative

duties. This would only be worthwhile for the firm if it is indeed cost effective but may be worth

pursuing given the low number of employees and relatively low number of processed claims.

Conclusion

Frontline has seen rapid growth internally and financially over the past few years. It is

approaching one hundred employees and has some crucial decisions to make within the next one

to two years, many of them dealing with the possibility of self-insuring. After speaking with

many of their key decision makers as well as their broker, the company has a firm grasp on the

importance of offering fair and competitive benefits to its employees. It is vital to the company’s

culture that they continue to value the satisfaction of their employees as much as they do now. If

Frontline is true to its mission statement and business model, and is able to overcome the

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 29/32

912619478 Frontline Technologies

912479299 Page 13

obstacles it will likely face in converting to a self-insured approach, the future certainly is bright

for this young company.

The consultants would like to take this time to thank the management team and staff of

Frontline Technologies for the opportunity to review and comment on the benefits program at

your organization. We found the company to be a fascinating and compelling player in a highly

competitive market. We look forward to continuing to partner with your team to strive for a best

of breed compensation and benefits program that attracts and retains the best talent in your

market space.

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 30/32

912619478 Frontline Technologies

912479299 Page 14

Bibliography

Geisel, Jerry. "Self Funded Health Plans under Scrutiny." Business Insurance, 3 Mar.2011. Web.

09 Dec. 2011.

<https://blackboard.temple.edu/webapps/blackboard/content/contentWrapper.jsp?content

_id=_2421233_1>.

Halterman, Steven L. "Self Funding Health Insurance for Small Employers: Is It the Right Way

to Go?"

Https://blackboard.temple.edu/@@/BE9834EFD8AAC944CEF37E0E8DCC7028/course

s/1/Drennan_RMI205/content/_2421220_1/Self%20Funding%20for%20Small%20Emplo

yers.pdf . Employee Benefits Journal, Sept. 2000. Web. 1 Dec. 2011.

Pillsbury. "Health Care Reform Update: Changes Plan Sponsors Should Make This Year."

Pillsbury Law (2010). Client Alert, 8 Sept. 2010. Web. 1 Dec. 2011.

The Segal Company. "Keeping Health Funds Healthy: The Importance of Reserves." Newsletter

- Benefits, HR and Compensation Consulting July 2003. Print.

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 31/32

912619478 Frontline Technologies

912479299 Page 15

December 9, 2011

Colleen DewanHuman Resources ManagerFrontline Technologies

397 Eagleview Blvd.Exton, PA 19341

Dear Colleen,

We would like to begin by thanking you for taking time out of your busy schedule and meetingwith us last Wednesday, December 7. We also want to thank you for takings us on a tour of Frontline’s facilities and setting up the different meetings that we had there at Frontline. Weappreciate your willingness to help us out with our paper and we are extremely thankful for yourhelp.

We also ask that if you could pass along our gratitude toward Todd Orlando (the Chief FinancialOfficer), Matt Bachman (the Controller), and Kimberly Phelps (Senior Benefits Consultant fromElite Group) for also taking time to sit down and meet with us was well as making themselvesavailable to call them if we had any further questions after the interview was over.

We thank you once again for your help and we will be sending you a final copy of our paper foryou to look over. If you have any comments or questions regarding our paper feel free to contactone of us anytime you would like

Thank you.

Sincerely,

Matthew McGarveyChristopher Rockelman

8/2/2019 MATTHEW E MCGARVEY - FrontlineTechnologies.fall2011

http://slidepdf.com/reader/full/matthew-e-mcgarvey-frontlinetechnologiesfall2011 32/32

December 9, 2011

Roland ThompsonManaging PartnerFrontline Technologies

397 Eagleview Blvd.Exton, PA 19341

Dear Roland:

We would like to thank you for taking the time out of your schedule to sit down and talk with uslast Wednesday, December 7. It meant a lot to us that you would allow us to talk with you andlearn a little more about the history of Frontline. You helped us with a considerable amount of our paper. We greatly appreciated all that you had to say and we were fascinated with some of the stories you offered. Sitting down with you gave us a better understanding of Frontline as a

whole as well as the benefits offered by the company.

We will gladly send you a copy of our final paper for you to read over if you would like. Feelfree to contact us with any comments or concerns dealing with any of the information provided.Once again we truly are thankful for you sitting down and speaking with us. This paper wouldnot be possible without your help.

Thank you.

Sincerely,

Matthew McGarveyChristopher Rockelman