math 476/567: actuarial risk theory professor rick gorvett 374 altgeld hall university of illinois...

TRANSCRIPT

Math 476/567:Actuarial Risk Theory

Professor Rick Gorvett

374 Altgeld Hall

University of Illinois

at Urbana-Champaign

Fall 2015

Syllabus

• Office Hours: 3-4 pm Tuesdays, 3-4 pm Wednesdays, or by appointment

• Textbook: McDonald, Derivatives Markets, 3rd edition

• Exam dates: 3 exams, per syllabus

• Grades: Exams, homeworks, project, possible other assignments

Me

• Director of the UIUC Actuarial Science Program

• MBA (University of Chicago)

• Ph.D. in Finance (UIUC)

• FCAS: Fellow of the CAS

• ASA: Associate of the SOA

• CERA: Chartered Enterprise Risk Analyst

• Actuarial corporate / consulting experience

(I wish)

Class Objectives

• Understand the mathematical foundations

of stochastic processes and financial options

• Learn Exam MFE material

• Appreciate this material in a broad, cross-

disciplinary framework

Class Plan

• Option pricing theory

• Stochastic processes

– Brownian motion

• Stochastic simulation

• Interest rate modeling

Stochastic Processes

• Stochastic process: collection of random variables over time; X(t), where t is typically a time index; X(t) is the “state” of the process at time t.

• Examples:– “The drunk”– Coin tosses:

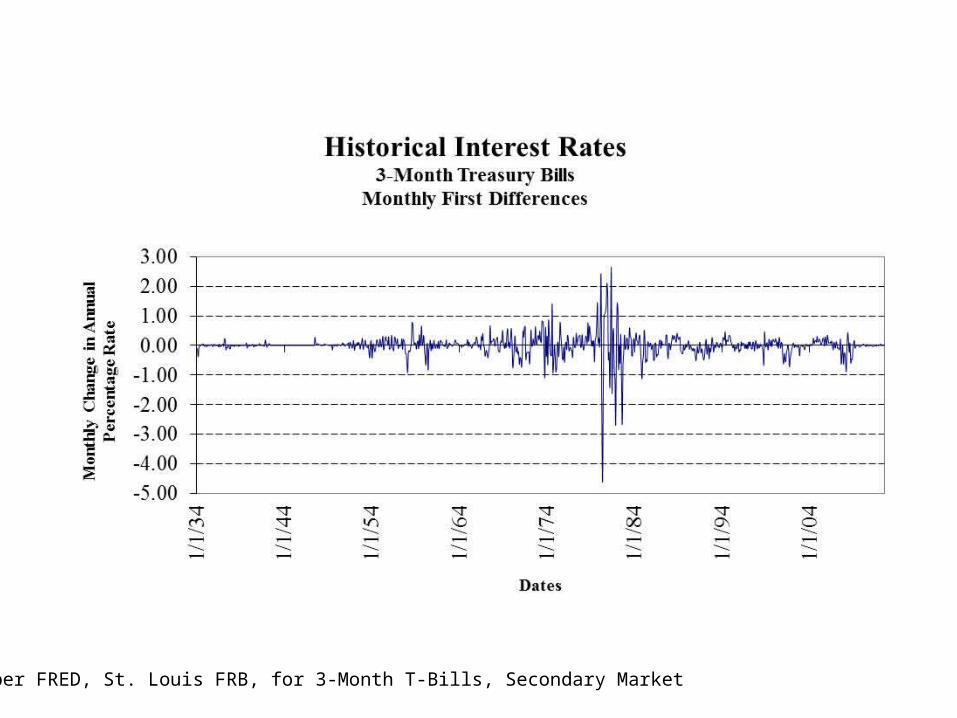

HTTHTHTHHTHT vs HHHHTTTTHHHT– Financial / economic series

Data per FRED, St. Louis FRB, for 3-Month T-Bills, Secondary Market

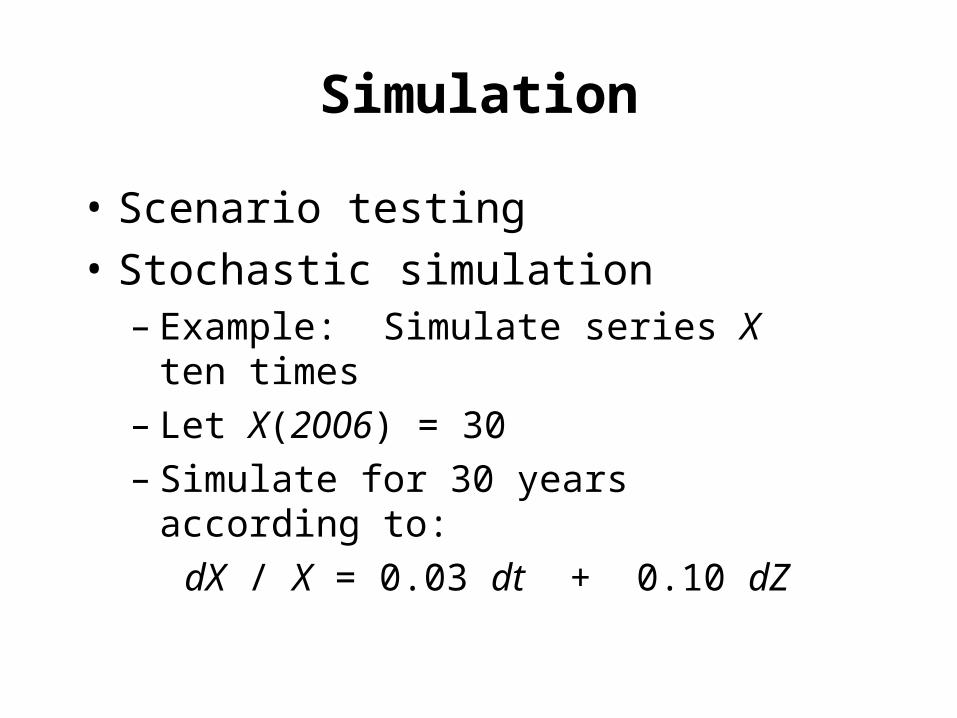

Simulation

• Scenario testing

• Stochastic simulation– Example: Simulate series X ten times– Let X(2006) = 30– Simulate for 30 years according to:

dX / X = 0.03 dt + 0.10 dZ

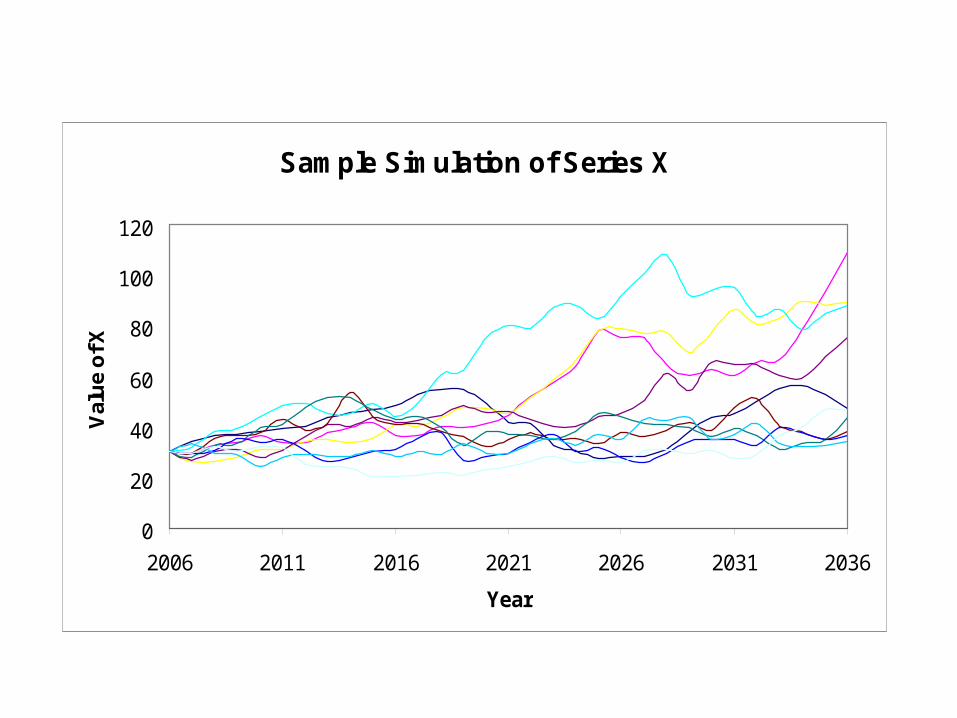

Sample Simulation of Series X

0

20

40

60

80

100

120

2006 2011 2016 2021 2026 2031 2036

Year

Val

ue

of X

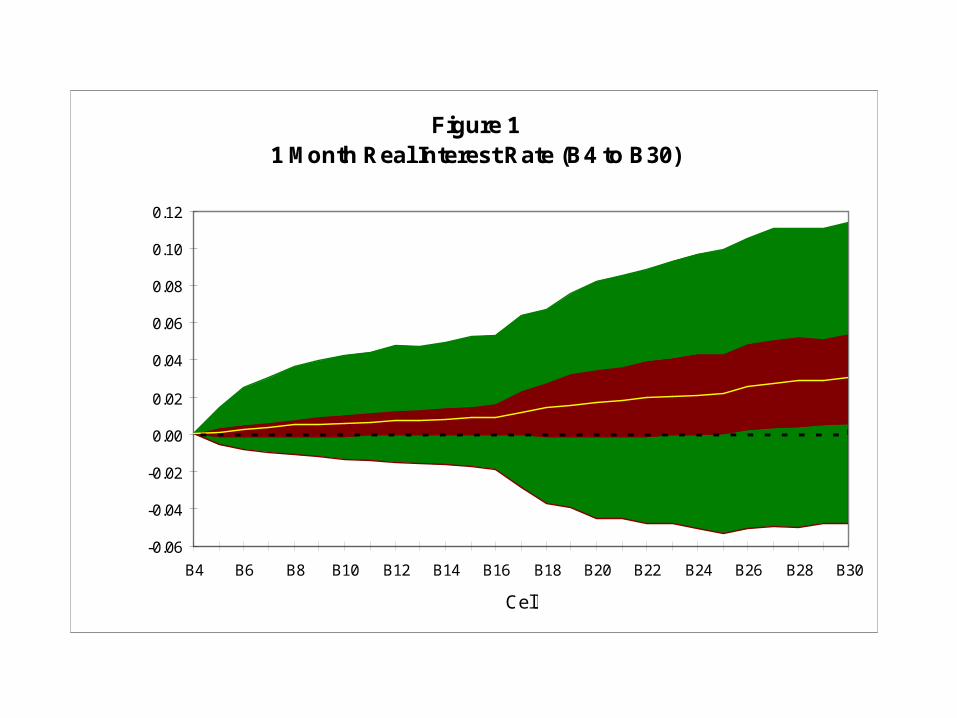

Figure 11 Month Real Interest Rate (B4 to B30)

-0.06

-0.04

-0.02

0.00

0.02

0.04

0.06

0.08

0.10

0.12

B4 B6 B8 B10 B12 B14 B16 B18 B20 B22 B24 B26 B28 B30

Cell

The Actuarial ScienceResearch Triangle

Mathematics

ActuarialScience

Finance

Stochastic Calculus /Ito’s Lemma

Financial Mathematics

PortfolioTheory

ContingentClaimsAnalysis

Fuzzy SetTheory

Markov ChainMonte Carlo

Chaos andComplexity

Theoryof Risk

DynamicFinancialAnalysis

InterestRateModeling

InterestTheory

Actuarial Science and Finance

• “Coaching is not rocket science.”

- Theresa Grentz, University of Illinois Women’s Basketball Coach

• Are actuarial science and financial mathematics “rocket science”?

• Certainly, lots of quantitative Ph.D.s are on Wall Street and doing actuarial-

or finance-related work• But….

Actuarial Science and Finance (cont.)

• Actuarial science and finance are not rocket science – they’re harder

• Rocket science:– Test a theory or design– Learn and re-test until successful

• Actuarial science and finance– Things continually change – behaviors, attitudes,….– Can’t hold other variables constant– Limited data with which to test theories

Why is this Option Stuff So Important?

PayoffOf CallOption

ST (Value of Underlying Asset)

X(Exercise price)

Insurance is an Option

PaymentUnderInsurancePolicy

ST (Size of Loss)X(Deductible)

A Sampling ofOptions

and Other Derivatives through History

Ancient Greece

“There is the anecdote of Thales the Milesian and his financial device… He was reproached for his poverty, which was supposed to show that philosophy was of no use. According to the story, he knew by his skill in the stars while it was yet winter that there would be a great harvest of olives in the coming year; so, having a little money, he gave deposits for the use of all the olive-presses in Chios and Miletus, which he hired at a low price because no one bid against him. When the harvest-time came, and many were wanted all at once and of a sudden, he let them out at any rate which he pleased, and made a quantity of money. Thus he showed the world that philosophers can easily be rich if they like, but that their ambition is of another sort…”

- Aristotle, Politics, Book One, Part XI

Phoenician Shipping

Merchants and ship-owners used options to hedge their ships and cargoes

Mesopotamia

Mercantile forward contracts, written in cuneiform on clay tablets, circa 1700 BC

China

Forward contracts on rice, entered into prior to planting, circa 2000 BC

Belgium and The Netherlands

• Antwerp and Amsterdam

• Grain

• Herring

• Tulips

Tulip Bubble

• Mid-1630s

• Tulip demand exploded and prices skyrocketed

• Options and futures were used to ensure price and supply

• Bubble burst in 1637

America

• 19th century– “Privileges”

– Non-standardized / over-the-counter

• Synthetic loans– Financier Russell Sage

– Put-call parity

– Get around usury laws

Chicago Board Options Exchange

• Began trading standardized options on April 26, 1973

• 911 contracts traded on first day (options on 16 different “underlying” companies)

CBOE and Options

“…any history of the excitement in finance in the 1960s and 1970s must mention the options pricing work of Black and Scholes (1973) and Merton (1973b). These are the most successful papers in economics – ever – in terms of academic and applied impact. Every Ph.D. student in economics is exposed to this work, and the papers are the foundation of a massive industry in financial derivatives.”

- Eugene F. Fama, “My Life in Finance,” arXiv

Modeling Underlying Assets

“…distributions of stock returns are fat-tailed: there are far more outliers than would be expected from normal distributions – a fact reconfirmed in subsequent market episodes, including the most recent. Given the accusations of ignorance on this score recently thrown our way in the popular media, it is worth emphasizing that academics in finance have been aware of the fat tails phenomenon in asset returns for about 50 years.”

- Eugene F. Fama, “My Life in Finance,” arXiv

Next Time

• Review of financial options

• Begin binomial option pricing theory