mastering market realities in global meat industry

TRANSCRIPT

Dr. David Hughes

Some Reflections on China and Global

Trends for Chicken and Other Meat Products

Emeritus Professor of Food Marketing

@profdavidhughes

World Population: Who's Going Up and Who’s Going Down?

2010 2030 2050

- billion-

World 6.9 8.2 9.0

Africa 1.0 1.5 2.0

Asia 4.1 4.8 5.1

Europe 0.7 0.7 0.7

LAC* 0.6 0.7 0.8

North America 0.3 0.4 0.5

Oceania 0.04 0.04 0.05

*Latin America & Caribbean

Source: UN (population scenario planning)

Asian Mega-Cities Dominate Globally by 2030

China 2030 Demographic Profile Strikingly Similar to Japan Profile Now!

China Gets Old Before It Gets Rich (with all the associated social and health problems).

What Does This Mean for Chinese Meat Consumption Market Dynamics?

Strong Growth in Global Meat Demand Projected to 2030

Source: Nan-Dirk Mulder, Rabobank, 2015

Source: FAO

But, Look Out for an Increasingly Volatile

International Price Environment for Meat

and for Feed Inputs

(US$/M.T.)

2012 2013 2014 2015 2016

Roller Coaster Global Dairy Prices

Buckle Up Seat Belts

Crash Helmets On!

FAO Global Food Price Index: 1961 to 2016*

Source: FAO * to October 31st, 2016, released November 10th, 2016

Source: The Economist , June 27th, 2015, from Lancet Commission

on Climate Change, UK, 2015

High Population, Food Insecure Countries Expand Staple Food Production

Into Increasingly Marginal Land with Less Predictable (Highly Variable) Yields

Input Industry and

Environmentalists

Tussle Over GM

Drought-Tolerant

Grains & Oilseeds

January 4th and again January 7th, 2016

Reflective Tweet

mid-2014

January 11th, 2016

May, 2016

Importance of Food in the CPI*, Selected Countries

Volatile Prices for Food Staples Will Have a Huge Impact on Demand for

Discretionary Premium Foods

* CPI Consumer Price Index

World Meat Consumption With & Without China, 2016*

Source: GIRA, FAO and Hughes * forecast

430 mill.t.% 312

Fish & Seafood 33 34

Pork 25 17

Poultry 25 32

Beef 15 15

Sheep/lamb 2 2Pork and fish/seafood are the dominant meats in China, with chicken a late starter

and a slowing rate of growth most recently reflecting safety concerns, dietary

preferences, income pressures, etc.

Source: Nan-Dirk Mulder, Rabobank, 2016

Approved by US FDA

November, 2015

32 linear metres x

4 shelves of eggs!

Wu Mart, Hangzhou,

China (Nov. 19th, 2016)

“Free Range” Eggs

Popular for Food

Safety Attributes NOT

for Bird Welfare

Hangzhou, China

Meal for Six

Apartment in

Ningbo, 2006

Meal for Seven.

Apartment in

Hangzhou, 2016

For the Global Meat industry, There May Be Storm Clouds Ahead!

Markets for Protein are MUCH MORE than Meat and

Red Meat is in the Firing Line from Messaniac Zealots

Peak Meat: Per Capita Meat Consumption

Static or Declining in Most Developed Countries

Health 58%

Saving money 21

Animal welfare concerns 20

Food safety concerns 19

Environmental concerns 11

Groups more pre-disposed to reduce meat consumption:

• Women

• Older consumers (65+ years)

Source: NatCen Survey of British Social Attitudes, February 2016

Wonderfully Dated!

Now, “What’s for Dinner?”:

• Chinese

• Pasta

• TakeawayGone .. the way of all flesh!

Or, Increasingly for Millennials “What’s Dinner?”!

1992

(October, 2015)

Backed by Well-Heeled

Investors

Plant-Based Egg and Meat

Analogues Have Market Traction

And Don’t Forget Insect Protein!

What’s the Demographic Scene Like in Some Higher Income “Western” Countries?

And What are the Implications for the Food & Grocery Industry?

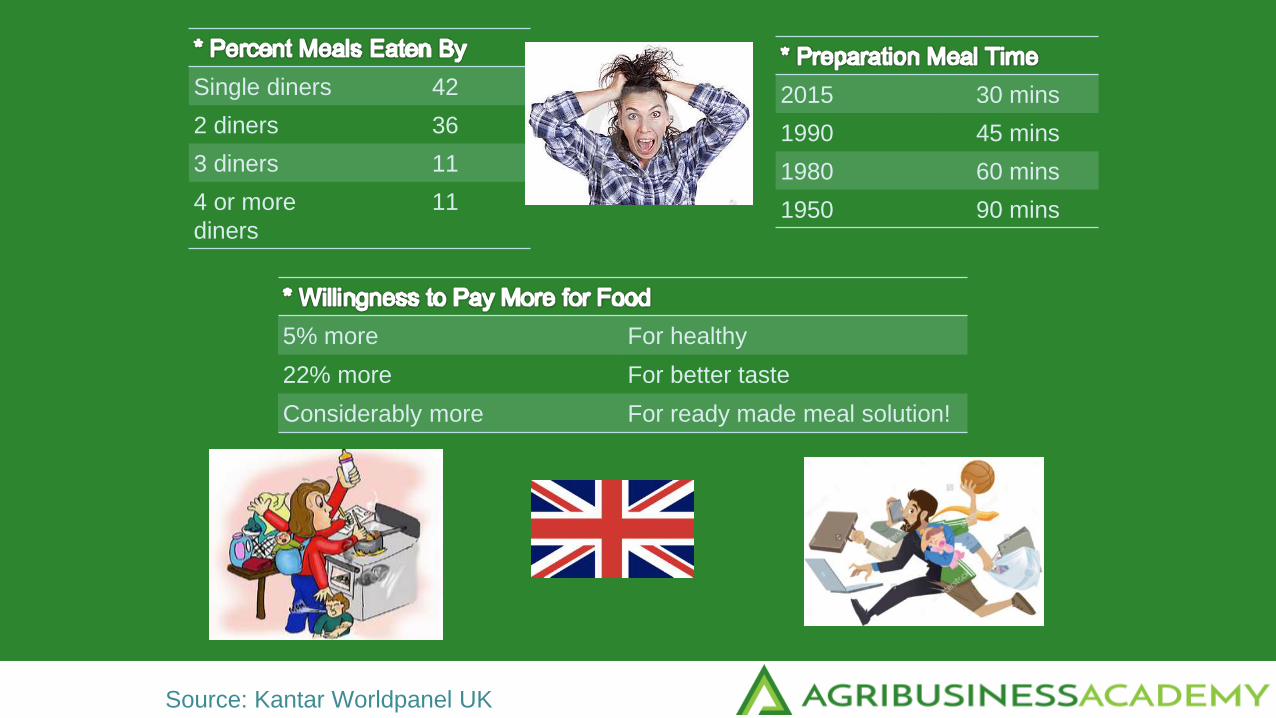

Single diners 42

2 diners 36

3 diners 11

4 or more

diners

11

2015 30 mins

1990 45 mins

1980 60 mins

1950 90 mins

5% more For healthy

22% more For better taste

Considerably more For ready made meal solution!

Source: Kantar Worldpanel UK

A One Person Portion Pack:

• 30+% of many high income

households are “solo” (1 person);

• salmon quick to cook and no mess;

• compelling health benefits;

• loved by ageing rich consumers

and women;

Albert Heijn’s “One-a-Day”

Egg Pack. Remember, 30+%

of Northern European urban

households are 1 person!

Increasing Complexity Driving Food Purchasing Behaviour

Consumers Want VALUE

but, increasingly, They

Want To Know Your About

VALUES

• savvy shopping

• local/national

- place of production

- care of local economy

- local is fresh/healthier

• provenance

• heritage

• sustainability

• animal welfare

• worker welfare

Source: Deloitte Inc. Food Value Equation Survey, 2015 and Hughes

“How’d You Like Your Meat?”

“With Adjectives, Please”:

• free-range ….;

• grass-fed

• free-from ..

• known provenance …

• Farmer Han ….

• Silkie ..

• rare breed …

• slow-growing …

• vegetarian diet …

• organic …..

• Omega-3 rich …...

• happy …

• environmentally-friendly …

Explosion of Premium Beef Brands for Export from Australia

The “Big 3” in USA:More ConvenienceStronger the Brand

Consumers Want

Adjectives in Their

Meat in Thailand

Consumers Want Their Meat “Free” Across the Globe!

And They Want Adjectives Added and Not Additives Added!

• Antibiotic-free

• Hormone-free

• Additive-free

• Campylobacter-free

• Salmonella-free

• E.coli-free

• GMO-free

• Free-range

• Gluten-free

• Woody breast-free

• Tropical rain forest devastation-free (beef from Brazil)

Bewildering Array of Labels

to Confuse the Shopper!

Source: “The O’Neill Report” on AMR, May, 2016 & The Economist (May 21-27th, 2016) and

The New Straits Times (August, 2016)

Scientists, Special Interest Groups,

Media Coalesce to Place Huge

Pressure on Global Meat Industry

(August 12th, 2016)

(August 12th, 2016)

Traceability in Meat: Home plus

in South Korea with TV Monitor

and Shoppers can Scan QR Codes

to Trace the Meat Back to the Farm

and Follow the Meat Story

Do Asian Consumers Differ From “Westerners” on Trends Relating to

Ingredients in Their Food Products? No!: Want to:

• recognise all ingredients on the label/list

• short and simple list

• natural/all natural*

• no artificial ingredients

• low or reduced fat/sugar/salt

• Asians much more aware of health attributes of food

• including “beauty” ingredients (e.g. Japan – collagen)

• but, simmering concerns about food safety aspects

• “Free From” trend not widespread

Source: Ingredion, 2015 and Hughes

* natural starch more acceptable than modified starch

The cost of Food FraudImpact of Food Fraud

Brand Damage• Tesco

Management

distraction• Fonterr

a (Melam

ine)

Legal costs• Fonterr

a (Botulis

m)

Increased Complianc

e• Meat Industry

(DNA testing)

Margin erosion• Tesco

Diminished Market

Share• Chipotl

e

The brands of Retailers, Food Service and Restaurants are reliant on all suppliers sharing the same level of integrity as the person whose brand and reputation is at stake.

Three Meal Solutions

For 2 People for £10.

That’s Tues-Thursday

sorted for RMB14/person

per meal – VERY good

value in the UK

The £10 (RMB85)

M&S Meal Deal

Food Retail and Food Service Converge

Types of Snacks Consumed in Past 30 Days, Globally and By Region

(Where’s the Egg On-the-Go Mini-Meals and Nibbles?!)

Source: Nielsen Global Snacking Report, 2014

A Rush of British Meat Snacks

Salmon Serious Competitor for PREMIUM MEATS in Global Meal & Snack Markets

• healthy

• calorie-controlled

• snack/mini-meal

• 5-a-Day claim

• simple ingredients

• convenient

• portable

• no refrigeration

• “fish-friendly”

• recyclable

• brand reassurance

• YES – it’s tasty

• and affordable!

Ticking the Trend Boxes

Four Major Factors Slowing Rate at Which

Value-Added Convenience Meat Products

Will Expand Market Share in Emerging Asian

Economies:

• Relatively Low Level of Household Income;

• Grandparents and Maids;

• Strong Family & Food Cultures in Asian Countries;

• Competitively-Priced Street Food.

But, From a Low Base, Convenience Meat Meals

and Snacks (particularly chicken) are Expanding

Rapidly!

Branded, Value-Added Chicken in China

7-11 is a serious

food service player

in Most Asian Markets.

- Market Cap Alibaba x3 Walmart

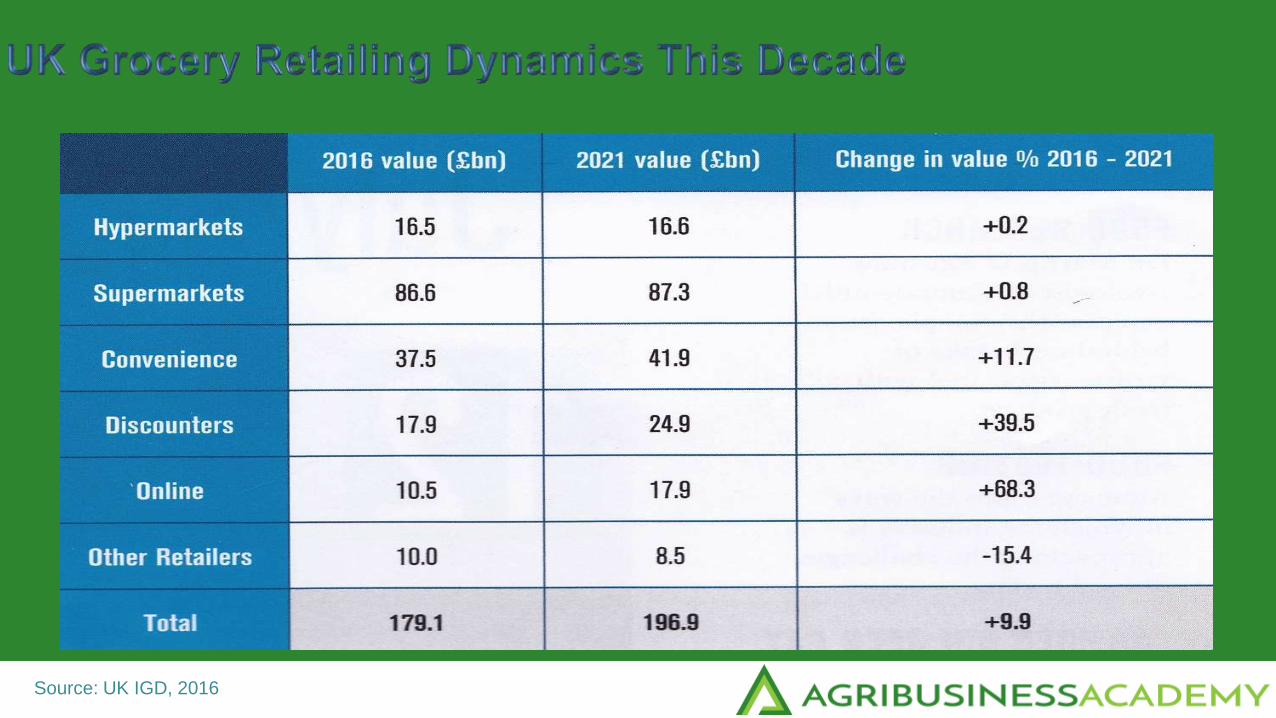

Source: UK IGD, 2016

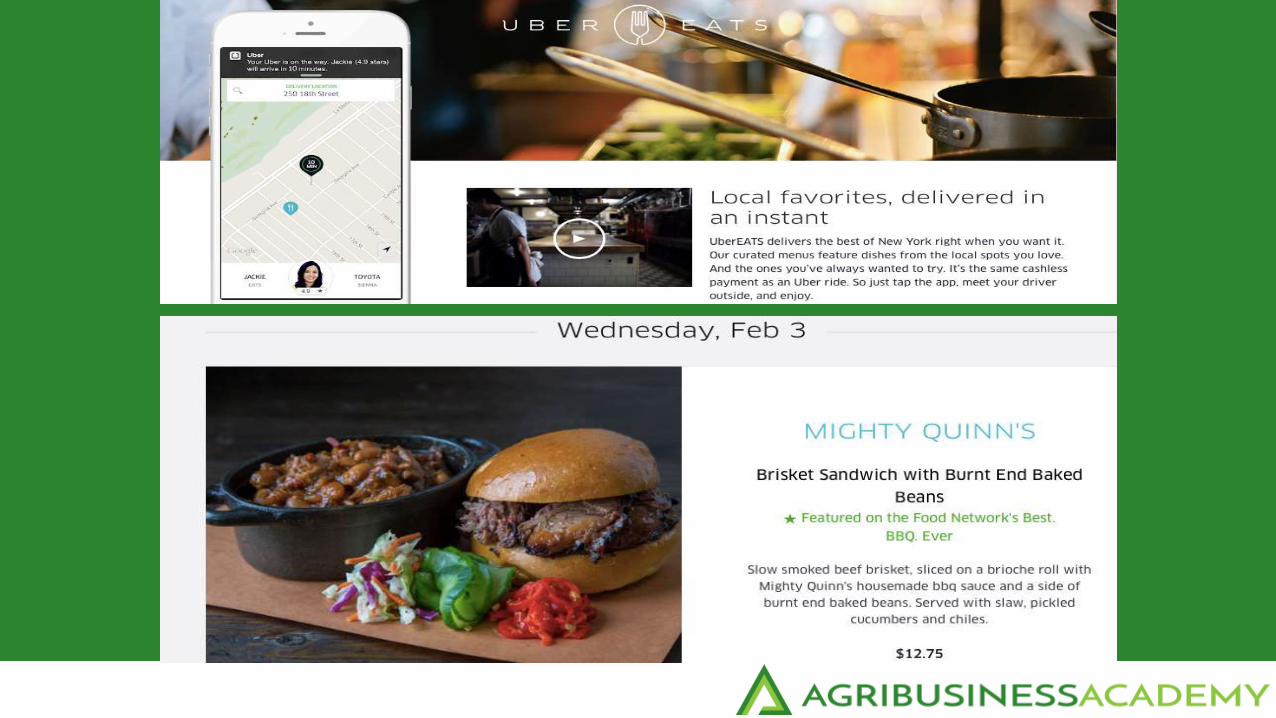

Retailers Target

Fast-Growing

Meal Kit Market

in UK

Raised US$500 Million in Venture Capital

Operating in 12 Countries To-Date

Some Examples of Sydney Restaurants Serviced by Deliveroo

• Globally, consumers less trusting of government, industry, “Big” Science, “Big” Farming, big anything!

• Pervasive media coverage of food scandals

• Shoppers want to know much more about where their food comes from & how animals/environment treated

• Most shoppers believe food companies should know “exactly” where everyingredient comes from

• Speed of social media communication both a blessing and a curse but, irrespective, a game changer

• Traceability & transparency in supply chains essential to building trust with all stakeholders. Understanding & compatibility with consumer values vitally important.

Source: Joanne Denney-Finch, IGD UK, October 8th, 2013, and Hughes

100% Purity is a Tough Ask! But Excellence in Supply Chain

Integrity is the Bed Rock of International Reputation for Food

Concluding Thoughts on Meat Marketing• meat demand (particularly chicken) will grow strongly this decade* - with

most of the growth coming in emerging markets )”peak meat” elsewhere

• expect strong competition from cheap farmed fish and, in the longer term, tasty, affordable plant protein products

• “commodity” chicken (noun) will struggle for good margin. Look for value-adding (adjectives) opportunities

• “slower-growing” chicken (more “natural”) with a story attract premiums

• meat “free-from” (antibiotics, hormones, cruelty) will become standard –no premium but penalty if not!

• emerging market consumers more focused on safe food than high animal welfare (in China, “green” relates more to food safety than environment

• expect more challenging business environment: more volatile feed prices, disease outbreaks, trade issues because of politics, economic boom/busts, etc.

• and for eggs (particularly for processing as demand for convenience

foods/snacks increase strongly

CONTACT POINTS:

e-mail:

Telephone contact:

mobile +44(0)7798 558276

@ProfDavidHughes

Consumer Blog: www.drfood.ca

Retail Blog: www.supermarketsinyourpocket.com