master trust market insight - health | aon€¦ · 6 master trust market insight chart 5: what form...

TRANSCRIPT

Master Trust Market InsightFebruary 2017

AonDefined Contribution | Delegated Services

Risk. Reinsurance. Human Resources.

Introduction

In the past five years the UK’s pension landscape appears

to have embraced the old adage that 'the only constant

is change'. While the goal of achieving the best possible

member outcomes has remained, with almost annual

changes to regulation and pension options, it’s starting to

feel like the playing field is continually shifting underfoot.

The government has introduced auto-enrolment, more

defined contribution (DC) scheme governance requirements,

charge caps and new pension freedoms, with the stated

intention of helping individual members find their unique

path to the best possible retirement outcomes.

While the intentions appear good and the theory seems

sound – increasing options can generally lead to greater

opportunity – these actions have also led to governance,

investment and administrative challenges. And, for trust-

based schemes, it has led to financial pressures and

difficulties associated with greater choice for members.

It is against this backdrop that master trusts are emerging

as a stable vehicle for DC provision and are increasing

in popularity. And, why not? Master trusts offer a

compelling combination of professional governance and

administration, investment options, improved member

engagement tools, flexibility, and communication for

members – thanks, in part, to embracing new technology.

They also use economies of scale to help keep costs down.

But, with over 100 master trusts now in existence in the UK,

there is increasing focus on the sustainability of the market.

Many expect a period of consolidation in the coming years,

which poses questions around the security of members’

benefits. Governance of master trusts is under scrutiny, too.

It is therefore no surprise that the government has proposed

new legislation covering the authorisation and supervision

of master trusts in the recent Pension Schemes Bill.

In light of all this, Aon undertook a survey of over 130

pension trustees, managers and employers to gain a better

understanding of what they see as the benefits, challenges

and opportunities of master trusts. By really understanding the

wants and needs of those considering a master trust, we can

make certain that the market evolves so that today’s DC savers

are well positioned for positive retirement outcomes in future.

We hope that you will agree that this is a timely report,

providing some helpful insights and analysis. If you would like

to discuss the findings in more detail, please get in touch.

Tony Britton Head of Aon Delegated DC Services [email protected] +44 (0)20 7086 2979

Milan Makhecha Principal [email protected] +44 (0)20 7086 8292

Aon 3

1. Growth in popularity of master trusts

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Some estimates indicate that there are over 100 master trusts in the

market today. Aon research* found that within five years, master trusts

could make up 13% of the DC pensions market, accounting for £70

billion in assets. Results of this survey seem to support these claims,

with 55% of respondents planning to use master trusts for at least

some part of their DC workforce within the next five years, compared

to only 37% of respondents that are using them today. (Chart 1)

Use a master trust for part of DC workforce 17% 34%

Use a master trust for all or part of DC workforce 20% 21%

Do not use master trusts — DB only 24% 20%

Do not use master trusts — GPP only 20% 18%

Do not use master trusts — own DC trust-based scheme 38% 25%

Q Now Q In 5 years

Chart 1: How much do master trusts feature in your current and future plans?

With the clear and sudden increase in the popularity of

master trusts it is worth asking why this has happened.

Throughout the survey our respondents consistently cited a

shift to professional governance as one of the most attractive

elements of moving to master trusts, and considered cost

and quality as key to choosing between them. They also saw

master trusts' potential to engage members through the

latest technology as a promising sign for the future.

The introduction of auto-enrolment by the Pensions

Act 2008, and its implementation since 1 January 2012, has

led employers into a whole new world of responsibility

and administration requirements. Add to this the pressures

of increased governance requirements laid down by the

Pensions Regulator (tPR) and the challenge of delivering

this within a charge cap and it is no surprise to see our

respondents list a shift to professional oversight as the

one of the most attractive aspects of master trusts.

Within five years, master trusts could make up 13% of the DC pensions market, accounting for £70 billion in assets

Respondents list a shift to professional oversight as the most attractive aspects of master trusts

* Aon Defined Contribution DC Survey 2015

4 Master Trust Market Insight

0% 10% 20% 30% 40% 50% 60% 70% 80%

Professional governance 75%

Reduced company/own trustee governance 75%

Ability to consolidate legacy plans 40%

Set up to accept all members 38%

Ability to offer decumulation solutions inside product 36%

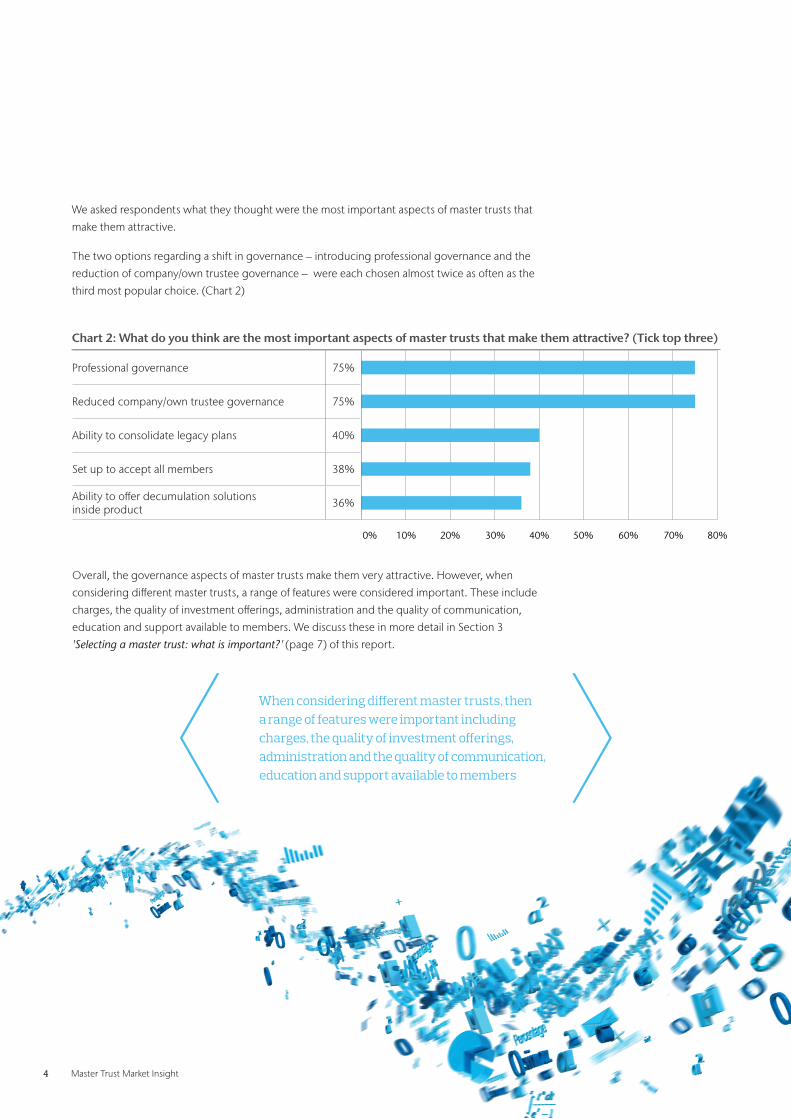

Overall, the governance aspects of master trusts make them very attractive. However, when

considering different master trusts, a range of features were considered important. These include

charges, the quality of investment offerings, administration and the quality of communication,

education and support available to members. We discuss these in more detail in Section 3

'Selecting a master trust: what is important?' (page 7) of this report.

Chart 2: What do you think are the most important aspects of master trusts that make them attractive? (Tick top three)

When considering different master trusts, then a range of features were important including charges, the quality of investment offerings, administration and the quality of communication, education and support available to members

We asked respondents what they thought were the most important aspects of master trusts that

make them attractive.

The two options regarding a shift in governance – introducing professional governance and the

reduction of company/own trustee governance – were each chosen almost twice as often as the

third most popular choice. (Chart 2)

Aon 5

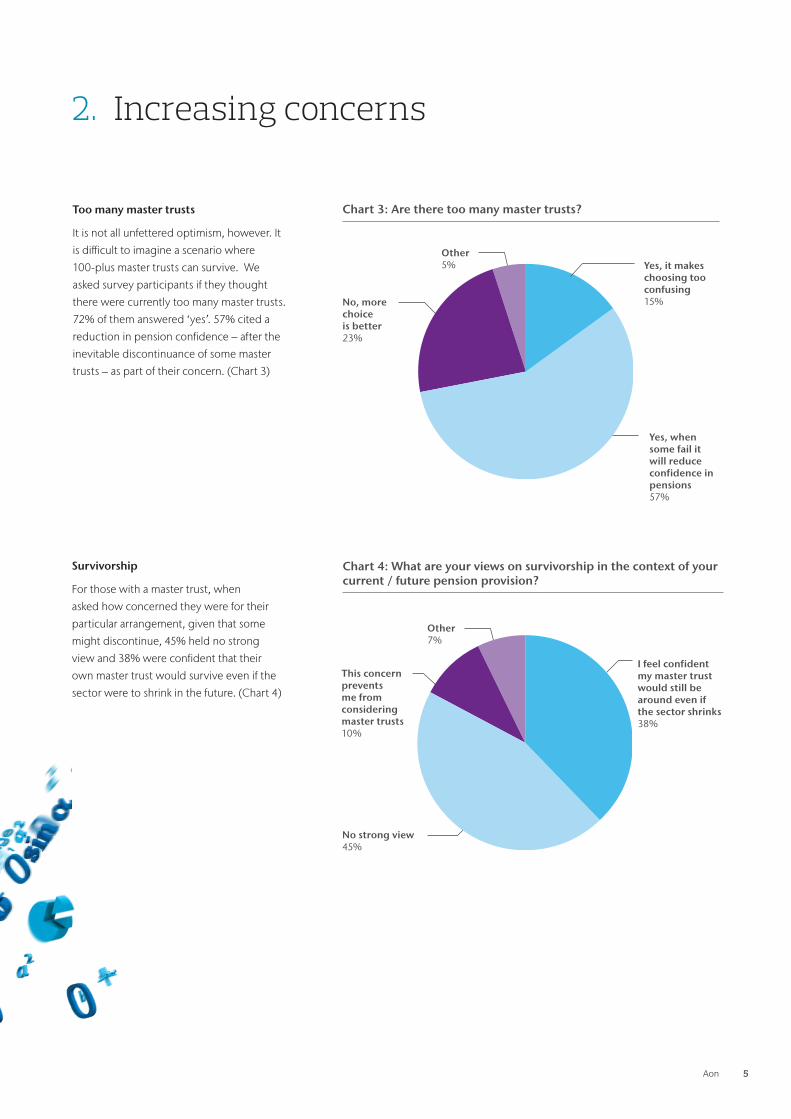

Too many master trusts

It is not all unfettered optimism, however. It

is difficult to imagine a scenario where

100-plus master trusts can survive. We

asked survey participants if they thought

there were currently too many master trusts.

72% of them answered ‘yes’. 57% cited a

reduction in pension confidence – after the

inevitable discontinuance of some master

trusts – as part of their concern. (Chart 3)

Chart 4: What are your views on survivorship in the context of your current / future pension provision?

Chart 3: Are there too many master trusts?

Survivorship

For those with a master trust, when

asked how concerned they were for their

particular arrangement, given that some

might discontinue, 45% held no strong

view and 38% were confident that their

own master trust would survive even if the

sector were to shrink in the future. (Chart 4)

Other 5%

Other 7%

No, more choice is better 23%

This concern prevents me from considering master trusts 10%

Yes, when some fail it will reduce confidence in pensions 57%

No strong view 45%

Yes, it makes choosing too confusing 15%

I feel confident my master trust would still be around even if the sector shrinks 38%

2. Increasing concerns

6 Master Trust Market Insight

Chart 5: What form would you like 'greater protections' to take in master trusts?

Chart 6: If you were looking to appoint a master trust, where would you start your search?

Other 4%

Other 4%

Regulation by the FCA, not TPR 21%

Would approach a number of consultancies to tender for selection 48%

Higher governance standards 22%

Third party evaluator 13%

The pensions media 2%

A levy on all master trusts to a central fund to pay out when or if a master trust fails 12%

Holding assets in escrow or similar to meet costs of exit 13%

Your existing DC benefit consultant 21%

A living will setting out how members will be protected on exit 15%

Holding capital to cover future events 13%

Your existing scheme provider 10%

Greater protections

However, these concerns are being

addressed. The recent Pension

Schemes Bill featured an authorisation

and supervisory regime, or 'greater

protections' for master trusts. What

exactly this will involve is yet to be seen

but our respondents – who share in these

concerns – had some ideas (their responses

were provided before the Pension

Schemes Bill was published). (Chart 5)

Interestingly, this provided one of the

most evenly split set of responses in the

whole survey, with ‘higher governance

standards’ and ‘regulation by the FCA’ the

slightly more popular options. The Pension

Schemes Bill will go some way to addressing

these varied concerns, but perhaps not all.

Managing conflicts

True to the spirit of the current pension

climate, most of our respondents wanted

to explore all the options and pick the best

trust for them. This was evident in the fact

that 48% of them declared they would

seek out a number of consultancies and

undergo a tendering process when looking

to appoint a master trust. (Chart 6)

They were also keen to keep it all above

board, with 83% having concerns around

potential conflicts of interest if they were

approached by their existing consultancy.

However, it is worth noting from our

prespective that 53% of respondents would

simply need reassurance about how the

conflicts are managed.

Most of our respondents wanted to explore all the options and pick the best trust for them

Aon 7

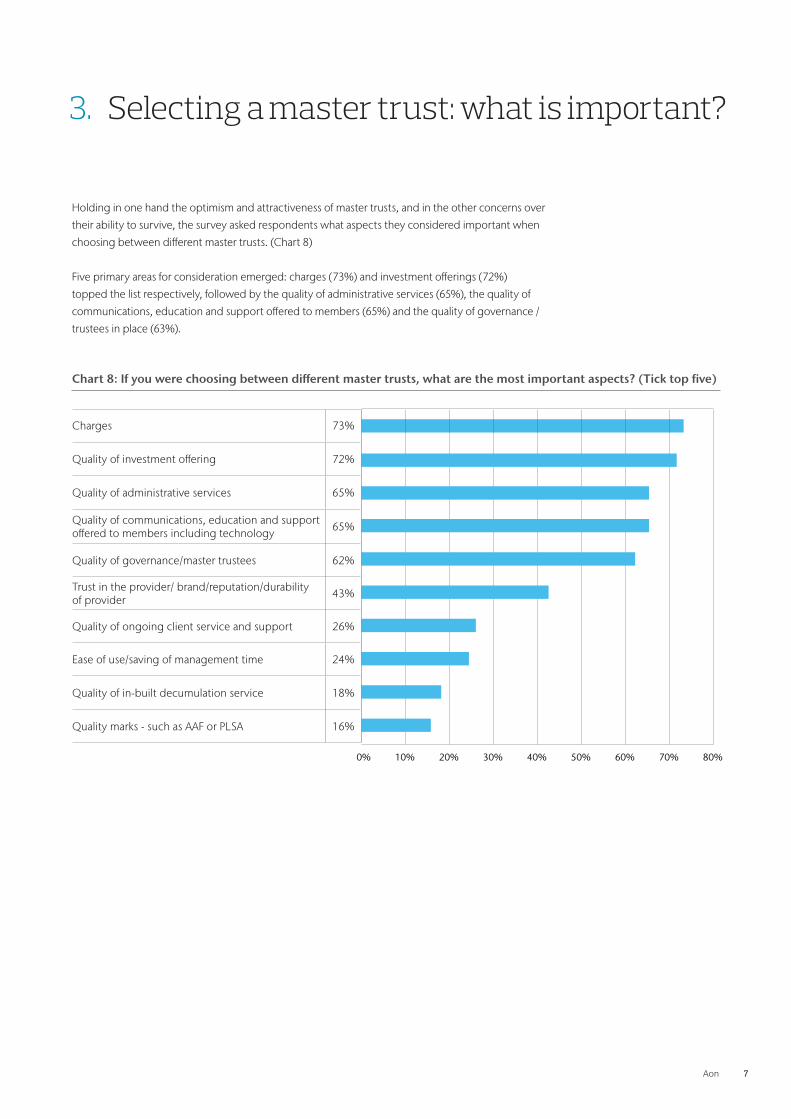

Holding in one hand the optimism and attractiveness of master trusts, and in the other concerns over

their ability to survive, the survey asked respondents what aspects they considered important when

choosing between different master trusts. (Chart 8)

Five primary areas for consideration emerged: charges (73%) and investment offerings (72%)

topped the list respectively, followed by the quality of administrative services (65%), the quality of

communications, education and support offered to members (65%) and the quality of governance /

trustees in place (63%).

0% 10% 20% 30% 40% 50% 60% 70% 80%

Charges 73%

Quality of investment offering 72%

Quality of administrative services 65%

Quality of communications, education and support offered to members including technology 65%

Quality of governance/master trustees 62%

Trust in the provider/ brand/reputation/durability of provider 43%

Quality of ongoing client service and support 26%

Ease of use/saving of management time 24%

Quality of in-built decumulation service 18%

Quality marks - such as AAF or PLSA 16%

Chart 8: If you were choosing between different master trusts, what are the most important aspects? (Tick top five)

3. Selecting a master trust: what is important?

8 Master Trust Market Insight

Charges

While we see an unsurprising focus on charges, it is encouraging to see the quality of the solution

provided by the master trust ranks nearly as highly. Offering charge-cap compliant and competitive

charges is clearly important for members. Add to this the level of competition in the master trust

market, and there is good value to be secured for members through a master trust arrangement.

However, it is equally important to provide a robust investment solution to help deliver good

member outcomes, and ideally one that offers a degree of future-proofing to stand the test of

time as regulations, markets and products change. The emphasis on administration services and

communication also highlights that these are seen as key to provide a quality, good value DC scheme.

Quality of investment offering

Being able to offer a future-proofed default strategy was

also seen as important; this helps to ensure that changes to

the default can be implemented easily and efficiently and is

something that master trust should be well placed to deliver.

Interestingly, respondents placed less emphasis on low

investment charges as a must have, preferring to be able

to offer members investment strategies that incorporate

best ideas and active management. And finally, there is a

clear message that offering a very large number of funds

is not important. (Chart 9)

Simplicity of communicating investment fund range to members' was considered important

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Simplicity of communicating investment fund range to members 80%

A future-proofed default strategy 73%

Ease of switching between funds 70%

Access to funds which incorporate best ideas for DC investing 66%

Inclusion of active management, where it adds value, within the default strategy 52%

A future-proofed range of funds 44%

Low investment charges, even at the expense of potentially better outcomes 42%

Ability to access the same fund range before and after retirement 38%

Inclusion of environment, social and governance factors within the strategy design 31%

Access to a very wide fund range - the number of funds matters more than the quality 15%

Access to individual managers including retail names 10%

Chart 9: In order to generate good member outcomes within a master trust, which elements of investment design / strategy do you believe are important?

Aon 9

Quality of communications, education and support offered to members

89% of respondents believe that their members

had limited or no interest in the structure

of their DC arrangement. (Chart 10)

Clearly, member engagement remains

an issue so it is little wonder it is ranked

in the top five of important aspects of

differentiating between master trusts.

Master trusts offer strong potential to solve the

engagement problem and member retirement

outcomes. Some of this potential comes from

the structure of the arrangement, but our

respondents said that the keys to their success

are the effectiveness of their design and use of

technology to communicate with members.

Respondents were almost unanimous in

considering technology within the design

of a master trust as either 'important'

or 'very important'. Almost half of them

reported that it would be a 'key part'

of their decision making. (Chart 11)

Chart 10: How much interest do you believe your members have in the structure of their DC arrangement (Trust-based, master trust, GPP etc)?

Other 1%

No interest 28%

Limited interest 61%

Interested and aware of the differences 10%

Respondents were almost unanimous in considering technology within the design of a master trust as either 'important' or 'very important'

0% 10% 20% 30% 40% 50%

Very important

The technology embedded within a master trust is a key part of my decision 48%

Important

I would consider technology amongst a range of other factors 49%

Not important The technology available would not influence my decision 3%

Chart 11: In your view, how important is technology within the design of a master trust?

10 Master Trust Market Insight

The results were similarly conclusive when discussing the

effectiveness of technology. (Chart 12)

Almost every area scored well but technology was highlighted

most as an effective means of ongoing communication and

giving members access to up-to-date account information.

Technology was highlighted most as an effective means of ongoing communication and giving members access to up-to-date account information

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Enabling members to access up-to-date information about their account 86%

As a portal for ongoing, routine scheme communication 82%

Access to pension planning tools 74%

Enabling members to carry out transaction activity eg. to switch funds 73%

Provision of educational material around pensions 62%

Delivering reminders / wake-up calls 51%

Wealth aggregation tool to facilitate pension planning / budgeting 39%

Chart 12: In selecting a master trust and being able to ensure good member engagement, how effective do you think technology is in each of the following areas?

Governance

Given that respondents had already

cited professional governance as one of

the most attractive elements of master

trusts, it is not surprising that 56% of

respondents considered it important that

the master trust trustee board includes

at least one independent, professional

trustee. What is perhaps more surprising

is that as many as 40% considered it ‘very

important’ that independent trustees

make up the entire board. (Chart 13)

Chart 13: How important do you believe it is that the master trust trustee board includes independent, professional trustees?

Very important All members of the master trust trustee board should be independent trustees 40%

Important At least one member of the master trust trustee board should be an independent professional trustee 56%

Not important The master trust trustee board does not need to include any independent trustee members 4%

56% of respondents considered it important that the master trust trustee board includes at least one independent, professional trustee

Aon 11

Respondents to our survey believe that 89% of their members have limited or no interest

in the structure of their DC provision, indicating that members rely on their employer to

select the right structure. This goes hand in hand with the results of Aon's 2016 DC Member

Survey, which suggests that members trust their employer when it comes to pensions.

Yet, the government's recent attempts to improve retirement outcomes for scheme members

– via automatic enrolment, more DC options, charge caps and new pension freedoms –

have introduced new pressures for employers. Many believe that master trusts can help

alleviate these pressures. They combine professional governance, administration, and

quality investment offerings as well as the potential to increase member engagement.

Many also believe that master trusts could help address this issue of member engagement by

focusing on their use of technology to communicate with members. By incorporating the latest

technology, master trusts have the ability to become the desired DC option for many schemes which

want to take advantage of their economies of scale, increased governance and administration.

While there are inevitable challenges and changes ahead — who will survive; what form 'greater

protections' will take – all the signs, including the results of this survey, point to master trusts

holding an increasingly important place in the provision of DC retirement savings in future.

Contact Tony BrittonHead of Aon Delegated DC Services +44 (0)20 7086 [email protected]

Milan Makhecha Principal Consultant+44 (0)20 7086 8292 [email protected]

Conclusion

About Aon Aon plc (NYSE:AON) is a leading global provider of

risk management, insurance brokerage and reinsur-

ance brokerage, and human resources solutions and

outsourcing services. Through its more than 72,000

colleagues worldwide, Aon unites to empower results

for clients in over 120 countries via innovative risk

and people solutions. For further information on our

capabilities and to learn how we empower results for

clients, please visit: http://aon.mediaroom.com.

© Aon plc 2017. All rights reserved.The information contained herein and the statements expressed are of

a general nature and are not intended to address the circumstances of

any particular individual or entity. Although we endeavor to provide

accurate and timely information and use sources we consider reliable,

there can be no guarantee that such information is accurate as of the

date it is received or that it will continue to be accurate in the future.

No one should act on such information without appropriate profes-

sional advice after a thorough examination of the particular situation.

Aon Hewitt Limited is authorised and regulated by the

Financial Conduct Authority. Registered in England & Wales.

Registered No: 4396810.

Registered Office:

The Aon Centre

The Leadenhall Building

122 Leadenhall Street

London

EC3V 4AN

www.aon.com

Risk. Reinsurance. Human Resources.

Aon Hewitt empowers organizations and individuals

to secure a better future through innovative talent,

retirement and health solutions. We advise, design

and execute a wide range of solutions that enable

clients to cultivate talent to drive organizational

and personal performance and growth, navigate

retirement risk while providing new levels of financial

security, and redefine health solutions for greater

choice, affordability and wellness. Aon Hewitt is a

global leader in human resource solutions, with over

35,000 professionals in 90 countries serving more

than 20,000 clients worldwide. For more information

on Aon Hewitt, please visit: aonhewitt.com

Follow Aon on Twitter: twitter.com/Aon_plc

Sign up for News Alerts:

http://aon.mediaroom.com/index.php?s=58

About Aon Hewitt