maruti shareholders-open-letter-iias-24 nov2015

TRANSCRIPT

Institutional Investor Advisory Services India Limited 15th Floor, West Wing, Dalal Street, Fort, Mumbai – 400 001

Phone +91 22 22721570 - 3 Fax: +91 22 2272 1574 www.iias.in CIN: U74990MH2010PLC204788

An open letter to the shareholders of Maruti Suzuki India

Limited

Allowing Suzuki to own the Gujarat plant and its manufacturing has implications that

extend beyond commercial arrangements. Suzuki is currently dependent on Maruti, but

allowing Suzuki to own the Gujarat plant will shift the balance of power in favour of Suzuki.

If the transaction is approved, Maruti will lose all control over its own destiny, and Maruti’s

shareholders will always remain subservient to the interest of Suzuki’s shareholders.

Equally important are the implications of such transactions on other family-run and MNCs

in India – they too may begin manufacturing in unlisted companies and allow the listed

company to merely trade.

24 November 2015

Dear Shareholder:

For a company with as strong a manufacturing track record as Maruti has, to willingly cede ground

to another manufacturer should be anathema - yet this is just what your company is proposing, by

allowing Suzuki to own the Gujarat plant. Make no mistake, this vote is about the shifting power

equation and whether shareholders will allow a manufacturer to continue to ‘manufacture and sell’

or let it shift gears, and ‘buy to sell.’ To put it simply, you - the shareholders of Maruti - need to

decide whether Maruti will continue to remain a manufacturer of cars or will it become a glorified

distributor.

Equally important are the implications of this vote on family run firms and on other MNC’s. If

shareholders agree to Suzuki doing owning the Gujarat plant, why should they not agree to the

Tata’s, Munjal’s, Mahindra’s or the Bajaj families proposing the same? Will Glaxo or Nestlé or

Holcim now set up fully owned subsidiaries and have their Indian arm only market the products?

If so, it will spell doom for the Indian equity markets.

About Maruti and this vote

Your company, Maruti currently has two facilities - in Gurgaon and in Manesar - which have a

combined capacity to manufacture 1.55 mn cars. Your company planned to expand its capacities

by setting up a third plant in Gujarat (1,500,000 cars annually – to be set up in a phased manner).

However, in early 2014, Maruti took us all by surprise when it announced that, Suzuki (and not

Maruti) will set up and own the Gujarat plant. Suzuki will manufacture the cars in Gujarat that will

be purchased by Maruti at cost and be sold under the Maruti product portfolio.

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 2 of 14

In order to execute this arrangement, your company now proposes to enter into two related party

transaction contracts with Suzuki Motor Gujarat Private Limited (SMGPL), a wholly-owned

subsidiary of Suzuki Motor Corporation (Suzuki), and as required by the Companies Act, 2013, is

seeking your approval for the following transactions:

i. Contract Manufacturing Agreement for manufacture and supply of vehicles for an initial

period of 15 years. All goods will be sold at cost by SMGPL to Maruti with no profit or loss for

SMGPL.

ii. Lease Deed for developing the plant on land owned by Maruti. As per the deed, SMGPL will

pay Maruti an annual aggregate rental of Rs.49.9 mn for the land an initial period of 15 years.

IiAS recommends that you vote AGAINST the resolution. Voting AGAINST this resolution

means that Maruti will own the Gujarat plant and not Suzuki – it will not result in any stoppage of

capacity creation at the Gujarat plant.

IiAS has had reservations about this deal since it was first announced in January 2014 and

continues to believe that the deal is not in Maruti’s long term interest. Our main contentions are:

Suzuki is squarely dependent upon Maruti for sales volumes and profits; owning the

Gujarat plant will limit Maruti’s growing criticality to the group

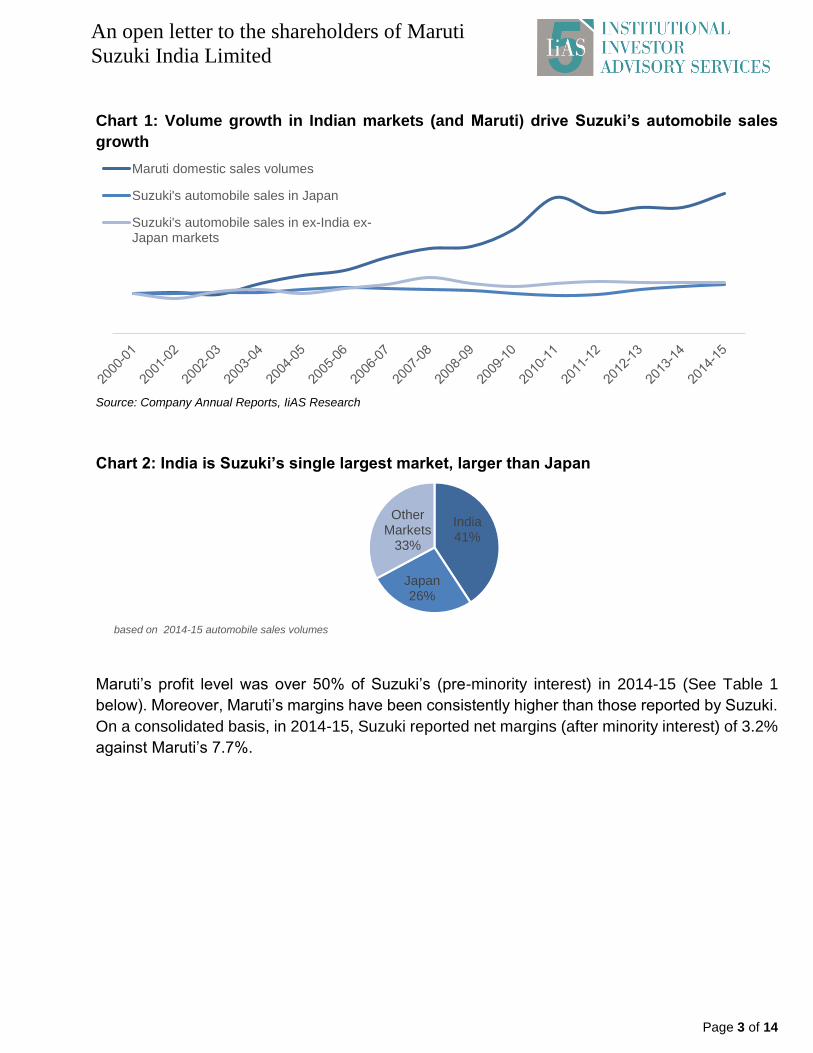

Suzuki is largely an automobile maker1; automobiles contributed to 89.5% of consolidated

revenues and 95.5% of (segment) profits in 2014-15. Suzuki’s automobile growth, and effectively

the company’s entire growth, over the past 15 years has emanated largely from Maruti’s growth.

Japan volumes have been almost flat and volumes in ex-India ex-Japan markets have also

reported limited growth. Maruti’s sales (including exports) accounted for 45% of Suzuki’s global

volumes and Maruti’s production accounted for 43% of Suzuki’s total automobile production

volumes in 2014-15. India, which is catered to solely by Maruti, has grown almost three times

faster than Suzuki’s sales volumes in Japan and the rest of the world (ex-India ex-Japan).

1 Other products include motorcycles, and marine and power products

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 3 of 14

Chart 1: Volume growth in Indian markets (and Maruti) drive Suzuki’s automobile sales

growth

Source: Company Annual Reports, IiAS Research

Chart 2: India is Suzuki’s single largest market, larger than Japan

Maruti’s profit level was over 50% of Suzuki’s (pre-minority interest) in 2014-15 (See Table 1

below). Moreover, Maruti’s margins have been consistently higher than those reported by Suzuki.

On a consolidated basis, in 2014-15, Suzuki reported net margins (after minority interest) of 3.2%

against Maruti’s 7.7%.

India41%

Japan26%

Other Markets

33%

based on 2014-15 automobile sales volumes

Maruti domestic sales volumes

Suzuki's automobile sales in Japan

Suzuki's automobile sales in ex-India ex-Japan markets

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 4 of 14

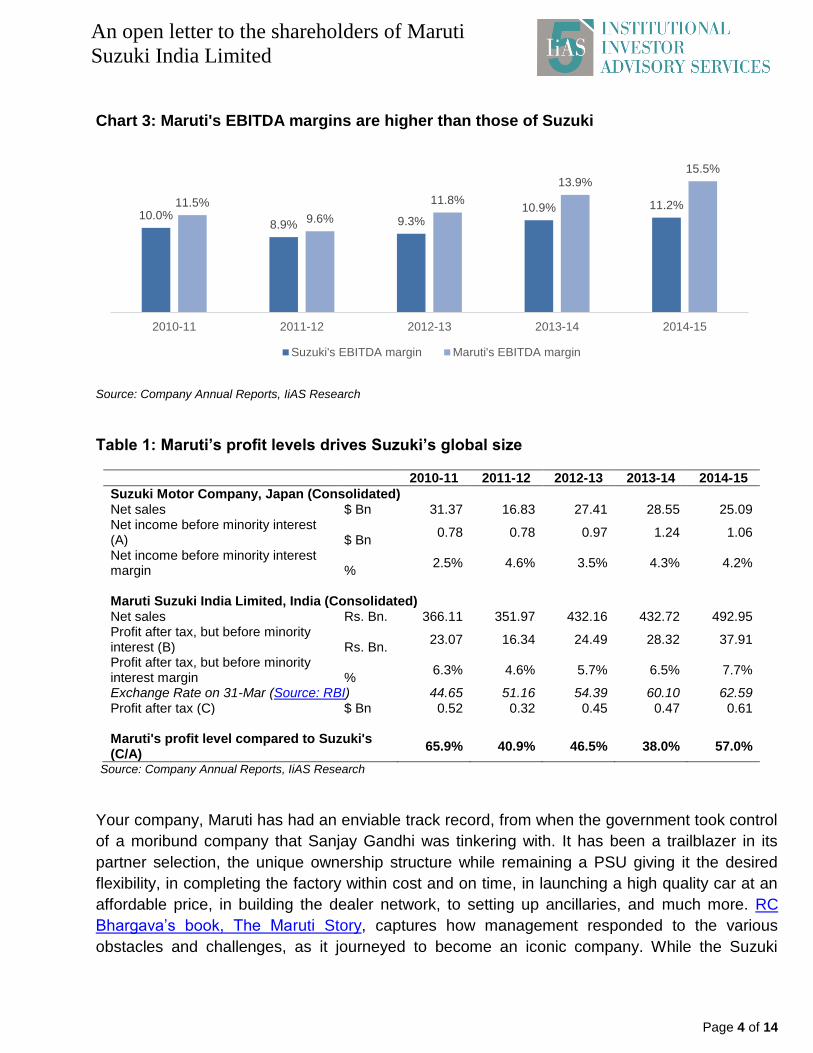

Chart 3: Maruti's EBITDA margins are higher than those of Suzuki

Source: Company Annual Reports, IiAS Research

Table 1: Maruti’s profit levels drives Suzuki’s global size

2010-11 2011-12 2012-13 2013-14 2014-15

Suzuki Motor Company, Japan (Consolidated) Net sales $ Bn 31.37 16.83 27.41 28.55 25.09 Net income before minority interest (A) $ Bn

0.78 0.78 0.97 1.24 1.06

Net income before minority interest margin %

2.5% 4.6% 3.5% 4.3% 4.2%

Maruti Suzuki India Limited, India (Consolidated) Net sales Rs. Bn. 366.11 351.97 432.16 432.72 492.95 Profit after tax, but before minority interest (B) Rs. Bn.

23.07 16.34 24.49 28.32 37.91

Profit after tax, but before minority interest margin %

6.3% 4.6% 5.7% 6.5% 7.7%

Exchange Rate on 31-Mar (Source: RBI) 44.65 51.16 54.39 60.10 62.59 Profit after tax (C) $ Bn 0.52 0.32 0.45 0.47 0.61

Maruti's profit level compared to Suzuki's (C/A)

65.9% 40.9% 46.5% 38.0% 57.0%

Source: Company Annual Reports, IiAS Research

Your company, Maruti has had an enviable track record, from when the government took control

of a moribund company that Sanjay Gandhi was tinkering with. It has been a trailblazer in its

partner selection, the unique ownership structure while remaining a PSU giving it the desired

flexibility, in completing the factory within cost and on time, in launching a high quality car at an

affordable price, in building the dealer network, to setting up ancillaries, and much more. RC

Bhargava’s book, The Maruti Story, captures how management responded to the various

obstacles and challenges, as it journeyed to become an iconic company. While the Suzuki

10.0%8.9% 9.3%

10.9% 11.2%11.5%

9.6%

11.8%

13.9%15.5%

2010-11 2011-12 2012-13 2013-14 2014-15

Suzuki's EBITDA margin Maruti's EBITDA margin

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 5 of 14

management was supportive, as was the government, it was the Indian management that ensured

that Maruti became the company it did, and in the process put India on the global auto map.

Suzuki has not seen this degree of success in any other market, not even in Japan, its home

market. With Maruti’s phenomenal success, it became critical to the group. Therefore, establishing

greater control over Maruti became equally critical. Suzuki first attempted to control Maruti by

wanting to own the Manesar plant. This decision was opposed by many Maruti executives,

including Mr. R C Bhargava – it was, in fact, Mr. R C Bhargava who convinced Osama Suzuki to

revise this decision. The decision to set up the Gujarat plant under Suzuki rather than Maruti

continues to reflect Suzuki’s need to establish greater ownership over Maruti. IiAS continues to

ask – what has changed now?

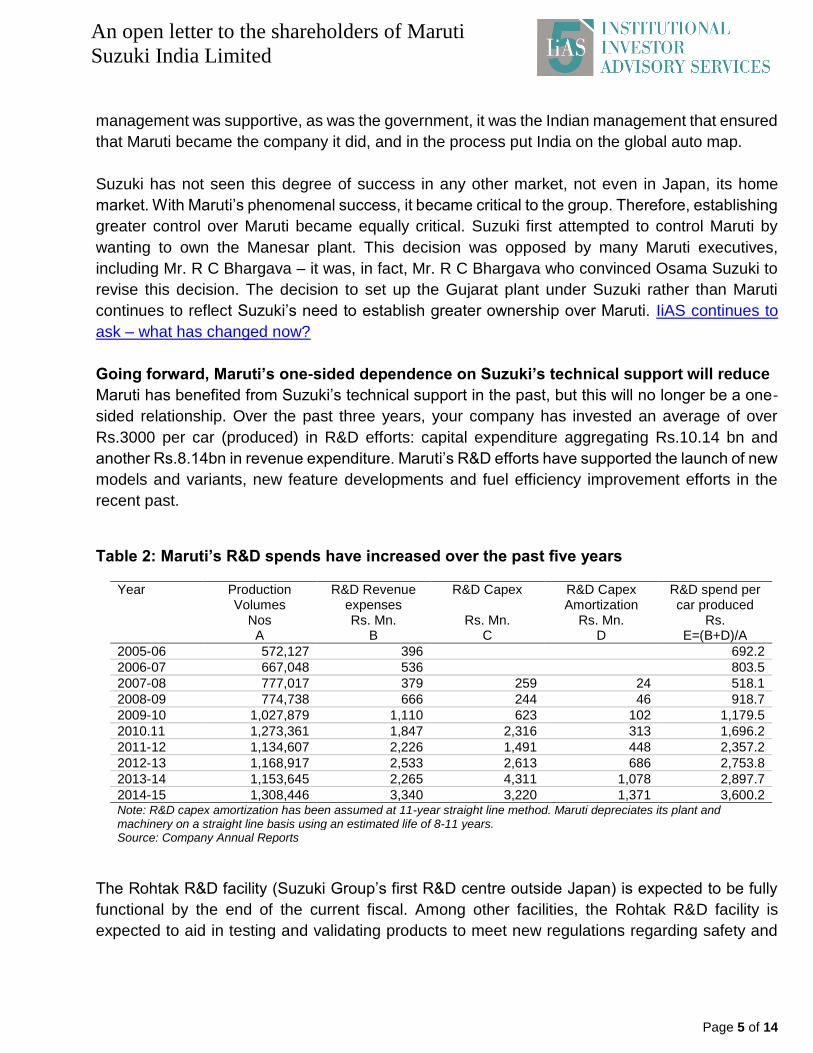

Going forward, Maruti’s one-sided dependence on Suzuki’s technical support will reduce

Maruti has benefited from Suzuki’s technical support in the past, but this will no longer be a one-

sided relationship. Over the past three years, your company has invested an average of over

Rs.3000 per car (produced) in R&D efforts: capital expenditure aggregating Rs.10.14 bn and

another Rs.8.14bn in revenue expenditure. Maruti’s R&D efforts have supported the launch of new

models and variants, new feature developments and fuel efficiency improvement efforts in the

recent past.

Table 2: Maruti’s R&D spends have increased over the past five years

Year Production Volumes

R&D Revenue expenses

R&D Capex R&D Capex Amortization

R&D spend per car produced

Nos Rs. Mn. Rs. Mn. Rs. Mn. Rs. A B C D E=(B+D)/A

2005-06 572,127 396 692.2

2006-07 667,048 536 803.5

2007-08 777,017 379 259 24 518.1

2008-09 774,738 666 244 46 918.7

2009-10 1,027,879 1,110 623 102 1,179.5

2010.11 1,273,361 1,847 2,316 313 1,696.2

2011-12 1,134,607 2,226 1,491 448 2,357.2

2012-13 1,168,917 2,533 2,613 686 2,753.8

2013-14 1,153,645 2,265 4,311 1,078 2,897.7

2014-15 1,308,446 3,340 3,220 1,371 3,600.2 Note: R&D capex amortization has been assumed at 11-year straight line method. Maruti depreciates its plant and machinery on a straight line basis using an estimated life of 8-11 years. Source: Company Annual Reports

The Rohtak R&D facility (Suzuki Group’s first R&D centre outside Japan) is expected to be fully

functional by the end of the current fiscal. Among other facilities, the Rohtak R&D facility is

expected to aid in testing and validating products to meet new regulations regarding safety and

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 6 of 14

environment. Most of Suzuki’s incremental investment in R&D facilities is largely being made in

India through Maruti. This is also why the company has publicly stated that royalty payouts for

newer models will be lower than the average 6% of sales that is being paid out currently.

IiAS believes that going forward, Suzuki will require Maruti’s R&D facilities and talent as much as

Maruti will require Suzuki’s product technology. With the relationship on product development

becoming less dependent and more co-dependent, Maruti must stand its ground and own the

Gujarat plant, rather than let Suzuki dictate terms.

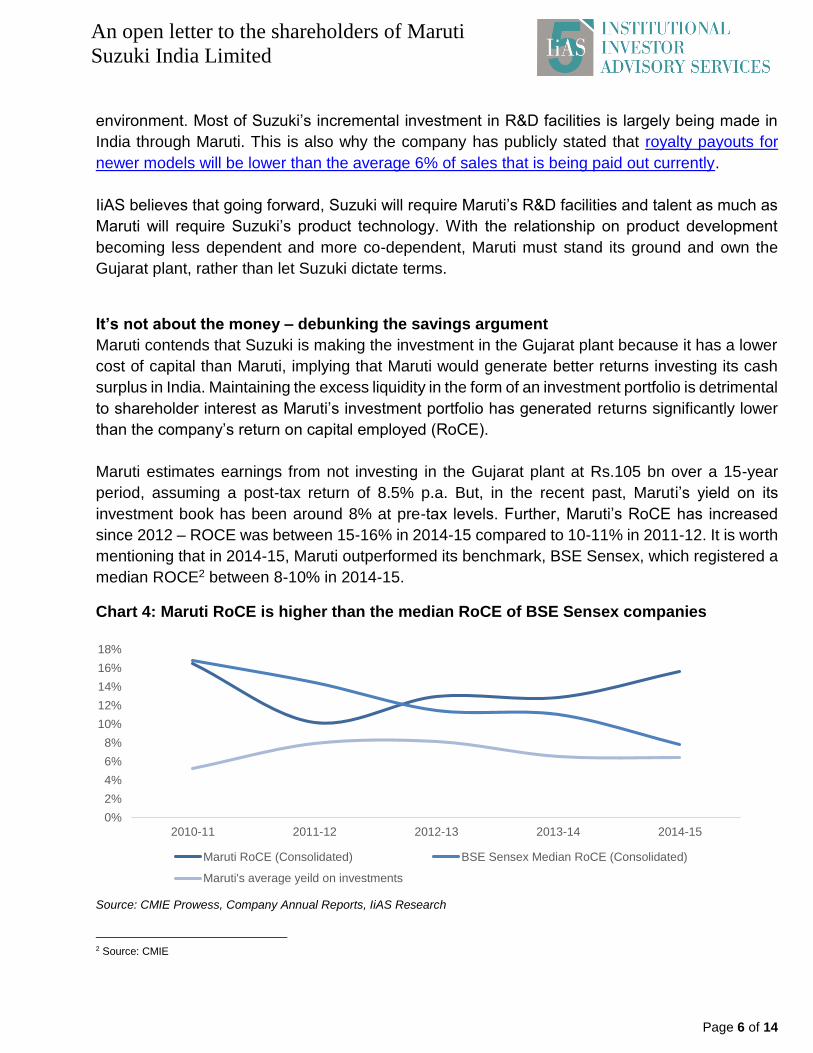

It’s not about the money – debunking the savings argument

Maruti contends that Suzuki is making the investment in the Gujarat plant because it has a lower

cost of capital than Maruti, implying that Maruti would generate better returns investing its cash

surplus in India. Maintaining the excess liquidity in the form of an investment portfolio is detrimental

to shareholder interest as Maruti’s investment portfolio has generated returns significantly lower

than the company’s return on capital employed (RoCE).

Maruti estimates earnings from not investing in the Gujarat plant at Rs.105 bn over a 15-year

period, assuming a post-tax return of 8.5% p.a. But, in the recent past, Maruti’s yield on its

investment book has been around 8% at pre-tax levels. Further, Maruti’s RoCE has increased

since 2012 – ROCE was between 15-16% in 2014-15 compared to 10-11% in 2011-12. It is worth

mentioning that in 2014-15, Maruti outperformed its benchmark, BSE Sensex, which registered a

median ROCE2 between 8-10% in 2014-15.

Chart 4: Maruti RoCE is higher than the median RoCE of BSE Sensex companies

Source: CMIE Prowess, Company Annual Reports, IiAS Research

2 Source: CMIE

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2010-11 2011-12 2012-13 2013-14 2014-15

Maruti RoCE (Consolidated) BSE Sensex Median RoCE (Consolidated)

Maruti's average yeild on investments

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 7 of 14

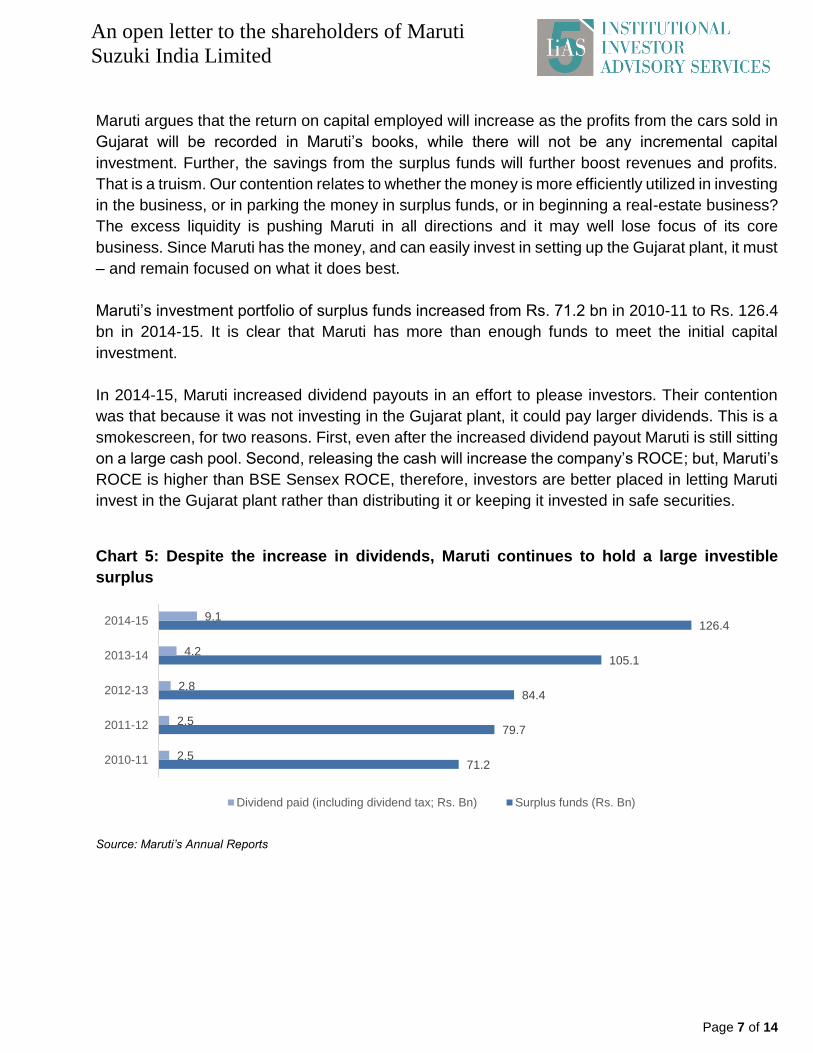

Maruti argues that the return on capital employed will increase as the profits from the cars sold in

Gujarat will be recorded in Maruti’s books, while there will not be any incremental capital

investment. Further, the savings from the surplus funds will further boost revenues and profits.

That is a truism. Our contention relates to whether the money is more efficiently utilized in investing

in the business, or in parking the money in surplus funds, or in beginning a real-estate business?

The excess liquidity is pushing Maruti in all directions and it may well lose focus of its core

business. Since Maruti has the money, and can easily invest in setting up the Gujarat plant, it must

– and remain focused on what it does best.

Maruti’s investment portfolio of surplus funds increased from Rs. 71.2 bn in 2010-11 to Rs. 126.4

bn in 2014-15. It is clear that Maruti has more than enough funds to meet the initial capital

investment.

In 2014-15, Maruti increased dividend payouts in an effort to please investors. Their contention

was that because it was not investing in the Gujarat plant, it could pay larger dividends. This is a

smokescreen, for two reasons. First, even after the increased dividend payout Maruti is still sitting

on a large cash pool. Second, releasing the cash will increase the company’s ROCE; but, Maruti’s

ROCE is higher than BSE Sensex ROCE, therefore, investors are better placed in letting Maruti

invest in the Gujarat plant rather than distributing it or keeping it invested in safe securities.

Chart 5: Despite the increase in dividends, Maruti continues to hold a large investible

surplus

Source: Maruti’s Annual Reports

71.2

79.7

84.4

105.1

126.4

2.5

2.5

2.8

4.2

9.1

2010-11

2011-12

2012-13

2013-14

2014-15

Dividend paid (including dividend tax; Rs. Bn) Surplus funds (Rs. Bn)

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 8 of 14

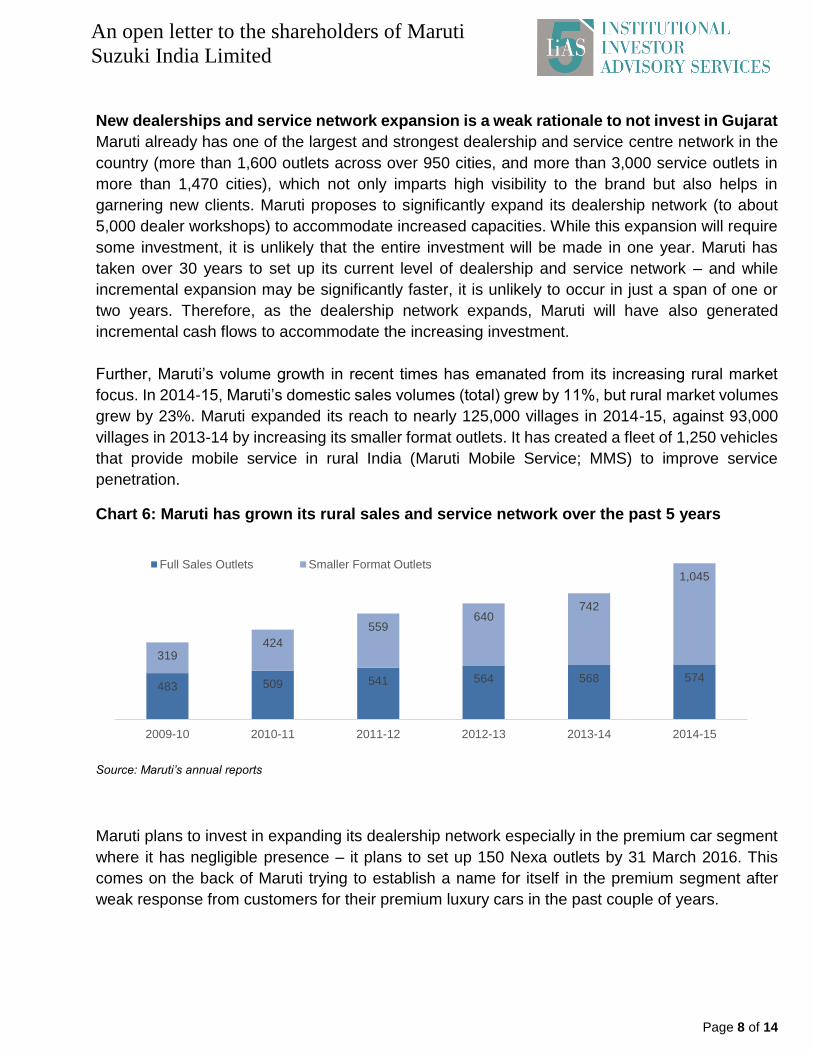

New dealerships and service network expansion is a weak rationale to not invest in Gujarat

Maruti already has one of the largest and strongest dealership and service centre network in the

country (more than 1,600 outlets across over 950 cities, and more than 3,000 service outlets in

more than 1,470 cities), which not only imparts high visibility to the brand but also helps in

garnering new clients. Maruti proposes to significantly expand its dealership network (to about

5,000 dealer workshops) to accommodate increased capacities. While this expansion will require

some investment, it is unlikely that the entire investment will be made in one year. Maruti has

taken over 30 years to set up its current level of dealership and service network – and while

incremental expansion may be significantly faster, it is unlikely to occur in just a span of one or

two years. Therefore, as the dealership network expands, Maruti will have also generated

incremental cash flows to accommodate the increasing investment.

Further, Maruti’s volume growth in recent times has emanated from its increasing rural market

focus. In 2014-15, Maruti’s domestic sales volumes (total) grew by 11%, but rural market volumes

grew by 23%. Maruti expanded its reach to nearly 125,000 villages in 2014-15, against 93,000

villages in 2013-14 by increasing its smaller format outlets. It has created a fleet of 1,250 vehicles

that provide mobile service in rural India (Maruti Mobile Service; MMS) to improve service

penetration.

Chart 6: Maruti has grown its rural sales and service network over the past 5 years

Source: Maruti’s annual reports

Maruti plans to invest in expanding its dealership network especially in the premium car segment

where it has negligible presence – it plans to set up 150 Nexa outlets by 31 March 2016. This

comes on the back of Maruti trying to establish a name for itself in the premium segment after

weak response from customers for their premium luxury cars in the past couple of years.

483 509 541 564 568 574

319424

559640

742

1,045

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Full Sales Outlets Smaller Format Outlets

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 9 of 14

Given this, how much investment does the Maruti expect to make in increasing its sales and

service outlets? IiAS believes that Maruti has sufficient funds to meet the requirements of

expanding and upscaling its sales and service network, and continue to invest in the Gujarat plant.

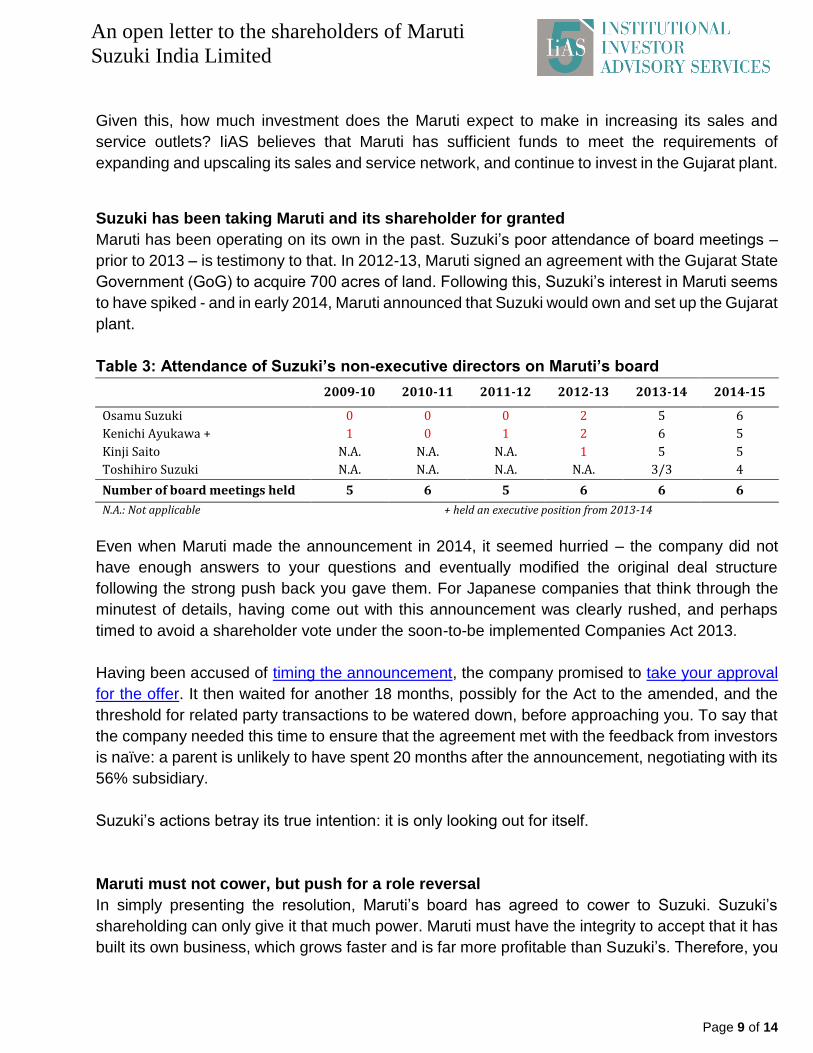

Suzuki has been taking Maruti and its shareholder for granted

Maruti has been operating on its own in the past. Suzuki’s poor attendance of board meetings –

prior to 2013 – is testimony to that. In 2012-13, Maruti signed an agreement with the Gujarat State

Government (GoG) to acquire 700 acres of land. Following this, Suzuki’s interest in Maruti seems

to have spiked - and in early 2014, Maruti announced that Suzuki would own and set up the Gujarat

plant.

Table 3: Attendance of Suzuki’s non-executive directors on Maruti’s board

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Osamu Suzuki 0 0 0 2 5 6

Kenichi Ayukawa + 1 0 1 2 6 5

Kinji Saito N.A. N.A. N.A. 1 5 5

Toshihiro Suzuki N.A. N.A. N.A. N.A. 3/3 4

Number of board meetings held 5 6 5 6 6 6

N.A.: Not applicable + held an executive position from 2013-14

Even when Maruti made the announcement in 2014, it seemed hurried – the company did not

have enough answers to your questions and eventually modified the original deal structure

following the strong push back you gave them. For Japanese companies that think through the

minutest of details, having come out with this announcement was clearly rushed, and perhaps

timed to avoid a shareholder vote under the soon-to-be implemented Companies Act 2013.

Having been accused of timing the announcement, the company promised to take your approval

for the offer. It then waited for another 18 months, possibly for the Act to the amended, and the

threshold for related party transactions to be watered down, before approaching you. To say that

the company needed this time to ensure that the agreement met with the feedback from investors

is naïve: a parent is unlikely to have spent 20 months after the announcement, negotiating with its

56% subsidiary.

Suzuki’s actions betray its true intention: it is only looking out for itself.

Maruti must not cower, but push for a role reversal

In simply presenting the resolution, Maruti’s board has agreed to cower to Suzuki. Suzuki’s

shareholding can only give it that much power. Maruti must have the integrity to accept that it has

built its own business, which grows faster and is far more profitable than Suzuki’s. Therefore, you

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 10 of 14

must insist that Suzuki have representation from Maruti on its board as well. In fact, given that

Maruti has demonstrated a stronger manufacturing capability that Suzuki, it must begin to own all

new plants that Suzuki sets up, rather than the other way around.

Shareholders must see through the razzle dazzle and ask – why do all of this at all?

The discussion on the Gujarat plant has been focused squarely towards the details of the

arrangement, including pricing structures and royalty payment. But the larger question remains

unanswered: why have this structure in the first place? IiAS believes that you, as Maruti’s minority

shareholders, must cut through the noise, and focus on the more material decision: Why should

you allow Maruti cede more control to Suzuki? Will Maruti generate better shareholder returns by

investing in the Gujarat plant, or by earning ‘higher-than-Japanese’ returns by leaving the money

in bank deposits or even in rolling out a dealership network? The answer is obvious.

On the Gujarat plant vote, our reservations stem from the fact that the proposal unnecessarily

complicates Maruti’s business model. Following the Gujarat transaction, the control over a large

part of its operations and cash flows would move significantly to Suzuki Japan. The balance of

power, already in favor of Suzuki, will tilt completely towards them. Over time, Suzuki could

undermine the criticality of Maruti and significantly increase the importance of SMGPL, bringing in

newer technologies, and expanding capacities: Maruti will, over time, cease to have any control

over its own destiny.

The Indian operation is the jewel in Suzuki’s portfolio. However, given that it is held as a 56.2%

subsidiary, implies Suzuki’s own share price does not reflect the full value of its Indian business.

By setting up a facility in Gujarat and manufacturing cars and then selling these to Maruti to

distribute, Suzuki hopes to directly capture a greater portion of the Indian businesses valuation in

its share price rather. We believe what Suzuki shareholders will gain – and make no mistake -

they will, you will lose.

Your vote is twice as valuable, exercise it

The dates of Maruti’s postal ballot are given below:

Outcome Date: 17 December 2015

Receipt Deadline: 15 December 2015, 5:00 PM

Notice Date: 27 October 2015

E-Voting Site: www.evoting.karvy.com

E-voting Period: 16 November 2015, 9:00 AM to 15 December 2015, 5:00 PM

Postal Ballot Notice Available on the BSE website

An open letter to the shareholders of Maruti

Suzuki India Limited

Page 11 of 14

Your company has given its rationale for this structure in its explanatory note and details on its

website. Our perspective, of course, is different.

You should be aware that e-voting is possible, so unlike the traditional show of hands, each vote

will count. So, it is important that you vote. But that’s not all. This is a related party transaction.

What it means is that Suzuki does not get to vote, but you do. Given Suzuki’s ~56.2% ownership,

only the remaining ~43.8% votes can be cast implying your one share equals 2.2 votes. In other

words as a shareholder, you can now punch well above your weight.

We hope you will take the above into account the above and exercise your vote.

Yours sincerely,

Please also read IiAS’ previous research on Maruti Royalty flows in Suzuki’s blood 19-Oct-2015

Why should it be any different now? 11-Sep-2014

Maruti launches the razzmatazz 09-Jun-2014

Minority shareholders get their say 15-Mar-2014

Legal Recourse for Maruti Investors 14-Mar-2014

Has Maruti timed its announcement? 07-Mar-2014

Maruti must invest in the Gujarat plant, not Suzuki 04-Mar-2014

Has Suzuki short-changed Maruti? 04-Feb-2014

Gujarat announcement weighs against Maruti's minority shareholders 28-Jan-2014

Royalty Payments and minority shareholders 24-Sep-2013

Disclaimer This document has been prepared by Institutional Investor Advisory Services India Limited (IiAS). The information contained

herein is solely from publicly available data, but we do not represent that it is accurate or complete and it should not be relied

on as such. IiAS shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent

error in the information contained in this report. This document is provided for assistance only and is not intended to be and

must not be taken as the basis for any voting or investment decision. The user assumes the entire risk of any use made of

this information. Each recipient of this document should make such investigation as it deems necessary to arrive at an

independent evaluation of the individual resolutions referred to in this document (including the merits and risks involved). The

discussions or views expressed may not be suitable for all investors. The information given in this document is as of the date

of this report and there can be no assurance that future results or events will be consistent with this information. This

information is subject to change without any prior notice. IiAS reserves the right to make modifications and alterations to this

statement as may be required from time to time. However, IiAS is under no obligation to update or keep the information current.

Nevertheless, IiAS is committed to providing independent and transparent recommendation to its client and would be happy

to provide any information in response to specific client queries. Neither IiAS nor any of its affiliates, group companies,

directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or

consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The

disclosures of interest statements incorporated in this document are provided solely to enhance the transparency and should

not be treated as endorsement of the views expressed in the report.

Confidentiality This information is strictly confidential and is being furnished to you solely for your information. This information should not be

reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole

or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a

citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication,

availability or use would be contrary to law, regulation or which would subject IiAS to any registration or licensing requirements

within such jurisdiction. The distribution of this document in certain jurisdictions may be restricted by law, and persons in

whose possession this document comes, should inform themselves about and observe, any such restrictions. The information

provided in these reports remains, unless otherwise stated, the copyright of IiAS. All layout, design, original artwork, concepts

and other Intellectual Properties, remains the property and copyright of IiAS and may not be used in any form or for any

purpose whatsoever by any party without the express written permission of the copyright holders.

IiAS Voting Policy IiAS' voting recommendations are based on a set of guiding principles, which incorporate the basic tenets of the legal

framework along with the best practices followed by some of the better governed companies. These policies clearly list out

the rationale and evaluation parameters which are taken into consideration while finalizing the recommendations. The detailed

IiAS Voting Guidelines are available at www.iias.in/IiAS-voting-guidelines.aspx. The draft report prepared by the analyst is

referred to an internal Review and Oversight Committee (ROC), which is responsible for ensuring consistency in voting

recommendations, alignment of recommendations to the IiAS’ voting criteria and setting and maintaining quality standards of

IiAS’ proxy reports. Details regarding the functioning and composition of the ROC committee are available at www.iias.in. In

undertaking its activities, IiAS relies on information available in the public domain i.e. information that is available to public

shareholders. However, in order to provide a more meaningful analysis, IiAS, generally seeks clarifications from the subject

company. IiAS reserves the right to share the information provided by the subject company in its reports. Further details on

IiAS policy on communication with subject companies are available at www.iias.in.

Analyst Certification The research analyst(s) for this report certify/ies that no part of his/her/their compensation was, is or will be, directly or indirectly

related to specific recommendations or views expressed in this report. IiAS’ internal policies and control procedures governing

the dealing and trading in securities by employees are available at www.iias.in.

Conflict Management IiAS and its research analysts may hold a nominal number of shares in the companies IiAS covers (including the subject

company), as on the date of this report. A list of IiAS’ shareholding in companies is available at www.iias.in.

However, IiAS, the research analyst(s) responsible for this report, and their associates or relatives, do not have

actual/beneficial ownership of one per cent. or more securities of the subject company, at the end of the month immediately

preceding the date of publication of this report. A list of shareholders of IiAS as of the date of this report is available at

www.iias.in. However, the preparation of this report is monitored by an internal Review and Oversight Committee (ROC) of

IiAS and is not subject to the control of any company to which such report may relate and which may be a shareholder of IiAS.

Other Disclosures IiAS further confirms that, save as otherwise set out above or disclosed on IiAS’ website (www.iias.in):

IiAS, the research analyst(s) responsible for this report, and their associates or relatives, do not have any financial interest

in the subject company.

IiAS, the research analyst(s) responsible for this report, and their associates or relatives, do not have any other material

conflict of interest at the time of publication of this report.

As a proxy advisory firm, IiAS provides subscription, databased and other related services to various Indian and

international customers (which could include the subject company). IiAS generally receives between INR 10,000 and INR

25,00,000 for such services from its customers. Other than compensation that it may have received for providing such

services to the subject company in the ordinary course, none of IiAS, the research analyst(s) responsible for this report,

and their associates or relatives, has received any compensation from the subject company or any third party for this

report.

None of IiAS, the research analyst(s) responsible for this report, and their associates or relatives, has received any

compensation from the subject company or any third party in the past 12 months in connection with the provision of

services of products (including investment banking or merchant banking or brokerage services or any other products and

services), or managed or co-managed public offering of securities of the subject company.

The research analyst(s) responsible for this report has not served as an officer, director or employee of the subject

company.

None of IiAS or the research analyst(s) responsible for this report has been engaged in market making activity for the

subject company.

About IiAS

Institutional Investor Advisory Services India Limited (IIAS) is a proxy advisory firm, dedicated to providing participants in the Indian market with independent opinion, research and data on corporate governance issues as well as voting recommendations on shareholder resolutions for over 600 companies. To know more about IIAS visit www.iias.in Office Institutional Investor Advisory Services 15th Floor, West Wing, P J Tower, Dalal Street, Fort, Mumbai - 400 001 India Contact [email protected] T: +91 22 2272 1570-3 F: +91 22 2272 1574