marketing management of iffco -...

TRANSCRIPT

111

CHAPTER 4

MARKETING MANAGEMENT OF IFFCO

4.1 Marketing Management 4.2 Sustainable and Efficient Fertilizer Marketing Strategy 4.2.1 Target and Achievement 4.2.2 Market Awareness 4.2.3 Stock Arrangement 4.2.4 Proper and Timely Placement 4.2.5 Harvesting Market Situation 4.2.6 Accessories 4.3 Fertilizer Transportation and Distribution Channel 4.4 Pricing Policies 4.5 Social, Ecological Aspects of Marketing 4.6 Fertilizer Industry Challenges and Opportunities in Changing Scenario 4.7 Discussion and Conclusion.

112

MARKETING MANAGEMENT OF IFFCO

Fertilizer Market is very complex phenomenon and its proper understanding

by each and every marketing employee is crucial to attain successes and efficiency

in marketing operation. In Fertilizer marketing sector where farmer is the ultimate

customer and user of the product, Fertilizer Marketing is some one different from

other marketing. IFFCO which deals only in cooperatives and Fertilizer are

distributed to the farmer by the cooperative societies either in cash or in credit basis.

Therefore, study of cooperatives societies, farmers purchasing behaviour and their

purchasing power is very important to manage efficient Fertilizer marketing while

IFFCO is concern.

4.1 Marketing Management:

The first principle of marketing management is that the compare must have an

active attitude toward the market. It can’t expect customers to buy a product simply

because it is produced. The management must actively study the market, persuade

customers, promote the product and organize distribution.

Marketing Management is an important operative function (as distinct from

managerial function) of management. It performs all managerial functions in the field

of marketing. It is responsible for planning, organizing, directing and controlling the

marketing activities. It is required to build up appropriate marketing-mix to achieve

the objectives of the business. The basis goals of marketing are satisfaction of

needs of customers and generation of revenue for the business. The marketing

manager looks after various aspects of marketing to achieve the objectives of

113

marketing viz., creation of customers and satisfaction of their wants and earning of

profits

As the Fertilizer scenario has been changing very fast since last 10 years and

nowadays the market has become highly competitive IFFCO has already reworked

its marketing strategy oriented to meet contemporary challenges and yet retaining

the philosophy of IFFCO, service to the farmers and strengthening the cooperatives.

Therefore, sustainable and efficient Fertilizer marketing strategy with reference to

IFFCO is given hereunder.

4.2 Sustainable Fertilizer Marketing Strategy:

Marketing of any product is complex phenomenon but Fertilizer marketing is

somewhat different from any other marketing. More than 70% population of India is

under Farming community of different level of living standards. Their needs are

different and purchasing powers vary from place to place. The crop cultivation is

quite different in same state of same crop. The Fertilizer consumption is directly

related to irrigation potentiality of the area and the crops which are being cultivated

there. Crops under cereals like rice, wheat, sorghum require more nutrients than

pulse crops. Likewise tuber crop like potato is heavy feeder crop. Plantation crop

like sugarcane, cash crop like cotton and tobacco which are grown in some pockets

need more fertilization than cereals and pulses.

In Chhattisgarh, 80% cultivated area under rice and rest 20% area include the

crops like lakhadi, chickpea, maize, urd, moong and wheat crops. Out of total

cultivated area only 26% area under assured irrigation and rest comes under rain fed

114

conditions where annual precipitation is near 750 mm but their distribution is very

uneven. Therefore, farmers are always fearful in so far as rainfall is concerned.

Therefore, in state like Chhattisgarh the scope of Fertilizer consumption is not

so encouraging. During the year 2003-04, the Fertilizer consumption was recorded

38.80 Kg./hectare which is very low, while national Fertilizer consumption is 100

Kg./hectare. As mentioned earlier, the Fertilizer consumption pattern varies from

district to district and also block-wise among the districts. For example, Janjagir

district where irrigation facilities are better than other districts, having Fertilizer

consumption 93.60 Kg/hectare followed by Dhamtari and Raipur.

4.2.1 Target

In Marketing field target fixation is very important. It is directly associated with

our aggressiveness to achieve the success. Target of Fertilizer distribution for the

area/district/state has to finalized on the following criteria—

1. Potentiality of the area.

2. Last Best Sales.

3. Marketing Cost.

4. Competitors.

5. Government Fertilizer policy.

Potentiality of the Area:

It includes the irrigation facilities, which type of crops are being raised by the

farmers, credit facilities and socioeconomic status of the area. For example, in

Janjagir district, irrigated area is about 80% and during kharif season, rice is main

115

crop while wheat crop is grown in large area in rabi season. Both the crops—rice

and wheat cereal crops require more fertilization. While in Durg cultivated area is

more than Janjagir district but irrigation is limiting factor, therefore, Fertilizer

consumption is lesser in Durg than Janjagir district. Therefore, it is must to first

workout the potentiality of the area while fixing the Fertilizer sales targets.

Last Best Sales Data:

Present Fertilizer sales planning is associated with the last year sales data of

the particular area. For justified planning one has to workout the last three years

sales and best sales of the last years.

Marketing Cost:

Government of India has been withdrawing the subsidy on Fertilizer since the

year 1992. Before the year 1992 all the Fertilizers were being distributed as per the

Government dispatches instructions under Essential Commodity Act. The difference

between the cost of production and distribution rates to the farmers is much more in

India and that heavy amount is borne by government of India that is called subsidy

which was directly given to the Fertilizer producers. But after August 1992,

government has changed their policy and huge amount of subsidy has been

withdrawing every year. Now Fertilizer producers and suppliers are free to sale their

produce every where in India. Therefore, Fertilizer manufacturers now have to

decide the areas of Fertilizer marketing which comes under economic zones. This

adhoc subsidy is given by government of India only on phosphatic and potassic

fertilizers. Urea still comes under ECA.

116

Therefore, cost effectiveness is the very important factor while determining

the sales target. The area which is very potential but marketing cost of that area is

comparatively high it requires more attention before fixing the sales targets.

Presently, phosphatic and potassic Fertilizers are decontrolled. Urea

Fertilizer is partially controlled by the Central Government and as such its distribution

is decided by them. Therefore, ECA allocation is fixed by the government of

controlled urea which is subsidized by the government.

Uncontrolled share of production needs marketing on those areas which are

economically suitable for manufacturers. For example, NPK and DAP Fertilizer plant

of IFFCO is situated in Kandla in Gujrat. Therefore, West Zone of India comprises of

Gujrat, Maharastra, Madhya Pradesh and Chhattisgarh states come under economic

zone for selling phosphatic Fertilizer as per IFFCO’s marketing is concerned. Two

urea producing plants are situated in Aonla near Bareilly and Phulpur near Allahabad

in Uttar Pradesh. Therefore, uncontrolled share of urea of both the plants are

economically viable in north and some part of central India like Uttar Pradesh, Bihar,

Panjab, Hariyana, Rajasthan, Delhi states. In Chhattisgarh most part of the

controlled IFFCO urea comes from Phulpur plant and their ECA allocation vary in

between 30 and 40 thousand metric tones. IFFCO may be interested to sale some

quantity of free urea in those districts which are near to Phulpur plant. Therefore,

marketing cost play a very key role for fixing the target for particular area.

Competitors:

Very sharp eyes on competitors’ activities and their planning are very much

essential. One should have very vigilant in market to get the information. Brand

117

Loyalty of the particular product among the farmers of a particular area plays

important role which set the sales target. For example, IFFCO NPK (12-32-16)

complex Fertilizer is very popular among the farmers of West Zone. In Chhattisgarh

district like Ambikapur, Jashpur, Bilaspur, Durg, Mungeli have very much demand of

IFFCO NPK (12-32-16) and IFFCO urea. Therefore, IFFCO is very cautious to plan

their distribution of above Fertilizers in these districts.

Government Fertilizer Policy:

IFFCO is a cooperative institution and its produce is only sold to the farmers

through cooperatives. IFFCO don’t sale its Fertilizers in Private Sector, that is,

private traders/dealers. Cooperative Sector is governed by the state government

and its Fertilizer distribution policy play very important role to harvest the sales

volume of Fertilizer of particular state. In State like Chhattisgarh where

cooperatives are not so economically sound and are depend on funds on state Apex

Banks and Nabard Banks. Therefore, district-wise cooperative banks viability is

limited factor while selling of Fertilizer through cooperatives. For example, district

like Raigarh, Ambikapur, Jashpur, where cooperative banks and their primary

agriculture cooperative societies are functionless due to poor economic conditions,

whereas IFFCO Fertilizers especially IFFCO NPK (12-32-16) Fertilizer is very-very

popular among the farmers of these districts. Therefore, to meet out the farmers

demand IFFCO has to sale their products through Indian Agro Marketing

Cooperative Limited (IAMCO). IAMCO is a cooperative organization that has been

permitted to open their cash sale centers in whole districts of Chhattisgarh for

Fertilizer cash sales.

118

4.2.1 Sales Target Achievement:

Marketing means achievement of sales targets at reasonable marketing cost.

Success of marketing achievement depends on the following factors—

1. Market Awareness

2. Stock Arrangement

3. Proper and Timely Placement

4. Harvesting Marketing Situation.

4.2.2 Market Awareness:

Market awareness is first tool to lineup the marketing system. For market

awareness one should has updated regarding marketing channels running in the

area, what are the potential pockets of Fertilizer consumptions. Demand of farmers

and their expectations should be kept in mind regularly. Knowledge of competitors’

activities and their planning is also required attention for achieving the targets. In

spite of that regular promotional work should be carried out for development of

existing market and for creating new market.

4.2.3 Stock Arrangement:

Proper and timely stocking prior to season is very essential for best output of

sales. As per need of the area one should has to decide that what product is to be

stocked in advance and which Fertilizer may be arranged at the time of sale season.

Stock quantity and their time have to work out on the lifting pattern. Place of stock

either in rake point buffer godowns or in feeder warehouse is also point of similar

importance.

119

4.2.4 Proper and Timely Placement:

Proper and timely placement of the stock to the sale points assures the sales

success which is largely depend on the transporting facilities and the destinations of

feeding. Therefore, transportation is very vital and essential factor to achieve the

sale goals. IFFCO is operating 6 rake points in the state. Although Durg is having

rake point facility but IFFCO is not operating this rake point due to the reason of

marketing cost. In Durg, Fertilizer is fed from Rajnandgaon, Raipur and Bilaspur

Rake points. Therefore districts like Durg where own rake point is not working and

feeding is depend on other districts, advance stocking of particular quantity at right

time is a must to survive in market and getting success in sales in peak sale season.

4.2.5 Harvesting Market Situation:

At the time of starting the sale season and during the sales days, continuous

close contact to the customers/farmers and related executives of cooperatives and

state government is very important to harvest the prevailing marketing situation.

Continuous monitoring of marketing pockets, cropping pattern, rainfall pattern where

area comes under rain-fed condition also require close watch. Assessment of day-

to-day need of market is also important to lineup the marketing.

4.2.6 Accessories:

Market of any product depends upon the team work and support of work

done. Marketing refers to the group of people in an enterprise who are carrying out

management functions. It is a directive activity aiming at the effectiveness of

collective human efforts. Marketing is a goal-oriented activity.

120

4.3 Fertilizer Transportation and Distribution Channel:

Transportation of Fertilizers from the various production centers to the

consuming centers spread over throughout the country plays a very important role in

making the Fertilizers available to the farmers at right time, right place and in right

quantities. Physical distribution and logistics management of a product is one of the

very important aspects of marketing. It relates to the activities like demand,

forecasting, warehouse location and capacity, planning, transportation, handling of

the material and inventory planning and control etc. Fertilizer as a product has some

typical features. It is a bulk commodity, its production is uniformly distributed

throughout the year whereas its consumption is highly skewed and is confined to few

months only. In view of these and other typical features, its logistics management

assumes even greater significance. Its in-time availability in the form and quantity

demanded by the farmers at the doorsteps is very essential for its consumption to

take place.

IFFCO is producing urea, NAK/DPA from its four Fertilizer Plants located at

Kandla, Kelol, Aonla and Phulpur. The movement of Fertilizer iof every

manufacturing agency is decided on the basis of allocations made by government of

India for various states. Generally transportation by rail is satisfactory by and large

on a macro-level. Problems do arise for moving Fertilizers from particular plants for

particular destinations. This creates scarcity conditions causing hardship to the

farmers. Timely movement of Fertilizers is very essential to enable the farmers to

use the same during or just before the onset of monsoon. Any delay will only lead to

stock pilling of Fertilizers in the warehouses without contributing to increased

agricultural production. 70% of the state agriculture even today is depend upon

121

rainfall and the consumption of Fertilizer is seasonal in nature, depending upon

whether we have a good or a bad monsoon. But continuous production throughout

the year and necessary transport infrastructure to store the Fertilizers in the

warehouse is needed, so that farmers utilize the input when needed.

Chhattisgarh is a much diversified state in terms of geographical conditions. It

needs different Fertilizers in different regions at different times. Hence warehousing

planning is essential to distribute the Fertilizers to the farmers in right time and place.

The two most important aspects in this regard are—

(a) Where would the warehouse be located?

(b) How much space should be hired?

This strategy would go a long way in sizably cutting down market costs. But

due top change in cropping pattern, introduction of new varieties change in area

under irrigation weather conditions etc. would also be required to modify the logistics

arrangements from time to time. Important aspects of logistics management are

discussed hereunder:

4.3.1 Demand Forecast:

This is the basic ingredient for warehousing planning. For determining

optimum size and location of field warehouses an assessment of how much space is

needed and where it should be located.

4.3.2 Sales Force Composite Method:

Demand for Fertilizer needed in the particular area, in the season is estimated

from past records. Basically it is a subjective method and has no scientific basis.

122

4.3.3 Agronomic Requirement Method:

Fertilizer demand is estimated by multiplying the area under different crops by

the prevalent dosages of N, P2O5 and K2O and then aggregating them. An intimate

knowledge of the prevalent dosages is an important factor in this method.

4.3.4 Trend Projection:

This method basically projects the past trends. Here past Fertilizer sales

pertaining to different time periods are arranged chronologically yielding a time

series. A trend line is fitted to this time series by least square method. The trend

time is then projected into the future for purpose of extra potation.

4.3.5 Warehouse Planning:

Farmers are not properly equipped to purchase material before the season

and store it in advance to use it when required. Warehousing management affects

the availability of Fertilizers to the farmers and in the other it affects marketing cost of

the manufacturer to a great extent.

A large number of warehouse locations definitely ensures easily availability of

the product to the dealer and also proves to be an incentive for him as his cost of

transportation is low in this case. But administration of large number of warehouses

is difficult. This also involves the increase the marketing cost. Hence optimum

numbers of warehouses are required to ensure the availability of Fertilizer in

reasonable cost.

123

4.3.6 Buffer Godown:

This issue is of particular states in which the market size is quite large.

Establishment of buffer godown assumes special significance in surplus market

situation when manufacturers do have to stock their entire of season production.

This helps in uninterrupted production at the plants. IFFCO faced this situation and

has established few buffer godowns in this market in U.P. But buffer godown must

be located in high Fertilizer consuming areas.

4.3.7 Transportation:

Having located the warehousing points and also determined as to how much

of Fertilizer is to be moved to different warehouse locations, the next step is to

organize the movement of the materials.

In India two modes are available for transporting Fertilizers—rails and road.

Rail movement is best suited for Fertilizer movements over longer distances and

bulk commodities. Road transport also plays an important role in Fertilizer

movement in the vicinity of Fertilizer plants or from the rake points to the sales

points. Generally up to 200-250 kilometers have been found economically as well as

operationally convenient by road.

4.3.8 Storage.

Once the transportation is planned, the right place of storage and duration of

storage of Fertilizer had to be considered from various angles, such as—

1. Minimum inventory carrying cost.

2. Storage proximity to production centers.

3. Minimum transit time to consumption centers.

4. Storage proximity to nodal points.

5. Storage proximity to consumption centers.

124

4.3.9 Avoiding Intermediate Handling:

To minimize the freight charges intermediate handling must, therefore, be

minimized by—

1. Ensuring movement from rail head destination direct to dealer location.

2. Local transportation to warehouse.

3. Unloading to warehouse.

IFFCO is increasing its marketing through farmer service programmes. But

marketing strategies are drastically changed in scientific age. Marketing cost is

responsible for profit and loss of any business firm. If marketing cost is much that

whole amount of profit or more than that is expended, a firm can’t sustain its

presence in the market.

IFFCO in C. G. is marketing its products through state federation and Agro-

cooperatives and their policies are uniform throughout state.

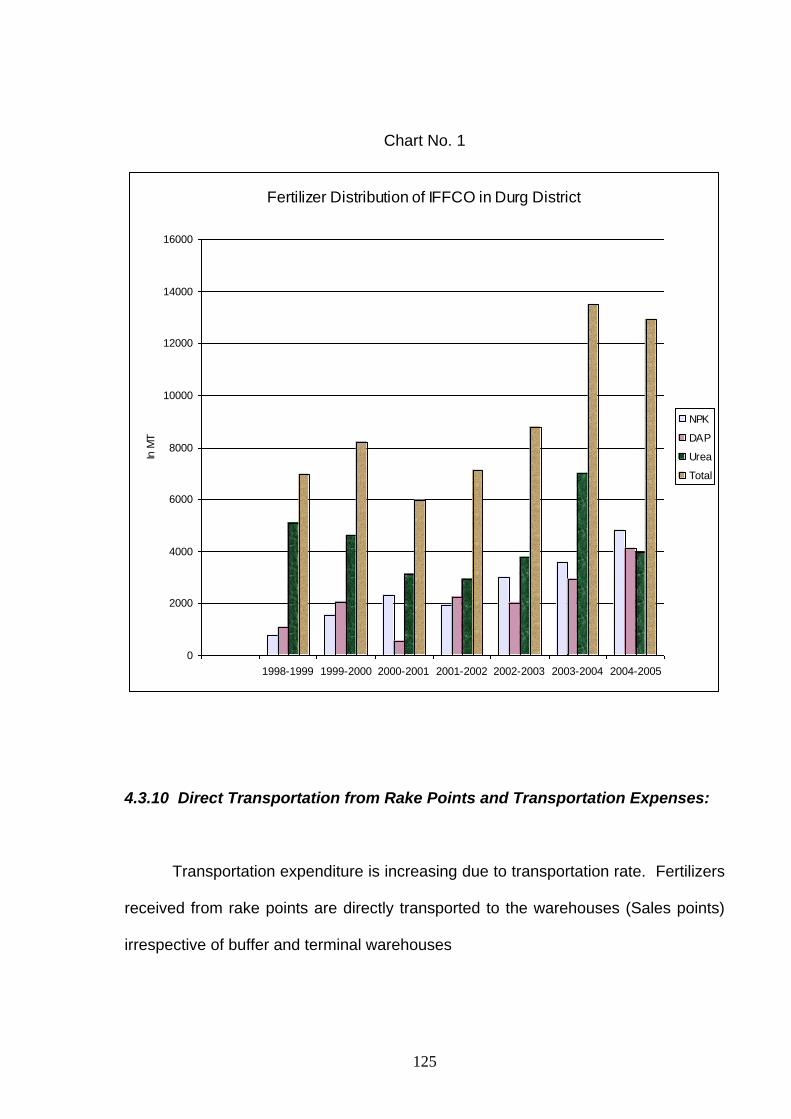

Table No. 4.1 Fertilizer Distribution by IFFCO in Durg District

(In MT)

Year NPK

(12-32-16)

DAP Urea Total

1998-1999 769 1078 5108 6955

1999-2000 1554 2069 4599 8222

2000-2001 2327 526 3103 5956

2001-2002 1936 2240 2937 7113

2002-2003 2994 2018 3777 8789

2003-2004 3566 2934 6983 13483

2004-2005 4844 4120 3961 12925

Source: IFFCO Field Office, Durg.

125

Chart No. 1

Fertilizer Distribution of IFFCO in Durg District

0

2000

4000

6000

8000

10000

12000

14000

16000

1998-1999 1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005

In M

T

NPK

DAP

Urea

Total

4.3.10 Direct Transportation from Rake Points and Transportation Expenses:

Transportation expenditure is increasing due to transportation rate. Fertilizers

received from rake points are directly transported to the warehouses (Sales points)

irrespective of buffer and terminal warehouses

126

Sale Point

Rail Line

Terminal Ware House Buffer Warehouse Transit warehouse

Fig. 1 Transportation and Distribution Pattern of IFFCO Fertilizers throughout PACS

Due to direct transportation from rack point to sale point maximum amount

were saved from Fertilizer handling and transportation. IFFCO marketing

management will try to concentrate the Fertilizer sales points nearer to the reach of

the farmers of warehouses of the primary cooperative societies of the district.

4.3.11 Government of Chhattisgarh Recognized Marketing Agencies:

At present in Chhattisgarh Fertilizer marketing is done through CG State

Marketing Federation (CGSMF) and CG Agro State Cooperation. These federations

127

are marketing Fertilizers through cooperative societies. The Fertilizers are

transported to their sales points. In 1992 IFFCO stopped to transport Fertilizers to

the warehouses of Federations. Then Marketing of IFFCO was adversely affected.

Nowadays IFFCO has again come back to its previous policy.

Following are the some of additional facilities provided by the agencies:

1. Manufacture/Import agencies provide advance reservation for Fertilizer

storage.

2. Advanced availability of Fertilizer from storage.

3. Supply Fertilizers to the sales points of these federations.

4. CG Agro State Corporation Supply Fertilizers directly to village level

cooperative societies.

5. Bonus on Fertilizer sale to the societies by state federation.

6. Manufacturers/Agencies provide Fertilizer as needed by customers.

4.3.12 Warehousing Reservation:

IFFCO management is active to sell maximum quantity of Fertilizers in

minimum reservation time in warehouses to increase the time over to maximum

profit and provide the Fertilizer to the farmers in minimum price.

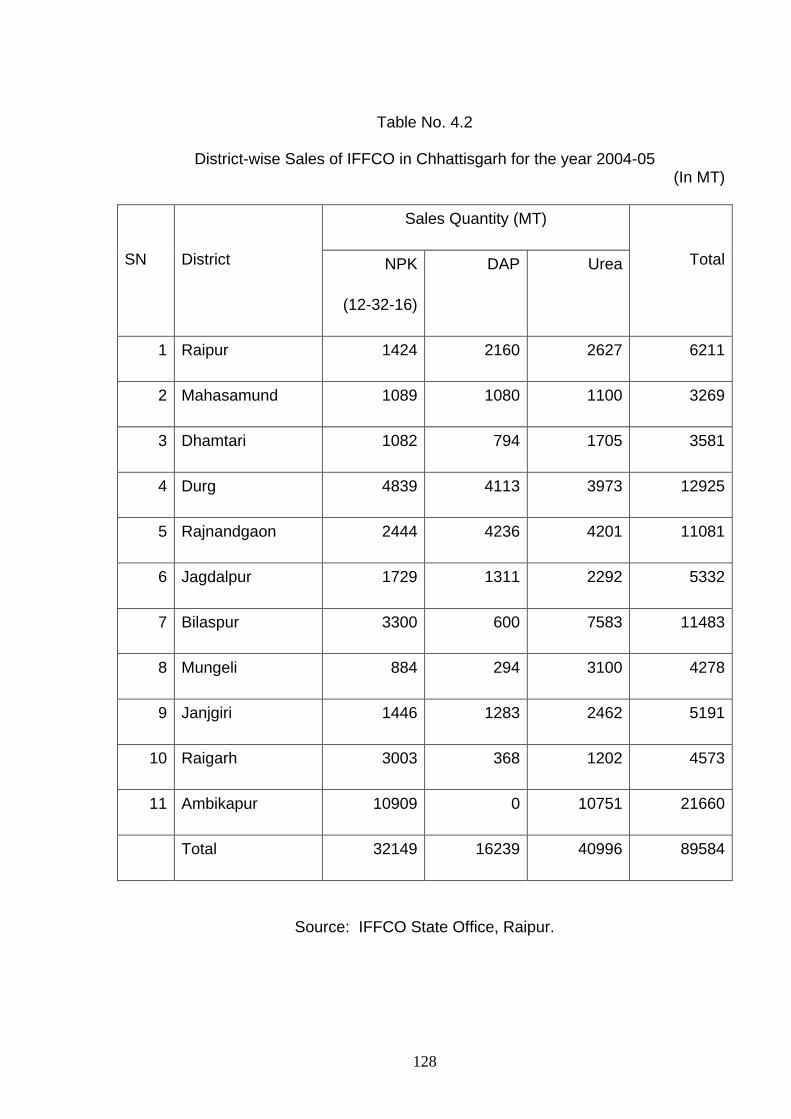

The total district-wise sales of IFFCO in Chhattisgarh for the year 2004-05 are

89584 MT. The maximum sale of IFFCO in Chhattisgarh was in Ambikapur district

and the lowest sale of IFFCO was in Mungeli. The data of District-wise sale of

IFFCO in Chhattisgarh are tabulated below.

128

Table No. 4.2

District-wise Sales of IFFCO in Chhattisgarh for the year 2004-05

(In MT)

SN

District

Sales Quantity (MT)

Total NPK

(12-32-16)

DAP Urea

1 Raipur 1424 2160 2627 6211

2 Mahasamund 1089 1080 1100 3269

3 Dhamtari 1082 794 1705 3581

4 Durg 4839 4113 3973 12925

5 Rajnandgaon 2444 4236 4201 11081

6 Jagdalpur 1729 1311 2292 5332

7 Bilaspur 3300 600 7583 11483

8 Mungeli 884 294 3100 4278

9 Janjgiri 1446 1283 2462 5191

10 Raigarh 3003 368 1202 4573

11 Ambikapur 10909 0 10751 21660

Total 32149 16239 40996 89584

Source: IFFCO State Office, Raipur.

129

Chart No. 2

District-wise Sales of IFFCO in Chhattisgarh for the year 2004-05

0

0

1424

1089

1082

4839

2444

1729

3300

884

1446

3003

10909

32149

0

2160

1080

794

4113

4236

1311

600

294

1283

368

0

16239

0

2627

1100

1705

3973

4201

2292

7583

3100

2462

1202

10751

40996

0

6211

3269

3581

12925

11081

5332

11483

4278

5191

4573

21660

89584

0 10000 20000 30000 40000 50000 60000 70000 80000 90000 100000

District

Raipur

Mahasamund

Dhamtari

Durg

Rajnandgaon

Jagdalpur

Bilaspur

Mungeli

Janjgiri

Raigarh

Ambikapur

Total

Sales Quantity (MT)

130

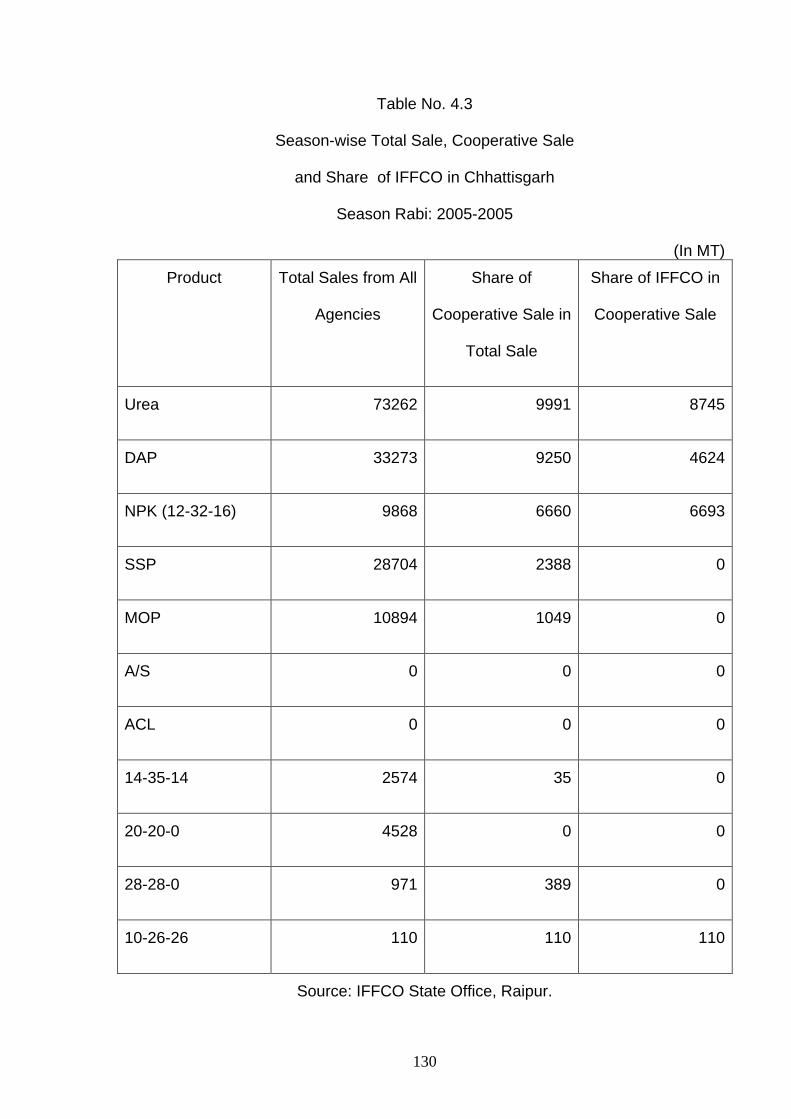

Table No. 4.3

Season-wise Total Sale, Cooperative Sale

and Share of IFFCO in Chhattisgarh

Season Rabi: 2005-2005

(In MT)

Product Total Sales from All

Agencies

Share of

Cooperative Sale in

Total Sale

Share of IFFCO in

Cooperative Sale

Urea 73262 9991 8745

DAP 33273 9250 4624

NPK (12-32-16) 9868 6660 6693

SSP 28704 2388 0

MOP 10894 1049 0

A/S 0 0 0

ACL 0 0 0

14-35-14 2574 35 0

20-20-0 4528 0 0

28-28-0 971 389 0

10-26-26 110 110 110

Source: IFFCO State Office, Raipur.

131

Chart No. 3

Season-wise Total Sale, Coop Sale and Share of IFFCO in Chhattisgarh

Season Rabi: 2004-05

(In MT)

0

73262

33273

9868

28704

10894

0

0

2574

4528

971

110

0

9991

9250

6660

2388

1049

0

0

35

0

389

110

0

8745

4624

6693

0

0

0

0

0

0

0

110

0 10000 20000 30000 40000 50000 60000 70000 80000

Product

Urea

DAP

NPK (12-32-16)

SSP

MOP

A/S

ACL

14-35-14

20-20-0

28-28-0

10/26/26

Series4

Series3

Series2

Series1

132

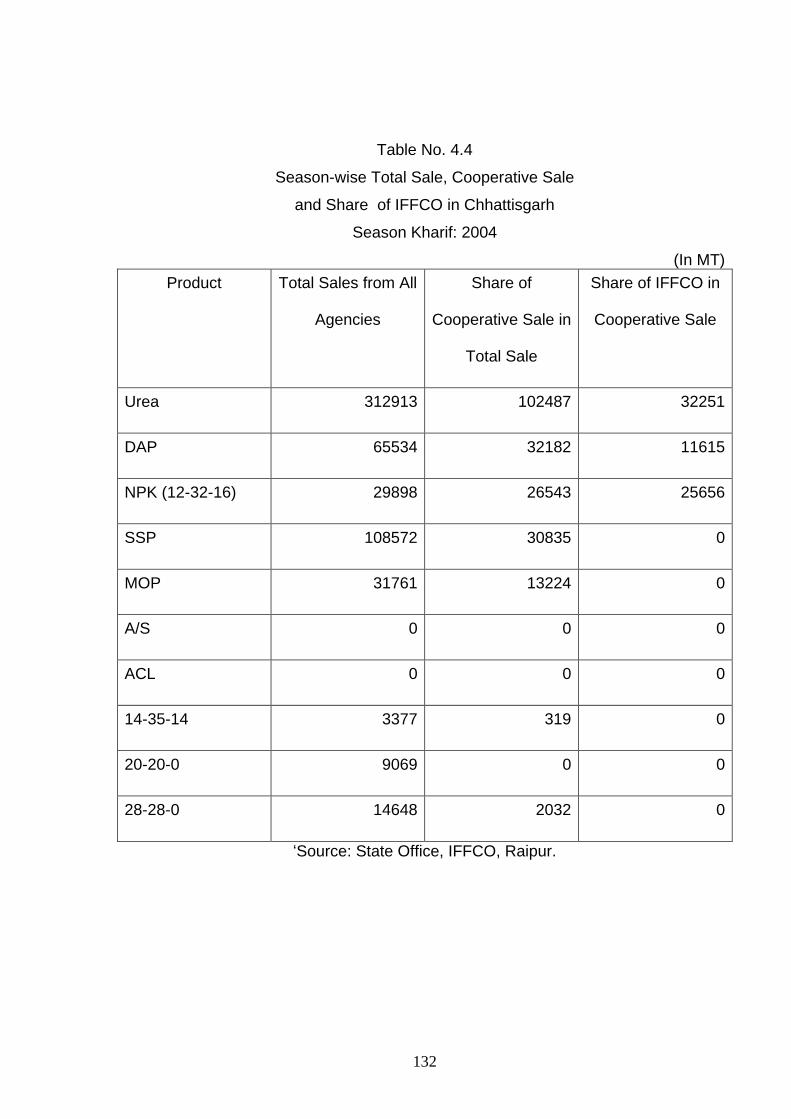

Table No. 4.4

Season-wise Total Sale, Cooperative Sale

and Share of IFFCO in Chhattisgarh

Season Kharif: 2004

(In MT)

Product Total Sales from All

Agencies

Share of

Cooperative Sale in

Total Sale

Share of IFFCO in

Cooperative Sale

Urea 312913 102487 32251

DAP 65534 32182 11615

NPK (12-32-16) 29898 26543 25656

SSP 108572 30835 0

MOP 31761 13224 0

A/S 0 0 0

ACL 0 0 0

14-35-14 3377 319 0

20-20-0 9069 0 0

28-28-0 14648 2032 0

‘Source: State Office, IFFCO, Raipur.

133

Chart No. 4

Season-w ise Total Sale, Coop. Sale and Share of IFFCO in Chhattisgarh Season Kharif: 2004 (In MT)

312913

65534

29898

108572

31761

0

0

3377

9069

14648

102487

32182

26543

30835

13224

0

0

319

0

2032

32251

11615

25656

0

0

0

0

0

0

0

0 50000 100000 150000 200000 250000 300000 350000

Urea

DAP

NPK (12-32-16)

SSP

MOP

A/S

ACL

14-35-14

20-20-0

28-28-0

Share of IFFCO in Coop sale

Share of Cooperative

Total Sales

134

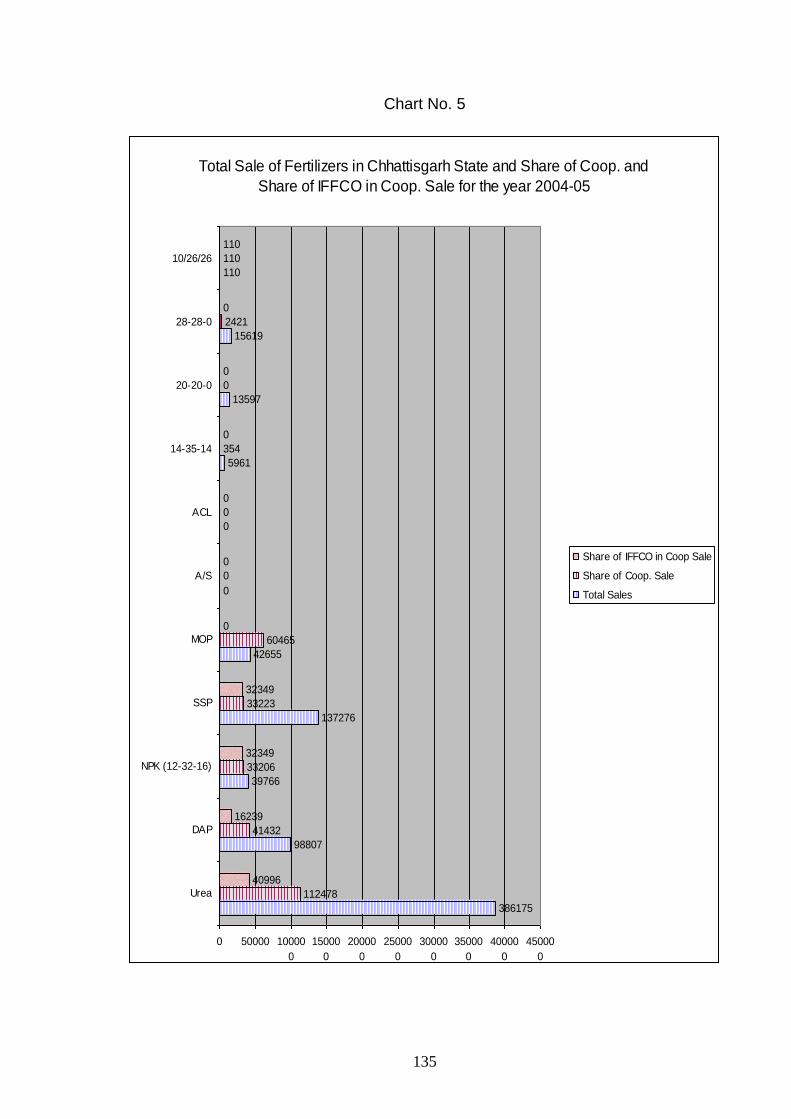

Table No. 4.5

Total Sale of all Fertilizers in Chhattisgarh State and share

Cooperative and Share of IFFCO in Cooperative Sale

for the Year 2004-05

(In MT)

Product Total Sales from All Agencies

Share of Cooperative Sale in

Total Sale

Share of IFFCO in Cooperative Sale

Urea 386175 112478 40996

DAP 98807 41432 16239

NPK (12-32-16) 39766 33206 32349

SSP 137276 33223 32349

MOP 42655 60465 0

A/S 0 0 0

ACL 0 0 0

14-35-14 5961 354 0

20-20-0 13597 0 0

28-28-0 15619 2421 0

10-26-26 110 110 110

Source: State Office, IFFCO, Raipur.

135

Chart No. 5

Total Sale of Fertilizers in Chhattisgarh State and Share of Coop. and

Share of IFFCO in Coop. Sale for the year 2004-05

386175

98807

39766

137276

42655

0

0

5961

13597

15619

110

112478

41432

33206

33223

60465

0

0

354

0

2421

110

40996

16239

32349

32349

0

0

0

0

0

0

110

0 50000 10000

0

15000

0

20000

0

25000

0

30000

0

35000

0

40000

0

45000

0

Urea

DAP

NPK (12-32-16)

SSP

MOP

A/S

ACL

14-35-14

20-20-0

28-28-0

10/26/26

Share of IFFCO in Coop Sale

Share of Coop. Sale

Total Sales

136

4.3.13 Other Measures for Increasing Profit:

1. Branches/Societies were allotted monthly and half monthly target for Fertilizer

selling and matter was briefed before Bank Marketing Federations and

agriculture officer to meet the target finalized. Due to this selling of Fertilizer

was increased.

2. Weekly Report related to total Fertilizer selling society-wise/Branch-wise was

demanded and comparative study was made for IFFCO-NPK. More receipt

orders (RO) were drawn for IFFCO NPK in comparison to other Fertilizers.

3. In the area of societies where NPK (12-32-16) was used less, farmers

meetings were held. As a result demand of NPK (12-32-16) was increased.

4. District officials of agriculture department, marketing federation and senior

officials of cooperative Banks were in societies in result NPK (12-32-16)

selling was favourable.

4.3.14 Fertilizer Distribution through CG Agro State Corporation:

CG Agro State Corporation is growing fast in the area of Fertilizer distribution.

Marketing of IFFCO Fertilizer through CG Agro has been started.

4.3.15 Time Availability of Fertilizers:

Fertilizer is the necessary input for increasing the farm output. Generally it is

seen that the Fertilizers are not made available to the farmers when they are

needed. Fertilizer is made available to the farmers in time to win the confidence for

137

IFFCO products. Loss in distribution of Fertilizer in one season can’t be

compensated in other season and many difficulties arise to sell the target limit to the

Fertilizers.

If management of IFFCO concentrates on above points and a concrete

strategy is formulated, the profit can be maximized by increasing business.

4.3.16 Suggestions to Improve Working Conditions:

Area Officers/Representatives engaged in marketing business of IFFCO

Fertilizers are facing many difficulties to furnish their duties efficiently. To overcome,

the following are some suggestions:

1. Rack handling work has to be done by government storage agency and not

by IFFCO transporters.

2. Marketing process should make simplified so that receipt can be received

early.

3. Customers/Farmers should be provided more knowledge about use of

balance Fertilizers.

In order to ensure efficient working atmosphere we have to change the

marketing policy from time to time after market researches and through efficient

utilization of Management Information System (MIS).

138

4.4 Pricing Policies

Pricing policies and decisions constitute the general framework within which

pricing decision should be made in order to achieve the pricing objectives. They

provide guidelines within which pricing strategy is formulated and implemented.

As a matter of fact calibration of relative prices level of different NPK products

under price control from 1978 to 2003-04 has counting to narrow down the gap

between the uses of levels of NPK.

The recent step depreciation of the rupee has produced a serious adverse

effect in the cost of imported products including raw materials, intermediates, capital

goods and components leading to higher production cost on the one hand and even

problems in arranging necessary import to support manufacturing operations in the

other.

Every segment of the fertilizer industry has been effected the impact is

particularly severe and disturbing in the phosphatic segment. This is because of

meeting the requirements of these fertilizers India is almost entirely dependent on

import either as basic raw materials, i.e. rock-phosphate and sulphur or

intermediates, i.e. phosphoric acid and ammonia for production at home or import as

finished product, i.e. DAP. In the potash segment we do not have natural resources

within the country and the entire requirements are met through import as finished

product, predominantly as muriate of potash (MOP). With reason the prices of

fertilizers are escalating from time to time. In the following table the statutory

139

controlled prices of urea, zincated urea and anhydrous ammonia are given which are

exclusive of state sales tax and local taxes:

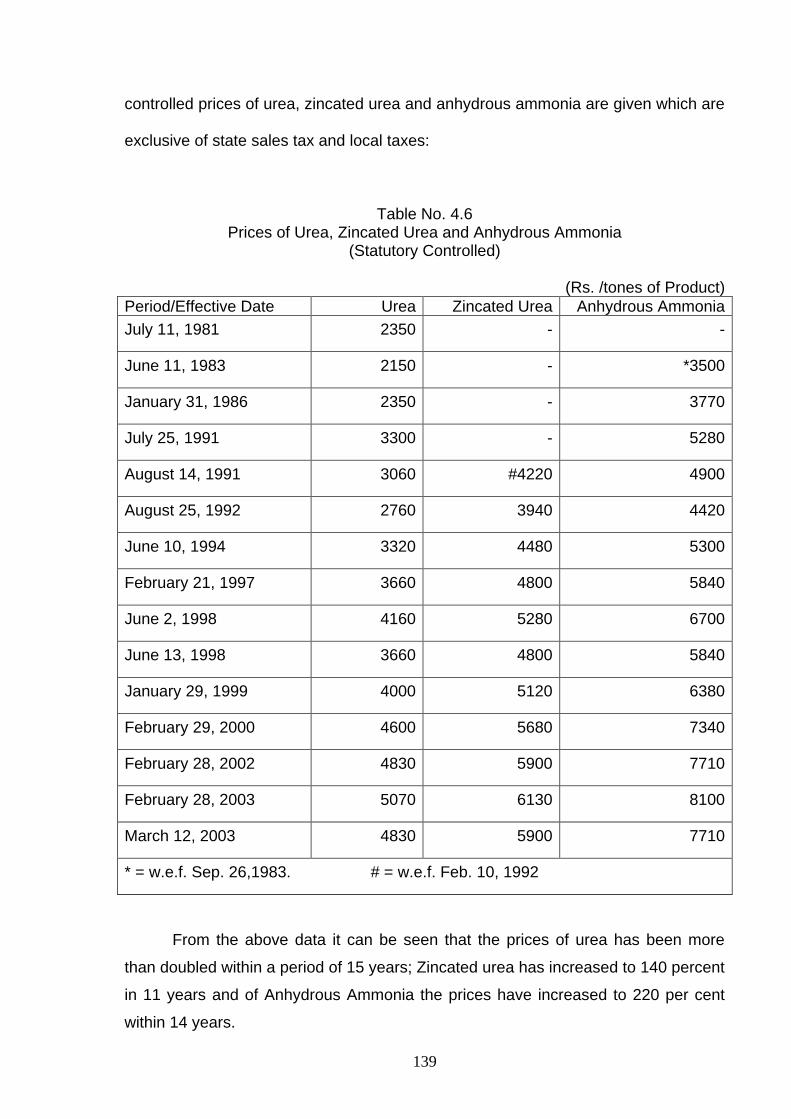

Table No. 4.6 Prices of Urea, Zincated Urea and Anhydrous Ammonia

(Statutory Controlled)

(Rs. /tones of Product)

Period/Effective Date Urea Zincated Urea Anhydrous Ammonia

July 11, 1981 2350 - -

June 11, 1983 2150 - *3500

January 31, 1986 2350 - 3770

July 25, 1991 3300 - 5280

August 14, 1991 3060 #4220 4900

August 25, 1992 2760 3940 4420

June 10, 1994 3320 4480 5300

February 21, 1997 3660 4800 5840

June 2, 1998 4160 5280 6700

June 13, 1998 3660 4800 5840

January 29, 1999 4000 5120 6380

February 29, 2000 4600 5680 7340

February 28, 2002 4830 5900 7710

February 28, 2003 5070 6130 8100

March 12, 2003 4830 5900 7710

* = w.e.f. Sep. 26,1983. # = w.e.f. Feb. 10, 1992

From the above data it can be seen that the prices of urea has been more

than doubled within a period of 15 years; Zincated urea has increased to 140 percent

in 11 years and of Anhydrous Ammonia the prices have increased to 220 per cent

within 14 years.

140

4.5 Social, Ecological Aspects of Marketing:

IFFCO as a cooperative institution society demands quality of life

management. Integrated business plans and controls are expected to act as

instruments of social change and these plans have to be implemented in order to

promote maximum public good and welfare. In addition to economic performance

IFFCO demonstrates social awareness and social performance. Dependence of

business on its environment is so complete that the very existence and survival as

well as growth of any organization depend upon its acceptance by the society.

Social responsibility mean an intelligent and objective concern for the welfare

of society that prevents IFFCO management from destructive activities, e.g.

monopoly power, unfair trade practices, ruthless exploitation of ecology and natural

resources and pollution of environment. Such destructive activities may be

immediately profitable to the business but they can’t be tolerated by society. Social

responsibility indicates personal obligation of people, as they act in their own

interest, to ensure that the rights and legitimate interests of others are not sacrificed

by the behaviour of IFFCO management as a whole.

4.5.1 Social Function of Marketing:

Marketing Management of IFFCO is concerned with the following four social

functions—

1. Survival.

2. Profitability

3. Service.

4. Social responsibility.

141

From the study, it is observed that the IFFCO at all level in an organization

are involved in resolving the conflict and reconciling the following responsibilities—

1. to the society as a whole.

2. to the customers (Farming community as a whole).

3. to the employees (Under HRD).

4. to the share holders.

5. to the Government.

Modern business is faced by many other social obligations, such as—

1. Environment free from pollution

2. Fair prices, fair quality and fair service.

Management of IFFCO believes that the modern business operates in a

socio-economic environment. It has to demonstrate not only its economic efficiency

but also consumer sensitivity and social awareness. This is also the concept of

IFFCO management that the business must assess not only the profitability of its

actions but also the overall effect those actions have an society and on the ecology

or environment.

4.5.2 Ecological Aspects of Marketing:

As a part of social responsibility of IFFCO management, care towards the

clean and healthy environment has been taken too. IFFCO has taken all steps to

prevent all types of pollution.

142

4.5.3 Fertilizer and Environmental Pollution:

IFFCO is one of the leading Fertilizer production and marketing cooperative in

India. Today Fertilizer has become an indispensable input of intensive agriculture

and its consumption is expected to increase sharply. Hence we can say that we

have to fight the environment pollution by two ways:

1. Pollution emitted by manufacturing unit of IFFCO.

2. Affect on soil, water and air by non judicious use of Fertilizers by the

farmers.

The first part of pollution control of IFFCO manufacturing units depend on the

technology. IFFCO is modernizing all its existing plants, introducing new

technologies which are satisfying the Indian standard for pollution control. Recently

Kaloi, Aonla and Phulpur Fertilizer plants have induced technologies to meet out

pollution force atmosphere in and around the plants. These technologies are of

Indian standard certified by Bureau of Indian Standards (BIS).

In the second part, excessive use of Fertilizers is increasing awareness of the

environmental degradation due to various anthropogenic activities has developed

suspicion towards the use of Fertilizers and concern has been expressed that over

reliance on mineral Fertilizer may cause unsustainable environmental penalties. It is

observed that the Fertilizer use efficiency by crops seldom exceeds 50 percent. The

remainder is lost from soil system by teaching, run off, de-nitrification and

volatilization. Therefore, it becomes pertinent to understand and evaluate the

environmental implications of Fertilizers use keeping in view the agricultural

productivity and nutritional security of India.

143

4.5.4 Pollution Problems with Fertilizers:

Three vital natural resources namely, soil, water and air are liable to be

affected by non-judicious use of Fertilizers.

1. Water Pollution:

The main problem associated with excess use of Fertilizers is the

entrophication of surface water. Available soil leak considerable amount of nutrients

which enrich the water body resulting in more growth of algae and other organisms

and thus impair the quality of water and limit its use. Application of nitrogenous

Fertilizers also results in increasing the concentration of nitrate in ground water

causes blue baby disease of young babies and cancer.

2. Air Pollution:

Nitrogenous Fertilizers contribute substantially towards emission of nitrogen

oxide such as nitric oxides and nitrogen dioxide which apart from causing global

warning, cause many disorders to animals and human beings. It also emits

ammonia ore of the agents causing acid rains.

4.5.6 Damage to the Crops and Soils:

Evidence showed that excessive use of Fertilizers particularly nitrogen, cause

lodging of crop, low sugar content in sugar crops, acidifying action and increased

incidence of weed and pest attacks. But this is due to imbalanced use of Fertilizers

which disturb the nutrient equilibriums in soil and plants particularly where only one

nutrient is used continuously. Thus it appears that unbalanced nutrient application is

bad but then the problem is with the farmers who are not aware of sound agricultural

practices. Many Fertilizers contain varying amount of trace elements lead to their

144

accumulation in soil and ground water aquifers. But this takes place if contaminated

Fertilizers are marketed. Government of India has laid down permissible limit for

impurities in Fertilizer materials and has formulated Fertilizer control under the law

specifying the quality of Fertilizers.

4.5.7 Pollution Abatement Strategies Taken by IFFCO:

Though no serious environmental problem has so far been observed in any

part of this country, but we have to take lesson from USA and Europe where soil

degradation due to excess use of Fertilizers is the major problem faced by

agronomists. Hence in India care should be taken to control the long term pollution

problems which may arise in future due to excess use of uncontrolled Fertilizers.

IFFCO has adopted two major approaches to minimize possible environmental

pollution due to Fertilizers application—Firstly, to improve the ability of plants to

compete with process which lead to losses of nutrients from soil plant system to

environment and secondly, reduction of losses.

While first one can be achieved by genetically and bio-technological means,

the second one calls for improved Fertilizer use efficiency by improving soil and crop

management practices. IFFCO has taken serious concern and many projects are

launched all over India related to bio-Fertilizers use and farm forestry under Farmer

Education Programmes.

In the context of emerging biotechnologies, IFFCO has initiated to develop

new plant types to use nutrients more efficiently so that there would e no loss of

applied nutrients. New strains of Rhizobium and blue-green algae with higher N

fixation capacity are in different laboratories of IFFCO chairs so that our dependency

145

on Fertilizers will reduce, thereby reducing threat to Fertilizer pollution. IFFCO

through its research and development and extension services is supplying integrated

plant nutrition system, the basic principle of which is the maintenance of soil fertility,

sustainable agricultural productivity and improving farmer’s profitability through

judicious and efficient use of mineral Fertilizer, organic matter, green manure,

biological nitrogen fixation and other inoculates have to be practiced. At the same

time IFFCO has taken measures to control soil erosion and other losses of Fertilizer

nutrients from soil systems to reduce pollution.

4.6 Fertilizer Industry: Challenges and Opportunities in Changing Scenario Indian agriculture continues to contribute more than 20 per cent of overall

Gross Domestic Production. Increased food production not only improves rural

economy but also reduces the pressure on amenities in urban areas on account of

lower rate of migration from rural area.

Fertilizers are crucial inputs for Indian agriculture. About 40-50 per cent

increase in food grain production is attributed to increased fertilizer use. The growth

in fertilizer consumption is directly linked to agricultural development. The role of

fertilizer has gained greater importance now, as the increased agricultural production

has to come from shrinking quantitative and qualitative resources, notably and and

water; in the coming years. During the past few years the goodgrain production is

stagnant around 212 MT and fertilizer consumption is also stagnant at 17 MT of

nutrients (NPK) and this need to be broken for attaining food security of the country

having over one billion population which is growing at much faster speed than the

counterparts in developed countries.

146

The economic reform programmes, initiated in 1991, brought about in the

wake of liberalization touching almost every segment in the country. The winds of

change swept over the fertilizer industry as well. In the midst of this, the fertilizer

sector was subjected to short-term and ad hoc measures, with the sole objective of

reducing fertilizer subsidy. In the last thirteen years since then, the industry that

changed th face of Indian agriculture and freed the country from the bondage of

importing food grains of inferior quality to feed the millions of hungry people, is now

reeling under tough policy environment. Thus the health of fertilizer industry has to

be stronger for sustainable agriculture to attain food security which in turn protects

the sovereignty of our country.

4.6.1 Present Fertilizer Scenario:

The gap between fertilizer consumption and indigenous production was

bridged by importing Urea, DAP and entire MOP besides phosphoric acid to

manufacture NP/NPK fertilizer within the country.

4.6.1.1 Fertilizer Production:

The indigenous production of N during the year 2003-04 through 55 plants

(out of which 32 are urea plants) was 10.56 MT by using 86.4 per capacity. Similarly

production of P was 3.62 MT during 2003-04 from 64 SSP plants and 20 NP/NPK

plants. Thus the total production of N and P was 14.18 MT during the year 2003-04.

The urea accounts for 83 per cent of total N production while DAP, NPK respectively

account of 8.0 and 7.3 per cent of total N production. In case of P production DAP,

NPK and SSP respectively account for 59.9, 29.2 and 10.9 per cent of total P

production.

147

4.6.1.2 Fertilizer Consumption

The total nutrient consumption was 16.90 MT during 2003-04 out of which

7.56 MT was in Kharif and 9.34 MT was in rabi season. In this year consumption of

N, P and K was respectably 11.15, 4.15 and 1.60 MT. Out of total nutrient

consumption UP has largest share (19.9), followed by AP (11.0), Punjab (9.1),

Maharashtra (8.5) and WB (6.6). These 5 states account for 55.1 per cent of total

fertilizer consumption in the country. Next in order were Haryana (6.0), Gujarat (6.0),

M.P. (5.8), Karnatraka (5.4), Rajasthan (4.6), Tamil Nadu (4.2) and Bihar (4.0).

These 12 states accounted for 91.1 per cent share in total fertilizer consumption in

the country. Balance 8.9 per cent consumed by remaining states.

Table No. 4.7 Season-wise consumption of N, P2O5 and K2O and Total by State

and Percentage variation (2002-03 and 2003-04)

West Zone:

State Nutrient Consumption (‘000 tonnes)

2002-03 2003-04 (P)

Chhattisgarh N 140.06 17.80 157.86 139.93 23.42 163.35

P2O5 61.94 8.88 70.82 51.40 11.74 63.14

K2O 18.64 3.01 21.65 16.53 4.45 20.98

Total 220.64 29.69 250.33 207.86 39.61 247.47

Source: Fertilizer Statistics, 2003-04, The FAI, p.I-86.

All India per hectare consumption of total nutrients was 90.4 Kg during 2003-

04. The major states which had per hectare consumption higher than all India

average included Punjab (184 Kg), Haryana (167 Kg), A.P. (136.8 Kg), UP and

148

Uttaranchal together (129.1 Kg), WB (126.7 Kg), Tamil Nadu (112.2 Kg) and Gujarat

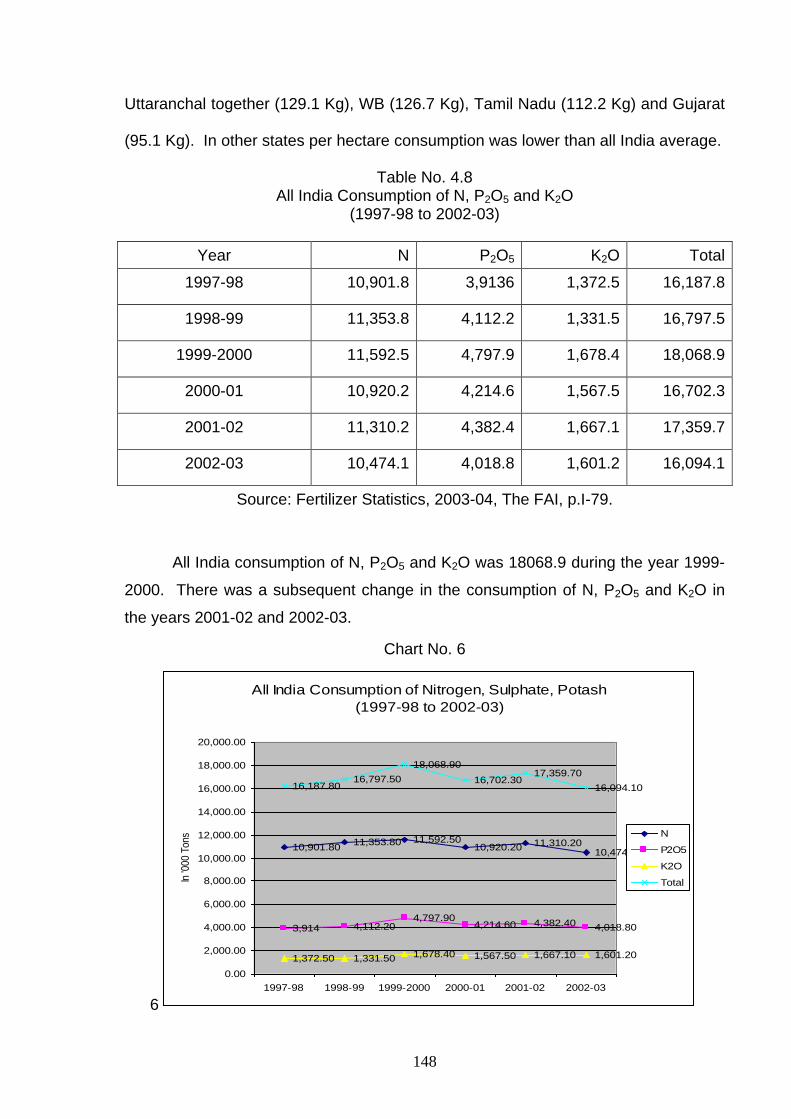

(95.1 Kg). In other states per hectare consumption was lower than all India average.

Table No. 4.8 All India Consumption of N, P2O5 and K2O

(1997-98 to 2002-03)

Year N P2O5 K2O Total

1997-98 10,901.8 3,9136 1,372.5 16,187.8

1998-99 11,353.8 4,112.2 1,331.5 16,797.5

1999-2000 11,592.5 4,797.9 1,678.4 18,068.9

2000-01 10,920.2 4,214.6 1,567.5 16,702.3

2001-02 11,310.2 4,382.4 1,667.1 17,359.7

2002-03 10,474.1 4,018.8 1,601.2 16,094.1

Source: Fertilizer Statistics, 2003-04, The FAI, p.I-79.

All India consumption of N, P2O5 and K2O was 18068.9 during the year 1999-

2000. There was a subsequent change in the consumption of N, P2O5 and K2O in

the years 2001-02 and 2002-03.

Chart No. 6

6

All India Consumption of Nitrogen, Sulphate, Potash

(1997-98 to 2002-03)

10,901.8011,353.80 11,592.50

10,920.20 11,310.2010,474.10

3,914 4,112.204,797.90

4,214.60 4,382.40 4,018.80

1,372.50 1,331.50 1,678.40 1,567.50 1,667.10 1,601.20

16,187.8016,797.50

18,068.90

16,702.3017,359.70

16,094.10

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

16,000.00

18,000.00

20,000.00

1997-98 1998-99 1999-2000 2000-01 2001-02 2002-03

In '0

00 T

ons N

P2O5

K2O

Total

149

Table No. 4.9

All India Consumption of Plant Nutrients per Unit of

Gross Cropped Area 1990-91 to 2003-04 (P)

Year Gross Cropped Area

(‘000 ha)

Consumption per Hectare/Kg

N P2O5 K2O Total

1990-91 185,742 43.06 17.34 7.15 67.55

1991-92 182,242 44.15 18.22 7.47 69.84

1992-93 185,700 45.38 15.31 4.76 65.45

1993-94(P) 186,580 47.10 14.31 4.87 66.28

1994-95(P) 188,053 50.56 15.59 5.98 72.13

1995-96(P) 187,471 52.40 15.46 6.17 74.02

1996-97(P) 189,592 54.34 15.70 5.43 75.47

1997-98(P) 190,570 57.21 20.54 7.20 84.94

1998-99(P) 193.034 58.82 21.30 6.90 87.02

1999-2000(P) 190,321 60.91 25.21 8.82 94.94

2000-01(P) 187,009 58.39 22.54 8.38 89.31

2001-02(P) 60.48 23.43 8.91 92.83

2002-03(P) 5601 21.49 8.56 86.06

2003-04(P) 59.23 22.05 8.54 89.82

P=Provisional

Source: Fertiliser Statistics 2003-04, FAI, New Delhi, p. I-113.

150

Chart No. 7

.

All India Consumlption of Plant Nutrients per Unit of Gross Cropped Area 1990-91 to 2003-04(O)

185,742

182,242

185,700

186,580

188,053

187,471

189,592

190,570

193.034

190,321

187,009

43.06

44.15

45.38

47.1

50.56

52.4

54.34

57.21

58.82

60.91

58.39

60.48

5601

59.23

17.34

18.22

15.31

14.31

15.59

15.46

15.7

20.54

21.3

25.21

22.54

23.43

21.49

22.05

7.15

7.47

4.76

4.87

5.98

6.17

5.43

7.2

6.9

8.82

8.38

8.91

8.56

8.54

67.55

69.84

65.45

66.28

72.13

74.02

75.47

84.94

87.02

94.94

89.31

92.83

86.06

89.82

0 50,000 100,000 150,000 200,000 250,000

1990-91

1991-92

1992-93

1993-94(P)

1994-95(P)

1995-96(P)

1996-97(P)

1997-98(P)

1998-99(P)

1999-2000(P)

2000-01(P)

2001-02(P)

2002-03(P)

2003-04(P)

Cropped Area Total

Cropped Area K2O

Cropped Area P2O5

Cropped Area N

Cropped Area

151

Chart No. 8

Consumption of Plant Nutrients in Major States (Kg.ha)#

(N+P2O5+K2O)

2003-04 and 2002-03

172

151

123125

128

117

74

86 8790

58

75

68

3942 43

47

37

29

184

167

137

127122

113

9590

8075

7166

64

55

49 47 4641 40

0

20

40

60

80

100

120

140

160

180

200

PUNJA

B

HARYANA

ANDHRA PRADES

H

UTTAR P

RADESH$

WES

T BEN

GAL

TAMIL

NADU

GUJARAT

ALL IN

DIA

BIHAR

KARNATAKA

KAMMU & K

ASHMIR

MAHARASHTRA

KERALA

MADHYA PRADES

H

HIMACHAL

PRADES

H

ASSAM

CHHATTIS

GARH

ORISSA

RAJASTH

AN

2002-03

2003-04

Source: Fertiliser Statistics 2003-04, FAI, New Delhi, p.I-115.

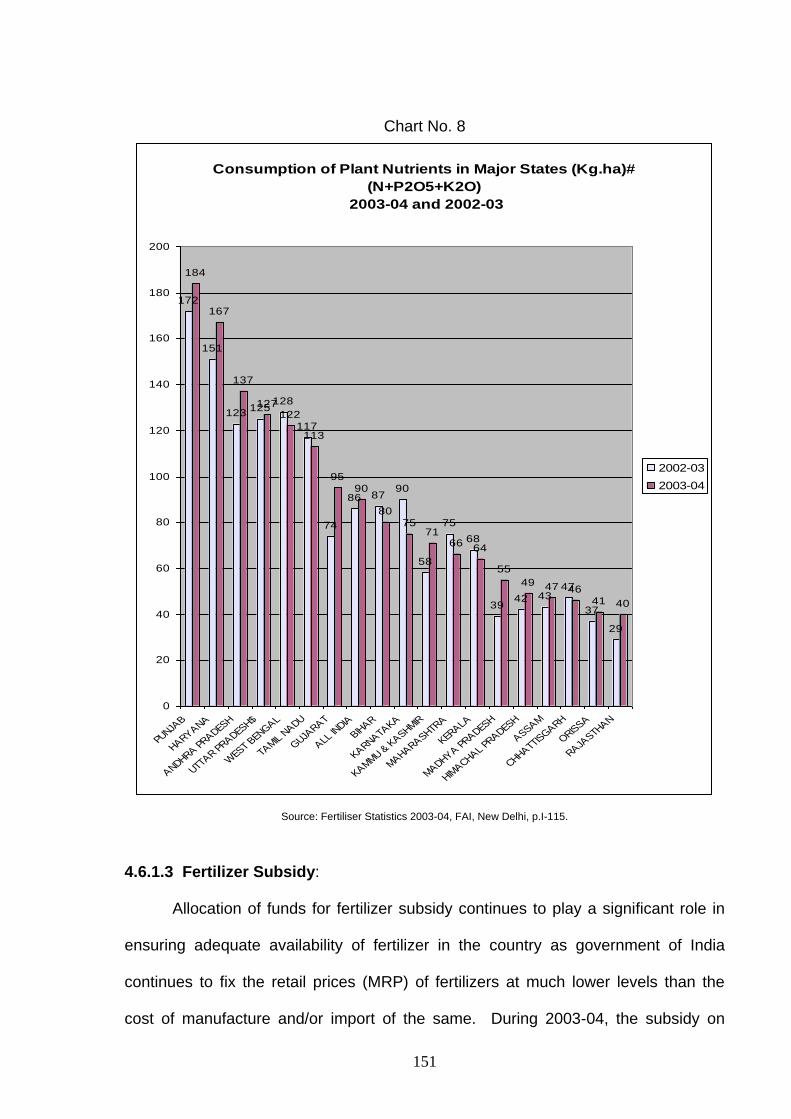

4.6.1.3 Fertilizer Subsidy:

Allocation of funds for fertilizer subsidy continues to play a significant role in

ensuring adequate availability of fertilizer in the country as government of India

continues to fix the retail prices (MRP) of fertilizers at much lower levels than the

cost of manufacture and/or import of the same. During 2003-04, the subsidy on

152

indigenous urea disbursed was 8140 crores and phosphatic fertilizers were 3656

crores, which totals to 11796 crores. However, during 2004-05 budget allocated for

fertilizer subsidy has been 12662 crores.

The increase in fertilizer subsidy was mainly due to significant increase in cost

fo raw materials/intermediates like naphtha, phosphoric acid, ammonia etc., coupled

with increase in cost of imported fertilizers, namely MOP and DAP, which are beyond

the control of the industry.

4.6.1.4 New Pricing Policy

The erstwhile Retention Pricing-cum-Subsidy Scheme (RPS) for urea

introduced in November 1977 which provided for unit-wise pricing and subsidy, came

to an end on March 2003. The new pricing scheme (NPS) for urea was implemented

from April 2003 with an objective to encourage efficiency parameter of international

standards based on—

Most efficient feed stock

State of the art technology

Ensure viable rate of return to the units.

The main features of the New Pricing Policy are:

(i) Change over from unit specific Retention Price to Group Retention

Price: all 32 urea units classified into 6 groups based on feedstock

and vintage.

153

(ii) Phased decontrol of urea distribution/movement: Accordingly

distribution of 25 and 50 per cent of reassessed capacity was taken

out of ECA respectively in kharif 2003 and rabi 2003-04. Primary

freight on urea distributed under free category (non ECA) was

reduced by Rs. 100/T as compared to the freight allowed on quantity

of urea distributed under ECA.

(iii) In stage-II, that is, from Kharif 2004 the policy has envisaged 100

decontrol of urea, but Government of India has decided to continue

to maintain 50 per cent ECA, however, reduction in CRC of 12 units

as well as preset energy norms for all the units.

(iv) No imbursement on investment for improvement in operation or no

mopping up of gains as a result of operational efficiency.

(v) Equated freight on the basis of average normative lead and rail-road

mix of each unit for the previous three years.

4.6.2 Challenges and Opportunities thrown up by the NPS:

4.6.2.1 Challenges:

(a) Unit’s return (normative 12 per cent post tax in RPS) under strain due

to:

Units having higher retention price than the group average are

losing.

Tightening of energy norms during stage-II on efficiency

consideration.

Reduction in concession during stage-II due to relduction in CRC.

154

Non-updating of conversion costs, which are based on 1999-

2000 with no revision.

(b) No recognition of capital addition made by units, particularly older

ones, since 1.4.2000.

(c) Reduction in freight subsidy of Rs. 100/T consequent to movement

decontrol may not be compensated by commensurate saving in freight

cost due to competition/inflation.

(d) Uncertainty in policy environment beyond March 2006.

In nut shell the challenges before fertilizer industry is to be operated on thin

margin by further improving the efficiency in production as well as in marketing

activities individually or mutually among themselves.

4.6.2.2 Opportunities:

The new pricing policy sets out to full decontrol.

Tremendous opportunities on saving freight.

No capping on production of urea.

Sale or use of byproducts such as ammonia, carbon dioxide etc. are permitted

if not converted to urea or considered surplus.

Export of urea against imports by GOI.

No mopping up of any improvements made by the units.

Opportunity to naphtha based units to change over to NG/LNG under special

policy/package.

No further reassessment of capacity.

155

Besides these, the national agricultural policy plans to achieve for grain

production of 320 MT by 2011-12 which trows opportunity of increase in demand to

nearly 28-30 MT of nutrients from present level of about 17 MT of nutrients. The

information technologies are increasing at much faster speed also give opportunity

for improving efficiency.

4.6.3 Strategy

Logically the strategies are made to take full advantage of opportunities as

well as to meet the challenges thrown at the industry, thus improving the strength of

the organizations.

4.6.3.1 Production Level

Switch over to cheap source of raw materials and energy saving by suitable

modification in the plants.

Forming of joint ventures in the countries where raw materials like LNG/Rock

phosphate, phosphoric acid etc., are cheaper and amply available to source

the raw materials on long term basis.

Product exchange among the companies needs to implement in true sense to

avoid long distance freight.

4.6.3.2 Marketing Level:

Economize transportation cost (rain and road) by following least cost matrix.

Improving handling so as to avoid loss to the materials.

Economize in warehousing cost by critical review of stock time to time.

Micro planning of stocking plan to meet the demands without overstocking.

156

Strengthening the distribution channel.

Effective promotional programme with active involvement of cooperative

dealers to educate farmers for better farming practices to increase crop

productivity and to improve soil health for sustainable agriculture.

Contractual farming as forward linkage to empower farmer and to benefit

industry in win-win situation. Custom hiring facilities of farm machinery can be

created for empowering farmers.

Use IT for fast, clear communication as well as for transfer of technical

knowledge in the form of agro-portals.

Motivate farmers and cooperative dealers to take advantage of forward trade

of agricultural communities, made possible by NCDEX.

Since organic manure improves fertilizer use efficiency, special thrust by

fertilizer industry is to be given to promote biogas, composing in rural areas

which are burnt as fuel to large extent.

Farmers are to be educated that they grow faster in self help grou0p (SHG).

Fertilizer industry needs to create alliances with seed industries or other input

industries for integrated and effective services to farmers.

4.7 Discussion and Conclusion:

4.7.1 Discussion

The Fertilizer marketing is entering in an era of new challenges. Besides

substantial increase in quantum to be marketed by IFFCO, marketing base will have

to be widened covering low consumption under development tribal areas very

remote from urban masses.

157

Moreover, these tasks will have to be performed in more difficult

circumstances than before. The policy environment will be not as favourable as in

past due to increasing Fertilizer subsidy burden. At the same time infrastructure

required to improve efficacy of Fertilizer marketing system is unlikely to keep pace

with Fertilizer market expansion. The alternatives available with the manufacturers

are to bring maximum economy in their operation through better resource

management, make renewed efforts to improve quality distribution channel and seek

government support in certain areas to achieve commercial viability of marketing

operations.

4.7.2 Conclusion:

Fertilizer is key input for attaining food security of this country. Subsidy burden

is being reduced or contained by implementing norms of international standard in

NPS. The fertilizer industry requires to reduce production cost as well as marketing

costs and to maintain high degree of efficiency for gaining competitive edge. The

second green revolution has to come by true transfer of technology on farmers field,

which not only will increase productivity but it will also enable to maintain and

improve soil health for sustainable agriculture. This task is very difficult due to

second generation problems, namely, deficiency of secondary and micro nutrients,

declining response of fertilizer use, incidences on new pests, lowering down of

ground water etc. come up in agriculture.