marketing alternatives

TRANSCRIPT

FEEDER CATTLE MARKETING ALTERNATIVES

James Mintert, Ph.D.Professor

Dept. of Agricultural EconomicsKansas State University

For Updated Livestock Marketing Information Visit The

K-State Livestock & Meat Marketing Web Site

www.agecon.ksu.edu/livestock

SellingQuality or grade that’s easiest to produce

Most convenient time

Most convenient place

Whatever price offered

Marketing

Identifying Quality or Grade with most profit potential

Most profitable time

Most profitable place

As a result, retain some control over price and profitability

Cattle Production Alternatives

•Background Own Calves Then Market

•Retain Ownership Of Calves For Finishing At Home

•Retain Ownership And Send To A Custom Feedlot

•Purchase Calves To Background Then Market

•Finish Backgrounded Calves At Home

•Finish Backgrounded Calves In A Custom Feedlot

Feeder Cattle Marketing Alternatives

•Market At Home Via Private Treaty

•Market At Local Auction

•Market Through Video Sale

•Market Via Internet

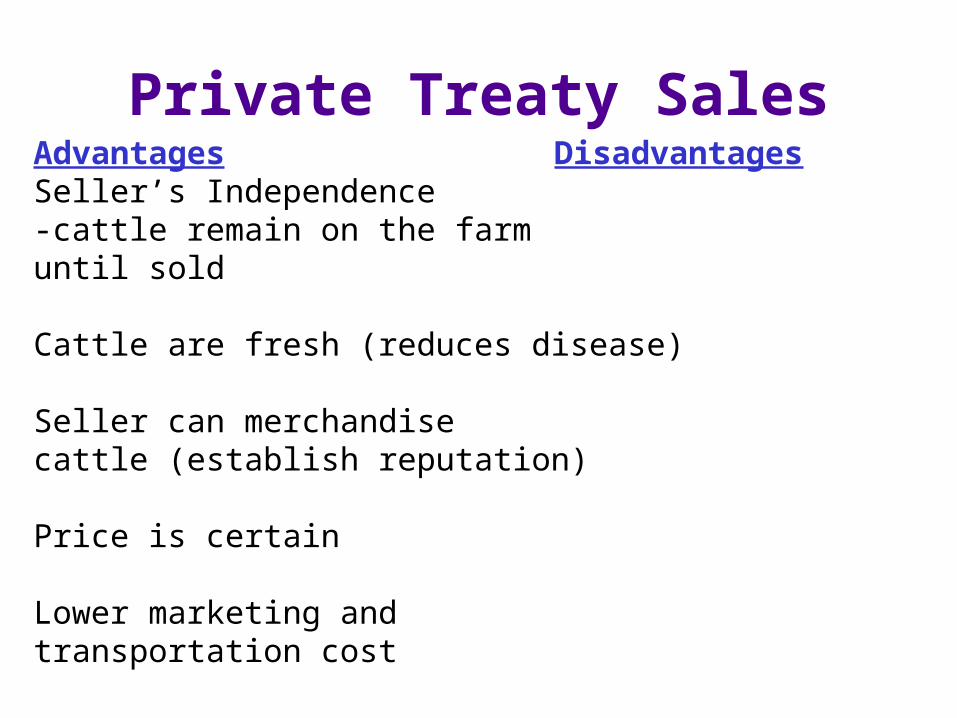

Private Treaty SalesAdvantages DisadvantagesSeller’s Independence -cattle remain on the farmuntil sold

Cattle are fresh (reduces disease)

Seller can merchandisecattle (establish reputation)

Price is certain

Lower marketing and transportation cost

Private Treaty SalesAdvantages DisadvantagesSeller’s Independence Seller totally responsible for-cattle remain on the farm success of saleuntil sold

Cattle are fresh (reduces disease) Seller must stay abreast of market

Seller can merchandisecattle (establish reputation) Seller assumes more risk

Price is certain $ Collection may be a problem

Lower marketing and Potential lack of competition

transportation cost

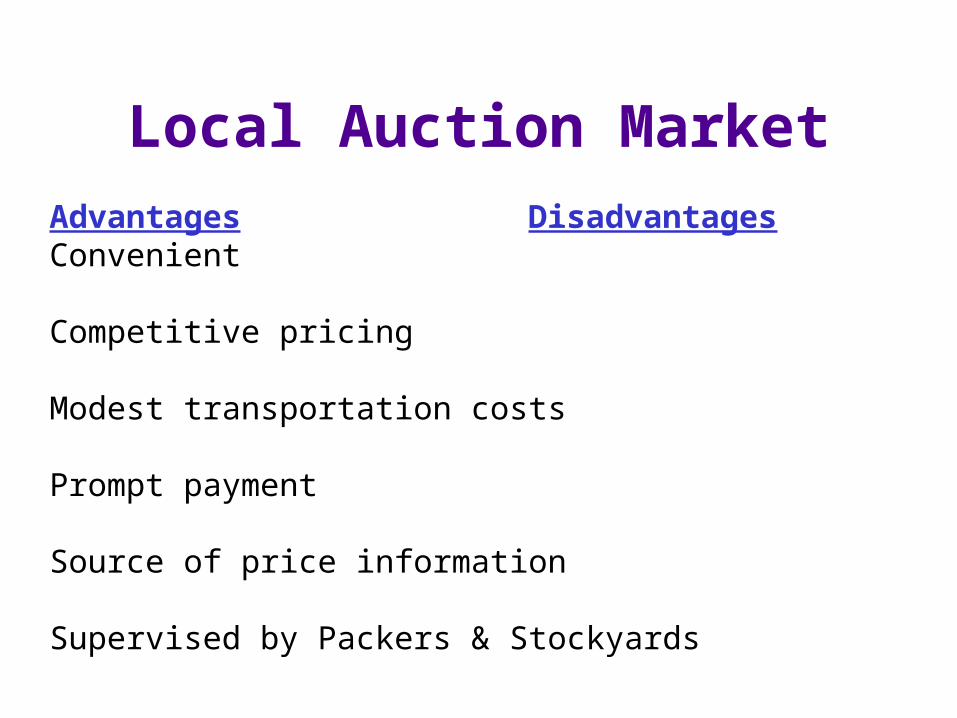

Local Auction MarketAdvantages DisadvantagesConvenient

Competitive pricing

Modest transportation costs

Prompt payment

Source of price information

Supervised by Packers & Stockyards

Local Auction MarketAdvantages DisadvantagesConvenient Seller has little effect on price

Competitive pricing Competition varies among sales

Modest transportation costs As a collection point - may spread disease

Prompt payment

Source of price information

Supervised by Packers & Stockyards

Video Auction SaleAdvantages DisadvantagesProducer sets sale conditions

Competitive pricing

Large number of buyers

Cattle remain on farm until sold

Video Auction SaleAdvantages DisadvantagesProducer sets sale Best suited for uniform loadsconditions 48,000-50,000 lbs.

Competitive pricing Must find market outlet for odd lots

Large number of buyers

Cattle remain on farm until Auctions held less frequently sold

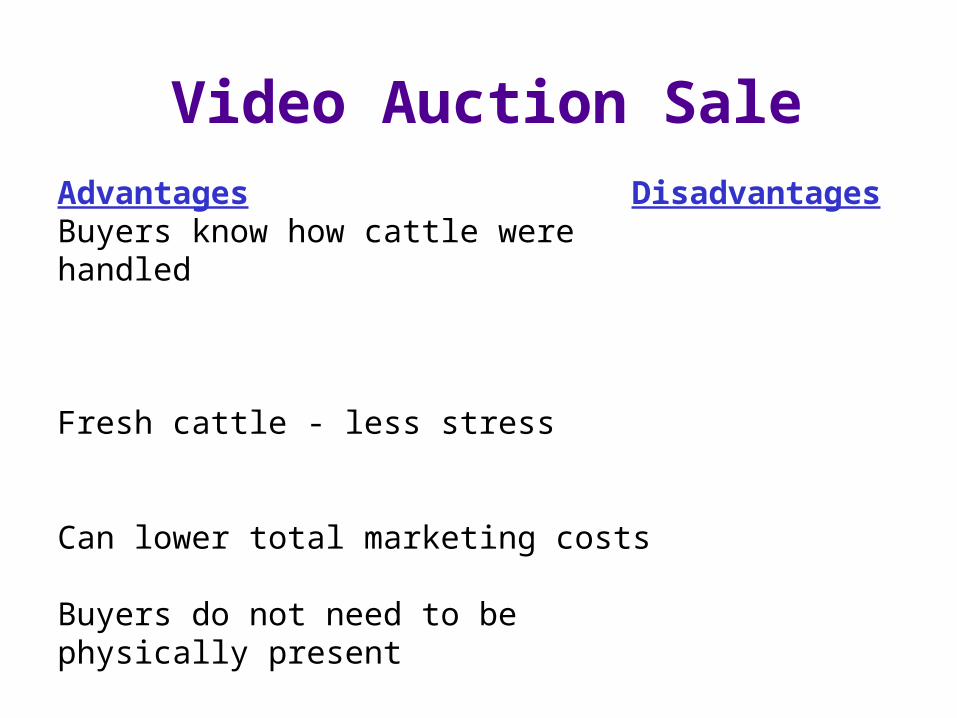

Video Auction SaleAdvantages DisadvantagesBuyers know how cattle werehandled

Fresh cattle - less stress

Can lower total marketing costs

Buyers do not need to be physically present

Video Auction SaleAdvantages DisadvantagesBuyers know how cattle were Requires consignment - have handled to commit cattle well in

advance of sale date-reduces flexibility

Fresh cattle - less stress Hard for buyers to estimateweight

Can lower total marketing costs Difficult for buyers toestimate flesh or condition

Buyers do not need to be physically present

Internet Auction SaleAdvantages Disadvantages

Essentially same advantages and disadvantages as Video Auction

Internet Brokerage SaleAdvantages DisadvantagesIndependence of seller cattle remain on the farmuntil sold

Cattle are fresh (reduces disease)

Seller can merchandisecattle (establish reputation)

Price is certain

Lower total marketing and transportation costs

Internet Brokerage SaleAdvantages DisadvantagesIndependence of seller Seller dependent on successcattle remain on the farm of auction web site in reaching until sold buyers

Cattle are fresh (reduces disease) Seller must stay abreast of market

Seller can merchandisecattle (establish reputation) Seller assumes more risk

Price is certain Potential lack of competition

Lower total marketing and transportation costs

Cattle Inventory Declined Again In 2000U.S. Cattle InventoryJanuary 1, 1925-2001

50

60

70

80

90

100

110

120

130

140

25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 00Year

Mill

ion

Hea

d

January 1, 2001 = 97.3 Million Head .

0.9% Less Than . on Jan. 1, 2000 .

Source: USDA

Current inventory is about 27% smaller than in 1975

K-State Research & Extension

Average Cycle Length Is About 10 Years

Cattle Inventories By Cycle .

75

85

95

105

115

125

135

1 2 3 4 5 6 7 8 9 10 11 12 13

Year of Cycle .

Cat

tle In

vent

ory

(Mill

ion

Hea

d)

1949-1958

1958-1967

1967-19791979-1990

1/1/01

Source: USDA & KSU

Plotting Inflation Adjusted Price vs. Per Capita Consumption Provides A Picture of Beef Demand

Beef Price Quantity RelationshipsAnnual, 1980-2000.

80

81

82

83

8485

86878800

89

275

300

325

350

375

400

425

450

64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80Per Capita Consumption - Retail Weight .

Def

late

d B

eef P

rice

- C

ents

per

Lb

Source: USDA & Commerce Dept. Price Deflated by GDP Implicit Price Deflator 1999=100

94 95

9390

92

91

9699

9897

Beef Price Quantity RelationshipsAnnual, 1980-2000.

80

81

82

83

8485

86878800

89

275

300

325

350

375

400

425

450

64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80Per Capita Consumption - Retail Weight .

Def

late

d B

eef P

rice

- C

ents

per

Lb

Source: USDA & Commerce Dept. Price Deflated by GDP Implicit Price Deflator 1999=100

94 95

9390

92

91

9699

9897

Declining Demand Has Plagued The Beef Industry For 20 Years

Beef Demand Declined Precipitously During The 1980’s

Beef Price Quantity RelationshipsAnnual, 1980-2000.

80

81

82

83

8485

86878800

89

275

300

325

350

375

400

425

450

64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80Per Capita Consumption - Retail Weight .

Def

late

d B

eef P

rice

- C

ents

per

Lb

Source: USDA & Commerce Dept. Price Deflated by GDP Implicit Price Deflator 1999=100

94 95

9390

92

91

9699

9897

Declining Demand Has Plagued The Beef Industry For 20 Years

Demand Continued To Decline During the 1990’s

Beef Price Quantity RelationshipsAnnual, 1980-2000.

80

81

82

83

8485

86878800

89

275

300

325

350

375

400

425

450

64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80Per Capita Consumption - Retail Weight .

Def

late

d B

eef P

rice

- C

ents

per

Lb

Source: USDA & Commerce Dept. Price Deflated by GDP Implicit Price Deflator 1999=100

94 95

9390

92

91

9699

9897

But showed signs of improving in 1999 & again in 2000

But Demand Showed Signs of Strengthening In 1999 & Again In 2000

Another Look At Demand

Compute a demand index

The index accounts for changes in beef quantity

The index relates current beef prices to prices expected if demand was held constant at some prior year’s level

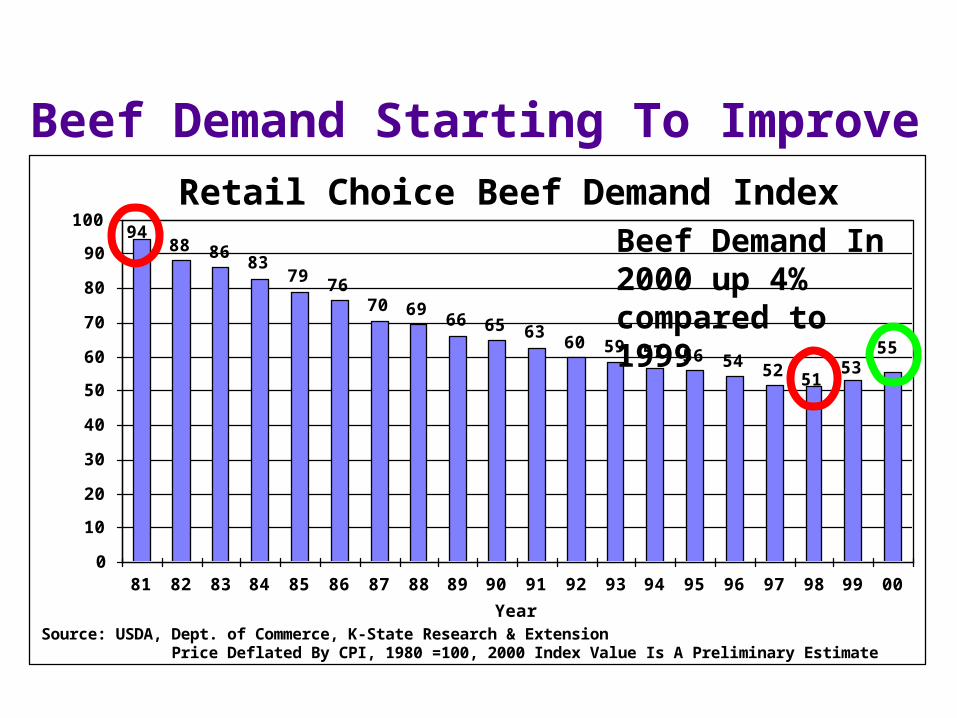

Beef Demand Starting To ImproveRetail Choice Beef Demand Index

88 86 8379 76

70 69 66 65 63 60 59 57 56 54 52 51

94

5553

0

10

20

30

40

50

60

70

80

90

100

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00Year

Inde

x Va

lue

Source: USDA, Dept. of Commerce, K-State Research & Extension Price Deflated By CPI, 1980 =100, 2000 Index Value Is A Preliminary Estimate

Beef Demand In 2000 up 4% compared to 1999

K-State Tenderness Value Study

Objective: Determine consumer perceptions and willingness to pay for tender beef

¦ In-store experiment conducted at several urban Kansas grocery stores - summer/fall 1998

Two tests, 1) blind taste test

2) tenderness revealed

What is the value of steak tenderness?

K-State Research and Extension

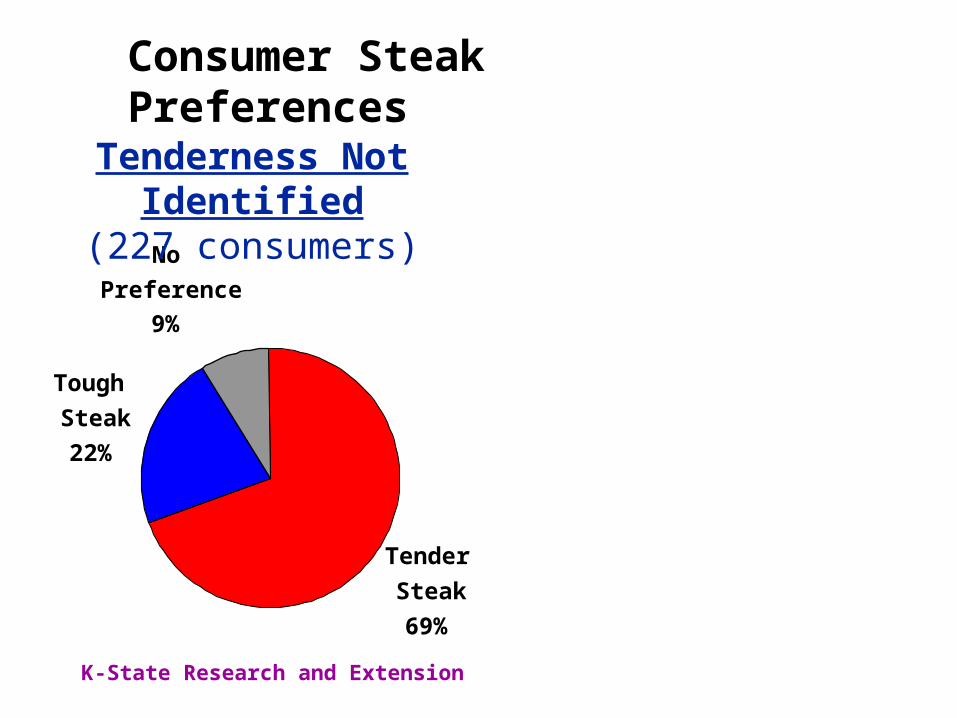

Consumer Steak Preferences

NoPreference

9%

TenderSteak69%

ToughSteak22%

Tenderness Not Identified(227 consumers)

K-State Research and Extension

Consumer Steak Preferences

NoPreference

9%

TenderSteak69%

ToughSteak22%

Tenderness Not Identified(227 consumers)

Tenderness Guaranteed(86 consumers)

TenderSteak84%

ToughSteak

9%

NoPreference

7%

Consumer Willingness to Pay for Tender Relative to Tough Ribeye Steak

(for those 69% preferring tender, 227 total consumers)

3

15

9

20

0 1 1 3 1 1 0 0

46

05

101520253035404550

$0.00 $0.67 $1.33 $2.00 $2.67 $3.33 $4.00Willingness to Pay ($/lb.)

Perc

ent o

f Res

pond

ents Average Willingness to pay

of those willing to pay $1.23/lb.

Consumer Willingness to Pay for Guaranteed Tender Relative to Tough Ribeye Steak

(for those 84% preferring tender, 86 total consumers)

14 6

27

06

0

13

03

04

36

05

101520253035404550

$0.00 $0.67 $1.33 $2.00 $2.67 $3.33 $4.00Willingness to Pay ($/lb.)

Perc

ent o

f Res

pond

ents

Average Willingness to payof those willing to pay $1.84/lb.

Beef Industry Opportunities

Provide consumer’s products they want

Some consumers willing to pay significantly for quality– Need to cater to these consumers

Food safety & health concerns need to be addressed continually

Liquidation Has Been Underway for 5 Years

U.S. Cattle Inventory Growth Rate1925-1999

-8

-6

-4

-2

0

2

4

6

8

25 30 35 40 45 50 55 60 65 70 75 80 85 90 95Year

Perc

ent

Source: USDA & KSU

But A Rebound In Profitability Will Lead To Inventory Increases

Estimated Cow-Calf Returns .

-100

-50

0

50

100

150

200

250

75 77 79 81 83 85 87 89 91 93 95 97 99 Year

$'s

Per C

ow

.

Source: K-State Research & Extension Returns ABove Variable Costs

KSU Projection For 2000

When inventories start to increase, slaughter will decline sharply

Heifer Slaughter Expected To Drop During 2001

Annual F.I. Heifer Slaughter .

6

7

8

9

10

11

12

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00

Year

Mill

ion

Head

Source: USDA .

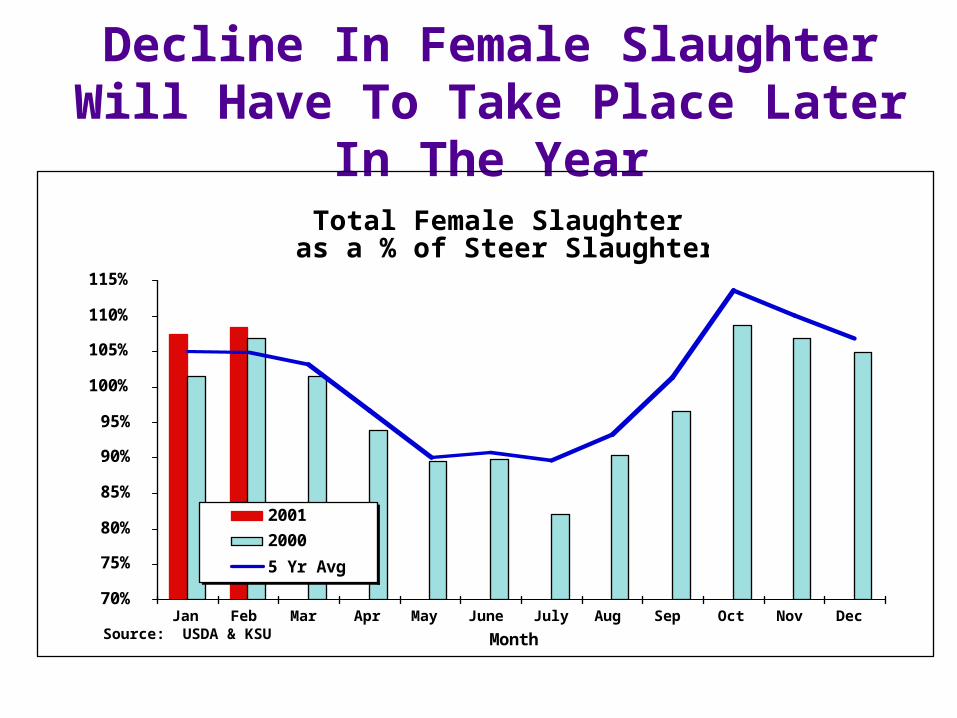

Decline In Female Slaughter Will Have To Take Place Later In The Year

Total Female Slaughter as a % of Steer Slaughter

70%

75%

80%

85%

90%

95%

100%

105%

110%

115%

Jan Feb Mar Apr May June July Aug Sep Oct Nov DecMonth

Fem

ale

Slt.

as %

of S

teer

Slt.

200120005 Yr Avg

Source: USDA & KSU

Total Cattle Slaughter Will Decline in 2001

Annual Commercial Cattle Slaughter .

31323334353637383940414243

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00

Mill

ion

Head

.

Source: USDA Year

& Slaughter Cattle Prices Headed Higher The Next Couple Of Years

Annual Average Steer Prices .W. KS 11-13 Cwt. .

35

40

45

50

55

60

65

70

75

80

75 77 79 81 83 85 87 89 91 93 95 97 99 01Year .

Stee

r Pric

e ($

/Cw

t.)

.

Source: USDA

What’s Taken Place This Winter?

Cattle Slaughter Down 5.9% This Winter vs. 2000

steer & heifer slaughter down 8.9%

but cow slaughter up vs. last year

Steer weights down 1.1%

Result, beef production down over 7.1% vs. 2000

Reduction in beef supplies pushed beef and cattle prices up vs. last year

Boxed Beef Values Were Record High, But Prices Have Declined As Slaughter Increased

Weekly Box Beef Cutout ValuesChoice, 550-700 Lb. Carcasses

95

100

105

110

115

120

125

130

135

140

1/06 2/17 3/31 5/12 6/23 8/04 9/15 10/27 12/08

$'s/

cwt.

200020015 Yr Avg

Source: AMS-USDA, Des Moines, IA & KSUWeek Ending

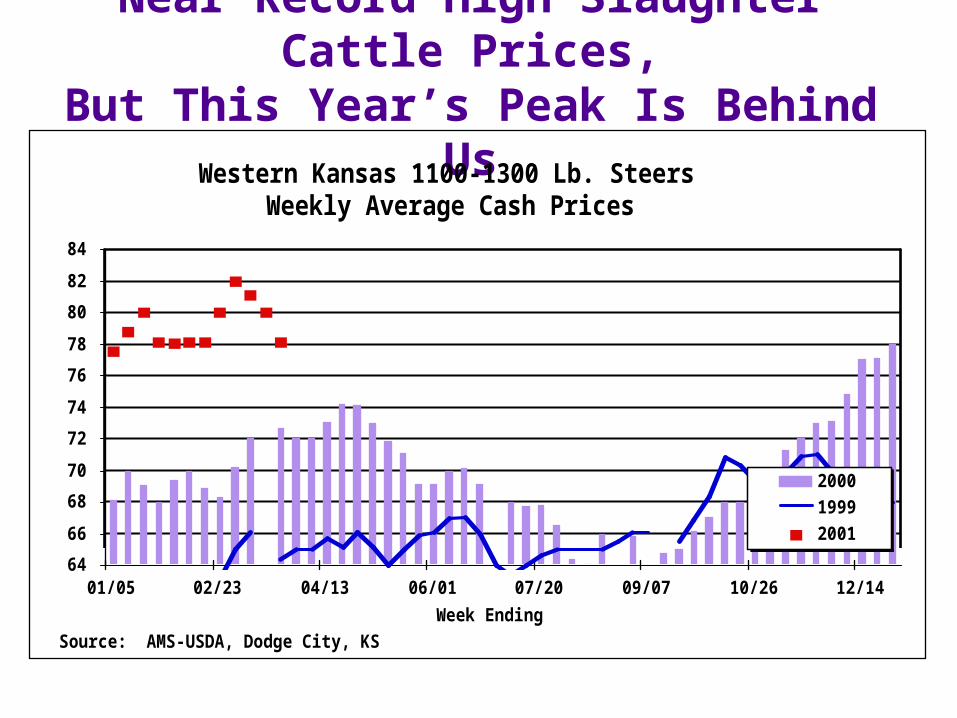

Near Record High Slaughter Cattle Prices,But This Year’s Peak Is Behind Us

Western Kansas 1100-1300 Lb. SteersWeekly Average Cash Prices

6466687072747678808284

01/05 02/23 04/13 06/01 07/20 09/07 10/26 12/14Week Ending

$/cw

t

200019992001

Source: AMS-USDA, Dodge City, KS

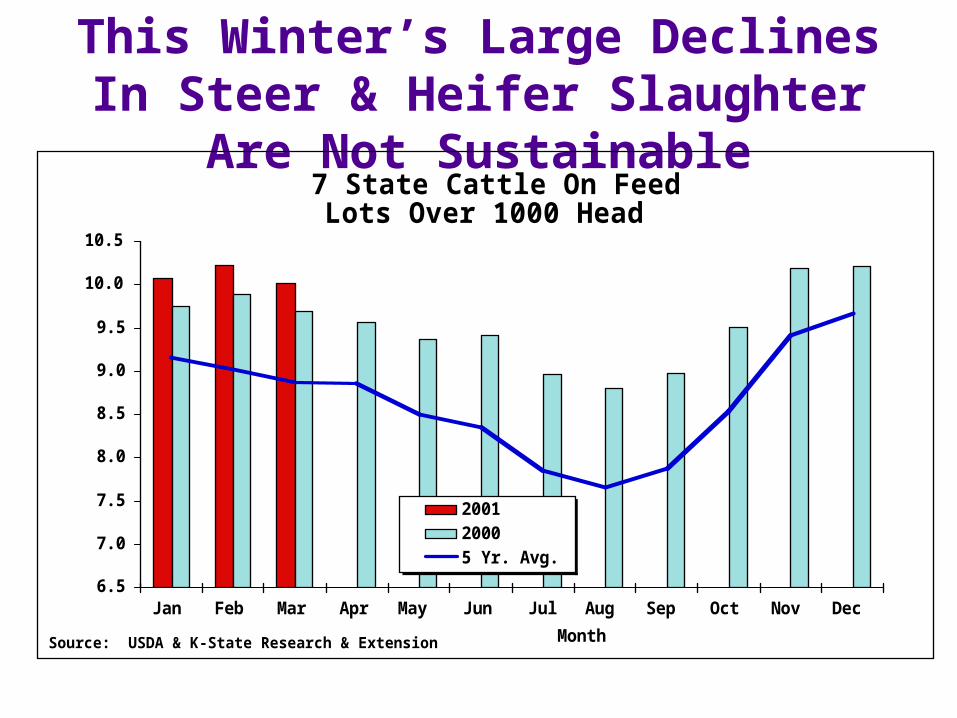

This Winter’s Large Declines In Steer & Heifer Slaughter Are Not Sustainable

7 State Cattle On Feed .Lots Over 1000 Head .

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecMonth

Mill

ion

Hea

d

200120005 Yr. Avg.

Source: USDA & K-State Research & Extension

Cattle Feeders Need To Play Catch-UpFed Cattle Marketings

% of On Feed Inventory

14%

15%

16%

17%

18%

19%

20%

21%

22%

23%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecMonth

% o

f On

Feed

Inve

ntor

y

200120005 Yr. Avg.

Source: USDA & K-State Research & Extension

Futures Suggest April Prices In High $70’sFollowed By A Seasonal Decline Into Summer

Mid-Month Futures Based Price Forecasts W. Kansas 1100-1350 Lb. Choice Steers

68

70

72

74

76

78

80

82

Apr.'01

May'01

Jun.'01

Jul.'01

Aug.'01

Sep'01

Oct.'01

Nov.'01

Dec.'01

Jan.'02

Feb.'02

Mar.'02

Month

$/cw

t.

3 Yr. Avg. BasisMost Neg. BasisMost Pos. Basis

Source: CME & K-StateForecasts = Friday's Futures Settlement Prices + Basis Estimates

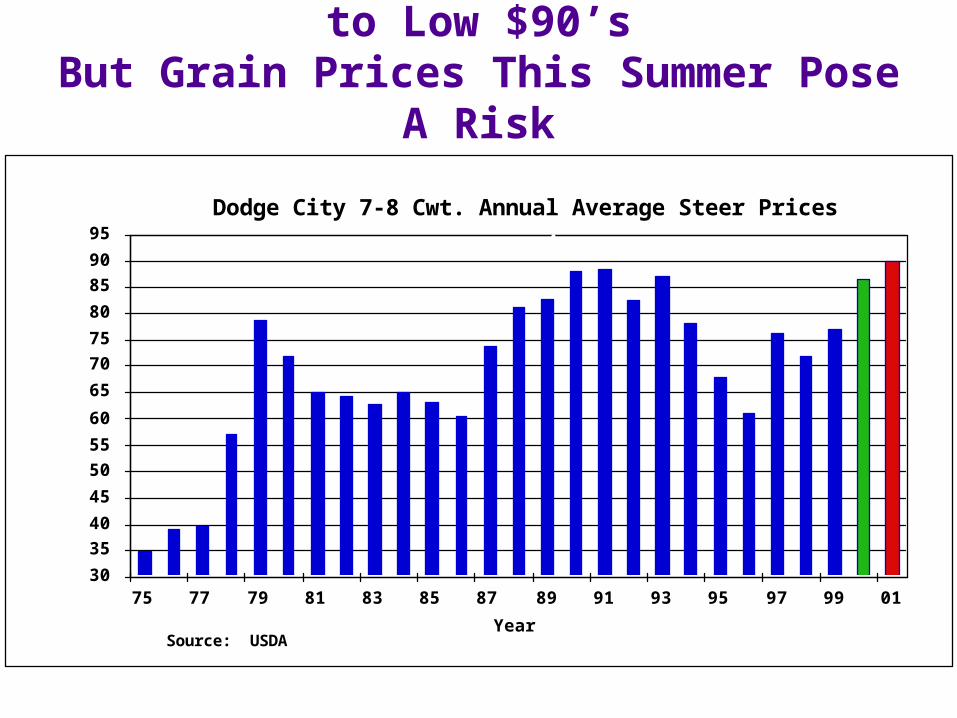

Feeder Cattle Prices In High $80’s to Low $90’sBut Grain Prices This Summer Pose A Risk

Dodge City 7-8 Cwt. Annual Average Steer Prices .

3035404550556065707580859095

75 77 79 81 83 85 87 89 91 93 95 97 99 01Year

Stee

r Pric

e ($

/Cw

t.)

.

Source: USDA

Feeder Futures Suggest A Tight Trading Range In ‘01& Feed Grain Prices Will Be Critical

Mid-Month Futures Based Price Forecasts . 700-800 Lb. Feeder Steers, Dodge City, KS .

828384858687888990919293

April'01

May'01

Jun.'01

Jul.'01

Aug.'01

Sep.'01

Oct.'01

Nov.'01

Dec.'01

Jan.'02

Month & Year .

$/cw

t.

.

3 Yr. Avg. Basis Most Neg. Basis Most Pos. Basis

Source: CME & K-State Forecasts =Friday's Settlement Prices + Basis Estimates

Summary Cow-Calf Producers In Drivers Seat Tougher For Margin Operators

– Cattle Finishers Could Lose $ This Summer

– Grazing Programs Carry Risk

Long-Term Outlook– Cyclical Peak In Cattle Prices Is Still Ahead Of Us

– Major Risk Is Beef Demand

Largest Beef ExportersRanked By Quantity Exported

1 Australia

2 U.S.

3 Brazil

4 European Union

5 Canada

6 New Zealand