market update: oil & gas enewsletter - kpmg · pdf filebeing recently accused of...

TRANSCRIPT

Oil markets – monthly round upDecember 2014

Global crude oil benchmarks took another dramatic fall in November as expectations that OPEC would maintain production levels were realised (c. 30/mbpd).

Over the course of the month ICE Brent traded as low as $69.78/b, a 4½ year low. NYMEX WTI meanwhile broke through a key notional support level at $70/b dipping to $65.69/b immediately after the OPEC announcement. The OPEC reference basket (ORB) price averaged $75.57/b in November – and is set to average out the year below $100/b, the first time in four years.

Market Update: Oil and Gas

OPEC chatter

Market sentiment was dominated by OPEC in the build up to the most eagerly-awaited get-together in recent memory. Saudi Arabian oil minister Ali al-Naimi was the focal point of media coverage ahead of the November 27 meeting – having being recently accused of initiating a ‘price war’ with the US after slashing the official selling price (OSP) of Saudi Arabian crude oil.

Presented below is a time series showing the volumes of social media posts discussing “OPEC” over the past three months, set against the changing price of crude oil. Key events, including the recent decision by OPEC to maintain production are marked, with the resulting changes in price highlighted.

OPEC social media analysis

CONTACT

Anthony Lobo Head of Oil & Gas EMEA and ASPAC

T: +44 20 7311 8482 E: [email protected]

OPEC Social Media Analysis

02/0

9/20

14

04/0

9/20

14

08/0

9/20

14

10/0

9/20

14

12/0

9/20

14

16/0

9/20

14

18/0

9/20

14

22/0

9/20

14

24/0

9/20

14

29/0

9/20

14

01/1

0/20

14

06/1

0/20

14

08/1

0/20

14

10/1

0/20

14

14/1

0/20

14

16/1

0/20

14

21/1

0/20

14

23/1

0/20

14

27/1

0/20

14

29/1

0/20

14

31/1

0/20

14

04/1

1/20

14

06/1

1/20

14

10/1

1/20

14

12/1

1/20

14

14/1

1/20

14

18/1

1/20

14

20/1

1/20

14

24/1

1/20

14

26/1

1/20

14

28/1

1/20

14

0K

10K

20K

Num

ber o

f Pos

ts

$60/b

$80/b

$100/b

ABCDEF

Time Series - Oil Prices Against Volume of Comments with Key Events

C. Wall Street Journal tweets that an oil price of $70 a barrel would likely triggercut in OPEC output ceiling. Over 400 retweets.

F. OPEC Secretary General Abdalla el-Badri said he expects OPEC to lower itsoutput target for 2015 at the organization’s November meeting in Vienna.

A. OPEC decision to maintain production D. Media Reports on OPEC members fighting for market share amid fallingprices

B. Kuwaiti Oil Minister Ali al-Omair said current oil prices are unlikely to have anegative impact on the economies of Kuwait and other Gulf oil producers. E. Iran calls for OPEC to cut production

Social Media Posts

ICE Brent Low Price

Key Date

Time Series – Oil Prices Against Volume of Comments with Key Events

Analysis provided by KPMG Data Insight Services // Unstructured Data Analytics

A. OPEC decision to maintain production.

B. Kuwaiti Oil Minister Ali al-Omair said current oil prices are unlikely to have a negative impact on the economies of Kuwait and other Gulf oil producers.

C. Wall Street Journal tweets that an oil price of $70 a barrel would likely trigger cut in OPEC output ceiling. Over 400 retweets.

D. Media Reports on OPEC members fighting for market share amid falling prices.

E. Iran calls for OPEC to cut production.

F. OPEC Secretary General Abdalla el-Badri said he expects OPEC to lower its output target for 2015 at the organisation’s November meeting in Vienna.

The analysis clearly demonstrates that OPEC continues to influence market sentiment and plays a significant role in the direction of oil price.

© 2014 KPMG LLP, a UK limited liability partnership, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

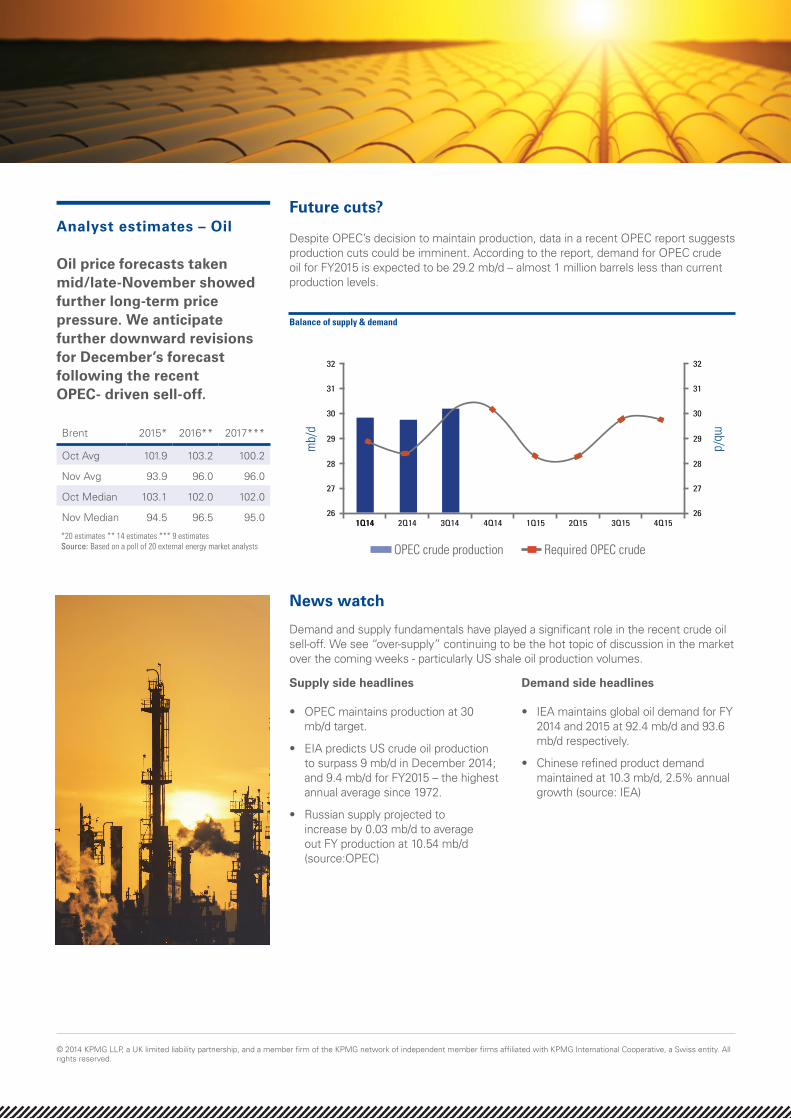

Analyst estimates – Oil

Oil price forecasts taken mid/late-November showed further long-term price pressure. We anticipate further downward revisions for December’s forecast following the recent OPEC- driven sell-off.

Brent 2015* 2016** 2017***

Oct Avg 101.9 103.2 100.2

Nov Avg 93.9 96.0 96.0

Oct Median 103.1 102.0 102.0

Nov Median 94.5 96.5 95.0

Future cuts?

News watch

Despite OPEC’s decision to maintain production, data in a recent OPEC report suggests production cuts could be imminent. According to the report, demand for OPEC crude oil for FY2015 is expected to be 29.2 mb/d – almost 1 million barrels less than current production levels.

Demand and supply fundamentals have played a significant role in the recent crude oil sell-off. We see “over-supply” continuing to be the hot topic of discussion in the market over the coming weeks - particularly US shale oil production volumes.

Balance of supply & demand

1Q14

32

26

27

28

29

30

31

32

26

27

28

29

30

31

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Supply side headlines Demand side headlines

• OPEC maintains production at 30 mb/d target.

• EIA predicts US crude oil production to surpass 9 mb/d in December 2014; and 9.4 mb/d for FY2015 – the highest annual average since 1972.

• Russian supply projected to increase by 0.03 mb/d to average out FY production at 10.54 mb/d (source:OPEC)

• IEA maintains global oil demand for FY 2014 and 2015 at 92.4 mb/d and 93.6 mb/d respectively.

• Chinese refined product demand maintained at 10.3 mb/d, 2.5% annual growth (source: IEA)

mb/

d mb/d

Required OPEC crudeOPEC crude production*20 estimates ** 14 estimates *** 9 estimatesSource: Based on a poll of 20 external energy market analysts

Brought to you by the KPMG Global Energy Institute – www.kpmg.com/energy

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2014 KPMG LLP, a UK limited liability partnership, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

Analyst estimates – Gas

Long term estimates for Henry Hub gas were revised down by analysts in November on stronger domestic production and ample supply for the approaching winter.

Henry Hub 2015* 2016** 2017***

Oct Avg 4.1 4.3 4.4

Nov Avg 3.9 4.2 4.4

Oct Median 4.1 4.3 4.4

Nov Median 4.0 4.2 4.5

Gas markets – monthly round up

USHenry Hub for prompt delivery was supported by colder-than-normal temperatures across the US in November. The front month contract traded as high as $4.544/MMBtu closing the month slightly higher than October (source: Bloomberg).

UK NBP Front month contract edged higher on seasonal effects of colder temperatures and unplanned outages in Norway. The December contract up to expiry (27th Nov) closed at 58.58p/th, up 5.4% (source: Bloomberg).

JAPAN The JKM contract, a spot reference for Liquefied Natural Gas cargoes assessed by Platts, averaged $10.77/MMBtu in November, the lowest level since February 2011. The fall in price was largely attributed to inventory builds in Japan and South Korea supressing the demand for incremental volumes.

Industry benchmarks

Thoughts from the oil & gas team

“OPEC is protecting itself in the longer term. Losing market share to the US would limit OPEC’s ability to influence oil prices in the future. OPEC has taken a gamble that shale oil production will reduce as a consequence of low oil price and high production costs. This is a high risk strategy and could inflict more pain on a number of already-disgruntled OPEC members, not to mention Russia.”

Emma Wild, Head of Upstream Advisory, KPMG in the UK

Oil: OPEC’s decision to maintain production

Oil: Upstream activity“The recent price fall will add further pressure to exploration budgets, as upstream players batten down the hatches and reduce their exposure to high risk prospects. The ability of some companies to service their debt in this market may also be impacted by the lower cash flows. However there are still investment opportunities to be had for those with significant cash and debt capacity.”

Anthony Lobo, Head of Oil & Gas, EMEA & ASPAC

“This is an opportune moment for oil-intensive users - such as airlines - to capitalise on the low price environment and secure long-term price protection. Oil producers on the other hand face a tricky dilemma – hedge at the current market rate - or postpone and potentially face further misery.”

George Johnson, Executive Advisor, Oil & Gas, KPMG in the UK

Oil: Hedging

HH

NBP

JKM

A $60/b world?Oil prices have tumbled almost 40% in five months putting an enormous strain on oil revenues and capital expenditure budgets for oil and gas companies. The price drop has also seen share prices of global oil majors and upstream companies fall significantly.

*18 estimates ** 14 estimates *** 5 estimatesSource: Based on a poll of 18 external energy market analysts (mid/late november 2014)