market update

TRANSCRIPT

Dear Client: Washington, Nov. 2, 2012

Though a better economy is likely in 2013… The gains won’t be clear until summer.So come Jan...whether it is Barack Obama againor Mitt Romney who sits in the Oval Office… The sluggish economy will remain a worry.Even dramatic policy shifts…and they’re not likely,given a closely divided Congress…would take timeto rev up the economic engine significantly.

Problem No. 1: Avoiding the fiscal cliff before year-end, when spending cuts kick inand the lower tax rates of the past decade expire. Deadlock would spell recession ahead,paring up to four percentage points from GDP growth. But we still expect a deal to buy more time,putting off tough decisions until the new Congressis seated, probably giving lawmakers till spring to act.

In any case, growth in early 2013 will slow,dipping from a bit better than 2% in the second halfof this year to only about 1.5% for Jan.-June of 2013.Tighter fiscal restraints...whether due to higher taxesor federal spending cuts, or both…will curb gains.Just ending the payroll tax break (a fair bet) would trim 0.5% from GDP, for example.

Little lift from overseas demand. Europe is likely to remain in a recessionthrough the first half...even powerhouse Germany is flagging. Plus China’s slowdownwill ripple through Asia. So U.S. export growth will be curbed, held to only about 5%. A similarly weak 3% bump for business spending. There’s not much incentivefor firms to release any of the $1.7-trillion stash they’re sitting on to expand factoriesand offices or buy new equipment while job growth and demand remain sluggish. Nor will government spending deliver much. Lawmakers in both partiesagree on the need to rein in Uncle Sam’s budget. And state and local governments,just regaining their equilibrium, are in no mood to launch major spending projects. Early 2013 will see a teeny boost from post-hurricane buying and building,but only enough to offset the spending hit in late 2012 and not an appreciable lift.

In the second half…considerably more pep. As the housing marketpicks up steam, it’ll add wealth to the economy and nurture consumer spending.The Federal Reserve will keep mortgage rates near all-time lows, encouraging buildingand buying. Plus, as the year unfolds...more eagerness among banks to make loans. By year-end, look for growth chugging along at a much healthier 3% pace. But for 2013 as a whole…another yearly gain in the 2% neighborhood. All told, about 2 million net new jobs…enough to lower the jobless rateto 7.5% and to keep consumer spending on an upward path, albeit a weak one.No better than this year’s 2% gain, maybe less, for this giant chunk of the economy.

1100 13th Street NW, Washington, DC 20005 • kiplinger.com • Vol. 89, No. 44

The Kiplinger Letter (ISSN 1528-7130) is published weekly for $117/one year, $199/two years, $263/three yearsby The Kiplinger Washington Editors, 1100 13th St. NW, Suite 750, Washington, DC 20005-4364.POSTMASTER: Send address changes to The Kiplinger Letter, P.O. Box 3297, Harlan, IA 51593.

Subscription inquiries: 800-544-0155 or [email protected] Editorial information: Tel., 202-887-6462; Fax, 202-778-8976;

E-mail, [email protected]; or website, kiplinger.com

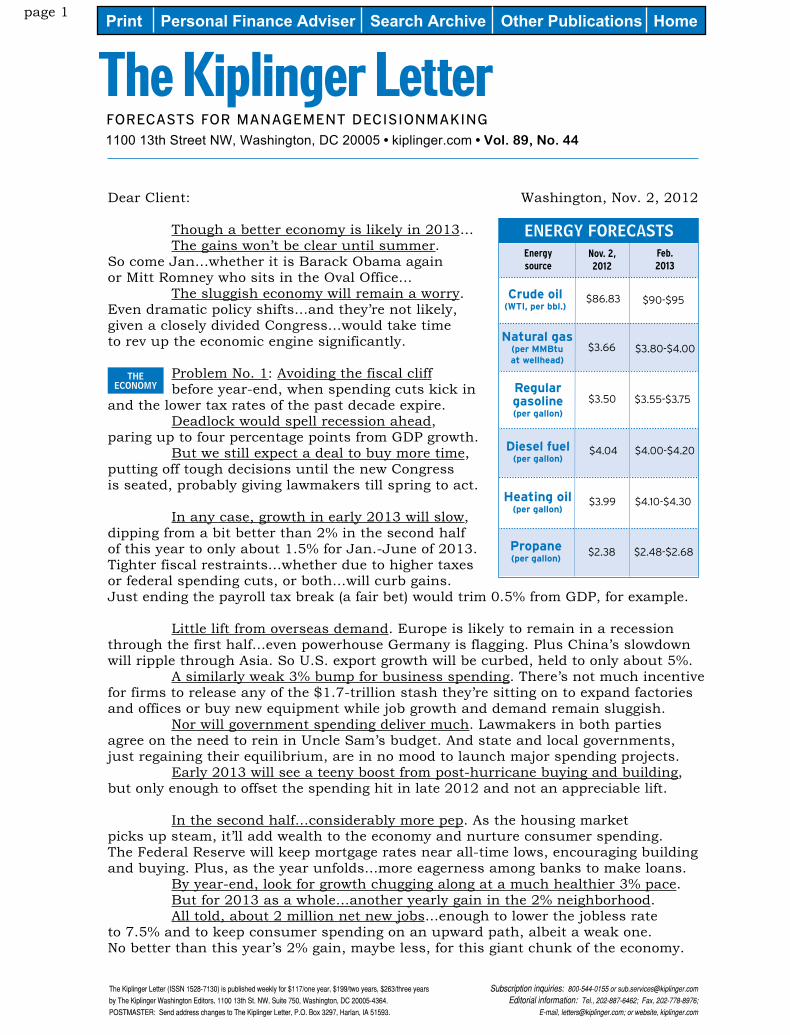

$86.83 $90-$95

$3.66 $3.80-$4.00

$3.50 $3.55-$3.75

$4.04 $4.00-$4.20

$3.99 $4.10-$4.30

$2.38 $2.48-$2.68

Feb.2013

Energysource

Nov. 2,2012

ENERGY FORECASTS

Crude oil(WTI, per bbl.)

Natural gas(per MMBtuat wellhead)

gasoline(per gallon)

Regular

Diesel fuel(per gallon)

Heating oil(per gallon)

Propane(per gallon)

THEECONOMY

Print Personal Finance Adviser Search Archive Other Publications Home page 1

Corporations aren’t done disappointing investors with lackluster earnings. Only a third of companies are likely to beat estimates in the third quarter…a far cry from the 56% that normally top analysts’ earnings forecasts. What’s more… Results for the next two quarters figure to fizzle, too. Blame slowing growthin Europe and China…S&P 500 firms depend on overseas markets for 45% of sales. The hit will be broad, from tech firms to energy and materials suppliers.Makers of consumer goods are bracing for a drop-off in spending early next year,while financial firms will struggle to raise revenue in the face of low interest rates.

Take Oct.’s auto sales with a grain of salt. Foul weather likely dinged themby about 30,000 vehicles. On the East Coast, the last few days of the month were lostto floods and blackouts as Hurricane Sandy pounded states from Va. to Maine. Nov. auto sales figures will more than make up the difference as shoppersmake buys planned for Oct. and replace vehicles crushed or flooded in the storm. When all is said and done, sales are still on track for 14.5 million in 2012. The growing U.S. market offers a tempting target for Europe’s automakers.Faced with slumping sales at home, European carmakers are rushing to compensate by shifting more production Stateside and tailoring models to suit American tastes.Luxury brands such as Audi and Mercedes are even rolling out new entry-level modelswith lower price tags to lure first-time customers and expand their market share.

Mobile phone programs are becoming big business, creating thousandsof jobs for programmers and buoying local economies across the country. By 2016,sales of mobile apps and related revenue will total $46 billion. In 2011...$10 billion. And it’s not just in Silicon Valley. Texas, N.J., Ga. and Ill. boast $1 billionor more in annual app-related revenue. Tech-heavy N.Y. and Wash. do even better. Driving the boom: Robust demand and low production costs. Typical appssell for 90 days before being replaced, keeping programmers busy and sales brisk.And they require little more to build than creativity and a fast Internet connection.

N.D.’s oil boom is spawning an industrial renaissance in the regionas railroads and pipeline operators race to keep up with demand to move crude oilto refineries. BNSF Railway, for example, is pouring millions into increasing capacity…$197 million this year and even bigger investments in years ahead. Also coming:Miles of pipeline to deliver Bakken Formation shale oil. Capacity will triple by 2015.

Nuclear safety will get a boost in 2014, when plant owners and operators plan to open two emergency depots to store and deploy critical safety gear.The sites, in Memphis, Tenn., and Phoenix, Ariz., will house key equipment…pumps,radiation monitors, protective suits…within 24 hours’ deployment to any U.S. plant. Setting up emergency depots poses challenges...from ensuring compatibilityof stored gear and existing systems at all 64 of the nation’s nuclear power plantsto coordinating emergency response plans with local and federal government officials. But the payoff will be worth the effort and the $40-million cost. U.S. plantsappear to have taken to heart the lesson from Japan’s 2011 nuclear disaster:Quick deployment of the right safety equipment is critical to preventing meltdowns.

Safety concerns are mounting at Europe’s nuclear plants, too. Regulators with the European Union’s nuclear watchdog recently faulted most of the 132 reactorsin the EU for some type of safety issue, after a long review following Japan’s crisis. The cost of bringing Europe’s plants up to snuff will be steep…$30 billion.Of the 18 facilities scheduled to shut down, most will keep running for another decade,and regulators want safety worries corrected pronto, forcing most plants to pony up. U.S. firms will have a chance to cash in, providing everything from sensorsto backup power systems and filters that safely vent gas when reactors overheat.

Remember, your subscription includes The Kiplinger Letter online

BUSINESSOUTLOOK

ENERGY

page 2 Nov. 2, 2012

On the horizon: Another giant leap in the speed of Internet communication. An innovative type of network coding using advanced mathematicsstreamlines how data packets are sent and received for a 10-fold increase in speed. Even better news: The new technology requires no infrastructure upgrades.It’s likely to be a must-have for cell companies seeking to improve their bandwidthto serve growing demand for data downloads…from movies to massive spreadsheets.Boston-based Code-On Technologies, a start-up by math wizards at MIT and Caltech,will license the technology. It’ll start rolling out commercial applications next year.

Software to greatly increase office workers’ productivity is also in the works.Developed at Carnegie Mellon Univ., it uses a type of artificial intelligence to automateand streamline mundane computer tasks…filling out forms, updating spreadsheets,even sorting and responding to some e-mail. Automating the data retrieval functionsmeans humans need only oversee the results rather than do the tasks from scratch.Because a typical office worker spends nearly half of each workday on such tasks,the potential for supercharging productivity is huge. Imagine a day with fewer e-mails. And for mechanical industries…a big boost from augmented reality eyeglasses.They make workers “smarter” by overlaying their view of equipment and machinerywith 3-D schematics, making maintenance and repair tasks, for example, easier.The glasses can also display video, respond to verbal commands and hand gesturesplus connect wirelessly with distant experts for assistance. Initial costs will be high…around $2,000 for a pair of the glasses. But uses in engineering, telecom, aviationand other industries abound, and the productivity payoff will be worth the investment.

By early 2013…good odds of a federal cybersecurity policy, with regs to follow. Win or lose, President Obama will step in if Congress doesn’t, ordering firmsinvolved with critical infrastructure…transportation, communications and power…to first share info with the feds and then beef up protection against disabling attacks.A bipartisan proposal for voluntary cooperation has the best odds of passing musterwith lawmakers, but it’s a long shot and may not go far enough for the White House.

For instant online access and searchable archives, go to kiplinger.com/start

As the campaign season draws to a close and voters head to the polls… A reminder about how we at Kiplinger see our role in covering elections,which is sometimes unclear to our readers during a bitter campaign like this: We forecast the outcomes of national elections, without endorsements,exploring what those outcomes will likely mean to you and your business. We aim for clear-eyed, objective judgments, free of bias and partisanship,which typify the journalism of some columnists, talk shows and cable news outlets. It’s easy to get information that supports your personal preferences. But it may not be useful information on which to base your plans.

Our readers are mostly in business, and we’re aware of your concerns.Heck, we’re in business, too, and we have many of the same worries you doabout the sluggish economy, higher taxes, more regulation and so on. But... Sound decisions aren’t based on what you…or we…want to happen. They’re based on good intelligence about what is most likely to happen.

Our presidential forecasting record has been very good...a correct callof every race since Eisenhower won his first term in 1952, including the electionsof Kennedy, Nixon, Carter and Reagan plus George W. Bush’s squeaker in 2000.(Our only blunder in 89 years...a doozy: Forecasting Dewey over Truman in 1948.) If we get the call wrong, it won’t be due to bias but rather to faulty analysisand projections. And we’ll apologize for the bad call...a disservice to our readers.

POLITICS &THE PRESS

TECH

HOMELANDSECURITY

page 3 Nov. 2, 2012

Can Obama win the electoral vote while Romney wins the popular vote? Yes, especially in the wake of the hurricane that tore through the Northeast.Flooding and damage will dampen turnout in N.Y., N.J., Conn., Pa., Md. and Del.,reducing the usual cushion for Democratic candidates, but Obama will still win them. The odds continue to favor another term for Obama, but not by a blowout.Romney seems on course for as many as 267 electoral votes…three short of victory…and he’s not likely to rack up fewer than 235 unless he loses to Obama in Fla.Obama may take as few as 271 (one more than needed) and likely not more than 303. Polls in a few key states are close enough that Romney could buck the odds.But at a time when Romney’s momentum was slowing, it was halted altogether,through no fault of his own, because Hurricane Sandy grounded both candidatesfor several days at a critical juncture. Mother Nature was this year’s Oct. surprise. In no case, though, could either candidate legitimately claim a mandate.

And don’t be taken aback if recounts leave election results in limbo for a bit. Because of the storm, some states may allow more provisional ballots,which will take more time to authenticate. Plus many states stipulate another countif the candidates are within a percentage point of each other...good odds of that. But no replay of Fla. in 2000. That was a once-in-your-lifetime occasion.Any recounts this time will be done in a matter of days, not more than a month. Still, lawyers for both sides are ready. Democrats have 5,000 in Fla. alone.And the counsel-to-voter ratio will be enormous in states that allow early voting,especially those with the biggest potential to change the outcome...think Ohio, Iowa,Colo. and Nev., along with the Sunshine State. Interest groups are lawyered up, too.

Plus election lawyers will be employed long after this race is settled. They’ll be battling for an edge in 2014 and 2016. At the center of the fight:A volley of state laws that require showing government identification at polling placesand a hodgepodge of election rules that make early voting widespread in some states.Some court rulings blocked voter ID efforts this year but left the door open for later.

Proof that neither candidate has long coattails? The Senate contests. In a quarter of states with both races, voters seem poised to split tickets…backing a presidential candidate from one party and a senator from the other one. Divided ballots will help Democrats hold on to the majority in the Senate.Once-vulnerable Democrats will keep Senate seats in Va. and Fla., and maybe in Mo.and Mont., too. Romney has a shot to carry the first two and will win the latter two.Other states where votes may be split on Election Day: Wis., Ind., N.D. and Nev.

If Romney loses the presidential race, expect calls for remaking the GOP. Preelection simmering of right-vs.-centrists will boil over in the aftermath.Conservatives who gave only lukewarm backing to Romney will say “we told you so”and demand candidates who take Republicans even further to the right next time.Mainstreamers will say they control the purse strings and should set the agenda. Neither side is inclined to cave, but neither will risk a fractured party:If the tea partyers or moderates set out on their own, the Democrats will benefit. In the Senate, Republican Leader Mitch McConnell of Ky. may be jettisoned,the scapegoat for blowing what was seen as a good chance to win control of that body.RNC Chm. Reince Priebus likely goes, but not House Speaker John Boehner of Ohio.

Yours very truly,

Nov. 2, 2012 THE KIPLINGER WASHINGTON EDITORS

Copyright 2012. The Kiplinger Washington Editors, Inc. Quotation for political or commercial use is not permitted. Duplicating an entire

issue for sharing with others, by any means, is illegal. Photocopying of individual items for internal use is permitted for registrants with

the Copyright Clearance Center, 222 Rosewood Drive, Danvers, MA 01923. For details, call 978-750-8400 or visit www.copyright.com.

POLITICS

page 4 Nov. 2, 2012