market segmentation - cng no pdfs/tiax_marketsegmentation.pdf · this market segmentation report...

TRANSCRIPT

Market Segmentation

Final Report

U.S. and Canadian Natural Gas Vehicle Market Analysis:

2 I

Legal Disclaimer

This report was prepared by TIAX for America’s Natural Gas Alliance on terms specifically limiting TIAX’s liability. Our conclusions are the result of the exercise of our best professional judgment based in part upon materials and information provided to us by our subcontractors and others.

TIAX accepts no duty of care or liability of any kind whatsoever to any third party, and no responsibility for damages or loss, if any, suffered by any third party, as a result of decisions made, or not made, or actions taken, or not taken, based on this document.

This report may be reproduced only in its entirety and only with the prior written consent of TIAX.

Copyrighted materials are the property of the respective owners.

4 II

Table of Contents

Introduction

3 Vehicle Market Segments3.1 On-road Vehicles3.2 Off-road Vehicles3.3 Available Natural Gas Engines3.4 Light- and Medium-Duty Vehicle Types3.5 Light- and Medium-Duty Population and

Fuel Use3.6 Heavy-Duty Vehicle Types3.7 Heavy-Duty Population and Fuel Use

Natural Gas Vehicle Market Statistics2.1 Current Natural Gas Vehicle Inventory2.2 End User Trends

Abbreviations

Lower Heating Value Energy Content Conversion Factors

Preface

Executive Summary

Chapter 1

Chapter 3

Chapter 4

Chapter 2

4 Characteristics of Vehicle Market Segments4.1 Overview4.2 Light-duty Passenger Cars and Trucks (Private)4.3 Light-Duty Passenger Cars and Trucks (Commercial/Government)4.4 Medium-Duty Private and Commercial Trucks4.5 Heavy-Duty: Package Delivery Cars4.6 Heavy-Duty: Utility Trucks4.7 Heavy-Duty: Vans, Stake/Flat Beds, and Others4.8 Heavy-Duty: School Buses 4.9 Heavy-Duty: Transit Buses4.10 Heavy-Duty: Refuse Trucks4.11 Heavy-Duty: Local and Regional Pickup and Delivery Trucks 4.12 Heavy-Duty: Line-Haul Trucks4.13 Off-road: Ground Support Vehicles4.14 Off-road: Construction Equipment4.15 Off-road: Mining Equipment4.16 Summary

5 Geographic Characteristics of Markets 5.1 Overview5.2 Infrastructure Availability5.3 Regional Policies, Incentives, and Mandates5.4 Fuel Cost Differentials5.5 Vehicle Concentrations5.6 Strategic Corridors

6 Recommendations

Chapter 5

Chapter 6

6III

CNG

DGE

DOE

DOT

EIA

EPA

FTA

GGE

GHG

GVWR

LNG

NAAQS

NGV

OEM

PTO

SVM

VIUS

Diesel

Gasoline

LNG

Natural gas

Compressed natural gas

Diesel gallon equivalent (=131.7 cubic feet of natural gas)

Department of Energy

Department of Transportation

Energy Information Administration

Environmental Protection Agency

Federal Transit Administration

Gasoline gallon equivalent (=115.6 cubic feet of natural gas)

Greenhouse gas

Gross vehicle weight rating

Liquefied natural gas (1 gallon LNG = 0.58 DGE)

National Ambient Air Quality Standards

Natural gas vehicle

Original equipment manufacturer

Power take-off

Small volume manufacturer

Vehicle Inventory and Use Survey

129,488 BTU/gal

113,602 BTU/gal

74,720 BTU/gal

983 Btu/cubic foot (=131.4 BTU/gal of volume)

Abbreviations

Lower Heating Value Energy Content Conversion Factors

Source: Argonne National Laboratory, “Greenhouse Gases, Regulated Emissions, and Energy Use in Transportation,” 1.8c

8IV

With the primary objective of identifying the most productive and effective means to increase the use of natural gas vehicles (NGVs) in the U.S. and Canada, the TIAX team has conducted a thorough and independent assessment of the NGV market. To identify the major market development and expansion opportunities, this assessment examines key technical, economic, regulatory, social, and political drivers and challenges that shape this market. TIAX has partnered with The CARLAB, Clean Fuels Consulting, the Clean Vehicle Education Foundation, Jack Faucett Associates, the Natural Gas Vehicle Institute, and St. Croix Research to provide perspective and insights into the development of the future NGV market.

• Segmentation of the vehicle market

• Identification of market decision drivers

• Assessment of market development actions

• Analysis of competing technologies

• Analysis of market scenarios

• Integration of overall market development opportunities

The market perspectives for which decision drivers and opportunities have been identified and assessed are: light- and medium-duty vehicle ownership and production; heavy-duty vehicle ownership and production; compressed natural gas infrastructure; liquefied natural gas infrastructure; and government.

Drawing on the respective expertise of each team member, TIAX presents an integrated assessment of the U.S. and Canadian NGV market in a collection of eight reports. Each report is capable of standing alone while integrating the data, ideas, and themes of the other seven reports. The collection of reports in this TIAX analysis of the NGV market is supported by America’s Natural Gas Alliance and is intended to be transparent and accessible to a broad audience.

Identifying the most productive and effective means to increase the use of natural gas vehicles

TIAX’s overall approach relies on six key stages

Preface

10V

Executive Summary

While market segments are unique and complex, several common factors affect the use of natural gas as a vehicle fuel

Over 100,000 natural gas vehicles (NGVs) are currently in use on the roads of the U.S. and Canada. These on-road NGVs displace more than 225 million gallons of gasoline and diesel fuel in applications ranging from buses to passenger cars. In addition to these on-road vehicles, there are tens of thousands of natural gas forklifts and other off-road equipment in use. The market segments in which natural gas has achieved the greatest penetration are high fuel use applications with significant mandates and/or incentives for the use of alternative fuels.

The North American vehicle fleet is very diverse, composed of relatively standardized vehicles such as pickup trucks and passenger cars, as well as highly specialized vehicles such as street sweepers and vacuum trucks (Figure ES-1). However, these vehicles can be grouped into several broad groups. Within the on-road market, the light- and medium-duty vehicle

market segments are predominately composed of mass-produced vehicles in a few common configurations. These familiar configurations include passenger cars, trucks, SUVs, vans, and work trucks. Owing to their versatility, light- and medium-duty vehicles are present in nearly every fleet. Heavy-duty, on-road vehicles are built for specific applications and are generally built to order for each customer. Light-duty cars and trucks are the most numerous vehicles but use the least fuel per vehicle, whereas heavy-duty vehicles consume the most fuel per vehicle, making their total cost of ownership very sensitive to fuel price. Off-road fleets are predominantly construction equipment or low-speed vehicles, highly specialized to particular applications.

While market segments are unique and complex, several common factors affect the use of natural gas as a vehicle fuel. Ultimately, vehicle applications subject to the greatest economic and environmental pressures are the same applications that have seen the greatest use of natural gas. In particular, mandates and incentives created to reduce regulated motor vehicle emissions have historically driven NGV deployment. Due to increasingly stringent emissions standards for motor vehicles that can be met with conventional fuels as well as natural gas, air pollutant emissions are becoming diminished drivers for use of alternative fuels in vehicle applications. Instead, greenhouse gas emissions and a reduction in transportation fuels from geopolitically unstable regions of the world are likely to be key policy and deployment drivers for NGVs in North America.

Finally, the development of future natural gas infrastructure will be affected by a combination of factors. Prospective anchor fleets that are motivated to adopt natural gas must be matched with infrastructure development. Growth of transportation markets along strategic corridors and their geographic proximity to natural gas resources have the potential to expand natural gas infrastructure significantly.

VI

Figure ES-1

North America’s vehicle market is complex. This report examines the various vehicle market segments and their ability to use to natural gas as a fuel.

7

4

3

6

5

2

1

0

1970 1975 1980 1985 1990 1995 201020052000

U.S. Petroleum Supplies

Year

Petroleum Supplies(trillion barrels)

29%

09%

62%

Annual Growth 0.96%

Imports

U.S. Offshore

U.S. Domestic

Light Duty

0-6,000

Type

Bus

es

Shuttle

Intercity

School

Trans

Short Haul

Port

Long Haul

Regional

Van

Tow

Moving

Divided

Beverage

Refuse

Dump

Cement

Sem

i-Tra

cto

rsTr

ucks

Application Example Pass Car Class 1 Class 2 Class 3 Class 4 Class 5 Class 6 Class 7 Class 8 Major Fuels in Use

6,001-10,000

10,001-14,000

14,001-18,000

18,001-18,600

18,601-28,000

28,001-33,000

33,001ormore

Medium Duty

Gross Vehicle Weight: Rating (GVWR)in bs.

Heavy Duty

Vehicle Type/Application

Range BaseFueling

InfrastructureVehicle

AvailabilityFuel Cost Sensitivity

EnvironmentalPolicies

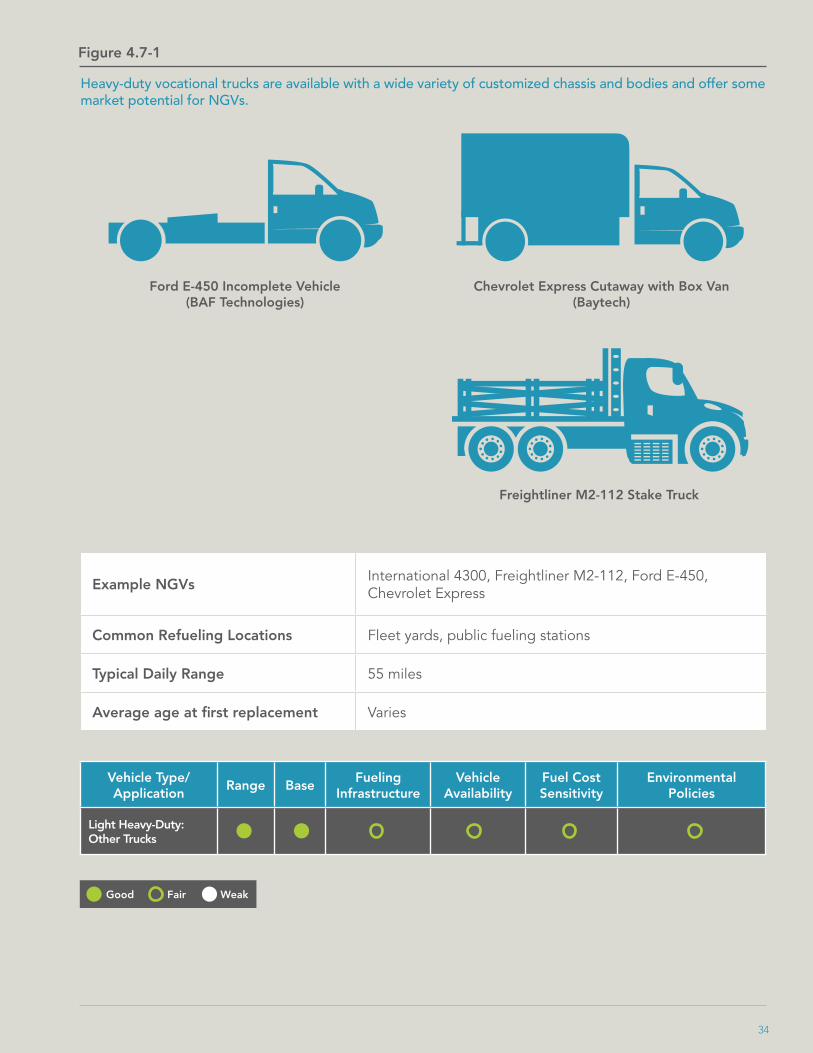

Light Heavy-Duty: Package Delivery Vans

12VII

1 Introduction

Over 100,000 natural gas vehicles (NGVs) are currently in use on the roads of the U.S. and Canada (Figure 1-1). These on-road NGVs displace more than 225 million gallons of gasoline and diesel fuel in applications ranging from buses to passenger cars. In addition, there are tens of thousands of natural gas forklifts and other off-road equipment in use. Delving further into the specific uses of NGVs, this report segments the market by vehicle type (e.g., passenger car), by end user application (e.g., public transit), and by geo-economic parameters (e.g., connected urban centers, goods movement corridors, and areas with similar policies). Each of these factors greatly impacts which markets and regions are most likely to adopt NGVs and helps define the potential degree of their market penetration.

Each vehicle market segment and application has its own unique characteristics in terms of vehicles employed, minimum performance requirements, drive cycle, and capital and operational costs. As a result, purchasing decisions tend to be made on case-by-case basis by individuals or fleets to meet user-specific requirements. General trends can be made within a vehicle class or within an application using generalized or average costs, annual mileage, vehicle service life, fueling prices, duty cycle, and refueling logistics. These trends can help identify potential opportunities for the growth of NGVs in particular markets, but they will not apply to every vehicle or fleet within that market. Geography will also impact these purchase decisions in terms of regional regulations, incentives, fueling infrastructure, fuel pricing structure, and public perception.

The overarching goal of this market segmentation report is to characterize how vehicles are used in North America—accounting for regional similarities and differences—to identify the challenges and opportunities that must be addressed for expansion of the NGV industry. This report begins by highlighting the current estimates of NGV penetration into the broad vehicle market and summarizing end user trends in Section 2. Next, Section 3 provides an overview of how the transportation sector is currently segmented in terms of vehicle types, applications, and fuel use. Following this overview, several market segments are reviewed in Section 4 based on key factors that impact the adoption of natural gas as a vehicle fuel. In Section 5, these discussions are followed by a look at the geographical segmentation of the market in terms of regional differences in policies and fuel prices that help explain the distribution of NGVs and natural gas infrastructure across the country. Section 5 also examines the major corridors for transportation and identifies areas where natural gas infrastructure may be targeted. Major recommendations are summarized in Section 6 for actions that will support the adoption of NGVs across all the potential market segments. Together, these sections identify and characterize specific sectors and applications with significant potential for expanded NGV use.

This market segmentation report provides an overview of the various vehicles and segments that compose the vehicle market, with a focus on natural gas vehicles in the various market segments.

1

Figure 1-1

These are a few examples of the thousands of NGVs in use in many different applications throughout North America.

...and many other applications: Passenger cars, semi-trucks, cargo vans, fork lifts

Segment Statistics

Segment Statistics

Segment Statistics

Total Vehicles 67,000

Natural Gas Vehicles 10,000

Petroleum Fuel Use (DGE) 670,000,000

Natural Gas Fuel Use (DGE) 150,000,000

Typical Daily Range (Miles) 90 to 130

Total Vehicles 140,000

Natural Gas Vehicles 1,400

Petroleum Fuel Use (DGE) 1,200,000,000

Natural Gas Fuel Use (DGE) 13,500,000

Typical Daily Range (Miles) 85

Total Vehicles 500,000

Natural Gas Vehicles 1,800

Petroleum Fuel Use (DGE) 570,000,000

Natural Gas Fuel Use (DGE) 2,300,000

Typical Daily Range (Miles) 30

Transit Buses

Refuse Trucks

School Buses

2

2 Natural Gas Vehicle Market Statistics

Over the last twenty years, NGVs have been deployed into a wide range of on-road and off-road applications, ranging from transit buses to forklifts. While some market segments have seen little to no penetration of natural gas, other sectors have shown strong acceptance of natural gas as a vehicle fuel. Assessing the levels of market penetration in each sector is challenging, as there are no comprehensive tracking or reporting systems for NGV sales or operation in North America. In the heavy-duty sector, this lack of tracking is partially attributable to the number of parties involved in the production of a heavy-duty vehicles, including engine manufacturers, vehicle manufacturers, vehicle modifiers, and alternative fuel vehicle converters. In the light-duty sector, alternative fuel vehicle converters contribute significantly to the total NGV population, thereby preventing accurate counts from being obtainable solely from vehicle manufacturers. As a result, this market segmentation report compiles data from multiple data sources to quantify and characterize current North American use of NGVs by vehicle type.

Table 2.1-1 presents the estimated NGV segment populations, fuel use, and market penetration for various vehicle types. High fuel use applications in dense urban settings, such as transit buses and refuse trucks, are the largest consumers of natural gas as a transportation fuel. However, the greatest numbers

of NGV deployments have been in the light-duty segment. Note that information for NGV deployments in Canada is not included in Table 2.1-1 due to a lack of available corresponding data within several market segments. However, according to Statistics Canada, the Canadian transportation sector is about 8 percent of the U.S. transportation sector by vehicle population.1 The Canadian government estimates that there are just over 12,000 NGVs in Canada: approximately 300 heavy-duty vehicles, 150 transit buses, 45 school buses, 9,450 light-duty vehicles, and 2,400 forklifts and ice-resurfacers. It is assumed that, while smaller, the Canadian vehicle market has similar drivers to the U.S. market and that the Canadian market would respond in predominately the same manner given the same set of conditions. However, Canada has unique characteristics that may ultimately influence the NGV market differently, including a much lower population that is geographically spread out, colder winter climates than the U.S., and higher fuel taxes than the U.S.

NGVs are also in use in some off-road applications. For example, the U.S. Environmental Protection Agency (EPA) NONROAD 2008 model and California Air Resources Board’s OFFROAD model suggest that a significant number of natural gas forklifts operate in the U.S. Based on the EPA NONROAD model, it is estimated that there are approximately 59,000 compressed natural gas (CNG) forklifts in the U.S., consuming 2,000 diesel gallons equivalent (DGE)2 of CNG per vehicle each year. This equates to an 8.5 percent market penetration by vehicle count and 6.1 percent penetration by fuel use. In contrast, liquefied petroleum gas (also called propane) is the leading fuel for forklifts, with an estimated 75 percent market share. In addition to forklifts, the NONROAD model reports small numbers (100 units or fewer) of natural gas sweepers/scrubbers and terminal tractors. By number of vehicles, this population is relatively small, but their collective estimated annual natural gas consumption is significant at approximately 5,000 DGE per year.

The heavy-duty market consumes the vast majority of natural gas as a transportation fuel, while the light-duty market has deployed the greatest number of natural gas fuel systems.

2.1 Current Natural Gas Vehicle Inventory

1 Statistics Canada. “Canadian Vehicle Survey: Annual.” 2009.2 One DGE is equal to the amount of energy in one gallon of diesel fuel.

3

Table 2.1-2

Natural gas vehicles have achieved the greatest market penetration in high-fuel-use applications like transit buses.

Vehicle Type Low High Low High Low High Low High

Transit bus 8,500b 12,320e 13% 18% 149,200e 151,365g 22% 23%

Refuse truck 1,300c 1,500c 1.4% 1.6% 12,856c 14,833c 1.4% 1.6%

School bus 1,360d 2,300b 0.3% 0.5% 1,696d,g 2,827d,g 0.3% 0.5%

Other heavy-duty truck 9,818a 14,778a 0.2% 0.3% 161,833a 161,838a 0.4% 0.4%

Total 20,978 30,898 0.2% 0.3% 325,585 330,863 0.7% 0.7%

Vehicle Type Low High Low High Low High Low High

Medium-duty truck4 10,000b 22,309a 0.03% 0.08% 17,623a 0.15%

Light truck 39,381a 71,500f 0.04% 0.07% 16,358a 0.02%

Passenger car 29,759a 0.02% 6,455a 0.01%

Total 79,140 123,568 0.03% 0.05% 40,436 0.03%

U.S NGV Population U.S Market Penetration(by vehicle count)

U.S Annual NGV Fuel Use (thousand DGE)

U.S. Market Penetration(by fuel use)

U.S NGV Population U.S Market Penetration(by vehicle count)

U.S Annual NGV Fuel Use (thousand GGE)3

U.S. Market Penetration(by fuel use)

On-Road Heavy-Duty Applications (>14,000 lbs GVWR)

On-Road Light- and Medium-Duty Applications (≤14,000 lbs GVWR)

Light-duty passenger car: includes cars from sub-compact to large station wagons, does not include minivans, SUVs, or pickups

Light-duty truck/van: includes Class 1 and Class 2a trucks, vans, minivans, pickups, SUVs

Medium-duty truck: includes Class 2b to Class 3 trucks and vans

Heavy-duty transit bus: bus with front and center doors and low-back seating for use in frequent-stop service

Heavy-duty refuse hauler: waste collection vehicle or garbage truck that collects trash from homes and businesses for transport to processing facility

Heavy-duty school bus: bus used for the purpose of transporting students between home and school, typically Class 6 or Class 7 vehicles

Other heavy-duty truck: Class 4 to 8 trucks, both tractor-trailers and straight trucks, does not include buses or refuse trucks

a) U.S. Energy Information Administration, “Alternatives to Traditional Transportation Fuels 2009,” April 2011b) Yborra, S. “Growth of the NGV Market: Lessons Learned Roadmap for Infrastructure Development,” 2008c) Cannon, J., “Greening Garbage Trucks: Trends in Alternative Fuel Use,” 2006d) Monahan, P., “School Bus Pollution Report Card 2006,” 2006e) American Public Transportation Association, “2012 Public Transportation Fact Book,” March 2012f) U.S. Census Bureau, “Vehicle in Use Survey,” 2002 g) U.S. DOE Energy Efficiency and Renewable Energy, Transportation Energy Data Book, Edition 31, 2012

4

3 One gasoline gallon equivalent (GGE) is equal to the amount of energy in one gallon of gasoline.4 Medium-duty truck data from EIA “Alternatives to Traditional Transportation Fuels” report was segregated based on the assumption that medium-duty pickups are

primarily Class 2a and Class 3. Other medium-duty trucks and vans are assumed to be Class 4 to Class 6. Assumption based on discussions with EIA staff.

2 Natural Gas Vehicle Market Statistics

From 2005 to 2008, the estimated number of NGVs in service has decreased slightly, while natural gas fuel consumption has increased.5 Figure 2.2-1 shows historical data from the Energy Information Administration (EIA) for various end user groups. Based on the EIA data, it appears that increases in the size of NGV fleets for private/municipal fleets and transit agencies have been offset by decreases in other fleets. This has resulted in slight decreases, approximately 3 percent, in the total estimated population of NGVs. In contrast, natural gas fuel use has increased by an estimated 14 percent over the same time period. These trends suggest that the majority of NGVs exiting the active fleet are vehicles with low annual fuel consumption, while new NGVs entering the U.S. fleet are higher fuel consumption vehicles such as transit buses. Further discussion follows about NGV usage trends in specific end user applications, as shown in Figure 2.2-1.

Transit Agencies - As the market with the highest penetration of NGVs and highest use of natural gas, transit agencies have maintained or slightly expanded their NGV inventories. Natural gas fuel consumption has increased in this market segment, offsetting decreases in other market segments.

State Agencies - Some decrease in the number of NGVs has corresponded with an increase in fuel consumption. Since 2006, fuel consumption appears to have remained steady.

Federal Agencies - A marked decrease in fuel consumption for federally operated NGVs has corresponded with only modest decreases in the number of NGVs in the federal fleet. This trend is counter to other end user groups, suggesting that high fuel use NGVs are being retired without replacement and/or there is an overall decrease in the use of NGVs in the federal fleet.

Alternative Fuel Providers - This end user group, which includes natural gas providers as well as propane and electricity providers, has shown relatively little change in fuel use, with modest decreases in NGV fleet size.

Private/Municipal - Collectively, private consumers, commercial entities, and local level governments own the largest number of NGVs in the U.S., commonly light-duty trucks and passenger cars. Both the fuel use and number of NGVs in this end user group have increased modestly.

Natural gas fuel consumption has trended higher between 2005 and 2008, while the number of NGVs has decreased slightly.

2.2 End User trends

5 U.S. EIA. “Alternatives to Traditional Transportation Fuels.” Note that there were significant changes in reporting methodologies in 2005. Data prior to 2005 are not shown due to these differences.

5

Figure 2.2-1

Natural gas fuel consumption has increased recently while the natural gas vehicle population has declined slightly.

0

0

125,000

175,000

225,000

100,000

100,000

200,000

75,000

75,000

150,000

50,000

25,000

25,000

50,000

125,000

2005

2005

20092008

20092008

2006

2006

2007

2007

Total Natural Gas Vehicles

Total Natural Gas Fuel Use

Private/Municipals

Private/Municipals

State Agencies

State Agencies

Alt Fuel Providers

Alt Fuel Providers

Federal Agencies

Federal Agencies

Transit Agencies

Transit Agencies

6

(thousand GGE)

Based on EIA data available at: http://www.eia.gov/renewable/afv/archive/index.cfm

Based on EIA data available at: http://www.eia.gov/renewable/afv/archive/index.cfm

3 Vehicle Market Segments

The North American on-road vehicle fleet is very diverse, composed of relatively standardized vehicles such as pickup trucks and passenger cars as well as highly specialized vehicles such as street sweepers and tow trucks. However, these vehicles can be grouped using common physical characteristics and usage criteria, including vehicle type, weight capacity, and duty rating.

On-road vehicles are designed to travel on public streets and motorways and must meet a variety of safety requirements to be so operated. In addition, each type of on-road vehicle is assigned a weight class that represents the maximum weight that it can safely support, including cargo and passengers. This weight rating is known as the gross vehicle weight rating (GVWR). In the U.S., Department of Transportation (DOT) designations are used and are defined as follows:

• Passenger Car/Light Truck

• Class 1: ≤6,000 pounds (light-duty)

• Class 2a: 6,001 to 8,500 pounds (light-duty)

• Class 2b: 8,501 to 10,000 pounds (medium-duty)

• Class 3: 10,001 to 14,000 pounds (medium-duty)

• Class 4: 14,001 to 16,000 pounds (heavy-duty)

• Class 5: 16,001 to 19,500 pounds (heavy-duty)

• Class 6: 19,501 to 26,000 pounds (heavy-duty)

• Class 7: 26,001 to 33,000 pounds (heavy-duty)

• Class 8: ≥33,001 pounds (heavy-duty)

It is not uncommon for a single vehicle to have different weight class designations depending on the equipment installed on the vehicle. For example, the 2012 Ford F-350 pickup truck may be a Class 3 or Class 4 vehicle depending on drive train and rear axle type.6

Vehicles are also commonly grouped by weight categories: light-duty, medium-duty, and heavy-duty. The precise definition of these categories varies significantly. For the purposes of this report, light-duty is considered to include passenger cars through Class 2a vehicles. Medium-duty includes Class 2b through Class 3 vehicles, and heavy-duty includes Class 4 through Class 8 vehicles. These groupings are consistent with those used for emissions certifications and represent a reasonable separation between trucks that are mass produced (light- and medium-duty) and those that are highly customized (heavy-duty). Figure 3.1-1 provides an overview of these grouping for several common vehicle types.

While there is some overlap in the light- and medium-duty truck markets, gasoline is the dominant fuel for light-duty vehicles. Diesel is the dominant fuel in medium-duty and heavy-duty applications, primarily due to the higher fuel efficiency and torque of compression ignition engines. In applications with relatively low fuel consumption, gasoline may compete with diesel for market share.

On-road vehicle markets are complex and include dozens of vehicle applications. Vehicle manufacturers take very different approaches to producing vehicles, depending on the type of vehicle being sold.

3.1 On-road Vehicles

6 Ford. “Super Duty Specifications.” http://www.ford.com/trucks/superduty/specifications/chassis. Accessed August 2012.

7

Figure 3.1-1

The on-road vehicle market is complex and segmented by various vehicle characteristics including weight class, vehicle type, and size.

Light Duty

0-6,000

Type

Bus

es

Shuttle

Intercity

School

Transit

Short Haul

Port

Long Haul

Regional

Van

Tow

Moving

Stake/ Flat Bed

Beverage

Refuse

Dump

Cement

Car Hauler

Utility Truck

Reefer

Tank

Van

Utility Van

Pickup

Cargo Van

Sub-compact

Compact

Med Sedan

Lg Sedan

Mini-Van

SUV

PassengerVan

Gasoline Diesel Natural Gas Propane

LightPickup

Steet Sweeper

Sem

i-Tra

cto

rsM

ediu

m a

nd H

eavy

Dut

y V

oca

tio

nal T

ruck

sLi

ght

and

Med

Dut

y V

oca

tio

nal

Truc

ks

Pas

seng

er C

ars

and

Lig

ht T

ruck

s

Application Example Pass Car Class 1 Class 2 Class 3 Class 4 Class 5 Class 6 Class 7 Class 8 Major Fuels in Use

6,001-10,000

10,001-14,000

14,001-16,000

16,001-19,500

19,501-26,000

26,001-33,000

33,001ormore

Medium Duty

Gross Vehicle Weight: Rating (GVWR) in lbs.

Heavy Duty

8

3 Vehicle Market Segments

Off-road vehicles are vehicles that cannot legally operate on public roads but may share many characteristics with on-road vehicles, including windows, tires, and self-propulsion. Off-road vehicles include construction and mining equipment such as bulldozers, graders, and dump trucks, as well as ground support vehicles, such as terminal tractors at ports and baggage handling equipment at airports. Because these vehicles do not travel on public roads, they are not classified by their vehicle weight rating like on-road vehicles, although they are often marketed based on weight capacity. Instead, they are grouped by vehicle type and the power rating of their engines. Figure 3.2-1 provides an overview of several common types of off-road equipment, grouped by the horsepower categories used for emissions inventories by the EPA. Note that while there may be examples of equipment outside the indicated horsepower ranges, the intent is to show common horsepower ranges by application.

Construction and mining equipment include engines that range in size from less than 50 horsepower to more than 4,000 horsepower. It is common practice to build essentially the same type of vehicle in a very large range of sizes and power ratings. For example, Caterpillar offers track-type tractors in engine power ranges from 96 horsepower to 850 horsepower.7 Construction and mining equipment tend to be very heavy and used to move large loads, necessitating the use of high torque engines. In addition, reliability and durability are major concerns given the severe service operations required of construction and mining vehicles. As a result, compression ignition engines are preferred in these applications, leading to the near exclusive use of diesel fuel in these market segments. The predominant difference between mining and construction equipment is that mining equipment tends to be larger than construction equipment, due to a focus on maximizing the throughput of material in mining applications.

Ground support vehicles are also off-road vehicles. Although some of these vehicles (e.g., terminal tractors) can look very similar to on-road vehicles, they are not permitted to operate on public roads. Ground support vehicles are generally dedicated to serving the operations of a single facility, such as a port terminal or warehouse. In essence, this circumstance creates captured fleets. Most ground support vehicles are equipped with engines less than 300 horsepower in size. Smaller vehicles like indoor forklifts commonly use spark-ignited engines fueled by gasoline, natural gas, or propane. For applications above 100 horsepower, compression-ignition engines fueled by diesel are the dominant power source.8 A good example of larger diesel-fueled ground support vehicles are terminal tractors, which typically move very heavy loads for short distances and are used commonly throughout North American seaport terminals.

Off-road fleets are predominantly construction equipment or low-speed vehicles, highly specialized to particular applications.

3.2 Off-road Vehicles

7 CAT. “Track-Type Tractors.” http://www.cat.com/equipment/track-type-tractors. Accessed August 2012.8 U.S. EPA 2008 NONROAD model.

9

Figure 3.2-1

Off-road vehicles and equipment are generally classified by engine size, which varies widely, and diesel is the dominant fuel.

>25 25-50 51-75 76-100 101-175 176-300 301-600 601-750 751+

Dump Truck

Bull Dozer

Grader

Earth Mover

Yard Truck

Self Loader

Baggage

Belt Loaders

Fork Lift

Off

-Hig

hway

Engine Horsepower

Major Fuels in Use

Gasoline Diesel Natural Gas Propane

Typical mining and construction equipment

Motor Grader

Backhoe Loader

Mining Truck

Wheel Loader

Typical ground support equipment

Indoor Forklift Tow Tractor Yard Hostler

10

3 Vehicle Market Segments

The broad range of vehicle types and applications offered in the North American market requires a diversity of engine types and sizes. Two types of OEMs are the key players in the process to mass produce conventional on-road vehicles: vehicle OEMs and engine OEMs. One process is for vehicle OEMs to produce and install their own engine into their own vehicle chassis (i.e., they are also engine OEMs), as is commonly done for manufacturing of light-duty passenger cars and trucks. A second process is for vehicle OEMs to purchase engines from engine OEMs and integrate them into their own vehicle chassis, as is common in the heavy-duty and off-road markets. Alternative fuel vehicles including NGVs tend to be manufactured through a variation of this process that involves additional players and step, due to the need for specialized on-board fuel storage systems made by other OEM types, who must coordinate closely with vehicle and engine OEMs, as well as third parties that specialize in vehicle aftermarket conversions.

Currently, the NGV market is served by a limited number of engine OEMs that typically offer a single natural gas engine model. In some cases, these engines are installed into vehicles on the factory line as is done with traditional diesel and gasoline engines.

The benefits of OEM installations of natural gas engines are significant, including the ability to mass produce NGVs with highly integrated vehicle/engine/fuel systems. This can increase vehicle reliability, efficiency, and cost savings compared to aftermarket conversions and provide customers with a single point of purchase and full vehicle warranty.

Where OEM products are not available, the natural gas vehicle market is served by SVMs and aftermarket converters. SVMs are companies that develop and certify natural gas conversions of existing diesel and gasoline engines. These companies are required to certify their conversions annually to the same emissions standards as OEMs. The costs and complexities of this annual recertification are a leading factor in limiting the number of natural gas conversions available on the market. While the SVMs provide natural gas-compatible engines, aftermarket converters are needed to make additional modifications to the vehicles before they can operate on natural gas. These modifications include fuel tank installations, engine installations or modifications per SVM requirements, and fuel line routing. Together, OEMs, SVMs, and aftermarket converters provide natural gas engine options for on-road vehicles from passenger cars to Class 8 semi-tractors.

Historically, natural gas engine OEMs and SVMs have focused on the on-road market and offered few NGV options for off-road vehicle end users. However, in some regions and market segments, off-road vehicle OEMs are beginning to use on-road engines to comply with various emissions regulations. This makes it more feasible to substitute on-road natural gas engines for diesel engines in both on- and off-road applications. This trend could help to significantly increase deployments of NGVs in the off-road vehicle segment. Table 3.3-1 shows available light-, medium-, and heavy-duty natural gas engines for North American markets and their representative end use applications. As shown, even though natural gas engine offerings are limited, their use covers a broad range of applications from passenger cars to eighteen-wheelers.

Natural gas engines are available for most vehicle applications through a combination of original equipment manufacturers (OEMs), small volume manufacturers (SVMs), and aftermarket converters.

3.3 Available Natural Gas Engines

11

Figure 3.3-1

Natural gas engines are available for most vehicle applications.9

9 Data based on information provided by NGVAmerica, “Guide to Available Natural Gas Vehicles and Engines,” May 14, 2011.

12

Class Supplier Engine Light

-dut

y Pas

seng

er C

ars

Shut

tle B

uses

Taxis

Other

Med

ium-D

uty

Truc

ks

Light

-Dut

y Tr

ucks

Tran

sit B

uses

Shor

t-Hau

l Tru

cks

Packa

ge Deli

very

Veh

icles

Scho

ol B

uses

Long

-Hau

l Tru

cks

Utility

Truc

ks

Draya

ge Tr

ucks

Refus

e Hau

lers

Other

Hea

vy-

Duty

Truc

ks

LD OEM+SVM Honda 1.8L

LD/MD OEM+SVM Ford 4.6L

LD/MD OEM+SVM GM 6.0L

LD/MD SVM Chrysler 4.7L

LD/MD SVM GM 6.2L

LD/MD SVM Ford 6.2L

LD/MD SVM Ford 6.8L

LD SVM Ford 2.0L

LD SVM Ford 2.3L

LD SVM Ford 2.5L

LD/MD SVM Ford 4.6L

LD/MD SVM Ford 5.4L

LD SVM GM 3.5L

LD SVM GM 3.9L

LD/MD SVM GM 4.8L

LD/MD SVM GM 5.3L

LD/MD SVM GM 6.0L

MD/HD Converter BAF Technologies6.8L V-10

MD/HD Converter IMPCO Technologies 4.8L HD

MD/HD Converter IMPCO Technolo-

gies 6.0L HD

MD/HD ConverterLandi Renzo

USA/Baytech 4.8L HD

MD/HD ConverterLandi Renzo

USA/Baytech 6.0L HD

MD/HD Converter Landi Renzo

USA/Baytech 8.1L HD

HD Converter

Emission Solutions Inc./International Truck

7.6L NGPhoenix

HD OEM Cummins Westport 8.9L ISL G

HD OEM Doosan InfracoreAmerica 11L GK12

HD OEM Westport Innovations15L GX

3 Vehicle Market Segments

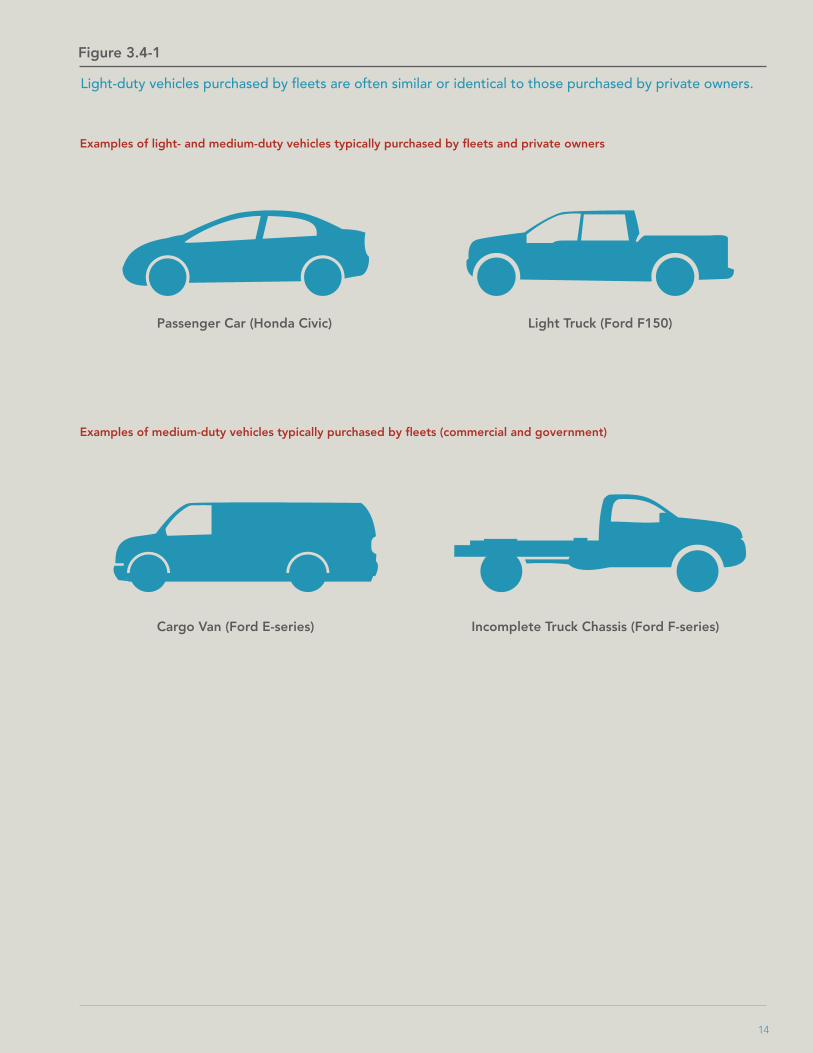

The light- and medium-duty vehicle market segments include passenger cars, pickup trucks, light work trucks, and cargo vans (Figure 3.4-1). Owing to their versatility, these vehicles are present in most fleets and are used for transportation or job functions that do not require specialized vehicle chassis. Due to their popularity, manufacturers are able to mass produce these vehicles with relatively few body/chassis/engine combinations. A consequence of this market structure is that individual fleets must often turn to third parties to integrate alternative fuel technologies into vehicles if the manufacturer does not provide them as standard options.

The U.S. passenger car and light truck market consists of approximately 230 million vehicles that are predominantly in the hands of private citizens and used for personal transportation. Only about 4 percent of passenger cars are in fleets of five or more vehicles.10 Light-duty vehicles are typically sold to private

customers through dealerships with few modifications and relatively short lead times.11 Because such a large majority of light-duty vehicles are purchased by private owners, offerings in this market segment are primarily dictated by consumer preferences. Purchase price and styling are significant market drivers, whereas fuel economy has only recently been significant when gasoline prices were near $4.00 per gallon. The relative priority of these market drivers reflects the relatively low fuel consumption per vehicle in the passenger car and light truck market. Incremental vehicle capital costs associated with major fuel economy improvements (e.g., hybridization) or the ability to operate on alternative fuels typically have very long payback periods when gasoline prices are low.

Like light-duty vehicles, medium-duty vehicles are also mass produced, but the vehicle body may be removed, added, or altered, and additional equipment may be added by the dealer or a third party vehicle modifier. Unlike the light-duty market, the majority of medium-duty vehicles are purchased for commercial use. Key market drivers in this segment are vehicle capability, reliability, and total cost of ownership. These factors have led to a significant use of compression-ignition engines and diesel fuel in the medium-duty market, although in low fuel use applications, the higher purchase price of a diesel-fueled vehicle may not be justified, and buyers may opt for gasoline vehicles. Additionally, for some users where fuel costs are a marginal decision driver, the increased purchase costs for diesel engines that comply with 2010 emissions standards are driving a shift toward spark-ignited (gasoline) engines. The standard practice of modifying medium-duty vehicles and working with multiple suppliers to complete a vehicle purchase provides an opportunity to integrate natural gas engines and fuel systems without significantly altering the typical medium-duty vehicle purchase process.

The light- and medium-duty vehicle markets are predominately composed of mass-produced vehicles in a few common configurations. Nearly every fleet utilizes light- and medium-duty vehicles to some degree.

3.4 Light- and Medium-Duty Vehicle Types

10 Automotive Fleet. “Fact Book.” www.fleet-central.com. 2012.11 See the Light- and Medium-Duty Vehicle Ownership and Production report of the overall TIAX assessment.

13

Figure 3.4-1

Light-duty vehicles purchased by fleets are often similar or identical to those purchased by private owners.

Examples of light- and medium-duty vehicles typically purchased by fleets and private owners

Examples of medium-duty vehicles typically purchased by fleets (commercial and government)

Passenger Car (Honda Civic)

Cargo Van (Ford E-series)

Light Truck (Ford F150)

Incomplete Truck Chassis (Ford F-series)

14

3 Vehicle Market Segments

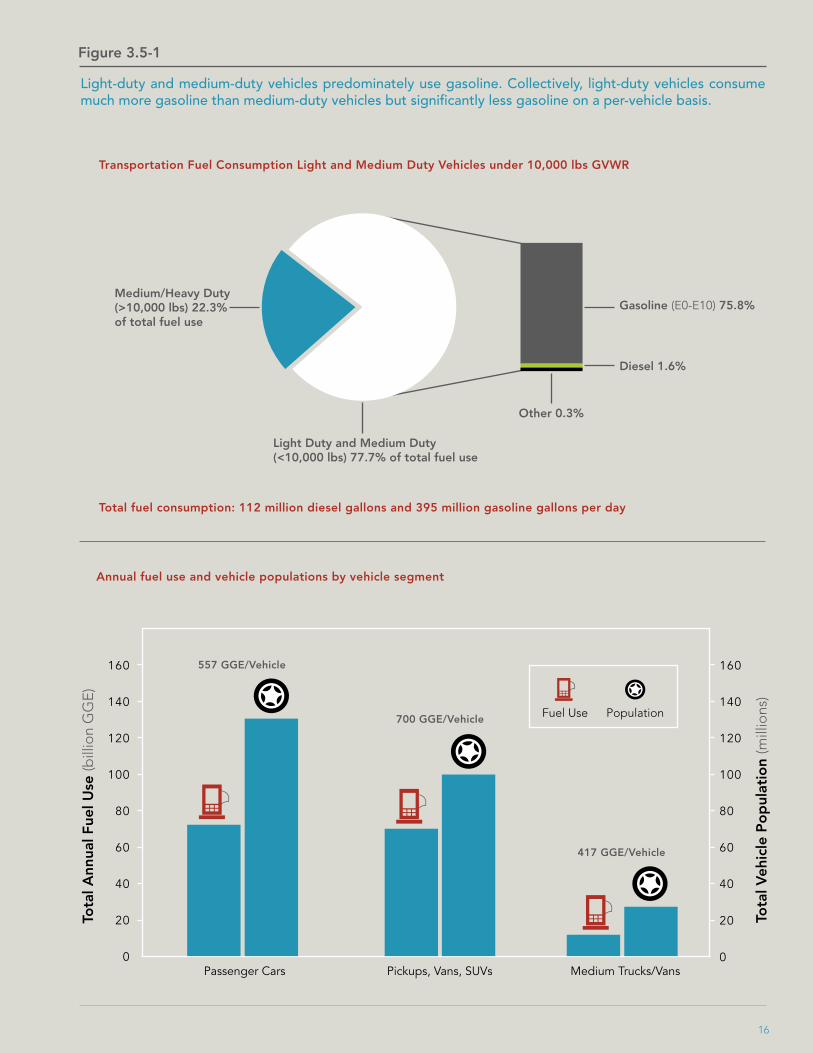

the light-duty market. Based on fuel use and vehicle population data,13 it is estimated that passenger cars consume approximately 557 GGE of fuel per vehicle annually, and light-duty trucks consume 700 GGE per vehicle annually. The higher fuel consumption in the light-duty truck segment is a combination of two factors: lower fuel economy compared to passenger cars and higher fraction of ownership by commercial owners as opposed to private owners.

As shown in Figure 3.5-1, light-duty vehicles in North America are predominately gasoline fueled. This is largely a result of the lower acquisition cost of gasoline vehicles compared to diesel vehicles, but other factors also come into play (e.g., emissions standards). In the light-duty segment, purchase price rather than fuel costs tends to be a much larger component of total ownership costs, due to low annual fuel consumption. Thus, even though diesel passenger cars generally offer significant fuel efficiency benefits compared to comparable gasoline vehicles, they currently constitute a very small part of the passenger car market, and this trend is unlikely to change in the near future. In contrast, for the medium-duty market, the predominant fuel has been diesel because of the importance of fuel costs in total ownership costs. However, gasoline has recently gained market share in the medium-duty market due to recent increases in the purchase, operation, and maintenance costs of new diesel engines. These increased costs are primarily attributable to the addition of costly and complex systems to meet stricter emissions regulations for diesel engines and are unlikely to change dramatically over the next few years. Because these increased costs affect not only the acquisition cost of the vehicle but also the operating and maintenance costs, medium-duty vehicle purchasers are more frequently adopting spark-ignited (gasoline) engines. The willingness of medium-duty vehicle purchasers to select spark-ignited engines opens the door to natural gas in this market segment because vehicle performance and reliability will be similar to gasoline engines while potentially providing significant fuel cost savings over gasoline or diesel.

Light-duty vehicles are the most numerous of all the market segments, accounting for 85 percent of the total on-road fleet by vehicle count.12 These vehicles also use the least fuel on a per-vehicle basis. Together, light-duty and light medium-duty vehicles consume about three-quarters of total U.S. vehicle fuel but at a lower per-vehicle fuel consumption rate than the heavy-duty market. Light- and medium-duty vehicles are predominately fueled with gasoline, although heavier (Class 2b and Class 3) medium-duty vehicles commonly use diesel.

Light-duty vehicles, by population, are predominately privately owned and used for personal transportation. Whether used for travel to work or other domestic needs, most privately owned vehicles are used for a small portion of the day. In contrast, commercial owners average twice the annual mileage of private users in

Light-duty cars and trucks are the most numerous vehicles and as a market segment consume the most fuel but use the least fuel per vehicle.

3.5 Light- and Medium-Duty Population and Fuel Use

12 U.S. DOE Energy Efficiency and Renewable Energy. “Transportation Energy Data Book.” Edition 31. 2012. Includes passenger cars and light trucks through Class 2a. 13 Ibid.

15

Figure 3.5-1

Light-duty and medium-duty vehicles predominately use gasoline. Collectively, light-duty vehicles consume much more gasoline than medium-duty vehicles but significantly less gasoline on a per-vehicle basis.

Transportation Fuel Consumption Light and Medium Duty Vehicles under 10,000 lbs GVWR

Total fuel consumption: 112 million diesel gallons and 395 million gasoline gallons per day

Tota

l Ann

ual F

uel U

se (b

illio

n G

GE

)

Tota

l Veh

icle

Po

pul

atio

n (m

illio

ns)

Annual fuel use and vehicle populations by vehicle segment

Medium/Heavy Duty (>10,000 lbs) 22.3% of total fuel use

Light Duty and Medium Duty (<10,000 lbs) 77.7% of total fuel use

Other 0.3%

Diesel 1.6%

Gasoline (E0-E10) 75.8%

160

80

120

40

140

60

100

20

0

160

80

120

40

140

60

100

20

0Passenger Cars

557 GGE/Vehicle

700 GGE/Vehicle

417 GGE/Vehicle

Pickups, Vans, SUVs Medium Trucks/Vans

PopulationFuel Use

16

3 Vehicle Market Segments

Heavy-duty vehicles are built for specific applications and are generally built to order for each customer.

3.6 Heavy-Duty Vehicle Types

Vocational trucks are typically ordered from the truck OEM with only the cab attached to the vehicle chassis. The truck is shipped from the OEM to a body builder that installs a customized body to the vehicle chassis. This is the same process that is used in the medium-duty market when specialized truck bodies are required. In the heavy-duty market, however, the vehicle purchaser typically has many more choices in configuring the vehicle chassis, cab, and engine. Because of the ability to customize the body and chassis, it is possible for the customer to purchase almost any vocational truck as a natural gas truck, provided at least one vehicle OEM offers a natural gas option for the base vehicle chassis. For example, Freightliner currently offers its M2-112 chassis with the Cummins ISL-G natural gas engine. As shown in Figure 3.6-1, this chassis can support a wide variety of vocational truck bodies as well as a semi-truck configuration. However, this chassis is designed for Class 7 and Class 8 applications and would not be ideal for Class 4 to Class 6 vehicles. Where natural gas options are not available from the vehicle OEM on a chassis in the proper weight class for a particular application, vocational truck purchasers must utilize SVMs to provide natural gas engine conversions. As with medium-duty vehicles, the standard practice of customizing heavy-duty vehicles provides an opportunity to integrate natural gas engines and fuel systems without significantly altering the typical heavy-duty vehicle purchase process.

Semi-trucks do not employ specialized bodies but instead use a fifth wheel to connect to and haul various semi-trailers. Despite the lack of a specialized body, semi-trucks are no less customized by the vehicle purchaser. Because semi-trucks travel more miles annually than any other vehicle type, fleets invest a great deal of time determining the precise combinations of engine, transmission, and drive train that will maximize fuel economy and minimize operating costs.

The heavy-duty market contains a diverse population of vehicles and can be separated into two general groups: vocational trucks and semi-trucks. Vocational trucks have specialty (purpose-built) bodies and support equipment; examples include cement mixers, street sweepers, and refuse trucks. This generally restricts their use to their intended application. Semi-trucks retain versatility by connecting to different trailers but are generally used for goods movement. While vocational trucks may be the most highly customized heavy-duty vehicles, both vocational and semi-trucks can be offered in thousands of configuration options by OEMs and numerous aftermarket vehicle modifiers.

17

Figure 3.6-1

As shown by these examples of four heavy-duty truck bodies on a single chassis, many heavy-duty vehicles are highly customized and intended for use in a specific application.

Semi-Truck

Tanker Truck

Fire Truck

Dump Truck

18

3 Vehicle Market Segments

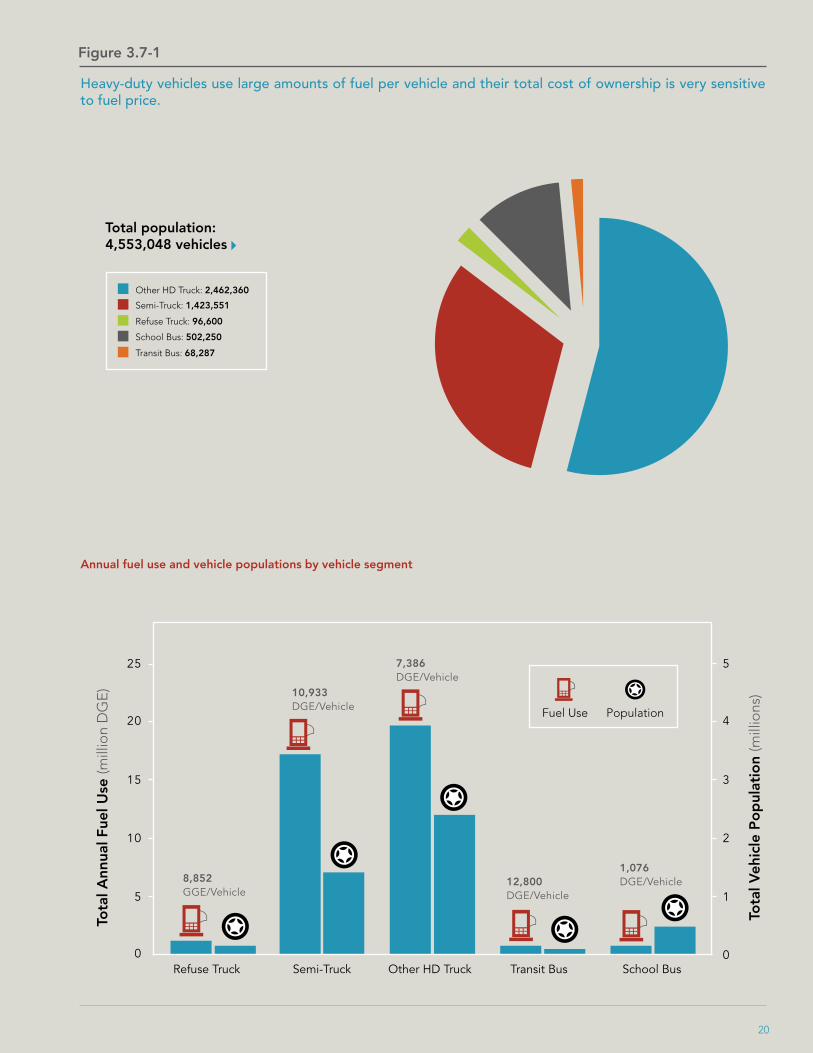

Heavy-duty vehicles consume the most fuel per vehicle, making their total cost of ownership very sensitive to fuel price.

3.7 Heavy-Duty Population and Fuel Use

There are approximately 11 million heavy-duty vehicles in use in the U.S.; about one-third of these are Class 7 and Class 8 semi-trucks used principally for goods movement. Various vocational trucks (excluding refuse trucks) comprise approximately 55 percent of the total heavy-duty fleet. These vehicles range in size from Class 4 to Class 8 and cover a wide range of applications. As shown in Figure 3.7-1, in most heavy-duty applications, the average truck fuel consumption exceeds 7,000 DGE per year. Note that for applications where vehicles must carry more than 60 DGE of natural gas, it is likely that fuel will be stored as liquefied natural gas (LNG) rather than CNG due to space limitations on the vehicle chassis.

In the heavy-duty market, the major cost focus when purchasing a vehicle is typically on total cost of ownership, including acquisition costs, fuel costs, and maintenance. This has traditionally meant that end users would elect to purchase diesel engines. The prevalence of diesel engines is evidenced by the fact that diesel comprises more than 90 percent of the fuel consumed by heavy-duty vehicles.15 However, in heavy-duty applications that have low mileage accumulation and low fuel use, there has been a shift from diesel to gasoline as fuel efficiency and high mileage durability are less of an issue. Further, decreases in diesel reliability due to additional emissions controls and increases in operating and maintenance costs from these same emissions controls have increased the total cost of ownership for diesel engines. This increase in costs makes total cost of ownership comparisons between diesel and natural gas engines more favorable for natural gas.16

Heavy-duty vehicles account for just over 4 percent of the fleet but use more than 28 percent of all of the transportation fuel in the U.S.14 The majority of fuel used in the heavy-duty market is diesel fuel due to the higher fuel economy and higher torque of compression-ignition diesel engines compared to spark-ignition gasoline engines. With fuel costs constituting such a large portion of total cost of ownership, fuels with significant price differentials relative to diesel, such as natural gas, can be an attractive option to significantly reduce total cost of ownership.

14 U.S. DOE Energy Efficiency and Renewable Energy. “Transportation Energy Data Book.” Edition 31. 2012. 15 Ibid.16 TIAX LLC. “Comparative Costs of 2010 Heavy-Duty Diesel and Natural Gas Technology.” Presented at 23rd Annual NGV Conference, San Francisco, CA. October 5-6, 2005.

19

Figure 3.7-1

Heavy-duty vehicles use large amounts of fuel per vehicle and their total cost of ownership is very sensitive to fuel price.

Total population: 4,553,048 vehicles

Other HD Truck: 2,462,360

Semi-Truck: 1,423,551

School Bus: 502,250

Refuse Truck: 96,600

Transit Bus: 68,287

Tota

l Ann

ual F

uel U

se (m

illio

n D

GE

)

Tota

l Veh

icle

Po

pul

atio

n (m

illio

ns)

Annual fuel use and vehicle populations by vehicle segment

525

420

315

210

15

0 0Refuse Truck Semi-Truck

8,852 GGE/Vehicle

10,933 DGE/Vehicle

12,800 DGE/Vehicle

7,386 DGE/Vehicle

1,076 DGE/Vehicle

Other HD Truck Transit Bus School Bus

20

PopulationFuel Use

4 Characteristics of Vehicle Market Segments

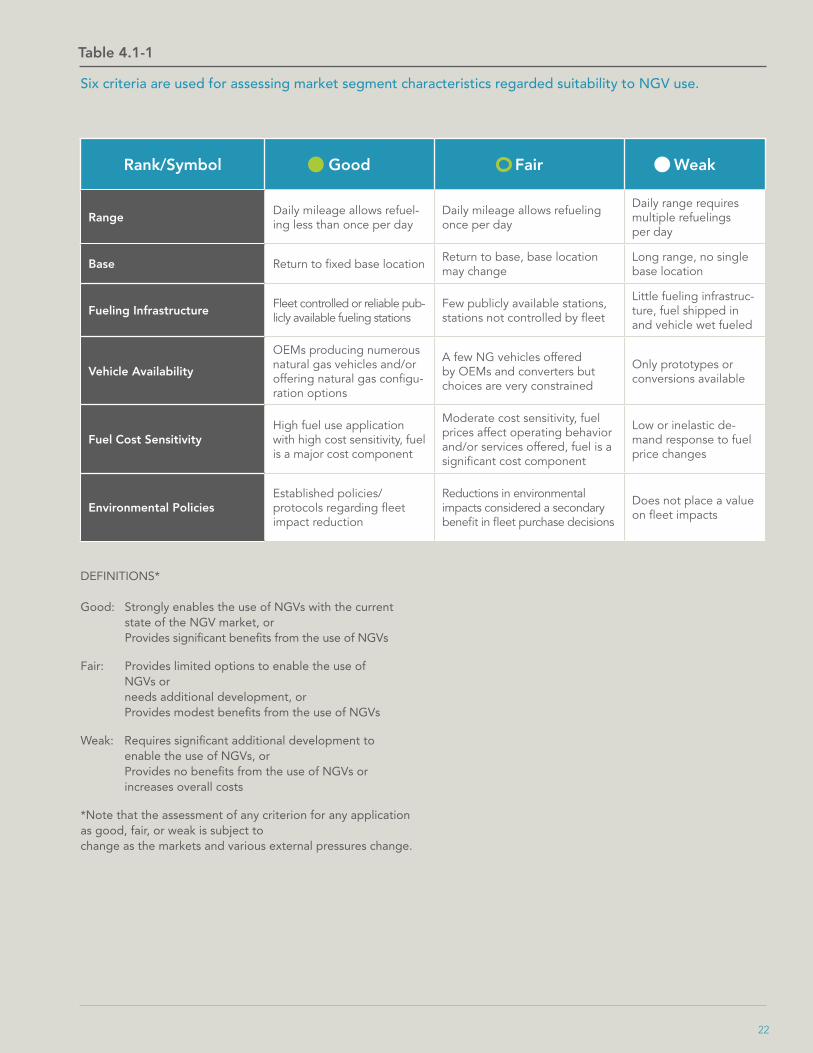

Market segments are unique and complex, with many specific vehicle applications. However, several common criteria can be used to broadly compare vehicle applications with regard to the use of natural gas as a vehicle fuel.

4.1 Overview

“Base” refers to the location where the vehicle is parked or stored when not in operation. Return-to-base applications, where the vehicle is returned to the same location each day, are the most conducive to NGV use because they allow for daily refueling, thereby minimizing onboard fuel storage requirements. These return-to-base applications often include centralized maintenance facilities and staff, allowing a few trained technicians to support numerous NGVs.

“Fueling Infrastructure” describes the typical method of refueling employed for a particular vehicle application as well as the potential for adding natural gas fueling infrastructure. Fleets that fuel their vehicles at fleet yards or operations centers (e.g. warehouses and ports) are best positioned to utilize nearby public fueling stations or install fleet-controlled natural gas fueling equipment.

“Vehicle Availability” describes the number and types of vehicles currently available for a particular application. In general, more vehicle and engine options help ensure that NGVs will be suitable to vehicle users within an application. OEM-provided options provide a single responsible party for warranty and service, making these offerings more appealing.

“Fuel Cost Sensitivity” considers the relative importance of fuel costs to other vehicle purchase and operating costs. In general, high fuel consumption applications are highly sensitive to fuel costs. Low fuel consumption applications tend to be more sensitive to purchase and maintenance costs.

“Environmental Policies” as a criterion attempts to describe whether vehicle users within a particular application are sufficiently motivated by internal policies or external regulations to make vehicle purchase decisions based on the relative environmental impacts of the vehicles. It is important to remember that the requirements and evaluations for each application are broad and high level. Given the diversity and complexity of the North American vehicle market, it is certain that many exceptions to these broad evaluations exist.

The following sections describe the attributes of several key specific vehicle segments within the overall market segments discussed above. In addition, several sub-segments are described that represent common types of operation within the broader segments. For example, the package delivery sub-segment of vehicles is described as it involves pickup and delivery operations that are very different from other sub-segments like utility trucks. The goal is to provide a high level description of these key market segments as they relate to the use of natural gas. To provide a consistent basis on which to compare the segments, each segment is evaluated with respect to six key criteria, as defined further below and ranked in Table 4.1-1.

“Range” describes the typical daily operating range of vehicles in a particular application. Range is given in miles traveled for on-road applications and operating hours for off-road applications. In most applications, whether on-road or off-road, it is preferred by vehicle users that the vehicle carry enough fuel to operate for several days or be able to miss a typical refueling event without running out of fuel. This provides the user with some margin of error if daily operations deviate from the norm. At a minimum, it is assumed that a vehicle must carry enough fuel to work through an entire shift or typical day of operation.

21

Table 4.1-1

Six criteria are used for assessing market segment characteristics regarded suitability to NGV use.

Rank/Symbol Good Fair Weak

RangeDaily mileage allows refuel-ing less than once per day

Daily mileage allows refueling once per day

Daily range requires multiple refuelings per day

Base Return to fixed base location Return to base, base location may change

Long range, no single base location

Fueling InfrastructureFleet controlled or reliable pub-licly available fueling stations

Few publicly available stations, stations not controlled by fleet

Little fueling infrastruc-ture, fuel shipped in and vehicle wet fueled

Vehicle Availability

OEMs producing numerous natural gas vehicles and/or offering natural gas configu-ration options

A few NG vehicles offered by OEMs and converters but choices are very constrained

Only prototypes or conversions available

Fuel Cost SensitivityHigh fuel use application with high cost sensitivity, fuel is a major cost component

Moderate cost sensitivity, fuel prices affect operating behavior and/or services offered, fuel is a significant cost component

Low or inelastic de-mand response to fuel price changes

Environmental PoliciesEstablished policies/protocols regarding fleet impact reduction

Reductions in environmental impacts considered a secondary benefit in fleet purchase decisions

Does not place a value on fleet impacts

DEFINITIONS*

Good: Strongly enables the use of NGVs with the current state of the NGV market, or Provides significant benefits from the use of NGVs

Fair: Provides limited options to enable the use of NGVs or needs additional development, or Provides modest benefits from the use of NGVs

Weak: Requires significant additional development to enable the use of NGVs, or Provides no benefits from the use of NGVs or increases overall costs

*Note that the assessment of any criterion for any application as good, fair, or weak is subject to change as the markets and various external pressures change.

22

4 Characteristics of Vehicle Market Segments

Light-duty passenger cars and trucks owned by private consumers represent the single largest vehicle market, but purchase decisions are driven by a number of factors beyond total cost of ownership.

4.2 Light-duty Passenger Cars and Trucks (Private)

Fueling Infrastructure - In certain regions, particularly dense urban areas, natural gas fueling infrastructure is accessible by the general public. However, outside these regions, fueling infrastructure may be sparse. This is the primary reason for consumer concerns regarding range for infrequent but long range travel. Establishing fueling infrastructure along strategic corridors, coupled with high visibility to consumers that natural gas is available, can help mitigate these concerns. Additionally, OEM offerings of bi-fuel NGVs can address infrastructure and range concerns at the cost of certainty that natural gas will be used as the primary fuel in the vehicle.

Vehicle Availability - Currently, the Honda Civic Natural Gas is the only passenger car offered by an OEM. Additionally, Ford and GM offer light-duty trucks equipped with “vehicle prep packages” that prepare the vehicle for conversion by aftermarket converters. The current selection of NGVs is small in comparison to the broad range of consumer vehicle choices in the light-duty market and requires an aftermarket conversion in most light-duty sub-segments.

Fuel Cost Sensitivity - The typical replacement cycle for passenger cars and light trucks is approximately six years.18 This, coupled with the relatively low annual fuel consumption, means that acquisition costs for the vehicle are significantly greater than the fuel costs over the life of the vehicle. Consumers have also demonstrated a generally inelastic demand response to fuel prices in the short term and long term.19 That is, consumers do not purchase less gas until fuel prices increase significantly. Increases in gasoline prices from additional taxes or decreases in natural gas prices from incentives or utility level pricing could widen the price spread sufficiently to motivate additional consumers.

Environmental Policies - Consumers place various levels of value on the reduction of environmental impacts; some consumers are willing to pay more for environmental benefits, but many are not.

The majority of light-duty vehicles are passenger cars and trucks owned by private consumers for the purpose of personal transportation. These applications are typified by low fuel use (575 to 825 GGE per year), and markets are primarily driven by consumer preferences rather than total cost of ownership calculations (Figure 4.2-1).

Range - Privately owned passenger cars and light-duty trucks travel, on average, 30 miles per day, a range easily attainable by NGVs. For example, the 2012 Honda Civic Natural Gas has an estimated range of 249 miles based on a combined EPA mileage rating of 31 miles per gallon and a 8.03 gallon onboard fuel capacity,17 providing several days of fuel for the average user.

Base - Private users generally return their vehicles to their home at the end of the day. Therefore, the user is able to become familiar with the existing fueling infrastructure and possibly install personal natural gas fueling infrastructure.

17 Honda. “2012 Honda Civic Natural Gas - Specifications.” http://automobiles.honda.com/civic-natural-gas/specifications.aspx. Accessed August 2012.18 Edmunds AutoObserver. “Car Owners Hanging Onto Their Current Rides.” http://www.autoobserver.com/2009/02/car-owners-hanging-onto-their-current-rides.html. February 2009.19 U.S. Federal Trade Commission. “Gasoline Price Changes: The Dynamics of Supply, Demand, and Competition.” 2005.

23

Figure 4.2-1

Light-duty passenger cars and trucks are the largest market segment by vehicle count and offer some market potential for NGVs.

Example NGVsHonda Civic Natural Gas, Ford F150 (BAF conversion, Chevrolet Malibu (IMPCO, Natural Drive conversions))

Common refueling locations Local public stations

Typical daily range 30 miles20

Average age at first replacement 6 years

Honda Civic Natural Gas

Ford F150 CNG Truck Home Fueling Appliance

Good Fair Weak

Vehicle Type/Application

Range BaseFueling

InfrastructureVehicle

AvailabilityFuel Cost Sensitivity

EnvironmentalPolicies

Passenger Car/Light Truck (Private)

20 U.S. DOE Energy Efficiency and Renewable Energy. “Transportation Energy Data Book.” Edition 31. 2012.

24

4 Characteristics of Vehicle Market Segments

Light-duty passenger cars and trucks owned by commercial and government fleets are generally the same basic vehicles offered to the private consumer market but may be modified for a specific job. Vehicle acquisition costs exceed fuel costs over the life of the vehicle, but environmental policies may drive some purchase decisions.

4.3 Light-Duty Passenger Cars and Trucks (Commercial/Government)

Fueling Infrastructure - Small fleets may rely on public fueling infrastructure or make use of personal fueling devices. Large fleets may also rely on public fueling infrastructure or install their own fueling equipment in conjunction with natural gas utilities and fuel providers. Initial capital costs and/or ongoing station maintenance may be deterrents to some fleets to the installation of their own fueling equipment, but tax credits and financial incentives may offset some of these concerns.

Vehicle Availability - Currently, the Honda Civic Natural Gas is the only passenger car offered by an OEM. GM has announced the availability of a CNG option for its Savanna full size van later this year. Additionally, Ford and GM offer light-duty trucks equipped with “vehicle prep packages” that prepare the vehicle for conversion by aftermarket converters. OEMs typically offer additional natural gas options to commercial/government customers, providing more choices than in the private consumer market. However, the availability of NGVs still does not provide OEM options in most light-duty market sub-segments.

Fuel Cost Sensitivity - The typical replacement cycle for passenger cars and light trucks in government and commercial fleets is shorter than private fleets at approximately three years.28 This is, in part, a function of the higher annual mileage of commercial fleets compared to private consumers. While annual fuel consumption increases with mileage, acquisition costs for the vehicle are still typically greater than the fuel costs over the life of the vehicle. Increases in gasoline prices from additional taxes or decreases in natural gas prices or utility level pricing could widen the price spread sufficiently to motivate more fleets to adopt natural gas.

Environmental Policies - Most government fleets are subject to environmental policies that affect fleet purchase decisions. Many commercial fleets are adopting environmental policies, but many of these policies only require tracking of fleet impacts and do not drive purchase decisions.

Commercial light-duty vehicles are passenger cars and trucks owned by companies for business-related activities. Annual mileage in these applications is approximately twice that of private consumers, with a corresponding increase in annual fuel consumption (Figure 4.3-1). Federal fleet vehicles have lower average annual miles than commercial fleet vehicles, similar to private consumers.

Range - It is estimated that the average daily range for light-duty business vehicles is approximately 100 miles, well within the range of most NGVs. Some high fuel use light-duty applications like taxis may require fueling at least once a day. This does not preclude successful application of NGVs to these markets, as evidenced by the ongoing successful use of natural gas taxis in the U.S. Applications requiring daily, long range driving will encounter the same range limitations based on available fueling infrastructure as seen in the private consumer market.

Base - Vehicles are commonly returned to the same location each night. In large fleets, the base is typically a commercial or government fleet yard with centralized fueling and maintenance.

25

Figure 4.3-1

Commercial and government users of light-duty passenger cars and trucks use the same vehicles as private consumers but typically with higher annual usage and also offer some market potential for NGVs.

Example NGVsHonda Civic Natural Gas, GMC Savanna, Ford Crown Victoria (BAF conversion)

Common refueling locations Public stations, fleet yards

Typical daily range 100 miles21

Average age at first replacement 3 years22

Honda Civic Natural Gas

Ford Crown Victoria

Good Fair Weak

GMC Savanna CNG Van

Vehicle Type/Application

Range BaseFueling

InfrastructureVehicle

AvailabilityFuel Cost Sensitivity

EnvironmentalPolicies

Passenger Car/Light Truck (Commercial)

21 U.S. DOE Energy Efficiency and Renewable Energy. “Transportation Energy Data Book.” Edition 31. 2012. Calculated from annual VMT assuming 250 work days per year. 22 Ibid.

26

4 Characteristics of Vehicle Market Segments

Medium-duty vehicles have shorter average range than light-duty vehicles but consume more fuel per vehicle. High fuel consumption applications like pickup and delivery services can be very sensitive to fuel costs.

4.4 Medium-Duty Private and Commercial Trucks

Base - The majority of medium-duty vehicles are return-to-base applications. However, the size of the fleet that operates the vehicle often determines the size and characteristics of the base location. Smaller fleets may simply garage the vehicle each night, similar to a private owner, and will not have access to time-fill fueling stations or dedicated mechanics.

Fueling Infrastructure - Large fleets may provide centralized fueling at fleet yards and could add natural gas fueling infrastructure at these locations. Smaller fleets and private owners need to rely on access to public fueling stations.

Vehicle Availability - Natural gas options for medium-duty vehicles are primarily provided by SVMs, principally for vehicles with GM or Ford engines in the 4.6L to 6L range, although GM recently announced the availability of a CNG-fueled GM Savanna van and Chevrolet Express van.

Fuel Cost Sensitivity - Medium-duty trucks include high fuel consumption applications like pickup and delivery vehicles as well as lower fuel consumption applications like work trucks. Given that low fuel consumption applications would consume less than the segment average of 1,100 GGE per year, putting them on par with light-duty pickups, it is expected that fuel cost sensitivity would be similar to light-duty applications. High fuel consumption applications are likely to be highly sensitive to fuel costs as in other segments.

Environmental Policies - Medium-duty vehicles are found in government, commercial, and private fleets. Most government fleets are subject to environmental policies that affect fleet purchase decisions. Many commercial fleets are adoption environmental policies, but many of these policies only require tracking of fleet impacts and do not drive purchase decisions. Private fleets are unlikely to make purchase decisions based on environmental impacts.

Most medium-duty vehicles are owned by commercial fleets, although some private consumers utilize large pickups for personal use. Medium-duty vehicles consist of Class 2b and Class 3 trucks, vans, and pickups (Figure 4.4-1). As with all market segments, use varies by vehicle owner, but common uses include pickup and delivery service and work trucks. Fuel costs can be significant in pickup and delivery service.

Range - Based on an estimated daily range of 55 miles for medium-duty trucks, the storage of 10 GGE of natural gas should provide at least one day of operating range and is easily achieved using current NGV fuel storage systems. Even in higher fuel use operations like pickup and delivery service, it is feasible to equip the vehicle with sufficient fuel capacity for a full day of operation.

27

Figure 4.4-1

Medium-duty vehicle chassis are mass produced, and customized bodies are added based on customer needs. Medium-duty vehicles may offer significant market potential for NGVs.

Example NGVs Varies

Common refueling locations Fleet yards, Local public gas stations

Typical daily range 55 miles23

Average age at first replacement Varies

Ford E-series Cutaway

Good Fair Weak

Isuzu NPR Eco-Max

Vehicle Type/Application

Range BaseFueling

InfrastructureVehicle

AvailabilityFuel Cost Sensitivity

EnvironmentalPolicies

Medium-Duty Private and Commercial Truck

Ford E-Series Cargo Van Ford F-series Incomplete Truck

23 U.S. DOE Energy Efficiency and Renewable Energy, “Transportation Energy Data Book.” Edition 31. 2012. Estimate based on average annual mileage for Class 3 trucks, assuming 250 work days per year.

28

4 Characteristics of Vehicle Market Segments

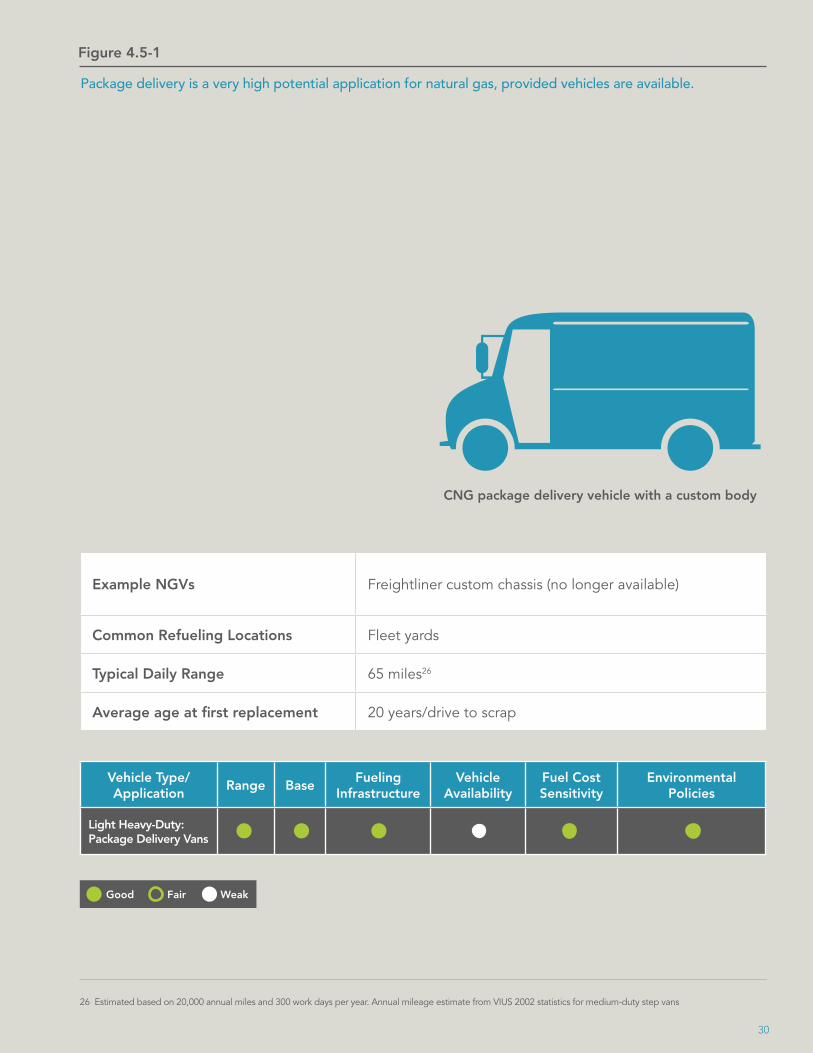

As a segment, package delivery vehicles have several attributes that are conducive to natural gas adoption, including high fuel consumption and high sensitivity to fuel costs.

4.5 Heavy-Duty: Package Delivery Vehicles

Base - Most package delivery vehicles are returned to fleet yards for fueling and maintenance. This environment is generally the most conducive to the introduction of new vehicles and fueling infrastructure.

Fueling Infrastructure - Most package delivery vehicles are fueled at the fleet yards as this provides the fleet with some ability to control fuel costs. Given proper route selection, most package delivery vehicles can operate from a single fueling location at the fleet yard. This model of fueling should be directly applicable to NGVs.

Vehicle Availability - Like most heavy-duty vehicles, package delivery vans are typically custom built. This allows fleet purchasers to specify a natural gas fuel system for a given vehicle type without necessarily causing significant increases in delivery lead time. However, no major engine OEM currently offers a natural gas engine in the 4.6L to 6L displacement range typical of package delivery cars. With the exit of Freightliner Custom Chassis from this market segment, there is a need for other OEMs to provide a natural gas package van option.

Fuel Cost Sensitivity - Purchasing fuel constitutes a major cost of operating package delivery trucks, outstripping maintenance costs. Given the cost-sensitive nature of package delivery service, fleet operators in this segment are likely to strongly value the lower fuel costs associated with operating NGVs in package delivery service.

Environmental Policies - All three major package delivery firms in the U.S. (FedEx, UPS, and the United States Postal Service) have adopted policies to reduce environmental impacts from their fleets, produce annual reports on their efforts, and purchase and demonstrate vehicles based on their environmental policies.

A typical package delivery car will be driven by the original purchaser until it is scrapped, approximately twenty years. During this time, fuel costs are the major component of operating costs.24 Further, package delivery is a narrow margin business and minimizing fleet costs is a priority. Given these economic conditions and the proven use by UPS of more than 1,000 NGVs (Figure 4.5-1),25 the package delivery segment could be a strong adopter of natural gas.

Range - Average daily ranges for package delivery vehicles vary by route, but an analysis of U.S. Census Bureau Vehicle Inventory and Use Survey (VIUS) data for similar step vans suggests an average daily range of 65 miles. Given the highly organized nature of the major package delivery firms with regard to routes, these companies could select routes that would allow an NGV to operate with a comfortable range margin.

24 National Renewable Energy Laboratory. “UPS CNG Truck Fleet Final Results.” 2002. Fuel costs estimated as a percentage of total operating costs per mile based on scaling fuel prices given in the report to $3.00 per DGE.

25 UPS. “UPS Deploys 245 New ‘Green’ Trucks.” Press release. January 2010.

29

Figure 4.5-1

Package delivery is a very high potential application for natural gas, provided vehicles are available.

Good Fair Weak

Vehicle Type/Application

Range BaseFueling

InfrastructureVehicle

AvailabilityFuel Cost Sensitivity

EnvironmentalPolicies

Light Heavy-Duty: Package Delivery Vans

Example NGVs Freightliner custom chassis (no longer available)

Common Refueling Locations Fleet yards

Typical Daily Range 65 miles26

Average age at first replacement 20 years/drive to scrap

CNG package delivery vehicle with a custom body

26 Estimated based on 20,000 annual miles and 300 work days per year. Annual mileage estimate from VIUS 2002 statistics for medium-duty step vans

30

27 Tomic, J., B. Van Amburg. “Heavy-Duty Hybrid Utility Trucks – HTUF Deployment Experiences and Results.” Presented at EVS-23, Anaheim, CA. 2007.

4 Characteristics of Vehicle Market Segments

Utility trucks consume more fuel than their daily range suggests due to extended idling needed to operate support equipment.

4.6 Heavy-Duty: Utility Trucks

Base - Utility trucks are typically return-to-base vehicles. Periodically, some utility vehicles may need to make extended trips to provide service in remote locations. In these cases, range may become an issue unless a bi-fuel NGV configuration is used. In typical operation, however, utility trucks will return to base each day and can benefit from fueling infrastructure and centralized maintenance at fleet yards.

Fueling Infrastructure - Utility fleets typically fuel their trucks centrally at the fleet yard. Because of their daily return-to-base operation, utility trucks can utilize fleet controlled, time-fill natural gas fueling infrastructure.

Vehicle Availability - Larger utility trucks in the Class 6 to 8 category are available in OEM natural gas configurations from Freightliner. Class 4 and 5 natural gas utility trucks are supplied by aftermarket conversions.