market research report : waste management market in india 2015 - sample

TRANSCRIPT

2

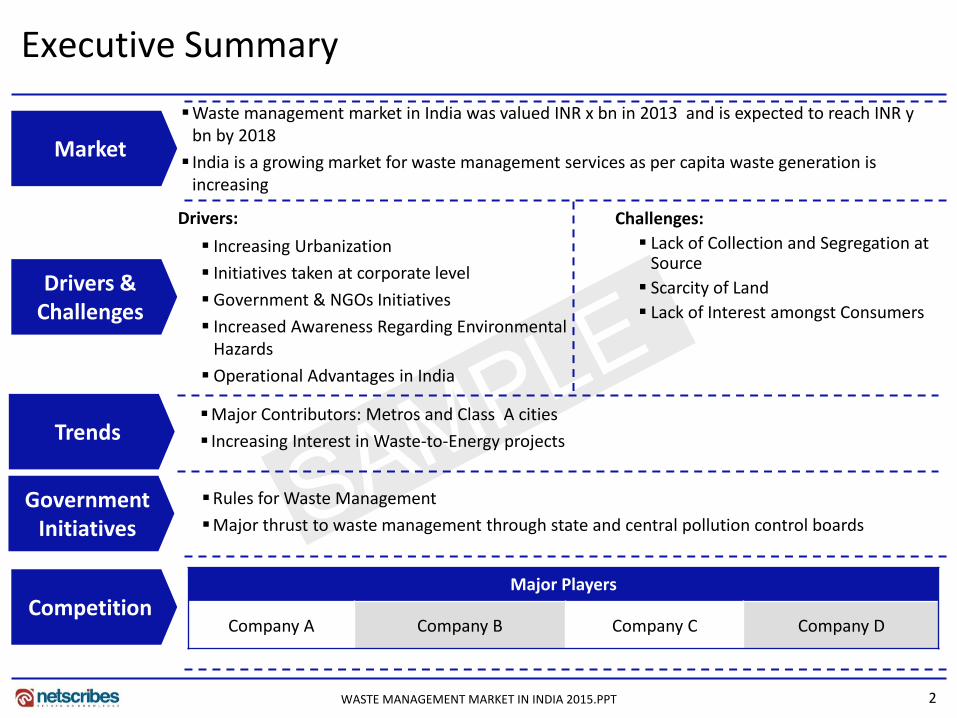

Executive Summary

Market

Drivers & Challenges

Government Initiatives

Competition

Waste management market in India was valued INR x bn in 2013 and is expected to reach INR y bn by 2018

India is a growing market for waste management services as per capita waste generation is increasing

Drivers:

Increasing Urbanization

Initiatives taken at corporate level

Government & NGOs Initiatives

Increased Awareness Regarding Environmental Hazards

Operational Advantages in India

Challenges:

Lack of Collection and Segregation at Source

Scarcity of Land

Lack of Interest amongst Consumers

Rules for Waste Management

Major thrust to waste management through state and central pollution control boards

Major Players

Company A Company B Company C Company D

Trends Major Contributors: Metros and Class A cities

Increasing Interest in Waste-to-Energy projects

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

3 WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

•Macroeconomic Indicators

•Market Overview

•Business Opportunities

•Drivers & Challenges

•Trends

•Government Regulations

•Competitive Landscape

•Strategic Recommendations

•Appendix

4

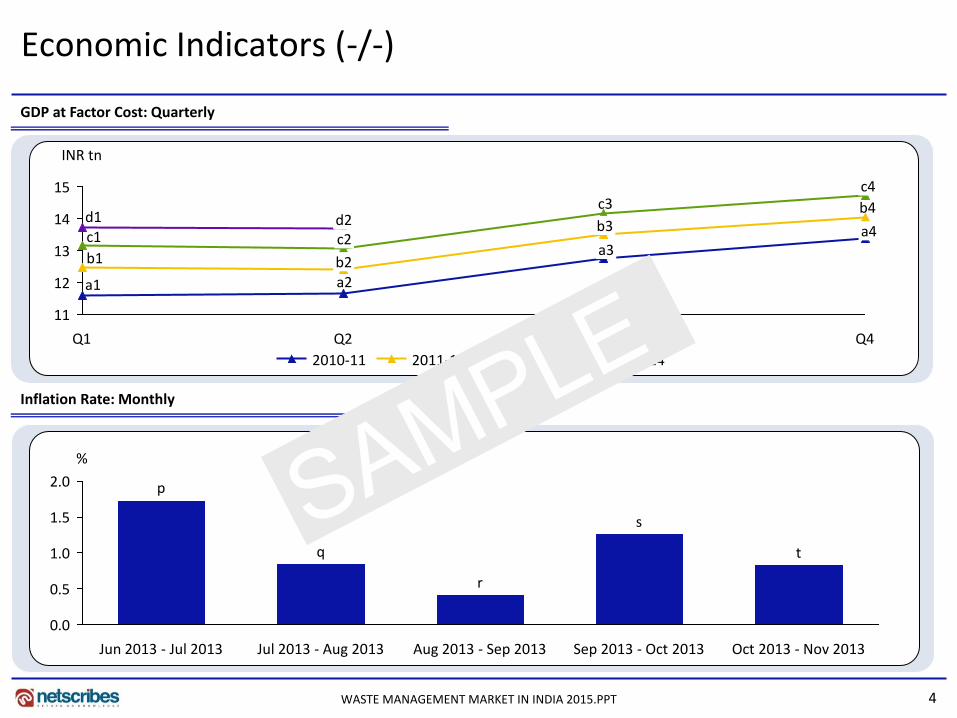

Economic Indicators (-/-)

GDP at Factor Cost: Quarterly

Inflation Rate: Monthly

11

12

13

14

15

INR tn

Q4

c4

d2 c2

b2 a2

Q1

d1 b4

a4

Q3

c3

b3

a3

Q2

c1

b1

a1

2013-14 2012-13 2011-12 2010-11

0.0

0.5

1.0

1.5

2.0

%

Oct 2013 - Nov 2013

t

Sep 2013 - Oct 2013

s

Aug 2013 - Sep 2013

r

Jul 2013 - Aug 2013

q

Jun 2013 - Jul 2013

p

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

5

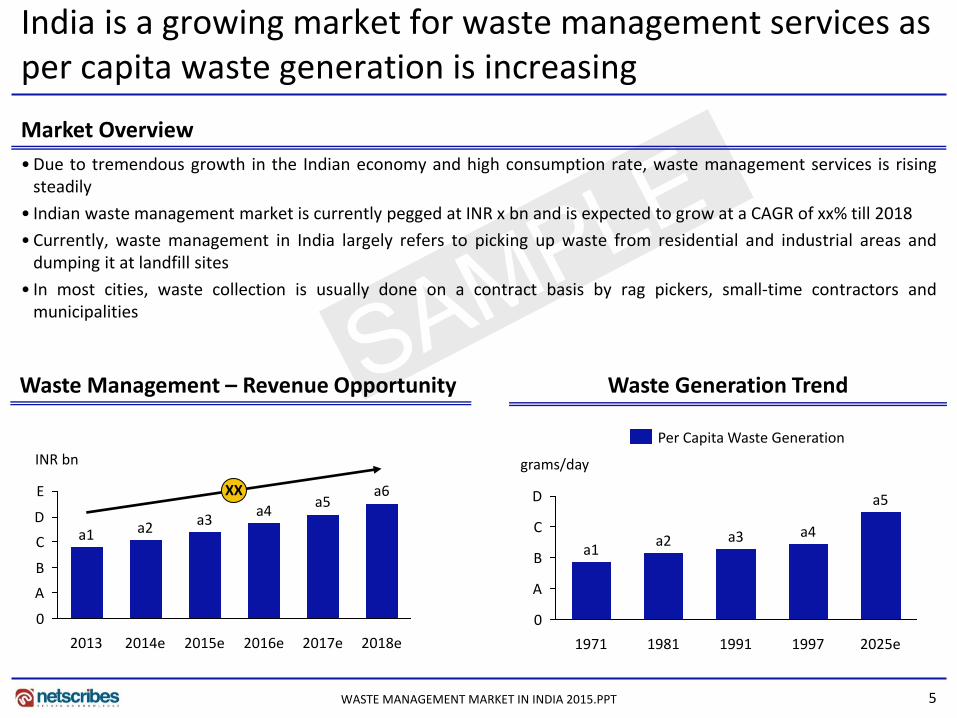

India is a growing market for waste management services as per capita waste generation is increasing

Waste Management – Revenue Opportunity

• Due to tremendous growth in the Indian economy and high consumption rate, waste management services is rising steadily

• Indian waste management market is currently pegged at INR x bn and is expected to grow at a CAGR of xx% till 2018

• Currently, waste management in India largely refers to picking up waste from residential and industrial areas and dumping it at landfill sites

• In most cities, waste collection is usually done on a contract basis by rag pickers, small-time contractors and municipalities

Market Overview

Waste Generation Trend

D

C

B

A

0

grams/day

a1

2025e

a5

1997

a4

1991

a3

1981

a2

1971

Per Capita Waste Generation

E

D

C

B

A

0

INR bn

2017e

a5

2016e

a4

2015e

a3

2014e

a2

2013

a1

XX

2018e

a6

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

6

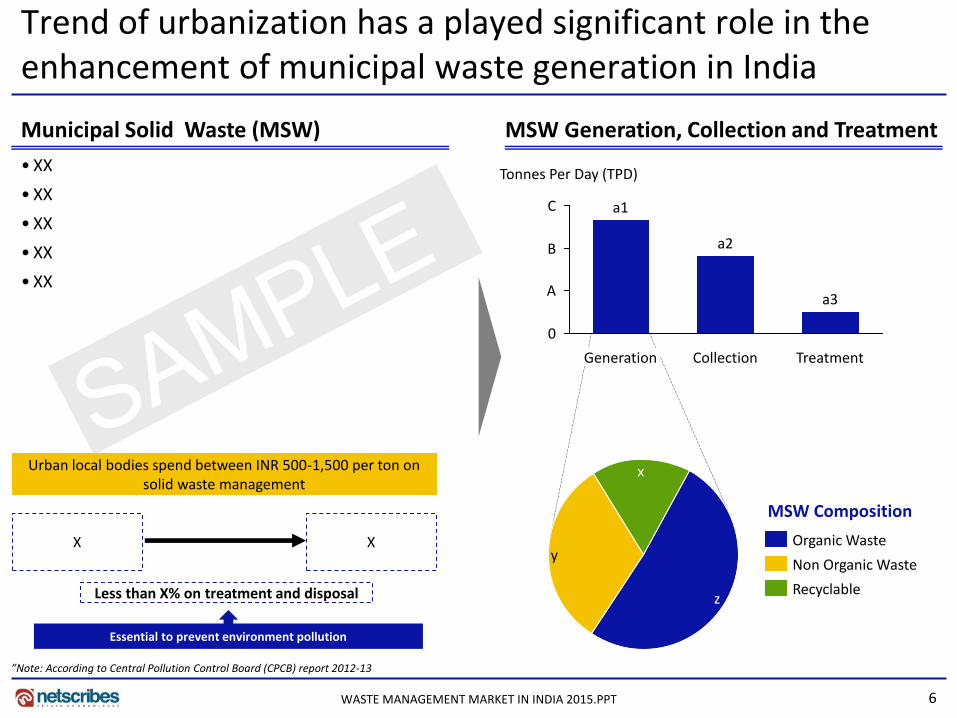

Trend of urbanization has a played significant role in the enhancement of municipal waste generation in India

MSW Generation, Collection and Treatment

• XX

• XX

• XX

• XX

• XX

Municipal Solid Waste (MSW)

”Note: According to Central Pollution Control Board (CPCB) report 2012-13

X X

Less than X% on treatment and disposal

Urban local bodies spend between INR 500-1,500 per ton on solid waste management

Essential to prevent environment pollution

C

B

A

0

a3

Collection

a2

Generation

a1

Tonnes Per Day (TPD)

Treatment

x

y

z Recyclable

Non Organic Waste

Organic Waste

MSW Composition

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

7

SAMPLE …every component of the waste to energy value chain

MSW to Energy Value Chain (2/2)

Business Opportunities (2/2)

Transportation and Logistics

MSW to energy recovery

Waste Management at Dumpsite

Organization/financing

• XX • XX

• XX • XX

• XX • XX

• XX • XX

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

8

SAMPLE Various companies will be benefitted in each part of the waste to energy value chain

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

Primary Collection and Segregation

• X

Separation of Wet Organic Wastes

• X

Transport and Logistics • X

Storage and Secondary Collection

• X

Waste Recycling • X

MSW Waste to Energy Recovery

• X

Management of Waste at Landfills

• X

Components In Value Chain

Companies that could benefit from the Waste to Energy sector

9

SAMPLE

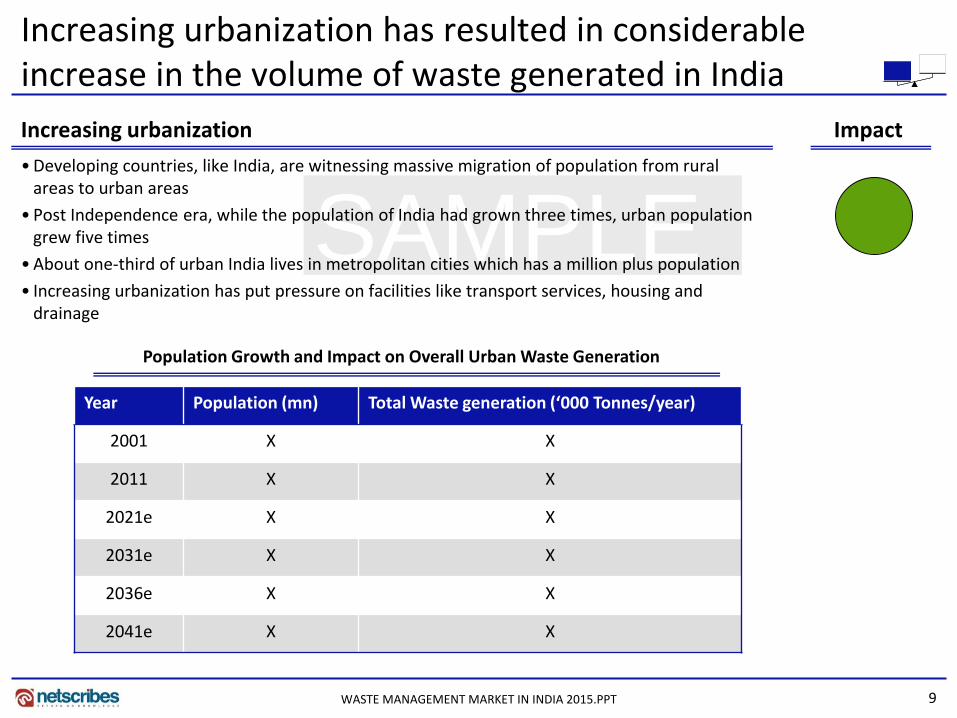

Increasing urbanization has resulted in considerable increase in the volume of waste generated in India

• Developing countries, like India, are witnessing massive migration of population from rural areas to urban areas

• Post Independence era, while the population of India had grown three times, urban population grew five times

• About one-third of urban India lives in metropolitan cities which has a million plus population

• Increasing urbanization has put pressure on facilities like transport services, housing and drainage

Increasing urbanization Impact

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

Population Growth and Impact on Overall Urban Waste Generation

Year Population (mn) Total Waste generation (‘000 Tonnes/year)

2001 X X

2011 X X

2021e X X

2031e X X

2036e X X

2041e X X

10

SAMPLE

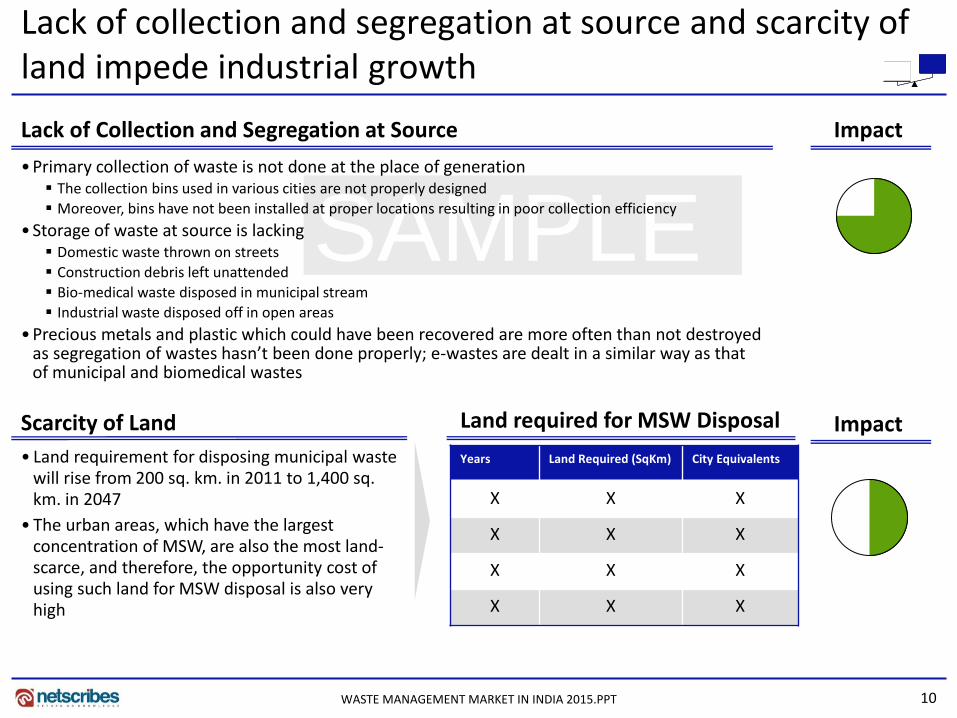

Lack of collection and segregation at source and scarcity of land impede industrial growth

Impact Lack of Collection and Segregation at Source

• Primary collection of waste is not done at the place of generation The collection bins used in various cities are not properly designed

Moreover, bins have not been installed at proper locations resulting in poor collection efficiency

• Storage of waste at source is lacking Domestic waste thrown on streets

Construction debris left unattended

Bio-medical waste disposed in municipal stream

Industrial waste disposed off in open areas

• Precious metals and plastic which could have been recovered are more often than not destroyed as segregation of wastes hasn’t been done properly; e-wastes are dealt in a similar way as that of municipal and biomedical wastes

Impact

• Land requirement for disposing municipal waste will rise from 200 sq. km. in 2011 to 1,400 sq. km. in 2047

• The urban areas, which have the largest concentration of MSW, are also the most land-scarce, and therefore, the opportunity cost of using such land for MSW disposal is also very high

Scarcity of Land Land required for MSW Disposal

Years Land Required (SqKm) City Equivalents

X X X

X X X

X X X

X X X

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

11

SAMPLE

Metropolitan cities and Class A cities generate over x% of waste in India

Major Contributors: Metros and Class A cities A handful of cities

account for the majority of waste

generated

• India produces around x lakh MT of e-waste per year Mumbai generates nearly 61,000 tonnes of electronic waste per year followed by New Delhi, which generates

43,000 tonnes of waste

Bangalore ranks third in terms of e waste generation and produces nearly 37,000 tonnes of waste per year

• Cities are getting more and more crowded resulting in more generation of waste

• Lot of people are migrating from villages to cities in search of jobs

Note: Waste generation quantities in 2011; Class A cities: Population Range: 1,00,000 – 4,999,999

Solid Waste Generation Share*

x

z

y

Others Class A Cities Metro Cities

Solid Waste Generation in Metro Cities*

0 C B A

Ton

nes Per D

ay

Bengaluru a6

Hyderabad a5

Chennai a4

Delhi a3

Kolkata a2

Mumbai a1

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

12

SAMPLE

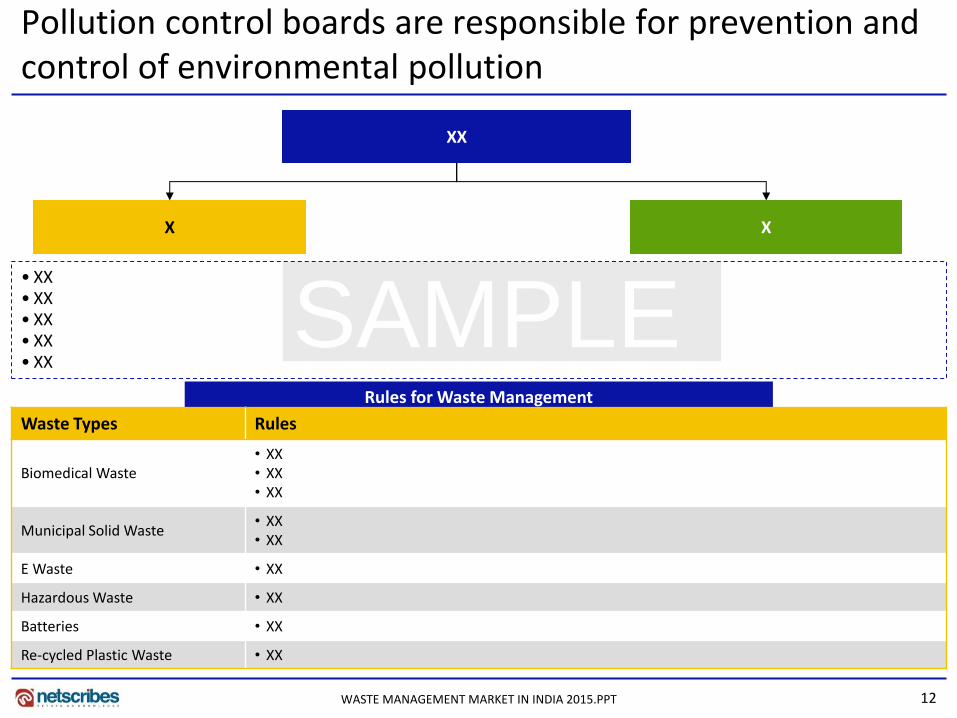

Pollution control boards are responsible for prevention and control of environmental pollution

XX

X X

• XX • XX • XX • XX • XX

Rules for Waste Management

Waste Types Rules

Biomedical Waste • XX • XX • XX

Municipal Solid Waste • XX • XX

E Waste • XX

Hazardous Waste • XX

Batteries • XX

Re-cycled Plastic Waste • XX

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

13

SAMPLE

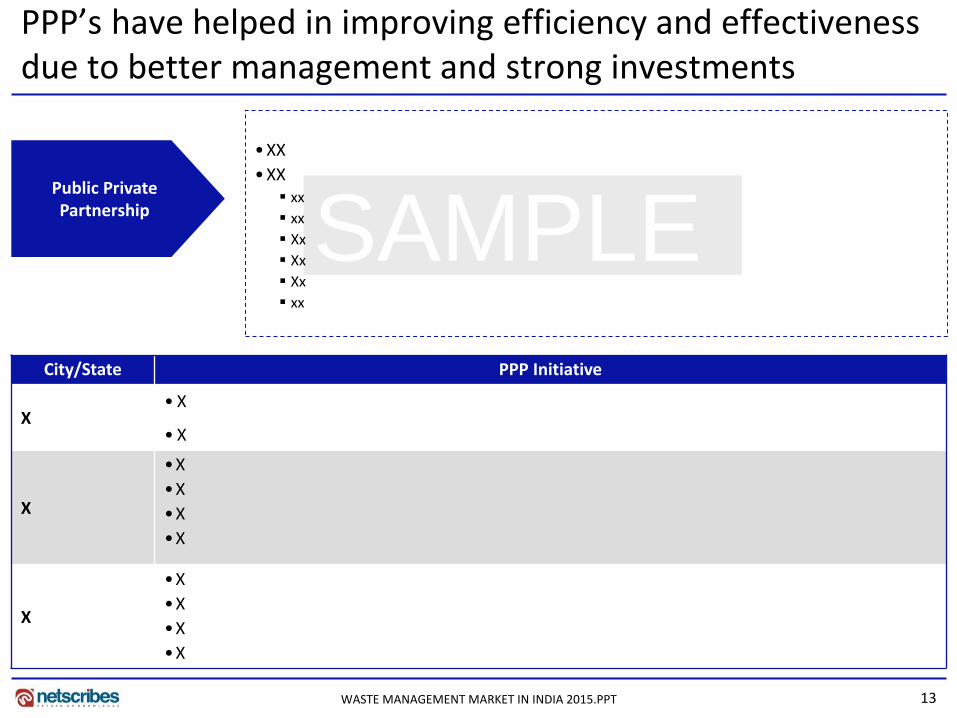

PPP’s have helped in improving efficiency and effectiveness due to better management and strong investments

Public Private Partnership

• XX

• XX xx

xx

Xx

Xx

Xx

xx

City/State PPP Initiative

X • X

• X

X

•X

•X

•X

•X

X

•X

•X

•X

•X

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

14

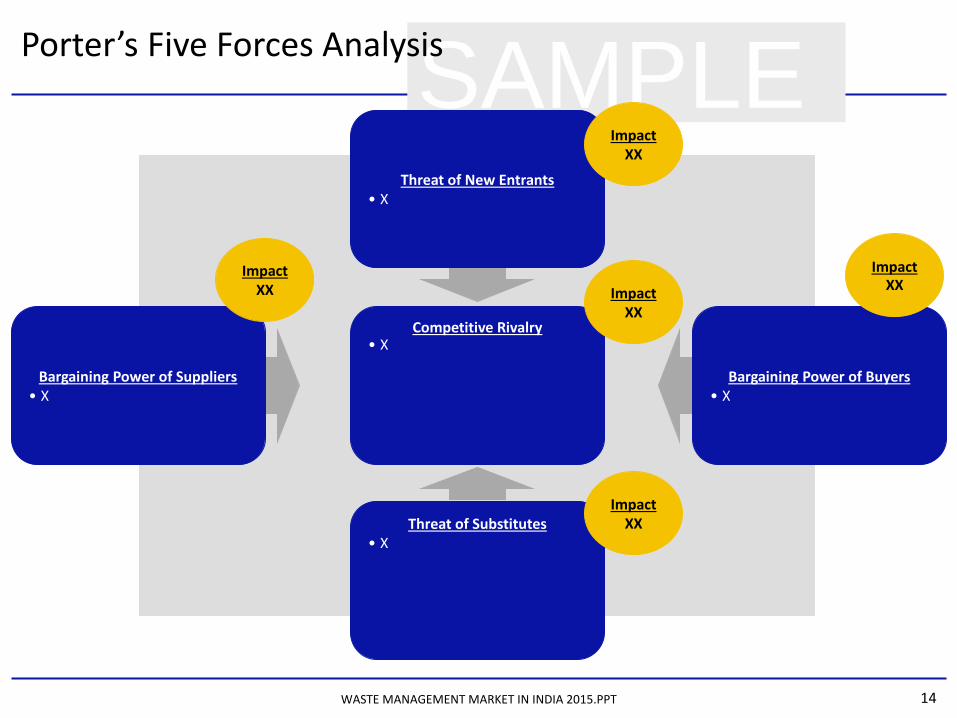

SAMPLE Porter’s Five Forces Analysis

Competitive Rivalry • X

Bargaining Power of Suppliers • X

Bargaining Power of Buyers • X

Threat of Substitutes • X

Threat of New Entrants • X

Impact XX

Impact XX

Impact XX

Impact XX

Impact XX

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

15

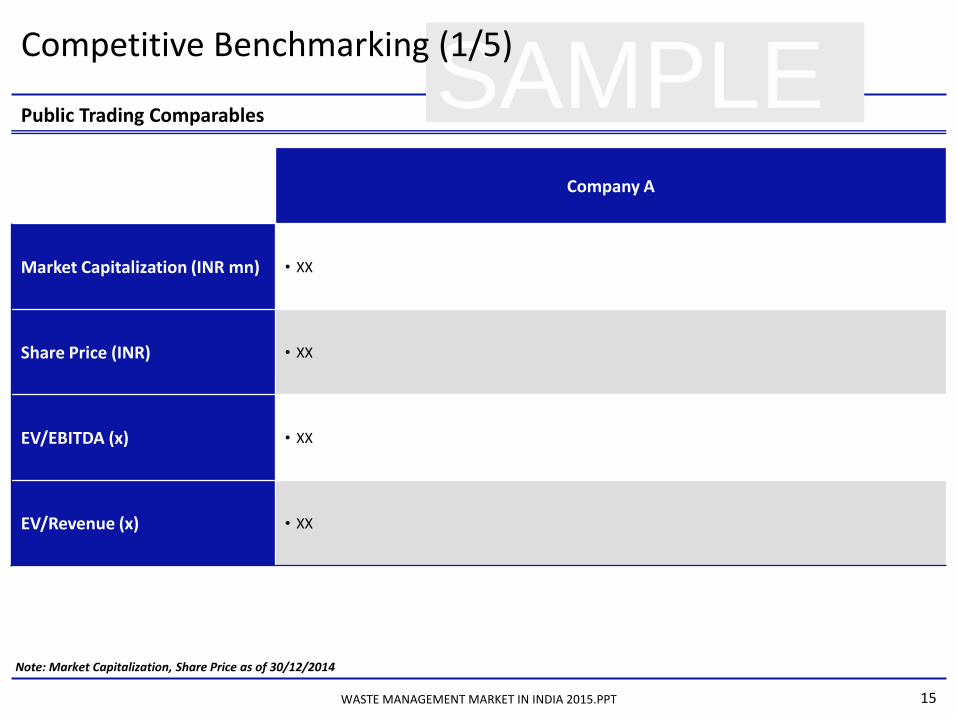

SAMPLE Competitive Benchmarking (1/5)

Public Trading Comparables

Company A

Market Capitalization (INR mn) • XX

Share Price (INR) • XX

EV/EBITDA (x) • XX

EV/Revenue (x) • XX

Note: Market Capitalization, Share Price as of 30/12/2014

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

16

SAMPLE Key Ratios of Top 3 Companies – Operational Basis (FY 2013) (X/X)

Competitive Benchmarking (X/X)

-10

-5

0

5

10

%

Company C

c2 c1

Company B

b2 b1

Company A

a2

a1

Net Margin Operating Margin

• XX

• XX

• XX

• XX

• XX

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

17

SAMPLE Public: Domestic Company – Company A(x/x)

Key People

Products and Services

Company Information Offices and Centres – India

Corporate Address • XX

Tel No. • XX

Fax No. • XX

Website • XX

Year of Incorporation • XX

Ticker Symbol • XX

Stock Exchange • XX

Category Products/Services

Waste Management Services

• XX

Name Designation

• XX • XX

• XX • XX

• XX • XX

• XX • XX

Mumbai

Head Office

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

18

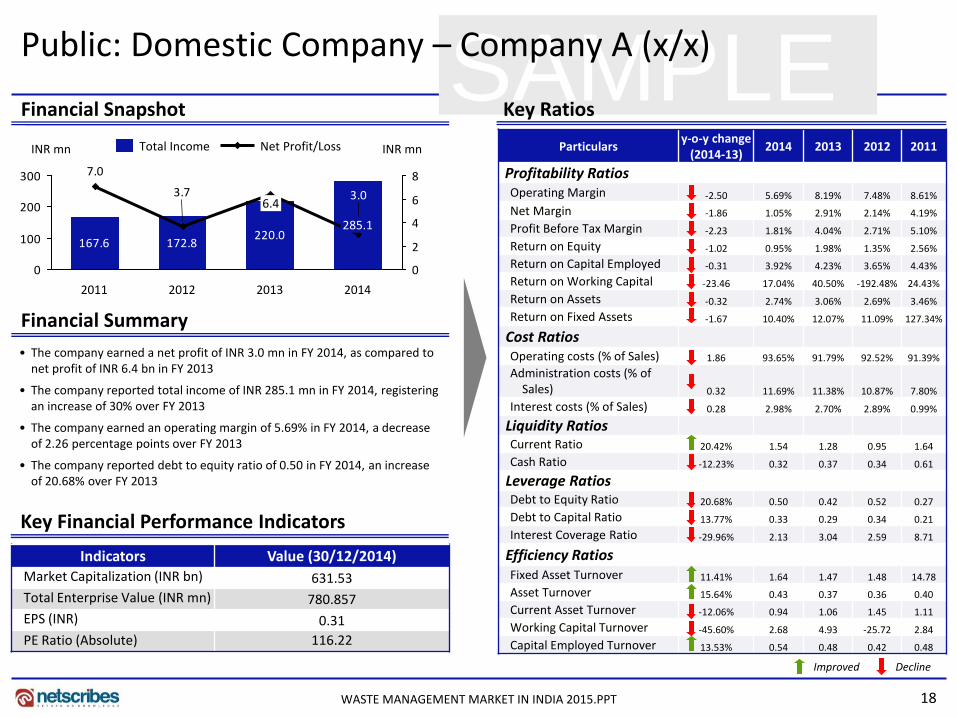

SAMPLE Financial Snapshot Key Ratios

Financial Summary

• The company earned a net profit of INR 3.0 mn in FY 2014, as compared to net profit of INR 6.4 bn in FY 2013

• The company reported total income of INR 285.1 mn in FY 2014, registering an increase of 30% over FY 2013

• The company earned an operating margin of 5.69% in FY 2014, a decrease of 2.26 percentage points over FY 2013

• The company reported debt to equity ratio of 0.50 in FY 2014, an increase of 20.68% over FY 2013

Key Financial Performance Indicators

Indicators Value (30/12/2014) Market Capitalization (INR bn) 631.53

Total Enterprise Value (INR mn) 780.857

EPS (INR) 0.31

PE Ratio (Absolute) 116.22

Particulars y-o-y change

(2014-13) 2014 2013 2012 2011

Profitability Ratios

Operating Margin -2.50 5.69% 8.19% 7.48% 8.61%

Net Margin -1.86 1.05% 2.91% 2.14% 4.19%

Profit Before Tax Margin -2.23 1.81% 4.04% 2.71% 5.10%

Return on Equity -1.02 0.95% 1.98% 1.35% 2.56%

Return on Capital Employed -0.31 3.92% 4.23% 3.65% 4.43%

Return on Working Capital -23.46 17.04% 40.50% -192.48% 24.43%

Return on Assets -0.32 2.74% 3.06% 2.69% 3.46%

Return on Fixed Assets -1.67 10.40% 12.07% 11.09% 127.34%

Cost Ratios

Operating costs (% of Sales) 1.86 93.65% 91.79% 92.52% 91.39%

Administration costs (% of Sales) 0.32 11.69% 11.38% 10.87% 7.80%

Interest costs (% of Sales) 0.28 2.98% 2.70% 2.89% 0.99%

Liquidity Ratios

Current Ratio 20.42% 1.54 1.28 0.95 1.64

Cash Ratio -12.23% 0.32 0.37 0.34 0.61

Leverage Ratios

Debt to Equity Ratio 20.68% 0.50 0.42 0.52 0.27

Debt to Capital Ratio 13.77% 0.33 0.29 0.34 0.21

Interest Coverage Ratio -29.96% 2.13 3.04 2.59 8.71

Efficiency Ratios

Fixed Asset Turnover 11.41% 1.64 1.47 1.48 14.78

Asset Turnover 15.64% 0.43 0.37 0.36 0.40

Current Asset Turnover -12.06% 0.94 1.06 1.45 1.11

Working Capital Turnover -45.60% 2.68 4.93 -25.72 2.84

Capital Employed Turnover 13.53% 0.54 0.48 0.42 0.48

Improved Decline

Net Profit/Loss Total Income

167.6220.0

172.8

3.7 3.0

7.0

0

100

200

300

0

2

4

6

8

INR mn INR mn

2011 2014

285.1

2013

6.4

2012

Public: Domestic Company – Company A (x/x)

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

19

SAMPLE Key Business Segments Key Geographic Segments*

Business Highlights

Description News

Overview

• XX • XX • XX • XX

Current and Pending Investors

• XX

Future Plan • XX

100%

80%

60%

40%

20%

0%

2014

x

e-Waste Management & Recycling

80%

100%

60%

40%

20%

0%

2012

x

India

The company has earned revenues from India only for

the last 4 fiscals

Public: Domestic Company – Company A (x/x)

The company has earned revenues from e-waste

Management and Recycling segment only for the last 4

fiscals

Note: Due to lack of critical data, the graph could not be generated for the year 2014

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

20

SAMPLE

• XX • XX

• XX • XX

T O

W S

Public: Domestic Company – Company A – SWOT Analysis (x/x)

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

21

SAMPLE Private: Domestic Company – Company B (x/x)

Key People

Products and Services

Company Information Offices and Centres – India

Category Products/Services

Water and Wastewater Management

XX Name Designation

XX XX

XX XX

XX XX

XX XX

Ahmedabad

Corporate Address XX

Tel No. XX

Fax No. XX

Website XX

Year of Incorporation XX

Head Office

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

22

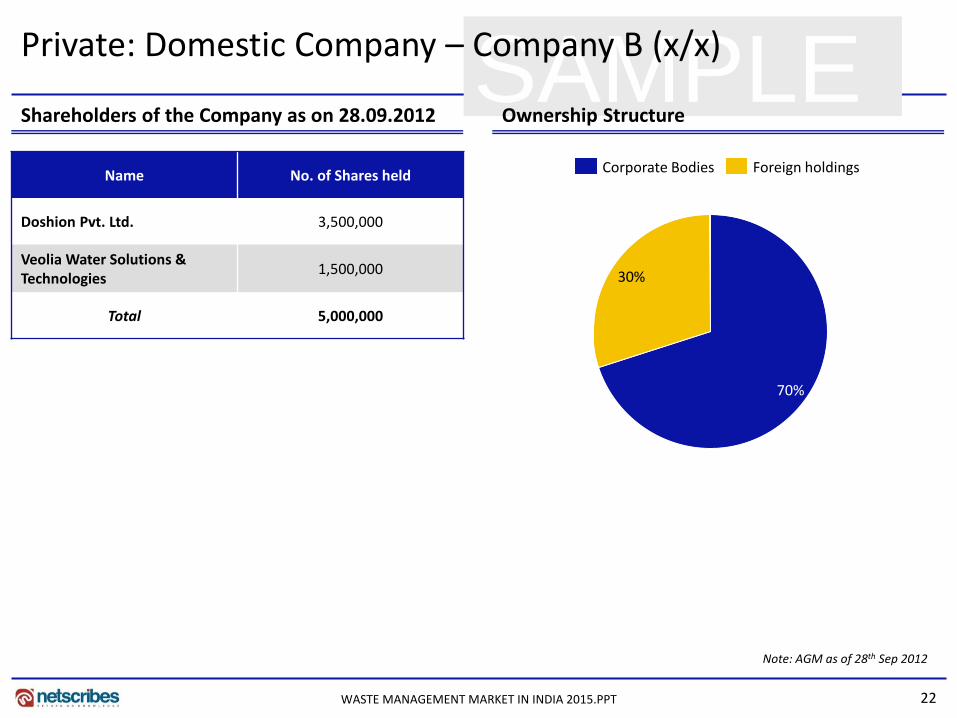

SAMPLE Shareholders of the Company as on 28.09.2012 Ownership Structure

Name No. of Shares held

Doshion Pvt. Ltd. 3,500,000

Veolia Water Solutions & Technologies

1,500,000

Total 5,000,000

30%

70%

Corporate Bodies Foreign holdings

Note: AGM as of 28th Sep 2012

Private: Domestic Company – Company B (x/x)

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

23

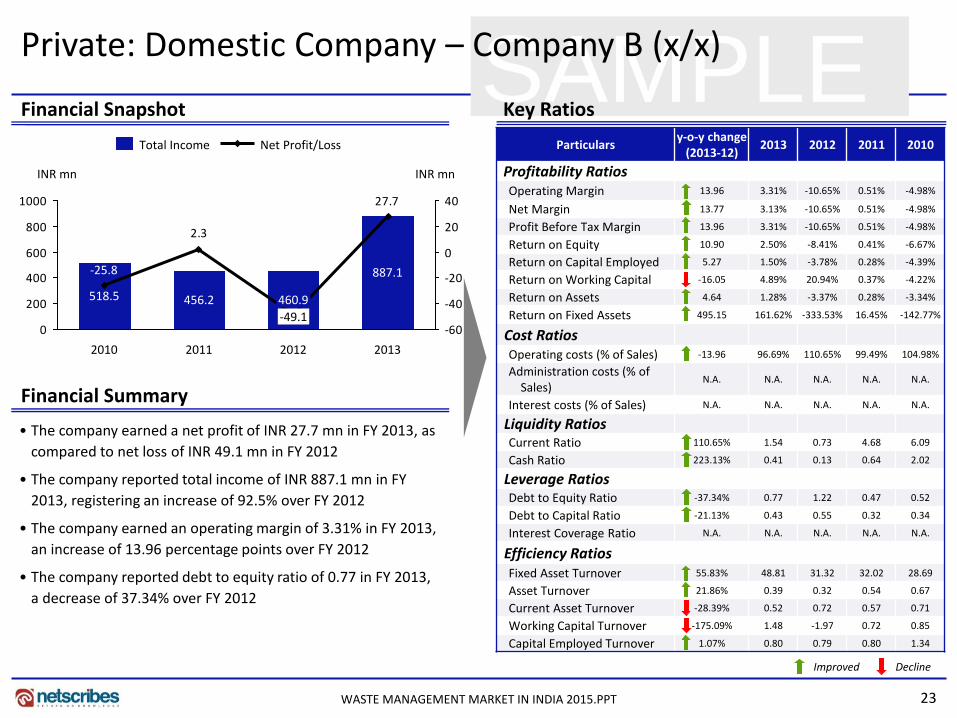

SAMPLE Financial Snapshot Key Ratios

Improved Decline

Financial Summary

• The company earned a net profit of INR 27.7 mn in FY 2013, as

compared to net loss of INR 49.1 mn in FY 2012

• The company reported total income of INR 887.1 mn in FY

2013, registering an increase of 92.5% over FY 2012

• The company earned an operating margin of 3.31% in FY 2013,

an increase of 13.96 percentage points over FY 2012

• The company reported debt to equity ratio of 0.77 in FY 2013,

a decrease of 37.34% over FY 2012

Net Profit/Loss Total Income

27.7

2.3

0

200

400

600

800

1000

-60

-40

-20

0

20

40

INR mn INR mn

2013

887.1

2012

-49.1

460.9

2011

456.2

2010

-25.8

518.5

Private: Domestic Company – Company B (x/x)

Particulars y-o-y change

(2013-12) 2013 2012 2011 2010

Profitability Ratios Operating Margin 13.96 3.31% -10.65% 0.51% -4.98%

Net Margin 13.77 3.13% -10.65% 0.51% -4.98%

Profit Before Tax Margin 13.96 3.31% -10.65% 0.51% -4.98%

Return on Equity 10.90 2.50% -8.41% 0.41% -6.67%

Return on Capital Employed 5.27 1.50% -3.78% 0.28% -4.39%

Return on Working Capital -16.05 4.89% 20.94% 0.37% -4.22%

Return on Assets 4.64 1.28% -3.37% 0.28% -3.34%

Return on Fixed Assets 495.15 161.62% -333.53% 16.45% -142.77%

Cost Ratios Operating costs (% of Sales) -13.96 96.69% 110.65% 99.49% 104.98%

Administration costs (% of Sales)

N.A. N.A. N.A. N.A. N.A.

Interest costs (% of Sales) N.A. N.A. N.A. N.A. N.A.

Liquidity Ratios Current Ratio 110.65% 1.54 0.73 4.68 6.09

Cash Ratio 223.13% 0.41 0.13 0.64 2.02

Leverage Ratios Debt to Equity Ratio -37.34% 0.77 1.22 0.47 0.52

Debt to Capital Ratio -21.13% 0.43 0.55 0.32 0.34

Interest Coverage Ratio N.A. N.A. N.A. N.A. N.A.

Efficiency Ratios Fixed Asset Turnover 55.83% 48.81 31.32 32.02 28.69

Asset Turnover 21.86% 0.39 0.32 0.54 0.67

Current Asset Turnover -28.39% 0.52 0.72 0.57 0.71

Working Capital Turnover -175.09% 1.48 -1.97 0.72 0.85

Capital Employed Turnover 1.07% 0.80 0.79 0.80 1.34

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

24

SAMPLE Business Highlights

Description News

Overview XX

Network XX

Awards XX

Private: Domestic Company – Company B (x/x)

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

25

SAMPLE Private: Domestic Company – Company B – SWOT Analysis (5/5)

XX XX

XX XX

T O

W S

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT

26

Thank you for the attention

About Netscribes, Inc. Netscribes, Inc. is a knowledge-consulting and solutions firm with clientele across the globe. The company’s expertise spans areas of investment & business research, business & corporate intelligence, content-management services, and knowledge-software services. At its core lies a true value proposition that draws upon a vast knowledge base. Netscribes, Inc. is a one-stop shop designed to fulfil clients’ profitability and growth objectives.

Waste Management – India report is part of Netscribe’s Energy Industry Series. For any queries or customized research requirements, contact us at:

Disclaimer: This report is published for general information only. Although high standards have been used in the preparation, “Netscribes” is not responsible for any loss or damage arising from use of this document. This document is the sole property of Netscribes and prior permission is required for guidelines on reproduction.

Phone: +91 22 4098 7600 E-Mail: [email protected]

WASTE MANAGEMENT MARKET IN INDIA 2015.PPT