market potential for credit insurance

TRANSCRIPT

1

MARKET POTENTIAL FOR CREDIT INSURANCE

NOVEMBER 14, 2003

i NDICUS ANALYTICS B - 17 GREATER KAILASH ENCLAVE 2

New Delhi 110048, India HTTP://WWW.INDICUS.NET, [email protected], (91-11) 29222838/63

2

Chapter 1

Introduction and Summary

Background • Credit to households one of the fastest growing segments of the financial sector. • Households comprise:

– Individuals – Proprietorships – Partnerships – HUFs

– Cooperatives and religious organizations Household Credit • Household credit market has been growing rapidly through the eighties and nineties and

is expected to continue. This is due to:

– Demographics: high proportion of population among younger age groups in the country

– Fast expanding consumption opportunities in the post-1991 reform period • Banks have always been the key credit provider to households in the formal sector and

will continue to be so as is the case internationally • Household credit has been growing at about …. percent through the nineties and this

expected to continue through the next decade • Growth has been, and is expected to be, similar for bank loans as well as other types of

loans

Changes in Financial Liabilities of Household Sector

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1970-71 1975-76 1980-81 1985-86 1990-91 1995-96 2000-01

Rs. 10 Mill

Total Loans Bank Loans

3

This study • Focuses on Credit to individuals

– Personal loans for consumption purposes

– Proprietorships, partnerships etc., for commercial purposes • Provided by organized sector both for personal and commercial purposes • It includes any formal loans whose repayment is affected by the health/life conditions of

the key borrowing individual • Kinds of loans included in the study

– Personal loans for durables, housing, others such as education – Professionals, self-employed, owners of small and tiny industries, agriculturists, etc.

Key Objectives of the study

– To identify insights into market characteristics that enables Max New York Life (MNYL) to satisfy credit-life insurance requirements

– Size of the accessible credit insurance industry – Characteristics of various segments of the credit industry

– What industry professionals believe

– What are the consumers ‘openness’ levels towards credit-life insurance The Market Size

– The credit-market size considered includes:

– Providers of personal credit – Providers of credit for commercial purposes

– The ‘accessible’ market includes lenders that are not currently allied to major insurance firm

Providers of Personal Credit

– Commercial banks: include different kinds of Banks, large and small, public and private, Indian and foreign

– Public Sector: includes State Bank of India and its associate banks as well as other nationalized banks

– Private sector (Indian): This includes the newly set-up HDFC Bank and ICICI bank as well as many older private sector banks. The larger private sector banks are associated with insurance firms, and therefore cannot be considered to be ‘accessible’. However many private banks are still not affiliated with any insurance firm.

– Private sector (Foreign): Some foreign banks are quite large and associated with a high degree of dynamism in providing personal loans such as Citibank. However many others are predominantly oriented towards financing commercial and trade requirements

– Regional Rural Banks: are typically small banks that have a high degree of rural reach. They are also un-affiliated with insurance firms.

4

� Credit Card loans: are provided by all types of banks, however the credit card lending is not-reported separately but as a part of overall ‘personal loans’. This study therefore has not been able to include them as a separate entity.

– Non Banking Finance Companies (NBFCs)

– Non-Housing NBFCs: These financial institutions grew rapidly through the nineties, however due to competition from the banking sector their growth has slowed down. It is expected that they will not be important players in the future. However, many automobile companies have their own NBFCs and these may continue to have some importance in the future. Most NBFCs are unaffiliated with insurance firms, though a few are.

– Housing finance companies: A few HFCs have been quite strong and are growing rapidly such as HDFC. However, few smaller ones are likely to survive the competition from Banks. The smaller HFCs are also unaffiliated though the larger ones such as HDFC are.

– Corporate loans to employees: Large public sector firms as well as a few [private sector non-financial firms are large providers of loans to their employees. Most such companies are unaffiliated with insurance firms.

Providers of Credit for Commercial Purposes

– Commercial banks

– Public Sector – Private sector (Indian) – Private sector (Foreign) – Regional Rural Banks � Kisan Credit Cards: Kisan credit cards are designed to enable easy credit to farmers

from Scheduled Commercial Banks. However these loans are categorized as direct agriculture loans and have not been separately dealt with.

– Credit Societies/ Cooperatives: Cooperative, credit societies, self help groups, have been important players; however they are typically poorly managed and subject to stringent regulatory oversight. Though they are predominantly un-affiliated with insurance firms, partnering with these institutions will be a long-term process, as they are not known for their flexibility.

– State finance and other development corporations: Many state organizations provide credit for ‘development’ or ‘socially desirable’ purposes. These include to disadvantaged sections, small-scale industries, etc. These organizations are also not known for their flexibility or dynamism. If current trends continue, they will soon become insignificant players. However many are reported to be changing and may be open to partnering. However, it is reported that single-person-dependent loans are not a high share of their total outstanding.

Purposes of Credit

– Housing: Housing loans are a rapidly expanding segment and are likely to remain so for the foreseeable future.

– Automobiles, Education, Health and other personal: These are not reported individually and it is not possible to disentangle the various components of the ‘other personal loans’.

5

There is significant flexibility related to duration of loans. Typically however for health and other consumption purposes loans tend to be for about 2 years, for automobiles for two to five years, and for education from five to 20 years. All are secured loans.

– Commercial: Almost all commercial loans are secured loans and could be highly short term to 5 to 20 years. Generally commercial loans to individuals have a good repayment history.

Commercial Bank Loans for Housing, Durables, & Other: Characteristics – Public Sector: Well spread across country

– Private sector (Indian): Dynamic, expanding rapidly

– Private sector (Foreign): Concentrating on metros and ‘premium’ customers

– Regional Rural Banks: large rural spread but many are poorly run Average Account Size of All Personal Loans

Amt/Acc (Rs) 2001

Consumer Durables

Housing Rest of Personal All Personal

Public Sector Foreign Banks RRBs Private Indian Total

Housing Finance Institutions: Characteristics

– Both SCBs and HFCs

– SCBs also considered previously

– Many not affiliated with insurance companies

– But could potentially offer own credit-life products

– Possibility of alliance is open – Cost of providing credit-life products/service of critical importance

Non Banking Finance Corporations (non-housing): Characteristics

– Have suffered loss in market share from Banks in the past

– RRBs the most aggressive players in this segment

– Banks report durable and auto loans under ‘Durables’ and ‘Rest of Personal’ categories

– Not possible to disentangle market size cleanly

Calculating Market Size

– Use 2001 as base year as data are provisional or estimates for later years

– First estimate total possible market for credit-life

– But some of this is inaccessible

– Then estimate all ‘accessible’ market size

Problem in estimating market size

– Non availability of categorization of purpose from many sources

– Non uniformity in categorization of purpose from many sources

– Only broad numbers available for some (eg. RRBs)

6

– Inter FI lending: Possibility of double counting – Focus more on identification of accessible markets

– Estimations at a single point in time as well as relevant break-ups of sub-components have been conducted taking into consideration the above factors

Total Market Size: Personal Loans

Rs Mill., 2001

All Personal Loans (Rs.

'000,000) Housing Durables

Auto & Other

Personal

Bank

SBI Associates

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank

HFCs

NBFCs

Corporates

Total

Total Market Size: Commercial Loans

Rs Mill., 2001

Priority Sr. Direct

Agriculture Loans

Priority Sr. Small-scale

industries

Priority Sr. Road & Water Transport

Priority Sr.-Retail Trade

Priority Sr.-Small Business

Priority Sr.-Professional

& Self Empl.

Priority Sr.-Food Processing not incl. SSI

Priority Sr. -

Export Credit (Foreign Banks)

Bank Total

SBI Ass

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank Total

HFCs

NBFCs

Corporates

Total

Other sources of credit • Include

o State financial corporations

7

o Cooperatives at different levels • However market size cannot be estimated for this segment • Large amount of lending within these categories of institutions and also from

commercial banks to these institutions combined with poor reporting

– Receive loans from SCBs and others under ‘Agriculture’ or ‘Priority’ head

– Highly regulated

– Most have personnel with low financial skill-base

– Highly structured operations

– Many are re-appraising role in changing economy

– Almost all loans backed by tangible assets in the case of SFCs and also for many cooperative loans

Other Commercial Bank Credit: Characteristics of Priority Sector

– Priority sector lending constitutes about 40 percent of all SCB lending

– Large part for agriculture, SSIs, and for export – But significant amounts to:

– Professionals – Artisans

– Shop owners, restaurants

– Call this the non-conventional market

Key Issues in the Accessing of the Non-conventional Market

– Regulations, state and central government policies and procedures

– Openness of government and public functionaries to allying with non-public sector entities

– Marketing capability at state and sub-state level

– Lobbying abilities Accessibility: Banks

– Negligible-Low Accessibility

– Foreign Private Sector Banks – Larger Indian Private Sector Banks – SBI and Affiliates

– Low-Medium Accessibility

– Smaller non-SBI public sector (some do not have any current plans for insurance related product-lines)

– Poorly performing RRBs

– Medium-High Accessibility

– Better performing RRBs

– Smaller Indian Private Sector Banks

8

Accessibility: Housing Finance Companies

– Consistent long term fall

– Shares expected to be lower in coming years due to aggressive private SCBs

– Largest fall in market share of smaller players

– Possibility of accessing larger players low

– HDFC, GICHF, LICHF, Canfin, etc.

– Indicates falling long term potential for credit-life through HFCs Accessibility: Non Banking Finance Companies (non-housing)

– Medium-High:

– NBFCs associated with auto companies

– Smaller NBFCs such as Nidhis, etc.

– But falling size – Outstanding in 2003 in the region of Rs 80,000 mill (hire purchase and lease) Accessibility: Corporate Employee Loans

– Medium to High

– Have not normally partnered with FIs

– Do not have required financial skill-base

Accessibility: Cooperatives

– Low to Medium

– Need exists

– Not ‘attached’ to competing FIs

– But highly regulated – Not clear what permissions or procedures will be required Accessibility: SFCs

– Medium to High

– Significant part of credit not for consumption related loans

– Consider expanding scope to include credit-life to proprietorships as well

– Could cover:

– Professionals – Proprietorships – Artisans

– Disadvantaged sections

9

Accessible Market: Personal Loans

Rs Mill. 2001 Housing Durables

Auto & Other

Personal All Personal

Loans

Banks

SBI Ass

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank

HFCs

NBFCs

Corporates

Total

Accessible Market: Relevant Commercial Loans from Priority Sector Advances

Rs Mill. 2001

Priority Sr. Direct

Agriculture Loans

Priority Sr. Small-scale

industries

Priority Sr. Road & Water Transport

Priority Sr.-Retail Trade

Priority Sr.-Small Business

Priority Sr.-Professional

& Self Empl.

Priority Sr.-Food Processing not incl. SSI

Priority Sr. -

Export Credit (Foreign Banks)

Total (Relevant Priority Sector)

Banks

SBI Ass

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank

HFCs

NBFCs

Corporates

Total

10

Total Accessible Market: Banks, corporate, NBFCs etc.

Rs Mill. 2001

All Personal Loans (Rs. '000,000)

Total (Relevant Priority Sector) Total

Banks

SBI Ass

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank

HFCs

NBFCs

Corporates

Total

Total Accessible Market Size

– Total accessible market size of about Rs 1,555 Billion as of 2001

– Market has been growing at about 20% in early 2000s but is expected to grow by about 15% annually this decade

– Conservative estimates as this does not include those by SFCs, cooperatives etc.

– Avoid possibilities of double counting Characteristics of borrowers: SEC • Socio-Economic Classification (SEC A, B, C, D & E): SEC A indicates better incomes as

well as potential income than that for SEC B and so on. SEC categorization is based on a combination of education and occupation characteristics. Overall we find that

– Inclination to borrow is somewhat evenly divided between different SEC segments

– However typical size of loans varies

– The openness to credit-life insurance is not dependent upon SEC status of a person.

– However those in lower SECs had great difficulty in understanding the concept of SEC

– Financial institution representatives informally reported larger defaults and ‘fraudulent’ activity among lower SECs

Overall, it appears that SEC categorization should not form the basis of any credit-life marketing strategy Characteristics of borrowings: Geographic

– The southern region accounts for a large part of the total credit – Western and northern regions next in importance

– Eastern region least importance

11

– If economic growth is an indication, the importance of the western half of India is only going to increase.

– The western half includes the area starting from Punjab, Haryana, Delhi, Rajasthan, Gujarat, Maharashtra, Karnataka, Kerala and also Tamil Nadu and Andhra Pradesh.

The following two maps show the share of each state in India’s total (i) relevant priority sector credit and (ii) personal loans, by commercial banks. Darker shades in each represent a higher share. Note that despite lower populations the southern states top among all states in the share of total loans in both categories.

12

Inclinations of the consumers

– Surety and not investment/tax saving are of critical factor in insurance decisions of most – this also reflects need for credit-insurance

– Consumers are not necessary loyal to brands/past relationships – they are most concerned with price, range of options, and then with quality of services.

– Formal sources of information are of least importance – friends, family, colleagues tend to be the most preferred sources of information

Views towards credit-life insurance

– Consumers are on the whole positive about the idea of credit-life insurance

– Different types of consumers – across age, socio-economic profile, asset ownership, as well as family structure, all show relatively high levels of appreciation for the concept

13

– However premiums will be of critical importance

– The results suggest that one time premiums and large amounts not preferred – some preference for including credit-life insurance within the regular repayment structure

Cost of credit life

– Seven in ten consumers are open to purchasing credit life at a very low premium of Rs 20 for a Rs 1000 repayment (2 percent of the repayment).

– However this falls to three in ten if premium at 2% is continued but repayment amount is increased to Rs 10,000.

– When the premium amount is kept the same at Rs 5000 but the extra percentage paid for credit life is changed from 0.5 to 6% (Rs 25 to Rs 300) we find only a small fall in the preference for credit-life

– This implies that the rupee amounts will play a critical role in consumer acceptability

– That is, larger premiums could be charged as long as they are broken into small amounts Consumer characteristics and credit-life

– SEC profile: Higher SECs are more likely to prefer credit life insurance

– Asset Profile: The economically better off are somewhat more likely to purchase credit-life insurance

– Family type: Family type does not appear to play an important role in consumer preferences

– Household size: Those in larger households are somewhat less likely top prefer credit-life insurance.

Characteristics of Credit

– Average amounts: Vary considerably across types of consumer, institution, segment, etc.

– Time-profile: Time profile varies, but does not necessarily play a role directly in the attractiveness of credit-life services. The key determinant is the amount of the premium paid. Moreover, money illusion appears to play a role. That is, consumers do not prefer larger amounts (one time payments).

– NPAs: Most FI representatives were unaware of what percentage of their NPAs in their institution were due to death of the borrower.

– Expected growth: We expect a 15 percent annual growth in the different xomponents fo credit. This is also in line with what industry professionals feel. However some even expect growth to be in the range of 20 to 25 percent annually in the coming decade.

In informal discussions with both consumers as well as financial institution representatives we could not identify any of the above as a significant enough factor for basing a marketing strategy on. This was as Lenders views

– Senior and middle managers were all positive to the idea of credit-life insurance

– All believed that their institutions could potentially partner with other institutions

14

– However no one could categorically commit to the same – they considered this to be a decision that only the senior managers collectively could take

– For government entities partnering with an MNC might be an issue

– Believed that the key potential advantages were:

– Reduction of their risk profile

– Reduction in risk for consumer

– Did not think that their profits would be a key criteria for partnering

– However, a share of the credit-life premiums might smoothen decisions

– Lenders preferred the following types of loans the most for credit insurance services:

– Long-term loans especially greater than three years

– Short-term loans of large amounts

– (However consumers do not necessarily have such preferences)

– Some respondents were also in favor of compulsory coverage

– Emphasized importance of simple documentation for such a service

– Some preference for adding credit-life policies to new products not existing products as it may lead to confusion

Summary

• This is a large enough accessible market for a non-affiliated insurance firm • Accessing the bulk of the market would involve interacting with both the private and

public sector • However scales can best be achieved if public sector financial institutions are accessed. • The southern part of India is the largest market • Consumers suffer from ‘illusion’ and are more likely to be agreeable to pay high

premiums if it is broken into smaller parts • Though the better off consumers will be more willing to purchase credit-life, significant

shares of the less well off will be interested • Financial institutions will generally be open to the idea of partnering with other

institutions • But some concerns may be there in some public sector entities about partnering with

MNCs • Moreover death does not appear to be an important contributor to NPAs in the

perception of financial institution respondents. This may make it difficult to ally with them without some other incentive to partnering institution.

• Consumers would be more open to it as they are highly family oriented • The key marketing challenge is therefore less related to design of credit-life products and

more towards the creation of alliances with different types of lenders.

15

Chapter 2

Views of Financial Institutions’ Personnel

1. Background The idea behind involving Personnel from Financial Institutions was to get insights on: • Familiarity with credit life insurance • Personal views on credit life insurance • Their institution’s views on allying with insurance firms for such products • Appropriateness of institution’s openness level – whether the market is ‘ready’ • Perceived advantages and hindrances in offering such products Such an exercise is aimed at providing insights into the possibility of offering credit-life insurance through different types of financial institutions. The persons interviewed included Senior Managers/Managers from various types of Financial Institutions - Nationalised Banks, Cooperative Banks, Regional Rural Banks etc. The interviews were conducted in 2 states- Delhi and Madhya Pradesh. Representatives of the following classes of financial institutions were interviewed • Public Sector Bank (PSB) • Regional Rural Bank • Cooperative Bank • Housing Finance Bank • NBFC • Direct Sales Agent A set of questions was identified; respondents were then queried by way of a structured questionnaire (refer appendix 1). A prior appointment was fixed with representatives of financial institutions and an interviewer personally visited the offices to get responses to the questionnaire. In most cases a single question had to be verbally asked in different ways to gain an insightful enough answer (most respondents had a proclivity for single sentence responses).

16

2. Synopsis The brief summary of the responses is presented here. Most respondents were aware of the concept of credit-life insurance. However many were not aware of the details and also how it worked. They tended to be quite positively inclined to including credit-life as an add-on to their credit. For this purpose they were open to allying/partnering with other organizations. They also felt that their very senior management (which ultimately would take the partnering decision) would be open to alliances.

2.1 The loan procedure This question was aimed at understanding the criteria deployed by banks to assess the borrowers. All banks/ lending agencies have their own system of evaluation. The common criteria that emerge are: • Educational Qualifications • For Salaried class- Current salary, profile, status • For Business-Business reputation, Assets, Turnover • Credit repayment record • Family background • Minimum income level • Property- Whether house is rented or owned • Location of residence Most respondents sited at least 4 out of these as indispensable factors in assessing borrowers. Of these credit repayment record, family background (as also reflected in location of residence), salaries and occupation were the most critical. When pressed, it was difficult for respondents to clearly rank various factors in order of importance. 2.2 Risk factors All financial institutions take a risk when they lend, as there are always chances of non-repayment of loans. The questions were aimed at identifying risk factors encountered by a financial institution while lending and the precautions taken to mitigate these factors. None of the respondents were aware of the percentage distribution of NPAs due to various possible causes/risk factors. They were queried about the following risk factors: • Health problems • This is an important factor but most have backups in forms of collaterals/ guarantees to

recover the loan

17

• Generally there are no medical check ups of potential borrowers • Death • As death cannot be predicted it poses an obvious threat, especially in cases where one

key man runs the business • To lessen the risk some institutions specify age groups for lending. That is, many do not

provide loans to those above 60 years of age. • Most ask for collaterals/ security to recover loans • Loss of Income/ employment • Most individuals repay loans from current income • To lessen this risk all institutions conduct thorough checkups of individual’s and their

family’s backgrounds (as listed in ‘Loan procedure’ above) • Some institutions prefer government employees and some are averse to government

employees • Loans are generally extended to professionals who are highly qualified or who have

guarantors to take care of the loan • Most have not had any experiences of fraud cases, however fraud remains a perceived

risk • Many are also averse to provide loans to police, lawyers and politicians as sometimes it is

difficult to recover from them

2.3 NPA due to death This question helped find whether the organization has NPA (Non Performing Assets) due to death. As credit life insurance means insuring the person’s debts after his death it is important to understand this factor. Key findings: • Financial Institutions (FIs) have NPA but believe that death is not an important cause. • Most have collaterals/ security to recover NPAs • Some do not extend loans to persons beyond a specified upper age limit

2.4 Product segment: This question aims to identify the kinds of credit (product segments) that the respondents felt should be covered under credit life insurance. :

• Products involving large loan amounts such as

• Housing loans • Car loans • Educational loans

18

2.5 Tenure This question identifies time spans for loan repayment that the respondents felt should be covered under credit life insurance.

• Most favor long-term loans • Any loan for more than 3 years should be covered, since after 3 years predictions about

ability to repay are difficult • Short-term loans of a large amount are also favored 2.6 Acceptability of credit life insurance in India The idea was to utilize their better-informed perception in assessing the prospects of credit life insurance in India. According to the respondents: • Credit life insurance will be accepted • Reason- it would lead to family security and ease of mind • However, awareness has to be spread • Amount or % of premium should be minimal • Some FIs even want it to be made a part of policy so that all persons have to take it 2.7 Channels for distribution This question was aimed at understanding the distribution channels set up by FIs for credit disbursement. The responses reveal: • The bigger FIs and some smaller ones have their own channels in form of branches –

for example Canara Bank, Corporation Bank etc. • Few small FIs - Cooperative banks, Regional Rural Banks etc. have some tie ups for

distribution • But own channels remain the most prevalent across different types of institutions 2.8 Willingness to pay premium This question was asked to gain insights into whether persons would pay premium for availing credit life insurance. Most answers are: • Yes they would pay • Awareness/education has to be spread • Premium amount should be minimal

19

2.9 Critical persons The idea behind this question was to find who are the decision makers in the institution who could be approached for taking a decision regarding introduction of credit life insurance. The responses are: • In most cases it is the senior management that takes decisions • Most respondents feel that senior management would accept it • However, all raised queries about cost to the consumer and also the structuring of the

alliance 2.10 Key benefits This question aimed at understanding what would be the key benefits for the institution if it accepts credit life insurance. Following are identified as key benefits: • Ease of ‘selling’ credit- all say that it will ease the process of selling credit as it would

reduce the consumers perceived risk • Lower risk of credit repayment - all agree that it will reduce the risk involved for both

the borrower as well as the lender • Other potential benefits such as the financial institution’s share of the premium were not

considered to be important 2.11 Key success factors This question aimed at identifying the key factors that would help in ensuring acceptance and success of credit life insurance in India. The key success factors are: • Cost- should be minimal • Ease of access- should be very easily accessible, minimum documentation, hassle free • Product design- should involve options to choose from • Integrability with your range of credit products- this is considered very important by

most as it will benefit both clients as well as lenders • Interest in attaching with existing products – most believe that credit life insurance

should not be tried with existing products, as it would lead to confusion. Should be tried with new products

20

Chapter 3

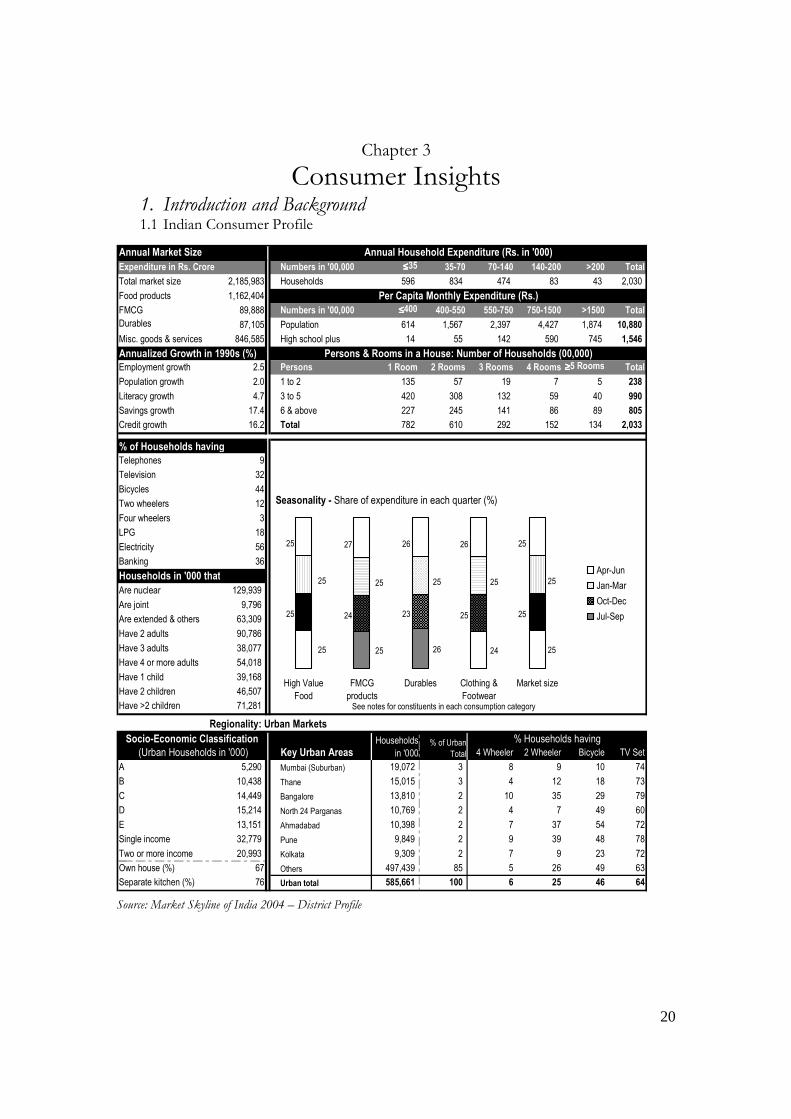

Consumer Insights 1. Introduction and Background 1.1 Indian Consumer Profile

1.2 1.3 1.4 1.5

Source: Market Skyline of India 2004 – District Profile Source: Market Skyline of India 2004 – District Profile

Annual Market Size

Numbers in '00,000 ≤≤≤≤35 35-70 70-140 140-200 >200 Total

Total market size 2,185,983 Households 596 834 474 83 43 2,030

Food products 1,162,404

FMCG 89,888 Numbers in '00,000 ≤≤≤≤400 400-550 550-750 750-1500 >1500 Total

Durables 87,105 Population 614 1,567 2,397 4,427 1,874 10,880

Misc. goods & services 846,585 High school plus 14 55 142 590 745 1,546

Annualized Growth in 1990s (%)

Employment growth 2.5 Persons 1 Room 2 Rooms 3 Rooms 4 Rooms ≥≥≥≥5 Rooms Total

Population growth 2.0 1 to 2 135 57 19 7 5 238

Literacy growth 4.7 3 to 5 420 308 132 59 40 990

Savings growth 17.4 6 & above 227 245 141 86 89 805

Credit growth 16.2 Total 782 610 292 152 134 2,033

% of Households having

Telephones 9

Television 32

Bicycles 44

Two wheelers 12

Four wheelers 3

LPG 18

Electricity 56

Banking 36

Households in '000 that

Are nuclear 129,939

Are joint 9,796

Are extended & others 63,309

Have 2 adults 90,786

Have 3 adults 38,077

Have 4 or more adults 54,018

Have 1 child 39,168

Have 2 children 46,507

Have >2 children 71,281 See notes for constituents in each consumption category

Regionality: Urban Markets

Key Urban Areas 4 Wheeler 2 Wheeler Bicycle TV Set

A 5,290 Mumbai (Suburban) 19,072 3 8 9 10 74

B 10,438 Thane 15,015 3 4 12 18 73

C 14,449 Bangalore 13,810 2 10 35 29 79

D 15,214 North 24 Parganas 10,769 2 4 7 49 60

E 13,151 Ahmadabad 10,398 2 7 37 54 72

Single income 32,779 Pune 9,849 2 9 39 48 78

Two or more income 20,993 Kolkata 9,309 2 7 9 23 72

Own house (%) 67 Others 497,439 85 5 26 49 63

Separate kitchen (%) 76 Urban total 585,661 100 6 25 46 64

Per Capita Monthly Expenditure (Rs.)

Persons & Rooms in a House: Number of Households (00,000)

Socio-Economic Classification Households

in '000% of Urban

Total

% Households having

(Urban Households in '000)

Annual Household Expenditure (Rs. in '000)

Expenditure in Rs. Crore

25 25 26 24 25

25 25 25 25 25

High Value

Food

FMCG

products

Durables Clothing &

Footwear

Market size

25 24 23 25 25

25 27 26 26 25

High Value

Food

FMCG

products

Durables Clothing &

Footwear

Market size

Seasonality - Share of expenditure in each quarter (%)

High Value

Food

FMCG

products

Durables Clothing &

Footwear

Market size

Apr-Jun

Jan-Mar

Oct-Dec

Jul-Sep

21

Table 1: Distribution of credit DISTRIBUTION OF CREDIT- MAJOR CITIES (New Delhi, Mumbai, Calcutta, Chennai, Pune,

Hyderabad, Bangalore)

SEC A SEC B SEC C SEC D SEC E Total

Housing

Durables

Personal

Residual

Total

Housing

Durables

Personal

Residual

Total Source: Estimates from NSSOs Large expenditure survey – 55th round

• Most credit is for ‘personal’ uses. This includes:

• Education • Consumption including marriages, festivals, ceremonies and health

requirements • Credit cards etc.

• Housing is the other key segment • The term ‘residual’ includes the unexplained part of total loans • There are few differences between different SEC groupings

Sample Size

• Total Respondents: 1660 • SEC classification

Table 2: Socio-economic classification

SEC Freq. Percent

A1

A2

B1

B2

C

Others

Total

• Most respondents belong to SEC A1, A2 and B1

22

• The sample captures a large share of young and middle aged persons

Table 3: Number of adults per family

Adults Freq. Percent

Missing

1

2

3

4

5

6

7

8

>8

Total

• Most respondents belong to families with 2 to 4 adult members

Figure 1: Age Distribution of Respondents

0

20

40

60

80

100

120

19 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60 62 64 66 71

Freq.

23

Table 4: Type of family

Family type Freq. Percent

Joint

Extended

Nuclear

Other

Total

• Joint families are those that contain more than one married sibling sharing a single

kitchen • Extended households include those where parents share a kitchen with a married

child • Largest sample is of members of nuclear families • Extended families are the next large set

Table 5: Ownership of house

House type Freq. Percent

Self

Rented

Total

• Most respondents own the house they live in

Table 6: Ownership of vehicles

Automobile Freq. Percent

4 Wheeler

2 Wheeler

Bicycle

None

Total

• The sample captures the well off • Almost half of the respondents own a 4 wheeler • Two-wheelers are owned by a large share of the respondents

24

Table 7: Motivation

Work motivation Percent

Work for my family’s happiness/comfort

Work for self-satisfaction/comforts

Total

• Family’s comfort and happiness is the predominant motivation for the bulk of the

respondents

2. Borrowing and Insurance Behavior Table 8: Type of insurance

Type of insurance

Life insurance

Accident insurance

Health insurance

Fire insurance

Calamities insurance

No

Yes

Missing

Total

• Most families / individuals have life insurance • Half do not have health insurance • Most prefer to have accident insurance • Fire and calamities insurance is held by few

Table 9: Motives for insurance

Motive for investment

Investment Tax savings Surety Family Pressure

Very important

Important

Less Important

Not Important

Missing

Total

• More than three fourths consider surety to be the most insurance factor for

insurance • Investment and tax savings are also considered to be important but this preference is

not as strong

25

• Family pressure was considered by most to be unimportant

Table 10: Criteria for insurance

Criteria for choosing the creditor

Low interest rate

Customer friendliness of creditor

Range of credit

terms/options

Past relationship

Ease of access of creditors

office

Very important

Moderately Important

Important

Less Important

Not Important

Missing

Total

• Low interest rates are the most important determinants of loan-scheme for almost

four fifths of the respondents • Customer friendliness and range of credit are next in importance

Table 11: Sources of information

Source of information on loans

Very important

Moderately Important Important

Less Important

Not Important Missing

Total

Friends or family

Office colleagues and associates

Prospective creditor

Other specialists

Internet search

Magazines and books

Advertisement

Other (Specify)

• Relations, friends, office colleagues and associates are considered to be very

important sources of information by most respondents • Formal sources of information are not as important • However information from the creditor is next in importance • Media is not considered a very important source of information by most

26

3. Views on Credit Insurance

3.1 Policy Preference 1

Table 12: Preference for credit-life Sec 1020 with

credit-life is preferred to 1000 w/out credit life

3060 with credit-life is preferred to 3000 w/out credit life

5100 with credit-life is preferred to 5000 w/out credit life

7650 with credit-life is preferred to 7500 w/out credit life

10200 with credit-life is preferred to 10000 w/out

credit life

Total

• At minimal premiums credit-life insurance is preferred by more than 70 percent • Each of the options above imply a marginal credit life premium of 2% over the total

premium • Note the large fall in percentage preferring credit life as the basic amount increases • This suggests that large money amounts are not preferred • A large number of respondents were found to be in favor of credit life in this set of

queries • More importantly, amount matters much more than percentage; that is, consumers

may be willing to pay more as long as amount of extra premium paid is not large

Table 13: Preference for credit-life Sec 1020 with

credit-life is preferred to 1000 w/out credit life

3060 with credit-life is preferred to 3000 w/out credit life

5100 with credit-life is preferred to 5000 w/out credit life

7650 with credit-life is preferred to 7500 w/out credit life

10200 with credit-life is preferred to 10000 w/out

credit life

A1

A2

B1

B2

Others

Total

• Higher SECs are more likely to prefer credit-life • However even the lower SECs have some preference for the same

27

Table 14: Number of adults per family

Adults 1020 with

credit-life is preferred to 1000 w/out credit life

3060 with credit-life is preferred to 3000 w/out credit life

5100 with credit-life is preferred to 5000 w/out credit life

7650 with credit-life is preferred to 7500 w/out credit life

10200 with credit-life is preferred to

10000 w/out

credit life

Missing

1

2

3

4

5

6

7

8

Total

• Larger families lead to lesser need for insurance • This is because larger families tend to self-insure implicitly

Table 15: Type of family

Family type 1020 with credit-life is preferred to 1000 w/out credit life

3060 with credit-life is preferred to 3000 w/out credit life

5100 with credit-life is preferred to 5000 w/out credit life

7650 with credit-life is preferred to 7500 w/out credit life

10200 with credit-life is preferred to 10000 w/out

credit life

Joint

Extended

Nuclear

Other

Total

• Family type is less important than family size • Other factors such as automobile ownership or home ownership (proxies for

economic class) have no significant impact on credit-life insurance • Neither does age have a significant impact on proclivity towards credit-life except for

those above 60 years of age

28

Chapter 4

Market Size

Synopsis & Insights

Background

Different components of the formal credit market are studied in this section. These include: • Housing finance • Consumer durables finance • Automobile finance • Employee loans • Personal loans • Priority Sector lending by Banks • Loans by State Finance Corporations and Cooperatives Of these the last are not included in the calculation of overall market sizes due to significant lending between different financial institutions. There inclusion could lead to double counting. Market Size Market sizes have been calculated from information contained in various parts of this chapter. This has been done at a company/institution-level basis in the accompanying MS Excel spreadsheet. The Market Size includes

– The credit-market size considered includes:

– Providers of personal credit

– Providers of credit for commercial purposes

– The ‘accessible’ market includes lenders that are not currently allied to major insurance firm

29

Providers of Personal Credit

– Commercial banks: include different kinds of Banks, large and small, public and private, Indian and foreign

– Public Sector: includes State Bank of India and its associate banks as well as other nationalized banks

– Private sector (Indian): This includes the newly set-up HDFC Bank and ICICI bank as well as many older private sector banks. The larger private sector banks are associated with insurance firms, and therefore cannot be considered to be ‘accessible’. However many private banks are still not affiliated with any insurance firm.

– Private sector (Foreign): Some foreign banks are quite large and associated with a high degree of dynamism in providing personal loans such as Citibank. However many others are predominantly oriented towards financing commercial and trade requirements

– Regional Rural Banks: are typically small banks that have a high degree of rural reach. They are also un-affiliated with insurance firms.

– Credit Card loans: are provided by all types of banks, however the credit card lending is not-reported separately but as a part of overall ‘personal loans’. This study therefore has not been able to include them as a separate entity.

– Non Banking Finance Companies (NBFCs)

– Non-Housing NBFCs: These financial institutions grew rapidly through the nineties, however due to competition from the banking sector their growth has slowed down. It is expected that they will not be important players in the future. However, many automobile companies have their own NBFCs and these may continue to have some importance in the future. Most NBFCs are unaffiliated with insurance firms, though a few are.

– Housing finance companies: A few HFCs have been quite strong and are growing rapidly such as HDFC. However few smaller ones are likely to survive the competition from Banks. The smaller HFCs are also unaffiliated though the larger ones such as HDFC are.

– Corporate loans to employees: Large public sector firms as well as a few private sector non-financial firms are large providers of loans to their employees. Most such companies are unaffiliated with insurance firms.

Providers of Credit for Commercial Purposes

– Commercial banks

– Public Sector

– Private sector (Indian)

– Private sector (Foreign)

– Regional Rural Banks

– Kisan Credit Cards: Kisan credit cards are designed to enable easy credit to farmers from Scheduled Commercial Banks. However these loans are categorized as direct agriculture loans and have not been separately dealt with.

30

– Credit Societies/ Cooperatives: Cooperative, credit societies, self help groups, have been important players; however they are typically poorly managed and subject to stringent regulatory oversight. Though they are predominantly un-affiliated with insurance firms, partnering with these institutions will be a long-term process, as they are not known for their flexibility.

– State finance and other development corporations: Many state organizations provide credit for ‘development’ or ‘socially desirable’ purposes. These include to disadvantaged sections, small-scale industries, etc. These organizations are also not known for their flexibility or dynamism. If current trends continue, they will soon become insignificant players. However many are reported to be changing and may be open to partnering. However, it is reported that single-person-dependent loans are not a high share of their total outstanding.

Purposes of Credit

– Durables: Consumer durables

– Housing: Housing loans are a rapidly expanding segment and are likely to remain so for the foreseeable future.

– Automobiles, Education, Health and other personal: These are not reported individually and it is not possible to disentangle the various components of the ‘other personal loans’. There is significant flexibility related to duration of loans. Typically however for health and other consumption purposes loans tend to be for about 2 years, for automobiles for two to five years, and for education from five to 20 years. All are secured loans.

– Commercial: Almost all commercial loans are secured loans and could be highly short term to 5 to 20 years. Generally commercial loans to individuals have a good repayment history.

Commercial Bank Loans for Housing, Durables, & Other: Characteristics

– Public Sector: Well spread across country

– Private sector (Indian): Dynamic, expanding rapidly

– Private sector (Foreign): Concentrating on metros and ‘premium’ customers

– Regional Rural Banks: large rural spread but many are poorly run What SCBs lend for

– Durables: Includes consumer durables, PCs, etc

– Housing: Housing purchase, repair and construction

– Other Personal

– Credit Cards

– Automobiles

– Education, Health Etc.

– Not all SCBs follow exactly same categorization

31

Average Account Size of All Personal Loans Amt/Acc (Rs) 2001

Consumer Durables

Housing Rest of Personal All Personal

Public Sector Foreign Banks RRBs Private Indian Total

Housing Finance Institutions: Characteristics

– Both SCBs and HFCs

– SCBs also considered previously

– Many not affiliated with insurance companies

– But could potentially offer own credit-life products

– Possibility of alliance is open

– Cost of providing credit-life products/service of critical importance

– Non Banking Finance Corporations (non-housing): Characteristics

– Have suffered loss in market share from Banks in the past

– RRBs the most aggressive players in this segment

– Banks report durable and auto loans under ‘Durables’ and ‘Rest of Personal’ categories

– Not possible to disentangle market size cleanly

Calculating Market Size

– Use 2001 as base year as data are provisional or estimates for later years

– First estimate total possible market for credit-life

– But some of this is inaccessible

– Then estimate all ‘accessible’ market size Problem in estimating market size

– Non availability of categorization of purpose from many sources

– Non uniformity in categorization of purpose from many sources

– Only broad numbers available for some (eg. RRBs)

– Inter FI lending: Possibility of double counting

– Focus more on identification of accessible markets

– Estimations at a single point in time as well as relevant break-ups of sub-components have been conducted taking into consideration the above factors

32

Total Market Size: Personal Loans

Rs Mill., 2001

All Personal Loans (Rs.

'000,000) Housing Durables

Auto & Other

Personal

Bank

SBI Associates

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank

HFCs

NBFCs

Corporates

Total

Total Market Size: Commercial Loans

Rs Mill., 2001

Priority Sr. Direct

Agriculture Loans

Priority Sr. Small-scale

industries

Priority Sr. Road & Water Transport

Priority Sr.-Retail Trade

Priority Sr.-Small Business

Priority Sr.-Professional

& Self Empl.

Priority Sr.-Food Processing not incl. SSI

Priority Sr. -

Export Credit (Foreign Banks)

Bank Total

SBI Ass

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank Total

HFCs

NBFCs

Corporates

Total

Other sources of credit: State financial corporations

– Cooperatives at different levels

– However market size cannot be estimated for this segment

– Large amount of inter-lending with these categories of institutions and also from commercial banks to these institutions

– Difficult to make an estimate

33

Credit Societies/Cooperatives: Characteristics

– Receive loans from SCBs and others under ‘Agriculture’ or ‘Priority’ head

– Highly regulated

– Most have personnel with low financial skill-base

– Many not viable in the medium-long term

– Include

– The Primary Agricultural Co-operative Societies – District Central Co-operative Banks – State Co-operative Banks – Comparative Share of Co-operative Banks vis-a-vis SCBs

State -Level Finance Corporations: Characteristics

– State financial corporations

– Institutions oriented towards disadvantaged sections

– Development institutions such as tourism development

– Highly structured operations

– Many are re-appraising role in changing economy State -Level Finance Corporations: Provide credit to

– Companies

– Proprietorships and Partnerships

– Professionals

– Artisans

– Deprived sections

– Credit predominantly for ‘productive purposes’

– Also includes that for

– Automobiles – Housing

– Other assets: Shops, restaurants, cattle etc.

– Almost all loans backed by tangible assets Other Commercial Bank Credit: Characteristics of Priority Sector

– Priority sector lending constitutes about 40 percent of all SCB lending

– Large part for agriculture, SSIs, and for export

– But significant amounts to:

– Professionals

– Artisans

– Shop owners, restaurants

34

Key Issues in the Accessing of the Non-conventional Market

– Regulations, state and central government policies and procedures

– Openness of government and public functionaries to allying with non-public sector entities

– Marketing capability at state and sub-state level

– Lobbying abilities

Accessibility: Banks

– Negligible-Low Accessibility

– Foreign Private Sector Banks

– Larger Indian Private Sector Banks

– SBI and Affiliates

– Low-Medium Accessibility

– Smaller non-SBI public sector (some do not have any current plans for insurance related product-lines)

– Poorly performing RRBs

– Medium-High Accessibility

– Better performing RRBs

– Smaller Indian Private Sector Banks Accessibility: Housing Finance Companies

– Consistent long term fall

– Shares expected to be lower in coming years due to aggressive private SCBs

– Largest fall in market share of smaller players

– Possibility of accessing larger players low

– HDFC, GICHF, LICHF, Canfin, etc. – Indicates falling long term potential for credit-life through HFCs

Accessibility: Non Banking Finance Companies (non-housing)

– Medium-High

– NBFCs associated with auto companies – Smaller NBFCs such as Nidhis, etc. – But falling size

– Outstanding in 2003 in the region of Rs 80,000 mill (hire purchase and lease) Accessibility: Corporate Employee Loans

– Medium to High

– Have not normally partnered with FIs

– Do not have required financial skill-base

35

Accessibility: Cooperatives

– Low to Medium

– Need exists

– Not ‘attached’ to competing FIs

– But highly regulated

– Not clear what permissions or procedures will be required Accessibility: SFCs

– Medium to High

– Significant part of credit not for consumption related loans

– Consider expanding scope to include credit-life to proprietorships as well

– Could cover:

– Professionals

– Proprietorships

– Artisans

– Disadvantaged sections

Accessible Market: Personal Loans

Rs Mill. 2001 Housing Durables

Auto & Other

Personal All Personal

Loans

Banks

SBI Ass

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank

HFCs

NBFCs

Corporates

Total

36

Accessible Market: Relevant Commercial Loans from Priority Sector Advances

Rs Mill. 2001

Priority Sr. Direct

Agriculture Loans

Priority Sr. Small-scale

industries

Priority Sr. Road & Water Transport

Priority Sr.-Retail Trade

Priority Sr.-Small Business

Priority Sr.-Professional

& Self Empl.

Priority Sr.-Food Processing not incl. SSI

Priority Sr. -

Export Credit (Foreign Banks)

Total (Relevant Priority Sector)

Banks

SBI Ass

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank

HFCs

NBFCs

Corporates

Total

Total Accessible Market: Banks, corporate, NBFCs etc.

Rs Mill. 2001

All Personal Loans (Rs. '000,000)

Total (Relevant Priority Sector) Total

Banks

SBI Ass

Nationalized

Indian Pvt

Foreign

RRBs

Non Bank

HFCs

NBFCs

Corporates

Total

Total Accessible Market Size

– Total accessible market size of about Rs 1,555 Billion as of 2001

– Market has been growing at about 20% in early 2000s but is expected to grow by about 15% annually this decade

– Conservative estimates as this does not include those by SFCs, cooperatives etc.

– Avoid possibilities of double counting

37

I. Housing Finance

1. Data Description The Housing Finance (HF) industry in India has two major segments consisting of Scheduled Commercial Banks (SCBs) and specialized Housing Finance Companies (HFCs). While there is a significant amount of data available for the SCBs, the data on HFCs is limited. Two sources of data have been used for this analysis: (1) Reserve Bank of India and (2) Annual accounts of the major HFCs. (1) The RBI data coverage is in three parts for the years ending March 31st in 2000, 2001 and 2002.

(i) An occupational classification of bank credit gives a state-wise break-up of credit going to different sectors, by different types of scheduled commercial banks. The data is further broken up for each state, but for the purposes of this analysis we use a regional classification (See Appendix II).

(ii) The Scheduled Commercial Bank’s advances under Priority Sector (2000 and 2001) gives a statewise (regional) break-up of credit given by the banks either directly or indirectly. Indirect credit is typically through HFCs where the banks lend to HFCs against an earmarked portfolio of accounts.

(iii) State and Population Group wise Classification of Outstanding Credit of Small Borrowal Accounts of Scheduled Commercial Banks According to Occupation

The RBI data has a hierarchical structure; (ii) is a subset of (i) and (iii) is a sub-set of (ii). While for all market related analysis, we rely on data from (i), we also provide an analysis of data from (ii) and (iii) to give an idea of the characteristics of the different market segments. (2) Annual financial statements of 15 HFCs for 5 years 1998 – 2002. (3) CRIS INFAC Retail Finance Annual Review: January 2003. 2 Formal Credit In The Housing Finance Sector

2.1 Market Size Of The Housing Finance Sector

The HF industry has been growing at a healthy CAGR, estimated to be in the 25-30% range. While market size can be defined in many ways – annual sanction, annual disbursement of housing loans, outstanding credit for housing purposes, we define the market as the stock of outstanding loans to the housing sector. The size is estimated as follows: (Housing Loans O/S for HFCs – Bank Borrowings by HFCs) + SCB O/S Housing Loans

38

Table 1: Select Financials Of 15 Housing Finance Companies In India, 1998-2002 (Amount in Rs. bill.)

Select Financials for HFCs (from B/S)* 1998 1999 2000 2001 2002

Networth

Borrowings

Banks

Financial Institutions

Foreign

Bonds/Debentures

Fixed Deposits

Housing Loans

YOY Growth (%) Source: Financial Statements of HFCs (Prowess, CMIE)

* A list of the HFCs whose financials are reported here is given in Appendix 1

Table 2: Estimate Of Housing Finance Market Size, 2000-2002 (Amount in Rs. bill.)

Market Size Estimate 2000 2001 2002

HFC Housing Loans O/S A

Bank borrowing by HFCs B

Net Housing Loans by HFCs (A) - (B) = C

Housing Loans O/S for SCBs D

Market Size (C) + (D)

YOY Growth in Market Size (%)

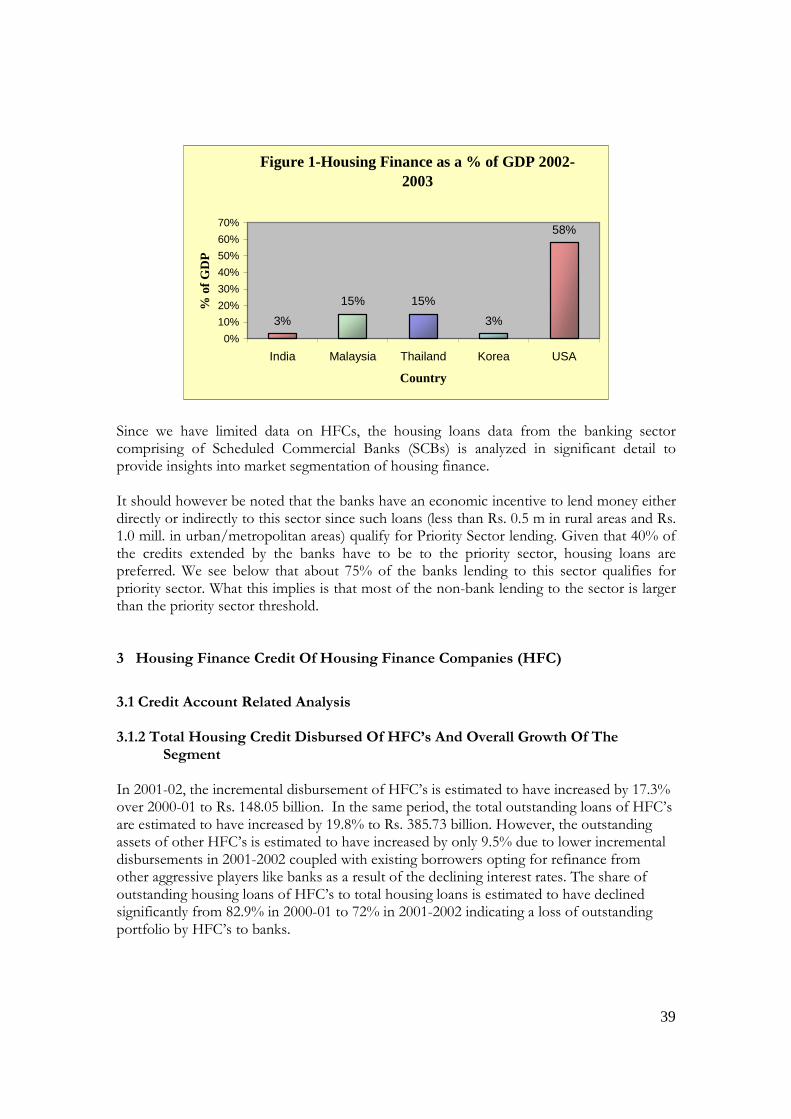

A market size of approximately Rs. 525 billion translates to about 3% of the country’s GDP, which is small in comparison to other countries (see Fig 1). It is useful to bear in mind that the housing finance market is comparatively young in India. According to CRISIL, the housing finance market enjoys a market share of 52% in the key retail finance market. In existence for over two decade, the buoyancy of the market is a recent phenomenon, in the last 3-4 years. The tax incentives for owner occupied homes under section 88 of the IT Act, combined with the reduction in the interest rates gave a fillip to the market in recent years. The size of the new mortgages sanctioned and the amounts disbursed have grown much faster than the housing loans outstanding, suggesting that a large proportion of the housing loans were refinanced due to the significant fall in the interest rates. For instance, during the financial year 2001 housing loans disbursement for HDFC was Rs. 58.03 billion while its loan outstanding rose by Rs. 31.5 billion. Also, for the financial year 2002, the corresponding figures were Rs. 76.17 billion and Rs. 39.83 billion respectively.

39

Figure 1-Housing Finance as a % of GDP 2002-2003

3%

15% 15%

3%

58%

0%

10%

20%

30%

40%

50%

60%

70%

India Malaysia Thailand Korea USA

Country

% o

f G

DP

Since we have limited data on HFCs, the housing loans data from the banking sector comprising of Scheduled Commercial Banks (SCBs) is analyzed in significant detail to provide insights into market segmentation of housing finance. It should however be noted that the banks have an economic incentive to lend money either directly or indirectly to this sector since such loans (less than Rs. 0.5 m in rural areas and Rs. 1.0 mill. in urban/metropolitan areas) qualify for Priority Sector lending. Given that 40% of the credits extended by the banks have to be to the priority sector, housing loans are preferred. We see below that about 75% of the banks lending to this sector qualifies for priority sector. What this implies is that most of the non-bank lending to the sector is larger than the priority sector threshold. 3 Housing Finance Credit Of Housing Finance Companies (HFC)

3.1 Credit Account Related Analysis 3.1.2 Total Housing Credit Disbursed Of HFC’s And Overall Growth Of The

Segment

In 2001-02, the incremental disbursement of HFC’s is estimated to have increased by 17.3% over 2000-01 to Rs. 148.05 billion. In the same period, the total outstanding loans of HFC’s are estimated to have increased by 19.8% to Rs. 385.73 billion. However, the outstanding assets of other HFC’s is estimated to have increased by only 9.5% due to lower incremental disbursements in 2001-2002 coupled with existing borrowers opting for refinance from other aggressive players like banks as a result of the declining interest rates. The share of outstanding housing loans of HFC’s to total housing loans is estimated to have declined significantly from 82.9% in 2000-01 to 72% in 2001-2002 indicating a loss of outstanding portfolio by HFC’s to banks.

40

3.1.2 Number And Average Size Of Accounts Financing from HFC’s are generally in the form of term loans. During the 1998-99 to 2001-02 period, the average size of the retail loan is estimated to have increased from Rs. 152,000 to Rs. 225,000, a CAGR of 18.9%. In 2001-02 the average loan size of HDFC was Rs. 357,500, an increase of 10.9% over the previous year 2000-01. The number of housing loans disbursed by HDFC increased by 18.3% to 213,000. The average loan size of LIC Housing Finance and Dewan Housing Finance was Rs. 313,500 and Rs. 224,400. Housing finance companies while sanctioning loans give higher credit to households having more than one earning member and sanctions loan amounts upto a maximum of 36 months of average household income. HFC’s finance loans upto a limit of 85% and in select construction projects upto 100% of the value of the house. 3.1.3 Average Tenure Most HFC’s offer housing loans for a period of 15-20 years. During the 1996-2002 periods, the tenure of loans available increased from 7-10 years to 20-30 years. However the average tenure of loan at origination ranges from 10-14 years, while the average duration of outstanding loans is 7-8 years. Interest rates for shorter tenure loans (below 5 years) are lower than longer tenure loans (15 years and above) by 75-175 basis points. 3.1.4 Average EMI During the 1995-1996 period, the EMI on housing loans is estimated to have declined by almost 50%. The EMI on a 20-year loan at 8.5% interest is Rs. 870 per and on a 7 year, loan at 18% interest is approximately Rs. 1590). 3.2 Analysis Of The Competitive Scenario Of The HFC Segment 3.2.1 Major Players In The HFC Segment There are approximately 350 HFC’s in India of which only 31 are approved and registered with the NHB for refinancing. The major players are:

• Housing Development Finance Corporation

• Life Insurance Company Housing Finance

• General Insurance Company Housing Finance

• Dewan Housing Finance Corporation Ltd.

• Canfin Homes Ltd.

3.2.2 Current Performance Of The HFC Players In 2001-02, the disbursements of HFC’s like HDFC, LIC Housing Finance and Canfin Homes increased by 31.3%, 25.5% and 28% respectively over 2000-01.

41

3.2.3 Credit Ratings Of The HFC’s Credit ratings of the major HFC’s are listed below. See Appendix IV for a detailed list of credit ratings for all HFC’s.

• Housing Development Finance Corporation-AAA (CRISIL)

• Life Insurance Company Housing Finance-AAA (CRISIL)

• General Insurance Company Housing Finance-AA (CARE)

• Dewan Housing Finance Corporation Ltd.-AA (CARE, Fitch)

• Canfin Homes Ltd.-A+ (CRISIL) 3.2.4 Non Performing Assets (NPA) of HFC The average gross NPA of the industry is estimated at 2-2.5% of the outstanding portfolio. However, it varies between 1-5%. In 2001-02, gross NPA of HDFC was .91% of the portfolio. The industry credit loss is determined at 20-40 basis points 3.2.5 Market Share Of The HFC’s Table 3: Incremental Disbursements Of The HFC’s In The Housing Finance Sector (Rs. bill.)

Particulars 1998-99 1999-00 2000-01 2001-02

HDFC LICHF

GICHF Dewan HF Canfin Homes

Other HFCs All HFCs

Source: CRIS INFAC Retail Finance Annual Review: January 2003

Table 4: Outstanding Loans Of HFC’s In The Housing Finance Sector

(Rs. bill.) Particulars 1998-99 1999-00 2000-01 2001-02

HDFC

LICHF

GICHF Dewan HF Canfin Homes

Other HFCs All HFCs Source: CRIS INFAC Retail Finance Annual Review: January 2003

In 2001-02, the aggregate market share of all HFC’s in aggregate retail disbursements declined by 9.1% to 59.2%. Most of the HFC’s have lost their market share to the banks. However, the largest loosing segment has been the small and medium sized HFC’s with a loss of 7.2% in market share. The market share of small and medium HFC’s declined from

42

25% in 2000-01 to 17.8% in 2001-02. Market share of HDFC declined from 31.4% in 2000-01 to 30.5% in 2001-02. 4. Commercial Banks In Housing Finance 4.1 Market Size And Growth Of Housing Finance From Banks, 2000-2002

Table 5: Total Outstanding Of Housing Loan By Scheduled Commercial Banks

Particulars 2000 2001 2002 Total Outstanding (Rs. bill.) Total Accounts Amount Per Account (Rs. mill.) Growth in O/s (Rs. bill.) Growth Rate in Total O/s (%)

Source: Reserve Bank of India data on State and Bank Group-wise Classification of Outstanding Credit of Scheduled Commercial Banks According to Occupation

4.2 Outstanding Housing Credit By Type Of Scheduled Commercial Banks Table 6: Outstanding Housing Credit And Market Share By Type Of SCBs - 2000-

2002

(Rs. mill. / (%)

Outstanding Loans/Market Share 2000 2001 2002

SBI & Associates

Nationalized banks

Other SCB

Foreign Banks

RRB

All SCB

Source: Reserve Bank of India data on State and Bank Group-wise Classification of outstanding Credit of Scheduled Commercial Banks According

• Table 6 shows that the nationalized banks along with State Bank of India and Associates (SBI) dominate 80% of the market for housing finance in India. Between 2000 and 2001, SBI has gained market share at the expense of the Nationalized banks

43

Figure 2-Bank Groupwise Housing Loan Outstanding Per Account

00.10.20.30.40.50.60.70.8

SB

I & A

ss

Nat

iona

lised

bank

s

For

eign

Ban

ks

RR

B

Oth

er S

CB

Bank Group

Am

ou

nt

O/s

per

Acc

ou

nt

(Rs

mn

) 2000

2001

2002

Source: Reserve Bank of India data on State and Bank Group-wise Classification of outstanding Credit of

Scheduled Commercial Banks According to Occupation

• The quantum of housing loan disbursed per account, is the highest for foreign banks as compared to other bank groups as shown in Figure 2 above although their market share has remained in the 6-8% bracket in the period 2000-2002.

Table 7: Region Wise Market Share Each Bank Type In Outstanding Housing Credit For 2002 (in %)

Region/Bank SBI & Associates

Nationalized Banks

Foreign Banks

RRB Other SCB

All Banks

Northern region North-eastern region Eastern region Central region Western region Southern region

All India Source: Reserve Bank of India data on State and Bank Group-wise Classification of outstanding Credit of Scheduled Commercial

Banks According to Occupation

Table 8: Bank Wise Market Share In Each Region For Outstanding Housing Credit, 2002 (in %)

Region/ Bank SBI & Associates

Nationalized Banks

Foreign Banks

RRB Other SCB

All Banks

Northern region North-eastern region Eastern region Central region Western region Southern region All India Source: Reserve Bank of India data on State and Bank Group-wise Classification of outstanding Credit of Scheduled Commercial Banks According to Occupation

44

Table 9: Bank-Wise Market Share In Each Population Group For Outstanding

Housing Credit-2002 (in %)

SBI & Nationalized Foreign RRB Other All SCB

Population Groups Associates Banks Banks SCB

Rural

Semi-Urban

Urban

Metropolitan

All India Source: Reserve Bank of India data on Population and Bank Group wise classification of outstanding credit of Scheduled Commercial Banks

According to Occupation

• Amongst all SCB, SBI & Associates and Nationalized Banks together have over 70% of Housing Loan market share across each of the population group sectors for the year 2002, as can be seen from Table 9.

Table 10: Population Group-Wise Market Share Of Each Bank Type In Outstanding Housing Loan Credit For 2002 (in %)

SBI & Nationalized Foreign RRB Other All SCB

Population Groups Associates Banks Banks SCB

Rural

Semi-Urban

Urban

Metropolitan

All India Source: Reserve Bank of India data on Population and Bank Group wise classification of outstanding credit of Scheduled Commercial Banks

According to Occupation

Table 11: Commercial Banks In Housing Finance – The Population Group

Perspective (Amount in Rs. mill.)

2000 2001 2002

Population group Amount O/s Amt per Acc. Amount O/s Amt per Acc. Amount O/s Amt per Acc.

Rural

Semi Urban

Urban

Metropolitan

All India Source: Reserve Bank of India data on Population and Bank Group wise classification of outstanding credit of Scheduled

Commercial Banks According to Occupation

45

• Referring to Table 11, we observe that the Urban and Metropolitan group of the population together occupied 70% of the Housing Loan Market for the year 2002. We also see that each of the population group has more than doubled its loan per housing account in 2002 on comparison with data from 2000. What could possibly have helped such a steep rise?

5. Formal Credit in Housing Finance Sector By Location

5.1 Region-Wise Housing Loans Outstanding Between 2000-2002

• Referring to Table 12, we observe that the western and southern region enjoyed a market share of 59%-61% during 2002.

Table 12: Region-Wise Housing Loans Outstanding And Amount Outstanding Per

Housing Loan By All SCB

(Rs. mill.)

Particulars 2000 2001 2002

Regions Of India No. Of Accounts

Amount O/s

Amt. per Acc.

No. Of Accounts

Amount O/s

Amt per Acc.

No. of Accounts

Amount O/s

Amt per Acc.

Northern region

North eastern region

Eastern region

Central region

Western Region

Southern region

All India

Source: Reserve Bank of India data on State and Bank Group-wise Classification of outstanding Credit of Scheduled Commercial Banks According to Occupation

• Amount disbursed per loan has increased significantly between 2000 and 2002 in almost all the regions as can be seen from Table 12. The western region has grown the maximum in 2002 to an amount of Rs0.23m per account as shown in Table 12. This is probably due to the high property prices in Bombay.

• The loans per account is the highest in the western and southern regions which matches the previous observation of the two regions dominating almost 60% of market share in the period 2000-2002. Although the market share of the southern region is higher, the loans per account are lower than that of the western region. This highlights the existence of high property prices in Bombay, which is likely to dominate the regions’ demand for housing loans.

46

5.3 ‘Big Players’ State Wise Analysis

Table 13: Cumulative Market Share Of Housing Credit Of 10 Top States In % States

Cumulative Share, O/s States’ Market Share

Maharashtra Tamil Nadu Karnataka Andhra Pradesh Kerala Uttar Pradesh West Bengal Delhi Rajasthan Gujarat All India

Source: Reserve Bank of India data on State and Bank Group-wise Classification of outstanding Credit of Scheduled Commercial Banks According to Occupation

6. Priority Sector Lending Of Housing Credit Table 14: All India Housing Loan Advances Under Priority Sector 2000 And 2001

(Amount in Rs. mill.)

2000

Direct Finance Indirect Finance Total

No. of Accounts Amount O/s No. of Accounts

Amount O/s No. of Accounts

Amount O/s

2001

Direct Finance Indirect Finance Total

No. of Accounts Amount O/s No. of Accounts

Amount O/s No. of Accounts

Amount O/s

Source: Reserve Bank of India “ Scheduled Commercial Bank’s Advances under Priority Sector”

• The housing loan advances under priority sector, which stood at Rs. 123.59 bill. in the year 2000, rose by 68.71% for the following year. The growth can be accredited firstly to the direct housing finance segment which rose from Rs. 55.26 bill. in 2000 by a high 89.25% in 2001 and secondly to the indirect housing finance segment, which saw it’s outstanding reach Rs.103.93 bill. in year 2001- a growth of 52.10% over it’s previous year account.

• The percentage contribution to the overall outstanding by the direct housing finance under priority sector jumped from 44.71% in 2000 to 50.15% in 2001.

*Refer to Appendix III for definition of Priority Sector Lending

47

Table 15: Region Wise Amount Per Account For SCB’s Advances To Priority Sector (Amount in Rs. mill.)

2000 2001

Regions of India No. of Amount Amount No. of Amount Amount

Accounts Outstanding per account Accounts Outstanding per account

Northern Region

North-Eastern Region Eastern Region

Central Region

Western Region

Southern Region All India

Source: Reserve Bank of India “ Scheduled Commercial Bank’s Advances under Priority Sector”

• As we can see from Table 15, the Western region has a very high value for outstanding amount per housing loan under priority sector in comparison with the other regions for both the concerned years. The reason for this could be the presence of Mumbai and other industrial cities in this region.

• The only substantial change that can be seen for both segments of housing loans under priority sector for the concerned years has been from the southern region. An apparent loosening of hold of the market in this region is complemented by the western region’s increase in hold in these segments.

7. Non -Priority Sector Outstanding In The Housing Finance Sector

7.1 Definition & Features Of Small Borrowal Accounts In Housing Credit Sector

With reference to the ‘Basic Statistical Return of Scheduled Commercial Banks in India’- Volume 31, a home publication of Reserve Bank of India, all borrowal accounts with the credit limit of Rs. 2 lakh or less of all scheduled commercial banks including Regional Rural Banks, are classified as ‘small borrowal accounts’ or non-priority sector borrowals, from March 1999 survey onwards.

Non- Priority Sector O/S= All Bank Total O/S- Priority Sector O/S Table 16

Particulars 2000 2001

Total Outstanding (Rs. bill.) Total Accounts

Amount per Account (Rs. mill.) Source: Reserve Bank of India “ Scheduled Commercial Bank’s Advances under Priority Sector” and data on State and Bank

GroupWise Classification of O/S Credit of SCB’s.

48

II. Personal Loans 1. Data Description The personal loan (PL) segment of bank lending consists of loans given to individuals for unspecified purposes. This segment includes both “unsecured “ credit as well as credit “secured” against a variety of collateral- property, shares, other financial securities, etc. It is difficult to ascertain the purposes of these loans, but it is a growing segment of the consumer finance market. The only source of data used for this analysis is from the database of the Reserve Bank of India. The RBI data coverage is in three parts for the years ending March 31st in 2000, 2001 and 2002.

(i) An occupational classification of bank credit gives a state-wise break-up of credit going to different sectors, by different types of scheduled commercial banks. The data is further broken up for each state, but for the purposes of this analysis we use a regional classification.

(ii) Population group wise and Bank group wise classification of outstanding credit

of Scheduled Commercial Banks According to Occupation.

2. Commercial Banks In Personal Loan Segment 2.1 Market Size And Growth Of PL Credit From Banks, 2000-2002

Table 17: Total Outstanding In PL By Scheduled Commercial Banks

Particulars 2000 2001 2002

Total Outstanding (Rs. bill.)

Total Accounts

Amount per Account (Rs. mill.)

Growth in O/s (Rs. bill.)

Growth Rate in Total O/s (%) Source: Reserve Bank of India data on State and Bank Group Wise Classification of Outstanding Credit of Scheduled

Commercial Banks According to Occupation

• The PL sector has grown marginally by 1.465 between 2001-02 with corresponding growth in outstanding worth Rs. 20 billion approximately.

49

2.2 Outstanding PL Credit By Types Of Scheduled Commercial Banks, 2000-2002

Table 18: Outstanding Credit In PL Segment By Types Of SCB’s (2000-2002)

(Rs. mill.)

Outstanding Loans 2000 2001 2002

SBI &Associates

Nationalized Banks

Foreign Banks

RRB

Other SCB

All SCB Source: Reserve Bank of India data on State and Bank Group Wise Classification of Outstanding Credit of Scheduled

Commercial Banks According to Occupation

• Table 18 shows that for the period 2000-2002, there has been no significant shift in the market share of the different types of banks. About 65-70% of the personal loan market was dominated by SBI & Associates and nationalized banks.

Table 19: Region Wise Market Share Of Each Bank Type In Outstanding Credit For

Personal Loan 2002

(in %)

Region/Bank SBI &

Associates Nationalized

Banks Foreign Banks RRB

Other SCB

All Banks

Northern Region

North-Eastern Region