market outlook: volatility as economic worries … outlook: volatility as economic worries persist...

TRANSCRIPT

0

Market Outlook: Volatility As Economic Worries Persist

RHB Research Institute11 December 2010

1

Strong performance in recent months on the back of rising inflows of foreign portfolio funds into emerging markets.

Interesting times given G3 quantitative easing (including the latest QE (2) by the US), currency war and influx of hot money into the emerging markets.

Positive near-term outlook but may not be sustainable. We believe the market may move into a phase of greater volatility in the months ahead.

In the near term, the market is also supported by domestic news flow, including the impending award of projects, Sarawak state elections and possible early general elections

Market outlook

2

Reinvigorating private investment and intensifying human capital development.

Balancing fiscal consolidation with growth.

No substantial new information that will excite equity investors in the immediate term.

Consequently, our views on the market outlook, earnings and sector calls remain relatively unchanged.

Focused attention primarily on private sector projects that are already in the news.

Major positive: timelines for the major projects have been set and are mostly expected to begin in 2011.

The 2011 Budget: Setting the pace towards transformation

3

RM 40bn MRT project.

RM26bn KL International Financial District.

RM10bn redevelopment of the Rubber Research Board land in Sungai Buloh.

Six toll roads, including the West Coast Expressway.

New Inclusions

The “revived” RM5bn warisan Merdeka integrated development comprising a 100-storey tower led by PNB.

The “River of Life”, ie. The clean-up / beautification of the Klang Valley (RM1.9bn allocation under environment preservation).

The Academic Centre, i.e. a JV between Academic Medical College, Johns Hopkins Medicine International and Royal College of Surgeons, Ireland (to bring in RM2bn private investment).

Key projects to kick-start in 2011

4

Key projects to be implemented

Funded By Development ExpenditureRural infrastructure 6,900• Rural water & electricity in Sabah & Sarawak 2,700• Rural roads in Sabah & Sarawak 2,100 East Malaysia-based contractors• Rural roads in Peninsular Malaysia 696• Rural water & electricity in Peninsular Malaysia 556• Housing for rural hardcore poor 300Building/upgrading of schools, hostels, facilities & equipment 6,400 Mid-sized contractorsEnvironmental preservation projects 1,900• “River of Life” and greening of KL na YTL• Preservation of marine sources and coastal areas in Melaka,

Kelantan, Terengganu & Pahang na Emas Kiara, MRCBCorridor & regional development 850• Iskandar Malaysia 339• East Coast Economic Region (ECER) 178• Northern Corridor Economic Region (NCER) 133• Sabah Development Corridor 110• Sarawak Corridor of Renewable Energy (SCORE) 93Public housing 568Aquaculture zones in Sabah & Sarawak 252 East Malaysia-based contractorsDrainage & irrigation in Muda Agriculture Development Area, Kedah 235Basic infrastructure for swiftlet nets, aquaculture, seaweeds,

ornamental fish and herbs & spices ventures 135Integrated eco-nature resort in Nexus Karambunai, Sabah 100 KarambunaiHotels & resorts in remote areas 85Diagnostic lab at Agriculture College in Kubang Pasu, Kedah 70Shaded walkways in KLCC-Bukit Bintang area 50

Project Value Potential beneficiaries(RMm)

(cont’d…)

5

Key projects to be implemented

Via Public-Private Partnership (PPP)/Private InvestmentMRT in Greater KL 40,000 Gamuda, MMCKuala Lumpur International Financial District (KLIFD) 26,000 1MDB (Awarded),

Mudabala (Awarded)Development of Malaysia Rubber Board land in Sg Buloh 10,000 EPF (Awarded), MRCBWarisan Merdeka integrated development with a 100-storey tower 5,000 PNB (Awarded)Academic Medical Centre 2,000Ampang-Cheras-Pandan Elevated Highway naGuthrie-Damansara Expressway naDamansara-Petaling Jaya Highway naPantai Barat-Banting-Taiping Highway (West Coast Expressway) na Kumpulan Europlus, IJMSungai Dua-Juru Highway naParoi-Senawang-KLIA Highway na300MW combined-cycle gas power plant in Kimanis, Sabah na Zelan, MudajayaInternational Islamic University Malaysia Teaching Hospital in Kuantan, Pahang na Ahmad Zaki (Awarded)Women and Children’s Hospital in KL na RanhillIntegrated Health Research Institute Complex in KL na

Project Value Potential beneficiaries(RMm)

6

The detailed ETP blueprint

Driven by the 12 National Key Economic Areas (NKEAs) and supported by the 8 strategic reform initiatives (SRIs).

Identified 131 Entry Point Projects (EPPs) and 60 Business Opportunities (BOs).

Total investment of about US$444bn (RM1.3trn) required over the next 10 years, of which 92% is expected to be funded by the private sector (73% from domestic, of which 68% from non-GLCs).

Major projects include:

i). The RM40bn MRT project;

ii). The high-speed rail from KL to Singapore and Penang;

iii). The clean-up/beautification of the Klang River;

iv). Creation of a regional oil storage and trading hub by 2017; and

v). making Malaysia a preferred Asian hub for oil field services by 2015.

(cont’d…)

7

The success of the ETP could depend on the effective implementation of certain NKEAs.

In our view, the Greater KL NKEA holds great potential as enabler for the construction and housing sectors, but it is also cross-linked to other NKEAs such as financial services, tourism, and education.

Conceptually the plan is sound, and is ready to go in our view, but execution risk from political and social perspective is relatively high.

Securing the buy-in from private sector is key.

Overall, the ETP will likely continue to provide news flow for the market and certain key sectors.

The detailed ETP blueprint

8

9 key private sector-led projectsValue (RMm)

1. LFoundry relocation of wafer fab to Malaysia 1,900

2. Mydin – 14 new branches and assist in upgradingsmall sundry shops 1,000

3. St. Regis in KL Sentral (hotel) 1,200

4. Schlumberger – Eastern Hemisphere Global FinancialServices Hub and Shared Services in Bandar Utama 300

5. Malaysia Airports – 25 years concession for WCT tobuild the integrated complex for the new LCCT (KLIA2) 486

6. 1MDB and Mudabala – KL International Financial District 26,000

7. Premium Renewable Energy – Bioplant in Lahad Datu 124

8. Asia e-University – gateway university for internationaleducation for distance and online learning 100

9. Genting Plantation Johor Premium Outlet 150

9

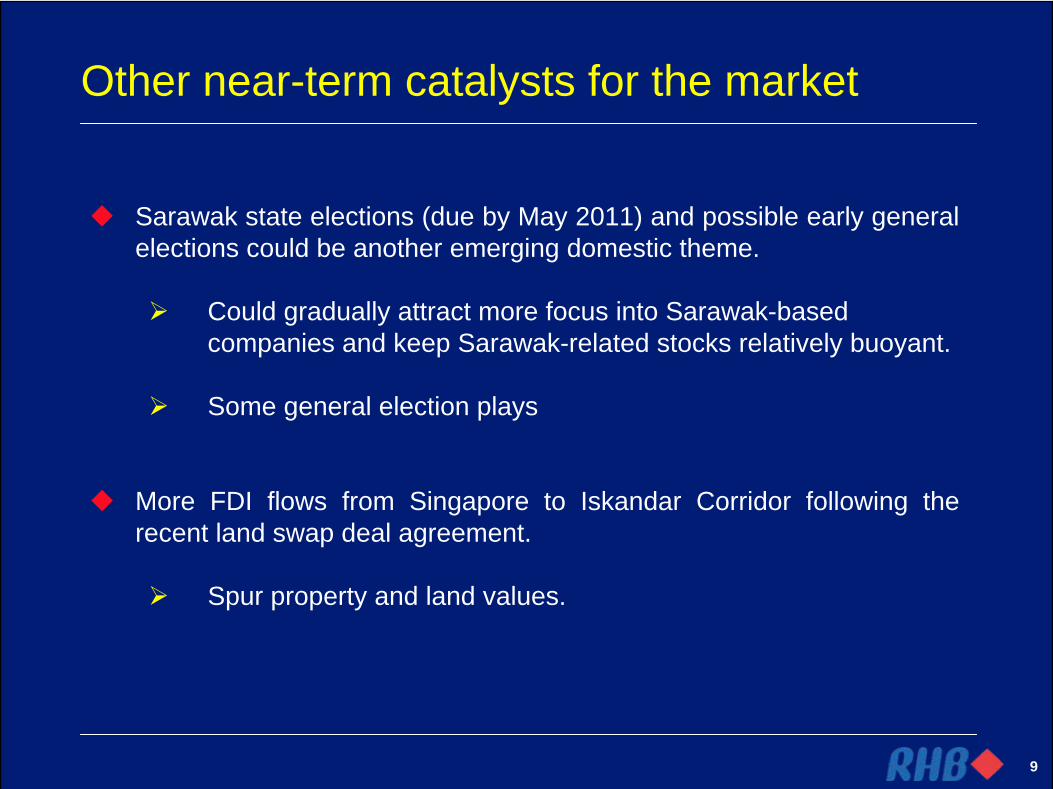

Other near-term catalysts for the market

Sarawak state elections (due by May 2011) and possible early general elections could be another emerging domestic theme.

Could gradually attract more focus into Sarawak-based companies and keep Sarawak-related stocks relatively buoyant.

Some general election plays

More FDI flows from Singapore to Iskandar Corridor following the recent land swap deal agreement.

Spur property and land values.

10

Investors’ focus likely turning to 2011

We believe there is still room for the market to trend higher in 2011.

Primarily on the view that global economic recovery is more sustainable than feared.

Sustained corporate earnings growth (+14.5% projected for 2011) will continue to create new shareholders’ value for investors.

Our end-2011 FBM KLCI target remains unchanged at 1,640 based on 15x mid-cycle 2012 earnings.

This, however, will not be without volatility as the global economy enters into a period of slowing growth in an uneven phase of recovery.

11

Uncertainty persists in the global economy

Whilst industrial production and services activities have recovered globally from low levels in 2009, the pace of recovery has lost some momentum of late.

Global manufacturing & services activities

Index

PMI manufacturing

Source: Institute for supply management (ISM), RHBRI.

PMI services

Industrial production in major economies

% yoy

Source: Bloomberg, RHBRI

-50

-40

-30

-20

-10

0

10

20

30

40

05 06 07 08 09 10

US Eurozone

Japan China

30

35

40

45

50

55

60

65

05 06 07 08 09 10

12

Weak economic recovery momentum in the US

Source: Bloomberg, RHBRISource: Bloomberg, RHBRI

US economic growth still subpar Improving but still weak labour market conditions

(000)% yoy % of labour force

Non-farm payrolls (LHS)

Unemployment rate (RHS)

-1000

-800

-600

-400

-200

0

200

400

600

00 01 02 03 04 05 06 07 08 09 100

2

4

6

8

10

12

-8

-6

-4

-2

0

2

4

6

8

10

05 06 07 08 09 10

GDP

Exports

consumer spending

13

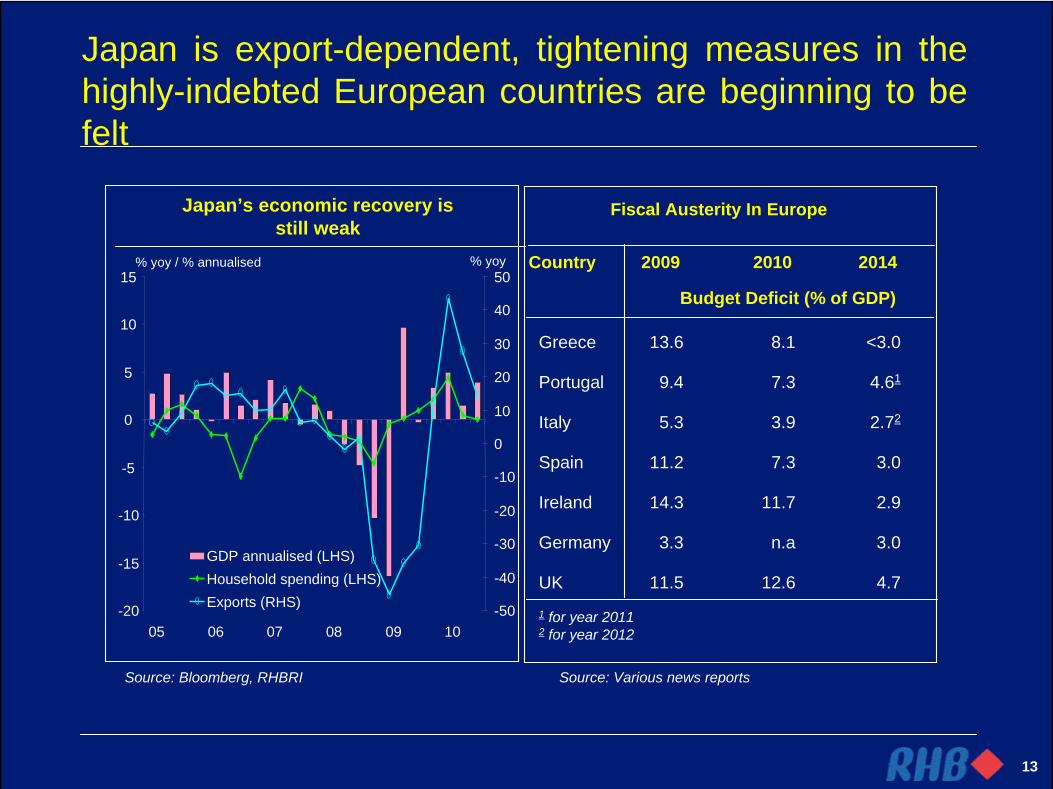

Japan is export-dependent, tightening measures in the highly-indebted European countries are beginning to be felt

Source: Bloomberg, RHBRI

Country 2009 2010 2014

Budget Deficit (% of GDP)

Source: Various news reports

Greece 13.6 8.1 <3.0

Portugal 9.4 7.3 4.61

Italy 5.3 3.9 2.72

Spain 11.2 7.3 3.0

Ireland 14.3 11.7 2.9

Germany 3.3 n.a 3.0

UK 11.5 12.6 4.71 for year 20112 for year 2012

Fiscal Austerity In EuropeJapan’s economic recovery is still weak

% yoy / % annualised % yoy

-20

-15

-10

-5

0

5

10

15

05 06 07 08 09 10-50

-40

-30

-20

-10

0

10

20

30

40

50

GDP annualised (LHS)Household spending (LHS)Exports (RHS)

14

Unwelcome capital inflows, causing volatility to currencies and surging asset prices.

Fear of unsustainable asset bubble in China.

Many emerging / developing economies are facing with a different set of issues

Surging asset prices in some countries led to fears of asset bubbles

% yoy

Hong Kong

China

(Property prices)

Source: Bloomberg, RHBRI.

PMI(RHS)

Fixed-assetInvestment

(LHS) Loan growth(LHS)

China’s economic slowdown appears to have stabilised

% yoy Index

Source: Bloomberg, RHBRI.

-20

-10

0

10

20

30

40

06 07 08 09 1010

15

20

25

30

35

40

06 07 08 09 100

10

20

30

40

50

60

70

15

Normalisation of policies will continue in these countries, albeit at a slower pace.

Some emerging economies also face with rising inflation

Rising inflation a concern in some countries

Source: Bloomberg, RHBRI.

% yoy (CPI / WPI)

Vietnam

India

China

% p.a

Rising interest rates in some countries

Source: Bloomberg, RHBRI.

Australia

India

2

3

4

5

6

7

8

9

10

05 06 07 08 09 10-5

0

5

10

15

20

25

30

06 07 08 09 10

16

Immediate key issues facing Asian countries

Currency battles across the globe.

Quantitative easing in G3 countries / currency intervention

G3 liquidity is flooding Asia’s equity, bond and currency markets to seek higher return.

Destabilising capital inflows a key risk to Asian growth.

17

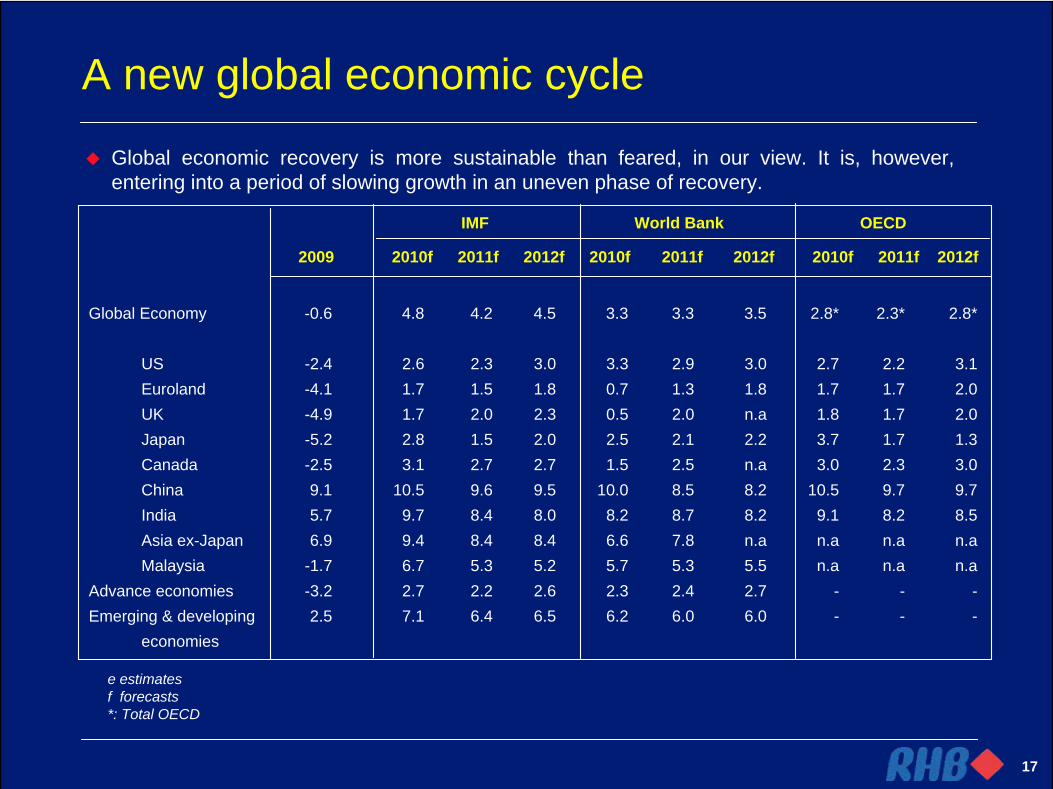

Global economic recovery is more sustainable than feared, in our view. It is, however, entering into a period of slowing growth in an uneven phase of recovery.

e estimatesf forecasts*: Total OECD

Global Economy -0.6 4.8 4.2 4.5 3.3 3.3 3.5 2.8* 2.3* 2.8*

US -2.4 2.6 2.3 3.0 3.3 2.9 3.0 2.7 2.2 3.1Euroland -4.1 1.7 1.5 1.8 0.7 1.3 1.8 1.7 1.7 2.0UK -4.9 1.7 2.0 2.3 0.5 2.0 n.a 1.8 1.7 2.0Japan -5.2 2.8 1.5 2.0 2.5 2.1 2.2 3.7 1.7 1.3Canada -2.5 3.1 2.7 2.7 1.5 2.5 n.a 3.0 2.3 3.0China 9.1 10.5 9.6 9.5 10.0 8.5 8.2 10.5 9.7 9.7India 5.7 9.7 8.4 8.0 8.2 8.7 8.2 9.1 8.2 8.5Asia ex-Japan 6.9 9.4 8.4 8.4 6.6 7.8 n.a n.a n.a n.aMalaysia -1.7 6.7 5.3 5.2 5.7 5.3 5.5 n.a n.a n.a

Advance economies -3.2 2.7 2.2 2.6 2.3 2.4 2.7 - - -Emerging & developing 2.5 7.1 6.4 6.5 6.2 6.0 6.0 - - -

economies

IMF World Bank OECD

2009 2010f 2011f 2012f 2010f 2011f 2012f 2010f 2011f 2012f

A new global economic cycle

18

“V-shape” export recovery set to normalise as low base effect fizzles out.

Speed bumps from Europe and China.

M’sia: slowing economic growth in the 2H

Exports and industrial production in M’sia slowing down rapidly

% yoy

Source: Dept of statistics, RHBRI

% yoy

China

Europe

M’sia’s exports to China & Europe will likely slow down further in the months ahead

Source: Dept of statistics, RHBRI

% yoy

Exports

IPI

-60

-40

-20

0

20

40

60

80

100

120

140

160

06 07 08 09 10-40

-30

-20

-10

0

10

20

30

40

-40

-30

-20

-10

0

10

20

30

40

50

06 07 08 09 10

19

Expect the Malaysian economic growth to slow down and normalise to 5.0% in 2011

f: forecasts

Agriculture 4.3 0.4 -0.4 5.9 6.8 2.4 2.7 0.4 3.8 4.0 3.4 4.5

Manufacturing 1.3 -14.5 -8.6 5.0 17.0 16.0 7.5 -9.4 11.5 8.0 10.8 6.7

Mining & quarrying -2.4 -3.5 -3.6 -2.8 2.1 1.1 -1.0 -3.8 1.5 2.3 1.0 2.9

Construction 4.2 4.5 7.9 9.3 8.7 4.1 2.8 5.8 4.2 3.2 4.9 4.4

Services 7.4 1.7 3.4 5.2 8.5 7.3 5.4 2.6 6.5 4.6 6.5 5.3

GDP 4.7 -3.9 -1.2 4.4 10.1 8.9 5.3 -1.7 7.3 5.0 7.0 5.0-6.0

Consumption Public 10.7 1.5 9.4 0.7 6.3 6.9 -10.2 3.1 -1.4 4.5 0.2 4.6Private 8.5 0.3 1.3 1.6 5.1 7.9 7.1 0.7 6.3 5.4 6.7 6.3

Fixed capital formation 0.7 -9.6 -7.9 8.2 5.4 12.9 9.8 -5.6 9.3 6.3 11.6 5.3Public 0.5 n.a n.a n.a n.a n.a n.a 8.0 10.8 4.9 8.3 0.6Private 1.0 n.a n.a n.a n.a n.a n.a -17.2 8.6 7.8 15.2 10.2

Agg. domestic demand 6.8 -2.2 0.1 2.8 5.3 9.0 5.0 -0.5 5.8 5.5 6.9 5.8

Exports of goods andnon-factor services 1.6 -17.9 -12.9 6.0 19.3 13.8 6.6 -10.4 9.7 7.6 11.6 6.7

Imports of goods and non-factor services 2.2 -19.4 -13.2 7.0 27.5 21.9 11.0 -12.3 13.9 8.4 16.6 7.2

GDP 4.7 -3.9 -1.2 4.4 10.1 8.9 5.3 -1.7 7.3 5.0 7.0 5.0-6.0

2008 2009 2010 2009 2010f 2011f 2010f 2011f

Q2 Q3 Q4 Q1 Q2 Q3

% Growth in Real Terms

Q2 Q3 Q4 Q1 Q2 Q3

% Growth in Real Terms

2008 2009 2010 2009 2010f 2011f 2010f 2011f

Source: Dept of Statistics, Ministry of Finance and RHBRI.

RHBRI MOF

RHBRI MOF

20

Revenue 158.6 162.1 165.8 2.2 2.3Operating Expenditure 157.1 152.2 162.8 -3.1 7.0Current balance 1.6 10.0 3.0Gross development expenditure 49.5 54.0 49.2 9.1 -9.0

Less : Loan recoveries 0.5 0.7 0.7 41.0 -6.8Net development expenditure 49.0 53.3 48.5 8.8 -9.0Overall balance -47.4 -43.3 -45.5

% to GDP -7.0 -5.6 -5.4

Federal Government revenue and expenditure proposals

1 : Budget estimate, excluding 2011 tax measures.Source : Ministry of Finance Economic Report 2010/2011

2009 2010(e) 20111(f) 2010(e) 2011(f)(RM bn) (%, change)

Federal Government Financial Position

Less expansionary but still contributing to growth.

21

Consolidated Public Sector* Finance

Revenue 134.0 132.8 138.6 4.4 -0.9 4.4Operating expenditure 170.3 168.0 176.8 3.2 -1.3 5.2NFPEs current surplus 101.2 94.2 93.2 -15.2 -6.9 -1.1Public sector current balance 64.9 59.0 55.0

% of GDP +9.6 +7.6 +6.6Development expenditure 111.3 119.1 118.5 -10.5 7.0 -0.5

General government 54.5 57.1 54.8 7.9 4.8 -4.1NFPEs 56.8 62.0 63.7 -23.1 9.2 2.8

Overall balance -46.4 -60.1 -63.5% of GDP -6.8 -7.8 -7.6

1 : Budget estimate, excluding 2011 tax measures.Source : Ministry of Finance Economic Report 2010/2011* Includes the state governments, statutory authorities, local governments and non-financial public enterprises (NFPEs)

2009 2010(e) 20111(f) 2009 2010(e) 2011(f)(RM bn) (%, change)

Also less expansionary than in 2010.

22

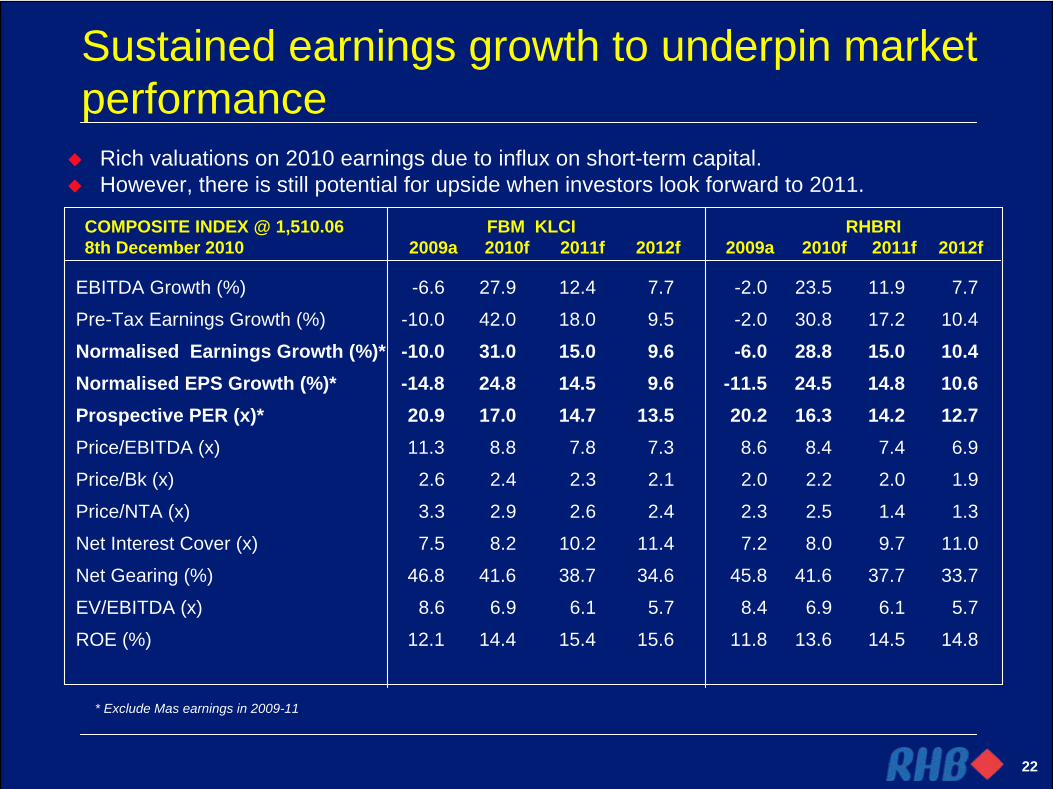

Sustained earnings growth to underpin market performance

Rich valuations on 2010 earnings due to influx on short-term capital.

However, there is still potential for upside when investors look forward to 2011.

EBITDA Growth (%) -6.6 27.9 12.4 7.7 -2.0 23.5 11.9 7.7

Pre-Tax Earnings Growth (%) -10.0 42.0 18.0 9.5 -2.0 30.8 17.2 10.4

Normalised Earnings Growth (%)* -10.0 31.0 15.0 9.6 -6.0 28.8 15.0 10.4Normalised EPS Growth (%)* -14.8 24.8 14.5 9.6 -11.5 24.5 14.8 10.6Prospective PER (x)* 20.9 17.0 14.7 13.5 20.2 16.3 14.2 12.7Price/EBITDA (x) 11.3 8.8 7.8 7.3 8.6 8.4 7.4 6.9

Price/Bk (x) 2.6 2.4 2.3 2.1 2.0 2.2 2.0 1.9

Price/NTA (x) 3.3 2.9 2.6 2.4 2.3 2.5 1.4 1.3

Net Interest Cover (x) 7.5 8.2 10.2 11.4 7.2 8.0 9.7 11.0

Net Gearing (%) 46.8 41.6 38.7 34.6 45.8 41.6 37.7 33.7

EV/EBITDA (x) 8.6 6.9 6.1 5.7 8.4 6.9 6.1 5.7

ROE (%) 12.1 14.4 15.4 15.6 11.8 13.6 14.5 14.8

COMPOSITE INDEX @ 1,510.06 FBM KLCI RHBRI 8th December 2010 2009a 2010f 2011f 2012f 2009a 2010f 2011f 2012f

* Exclude Mas earnings in 2009-11

23

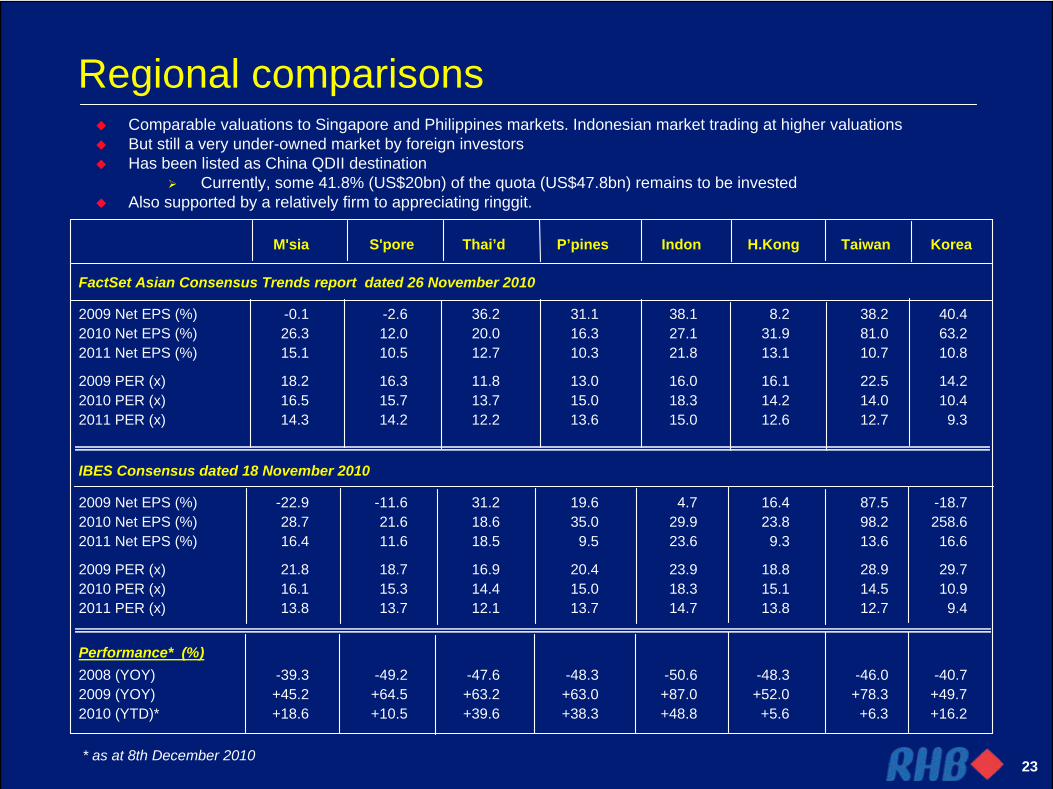

Regional comparisons

Comparable valuations to Singapore and Philippines markets. Indonesian market trading at higher valuations

But still a very under-owned market by foreign investors

Has been listed as China QDII destination

Currently, some 41.8% (US$20bn) of the quota (US$47.8bn) remains to be invested

Also supported by a relatively firm to appreciating ringgit.

* as at 8th December 2010

FactSet Asian Consensus Trends report dated 26 November 2010

2009 Net EPS (%) -0.1 -2.6 36.2 31.1 38.1 8.2 38.2 40.42010 Net EPS (%) 26.3 12.0 20.0 16.3 27.1 31.9 81.0 63.22011 Net EPS (%) 15.1 10.5 12.7 10.3 21.8 13.1 10.7 10.8

2009 PER (x) 18.2 16.3 11.8 13.0 16.0 16.1 22.5 14.22010 PER (x) 16.5 15.7 13.7 15.0 18.3 14.2 14.0 10.42011 PER (x) 14.3 14.2 12.2 13.6 15.0 12.6 12.7 9.3

IBES Consensus dated 18 November 2010

2009 Net EPS (%) -22.9 -11.6 31.2 19.6 4.7 16.4 87.5 -18.72010 Net EPS (%) 28.7 21.6 18.6 35.0 29.9 23.8 98.2 258.62011 Net EPS (%) 16.4 11.6 18.5 9.5 23.6 9.3 13.6 16.6

2009 PER (x) 21.8 18.7 16.9 20.4 23.9 18.8 28.9 29.72010 PER (x) 16.1 15.3 14.4 15.0 18.3 15.1 14.5 10.92011 PER (x) 13.8 13.7 12.1 13.7 14.7 13.8 12.7 9.4

Performance* (%)2008 (YOY) -39.3 -49.2 -47.6 -48.3 -50.6 -48.3 -46.0 -40.72009 (YOY) +45.2 +64.5 +63.2 +63.0 +87.0 +52.0 +78.3 +49.72010 (YTD)* +18.6 +10.5 +39.6 +38.3 +48.8 +5.6 +6.3 +16.2

M'sia S'pore Thai’d P’pines Indon H.Kong Taiwan Korea

24

In summary…

Positive near-term outlook due to influx of short-term capital but may not be sustainable.

Potential reversal of capital flows can cause the equity market to be volatile until a clearer picture emerges from the global economy.

The market correction, if any, however, is not likely to be sharp given ample liquidity and sustainable economic and earnings growth, albeit at more moderate pace moving forward.

Overall, the longer-term outlook remains positive and we expect the FBM KLCI to trade towards 1,640 at end-2011.

25

Market strategy

Whilst we acknowledge that the longer-term economic picture remains positive for the equity market, any reversal of short-term capital can have a disproportionate impact on the market in the foreseeable future.

Ride the volatility and top slice news flow-driven stocks where valuations have become rich. This would provide more room for investors to accumulate fundamentally robust stocks on weakness.

Stock picking is key.

Still a tactical play on construction and property stocks given a flurry of news flow and impending award of projects.

Continue to see values in the banking sector and positive on plantation and timber sectors.

26

Top PicksStocks FYE Price Fair Mkt Cap EPS Eps Growth PER P/BV P/CF GDY

(8/12/10) Value (sen) (%) (X) (x) (x) (%)(RM/s) (RM/s) RM mil 11f 12f 11f 12f 11f 12f 11f 11f 11f

CIMB Dec 8.70 9.80 64,665 57.8 67.0 19.3 15.9 15.1 13.0 2.4 n.a. 1.4

IOI Jun 5.78 7.15 36,860 34.7 37.4 32.4 7.8 16.7 15.5 3.4 14.8 2.9

KLK Sep 21.90 24.50 23,378 136.2 144.1 60.9 5.8 16.1 15.2 3.6 15.7 3.9

Gamuda Jul 3.77 4.51 7,607 19.0 20.5 36.5 7.9 19.9 18.4 2.1 49.3 3.2

MAHB Dec 6.22 8.02 6,842 44.9 49.9 20.5 11.3 13.9 12.5 1.8 9.8 3.2

Parkson Jun 5.69 7.36 5,897 35.6 46.2 29.2 29.9 16.0 12.3 2.6 5.3 1.8

SP Setia Oct 5.36 5.94 5,450 22.8 27.4 14.6 19.8 23.5 19.6 2.5 43.6 2.7

Kencana July 2.06 2.60 3,416 13.7 15.5 67.3 12.9 15.0 13.3 3.4 10.7 0.5

IJM Land^ Mar 2.98 3.65 3,302 19.4 21.3 53.0 9.8 15.4 14.0 1.7 12.3 1.0

Jaya Tiasa^ Apr 4.09 4.83 1,156 47.7 52.0 65.5 8.9 8.6 7.9 0.9 5.6 0.0

APM Dec 5.25 6.07 1,058 71.4 81.8 14.2 14.5 7.4 6.4 1.3 3.0 2.5

HSL Dec 1.80 2.27 1,001 16.2 17.7 21.4 8.9 11.1 10.2 2.3 13.1 1.4

27

Sector Weightings & ValuationsCovered Stocks MktCap Weight EPS Growth PER Recommendation

(RMbn) (%) (%) (x)

Banks & Finance 217.4 25.7 25.1 14.3 11.4 13.4 12.0 OverweightGaming 67.0 7.9 52.4 2.3 9.3 14.0 12.8 OverweightOil & Gas 35.3 4.2 48.6 18.0 10.5 15.3 13.9 OverweightConstruction 23.6 2.8 25.3 18.0 6.8 17.6 16.5 OverweightProperty 23.0 2.7 7.1 15.8 11.6 13.2 11.8 OverweightMotor 21.2 2.5 64.9 11.6 16.6 9.4 8.1 OverweightMedia 14.5 1.7 36.3 10.1 9.4 12.2 11.2 OverweightTimber 3.6 0.4 78.5 41.3 11.4 8.2 7.4 OverweightPlantation 122.4 14.5 6.5 27.9 5.6 16.3 15.4 NeutralTelecommunications 111.6 13.2 26.3 11.7 9.5 15.2 13.8 NeutralPower 63.3 7.5 8.8 13.2 10.3 12.8 11.6 NeutralConsumer 33.9 4.0 -4.9 11.5 17.9 15.7 14.1 NeutralBuilding Materials 12.4 1.5 5.0 36.9 10.7 11.0 9.9 NeutralManufacturing 7.0 0.8 14.6 13.9 10.1 9.8 8.9 NeutralSemiconductors & IT 4.3 0.5 17.7 -18.3 21.3 10.5 8.6 NeutralInsurance 3.8 0.4 -11.8 11.1 31.9 11.4 8.6 NeutralTransportation* 59.3 7.0 55.4 5.3 15.6 18.8 14.0 UnderweightInfrastructure 23.0 2.7 10.0 38.7 8.6 11.4 10.5 Underweight

846.7 100.0

* Exclude MAS earnings in 09-11Note : RHBRI's Basket

FY10 FY11f FY12f FY11f FY12f

28

High Dividend Yielding StocksHigh Dividend Yielding Stocks

^ FY11 & FY12 refer to FY12 & FY13 forecasts.

Glomac^ 1.69 8.6 10.3 0.8 12.2 OutperformVS Industry 1.79 8.6 9.7 1.0 12.8 OutperformCSC Steel 1.77 8.5 8.5 0.8 9.8 OutperformMaxis 5.38 8.4 9.1 n.m 26.9 OutperformDigi 24.64 8.2 8.7 27.0 85.5 OutperformAXIS Reit 2.35 8.0 8.0 1.3 11.2 OutperformQuil Capita 1.08 7.9 8.2 0.8 6.7 OutperformEvergreen 1.38 7.2 4.3 0.8 15.9 OutperformParamount 4.78 7.2 8.1 0.9 12.9 OutperformAdventa^ 2.08 7.1 8.3 1.3 22.3 OutperformP Gas^ 11.30 6.9 7.1 3.6 46.0 OutperformMCIL^ 0.88 6.8 7.1 1.4 13.3 OutperformSunway REIT 1.00 6.8 7.4 1.0 6.9 OutperformSTAR 3.41 6.7 6.7 2.3 16.0 OutperformFreight 0.98 5.6 5.6 1.1 17.2 OutperformMedia Prima 2.33 5.6 6.4 2.8 16.3 OutperformCBIP 3.60 5.6 5.6 1.4 23.6 OutperformPublic Bank (F/ L) 12.80 5.3 5.8 3.1 24.5 OutperformDaibochi 2.36 8.5 9.0 3.0 14.1 Market PerformTM 3.43 7.7 7.7 2.0 7.2 Market Perform Amway 8.15 6.9 7.1 6.4 39.6 Market Perform B-Toto^ 4.25 6.4 6.6 n.m 82.3 Market Perform

Share Price Gross Div. Yield (%) P/NTA (x) ROE (%) Recommendation(8/12/10)(RM/shr) FY11f FY12f FY11f FY11f

29

Bank & Finance

^ FY11 & FY12 refer to FY12 & FY13 forecasts# Not under our coverage, IBES estimates are used.

Maybank OP 8.40 10.40 61.5 68.8 14.1 11.7 13.6 12.2 2.0 4.2 -0.1CIMB OP 8.70 9.80 57.8 67.0 19.3 15.9 15.1 13.0 2.4 1.4 9.4PBB-F OP 12.80 15.40 96.0 105.7 12.8 10.0 13.3 12.1 3.1 5.3 3.6PBB-L OP 12.80 15.40 96.0 105.7 12.8 10.0 13.3 12.1 3.1 5.3 4.4AMMB^ OP 6.42 7.26 50.1 54.3 15.6 8.3 12.8 11.8 1.7 4.2 10.1HL Bank OP 9.27 11.00 71.3 75.0 4.6 5.2 13.0 12.4 1.9 2.6 2.5Affin OP 3.18 4.27 35.6 38.4 8.5 8.0 8.9 8.3 0.9 3.1 3.6RCE^ OP 0.53 0.95 12.9 13.2 6.6 2.6 4.1 4.0 0.7 3.8 -17.3AFG MP 3.15 3.60 28.2 30.0 8.9 6.3 11.2 10.5 1.4 2.7 2.6EON Cap UP 6.96 7.30 75.4 82.1 15.0 8.9 9.2 8.5 1.1 0.0 -0.6RHB Cap# NR 8.50 NR 71.3 80.9 11.1 13.5 11.9 10.5 1.4 3.0 21.1

Recom Price Fair EPS EPS Gwth PER P/BV GDY Price Chg (8/12/10) Value (sen) (%) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 3mths

We believe the sector is the best proxy to the economy and would help take the lead in lifting the market to higher grounds.

Loan applications have remained healthy, notwithstanding three OPR hikes thus far. We expect consumer spending to remain resilient next year on the back of high savings and rising consumerism and this would help support household loans. Fund raising activities by corporates could also pick up next year as key projects under the 10MP and Federal land deals get implemented.

Amid positive GDP growth and ample liquidity, capital market activities could continue to remain buoyant and this would help support non-interest income ahead.

The minimum capital levels banks would be required to hold under Basel III was announced in mid-Sep, which, we believe, virtually puts to rest lingering concerns investors may have had with respect to capital adequacy. By our calculations, the banks under our coverage should comfortably meet the minimum common equity ratio schedule. With that we see scope for some of the banks (e.g. Maybank, CIMB and AFG) to raise dividends.

Despite the recent five new banking licences issued, we believe earnings growth of the local banks remain intact. This is because: 1) the new commercial banking licences are niche banks and unlikely to compete head-on with the domestic institutions; and 2) the local banks are already very competitive given their increased share of overall assets as well as overseas ventures.

We are maintaining our Overweight stance on the sector. Maybank, CIMB, Public Bank, AMMB and HL Bank are all rated Outperform for bigger cap and liquidity exposure while smaller market capitalised stocks like Affin and RCE are also rated as Outperform.

30

Building Materials

CSC Steel OP 1.77 2.12 21.2 23.2 6.0 9.4 8.4 7.6 0.5 0.8 8.5 5.4YTL Cement OP 4.75 5.59 60.1 59.8 19.8 -0.4 7.9 7.9 4.1 1.3 3.2 19.3Ann Joo MP 2.89 3.14 38.9 41.1 29.5 5.6 7.4 7.0 5.7 1.1 5.2 9.5LM Cement UP 7.51 7.42 46.4 53.3 30.2 15.0 16.2 14.1 9.0 2.0 5.1 -0.5Hiap Teck UP 1.20 1.18 16.4 17.6 6.1 7.4 7.3 6.8 6.5 0.6 1.3 0.0Kinsteel UP 0.81 0.76 7.6 8.7 +>100 13.5 10.5 9.3 5.1 0.9 1.2 -3.6Sino Hua An UP 0.34 0.33 3.3 3.6 +>100 10.0 10.4 9.4 7.1 0.5 0.0 0.0Perwaja Holdings UP 0.94 0.98 8.5 14.3 +>100 68.2 5.0 4.5 8.0 0.5 0.0 -12.1

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 110f 12f 11f 11f 11f 3 mths

NeutralNeutral

Cement: Domestic cement consumption is expected to be strong in 2011 given the implementation of large- scale public construction projects and robust property development activities. In addition, domestic net selling prices for cement are also expected to be higher due to lesser rebates given by the cement producers. However, this will be partly offset by higher production costs (in particular, coal, diesel and electricity).

Steel: Increase in construction activities and infrastructure developments are expected to sustain the domestic demand for long steel products in 2011, although situation in the global steel sector might not be rosy due to the overcapacity issue, particularly in China. Managing volatility in prices, demand, and raw material costs will be the key challenges for steel producers going forward.

31

Sunway Hldgs OP 2.23 2.74 27.0 30.4 10.6 12.7 8.3 7.3 6.9 1.4 1.3 32.0HSL OP 1.80 2.27 16.2 17.7 21.4 8.9 11.1 10.2 6.5 2.3 1.4 12.5Fajarbaru OP 1.12 1.37 14.4 15.2 -10.8 5.5 7.8 7.4 1.8 1.3 5.4 12.9Gamuda TB 3.77 4.51 19.0 20.5 36.5 7.9 19.9 18.4 21.9 2.3 3.2 6.8MRCB TB 2.02 2.30 6.3 6.6 +>100 4.9 32.2 30.7 20.1 2.1 0.0 11.0IJM Corp^ MP 6.20 6.16 32.6 34.2 2.7 5.0 19.0 18.1 10.1 1.5 1.8 21.8WCT UP 3.00 2.55 19.0 19.6 9.8 2.9 15.8 15.3 13.5 1.6 2.0 4.9^ FY11 & FY12 refer to FY12 & FY13 forecasts

ConstructionRecom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg

(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Overweight. Gross development expenditure in 2011 is projected at RM49.2bn, down -9% from RM54bn estimated for 2010. However, this will be cushioned by projects to be carried out on a Public-Private Partnership (PPP) or privatised basis, projected to rack up RM12.5bn private investment, anchored by RM1bn facilitation fund.

Key large-scale projects to kick-start in 2001 are the RM40bn MRT project, the RM26bn KL International Financial District (KLIFD), the RM10bn redevelopment of the Rubber Research Board land in Sungai Buloh and six toll roads including the West Coast Expressway. Others include the RM5bn Warisan Merdeka integrated development comprising a 100-storey tower led by PNB, the “River of Life”, i.e. the clean-up/beautification of the Klang Valley (funded by part of the RM1.9bn allocation under environmental preservation) and the RM2bn Academic Medical Centre (a JV with Johns Hopkins Medicine International and Royal College of Surgions, Ireland).

For the LRT, tenders for the first four packages (two main contracts and two sub-contracts) already closed in end-Aug 2010, Tenders for the remaining four packages (two main contracts and two sub-contracts) will also be called soon. We expect the award of the first four packages to happen by the end of the year, and if not, by early next year.

Buoyed by news flow, we foresee construction stocks to continue to generally outperform the market from 4Q2010. Our top “tactical” pick is Gamuda as we believe its share price will be buoyed by the sustained news flow from the RM40bn MRT project. Our top “value” pick is Fajarbaru due to its undemanding valuations, it being a strong contender for work packages of the LRT line extension project given its strong foreign partner, i.e. China Railway Construction Corporation, and a strong balance sheet with a net cash per share of 75sen.

32

ConsumerConsumer

^ FY11 & FY12 refer to FY12 & FY13 forecasts

Faber OP 2.66 3.77 34.7 38.8 31.8 11.7 7.7 6.9 2.8 1.8 3.0 -7.0KPJ Health OP 3.80 4.39 25.9 29.6 12.4 14.0 14.7 12.9 8.4 1.7 4.2 8.0C.I. Hldgs OP 3.75 4.90 34.8 40.4 29.8 15.9 10.8 9.3 6.2 3.6 2.8 34.9Carlsberg OP 6.25 6.60 2.0 2.2 4.8 11.2 13.4 12.0 8.6 3.1 4.1 22.1Parkson OP 5.69 7.36 35.6 46.2 29.2 29.9 16.0 12.3 3.8 2.6 1.8 1.6QL R OP 5.70 6.50 39.4 44.1 14.0 11.9 14.5 12.9 6.4 3.1 2.3 24.5AEON MP 6.03 6.47 54.8 58.4 5.6 6.6 11.0 10.3 2.1 1.6 2.0 10.0Amway MP 8.15 8.30 51.4 55.6 1.7 8.2 15.9 14.7 9.8 6.4 6.9 1.9Daibochi MP 2.36 2.95 24.7 27.1 7.5 9.7 9.6 8.7 5.6 3.0 8.5 -20.5Hai-O^ UP 2.96 2.84 28.6 32.2 2.5 12.6 10.4 9.2 6.1 1.0 6.4 -11.1BAT UP 45.86 42.92 234.6 231.8 -7.3 -1.2 19.6 19.8 13.6 69.3 4.6 -2.8KFCH UP 3.81 3.85 22.5 26.1 16.7 15.7 16.9 14.6 8.7 1.9 1.8 35.6

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Retail and MLM players to be driven by consumer spending. RHBRI’s economics team forecasts that consumer spending will likely grow at a softer rate of 5.4% in 2011 (vs. 5.6% estimated for 2010) as it is coming from a slightly higher base. We expect consumer spending growth to continue to drive topline growth for AEON, Hai- O and Amway. Parkson would also be driven by the growth in local consumer spending, however, we believe that its core driver would be its China department stores (95% of PBT), especially as China recently announced measures to gradually double its minimum wage by 2015.

Consumer spending growth will also drive F&B. Consumer spending growth will drive revenues for both KFC and QL Resources. However, in the longer run, we believe KFC’s expansion locally and overseas, mainly India, will likely be the revenue driver. For QL, we are positive on its outlook given its recent acquisition of a 23.29%stake in Lay Hong, which has a similar business activity, i.e. eggs, broiler farming and feedmill. We believe the acquisition will provide synergistic benefits and incremental earnings.

Healthcare poised for growth and resilient earnings. Both public and private healthcare sectors are poised for growth in FY11. Private healthcare business will grow on the back of growing uptake in medical insurance policies. Meanwhile, with strong news flow on the M&A in private healthcare sector in the region, we believe that KPJ will be in investors’ spotlight and deserves to be trading at a higher valuation, further narrowing its discount to regional peers’ PER of 18x.

Polyester film prices to affect Daibochi’s margins going forward. We expect Daibochi’s margins to improve following an expected oversupply of plastic resin, its main raw material. However, the improved margins could potentially be offset by rising polyester film prices, which has risen ~50% YTD. Demand wise, we expect its continuous product innovation and foray into the non-F&N sector will continue to drive revenue growth.

Excise duty on cigarettes were increased in early October, effectively increasing cigarette prices by 7.5%, which would put further downward pressure on TIV. However, the brewers were spared another year of an excise duty hike, which augurs well for Carlsberg.

Top pick is Faber. We like KPJ due to its resilient earnings, leading position and expansion plans in Malaysia coupled with strong news flow from the sector.

33

Gaming

^ FY11 & FY12 refer to FY12 & FY13 forecasts * Normalised

Genting Bhd OP 10.80 12.80 79.1 88.7 -1.1 12.1 13.7 12.2 5.2 2.6 1.3 15.1Genting M'sia OP 3.44 4.50 23.5 24.7 7.0 5.2 14.6 13.9 8.0 1.6 2.2 15.1B-Toto^ MP 4.25 4.50 30.0 30.9 13.1 3.1 14.2 13.8 9.9 n.m 6.4 1.4Genting S'pore MP S$2.18 S$2.40 9.5 11.5 17.4 21.7 23.0 18.9 9.5 5.3 0.0 38.0

Recom Price Fair EPS * EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Upgrade to Overweight (from Neutral), given our upgrade in Genting Malaysia’s (GM) recommendation). We believe the casino gaming space has great potential, coming from a recovering economy and exciting growth opportunities in new frontiers.

We believe it is time to relook at GM on the back of three key points: (1) Longer-term upside potential of new projects has not been factored in by the market - given that one of the acquisitions (Genting UK) was clouded by the fact that it was a related party acquisition and the other (Genting NY) was deemed to have a relatively small ROI ; (2) Malaysian business continues to be a sturdy backbone for GM’s operations – recording 5% yoy visitor arrival growth in 1H10; and (3) Beneficiary of 19.6%-owned Genting HK’s successful turnaround – as its market value now makes up 7% of GM’s SOP (from 4% at beg-2010). We believe that GM has been punished enough already, given its lagging share price versus its sister companies in Malaysia and Singapore. Our fair value for GM is now RM4.50 and we upgrade our recommendation to Outperform (from market perform).

Although we continue to be optimistic on Genting Singapore’s (Market Perform, FV = S$2.40) prospects, we believe there may be a bit of market disappointment on the recently released set of results and on the seemingly less bullish guidance from management going forward. In the longer-term, Genting will continue to be a beneficiary of GenS’ growing profits, given its 54.3% stake in GenS, which results in an earnings contribution of 50-55% to the group; stronger earnings growth from the plantation division on the back of high CPO prices; and any longer-term potential upside from GM’s new projects. In addition, the valuation gap between Genting and Genting Singapore provides investors with an arbitrage opportunity, as Genting is a much cheaper entry point into GenS, both on a PE (by 40- 50%) and an EV/EBITDA (by 60-70%) basis. Maintain Outperform on Genting with fair value of RM12.80

As for BToto, prospects look bleak after the pool betting duty hike which would reduce its earnings by 12% p.a.. Note that this does not take into account a potential reduction in prize payouts, although this could be slightly offset by a resultant fall in sales volumes. Nevertheless, the potential of higher dividends given Berjaya Land’s need for RM711m in cash for its convertible bonds maturing in Aug 2011, could provide support for BToto’s share price. Maintain Market Perform with fair value of RM4.50

34

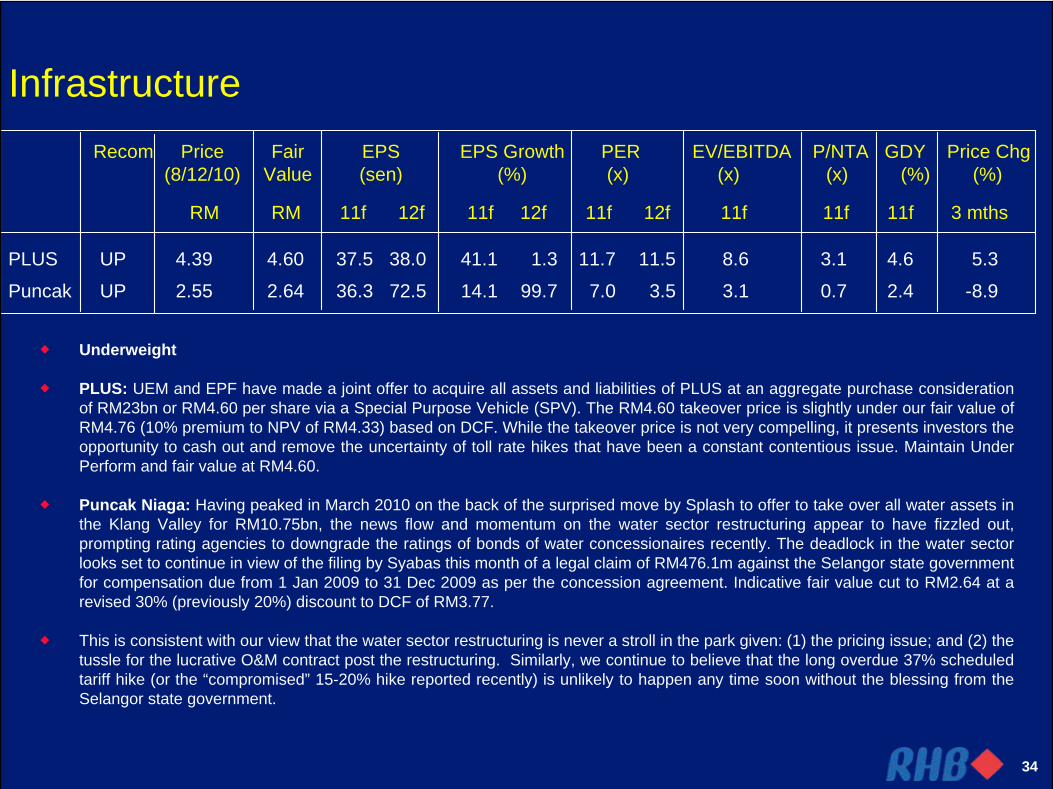

Infrastructure

PLUS UP 4.39 4.60 37.5 38.0 41.1 1.3 11.7 11.5 8.6 3.1 4.6 5.3

Puncak UP 2.55 2.64 36.3 72.5 14.1 99.7 7.0 3.5 3.1 0.7 2.4 -8.9

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Underweight

PLUS: UEM and EPF have made a joint offer to acquire all assets and liabilities of PLUS at an aggregate purchase consideration of RM23bn or RM4.60 per share via a Special Purpose Vehicle (SPV). The RM4.60 takeover price is slightly under our fair value of RM4.76 (10% premium to NPV of RM4.33) based on DCF. While the takeover price is not very compelling, it presents investors the opportunity to cash out and remove the uncertainty of toll rate hikes that have been a constant contentious issue. Maintain Under Perform and fair value at RM4.60.

Puncak Niaga: Having peaked in March 2010 on the back of the surprised move by Splash to offer to take over all water assets in the Klang Valley for RM10.75bn, the news flow and momentum on the water sector restructuring appear to have fizzled out, prompting rating agencies to downgrade the ratings of bonds of water concessionaires recently. The deadlock in the water sector looks set to continue in view of the filing by Syabas this month of a legal claim of RM476.1m against the Selangor state government for compensation due from 1 Jan 2009 to 31 Dec 2009 as per the concession agreement. Indicative fair value cut to RM2.64 at a revised 30% (previously 20%) discount to DCF of RM3.77.

This is consistent with our view that the water sector restructuring is never a stroll in the park given: (1) the pricing issue; and (2) the tussle for the lucrative O&M contract post the restructuring. Similarly, we continue to believe that the long overdue 37% scheduled tariff hike (or the “compromised” 15-20% hike reported recently) is unlikely to happen any time soon without the blessing from the Selangor state government.

35

Insurance

Allianz* OP 4.22 5.34 38.9 45.2 19.9 16.2 10.8 9.3 1.7 4.1 2.2MNRB^ OP 2.77 3.41 19.5 29.5 -35.9 51.0 14.2 9.4 0.6 3.6 3.4Kurnia Asia UP 0.36 0.25 2.8 6.0 +>100 n.m 12.9 5.9 1.5 1.6 -14.5LPI Capital UP 12.14 11.40 70.2 82.9 12.4 18.0 17.3 14.6 1.6 5.7 3.4^ FY11 & FY12 refer to FY12 & FY13 forecasts * Price and fair value are ex-rights. EPS is not diluted until conversion of ICPS to shares.

Recom Price Fair EPS EPS Gwth PER P/NTA GDY Price Chg (8/12/10) Value (sen) (%) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 3mths

Neutral.

No clear decision by BNM yet with regards to the new scheme for the TPBID policies. But we believe BNM would not be able to delay the reforms for too long.

Four new family takaful licences were awarded to four JV’s: AIA-Alliance Bank, AMMB-Friends Provident Group Plc, ING-Public Bank-Public Islamic Bank, and Great Eastern-Koperasi Angkatan Tentera. The new licences will increase competition in the life insurance segment.

Life insurance growth will be backed by the low penetration rate relative to other countries in the region, higher medical costs, additional disposable income, the tax relief announced in the 2010 Budget and increased awareness on life products. Competition is expected to heat up as four new family takaful licences were issued.

General insurance growth will be backed by increase in demand following increase in business activities from the economic recovery, and improving Motor TIV growth. Recent merger between HLA’s general insurance arm and MSIG Insurance indicates a changing competitive landscape, as MSIG will be the second largest general insurer in the country, with the biggest fire and marine cargo portfolio.

Top Pick is Allianz.

36

Manufacturing

^ FY11 & FY12 refer to FY12 & FY13 forecasts

Adventa OP 2.08 2.47 33.8 43.3 53.2 28.1 6.2 4.8 5.7 1.3 7.1 -13.0

VS Industry OP 1.79 2.24 32.5 36.5 42.0 16.3 6.4 5.5 3.7 1.0 8.6 36.6

Kossan OP 3.32 4.25 44.7 47.2 20.3 5.6 7.4 7.0 4.8 1.8 3.8 4.7

Top Glove UP 5.38 5.40 41.4 46.0 -0.4 11.2 13.0 11.7 7.1 2.6 4.0 -3.6

Hartalega^ MP 5.26 5.64 55.7 59.1 16.9 6.0 9.4 8.9 6.3 2.2 5.1 11.9

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Neutral.

Softening external demand for the country’s exports that could persist into 1H2011. This would translate to slowing manufacturing activities going forward.

We are cautious on the near-term outlook for the glove manufacturers largely due to: 1) slowdown in demand for rubber gloves as customers opt to run down their inventory levels due to high latex price; 2) high latex price; and 3) weakening US$ against RM (by around 10.5% YTD). The slow down in orders has adversely affected some glove manufacturers to adjust prices for the higher costs. Given the challenging near-term outlook for the sector, we maintained our Neutral stance on the rubber gloves sub-sector.

37

Media

^ FY11 & FY12 refer to FY12 & FY13 forecasts

Media Prima OP 2.33 2.82 16.9 19.6 17.1 15.9 13.8 11.9 7.5 2.8 5.6 12.6

Star OP 3.41 4.01 25.1 26.6 5.3 6.3 13.6 12.8 7.1 2.3 6.7 -4.2

MCIL^ OP 0.88 1.20 9.8 10.4 8.6 6.0 9.0 8.5 4.2 1.4 6.8 3.5

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Overweight

While YTD (Jan-Oct) adex growth stood at 17.1% yoy, we expect the growth rate to slow down in 4Q10 following the strong start to the global economic recovery in 1HFY10 given that adex will now be coming from a higher base. Nevertheless, adex growth should continue to remain healthy, supported by sporting events such as the Commonwealth Games and upcoming festive season.

At the cost side, newsprint prices have crept up recently, but the weakening US$ against RM should help to improve margins for the companies moving forward.

Media Prima (FV=RM2.82) remains our preferred pick as we believe adex (especially TV) will be a prime beneficiary of a recovering economy. In addition, Media Prima now controls NSTP and will be able to fully consolidate NSTP’s strong 2010 earnings growth. Potentially, there could be merger synergies that the enlarged entity may be able to reap. In addition, another potential catalyst is that the enlarged entity may be able to command better valuations.

We also like MCIL its as valuations are currently trading at a cheaper discount to Star’s despite both companies offering roughly similar earnings growth.

38

MotorMotor

^ FY11 & FY12 refer to FY12 & FY13 forecasts

MBM OP 3.09 4.96 58.4 64.2 6.6 9.8 5.3 4.8 13.8 0.7 3.9 -2.5Proton^ OP 4.76 5.60 75.2 78.0 11.6 3.8 6.3 6.1 7.1 0.5 0.0 1.3APM OP 5.25 6.07 71.4 81.8 14.2 14.5 7.4 6.4 3.2 1.3 2.5 19.3UMW MP 6.91 7.47 60.6 67.9 9.2 12.1 11.4 10.2 5.4 1.7 3.5 4.7T Chong MP 5.48 6.16 45.3 67.3 16.2 48.6 12.1 8.1 9.0 2.0 2.2 8.9

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

TIV numbers have soared since the beginning of the year, reaffirming our view that 2010 is the second year of a new 3-year cycle for motor stocks which began in 2009. As at October, YTD TIV is 505,613. This achieves 86% of our full-year forecasts of 587,350 and met 89% of MAA’s forecast of 570,000.

Our 2010 earnings growth is expected to continue gaining traction on the back of: 1) sustained industry TIV growth; and 2) strengthened RM against US$ and Yen that would help to reduce costs of imported materials; and 3) positive consumer sentiment with the greater stability of the economy.

Our top-pick is now APM (FV = RM 6.07). The stock has performed well in the year, with 6MFY10 net profit of RM54.9m. Going into FY11, growth prospects will be underpinned by a) Tan Chong’s entry into the small car segment and the Indochina market; and b) consolidation of their Seri Kembangan facilities to Port Klang that would improve its operating efficiency.

39

Oil & Gas

^ FY11 & FY12 refer to FY12 & FY13 forecasts

Kencana OP 2.06 2.60 13.7 15.5 67.3 12.9 15.0 13.3 9.0 3.5 0.5 31.2Dialog OP 1.61 1.94 7.7 9.8 30.7 26.5 20.9 16.5 21.6 5.3 2.6 46.4SapuraCrest ^ OP 2.82 3.34 18.5 19.5 10.0 5.2 15.2 14.5 4.6 2.4 2.5 16.5P Gas^ OP 11.30 13.51 72.9 75.6 2.7 3.7 15.5 14.9 8.2 3.6 6.9 5.4KNM Group OP 2.14 2.33 18.0 25.2 +>100 39.7 11.8 8.5 9.1 4.3 3.8 32.1Dayang OP 2.78 3.86 22.4 25.8 26.5 15.2 12.4 10.8 6.8 2.3 2.4 34.3Petra Perdana UP 0.85 0.44 4.6 8.5 139.7 83.8 18.3 10.0 7.9 0.7 2.4 -16.3Wah Seong UP 2.00 2.02 12.6 14.6 89.5 15.9 15.8 13.7 6.1 1.6 2.3 -2.0

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

We gather from our discussions with industry players that 2011 will see the return of contracts. Many oil and gas players have reiterated that the forward outlook is more positive compared to this time last year (Nov 2009) and are relatively optimistic in regards to the coming year’s prospects.

While the talk of contract flows is hardly new, we believe that the situation could be different this time around. Firstly, the sector has been highlighted as one of the twelve key economic areas that will transform the Malaysian economy and the Government has been a major source of news flow for the sector in recent weeks. Secondly, potential M&As or new listings (eg. Bumi Armada) could continue to provide “heat” for the sector.

Near-term contracts include 1) Petronas’ hook-up and commissioning (HUC) and topside maintenance contracts; and 2) Sepat marginal oil field project worth US$250m. MMHE has also mentioned that they look to close some contract bids within the next 6- 9months.

Winners will be the brownfield, topside maintenance and HUC players such as Kencana, Dayang, Sarku Engineering and Petra Energy. Fabricators are also likely champions in the near-term, given that new oilfield developments will see a need for new structures to be built.

In view of the strong contract pipeline for the sector we upgrade our call on the market to Overweight (from neutral previously). Our top pick at this juncture is Kencana, while our longer-term pick is Dialog.

40

IOI Corp OP 5.78 7.15 34.7 37.4 32.4 7.8 16.7 15.5 19.5 3.2 2.9 6.1KLK OP 21.90 24.50 136.2 144.1 60.9 5.8 16.1 15.2 23.2 3.7 3.9 28.5First Resources OP S$1.54 S$1.60 9.3 9.8 24.9 5.1 11.5 11.0 19.6 2.1 2.1 40.0CBIP OP 3.60 5.05 57.1 60.0 22.4 5.1 6.3 6.0 23.6 1.4 5.6 4.7Sime Darby MP 8.78 9.75 52.4 55.5 17.5 6.1 16.8 15.8 14.8 2.4 3.5 7.1IJM Plantation^ MP 2.96 2.90 18.2 15.4 5.1 -15.0 16.3 19.2 10.9 1.7 2.5 18.4Genting Plant UP 8.59 8.70 54.5 53.0 18.9 -2.7 15.8 16.2 13.7 2.0 1.6 9.7

Plantations

^ FY11 & FY12 refer to FY12 & FY13 forecasts * Normalised

Recom Price Fair EPS * EPS Growth PER ROE P/NTA GDY PriceChg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

CPO prices have continued to stay above the RM3,000/tonne mark, due to, we believe: (1) the intensifying La Niña phenomenon – now considered to be a moderate to strong event; (2) the increased financial demand – as monthly CPO futures Vol/OI ratio has risen to a high of 6.2x in Aug, before falling slightly to current estimated levels of 5.6x, 40% higher than average historical levels of 4x. This means that financial demand for CPO is moving towards the highs seen in 2007/2008, which we believe could continue in the short term, given the increased liquidity in the market and the movement of funds back to asset classes like commodities due to the persistent weakness of the US$; (3) a contagion effect from the spike in soyoil, corn and rapeseed oil prices; (4) demand rebalancing activities as the discount between CPO versus soybean oil and rapeseed oil widened; and (5) impact from the sustained crude oil prices of above US$80/barrel. We believe the current strength in CPO prices could continue potentially until the 1H2011, before moderating in the second half of the year.

Our CPO price assumptions are RM2,700/tonne for CY2010 (from RM2,500), RM2,900/tonne for CY2010 (from RM2,700) and RM2,700/tonne for CY2012 (from RM2,500).

Despite our more positive near-term outlook on prices and the upgrade in our earnings and target prices, we are maintaining our Neutral recommendation on the sector. The main reason for this is our Market Perform recommendation on Sime Darby, a heavyweight plantation stock. We continue to uphold our belief that a trading strategy should be adopted, given the volatile market environment. We note that at current price levels, the implied CPO price based on our earnings estimates and our target PE valuations for some stocks are still significantly below current CPO prices, giving rise to several trading opportunities. No change to our Outperform recommendations on IOIC, KLK, First Resources and CBIP, Market Perform recommendations on Sime Darby and IJMP and Underperform recommendation on Genting Plantations.

41

Power

Tenaga MP 8.58 9.40 68.9 78.1 17.9 13.2 12.4 11.0 6.0 1.2 3.2 -4.1

YTL Power UP 2.43 2.20 17.8 18.3 3.3 3.3 13.7 13.2 9.9 1.9 7.2 4.7

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY PriceChg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Neutral – In our view, the main focus for the sector next year would be on industry reforms. These could potentially include: 1) renegotiations on the first generation power purchase agreements (PPAs) with the independent power producers (IPPs), which are ongoing; 2) the removal of subsidies for natural gas; and 3) a formal tariff formula for TNB.

A compromise reached from the renegotiation of PPAs will be positive for TNB in terms of lower capacity payments that TNB would need to pay. This could then be passed on to consumers either in terms of lower tariffs or lower hikes required for higher fuel costs. As for the IPPs, we believe, at the minimum, the players would be looking at an NPV neutral outcome to the negotiations.

Separately, Pemandu has proposed to remove gas subsidy to the power sector by 2015 but TNB would be allowed to raise electricity tariffs accordingly to pass on the higher cost. We estimate that the impact should be neutral to TNB, depending on demand.

Timing remains a question mark on the formalisation a formal tariff formula. The formalisation of the formula would, in our view, be positive nonetheless in terms of: 1) allowing TNB to pass on higher fuel costs in a more timely manner while cost savings could be passed back to consumers quicker; 2) aid transparency; and 3) the formula could incorporate efficiency/service quality measures that reward (or penalise) TNB according to the achievement of targets and spur TNB to improve efficiency and service quality.

In the meantime, potential mitigating factors include: 1) strengthening of the ringgit versus US dollar; and 2) stronger demand (especially to help cover higher capacity payments).

Following the release of its 4QFY10 results, we have downgraded TNB from Outperform to Market Perform as we lowered our FY11-12 net profit forecasts by 8-10% respectively mainly due to lower-than-expected 4QFY10 results, upward revision in future coal cost assumptions and higher depreciation expense. Going forward, while we expect electricity demand to remain healthy, the growth rate would likely moderate as demand would now be coming from a higher base. We have assumed FY11 demand growth of +4.5%, slightly below our GDP growth projection of 5%.

We think the market would be watching YTLP’s WiMAX rollout (officially launched on Nov 19) and strategy closely. A potential concern here is that YTLP could decide to start a price war in order to win subscribers, especially given that it would be coming into the market with a largely unutilised network. For now, management’s reassurance regarding dividends means that a key investment thesis for the stock remains intact, i.e. attractive dividend yields. Due to its recent surge in share price however, we have downgraded YLTP to Underperform.

42

Property

^ FY11 & FY12 refer to FY12 & FY13 forecasts* NAV per share

Recom Price Fair EPS EPS Growth PER ROE P/NTA RNAV GDY Price Chg(8/12/10) Value (sen) (%) (x) (%) (x) (%) (%)

SP Setia OP 5.36 5.94 22.8 27.4 14.6 19.8 23.5 19.6 10.7 2.5 4.95 2.7 26.7Glomac^ OP 1.69 2.09 24.3 28.9 23.3 18.8 6.9 5.8 12.2 0.8 2.46 8.6 19.9Sunway City OP 4.52 5.80 41.3 48.2 18.6 16.8 11.0 9.4 8.0 0.9 6.44 1.9 22.8Axis REIT OP 2.35 2.67 18.7 18.9 12.3 0.8 12.6 12.5 11.2 1.3 1.60* 8.0 10.8Quill Capita OP 1.08 1.23 9.3 9.6 4.7 3.4 11.6 11.2 6.7 0.8 1.38* 7.9 6.9IJM Land OP 2.98 3.65 19.4 21.3 53.0 9.8 15.4 14.0 11.3 2.0 3.18 1.0 32.4Mah Sing OP 1.78 2.50 17.2 22.0 22.8 27.6 10.3 8.1 14.9 1.5 2.11 3.9 4.7Paramount OP 4.78 6.20 68.4 77.7 7.0 13.6 7.0 6.2 12.9 0.9 8.93 7.2 17.2Sunway REIT OP 1.00 1.05 6.7 7.3 10.1 8.6 14.7 13.6 6.9 1.0 0.97 6.8 0.9YNH Prop TB 1.70 2.17 17.6 20.3 11.6 15.2 9.7 8.4 9.0 0.9 3.10 2.6 0.0KLCC Prop MP 3.53 3.82 27.3 28.2 3.8 3.1 12.9 12.5 4.6 0.6 4.47 3.1 8.6Hunza Prop MP 1.64 1.58 27.6 20.9 3.4 -24.2 5.9 7.8 12.2 0.7 3.16 3.4 18.0Sunrise UP 3.01 2.80 29.9 33.2 10.6 11.1 10.1 9.1 12.8 1.2 4.12 1.4 48.3

RM RM 11f 12f 11f 12f 11f 12f 11f 11f RM 11f 3 mths

Overweight. We maintain our positive view on the sector. The impact of 70% LTV cap for third home mortgage and onwards will be moderate on the property sector, as young population is typically the first and second home buyers.

Key factors driving demand: (1) Faster growth in young demographics; (2) Easy financing in addition to aggressive incentives offered by developers; (3) Strengthening in ringgit to spur foreign participation; (4) Property is a preferred hedge against inflation; and (5) M&A activities to spur investors interest on the sector.

News flow supporting the sector: (1) The awards of Sg Buloh land parcels and the subsequent farming out of the sub- divided land parcels to various developers; (2) The increased sentiment and interest in land and properties in Iskandar Malaysia on expectation of rising investment on improving ties between Malaysia and Singapore; and (3) Integrated MRT network to benefit property development along the rail lines.

Key risks for the sector: (1) Other regulatory risks; and (2) Country risk.

MREITs are back in flavour by foreigners, due to better investibility, attractive dividend yield and expected currency gain arising from the strengthening of ringgit.

43

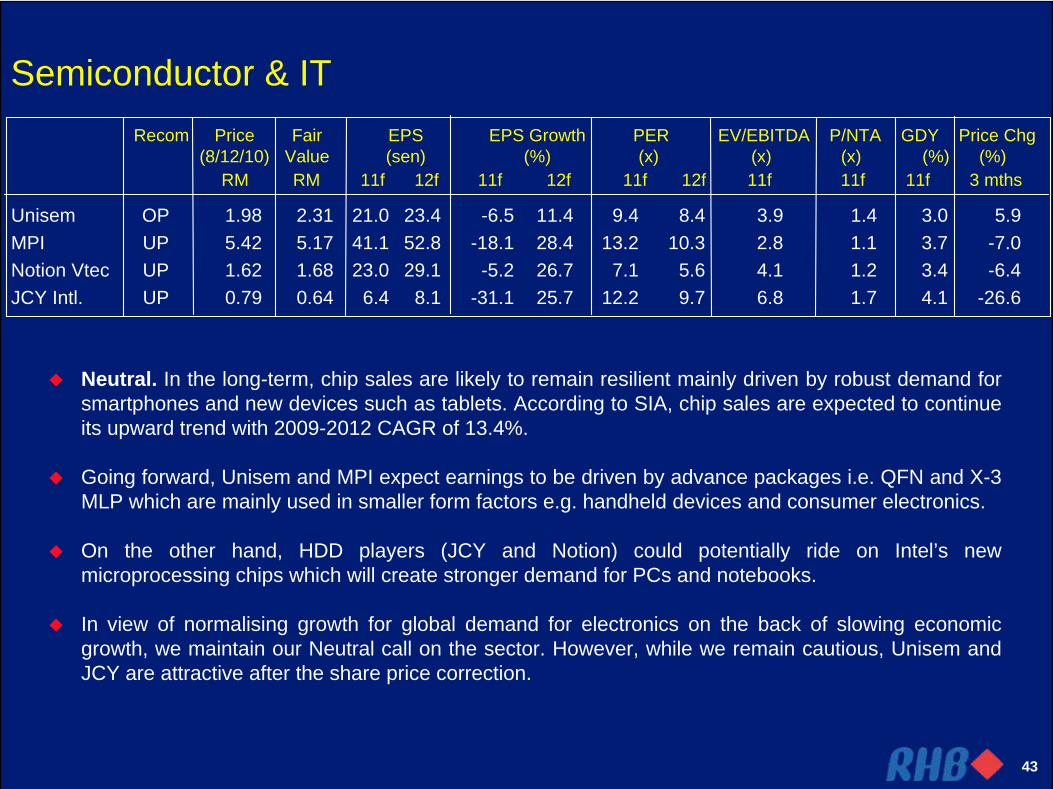

Semiconductor & IT

Unisem OP 1.98 2.31 21.0 23.4 -6.5 11.4 9.4 8.4 3.9 1.4 3.0 5.9MPI UP 5.42 5.17 41.1 52.8 -18.1 28.4 13.2 10.3 2.8 1.1 3.7 -7.0Notion Vtec UP 1.62 1.68 23.0 29.1 -5.2 26.7 7.1 5.6 4.1 1.2 3.4 -6.4JCY Intl. UP 0.79 0.64 6.4 8.1 -31.1 25.7 12.2 9.7 6.8 1.7 4.1 -26.6

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

Neutral. In the long-term, chip sales are likely to remain resilient mainly driven by robust demand for smartphones and new devices such as tablets. According to SIA, chip sales are expected to continue its upward trend with 2009-2012 CAGR of 13.4%.

Going forward, Unisem and MPI expect earnings to be driven by advance packages i.e. QFN and X-3 MLP which are mainly used in smaller form factors e.g. handheld devices and consumer electronics.

On the other hand, HDD players (JCY and Notion) could potentially ride on Intel’s new microprocessing chips which will create stronger demand for PCs and notebooks.

In view of normalising growth for global demand for electronics on the back of slowing economic growth, we maintain our Neutral call on the sector. However, while we remain cautious, Unisem and JCY are attractive after the share price correction.

44

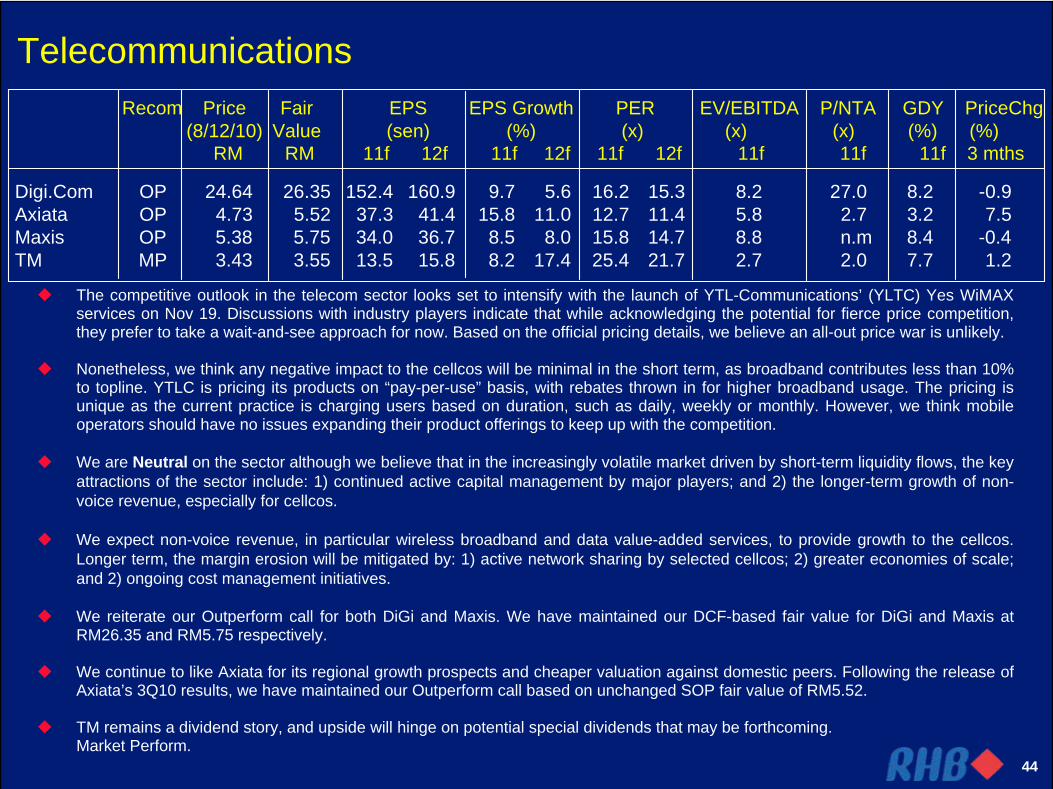

Telecommunications

Digi.Com OP 24.64 26.35 152.4 160.9 9.7 5.6 16.2 15.3 8.2 27.0 8.2 -0.9Axiata OP 4.73 5.52 37.3 41.4 15.8 11.0 12.7 11.4 5.8 2.7 3.2 7.5Maxis OP 5.38 5.75 34.0 36.7 8.5 8.0 15.8 14.7 8.8 n.m 8.4 -0.4TM MP 3.43 3.55 13.5 15.8 8.2 17.4 25.4 21.7 2.7 2.0 7.7 1.2

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY PriceChg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

The competitive outlook in the telecom sector looks set to intensify with the launch of YTL-Communications’ (YLTC) Yes WiMAX services on Nov 19. Discussions with industry players indicate that while acknowledging the potential for fierce price competition, they prefer to take a wait-and-see approach for now. Based on the official pricing details, we believe an all-out price war is unlikely.

Nonetheless, we think any negative impact to the cellcos will be minimal in the short term, as broadband contributes less than 10% to topline. YTLC is pricing its products on “pay-per-use” basis, with rebates thrown in for higher broadband usage. The pricing is unique as the current practice is charging users based on duration, such as daily, weekly or monthly. However, we think mobile operators should have no issues expanding their product offerings to keep up with the competition.

We are Neutral on the sector although we believe that in the increasingly volatile market driven by short-term liquidity flows, the key attractions of the sector include: 1) continued active capital management by major players; and 2) the longer-term growth of non- voice revenue, especially for cellcos.

We expect non-voice revenue, in particular wireless broadband and data value-added services, to provide growth to the cellcos. Longer term, the margin erosion will be mitigated by: 1) active network sharing by selected cellcos; 2) greater economies of scale; and 2) ongoing cost management initiatives.

We reiterate our Outperform call for both DiGi and Maxis. We have maintained our DCF-based fair value for DiGi and Maxis at RM26.35 and RM5.75 respectively.

We continue to like Axiata for its regional growth prospects and cheaper valuation against domestic peers. Following the release of Axiata’s 3Q10 results, we have maintained our Outperform call based on unchanged SOP fair value of RM5.52.

TM remains a dividend story, and upside will hinge on potential special dividends that may be forthcoming. Market Perform.

45

Timber

^ FY10& FY11 refer to FY11 & FY12 forecasts

Jaya Tiasa^ OP 4.09 4.83 47.7 52.0 65.5 8.9 8.6 7.9 6.3 0.9 0.0 15.5Ta Ann OP 4.75 5.92 46.4 54.9 53.2 18.3 10.2 8.7 6.6 1.4 3.3 3.4Evergreen OP 1.38 2.57 25.7 26.4 12.2 2.6 5.4 5.2 4.5 0.8 7.2 -10.4WTKH OP 1.16 1.44 12.0 14.9 57.2 24.0 9.6 7.8 5.9 0.6 4.0 3.6

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY PriceChg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Improvement in Japan’s housing starts has further gained momentum in August and September 2010, recording a better-than-expected yoy growth of 20.5% and 17.5% respectively. Building permits for August 2010 were also encouraging with a 19.3% yoy growth.

According to latest Japan Lumber report in Oct, tropical logs prices continue to firm up as supply of logs remains tight, while demand from India is still very strong. For tropical plywood, average selling prices are also climbing up on the back of steady demand from Japan. Besides that, timber companies which have significant oil palm plantations such as Jaya Tiasa and Ta Ann are also set to benefit from the current rising CPO prices.

Our top pick now is Jaya Tiasa. We expect strong earnings growth for Jaya Tiasa going forward due to the sharp increase in FFB production owing to increasing mature hectarage. There is going to be a significant change to Jaya Tiasa’s earnings profile, where its plantation division will contribute about 78-83% of earnings from FY04/11 onwards (from only about 44% in FY04/10). In addition, earnings from its timber division are also improving on the back of higher selling price for logs (due to strong demand from India) and firmer selling prices for plywood.

46

Transport / Logistics

^ FY11 & FY12 refer to FY12 & FY13 forecasts

ILB OP 1.01 1.47 11.3 14.3 95.3 26.0 8.9 7.1 7.9 0.5 3.0 7.4Freight Mgmt OP 0.98 1.57 15.4 16.0 13.8 4.2 6.4 6.1 3.9 1.1 5.6 3.7MAHB OP 6.22 8.02 44.9 49.9 20.5 11.3 13.9 12.5 10.3 3.3 3.2 15.2AirAsia UP 2.72 2.10 17.5 18.2 -23.9 4.3 15.6 14.9 11.5 2.0 0.0 47.8MAS UP 2.04 1.91 13.6 16.1 n.a. 18.1 15.0 12.7 10.5 1.9 0.0 -9.3MISC ^ UP 8.45 8.14 39.7 47.4 12.4 19.3 21.3 17.8 12.3 1.6 4.4 -4.0

Recom Price Fair EPS EPS Growth PER EV/EBITDA P/NTA GDY Price Chg(8/12/10) Value (sen) (%) (x) (x) (x) (%) (%)

RM RM 11f 12f 11f 12f 11f 12f 11f 11f 11f 3 mths

Underweight. The outlook for the local low-cost air travel sector has turned cloudy with MAS’s decision to expand its 100%-owned Firefly into a full-fledged low-cost carrier, backed by a fleet of 30 fuel-efficient 189-seater Next Generation 737-800 aircraft by 2015 that gives Firefly the firepower to compete head-on with AirAsia’s A320 fleet.

We expect Firefly, a new entrant (to the jet segment), to go all out to capture market share at the expense of profitability by heavy price discounting while AirAsia may also want nip the competition in the bud by dropping fares. A full-scale price will weigh down on yields of both players.

MAHB offers investors exposure to the booming air travel sector. It stands to gain from the price war between AirAsia and Firefly as passenger volume increases as airlines drop fares.

The shipping sector will continue to be weighed down by weak freight rates on the back of just a mild recovery in volumes while new capacity continues to flood the market.

One key speed bump to the recovery of the transportation and logistics sector as a whole is rising crude oil prices that could crimp margins.

47

THANK YOU