market outlook - sbi funds outlook_july 2017.pdf · indian stock market snapshot: june 2017 ....

TRANSCRIPT

Market Outlook

July 2017

EQUITY MARKET

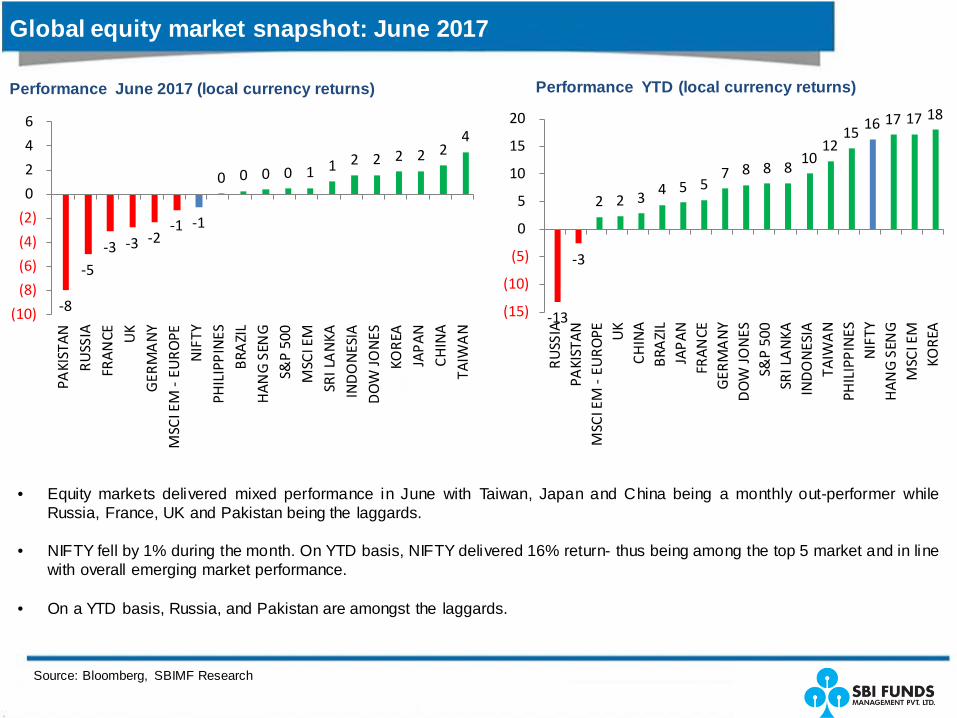

Global equity market snapshot: June 2017

Source: Bloomberg, SBIMF Research

• Equity markets delivered mixed performance in June with Taiwan, Japan and China being a monthly out-performer while Russia, France, UK and Pakistan being the laggards.

• NIFTY fell by 1% during the month. On YTD basis, NIFTY delivered 16% return- thus being among the top 5 market and in line with overall emerging market performance.

• On a YTD basis, Russia, and Pakistan are amongst the laggards.

Performance June 2017 (local currency returns) Performance YTD (local currency returns)

-8

-5 -3 -3 -2

-1 -1

0 0 0 0 1 1 2 2 2 2 2 4

(10)

(8)

(6)

(4)

(2)

0

2

4

6

PAKI

STAN

RUSS

IAFR

ANCE U

KG

ERM

AN

YM

SCI E

M -

EURO

PEN

IFTY

PHIL

IPPI

NES

BRA

ZIL

HAN

G S

ENG

S&P

500

MSC

I EM

SRI L

AN

KAIN

DO

NES

IAD

OW

JON

ESKO

REA

JAPA

NCH

INA

TAIW

AN

-13

-3

2 2 3 4 5 5 7 8 8 8

10 12

15 16 17 17 18

(15)

(10)

(5)

0

5

10

15

20

RUSS

IAPA

KIST

ANM

SCI E

M -

EURO

PE UK

CHIN

ABR

AZI

LJA

PAN

FRAN

CEG

ERM

AN

YD

OW

JON

ESS&

P 50

0SR

I LA

NKA

IND

ON

ESIA

TAIW

AN

PHIL

IPPI

NES

NIF

TYH

ANG

SEN

GM

SCI E

MKO

REA

Indian stock market snapshot: June 2017

Performance in June 2017

Source: Bloomberg, SBIMF Research

• Nifty and Sensex are down by 1% each in June. Performance down the capitalization curve was mildly positive with Mid Cap and Small Cap Index rising 0.1% and 2% respectively.

• Sector-wise: Real Estate and Pharma outshined during the month, while Oil& Gas, PSU and IT under-performed.

• YTD, Nifty and Sensex are up by 16% each. Sector-wise performance has been positive across all sectors on a YTD basis (barring Pharma and IT). Real estate has out-performed significantly (up 62%.)

Performance YTD

-7 -7

-4 -3 -3

-1 -1 -1 -1 0

0 1

2 3

5 6

(8)

(6)

(4)

(2)

0

2

4

6

8

OIL

& G

AS

PSU IT

AUTO

CAP

GO

OD

S

NIF

TY

BAN

KEX

BSE

100

SEN

SEX

BSE

500

MID

CAP

MET

ALS

SMAL

L CA

P

FMCG

PHAR

MA

REAL

EST

ATE

-4 -3

5 9

13 16 16 16 17 19 22

25 27 28 28

62

(10)

0

10

20

30

40

50

60

70

PHAR

MA IT

PSU

OIL

& G

AS

MET

ALS

AUTO

SEN

SEX

NIF

TY

BSE

100

BSE

500

MID

CAP

CAP

GO

OD

S

BAN

KEX

SMAL

L CA

P

FMCG

REAL

EST

ATE

Source: CMIE, SBIMF Research,

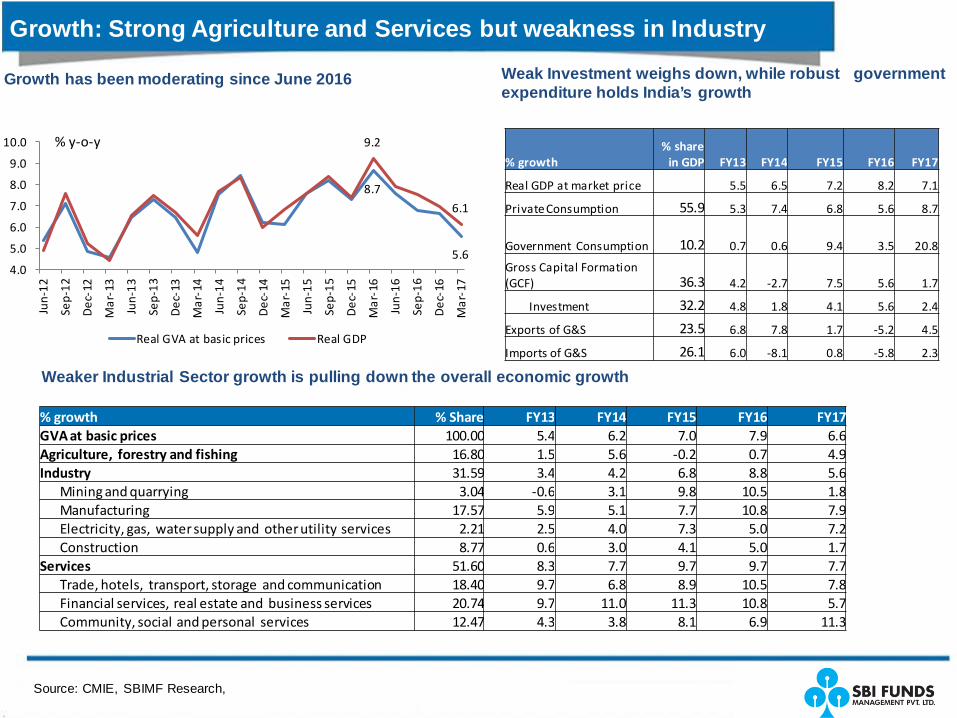

Growth: Strong Agriculture and Services but weakness in Industry

Growth has been moderating since June 2016

Weaker Industrial Sector growth is pulling down the overall economic growth

8.7

5.6

9.2

6.1

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Real GVA at basic prices Real GDP

% y-o-y

% growth % Share FY13 FY14 FY15 FY16 FY17 GVA at basic prices 100.00 5.4 6.2 7.0 7.9 6.6 Agriculture, forestry and fishing 16.80 1.5 5.6 -0.2 0.7 4.9 Industry 31.59 3.4 4.2 6.8 8.8 5.6 Mining and quarrying 3.04 -0.6 3.1 9.8 10.5 1.8 Manufacturing 17.57 5.9 5.1 7.7 10.8 7.9 Electricity, gas, water supply and other utility services 2.21 2.5 4.0 7.3 5.0 7.2 Construction 8.77 0.6 3.0 4.1 5.0 1.7 Services 51.60 8.3 7.7 9.7 9.7 7.7 Trade, hotels, transport, storage and communication 18.40 9.7 6.8 8.9 10.5 7.8 Financial services, real estate and business services 20.74 9.7 11.0 11.3 10.8 5.7 Community, social and personal services 12.47 4.3 3.8 8.1 6.9 11.3

% growth % share

in GDP FY13 FY14 FY15 FY16 FY17

Real GDP at market price 5.5 6.5 7.2 8.2 7.1

Private Consumption 55.9 5.3 7.4 6.8 5.6 8.7

Government Consumption 10.2 0.7 0.6 9.4 3.5 20.8

Gross Capital Formation (GCF) 36.3 4.2 -2.7 7.5 5.6 1.7

Investment 32.2 4.8 1.8 4.1 5.6 2.4

Exports of G&S 23.5 6.8 7.8 1.7 -5.2 4.5

Imports of G&S 26.1 6.0 -8.1 0.8 -5.8 2.3

Weak Investment weighs down, while robust government expenditure holds India’s growth

Source: CMIE, pib.nic.in, SBIMF Research,

Agriculture: Sowing data paints favourable prospects

Agriculture production (mn tonnes) Foodgrains Oilseeds Sugar Cane Horticulture FY06 209 28 281 183 FY07 217 24 356 192 FY08 231 30 348 211 FY09 234 28 285 215 FY10 218 25 292 223 FY11 244 32 342 241 FY12 259 30 361 257 FY13 257 31 341 269 FY14 265 32 352 277 FY15 252 27 362 278 FY16 (final estimate) 252 22 348 286 FY17 (3rd estimate) 273 33 306 287 % CAGR between FY06 to FY16 1.9 -2.3 2.2 4.6 % growth in FY16 -0.2 -16.6 -3.8 3.0 % growth in FY17 8.7 46.2 -12.2 0.5

FY17 Food grains and oilseeds showed a record production growth of 8.7% and 46% respectively. Horticulture was flat while Sugarcane production fell

Continued improvement in FY18 sowing (+9% period to Date) bodes well for Agricultural output , but…

Crop Sowing (in lakh hectare) as of 7th July Area sown in FY18 Area sown in FY17 Rice 79.8 75.3 Pulses 44.1 35.9 Coarse Cereals 80.8 70.1 Oilseeds 72.9 69.7 Sugarcane 47.9 45.2 Jute & Mesta 7.0 7.3 Cotton 71.8 67.9 Total 404.3 371.4

…falling food prices somewhat dents the rise in agricultural income

-2 -5

0

5

10

15

20

May

-13

Aug

-13

Nov

-13

Feb-

14

May

-14

Aug

-14

Nov

-14

Feb-

15

May

-15

Aug

-15

Nov

-15

Feb-

16

May

-16

Aug

-16

Nov

-16

Feb-

17

May

-17

WPI: Food (% y-o-y)

Source: CMIE, SBIMF Research,

Rural Demand to pick-up

Rural wages are gradually rising

• Rural demand had weakened owing to unfavourable weather conditions in FY15 and FY16 leading to the pile-up in agri-debt, fall in rural wages and falling construction activities.

• Situation seems to be turning at the margin. Agricultural income improved in FY17 due to increased agricultural output. For FY18 as well, the outlook on monsoon and sowing is favourable.

• Construction activities are also improving due to pick-up in rural road projects, irrigation projects and Increased execution of housing for all under PMAY- Gramin.

• Government has also increased its allocation to MGNREGA this year

• Farm loan waiver has gained traction. So far loan waivers up to 1% of GDP has already been announced. It is an unfavourable development from the overall macro perspective as it spoils the credit culture, can be inflationary and puts pressure on the government deficit. However, from rural perspective it alleviates some of the debt concerns in the rural area and frees up the income for consumption spending, albeit with a lag.

6.1

6.9

3.03.54.04.55.05.56.06.57.07.5

Non-agricultural occupations : Contruction workers (% y-o-y)

Rural wages (% y-o-y)

Higher allocation under MGNREGA by government

335 358

292 303 330 325

373

445 480

-25.0-20.0-15.0-10.0-5.00.05.010.015.020.025.0

-

100

200

300

400

500

600

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17RE FY18BE

MGNREGA Spend (Rs. Billion) % y-o-y- RHS

Source: CMIE, SBIMF Research, NB: * AP and Telangana started their waiver program in 2014- spread over 4 years

Farm Loan waiver

• The timing of the 2008 loan waiver was commensurate with many other measures by the government such as implementation of 6th Pay commission, launching of MGNREGA scheme, tax incentives, double digit growth in MSP. At the same time, food prices were rising exponentially, implementation of MGNREGA had led to a double digit growth in rural wages. All this together led to nearly 40% rise in average monthly expenditure of rural households. In this round, while we do expect some consumption stimulus in the rural economy from the loan waiver and many other on-going developments (road construction, PMAY-G, higher devolvement under MGNREGA, increased food production), we do not expect the consumption boost of a similar scale this time as most of the other fire-powers are missing (muted MSP hikes, modest growth in rural wages, weak food prices).

2008 Farm Loan Waiver 2017 Farm Loan Waiver

Implementing body

Central government at Pan India level 7 States so far (UP, Maharashtra, Punjab, Karnataka, Tamil Nadu, AP*, Telangana*)

Announcement Period

Feb 2008 AP, Telangana- 2014; UP- April 2017; Tamil Nadu- January 2017; Maharashtra, Punjab, Karnataka- June 2017

Completion Period

Dec 2010 AP and Telangana has commenced paying the banks, rest of the states yet to commence

Amount Involved Announcement of: Rs. 717 billion (1.6% GDP, 8.3% Agri GDP) Actual disbursement: Rs. 525 billion (1.2% GDP, 6.1% Agri GDP)

Announcement: Rs. 1,380 billion (1% of GDP, 5% of Agri GDP) Actual disbursement: To be seen

No. of Beneficiaries

~37 million (26% of total farmer families in India) ~ 40 million (expected, but restricted to farmers of the 7 states)

Average / farmer ~Rs. 14,000 Rs. 34,000 (expected)

Impact: • Additional fiscal burden of 1.2% spread over FY09 to FY11,

• Loan waiver along with other developments led to ~40% increase in agriculture families’ consumption expenditure (impact most pronounced in jewellery and consumer durable spending)

• No impact on bank Agriculture loan growth

• Expect State Fiscal deficit to be impacted by 50 bps over FY18 and FY19 (over and above the accounted) accompanied with 70bps decrease in FY17 capital expenditure (vs. budgeted)

• Marginal increase in consumption expenditure • Initial signs of weakness Agriculture credit growth seen

Source: CMIE, SBIMF Research,

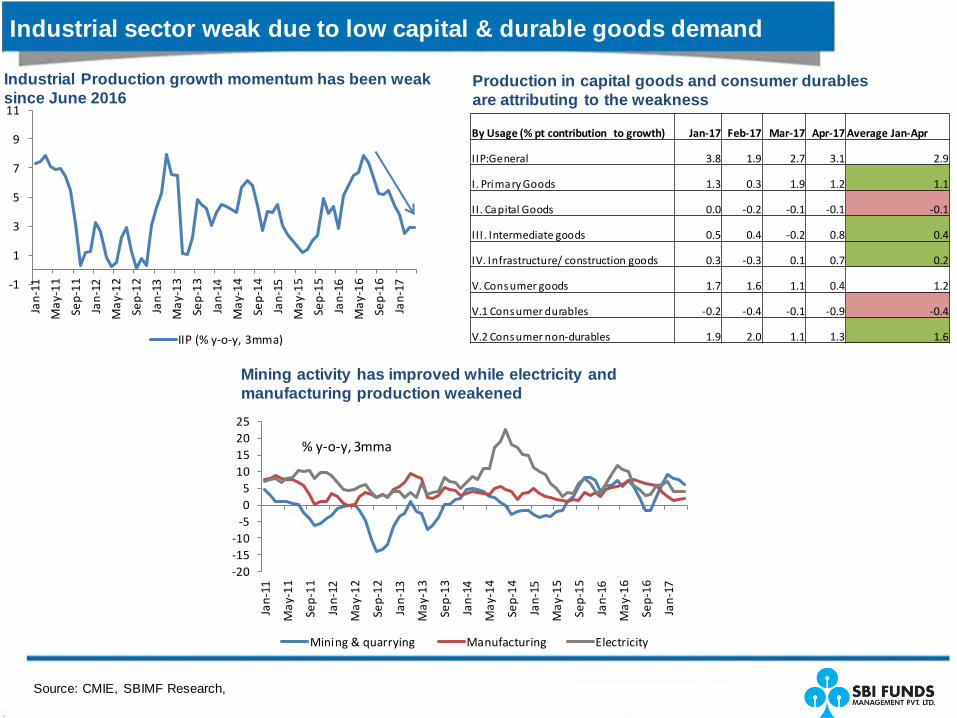

Industrial sector weak due to low capital & durable goods demand

-1

1

3

5

7

9

11

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

May

-15

Sep-

15

Jan-

16

May

-16

Sep-

16

Jan-

17

IIP (% y-o-y, 3mma)

By Usage (% pt contribution to growth) Jan-17 Feb-17 Mar-17 Apr-17 Average Jan-Apr

I IP:General 3.8 1.9 2.7 3.1 2.9

I . Primary Goods 1.3 0.3 1.9 1.2 1.1

I I . Capital Goods 0.0 -0.2 -0.1 -0.1 -0.1

I I I . Intermediate goods 0.5 0.4 -0.2 0.8 0.4

IV. Infrastructure/ construction goods 0.3 -0.3 0.1 0.7 0.2

V. Consumer goods 1.7 1.6 1.1 0.4 1.2

V.1 Consumer durables -0.2 -0.4 -0.1 -0.9 -0.4

V.2 Consumer non-durables 1.9 2.0 1.1 1.3 1.6

Industrial Production growth momentum has been weak since June 2016

Production in capital goods and consumer durables are attributing to the weakness

-20-15-10

-505

10152025

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

May

-15

Sep-

15

Jan-

16

May

-16

Sep-

16

Jan-

17

Mining & quarrying Manufacturing Electricity

% y-o-y, 3mma

Mining activity has improved while electricity and manufacturing production weakened

Source: CMIE, SBIMF Research,

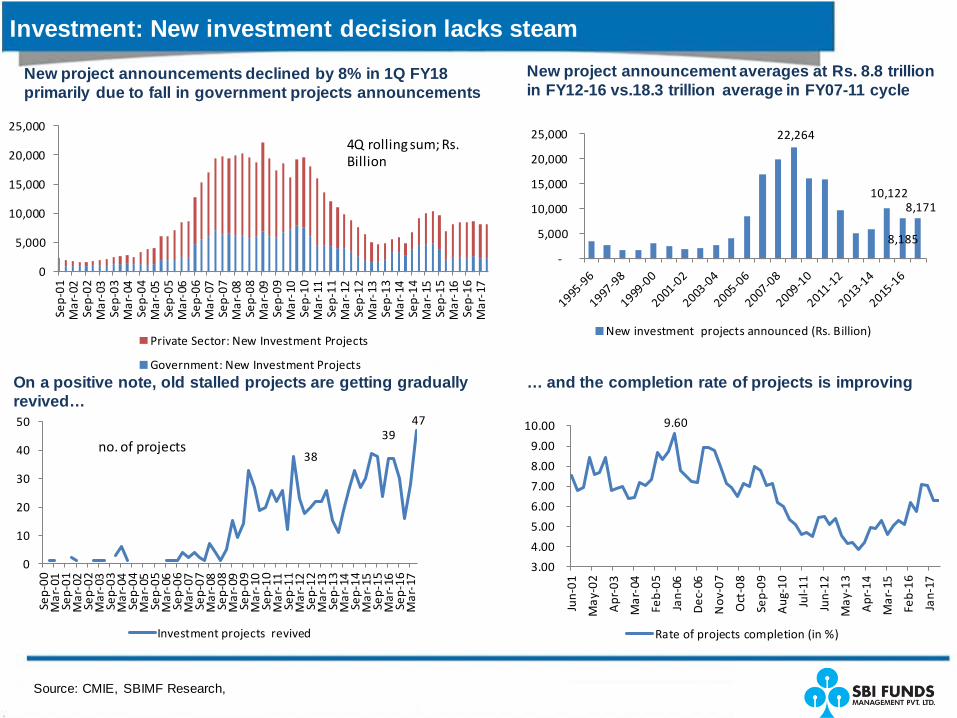

Investment: New investment decision lacks steam

0

5,000

10,000

15,000

20,000

25,000

Sep-

01M

ar-0

2Se

p-02

Mar

-03

Sep-

03M

ar-0

4Se

p-04

Mar

-05

Sep-

05M

ar-0

6Se

p-06

Mar

-07

Sep-

07M

ar-0

8Se

p-08

Mar

-09

Sep-

09M

ar-1

0Se

p-10

Mar

-11

Sep-

11M

ar-1

2Se

p-12

Mar

-13

Sep-

13M

ar-1

4Se

p-14

Mar

-15

Sep-

15M

ar-1

6Se

p-16

Mar

-17

Private Sector: New Investment Projects

Government: New Investment Projects

4Q rolling sum; Rs. Billion

New project announcements declined by 8% in 1Q FY18 primarily due to fall in government projects announcements

22,264

10,122

8,185

8,171

-

5,000

10,000

15,000

20,000

25,000

New investment projects announced (Rs. Billion)

New project announcement averages at Rs. 8.8 trillion in FY12-16 vs.18.3 trillion average in FY07-11 cycle

On a positive note, old stalled projects are getting gradually revived…

… and the completion rate of projects is improving

9.60

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Jun-

01

May

-02

Apr

-03

Mar

-04

Feb-

05

Jan-

06

Dec

-06

Nov

-07

Oct

-08

Sep-

09

Aug

-10

Jul-1

1

Jun-

12

May

-13

Apr

-14

Mar

-15

Feb-

16

Jan-

17

Rate of projects completion (in %)

38

39 47

0

10

20

30

40

50

Sep-

00M

ar-0

1Se

p-01

Mar

-02

Sep-

02M

ar-0

3Se

p-03

Mar

-04

Sep-

04M

ar-0

5Se

p-05

Mar

-06

Sep-

06M

ar-0

7Se

p-07

Mar

-08

Sep-

08M

ar-0

9Se

p-09

Mar

-10

Sep-

10M

ar-1

1Se

p-11

Mar

-12

Sep-

12M

ar-1

3Se

p-13

Mar

-14

Sep-

14M

ar-1

5Se

p-15

Mar

-16

Sep-

16M

ar-1

7

Investment projects revived

no. of projects

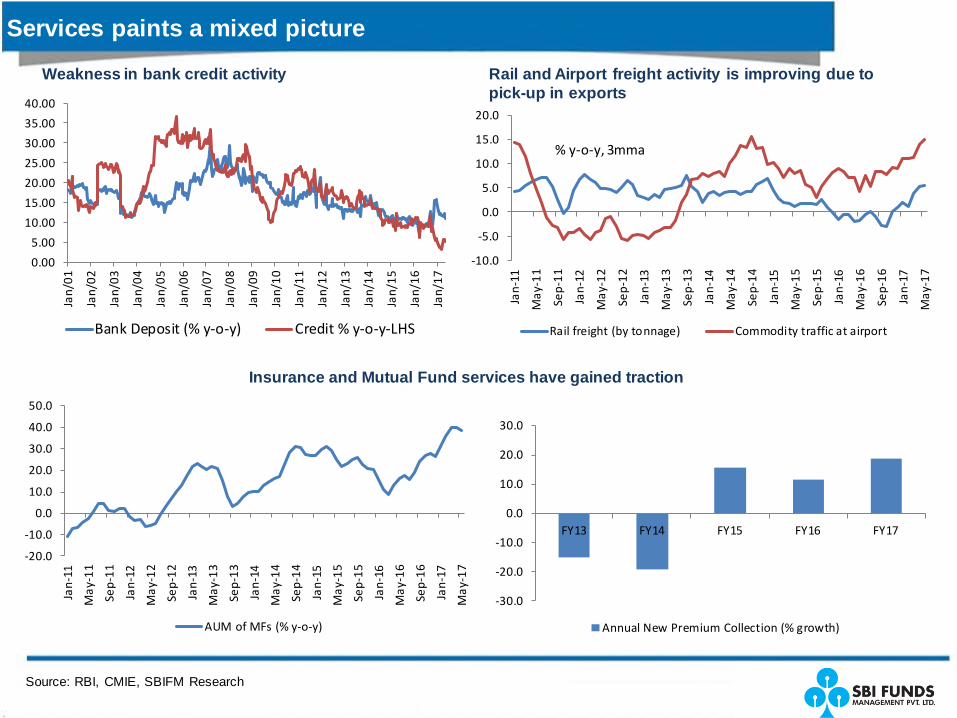

Services paints a mixed picture

Source: RBI, CMIE, SBIFM Research

Weakness in bank credit activity Rail and Airport freight activity is improving due to pick-up in exports

Insurance and Mutual Fund services have gained traction

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

FY13 FY14 FY15 FY16 FY17

Annual New Premium Collection (% growth)

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

Jan/

01

Jan/

02

Jan/

03

Jan/

04

Jan/

05

Jan/

06

Jan/

07

Jan/

08

Jan/

09

Jan/

10

Jan/

11

Jan/

12

Jan/

13

Jan/

14

Jan/

15

Jan/

16

Jan/

17

Bank Deposit (% y-o-y) Credit % y-o-y-LHS

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

May

-15

Sep-

15

Jan-

16

May

-16

Sep-

16

Jan-

17

May

-17

Rail freight (by tonnage) Commodity traffic at airport

% y-o-y, 3mma

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

May

-15

Sep-

15

Jan-

16

May

-16

Sep-

16

Jan-

17

May

-17

AUM of MFs (% y-o-y)

Source: CBEC, Ministry of Rural Development, Elara Securities, SBIMF Research; NB: Based of 1482 items under the HS Code classification as of 11th June; Does not include additional cess which has been imposed on 55 items so far

Reforms by government makes market positive about future growth

GST: Government finalized the rates on all items and most items will attract an effective tax rate of less than 18%*

Tax Rate # Items

0% 9.6% of the items

5% 19.9% of the items

12% 16.6% of the items

18% 37.7% of the items

28% 16.1% of the items

Affordable Housing Vision of the government picks up pace

1080 1083 1182

1803

3200

5100 5100

0

1000

2000

3000

4000

5000

6000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E

No. of Rural HousingCompleted (in '000)

Key Reforms in recent months • Affordable Housing picks-up pace: The government has targeted construction of 51 lakh houses in 2017-18 that would

meet its target of one crore houses by 2019 under the revised Pradhan Mantri Awaas Yojana Gramin (PMAY-G) and hopes to bring down the building time to 6-12 months from 18 months to 3 years earlier. Over 32 lakh houses have been reported complete in FY17 and 18 lakh in FY16.

• Real Estate Regulation Act: was implemented on a nation-wide basis on 1st May. RERA ensures that there is enough long term visibility for players with strong corporate governance, brand and capital allocation standards

• Ordinance to speed up NPA resolution: Government has passed an ordinance to empower the RBI to setup oversight committees and giving immunity to bankers. This is a positive move for clearing stressed loans which are 13% of total loans.

Government Infrastructure push positive for growth

Source: Spark, Government documents, SBIFM Research

299 384 386

932

1307 1432

0

200

400

600

800

1000

1200

1400

1600

FY13 FY14 FY15 FY16 FY17RE FY18BE

Road infra (Rs. Billion)

Spending on Road construction has jumped 3.7x times in last 3 years

Execution has picked up pace in Road construction

492 520 643

935

1210 1310

0

200

400

600

800

1000

1200

1400

FY13 FY14 FY15 FY16 FY17RE FY18BE

Railways infra (Rs. Billion)

Spending on Railways has jumped 2 times in last 3 years

Railways- another key area of spend

55

90 84

121

196 199

0

50

100

150

200

250

FY13 FY14 FY15 FY16 FY17RE FY18BE

Metro and MRTS Projects

Metro spending projected to grow at 12%

Metro construction happening in partnership with states and JICA

980 960 1059 1145

1441 1565

0

500

1000

1500

2000

FY13 FY14 FY15 FY16 FY17RE FY18BE

Rural and Agri Spending

Irrigation and Rural Development

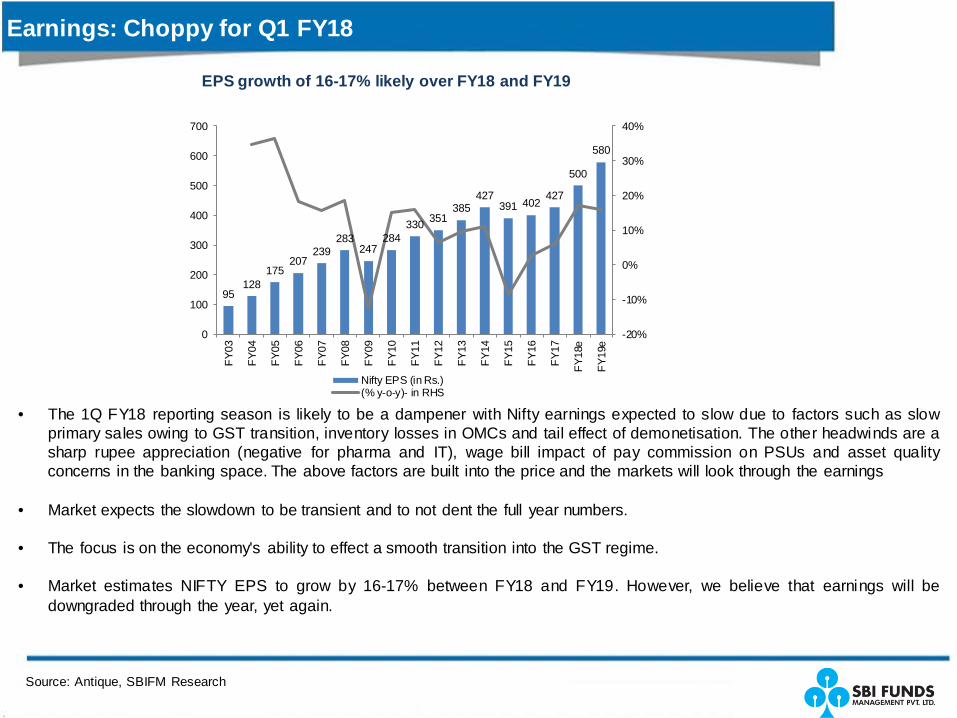

Earnings: Choppy for Q1 FY18

Source: Antique, SBIFM Research

EPS growth of 16-17% likely over FY18 and FY19

• The 1Q FY18 reporting season is likely to be a dampener with Nifty earnings expected to slow due to factors such as slow primary sales owing to GST transition, inventory losses in OMCs and tail effect of demonetisation. The other headwinds are a sharp rupee appreciation (negative for pharma and IT), wage bill impact of pay commission on PSUs and asset quality concerns in the banking space. The above factors are built into the price and the markets will look through the earnings

• Market expects the slowdown to be transient and to not dent the full year numbers.

• The focus is on the economy's ability to effect a smooth transition into the GST regime.

• Market estimates NIFTY EPS to grow by 16-17% between FY18 and FY19. However, we believe that earnings will be downgraded through the year, yet again.

95 128

175 207

239 283

247 284

330 351 385

427 391 402

427

500

580

-20%

-10%

0%

10%

20%

30%

40%

0

100

200

300

400

500

600

700

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

e

FY19

e

Nifty EPS (in Rs.)(% y-o-y)- in RHS

Source: Morgan Stanley, SBIMF Research,

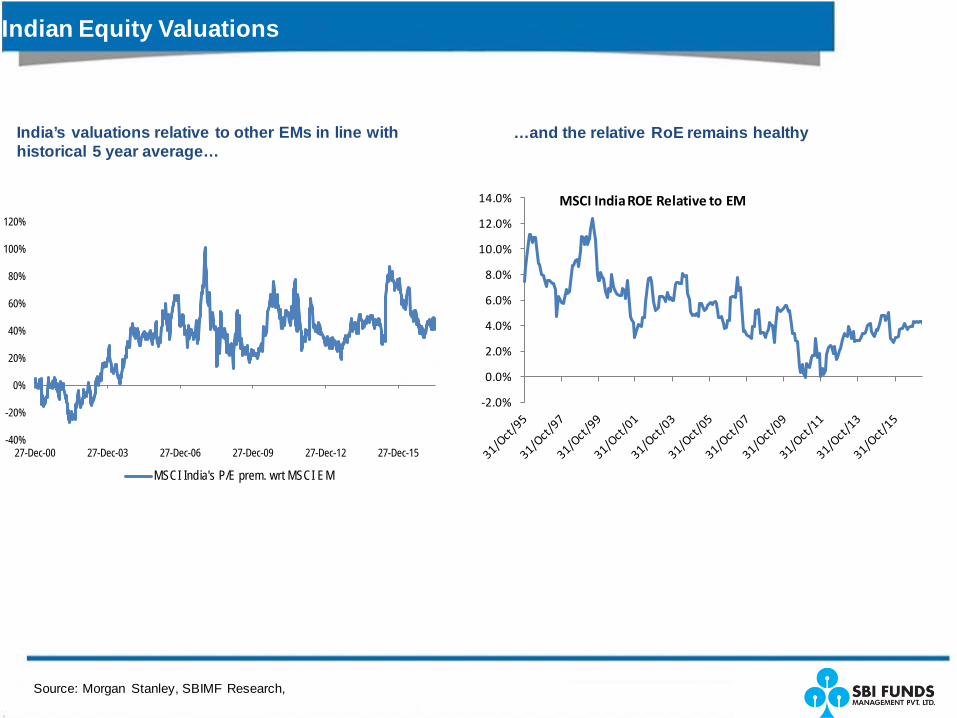

Indian Equity Valuations

India’s valuations relative to other EMs in line with historical 5 year average…

…and the relative RoE remains healthy

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0% MSCI India ROE Relative to EM

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

27-Dec-00 27-Dec-03 27-Dec-06 27-Dec-09 27-Dec-12 27-Dec-15

MSCI India's P/E prem. wrt MSCI EM

Liquidity: Robust inflow from FIIs and Domestic Mutual Fund

Source: MOSL NSDL, SBIMF Research

FIIs have invested US$ 23 billion in India YTD, of which ~US$ 8.5 billion is invested in Indian equity market

Domestic Mutual Funds, too, continue to pump money in the Indian equity market

Insurance companies, however, have been a net seller in the India equity market

8.4 10.4

3.2

-0.1

6.6

4.1

6.2

3.5 2.3

6.0

0.2

-2.6

-0.3

1.2 1.7

4.6

-4.6

6.6

1.8

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

June

-16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

-1.4 -1.4 -1.0

-0.6 -0.8 -1.3

0.1

2.7 2.4 1.5

3.7 3.9

2.1

0.4 1.0 1.0

4.7

1.7

4.6

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

June

-16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

-2.1

-4.9

-0.3 -0.2

-3.9

-0.9

-2.8 -3.0

-2.0 -2.4

1.3

0.3

-0.1

0.5

-0.6

-2.2

0.5

-1.5

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

June

-16

Sep-

16

Dec

-16

Mar

-17

Equity Market outlook

• Indian equity market had depicted a gain of 16.3% in 1H 2017, albeit marginally less than emerging market returns of 17.2% (for MSCI-EM). The market fell 1% during the last month. That said, July started on a positive note as market cheered the country’s transition to Goods and Services tax (GST). As of 11th July, NIFTY stands at its historic al high of 9816.

• Real estate sector was among the best performing sector as RERA became effective from 1st May while IT and Pharma sectors were the laggards likely reflecting the effect of currency appreciation on these export oriented sectors.

• On the global front, while the key economies are expected to tighten their monetary policy, there is a rising expectations of fiscal stimulus - with infrastructure and defence spending likely to take the lead. Global trade cycle is also improving gradually.

• Locally, the country embarked on GST. While, the business face some implementation challenges in the first month of the new indirect tax regime, it is expected to lead to significant efficiency gains in the long run.

• RBI identified 12 large NPA accounts which require increased provisioning by the banks. Banks have also been asked to resolve 55 cases of bad loans within six months or refer to the Insolvency and Bankruptcy Code. Higher provisioning could lead to muted earnings for banks going ahead.

• Earnings over 1H FY18 could also be disrupted from the GST implementation, thus challenging the 20% of NIFTY earnings growth pencilled in by the market.

• Valuations are already rich owing primarily to robust equity market participation by FIIs and Domestic Mutual funds. FIIs have invested US$ 8.5 billion between Jan to June, while DIIs have invested US$ 3.4 billion during the same period.

• Sensex is trading around 19 times 1-year forward earnings as investors bet on the long-term growth potential of the economy. In such a scenario, we continue to remain focussed on bottom up stock picking.

Valuations are at +18 times on 1 year forward earnings

Source: Bloomberg, SBIMF Research

7.0

9.0

11.0

13.0

15.0

17.0

19.0

21.0

23.0

25.0

Feb/

06Ju

l/06

Dec

/06

May

/07

Oct

/07

Mar

/08

Aug

/08

Jan/

09Ju

n/09

Nov

/09

Apr

/10

Sep/

10Fe

b/11

Jul/

11D

ec/1

1M

ay/1

2O

ct/1

2M

ar/1

3A

ug/1

3Ja

n/14

Jun/

14N

ov/1

4A

pr/1

5Se

p/15

Feb/

16Ju

l/16

Dec

/16

Sensex 1Y fwd…

Mean: 16

+1 SD

-1 SD

FIXED INCOME MARKET

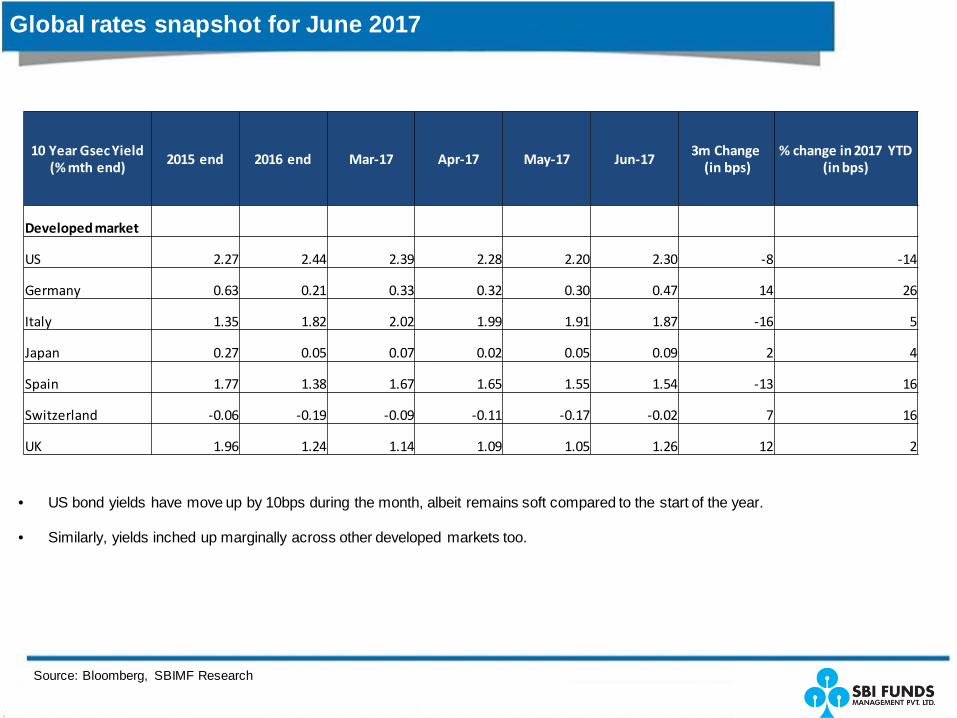

Global rates snapshot for June 2017

• US bond yields have move up by 10bps during the month, albeit remains soft compared to the start of the year.

• Similarly, yields inched up marginally across other developed markets too.

Source: Bloomberg, SBIMF Research

10 Year Gsec Yield (% mth end) 2015 end 2016 end Mar-17 Apr-17 May-17 Jun-17 3m Change

(in bps) % change in 2017 YTD

(in bps)

Developed market

US 2.27 2.44 2.39 2.28 2.20 2.30 -8 -14

Germany 0.63 0.21 0.33 0.32 0.30 0.47 14 26

Italy 1.35 1.82 2.02 1.99 1.91 1.87 -16 5

Japan 0.27 0.05 0.07 0.02 0.05 0.09 2 4

Spain 1.77 1.38 1.67 1.65 1.55 1.54 -13 16

Switzerland -0.06 -0.19 -0.09 -0.11 -0.17 -0.02 7 16

UK 1.96 1.24 1.14 1.09 1.05 1.26 12 2

Emerging Market Bond yields- June 2017

Source: Bloomberg, SBIMF Research

Bond yields depicts movements on both sides in the Emerging markets. Korea, Philippines and China depicted the rise in bond yields while bond yields fell or remain flat for other key EMs YTD

10 Year Gsec Yield (% mth end) 2015 end 2016 end Mar-17 Apr-17 May-17 Jun-17 3m Change

(in bps) % change in 2017 YTD

(in bps)

Emerging Market

Brazil 16.5 11.4 10.1 10.3 10.7 10.5 47 -87

China 2.8 3.0 3.3 3.5 3.6 3.6 28 53

India 7.8 6.5 6.7 7.0 6.7 6.5 -18 -2

Indonesia 8.7 7.9 7.0 7.0 6.9 6.8 -22 -112

Korea 2.1 2.1 2.2 2.2 2.2 2.2 3 14

Malaysia 4.2 4.2 4.1 4.0 3.9 3.9 -22 -27

Philippines 3.9 4.6 4.6 4.7 4.7 4.7 8 8

Russia 9.6 8.4 7.9 7.6 7.6 7.7 -22 -67

South Africa 9.8 8.9 8.9 8.7 8.6 8.8 -10 -14

Taiwan 1.0 1.2 1.1 1.0 1.0 1.1 -3 -13

Thailand 2.5 2.6 2.7 2.7 2.6 2.5 -21 -17

India Rates Snapshot for June 2017

• Indian bond yields continued to fall in June on account of soft inflation print and building hopes of rate cut by RBI.

• Money market rates, were mostly flat during the month as system liquidity continues to be ample.

• Crude oil prices fell sharply -7.9% over the month and -11.7% YTD.

• Rupee has appreciated sharply on YTD basis owing to massive FII inflows in the debt and equity market.

Source: Bloomberg, PPAC, CCIL, SBIMF Research; NB: **Crude oil price is average $/barrel for the month, rest of the data are % month end; *Corporate bond rate is for AAA rated bonds ,*** Refers to PSU Banks CD rate; # INR and Oil price changes are % change

Apr-17 May-17 Jun-17 m-o-m change (in bps) Change YTD (in bps)

1 Yr T-Bill 6.41 6.44 6.36 -9 3

3M T-Bill 6.18 6.28 6.29 0 9

10 year GSec 6.96 6.66 6.51 -15 0

3M CD*** 6.35 6.35 6.33 -2 5

12M CD*** 6.75 6.73 6.63 -10 0

3 Yr Corp Bond* 7.60 7.46 7.29 -17 0

5 Yr Corp Bond* 7.71 7.53 7.41 -12 4

10 Yr Corp Bond* 7.90 7.75 7.57 -18 -1

1 Yr IRS 6.52 6.42 6.25 -17 7

5 Yr IRS 6.82 6.57 6.29 -27 3

Overnight MIBOR Rate 6.18 6.25 6.25 0 0

INR/USD 64.2 64.5 64.6 -0.1 5.2#

Crude Oil Indian Basket** 52.6 50.6 46.6 -7.9 -11.7#

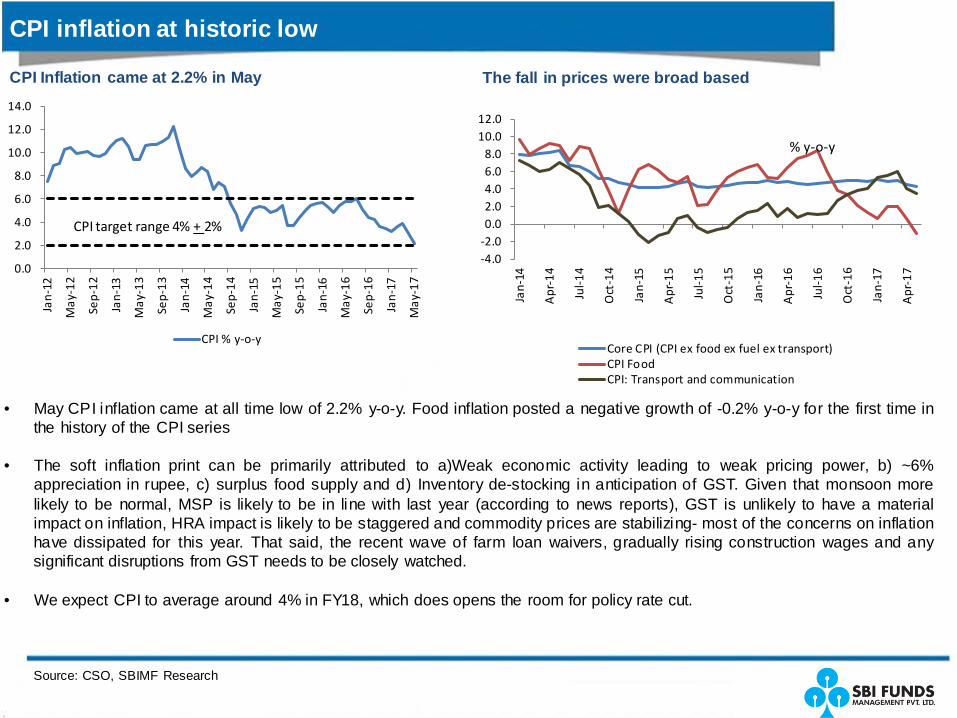

CPI inflation at historic low

Source: CSO, SBIMF Research

• May CPI inflation came at all time low of 2.2% y-o-y. Food inflation posted a negative growth of -0.2% y-o-y for the first time in the history of the CPI series

• The soft inflation print can be primarily attributed to a)Weak economic activity leading to weak pricing power, b) ~6% appreciation in rupee, c) surplus food supply and d) Inventory de-stocking in anticipation of GST. Given that monsoon more likely to be normal, MSP is likely to be in line with last year (according to news reports), GST is unlikely to have a material impact on inflation, HRA impact is likely to be staggered and commodity prices are stabilizing- most of the concerns on inflation have dissipated for this year. That said, the recent wave of farm loan waivers, gradually rising construction wages and any significant disruptions from GST needs to be closely watched.

• We expect CPI to average around 4% in FY18, which does opens the room for policy rate cut.

CPI Inflation came at 2.2% in May The fall in prices were broad based

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

May

-15

Sep-

15

Jan-

16

May

-16

Sep-

16

Jan-

17

May

-17

CPI % y-o-y

CPI target range 4% + 2%

-4.0-2.00.02.04.06.08.0

10.012.0

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Oct

-16

Jan-

17

Apr

-17

Core CPI (CPI ex food ex fuel ex transport)CPI FoodCPI: Transport and communication

% y-o-y

Source: Bloomberg, SBIMF Research,

Commodity prices pressures gradually easing

In 2015, all the commodities registered a price decline mainly due to China, global growth slowdown and excess capacity. In 2016, prices rose across most commodities (barring Uranium, wheat and corn)

Despite 2016 price rise, overall commodity index still far lower than 2014 highs

In 2017, price pressures seems to gradually easing as supply conditions respond to 2016 price rise

-25.0-20.0-15.0-10.0

-5.00.05.0

10.015.020.025.0

Iron

Ore

Suga

rW

TIG

asol

ine

Bren

tH

eati

ng O

ilG

as O

ilN

atur

al G

asCo

ffee

Nic

kel

Tin

Soyb

eans

Cott

onLe

adU

rani

umPl

atin

umCo

rnCo

alSi

lver

Zinc

Copp

erG

old

Alu

min

ium

Whe

atPa

lladi

um

% change YTD in 2017

-60.0-40.0-20.0

0.020.040.060.080.0

100.0% change in 2015 % change in 2016

90

110

130

150

170

190

210

230

Jan-

05

Sep-

05

May

-06

Jan-

07

Sep-

07

May

-08

Jan-

09

Sep-

09

May

-10

Jan-

11

Sep-

11

May

-12

Jan-

13

Sep-

13

May

-14

Jan-

15

Sep-

15

May

-16

Jan-

17

CRB Food Index CRB Commodity Index

Jan 2010=100

Liquidity overhang from demonetization to stay over the year

Source: RBI, SBIMF Research

• Overhang of liquidity consequent upon demonetization continues to weigh on money markets for nine months in succession.

• RBI has issued Rs. 1.9trillion of MSS and CMBs to mop-up the excess liquidity. Rs. 200 billion of OMO sales has announced in

July so far. Despite these measures, at +3 trillion, the banking system liquidity is ample.

• The robust foreign capital inflow had led RBI to build US$ 22 billion of reserves book in the spot market YTD (inclusive of revaluation gains/ losses) and US$ 13billion of short-term forward book. If the central bank is unable to roll-over the forward contracts, this will lead to additional liquidity injection through the year.

• Factoring in the current pace of weekly withdrawal and other stated dynamics, the system looks in a comfortable liquidity situation over the next couple of months, lest the RBI intervention gets more active.

Liquidity surplus averaged at Rs. 3.1 trillion during June The pace of currency withdrawal has slowed down in June 18.0

9

15.3

CIC beforedemonetization (Rs.

Trillion)

CIC on 6th Jan (thelowest point)

CIC as of 23rd June 2017

-4000

-2000

0

2000

4000

6000

8000

10000

Banking System Liquidity (Rs. Billion)

+1% of NDTL

-1% of NDTL

Overall external account is comfortable

Exports depicting a cyclical recovery and overall trade deficit is contained

Source: CMIE, RBI, SBIFM Research

Low trade deficit has helped Current Account deficit to stay below 2% of GDP

India’s Net FDI inflow sufficient to fund Current account deficit since FY15

FX reserves at US$ 387bn as of June end is sufficient to finance 11 months of import

-8.0 -7.0 -6.0 -5.0 -4.0 -3.0 -2.0 -1.0 -

-35.0

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

-

Mar

-11

Aug

-11

Jan-

12

Jun-

12

Nov

-12

Apr

-13

Sep-

13

Feb-

14

Jul-1

4

Dec

-14

May

-15

Oct

-15

Mar

-16

Aug

-16

Jan-

17

Current Account Balance (US$ bn) as % of GDP - RHS

0

5

10

15

20

25

30

1520253035404550

Jan-

10

Jun-

10

Nov

-10

Apr

-11

Sep-

11

Feb-

12

Jul-1

2

Dec

-12

May

-13

Oct

-13

Mar

-14

Aug

-14

Jan-

15

Jun-

15

Nov

-15

Apr

-16

Sep-

16

Feb-

17

Trade Deficit (USD bn)- RHS Exports (USD bn)

Imports (USD bn)

48

78 88

32 28 22

15

33

12 22 20 22

33 36 36 36

0

20

40

60

80

100

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

E

CAD FDI

USD bn

67891011121314

260

280

300

320

340

360

380

400

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12A

pr-1

2Ju

l-12

Oct

-12

Jan-

13A

pr-1

3Ju

l-13

Oct

-13

Jan-

14A

pr-1

4Ju

l-14

Oct

-14

Jan-

15A

pr-1

5Ju

l-15

Oct

-15

Jan-

16A

pr-1

6Ju

l-16

Oct

-16

Jan-

17A

pr-1

7

FX reserves (USD bn)- LHS Import cover (in months RHS)

Currency: Massive appreciation due to strong FII flows

Source: Bloomberg, SBIMF Research

Rupee depicted appreciation bias between Jan-June 2017 in line with other Emerging market currencies

DXY falls below 100 since April Rupee appreciated by 5.2% YTD and holds at~64-65 levels

-1.7 -1.6 -1.4

0.1 0.9 2.4 4.5 4.5 5.1 5.2 5.4 5.6 6.2 8.9 13.1 14.4

-30-25-20-15-10

-505

1015

Phili

ppin

e Pe

so

Braz

il Re

al

Colo

mbi

an P

eso

Turk

ey L

ira

Indo

nesi

an R

upia

h

Chin

ese

renm

inbi

Mal

aysi

an R

ingi

tt

Russ

ian

Roub

le

Afr

ican

Ran

d

Indi

an R

upee

Kore

an W

on

Thai

Bah

t

Taiw

anes

e D

olla

r

Hun

gari

an F

orin

t

Polis

h Zl

oty

Mex

ican

Pes

o

% change in 2014 % change in 2015 % change in 2016 % change YTD (June end)

5759616365676971

Jan-

14Fe

b-14

Mar

-14

Apr

-14

May

-14

Jun-

14Ju

l-14

Aug

-14

Sep-

14O

ct-1

4N

ov-1

4D

ec-1

4Ja

n-15

Feb-

15M

ar-1

5A

pr-1

5M

ay-1

5Ju

n-15

Jul-1

5A

ug-1

5Se

p-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16Fe

b-16

Mar

-16

Apr

-16

May

-16

Jun-

16Ju

l-16

Aug

-16

Sep-

16O

ct-1

6N

ov-1

6D

ec-1

6Ja

n-17

Feb-

17M

ar-1

7A

pr-1

7M

ay-1

7Ju

n-17

Indian Rupee

103

96

70

75

80

85

90

95

100

105

Jan-

05M

ay-0

5Se

p-05

Jan-

06M

ay-0

6Se

p-06

Jan-

07M

ay-0

7Se

p-07

Jan-

08M

ay-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

ay-1

0Se

p-10

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14M

ay-1

4Se

p-14

Jan-

15M

ay-1

5Se

p-15

Jan-

16M

ay-1

6Se

p-16

Jan-

17M

ay-1

7

DXY Index

In the last monetary policy (held in June), while the RBI kept the policy rate unchanged and stance neutral, the narratives were definitely less hawkish.

The central bank acknowledged the weaker than expected growth data

for 4Q as well as lower than expected inflation, but opined the need to have a more detailed study of both the prints.

Further, while acknowledging the lower inflation prints in recent months, the central bank continues to appear guarded. They cited that the food prices may be depicting a mixed impact of lingering effects of demonetization which have overlapped with excess food supply situation in some food items. These have contributed to the better-than-expected April inflation of 3%, but blur the future outlook on inflation.

Present stance of RBI factors in the lower inflation prints over the first half of FY17-18 (2.0-3.5%) and 2HFY18 inflation to range in 3.5-4.5%.

According to their media communication, the recent release of CSO revised series on IIP and WPI has likely impacted the growth estimates of the economy and need to be analysed in greater detail.

On balance, given the less-hawkish tone of the statement, it appears that unless the trends on inflation were to be reverse significantly, the ground has been laid for the MPC to sound more accommodative and deliver a rate cut during the year.

Policy Rate Outlook

Source: RBI, CSO, SBIFM Research

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Jun-

05

Mar

-06

Dec

-06

Sep-

07

Jun-

08

Mar

-09

Dec

-09

Sep-

10

Jun-

11

Mar

-12

Dec

-12

Sep-

13

Jun-

14

Mar

-15

Dec

-15

Sep-

16

Repo Rate (mth end, %)

Bond market dynamics have changed considerably in last two months primarily due to change in inflation trajectory.

The recent fall in food inflation has been unexpectedly acute. Favourable monsoon and sowing pattern thus far into the Kharif season, contained MSP announcement and weakness in global food prices adds to the comfort of the food inflation trajectory. The present print of ~2% inflation looks unsustainable and near-term uncertainty around inflation has accentuated owing to multiple factors of 7th Pay commission implementation, GST, unsustainably low food prices, fiscal profligacy in farm loan. But despite all this, one could comfortably fathom inflation to average around 4% over the next couple of years owing to falling cost of production in Indian economy.

Broad economic activity is weak with most of the economic fire-power coming from government spending (both revenue and capital).

The near-term growth inflation dynamics warrants the incremental accommodation in RBI’s monetary policy.

The debt market had a whopping inflow of US$ 14.6 billion between January to June. Robust capital inflow has led the FX reserves to go up by US$ 22 billion in 2017 (till 23rd June) and RBI’s long forward position to go up from near nil to US$ 13.5 billion as of April end. If the central bank is unable to roll-over its forward book, it could further add to the liquidity glut of the market.

The central bank has decided to conduct a Rs. 200 billion of OMO sale in July so far. But it has been re-emphasizing that they will be doing so in a non-disruptive fashion. Owing to these mix of factors, liquidity may take its own sweet time to normalize.

The favourable liquidity and growth inflation dynamics makes us positive on outlook more confident to maintain relatively high duration in our portfolio.

Debt Market Outlook

Source: Bloomberg, SBIFM Research

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Apr

-09

Oct

-09

Apr

-10

Oct

-10

Apr

-11

Oct

-11

Apr

-12

Oct

-12

Apr

-13

Oct

-13

Apr

-14

Oct

-14

Apr

-15

Oct

-15

Apr

-16

Oct

-16

Apr

-17

10 year GSec yield (mth end, %) Repo Rate (mth end, %)

Thank you

Disclaimer

This presentation is for information purposes only and is not an offer to sell or a solicitation to buy any mutual fund units/securities. These views alone are not sufficient and should not be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party. All opinions and estimates included here constitute our view as of this date and are subject to change without notice. Neither SBI Funds Management Private Limited, nor any person connected with it, accepts any liability arising from the use of this information. The recipient of this material should rely on their investigations and take their own professional advice. Mutual Funds investments are subject to market risks, read all scheme related documents carefully. Asset Management Company: SBI Funds Management Private Limited (A joint venture with SBI and AMUNDI). Trustee Company: SBI Mutual Fund Trustee Company Private Limited.

Contact Details

SBI Funds Management Private Limited

(A joint venture between SBI and AMUNDI)

Corporate Office: 9th Floor, Crescenzo, C-38 & 39, G Block, Bandra Kurla Complex, Bandra (East), Mumbai - 400 051 Tel: +91 22 6179 3000 Fax: +91 22 6742 5687/88/89/90/91 Website: www.sbimf.com

Call: 1800 425 5425

Visit us @ www.youtube.com/user/sbimutualfund

SMS: “SBIMF” to 56161

Email: [email protected]

Visit us @ www.facebook.com/SBIMF