marine money japan ship finance forum€¦ · marine money japan ship finance forum . contents 1....

TRANSCRIPT

Current Situation in Shipbuilding -World and Japan-

Masashi Terakado

The Shipbuilders’ Association of Japan

May 12th, 2016

Marine Money Japan

Ship Finance Forum

Contents

1. Current Situation and Projection on Seaborne Trade

2. World Shipbuilding Industry

3. Advantages of Japanese Shipbuilders

4. Measures on International Regulations

1

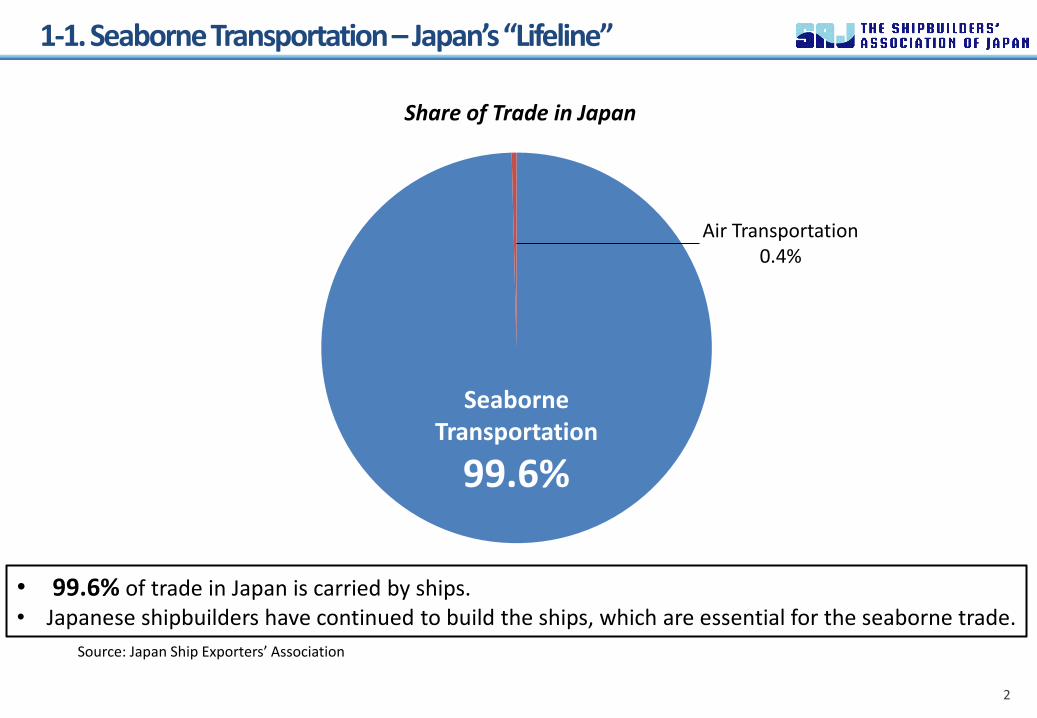

1-1. Seaborne Transportation – Japan’s “Lifeline”

2

• 99.6% of trade in Japan is carried by ships. • Japanese shipbuilders have continued to build the ships, which are essential for the seaborne trade.

Share of Trade in Japan

Seaborne Transportation

99.6%

Air Transportation 0.4%

Source: Japan Ship Exporters’ Association

1-2. World Seaborne Trade

3

Source: Clarkson

0

2

4

6

8

10

12

86 90 95 00 05 10 15

(Bill.Ton)

Iron Ore

Coal

Grain

Container

Crude Oil

Oil Products

Other Cargo

Iron Ore

Coal

Grain

Crude Oil

Container

Oil Products

Other Cargo

1986 2015 86/15

Iron Ore 0.3 1.4 5.2%

Coal 0.3 1.2 5.2%

Grain 0.2 0.4 3.0%

Container 0.2 1.7 8.4%

Crude Oil 1.0 1.9 2.1%

Oil Products 0.4 1.0 3.5%

Other Cargo 1.4 3.2 3.0%

Total 3.7 10.8 3.7%

Contents

1. Current Situation and Projection on Seaborne Trade

2. World Shipbuilding Industry

3. Advantages of Japanese Shipbuilders

4. Measures on International Regulations

4

2-1. History of World Shipbuilding Industry

5

0

20

40

60

80

100

120

65 70 75 80 85 90 95 00 05 10 15

(Mill.GT) World Completions (1965-2015)

Japan Korea Europe China Others

Japan: Largest Market Share 1967-1999

Oil Crisis (1973&1979)

1975 34.2

mil. gt

2011 101.8 mil. gt

Rise in Korea 1995-

Rise in China 2005-

Bankruptcy of Lehman Brothers

(2008)

suffering situation again

suffering situation

Completion Data: IHS

2-2. Oversupply of Fleet

6

GAP

100

150

200

250

300

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Index (1990=100) Index Comparison between Seaborne Trade and Fleet

Seaborne Trade FleetSource: Clarkson

2-3. Problems in Shipbuilding Industry - Overcapacity and Oversupply

7

Imbalance of supply & demand

Low newbuilding price level

Unsustainable business

Government intervention

Distortion

of market Imbalance of

supply and demand

Low freight

price level

Unsustainable business

Incentive to

buy newbuilding

Additional fleet

Additional capacity

Shipbuilding Shipping

Bad Cycle in Shipbuilding and Shipping

Contents

1. Current Situation and Projection on Seaborne Trade

2. World Shipbuilding Industry

3. Advantages of Japanese Shipbuilders

4. Measures on International Regulations

8

3-1. Completions by Shiptype of Japan, Korea, China (2015)

9

39%

5% 6% 5% 6% 20% 19%

8%

52% 56%

83%

38% 19%

34%

49% 31% 30%

12%

27% 37%

37%

3% 12% 9%

29% 24% 10%

0%

20%

40%

60%

80%

100%

BC CONT Tanker LNGC Offshore Other Total

Other

China

Korea

Japan

9%

39%

31%

10%

5% 6%

48%

21%

15%

1%

3% 10%

BC

CONT

Tanker

LNGC

Offshore

Other[値]

6%

6%

1%

[値]

11%

Japan Korea China

World Completion share by shiptype

Source: IHS

3-2. Contracts (Orders) of Export Ship in Japan

10

71%

16%

13%

Share of Contracts in 2014

Share of Contracts in 2015

14.6

12.3 12.1

26.8

19.5

14.0

26.6

24.7

19.4

5.7

11.2

9.0 8.1

14.6 14.8

22.2

0

5

10

15

20

25

30

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

(Mill.GT)

Bulker Tanker Others

45%

34%

21%

Bulker Tanker OthersSource: Japan Ship Exporters’ Association

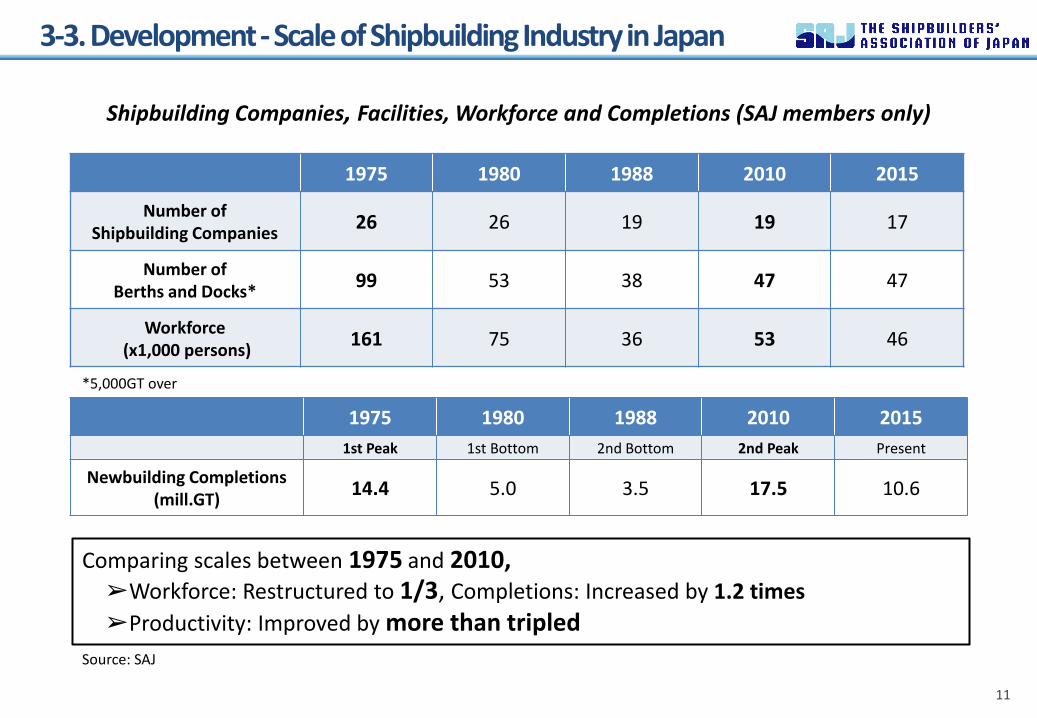

3-3. Development - Scale of Shipbuilding Industry in Japan

11

Comparing scales between 1975 and 2010, ➢Workforce: Restructured to 1/3, Completions: Increased by 1.2 times

➢Productivity: Improved by more than tripled

1975 1980 1988 2010 2015

Number of Shipbuilding Companies

26 26 19 19 17

Number of Berths and Docks*

99 53 38 47 47

Workforce (x1,000 persons)

161 75 36 53 46

Shipbuilding Companies, Facilities, Workforce and Completions (SAJ members only)

1975 1980 1988 2010 2015

1st Peak 1st Bottom 2nd Bottom 2nd Peak Present

Newbuilding Completions (mill.GT)

14.4 5.0 3.5 17.5 10.6

*5,000GT over

Source: SAJ

3-4. Comparison among Shipbuilding Industries of Japan, Korea, China

12

Productivity* Technology

Facility Capacity (Mill.CGT)

Workforce (10,000 persons)

Productivity (CGT per person)

Quality/ Performance

Research/ Development

Scale of Workforce

Japan 6.3 5 126

[100] ◎ ○ △

Korea 11.7 11 106 [84]

○ ○ ◎

China 19.7 49 40

[32] △ △ ○

*Numbers in 2012 adopted for comparison

3-5. Japan’s Orderbook Share by Nationality of Shipowner

13

37%

4%

4%

3% 2% 1%

41%

8%

End of December, 2015: Total 43.1 mill.GT

JAPAN CHINESE TAIPEI GREECE US SINGAPORE BERMUDA UNCONFIRMED OTHERS

Source: IHS

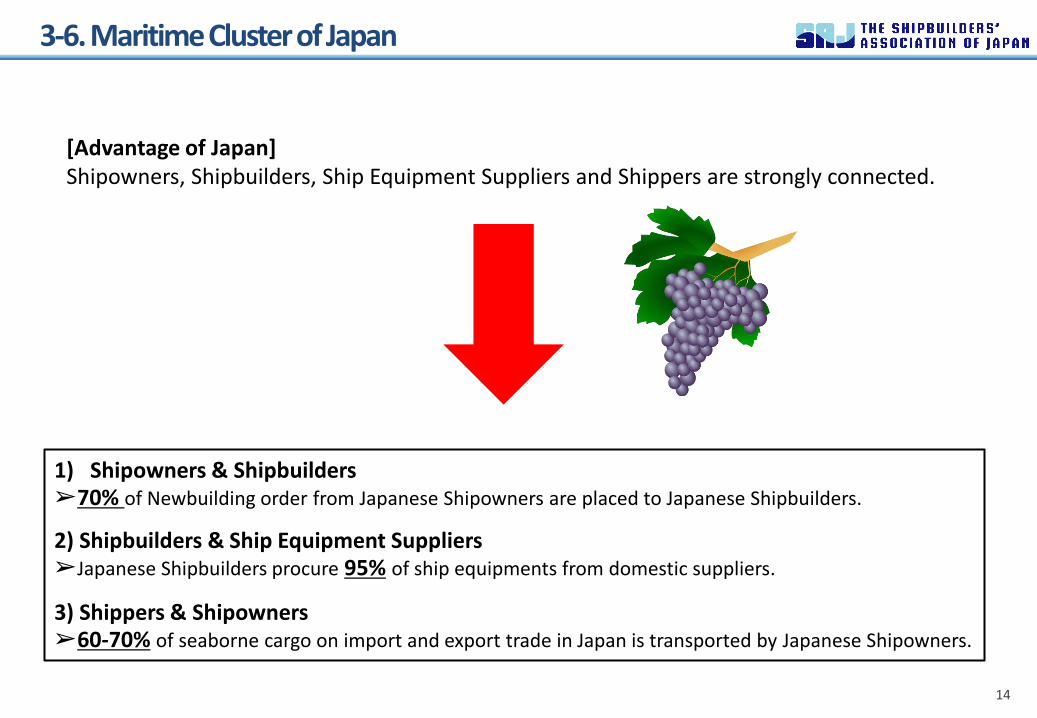

3-6. Maritime Cluster of Japan

14

[Advantage of Japan] Shipowners, Shipbuilders, Ship Equipment Suppliers and Shippers are strongly connected.

1) Shipowners & Shipbuilders ➢70% of Newbuilding order from Japanese Shipowners are placed to Japanese Shipbuilders.

2) Shipbuilders & Ship Equipment Suppliers ➢Japanese Shipbuilders procure 95% of ship equipments from domestic suppliers.

3) Shippers & Shipowners ➢60-70% of seaborne cargo on import and export trade in Japan is transported by Japanese Shipowners.

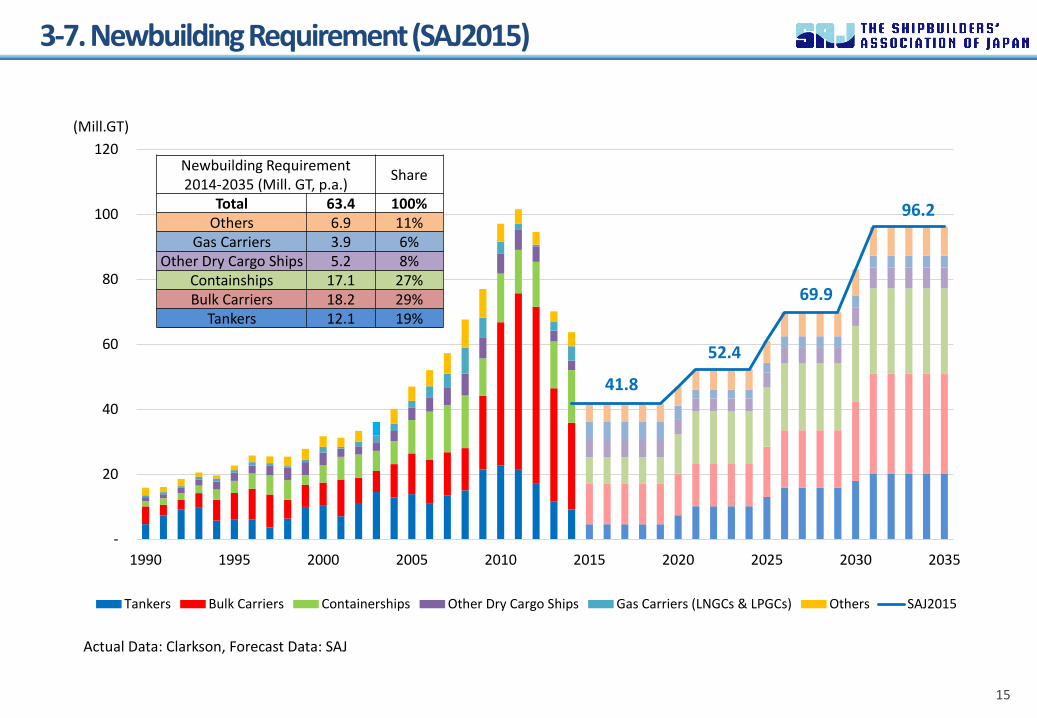

3-7. Newbuilding Requirement (SAJ2015)

15

41.8

52.4

69.9

96.2

-

20

40

60

80

100

120

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

(Mill.GT)

Tankers Bulk Carriers Containerships Other Dry Cargo Ships Gas Carriers (LNGCs & LPGCs) Others SAJ2015

Newbuilding Requirement 2014-2035 (Mill. GT, p.a.)

Share

Total 63.4 100% Others 6.9 11%

Gas Carriers 3.9 6% Other Dry Cargo Ships 5.2 8%

Containships 17.1 27% Bulk Carriers 18.2 29%

Tankers 12.1 19%

Actual Data: Clarkson, Forecast Data: SAJ

3-8. Current Situation and Projection in the Shipbuilding Industry

16

Summary

• The seaborne trade is projected to increase worldwide along with the world population growth.

• A number of existing aged vessels are expected to be demolished steadily.

➢The two factors above will create newbuilding demand.

• The point is “Who’s the one to build the vessels?”

➢Advantages of Japanese Shipbuilders

1) Productivity

2) Technology

3) Maritime Cluster

Contents

1. Current Situation and Projection on Seaborne Trade

2. World Shipbuilding Industry

3. Advantages of Japanese Shipbuilders

4. Measures on International Regulations

17

4-1. IMO Regulations and Newbuilding Contracts

18

0.0

1.0

2.0

3.0

4.0

5.0

4 5 6 7 8 9 101112 1 2 3 4 5 6 7 8 9 101112 1 2 3 4 5 6 7 8 9 101112 1 2 3 4 5 6 7 8 9 101112 1 2 3 4 5 6 7 8 9 101112 1 2 3

2011 2012 2013 2014 2015

(fiscal year)

Contracts of Export Ship (2011-2015)

Others

Cargo Ship

Tanker

Bulk Carrier

Average

(Mill.GT)

New Common Structural Rules for vessels contracted

on or after July 1st, 2015

New Noise Code for vessels contracted

on or after July 1st, 2014

Tier III NOx regulation for vessels started to build

on or after January 1st, 2016

Source: Japan Ship Exporters’ Association

4-2. New Measures on International Regulations

19

From ASEF’s website

4-3. New Measures on International Regulations

20

From ASEF’s website

21

Thank you for your attention!

15-12, Toranomon 1-Chome, Minato-Ku, Tokyo, 105-0001, Japan TEL: +81-(0)3-3580-1563