marine insurance casualty trends - iumicontents •iumi facts & figures committee •the global...

TRANSCRIPT

ASTRID SELTMANN

Vice chair, IUMI Facts & Figures CommitteeAnalyst/Actuary, The Nordic Association of Marine Insurers (Cefor)

Marine Insurance – Casualty trends

CONTENTS

• IUMI Facts & Figures Committee

• The Global Marine Insurance Market

• Vessel values & fleet trends with impact on casualty trends

• CASUALTY TRENDS

Main data sourcesPremiums: IUMI (Global Marine Insurance Report, September 2018)Fleet data: Lloyds List Intelligence, Clarksons Research, Vessel values: Nordic Marine Insurance Statistics (NoMIS)Casualties: Nordic Marine Insurance Statistics (NoMIS)

p. 21-24: Lloyds List Intelligence

CONTENTS – CASUALTY TRENDS

SHIPOWNERS’ LIABILITY

• Pool claims International Group of P&I Clubs

HULL CASUALTY TRENDS

• Total and major losses

• Trends by type of casualty

• Trends by age group & vessel type

• Cost driving factors

SPECIAL

• Detentions – Indicator of future casualties

• Fires on container vessels

IUMI FACTS & FIGURES COMMITTEE

IUMI FACTS & FIGURES – STATS & PROJECTS

Spring – newest edition March 2019

• Spring statistics & analysis for Hull, Cargo, Offshore energy

Autumn – next publication at IUMI conference 15-18 Sept. 2019 Toronto

• Report on World Merchant Fleet and World Trade (F&F chair)

• Global Marine Insurance Report & data downloads (Astrid Seltmann)

• Fact Sheets Hull, Energy, Cargo

• Cost inflation indices for Hull and Cargo business

• Update on major claims database project

(pilot run 2018, new data collection 2019 from 7 (cargo: 9) associations)

• New 2018: IUMI Stats Report – Market analysis based on conference

publications

Other projects

• Analyse new demands (fishing vessels, yachts, carriers & marine liability, …)

• Cooperation with other maritime forums such as IUMI @ IMO

THE GLOBAL MARINE INSURANCE MARKET

MARINE PREMIUM 2017BY LINE OF BUSINESS

Source: IUMI Global Marine Insurance Report 2018

Total estimate 2017: 28.5 USD billion / Change 2016 to 2017: +2%

NB: Exchange rate effects!

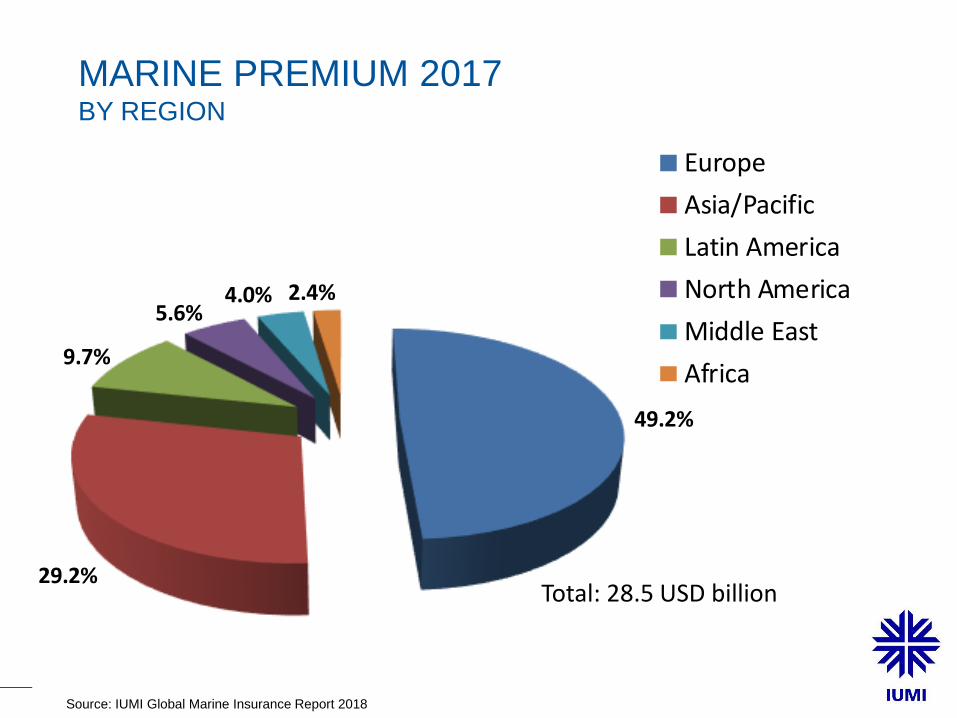

49.2%

29.2%

9.7%

5.6%4.0% 2.4%

2017Europe

Asia/Pacific

Latin America

North America

Middle East

Africa

MARINE PREMIUM 2017BY REGION

Total: 28.5 USD billion

Source: IUMI Global Marine Insurance Report 2018

62%

30%

6% 2%

UK

Nordic

Japan

US

Calls 2017:UK: 1.92 Nordic: 0.92Japan: 0.20US: 0.07

Total: 3.11 (USD billion)

P&I CLUBS INTERNATIONAL GROUPPROTECTION & INDEMNITY = SHIPOWNERS’ LIABILITY

GROSS CALLS (PREMIUM) 2017 – OPERATIONAL LOCATION

by country of registration

Source: IUMI Global Marine Insurance Report 2018

VESSEL VALUES

& WORLD FLEET

Foto: Astrid Seltmann

80%

90%

100%

110%

120%

130%

140%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

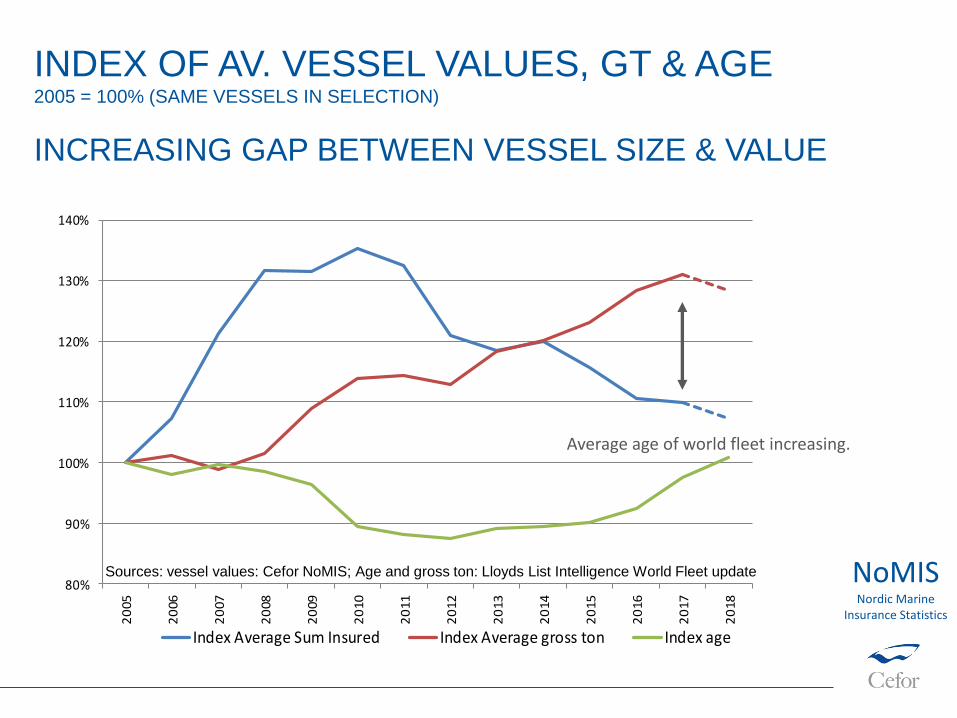

Index Average Sum Insured Index Average gross ton Index age

Sources: vessel values: Cefor NoMIS; Age and gross ton: Lloyds List Intelligence World Fleet update

Average age of world fleet increasing.

INDEX OF AV. VESSEL VALUES, GT & AGE2005 = 100% (SAME VESSELS IN SELECTION)

INCREASING GAP BETWEEN VESSEL SIZE & VALUE

NoMISNordic Marine

Insurance Statistics

0

500

1000

1500

2000

2500

3000

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

< 5000 gt >= 5000

NEWBUILDS WORLD FLEET –

LESS & LARGER VESSELSVESSELS LESS THAN AND ABOVE 5,000 GROSS TON

Source: Lloyds List Intelligence, World Fleet Update, as of January 2019; Graph: Cefor Annual Report 2018

Less newbuilds =>

Increasing fleet age.

Newbuilds larger in size.

NoMISNordic Marine

Insurance Statistics

ANNUAL CHANGE IN VESSEL VALUESCOMPARING INS. VALUE OF SAME VESSELS IN TWO CONSECUTIVE YEARS

NoMISNordic Marine

Insurance Statistics

6.2%

2.1%

8.8%

2.4%

-15.5%

-7.5%

-4.6%

-6.7% -6.1% -5.9%

-9.2%-7.6%

-6.0%

-3.1%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Source: Cefor Annual Report 2018

Strong reduction 2015/16 mainly connected

to bulk & supply/offshore market challenges.

Bulk signs of recovery in 2017.

2018: Normalisation

(some value reduction

due to aging of vessels).

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0.00

20.00

40.00

60.00

80.00

100.00

120.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Change in average sum insured (%) Oil Price, USD (Brent), annual average

Source: Cefor Annual Report 2018

OFFSHORE VESSEL VALUES & OIL PRICE

NoMISNordic Marine

Insurance Statistics

Waiting for recovery in offshore market…

CASUALTY

TRENDS© Astrid SeltmannFoto: Astrid Seltmann

TYPES OF (INSURED) CASUALTIES

• Physical damage – vessels, offshore energy units, cargo

• Third party liability

‐ To object e.g. collision

‐ People (passengers, crew)

‐ Environmental damage (e.g. oil spill)

• Loss of income

• Terror etc.

**Int. Group Excess of Loss Reinsurance

LIABILITY: P&I POOL CLAIMS BY POLICY YEAR

Source: IG P&I Annual Review 2017/18

P&I is a complex business with high liabilities!

Modest claims impact in recent years, but: End of 2018 / 1st quarter 2019 number of severe casualties affecting P&I!

???

HULL CASUALTY TRENDS – FREQUENCY

0.0%

0.1%

0.2%

0.3%

0.4%

in % of Vessels in % of GT

TOTAL LOSSES 2000-2018 (LLI) AS % OF WORLD FLEET, VESSELS > 500 GT

Total losses:

Long-term positive trend.

Sources: Losses: Lloyds List Intelligence; Fleet numbers: Clarksons Research

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

partial claims (< 75%SI, left axis) TLO claims (>75% SI, right axis)

Source: Cefor Annual Report 2018 NoMISNordic Marine

Insurance Statistics

CLAIMS FREQUENCY* (NOMIS):

LONG-TERM POSITIVE TREND

Total loss frequency

Partial loss frequency

Pre-financial crisis peak

* = No. of claims divided by no. of insured vessels

HULL CASUALTY TRENDS – COST

0

20,000

40,000

60,000

80,000

100,000

120,000

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Claim cost per vessel Claim cost per vessel excluding total losses

Source: Cefor Annual Report 2018

CLAIM COST PER VESSEL AS OF 31 DEC 18

STABILIZING AT LOW LEVEL

INCLUDING/EXCLUDING TOTAL LOSSES

Strong total loss impact

2003-08: Strong increasein repair cost per vessel.

Since 2009: repair cost stable;Volatility by major claims impact.

NoMISNordic Marine

Insurance Statistics

16-18: little total loss impact

0

20,000

40,000

60,000

80,000

100,000

120,000

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Claim cost per vessel Claim cost per vessel excluding total losses

Source: Cefor NoMIS stats as of 31 March 2019

*

* 1st quarter figures only

CLAIM COST PER VESSEL AS OF 31 MAR 19

STRONG TOTAL LOSS IMPACT 1ST QUARTER 2019!INCLUDING/EXCLUDING TOTAL LOSSES

NoMISNordic Marine

Insurance Statistics

1st quarter 2019: renewed total loss impact

0

20,000

40,000

60,000

80,000

100,000

120,000

19

96

19

97

19

98

1999

2000

2001

2002

2003

2004

2005

20

06

20

07

20

08

20

09

20

10

20

11

20

12

2013

2014

2015

2016

2017

2018

> 50 MUSD

30-50 MUSD

10-30 MUSD

5-10 MUSD

1-5 MUSD

<= 1 MUSD

IBNR

2012/13/15:strong major claims impact

2004: first claim > USD 50 million

2014,16-18:little major claims impact

Claim bands:

CLAIM COST PER VESSEL AS OF DEC 2018:

3 YEARS WITHOUT CLAIMS > USD 30 MILLION

Source: Cefor Annual Report 2018

NoMISNordic Marine

Insurance Statistics

Claim bands:

CLAIM COST PER VESSEL AS OF 31 MARCH 19

MAJOR CLAIMS REVIVAL

NoMISNordic Marine

Insurance Statistics0

20,000

40,000

60,000

80,000

100,000

120,00019

96

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

> 50 MUSD

30-50 MUSD

10-30 MUSD

5-10 MUSD

1-5 MUSD

<= 1 MUSD

IBNR

Source: Cefor NoMIS stats as of 31 March 2019

*

* 1st quarter figures only

1st quarter 2019:

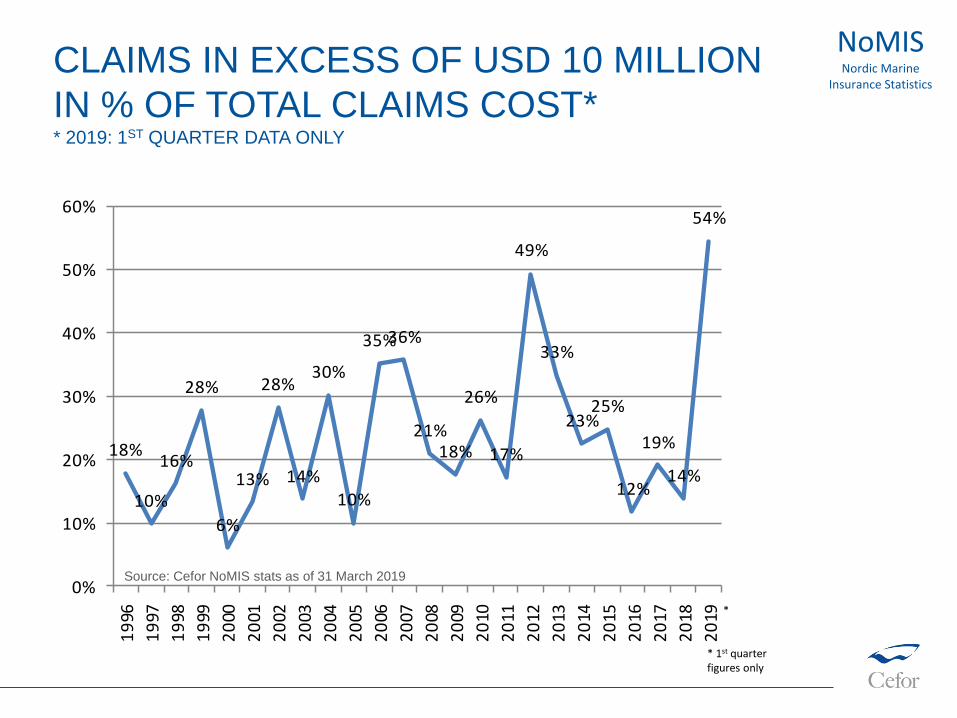

CLAIMS IN EXCESS OF USD 10 MILLION

IN % OF TOTAL CLAIMS COST** 2019: 1ST QUARTER DATA ONLY

NoMISNordic Marine

Insurance Statistics

18%

10%

16%

28%

6%

13%

28%

14%

30%

10%

35%36%

21%18%

26%

17%

49%

33%

23%25%

12%

19%

14%

54%

0%

10%

20%

30%

40%

50%

60%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Source: Cefor NoMIS stats as of 31 March 2019

*

* 1st quarter figures only

HULL CASUALTIES – BY TYPE OF CASUALTY

TOTAL LOSSES 2004 – 2018by cause, all vessel types, vessels > 500 GT

(Lloyds List Intelligence categories)

0% 10% 20% 30% 40% 50% 60%

Other

Machinery

Hull Damage

Collision/contact

Fire/explosion

Grounding

Weather

Frequency ( % of all total losses for the period)

2004 -2008

2009-2013

2014-2018

Source: LLI, total losses as reported by Lloyds List

41.2%

2.3%11.5%

20.1%

8.5%

1.9%

14.5%

2013-2017

Machinery

Fire/Explosion

Collision

Contact

Grounding

Heavy weather

Other / unknown

44.7%

1.9%9.2%

19.6%

7.5%

2.4%

14.7%

2018

Machinery

Fire/Explosion

Collision

Contact

Grounding

Heavy weather

Other / unknown

NoMISNordic Marine

Insurance Statistics

NUMBER OF CLAIMS – BY TYPE OF CASUALTY(CEFOR NOMIS CATEGORIES)

Total number of claims:

2013-2017: 17,208 2018: 3,096

38.2%

13.0%12.4%

7.8%

14.8%

3.2%

10.6%

2013-2017

Machinery

Fire/Explosion

Collision

Contact

Grounding

Heavy weather

Other / unknown

42.4%

11.6%

11.4%

8.5%

14.0%

1.7%

10.5%

2018

Machinery

Fire/Explosion

Collision

Contact

Grounding

Heavy weather

Other / unknown

NoMISNordic Marine

Insurance Statistics

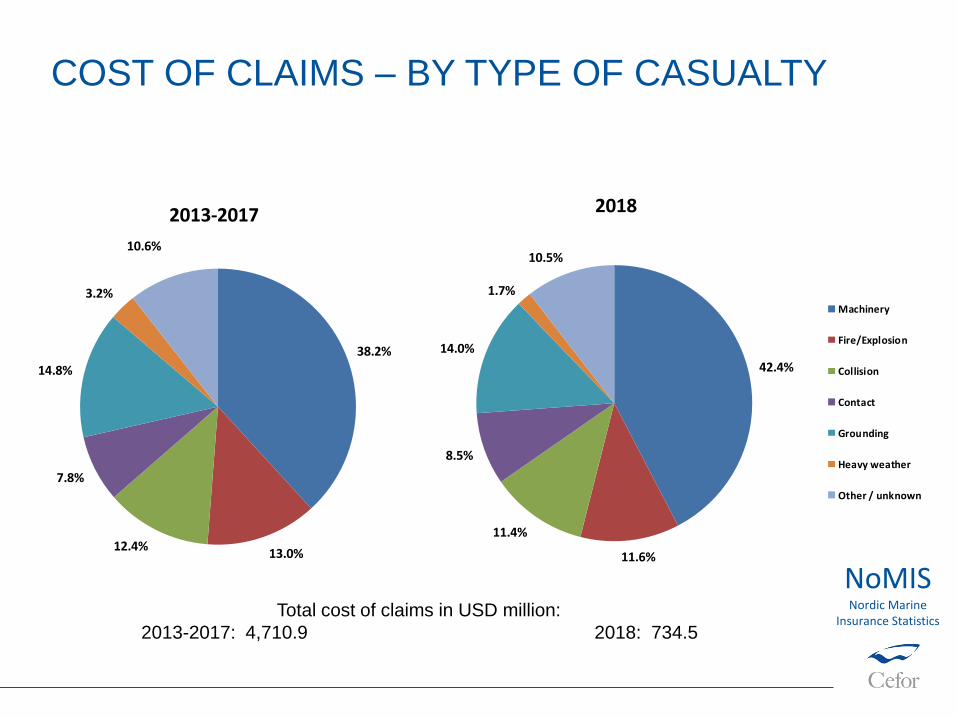

COST OF CLAIMS – BY TYPE OF CASUALTY

Total cost of claims in USD million:

2013-2017: 4,710.9 2018: 734.5

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Machinery

Collision, Contact,Grounding

Other

Fire/Explosion

Heavy weather

FREQUENCY OF CLAIMS > USD 500,000BACK TO PRE-BOOM LEVEL

NoMISNordic Marine

Insurance Statistics

Source: Cefor Annual Report 2018

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Fire/Explosion

Collision, Contact,Grounding

Machinery

Heavy weather

Other

AVERAGE CLAIM COST AS OF DEC 2018STRONG VOLATILITY OF FIRE/EXPLOSION COST

USD 1,000

NoMISNordic Marine

Insurance Statistics

AVERAGE CLAIM COST AS OF MARCH 2019 1ST QUARTER 2019: NEW STRONG IMPACT ON COST BY SEVERE

FIRE/EXPLOSION AND NAVIGATIONAL-RELATED CASUALTIES

USD 1,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Fire/Explosion

Collision, Contact,Grounding

Machinery

Heavy weather

Other

*

* 1st quarter figures only

CLAIMS TRENDS

BY AGE GROUP AND VESSEL TYPE

NoMISNordic Marine

Insurance Statistics

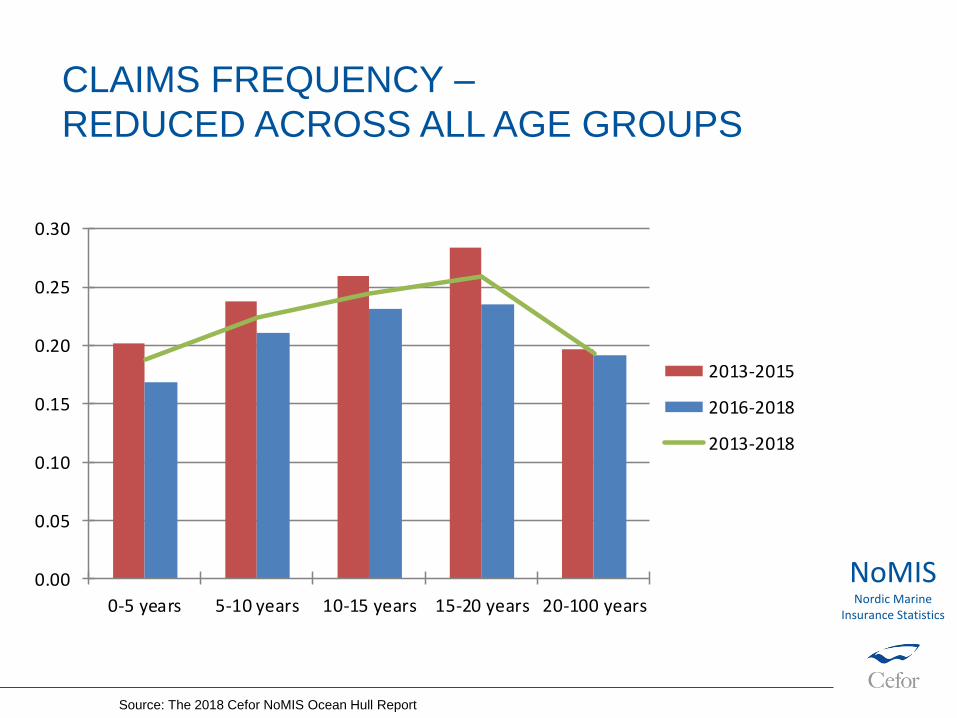

Source: The 2018 Cefor NoMIS Ocean Hull Report

CLAIMS FREQUENCY –

REDUCED ACROSS ALL AGE GROUPS

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0-5 years 5-10 years 10-15 years 15-20 years 20-100 years

2013-2015

2016-2018

2013-2018

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

0-5 years 5-10 years 10-15 years 15-20 years 20-100 years

2013-2015

2016-2018

2013-2018

CLAIM COST PER VESSEL –

REDUCED ACROSS ALL AGE GROUPS

NoMISNordic Marine

Insurance Statistics

Source: The 2018 Cefor NoMIS Ocean Hull Report

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

Bulk Cargo Cont./Car/RoRo Passenger Tank Supply/Off

2013-2015

2016-2018

2013-2018

CLAIMS FREQUENCY, BY VESSEL TYPE

NoMISNordic Marine

Insurance Statistics

Source: The 2018 Cefor NoMIS Ocean Hull Report

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Bulk Cargo Cont./Car/RoRoPassenger Tank Supply/Off

2013-2015

2016-2018

2013-2018

CLAIM COST PER VESSEL BY VESSEL TYPE

NoMISNordic Marine

Insurance Statistics

Source: The 2018 Cefor NoMIS Ocean Hull Report

Sources: Claim indices: Cefor NoMIS data as of 31.12.2018; Exchange rates: Norges Bank, Ship operation costs: Moore Stephen’s, Steel: CRU Steel Price Index

COST DRIVING FACTORS

NoMISNordic Marine

Insurance Statistics

CASUALTY TRENDS – FREQUENCY

• Total loss frequency

‐ Long-term positive trend

‐ Stabilizing around the probably minimum achievable level.

‐ Result of increased focus on safety measures?

• Overall claims frequency

‐ Long-term positive trend

‐ Low volatility since 2012, stabilizing around 23%.

• Many influencing factors

‐ Vessel utilization (type of trade, overcapacity, maintenance, lay-ups)

‐ Younger & bigger vessels

‐ Change in insurer deductibles (higher deductibles = less claims reported)

‐ Exchange rates

(strong dollar may ‘reduce’ claims cost -> less claims exceed insurer

deductibles)

‐ …

CASUALTY TRENDS – REPAIR COST

• Down after financial crisis peak

• Stabilization at modest level in recent years.

• Reduced last 3 years over all age groups and nearly all vessel types.

• Various drivers (correlation with certain parameters)

‐ Steel price

‐ USD exchange rate

(Strong USD may have kept cost down, as repairs often paid in other

currencies).

‐ Labour cost

‐ Maintenance routines

‐ …

MAJOR (= COSTLY) LOSSES

• More expensive single claims – increasing vessel sizes, more complex objects

• Increasing Volatility - strong impact in some years, little in others

• Strong influence on the cost also in years with few major losses – The 1%

most expensive claims account for minimum 30% of the claims cost in any year.

• Random occurrence – Difficult to estimate major claims impact for a specific year

• Fires on container vessels are a concern.

• 1st quarter 2019 casualties demonstrate all of the above

Terminology: ‘Serious’ casualties versus ‘major’ losses

IMO, LLI etc. define casualty ‘seriousness’ related to the nature of the event.

Insurers are impacted by ‘major’ claims = extraordinary costly casualties.

The majority of ‘serious’ casualties are no ‘major’ claims in terms of cost. For details on the comparison, check

https://cefor.no/globalassets/documents/statistics/nomis/2017/2017-half-year-claims-trends_250817.pdf

DETENTIONS – INDICATOR OF FUTURE CLAIMS

SCOPE/DESIGN OF DETENTION ANALYSIS

• ‘Vessels with detentions’ defined as:

Vessels with at least one detention in a 3-year period prior to the underwriting

year, i.e. prior to the year of the insurance coverage to which the analyzed

claims attach.

• Scope of analysis / Test groups:

‐ Vessels with detentions against vessels without detentions in same period.

‐ All vessels, and vessels < 10,000 gross ton

(Vessels < 10,000 gross ton are a more homogenous group. Smaller and older vessels are more

prone to total losses, thus this group is of special interest when analysing the correlation between

total losses and detentions)

• Casualty trends compared:

‐ Claims frequency

‐ Total loss frequency

‐ Claim cost per vessel

NoMISNordic Marine

Insurance Statistics

CLAIMS FREQUENCY – HIGHER FOR ALL

VESSELS WITH DETENTIONS

NoMISNordic Marine

Insurance Statistics

Source: Cefor Annual Report 2018

0%

5%

10%

15%

20%

25%

30%

35%

<= 5 years 5-10 years 10-15 years 15-20 years > 20 years

Vessels without detentions Vessels with detentions

Vessels all sizes Vessels < 10,000 gross ton

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

<= 5 years 5-10 years 10-15 years 15-20 years > 20 years

Vessels without detentions Vessels with detentions

TOTAL LOSS FREQUENCY – HIGHER FOR

VESSELS WITH DETENTIONS EXCEPT YOUNGEST

NoMISNordic Marine

Insurance Statistics

Source: Cefor Annual Report 2018

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

<= 5 years 5-10 years 10-15 years 15-20 years > 20 years

Vessels without detentions Vessels with detentions

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

0.90%

<= 5 years 5-10 years 10-15 years15-20 years > 20 years

Vessels without detentions Vessels with detentions

Vessels all sizes Vessels < 10,000 gross ton

CLAIM COST PER VESSEL (USD) – HIGHER FOR

VESSELS WITH DETENTIONS EXCEPT YOUNGEST

NoMISNordic Marine

Insurance Statistics

Source: Cefor Annual Report 2018

0

20,000

40,000

60,000

80,000

100,000

120,000

<= 5 years 5-10 years 10-15 years15-20 years > 20 years

Vessels without detentions Vessels with detentions

0

20,000

40,000

60,000

80,000

100,000

120,000

<= 5 years 5-10 years 10-15 years 15-20 years > 20 years

Vessels without detentions Vessels with detentions

Vessels all sizes Vessels < 10,000 gross ton

DETENTIONS –

INDICATOR OF FUTURE CASUALTIES

• Claims frequency

‐ was generally higher for vessels across all age groups.

• Total loss frequency

‐ Higher for vessels with detentions except the youngest vessels

‐ The gap in the total loss frequency widens with age

‐ Strong increase already from 5 years for vessels with detentions.

Vessels without detentions only show a substantial increase in the total

loss frequency after 15 (20) years.

‐ Vessels younger than 5 years become seldom total losses.

‐ When checking the reason for detentions (Equasis), these clearly

indicated a causal connection with the type of total loss incurred later

(i.e. not only an incidental statistical correlation).

• Claim cost

‐ Generally higher for vessels with detentions except the youngest.

NoMISNordic Marine

Insurance Statistics

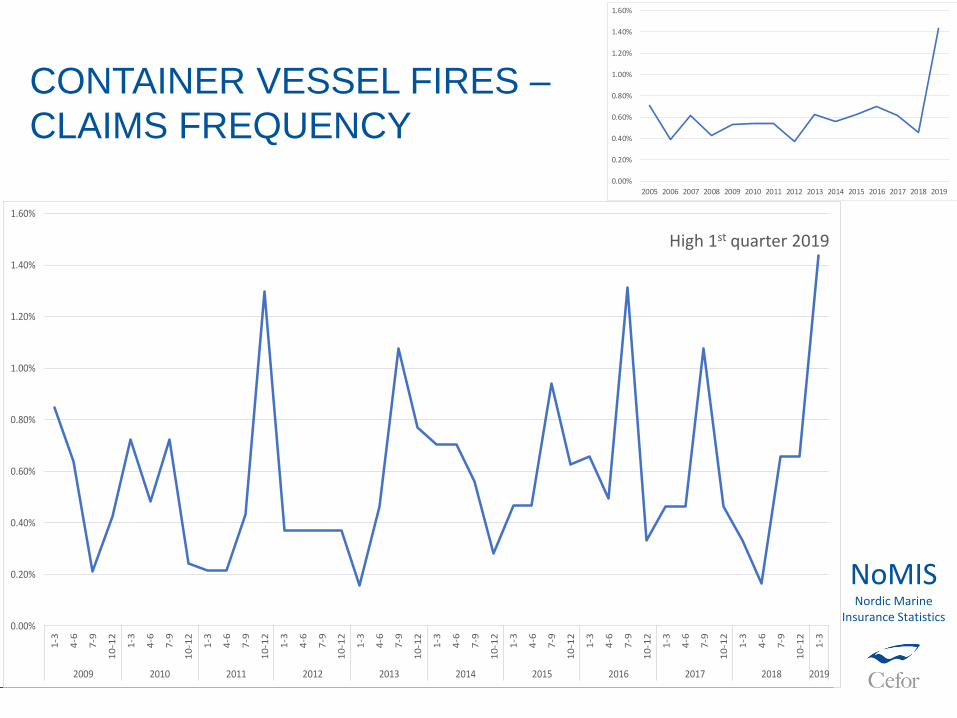

FIRES ON CONTAINER VESSELS

CONTAINER VESSEL FIRES –

NO. OF OCCURRENCES

IN NOMIS DATABASE

0

1

2

3

4

5

6

7

8

9

10

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

High 1st quarter 2019

NoMISNordic Marine

Insurance Statistics

0

2

4

6

8

10

12

14

16

18

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

vessels <= 100,000 gross ton vessels > 100,000 gross ton

Increasing Number of fires on large container vessels -> *

*

* 1Q

figures

only

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

4-6

7-9

10

-12

1-3

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

CONTAINER VESSEL FIRES –

CLAIMS FREQUENCY

High 1st quarter 2019

NoMISNordic Marine

Insurance Statistics

ISSUES TO MONITOR

High-value risks

Arctic risks

© Astrid Seltmann

© Astrid Seltmann

© Astrid Seltmann

Navigation

Oil price, fuel quality

New technology

Climate change

Changes in regulation (liabilities)

Human factor/Qualification

Dagfinn Bakke(Foto by Astrid Seltmann)Value accumulation

MSC Safety discussions!

Cyber risk

Fire on RoRo & Container vessels

Internet of things/complex technologies

NEW IUMI STATS REPORT 2018 (PUBLIC)

IUMI Statistics: https://iumi.com/statistics

OTHER IUMI REPORTS 2017/18

and:

• Cargo, Hull and Energy Fact Sheets

• Hull and Cargo inflation indices

• Data downloads

IUMI Statistics: https://iumi.com/statistics

Conference publications: Spring statistics on Cargo, Hull, Offshore energy:

+ half-year trend updates

Cefor NoMIS Statistics at http://cefor.no/Statistics/NOMIS/

CEFOR PUBLICATIONS 2019

NORDIC MARINE INSURANCE STATISTICS (NOMIS)

Published 11 April 2019