marcia s. wagner, esq.. heightened regulatory requirements and a shifting fiduciary landscape...

TRANSCRIPT

Enhanced Service Opportunities Related to

ERISA Plans

Marcia S. Wagner, Esq.

Heightened regulatory requirements and a shifting fiduciary landscape require those serving employee benefit plans, including accounting the profession, to respond with additional services that will ensure the viability of their clients’ plans.

Introduction

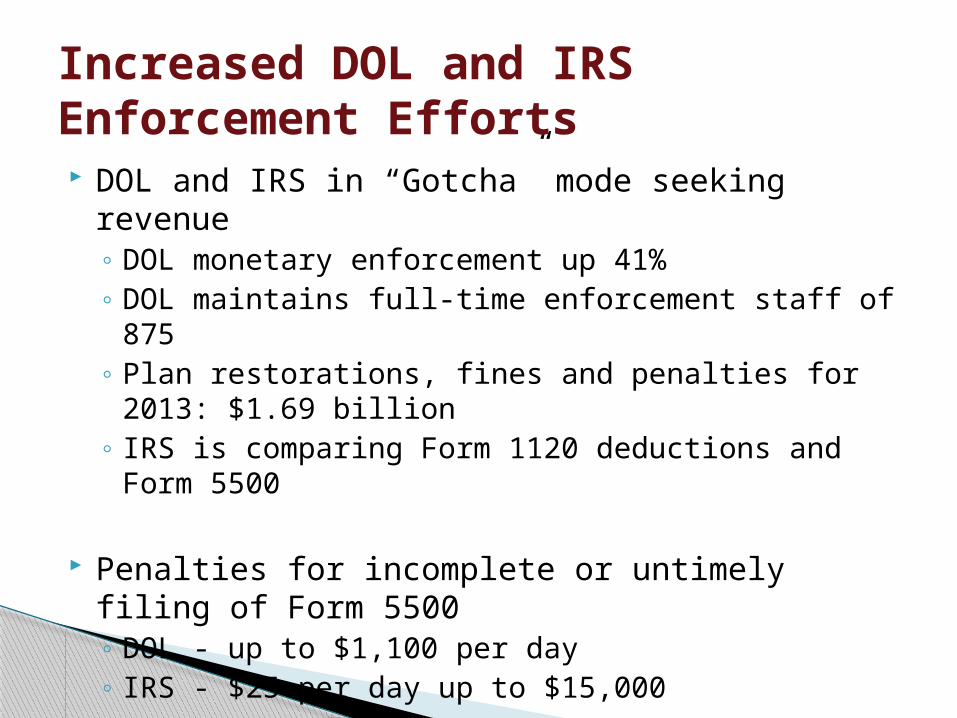

DOL and IRS in “Gotcha” mode seeking revenue◦ DOL monetary enforcement up 41%◦ DOL maintains full-time enforcement staff of 875◦ Plan restorations, fines and penalties for 2013: $1.69 billion◦ IRS is comparing Form 1120 deductions and Form 5500

Penalties for incomplete or untimely filing of Form 5500◦ DOL - up to $1,100 per day◦ IRS - $25 per day up to $15,000

Increased DOL and IRS Enforcement Efforts

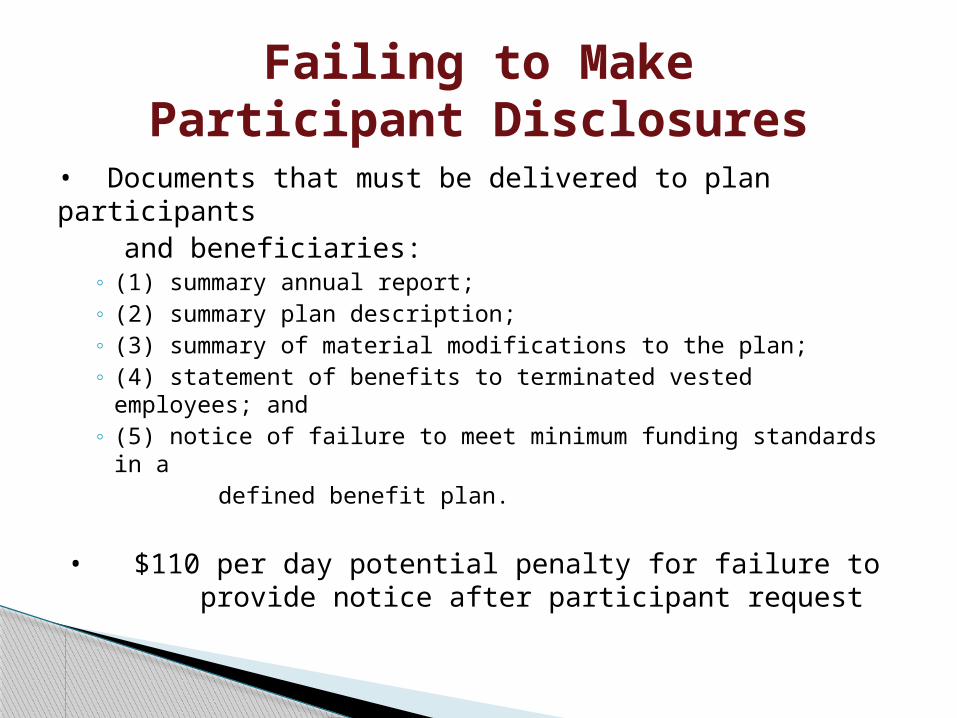

• Documents that must be delivered to plan participants and beneficiaries:

◦ (1) summary annual report;◦ (2) summary plan description; ◦ (3) summary of material modifications to the plan; ◦ (4) statement of benefits to terminated vested employees; and ◦ (5) notice of failure to meet minimum funding standards in a defined benefit plan.

• $110 per day potential penalty for failure to provide notice after participant request

Failing to MakeParticipant Disclosures

• Sponsors of employee benefit plans are subject to ERISA fiduciary duties of loyalty, prudence, asset diversification and must follow plan documents

• In recent years employers have become subject to increased regulatory duties relating to:

- Selection of plan investments and service providers; the reasonableness of plan fees; disclosures to participants; and

selecting annuity providers- Many sponsors seek relief from these and other responsibilities

• Consequences of breaching fiduciary duties are expensive:- Making plan whole for plan losses or restoring lost profits - Settlements against large employers in private class action litigation

over investment fees have ranged from $15 million to $35 million

• Enhanced fiduciary services are in demand to relieve employers of the new duties as well as burdens of day-to day plan operation

ERISA Fiduciary Duties

Civil Actions Under ERISA◦ May be brought by DOL, participants or co-

fiduciaries◦ Fiduciary is personally liable for losses

caused by breach DOL Civil Penalty

◦ Penalty amount is 20% of applicable recovery amount

Excise Taxes Potential Co-Fiduciary Liability Employer error resulted in $1.69 billion of

recoveries through DOL enforcement in 2013

Prohibited Transactions

Plan Disqualification ◦ Document failure◦ Operational failure◦ Demographic failure◦ Employer eligibility failure

Consequences of Disqualification◦ Plan trust pays taxes on earnings◦ Employees taxed on vested plan interest◦ Loss of employer deductions

Penalties reduced or eliminated if failure identified and corrected before IRS discovery◦ TPA or consultant review can prevent the failure by providing

updated documents◦ Failures identified in plan audits can also be timely corrected

Plan Disqualification

Typical cause of plan document failures◦ New law or regulation goes into effect and plan is not timely amended◦ Plan not amended during 5-year amendment cycle for good faith or interim

amendments

Language change is frequently minor and may have no actual impact on participants Minor change can still jeopardize tax-qualification or result in compliance fees

payable to IRS

TPA, working with counsel, can more efficiently identify and implement needed amendments than brokers and financial institutions One size does not fit all Requirements of DC v. DB plans Broad coverage v. one-man plans

Plan Documentation

Core Service Provided by 3(21) fiduciary◦ Assisting Plan Sponsor in selection and

monitoring of Plan’s investment menu options

◦ Advice is non-discretionary (i.e., consists of recommendations)

Related Services◦ Assisting with IPS document where Plan

Sponsor is responsible for reviewing and adopting IPS

◦ Providing quarterly reports and meeting with Plan Sponsor annually

◦ May also offer non-fiduciary services

Investment Advice Fiduciary Model

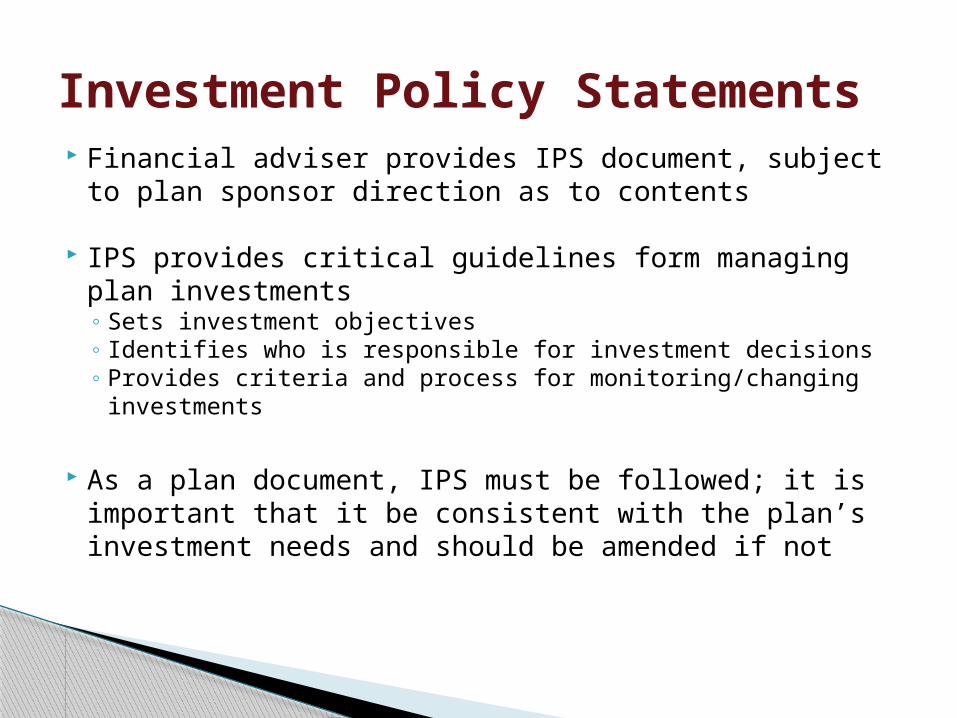

Financial adviser provides IPS document, subject to plan sponsor direction as to contents

IPS provides critical guidelines form managing plan investments◦ Sets investment objectives◦ Identifies who is responsible for investment decisions◦ Provides criteria and process for monitoring/changing

investments

As a plan document, IPS must be followed; it is important that it be consistent with the plan’s investment needs and should be amended if not

Investment Policy Statements

Duty to Ensure Fees are Reasonable◦ New plan Sponsor and participant-level disclosure rules

◦ Class action lawsuits claiming fiduciary breaches due to excessive fees.

Fee Policy Statement is recommended best practice

◦ FPS offers procedural discipline for fiduciary’s review of fees.

◦ Review under FPS should be coordinated with IPS.

◦ FPS itself can help demonstrate prudence

◦ Assistance of financial adviser is critical

General Guidelines◦ Need to gather all relevant information.

◦ Evaluate fees in light of services provided.

◦ Never look for provider with cheapest fees

Fee Policy Statements

Plan sponsors have a fiduciary duty to ensure the reasonableness of plan fees but typically do not have the necessary expertise or resources to make this determination

Benchmarking services are potential remedy◦ Assist the employer in its efforts to identify all plan fees, including

“hidden” indirect compensation.

◦ Equip the employer with tool to be used as part of a prudent review process to monitor the plan’s services and fees.

◦ Provide the employer with competitive pricing information that a Prudent Expert might have, to help assess reasonableness

◦ Role of financial advisor Selection of benchmarking service provider Provide benchmarking service with in-house staff

Benchmarking Services

TOP THREE ERISA COMPLIANCE MISTAKES

1. Compensation Done Incorrectly2. Controlled Group Issues3. Automatic Enrollment Failures

Amount of plan benefits or contributions frequently expressed as percent of compensation◦ Code §401(a)(17) limits annual compensation that can be taken into

account Limit in 2014 will be $260,000

Plan definition of compensation must be nondiscriminatory under Code §414(s)◦ Designed based safe harbors

Include regular or base salary or wages and commissions, tips, overtime, premium pay and bonuses

Exclude reimbursements, expense allowances, fringe benefits, moving expenses and deferred compensation

◦ Reasonable formula not favoring HCEs Examples: Rate of pay vs. actual pay - Pay only while plan participant vs. pay for

entire plan year Plan that includes bonuses but excludes overtime might be treated as

discriminatory Test is whether average percentage of total compensation included under the

definition for HCEs exceeds by more than de minimis amount the average percentage of total compensation included for NHCEs

Compensation Done Incorrectly

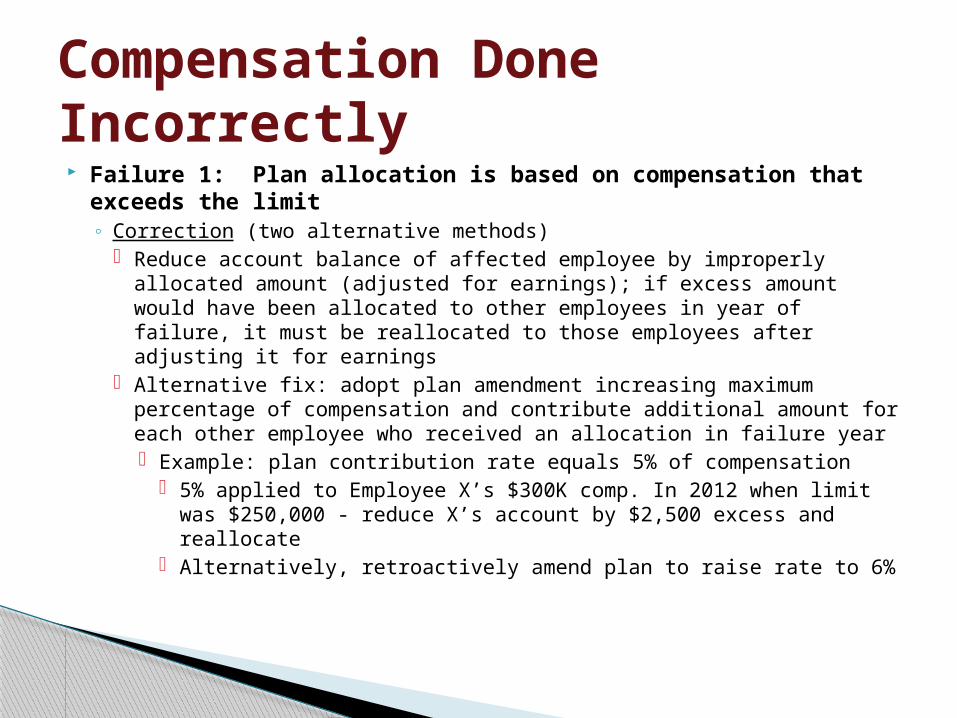

Failure 1: Plan allocation is based on compensation that exceeds the limit◦ Correction (two alternative methods)

Reduce account balance of affected employee by improperly allocated amount (adjusted for earnings); if excess amount would have been allocated to other employees in year of failure, it must be reallocated to those employees after adjusting it for earnings

Alternative fix: adopt plan amendment increasing maximum percentage of compensation and contribute additional amount for each other employee who received an allocation in failure year Example: plan contribution rate equals 5% of compensation

5% applied to Employee X’s $300K comp. In 2012 when limit was $250,000 - reduce X’s account by $2,500 excess and reallocate

Alternatively, retroactively amend plan to raise rate to 6%

Compensation Done Incorrectly

Failure 2: improper exclusion of bonuses, overtime, commissions or another element of compensation from base on which employees may make elective deferrals◦ Correction: employer contribution equal to 50% of missed

deferral opportunity which would be the employee’s elected percentage of compensation that would have been deferred from the excluded compensation element. Also contribute any applicable match and lost earnings

Failure 3: Improper deferral on items not included in plan definition of compensation◦ Correction: Distribute excess elective deferrals plus earnings to

participant. Forfeit match related to excess deferrals and either reallocate or use to offset future employer contributions

Compensation Done Incorrectly

Rules apply as if all controlled group employees worked for employer adopting the plan◦ Applies to eligibility, vesting, minimum participation, determining

contributions and benefits, nondiscrimination, compensation limits, top heavy rules and simplified employee pension and simple retirement accounts

Minimum Participation Example◦ Failure: Company A maintains a qualified plan with a one year

service requirement only for its employees. A is a member of a controlled group of corporations that includes Company B. Employee X completes 3 years of service with Company B and then transfers to Company A.

◦ Correction: The plan must recognize X’s service with Company B and admit her as a participant immediately.

Controlled Group Issues

Highly Compensated Employee Example◦ Failure: Company C and Company D are controlled group members

each of which pay Employee Y a salary of $60,000 for 2013.◦ Correction: For purposes of nondiscrimination testing, Employee Y

will be considered highly compensated, since the HCE limit for 2014 is $115,000 and Employee Y’s aggregate compensation is $120,000

Discrimination Testing Example◦ Failure: Company E maintains a 401(k) plan for its employees that

has never been extended to its wholly-owned subsidiary, Company F. When the minimum coverage test is run, including the employees of F Company, the 401(k) plan fails to satisfy Code §410(b) and, as a result ceases to be tax-qualified.

◦ Correction: NHCEs of Company F must be included as participants on a retroactive basis and receive a QNEC sufficient to pass ADP/ACP test

Controlled Group Issues

Applies to any plan allowing auto salary deferrals Employees automatically enrolled in plan at default

percent unless elect otherwise◦ Plan document specifies percent ◦ Employees can opt out or elect different percent◦ Default percentage must be uniformly applied

Notice Requirements◦ Written explanation of right to opt out or elect to defer a percent of

pay other than default percentage

Automatic Enrollment

Failure 1• Plan sponsor fails to implement plan’s auto enrollment provisions by not

deferring salary of an employee who failed to make electionCorrection 1• Nonelective employer contribution under IRS VCP procedure • Corrective contribution is employee’s compensation multiplied by 50% of

plan’s auto enrollment deferral percentage

Failure 2• Employee never receives enrollment materials and is, therefore treated as an excluded participant rather than a participant whose election has not been implementedCorrection 2• Nonelective employer contribution under VCP Corrective contribution is employee’s compensation multiplied by • 50% average deferral percentage for the employee’s group (NHCE or HCE)

Automatic Enrollment

Marcia is a specialist in pension and employee benefits law, and she is the principal of The Wagner Law Group, one of the nation’s largest boutique law firms, specializing in ERISA, employee benefits and executive compensation, which she founded over 18 years ago. A summa cum laude and Phi Beta Kappa graduate of Cornell University and a graduate of Harvard Law School, she has practiced law for over twenty-seven years. Ms. Wagner was appointed to the IRS Tax Exempt & Government Entities Advisory Committee and ended her three-year term as the Chair of its Employee Plans subcommittee, and received the IRS’ Commissioner’s Award. Ms. Wagner has also been inducted as a Fellow of the American College of Employee Benefits Counsel. For the past six years, 401k Wire has listed Ms. Wagner as one of its 100 Most Influential Persons in the 401(k) industry, and she has received the Top Women of Law Award in Massachusetts and is listed among the Top 25 Attorneys in New England by Boston Business Journal.

Speaker Biography – Marcia S. Wagner

Marcia S. Wagner, Esq.99 Summer Street, 13th Floor

Boston, MA 02110Tel: (617) 357-5200 Fax: (617) 357-5250 Website: www.wagnerlawgroup.com

A0126584.PPTX

Enhanced Service Opportunities Related to ERISA Plans