march 29, 2021 s tock tales

TRANSCRIPT

Stock Tales are concise, holistic stock reports across wider spectrum of sectors. Updates will not be periodical but based on significant events or change in price.

Stock_____

TALES

March 29, 2021

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Stock T

ale

s

March 29, 2021

CMP: | 3624 Target: | 4270 (18%) Target Period: 15 months

Dixon Technologies (India) (DIXTEC)

BUY

Rising star in domestic manufacturing space...

Dixon Technologies (DTL) is India’s leading electronic manufacturing service

(EMS) provider to various multinational/domestic companies in India. The

company is one of the biggest beneficiaries of the government’s production

linked incentive (PLI) scheme for mobile phones and other electronic

products. We believe PLI benefits will start flowing in from Q4FY21E

onwards while in future DTL’s mobile revenue will grow multi-fold (~14x

jump) over FY20-23E. DTL has also applied for PLI in the lighting, electronic

wearables and other electronic products (laptop/notebooks). This opens up

a significant growth opportunity for DTL, going forward (we see 4x jump in

revenue FY20-23E). Further, prudent working capital management and

future expansion through internal accruals will keep balance sheet light and

return ratios elevated (RoE: 39%, RoCE: 44%) for DTL, going forward.

Strong play in emergent domestic EMS industry

The Indian electronic manufacturing services (EMS) industry is likely to grow

at a CAGR of 45% over the next five years to become a ~US$152 billion (bn)

industry. We believe the China+1 strategy by various MNCs alongside

various government measures will help boost domestic EMS industry, going

forward. DTL being one of the largest EMS players, is well set to reap the

benefits of said growth opportunities. The company’s manufacturing

capacity in the LED TV, washing machines and LED lighting can serve ~26%,

28% and 45% of total domestic requirements (in volume term), respectively.

Focus to improve ODM for customer retention

DTL’s share of original design manufacturer (ODM) revenue has increased

from 22% in FY17 to 34% by FY20, which has also helped in ~140 bps

expansion in EBITDA margin. DTL plans to increase ODM revenue share in

consumer electronics from current 6% to 15% in the next two years, which

will help drive segment EBITDA margin higher. However, overall EBITDA

margin is expected to remain flat in FY20-23E considering a significant rise

in revenue from mobile business (OEM model).

Lean balance sheet supports strong RoEs, RoCEs

DTL has registered healthy RoE, RoCE of 22%, 26%, respectively, in FY20.

The future capex will largely be funded through internal accruals. We believe

prudent working capital management and higher asset turn in the mobile

business will result in higher RoE, RoCE, going forward.

Valuation & Outlook

We believe significant future growth potential in domestic electronic

manufacturing coupled with DTL’s plan to increase backward integration can

bring in more customers and would lead to a revenue & earnings CAGR of

56% & 66%, respectively, in FY20-23E. We believe DTL may continue to

command premium valuation due to its significant future growth

opportunities, high return ratios and lean working capital days. We assign a

BUY rating to the stock with a target price of | 4270/share, valuing the

company at 45x FY23E earnings.

Key Financial Summary

| Crore FY19 FY20E FY21E FY22E FY23E (CAGR 20-23E)

Net sales 2984.5 4400.1 6268.2 11843.8 16539.2 55.5

EBITDA 134.9 223.1 302.5 554.1 814.5 54.0

EBITDA Margin(%) 4.5 5.1 4.8 4.7 4.9

Net Profit 63.3 120.5 173.1 367.6 549.5 65.8

EPS (|) 11.2 20.6 29.6 62.8 93.9

P/E(x) 324.0 176.1 122.6 57.7 38.6

RoE (%) 16.7 22.3 25.4 37.6 38.6

RoCE (%) 22.4 26.3 26.3 40.1 43.9

Source: ICICI Direct Research, Company

Stock Data

Particular Amount

Market Cap (| Crore) 21,222.1

Total Debt (FY20) (| Crore) 82.8

Cash & Inv (FY20) (| Crore) 100.1

EV (| Crore) 21,204.8

52 week H/L 4588/ 624

Equity capital (| Crore) 11.6

Face value (|) 2.0

Price Performance `f

0

5000

10000

15000

20000

0

1000

2000

3000

4000

5000

May-18

Oct-18

Mar-19

Aug-19

Jan-20

Jun-20

Nov-20

Dixon NSE

Key Highlights

Strong play in government approved

PLI scheme for mobile phones

manufacturing. Mobile phone revenue

would see ~14x jump over FY20-23

Lean Balance sheet, strong return

rations and quality management

Risk to our call

Delay/less volume offtake by key

clients in mobile segment

Strong competition from global and

domestic EMS player restrict margin

movement

Research Analyst

Sanjay Manyal

Hitesh Taunk

ICICI Securities | Retail Research 2

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Company Background

Business profile

Dixon Technologies (DTL) was started in 1993. In 1994, the company

commenced manufacturing of colour television. At present, DTL’s six

business segments 1) consumer electronics (mainly TV), 2) lighting solutions

(LED lights), 3) home appliances (washing machines), 4) mobile & EMS, 5)

security devices (CCTV, DVR), 6) reverse logistics contribute 48%, 26%, 9%,

12%, 5% and 0.4%, respectively, to the company’s total topline. The

company mainly operates through two business models: 1) original

equipment manufacturer (OEM), 2) original design manufacturer (ODM). The

ODM revenue contribution for the company increased from 22% in FY17 to

38% in FY20. This is largely due to expansion in backward integration and

improved ability in designing & developing products through in-house R&D.

While a significant chunk of the business comes from the OEM business, the

company has increased focus on increasing the mix of ODM share in

consumer electronics and lighting business in future. Marquee clients

include global MNCs such as Samsung, Xiaomi, Motorola, Panasonic,

Phillips, etc and domestic majors such as Voltas-Beko, Havells-Lloyd,

Godrej, Bajaj Electricals, Crompton Greaves, etc.

DTL recorded strong revenue CAGR of 39% in FY17-20 to | 4400 crore led

by 35%, 28% and 27% revenue CAGR in the consumer electronics, home

appliances and lighting segments, respectively. The company has a strong

balance sheet with a stringent working capital cycle of a mere six days along

with RoCE & RoE of 26% and 22%, respectively.

Exhibit 1: DTL’s business profile

Revenue

(| crore)

EBITDA

Margin

Consumer

Electronics

Smart TVs, ultrahigh

definition,commercial

and signage display

3.6 2095 2.4% 48% 6% 35% 26%

Lighting

Solutions

Indoor lighting and LED

bulbs

Bulb- 240

Batens- 24

Downlighters- 6

1140 8.6% 26% 87% 27% LED- 45%

Home

appliances

Washing machines-

Semi automatic, top

loading

Semi auto-1.2

Top loading- 0.6

396 11.6% 9% 100% 28% 28%

Mobile &

EMS

Feature phones

Smart Phones

Feature- 27

Smart phone- 3

537 3.6% 12% Nil NM 10%**

Security

Devices

CCTV, Digital Video

Recorders

(DVRs).

CCTV- 27

DVR- 1.8

216 3.3% 5% 100% 93%* 25%^

Reverse

Logistics

Repair & Refurbishment -

Set up box, Mobile

phones, LED Tv

- 16 16.9% 0.4% NM NM _

Capacity % of

total industryRevenue CAGR

(FY17-20)

FY20

Product Product discription

Production Capacity

(mn units/annum)

Revenue

contr. % of

total

ODM Share

(%) of

segment

Source: Company, ICICI Direct Research, * YoY growth in FY20, ** plans 5x expansion in smart phone capacity in next two years, ^ value market share

ICICI Securities | Retail Research 3

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Exhibit 2: Major clientele as on FY20

Source: Company, ICICI Direct Research,

Exhibit 3: Journey of Dixon so far

Assembly

Capability

CTV and VCR

assembly started

Added assembly of PCBs,

DVDs, CFL bulbs & STBs

Added ODM for CTV,

DVD & CFL bulbs

Started LCD/LED TVs,

Mobile Phones, CCTVs

Achievements

Joined hands with

the Global Consumer

Electronics Giants

Acquired leading Indian

Consumer Durable brands

as Customers

1st Indian company

to develop STB-ODM

solution

PLI, Significant client addition,

exploring export oppertunities

Manufacturing

First manufacturing

facility operational at

Noida

Established Multilocation

footprint

Started Sheet metal &

plastic moulding

Washing Machine & LED

Lighting, Magnetic and power

supplies , Security Cameras

Prescriptive

EMS

Operations

Operational

Sophistication

ODM &

Backward

Integration

High Value- Added

Products

Mid to late 90's 2000-2008 2008-2010 Last 10 years

Source: Company, ICICI Direct Research,

ICICI Securities | Retail Research 4

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Investment Rationale

Indian EMS industry: Ready to fly

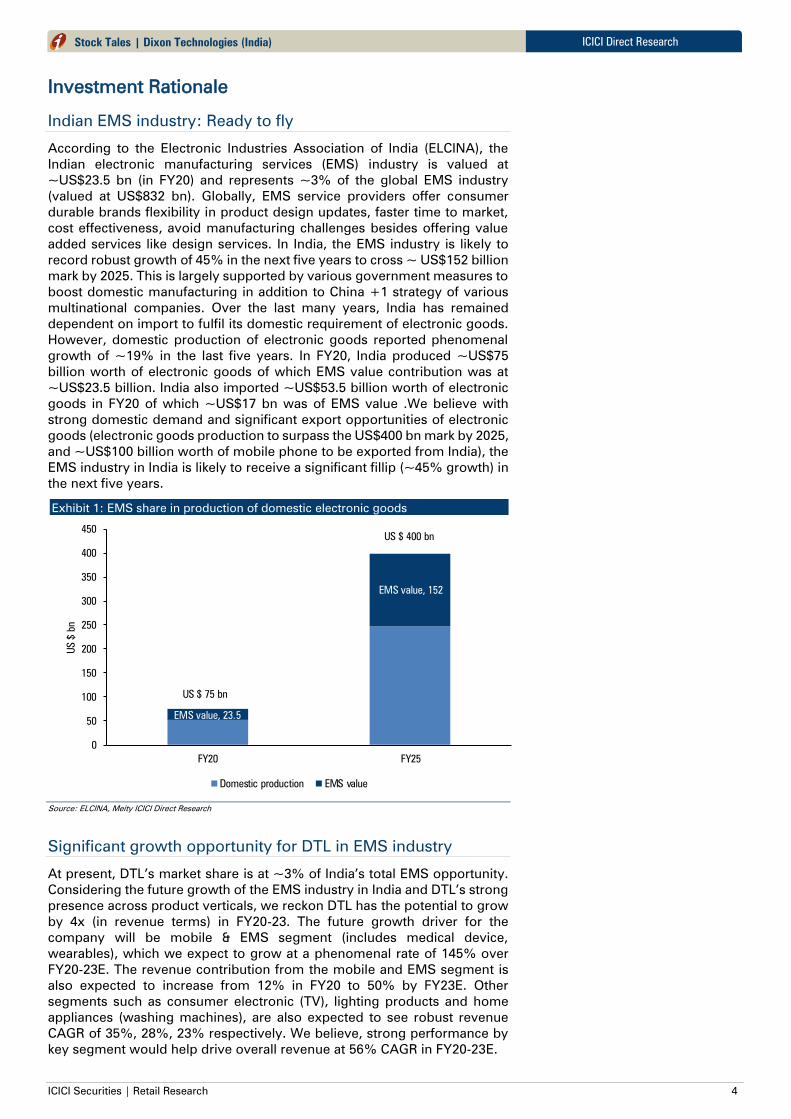

According to the Electronic Industries Association of India (ELCINA), the

Indian electronic manufacturing services (EMS) industry is valued at

~US$23.5 bn (in FY20) and represents ~3% of the global EMS industry

(valued at US$832 bn). Globally, EMS service providers offer consumer

durable brands flexibility in product design updates, faster time to market,

cost effectiveness, avoid manufacturing challenges besides offering value

added services like design services. In India, the EMS industry is likely to

record robust growth of 45% in the next five years to cross ~ US$152 billion

mark by 2025. This is largely supported by various government measures to

boost domestic manufacturing in addition to China +1 strategy of various

multinational companies. Over the last many years, India has remained

dependent on import to fulfil its domestic requirement of electronic goods.

However, domestic production of electronic goods reported phenomenal

growth of ~19% in the last five years. In FY20, India produced ~US$75

billion worth of electronic goods of which EMS value contribution was at

~US$23.5 billion. India also imported ~US$53.5 billion worth of electronic

goods in FY20 of which ~US$17 bn was of EMS value .We believe with

strong domestic demand and significant export opportunities of electronic

goods (electronic goods production to surpass the US$400 bn mark by 2025,

and ~US$100 billion worth of mobile phone to be exported from India), the

EMS industry in India is likely to receive a significant fillip (~45% growth) in

the next five years.

Exhibit 1: EMS share in production of domestic electronic goods

EMS value, 23.5

EMS value, 152

0

50

100

150

200

250

300

350

400

450

FY20 FY25

US

$ bn

Domestic production EMS value

US $ 75 bn

US $ 400 bn

Source: ELCINA, Meity ICICI Direct Research

Significant growth opportunity for DTL in EMS industry

At present, DTL’s market share is at ~3% of India’s total EMS opportunity.

Considering the future growth of the EMS industry in India and DTL’s strong

presence across product verticals, we reckon DTL has the potential to grow

by 4x (in revenue terms) in FY20-23. The future growth driver for the

company will be mobile & EMS segment (includes medical device,

wearables), which we expect to grow at a phenomenal rate of 145% over

FY20-23E. The revenue contribution from the mobile and EMS segment is

also expected to increase from 12% in FY20 to 50% by FY23E. Other

segments such as consumer electronic (TV), lighting products and home

appliances (washing machines), are also expected to see robust revenue

CAGR of 35%, 28%, 23% respectively. We believe, strong performance by

key segment would help drive overall revenue at 56% CAGR in FY20-23E.

ICICI Securities | Retail Research 5

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Domestic mobile production to grow 5x under PLI

The central government aims to create a self-reliant India (Atmanirbhar

Bharat) in the field of electronic manufacturing wherein India will not only

stand to fulfil its domestic requirements but also be a manufacturing hub of

the world. To make India a global manufacturing hub for electronics the

government launched three schemes on April 2020, which are production

linked incentives (PLI) scheme, scheme for promotion of manufacturing of

electronic components and semiconductors (SPECS) and modified

electronic manufacturing cluster (EMC).

PLI for large scale electronics manufacturing proposes a financial incentive

to boost domestic manufacturing and attract large investments in the

electronics value chain (including components and semiconductor

packaging). In case of mobile phones, the scheme will extend an incentive

of 4% to 6% on incremental sales (over base year) of goods manufactured

in India for five years subsequent to the base year (FY20 will be treated as

base year). The government has outlined ~ | 40, 951 crore under the PLI for

a tenure of five years. Similarly, the SPECS notified for manufacturing of

electronics components and semiconductors has a budget outlay of | 3,285

crore spread over eight years. The notified EMC 2.0 has a total incentive

outlay of | 3,762 crore spread over eight years with the objective to create

10 lakh direct and indirect jobs under the scheme.

Exhibit 2: PLI scheme eligibility criteria

Source: PLI Presentation Government of India, ICICI Direct Research

On the domestic front, Padget Electronic (100% of subsidiary of Dixon

Technologies), Lava, Bhagwati (Micromax), UTL Neolyncs and Optiemus

Electronics have received approval under PLI schemes for the

manufacturing of mobile phones (invoice value below | 15,000). These

domestic companies have proposed a production output of | 1.25 lakh crore

over the next five years.

International companies such as Samsung, Foxconn Hon Hai, Rising Star,

Wistron and Pegatron have received PLI approvals (for manufacturing

mobile invoice value | 15,000 and above). Apple (37%) and Samsung (22%)

together account for nearly 60% of global sales of mobile phones.

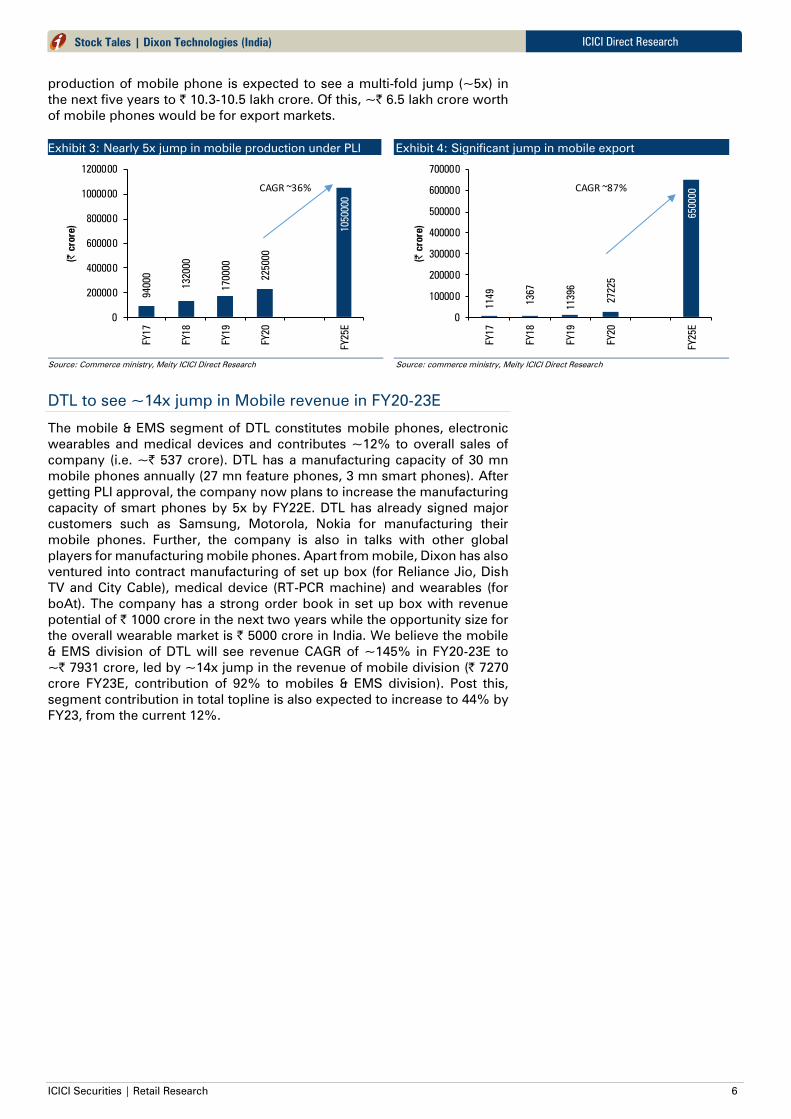

In the last four years, domestic mobile production witnessed strong growth

of ~34% to | 2.25 lakh crore backed by strong domestic demand and import

curb by central government (through increased custom duty). Further, with

China + 1 strategy of global brands/manufacturers and increased value

addition (to 35-40% from 15-20% currently) through PLI, domestic

ICICI Securities | Retail Research 6

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

production of mobile phone is expected to see a multi-fold jump (~5x) in

the next five years to | 10.3-10.5 lakh crore. Of this, ~| 6.5 lakh crore worth

of mobile phones would be for export markets.

Exhibit 3: Nearly 5x jump in mobile production under PLI 94000

132000

170000

225000

1050000

0

200000

400000

600000

800000

1000000

1200000

FY17

FY18

FY19

FY20

FY25E

(| crore)

CAGR ~36%

Source: Commerce ministry, Meity ICICI Direct Research

Exhibit 4: Significant jump in mobile export

1149

1367

11396

27225

650000

0

100000

200000

300000

400000

500000

600000

700000

FY17

FY18

FY19

FY20

FY25E

(| crore)

CAGR ~87%

Source: commerce ministry, Meity ICICI Direct Research

DTL to see ~14x jump in Mobile revenue in FY20-23E

The mobile & EMS segment of DTL constitutes mobile phones, electronic

wearables and medical devices and contributes ~12% to overall sales of

company (i.e. ~| 537 crore). DTL has a manufacturing capacity of 30 mn

mobile phones annually (27 mn feature phones, 3 mn smart phones). After

getting PLI approval, the company now plans to increase the manufacturing

capacity of smart phones by 5x by FY22E. DTL has already signed major

customers such as Samsung, Motorola, Nokia for manufacturing their

mobile phones. Further, the company is also in talks with other global

players for manufacturing mobile phones. Apart from mobile, Dixon has also

ventured into contract manufacturing of set up box (for Reliance Jio, Dish

TV and City Cable), medical device (RT-PCR machine) and wearables (for

boAt). The company has a strong order book in set up box with revenue

potential of | 1000 crore in the next two years while the opportunity size for

the overall wearable market is | 5000 crore in India. We believe the mobile

& EMS division of DTL will see revenue CAGR of ~145% in FY20-23E to

~| 7931 crore, led by ~14x jump in the revenue of mobile division (| 7270

crore FY23E, contribution of 92% to mobiles & EMS division). Post this,

segment contribution in total topline is also expected to increase to 44% by

FY23, from the current 12%.

ICICI Securities | Retail Research 7

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Exhibit 5: PLI schemes to support nearly strong growth in

mobile & EMS division revenues

811

670

355

537

1074

4817

7931

0

1000

2000

3000

4000

5000

6000

7000

8000

9000FY17

FY18

FY19

FY20

FY21E

FY22E

FY23E

(| crore)

CAGR ~145%

Source: Company, ICICI Direct Research

Exhibit 6: Mobiles & EMS division margin expected to

normalise post FY21

0.6

1.0

2.1

3.6

5.2

4.04.2

0

1

2

3

4

5

6

FY17 FY18 FY19 FY20 FY21E FY22E FY23E

(%

)

Source: Company, Meity ICICI Direct Research

Consumer electronics: Import restrictions, customer addition to

drive segment sales

The Indian LED TV market is estimated to grow at a CAGR of 10% in FY19-

23E from 14 million units in FY19 to 21 mn units by FY23. In value terms, the

industry is expected to grow at | 32,200 crore in FY23E from | 22,000 crore

in FY19 supported by an improved mix and volume growth. The demand is

expected to be largely driven by higher internet penetration, rising content

consumption, falling price of entry level smart TVs, low levels of multi-TV

homes in urban markets and rising work from home culture. This, along with

restrictions on import of LED TVs by government (import value of TV set in

FY19 was at ~| 7000 crore) is expected to boost domestic manufacturing of

LED TV, which is a significant positive for Dixon Technologies.

Dixon is a market leader in the LED TV manufacturing. DTL has LED TV

manufacturing capacity of 3.6 mn units by the end of FY20, which has

increased to 4.4 mn in FY21E i.e. 22% YoY growth. The company further

plans to increase LED TV manufacturing capacity by 25% in FY22E to 5.5 mn

units. The 52% increase in LED TV manufacturing capacity in two years was

mainly due to rising demand from existing customers (for new SKUs) and

addition of new clients. Dixon has marquee customers in this segment

including both domestic & global brands. The major customers in this

segment are Xiaomi, Samsung, Panasonic, TCL, Lloyd, Flipkart, Philips,

Toshiba, Vu, One Plus, etc. Unlike lighting and home appliances segment

(where ODM revenue share is 87% and 100%, respectively), the ODM share

in consumer electronics is at 6%. With increased backward integration

(increased SMT line by 80% YoY to 1.8 mn in FY20) the company is looking

to increase ODM share in consumer electronics from the current 6% to 15-

20% in the next two to three years, which would help increase the EBITDA

margin of the segment, going forward. We build-in revenue CAGR of 35%

for the consumer electronic segment in FY20-23E.

ICICI Securities | Retail Research 8

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Exhibit 7: TV industry to continue to grow at CAGR 10%

18291

19776

22189

32104.2

0

5000

10000

15000

20000

25000

30000

35000

FY17

FY18

FY19

FY23E

(| crore)

CAGR ~10%

Source: commerce ministry, ICICI Direct Research

Exhibit 8: India’s TV import increases 11% in FY15-19

4709

3071

3636

4658

7120

0

1000

2000

3000

4000

5000

6000

7000

8000

FY15

FY16

FY17

FY18

FY19

(| crore)

CAGR ~11%

Source: Commerce ministry, ICICI Direct Research

Exhibit 9: Customer addition to help drive growth for DTL

845

1073

1194 2

095

3527

4479 5

167

0

1000

2000

3000

4000

5000

6000

FY17

FY18

FY19

FY20

FY21E

FY22E

FY23E

(| crore)

CAGR ~35%

Source: Company, ICICI Direct Research

Exhibit 10: Expect marginal improvement in EBITDA margin

3.0

2.22.1

2.4

2.82.9

3.1

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FY17 FY18 FY19 FY20 FY21E FY22E FY23E

(%)

Source: Company, Meity ICICI Direct Research

Lighting segment: Focus on improving product mix, export

opportunities

According to industry estimates, the global LED lighting market is valued at

~US$76 billion in 2020 and is expected to continuously grow at ~14%

CAGR to cross US$160 billion by 2026 supported by growing needs of

energy efficient products across the globe. The Indian LED lighting industry,

which is valued at | 18,000 crore, recorded phenomenal growth of 29% in

FY15-20 mainly due to replacement of conventional lighting products to LED

lights. The LED lighting industry is likely to continue to grow at a CAGR of

11% in FY20-23E backed by government’s Unnat Jyoti by Affordable LEDs

for All (Ujala) and Street Lighting National Programme (opportunity size of

| 8000 crore).

Dixon is the key supplier to Signify (earlier Phillips), Panasonic Life solutions,

Wipro, Bajaj, Syska, Orient, Havells, Polycab, Luminous etc for their lighting

requirements (LED bulbs, battens and down lighters). Dixon has ~ 240

million (mn) LED bulbs manufacturing capacity (which is ~45% of India’s

total LED bulb requirements) and 24 mn & 14.4 mn manufacturing capacity

of battens & down lighters, respectively (~25% of India’s total

requirements). While the company sees commercial LED lightings and LED

street lighting as a big opportunity for future growth drivers in the domestic

markets, it is also exploring export opportunities for lighting products. The

central government aims to promote domestic manufacturing of LED lights

in India for which a PLI has also been approved (a PLI worth | 6238 crore

has been approved for AC and LED lighting products).

ICICI Securities | Retail Research 9

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Dixon’s ODM share of lighting revenue is 87% due to its backward

integration capabilities (in sheet metal, plastic moulding & wound

components) and strong R&D backup to develop low cost products. As a

result, the lighting division segment EBITDA margin at 8.6% (in FY20) is

much higher compared to company level EBITDA margin of ~5%. Further,

for FY20-23E we build in ~28% revenue CAGR for lighting segment revenue

and margin improvement of ~100 bps over the same period.

Exhibit 11: Better mix, export opportunities to drive growth

of lighting division

551

774 919

1140

1084

1657

2386

0

500

1000

1500

2000

2500

3000

FY17

FY18

FY19

FY20

FY21E

FY22E

FY23E

(| crore)

CAGR ~28%

Source: Company, ICICI Direct Research

Exhibit 12: Improved product mix to drive EBITDA margin in

FY20-23E

3.2

6.1

7.2

8.6

9.39.6 9.7

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FY17 FY18 FY19 FY20 FY21E FY22E FY23E

(%

)

Source: Company, Meity ICICI Direct Research

Home appliances: New capacity, client addition to drive future

growth

The home appliances segment of the company mainly comprises washing

machines. DTL was mainly present in the semi-automatic washing machines

category until FY20. However, the company has now started manufacturing

top loading automatic washing machines with initial capacity of ~0.6 million

units annually (revenue flow will start from FY21). The company currently

has 140 models from 6.0 Kg to 10 Kg in the semi-automatic machine

category and has the largest capacity in India of ~1.2 million units (almost

28% of the Indian market requirement). The home appliances business is a

100% ODM business and DTL has acquired in-house capabilities for

designing the complete range of semi-automatic washing machines. Also,

the company has in-house development of new design concepts with

additional features like magic filter, water fall, side scrubber and air dry. The

major customers in this segment are Samsung, Godrej, Panasonic, Lloyd,

Flipkart, Haier, Voltas- Beko, Reliance Industries, etc.

The Indian washing machine industry is pegged at | 10,600 crore and is likely

to surpass the | 15000 mark by FY23 at a CAGR of ~12%. The growth would

largely be driven by growing working population, increasing in number of

nuclear families, absence of domestic helps (amid pandemic) and rising

trend of working women to drive urban consumption. We believe the home

appliances segment of the company will grow at a CAGR of 23% in FY20-

23E to | 740 crore led by addition of newer top loading washing machine

categories and client additions in the existing product category. On the

margin front, we believe EBITDA margin is likely to normalise from FY20

level and settle at ~10.6% in FY23.

ICICI Securities | Retail Research 10

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Exhibit 13: Client addition to drive growth in home appliance

188 2

50

374

396

409

619

739

0

100

200

300

400

500

600

700

800

FY17

FY18

FY19

FY20

FY21E

FY22E

FY23E

(| crore)

CAGR ~23%

Source: Company, ICICI Direct Research

Exhibit 14: Gradual margin improvement FY21-23

16.3

12.3

9.9

11.6

10.310.1

10.6

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY17 FY18 FY19 FY20 FY21E FY22E FY23E

(%

)

Source: Company, ICICI Direct Research

Security Systems: Improved discretionary spend to drive

segment performance

DTL entered into a security surveillance system in FY18 through a JV with

Aditya Infotech for manufacturing security devices including CCTVs & digital

video recorders (DVRs). “CP Plus”, trademark owned by Aditya Infotech, is

one of the leading industry players in the field of physical security with a

marker share of 24% and has been No.1 security and surveillance brand for

the past six years. DTL’s security systems contribute ~5% to the company’s

overall revenue (FY20 revenue at ~ | 216 crore).

The Indian security industry is consistently growing and expanding with

opportunities emanating from the government and private sector verticals.

The key drivers of this growth are increase in organised real estate sector,

rise in threat perception, growing crime rates, data thefts, remote

monitoring, growth of public infrastructure. Growth would be aided by

government initiatives leading to rise in demand for security equipment. We

build in ~11% revenue CAGR for security system in FY20-23E with a slight

improvement in EBITDA margin at 3.3%.

Exhibit 15: Moderate growth in segment

112

216

161

254

297

0

50

100

150

200

250

300

350

FY19

FY20

FY21E

FY22E

FY23E

(| crore)

CAGR ~11%

Source: Company, ICICI Direct Research

Exhibit 16: Margin to remain at FY20 level

1.1

3.3

3.1

3.3 3.3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FY19 FY20 FY21E FY22E FY23E

(%

)

Source: Company, Meity ICICI Direct Research

Reverse logistics: Expect flattish revenue growth

The reverse logistics business of the company involves repair &

refurbishment of set top boxes, LED TV panels & mobile phones. It is one of

the few companies to have panel repairing and LED TV refurbishment

facilities. This business is more strategic in nature, more to enhance the

stickiness with customers and provide them end-to-end solution. The

segment’s contribution in topline is miniscule at 0.4% (| 16 crore in FY20).

We build in flattish revenue for the segment with improvement in EBITDA

margin at ~10%.

ICICI Securities | Retail Research 11

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Focus to increase share of ODM business

Dixon Technologies operates under two business models, original

equipment manufacturer (OEM) and original design manufacturer (ODM). In

OEM, Dixon provides fully integrated end-to-end product and solution suite

to original equipment manufacturers ranging from global sourcing,

manufacturing, quality testing and packaging to logistics. Here R&D and

designing portion is done by the customers themselves. In the ODM model,

the complete value chain is controlled by the EMS player on behalf of a

leading brand. The scope of work starts right from design and development

of products, manufacturing and supply. While the OEM business is less

capital intensive, the ODM business requires additional investment in R&D

as well as working capital. However, the ODM model commands

significantly high margin compared to OEM and increased customer

stickiness.

While at present Dixon has a meaningful revenue contribution from OEM

segment (~66% of revenue in FY20), the revenue contribution of ODM has

grown notably. In the last four years, ODM revenue contribution to total

revenue increased from 22% in FY17 to 34% in FY20. Dixon’s share in ODM

is higher in the home appliances i.e. washing machine (100%), lighting

(~9870%) and consumer electronics i.e. TV (6%). Dixon further aims to

increase share of ODM in the lighting and consumer electronic segment to

95-96% and 15-20%, respectively, in the near future.

Exhibit 17: Strong growth in ODM revenue

537 624

1135

1514

0

200

400

600

800

1000

1200

1400

1600

FY17

FY18

FY19

FY20

(| crore)

CAGR ~41%

Source: Company, ICICI Direct Research

Exhibit 18: ODM share of business

6%

87%

100%

0%

20%

40%

60%

80%

100%

120%

Consum

er

Ele

ctronic

s

Lig

htin

gs

Hom

e a

ppliances

Source: Company, Meity ICICI Direct Research

ICICI Securities | Retail Research 12

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Financials

Revenue CAGR of 56% in FY20-23 led by mobile & EMS division

DTL is likely to see consolidated revenue CAGR of 56% to | 16,539 crore in

FY20-23E led by the company’s mobile & EMS division, which is likely to

grow strongly at ~145% CGAR during the same period. We believe

opportunities in the newer segment (like wearables, top loading automatic

washing machines) addition of new clients and increased wallet share from

existing clients would help drive revenue for DTL.

Exhibit 19: Strong revenue growth over FY20-23E

2457

2842

2984

4400 6

268

11844

16539

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

FY17

FY18

FY19

FY20

FY21E

FY22E

FY23E

(| crore)

CAGR ~56%

Source: Company, ICICI Direct Research

Operating leverage, higher ODM share of lighting & consumer

electronics to help maintain EBITDA margin

DTL recorded an EBITDA margin expansion by ~140 bps in FY17-20E led by

higher operating leverage and sharp increase in revenue contribution of the

ODM business. The ODM revenue of the company recorded phenomenal

growth of 41% in FY17-20E while its contribution in revenue increased from

22% to 34% during the same period. The EBITDA margin of the ODM

business was up ~600-700 bps compared to the OEM segment margin.

However, for FY20-23E, we believe the EBITDA margin will remain at ~5%

given a significant rise in the contribution of mobile & EMS business (which

will be OEM in nature). Finally, strong revenue growth coupled with saving

in interest cost would help drive PAT at a CAGR of 66% in FY20-23E.

Exhibit 20: EBITDA to grow strongly in FY20-23

91113

135

223

305

554

814

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

100

200

300

400

500

600

700

800

900

FY17

FY18

FY19

FY20

FY21E

FY22E

FY23E

(%

)

(| crore)

EBITDA EBITDA Margin

Source: Company, ICICI Direct Research

Exhibit 21: Robust PAT CAGR of 66% in FY20-23E

48

61

63

121 1

73

368

550

0

100

200

300

400

500

600

FY17

FY18

FY19

FY20

FY21E

FY22E

FY23E

(| crore)

CAGR ~66%

Source: Company, Meity ICICI Direct Research

ICICI Securities | Retail Research 13

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Robust profitability, lean b/s lead to strong RoCE, RoE

DTL posted healthy RoE, RoCE of 22%, 26%, respectively, in FY20. The

company is aiming at a capex of ~| 150-160 crore in the next two years,

which will largely be used to increase the capacity of mobile & EMS (mobile

manufacturing capacity will increase from current 30 mn to 50 mn by FY23).

The capex will largely be funded through internal accruals. This, coupled

with prudent working capital management, going forward, is likely to result

in strong RoE, RoCE of 39% and 44% in FY23E.

Exhibit 22: Trend of return ratios, going forward

34

28

22

26 26

40

44

24

19

17

22

25

3839

0

5

10

15

20

25

30

35

40

45

50

FY17 FY18 FY19 FY20 FY21E FY22E FY23E

(%

)

RoCE RoE

Source: Company, ICICI Direct Research

Exhibit 23: Valuation Matrix (Peer)

FY20 FY21E FY22E FY23E FY20 FY21E FY22E FY23E FY20 FY21E FY22E FY23E FY20 FY21E FY22E FY23E FY20FY21E FY22E FY23E FY20FY21E FY22E FY23E FY20 FY21EFY22E FY23E

Dixon Tech 21,222 4400.1 6268.2 11843.8 16539.2 5.1 4.8 4.7 4.9 120.5 173.1 367.6 549.5 0.2 0.3 0.2 0.1 22.3 25.4 37.6 38.6 26.3 26.3 40.1 43.9 176.1 122.6 57.7 38.6

Amber Ent 9,670 3962.8 3277.1 5375.8 6695.2 7.8 7.1 8.2 8.7 164.1 100.5 229.8 328.7 0.3 0.2 0.2 0.1 14.5 6.5 13.0 15.8 14.3 8.4 15.3 18.7 58.9 103.0 45.1 31.5

D/E RoE RoCE PEMcap

| crore

Sales EBITDA margin PAT

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 14

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Risks & Concerns

Higher dependence on key customers

At present, the company has high dependency on a few customers on its

key products consumer electronic (Samsung and Xiaomi contribute ~75%

in segment revenue) and mobile division (new customers signed are

Motorola and Nokia under PLI). While the company is planning to add more

customers for said divisions, buy no renewal or delay/cancelation of orders

from existing customers poses risk on revenue growth going forward.

Competition from global EMS players

The international companies such as Foxconn Hon Hai, Rising Star, Wistron

and Pegatron have received PLI approvals along with the world’s largest

players in the EMS industry. Their scale and strong backward integration in

the component manufacturing capacity (in mobile phones) could be a risk

for Dixon in getting large margin orders.

Global shortage of semiconductor may delay order execution

Globally, electronic manufacturing services providers are facing shortage of

chips (semiconductors) for manufacturing electronic goods. This is largely

due to trade war with China and a significant rise in demand for cell phones,

laptops, other work-from-home devices amid pandemic. This coupled with

shortage of containers may lead to delay in procurement of key electronic

inputs. This may delay order execution for EMS providers like Dixon

Technologies.

Margin risk amid volatility in input prices

The company is largely dependent on import for key components (~55% of

total COGS is imported) for its products (for example open cell panels make

up for ~60% of the cost of manufacturing LED TV sets, which is fully

imported. While the company works with complete pass through

mechanism of cost to its customers, we believe a delay in passing on of raw

material prices amid high volatility scenario may dent margins.

ICICI Securities | Retail Research 15

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

Financial Summary (consolidated)

Exhibit 24: Profit & Loss Statement

(Year-end March) FY20 FY21E FY22E FY23E

Revenue 4,400.1 6,268.2 11,843.8 16,539.2

Growth (%) 47.4 42.5 88.9 39.6

Raw material expense 3,913.3 5,547.5 10,697.5 14,858.9

Employee expenses 118.0 126.5 204.3 284.5

Other expenses 198.9 226.7 387.9 581.3

Total Operating Exp 4,177.1 5,962.9 11,289.7 15,724.8

EBITDA 223.1 305.3 554.1 814.5

Growth (%) 65.4 36.8 81.5 47.0

Depreciation 36.5 40.7 47.4 67.8

Interest 35.0 28.7 19.3 17.8

Other Income 5.2 0.7 3.6 5.0

PBT 156.8 236.5 491.0 733.9

Total Tax 36.3 60.4 123.3 184.3

PAT 120.5 176.2 367.6 549.5

Source: Company, ICICI Direct Research

Exhibit 25: Cash Flow Statement

(Year-end March) FY20 FY21E FY22E FY23E

Profit after Tax 120.5 173.1 367.6 549.5

Add: Depreciation 36.5 42.6 47.4 67.8

(Inc)/dec in Current Assets 27.3 -524.9 -1350.3 -1107.2

Inc/(dec) in CL and Provisions 7.0 430.4 1312.1 1071.2

Others 35.0 28.7 19.3 17.8

CF from operating activities 226.3 149.9 396.1 599.2

(Inc)/dec in Investments 7.6 0.0 -120.0 -170.0

(Inc)/dec in Fixed Assets -192.3 -150.0 -150.0 -150.0

Others 67.4 19.3 5.0 5.0

CF from investing activities -117.2 -130.7 -265.0 -315.0

Issue/(Buy back) of Equity 0.2 0.1 0.0 0.0

Inc/(dec) in loan funds -53.3 120.0 -20.0 -10.0

Dividend paid & dividend tax -8.3 -35.1 -70.3 -105.4

Others 15.7 -27.6 -19.3 -17.8

CF from financing activities -45.6 57.4 -109.5 -133.2

Net Cash flow 63.4 76.6 21.5 151.0

Opening Cash 36.7 100.1 176.8 198.3

Closing Cash 100.1 176.8 198.3 349.3

Source: Company, ICICI Direct Research

Exhibit 26: Balance Sheet

(Year-end March) FY20 FY21E FY22E FY23E

Liabilities

Equity Capital 11.6 11.7 11.7 11.7

Reserve and Surplus 529.8 668.9 966.2 1,410.3

Total Shareholders funds 541.3 680.6 977.9 1,422.1

Total Debt 82.8 202.8 182.8 172.8

Other non current liabilities 104.4 106.4 111.4 116.4

Total Liabilities 728.5 989.8 1,272.1 1,711.3

Assets

Gross Block 488.4 638.4 788.4 938.4

Less: Acc Depreciation 82.5 125.1 172.5 240.3

Total Fixed Assets 415.5 522.8 625.5 707.7

Investments 0.0 0.0 120.0 290.0

Inventory 497.8 807.1 1,395.3 1,993.8

Debtors 515.1 738.4 1,460.2 1,903.1

Loans and Advances 0.0 0.0 0.0 0.0

Other CA 133.1 125.4 165.8 231.5

Cash 100.1 176.8 198.3 349.3

Total Current Assets 1,246.2 1,847.7 3,219.6 4,477.8

Creditors 939.1 1,356.7 2,595.9 3,625.0

Provisions 10.9 15.7 64.9 87.0

Other CL 18.7 26.7 50.4 70.4

Total Current Liabilities 968.7 1,399.1 2,711.2 3,782.5

Net current assets 277.5 448.6 508.4 695.3

Other non current assets 35.6 18.3 18.3 18.3

Total Assets 728.5 989.8 1,272.1 1,711.2

Source: Company, ICICI Direct Research

Exhibit 27: Key Ratios

(Year-end March) FY20 FY21E FY22E FY23E

Per share data (|)

EPS 20.6 29.6 62.8 93.9

Cash EPS 26.8 36.9 70.9 105.4

BV 92.5 116.2 167.0 242.9

DPS 1.4 6.0 12.0 18.0

Operating Ratios (%)

EBITDA Margin 5.1 4.8 4.7 4.9

PAT Margin 2.7 2.8 3.1 3.3

Asset Turnover 9.0 9.8 15.0 17.6

Inventory Days 41.3 47.0 43.0 44.0

Debtor Days 42.7 43.0 45.0 42.0

Creditor Days 77.9 79.0 80.0 80.0

Return Ratios (%)

RoE 22.3 25.4 37.6 38.6

RoCE 26.3 26.3 40.1 43.9

RoIC 31.0 32.0 51.9 67.0

Valuation Ratios (x)

P/E 176.1 122.6 57.7 38.6

EV / EBITDA 95.1 70.2 38.1 25.5

EV / Net Sales 4.8 3.4 1.8 1.3

Market Cap / Sales 4.8 3.4 1.8 1.3

Price to Book Value 39.2 31.2 21.7 14.9

Solvency Ratios

Debt / Equity 0.2 0.3 0.2 0.1

Current Ratio 1.2 1.2 1.1 1.1

Quick Ratio 0.7 0.6 0.6 0.6

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 16

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

RATING RATIONALE

ICICI Direct endeavors to provide objective opinions and recommendations. ICICI Direct assigns ratings to its

stocks according to their notional target price vs. current market price and then categorizes them as Buy, Hold,

Reduce and Sell. The performance horizon is two years unless specified and the notional target price is defined

as the analysts' valuation for a stock

Buy: >15%

Hold: -5% to 15%;

Reduce: -15% to -5%;

Sell: <-15%

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities | Retail Research 17

ICICI Direct Research

Stock Tales | Dixon Technologies (India)

ANALYST CERTIFICATION

I/We, Sanjay Manyal;, MBA (Finance), Hitesh Taunk MBA(Finance), Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our

views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. It is also confirmed that above

mentioned Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months and do not serve as an officer, director or employee of the companies mentioned in

the report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products.

ICICI Securities is Sebi registered stock broker, merchant banker, investment adviser, portfolio manager and Research Analyst. ICICI Securities is registered with Insurance Regulatory Development Authority of India Limited (IRDAI)

as a composite corporate agent and with PFRDA as a Point of Presence. ICICI Securities Limited Research Analyst SEBI Registration Number – INH000000990. ICICI Securities Limited SEBI Registration is INZ000183631 for stock

broker. ICICI Securities is a subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture

capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship

with a significant percentage of companies covered by our Investment Research Department. ICICI Securities and its analysts, persons reporting to analysts and their relatives are generally prohibited from maintaining a financial

interest in the securities or derivatives of any companies that the analysts cover.

Recommendation in reports based on technical and derivative analysis centre on studying charts of a stock's price movement, outstanding positions, trading volume etc as opposed to focusing on a company's fundamentals and, as

such, may not match with the recommendation in fundamental reports. Investors may visit icicidirect.com to view the Fundamental and Technical Research Reports.

Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.

ICICI Securities Limited has two independent equity research groups: Institutional Research and Retail Research. This report has been prepared by the Retail Research. The views and opinions expressed in this document may or may

not match or may be contrary with the views, estimates, rating, and target price of the Institutional Research.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected

recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would

endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI

Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in

circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein

is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers

simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting

and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who

must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient.

The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities

whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks

associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-

managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other

benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of

interest at the time of publication of this report.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of

the research report.

Since associates of ICICI Securities and ICICI Securities as a entity are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or

use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in

all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction