manufacturing and production sales tax...

TRANSCRIPT

Manufacturing and Production Sales Tax Exemptions: Not Just for Manufacturers

THURSDAY, SEPTEMBER 18, 2014, 1:00-2:50 pm Eastern

WHOM TO CONTACT

For Assistance During the Program: - On the web, use the chat box at the bottom left of the screen

- On the phone, press *0 (“star” zero)

If you get disconnected during the program, you can simply call or log in using your original instructions and PIN.

IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you must: • Attendees must listen throughout the program, including the Q & A session, in order to qualify for full continuing

education credits. Strafford is required to monitor attendance.

• Record verification codes presented throughout the seminar. If you have not printed out the “Official Record of Attendance,” please print it now (see “Handouts” tab in “Conference Materials” box on left-hand side of your computer screen). To earn Continuing Education credits, you must write down the verification codes in the corresponding spaces found on the Official Record of Attendance form.

• Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Tips for Optimal Quality

Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, you may listen via the phone: dial 1-866-873-1442 and enter your PIN when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Manufacturing and Production Sales Tax Exemptions

Sept. 18, 2014

Susan Traylor Bittick

Ryan

Mark A. Loyd

Bingham Greenebaum Doll

Thomas E. Mazurek, Jr

Tronconi Segarra & Associates

Andrew J. Toth

Tronconi Segarra & Associates

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN. You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

5

SOLUTIONS BEYOND THE OBVIOUS

Manufacturing and Production Sales Tax Exemptions: Not Just for Manufacturers Andrew J. Toth, CPA Partner

S E P T E M B E R 1 8 , 2 0 1 4

Manufacturing Overview

TRONCONI SEGARRA & ASSOCIATES LLP

Manufacturing Overview

– From Merriam-Webster Dictionary: Manufacture – noun

1) something made from raw materials by hand or by machinery

2) a: the process of making wares by hand or by machinery especially when carried on systematically with division of labor; b: a productive industry using mechanical power and machinery

3) the act or process of producing something

7

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– From Merriam-Webster Dictionary: Manufacture – verb

1) to make (something) usually in large amounts by using machines

2) to create (something, such as a false story or explanation) by using your imagination often in order to trick or deceive someone

8

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Manufacturing for Sales Tax Most states provide an exemption from sales tax or

a reduced rate of sales tax for machinery and equipment used in “manufacturing” or “production”.

» The underlying theory is to prevent the cascading of sales tax that would be caused by taxing purchases used or consumed in the manufacturing process.

9

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Unfortunately when state revenue departments apply their interpretation of “manufacturing” or “production” it is not as clear as the dictionary definitions above.

» As the definitions are not uniform it adds to the complexity of operating multi-state manufacturing businesses.

10

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

What to look for in state statutes to determine a state’s sales tax treatment of purchases related to manufacturing:

» definition of manufacturing » machinery and equipment used in manufacturing » ingredients and component parts used in

manufacturing » property consumed or used in manufacturing » where the manufacturing process begins and ends

11

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Over time states have developed tests for determining what is manufacturing/production Physical Change Test

» Defines manufacturing as the process of changing the form or composition of materials.

» Usually allows an exemption for machinery and equipment used directly in making a change to materials.

Integrated Plant Theory » Is a broader interpretation of the manufacturing process

that relies less on the physical relationship of purchases. » Provides and exemption for equipment and machinery that

is integral and necessary to the manufacturing process.

12

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Machinery and Equipment Language that limits eligible manufacturing

purchases » Directly – during production the machinery and/or

equipment must act upon the material to form the product, have an active causal relationship in production.

» Predominately – used more than 50% of the time in manufacturing.

» Exclusively – solely used in manufacturing - 100%. » Mixed or proportional use – exemption determined by the

portion of time equipment is used in an exempt manufacturing process.

13

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Arizona – Machinery or equipment used directly in manufacturing….

Florida – “Industrial machinery and equipment” means tangible personal

property or other property that has a depreciable life of three years or more and that is used as an integral part in the manufacturing…

Iowa – directly and predominately used in processing by a

manufacturer. Machinery and equipment is directly used in manufacturing if it is used to initiate, sustain or terminate a processing activity. Relevant issues include the physical and temporal proximity between the item and the activity, and the active causal relationship between the item and the activity.

14

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Kansas – The following sales are exempt: (1) all sales of machinery and

equipment used as an integral or essential part of an integrated production operation by a qualified manufacturing or processing plant or facility; (2) all sales of installation, repair and maintenance services performed on such machinery and equipment; and (3) all sales of repair and replacement part and accessories purchased for such machinery and equipment.

Massachusetts – Machinery is used directly and exclusively in actual

manufacture, conversion or processing when it is used solely during a manufacturing, conversion or processing operation to effect direct and immediate physical change on tangible personal property to be sold….

15

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Michigan – Property is exempt to the extent it that the property is used for

exempt purposes under the statute. The exemption is limited to the percentage of exempt use to total use….

New Jersey – The primary use requirement, with respect to a single unit of

machinery, apparatus or equipment that is put to use in two different activities, one of which is a direct use and the other of which is not a direct use, the property meets the primary use requirement for exemption only if the manufacturer, processor, assembler or refiner makes use of that property more than 50% of the time directly in manufacturing, processing, assembling or refining operations.

16

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

New York State

– Machinery or equipment used or consumed directly and predominantly in producing for sale tangible personal property….

South Carolina – Generally, a machine qualifies for the exemption if it is

integral and necessary to the manufacturing process, and if the product being manufactured is being manufactured for sale. A machine is integral and necessary for the manufacturing process if it meets three requirements:

1) It is used at a manufacturing facility; 2) It is used in and serves as an essential and indispensable

component part of the manufacturing process on an ongoing and continuous basis and

3) It is substantially used in manufacturing tangible personal property for sale. More than one-third of a machine's use in manufacturing is considered substantial.

17

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

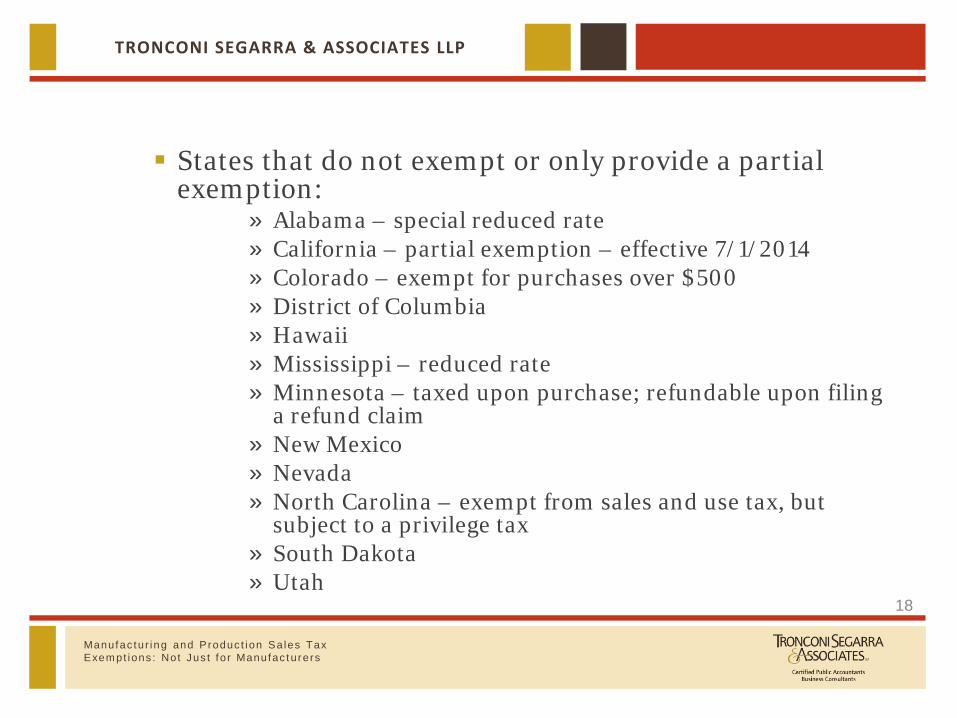

States that do not exempt or only provide a partial

exemption: » Alabama – special reduced rate » California – partial exemption – effective 7/1/2014 » Colorado – exempt for purchases over $500 » District of Columbia » Hawaii » Mississippi – reduced rate » Minnesota – taxed upon purchase; refundable upon filing

a refund claim » New Mexico » Nevada » North Carolina – exempt from sales and use tax, but

subject to a privilege tax » South Dakota » Utah

18

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Ingredients (Raw Materials) and Component Parts Almost all states provide an exemption for

ingredients or components that become incorporated into the finished product, including many of the states that do not provide an exemption for manufacturing machinery and equipment. Most states recognize that these types of purchases are not for consumption, but for resale.

19

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Arizona – purchases of items to be incorporated into manufactured or

fabricated products are considered sales for resale.

California – purchases of ingredients or components that become part of

a manufactured product are exempt.

Florida – The sale, use, consumption, or storage of industrial materials,

including chemicals and fuel, used in future processing, manufacturing, or conversion into tangible personal property for resale where the industrial materials become component parts of the finished product is exempt from tax.

20

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

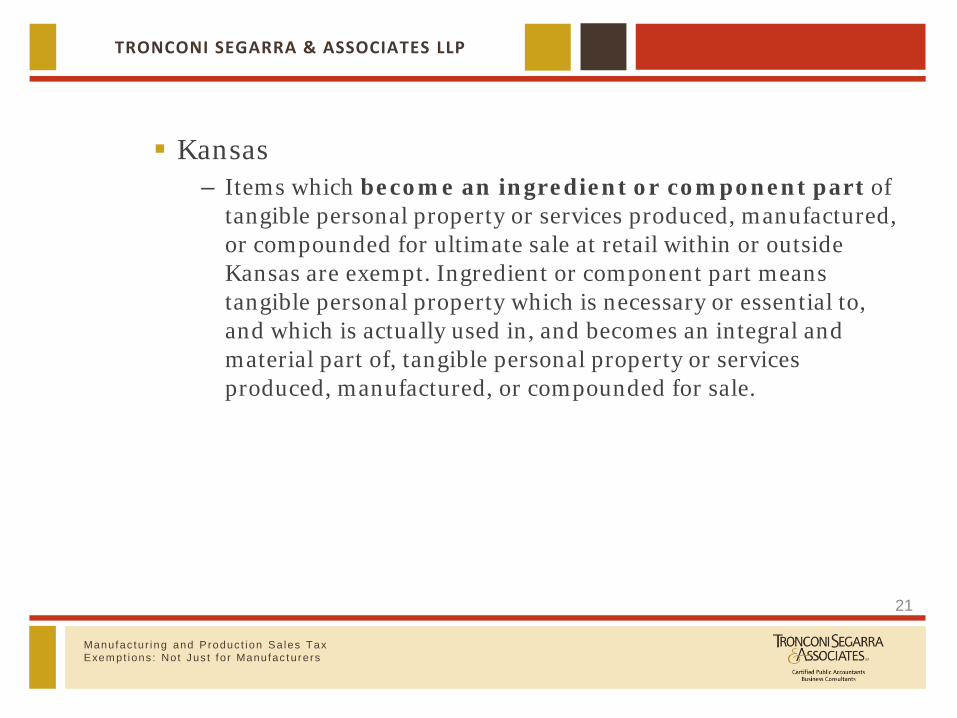

Kansas – Items which become an ingredient or component part of

tangible personal property or services produced, manufactured, or compounded for ultimate sale at retail within or outside Kansas are exempt. Ingredient or component part means tangible personal property which is necessary or essential to, and which is actually used in, and becomes an integral and material part of, tangible personal property or services produced, manufactured, or compounded for sale.

21

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Massachusetts – To be exempt, materials, tools and fuel must become an

ingredient or component part in actual manufacture for tangible personal property to be sold ….

New Jersey – The sale or use of property that is converted into or

becomes a component part of a product produced for sale or for market sampling by the purchaser is not subject to sales or use tax.

22

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Property used or consumed Some states exempt from sales tax materials or

property that are used or consumed in the manufacturing process. These are typically items such as chemicals, solvents, reagents, catalysts, oils, fuels, gases and utilities.

23

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Arizona – exemption from tangible personal property tax does not include

expendable materials.

California – purchases of tangible personal property consumed in

manufacturing that does not become an ingredient or component part of the manufactured item is taxable.

Kansas – Property which is consumed means tangible personal property

which is essential or necessary to, and which is used in the actual process of and consumed, depleted or dissipated within one year in, the activities of production, manufacture, processing….. Among the property deemed consumed are (1) electricity, gas and water; and (2) petroleum products, lubricants, chemicals, solvents, reagents and catalysts.

24

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

New Jersey – Sales of materials, such as chemicals and catalysts, used to

induce or cause a refining or chemical process, which materials are an integral or essential part of the processing operation, but do not become a component part of the finished product, are also exempt from the state sales and use tax.

Texas – lubricants, chemicals, chemical compounds, gases, or liquids

that are used or consumed during the actual manufacturing, processing, or fabrication of tangible personal property for ultimate sale if their use or consumption is necessary and essential to prevent the decline, failure, lapse, or deterioration of exempt equipment.

25

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Where production begins and ends Production generally begins at the point raw

materials are first introduced into the production process.

– Start of production varies by state, but this could be: » at the point which raw materials are unloaded » after the point where raw materials are

inspected/and or weighed » at the point where raw materials are placed in

production

26

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

States that hold closely to the “physical change test” will more narrowly define the beginning of production. For example equipment used for storage and handling of raw materials before it enters production would be taxable.

27

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Manufacturing generally ends at the point the raw materials are in a state that whereby they are ready for sale.

– Depending on a particular state’ statutes this could be at the point:

» direct processing is complete » product is placed in package or a container for sale to

the customer » product is packaged for shipment out of the

manufacture’s plant

28

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Kansas – Integrated production operation means an integrated series of

operations engaged in at a manufacturing or processing plant or facility to process, transform or convert tangible personal property by physical, chemical or other means into a different form, composition or character from that in which it originally existed. Integrated production operations include packaging operations; preproduction operations to handle, store and treat raw materials; postproduction handling, storage, warehousing and distribution operations; and waste, pollution and environmental control operations.

29

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

New Jersey – The term “production,” for purposes of the exemption, is

limited to those operations commencing with the introduction of raw materials into a systematic series of manufacturing, processing, assembling or refining operations and ceasing when the product is in the form in which it will be sold to the ultimate consumer. Production does not include any activities which are distributive in nature.

– A machine which packs a product into shipping cases after the product is in the form in which it will be purchased by the ultimate consumer is not considered to be used in production.

30

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

South Carolina – Generally, material handling machinery and/or mechanical

conveyors are subject to tax up to the point where materials go into the process. Thus, the machine feeding the first processing machine is exempt; the last machine to come within the exemption is the machine that discharges the finished product from the last machine used in the process. Machinery used for transporting (in process) material from one process stage to another is also exempt.

Virginia – Manufacturing, processing, refining, or conversion includes the

production line of the plant from the handling and storage of raw materials at the plant site through the last step of production where the product is finished or completed for sale and conveyed to a warehouse.

31

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Conclusion – While most states provide an exemption or reduced rate

for purchases used in manufacturing, it is important to recognize that differences exist in state laws and regulations as they apply to these purchases.

– Beware that differences may even exist in taxing jurisdictions (localities) within a state. A thorough understanding is necessary to prevent excessive overpayments or underpayments of sales tax.

32

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Contact

Andrew J. Toth, CPA Partner Tronconi Segarra & Associates LLP 8321 Main Street Williamsville, NY 14221 (716) 633-1373 [email protected]

33

Slide Intentionally Left Blank

Manufacturing and Production Sales Tax Exemptions: Not Just for Manufacturers 2014 Legislative Update

Susan Traylor Bittick Principal and Practice Leader, Public Affairs Ryan, LLC September18, 2014

2014 Legislative Update: Overview

While 2013 was a banner year for manufacturing exemptions across the country, the trend slowed significantly in 2014. – Important new developments in states like AZ and GA.

Instead, 2014 is noted as: – The year many 2013 changes actually became effective. – A year in which percentages improved due to continued phase-ins

of exemptions. – A year for continued refinement through rule-making.

Looking ahead to 2015: – LA – TX

36

2014 Legislative Update: New Developments

AZ – Senate Bill 1413, effective August 1, 2014, exempts from

transaction privilege and use taxes sales of electricity and natural gas to businesses engaged in manufacturing or smelting.

– To obtain the benefit: Manufacturing/smelting businesses provide utility companies an exemption certificate certifying this exemption applies. Exemption certificate – Form 5014 - available on the AZDOR website.

– To qualify: Business must be “principally engaged” in manufacturing or smelting operations. “Principally engaged” means at least 51% of the purchaser’s business

must involve manufacturing or smelting operations.

37

2014 Legislative Update: New Developments, cont.

AZ, cont. – “Manufacturing” means process of transforming tangible property

into a different product with a distinctive name, character or use. Does not include “processing, fabricating, job printing, mining, generating electricity, or operating a restaurant.”

– “Smelting” means “melting or fusing a metalliferous mineral, often with an accompanying chemical change, usually to separate the metal.”

– Applies to both state and county taxes. – Cities and towns may either tax or exempt, in whole, the gross

proceeds of sales or gross income from sales of natural gas and electricity to businesses that use at least 51% of such natural gas or electricity in manufacturing or smelting operations in that city or town.

38

2014 Legislative Update: New Developments, cont.

GA – House Bill 900, effective July 1, 2014. – Extends the manufacturing exemption to consumable supplies that

are necessary and integral to the manufacturing process. – Defines consumables supplies as “tangible personal property,

other than machinery, equipment, and industrial materials that is consumed or expended during the manufacture of tangible personal property.” Includes “water treatment chemicals for use in, on, or in conjunction

with machinery or equipment and items that are readily disposable.” Excludes packaging supplies and energy.

39

2014 Legislative Update: Effective Dates

AR – Enacted in 2013 and effective July 1, 2014: 1% partial refund of state sales and use tax on equipment that

modifies, replaces, or repairs existing manufacturing equipment. Reduction of the sales tax rate applicable to electricity and natural gas

used in manufacturing. Exemption on sales of utilities used for commercial grain drying and

storage. » Cover electricity, LP gas, and natural gas » Each utility used for an exempt purpose must be separately

metered from those used for non-exempt purpose Timber harvesting machinery, equipment and related attachments

when told to a person whose primary activity is timber harvesting and who uses the machinery and equipment exclusively in timber harvesting. Does not cover repair/replacement parts.

40

2014 Legislative Update: Effective Dates, cont.

AR, cont. Exemption from gross receipts tax for sand and other proppants used

to complete a new oil or gas well or to recomplete, redrill or expand an existing oil or gas well.

AR Pollution Control – Effective October 1, 2013. – Exempts from sales and use tax sales of machinery and

equipment required by state or federal law to be used in the refining of petroleum-based products to remove sulfur pollutants from the refined product. The Act also exempts repair parts and labor to repair the exempt machinery and equipment.

41

2014 Legislative Update: Effective Dates, cont.

CA – Authorized by Senate Bill 90 passed in 2013 and effective as of

July 1, 2014. – Provides businesses primarily engaged in manufacturing or in

R&D in fields of biotechnology, physical engineering and life sciences a partial exemption of sales and use tax on certain equipment purchases and leases. Reduces the state sales tax rate from 7.5% to 3.3125%. Limited to the first $200 million in exempt purchases per calendar year

made by a single taxpayer or combined reporting unit. – BOE issued guidance in Reg. 1525.4, also effective July 1, 2014. – BOE has promulgated a partial exemption certificate. – BOE also suggests taxpayers get written confirmation that they

qualify. 42

2014 Legislative Update: Effective Dates, cont.

CA, cont. – Qualifying TPP generally includes machinery and equipment and

certain other items purchased for use in any stage of manufacturing or R&D activities including equipment used to operate, regulate or maintain the machinery, such as computers and items used in pollution control and any special-purpose buildings integral to the manufacturing process.

– Also applies to TPP purchased by contractors for use in construction contracts that are integral to manufacturing and R&D activities.

– Not included: Consumables; furniture, inventory, and equipment used in the extraction process; equipment used to store finished products that have completed the manufacturing, processing, refining, fabricating, or recycling process, or items used primarily in administration, general management, or marketing

43

2014 Legislative Update: Effective Dates, cont.

FL – Authorized in 2013 by House Bill 7007, the expanded FL

exemption is now in effect as of April 30, 2014. – What it means: Exemption no longer limited to new and expanded

businesses. Applies to businesses whose primary business operations at the

location where the machinery and equipment is located falls within NAICS Codes 31–33. » The general “manufacturing” codes cover printing, wood

production, manufacturing paper, food, pharmaceuticals, plastic, etc.

» “Primary” business activity means more than 50% of the activities conducted at the location.

Covers industrial machinery and equipment, defined to mean three-year depreciable property.

44

2014 Legislative Update: Effective Dates, cont.

FL, cont. – Must be used in an “integral part” in the manufacturing, processing,

compounding, or production of tangible personal property for sale. – Includes parts and accessories if purchased prior to the date the

machinery and equipment is placed in service. – Does not include: Buildings and structural components of buildings unless they are so

closely related to the machinery and equipment that it houses or supports the machinery and equipment and would be expected to be replaced when they are.

Heating and air conditioning unless sole justification is to meet requirements of the production process.

– See DOR sample Exemption Certificate which purchaser can issue to seller to protect seller from tax liability on non-qualifying transactions

45

2014 Legislative Update: Effective Dates, cont. TX Telecommunication Rebate – First refund claims were due on September 2, 2014 for purchases

made September 1 – December 31, 2013. – Claims due March 31 for subsequent years, beginning in 2015. – Capped at $50 million per year, prorated among all submitting

claims. – Covers TPP purchased, leased or rented by cable television,

Internet access service or telecommunications service providers or “subsidiaries” on which Texas state sales and use tax was paid by the provider or subsidiary.

– TPP must have been directly used or consumed by the provider or subsidiary in or during the distribution of cable television service, provision of Internet access service; or transmission, conveyance, routing or reception of telecommunications services.

– “Subsidiary” requires provider to own/control at least 50%. 46

2014 Legislative Update: Continued Phase-Ins

GA – Second year of four-year phase-in of an exemption covering

utilities used in manufacturing, authorized in 2012 by House 386. 50% exemption. Will be 100% in 2016. Applies to state sales tax and local tax except taxes dedicated to

education. Applies generally to all energy “necessary and integral” to the

production of tangible personal property at a GA manufacturing plant. Energy includes: natural or artificial gas, oil, gasoline, electricity, solid

fuel, wood, waste, ice, steam, water, or other materials necessary and integral for heat, light, power, refrigeration, climate control, processing, or any other use in any phase of the manufacture of tangible personal property.

47

2014 Legislative Update: Continued Phase-Ins, cont.

NM – Second year of five-year phase in of gross receipts deduction for

sales of tangible property consumed in the manufacturing, authorized in 2012 by House Bill 184. 40% exemption for receipts received in 2014 calendar year; becomes

100% in 2017. – Non-taxable transaction certificate required. – Covers TPP incorporated into, destroyed, depleted or transformed

in the process of manufacturing a product, such as electricity, fuels, water, manufacturing aids and supplies, chemicals, gases, repair parts, spares and other tangibles used to manufacture a product. Does not include TPP used in power generation, processing of natural resources or the preparation of food for immediate consumption on or off premises.

48

2014 Legislative Updated: Looking Ahead to 2015

LA – Manufacturing exemption is experiencing growing pains. Originally enacted in 2004 and phased in.

– Covers machinery and equipment that is eligible for depreciation for federal income tax purposes and that is used as an integral part of: Manufacturing of tangible personal property for sale, and; Production, processing, and storing of food and fiber or of timber.

– Computers and software used directly in the manufacturing process. – Pollution control equipment used to control pollution produced by the

manufacturing process. – Machinery and equipment used for testing or measuring raw materials

or the finished product when it is a necessary part of the manufacturing process.

49

2014 Legislative Updated: Looking Ahead to 2015, cont. LA, cont.

– Continued problems in DOR management of exemption certificates. – New questions over what is actually covered. Revisiting the question of what it means to be “eligible for depreciation.” Interested parties now in discussions with DOR.

– Taxpayer disputes regarding pollution control component. Exemption covers equipment intended to eliminate, prevent, treat or

reduce the volume or toxicity or potential hazards of industrial pollution of air, water, groundwater, noise, solid waste or hazardous waste. » Must show either a net decrease in volume or toxicity or potential

hazards of pollution control or that installation is necessary to comply with federal or state environmental laws or regulations.

» Both the DOR and the DEQ must agree that equipment is necessary. – 2015 is a “fiscal” session year for LA – tax legislation accepted.

50

2014 Legislative Updated: Looking Ahead to 2015, cont.

TX – Telecommunication Rebate. Expect a bill to increase or remove the cap applicable to

telecommunication rebate. Possibly also address the definition of a “subsidiary.”

– Intraplant Transportation. Recurring problem with the TX manufacturing exemption, subject to

frequent litigation. Expect House Bill 2047 to be re-filed to clarify that certain cranes used

in manufacturing of large off-shore drilling platforms are exempt. » Covered cranes used to position, place, or hold property, while the

manufacturing process is occurring. » Intended to distinguish cranes used in this manner from those used

for intraplant transportation.

51

2014 Legislative Updated: Looking Ahead to 2015, cont.

TX, cont. – Does “Manufacturing“ Include Oil and Gas Production? Question raised in Southwest Royalties, Inc. v. Combs et al., in which

taxpayer seeks refund for taxes paid on downhole equipment under the manufacturing exemption .

In 2013, this case spurred the filling of House Bill 3113, which would have amended the manufacturing exemption to provide that “bringing oil or gas to the surface of the earth is not considered manufacturing, fabricating or processing for ultimate sale.”

Died without a hearing. Will we see it again?

» Taxpayer has lost at both the trial and appellate courts and is now petitioning the Texas Supreme Court for review.

» Change of administration at the Texas Comptroller’s Office.

52

Contacts:

Susan Traylor Bittick Principal and Practice Leader, Public Affairs Ryan, LLC 512.476.0022 [email protected]

53

Slide Intentionally Left Blank

JURISDICTIONS THAT OPEN UP THE EXEMPTION TO INDUSTRIES NOT

THOUGHT OF AS MANUFACTURING Mark A. Loyd, Esq. Bingham Greenebaum Doll LLP [email protected]

Machinery & Equipment Exemptions

Application of State manufacturing exemptions beyond the manufacture of traditional tangible personal property:

• Expanded Statutes.

• Manufacture to the Fullest Extent of the Statutory Definition.

56

Machinery & Equipment Exemptions

Manufacturing Machinery – Example

KY: Machinery for New and Expanded Industry KRS 139.480(10) • Used directly in a manufacturing or processing production process. KRS 139.010(15)(a).

• “Manufacturing” means any process through which material having little or not commercial value for its intended use before processing has appreciable commercial value for its intended use after processing by the machinery. KRS 139.010(16).

• “Processing production” includes the processing and packaging of raw materials, in-process materials, and finished products; the processing and packaging of farm and dairy products for sale; and the extraction of minerals, ores, coal, clay, stone, and natural gas. KRS 139.010(15)(c).

57

Machinery & Equipment Exemptions Mining, Extraction and Processing

KY Includes: • Extraction of minerals, ores, coal, clay, stone and natural gas. KRS 139.010(15)(c) • Processing and packaging of raw materials. KRS 139.010(15)(c).

IN Includes: • “[E]xtraction, mining, processing, refining, or finishing of other tangible personal

property.” I.C. 6-2.5-5-3(b). KS Includes:

• “[P]rocessing, mining, drilling, refining or compounding of tangible personal property, the treating of by-products or wastes derived from any such production process….” K.S.A. § 79-3606(h).

PA Includes: • “[R]efining, blasting, exploring, mining and quarrying for, or otherwise extracting

from the earth or from waste or stock piles or from pits or banks any natural resources, minerals and mineral aggregates including blast furnace slag.” 72 P.S. § 7201(c)(3).

58

Machinery & Equipment Exemptions Commercial Printing

KY: Commercial Printing – Manufacturing. Revenue Cabinet v. Lexington Herald-Leader Co., 1998 – CA- 001481-MR (Ky. App. 2001).

IN: Commercial Printing – Manufacturing – I.C. 6-2.5-5-3(a)(2).

KS: “Newspaper printing” – Manufacturing. K.S.A. § 79-3606(kk)(2)(D). PA: “[P]ublishing of books, newspapers, magazines and other periodicals and

printing” – Manufacturing. 72 P.S. 7201(c)(2). TX: “[P]roduction of a publication for the dissemination of news of a general

character of a general interest that is printed on newsprint and distributed to the general public free of charge…” – Manufacturing. Tex. Tax Code § 151.318(o).

59

Machinery & Equipment Exemptions

Water Treatment Plant

KY: Sewage Treatment Plant – Not Manufacturing because not saleable product.

KY: Water Treatment Plant – Manufacturing because saleable product.

60

Machinery & Equipment Exemptions Electricity

KY: Generator and Transformation of Electricity – Manufacturing Luckett v. WLEX.TV, Inc., 438 S.W.2d 520 (Ky. 1968).

IN: Electricity Generating – Not Manufacturing – I.C. 6-2.5-5-3(c).

KS: “Electricity power generation” – Manufacturing. K.S.A. § 79-3606(kk)(2)(D).

NY: “Machinery or equipment for use or production of…electricity” – Manufacturing. N.Y. Tax Law § 1115(a)(12).

61

Machinery & Equipment Exemptions Telecommunication Services

KY: Television Broadcasting –Not Manufacturing – WLEX-TV, supra. AZ: “Telecommunications.” “Central office switching equipment, switchboards,

private branch exchange equipment, microwave radio equipment and carrier equipment including optical fiber, coaxial cable and other transmission media that are components of carrier systems” – Exempt. Ariz. Rev. Stat. Ann. § 42-5061(B)(3).

NY: “[T}elecommunications services for sale or internet access services for sale or any combination thereof” – Exempt. N.Y. Tax. Laws § 1115(a)(12-a).

62

Machinery & Equipment Exemptions

KY Includes: • Farm Machinery. KRS 138.480(11) • Processing and packaging of farm and dairy products for sale. KRS

138.010(15)(c).

CA Includes: • “Farm equipment and machinery… to be used primarily in producing and

harvesting agricultural products.” Cal. Tax Code § 6356.5.

TX Includes: • “[F]arm or ranch…in the production of: (A) food for human consumption; (B)

grass; (C) feed for animal life; or (D) other agricultural products. Tex. Tax Code § 151.316(7).

63

64

Contact

Mark A. Loyd Bingham Greenebaum Doll LLP 3500 National City Tower 101 South Fifth Street Louisville, KY 40202 502-589-4200 [email protected]

Slide Intentionally Left Blank

SOLUTIONS BEYOND THE OBVIOUS

S E P T E M B E R 1 8 , 2 0 1 4

Other Exemptions Related to Production Activities

Manufacturing and Production Sales Tax Exemptions: Not Just for Manufacturers Thomas E. Mazurek, Jr., CPA Principal

TRONCONI SEGARRA & ASSOCIATES LLP

Other Exemptions Related to Production Activities

– Many states limit their manufacturing or “production” exemption to just machinery and equipment used directly in production activities.

67

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Direct use may be limited to: » Boilers, furnaces, generators, ovens » Milling machinery and related tooling » M&E used to produce, change or assemble a product » Computerized control systems » Conveyors » Process piping » Packaging equipment

68

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

What about machinery, equipment, tools, supplies, etc. that are not considered to be used directly in production activities , but are still necessary or critical for production?

» Material Handling Equipment » Utilities » Quality Control » Pollution Control » Research & Development

69

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

States address the taxability of these activities differently:

» Part of the “production” exemption. » Separate section or paragraph in the sales & use tax

law or regulations. » Administrative pronouncement or other technical

guidance.

70

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Material Handling Equipment Machinery and equipment used to transport,

handle or convey raw materials, work-in-process and/or finished goods through the production process may be exempt from sales & use tax.

– Where the production process begins and ends typically dictates what Material Handling Equipment is taxable or exempt.

71

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Illinois » Machinery and equipment is used for exempt purposes if it

conveys, handles, or transports the personal property within production stations on the production line or directly between production stations or buildings within the same plant.

– Michigan » Property that is eligible for an industrial processing

exemption includes machinery, equipment, or materials used within a plant site or between plant sites operated by the same person for movement of tangible personal property in the process of production. Property exempt under this provision includes front end loaders, forklifts, lifts, skid steers, multipurpose loaders, etc.

72

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Nebraska » Machinery and equipment used in manufacturing includes

M&E used to transport, convey, handle, or store raw materials or components used in manufacturing or the products produced by the manufacturer for sale.

– Pennsylvania » The purchase or use by a manufacturer or processor of

property, when predominantly used directly in manufacturing or processing, is exempt from tax: machinery, equipment, parts, foundations, repair parts, and supplies used in the actual production, or to transport, convey, handle, or store the product from the first production operation to the time the product is packaged for the ultimate consumer.

73

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

A number of states do not exempt Material Handling Equipment used in production activities:

– Alabama » Material handling equipment is taxable at the regular sales

tax rate.

– Texas » Manufacturers, fabricators, and processors are taxable on

intra-plant transportation equipment such as conveyors, forklifts, cranes and hydraulic lifts, unless otherwise exempt.

74

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Other considerations – Material Handling Equipment used to move finished

goods in a warehouse are typically considered to be used in the shipping process and subject to tax.

– Forklifts and other equipment used throughout a production facility can sometimes be treated as a whole rather than individual units in order to determine taxability.

» May need to prepare usage study or other time analysis.

– Consider cranes, hoists and similar M&E as well.

75

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Utilities Electricity, natural gas, steam, water and other

sources of fuel used in production activities may be exempt from sales & use tax if used to:

» Operate machinery and equipment. » Create conditions necessary for the manufacture of

tangible personal property. » Perform an actual part of the manufacture of

tangible personal property.

Tax treatment varies from state-to-state.

76

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

A number of states do not tax utilities delivered through mains, lines or pipes:

» California » Illinois » Kansas » Louisiana » Ohio » Virginia » Washington and others…

77

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

A decreasing number of states tax utilities used in production at a reduced rate:

» Maine – An exemption applies to 95% of the sale price of all fuel and electricity purchased for use at a manufacturing facility. The remaining 5% of the sale price is subject to the sales & use tax at the general rate.

» Mississippi – Prior to July 1, 2014, a special industrial utility rate of 1.5% applied when the electricity, current, power, steam, coal, natural gas or other fuel was sold to or used by a manufacturer, custom processor, or public service company for industrial purposes.

» Tennessee – Gas, electricity, fuel, oil, coal, and other energy fuels sold to or used by manufacturers is taxed at 1.5% until January 1, 2015.

78

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Other states tax utilities based on their percentage of use in production activities:

– Predominant use (> 50%) » Indiana – The exclusion from sales tax applies only if

nontaxable utilities are separately metered and are predominately used by the purchaser for the excepted uses. “Predominately used” means more than 50% of the utilities are consumed for the exempted use.

» Maryland – The sale of gas, electricity, steam, oil or coal, consumed directly and predominantly in a production activity is not subject to the tax.

» Texas – Natural gas or electricity used during a regular monthly billing period for both exempt and taxable purposes under a single meter is totally exempt or taxable based upon the predominant use of the natural gas or electricity measured by that meter.

79

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Exclusive use (>75% or more) » Connecticut – Sales of electricity, gas and bottled gas also

are exempt when made to industrial manufacturing plants, so long as the building is metered and at least 75% of the electricity, gas or bottled gas is used for industrial, fabricating, or agricultural processing purposes.

» New York – The production exemption also applies to purchases of fuel, gas, electricity, refrigeration, and steam, and gas, electric, refrigeration, and steam services used directly and exclusively in the production process.

80

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

A number of states also tax utilities used in production:

– New Jersey – The exemption also not apply to energy used in connection with machinery and equipment used or consumed to produce tangible personal property through manufacturing, processing, assembling or refining.

81

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Other considerations – Manufacturers may need to meet certain requirements in

order to claim a sales & use tax exemption for utilities used in production:

» An energy assessment or usage study listing taxable and exempt M&E and annual energy consumption.

» Certification by a licensed engineer. » An exemption certificate filed with the state taxing

authority and/or applicable utility provider.

82

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Quality Control Machinery and equipment, tools and supplies used

to test a product during the production process may be exempt from sales & use tax.

» Where quality control functions are performed is typically immaterial.

(production line v. laboratory or testing area)

83

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Colorado » Machinery performing testing of a particular product

tested during the manufacturing process, or testing as a step in a continuous manufacturing line process is directly used in manufacturing.

– Georgia » Testing and quality control machinery or equipment

located at a manufacturing plant used to test the quality of industrial materials, work in process, or finished goods is considered necessary and integral to the manufacture of tangible personal property.

– Kansas » “Machinery and equipment used directly and primarily”

shall include…testing equipment to determine the quality of the finished product.

84

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– New York » The purchase of machinery and equipment by a

manufacturer for use directly and predominantly in quality control of the manufactured product while it is still on the production line is exempt from all state and local sales and use taxes.

– Pennsylvania » The purchase or use by a manufacturer or processor of

property when predominantly used directly in manufacturing or processing, is exempt from tax… items used to test and inspect the product throughout the production cycle.

– South Carolina » Other machinery and equipment exempt from tax

includes… quality control machines used in a lab at a manufacturing facility to test sample products being manufactured for sale.

85

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Other considerations – Machinery & Equipment used to test the following are

typically subject to sales & use tax: » Raw materials prior to acceptance or placement into

storage. » Manufactured product after it is finished.

86

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Pollution Control Machinery & equipment used to eliminate,

prevent, treat, or reduce the volume, toxicity or potential hazards of industrial pollution resulting from manufacturing may be exempt from sales & use tax.

» Includes air, water, wastewater, noise, solid waste or hazardous waste.

87

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Arizona » An exemption is provided for machinery and equipment,

including related structural components, that is employed to prevent, monitor, control or reduce land, water or air pollution.

– Indiana » Sale of tangible personal property is exempt from sales &

use tax if it constitutes, is incorporated into, or is consumed in the operation of a device, facility, or structure predominately used and acquired for the purpose of complying with state, local, or federal governmental environmental quality laws, regulations or standards by persons engaged in manufacturing…

88

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Louisiana » Eligible machinery and equipment includes…machinery

and equipment necessary to control pollution at a plant facility where pollution is produced by the manufacturing operation.

– New Jersey » Certain effluent treatment or conveyance equipment are

exempt from sales and use tax if the Commissioner of the Department of Environmental Protection issues a determination that the equipment and its use will benefit the environment.

89

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– New York » Machinery and equipment qualifies for exemption from all

state and local sales taxes when purchased by a manufacturer and used directly and predominantly in treating, burying, or storing waste materials, when over 50% of the waste results from the manufacturer’s own production processes.

– Texas » Tangible personal property used or consumed in the actual

manufacturing, processing, or fabrication of tangible personal property for ultimate sale if the use or consumption of the property is necessary and essential to a pollution control process is exempt from tax.

90

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Other considerations – Pollution control devices or systems may need to:

» Be certified or approved by the State Dept. of Environmental Quality or similar agency.

» Demonstrate targeted levels of reduced emissions; – Building materials used to construct a pollution control

device or system (i.e., smokestack, wastewater retention pond, etc.) may not qualify for a sales & use tax exemption.

91

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Research & Development What is considered R&D?

» Work directed toward the innovation, introduction and improvement of products and processes.

What is not considered R&D? » Testing or inspecting materials or products for

quality control. » Efficiency surveys. » Management studies. » Consumer surveys, advertising and promotions. » Research for literary, historical or similar projects.

92

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Most states provide a sales & use tax exemption for tangible personal property used in R&D:

– California » On or after July 1, 2014, and before July 1, 2022, there is

partial exemption of 4.1875% from state sales and use taxes for gross receipts from the sale of, and the storage, use, or other consumption in-state of (1) qualified tangible personal property purchased for use by a qualified person for use primarily in R&D.

– Florida » Machinery & Equipment used predominantly for R&D is

exempt from the tax.

93

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Massachusetts » An exemption is provided for the sale or use of materials,

tools and fuel or any substitute that is used or consumed directly and exclusively in R&D by a manufacturing corporation or a R&D corporation. An exemption is also provided for the sale or use of machinery or replacement parts for the machinery used in similar circumstances for R&D.

– Michigan » Sales of tangible personal property to the following are

exempt: an industrial processor for use or consumption in industrial processing. Research or experimental activities are included in the definition of industrial processing.

94

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– New York » Sale of tangible personal property bought for use or

consumption directly and predominantly in R&D in the experimental or laboratory sense is exempt from tax, but installation and repair services performed on exempt equipment do not qualify for the exemption.

– Texas » Effective January 1, 2014, an exemption from sales and use

tax is provided for the sale, storage, or use of depreciable tangible personal property directly used in qualified research (as defined by IRC §41) if the property is sold, leased, or rented to, or stored or used by, a person who is engaged in qualified research and will not claim a credit under Subchapter M, Chapter 171 on a franchise tax report for the period during which the sale, storage, or use occurs.

95

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Washington » Machinery and equipment used as an integral part of a

R&D operation can be exempt from tax. Conditions for this exemption are the same as those for manufacturers.

96

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– Other Areas States may provide sales & use tax exemptions for:

» Integrated systems and equipment used to reduce contamination or to control temperature, humidity, airflow, vibration or other environmental conditions required for manufacturing. (i.e., cleanrooms)

» Lighting (specialized or otherwise) » Industry-specific production requirements.

97

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

– In conclusion… More than just the machinery and equipment used

directly in production activities may be exempt from sales & use tax. Every state defines and taxes manufacturing and

production sales & use tax exemptions differently and what’s considered exempt in one state maybe considered taxable in another.

98

Manufac tur ing and Produc t ion Sa les Tax Exempt ions : Not Jus t fo r Manufac t urers

TRONCONI SEGARRA & ASSOCIATES LLP

Contact

Thomas E. Mazurek, Jr., CPA Principal Tronconi Segarra & Associates LLP 8321 Main Street Williamsville, NY 14221 (716) 633-1373 [email protected] @tronconisegarra

99