manual for the open fiscal lng model - ei sourcebook 2016/manual for the open fiscal... · manual...

TRANSCRIPT

1

Manualforthe

OpenUpstreamGasandLNGModel

ByWolfgangMeinhart

Developedby:T.M.Mitro,Co-DirectorGraduateCertificateinGlobalEnergy,Developmentand

SustainabilityattheUniversityofHoustonAnd

ColumbiaCenteronSustainableInvestmentatColumbiaUniversity

2

TableofContents

1. Introductionandpurposeofthemodel........................................................................3a. Purposeofamodelingeneral.........................................................................................3b. PurposeoftheupstreamandLNGmodel.......................................................................4c. UseoftheupstreamandLNGmodelfordifferentparties..............................................4

2. Explanationofthedifferentstructures.........................................................................5a. NaturalGascomparedtoCrudeOilProjects...................................................................5b. GasProjectSegments,OwnershipStructures,RisksandFinances.................................5c. FiscalArrangementsbySegment....................................................................................8

3. Usingthemodel..........................................................................................................12a. Structure........................................................................................................................12b. CalculationsandOutputs...............................................................................................13

4. Assumptionsandinputvariables................................................................................175. Mozambiqueexample.................................................................................................21a. Assumptionsandreferences.........................................................................................21b. AskingtherightquestionsregardingtheassumptionsandInterpretingtheresults....22

6. Whatthemodeldoesnotinclude...............................................................................25

3

1. Introductionandpurposeofthemodel

a. PurposeofamodelingeneralAfinancial/fiscalmodelprovidesforecastedreturnsofaprojecttotheinvestorandgovernment.Theseestimatesarebasedonfiscal,market,technicalandcorporate inputvariables,manyofwhichareforwardlookingassumptions.Investorsusefinancialmodelstodeterminewhethertogoaheadwithaparticularinvestment.Governmentsusemodelstocomparetheirfiscalregimeswiththeirpeercountriesandtoassesshowmuchrevenuewillflowintothestatecoffersfromaparticularproject.Amodelisfundamentaltohelpanswerthefollowingquestions:

• Whatisthefairnessofthecurrentandpotentialdeals?• Whatistheequitabilityofthefiscalregimeforinvestorsandthegovernment?• Whatisthetrade-offbetween“quickmoney”throughfront-loadedpaymentssuchasa

signaturebonusascomparedtochargingback-loadedpaymentsuchasahigherprofittax?

• Whatistheefficiencyoftaxincentives?• Whatimpactdotaxregimechangeshaveonthefinancialflowstobothparties?• Howdoesthefiscalregimecomparewithothers?• Howdochangesintheownershipandcommercialstructureaffectthefinancialflowsto

bothparties?• Whatareexpectedrevenueflowsfromextractiveindustryprojectsandwhatlong-term

publicinvestmentpoliciescanbefundedandplanned?• Howdorevenueflowsalterifmarketfactors(forexample,changesinpricesorcosts)or

technicalfactorschange?

Tosupportprojectnegotiations,itiscrucialforgovernmentstousefiscalmodelstoassesstheimpactof thenegotiated fiscal termson the returns to the investorand the revenues to thegovernment.Ideallythecompanyandgovernmentsharetheirrespectivemodelstoensurefiscalnegotiations are undertaken on a common understanding. It may be, for example, that thepartiesusedifferentassumptionsregarding futureprices,costs,newdiscoveriesor feedstocksourcestoaplant,etc;whichmayleadtoanimpasseinnegotiationsgiventhatthegovernmentrevenues and investor returns are highly affected by these assumptions. By agreeing on theunderlyingassumptionsandwaysofcalculatingthefinancialflows,bothpartiescannegotiateonthesamebasis.Wenotehoweverthat inagreeingonassumptionsthegovernmentshouldrecognizethatthecompaniesusuallyhavemoreexperienceandinformation.Soacomprehensivedescriptionanddiscussionoftheassumptionsisavitalsteptoassureabalancedunderstandingandidentificationofriskstothegovernment.Given that civil society groups normally do not have access to fiscal models, the use of anindependent ‘open’model suchas thisonemaybe theonlyalternative forassessingprojectreturns and government revenues. They key challenge becomes gaining access to the mainassumptionsthatarenecessaryinordertoperformsuchamodelingexercise.

4

b. PurposeoftheupstreamandLNGmodelThismodelhasbeendevelopedfortrainingpurposes. ItmodelsthegasvaluechainfromtheupstreamprojecttotheuseofgasundertheformofLPG,LNGorasfeedstockforlocalindustrialor power generation uses. It allows users to assess the different LNG structures that can beconsidered when producing LNG: the tolling structure, the Independent Plant Owner/BuyerModelandtheRelatedPartyPlantOwner/BuyerModel.Itprovidesvariousfiscalregimeoptionsfor the upstream and mid-stream sectors to understand the impacts of changes on thegovernment take and the private sector returns. It also allows for users to add additionalupstreamfieldstotheLNGprojectandunderstandwhatimpactthishasontheLNGeconomicswhentheprocessingfacilitiesareshared.

c. UseoftheupstreamandLNGmodelfordifferentpartiesVarious interested parties use project economics models for sometimes related, but oftendifferentpurposes.Upstream Investors – Usually international oil companies and national oil companies areinvestingindevelopingtheupstreamgasdiscoveries.Theyusemodelstoreasonablyensuretheywillachieveanadequatereturnontheirinvestmentsrelativetotheexpectedrangeofgeologic,operational,andpoliticalandmarketrisksthattheytakeon.If they are required to “Carry” state oil company investments, they alsowant to assess thelikelihoodthatthosecarriescanberepaidunderavarietyofscenarios.Investors in the LNG Plant – Usually these are international oil companies and national oilcompanies and oftenmay include international gas buyers, construction companies or localutilitycompanies.Theyareinterestedinassessingtheeconomicviabilityoftheirinvestmentsunderarangeofoperationalandmarketrisksandevaluatingthereliabilityofgassupply.GovernmentsandNationaloilcompanies–Wanttoensuretheprojectsareeconomicallyviableandcontinuetoattractinvestors,butatthesametimeachievethemaximumfinancialbenefitsforthecountrygiventhattheirnaturalresourcesrepresentafiniteassetthatdepletesovertime.Governmentsneedtoplanhowmuchrevenuecanbeexpectedintothegovernmenttreasury,thetimingofthosereceiptsandthevolatilityoverthelifeoftheproject.Nationaloilcompaniesmayneedtoevaluatewhethertheirshareoftheprojectinvestmenthassufficientreturnstobefinancedbylenders.Financialsector–Privatebanksandmulti-lateralslendingdirectlytotheprojectinvestorsutilizeprojecteconomicstoassesstheunderlyingabilityoftheborrowerstorepaytheirprojectloansandquantifytheriskfactorsthatcouldcausedelaysordefaultsinpayment.Financialinstitutionsmakinggeneralpurposeloanstothecountryortolocalbusinesseswillbeinterestedinknowinghowmuchadditionalrevenuesthegovernmentwillbecollecting,whichmayassistinrepayingloans.Credit rating agencies use economicmodels to forecast sources of government and countrywealthtoassistintheirassessmentsanddevelopingtheirratings.

5

CivilSociety–Wanttoknowthatthedealbetweenthegovernmentandtheprivateinvestorsisreasonableandthatitachievesthemaximumreturnsforthecountrywhilestillencouragingnewinvestment. Themodel also serves as ameans of independently evaluatingwhat should becoming into the government treasury in any period and comparing that to actual reportedrevenues.GasBuyers–InternationalLNGbuyersorlocalutilitycompanieswanttoassessthebasicviabilityandreliabilityoftheprojectsandwhethertheycancontinuetooperateandsupplythemwithgasunderavarietyoffuturemarketconditions.

2. Explanationofthedifferentstructures

a. NaturalGascomparedtoCrudeOilProjectsNaturalgasprojectsaredifferentthanoilprojects,becauseofthefollowingfactors:

• Naturalgascannotbeeasilystoredandcostsoftransportation(pipelineandtankers)andtreating(separationofliquidsandliquefactionandregasification)aremuchhigherthanforoil.Eachsegmentoftransportationandtreatingofnaturalgasentailsverydifferentcosts,technologiesandriskscomparedtotheupstreamextraction.

• Greatereconomiesof scaleareoften required for LNGplants tobeeconomically andoperationallyviable;consequentlythegastobesuppliedtoanLNGplantoftencomesfromseveraldifferentblocks,eachwithdifferentinvestors.

• Marketsforgasaresmallerandmoresegmentedthanforoil.

b. GasProjectSegments,OwnershipStructures,RisksandFinancesBecauseoftheabovevariationsinrisksandtechnicalprocessesvarioussegmentsofgasprojectsoftentakeadifferentlegalandownershipform.Activitiesandinvestmentsinthenaturalgas“value chain” are quite often split between different entities or groups of investors and notundertakenbythesamegroupofinvestors.Commercialinterests,taxandfiscaltreatmentmayvarybysegment.Upstream–Theownershipandlegalstructureareusuallydeterminedbythegovernmentwhodecideswhichpartiesareawardedtherightstoexploreandexploittheoilandgasreservesinaparticularblock.Usuallythisisagroupofcompaniescomprisinganunincorporatedjointventure(JV),oftentimes including thenationaloil company. Theremaybemore thanoneblock thatproducesgasinaregionandeachofthoseblockswillhaveadifferentsetofowners/investors.Duetothehighrisksofnotfindingexplorationsuccessorreservesbeinguneconomic,successfulupstreamprojectsoftenearnhigherratesofreturnsthantheothersegmentsofthevaluechain,e.g.15%orhigher.GasGatheringPipeline(s)–Thegasproducedintheupstreamsectormustbetransportedtoshoretobeprocessed.Ifonlyoneblockusesthispipeline,oftentheupstreamblockpartnersmayalsobuildandownthegaspipelineeitherthroughthesameJVorviaadifferentcompanythat they form. Ifmore thanoneblockuses thegaspipeline, then theremaybea separatecompanywiththesameordifferentownershipthatchargesatarifftotheupstreamproducers

6

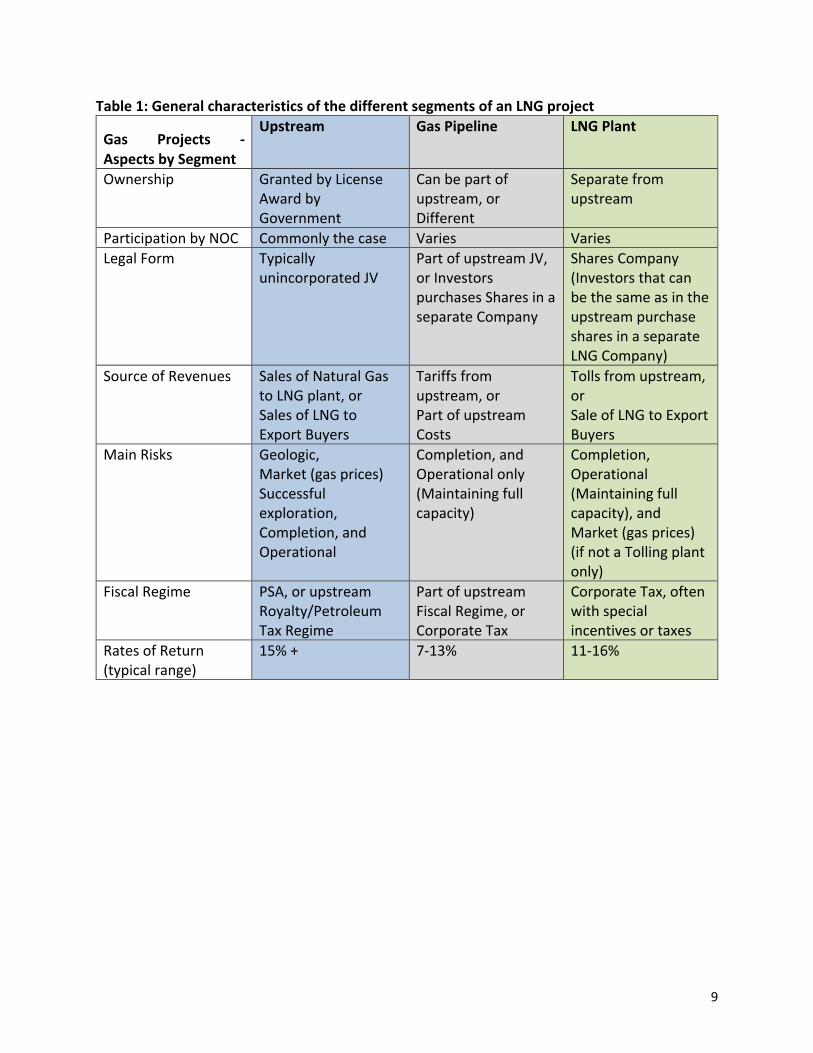

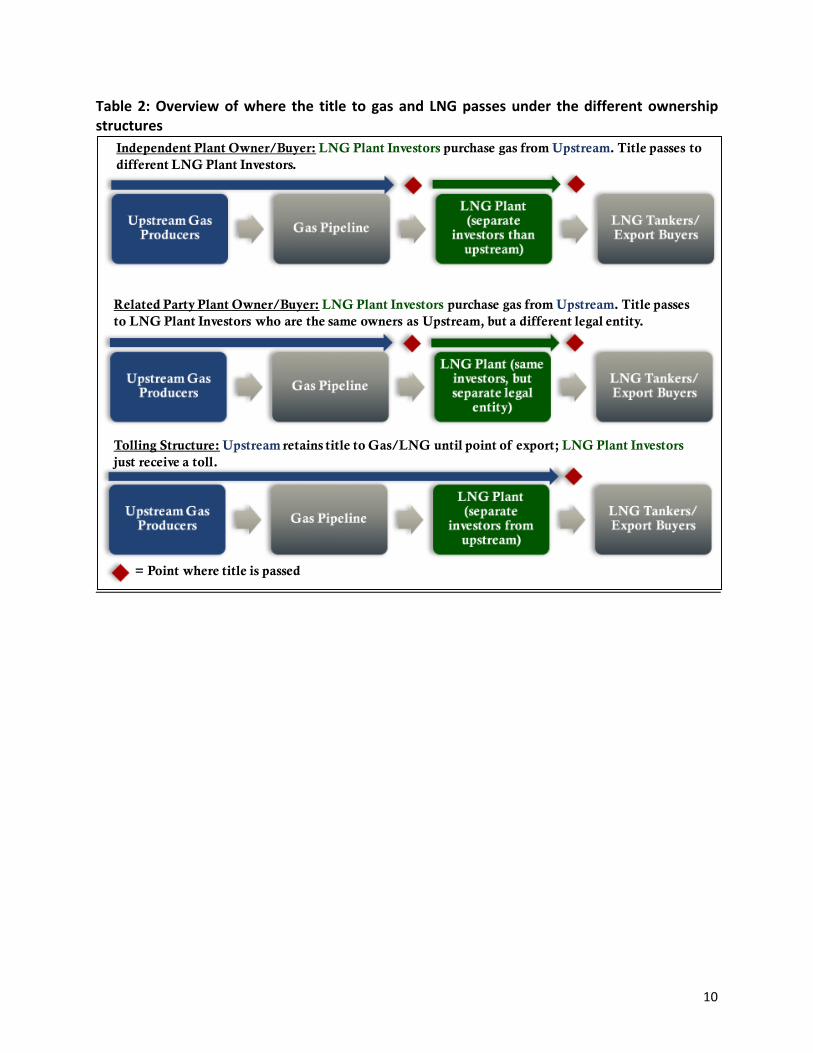

touseit(seeline95inthe‘Assumptions&Results’sheetinthemodel).UnlessitispartoftheupstreamJV,thegaspipelinedoesnottakeownershipofthenaturalgas–itisconsideredtobeashipperonly.Itiscommontohavemostoftheupstreampartnersalsobepartnersinthegaspipeline.Butitisimportanttonotethatthispipelineisastrategicassetandhasthepotentialtobemonopolizedbecauseanyonesetofownersmaydecidetorestrictitsuseorchargeveryhightariffs to any new blocks thatwant to use it. Consequently,many countries regulate thesepipelinesortakeownership1throughthegovernmenttoensurethatitscapacityremainsopenandreasonablypricedtoanynewproducers.Sincepipelineshaverelativelylowtechnicalandcommercialrisk,theyoftenearnonlymediumlevelofreturn–typicallyintherangeof8-12%.LPGExtraction–Dependingonthe“richness”(carboncontent)ofthenaturalgasproduced,itmaybemoreeconomictoextractandseparatelyselltheliquidsfromthenaturalgasstreamasLiquefied Petroleum Gas (Butane, Propane, etc.) prior to the liquefaction process. Theinvestmenttoextractliquidsfromthegasstreamcanbemadebytheupstreamgroupormaybemade by the LNGplant owners. Thismodel (Cell C14 in the ‘Assumptions&Results’ sheet)providestheoptionofevaluatingeitherLPGinvestoralternative,ornoLPGextractionatallifthegas stream is not considered to be “wet”. LPG extraction revenues typically would only bereceivedbytheLNGplantownersiftheplantownerstooktitletothegasstream,whichisnotthecaseinanormaltollingscenario(seeTable2).LNGPlant–Theseplantsoftenrequireproductionfromseveraldifferentblocksinordertobeeconomicandentailverydifferenttechnicalandcommercialrisksthanupstreaminvestments.InadditiontherecanbeclearcommercialconflictsofinterestbetweenupstreamsuppliersofgasandtheLNGplantasthebuyerofgasandresellerofLNG.BecauseofthesefactorsitismostcommonthattheLNGinvestorsareacompletelyseparategroupthantheupstreaminvestors,althoughitisnotuncommontoincludesomeoftheupstreaminvestorsintheLNGgroupaswell.TypicallytheLNGplantcommercialstructureisoneofthreeoptions:

1. TollingPlantModel–TheLNGplantinvestorspaythecapitalandoperatingcostsoftheplant,buttheownershipoftheproducedgasremainswiththeupstreamproducers.TheLNGplantownerschargeanegotiatedfeeperunitofgasprocessedastheirsourceofrevenues(Line97ofthe‘Assumptions&Results’sheetinthemodel).AfterpayingfortheprocessingofgasintoLNG,theupstreamownersmarketandsellthegasintotheexportmarket.

2. IndependentPlantOwner/BuyerModel-SeparateLNGplantownersarethebuyersoftheunprocessedgas.Underthisstructure,aseparategroupofLNGplantinvestorspaysthecapitalandoperatingcostsoftheLNGplant,andthoseLNGinvestorspurchaseandtaketitleofthegasonanarms-lengthbasisfromtheupstreamownersasitentersthe

1Angolaisacaseinpoint:Aspartoftheoveralldealtheupstreamblockswererequiredtopayallcapitalcostsofthegaspipelines,andcouldincludethemintheirPSAcostrecovery.Uponcompletionofconstruction,thefullownershipwastransferredtoSonangol,theStateownedcompany.AlloftheLNGpartnerswerepartofthemanagementofthepipelineandsharedtheoperatingcosts,butultimatecontrolandownershipwaspassedtotheStateasitwasviewedasastrategicassetnecessarytoenablenewfieldstobeabletoaccesstheLNGplant.

7

plant“gate”fromthegaspipeline.TheLNGinvestorsthenselltheLNGintotheexportmarket.

3. RelatedPartyPlantOwner/BuyerModel-UpstreaminvestorsownandoperatetheLNG

plant.Thisissimilartothemodeloptionabove,buttheownershipoftheLNGplantisthesameastheupstreamownershipgroup.Duetoseparatetaxregimesthattypicallytreatupstream activities differently than an LNG plant, there is usually a requirement toestablishatransferprice(Line4ofthe‘Assumptions&Results’sheetinthemodel)fromtheupstreamtotherelatedpartiesinLNGplant.TheGovernmentwouldnormallybethearbiterofwhatconstitutesafairtransferpricefortaxpurposes.

Themodelpermitstheassessmentofthethreestructures.TheIndependentPlantOwner/BuyerModel and the Related Party Plant Owner/Buyer Model structures are evaluated in theworksheetscalled“LNGequity”and“ConsolidatedLNGequity”.Themodelwouldrequirethesameitemsofinputandwouldutilizethesamecomputation.Thedifferencebetweenthesetwostructureswouldbethatonewoulduseanarms-lengthmarketpriceandtheotherwoulduseanagreed transfer price.2 Even though theownership structuremaybedifferent, the fiscal andeconomic result should be the same. Users of themodel can assess the impact on investorreturns and government revenues under different transfer price scenarios (in the sensitivityanalysissectionofthe‘Assumptions&Results’sheet).Thetollingplantstructureisevaluatedintheworksheetscalled“LNGTolling”and“ConsolidatedLNGTolling”sheets.There can be variations in all of these forms, so the substance of the structure must bescrutinizedtoensuretherightoptionisselectedinthemodel,nottomentioninreviewingtheactualproposalsgivenbytheinvestor.LNGTankers–ThereareseveraloptionsforownershipandcontrolofthehighcostspecializedrefrigeratedLNGtankers.InmanycasesLNGbuyersownorcharterhireandmanagetheseLNGtankers(Line8ofthe‘Assumptions&Results’sheetinthemodel);andtheLNGissoldonanfreeonboard (FOB)basis from theLNGplant (Line7of the ‘Assumptions&Results’ sheet in themodel).InothercasestheLNGsellersthemselvesmayownorcharterhiretheLNGvessels;andinthosecasestheLNGmaybesoldonaDeliveredex-Ship(DES)basispriceasdeterminedatmarketat theregasificationreceivingterminalcountry (Line9of the ‘Assumptions&Results’sheetinthemodel).ThereareoftenvariationswherebytheLNGownersmayownorcharterhiresomevesselsandsellthosecargoesonaDESbasis,butwillselltheremainderoftheLNGtobuyersonaFOBbasisunderanarrangementwherethebuyersarrangeandpaythecostsoftheirownLNGvessels.ThemodelallowsuserstoeitherchoosetheFOBorDESmethod.Iftheproject

2Forthepurposeofthemodel,nodistinctionismadebetweenasaletoanunrelatedorarelatedparty.Thereisonly1)thefinalexportpriceoftheLNG,and2)thepricethattheLNGplantownerspaytotheupstreamownerstoacquirethegas("transferprice").Themethodsfordeterminingeitherofthosepricescanvaryconsiderably(dependingonsuchfactorsasthecostandscopeandnumberoftrainsoftheLNGplant,whetherthegasiswetordry,thedistanceandcosttotransportthegastotheplant,andwhatmarkettheLNGisbeingsoldinto).Toderivethetransferprice,asimplisticpercentageformulaisused,irrespectiveofwhethertheLNGownerswererelatedtotheupstreamowners.Itwouldalwaysbeuptothegovernmenttocontinuallyreviewortrytoadjustanypricesproposedbetweenrelatedpartiesduringthelifeoftheplant.

8

usesamixofbothmethods,theusermustcomputetheaveragepriceandaveragetankercostsoutsidethemodelbeforeinputtinginanyoneyear.

c. Fiscal3ArrangementsbySegment• TheupstreamsectorfiscaltermsaredeterminedbythePSAorlegislationregardingtaxes

androyalties. The informationrequired for the input intothemodelcanbeobtainedfromthosedocuments.

• Thegaspipelinecostsusuallyareeitherconsideredpartoftheupstreamcostsforfiscalpurposes,orifaseparateentity,wouldtypicallybepartofthecountry’scorporateincometaxregime.

• TheLNGplantisusuallypartofthecountry’scorporateincometaxregime,butinmanycasestheplantownersnegotiatefiscaltermsthatcouldincludefeaturessuchas:

o Permitting some capital costs from LNG tobe taken as deductions against theupstreamfiscalregime.Typically,thiswouldonlybepossibleinsituationswheretheLNGequityinvestorsarethesameastheupstreaminvestors.

o Aspecifiedperiodoftaxholidaysortaxexemptionso Special levy imposed if gasprices rise abovea certain level and the LNGplant

investorsarethesellersoftheLNG.o WhentheLNGplantisownedbythesamegroupofinvestorsastheupstream,

thereisusuallyan“arms-length”typeoftransferpricingrequiredforthegasinordertodeterminethetaxandfiscaltreatmentandsplitbetweentheupstreamfiscalregimeandthedownstream.

Tables1,2,3below,summarizetheaboveexplanations.

3Notethatthemodelallowstousetwotypesofprofitsharingarrangements–R-Factorbasedandproduction-based

9

Table1:GeneralcharacteristicsofthedifferentsegmentsofanLNGproject

Gas Projects -AspectsbySegment

Upstream GasPipeline LNGPlant

Ownership GrantedbyLicenseAwardbyGovernment

Canbepartofupstream,orDifferent

Separatefromupstream

ParticipationbyNOC Commonlythecase Varies VariesLegalForm Typically

unincorporatedJVPartofupstreamJV,orInvestorspurchasesSharesinaseparateCompany

SharesCompany(InvestorsthatcanbethesameasintheupstreampurchasesharesinaseparateLNGCompany)

SourceofRevenues SalesofNaturalGastoLNGplant,orSalesofLNGtoExportBuyers

Tariffsfromupstream,orPartofupstreamCosts

Tollsfromupstream,orSaleofLNGtoExportBuyers

MainRisks Geologic,Market(gasprices)Successfulexploration,Completion,andOperational

Completion,andOperationalonly(Maintainingfullcapacity)

Completion,Operational(Maintainingfullcapacity),andMarket(gasprices)(ifnotaTollingplantonly)

FiscalRegime PSA,orupstreamRoyalty/PetroleumTaxRegime

PartofupstreamFiscalRegime,orCorporateTax

CorporateTax,oftenwithspecialincentivesortaxes

RatesofReturn(typicalrange)

15%+ 7-13% 11-16%

10

Table2:Overviewofwhere the title to gasand LNGpassesunder thedifferentownershipstructures

Independent Plant Owner/Buyer: LNG Plant Investors purchase gas from Upstream. Title passes to different LNG Plant Investors.

Related Party Plant Owner/Buyer: LNG Plant Investors purchase gas from Upstream. Title passes to LNG Plant Investors who are the same owners as Upstream, but a different legal entity.

Tolling Structure: Upstream retains title to Gas/LNG until point of export; LNG Plant Investorsjust receive a toll.

= Point where title is passed

11

Table3:Overviewofwhich segment isbearing the risk factoraccording to the commercialstructure

RiskFactor: TollingStructure EquityStructure–LNGPlantownersaresameasupstream

EquityStructure–LNGPlantownersareseparate

LNGmarketpricerisks

Upstreambearsfullrisk LNGplantinvestorsbearfullrisk

LNGplantinvestorsbearfullriskunlesstransferpricefromupstreamislinkedtomarketprice

Gastransferpricetoplant

Notapplicablesincegasisnotsoldtoplant

Upstreamownerswantaslowaspossible

Upstreamownerswantashighaspossibleandplantownersaslowpossible–whichwillgetthepartiestoatruearm’slengthprice

Upstreamproductionandreservesrisks

BothupstreamandLNGinvestorsbearriskunlessthereisasend-or-payclausetoprotectplantinvestors

BothupstreamandLNGinvestorsbearrisk,butcouldentailashiftduetodifferentfiscalregimes.

BothupstreamandLNGinvestorsbearriskunlessthereisatake-or-payclausetoprotectplantinvestors

LNGplantoperabilityanddowntimerisks

BothupstreamandLNGinvestorsbearriskunlessthereisatake-or-payclausetoprotectupstreaminvestors

BothupstreamandLNGinvestorsbearrisk

BothupstreamandLNGinvestorsbearriskunlessthereisatake-or-payclausetoprotectupstreaminvestors

LNGplantcapitalcostrisks

LNGplantinvestorstakefullrisk,unlesstollingtariffformulaislinkedtocosts

LNGplantinvestorsbearfullrisk

LNGplantinvestorsbearfullrisk

LNGevaporationproductloss

Upstreambearsfullcost LNGplantinvestorsbearfullcost

LNGplantinvestorsbearfullcost

Upstreamcapitalcostrisks

Upstreambearsfullrisk Upstreambearsfullrisk

Upstreambearsfullrisk

12

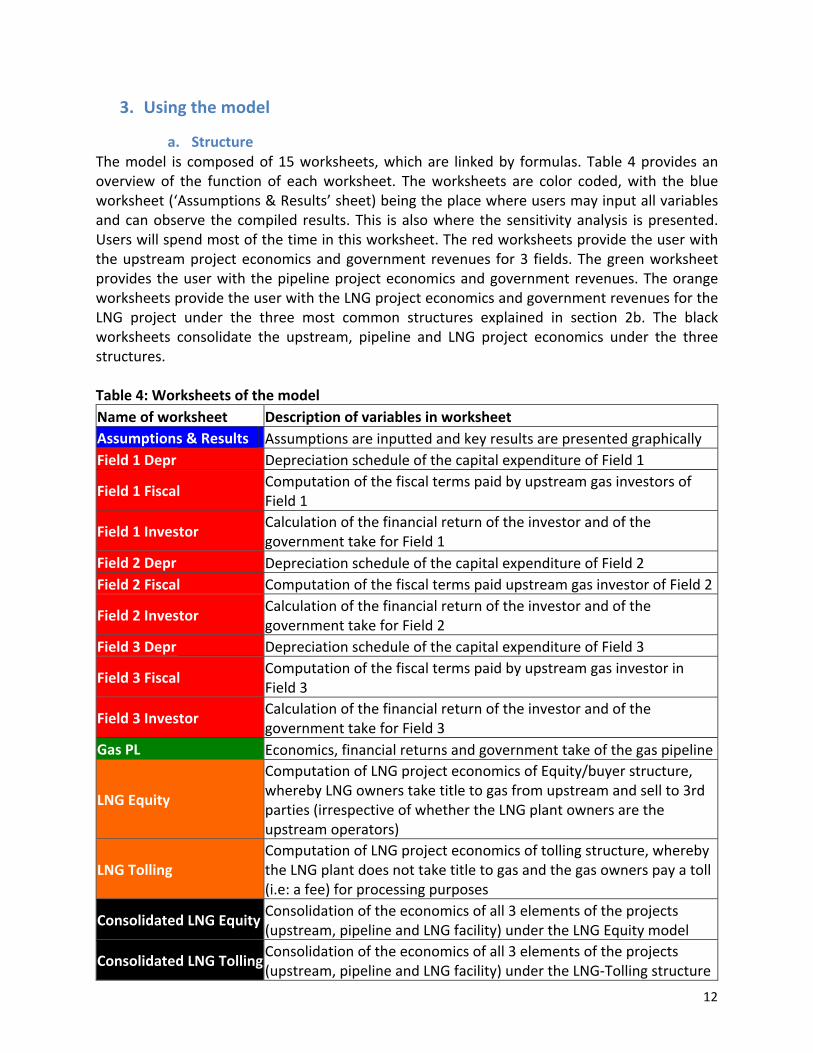

3. Usingthemodel

a. StructureThemodel is composedof15worksheets,whichare linkedby formulas.Table4providesanoverview of the function of eachworksheet. Theworksheets are color coded,with the blueworksheet(‘Assumptions&Results’sheet)beingtheplacewhereusersmayinputallvariablesandcanobserve thecompiled results.This isalsowhere thesensitivityanalysis ispresented.Userswillspendmostofthetimeinthisworksheet.Theredworksheetsprovidetheuserwiththeupstreamprojecteconomicsandgovernment revenues for3 fields.Thegreenworksheetprovidestheuserwiththepipelineprojecteconomicsandgovernmentrevenues.TheorangeworksheetsprovidetheuserwiththeLNGprojecteconomicsandgovernmentrevenuesfortheLNG project under the three most common structures explained in section 2b. The blackworksheets consolidate the upstream, pipeline and LNG project economics under the threestructures.Table4:WorksheetsofthemodelNameofworksheet DescriptionofvariablesinworksheetAssumptions&Results AssumptionsareinputtedandkeyresultsarepresentedgraphicallyField1Depr DepreciationscheduleofthecapitalexpenditureofField1

Field1Fiscal ComputationofthefiscaltermspaidbyupstreamgasinvestorsofField1

Field1Investor CalculationofthefinancialreturnoftheinvestorandofthegovernmenttakeforField1

Field2Depr DepreciationscheduleofthecapitalexpenditureofField2Field2Fiscal ComputationofthefiscaltermspaidupstreamgasinvestorofField2

Field2Investor CalculationofthefinancialreturnoftheinvestorandofthegovernmenttakeforField2

Field3Depr DepreciationscheduleofthecapitalexpenditureofField3

Field3Fiscal ComputationofthefiscaltermspaidbyupstreamgasinvestorinField3

Field3Investor CalculationofthefinancialreturnoftheinvestorandofthegovernmenttakeforField3

GasPL Economics,financialreturnsandgovernmenttakeofthegaspipeline

LNGEquity

ComputationofLNGprojecteconomicsofEquity/buyerstructure,wherebyLNGownerstaketitletogasfromupstreamandsellto3rdparties(irrespectiveofwhethertheLNGplantownersaretheupstreamoperators)

LNGTollingComputationofLNGprojecteconomicsoftollingstructure,wherebytheLNGplantdoesnottaketitletogasandthegasownerspayatoll(i.e:afee)forprocessingpurposes

ConsolidatedLNGEquityConsolidationoftheeconomicsofall3elementsoftheprojects(upstream,pipelineandLNGfacility)undertheLNGEquitymodel

ConsolidatedLNGTollingConsolidationoftheeconomicsofall3elementsoftheprojects(upstream,pipelineandLNGfacility)undertheLNG-Tollingstructure

13

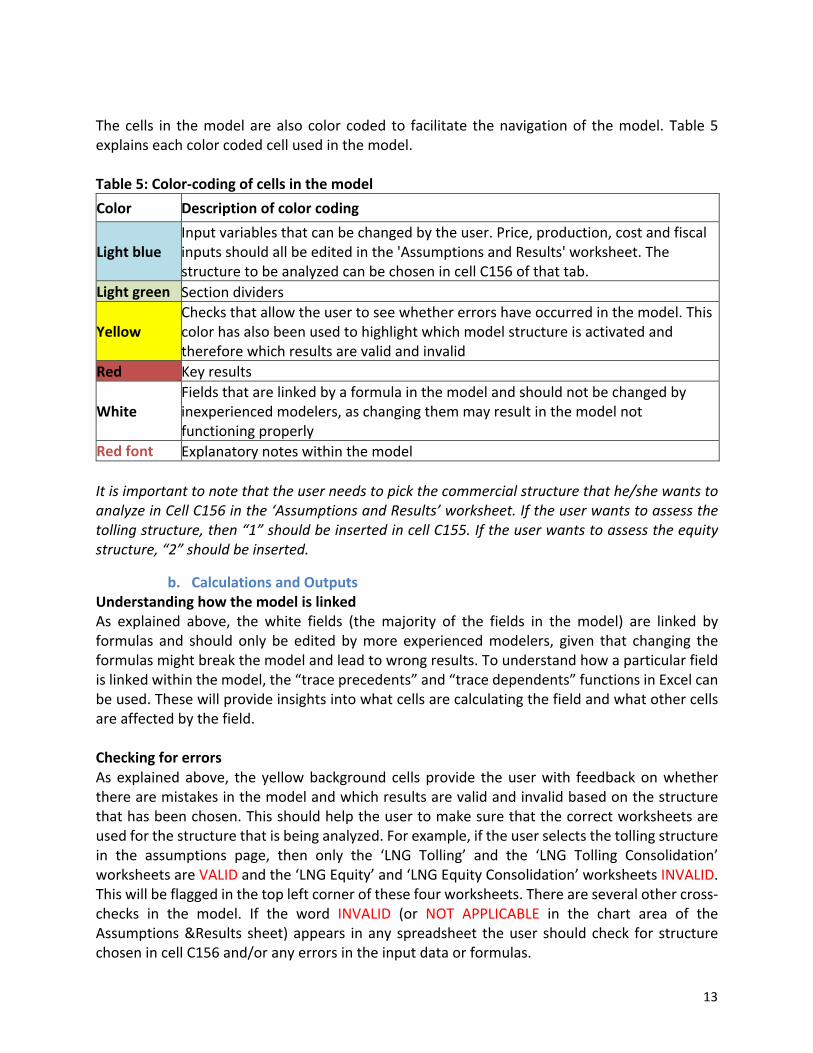

Thecells in themodelarealsocolor coded to facilitate thenavigationof themodel.Table5explainseachcolorcodedcellusedinthemodel.Table5:Color-codingofcellsinthemodelColor Descriptionofcolorcoding

LightblueInputvariablesthatcanbechangedbytheuser.Price,production,costandfiscalinputsshouldallbeeditedinthe'AssumptionsandResults'worksheet.ThestructuretobeanalyzedcanbechosenincellC156ofthattab.

Lightgreen Sectiondividers

YellowChecksthatallowtheusertoseewhethererrorshaveoccurredinthemodel.Thiscolorhasalsobeenusedtohighlightwhichmodelstructureisactivatedandthereforewhichresultsarevalidandinvalid

Red Keyresults

WhiteFieldsthatarelinkedbyaformulainthemodelandshouldnotbechangedbyinexperiencedmodelers,aschangingthemmayresultinthemodelnotfunctioningproperly

Redfont ExplanatorynoteswithinthemodelItisimportanttonotethattheuserneedstopickthecommercialstructurethathe/shewantstoanalyzeinCellC156inthe‘AssumptionsandResults’worksheet.Iftheuserwantstoassessthetollingstructure,then“1”shouldbeinsertedincellC155.Iftheuserwantstoassesstheequitystructure,“2”shouldbeinserted.

b. CalculationsandOutputsUnderstandinghowthemodelislinkedAs explained above, the white fields (themajority of the fields in themodel) are linked byformulas and should only be edited bymore experiencedmodelers, given that changing theformulasmightbreakthemodelandleadtowrongresults.Tounderstandhowaparticularfieldislinkedwithinthemodel,the“traceprecedents”and“tracedependents”functionsinExcelcanbeused.Thesewillprovideinsightsintowhatcellsarecalculatingthefieldandwhatothercellsareaffectedbythefield.CheckingforerrorsAsexplainedabove, the yellowbackground cells provide theuserwith feedbackonwhethertherearemistakesinthemodelandwhichresultsarevalidandinvalidbasedonthestructurethathasbeenchosen.Thisshouldhelptheusertomakesurethatthecorrectworksheetsareusedforthestructurethatisbeinganalyzed.Forexample,iftheuserselectsthetollingstructurein the assumptions page, then only the ‘LNG Tolling’ and the ‘LNG Tolling Consolidation’worksheetsareVALIDandthe‘LNGEquity’and‘LNGEquityConsolidation’worksheetsINVALID.Thiswillbeflaggedinthetopleftcornerofthesefourworksheets.Thereareseveralothercross-checks in the model. If the word INVALID (or NOT APPLICABLE in the chart area of theAssumptions&Results sheet)appears inany spreadsheet theuser should check for structurechosenincellC156and/oranyerrorsintheinputdataorformulas.

14

Checkingandunderstandingtheresults• Checkingthatprojectandinvestorreturnsarereasonable–Usersshouldcheckthenet

present value (NPV) and internal rate of return (IRR) for each of the segment of theproject.4BoththeNPVandIRRindicatorstakeintoaccountthetime-valueofmoney.Ahigher discount rate used for the NPV calculation means that later cash flows arediscounted at a higher rate (i.e. that later cash flows are worth less). The IRR is thediscountrateatwhichNPV=0.Table1ofthisguideprovidesaroughreferenceastowhatrangeofreturns(IRR)arerequiredforeachsegment(theseratesareonlyballparkfiguresandneedtoberiskadjusted).Allofthesegmentsneedtobecommerciallyviableinorderfor thewhole project to go ahead and attract investors. If the results show that theindividualsegmentsareearningmuchlowerormuchhigherratesofreturn,itmaybeasignthattheassumptionsneedtobereviewed,thattheprojectisnoteconomicand/orthatthefiscalsystemistooonerous.Iftheratesofreturnarehigh,thecommercialtermsmaybeundulyskewedtotheinvestorswiththegovernmentbeingabletoincreasetaxesandstillattractinginvestors.

• CheckingthattheGovernmentTake(GT)isreasonable-AnotherfactortolookatistheGT,whichisdefinedasallpaymentsgoingtothegovernment(royalties,Government’sshareofproductionunderaPSA,incometaxes,etc)dividedbythepre-taxprojectcashflows.Giventhehigherreturnsontheupstreamsegment,GTtendstobehighertherethanforthepipelineandLNGsegment.ApartfromreviewingtheGTfortheindividualprojects, the consolidated GT should also be reviewed to assess whether subsidies,incentivesorfiscalreliefsgrantedinoneormoresegments(necessarytoreachtheNPVandIRRtomakethosesegmentsattractiveforinvestors)areworthitonaconsolidatedbasis.

• Checking the interpretation of the fiscal terms, assessing the impacts of differentstructuresandpotentialforprofitshifting-Whendecidingonthecommercialandlegalownershipstructurefortheprojectitisimportanttounderstandhowthefiscaltermsareinterpreted,asdifferentinterpretationsmayhavealargeimpactontherevenueflows.Forinstance,whenconsideringatollingstructuretheupstreaminvestorsmayfindthattreatingthetollingcostsassimpleoperatingcostsubjecttocostrecoverymaycreateadisadvantage by displacing or deferring recovery of costs from the other upstreamoperationsandcapitalspending.Whencomparedtoothercommercialorlegalstructures,suchastheequityoptionofsellingthegastotheLNGplant,theinvestoreconomicsarenegatively affected. In this type of case, the upstream operators may seek aninterpretationofthePSAthatwouldallowthemequivalencywiththeotherownershipoptions.Inthisexample,ameansofachievingthatparitywouldbeto“netback”thefinalLNG FOB price by netting out the tolling costs.5 These interpretations can be verytechnicalandnoteasytofollow,butcanbecriticaltothefinancialreturnstoinvestorsandtotheGovernment.

4CellsC38andC39ofthe‘investor’worksheetsforfield1,2,3;cellsC37andC38ofthe‘GasPL’worksheet;cellsC44andC45ofthe‘LNGequity’worksheet,cellsC33andC34ofthe‘LNGTolling’worksheet;cellsC31andC32ofthe‘ConsolidatedLNGequity’worksheet’;andcellsC29andC30ofthe‘ConsolidatedTolling’worksheet.5ThisiswhatthismodeldoesinLines4-5ofthe‘FieldXFiscal’sheets.

15

AnotherinterpretationexamplecomesfromcountrieswherethegovernmentallowstheinvestorstointerpretthePSAinsuchawaytopermitsomeoftheLNGcapitalcoststobeconsidered“upstream”innatureandtherebybecomepartofPSACostRecovery.SinceeffectiveGovernmentTake isgenerallyhigher in theupstream, thishas the impactofimprovingtheinvestor’srateofreturnbyreducingprofitgasandtaxes. Thiscanbealegitimatemeansof incentivizingLNGinvestment,butmustberecognizedasbeing, ineffect,asubsidybythegovernment. ThislattertypeofinterpretationwouldnormallynotbeconsideredunlesstheprojectstructurewastheRelatedPartyPlantOwner/BuyerModelwhere the upstream investorswere the same as the LNGplan investors. ThemodelprovidesoptionstoallowforthepipelineandLNGexpenditurestobedeductedfromtheupstreamproject.6Furthermore,themodelalsoallowsforthetransferpricefromtheupstreamtotheLNGprojecttobeadjusted.Ifthetransferpriceisreduced,theupstreamprojectwillappearlesseconomic,while theLNGprojectappearsmoreeconomic. This impact shouldbeviewedwithcautionasareductionofthetransferpricewillalsoresultinafallinoverallgovernment revenues given that the LNG segment is taxed at a lower rate than theupstreamsegment.IfupstreamownersalsoowntheLNGplanttheywillhaveanaturalbenefitandincentivetoshiftrevenuestoalowertaxregime,whichmeanslessforthegovernment.

• Understandingthetimingofgovernmentrevenues.Asnotedabove,earlyreturnstotheinvestorwill increase the IRR andNPVof theproject.Given thehigh levels of capitalexpenditurerequiredforoilandgasprojects,itiscommonforcountriestoallowforcostrecoveryanddepreciationinthefiscalterms.Thiswillresultingovernmentrevenueflowsbeingdelayed. The consolidatedworksheetsprovide the government and civil societywith an indication ofwhen revenues from the various segments should be expected,whichmayhelpgovernmentsinfiscalplanningandmanageexpectationsofcivilsociety.

• Checkingthecompetitivenessofthefiscalterms.Inordertotestthecompetitivenessofthe fiscal terms, itmaybeworthwhile runninga“benchmarking”evaluationofsimilarprojectsinthesamecountryorinanothercountry(Seesourcesofdataandassumptionssectionofwheredataforsimilarprojectsmaybefound).

• Understandingthesensitivityanalysis.Itisimportanttotesttheresilienceoftheresultsunderarangeofcircumstances.Thisexercise iscalled“sensitivityanalysis”.While theresultsfortheinvestorsandforthegovernmentmaylookreasonableinthebasecase,itisimportanttoensurethattheseresultsholdundermodifiedassumptions.Forexample,itshouldbetestedthattheinvestorIRRandNPVindicatorsdonotcompletelycollapsewhenthegaspricesmoderatelyfallandthatgovernmenttakeincreaseswithariseingasprices.Ifeitheristhecase,itislikelythattherewillbepressuresforthecontracttoberenegotiatedwhencommoditypriceschange.Thismodelprovidesforsensitivityanalysesfromline237inthe‘AssumptionsandResults’worksheet.Apartfrompricechanges,the

6Themodelgivesthispossibilityinlines61-65and77-85ofthe‘Assumptions&Results’sheet.

16

sensitivityanalysis tests the impactsofvaryingassumptions regarding theproduction,capitalexpenditure,tollingfeesanddelayinproductionstart.

o The sensitivity analyses are calculated using the ‘data table’ function in Excel,whichcannotbetracedbythe‘traceprecedents’function.Ifaparticularresultinthesensitivityanalysisissurprisingandtheuserisunfamiliarwiththe‘datatable’function,itisrecommendedtore-runthemodelwiththerevisedassumptionstobetterunderstandtheresults.

o Totestthesensitivityoflowerproductionvolumesandproductionstartdelays,themodelincludesadditionalinputvariablesfortheupstreamgasfield1,whichhavenotbeenreplicatedforfields2and3.Thisisforillustrativepurposes.Thesame sensitivities should be performed for these two other fields once moreinformationisavailable.

17

4. AssumptionsandinputvariablesInputassumptionshaveasignificantimpactonthemodeledresults.Iftheinputassumptionsarewrong,theresultswillalsobewrong.Thereforeacarefulreviewneedstobeundertakenoftheavailableinformation.Themostsignificantinputassumptionsanddataareasfollows:Forecastprices–GenerallyLNGandnaturalgasthatisproducedandsoldfromanycountryispricedbasedoninternationalmarkets.Thosemarketsaredividedintothreeregionalmarkets:1)NorthAmerica,where thepricingpoint is called “HenryHub”and is theprimaryprice fornaturalgas futurescontracts tradedontheNewYorkMercantileExchangeandtheover-the-counter(OTC)swapstradedonthe IntercontinentalExchange(ICE);2)AsiawherethepricingbenchmarkiscalledJapanCustoms–clearedCrude(JCC),whichistheaveragepriceofcrudeofthesecondlargestAsianimporterandisacommonlyusedindexinlongtermLNGcontractsinJapan,KoreaandTaiwan;and3)EuropewherethetradingpointiscalledtheNationalBalancingPoint,whichisthevirtualtradinglocationforthesaleandpurchaseandexchangeofUKnaturalgasandisthepricinganddeliverypointfortheICEFuturesEuropenaturalgascontract.LNGpricingreferencesandbenchmarksarestillevolving.LNGpricestypicallyareagreedwithindividualbuyersunderacontractformula.Theseformulaecanvary,buttypicalmethodsinclude:

• Directlylinkedtoapublishednaturalgasindexpriceatalargenaturalgasmarket,e.g.HenryHub.

• Directly linkedtoapublishedcrudeoil indexpriceforawidelytradedcrudetype,e.g.Brent. This typeofpricewouldalso requireanadjustment to recognize thedifferentenergy content, processing requirements and standard ofmeasurement of oil versusnaturalgas.

• Anagreedblendedmixoftheabovetwobasicmethods.

ThesepricesareusuallyonaDESbasis(atthemarket)andmaybefurtheradjustedtoanFOBbasistorecognizetransportationcoststoreachsuchreferencemarkets,energyorBTUcontentofthegas,andwhetherthecontractisshortorlongerterminnature.Markets are affected by general growth in energy consuming economies and its effect ondemand forenergy,easeof substitutionofone typeof fuel foranother,andcompetingLNGprojects inotherpartsof theworld. Often itmaybebest touseas abase casea generallyrecognized forecast of prices, such as those from the World Bank (seehttp://www.worldbank.org/en/research/commodity-markets).Allthatweknowaboutanypriceforecastisthatitwillbewrong,sotestingarangeofsensitivitycasesforpricesisessentialtobetterunderstandtherisksandupsidesandhowtheymayaffectthekeyresults.Productionforecasts–Notonlyareupstreamproductionratesandreservesneededtorunthemodel,itisalsoimportanttonotethatfornaturalgasprojectsthereisalwaysacertainamountof“productloss”asthenaturalgasmaybeusedasafuelinrunningmachineryorequipment,

18

plusintheprocessofbeingcooledtoaliquidformorbeingwarmedbackintoagaseousformandstoredusuallyentailsa certainamountofevaporation. Keep inmind that fullupstreamproductioncapacitywillalwaysconstrainedbytheLNGplantdesignedcapacitytotakethegasand by any LNG plant downtime for maintenance or emergency shut-ins. Consequently,upstreamproductionforecastsmusttakethisintoaccount.Themodelincludesinputforthesefactors.7Withrespecttoproductlossduetoevaporationorrunningmachinery,intheTollingmodeltheupstreamgasownersbeartheimpactofanyproductlossorevaporationduringtheLNGplantprocessingastheywouldstillpaythetollbasedonproductgoingintotheplantandstillretainownershipofthegas.8IntheEquitymodeltheLNGplantownersbeartheeconomicimpactoftheproductlosssincetheytooktitletothegasattheLNGplantgate9(seeTable3).Domesticsupplyofgas–SincenaturalgasandLPGcanbeusedrelativelycheaplyandeasilydomesticallyforelectricalpowergenerationordirectindustrialorconsumerpurposes,mostLNGprojectscontainsomerequirementfornaturalgasorLPGtobesuppliedtolocalmarkets.Thenegotiationofthevolumestobededicatedforthispurpose,thedeterminationofthesalespriceandthetaxtreatmentcanbecomecriticalissuestoinvestorsandthegovernment.Thechallengeisthattheamountactuallyutilizedinthedomesticmarketmaybuildorvaryannuallyasthegasmarketsarebeingdevelopedwhereasinvestorsarelocked-ininlong-termgascontractswithgasbuyers.Themodelpermitsarangeofassumptionstobeincorporated.10Capitalcostsforecasts–Sincecapitalcostsoccurintheverybeginningofaprojecttheyhaveamuch greater impact on discounted value indicators. In addition, cost overruns have adisproportionateimpactonhostgovernmentsduetotheinterplayofgovernmenttakefactorsandthemorerestrictedoptionsfor financingtypicallyavailabletogovernment. Also,severalstudies indicate that most companies tend to greatly underestimate the capital costs onmegaprojects.Thesefactorstakentogethermeanthattestingcapitalcostsensitivityanalyses,especiallytestingforlargeoverruns,areespeciallyimportantforanyhostgovernmentornationaloil company (themodel allows this in the sensitivity analysis section of the ‘Assumptions &Results’sheet).Formoreinformationonwhysuchanalysisiscrucial,see:http://www.spe.org/ogf/print/archives/2012/02/02_12_08_Feat_Cost_Est.pdfhttp://www.costandvalue.org/download/?id=2047http://www.ogdeestimating.com/services/field-development/type-of-estimatehttp://www.ey.com/GL/en/Industries/Oil---Gas/EY-spotlight-on-oil-and-gas-megaprojects#.VhlIRexVikoFiscaltermsandtaxes–Asexplainedabove,thisinformationshouldbeavailablefrompublishedpetroleum and tax laws of the country, plus any agreements, such as Production Sharing

7See‘Assumptions&Results’sheet,lines24and258See‘FieldXInvestor’sheet,line129See‘LNGEquity’sheet,line1310See‘Assumptions&Results’sheet,lines10-11and26-28

19

Agreements,11betweenthegovernmentandtheupstreaminvestors.Oftentimes,thedetailsoftheLNGfiscaltermsarenotagreeduntilrightbeforetheFinalInvestmentDecisionismade.Unitsofmeasurement – Extremecaremustbe takenwhenenteringdata intoaneconomicsmodeltoensurethattheunitsofmeasureareknownandaremadeconsistentwithinthemodel,andthatconversionsareperformedwherenecessary.Thefollowingindustryconventionshouldbetakenintoaccount:

1. Naturalgasproduction,gasreservesandpipelinecapacityaretypicallymeasuredinunitsofvolume,suchasThousandsofStandardCubicFeet (MCF)orThousandsofCubic Meters (MCM). When referring to gas reserves it is common to use ameasurementofTrillionofCubicFeet(TCF).

2. LNG Plant capacity and LNG Tanker capacity are commonly measured in units ofweight,typicallyinMetricTons(MT)sincetheyareproducingortransportinggasinaliquidform.

3. Condensate(liquidspresentinwetgasfields)iscommonlymeasuredinBarrels,whileLPGmaybemeasuredinBarrelsorMetricTons.

4. InmanycasescapacityismeasuredasanamountPERDAYwhileinothersituationsvolumesarereferredtoasanamountPERANNUM.

5. Insomecaseswherethereisahighliquidscontentinthenaturalgasstreamthegasmay be measured or referenced in units relating to its energy content, typicallyThousandsofBritishThermalUnits(MBTU)orinsomecasesasGigajoules.

6. MostnaturalgasandLNGsalespricesarequotedandpaidinU.S.Dollars.Acommonlyreferenced unit in price quotes for natural gas is Dollars per MCF and may beconvertedtoapriceperMTforLNG.

7. MosttariffsortollsarereferencedinU.S.dollars.PipelinetariffsareusuallyapriceperMCF.LNGTollingtariffsmaybeapriceperMCForinmanycasesapriceperMT.

8. Also, attentionmust be paid to the “thousands” conventions. In the petroleumindustry, “M” typically is used to refer to one-thousand and “MM” refers to one-million(orathousandthousands).Theeconomicsmodelitselfusuallyreferstoinputandoutputamountsexpressedinmillions,orMM.

Thebelowtablescanhelpuserswithconversionswherenecessary: 11Seeresourcecontracts.orgforadatabaseofpubliclyavailablecontracts.

20

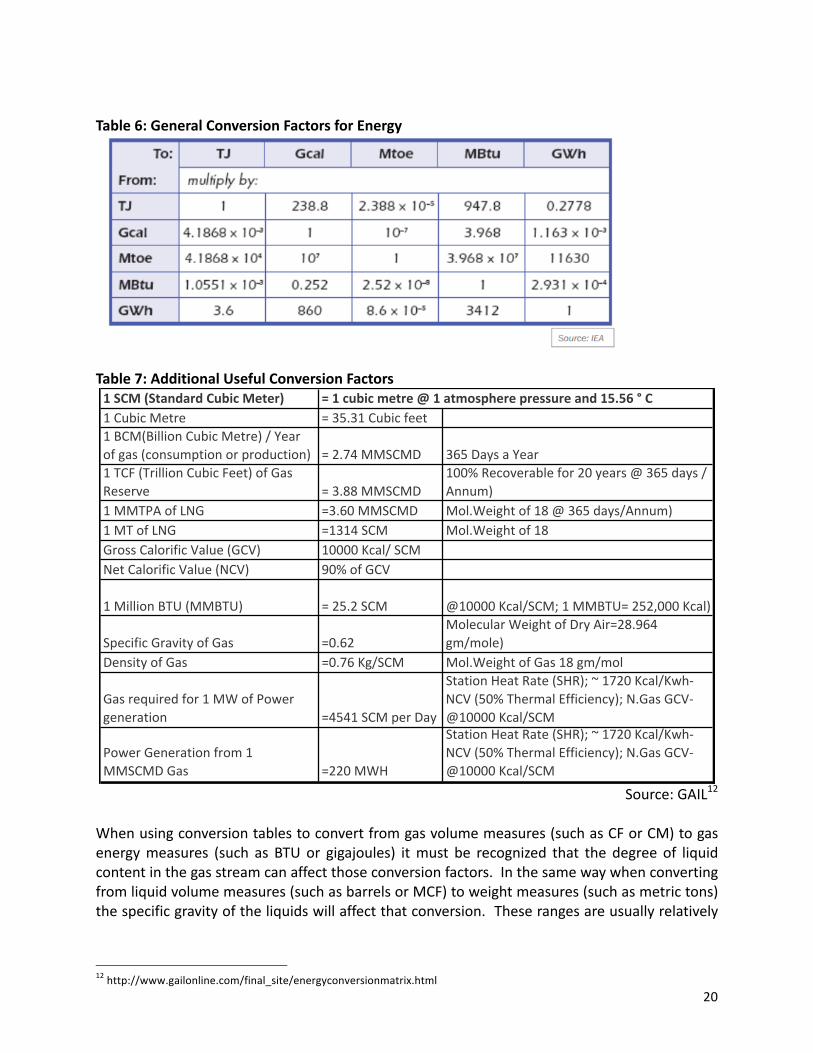

Table6:GeneralConversionFactorsforEnergy

Table7:AdditionalUsefulConversionFactors

Source:GAIL12

Whenusingconversiontablestoconvertfromgasvolumemeasures(suchasCForCM)togasenergymeasures (such as BTUor gigajoules) itmust be recognized that the degree of liquidcontentinthegasstreamcanaffectthoseconversionfactors.Inthesamewaywhenconvertingfromliquidvolumemeasures(suchasbarrelsorMCF)toweightmeasures(suchasmetrictons)thespecificgravityoftheliquidswillaffectthatconversion.Theserangesareusuallyrelatively

12http://www.gailonline.com/final_site/energyconversionmatrix.html

1SCM(StandardCubicMeter)1CubicMetre =35.31Cubicfeet1BCM(BillionCubicMetre)/Yearofgas(consumptionorproduction) =2.74MMSCMD 365DaysaYear1TCF(TrillionCubicFeet)ofGasReserve =3.88MMSCMD

100%Recoverablefor20years@365days/Annum)

1MMTPAofLNG =3.60MMSCMD Mol.Weightof18@365days/Annum)1MTofLNG =1314SCM Mol.Weightof18GrossCalorificValue(GCV) 10000Kcal/SCMNetCalorificValue(NCV) 90%ofGCV

1MillionBTU(MMBTU) =25.2SCM @10000Kcal/SCM;1MMBTU=252,000Kcal)

SpecificGravityofGas =0.62MolecularWeightofDryAir=28.964gm/mole)

DensityofGas =0.76Kg/SCM Mol.WeightofGas18gm/mol

Gasrequiredfor1MWofPowergeneration =4541SCMperDay

StationHeatRate(SHR);~1720Kcal/Kwh-NCV(50%ThermalEfficiency);N.GasGCV-@10000Kcal/SCM

PowerGenerationfrom1MMSCMDGas =220MWH

StationHeatRate(SHR);~1720Kcal/Kwh-NCV(50%ThermalEfficiency);N.GasGCV-@10000Kcal/SCM

21

small,butcancreatedifferencesfromtheconversionsusedbyacompanyorgovernmentintheirmodels

5. MozambiqueexampleFor illustrative purposes, the input values in the model are based on publicly availableinformation on the Rovuma basin LNG project in Northern Mozambique. However noquantitative conclusions can be drawn from this analysis given that the data is still verypreliminaryand therewereanumberofdatagaps.Furthermore, someof thenumbershavebeenadaptedtobettershowtheimpactofthedifferentprojectstructures.ThesecondupstreamfieldhasbeenincludedtoillustratetheimpactofadditionalvolumesontheLNGeconomicsandhasthesamecharacteristicsasthefirstupstreamfield.

a. AssumptionsandreferencesFiscalTerms

• UpstreamFiscalTermsarebasedonBlock1PSAfrom2006,withsomeexception.BonusamountsindicatedinthePSAandwithholdingtaxarenotincluded.

• A$1Billionunrecoveredexplorationcostisincluded(outof$2Billiontotalunrecoveredexplorationcosts),basedontheStandardBankreport.13Itwasassumedthatsomeofthatamountisnotrecoverableastheywouldbeoutsidetheringfence.

• Forthegaspipelinesegmentthestandardcorporateincometaxof32%withnotaxreliefor investment uplift (such as was provided for the Pande Temare project) is used(PetroleumLawNo27/2014).

• For the LNG segment the standard corporate income taxof 32%withno tax relieforinvestmentupliftisused(PetroleumLawNo27/2014).

TechnicalandCommercialInputs• TheLNGproductionvolumesareestimatedbasedonfourLNGtrainsat6milliontonnes

perannumeach.ThisisequivalenttoatotalLNGplantoutputofapproximately1,062millioncubicfeetperday(MMCFD). Theupstreamproduction isassumedtobe1650MMCFDperfieldbeforetakingaccountforLNGproductionlossesofLNGplantdowntime.

• ItisassumedthattwoupstreamprojectsaresupplyingtheLNGplant.Figuresforbothfieldsarethesame.

• The pipeline construction has been scheduled to conclude one year before start ofoperations to allow for line testing, inspections and potential modification prioroperation.

• Basedonthereviewedmaterial,themodelusesthetollingstructureasthebasecase.• Thecapitalcostandtimingofexpenditurefiguresarebasedoneducatedguessesand

adapted toprovide reasonable return rates for thedifferent segmentsof theproject.Excludingthefinancingcostandcapitalizedinterest,thesefiguresarerelativelyclosetotheStandardBankreportestimates.

• NoLPGorCondensateproductionisassumed.Theremaybesomecondensateproducedbytheupstreamprojects,whichwouldincreasetheprofitability.

13 Standard Bank (2014) Mozambique LNG: Macroeconomic Study

22

• 2% domestic gas sales are assumed. This would have to be adjusted when theGovernment’srequirementfordomesticsalebecomesclearer.

• DuetodatagapsregardingtheLNGtollingratesandoperatingcosts,thesefiguresarebasedoneducatedguesses.Thetollingratewillinvolveacommercialnegotiation.

• UndertheLNGtollingarrangementitisassumedthatthegaspricetobeusedunderthePSA termsare tobe interpretedas theFOBExportprice less the LNG toll itself. Thisimpactsthecostrecoverycap.Itmaybearguedthata"Wellhead"typeofpriceforgasisreallyNETofthetollthatwouldneedtobeincurredpriortobeabletosellthegas(eventhoughthewellheadconceptisnotusedinthePSAperse).AcommercialreasonisthatcompaniesmaynotbewillingtoagreetoaninterpretationofthePSAwherebypayingatolltoathirdpartytoprocess/liquefythegaswouldputtheminaworsesituationthanselling thegasdirectly toaplantownerat the samenetbackprice strictlydue to themechanicsofhowtheCostRecoverycapfunctions.

Themaindocumentsreviewedforthepurposeofthismodelinclude:• 2006PSABlock114• Mozambique’sPetroleumLawNo27/2014• ICFInternational(2012)NaturalGasMasterPlanforMozambique:DraftReportExecutive

Summary• StandardBank(2014)MozambiqueLNG:MacroeconomicStudy• TheOxfordInstituteforEnergyStudies(2014)Mozambique’sLNGRevolution:Apolitical

riskoutlookfortheRovumaLNGventures

b. Asking the right questions regarding the assumptions and Interpreting theresults

FiscalTermsThe Fiscal Terms are based on an existing PSA and existing tax laws inMozambique, but doincludeanassumed“agreedinterpretation”regardingthenetbackoftolling. Somequestionsthatmightbeaskedare:

• Willthesetermscontinuefor30+yearsevenifcostsandmarketsandproductionvary?• Arethereanyother“interpretations”thatendupbeingagreed(ornotagreed)withthe

governmentthatwerenotmodeledthatmightcreateadifferentresult?

CommercialAssumptions• IsaconstantFOBexportpriceof$8.50perMCFrealistic intoday’smarket,orwhat is

anticipatedforthe lifeof theproject? Ifpriceassumptionsarechanged,what impactmightthathaveoncosts,tariffsorotherinputassumptions?

• Isanassumeddomesticgaspriceof$2.50consistentwithothertermsandassumptions?• DoesaLNGtollof$4.00reasonableandcommerciallyviabletoallparties?Willitchange

overtimeifworldmarketschangeornewprojectscomeintotheplantasfeedstock?• DoesthisLNGtolloptionyieldsignificantlydifferentresultsthanutilizinganLNGequity

option?Ifso,whatcausedthedifferenceanddoesthatcauseanyconcern?

14http://www.resourcecontracts.org/contract/ocds-591adf-MZ0646925511RC/view

23

TechnicalAssumptionsTheeconomicsassumerecoverablereservesof34TCF.

• Are there sufficient reserves already discovered in this area to provide this level ofproductiontoconstantlyfeedintotheLNGplanonanuninterruptablebasis,thatis,morethan34TCFinreservesinordertocoverunexpectedshut-insorsomefieldsperformingatlessthanexpectations?Aretheinvestorsandthegovernmentrelyingtoomuchonthehopethatadditionalreserveswillbediscoveredinthefuture?

• Arereservessohighthatitindicatesthatitmightbelessthanefficienttobuildonlya4-TrainLNGplant?

Totalcapitalcostsforallprojectsectorswere$28billion,including$16.8billionfortheLNGplant.• Areestimatedcapitalcoststoolow?SomesingletrainLNGplantshavecostsmorethan

what was assumed for this 4-Train plant. A high proportion of energy sector“megaprojects”overruntheiroriginalbudgetsbyasizablepercentage.

• Arecoststoohighandconsequentlyunderstatetherealreturnstoinvestors?• Arethereanybenchmarkstocomparecosts?• Havetheappropriaterangeofsensitivityanalysesbeenrunandevaluated?

NoCondensateorLPGhasbeenincluded.• If indeedtherewouldbesomecondensateorLPGextractedfromthegasstreamboth

thecapitalcostsandtheresultantnetrevenueswouldbehigherandprojecteconomicresults would likely improve.15 What would these look like and what fiscal terms(upstreamorLNG)wouldbeapplied?

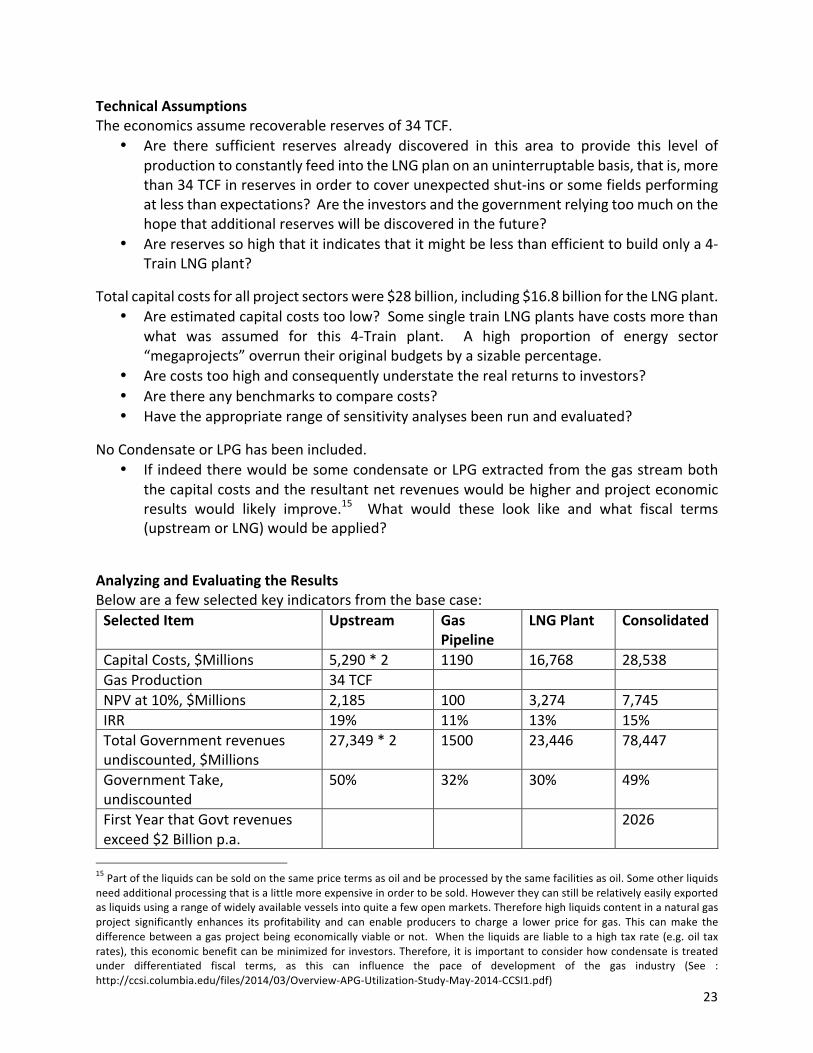

AnalyzingandEvaluatingtheResultsBelowareafewselectedkeyindicatorsfromthebasecase:SelectedItem Upstream Gas

PipelineLNGPlant Consolidated

CapitalCosts,$Millions 5,290*2 1190 16,768 28,538GasProduction 34TCF NPVat10%,$Millions 2,185 100 3,274 7,745IRR 19% 11% 13% 15%TotalGovernmentrevenuesundiscounted,$Millions

27,349*2 1500 23,446 78,447

GovernmentTake,undiscounted

50% 32% 30% 49%

FirstYearthatGovtrevenuesexceed$2Billionp.a.

2026

15Partoftheliquidscanbesoldonthesamepricetermsasoilandbeprocessedbythesamefacilitiesasoil.Someotherliquidsneedadditionalprocessingthatisalittlemoreexpensiveinordertobesold.Howevertheycanstillberelativelyeasilyexportedasliquidsusingarangeofwidelyavailablevesselsintoquiteafewopenmarkets.Thereforehighliquidscontentinanaturalgasproject significantly enhances its profitability and can enable producers to charge a lower price for gas. This canmake thedifferencebetweenagasprojectbeingeconomicallyviableornot. Whentheliquidsare liabletoahightaxrate(e.g.oiltaxrates),thiseconomicbenefitcanbeminimizedforinvestors.Therefore,itisimportanttoconsiderhowcondensateistreatedunder differentiated fiscal terms, as this can influence the pace of development of the gas industry (See :http://ccsi.columbia.edu/files/2014/03/Overview-APG-Utilization-Study-May-2014-CCSI1.pdf)

24

FirstYearthatInvestorNetCashFlowsexceed$2Billionp.a.

2021

Somequestionsthatmightarisefromtheseresults:

• AretherelativeIRRsforeachprojectsector(e.g.upstream15%,gaspipeline11%,LNGplant15%)reasonablecomparedtotheirrisksandtoothersimilarinvestmentsaroundtheworldortheregion?

• DotheNPVsat10%seemreasonableforeachprojectsectorrelativetothesizeoftheinvestmentandtherisk?Arethesesufficienttoattracttheinvestmentbutatthesametimenotyieldingtoomuchoftherent?

• Howdo these IRRsorNPVschangeusingdifferentassumptions?Check thesensitivityanalysistoseewhethertheseindicatorscollapseduetochangesintheassumptions.

• Thetimingofcash flows iscritical indeterminingNPVand IRR.Check the impactofaproductiondelayoffield1inthesensitivityanalysis.

• Timingofcash flows isalso important to thegovernment in termsof thegovernmenttreasury’soverallbudgetingfor inflowsandspendingormanagingofsovereignwealthfunds.Itcanalsobeinstructiveinevaluatingthedistributionbetweenthegovernmentandtheinvestors.LookingatthebasecasethefirstyearofsignificantNETcashflowstoinvestorsis2021whentheyearnover$2billionnet,whereasthegovernmentdoesnotreach$2billionayearuntil2026.TherealityisthattheGovernmentdoesnotreceivemuchoftheirinflowsuntilthelasthalfoftheprojectlife,whereastheinvestorsreachtheirnetinflowsrightafterproductionstart.

• Overall percentage split of government take is another important indicator. In theupstreamsectorthegovernmenttakeis50%ofthetotalnetcashflows,butisonly31-32%forthegaspipelineandLNGsector.Thisisareflectionofthefiscalandtaxtermswhicharetypicallymuchhigherintheupstream.Butwhenthesearecomparedtoothersimilar projects with similar risks in other countries to evaluate, do they look to becompetitiveandconsistent?

25

6. Whatthemodeldoesnotinclude1.Technical InputData -Themodeldoesnotcreate forecastsofproduction,costsorprices.Thesemustbeobtainedfromareliablesourcesuchasoneofthecompaniesthatareinvestingin the projects, the government or an assessment from an independent party such as anengineeringfirm,aconsultant,abank,oraninternationalorganizationsuchastheWorldBank.If completely reliable engineering detailed level data is not available, it becomes evenmoreimportanttotesttheeconomicresultsbyrunningscenarioswithwidevariationintheinputdata.

2.Explorationcosts–Thismodelfocusesonthedecisionstobemadeafteradiscoveryhasbeenmade,soexplorationcostsarenotincluded(onlysomeofitasrecoverablecostsunderthePSAareincluded).However,fiscaltreatmentofexplorationcostscouldbecomeafactorifpast“sunk”explorationcostsarepermittedtobreakthe“ringfence”tobeusedincostrecovery.Atsomepointthismaybecomeanegotiatingpointinprojectsgoingforwardandhaveanimpactontheeconomics.3.FullDecommissioningCostsFunctionality–Decommissioningcostshavebeenincludedasanupstreaminputitem.However,thiscanbecomplexforacoupleofreasons.Oneisthatthesecostsareoftenrequiredtobepre-fundedbytheupstreampartnersaccordinglytoacomplexandsometimesarbitraryformula,andtherelatedcostrecoveryortaxdeductibilitytreatmentcanvarysignificantly.Ifthecoststakeplaceattheendofthefieldlifethenlosscarrybackprovisionsmust be considered, which creates an added complexity. And decommissioning is notstraightforwardforfieldsthatarefeedingintoanLNGplant.Oftentimesanindividualfieldmaystopproducing,yetitsinfrastructuremayendupbeingusedorleasedformanyyearsbyothersupplierstotheLNGplantasprocessing,compressionstations,transportation,treatingorevengasstorage.Thismeanstheultimatedecommissioningfromanyonefieldmaybedelayedbyyears.Consequently,themodelonlyincludesprovisionforaverysimplepayasyougocashbasisfundingandnolosscarrybackprovisionsfortaxorproductionsharing.4.Differentiation of investor equity shares - Themodel does not differentiate between therespectiveinvestorequitysharesinthevarioussegments.Theyaretreatedasonegroupforeachsegment.However,inmanycasesthegovernmentmayhavetheoptiontotakeanequityshareinanyorallofthesegments.Inthatcase,attentionmustbepaidtovariousfactorsandimpacts,suchas:

• Theamountofcapitalcoststhatwouldhavetobefinancedbythegovernmentfromitsownsourcesorfromlenders.

• Thereturnsthatcanbeexpectedbythegovernment(anditslenders)fromitsequityinvestment.

• Howmuchproductionoroutputwillbeavailabletothegovernmenttomarketorutilizeforincountryneeds.

• HowtheseresultsareimpactedbypossiblechangesintheLNGmarket,transferprices,tolls,projectstructure,recoverablereservesorcostoverruns.

26

5.CarryoftheState'sinterestduringexplorationordevelopment-ThisisacommonoptioninPSA'sespeciallyasameansoftheforeigninvestors“lending”tothestateoilcompany;buttherearemanyvariationsonhowtherepaymentsworkandarequitecomplextomodel.AndinmanycasesthecarryandrepaymenttermsendupvaryingfromthebasicPSArequirementsonceaprojectinvolvesLNGandthecarrybecomespartofamuchlargergovernmentsharefinancingdiscussionandnegotiation. Inmostrespectscarryingor financingthestatesharebecomesaseparatefinancingnegotiationanddecisionratherthananintegralpartofthebasicgasvaluechain economics. But a carryoftenentails high costs to the government since a carryoftenrequirestheoilcompaniestakingoncertainadditionalrisks.ThetermsofthesecarriesmustbecarefullyanalyzedandmodelledtodeterminetheirimpactontheGovernmentunderavarietyofassumptionsandcostconditions.6.Financing-Borrowingandfinancingcaninsomecaseshaveanimpactifinterestondebtispermitted as a tax deduction. But a common analytical mistake is to focus on leveragedeconomics,soitisrecommendedthatfinancingeffectsnotbeconsideredinamodelinordertoavoidconfusingtheimpactsandcompromisingtheanalyticalvalidityofthemodel.Financingisofcourseahugefactorinmega-projectssuchasLNG,especiallythegovernmentshareorforthesmallerindependentcompanies;butitmustbeclearlysegregatedasaseparatetypeofanalysis.Ifinterestcostsonloansfromaffiliatedpartiesarepermittedastaxdeductions,greatcaremustbetakentoensuretheyarenotexcessive.(http://www.afr.com/business/energy/gas/chevron-claimed-gorgon-bonanza-would-pay-for-tax-for-cuts-for-everyone-20151116-gl0jo1)7.WithholdingTaxonDividends–Noprovisionhasbeenmadeinthemodelsincewithholdingtaxinmanycasesisreallyjustaminortimingdifferenceonpaymentofcorporatetaxes.Inothercaseswithtaxtreatiesthecompaniesgetafullrelieforcreditforwithholdingtaxes.IntheeventthattheWHTinanyplacedoesnothavethesetypesof“relief”featuresanditbecomesarealfinal tax, themodel can cover this through utilizing the other tax components (surcharge orspecialtax)thathavebeensetupinthemodel.8.NonQuantifiableFinancialResults–Economicsmodelstypicallyfocusonlyonquantifiablefinancial results of a project. Most agreement and regulatory provisions do have financialimpactsandthesecanbereflected.However,manyotherprojectagreementsandpetroleumregulationshaveconsequencesthatcannotbeeasilymodeled.Someofthoseinclude:

• Controlofprojectdecisions, suchas:approvingprojectsgoingahead,moving into thedevelopmentphase,relinquishment,salesofinterest,contractingandprocurement.

• Localcontentandlocalemploymentrequirementsandpolicies• Environmentalregulationsandstandards,• Communityengagementandconsultation• Controlandcomplianceofoilfieldservicescontractorsandtheirimpact• TheSaleandPurchaseAgreement itselfmayprotect theupstreamand theLNGplant

investors froma varietyofmarket andoperationsdisruptions through send-or-payortake-or-payclause.