managing your resources chapter 8 “you are good when you strive to give of yourself. yet you are...

TRANSCRIPT

Managing Your Resources

Chapter 8

“You are good when you strive to give of yourself.

Yet you are not evil when you seek gain for yourself. ”

Kahlil Gibran, Author

© 2010 McGraw-Hill Higher Education. All rights reserved.McGraw-Hill

8-2

Learning Objectives• Outline the three steps in time management and in

money management.

• Describe the three categories of time and the three categories of expenses.

• Explain how to make a to-do list and a schedule.

• Define procrastination and explain its causes.

• Describe the criteria for an effective budget.

• Cite ways to reduce excess spending.

8-3

Taking Control Of Your Time• Time Management The planned, efficient use of time.

• Step 1 Analyze How You Use Your Time

Assign your activities to three different time categories:

Committed Time –work, family, volunteering, and other activities that relate to your long and short term goals.

Maintenance Time –the time you spend taking care of yourself and your surroundings.

Discretionary Time –the time you can use to do whatever you wish.

Activity 40: Time-Demand Survey

8-4

Time Control continued…

• Step 2 Prioritize Your Activities Look at your work, school, family and social obligations. Which ones are most relevant to your goals and values? Generally, discretionary time can be cut first, but don’t eliminate all fun and relaxation to get more done. And, don’t forget sleep!

Personal Journal 8.1 Prioritizing Your Life

Success Secret• Make time for activities that relate to your goals.

8-5

Time Control continued…• Getting More from Your Time Spend 80% of your time

and energy on your top priorities.

• Activities that should be LOW priority for everyone include:

• time spent with people who don’t make you feel good about yourself,

• distractions like video games and watching constant television,

• tasks you don’t enjoy or do very well, that you could eliminate or even hire someone else to do,

• tasks that save a little money, but consume lots of time, such as clipping coupons for food you don’t buy.

Activity 41 Examining Your Priorities

8-6

Time Control continued…

• Step 3 Create a Plan for Your Time

Make a To-Do List –in priority order, then stick to it!

Make a Schedule –a chart showing dates and times when tasks must be completed.

Activity 42: Time Management Practice

Identify Your Prime Time –plan your most important tasks for your high-energy time of the day.

Personal Journal 8.2 What’s Your Prime Time?

8-7

Tackling Procrastination

• Procrastination The habit of putting off tasks until the last minute.

• Why We Procrastinate…Everyone procrastinates sometimes. But many people use procrastination to avoid taking charge of their lives.

Activity 43: Do You Procrastinate?

Success Secret• Get Started! Divide your project into segments, then

tackle just one.

8-8

Money Matters• Money Management The intelligent use of money

to achieve your goals.

• Early Lessons About Money Our attitudes about money are strongly influenced by the example our parents set for us.

• Money is a Tool The most useful attitude toward money is a practical one: money is a tool to take care of our basic needs and achieve important goals.

• Your Money and You

Personal Journal 8.3 How Do You See Money?

8-9

Managing Your Finances

• Finances Your monetary resources.

• Step 1: Analyze How You Use Your MoneyAssign your expenses to three different categories:

• Fixed committed expenses –necessary, fixed, monthly expenses such as rent, car payment, etc.

• Variable committed expenses –necessary expenses that vary monthly such as food, laundry, tuition and books, auto repairs, gifts, etc.

• Discretionary Expenses –lifestyle expenses that are fun, but not strictly necessary including entertainment, meals out, cable TV, etc.

Activity 44: Expense Log

8-10

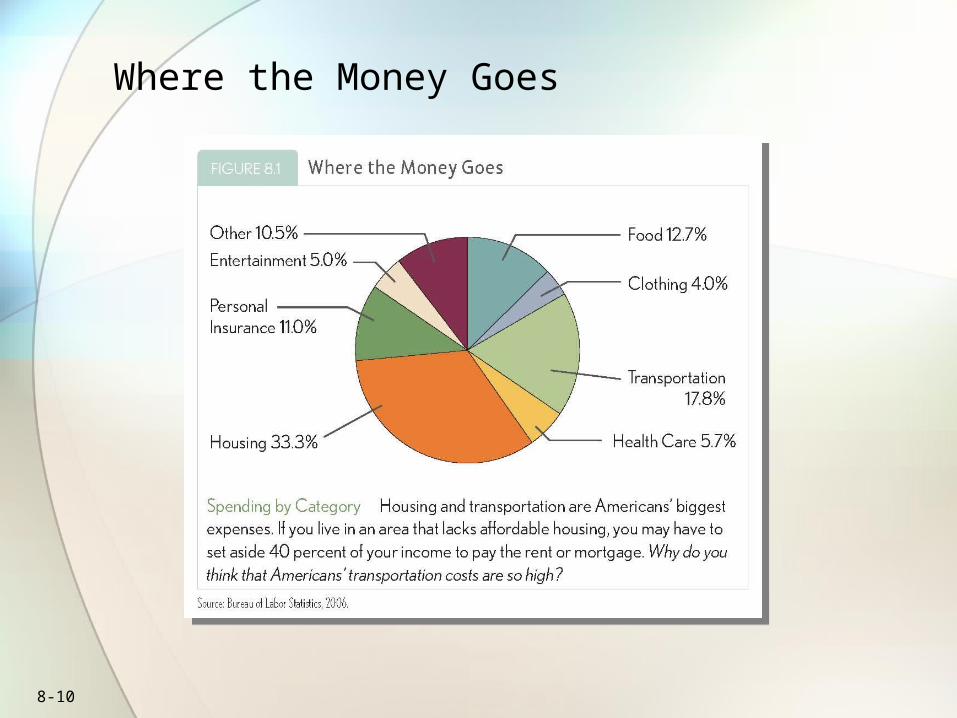

Where the Money Goes

8-11

Managing Your Finances continued…

• Step 2: Prioritize Your Expenses

Use your values and goals to determine how you will use your money. Don’t forget a savings category of 10% of your annual income.

Success Secrets• The recipe for financial success is “spend less than you

earn.”• Look at money as a tool to achieve your goals, not as a

goal in itself.

8-12

Managing Your Finances continued…

• Step 3: Create a Plan for Your Money

Income All the money you receive during a fixed time period.

Budget A money-management plan that specifies how you will spend your money during a particular period. An effective budget meets these criteria:• It is realistic, taking into account all of your expenses.• It is balanced, with expenses equal to or less than your income.• It centers around your goals and values and includes savings.• It can be modified if necessary.

Activity 45: Budget Worksheet

8-13

Stretching Your Resources

• Impulse Buying Spending money on the spur of the moment, without planning.

• Drop the Shopping Habit Ask Yourself:• Do I really need this item?• What other bills do I have to pay?• Have I allowed for this item in my budget?• Do I own something similar already?• Is there something less expensive that is as good? • Is this the best time to buy?

Personal Journal 8.4 Look Before You Leap

8-14

Using Credit Wisely

• Credit (loan) Money you can use before having to pay back the lender.

• The Perils of Credit If you don’t pay off your credit car bill monthly, you incur finance charges which add up quickly. Ask yourself whether you overuse credit:

• to pay overdue bills, especially other credit cards• to buy an item that costs $5.00 or less• to pay for a vacation• to pay for a large purchase you hadn’t saved for

8-15

Using Credit Wisely

• Your Credit Record A log of the financial habits of a person who buys on credit that employers, landlords and banks can access at any time.

• Having a good credit record is essential for renting an apartment or buying a house, car, etc.

• To establish good credit, pay all bills promptly, avoid

large debts, and do not bounce checks.

Success Secret• Resist the temptation to overspend.