managing our carbon emissions - guildford … our carbon emissions.pdf · usina santa elisa mill in...

TRANSCRIPT

Managing our Carbon Emissions

Dr Bill Kyte OBE

Talk given to GEF 26 April 2017

or

How can we be made to do so?

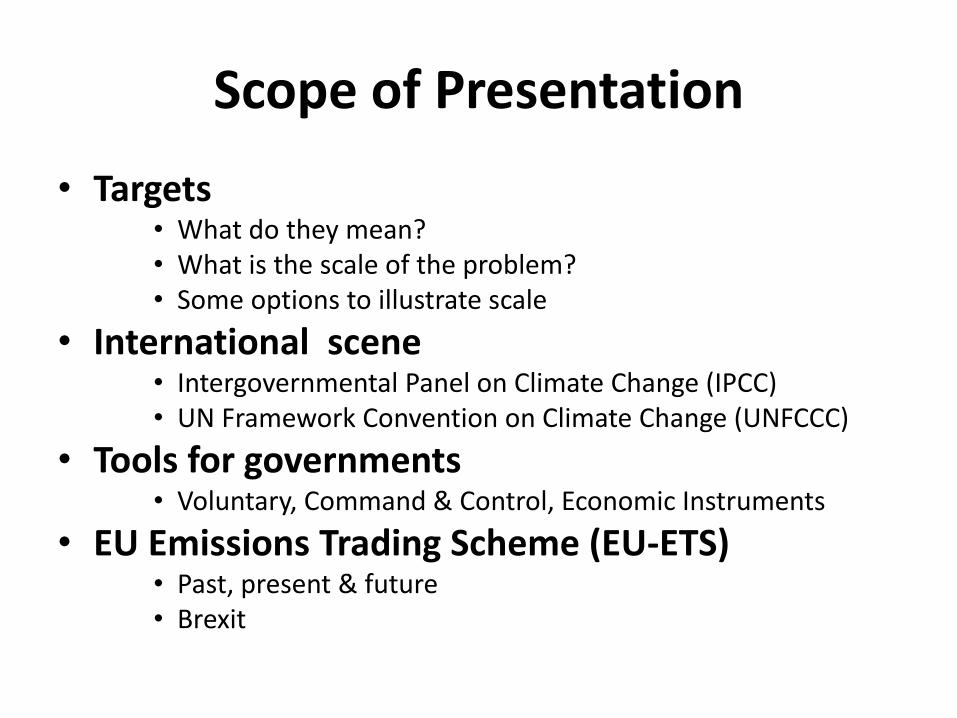

Scope of Presentation

• Targets • What do they mean? • What is the scale of the problem? • Some options to illustrate scale

• International scene • Intergovernmental Panel on Climate Change (IPCC) • UN Framework Convention on Climate Change (UNFCCC)

• Tools for governments • Voluntary, Command & Control, Economic Instruments

• EU Emissions Trading Scheme (EU-ETS) • Past, present & future • Brexit

Assumptions

• For this talk I will assume that:

• Enhanced Global Warming (Climate change) is real

• Climate change is caused by mankind’s actions

• There is a need to restrict temp rise to 2o C (1.5oC)

• There is a need for local, national, regional & global action

• The Paris agreement will hold

Targets

What should be targeted?

• Emissions of greenhouse gases (GHG)

• Concentration of GHGs in atmosphere

• Temperature rise

It is not simple

What is the Target

• 2o C has been identified as a ‘threshold’ above which there is a significant increase in ‘dangerous’ impacts and therefore has been adopted as a political target.

• Many would argue that 1.5o C is more appropriate.

CO2 emissions stock and average temperature

What does 2oC imply?

• International • 1,000 Gt C total carbon budget

• Emissions peak by 2020

• Only 50% of 1990 global emissions by 2050

• EU • 40% by 2030 of 1990 emissions – legally binding

• 80-95% by 2050 - aspiration

• UK • 57% by 2030 of 1990 emissions – legally binding

• 80% by 2050 - legally binding

GHG Emissions by Sector

Emissions Sector Percentage

Transportation 14

Electricity & Heat 25

Industry 14

Fossil fuel production 14

Land use change 18

Agriculture 14

Waste 4

What is the Scale of the Problem?

In 2004 two US academics came up with a concept of how to stabilise emissions through the use of ‘wedges’ as a strategy whereby each wedge would reduce carbon emissions rising from zero to 1 gigaton of carbon/year in 50 years time.

This would give a cumulative reduction of 25Gt over 50 years.

Options for change – enabling technologies

A further shift

to natural gas

Nuclear

power

Renewables Bio-products Carbon capture

and storage

Mass

transportation

Road

transport

Buildings Low energy

appliances

Doing things

differently

Energy conservation and efficiency

Emission reduction

Effort needed for

1 wedge:

• 1,400 new gas fired

power stations

• ~2 per month

Natural Gas for Power Generation

Current proven reserves of natural gas ~ 65

years

Increased shift to gas would reduce this

Challenge is to discover new reserves of

natural gas, and equally importantly, bring

this gas to markets

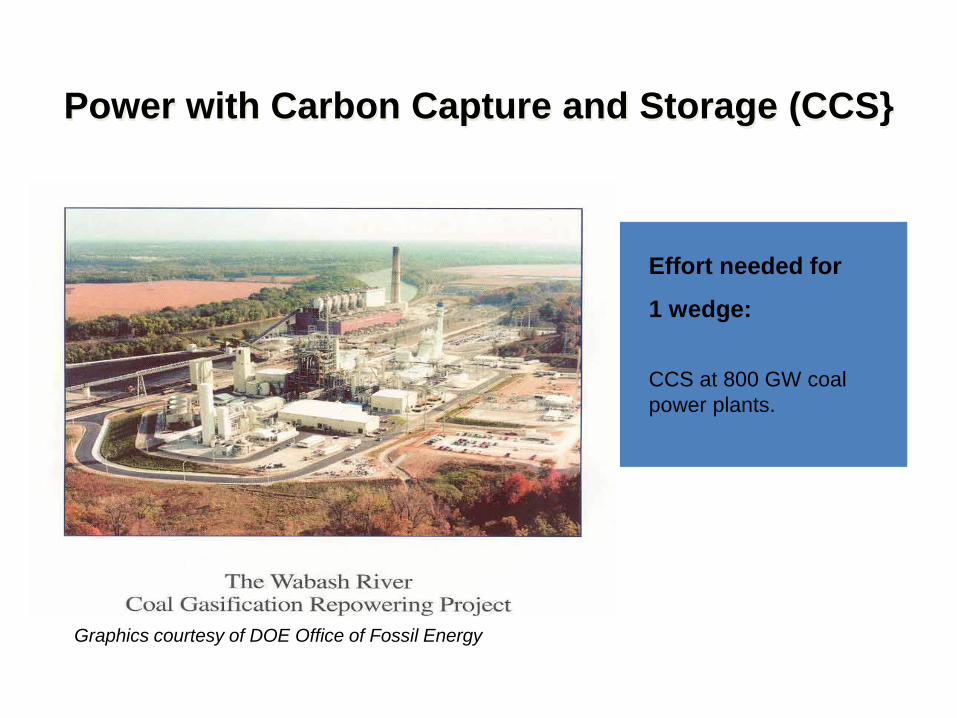

Power with Carbon Capture and Storage (CCS}

Graphics courtesy of DOE Office of Fossil Energy

Effort needed for

1 wedge:

CCS at 800 GW coal

power plants.

Carbon Storage

Effort needed by 2054 for 1 wedge:

3,500 Sleipners

A flow of CO2 into the Earth equal to the

flow of oil out of the Earth today

Graphic courtesy of Statoil ASA

Start now to gain experience with

the permitting of storage sites.

Effort needed by 2054 for 1 wedge:

Add 700 GW (twice current capacity):

fourteen 1-GW plants/year.

Nuclear Electricity

Graphic courtesy of NRC

Plutonium (Pu) produced by 2054, if fuel cycles

are unchanged: 4000 t Pu (and another 4000 t

Pu if current capacity is continued).

Compare with ~ 1000 t Pu in all current spent

fuel, ~ 100 t Pu in all U.S. weapons.

10 kg ~ Pu critical mass. Potential Pitfalls:

Nuclear proliferation and terrorism

Nuclear waste, NIMBY

Wind Electricity

Effort needed for

1 wedge:

400,000 5 MW windmills

Needs: 2,000 GW

Today: 433 GW

Land cover 30 million

hectares (size of

Germany)

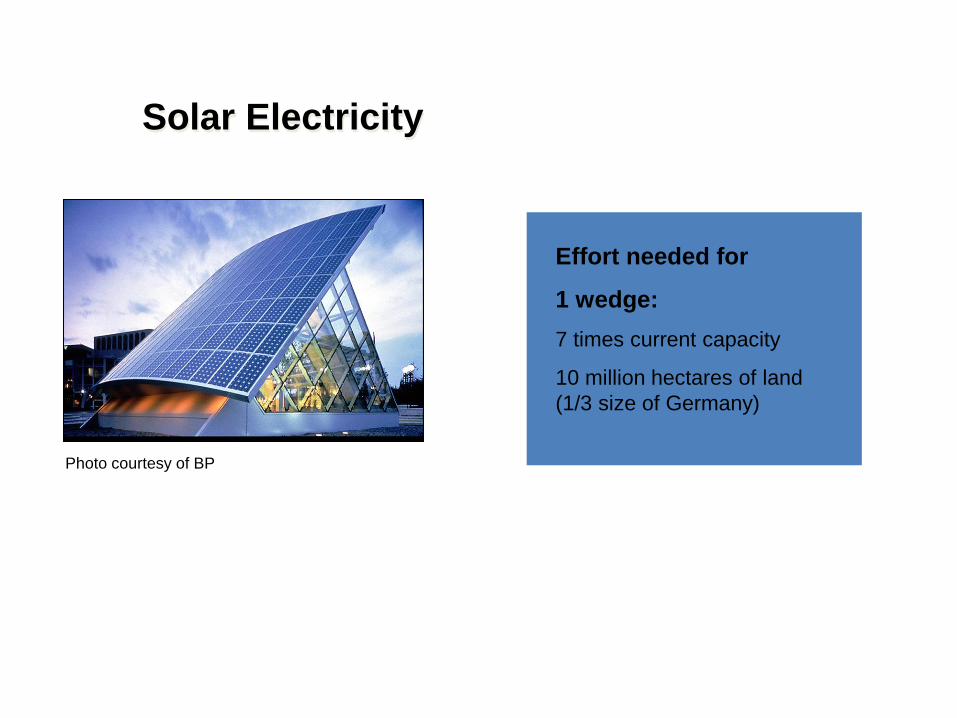

Solar Electricity

Effort needed for

1 wedge:

7 times current capacity

10 million hectares of land

(1/3 size of Germany)

Photo courtesy of BP

Biofuels

Effort needed

1 wedge:

Two billion 60 mpg cars

running on biofuels

250 million hectares of

high-yield crops (one

sixth of world cropland).

Usina Santa Elisa mill in Sertaozinho, Brazil

(http://www.nrel.gov/data/pix/searchpix.cgi?getrec=5691971&display_type=verbose&search_reverse=1_

Effort needed for

1 wedge:

Mass transportation replaces half of

projected road travel

Mass Transportation

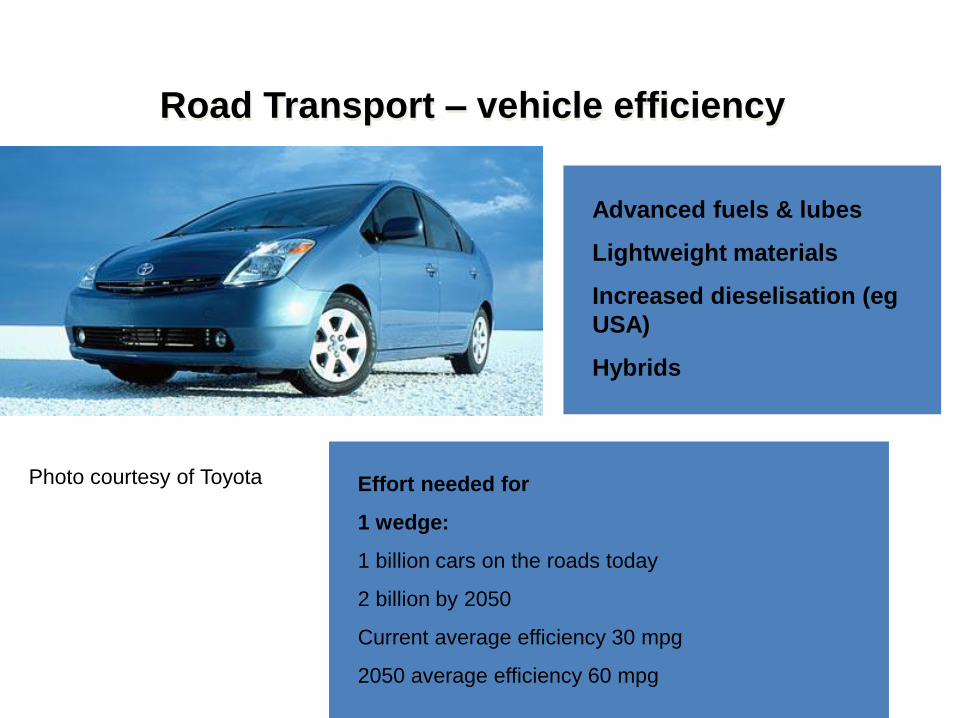

Road Transport – vehicle efficiency

Effort needed for

1 wedge:

1 billion cars on the roads today

2 billion by 2050

Current average efficiency 30 mpg

2050 average efficiency 60 mpg

Advanced fuels & lubes

Lightweight materials

Increased dieselisation (eg

USA)

Hybrids

Photo courtesy of Toyota

Buildings / Low Energy Appliances

Space heating/cooling

Water heating

Lighting

Appliances

Effort needed for

1 wedge:

Buildings emit 3.9 Gt/yr carbon = 20% of total

Cutting emissions by 25% from 2050 BAU =

1 Gt/yr C

More than half the potential in developing

regions

Example:

10 billion incandescent lamps today

50 billion by 2050

Full replacement with efficient bulbs would

reduce 0.5 Gt/yr C in 2054, assuming existing

carbon intensity of power generation

Doing things differently

Not a capping or reduction in

valuable activity.

Reducing unnecessary, and

unvalued waste: eg current standby

capacity in USA = xx large power

stations running at full capacity.

A shift in perception of “wealth” and

“value” – recent examples of low-

carbon wealth creation:

- cell phones

- IT / software / computer games

Urban Design

Telecommuting

Radical business models

Low-carbon wealth creation

2004 - Humanity Already has the Tools

• Emissions rise can be balanced by wedges reduction

• AVAILABILITY: Most wedge technologies are already deployed somewhere at commercial scale.

• PORTFOLIO: No single wedge technology can do the whole job, or even half the job.

• CHOICE: Not every wedge technology is needed.

* UPDATE Emissions are now 9.8 Gt C (2015)

*

More wedges

• Use renewables to generate hydrogen for: • Fuel cells for transport

• Injection into gas mains (10% possible without adaption)

• Halt deforestation coupled with reforestation • Reforestation about half the size of Australia

• Employ conservation tillage on all cropland • No ploughing

• Use sequestration from fossil fuel plants for: • Synfuels

• Hydrogen

2017 - Humanity Still has the Tools

• Emissions are rising much faster than wedge reductions

• AVAILABILITY: All wedge technologies are already deployed somewhere at commercial scale.

• PORTFOLIO: No single wedge technology can do the whole job, or even a substantial fraction of the job.

• CHOICE: Every wedge technology is needed.

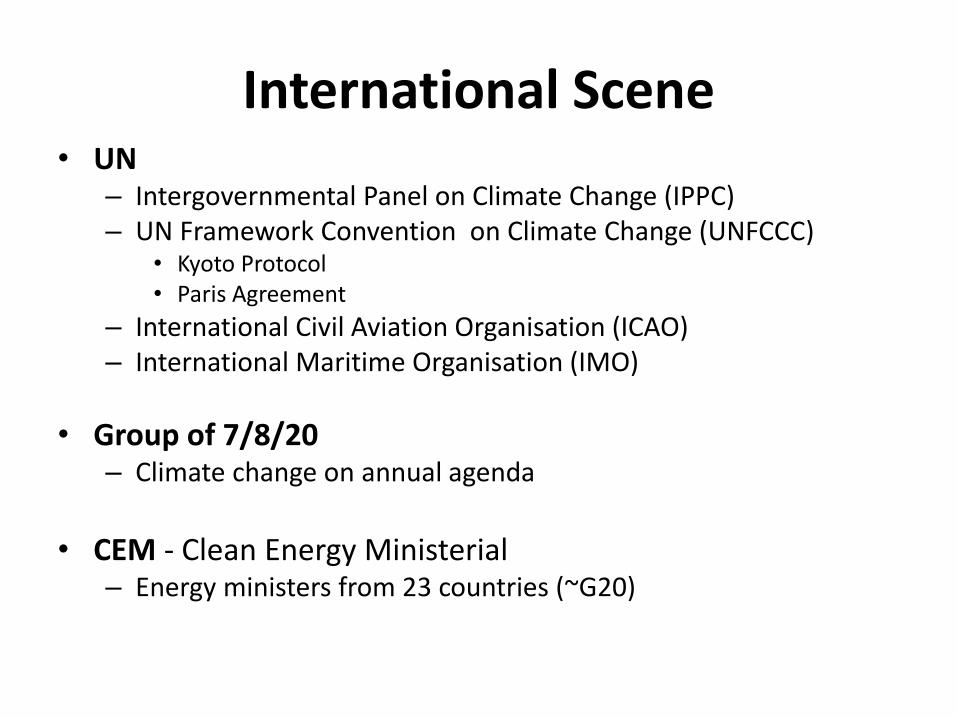

International Scene

International Scene • UN

– Intergovernmental Panel on Climate Change (IPPC) – UN Framework Convention on Climate Change (UNFCCC)

• Kyoto Protocol • Paris Agreement

– International Civil Aviation Organisation (ICAO) – International Maritime Organisation (IMO)

• Group of 7/8/20 – Climate change on annual agenda

• CEM - Clean Energy Ministerial

– Energy ministers from 23 countries (~G20)

International Panel on Climate Change (IPCC)

International Issues

• Equity

– Common but Differentiated Responsibilities

– Historical/Future Emissions

• Finance

• Market/Non-market instruments

• Mitigation/Adaptation

Different ways of ranking emissions % of global emissions

Emissions per capita

Carbon intensity per GDP

Cumulative 1850-2012

Estimated 2030 Gt CO2e

China 24.0 Qatar 51.7 Iraq 3.21 US 366 China 15.4

US 17.7 Kuwait 34.1 Uzbekistan 2.01 EU 329 India 7.2

EU 12.1 Net Antilles 32.3 Qatar 1.67 China 150 US 7.1

India 5.4 UAE 30.8 Mongolia 1.63 Russia 103 EU 4.3

Russia 5.2 Bahrain 29.7 N Korea 1.56 Germany 85 Russia 2.7

Japan 3.8 Trin/Tob 27.9 Net Antilles 1.53 UK 70 Japan 1.2

Germany 2.6 Aruba 23.1 Kazakhstan 1.49 Japan 51 Brazil 0.7

Canada 1.8 Luxemb’g 22.7 Trin/Tob 1.43 India 38 S Africa 0.5

UK 1.8 Brunei 19.4 Bahrain 1.32 UK 0.4

S Korea 1.6 Falkands 19.4 Jamaica 1.32

Mexico 1.5 US 19.1 Turkm’n 1.19

Australia 17.6 UAE 1.15

TOP 4 – 59%

TOP 6 – 68%

TOP 15 – 81%

Carbon Flows through trade

The lifetime of energy infrastructure

5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 ++

The rate of technological change is closely related to the lifetime of the relevant capital stock and equipment

Motor vehicles 12 – 20 years

Nuclear 30 – 60 years

Coal power 45+ years

Hydro 75+ years

Gas turbines 25+ years

Buildings 45+++ years

Source WBCSD

Early Meetings

• 1972 First Earth Summit, Stockholm – Main focus on air, land & water pollution

• 1979 Long Range Transboundary Air Pollution – Focus on SO2, NOX & Ozone, mention of climate

• 1988 IPCC formed by WMO & UNEP – Gather facts for Assessment Reports

• AR1(1990), 2(1995), 3(2001), 4(2007), 5(2014), 6(2021) • WG1(Science), WG2(Impacts), WG3(Mitigation), SPM

• 1990 World Climate Conference, Geneva • 1992 Rio Convention at Earth Summit

UN Framework Convention on Climate Change (UNFCCC)

• 1992 Rio Convention – UNFCCC

• 1997 Kyoto Protocol – binding national targets for Annex 1 countries of -5.2% by 2012 from 1990

– Kyoto 1 (2005-2012) – ratified 2004, in force 2005

– Kyoto 2 (2013-2020) – agreed in 2012, not yet ratified

• 2015 Paris Agreement – pledge & review – Intended National Determined Contributions (INDC)

Why is international agreement so slow?

• 197 Parties (countries) involved – 2,000+ negotiators from environment ministries

• All decisions by ‘consensus’

• Negotiating blocks with differing agendas – Mitigation/Adaptation/Sinks

• Limited negotiation time

• ‘Nothing is agreed until everything is agreed’

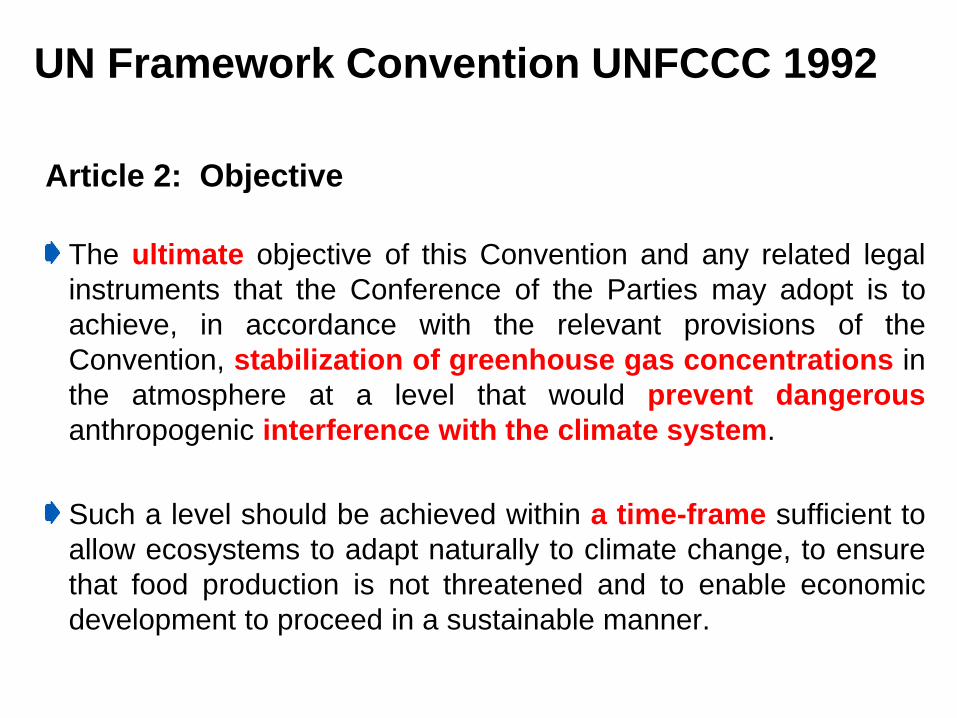

UN Framework Convention UNFCCC 1992

Article 2: Objective

The ultimate objective of this Convention and any related legal

instruments that the Conference of the Parties may adopt is to

achieve, in accordance with the relevant provisions of the

Convention, stabilization of greenhouse gas concentrations in

the atmosphere at a level that would prevent dangerous

anthropogenic interference with the climate system.

Such a level should be achieved within a time-frame sufficient to

allow ecosystems to adapt naturally to climate change, to ensure

that food production is not threatened and to enable economic

development to proceed in a sustainable manner.

The climate negotiationing cycle

International Climate Negotiations

1992 – 1st Earth Summit in RIO

• Adoption of Climate Convention (UNFCCC)

1995 - COP-1 in BERLIN

• The bifurcation point – CBDR

1996 - COP-2 in GENEVA

• The Ministerial Declaration calls for ‘legally binding quantified

emissions reduction targets’ for developed countries (and market

flexibility - US)

1997 - COP- 3 in KYOTO

• The first historic decision on internatonial regulation of

greenhouse gas emissions reduction – Annex 1 countries

only

International Climate Negotiations

2000 – COP-6 in The Hague

• Should have completed the implementation decisions but

failed because of non-agreement between EU and US -

reconvened as COP-6 bis (summer 2001)

2001- COP-7 in Marrakech

• Marrakech Accords for CDM & JI

2005 - COP-11 in Montreal

• Kyoto Protocol operational + Launch of International Dialogue

2007- COP- 13 in Bali

• The road to Copenhagen : the Bali Action Plan ( 2 years )

International Climate Negotiations

2009 – COP-15 in Copenhagen

• Copenhagen Accord noted but not adopted, but in fact a

breakthrough in the process – move from top-down to

bottom-up

2010 - COP-16 in Cancun

• Taking back of trust on board and first business dialogue

2011 - COP-17 in Durban

• Solidifying Cancun decisions on TEC/CTCN and GCF and launch of

the Durban Platform, as a single negotiating body

2015- COP- 21 in PARIS

• The Paris Agreement - the second historic decision on

internatonial regulation of greenhouse gas emissions

reduction (+ adaptation and resilience) – all countries

The heart of the Paris Agreement Parties to the Paris text agree :

To hold increase in global average temperature to “well below”

2°C and “pursue efforts” to limit increase to 1.5°C

National Commitmrnts to limit temperature increase. “The efforts

of all parties will represent a progression over time.” New NDCs

every five years

To aim to reach a global peaking of emissions “as soon as

possible.” Aim for balance between emissions and sinks post

2050

Developed countries to lead emission reduction efforts

Compliance committee reports on countries’ progress annually

Progress check : “global stocktake” every 5 years from 2023

Impact of INDCs on global emissions

30

35

40

45

50

55

60

65

70

75

80

2015 2020 2025 2030 2035 2040

GtCO2-e

Copenhagen Paris SubsequentCycles

Copenhagen

INDCs Paris

IPCC Window for 530-580 ppm CO2-e (1,000 Gt C)

INDCs - The landscape of regulation : references to carbon tax, ETS and International market mechanisms

Planned / possible use of int'al market mechanisms

No specific references or no INDC yet

Domestic ETS and carbon taxes

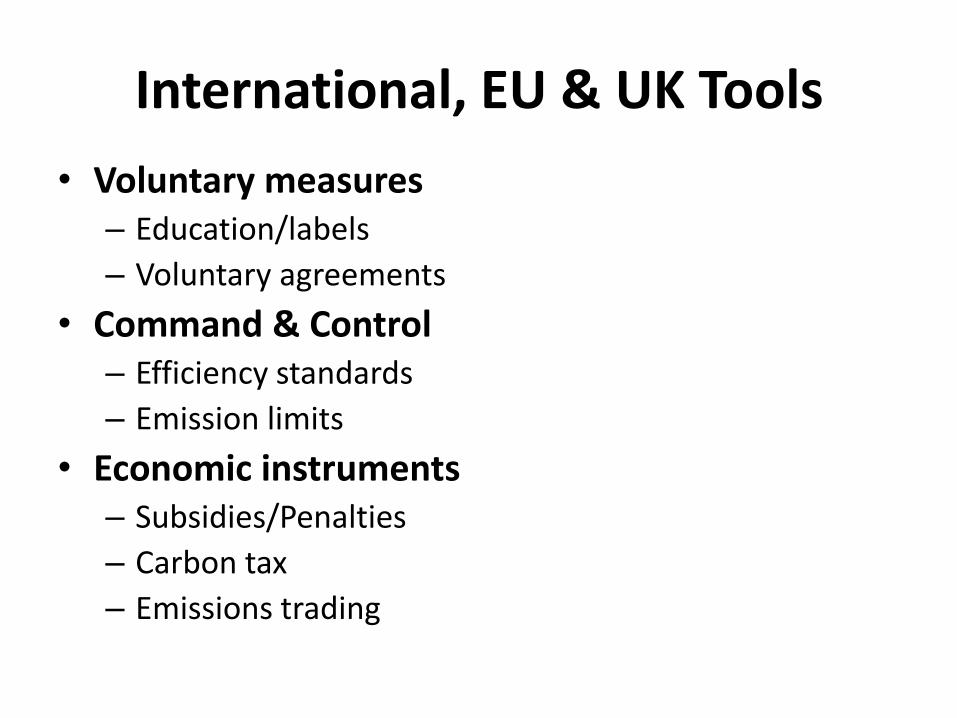

Tools for Governments

What are the tools?

• Policies to:

– Reduce emissions

– Invest in clean technologies

International, EU & UK Tools

• Voluntary measures – Education/labels

– Voluntary agreements

• Command & Control – Efficiency standards

– Emission limits

• Economic instruments – Subsidies/Penalties

– Carbon tax

– Emissions trading

Economic Instruments

• Subsidies • Kick-starting technologies, should be short term

• Carbon Tax • Carbon price known but emissions reduction unknown

• Emissions trading • Emissions reduction known but price unknown

• In theory, a carbon tax and an emissions trading scheme deliver the same result

• In practice, there are significant differences

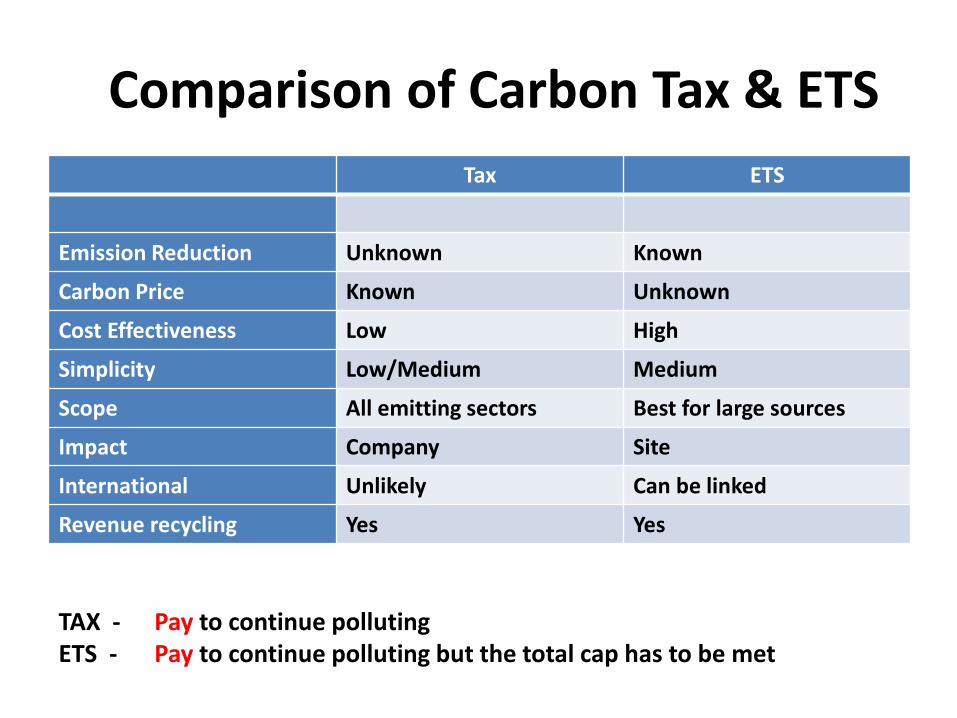

Comparison of Carbon Tax & ETS

Tax ETS

Emission Reduction Unknown Known

Carbon Price Known Unknown

Cost Effectiveness Low High

Simplicity Low/Medium Medium

Scope All emitting sectors Best for large sources

Impact Company Site

International Unlikely Can be linked

Revenue recycling Yes Yes

TAX - Pay to continue polluting ETS - Pay to continue polluting but the total cap has to be met

Emissions Trading – Cap & Trade

• Define sectors to be capped

• Set up cap – can decrease over time

• Set up MRV and compliance rules

• Set up non-compliance penalties

• Allocate allowances to covered sites • Grandfather, benchmark,auction

• Allow market to find least cost reductions

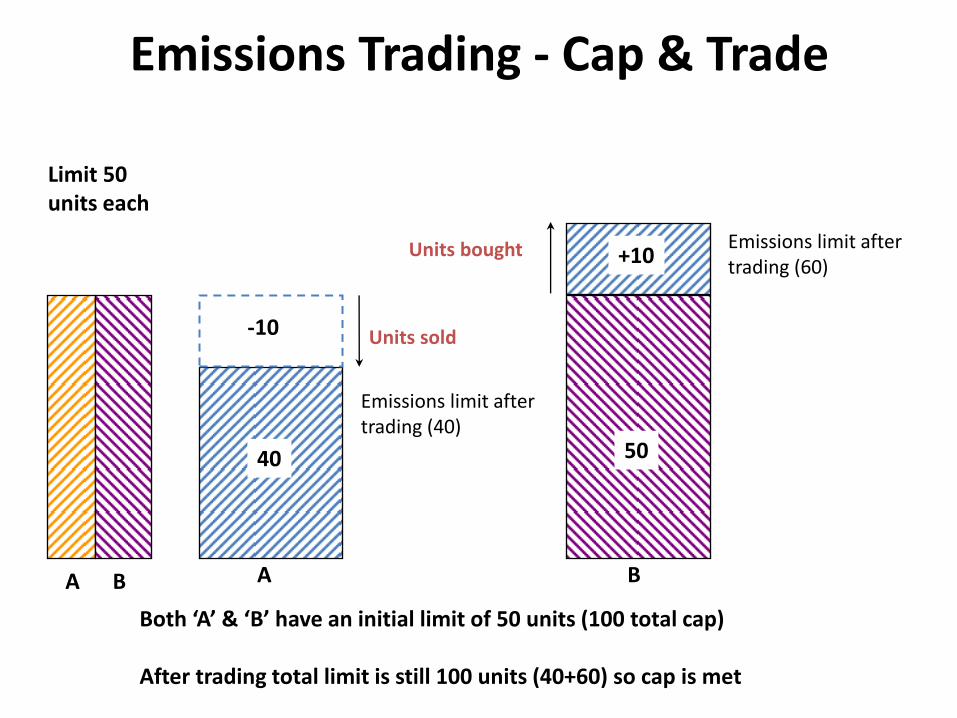

Emissions Trading - Cap & Trade

Both ‘A’ & ‘B’ have an initial limit of 50 units (100 total cap)

A B

50 50

-10

40

+10

Units sold

Emissions limit after trading (40)

Units bought

A B

Emissions limit after trading (60)

50

Emissions Trading - Cap & Trade

Both ‘A’ & ‘B’ have an initial limit of 50 units (100 total cap) After trading total limit is still 100 units (40+60) so cap is met

Limit 50 units each

A B

Emissions Trading - Cap & Trade

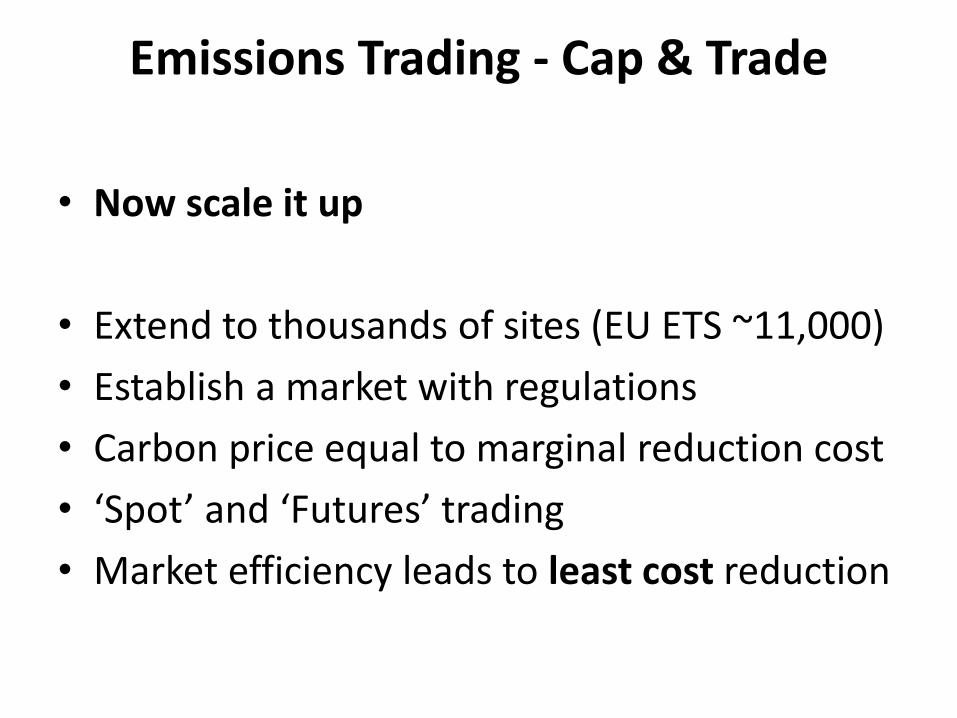

• Now scale it up

• Extend to thousands of sites (EU ETS ~11,000)

• Establish a market with regulations

• Carbon price equal to marginal reduction cost

• ‘Spot’ and ‘Futures’ trading

• Market efficiency leads to least cost reduction

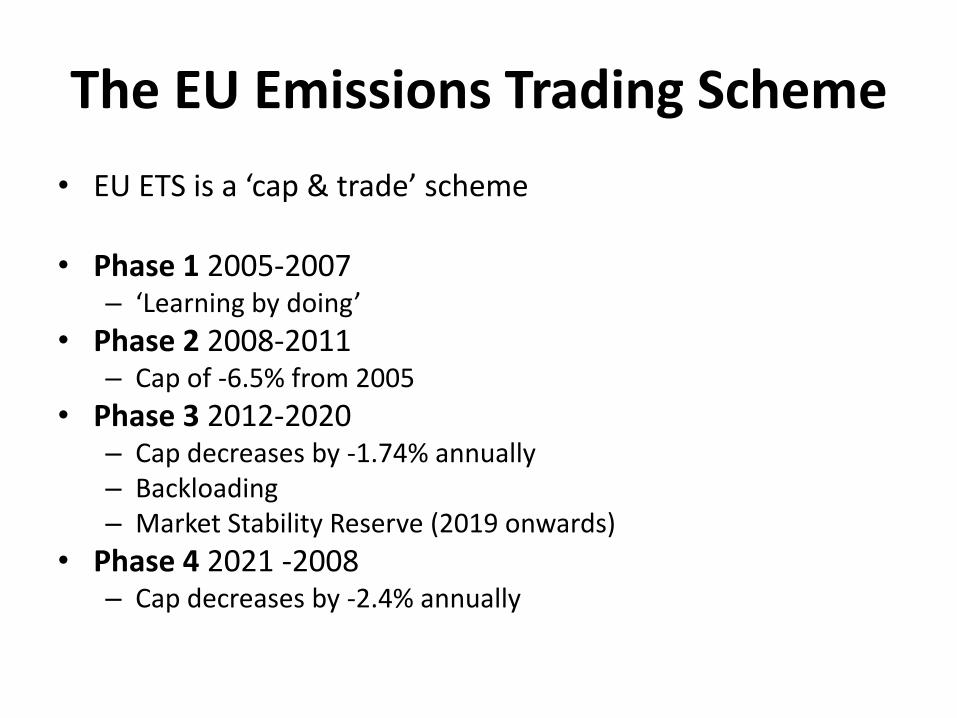

EU Emissions Trading Scheme

The EU Emissions Trading Scheme

• EU ETS is a ‘cap & trade’ scheme • Phase 1 2005-2007

– ‘Learning by doing’

• Phase 2 2008-2011 – Cap of -6.5% from 2005

• Phase 3 2012-2020 – Cap decreases by -1.74% annually – Backloading – Market Stability Reserve (2019 onwards)

• Phase 4 2021 -2008 – Cap decreases by -2.4% annually

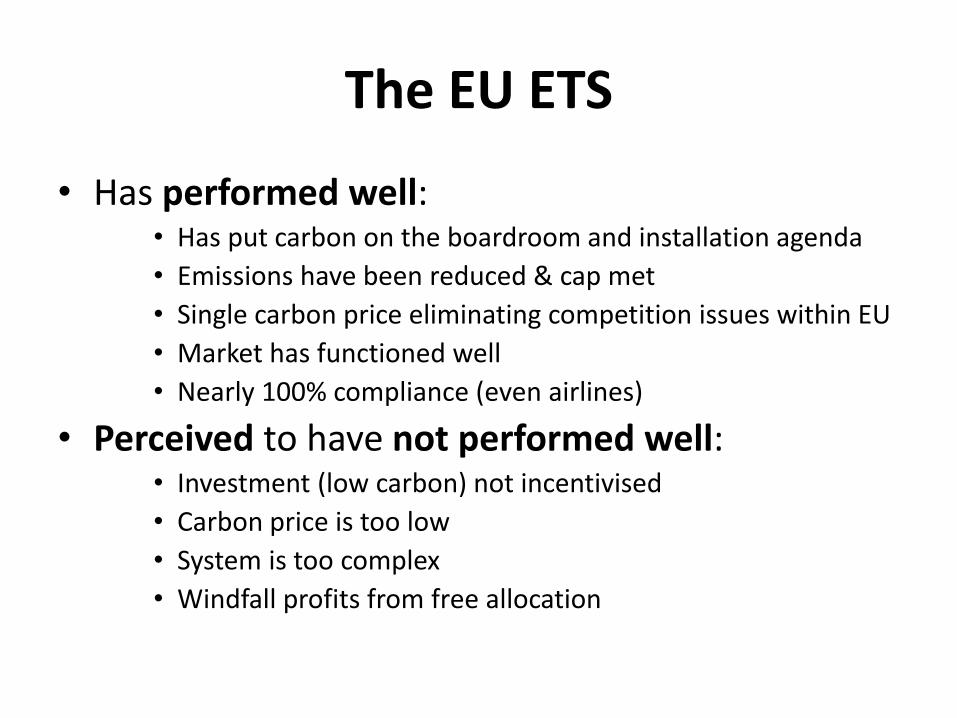

The EU ETS

• Has performed well: • Has put carbon on the boardroom and installation agenda

• Emissions have been reduced & cap met

• Single carbon price eliminating competition issues within EU

• Market has functioned well

• Nearly 100% compliance (even airlines)

• Perceived to have not performed well: • Investment (low carbon) not incentivised

• Carbon price is too low

• System is too complex

• Windfall profits from free allocation

Reasons & Remedies • Reasons

– Overlapping policies – CDM & JI imports – Recession – Continued free allocation to avoid carbon leakage

• Remedies • Ideal

– Revise cap to align with 2oC and with auctioning for all – Better analysis & integration of overlapping policies – Remove subsidies from technologies that are competitive

• Proposed for EU ETS Phase 4 – Increase annual reduction factor from -1.74% to -2.4% – More focussed benchmarks and free allocation rules – Market Stability Reserve from 2019

17 Carbon markets worldwide International Emissions Trading

New Zealand

Tokyo &

Saitama

RGGI

California

Beijing

Tianjin

Shanghai

Chongqing

Hubei

Shenzhen Guangdong

EU ETS

South Korea Switzerlan

d

Washington

Rio de Janeiro

Sao Paulo

Kazakhstan

Taiwan

Vietnam

South Africa

Mexico

China US

Canada

Alberta Ontario

ETS in place

Subnational ETS in place

ETS Being Designed

Carbon Tax with Offsets

Being designed or in place

Linkages

Trinidad and Tobago

Ukraine

Hybrid Carbon Pricing

British

Columbi

a

Australia

Thailand

Oregon

Quebec

Nova

Scotia

Carbon markets cover +40% of global GDP and 12% of gIIlobal CO2 emissions International Markets

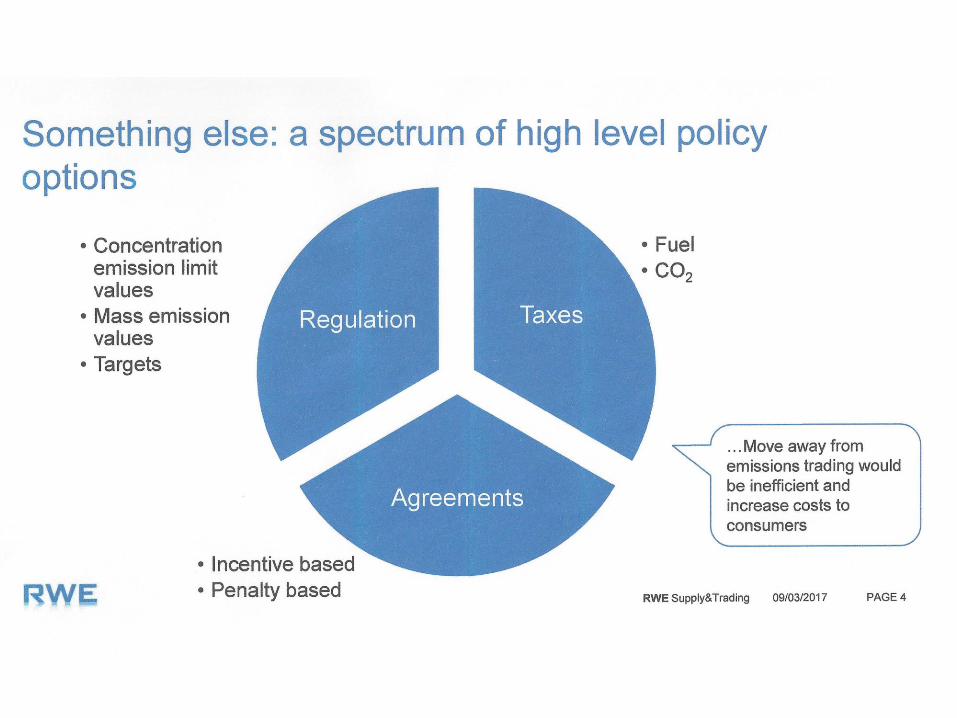

Brexit

Brexit & UK Climate Policy

• UK has commitments:

– Carbon Budget

– Paris Agreement

• The UK will need a range of policies probably including an ETS

Post Brexit Options

Fuel Poverty

Affordable

Warmth

Scheme

DTI & Trans

Co £20m

Domestic

Company

Cars

Tax relief

related to

emissions

Tax on Work

Parking

To

encourage

use of public

transport

New Deal

for

Transport

DETR on

transport

Transport

Fuel Duty

May be

increased

Transport Integrated

Transport

Strategy

Actions to meet Kyoto (-12.5% GHG)

Emissions Trading

Scheme

Green Tariff

Endorsement

by Energy

Savings Trust

CHP and Renewables

Areas Not Tackled Directly

•Agriculture

•Landfill

•Electricity Production

•Oil industry

•Aviation

Industry

Other

International

Emissions

Trading

Projects

Avoidance

of emissions

Voluntary

Agreement

Reduce emissions

Actions to meet Government Target (-20%

CO2)

Assumed

Power

Station Mix

DTI projections

Enhanced

Capital

Allowances

Energy efficiency

measures

Climate

Change

Levy

Actions

involving

only Energy

Industry

CCL

Exemption

Renewables

& CHP

Promote

Renewables

& CHP

Use revenue

from CCL

NFFO

PES

obligation

Supplier

Renewable

Obligation

Green

Certificate

Trading

Meet supplier

obligation

CCL

Agreements

Fuel efficiency

or emission

targets for CCL

reduction

Promote

Energy

Efficiency

Revenue from

CCL for energy

efficiency in

business

EESoPs

Energy Eff

Stndrd Perform.

Home

Energy

Efficiency

Scheme (HEES)

£330m DETR

Green

Trading

International

Flare

Consents

Scheme

Aviation

Emissions

Scheme

Build

CHP?

10GW(e)

Installed

CHP capacity

Branding

Perceptions

Local

Agenda 21

Public sector

energy efficiency

IPPC

BAT

& energy

efficiency

Export Credit

Guarantee

Application must

include environmental

assessment

EU Emissions

Trading

Scheme

FFL

Income

10%

supply from

renewables

Car Tax

Relate to

car emissions

EU

22-23%

renewable

supply directive

Market Trans.

Measures

Investment

energy eff.

Electricity

Association

Fuel poverty

task force

UK Climate &

Energy Policies

Thank You