managing fraud risk in the digital age · 2019-11-24 · coso fraud risk management framework the...

TRANSCRIPT

MANAGING FRAUD RISK

IN THE DIGITAL AGE

November 2019

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

1 FRAUD FACTS

2 COSO FRAUD RISK MANAGEMENT

FRAMEWORK

3 THE NEED FOR DIGITAL TOOLS

4 DATA ANALYTICS IN FRAUD RISK

MANAGEMENT

5 ACHIEVING REAL TIME MONITORING

6 PREDICTIVE ANALYTICS

Agenda

FRAUD FACTS

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

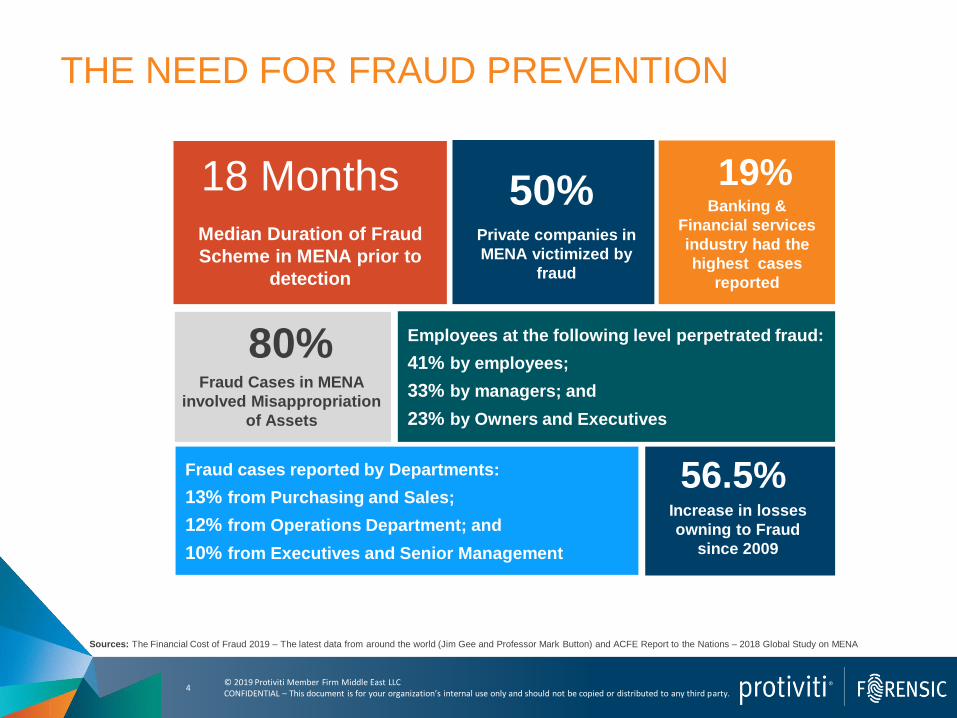

THE NEED FOR FRAUD PREVENTION

4

Sources: The Financial Cost of Fraud 2019 – The latest data from around the world (Jim Gee and Professor Mark Button) and ACFE Report to the Nations – 2018 Global Study on MENA

Employees at the following level perpetrated fraud:

41% by employees;

33% by managers; and

23% by Owners and Executives

Fraud cases reported by Departments:

13% from Purchasing and Sales;

12% from Operations Department; and

10% from Executives and Senior Management

Fraud Cases in MENA

involved Misappropriation

of Assets

80%

Private companies in

MENA victimized by

fraud

50% Banking &

Financial services

industry had the

highest cases

reported

19%

Increase in losses

owning to Fraud

since 2009

56.5%

18 Months Median Duration of Fraud

Scheme in MENA prior to

detection

COSO FRAUD RISK

MANAGEMENT

FRAMEWORK

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

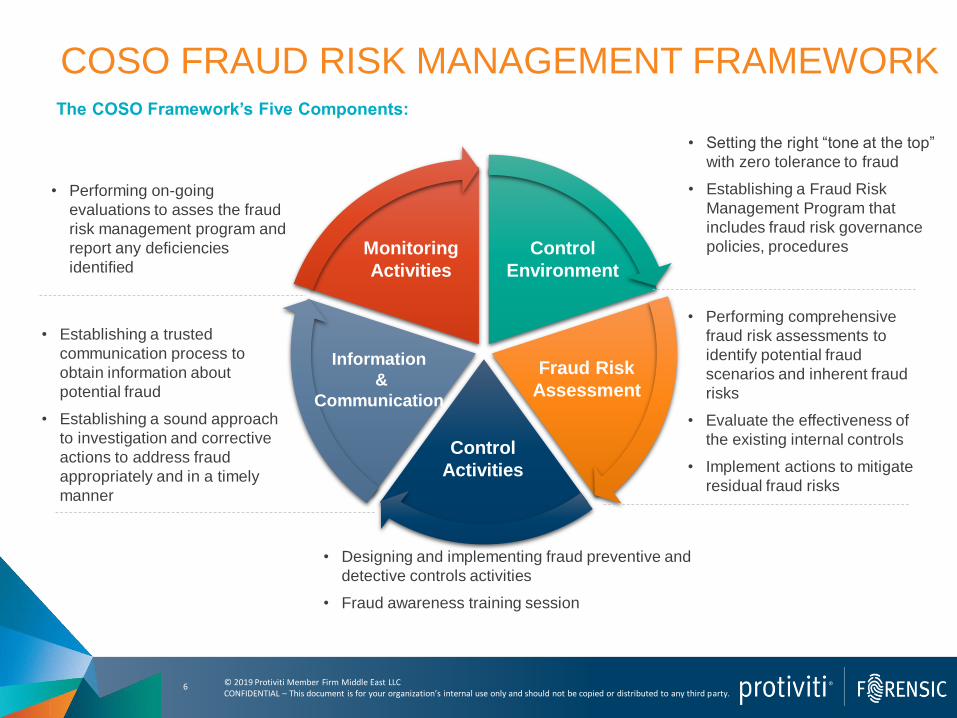

COSO FRAUD RISK MANAGEMENT FRAMEWORK The COSO Framework’s Five Components:

6

• Setting the right “tone at the top”

with zero tolerance to fraud

• Establishing a Fraud Risk

Management Program that

includes fraud risk governance

policies, procedures

• Performing comprehensive

fraud risk assessments to

identify potential fraud

scenarios and inherent fraud

risks

• Evaluate the effectiveness of

the existing internal controls

• Implement actions to mitigate

residual fraud risks

• Designing and implementing fraud preventive and

detective controls activities

• Fraud awareness training session

• Establishing a trusted

communication process to

obtain information about

potential fraud

• Establishing a sound approach

to investigation and corrective

actions to address fraud

appropriately and in a timely

manner

• Performing on-going

evaluations to asses the fraud

risk management program and

report any deficiencies

identified Monitoring

Activities

Control

Environment

Fraud Risk

Assessment

Control

Activities

Information

&

Communication

THE NEED FOR DIGITAL

TOOLS

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

“The goal is to turn data into information,

and information into insight.”

- Carly Fiorina, former Executive, President, and Chair of Hewlett-Packard Co.

8

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

THE NEED FOR DIGITAL TOOLS

9

9

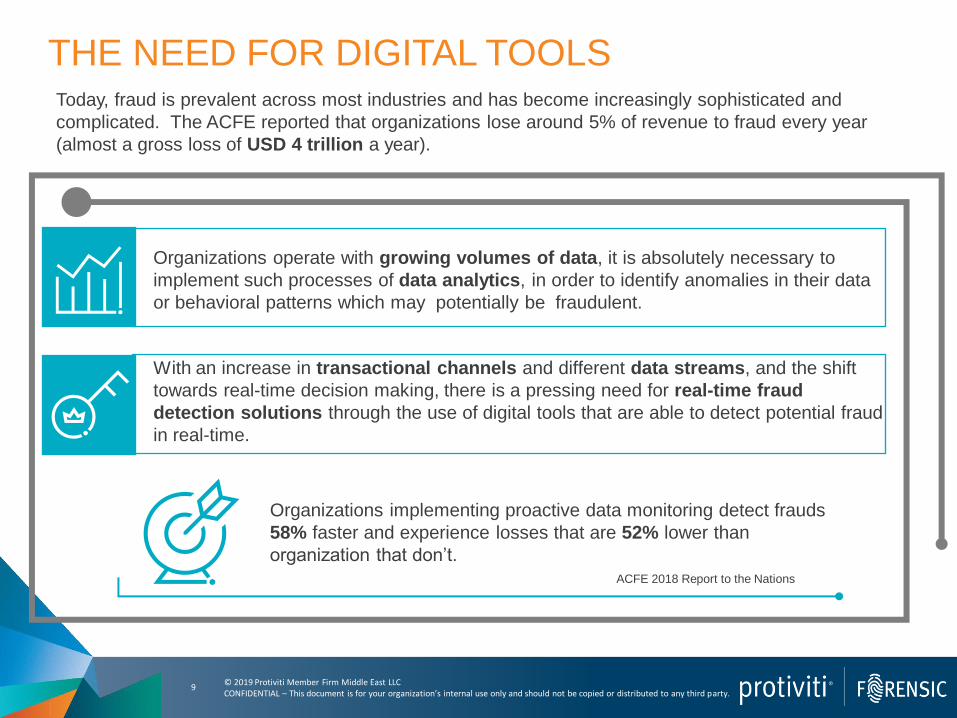

Today, fraud is prevalent across most industries and has become increasingly sophisticated and

complicated. The ACFE reported that organizations lose around 5% of revenue to fraud every year

(almost a gross loss of USD 4 trillion a year).

Organizations implementing proactive data monitoring detect frauds

58% faster and experience losses that are 52% lower than

organization that don’t.

With an increase in transactional channels and different data streams, and the shift

towards real-time decision making, there is a pressing need for real-time fraud

detection solutions through the use of digital tools that are able to detect potential fraud

in real-time.

Organizations operate with growing volumes of data, it is absolutely necessary to

implement such processes of data analytics, in order to identify anomalies in their data

or behavioral patterns which may potentially be fraudulent.

ACFE 2018 Report to the Nations

DATA ANALYTICS IN

FRAUD RISK

MANAGEMENT

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

DATA ANALYTICS IN FRAUD RISK

MANAGEMENT

The team will make recommended changes to the following key areas based on our analysis to drive improvements and efficiencies:

• E-mail and e-Communications (social media, collaborative tools (instant messaging, etc.)

• Confidential and Vital Records handling

• Legal Hold procedures

• Alternate storage media (Portable USB, etc.)

• Archive and Back-up

• Records Disposition

• Agree on Definition (Transfer, Convert, Archive, or Destroy)

• Release to 3rd Parties

• Conversion for permanent preservation

• Exception Handling procedures

Data analytics, as it applies to fraud examination, refers to the use of analytics software

to identify trends, patterns, anomalies, and exceptions within data:

• The standard common audit approach of sample testing is a valid audit approach,

however it is not as effective for fraud detection and prevention purposes;

• Fraud data analysis requires the effective use of technological tools to translate the data

and information of an organization into analytics test to provide deeper insight into how

well internal controls are operating;

• Data analytics enables organizations to connect information from different data sources in

order to analyze trends and identify anomalies which could be potential instances of

fraud or noncompliance;

• Proactive data analysis and continuous monitoring are effective tools for anti-fraud

controls and in helping reduce fraud losses and fraud scheme duration;

• Fraud investigation skills are applied to the data analysis results in order to review

potential instances of fraud or identified red flags.

11

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

USING DATA ANALYTICS IN FRAUD RISK

MANAGEMENT

12

The simple idea for using data analytics to detect fraud is to analyze an entire

population of transactional data in order to identify anomalies or other indicators of

fraudulent activities within an organization

Designed to identify the

anomalies and irregular

transactions that are outside

of the norm

1 Statistical

analysis

Designed to test for specific

fraud scenarios or schemes

that may indicate a high

probability of fraud

1 Analytic

testing

Designed to compare and

connect data from different

sources and systems in ways

that could not have been done

manually

1 Comparative

testing

The different ways data analysis can be used:

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

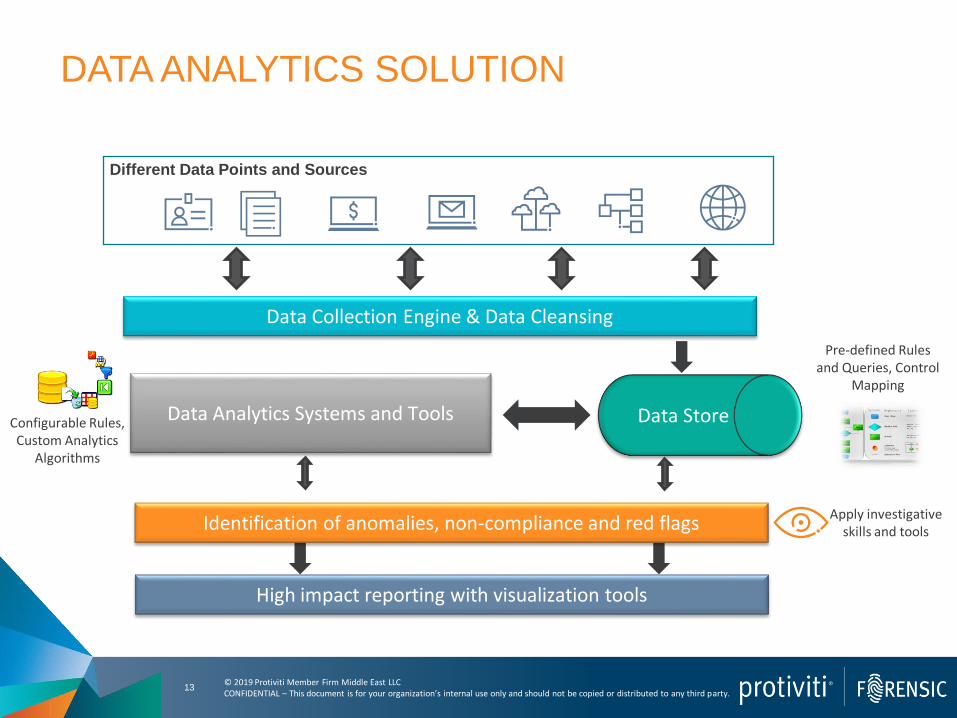

DATA ANALYTICS SOLUTION

Data Collection Engine & Data Cleansing

Data Store

Pre-defined Rules and Queries, Control

Mapping

Data Analytics Systems and Tools Configurable Rules, Custom Analytics

Algorithms

High impact reporting with visualization tools

Different Data Points and Sources

13

Identification of anomalies, non-compliance and red flags Apply investigative

skills and tools

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

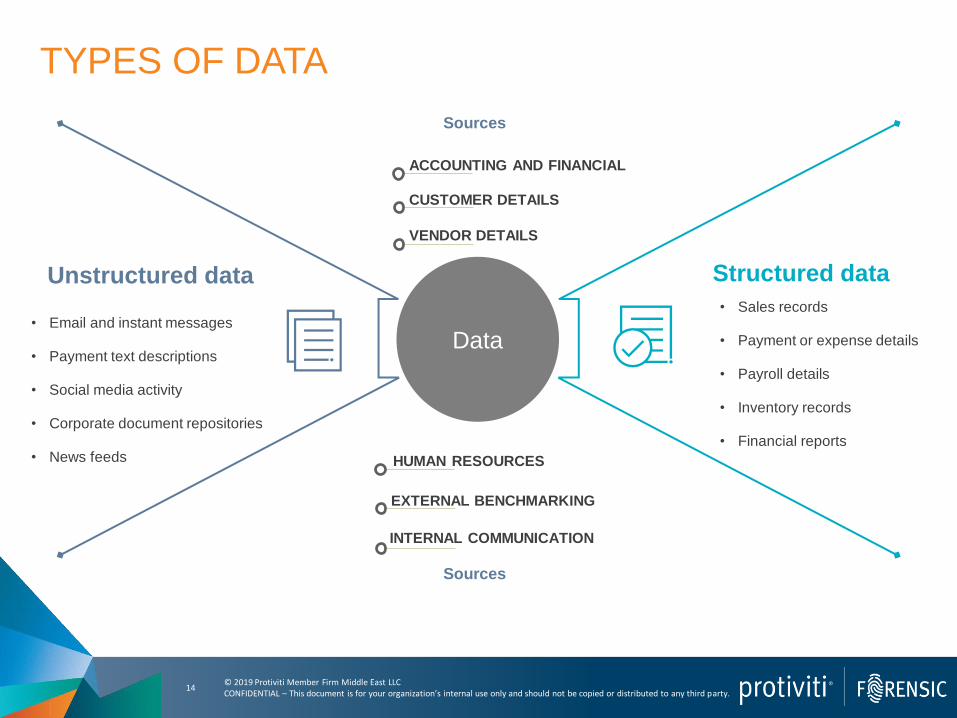

TYPES OF DATA

14

Sources

Sources

Data

Unstructured data

• Email and instant messages

• Payment text descriptions

• Social media activity

• Corporate document repositories

• News feeds

Structured data

• Sales records

• Payment or expense details

• Payroll details

• Inventory records

• Financial reports

ACCOUNTING AND FINANCIAL

CUSTOMER DETAILS

VENDOR DETAILS

EXTERNAL BENCHMARKING

INTERNAL COMMUNICATION

HUMAN RESOURCES

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

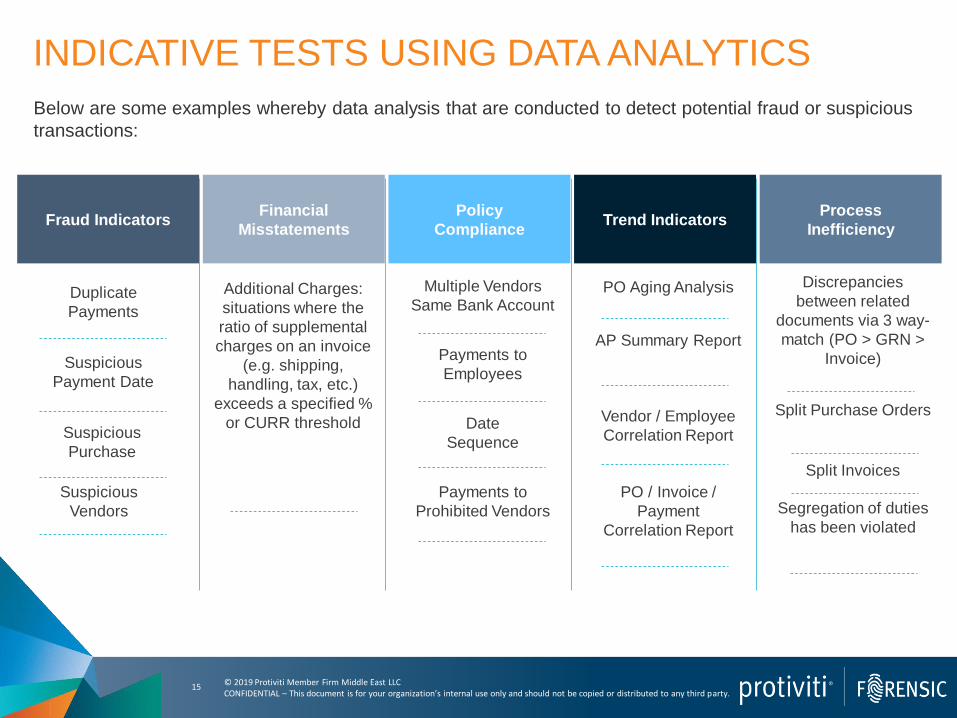

INDICATIVE TESTS USING DATA ANALYTICS

Fraud Indicators Financial

Misstatements

Policy

Compliance Trend Indicators

Process

Inefficiency

Multiple Vendors

Same Bank Account

Payments to

Employees

Duplicate

Payments

PO Aging Analysis

Date

Sequence

Discrepancies

between related

documents via 3 way-

match (PO > GRN >

Invoice) Suspicious

Payment Date

Split Purchase Orders

Split Invoices

Payments to

Prohibited Vendors Segregation of duties

has been violated

AP Summary Report

Vendor / Employee

Correlation Report

PO / Invoice /

Payment

Correlation Report

Additional Charges:

situations where the

ratio of supplemental

charges on an invoice

(e.g. shipping,

handling, tax, etc.)

exceeds a specified %

or CURR threshold Suspicious

Purchase

Suspicious

Vendors

Below are some examples whereby data analysis that are conducted to detect potential fraud or suspicious

transactions:

15

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

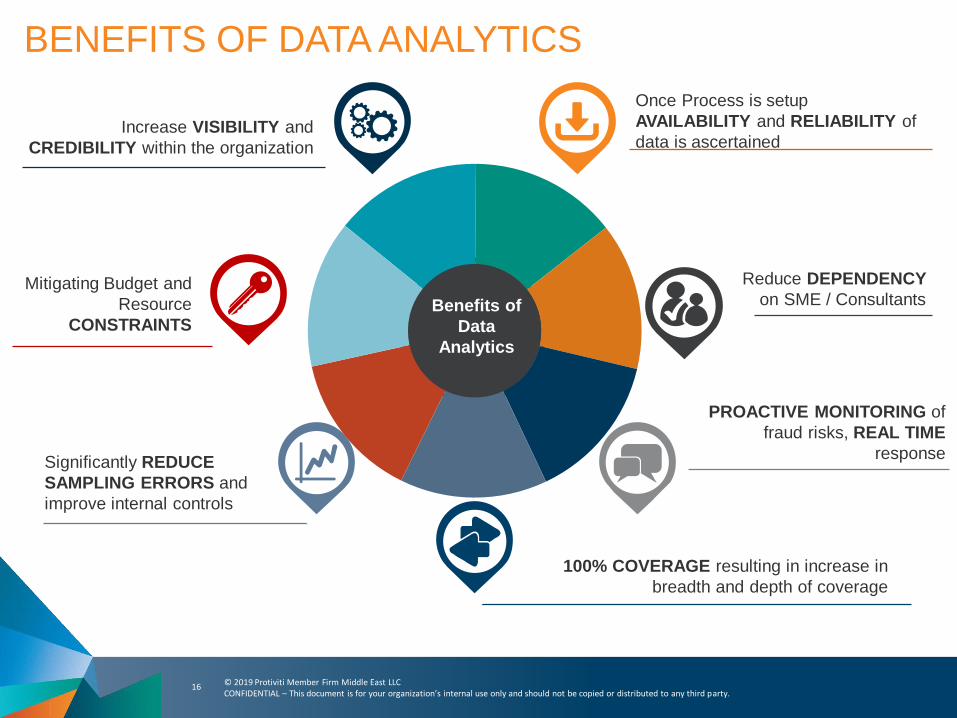

BENEFITS OF DATA ANALYTICS

Mitigating Budget and

Resource

CONSTRAINTS

Significantly REDUCE

SAMPLING ERRORS and

improve internal controls

Reduce DEPENDENCY

on SME / Consultants

100% COVERAGE resulting in increase in

breadth and depth of coverage

PROACTIVE MONITORING of

fraud risks, REAL TIME

response

Once Process is setup

AVAILABILITY and RELIABILITY of

data is ascertained

Benefits of

Data

Analytics

Increase VISIBILITY and

CREDIBILITY within the organization

16

ACHIEVING REAL TIME

MONITORING

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

18

CONTINUOUS MONITORING IN FRAUD RISK

MANAGEMENT

It is important to detect fraud sooner rather than later in order to minimize losses and damages

caused by fraud. Continuous monitoring enables organizations to repeat the set up data analytic tests

against most recent and new transactions.

What does this mean?

Automating the process of data collection and generating data analytics

to detect potential fraudulent activities:

Running the scripts and fraud rules that have already been established to test

for different indicators of fraud on a regular basis. The frequency will depend

on the objective of each test and the size of the organization.

The exceptions identified will automatically be routed to the selected

department for further review.

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

19

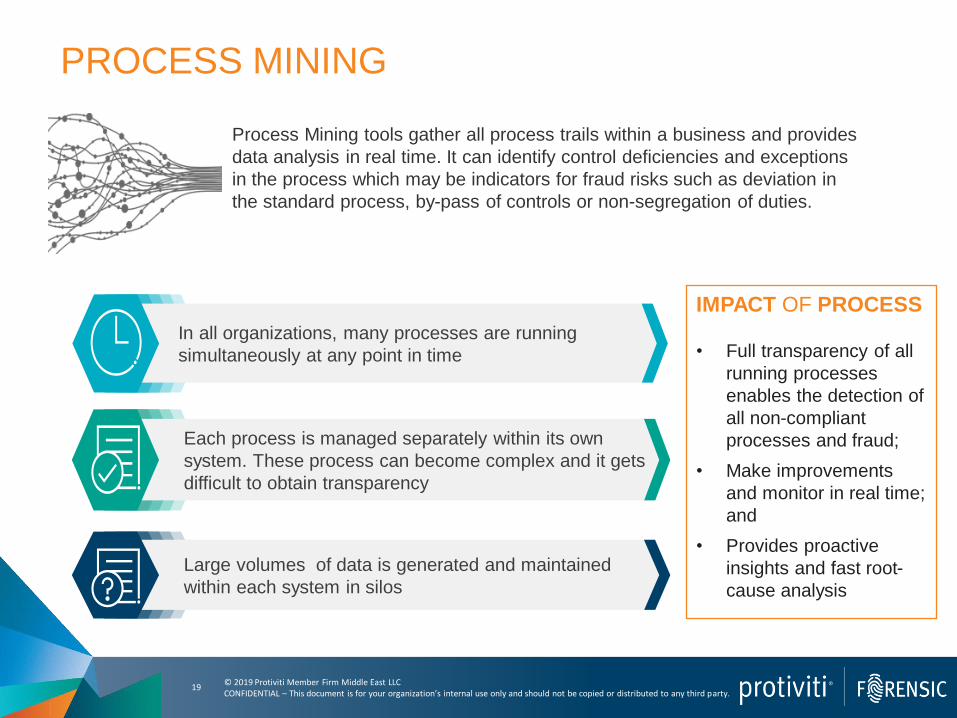

Process Mining tools gather all process trails within a business and provides

data analysis in real time. It can identify control deficiencies and exceptions

in the process which may be indicators for fraud risks such as deviation in

the standard process, by-pass of controls or non-segregation of duties.

PROCESS MINING

In all organizations, many processes are running

simultaneously at any point in time

Each process is managed separately within its own

system. These process can become complex and it gets

difficult to obtain transparency

Large volumes of data is generated and maintained

within each system in silos

IMPACT OF PROCESS

• Full transparency of all

running processes

enables the detection of

all non-compliant

processes and fraud;

• Make improvements

and monitor in real time;

and

• Provides proactive

insights and fast root-

cause analysis

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

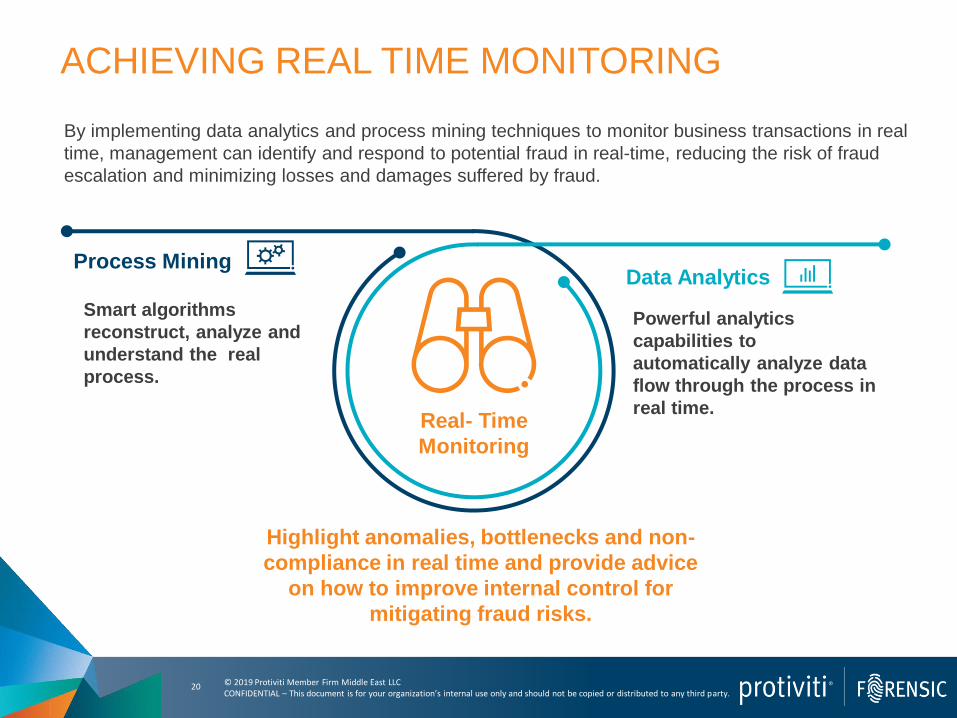

Data Analytics Process Mining

Smart algorithms

reconstruct, analyze and

understand the real

process.

Powerful analytics

capabilities to

automatically analyze data

flow through the process in

real time.

ACHIEVING REAL TIME MONITORING

By implementing data analytics and process mining techniques to monitor business transactions in real

time, management can identify and respond to potential fraud in real-time, reducing the risk of fraud

escalation and minimizing losses and damages suffered by fraud.

20

Real- Time

Monitoring

Highlight anomalies, bottlenecks and non-

compliance in real time and provide advice

on how to improve internal control for

mitigating fraud risks.

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

21

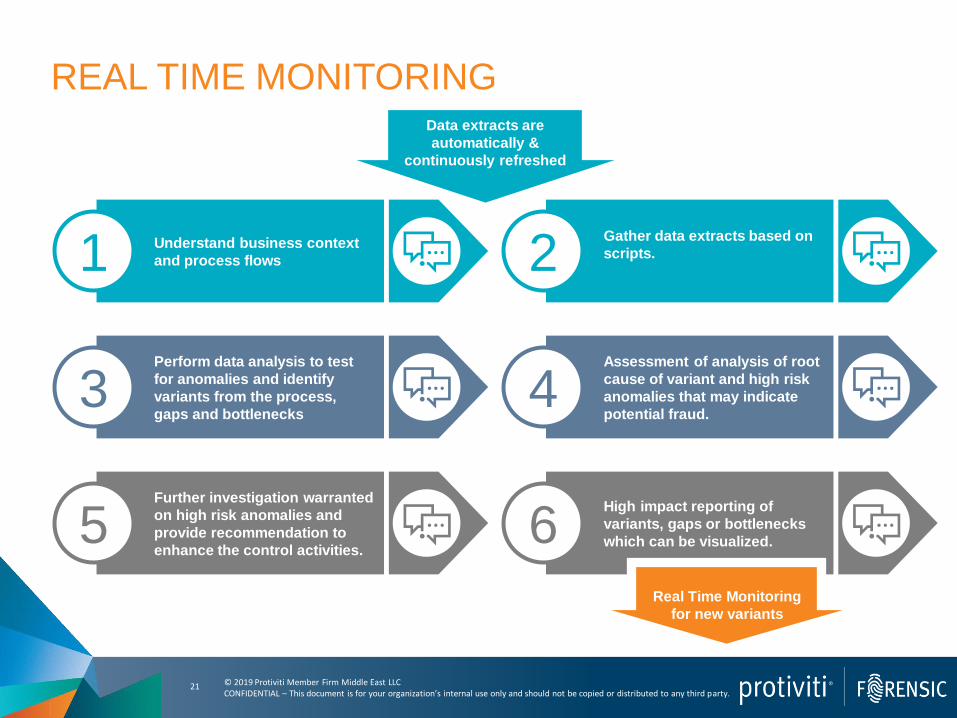

Gather data extracts based on

scripts. 2

Perform data analysis to test

for anomalies and identify

variants from the process,

gaps and bottlenecks 3

Assessment of analysis of root

cause of variant and high risk

anomalies that may indicate

potential fraud. 4

Further investigation warranted

on high risk anomalies and

provide recommendation to

enhance the control activities. 5

High impact reporting of

variants, gaps or bottlenecks

which can be visualized. 6

Understand business context

and process flows 1

Real Time Monitoring

for new variants

Data extracts are

automatically &

continuously refreshed

REAL TIME MONITORING

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

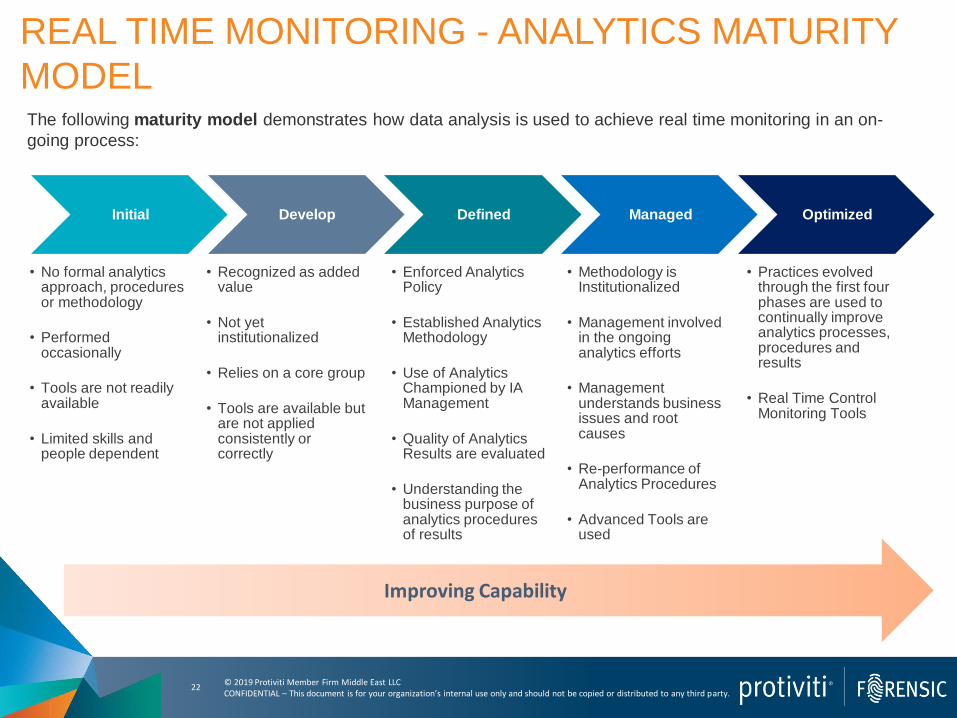

Initial

• No formal analytics approach, procedures or methodology

• Performed occasionally

• Tools are not readily available

• Limited skills and people dependent

Develop

• Recognized as added value

• Not yet institutionalized

• Relies on a core group

• Tools are available but are not applied consistently or correctly

Defined

• Enforced Analytics Policy

• Established Analytics Methodology

• Use of Analytics Championed by IA Management

• Quality of Analytics Results are evaluated

• Understanding the business purpose of analytics procedures of results

Managed

• Methodology is Institutionalized

• Management involved in the ongoing analytics efforts

• Management understands business issues and root causes

• Re-performance of Analytics Procedures

• Advanced Tools are used

Optimized

• Practices evolved through the first four phases are used to continually improve analytics processes, procedures and results

• Real Time Control Monitoring Tools

Improving Capability

REAL TIME MONITORING - ANALYTICS MATURITY

MODEL The following maturity model demonstrates how data analysis is used to achieve real time monitoring in an on-

going process:

22

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

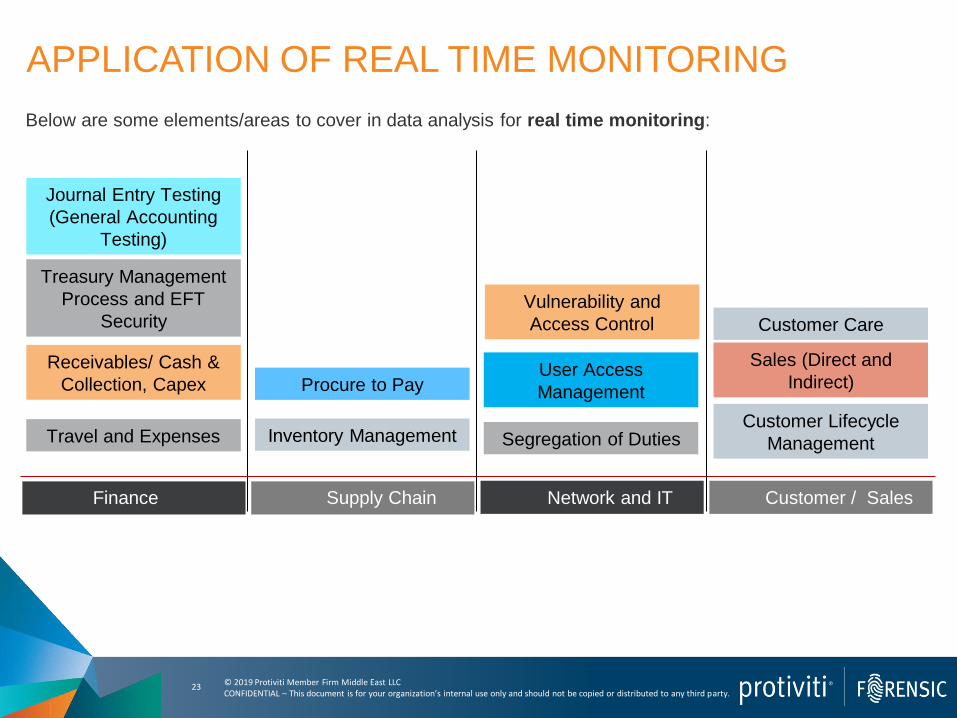

APPLICATION OF REAL TIME MONITORING

Procure to Pay

Travel and Expenses Inventory Management

Receivables/ Cash &

Collection, Capex

Treasury Management

Process and EFT

Security

User Access

Management

Journal Entry Testing

(General Accounting

Testing)

Customer Care

Customer Lifecycle

Management

Sales (Direct and

Indirect)

Finance Supply Chain Network and IT Customer / Sales

Segregation of Duties

Vulnerability and

Access Control

Below are some elements/areas to cover in data analysis for real time monitoring:

23

PREDICTIVE ANALYTICS

© 2019 Protiviti Member Firm Middle East LLC CONFIDENTIAL – This document is for your organization’s internal use only and should not be copied or distributed to any third party.

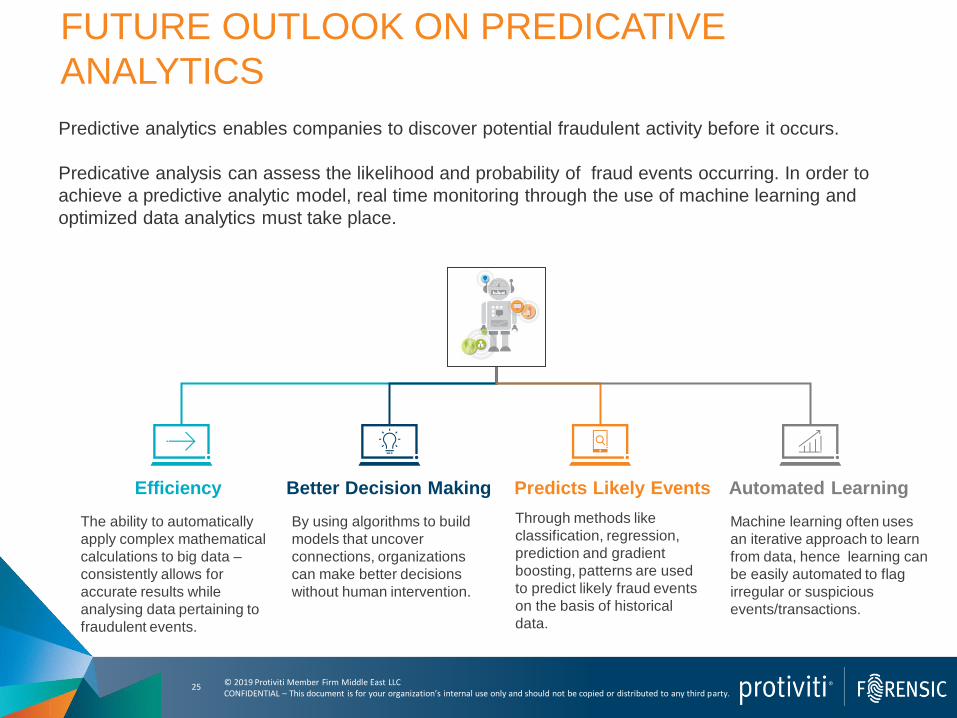

Predictive analytics enables companies to discover potential fraudulent activity before it occurs.

Predicative analysis can assess the likelihood and probability of fraud events occurring. In order to

achieve a predictive analytic model, real time monitoring through the use of machine learning and

optimized data analytics must take place.

FUTURE OUTLOOK ON PREDICATIVE

ANALYTICS

Efficiency

The ability to automatically

apply complex mathematical

calculations to big data –

consistently allows for

accurate results while

analysing data pertaining to

fraudulent events.

Predicts Likely Events Better Decision Making

By using algorithms to build

models that uncover

connections, organizations

can make better decisions

without human intervention.

Automated Learning

Machine learning often uses

an iterative approach to learn

from data, hence learning can

be easily automated to flag

irregular or suspicious

events/transactions.

Through methods like

classification, regression,

prediction and gradient

boosting, patterns are used

to predict likely fraud events

on the basis of historical

data.

25

Protiviti is a global consulting firm that delivers deep expertise, objective

insights, a tailored approach and unparalleled collaboration to help

leaders face the future with confidence. Protiviti and our independently

owned Member Firms provide consulting solutions in strategy,

organizational transformation, operations, finance, technology, data,

analytics, governance and risk to our clients through our network of more

than 70 offices in over 20 countries.

We have served more than 60 percent of Fortune 1000® and 35 percent

of Fortune Global 500® companies. We also work with smaller, growing

companies, including those looking to go public, as well as with

government agencies. Protiviti is a wholly owned subsidiary of Robert Half

(NYSE: RHI). Founded in 1948, Robert Half is a member of the S&P 500

index.