managing brazil risk: practical strategies, lessons, and ... · managing brazil risk: practical...

TRANSCRIPT

Managing Brazil Risk: Practical Strategies, Lessons, and

Solutions for Exploration, Production, and Services

Companies

November 9, 2011

Strategies for Dealing with Brazilian Local Content

RequirementsPresented by

William Prescott Mills [email protected]

November 9, 2011

I. Principles and Practice of Brazilian Local Content Requirements

II. Strategies for Managing Brazilian Local Content Requirements

I. Principles and Practice of Brazilian Local Content Requirements

● Sovereignty and Brazil

● Sources of Local Content Requirements

II. Strategies for Managing Brazilian Local Content Requirements

● Understanding Applicable Regulations

● Managing Relationships

● Analyzing Supply Chains

● Utilizing Available Resources

● Partnering Strategically

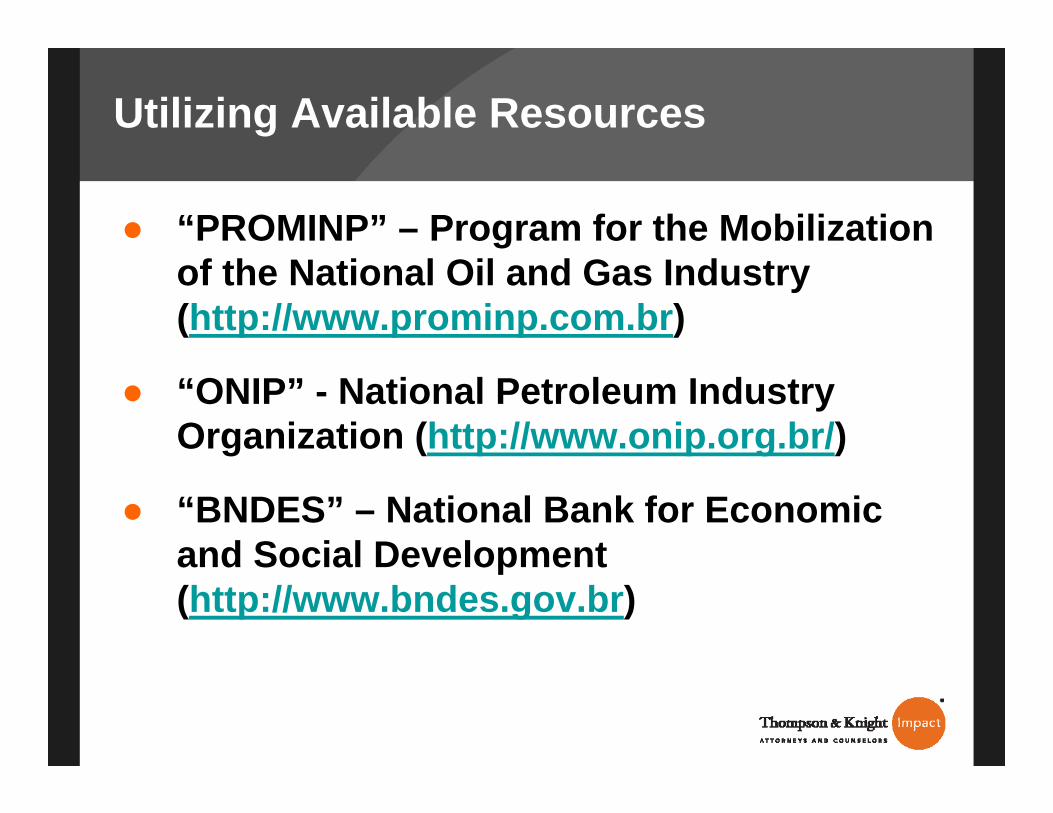

Utilizing Available Resources

● “PROMINP” – Program for the Mobilization of the National Oil and Gas Industry (http://www.prominp.com.br)

● “ONIP” - National Petroleum Industry Organization (http://www.onip.org.br/)

● “BNDES” – National Bank for Economic and Social Development (http://www.bndes.gov.br)

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

Challenges in Hiring, Challenges in Hiring, Firing and Managing Firing and Managing Brazilian EmployeesBrazilian Employees

Bruno TocantinsBruno Tocantins

Tocantins AdvogadosTocantins Advogados

November 9, 2011November 9, 2011

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

Current OverviewCurrent Overview

•• Brazilian employment market is very competitive for Brazilian employment market is very competitive for O&G companies O&G companies –– Difficulty in finding good Difficulty in finding good professionals professionals –– Huge competition for more qualified Huge competition for more qualified employeesemployees

•• Brazilian Labor Legislation is very protective toward Brazilian Labor Legislation is very protective toward employees employees -- CLT set employees' rightsCLT set employees' rights

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

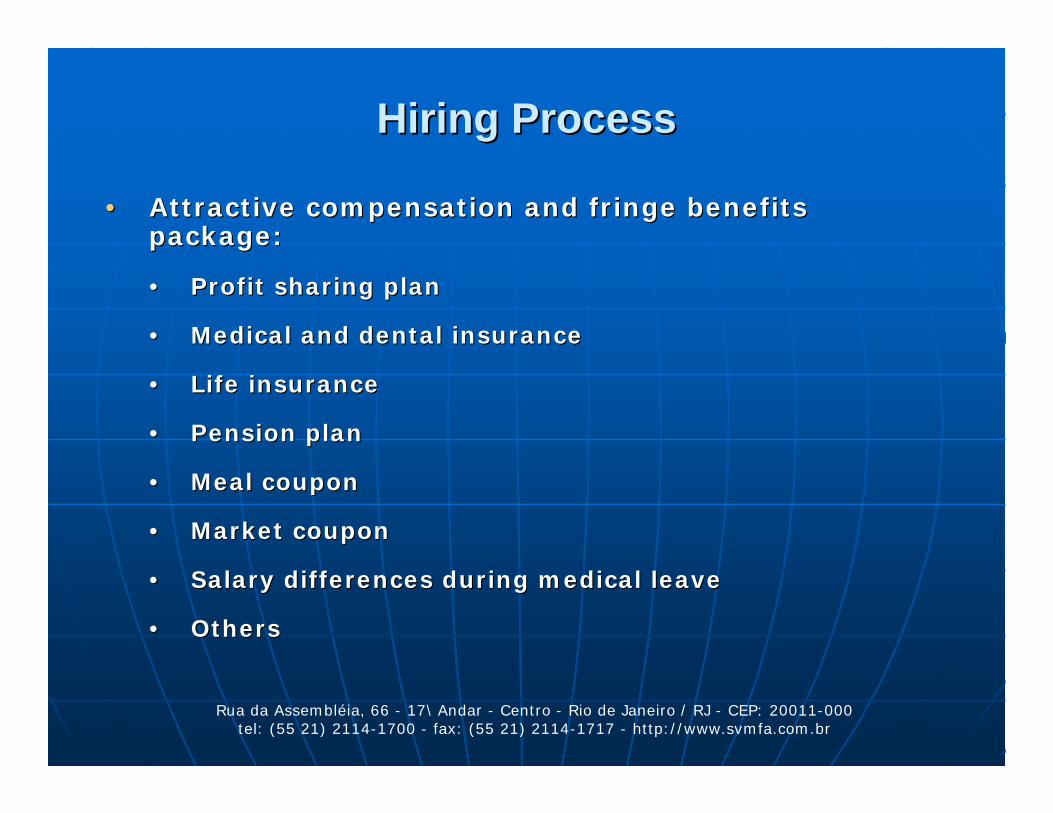

Hiring ProcessHiring Process

•• Attractive compensation and fringe benefits Attractive compensation and fringe benefits package:package:

•• Profit sharing planProfit sharing plan

•• Medical and dental insuranceMedical and dental insurance

•• Life insuranceLife insurance

•• Pension planPension plan

•• Meal couponMeal coupon

•• Market couponMarket coupon

•• Salary differences during medical leaveSalary differences during medical leave

•• OthersOthers

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

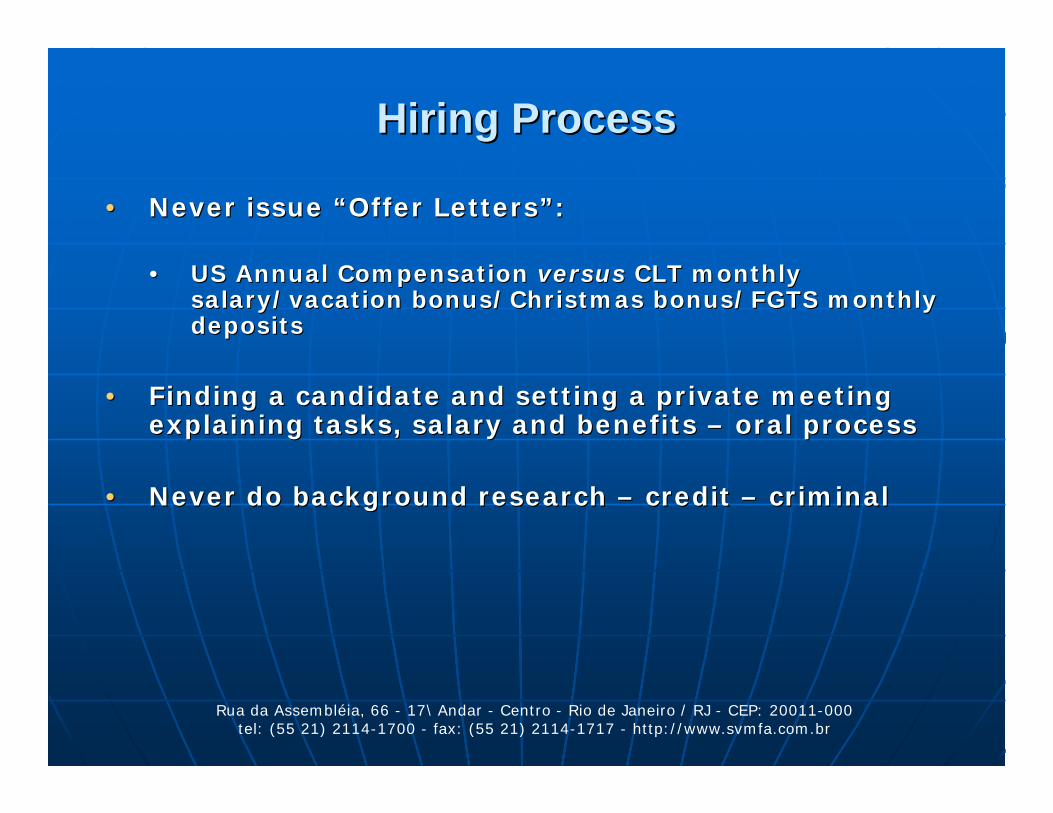

Hiring ProcessHiring Process

•• Never issue “Offer Letters”:Never issue “Offer Letters”:

•• US Annual Compensation US Annual Compensation versusversus CLT monthly CLT monthly salary/vacation bonus/Christmas bonus/FGTS monthly salary/vacation bonus/Christmas bonus/FGTS monthly depositsdeposits

•• Finding a candidate and setting a private meeting Finding a candidate and setting a private meeting explaining tasks, salary and benefits explaining tasks, salary and benefits –– oral processoral process

•• Never do background research Never do background research –– credit credit –– criminalcriminal

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

ManagingManaging

•• Attractive Monthly SalaryAttractive Monthly Salary

•• Attractive fringe benefit packageAttractive fringe benefit package

•• Professional Courses (MBA)Professional Courses (MBA)

•• Attractive program of both salary and position Attractive program of both salary and position increasesincreases

•• Direct channel with local HRDirect channel with local HR

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

Firing ProcessFiring Process

•• Free Employment Constitutional Principle:Free Employment Constitutional Principle:

(a)(a) Cover competitor’s offer; orCover competitor’s offer; or

(b)(b) Set NonSet Non--Competition Agreements with monthly Competition Agreements with monthly paymentspayments

•• Laying off (termination without legal cause) versus Laying off (termination without legal cause) versus Firing (termination with legal cause)Firing (termination with legal cause)

•• Reason for termination not necessary in laying off Reason for termination not necessary in laying off ––deliver the termination letter and pay mandatory deliver the termination letter and pay mandatory legal severancelegal severance

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

QuestionsQuestions

•• Which are the legal implications in the event a Which are the legal implications in the event a company is found doing the background research on company is found doing the background research on candidates’ files?candidates’ files?

•• Due to the “Free Employment Constitutional Due to the “Free Employment Constitutional Principle”, and in the case the employer pays the Principle”, and in the case the employer pays the entire tuition of a MBA course, is it possible for an entire tuition of a MBA course, is it possible for an employee to quit the job and go to a competitor right employee to quit the job and go to a competitor right after the end of the course?after the end of the course?

•• In terms of severance amounts, what is the In terms of severance amounts, what is the difference between laying off and firing an difference between laying off and firing an employee?employee?

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

Thank You!Thank You!

Bruno TocantinsBruno Tocantins

Tocantins AdvogadosTocantins Advogados

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

How to Effectively Partner How to Effectively Partner with a Brazilian Companywith a Brazilian Company

Antonio Luis FerreiraAntonio Luis Ferreira

Schmidt, Valois, Miranda, Ferreira & Agel AdvogadosSchmidt, Valois, Miranda, Ferreira & Agel Advogados

November 9, 2011November 9, 2011

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

•• IntroductionIntroduction

•• Limited Liability CompanyLimited Liability Company

•• JointJoint--Stock CompanyStock Company

•• Consortium (UVJ)Consortium (UVJ)

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

1.1 Introduction1.1 Introduction

•• Foreign Investment in BrazilForeign Investment in Brazil

According to Brazilian law, According to Brazilian law, foreign capitalforeign capital means any means any goods, machinery, equipment, cash and financial goods, machinery, equipment, cash and financial resources that enter the country for the production resources that enter the country for the production of goods or services, or for investment in economic of goods or services, or for investment in economic activities and that belong to individuals or legal activities and that belong to individuals or legal entities resident, domiciled or headquartered entities resident, domiciled or headquartered abroad. (Law # 4,131/62) abroad. (Law # 4,131/62)

Foreign Investments are subject to the Brazilian Foreign Investments are subject to the Brazilian Central Bank registration and monitoring. Central Bank registration and monitoring.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

•• Foreign Investment in BrazilForeign Investment in Brazil

•• Foreign investors may directly invest in Brazil by Foreign investors may directly invest in Brazil by acquiring shares/quotas/participation in an existing acquiring shares/quotas/participation in an existing corporate entity or consortium or by forming a new corporate entity or consortium or by forming a new one. one.

•• Public, state owned/controlled or private companiesPublic, state owned/controlled or private companies

•• Most widely used types of corporate entities are:Most widely used types of corporate entities are:

limited liability company (limited liability company (sociedade limitadasociedade limitada) under Law ) under Law # 10,406/02 # 10,406/02 –– Brazilian Civil Code);Brazilian Civil Code);

jointjoint--stock company (stock company (sociedade por açõessociedade por ações) under Law ) under Law # 6,404/76 # 6,404/76 –– Corporate Law. Corporate Law.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

•• Foreign Investment in BrazilForeign Investment in Brazil

•• Common features between Common features between limitadaslimitadas and jointand joint--stock stock companies: companies:

Partners’ liability is limited to the amount which they paid Partners’ liability is limited to the amount which they paid for their quotas or shares;for their quotas or shares;

Company must have at least two partners, whether Company must have at least two partners, whether individuals or legal entities, who need not be domiciled in individuals or legal entities, who need not be domiciled in Brazil;Brazil;

There are no minimum corporate capital requirements, There are no minimum corporate capital requirements, except in a few circumstances;except in a few circumstances;

The corporate capital may be distributed among the The corporate capital may be distributed among the partners as they find appropriate.partners as they find appropriate.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

1.2 Limited Liability Company (1.2 Limited Liability Company (limitadalimitada))

•• Main FeaturesMain Features

•• The stock of the The stock of the limitadalimitada is divided into quotas. is divided into quotas.

•• Each partner’s liability is limited to the amount of its Each partner’s liability is limited to the amount of its quotas, but all partners are jointly and severally liable quotas, but all partners are jointly and severally liable for the total amount of the corporate capital until it is for the total amount of the corporate capital until it is fully paid up.fully paid up.

•• No public subscription of the quotas is allowed and a No public subscription of the quotas is allowed and a limitadalimitada cannot trade its quotas, nor issue debentures cannot trade its quotas, nor issue debentures or obtain quotation in a stock exchange.or obtain quotation in a stock exchange.

•• The rendering of services as contribution of the The rendering of services as contribution of the quotaholders for the formation of the company’s capital quotaholders for the formation of the company’s capital is not allowed.is not allowed.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

•• Quotas and Company’s CapitalQuotas and Company’s Capital

•• There is no requirement that a minimum amount of the There is no requirement that a minimum amount of the stock be paid up front, nor is there any mandatory time stock be paid up front, nor is there any mandatory time limit for the stock to be fully paid up.limit for the stock to be fully paid up.

•• However, any stock increase may only be effected after However, any stock increase may only be effected after payment in full of the existing quotas and it is subject payment in full of the existing quotas and it is subject to preemptive rights during 30 days. to preemptive rights during 30 days.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

•• Quotas and Company’s CapitalQuotas and Company’s Capital

•• The existence and ownership of the quotas is evidenced The existence and ownership of the quotas is evidenced by the articles of association. by the articles of association.

•• Most resolutions may be taken with the approval of Most resolutions may be taken with the approval of partners representing 75% of the total corporate partners representing 75% of the total corporate capital (exceptions by law or in the articles of capital (exceptions by law or in the articles of association)association)

•• All transfers of quotas must be done by means of an All transfers of quotas must be done by means of an amendment to the articles of association and, unless amendment to the articles of association and, unless otherwise provided for in the articles of association, if otherwise provided for in the articles of association, if there is no opposition from quotaholders representing there is no opposition from quotaholders representing more than 25% of the stock of the more than 25% of the stock of the limitadalimitada, a , a quotaholder may freely transfer his quotas.quotaholder may freely transfer his quotas.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

•• ManagementManagement

•• The The limitadalimitada must be managed by one or more must be managed by one or more managers appointed in the articles of association or by managers appointed in the articles of association or by resolution.resolution.

•• A foreigner may be appointed as manager so long he or A foreigner may be appointed as manager so long he or she is resident and domiciled in Brazil. The she is resident and domiciled in Brazil. The limitadalimitadamay apply for a permanent visa on behalf of the may apply for a permanent visa on behalf of the manager so long as it holds a registered investment of manager so long as it holds a registered investment of at least R$600,000.00 (US$345,000.00) per foreign at least R$600,000.00 (US$345,000.00) per foreign officer/manager.officer/manager.

•• The articles of association describes the powers and The articles of association describes the powers and limitations of the manager or officer, as well as which limitations of the manager or officer, as well as which acts shall require the prior authorization from the acts shall require the prior authorization from the quotaholders.quotaholders.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

1.3 Joint1.3 Joint--Stock Company (Stock Company (Sociedade Sociedade AnônimaAnônima))

•• Main FeaturesMain Features

•• Each shareholder is liable only to the extent that the Each shareholder is liable only to the extent that the capital stock for which it has subscribed remains capital stock for which it has subscribed remains unpaid.unpaid.

•• May be formed by public or private subscription of May be formed by public or private subscription of shares. At least, 10% of the company’s capital shall be shares. At least, 10% of the company’s capital shall be fully paid in upon incorporation.fully paid in upon incorporation.

•• Securities of a closelySecurities of a closely--held company are not available held company are not available to the general market. to the general market.

•• Securities of a publiclySecurities of a publicly--held company may be traded on held company may be traded on the stock exchange or on the overthe stock exchange or on the over--thethe--counter market counter market (but only after 30% of the issue price has been paid) (but only after 30% of the issue price has been paid) and must be registered with the Brazilian Securities and must be registered with the Brazilian Securities Commission (CVM). Commission (CVM).

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

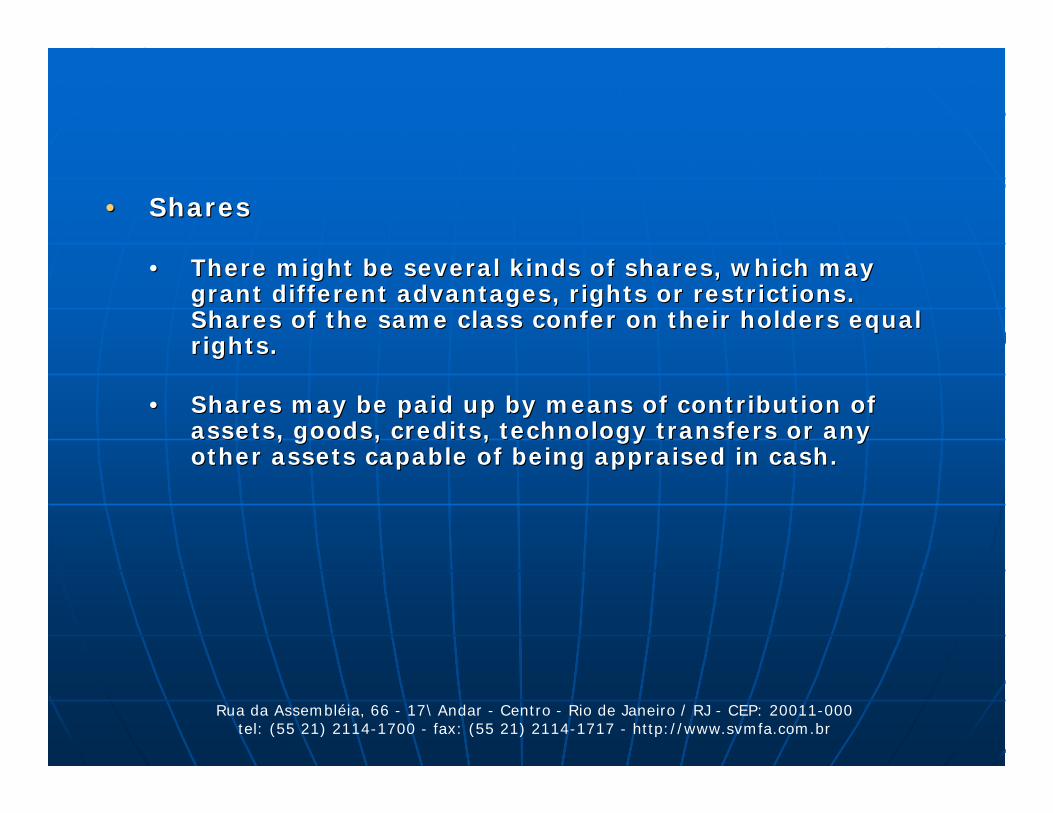

•• SharesShares

•• There might be several kinds of shares, which may There might be several kinds of shares, which may grant different advantages, rights or restrictions. grant different advantages, rights or restrictions. Shares of the same class confer on their holders equal Shares of the same class confer on their holders equal rights.rights.

•• Shares may be paid up by means of contribution of Shares may be paid up by means of contribution of assets, goods, credits, technology transfers or any assets, goods, credits, technology transfers or any other assets capable of being appraised in cash.other assets capable of being appraised in cash.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

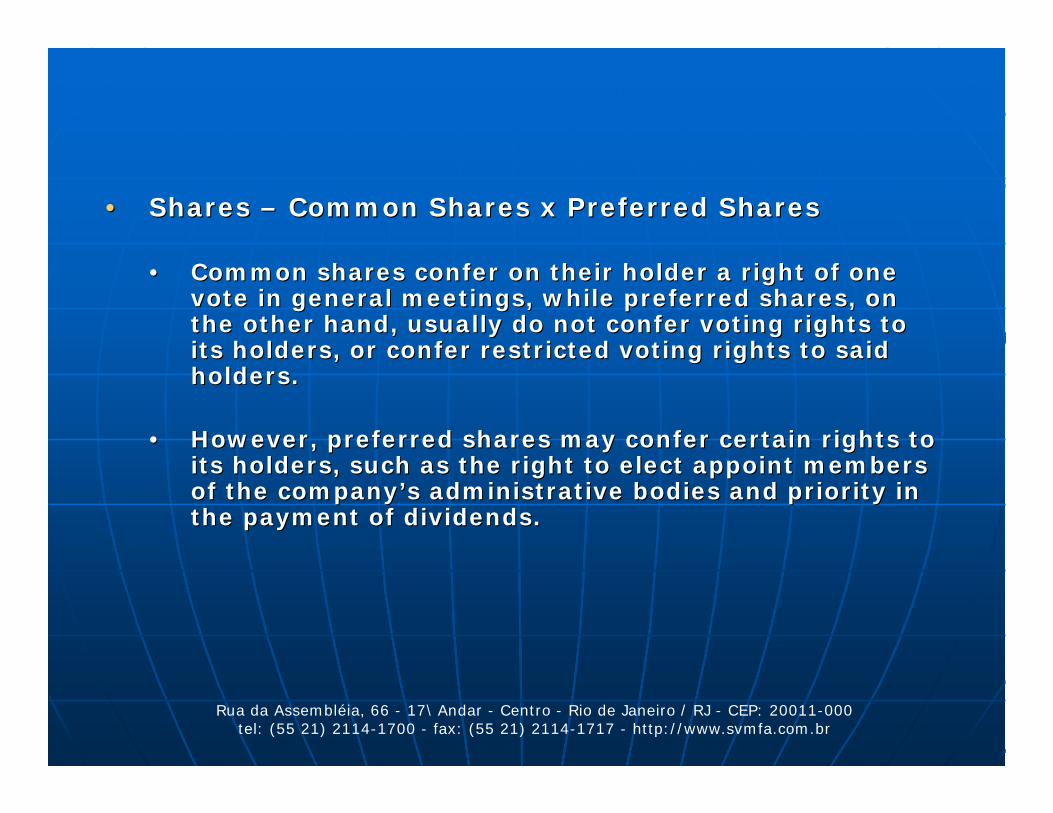

•• Shares Shares –– Common Shares x Preferred SharesCommon Shares x Preferred Shares

•• Common shares confer on their holder a right of one Common shares confer on their holder a right of one vote in general meetings, while preferred shares, on vote in general meetings, while preferred shares, on the other hand, usually do not confer voting rights to the other hand, usually do not confer voting rights to its holders, or confer restricted voting rights to said its holders, or confer restricted voting rights to said holders.holders.

•• However, preferred shares may confer certain rights to However, preferred shares may confer certain rights to its holders, such as the right to elect appoint members its holders, such as the right to elect appoint members of the company’s administrative bodies and priority in of the company’s administrative bodies and priority in the payment of dividends.the payment of dividends.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

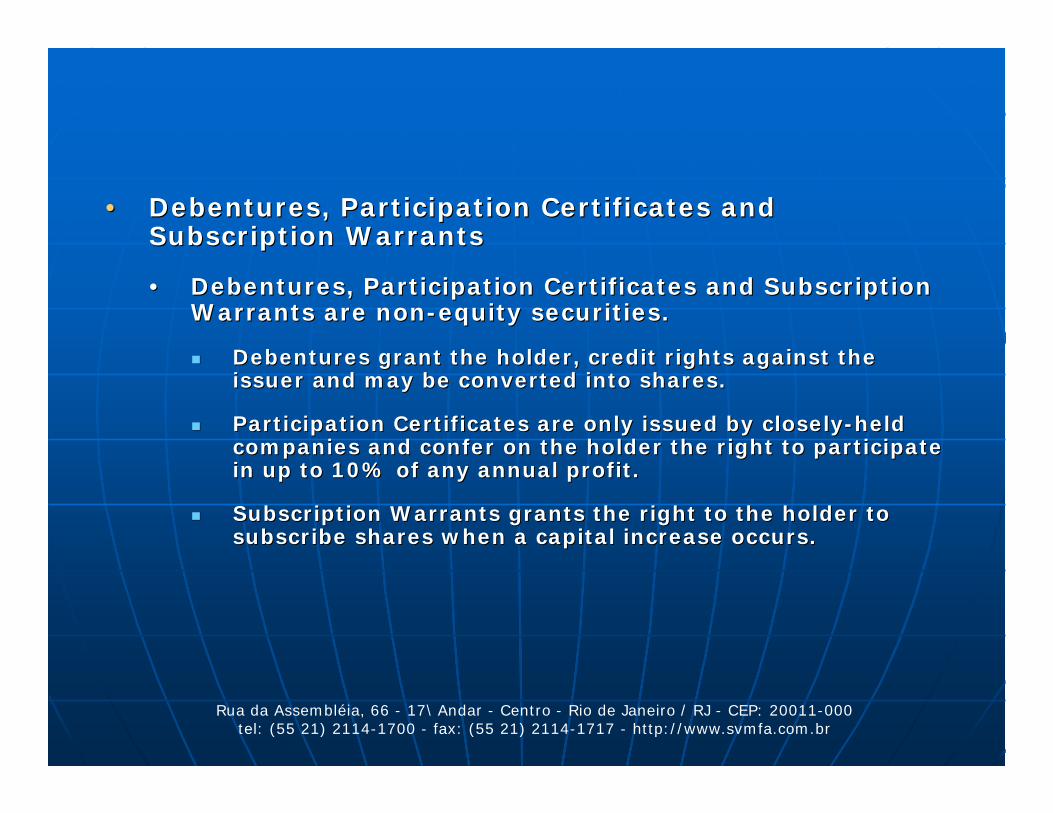

•• Debentures, Participation Certificates and Debentures, Participation Certificates and Subscription WarrantsSubscription Warrants

•• Debentures, Participation Certificates and Subscription Debentures, Participation Certificates and Subscription Warrants are nonWarrants are non--equity securities.equity securities.

Debentures grant the holder, credit rights against the Debentures grant the holder, credit rights against the issuer and may be converted into shares.issuer and may be converted into shares.

Participation Certificates are only issued by closelyParticipation Certificates are only issued by closely--held held companies and confer on the holder the right to participate companies and confer on the holder the right to participate in up to 10% of any annual profit.in up to 10% of any annual profit.

Subscription Warrants grants the right to the holder to Subscription Warrants grants the right to the holder to subscribe shares when a capital increase occurs.subscribe shares when a capital increase occurs.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

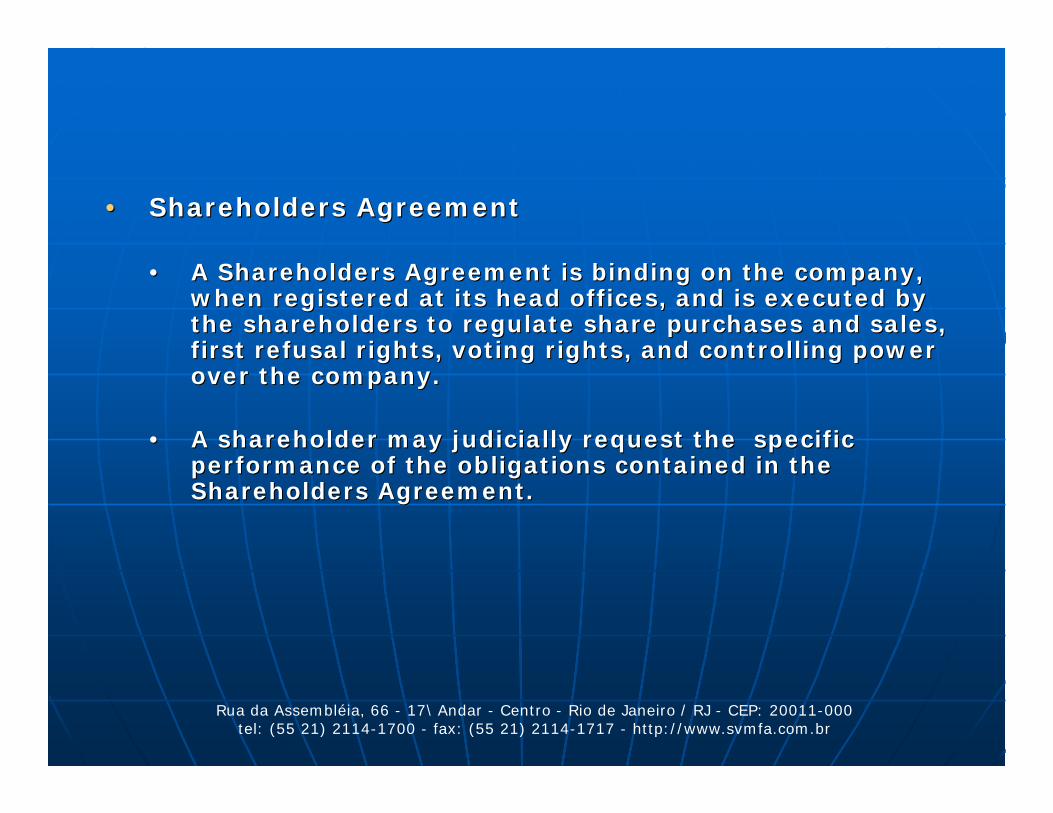

•• Shareholders AgreementShareholders Agreement

•• A Shareholders Agreement is binding on the company, A Shareholders Agreement is binding on the company, when registered at its head offices, and is executed by when registered at its head offices, and is executed by the shareholders to regulate share purchases and sales, the shareholders to regulate share purchases and sales, first refusal rights, voting rights, and controlling power first refusal rights, voting rights, and controlling power over the company.over the company.

•• A shareholder may judicially request the specific A shareholder may judicially request the specific performance of the obligations contained in the performance of the obligations contained in the Shareholders Agreement.Shareholders Agreement.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

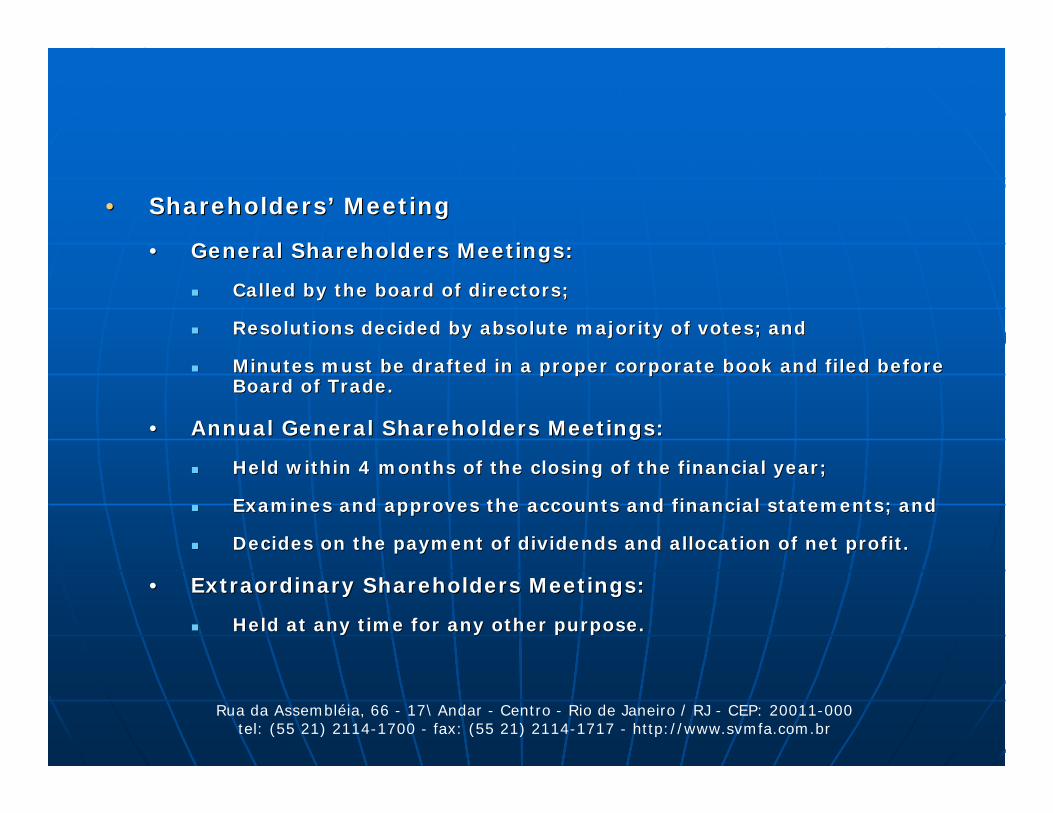

•• Shareholders’ MeetingShareholders’ Meeting

•• General Shareholders Meetings:General Shareholders Meetings:

Called by the board of directors;Called by the board of directors;

Resolutions decided by absolute majority of votes; andResolutions decided by absolute majority of votes; and

Minutes must be drafted in a proper corporate book and filed befMinutes must be drafted in a proper corporate book and filed before ore Board of Trade.Board of Trade.

•• Annual General Shareholders Meetings:Annual General Shareholders Meetings:

Held within 4 months of the closing of the financial year;Held within 4 months of the closing of the financial year;

Examines and approves the accounts and financial statements; andExamines and approves the accounts and financial statements; and

Decides on the payment of dividends and allocation of net profitDecides on the payment of dividends and allocation of net profit..

•• Extraordinary Shareholders Meetings:Extraordinary Shareholders Meetings:

Held at any time for any other purpose.Held at any time for any other purpose.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

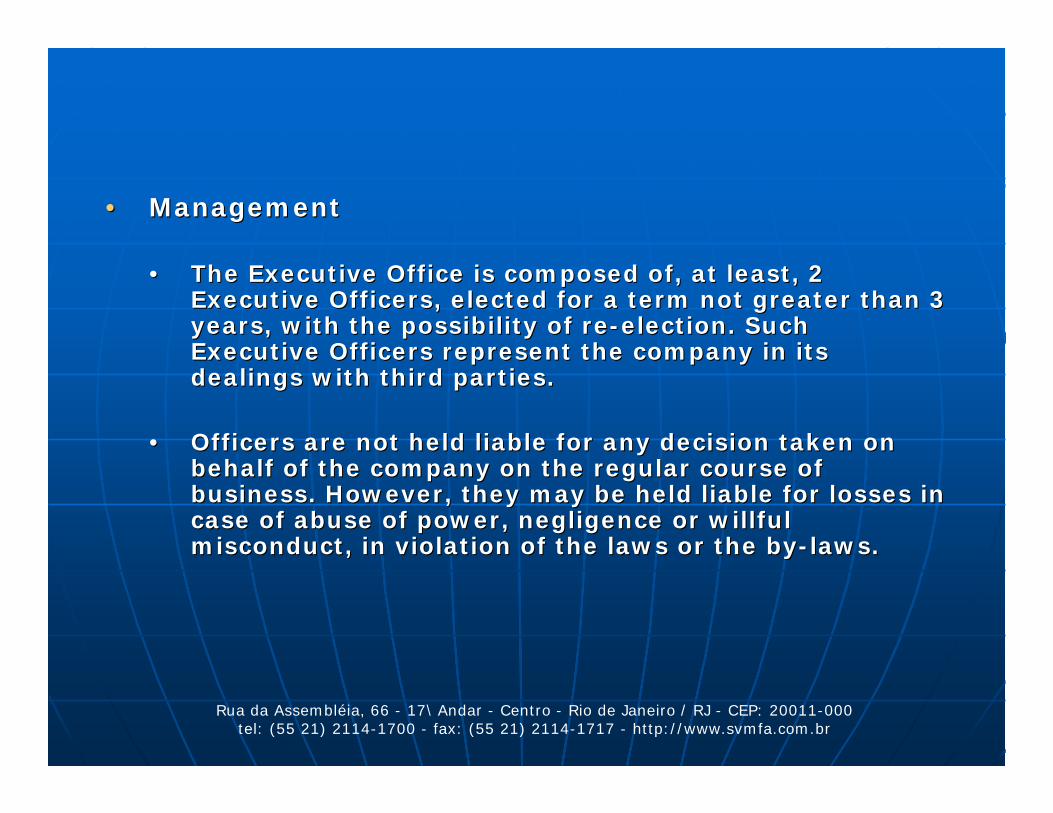

•• ManagementManagement

•• The Executive Office is composed of, at least, 2 The Executive Office is composed of, at least, 2 Executive Officers, elected for a term not greater than 3 Executive Officers, elected for a term not greater than 3 years, with the possibility of reyears, with the possibility of re--election. Such election. Such Executive Officers represent the company in its Executive Officers represent the company in its dealings with third parties.dealings with third parties.

•• Officers are not held liable for any decision taken on Officers are not held liable for any decision taken on behalf of the company on the regular course of behalf of the company on the regular course of business. However, they may be held liable for losses in business. However, they may be held liable for losses in case of abuse of power, negligence or willful case of abuse of power, negligence or willful misconduct, in violation of the laws or the bymisconduct, in violation of the laws or the by--laws. laws.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

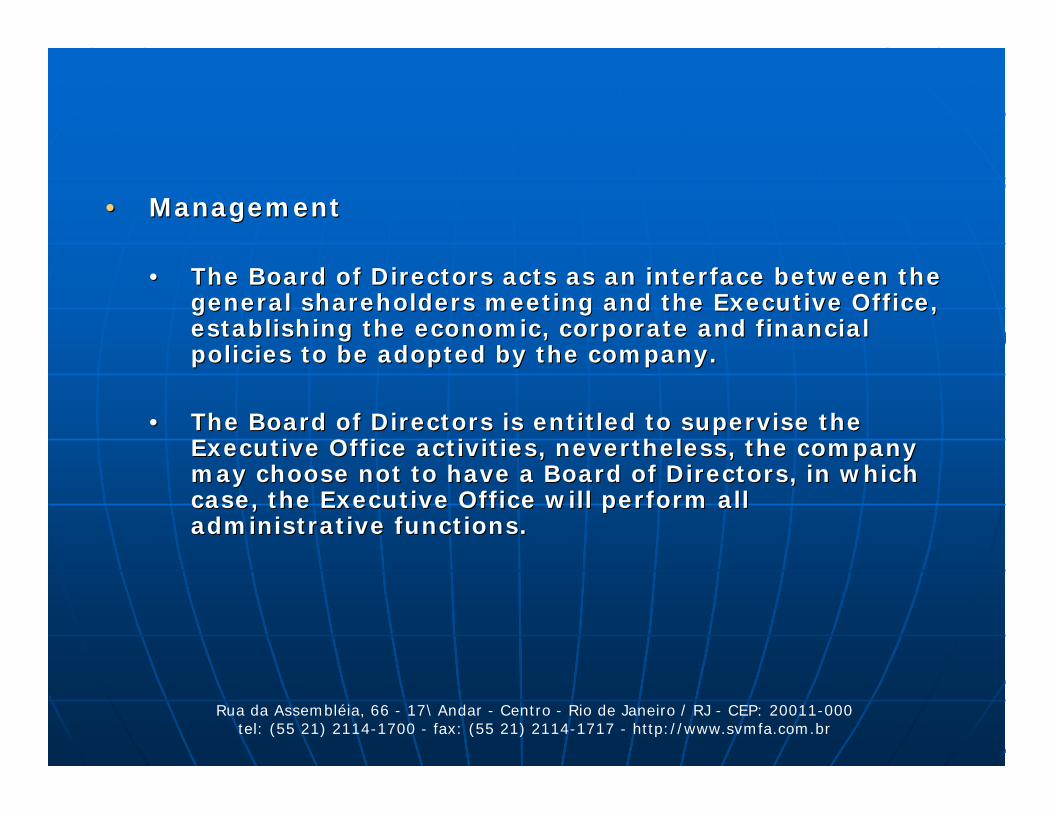

•• ManagementManagement

•• The Board of Directors acts as an interface between the The Board of Directors acts as an interface between the general shareholders meeting and the Executive Office, general shareholders meeting and the Executive Office, establishing the economic, corporate and financial establishing the economic, corporate and financial policies to be adopted by the company.policies to be adopted by the company.

•• The Board of Directors is entitled to supervise the The Board of Directors is entitled to supervise the Executive Office activities, nevertheless, the company Executive Office activities, nevertheless, the company may choose not to have a Board of Directors, in which may choose not to have a Board of Directors, in which case, the Executive Office will perform all case, the Executive Office will perform all administrative functions.administrative functions.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

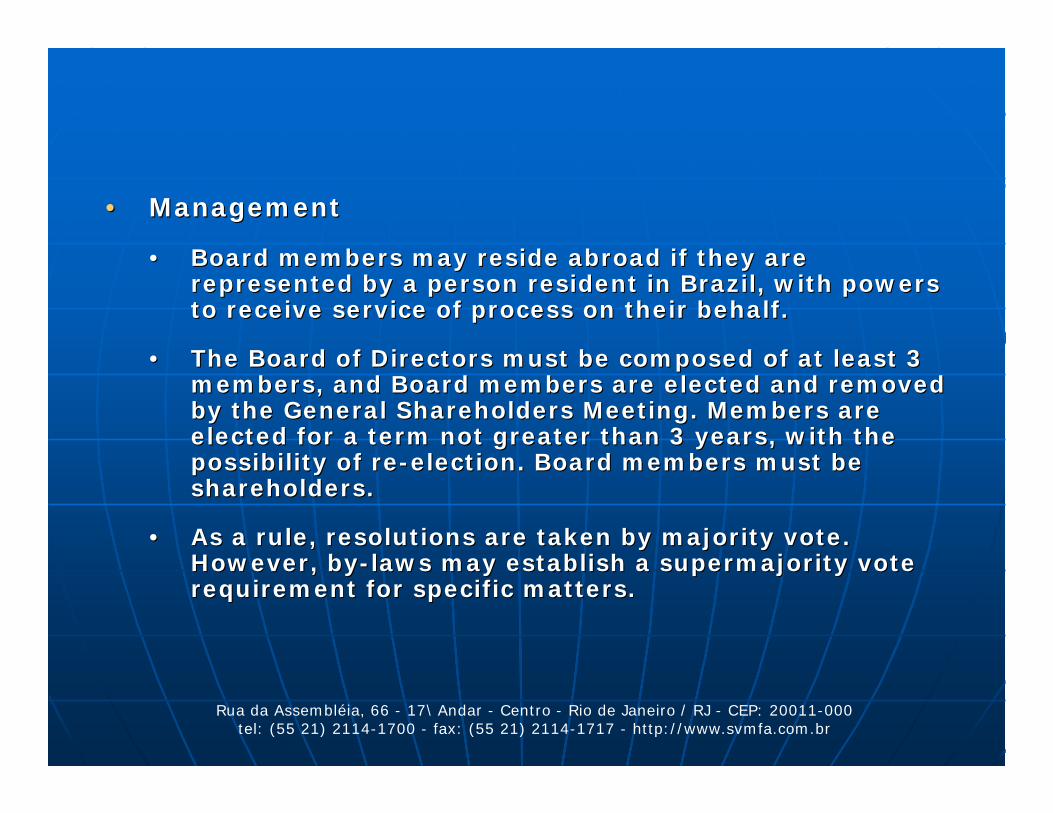

•• ManagementManagement

•• Board members may reside abroad if they are Board members may reside abroad if they are represented by a person resident in Brazil, with powers represented by a person resident in Brazil, with powers to receive service of process on their behalf.to receive service of process on their behalf.

•• The Board of Directors must be composed of at least 3 The Board of Directors must be composed of at least 3 members, and Board members are elected and removed members, and Board members are elected and removed by the General Shareholders Meeting. Members are by the General Shareholders Meeting. Members are elected for a term not greater than 3 years, with the elected for a term not greater than 3 years, with the possibility of repossibility of re--election. Board members must be election. Board members must be shareholders.shareholders.

•• As a rule, resolutions are taken by majority vote. As a rule, resolutions are taken by majority vote. However, byHowever, by--laws may establish a supermajority vote laws may establish a supermajority vote requirement for specific matters.requirement for specific matters.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

•• ManagementManagement

•• The Audit Committee must be mandatorily instated, The Audit Committee must be mandatorily instated, however, it is not required to operate on a permanent however, it is not required to operate on a permanent basis. The Audit Committee is composed of 3 to 5 basis. The Audit Committee is composed of 3 to 5 members (shareholders or not) and an equal number of members (shareholders or not) and an equal number of alternates.alternates.

•• The Audit Committee monitors the Senior Managers and The Audit Committee monitors the Senior Managers and informs the General Meeting accordingly.informs the General Meeting accordingly.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

1.4.1.4. Consortium Consortium –– Unincorporated jointUnincorporated joint--ventureventure

•• Corporate Law (Law 6.404/76) Corporate Law (Law 6.404/76) –– Arts. 278/279Arts. 278/279

•• Consortium AgreementConsortium Agreement

•• Rights and obligationsRights and obligations

•• Management (lidership)Management (lidership)

•• Participation Participation

•• PublicityPublicity

•• No joint liabilityNo joint liability

•• Petroleum Law (Law 9.748/97) Petroleum Law (Law 9.748/97) –– E&P activitiesE&P activities

•• Consortium Agreement/JOAConsortium Agreement/JOA

•• Construction and operation of Infrastructure ProjectsConstruction and operation of Infrastructure Projects

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

QuestionsQuestions

•• AAcquisition of shares, quotas or participationcquisition of shares, quotas or participation

•• Formation of a new entityFormation of a new entity

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

Thank You!Thank You!

Antonio Luis FerreiraAntonio Luis Ferreira

Schmidt, Valois, Miranda, Ferreira & Agel AdvogadosSchmidt, Valois, Miranda, Ferreira & Agel Advogados

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

Divestiture of Divestiture of Investments In BrazilInvestments In Brazil

Guilherme SchmidtGuilherme SchmidtSchmidt, Valois, Miranda, Ferreira & Agel AdvogadosSchmidt, Valois, Miranda, Ferreira & Agel Advogados

November 9, 2011November 9, 2011

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

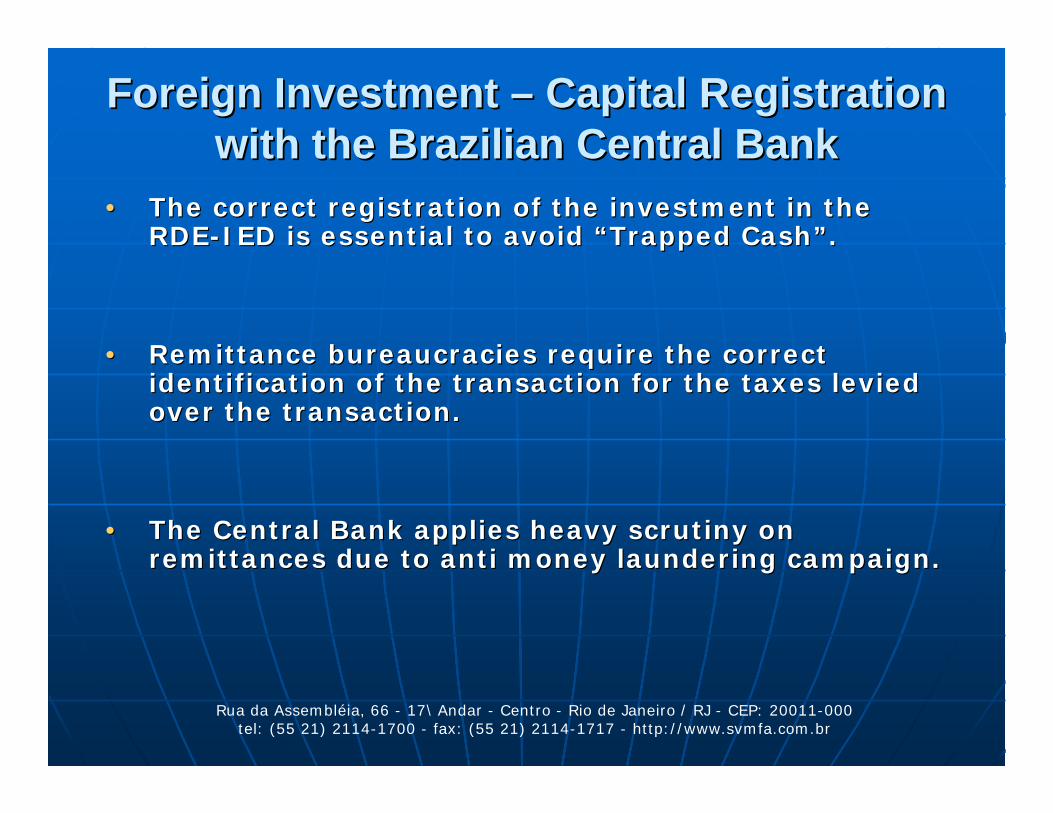

Foreign Investment Foreign Investment –– Capital Registration Capital Registration with the Brazilian Central Bankwith the Brazilian Central Bank

•• The correct registration of the investment in the The correct registration of the investment in the RDERDE--IED is essential to avoid “Trapped Cash”.IED is essential to avoid “Trapped Cash”.

•• Remittance bureaucracies require the correct Remittance bureaucracies require the correct identification of the transaction for the taxes levied identification of the transaction for the taxes levied over the transaction.over the transaction.

•• The Central Bank applies heavy scrutiny on The Central Bank applies heavy scrutiny on remittances due to anti money laundering campaign.remittances due to anti money laundering campaign.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

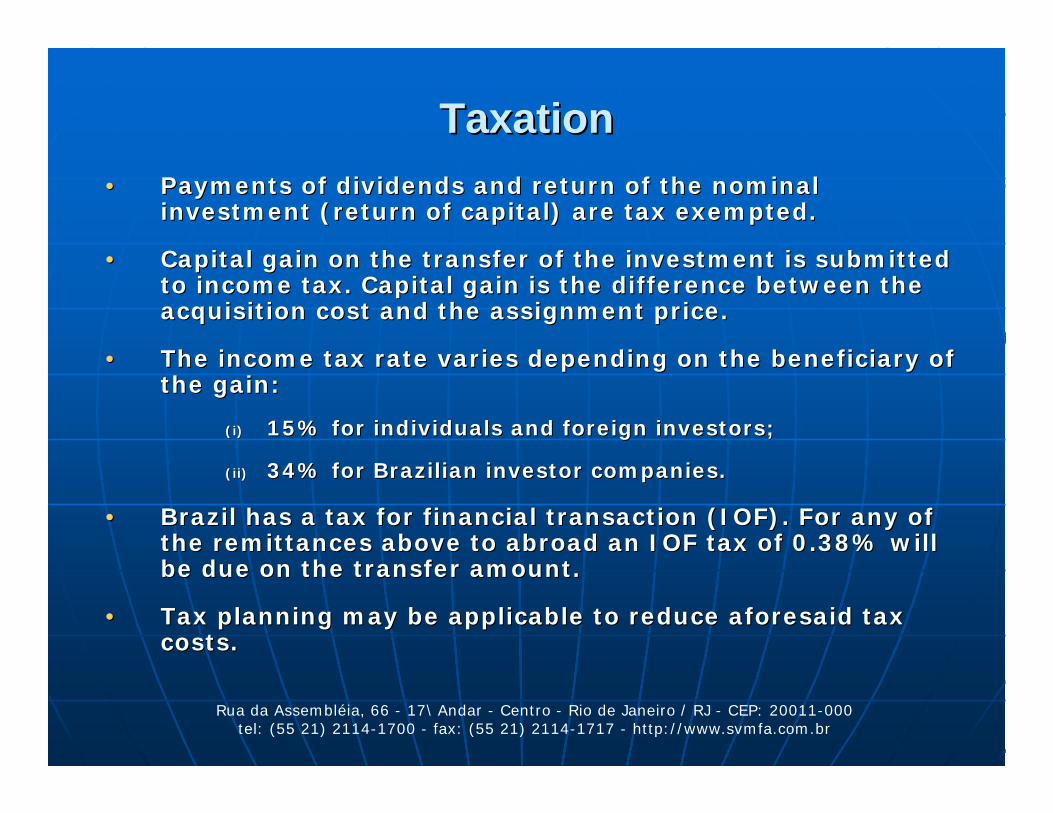

TaxationTaxation•• Payments of dividends and return of the nominal Payments of dividends and return of the nominal

investment (return of capital) are tax exempted.investment (return of capital) are tax exempted.

•• Capital gain on the transfer of the investment is submitted Capital gain on the transfer of the investment is submitted to income tax. Capital gain is the difference between the to income tax. Capital gain is the difference between the acquisition cost and the assignment price.acquisition cost and the assignment price.

•• The income tax rate varies depending on the beneficiary of The income tax rate varies depending on the beneficiary of the gain:the gain:

(i)(i) 15% for individuals and foreign investors;15% for individuals and foreign investors;

(ii)(ii) 34% for Brazilian investor companies. 34% for Brazilian investor companies.

•• Brazil has a tax for financial transaction (IOF). For any of Brazil has a tax for financial transaction (IOF). For any of the remittances above to abroad an IOF tax of 0.38% will the remittances above to abroad an IOF tax of 0.38% will be due on the transfer amount.be due on the transfer amount.

•• Tax planning may be applicable to reduce aforesaid tax Tax planning may be applicable to reduce aforesaid tax costs.costs.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

Capital Markets Divestiture Capital Markets Divestiture –– Selling the Selling the Control of a Listed Brazilian Company Control of a Listed Brazilian Company

•• Severe rules regarding divulging material facts on Severe rules regarding divulging material facts on the transfer of control the transfer of control –– CVM’s Rule 358.CVM’s Rule 358.

•• The transfer of control triggers the obligation for the The transfer of control triggers the obligation for the new controlling shareholder to perform a Tag Along new controlling shareholder to perform a Tag Along Offer in favor of the minority shareholders holding Offer in favor of the minority shareholders holding common shares common shares –– The Offering Purchase Price shall The Offering Purchase Price shall be at least 80% of the price paid for the shares held be at least 80% of the price paid for the shares held by the divesting controlling shareholders.by the divesting controlling shareholders.

•• For Companies listed in Special Governance Rules For Companies listed in Special Governance Rules such as the New Market the price shall be 100% of such as the New Market the price shall be 100% of the price paid for the shares held by the divesting the price paid for the shares held by the divesting controlling shareholders.controlling shareholders.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

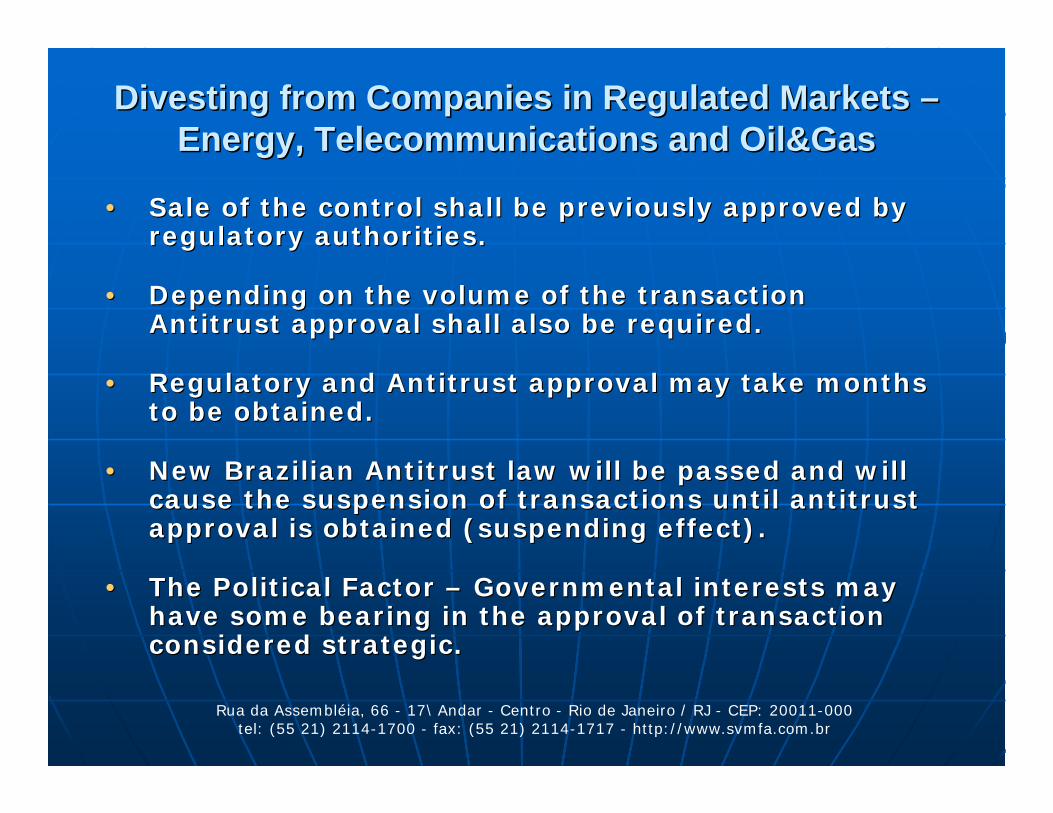

Divesting from Companies in Regulated Markets Divesting from Companies in Regulated Markets ––Energy, Telecommunications and Oil&GasEnergy, Telecommunications and Oil&Gas

•• Sale of the control shall be previously approved by Sale of the control shall be previously approved by regulatory authorities.regulatory authorities.

•• Depending on the volume of the transaction Depending on the volume of the transaction Antitrust approval shall also be required.Antitrust approval shall also be required.

•• Regulatory and Antitrust approval may take months Regulatory and Antitrust approval may take months to be obtained.to be obtained.

•• New Brazilian Antitrust law will be passed and will New Brazilian Antitrust law will be passed and will cause the suspension of transactions until antitrust cause the suspension of transactions until antitrust approval is obtained (suspending effect).approval is obtained (suspending effect).

•• The Political Factor The Political Factor –– Governmental interests may Governmental interests may have some bearing in the approval of transaction have some bearing in the approval of transaction considered strategic.considered strategic.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

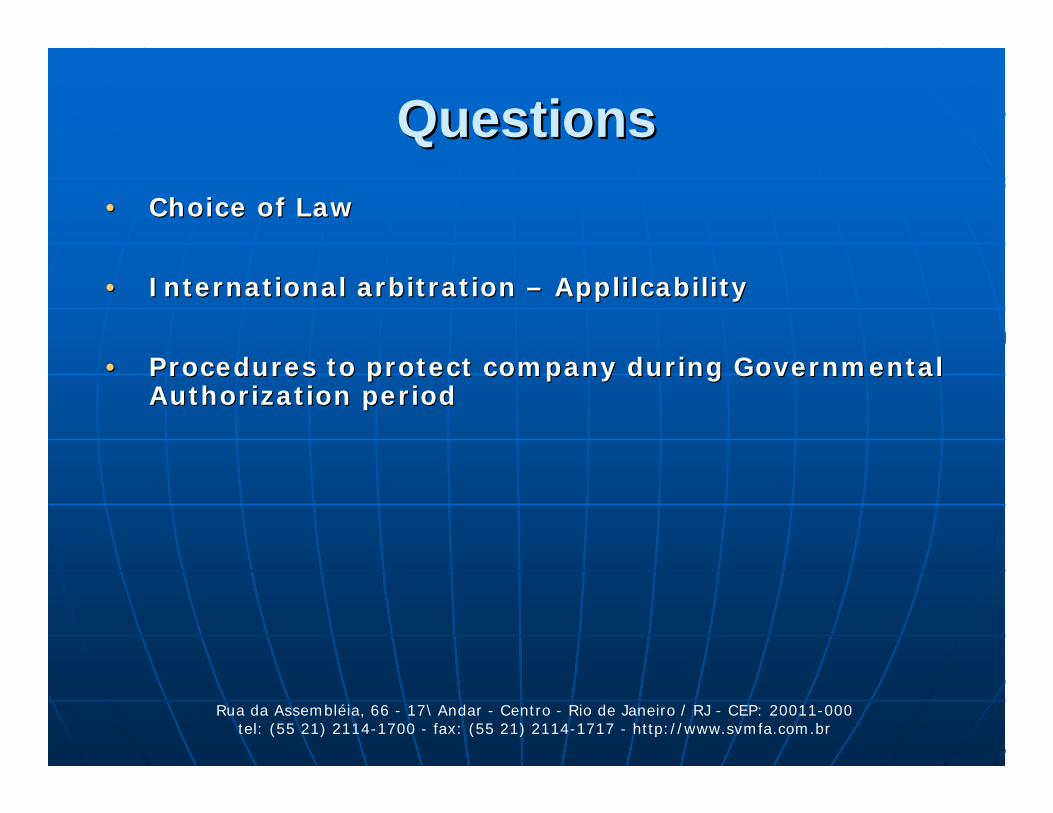

QuestionsQuestions•• Choice of LawChoice of Law

•• International arbitration International arbitration –– ApplilcabilityApplilcability

•• Procedures to protect company during Governmental Procedures to protect company during Governmental Authorization periodAuthorization period

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

Thank You!Thank You!

Guilherme SchmidtGuilherme SchmidtSchmidt, Valois, Miranda, Ferreira & Agel AdvogadosSchmidt, Valois, Miranda, Ferreira & Agel Advogados

Opportunities for Service Providers from the

New BNDES FacilityPresented by

Nara [email protected]

November 9, 2011

The Brazilian Development Bank

The Brazilian Development Bank – BNDESfinancing program to the oil and gas supply chain (“BNDES P&G”) was issued in August of 2011 under the new Brazilian industrial policy, Bigger Brazil Plan (in Portuguese, Plano Brasil Maior).

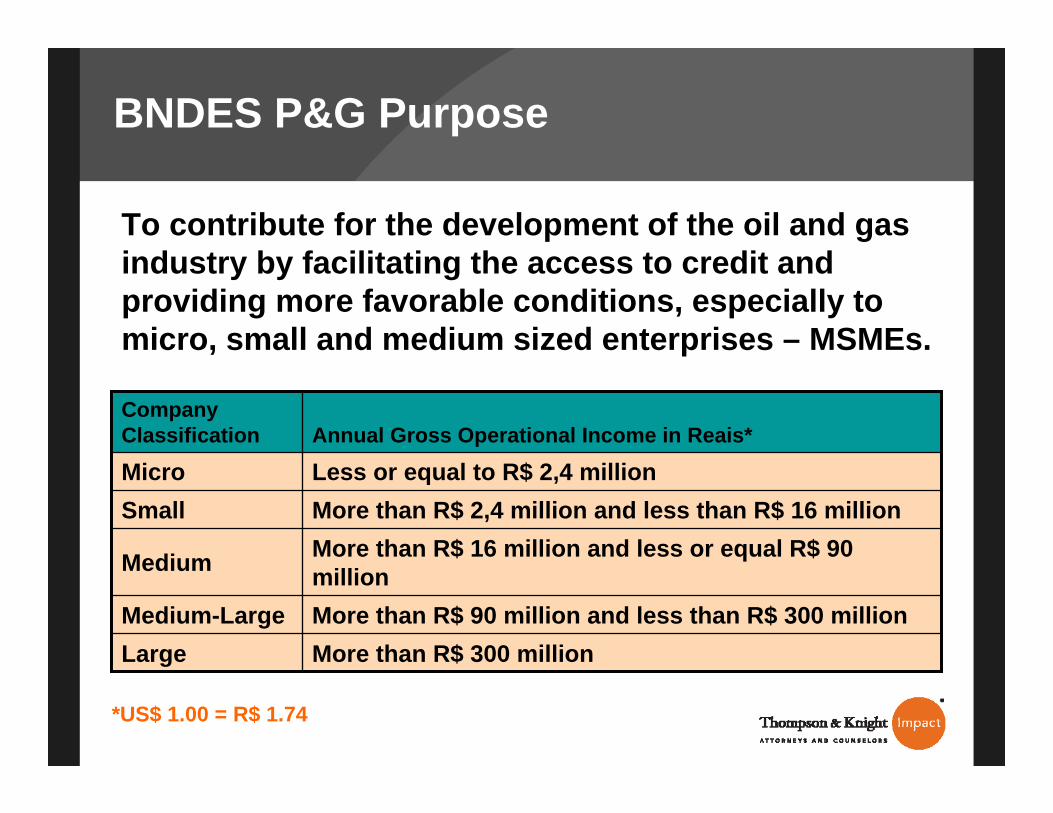

BNDES P&G Purpose

To contribute for the development of the oil and gas industry by facilitating the access to credit and providing more favorable conditions, especially to micro, small and medium sized enterprises – MSMEs.

More than R$ 300 millionLargeMore than R$ 90 million and less than R$ 300 millionMedium-Large

More than R$ 16 million and less or equal R$ 90 millionMedium

More than R$ 2,4 million and less than R$ 16 millionSmallLess or equal to R$ 2,4 millionMicroAnnual Gross Operational Income in Reais*

Company Classification

*US$ 1.00 = R$ 1.74

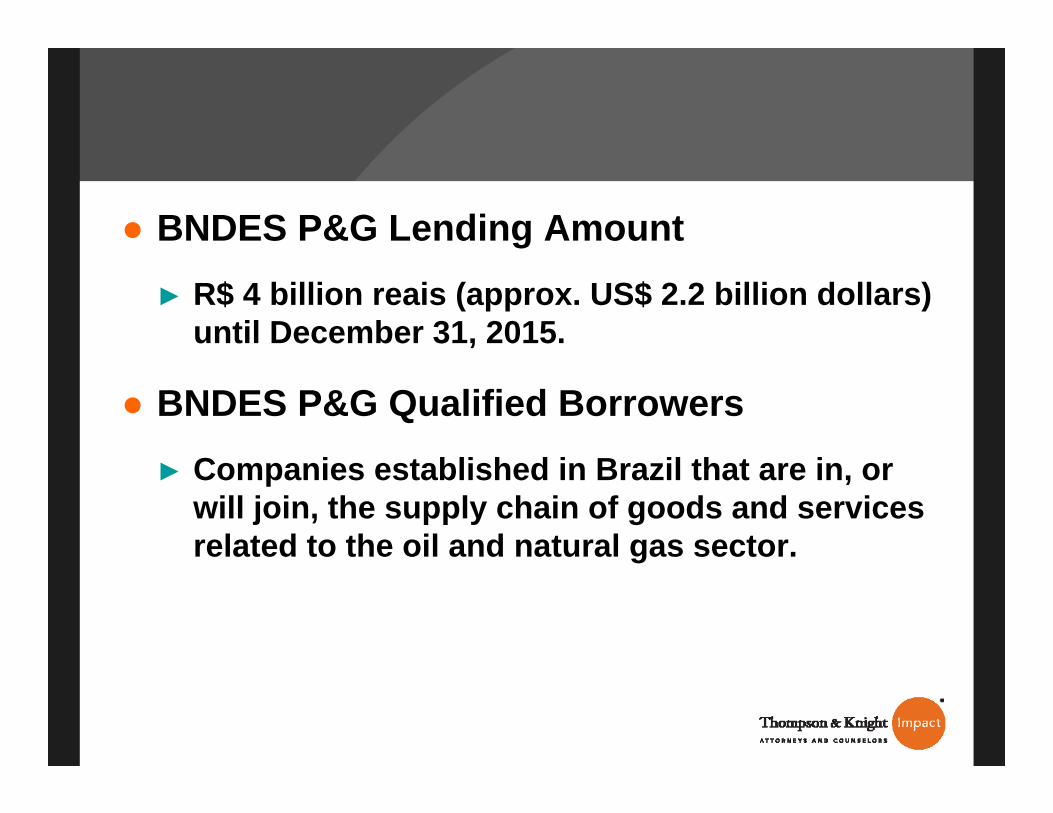

● BNDES P&G Lending Amount► R$ 4 billion reais (approx. US$ 2.2 billion dollars)

until December 31, 2015.

● BNDES P&G Qualified Borrowers► Companies established in Brazil that are in, or

will join, the supply chain of goods and services related to the oil and natural gas sector.

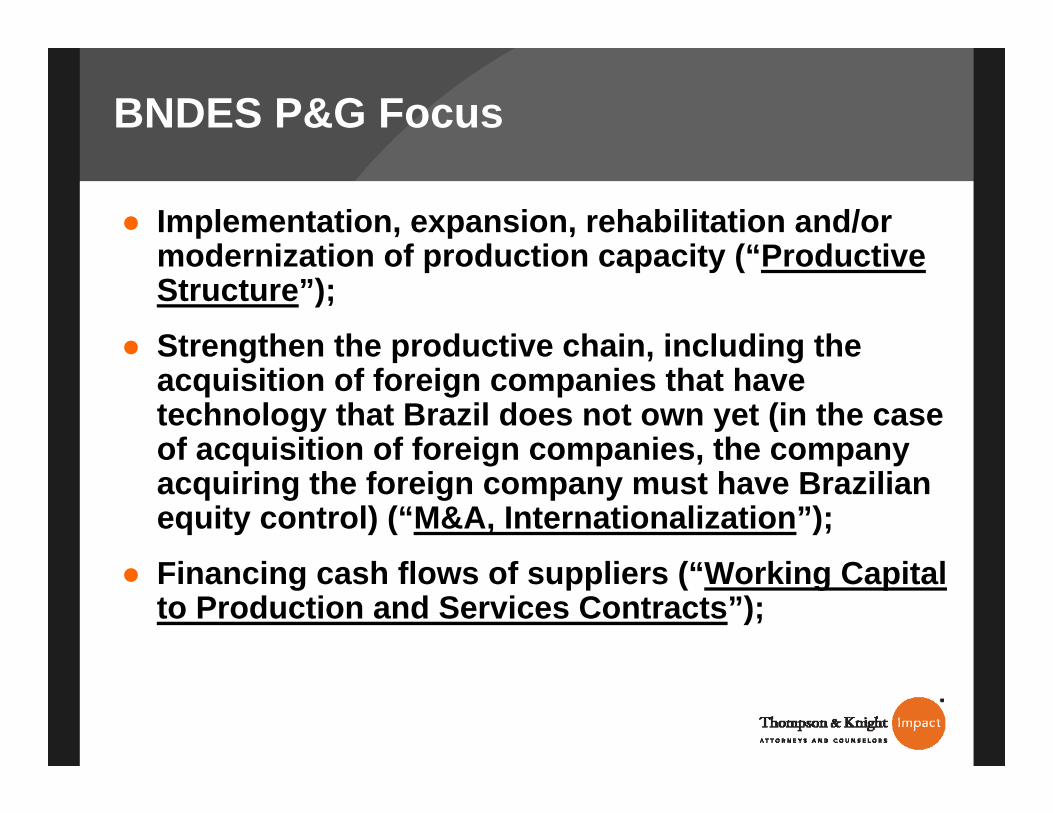

BNDES P&G Focus

● Implementation, expansion, rehabilitation and/or modernization of production capacity (“Productive Structure”);

● Strengthen the productive chain, including the acquisition of foreign companies that have technology that Brazil does not own yet (in the case of acquisition of foreign companies, the company acquiring the foreign company must have Brazilian equity control) (“M&A, Internationalization”);

● Financing cash flows of suppliers (“Working Capital to Production and Services Contracts”);

BNDES P&G Focus

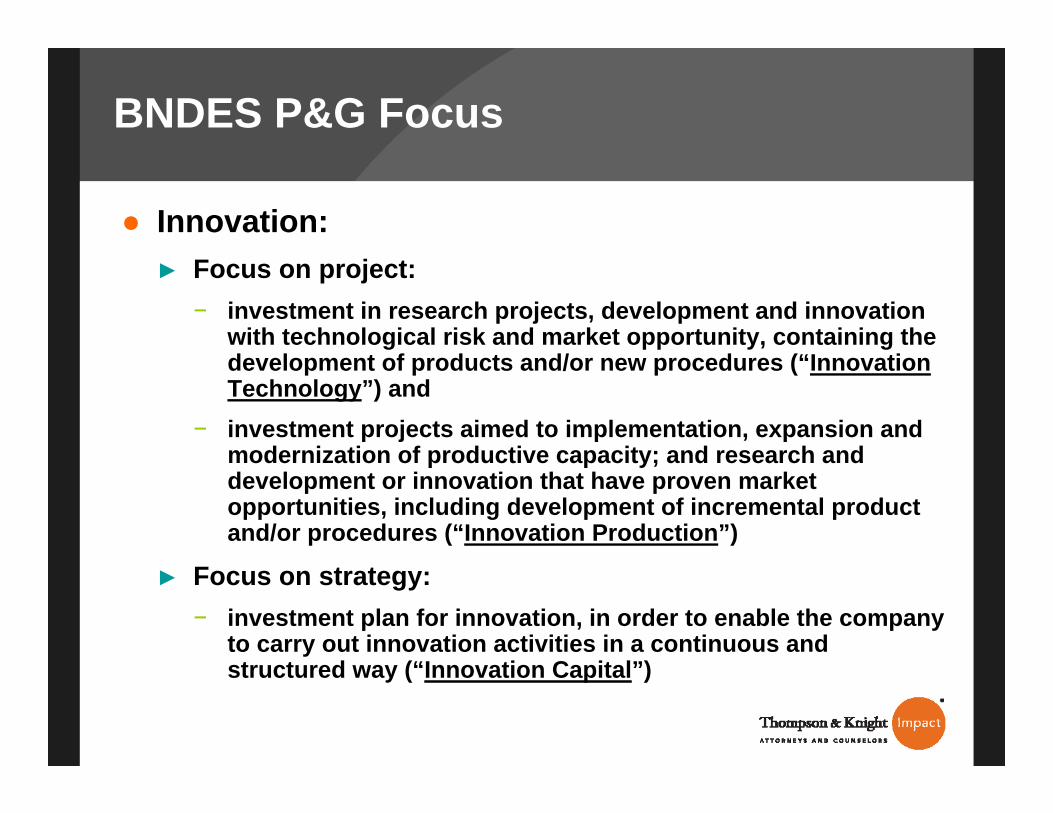

● Innovation:► Focus on project:

− investment in research projects, development and innovation with technological risk and market opportunity, containing the development of products and/or new procedures (“Innovation Technology”) and

− investment projects aimed to implementation, expansion and modernization of productive capacity; and research and development or innovation that have proven market opportunities, including development of incremental product and/or procedures (“Innovation Production”)

► Focus on strategy:− investment plan for innovation, in order to enable the company

to carry out innovation activities in a continuous and structured way (“Innovation Capital”)

BNDES P&G Procedure

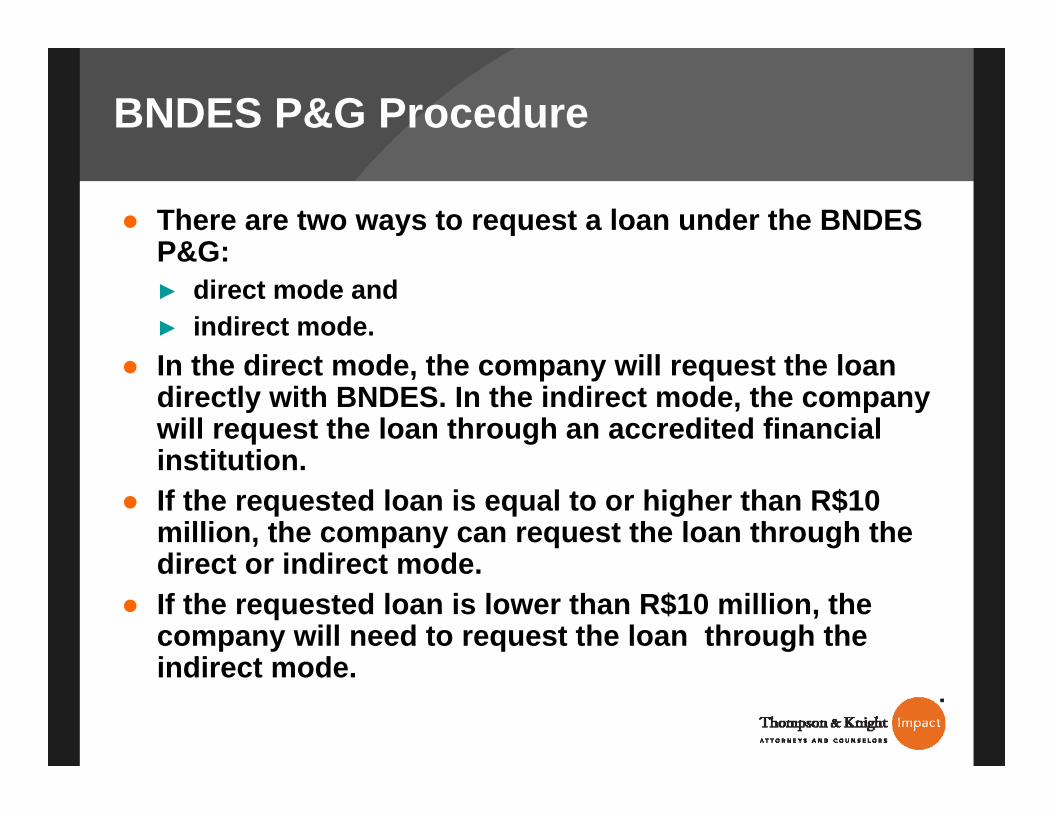

● There are two ways to request a loan under the BNDES P&G:► direct mode and► indirect mode.

● In the direct mode, the company will request the loan directly with BNDES. In the indirect mode, the company will request the loan through an accredited financial institution.

● If the requested loan is equal to or higher than R$10 million, the company can request the loan through the direct or indirect mode.

● If the requested loan is lower than R$10 million, the company will need to request the loan through the indirect mode.

BNDES P&G Procedure (cont.)

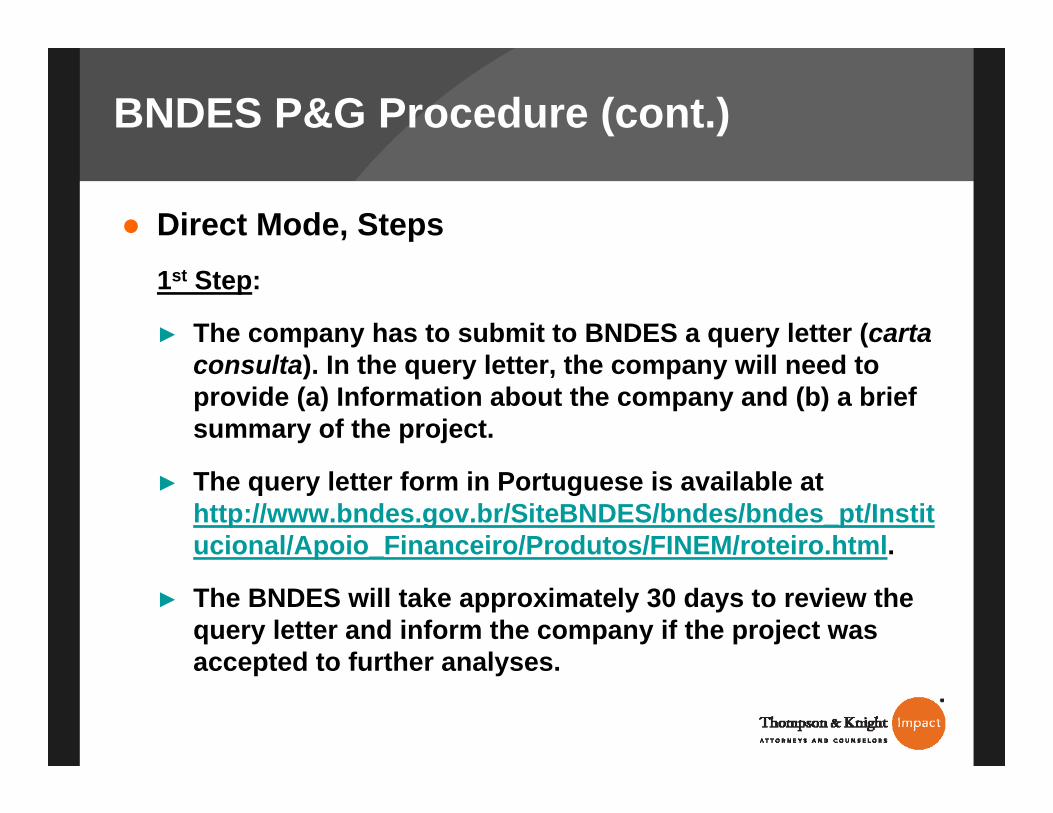

● Direct Mode, Steps1st Step:

► The company has to submit to BNDES a query letter (carta consulta). In the query letter, the company will need to provide (a) Information about the company and (b) a brief summary of the project.

► The query letter form in Portuguese is available at http://www.bndes.gov.br/SiteBNDES/bndes/bndes_pt/Institucional/Apoio_Financeiro/Produtos/FINEM/roteiro.html.

► The BNDES will take approximately 30 days to review the query letter and inform the company if the project was accepted to further analyses.

BNDES P&G Procedure (cont.)

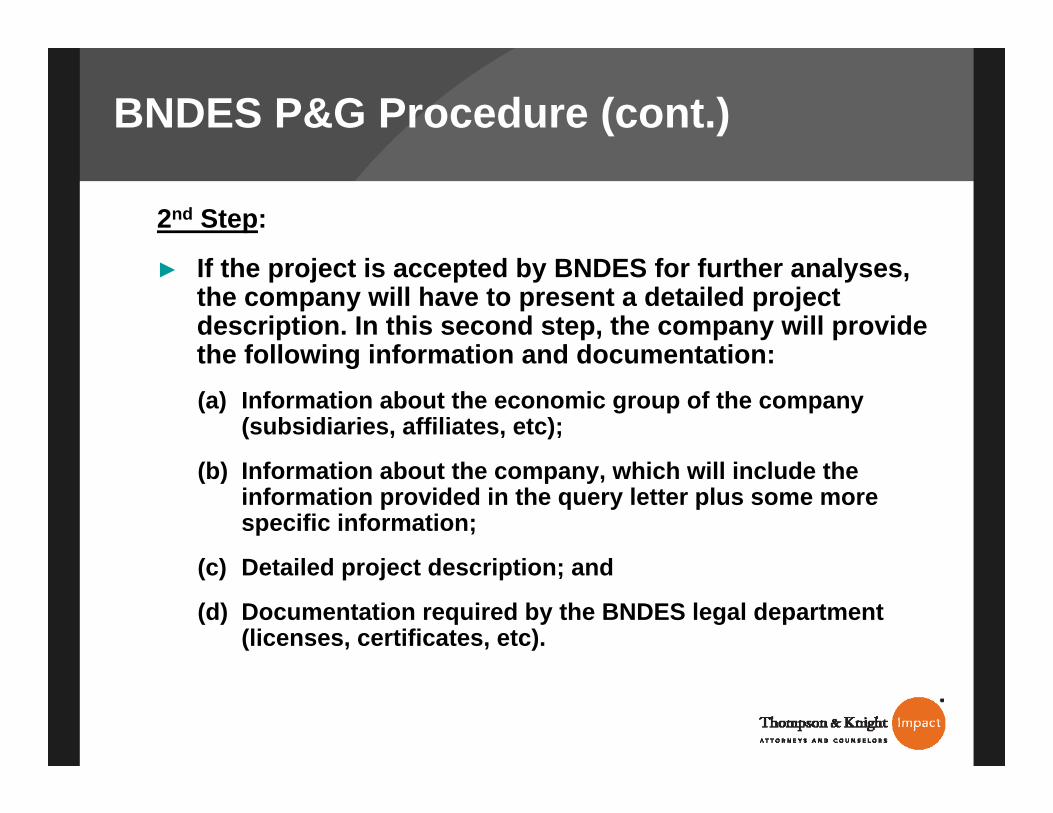

2nd Step:

► If the project is accepted by BNDES for further analyses, the company will have to present a detailed project description. In this second step, the company will provide the following information and documentation: (a) Information about the economic group of the company

(subsidiaries, affiliates, etc);

(b) Information about the company, which will include the information provided in the query letter plus some more specific information;

(c) Detailed project description; and

(d) Documentation required by the BNDES legal department (licenses, certificates, etc).

BNDES P&G Procedure (cont.)

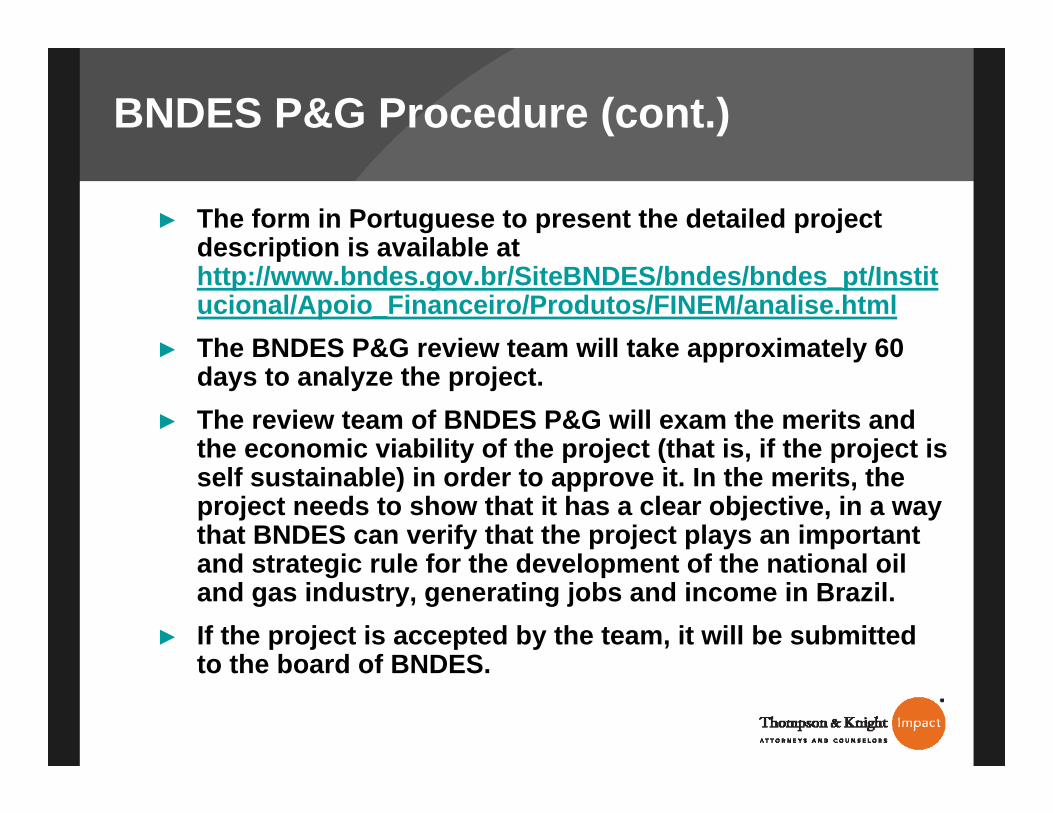

► The form in Portuguese to present the detailed project description is available at http://www.bndes.gov.br/SiteBNDES/bndes/bndes_pt/Institucional/Apoio_Financeiro/Produtos/FINEM/analise.html

► The BNDES P&G review team will take approximately 60 days to analyze the project.

► The review team of BNDES P&G will exam the merits and the economic viability of the project (that is, if the project is self sustainable) in order to approve it. In the merits, the project needs to show that it has a clear objective, in a way that BNDES can verify that the project plays an important and strategic rule for the development of the national oil and gas industry, generating jobs and income in Brazil.

► If the project is accepted by the team, it will be submitted to the board of BNDES.

BNDES P&G Procedure (cont.)

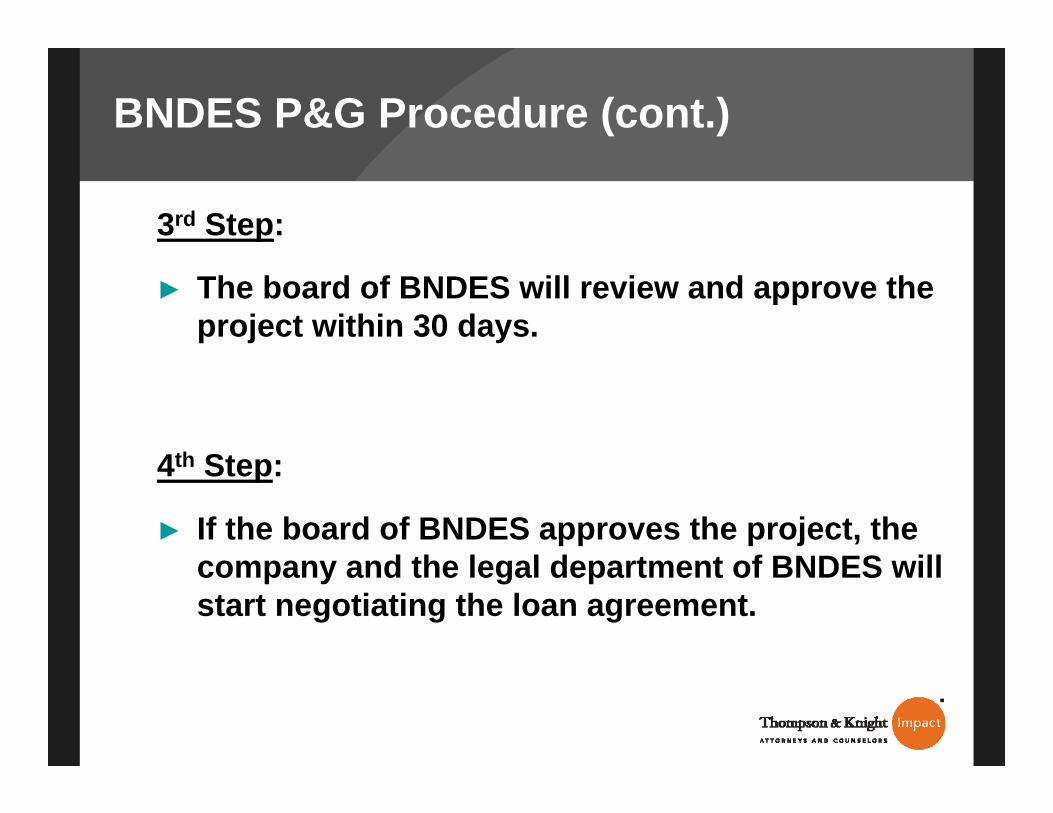

3rd Step:

► The board of BNDES will review and approve the project within 30 days.

4th Step:

► If the board of BNDES approves the project, the company and the legal department of BNDES will start negotiating the loan agreement.

BNDES P&G Procedure (cont.)

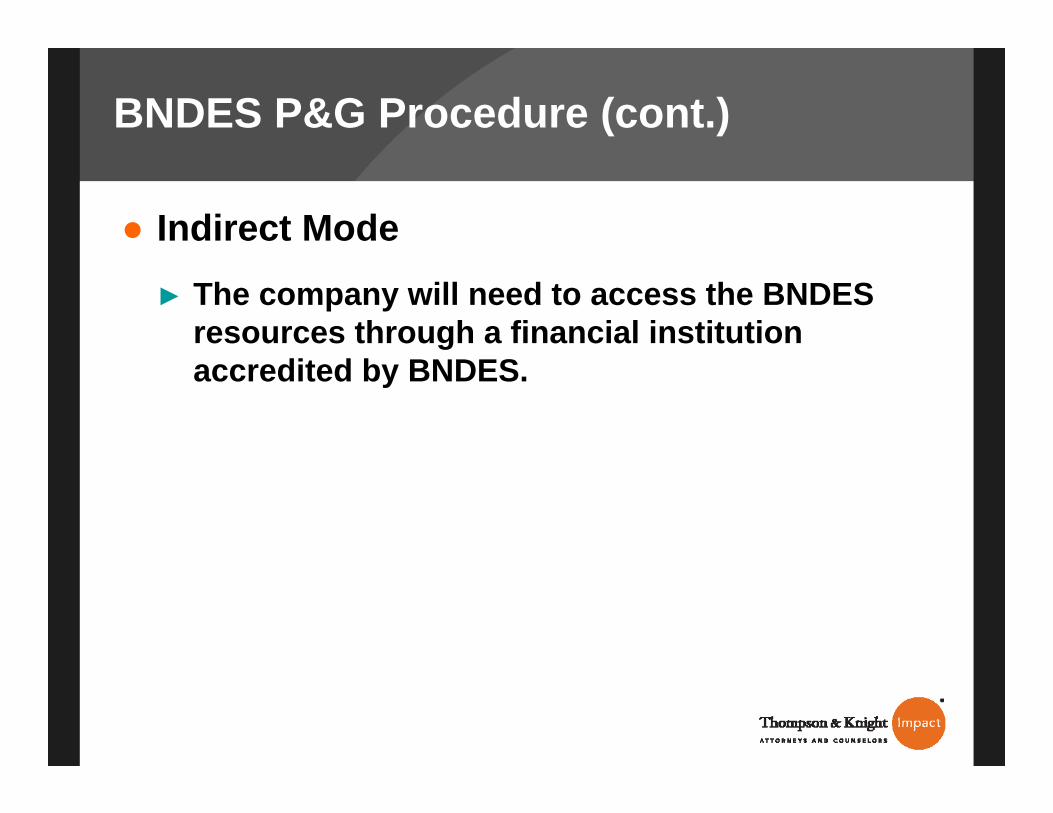

● Indirect Mode► The company will need to access the BNDES

resources through a financial institution accredited by BNDES.

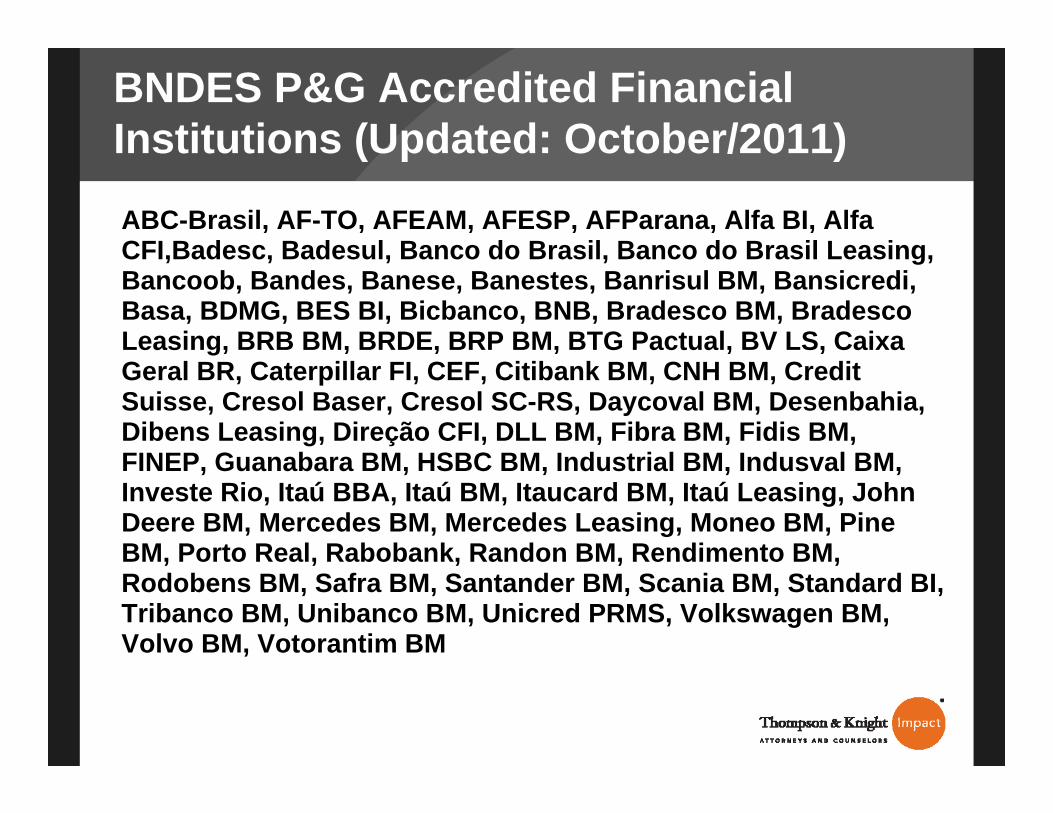

BNDES P&G Accredited Financial Institutions (Updated: October/2011)

ABC-Brasil, AF-TO, AFEAM, AFESP, AFParana, Alfa BI, Alfa CFI,Badesc, Badesul, Banco do Brasil, Banco do Brasil Leasing, Bancoob, Bandes, Banese, Banestes, Banrisul BM, Bansicredi, Basa, BDMG, BES BI, Bicbanco, BNB, Bradesco BM, BradescoLeasing, BRB BM, BRDE, BRP BM, BTG Pactual, BV LS, CaixaGeral BR, Caterpillar FI, CEF, Citibank BM, CNH BM, Credit Suisse, Cresol Baser, Cresol SC-RS, Daycoval BM, Desenbahia, Dibens Leasing, Direção CFI, DLL BM, Fibra BM, Fidis BM, FINEP, Guanabara BM, HSBC BM, Industrial BM, Indusval BM, Investe Rio, Itaú BBA, Itaú BM, Itaucard BM, Itaú Leasing, John Deere BM, Mercedes BM, Mercedes Leasing, Moneo BM, Pine BM, Porto Real, Rabobank, Randon BM, Rendimento BM, Rodobens BM, Safra BM, Santander BM, Scania BM, Standard BI, Tribanco BM, Unibanco BM, Unicred PRMS, Volkswagen BM, Volvo BM, Votorantim BM

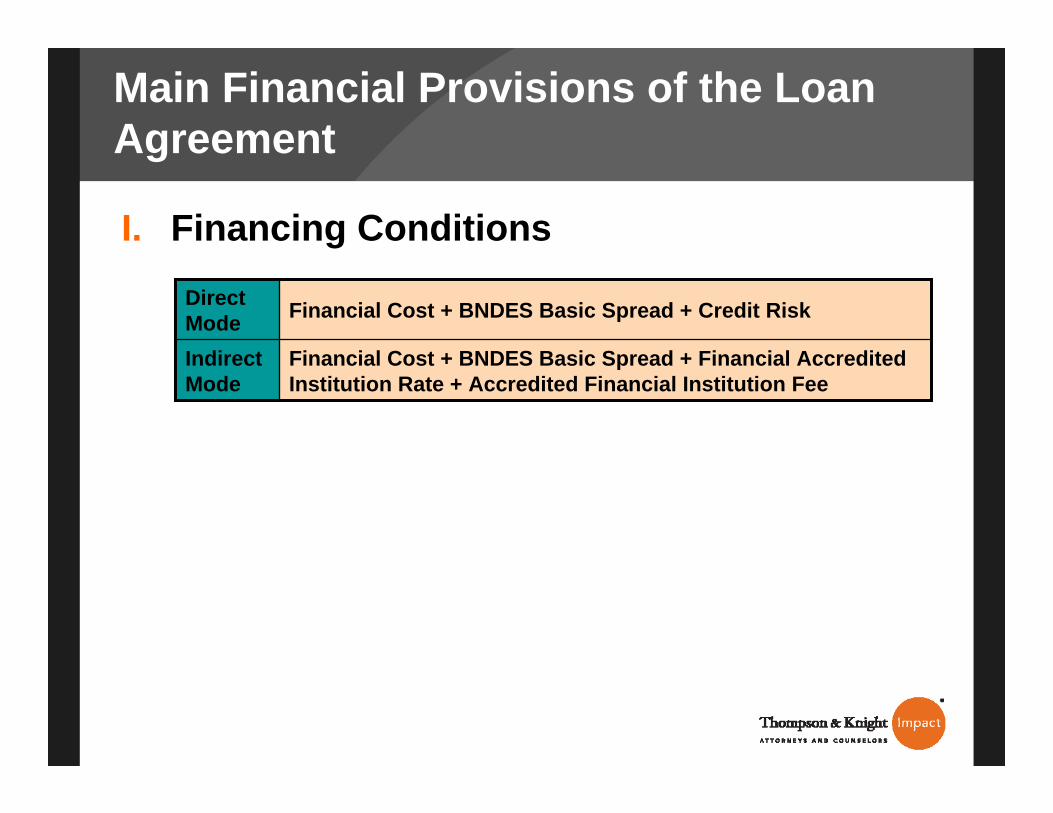

Main Financial Provisions of the Loan Agreement

I. Financing Conditions

Financial Cost + BNDES Basic Spread + Financial Accredited Institution Rate + Accredited Financial Institution Fee

Indirect Mode

Financial Cost + BNDES Basic Spread + Credit RiskDirect Mode

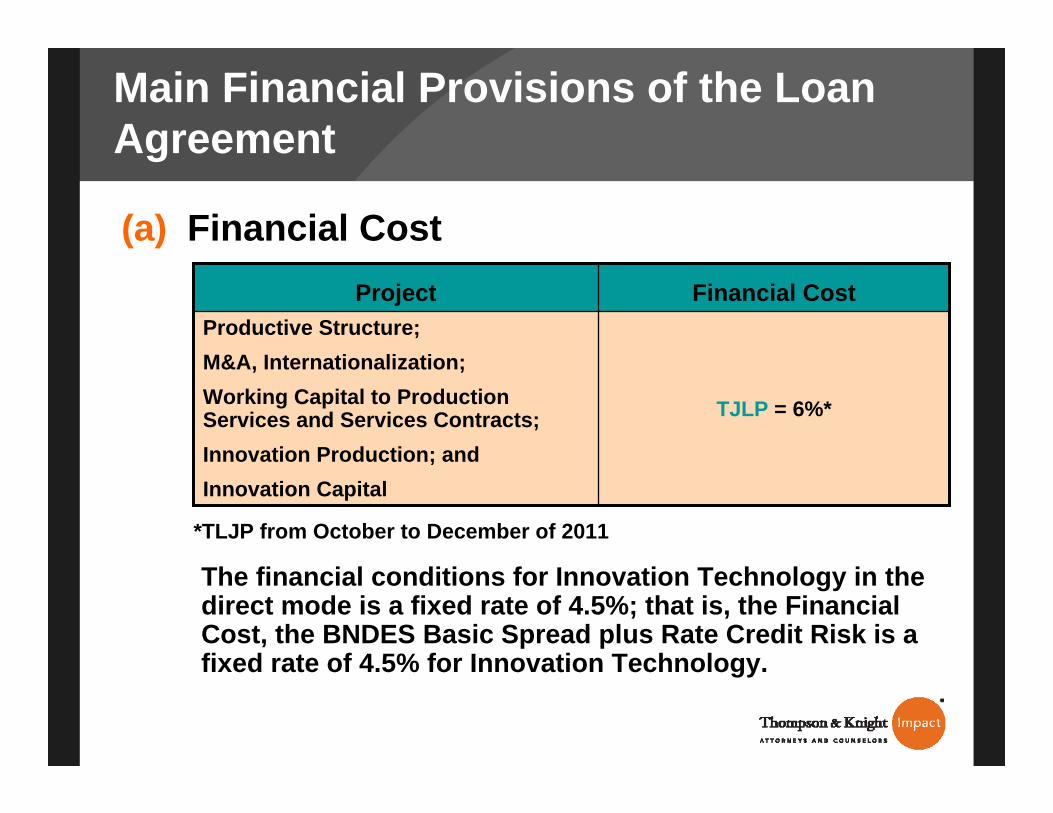

Main Financial Provisions of the Loan Agreement

(a) Financial Cost

TJLP = 6%*

Productive Structure;M&A, Internationalization;Working Capital to Production Services and Services Contracts;Innovation Production; andInnovation Capital

Financial CostProject

*TLJP from October to December of 2011

The financial conditions for Innovation Technology in the direct mode is a fixed rate of 4.5%; that is, the Financial Cost, the BNDES Basic Spread plus Rate Credit Risk is a fixed rate of 4.5% for Innovation Technology.

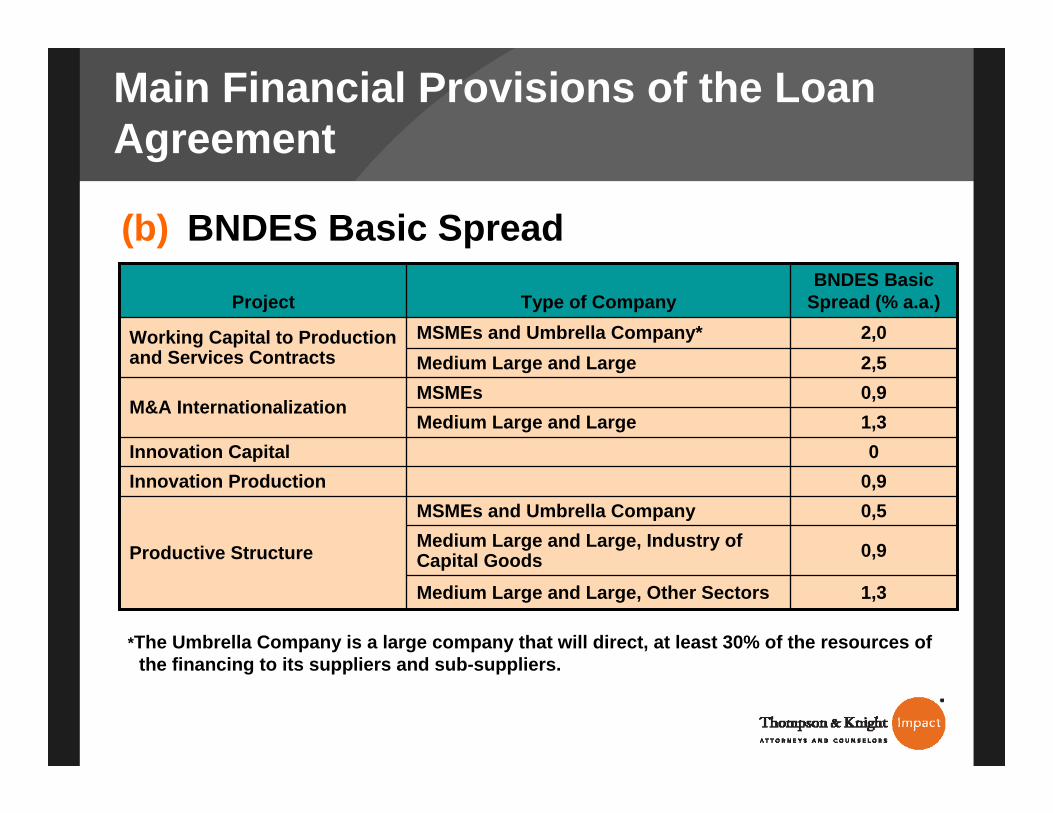

Main Financial Provisions of the Loan Agreement

(b) BNDES Basic Spread

1,3Medium Large and Large, Other Sectors

0,9Medium Large and Large, Industry of Capital Goods

1,3Medium Large and Large

2,5Medium Large and Large

0,5MSMEs and Umbrella Company

Productive Structure

0,9Innovation Production0Innovation Capital

0,9MSMEsM&A Internationalization

MSMEs and Umbrella Company*Type of Company

2,0Working Capital to Production and Services Contracts

BNDES Basic Spread (% a.a.)Project

*The Umbrella Company is a large company that will direct, at least 30% of the resources of the financing to its suppliers and sub-suppliers.

Main Financial Provisions of the Loan Agreement

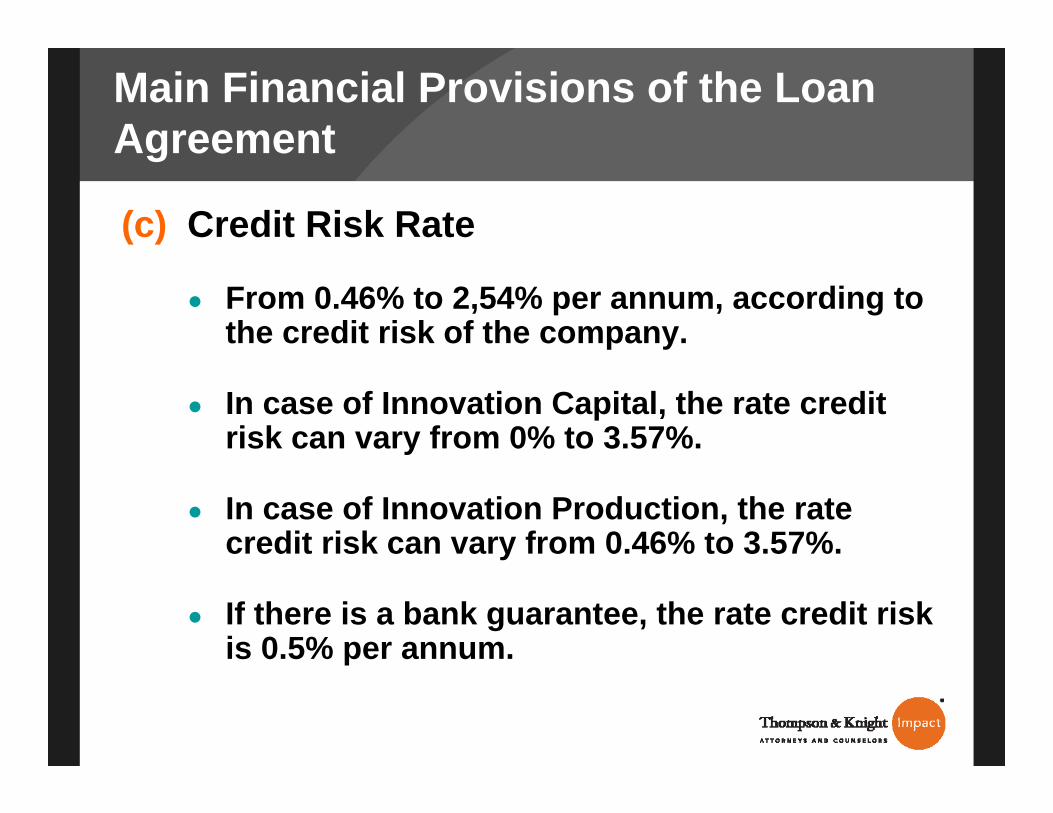

(c) Credit Risk Rate

● From 0.46% to 2,54% per annum, according to the credit risk of the company.

● In case of Innovation Capital, the rate credit risk can vary from 0% to 3.57%.

● In case of Innovation Production, the rate credit risk can vary from 0.46% to 3.57%.

● If there is a bank guarantee, the rate credit risk is 0.5% per annum.

Main Financial Provisions of the Loan Agreement

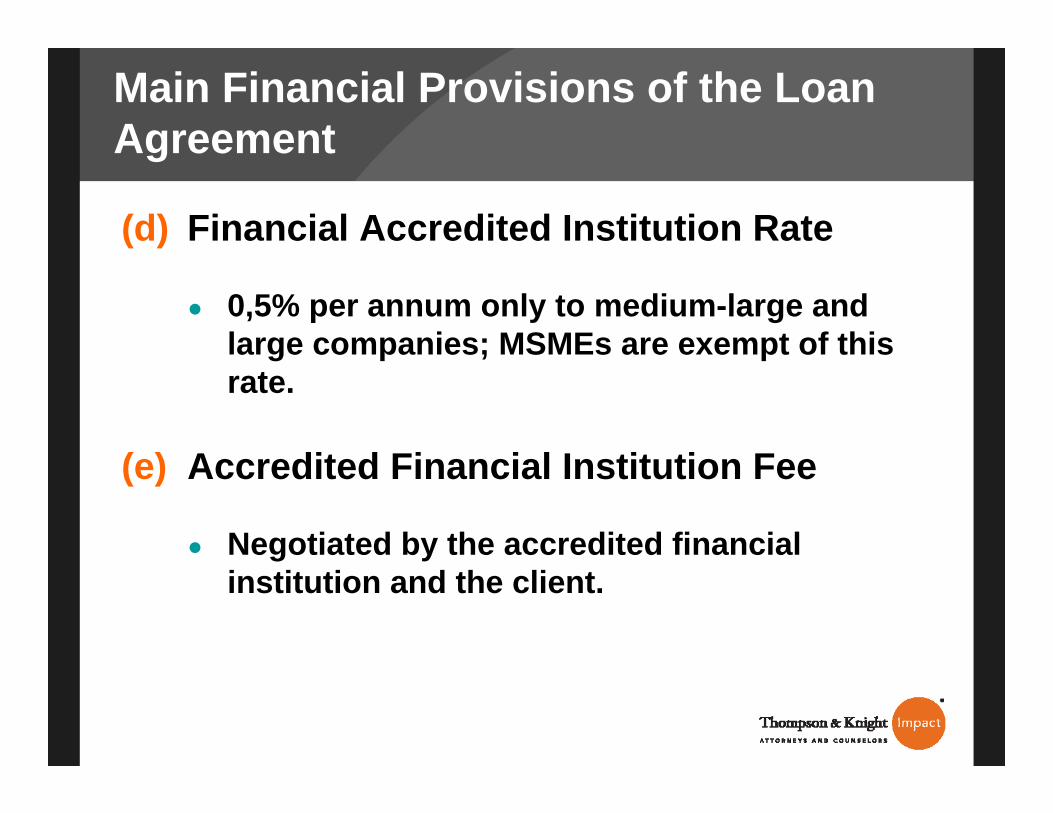

(d) Financial Accredited Institution Rate

● 0,5% per annum only to medium-large and large companies; MSMEs are exempt of this rate.

(e) Accredited Financial Institution Fee

● Negotiated by the accredited financial institution and the client.

Main Financial Provisions of the Loan Agreement

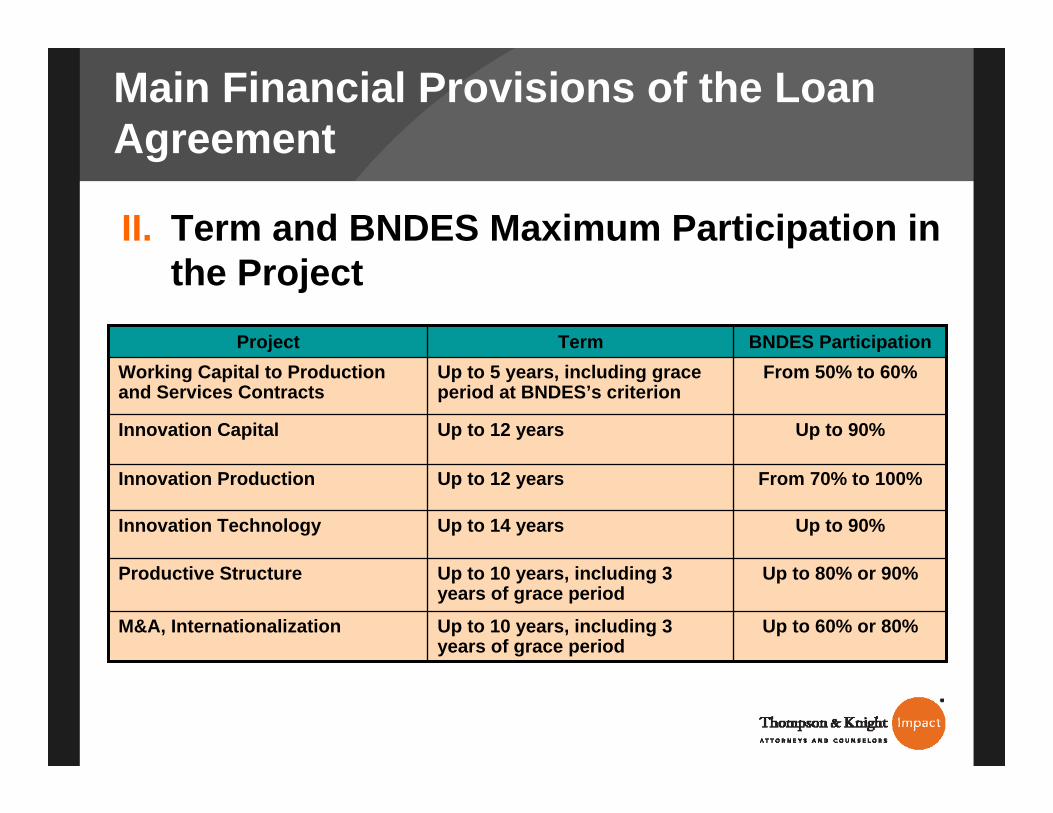

II. Term and BNDES Maximum Participation in the Project

Up to 90%Up to 12 yearsInnovation Capital

Up to 60% or 80%Up to 10 years, including 3 years of grace period

M&A, Internationalization

Up to 80% or 90%Up to 10 years, including 3 years of grace period

Productive Structure

Up to 90%Up to 14 yearsInnovation Technology

From 70% to 100%Up to 12 yearsInnovation Production

Up to 5 years, including grace period at BNDES’s criterion

TermFrom 50% to 60%Working Capital to Production

and Services Contracts

BNDES ParticipationProject

Main Financial Provisions of the Loan Agreement

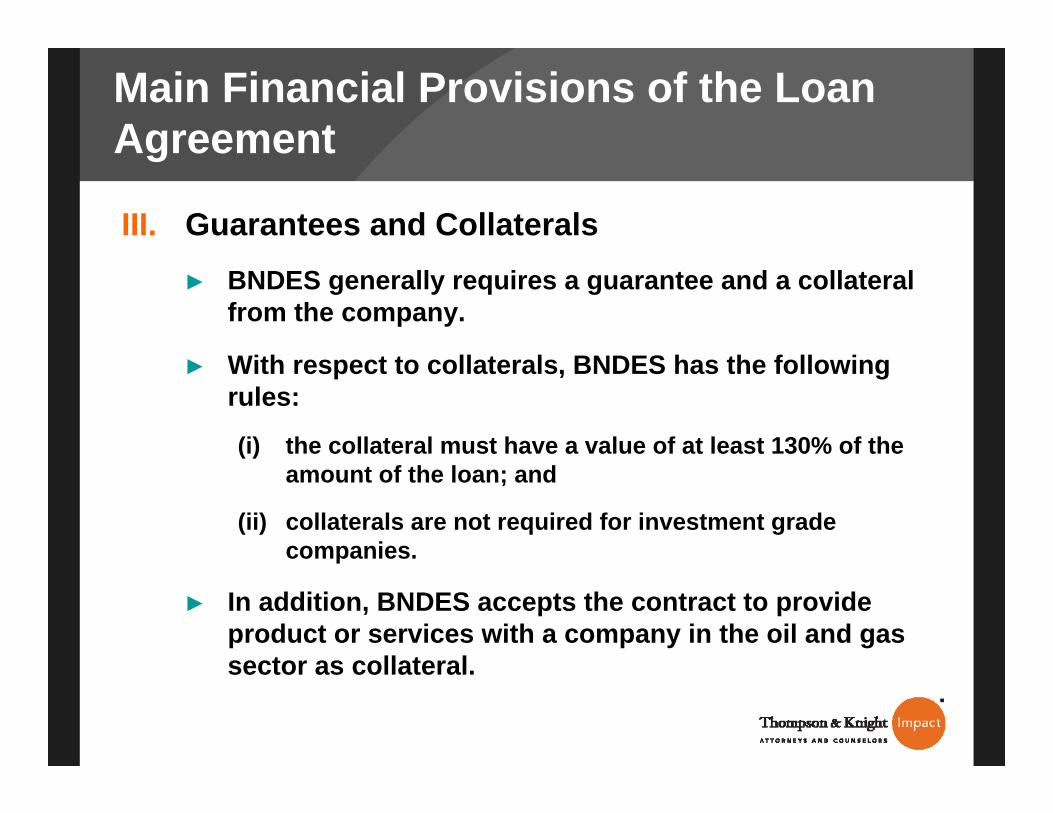

III. Guarantees and Collaterals► BNDES generally requires a guarantee and a collateral

from the company.

► With respect to collaterals, BNDES has the following rules:

(i) the collateral must have a value of at least 130% of the amount of the loan; and

(ii) collaterals are not required for investment grade companies.

► In addition, BNDES accepts the contract to provide product or services with a company in the oil and gas sector as collateral.

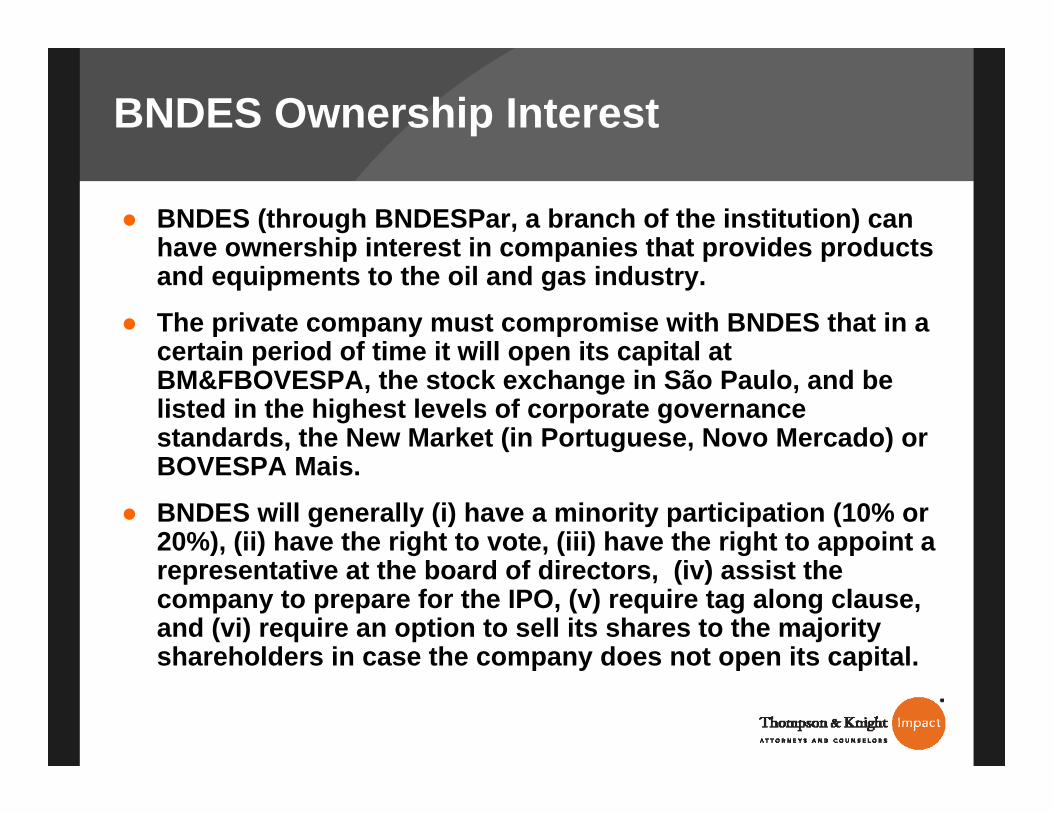

BNDES Ownership Interest

● BNDES (through BNDESPar, a branch of the institution) can have ownership interest in companies that provides products and equipments to the oil and gas industry.

● The private company must compromise with BNDES that in a certain period of time it will open its capital at BM&FBOVESPA, the stock exchange in São Paulo, and be listed in the highest levels of corporate governance standards, the New Market (in Portuguese, Novo Mercado) or BOVESPA Mais.

● BNDES will generally (i) have a minority participation (10% or 20%), (ii) have the right to vote, (iii) have the right to appoint a representative at the board of directors, (iv) assist the company to prepare for the IPO, (v) require tag along clause, and (vi) require an option to sell its shares to the majority shareholders in case the company does not open its capital.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

An Update on An Update on Upstream IssuesUpstream Issues

Paulo Valois Paulo Valois PiresPiresSchmidt, Valois, Miranda, Ferreira & Agel AdvogadosSchmidt, Valois, Miranda, Ferreira & Agel Advogados

November 9, 2011November 9, 2011

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

An Update on Upstream IssuesAn Update on Upstream Issues

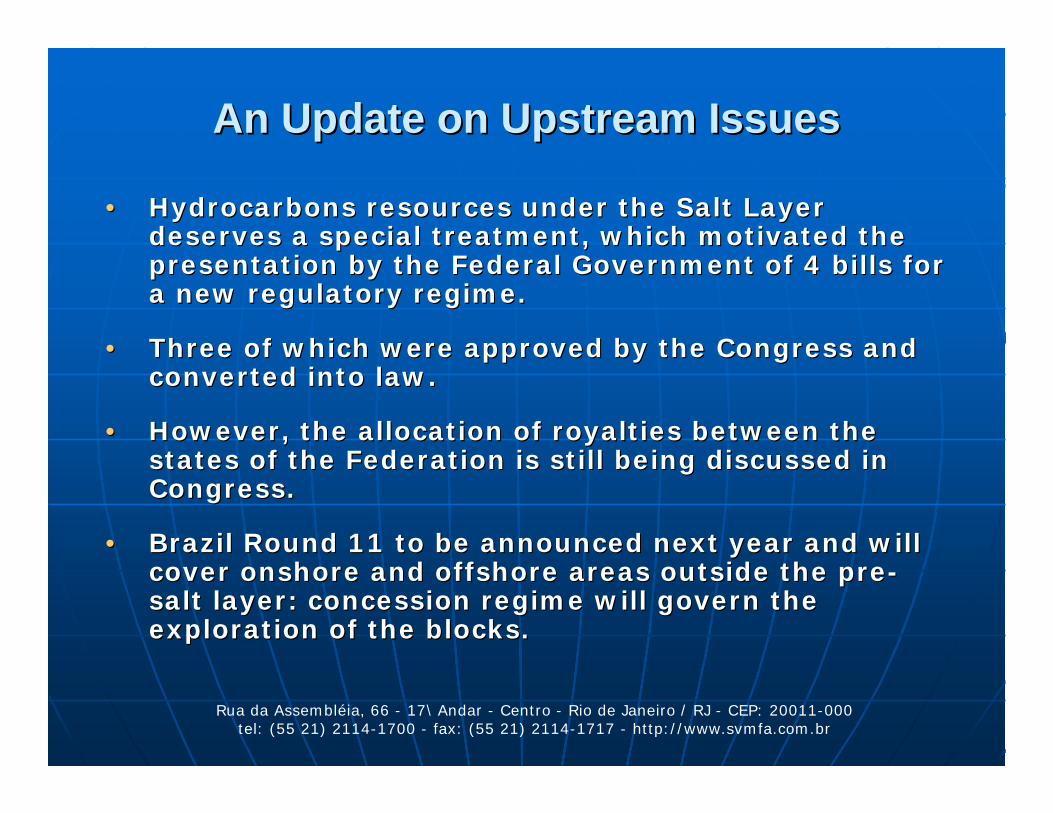

•• Hydrocarbons resources under the Salt Layer Hydrocarbons resources under the Salt Layer deserves a special treatment, which motivated the deserves a special treatment, which motivated the presentation by the Federal Government of 4 bills for presentation by the Federal Government of 4 bills for a new regulatory regime.a new regulatory regime.

•• Three of which were approved by the Congress and Three of which were approved by the Congress and converted into law.converted into law.

•• However, the allocation of royalties between the However, the allocation of royalties between the states of the Federation is still being discussed in states of the Federation is still being discussed in Congress. Congress.

•• Brazil Round 11 to be announced next year and will Brazil Round 11 to be announced next year and will cover onshore and offshore areas outside the precover onshore and offshore areas outside the pre--salt layer: concession regime will govern the salt layer: concession regime will govern the exploration of the blocks.exploration of the blocks.

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

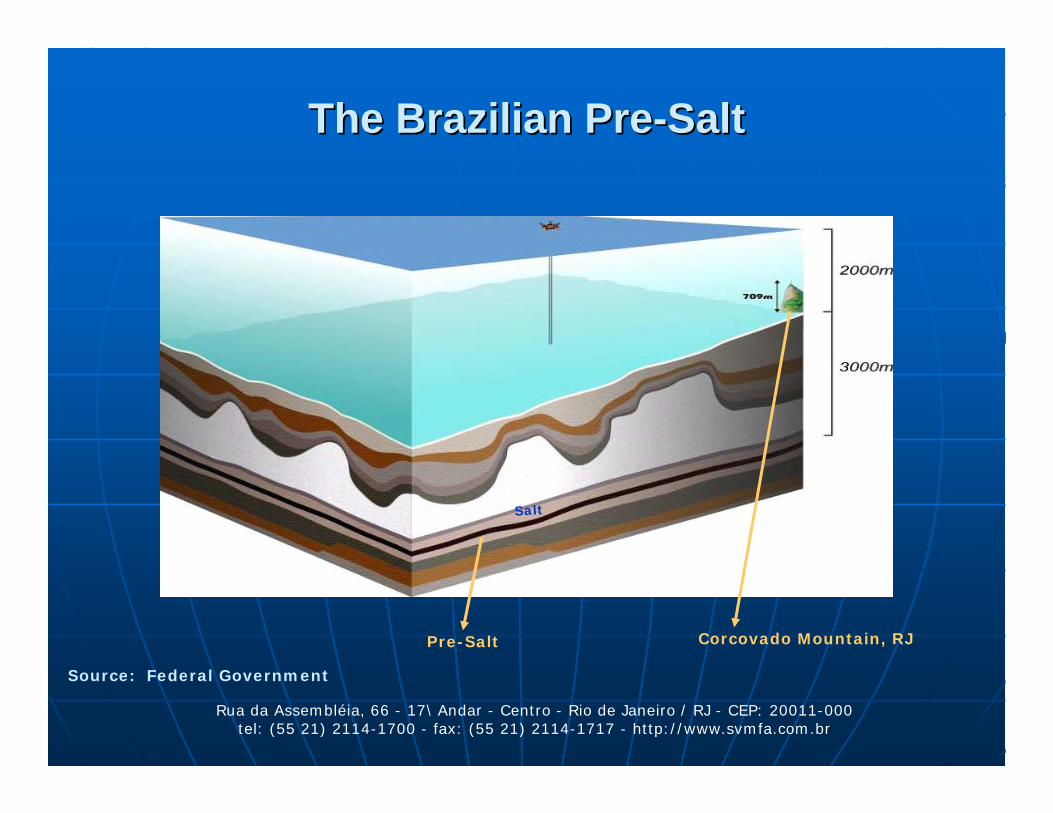

The Brazilian PreThe Brazilian Pre--SaltSalt

Source: Federal Government

Pre-Salt

Salt

Corcovado Mountain, RJ

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

1.2. Pre1.2. Pre--Salt FeaturesSalt Features

•• Approximately 800 km, from the State of Santa Approximately 800 km, from the State of Santa CatarinaCatarina to the State of to the State of EspíritoEspírito SantoSanto

•• Large reservoirs: Large reservoirs:

•• Between 5,000 and 7,000 meters depthBetween 5,000 and 7,000 meters depth

•• Water depth can be over 2,000 metersWater depth can be over 2,000 meters

•• Located under a salt layer Located under a salt layer

•• Total area of approximately 150.000 square km2 Total area of approximately 150.000 square km2

•• 28% of the area has already been licensed28% of the area has already been licensed

•• 24% of the area has PB’ participation24% of the area has PB’ participation

•• 72% of the area still to be assigned72% of the area still to be assigned

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

•• Has generated a lot of debates in the communityHas generated a lot of debates in the community

•• Complex coexistence of two regimesComplex coexistence of two regimes

•• Fostering the participation of “financial partners”Fostering the participation of “financial partners”

•• Limited options for offshore suppliers Limited options for offshore suppliers

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

1.3. 1.3. Introduction of Production SharingIntroduction of Production SharingAgreement (“PSA”) (continuation)Agreement (“PSA”) (continuation)

•• Uncertainty of the “actors” roles (CNPE; MME; ANP; Uncertainty of the “actors” roles (CNPE; MME; ANP; PB; PPSA; O&G companies)PB; PPSA; O&G companies)

•• High risks involved with the operations (postHigh risks involved with the operations (post--Macondo effects)Macondo effects)

•• Uncertainties when the first PSA Round will occurUncertainties when the first PSA Round will occur

•• Unitization issues Unitization issues

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

QuestionsQuestions

•• When will the government decide to call the first When will the government decide to call the first international bid round for the Preinternational bid round for the Pre--Salt?Salt?

•• What kind of partnership does the government What kind of partnership does the government expect for PETROBRAS?expect for PETROBRAS?

•• When will the Brazil Round 11 for areas outside the When will the Brazil Round 11 for areas outside the prepre--salt be launched? What kind of players will be salt be launched? What kind of players will be attracted?attracted?

Rua da Assembléia, 66 - 17\ Andar - Centro - Rio de Janeiro / RJ - CEP: 20011-000 tel: (55 21) 2114-1700 - fax: (55 21) 2114-1717 - http://www.svmfa.com.br

Thank You!Thank You!

Paulo Valois Paulo Valois PiresPiresSchmidt, Valois, Miranda, Ferreira & Agel AdvogadosSchmidt, Valois, Miranda, Ferreira & Agel Advogados