managing active etfs everything you need to know about guest speaker: darlene deremer (grail...

TRANSCRIPT

Managing Active ETFsEverything You Need to Know About

Guest Speaker: Darlene DeRemer (Grail Partners)K&L Gates Hosts: Boston (3/26/08) Stacy Fuller (DC), Francine Rosenberger (DC) and George Zornada (BO)New York (4/10/08): Stacy Fuller (DC), Beth Kramer (NY) and Francine Rosenberger (DC)San Francisco (4/15/08): Stacy Fuller (DC), Mark Perlow (SF) and Richard Phillips (SF)

Everything You Need to Know About Managing Active ETFs

ETF Basics 2007 Growth: 42% increase to $580 billion Key Concepts

Arbitrage mechanism Exchange Listing Transparency

Development Index-based ETFs Actively managed ETFs

Quant techniques/Large-cap securities Transparency – changing requirements

Everything You Need to Know About Managing Active ETFs

Overview

Background: The ETF Business SEC’s Proposed ETF Rules Launch Basics ETF Distribution Looking Ahead Q&A

Everything You Need to Know About Managing Active ETFs

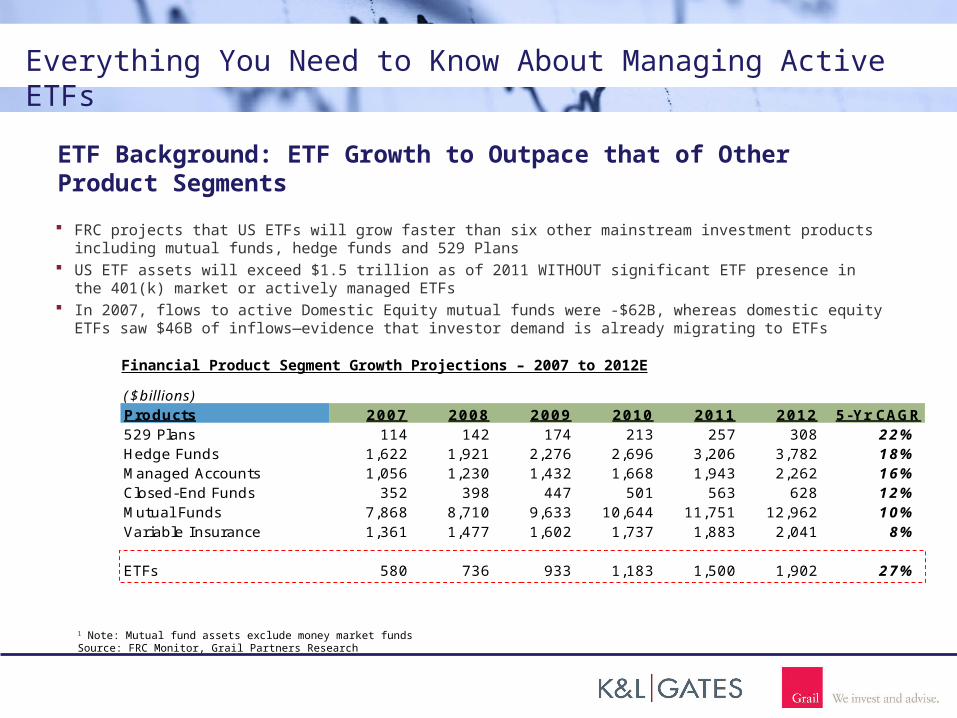

ETF Background: ETF Growth to Outpace that of Other Product Segments

FRC projects that US ETFs will grow faster than six other mainstream investment products including mutual funds, hedge funds and 529 Plans

US ETF assets will exceed $1.5 trillion as of 2011 WITHOUT significant ETF presence in the 401(k) market or actively managed ETFs

In 2007, flows to active Domestic Equity mutual funds were -$62B, whereas domestic equity ETFs saw $46B of inflows—evidence that investor demand is already migrating to ETFs

Financial Product Segment Growth Projections – 2007 to 2012E

($billions)Products 2007 2008 2009 2010 2011 2012 5-Yr CAGR529 Plans 114 142 174 213 257 308 22%Hedge Funds 1,622 1,921 2,276 2,696 3,206 3,782 18%Managed Accounts 1,056 1,230 1,432 1,668 1,943 2,262 16%Closed-End Funds 352 398 447 501 563 628 12%Mutual Funds 7,868 8,710 9,633 10,644 11,751 12,962 10%Variable Insurance 1,361 1,477 1,602 1,737 1,883 2,041 8%

ETFs 580 736 933 1,183 1,500 1,902 27%

1 Note: Mutual fund assets exclude money market fundsSource: FRC Monitor, Grail Partners Research

Everything You Need to Know About Managing Active ETFs

ETF Market Mechanics: Basic Operations

Secondary Market: NYSE Arca / NASDAQ

Broker/ Dealers

XYZ ETF Sponsor/ Manager

Market Maker

(Specialist or

Authorized Participant)

Basket of Securities(creation/

redemption units)

…in kind exchange for…

ETF Shares(50k or 100k ETF

shares)

Broker/ Dealers

Retail Investor

Hedge Fund/ Institutional

Investor

Index XYZ

Rule Set for ETF Portfolio

cash

ETF Shares

cash

ETF Shares

Primary Offering of Fund Shares

Fund Shareholders Secondary Market Participants ETF Share Creation/ Redemption

Investors can buy and sell ETF shares with the help of broker/ dealers throughout the day

Can be shorted and bought on margin Brokerages hold shares in Street name, like

individual stocks

Source: Grail Partners

Market Makers facilitate ETF trading:

Create initial ETF shares and hold in inventory to allow trading to commence

Maintain trading at NAV, by increasing or decreasing liquidity on the market in equilibrium with demand

Full transparency of index-based portfolio allows market participants to exploit arbitrage opportunities when shares trade away from NAV

ETF shares are created and redeemed through in-kind trading between the fund and market makers

The ETF portfolio itself rarely needs to trade securities directly because of this in-kind exchange mechanism

Financial Advisor

Everything You Need to Know About Managing Active ETFs

Active ETFs – Why are they more attractive than mutual funds?

ETFs have advantages vs. mutual funds:

Tax efficiency: in-kind trading of fund shares allows capital gains to be realized outside of the fund, at the participant level avoiding gains distribution from the fund

Low cost: an ETF trades like an individual stock, so transfer agency and other recordkeeping costs are minimal – somewhat offset by new costs in the dealer system, and commissions

Investor protection/ enhanced return:

Exchange trading eliminates the possibility of market timing

No cash held for redemption requests – better performance through full investment

Trading costs are absorbed by transacting investor, not the fund shareholders

Portfolio flexibility: ETFs are traded as individual equities, allowing investors to short and buy on margin as they build their portfolios

Source: Grail Partners

Everything You Need to Know About Managing Active ETFs

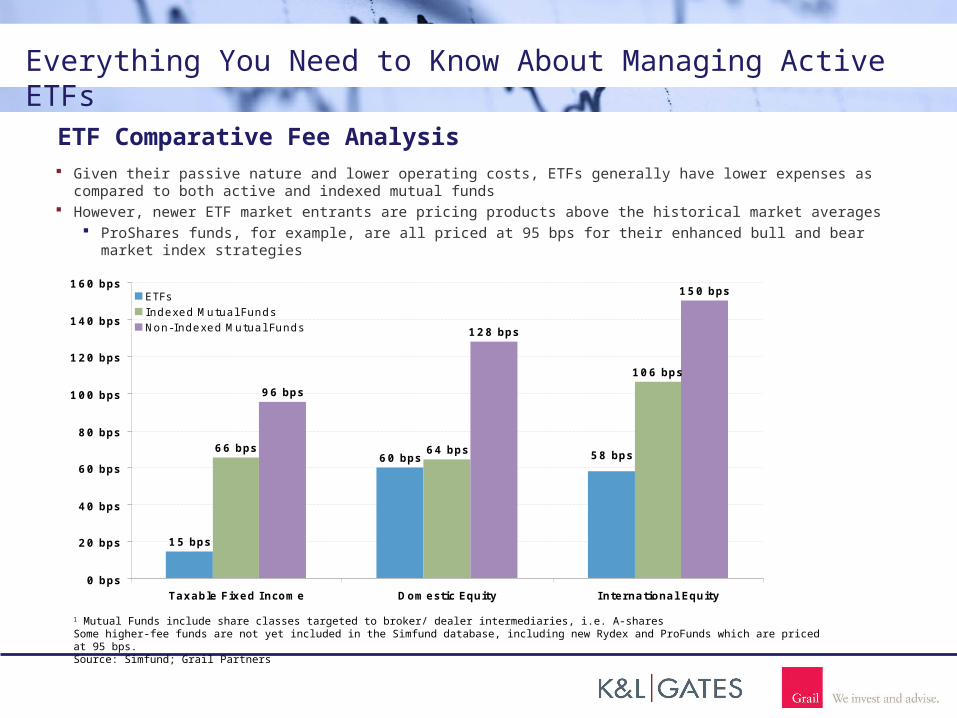

ETF Comparative Fee Analysis Given their passive nature and lower operating costs, ETFs generally have lower expenses as

compared to both active and indexed mutual funds However, newer ETF market entrants are pricing products above the historical market averages

ProShares funds, for example, are all priced at 95 bps for their enhanced bull and bear market index strategies

15 bps

60 bps66 bps 64 bps

106 bps

96 bps

128 bps

150 bps

58 bps

0 bps

20 bps

40 bps

60 bps

80 bps

100 bps

120 bps

140 bps

160 bps

Taxable Fixed Income Domestic Equity International Equity

ETFsIndexed Mutual FundsNon-Indexed Mutual Funds

1 Mutual Funds include share classes targeted to broker/ dealer intermediaries, i.e. A-sharesSome higher-fee funds are not yet included in the Simfund database, including new Rydex and ProFunds which are priced at 95 bps. Source: Simfund; Grail Partners

Everything You Need to Know About Managing Active ETFs

($billions)Sponsor Brand Name Funds ETF AUM Launch

1 Barclays iShares, iPath ETN 170 $306.2 20002 State Street SPDRs, streetTRACKS 67 158.0 19933 Vanguard VIPERs 37 44.3 20044 PowerShares PowerShares/ BLDRS 100 30.3 20025 ProFunds ProShares 58 15.6 20066 Merrill Lynch HOLDRS 17 7.4 19987 Rydex ExpressShares 31 6.1 20038 Deutsche Bank PowerShares (Commodity/ Currency) 13 5.9 20059 Van Eck Funds Market Vectors 12 5.0 2006

10 WisdomTree WisdomTree 40 4.3 200611 Claymore Various 29 1.8 200612 Victoria Bay Various 4 0.9 200613 First Trust First Trust 36 0.9 200514 ELEMENTS ELEMENTS ETNs 13 0.5 200715 XShares Various 31 0.2 200716 MacroMarkets MacroShares 2 0.2 200617 Goldman Sachs Goldman Sachs ETN 2 0.1 200718 Fidelity Tracking Stock 1 0.1 200319 Bear Stearns Bear Stearns ETN 1 0.1 200720 GreenHaven GreenHaven 1 0.0 200821 FocusShares FocusShares ISE 3 0.0 200722 Morgan Stanley Morgan Stanley 2 0.0 200823 SPA ETFs/ London & Capital SPA/ MarketGrader 6 0.0 200724 RevenueShares RevenueShares 3 0.0 200825 Ameristock Ameristock/ Ryan 5 0.0 200726 Lehman Brothers Lehman Brothers 2 0.0 200827 Ziegler NYSE ARCA 1 0.0 2007

687 $588.07Source: Bloomberg as of 3/24/08; Grail PartnersNote: This table includes non-ETF exchange traded products like HOLDRS, BLDRS and ETNs.1 ELEMENTS is a partnership between Nuveen Investments, Merrill Lynch, Swedish Export Credit Corporation and BNP Paribas2 MacroShares ETFs were launched through a JV with Claymore in 2006; MacroShares bought out Claymore’s 50% stake in 8/073 SPA ETFs is an affiliate of London & Capital

US ETF Assets by Sponsor

Everything You Need to Know About Managing Active ETFs

Industry Competitors DescribedFirm Product Pricing1 Distribution

Traditional IndexedTraditional indexing transitioned from mutual fund to ETF

BGI Wide range of traditional index offerings 170 ETFs; $306.2 B

36 bps BGI was first to aggressively target broad retail and institutional audiences

State Street Wide range of traditional index offerings 67 ETFs; $158.0 B

19 bps Mix of retail/ institutional

Vanguard Breadth of traditional, low-cost indexes 37 ETFs; $44.3 B

15 bps Vanguard targets its traditional no-load investors and other brokerage clients

Enhanced Indexed – Select FirmsUnique indexing, in both construction and strategies/ industries covered

Power-Shares2

US and international rules-based quant ETFs Leverage Rob Arnott fundamental indexes 100 ETFs; $30.3 B

39 bps Mix of retail/ institutional Leverages AIM wholesaler coverage given IVZ

ownership

ProFunds Unique exposure (shorting, double exposure) to range of US equity indexes

58 ETFs; $15.6 B

95 bps ProShares has launched ETFs with an established base of clients (RIAs) in its mutual fund offerings

Rydex Offering similar to that of ProShares 31 ETFs; $6.1 B

39 bps Rydex has launched ETFs with an established base of clients (RIAs) in its mutual fund offerings

Wisdom-Tree US and international equity ETFs weighted by fundamental metrics: div. income, rev.

40 ETFs; $4.3 B

51 bps Targets a mix of retail/ institutional investors

XShares Custom indexes focused on sector “verticals”; third party indexes

31 ETFs; $0.2 B

69 bps Sales force targets retail and institutional investors Proprietary and partnership ETFs

1 Reflects AUM-weighted average of all ETFs offered by the company2 Nasdaq transferred its QQQQ fund and 4 BLDRS to PowerShares 3/07, reducing PowerShares’ average pricingSource: Bloomberg, Grail Partners Research as of 3/24/08

Everything You Need to Know About Managing Active ETFs

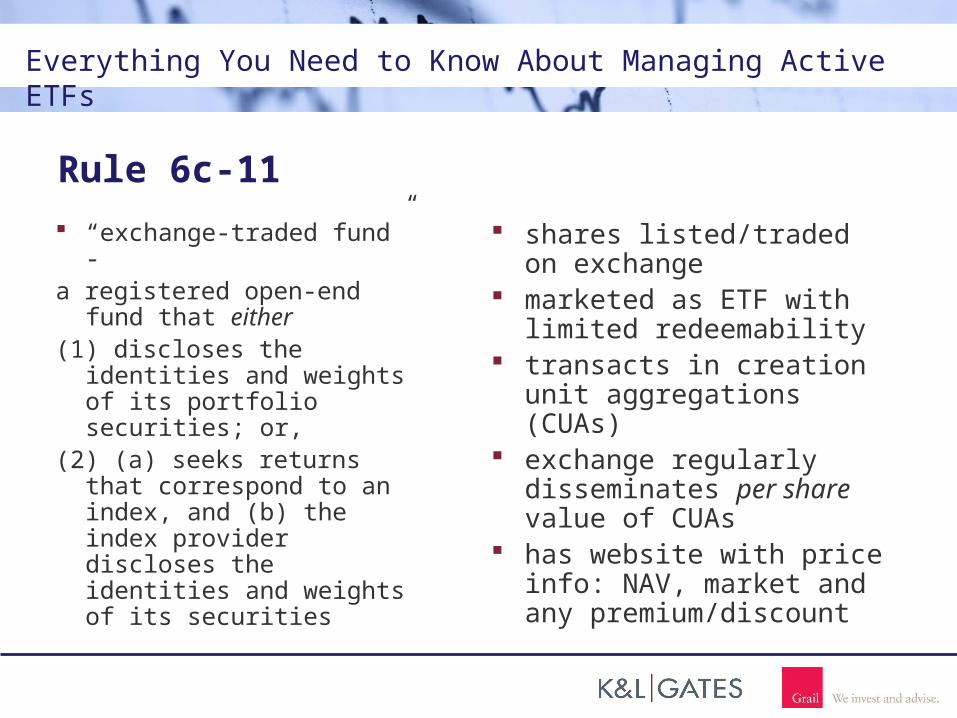

Rule 6c-11

“exchange-traded fund” - a registered open-end fund

that either(1) discloses the identities

and weights of its portfolio securities; or,

(2) (a) seeks returns that correspond to an index, and (b) the index provider discloses the identities and weights of its securities

shares listed/traded on exchange

marketed as ETF with limited redeemability

transacts in creation unit aggregations (CUAs)

exchange regularly disseminates per share value of CUAs

has website with price info: NAV, market and any premium/discount

Everything You Need to Know About Managing Active ETFs

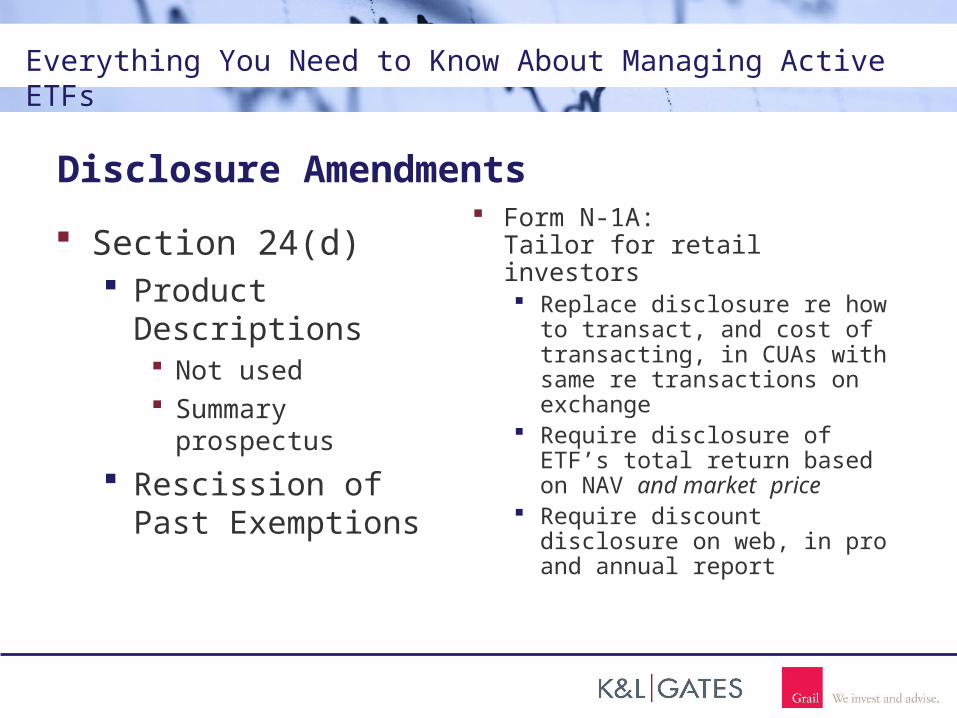

Disclosure Amendments

Section 24(d) Product Descriptions

Not used Summary prospectus

Rescission of Past Exemptions

Form N-1A: Tailor for retail investors Replace disclosure re how

to transact, and cost of transacting, in CUAs with same re transactions on exchange

Require disclosure of ETF’s total return based on NAV and market price

Require discount disclosure on web, in pro and annual report

Everything You Need to Know About Managing Active ETFs

Liberalization of Orders

Sampling Affiliated index-based ETFs Section 48(a) Asset basket requirements

Everything You Need to Know About Managing Active ETFs

Rule 12d1-4

Investments by registered and private funds 4 Conditions

Limitation on control of underlying fund by investing fund ETF is not a “fund of funds” Fees comply with NASD Conduct Rule 2830 No redemptions by investing fund with more than 3% of ETF

Compare traditional funds of funds Investments by registered funds only 12 Conditions

Everything You Need to Know About Managing Active ETFs

Conditions for Traditional Funds of Funds

Limitation on control of underlying fund by investing fund

Underlying fund is not a “fund of funds”

Fees comply with NASD Conduct Rule 2830

Waiver by investing fund of certain fees based on other fees received from underlying fund

Limitation on investing fund’s influence over underlying fund

Limitation on investments by underlying fund in underwritings involving affiliate of investing fund (“affiliated underwriting”)

Finding by underlying fund board re any investment by underlying fund in affiliated underwriting

Finding by underlying fund board that any payments to investing fund were reasonable for services received in return

Finding by investing fund board that consideration received by investing fund from underlying fund did not influence investment

Finding by investing fund board that no duplicative advisory fees

Requirement of Participation Agreement (to provide notice of conditions involving board findings)

Everything You Need to Know About Managing Active ETFs

Launch Basics

Choose Asset Class ETN / Grantor Trust – Corp Fin ETF – IM

Exemptive Application Rule 6c-11

Market Maker / Specialist Prepare Timeline: Precedented v. Novel Relief Register Product

ETN / Grantor Trust – S-1 and 8-A ETF – N-8A, N-1A and 8-A

Prospectus / PD v. Disclosure Amendments & Summary Prospectus Approach T&M / Exchange

No action relief Listing

Everything You Need to Know About Managing Active ETFs

Seed Capital: Tempering the Pace of Proliferation To support the secondary market, launching an ETF requires a minimum market inventory be established

to facilitate trading and market liquidity

Exchanges typically require at least two ETF “creation units” be issued (generally 200,000 shares) prior to fund launch. If a fund’s NAV starts at $25, this equals $5 million in AUM

This initial seed capital is typically provided by market specialists—often using borrowed securities in their effort to support a product that will yield secondary trading activity

But for those market makers, seeding ETFs is becoming a much less attractive proposition

The drag or costs of providing seed capital are real:

Cost of borrowing (up to 200 bps or more) to fund and hedge

ETF expense ratio (~50 bps and higher); ETF fees are increasing as more niche and quasi-active ETFs are launched

The proposition of acting as an ETF specialist itself has become less attractive:

Spreads in ETF trading have tightened

Given the merger of NYSE and AmEx, electronic trading will become the dominant method for ETF specialists, in turn diffusing the share of volume that the specialist can capture

Therefore, the lack of seed capital in the ETF market is expected to be a major industry “choke point” and inhibitor of product proliferation, particularly among smaller ETF sponsors

Source: Grail Partners

Everything You Need to Know About Managing Active ETFs

ETF Distribution

Distribution Specialists Other institutional investors Rule 12b-1 Plans IPOs Rule 12d1-4 Funds

Everything You Need to Know About Managing Active ETFs

Distribution: Mutual Funds vs. ETFs

Growth Areas

Mutual Funds - 2007

Fee-Based Intermediaries

30%

Proprietary Sales Force

5%Direct to Investor

10%

Fund Supermarkets

10%

Retirement Plans25%

Transaction Based Brokers

20%

ETFs - Anecdotal

Institutional investors (hedge funds, portfolio managers) play a larger proportional role in ETFs than is typical in mutual funds

ETFs’ offer of sector exposure and cash equitization are contributors

However, retail sources (RIAs, brokers, wealth advisors) have become a more significant force in ETF distribution in recent years

Fee-based programs help make advisors indifferent to product packages, and ETFs are benefiting from this phenomenon

Tracking sales by source in ETFs is more difficult than in mutual funds

Source: FRC, Grail Partners Research

Everything You Need to Know About Managing Active ETFs

Looking Ahead

Trends Next-generation ETFs

Semi-transparent ETFs Tracking Baskets Value Transparency Black Box

“‘Is it critical that arbitrage be tight and strong?’ We think that’s an important question that the Commission will need to consider going forward as we face applications for non-transparent ETFs.”

Timing