management’ss2.q4cdn.com/510341073/files/doc_downloads/presentations/final-q2... · source: bofa...

TRANSCRIPT

Certain statements made by us in this presentation that are not historical facts or that relate to future plans, events or performances

are forward-looking statements that reflect management’s current outlook for future periods, including statements regarding future

financial performance. These forward-looking statements are based upon our current expectations, and our actual results may differ

materially from those described or contemplated in the forward–looking statements. Factors that may cause our actual results to differ

materially from those contained in the forward-looking statements, include without limitation the following: 1) national and global

economic conditions, including the impact of changes in national and global credit markets and other changes on our customers; 2)

our ability to continue to attract and retain customers and maintain profit margins in the face of new and existing competition; 3) new

laws and regulations that could have a materially adverse effect on our operations and financial results; 4) significant labor

disturbances which could disrupt industries we serve; 5) increased costs and collateral requirements in connection with our insurance

obligations, including workers’ compensation insurance; 6) the adequacy of our financial reserves; 7) our continuing ability to comply

with financial covenants in our lines of credit and other financing agreements; 8) our ability to attract and retain competent employees

in key positions or to find temporary employees to fulfill the needs of our customers; 9) our ability to successfully complete and

integrate the MDT Personnel and other acquisitions that we may make from time to time; and 10) other risks described in our filings

with the Securities and Exchange Commission, including our most recent Form 10-K and Form 10-Q filings.

Use of estimates and forecasts:

Any references made to 2013 are based on management guidance issued April 24, 2013, and are included for informational purposes

only and are not an update or reaffirmation. We assume no obligation to update or revise any forward-looking statement, whether as a

result of new information, future events, or otherwise, except as required by law. Any other reference to future financial estimates are

included for informational purposes only and subject to factors discussed in our 10-K and 10-Q filings.

TRUEBLUE INVESTMENT HIGHLIGHTS

• Specialized leader in blue-collar staffing

• Well-positioned in growing staffing market

• Significant upside as construction market rebounds

• Compelling organic growth strategies

• Successful acquisition strategy

• Strong operating leverage

• Solid capital position supports growth

SPECIALIZED LEADER IN BLUE-COLLAR STAFFING

A CREDIBLE BUSINESS LEADER

Best Practices by

DHS/ICE Partner National

Agreement

Forbes Most

Trustworthy

Companies

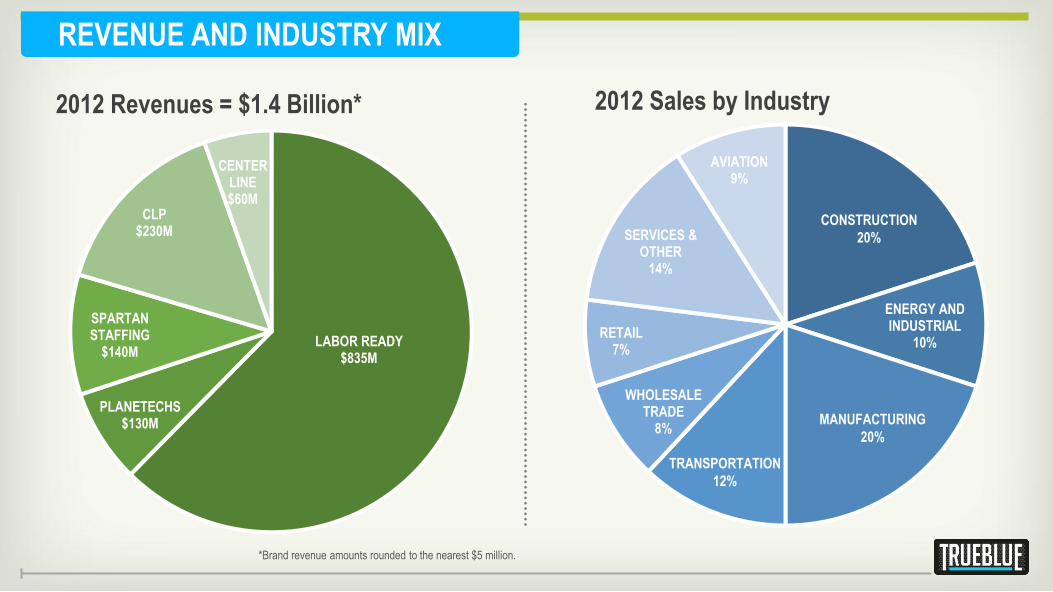

*Brand revenue amounts rounded to the nearest $5 million.

REVENUE AND INDUSTRY MIX

ENERGY AND INDUSTRIAL

10%

WHOLESALE TRADE

8%

RETAIL 7%

SERVICES & OTHER

14%

AVIATION 9%

CONSTRUCTION

20%

TRANSPORTATION

12%

MANUFACTURING

20%

2012 Sales by Industry

LABOR READY $835M

PLANETECHS $130M

SPARTAN STAFFING

$140M

CLP $230M

CENTER LINE $60M

2012 Revenues = $1.4 Billion*

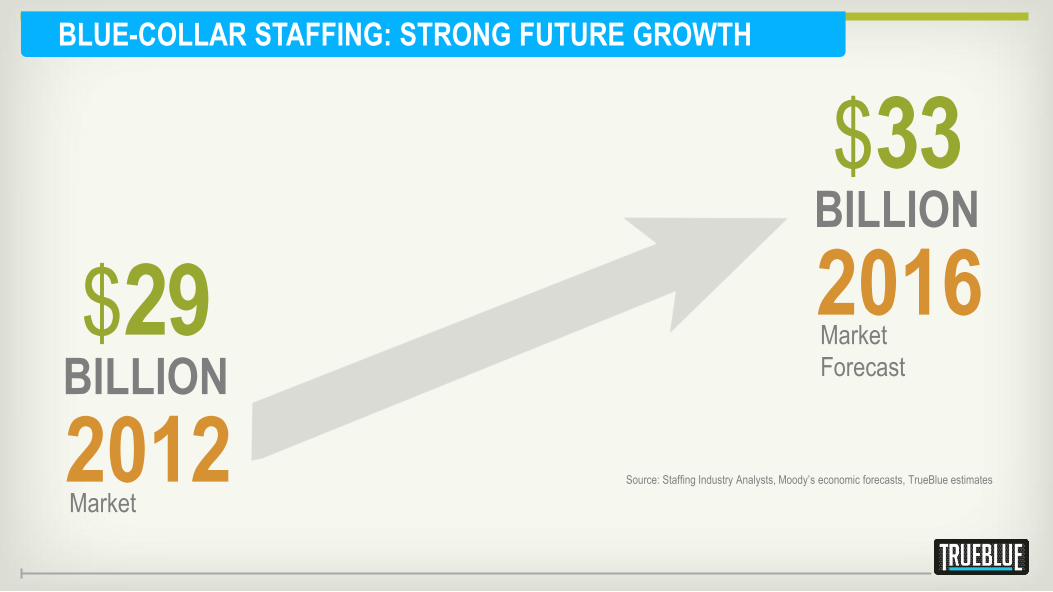

BLUE-COLLAR STAFFING: $29 BILLION INDUSTRY

$100 Billion Overall Industry

$29B

OFFICE IT

FINANCE

HEALTHCARE

OTHER

BLUE-COLLAR

STAFFING

BLUE-COLLAR STAFFING: STRONG FUTURE GROWTH

Source: Staffing Industry Analysts, Moody’s economic forecasts, TrueBlue estimates 2012

2016

$33 BILLION

$29 BILLION

Market

Market

Forecast

BUSINESSES CHOOSE TEMPORARY STAFFING

Why businesses are using more

temporary staffing:

Source: Bureau of Labor Statistics. Measures number of jobs added from help supply services as a

percentage of total non-farm payroll. Timeframe measured is 41 months from the start of the recoveries:

August 1991, May 2003, and September 2009.

Temp jobs as percentage of total jobs

added

1991 - 2003 Recoveries

8%

2009 - 2012 Recovery

16%

STAFFING INDUSTRY GROWTH DRIVERS: AFFORDABLE CARE ACT

Employers with more than 50 full-

time employees (30+ hours per

week) must either offer affordable

health coverage or pay a penalty.

Provide employers with

flexible solutions to comply

with ACA law.

OPPORTUNITY SITUATION

STAFFING INDUSTRY GROWTH DRIVERS: CONSTRUCTION

• Construction employment near

historic lows

• Positive momentum for housing

starts; construction employment

to follow

• Significant construction

revenue increase

• Multiplier effect on logistics,

retail and services

OPPORTUNITY SITUATION

Source: BofA Merrill Lynch Research, BLS, Census Bureau

Ho

usi

ng

Sta

rts

(1

000s

; lag

s fiv

e qt

rs.)

Co

nst

ruct

ion

Jo

bs

(a

s pe

rcen

t of l

abor

forc

e)

POISED FOR CONSTRUCTION REBOUND

Construction Jobs Follow Housing Starts

2500

2000

1500

1000

500

5.2

4.7

4.2

3.7

3.2

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

TRUEBLUE: STRONG CONSTRUCTION UPSIDE

* Based on incremental construction EBITDA margin assumptions of 20 percent. See 2013 Estimate - Operating Income to EBITDA and Adjusted EBITDA Reconciliation slide.

HISTORIC CONSTRUCTION TRENDS

2006 2012

INCREMENTAL

CONSTRUCTION

UPSIDE

Revenue $ 450M $ 280M $ 170M

Incremental

EBITDA*

$ 35M

STAFFING INDUSTRY GROWTH DRIVERS: MANUFACTURING

• U.S. Manufacturing Renaissance

• Increased incentives to “reshore”

including increasing wages in China,

offshore product quality concerns

• Decline in energy costs

• Provide flexible, skilled

labor force

• Closer-to-customer

improves service

OPPORTUNITY SITUATION

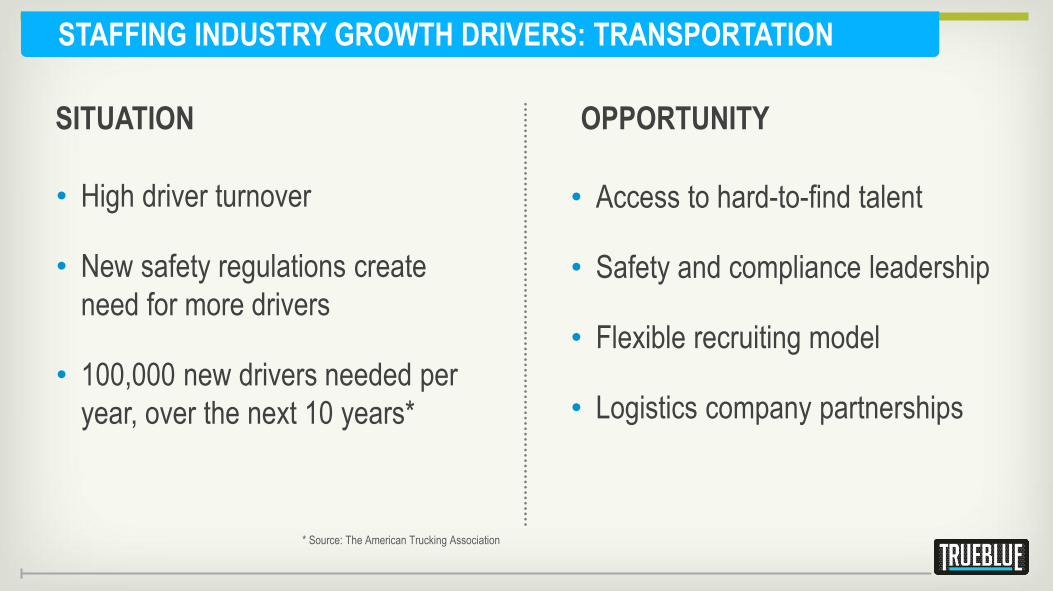

STAFFING INDUSTRY GROWTH DRIVERS: TRANSPORTATION

• High driver turnover

• New safety regulations create

need for more drivers

• 100,000 new drivers needed per

year, over the next 10 years*

• Access to hard-to-find talent

• Safety and compliance leadership

• Flexible recruiting model

• Logistics company partnerships

* Source: The American Trucking Association

OPPORTUNITY SITUATION

STAFFING INDUSTRY GROWTH DRIVERS: ENERGY

• Growing energy independence

• Skilled worker shortages

• More than 100,000 new jobs

in the solar industry by 2016*

• Deliver and manage skilled work

force in remote areas

• Deep technical knowledge within

green industries

• Partner with green industry trades

schools to fill skilled-worker gap

• Business process improvements,

not just service features

OPPORTUNITY SITUATION

* Source: The Solar Energy Industry Association

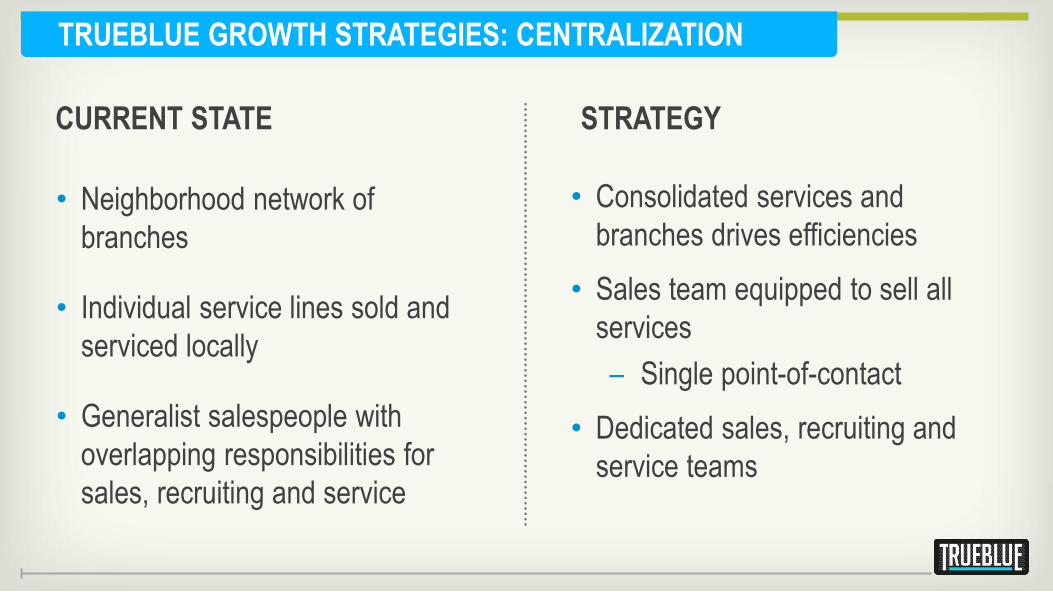

TRUEBLUE GROWTH STRATEGIES: CENTRALIZATION

STRATEGY CURRENT STATE

• Neighborhood network of

branches

• Individual service lines sold and

serviced locally

• Generalist salespeople with

overlapping responsibilities for

sales, recruiting and service

• Consolidated services and

branches drives efficiencies

• Sales team equipped to sell all

services

– Single point-of-contact

• Dedicated sales, recruiting and

service teams

TRUEBLUE GROWTH STRATEGIES: SPECIALIZATION

• Local sales strategies

• National sales and service

• Industry expertise

• Specialized recruiters

• Network of worker access points

• Additional vertical expertise

STRATEGY CURRENT STATE

Metro Area

Rural Area

Rural Area

Rural Area

Rural Area

CENTRALIZATION + SPECIALIZATION DRIVES VALUE

Sales teams equipped to sell all services will deliver higher revenue and specialized recruiters will deliver

higher quality workers as we consolidate our services and branch network to increase efficiency.

TRADITIONAL BRANCH NETWORK FUTURE BRANCH NETWORK

Metro Area

Rural Area

Rural Area

Rural Area

Rural Area

TRUEBLUE GROWTH STRATEGIES: TECHNOLOGY

STRATEGY CURRENT STATE

• Texting

– Fill more orders, faster

– Higher quality, more

workers

• Electronic placement

• Pay cards

• Electronic hiring process

• Social media recruiting

• Enhanced database

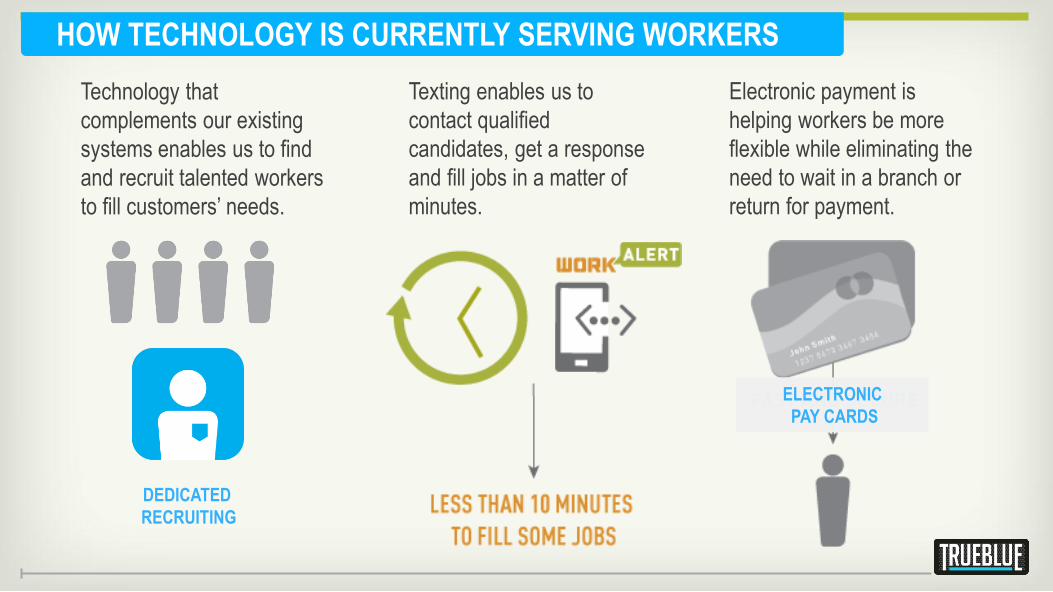

HOW TECHNOLOGY IS CURRENTLY SERVING WORKERS

DEDICATED

RECRUITING

ELECTRONIC

PAY CARDS

Electronic payment is

helping workers be more

flexible while eliminating the

need to wait in a branch or

return for payment.

Texting enables us to

contact qualified

candidates, get a response

and fill jobs in a matter of

minutes.

Technology that

complements our existing

systems enables us to find

and recruit talented workers

to fill customers’ needs.

SUCCESSFUL ACQUISITION STRATEGY

RESULTS CONSIDERATION

• ROIC*

• Strategic fit

• Cultural fit

• Limited financial risk

• New business capabilities

• Talent

• ROI >15% cost of capital

• $220M invested between 2004-2013

• Aggregated acquired companies ~40% of 2012 revenue

• Platforms established to seamlessly tuck in future acquisitions

* Return on Invested Capital

• Combined annual revenue of $1.6 billion

• Creates $1 billion revenue general labor staffing business

• Integration included about 60 branch consolidations

• Infusion of new talent, including industry-experienced sales force

* Based on 2014 estimate; assumes full year of revenue and certain synergies.

MDT: SUCCESSFUL INTEGRATION

Financial Review

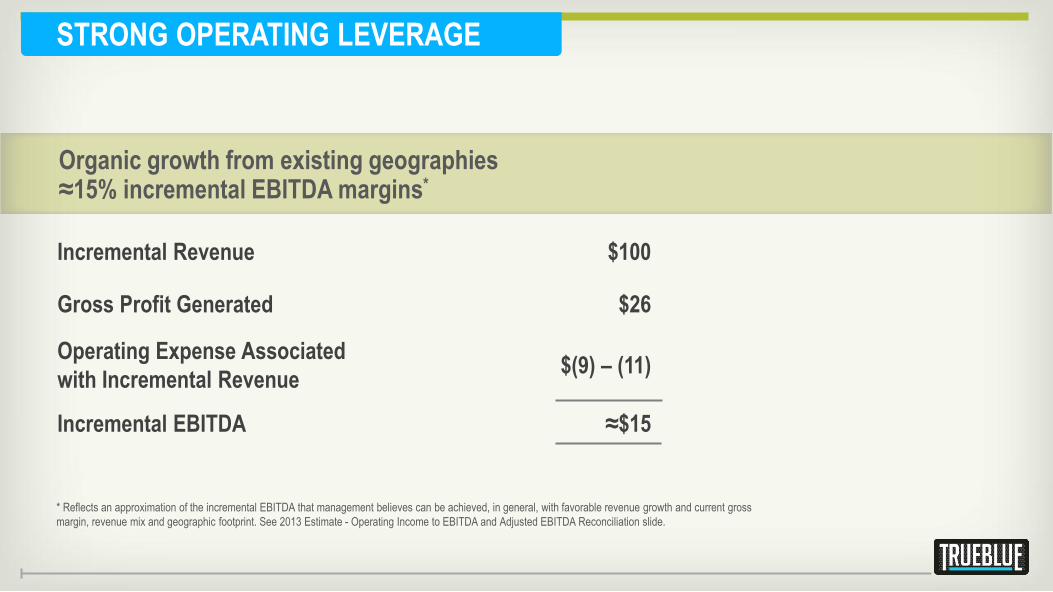

Incremental Revenue $100

Gross Profit Generated $26

Operating Expense Associated

with Incremental Revenue $(9) – (11)

Incremental EBITDA ≈$15

* Reflects an approximation of the incremental EBITDA that management believes can be achieved, in general, with favorable revenue growth and current gross

margin, revenue mix and geographic footprint. See 2013 Estimate - Operating Income to EBITDA and Adjusted EBITDA Reconciliation slide.

Organic growth from existing geographies ≈15% incremental EBITDA margins*

STRONG OPERATING LEVERAGE

Dollar amounts in millions Q-1 2013 Q-4 2012

Cash & investments

$ 111 $ 130

Borrowing Availability $ 71 $ 66

Total Liquidity Strong liquidity position to fund acquisition strategy

$ 182 $ 196

* The company took on debt in 2013 with the acquisition of MDT.

STRONG CAPITAL POSITION SUPPORTS GROWTH

Debt*

Low financial leverage balances strong operating leverage $ 31 $ 0

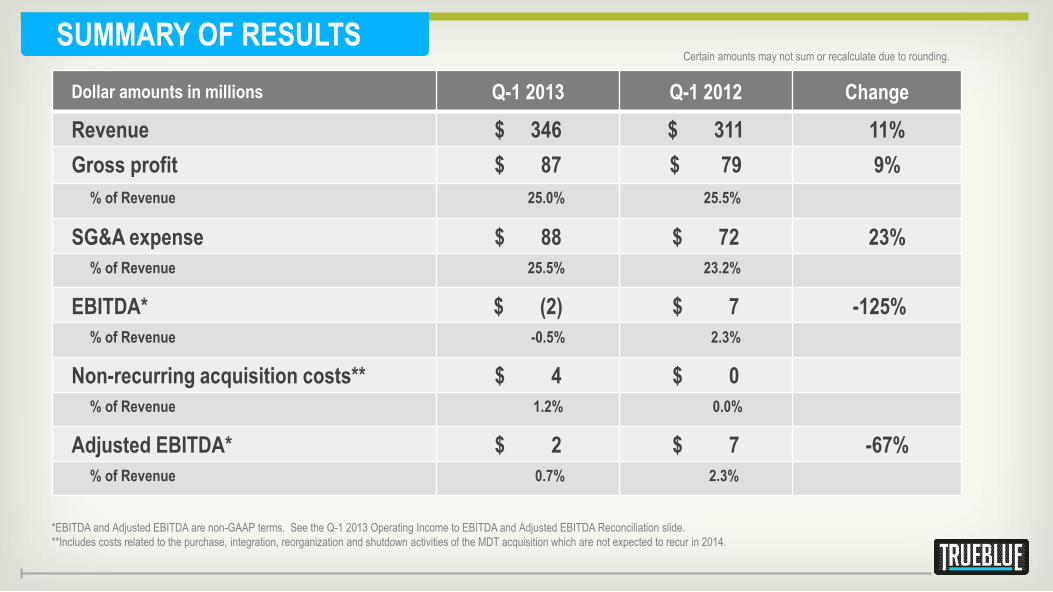

Dollar amounts in millions Q-1 2013 Q-1 2012 Change

Revenue $ 346 $ 311 11%

Gross profit $ 87 $ 79 9%

% of Revenue 25.0% 25.5%

SG&A expense $ 88 $ 72 23%

% of Revenue 25.5% 23.2%

EBITDA* $ (2) $ 7 -125%

% of Revenue -0.5% 2.3%

Non-recurring acquisition costs** $ 4 $ 0

% of Revenue 1.2% 0.0%

Adjusted EBITDA* $ 2 $ 7 -67%

% of Revenue 0.7% 2.3%

*EBITDA and Adjusted EBITDA are non-GAAP terms. See the Q-1 2013 Operating Income to EBITDA and Adjusted EBITDA Reconciliation slide.

**Includes costs related to the purchase, integration, reorganization and shutdown activities of the MDT acquisition which are not expected to recur in 2014.

SUMMARY OF RESULTS Certain amounts may not sum or recalculate due to rounding.

*Adjusted EBITDA excludes non-recurring costs related to the purchase, integration, reorganization and shutdown activities related to the MDT acquisition from EBITDA. EBITDA and Adjusted EBITDA are key

Measures used by management in evaluating performance. EBITDA and Adjusted EBITDA should not be considered a measure of financial performance in isolation or as an alternative to operating income (loss)

In the Statement of Operations in accordance with GAAP, and, as presented, may not be comparable to similarly titled measures of other companies.

Q-1 2013 OPERATING INCOME TO EBITDA AND

ADJUSTED EBITDA RECONCILIATION

Dollar amounts in millions

Q-1 2013 Q-1 2012

Income (loss) from operations $ (7) $ 2

Depreciation & amortization 5 5

EBITDA* (2) 7

Non-recurring acquisition costs 4 0

Adjusted EBITDA* $ 2 $ 7

2013 ESTIMATE – OPERATING INCOME TO EBITDA

AND ADJUSTED EBITDA RECONCILIATION

In millions

TrueBlue

Total

Income from operations 55 $ Depreciation & amortization 22

EBITDA* 77 Non-recurring costs 8

Adjusted EBITDA* 85 $

*Adjusted EBITDA excludes non-recurring costs related to the purchase, integration, reorganization and shutdown activities related to the MDT acquisition from EBITDA. EBITDA and Adjusted EBITDA are key

Measures used by management in evaluating performance. EBITDA and Adjusted EBITDA should not be considered a measure of financial performance in isolation or as an alternative to operating income (loss)

In the Statement of Operations in accordance with GAAP, and, as presented, may not be comparable to similarly titled measures of other companies.

• Specialized leader in blue-collar staffing

• Well-positioned in growing staffing market

• Significant upside as construction market rebounds

• Compelling organic growth strategies

• Successful acquisition strategy

• Strong operating leverage

• Solid capital position supports growth

TRUEBLUE INVESTMENT HIGHLIGHTS