management accounting financial statements (review & analysis) cost management budgeting cash...

TRANSCRIPT

Management Accounting

Financial Statements (review & analysis)

Cost Management

Budgeting

Cash Management

HO III – Management Accounting

Stephan DEMAEGHT

Balance Sheet presentations• Europe / USA• Country legal presentation• Internal presentation

Stephan DEMAEGHT

Financial Statements

Income Statement presentations• Legal presentation• Contribution Margin presentation• USALI presentation

Stephan DEMAEGHT

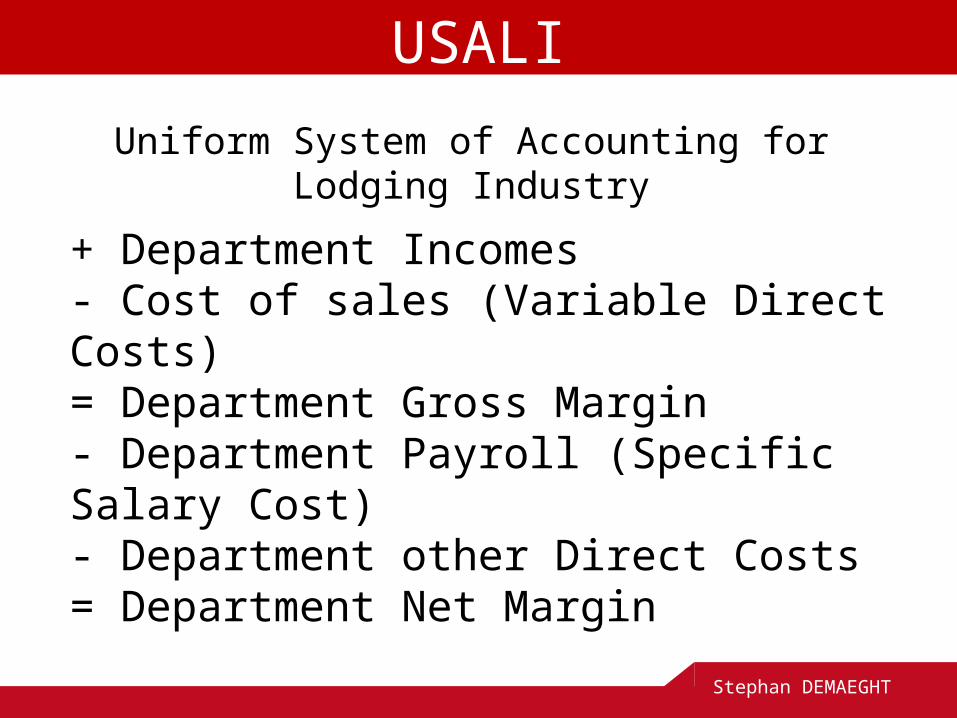

USALI

+ Department Incomes- Cost of sales (Variable Direct Costs)= Department Gross Margin- Department Payroll (Specific Salary Cost)- Department other Direct Costs= Department Net Margin

Uniform System of Accounting for Lodging Industry

Stephan DEMAEGHT

USALI∑ Department Net Margins for Operating Dpts.- ∑ Department Net Margins for Non Operating Dpts.- Undistributed Salary Cost- Undistributed Goods & Services- Undistributed other operating costs= GOP (Gross Operating Profit)- Management Fes- Rent & Property expenses= EBITDA (or NOP)+/- Financial result (+financial incomes – financial costs)- Depreciation/Amortization= Gross Ordinary Profit+/- Outstanding result (+outstand. incomes – outst. costs)= Gross Profit- Revenue Tax= NI (Net Profit or Net Income)

Ratios

• Profitability ratios (BS & IS)• Liquidity ratios (BS or BS & IS)• Investors ratios (Result from IS & Other infos)• Solvency ratios (BS)• Department ratios (need a detailed IS + extra

information)

Stephan DEMAEGHT

Financial Statements

COST MANAGEMENT

Where are the costs?

Cost Management

Stephan DEMAEGHT

Direct & Indirect Cost

• Direct Cost: linked to ONE particular department/division/product.

• Indirect Cost: linked to more than one particular department/division/product

Stephan DEMAEGHT

Cost Management

The same cost can be direct or indirect in function of the company.

• Fast-food restaurant:– Only hamburger and cheeseburger: cheese is

a direct cost for the product “cheeseburger”– Hamburger + cheeseburger + special cheese:

cheese is an indirect cost (for 2 products).• Hotel:

– Most probably, the cheese will be a direct cost for the department “kitchen”.

Stephan DEMAEGHT

Cost Management

Fast Food• Hamburger: bread + meat +

ketchup + mustard• Cheese: bread + meat +

cheese + ketchup + mustard• Big Bacon: bread + big meat +

cheese + barbecue sauce + bacon

• King Fish: bread + fish + tartar sauce + cheese

• Chicken Burger : bread + chicken + salad + pepper sauce

• Bread• Meat 100 gr• Meat 200 gr• Fish stick• Chicken filet• Cheese• Bacon• Salad• Ketchup• Mustard• Tartar sauce• Pepper sauce

Stephan DEMAEGHT

Cost Management

Indirect costs splitting

• As a % of the sales (food cost, advertising,…)• Per m2 occupied (fire insurance, interests for

mortgage loan, building depreciation,…)• Estimating labor time (salaries, social security,

…)• …

Stephan DEMAEGHT

Cost Management

Fixed & Variable Cost

• Fixed cost: doesn't change with sales revenues fluctuation.

• Variable cost: change in direct proportion of the sales revenues.

• Semi Fixed or Semi Variable costs: not directly variable with revenues but not strictly fixed

Stephan DEMAEGHT

Cost Management

Fast Food• Meat, cheese, fish sticks, bread, salad, sauces,...(food cost)

• Restaurant Manager Salary.• Restaurant Assistants Manager salaries.• Crew salaries.• Restaurant rent.• Kitchen furniture's renting.• Electricity.• Phone invoices.• Administration furniture's.• Bags, boxes and packing papers.• Cleaning products.• Fire insurance.

Stephan DEMAEGHT

Cost Management

How to split Total Costs into FC & VC?

Linear regression

Stephan DEMAEGHT

Cost Management

CVPThe

Cost – Volume – Profit Method

Stephan DEMAEGHT

Cost Management

Formula

• Sales = Total Costs + Profit• Sales = Fixed C. + Variable C. + GP• Sales = FC + (VC% * Sales) + GP• Sales – (VC% * Sales) = FC + GP• Sales * (1 – VC%) = FC + GP• Sales = (FC + GP) / (1 – VC. %)

Stephan DEMAEGHT

Cost Management

Formula

Sales = (FC + GP) / (1 - VC%)

Where: 1-VC% = Contribution Margin

Stephan DEMAEGHT

Cost Management

Break-Even Point

• It’s the Sales Revenue Level necessary to cover all operating costs.

• Below the Break-Even Point, you are loosing money. Above the BEP, you are winning.

• At the Break-Even Point: Fixed Costs + Variable Costs = Sales

Stephan DEMAEGHT

Cost Management

From CVP to BEP

Sales = (FC + GP) / (1-VC%)

at BEP, GP = 0

Sales = FC / (1-VC%)

Stephan DEMAEGHT

Cost Management

At Break Even Point:

Sales = FC/(1-VC%)

Stephan DEMAEGHT

Cost Management

Forecasting Incomes Required

Profit Wanted = GP

Sales = (FC + GP) / (1- VC%)

Sales = (150.000 + 50.000) / 0,63

Sales = 317.460 euros

Stephan DEMAEGHT

Cost Management

By how much Room Sales Revenue increase to cover a

new fixed cost?

New Sales Revenue= (original FC + additional FC + GP)

/ (1 – VC%)

Cost Management

Stephan DEMAEGHT

By how much Room Sales revenue increase to cover a

new investment?

New Sales Revenue= (FC + Investment Depreciation + GP)

/ (1 – VC%)

Cost Management

Stephan DEMAEGHT

How much Room Sales revenue increase to get a new GP?

New Sales Revenue= (FC + New GP) / (1 – VC%)

Or = (FC + original GP + additional GP)

/ (1- VC%)

Cost Management

Stephan DEMAEGHT

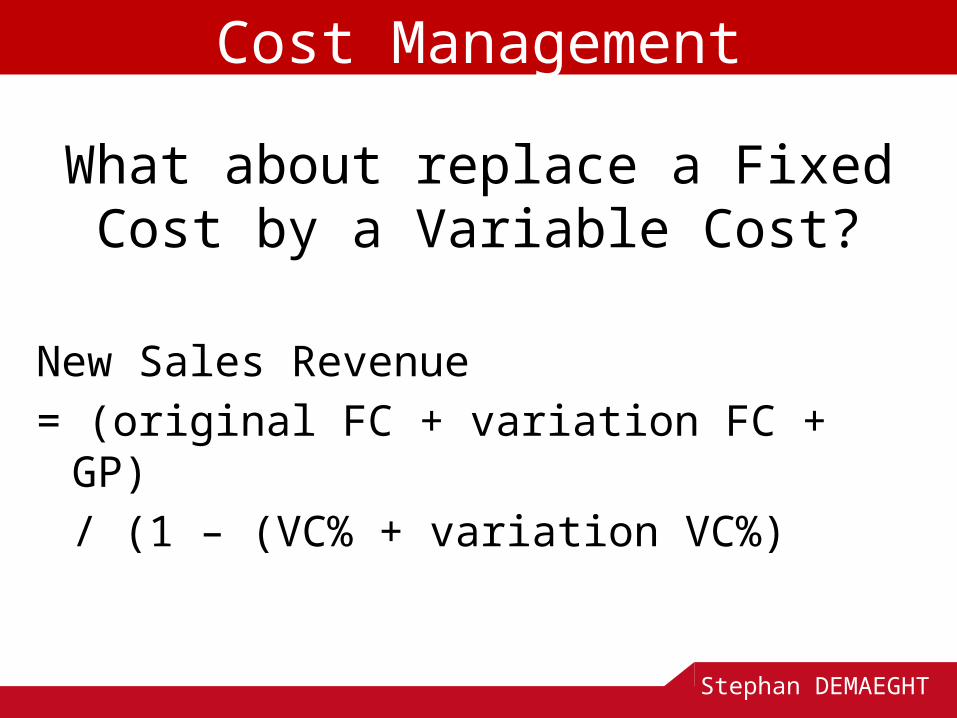

What about replace a Fixed Cost by a Variable Cost?

New Sales Revenue= (original FC + variation FC + GP)

/ (1 – (VC% + variation VC%)

Cost Management

Stephan DEMAEGHT

Income Statement Sales- Variable Costs

= Gross Margin- Fixed Costs

= Gross Profit- Revenue Tax

= Net Income

Cost Management

Stephan DEMAEGHT

Taxes effect

Net Income = GP – Tax

GP = NI + Tax

CVP Formula:

Sales = (FC + GP) / (1-VC%)

Sales = (FC + Net Income + Tax) / (1-VC%)

Cost Management

Stephan DEMAEGHT

Taxes rate

GP = NI + Tax (where Tax = GP * TR)

GP = NI + (GP * Tr)

GP – (GP * Tr) = NI

GP (1 – Tr) = NI

GP = NI / (1- Tr)

CVP Formula:

Sales = (FC + GP) / (1-VC%)

Sales = FC + (NI / (1 – Tr)) / (1-VC%)

Cost Management

Stephan DEMAEGHT

FC ∆ FC + ∆ GOP ∆ NI

BEP u = -------- ∆ SALES = ------------------- ∆ GOP = ----------

CMu 1 – VC% 1 - TR

FC FC + GOP NI

BEP = ------------- SALES = --------------- GOP = ---------

1 – VC% 1 – VC% 1 – TR

CM = 1 – VC% SALES

VC = VC% * Sales -VC

= GM

VC% = VC / Sales - FC

= GOP

Taxes = Tr * GOP -Taxes

= NI

Tr = Taxes/GOP

Stephan DEMAEGHT

Cost Management

Stephan DEMAEGHT

Cost Management

∆FC

∆FC + ∆GP ∆GP1-VC% ∆NI

New Sales Orig. Sales 1-Tr- Orig. Sales + ∆S ∆NI

= ∆S = New SalesFC + GP1-VC% NI

NI1-Tr

VC GP Rev. TaxSales GP

∆GP =

GP =

∆NI = New NI - Orig. NI

∆GP = New GP - Orig. GP

Tr =

∆S

Sales =S

VC%=

∆Sales =

Exercises

E.8.1 to E.8.9

P.8.1 to P.8.12

Cost Management

Stephan DEMAEGHT

BUDGETING

Budgeting

Stephan DEMAEGHT

Types of Budgets• Operating (sales & expenses analyze) or Pre-

Opening (Operating before opening) Budget.• Long Term (1 to 5 years) & Short Term (<1 year)

Budget.• Fixed (based on a certain activity level ) or Flexible

(including several activity levels) Budget.• Department Budget (limited to a specific dpt.) • Capital Budget (plan on several years to analyze a

new investment).• Master Budget (Sum of various previous budgets).

Budgeting

Stephan DEMAEGHT

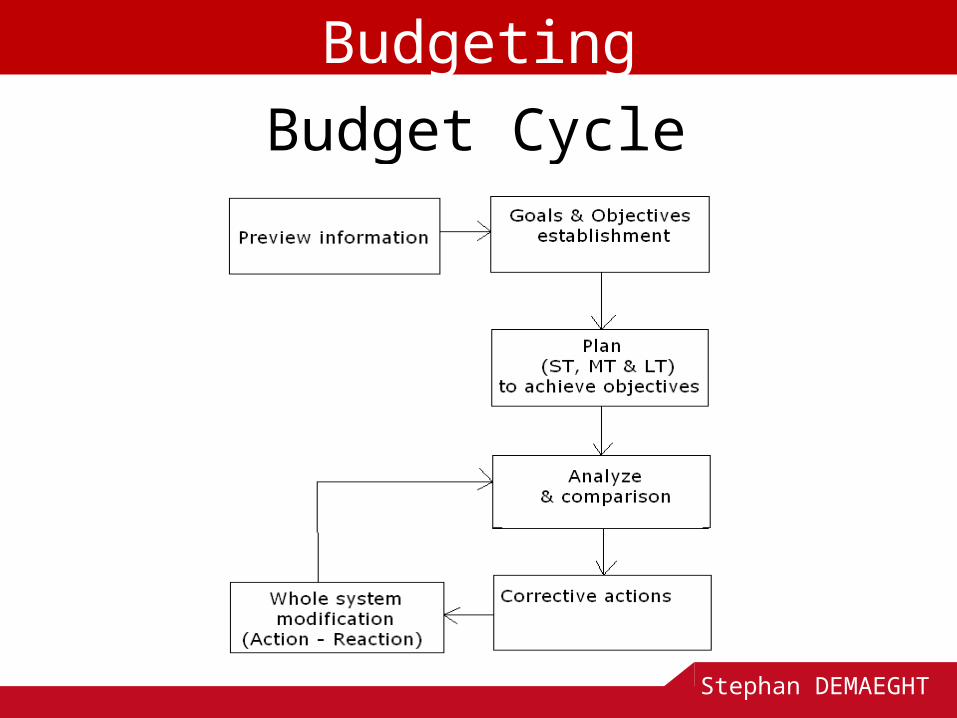

Budget Cycle

Budgeting

Stephan DEMAEGHT

Goals & Objectives establishment.

• Prudence and realism.• Real limiting factors:

– Number of rooms in a hotel.– Number of seats in a restaurant.– Staff productivity and quality.– Link between wage conditions and available

staff (you have the staff quality you pay for).– Customer demand and competition.

Budgeting

Stephan DEMAEGHT

Plan to achieve objectives.

• Meeting and stimulate the staff.• Order food, beverage and goods (quality

and quantity) to achieve sales forecasting.• Financial plans to achieve budget.

Budgeting

Stephan DEMAEGHT

Analyze & comparison

• Analyze differences between budget and actual results, explain, comment and assign responsibilities.

• Use the Comparative Horizontal Analysis.

Budgeting

Stephan DEMAEGHT

Variances

Budgeting

Stephan DEMAEGHT

ActualBudget

Pb

VrVb

Pr Price Variance: (Pr-Pb) * Vr

VolumeVariance = (Vr-Vb)* Pb

Variance Analysis• Price Variance:

– Real Average Check – Budget Av. Ch.• Sales Volume Variance:

– Sold Units – Sales Quantities Budgeted• Percentage Variance:

– Variance / Budgeted Figure• Cost Variance:

– Same as Price & Sales Volume variances but for the costs.

Budgeting

Stephan DEMAEGHT

Corrective actions• Changes to reach the budget (staff

motivation, advertising, improve communication, staff changes,…)

• Forecasting changes (change the prices, modify goals or objectives,…) to modify the budget

• !!!When you change one element of a structure, you change the whole structure!!

Budgeting

Stephan DEMAEGHT

Improve the budget

• Information provided from past budgeting cycles will help you to budget the future.

• Never forget we work with people, not only with numbers.

• Action – Reaction (you never finish).

Budgeting

Stephan DEMAEGHT

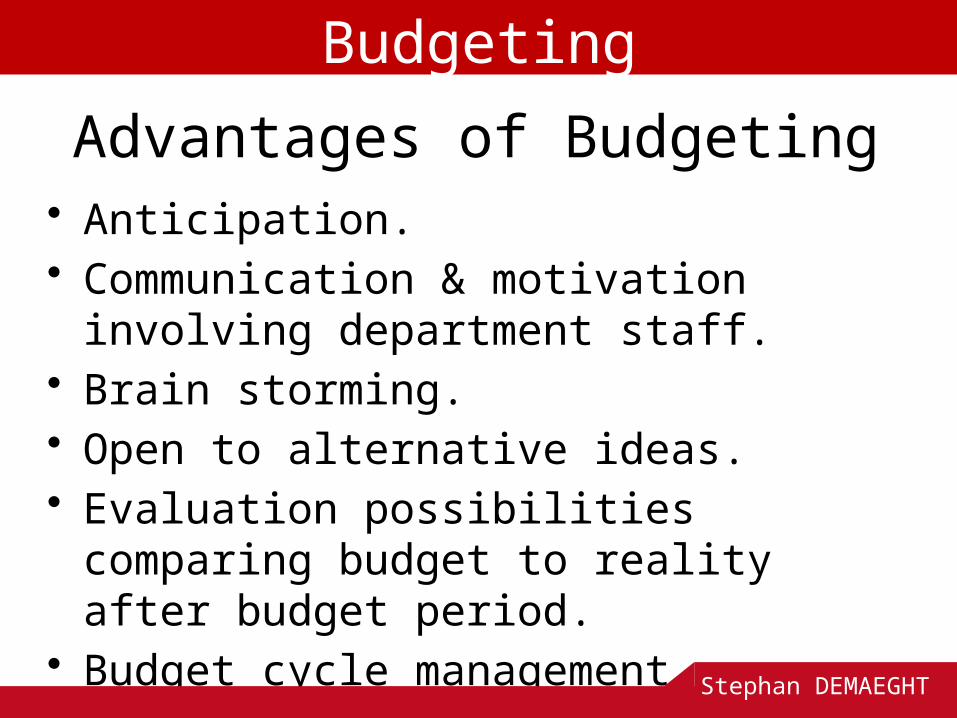

Advantages of Budgeting• Anticipation.• Communication & motivation involving

department staff.• Brain storming.• Open to alternative ideas.• Evaluation possibilities comparing budget

to reality after budget period.• Budget cycle management.

Budgeting

Stephan DEMAEGHT

Disadvantages of Budgeting• Time & cost to prepare budgets.• Many unknown factors.• Could oblige to give confidential

information before requirement.• Tendency to spend to the budget (in big

structures) or to overspend with the objective to increase expenses forecasting in next budget.

Budgeting

Stephan DEMAEGHT

Read & learn Advantages and disadvantages of Budgeting in

the book pages 372 & 373.

Budgeting

Stephan DEMAEGHT

Cash Management

Cash Flow

&

Working Capital

Cash Management

Stephan DEMAEGHT

Importance of Cash Management

• Difference between Net Income and Cash Flows (inflows – outflows)

• To be able to pay what you have to.• Cash forecasting.

Cash Management

Stephan DEMAEGHT

Total Cash Flow

Total Cash Flow

= Net Cash Flow from Operating Activities

+ Net Cash Flow from Investing Activities

+ Net Cash Flow from Financing Activities

Cash Management

Stephan DEMAEGHT

Cash Flow from Operating Act.Net CF from Op activities= NI + not paid charges – not received sales

Net Cash Flow from Operating Activities= Net Income+ Current Assets Decreases- Current Assets Increases+ Current Liabilities Increases- Current Liabilities Decreases+ Depreciation / Amortization Expenses

Cash Management

Stephan DEMAEGHT

Cash Flow from Investing Act.

Net Cash Flow from Investing Activities

= Sales of Fixed Assets

- Purchase of Fixed Assets

Cash Management

Stephan DEMAEGHT

Cash Flow from Financing Act.

Net Cash Flow from Financing Activities

= Long Term Liabilities Increases- Long Term Liabilities Decreases- Dividends Paid

+ Equity Capital Increases

- Equity Capital Decreases

Cash Management

Stephan DEMAEGHT

Exercises

• Book pages 452 – 461• E.10.1 to E.10.3• P.10.1 to P.10.2• P.10.4 • P.10.7

Cash Management

Stephan DEMAEGHT

Working Capital

Working Capital

= Current assets – Current Liabilities.

Statement of Changes in Working Capital is very similar to the Statement of Cash Flow.

Cash Management

Stephan DEMAEGHT

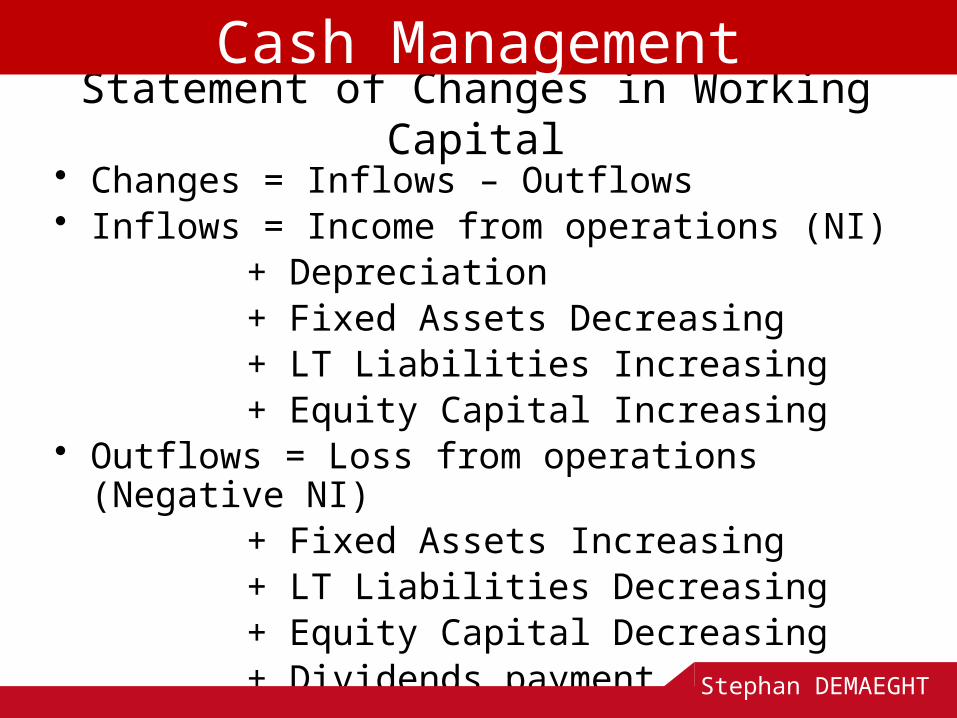

Statement of Changes in Working Capital• Changes = Inflows – Outflows• Inflows = Income from operations (NI)

+ Depreciation+ Fixed Assets Decreasing+ LT Liabilities Increasing+ Equity Capital Increasing

• Outflows = Loss from operations (Negative NI)+ Fixed Assets Increasing+ LT Liabilities Decreasing+ Equity Capital Decreasing+ Dividends payment

Cash Management

Stephan DEMAEGHT

Preparing Cash BudgetCash Receipts= Current month cash sales revenue+ Current month credit card receivable collections+ Previous month credit card receivable collections+ Previous month accounts receivable collectionsCash Disbursements= Current month cash purchases+ Previous month account payableNet Cash = Cash Receipts – Cash Disbursements

Cash Management

Stephan DEMAEGHT

Exercises

• Book p. 486- 487: E.11.7 to E.11.9• Book p. 487- 488: P.11.1 to P.11.5

Cash Management

Stephan DEMAEGHT