making investment decisions

TRANSCRIPT

3.6 Making 3.6 Making investment investment decisionsdecisions

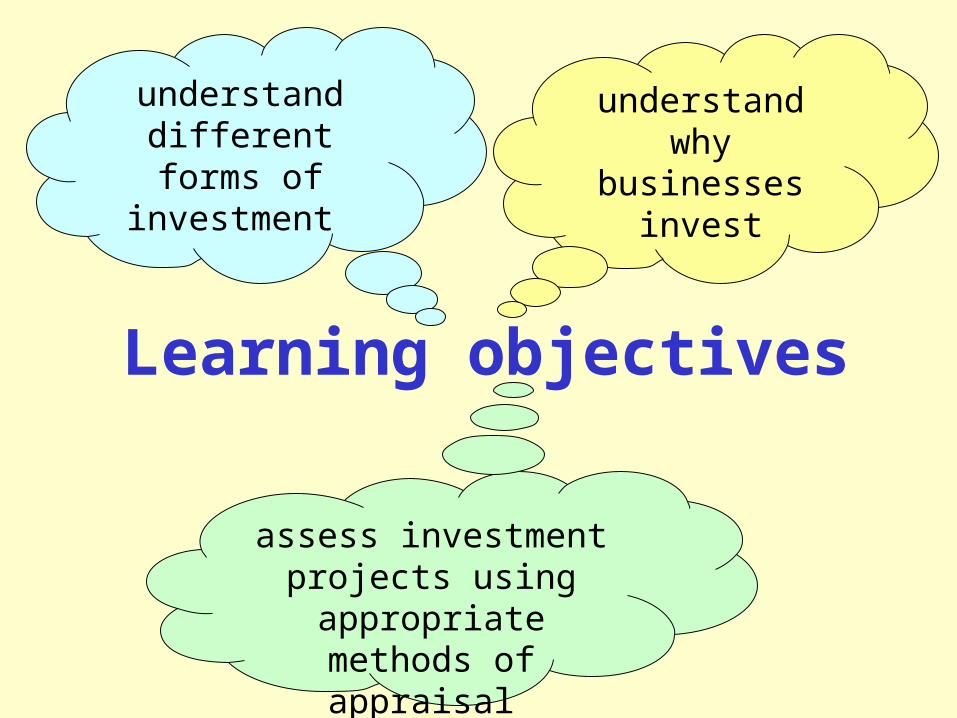

Learning objectives

understand different forms of investment

understand why

businesses invest

assess investment projects using

appropriate methods of appraisal

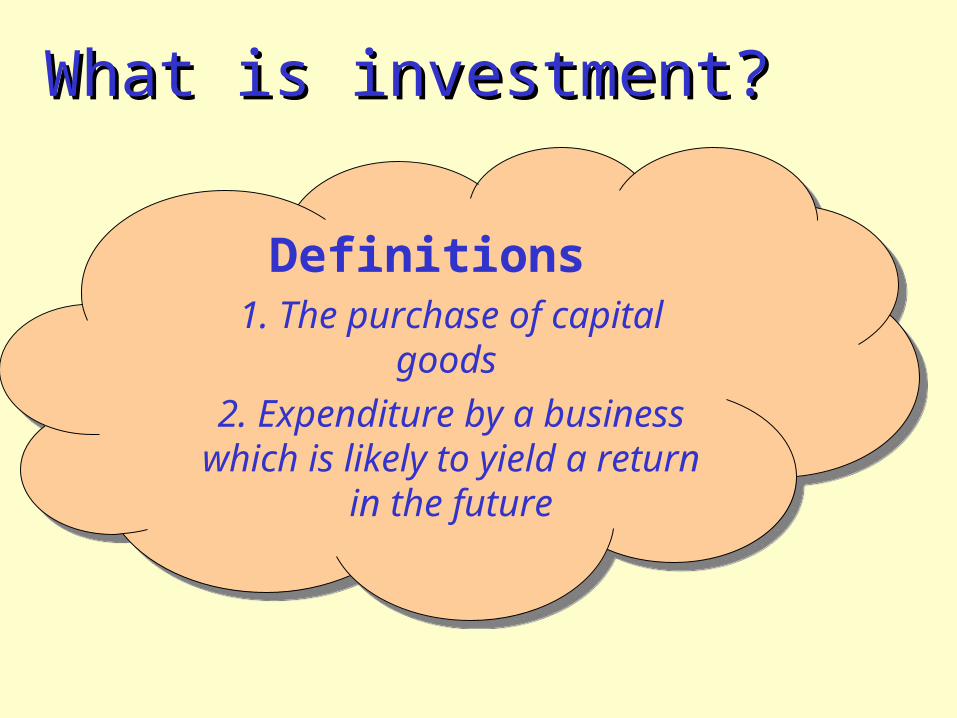

What is investment?What is investment?

Definitions1. The purchase of capital

goods 2. Expenditure by a

business which is likely to yield a return in the future

Definitions1. The purchase of capital

goods 2. Expenditure by a

business which is likely to yield a return in the future

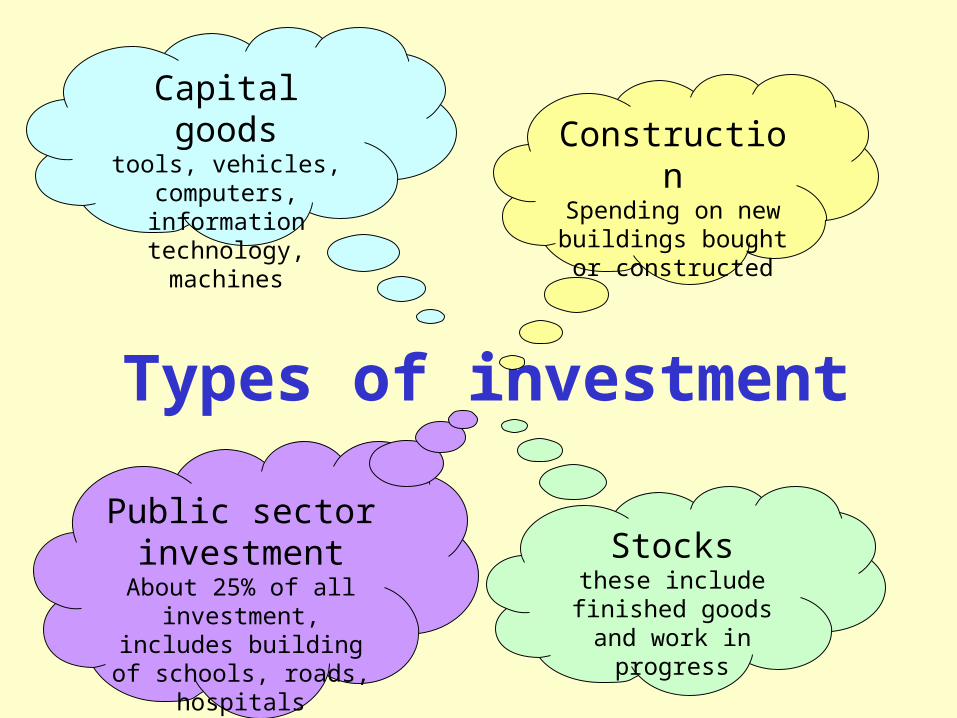

Types of investment

Capital goodstools, vehicles,

computers, information technology, machines

ConstructionSpending on new buildings bought or constructed

Stocksthese include

finished goods and work in progress

Public sector investmentAbout 25% of all

investment, includes building of schools,

roads, hospitals

Reasons for investment

To replace work out / obsolete

equipment

To replace work out / obsolete

equipment For research and

investment

For research and

investment

To minimise costs or improve quality

To minimise costs or improve quality

To grow the business

this can be organic growth or acquisitions

To grow the business

this can be organic growth or acquisitions

Factors affecting Factors affecting investmentinvestment

INVESTMENT DECISION

?

MOTIVES

BUSINESS CONFIDENCE

EXTERNAL FACTORS

COST REVENUE

RETURN

Investment appraisalInvestment appraisal

DefinitionHow a private sector

business might objectively evaluate an investment

project to decide:-whether or not it is

profitable-make comparisons between

different investment projects

DefinitionHow a private sector

business might objectively evaluate an investment

project to decide:-whether or not it is

profitable-make comparisons between

different investment projects

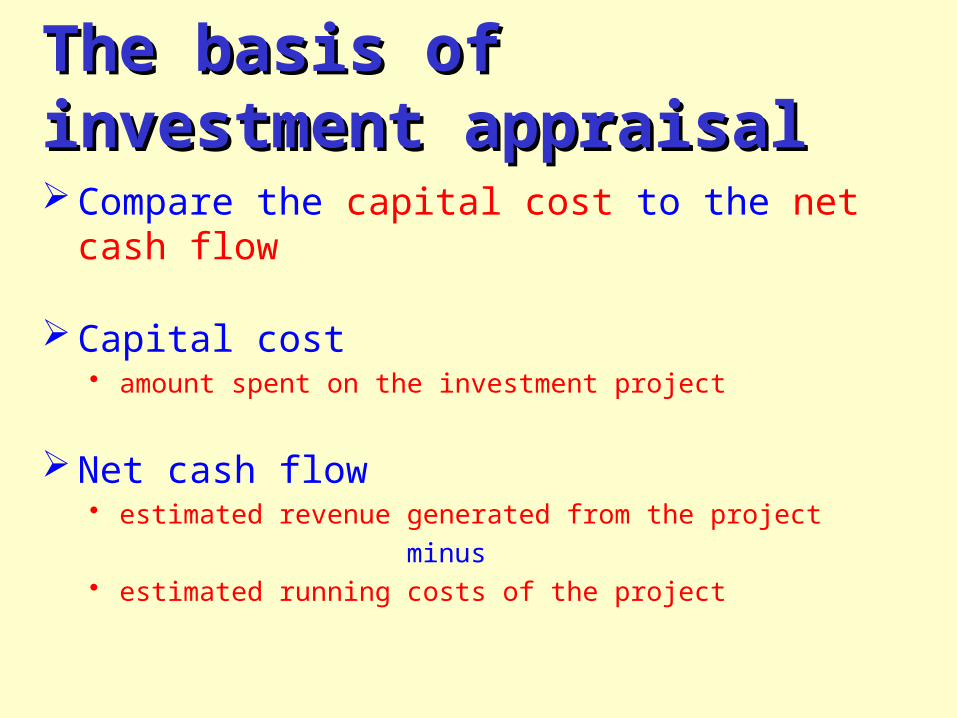

The basis of investment The basis of investment appraisalappraisalCompare the capital cost to the net cash

flow

Capital cost amount spent on the investment project

Net cash flow estimated revenue generated from the project

minus estimated running costs of the project

Methods of appraisal

Payback period

the amount of time it takes for the

project to payback initial outlay

Payback period

the amount of time it takes for the

project to payback initial outlay

Average rate of return

measures the met return each year as

a percentage of capital cost

Average rate of return

measures the met return each year as

a percentage of capital cost

Net present valuewhat the cash flow or profit earned

in the future is worth in today’s money

Net present valuewhat the cash flow or profit earned

in the future is worth in today’s money

Payback period – method 1

Estimate net cash flow

Estimate net cash flow Calculate

cumulative net cash flow

cash flow in each year adjusted for cost of the

project

Calculate cumulative net

cash flowcash flow in each year adjusted for cost of the

project

Calculate payback periodfound when cumulative net cash

flow is zero

Calculate payback periodfound when cumulative net cash

flow is zero

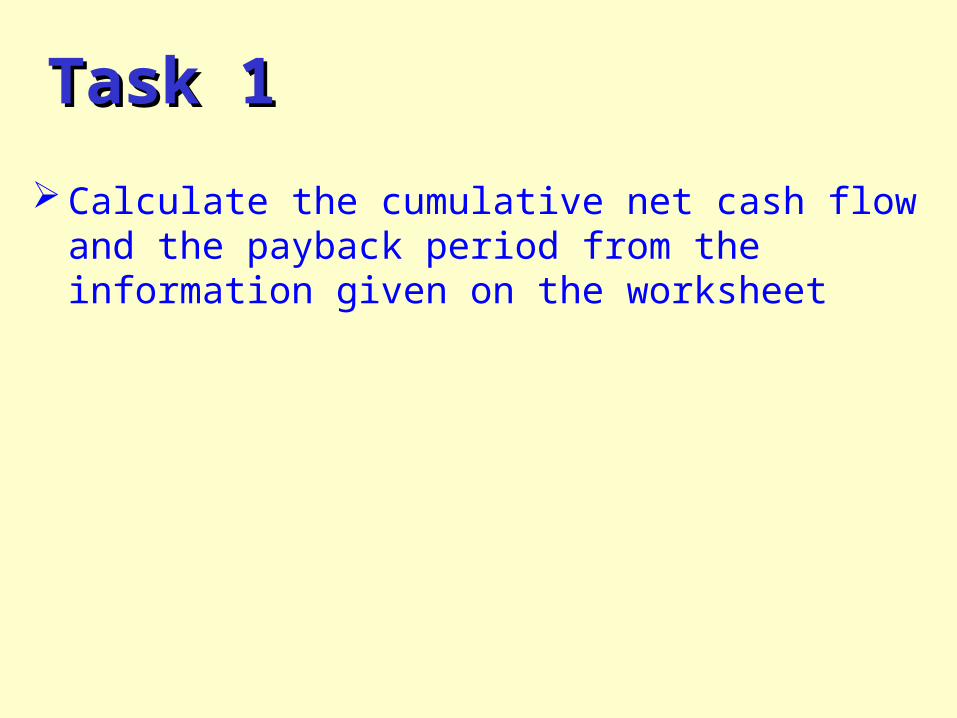

Calculate the cumulative net cash flow and the payback period from the information given on the worksheet

Task 1Task 1

Payback period – method 2

Find year before project

pays back

Find year before project

pays backCalculate ‘amount

required’ to payback

equals cumulative cash flow for that year = cost of project – sum of net

cash flows

Calculate ‘amount

required’ to payback

equals cumulative cash flow for that year = cost of project – sum of net

cash flows

Add remaining months to year

remaining months = amount required / net cash flow in year of

payback x 12

Add remaining months to year

remaining months = amount required / net cash flow in year of

payback x 12

An alternative ‘formula’ for calculating payback is

Years = last year in which cumulative cash flow is negative

Months =

Payback - alternativePayback - alternative

12 after yearin flow cash Net

flow cash cumulative negative Last

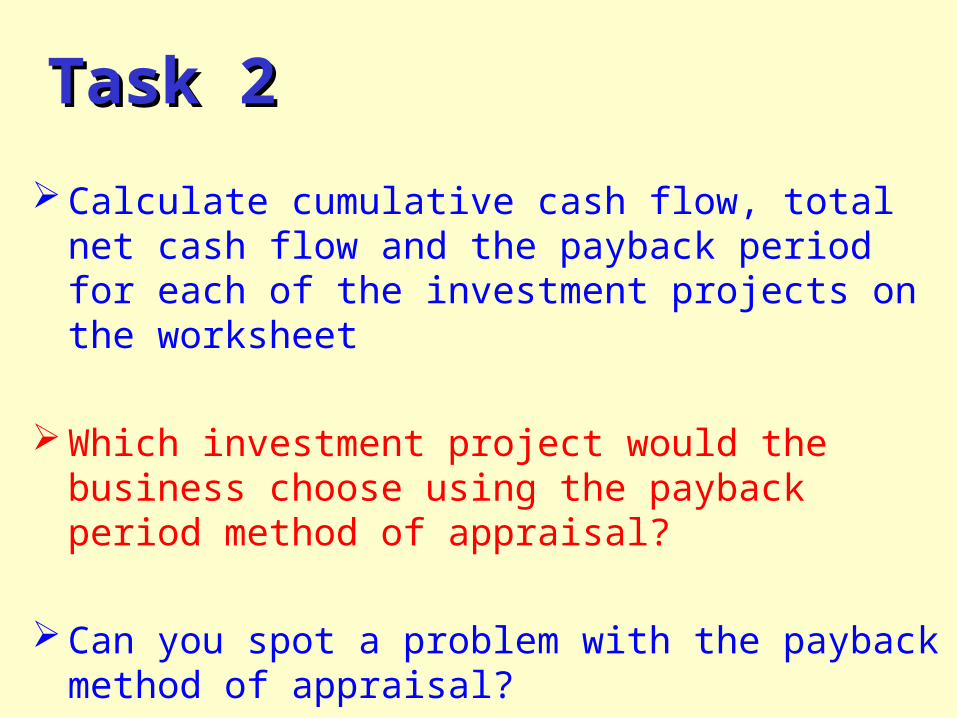

Calculate cumulative cash flow, total net cash flow and the payback period for each of the investment projects on the worksheet

Which investment project would the business choose using the payback period method of appraisal?

Can you spot a problem with the payback method of appraisal?

Task 2Task 2

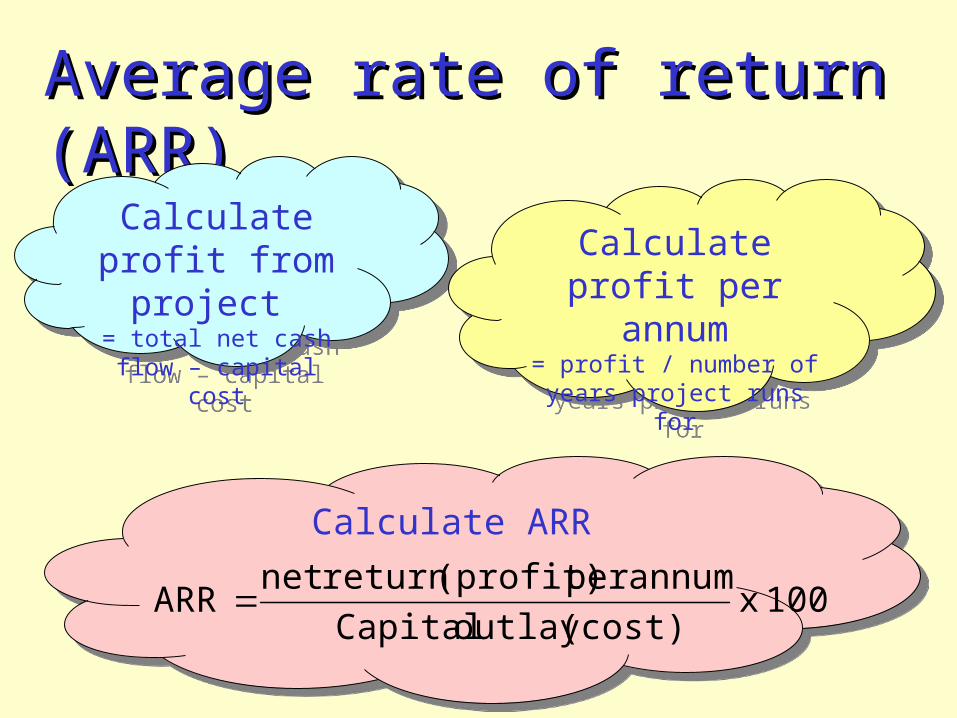

Average rate of return Average rate of return (ARR)(ARR)

Calculate profit from

project = total net cash flow

– capital cost

Calculate profit from

project = total net cash flow

– capital cost

Calculate profit per annum

= profit / number of years project runs for

Calculate profit per annum

= profit / number of years project runs for

Calculate ARRCalculate ARR

100 x (cost) outlay Capital

annum per (profit) return net ARR

Calculate the ARR for the three investment projects on the worksheet.

Which investment project should the business choose?

Task 3Task 3

Advantages and Advantages and disadvantagesdisadvantages

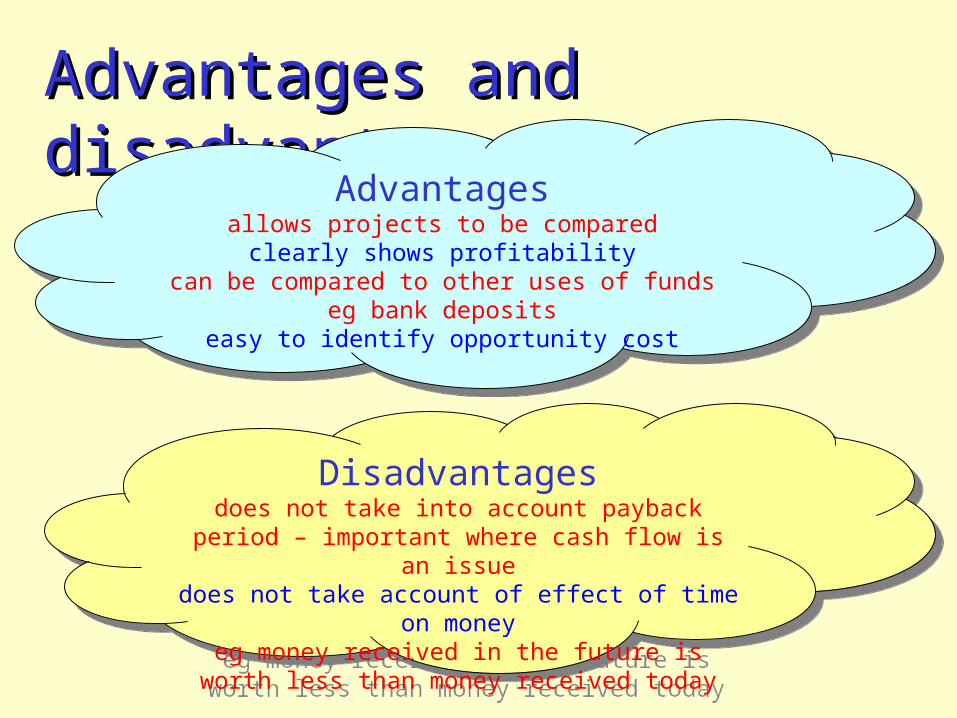

Advantagesallows projects to be compared

clearly shows profitabilitycan be compared to other uses of funds eg

bank depositseasy to identify opportunity cost

Advantagesallows projects to be compared

clearly shows profitabilitycan be compared to other uses of funds eg

bank depositseasy to identify opportunity cost

Disadvantagesdoes not take into account payback period –

important where cash flow is an issuedoes not take account of effect of time on

moneyeg money received in the future is worth less

than money received today

Disadvantagesdoes not take into account payback period –

important where cash flow is an issuedoes not take account of effect of time on

moneyeg money received in the future is worth less

than money received today

Net present value Net present value (NPV)(NPV)The underlying principle of the NPV

technique is that money received in the future is worth less that money received today

To understand this idea you should calculate the compound value of £100 invested over 5 years at a rate of interest of 10% what is £100 worth in 5 years time? what is £133 in three year’s time worth

today?

Net present value (NPV)Net present value (NPV)

Calculate present values of annual net

cash flows= discounted net cash

flows

Calculate present values of annual net

cash flows= discounted net cash

flows

Sum the present values

(discounted net cash

flows)

Sum the present values

(discounted net cash

flows)

Calculate NPV= total present values – initial cost of

investment

Calculate NPV= total present values – initial cost of

investment

Advantages and Advantages and disadvantagesdisadvantages

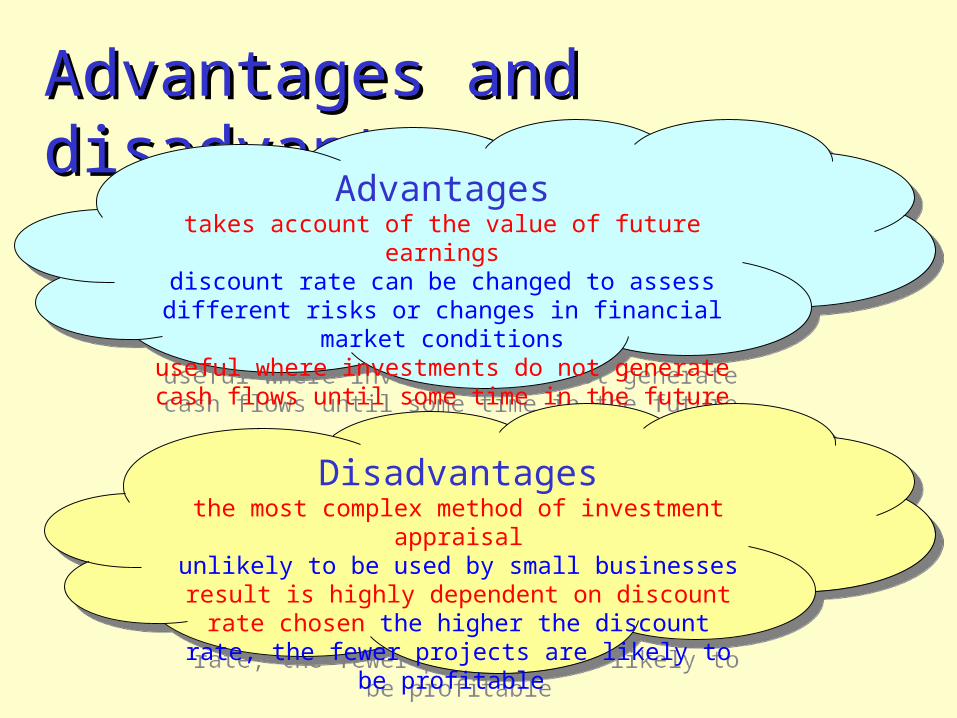

Advantagestakes account of the value of future earnings

discount rate can be changed to assess different risks or changes in financial market

conditionsuseful where investments do not generate cash

flows until some time in the future

Advantagestakes account of the value of future earnings

discount rate can be changed to assess different risks or changes in financial market

conditionsuseful where investments do not generate cash

flows until some time in the future

Disadvantagesthe most complex method of investment

appraisalunlikely to be used by small businesses

result is highly dependent on discount rate chosen the higher the discount rate, the fewer

projects are likely to be profitable

Disadvantagesthe most complex method of investment

appraisalunlikely to be used by small businesses

result is highly dependent on discount rate chosen the higher the discount rate, the fewer

projects are likely to be profitable