maintaining financial records and preparing accounts (fra) … · 2008-08-15 · maintaining...

TRANSCRIPT

Maintaining Financial Records and Preparing Accounts (FRA) (2003 Standards) Answers SECTION 1

Task 1.1

Purchases ledger control account

Bank 48,665 Opening balance 12,000

Closing balance 11,835 Credit purchases 48,500

60,500 60,500

Task 1.2 Credit purchases £48,500 Cash purchases £ 1,200 Total purchases £49,700 Task 1.3 Depreciation Cost November 2000 £6,000 Depreciation 2000-1, 15% reducing balance (£900) £900 Net Book Value October 2001 £5,100 Depreciation 2001-2, 15% reducing balance (£765) £765 Net Book Value October 2002 £4,335 Total depreciation £1,665

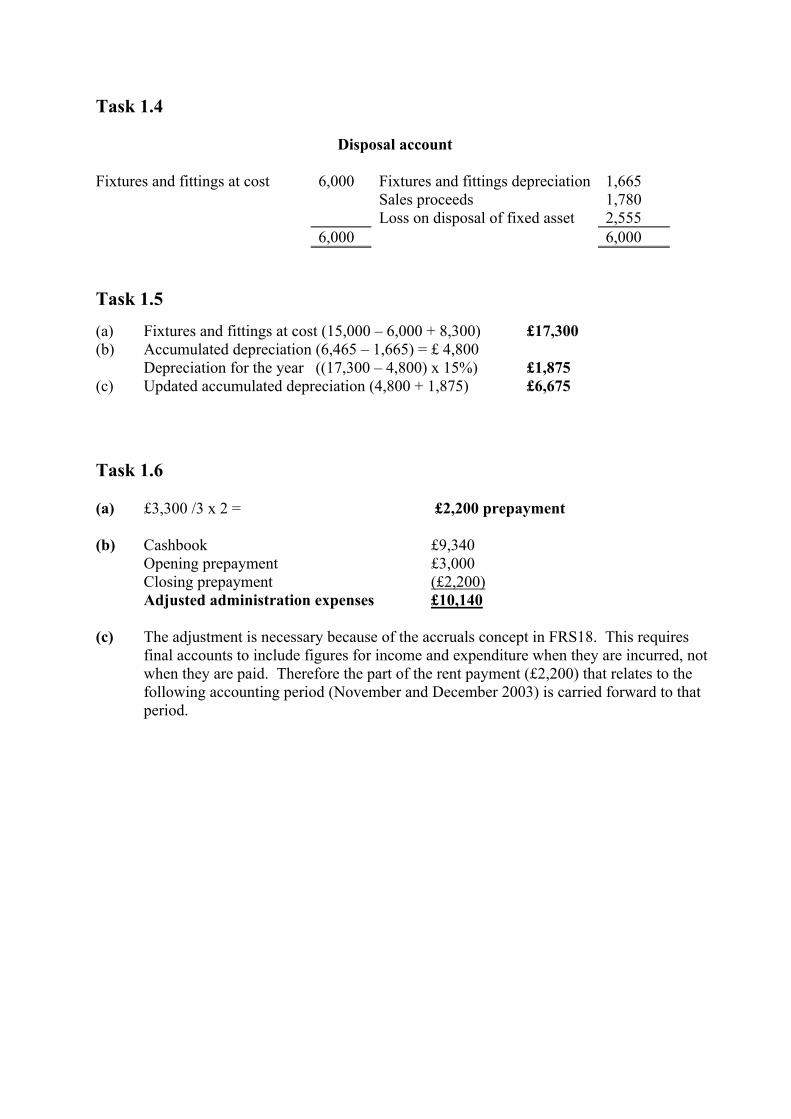

Task 1.4

Disposal account

Fixtures and fittings at cost 6,000 Fixtures and fittings depreciation 1,665 Sales proceeds 1,780 Loss on disposal of fixed asset 2,555 6,000 6,000

Task 1.5 (a) Fixtures and fittings at cost (15,000 – 6,000 + 8,300) £17,300 (b) Accumulated depreciation (6,465 – 1,665) = £ 4,800

Depreciation for the year ((17,300 – 4,800) x 15%) £1,875 (c) Updated accumulated depreciation (4,800 + 1,875) £6,675

Task 1.6 (a) £3,300 /3 x 2 = £2,200 prepayment (b) Cashbook £9,340

Opening prepayment £3,000 Closing prepayment (£2,200) Adjusted administration expenses £10,140

(c) The adjustment is necessary because of the accruals concept in FRS18. This requires

final accounts to include figures for income and expenditure when they are incurred, not when they are paid. Therefore the part of the rent payment (£2,200) that relates to the following accounting period (November and December 2003) is carried forward to that period.

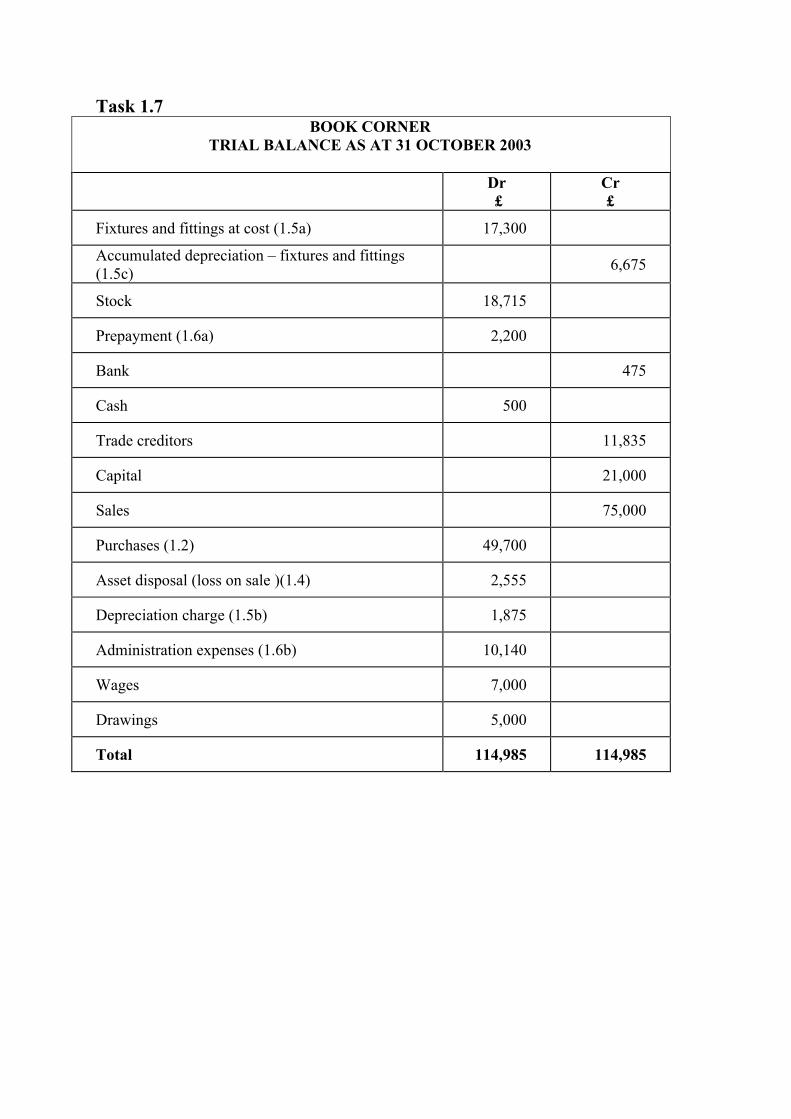

Task 1.7 BOOK CORNER

TRIAL BALANCE AS AT 31 OCTOBER 2003

Dr £

Cr £

Fixtures and fittings at cost (1.5a) 17,300

Accumulated depreciation – fixtures and fittings (1.5c) 6,675

Stock 18,715

Prepayment (1.6a) 2,200

Bank 475

Cash 500

Trade creditors 11,835

Capital 21,000

Sales 75,000

Purchases (1.2) 49,700

Asset disposal (loss on sale )(1.4) 2,555

Depreciation charge (1.5b) 1,875

Administration expenses (1.6b) 10,140

Wages 7,000

Drawings 5,000

Total 114,985 114,985

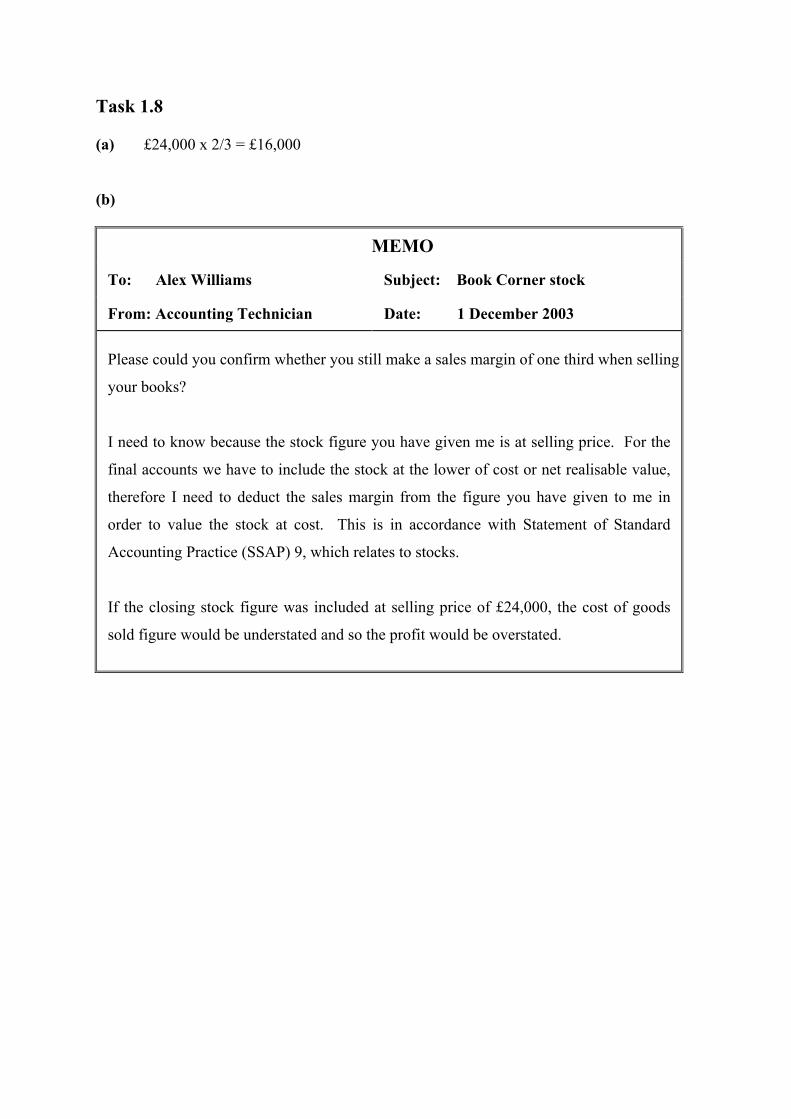

Task 1.8 (a) £24,000 x 2/3 = £16,000 (b)

MEMO

To: Alex Williams Subject: Book Corner stock

From: Accounting Technician Date: 1 December 2003

Please could you confirm whether you still make a sales margin of one third when selling

your books?

I need to know because the stock figure you have given me is at selling price. For the

final accounts we have to include the stock at the lower of cost or net realisable value,

therefore I need to deduct the sales margin from the figure you have given to me in

order to value the stock at cost. This is in accordance with Statement of Standard

Accounting Practice (SSAP) 9, which relates to stocks.

If the closing stock figure was included at selling price of £24,000, the cost of goods

sold figure would be understated and so the profit would be overstated.

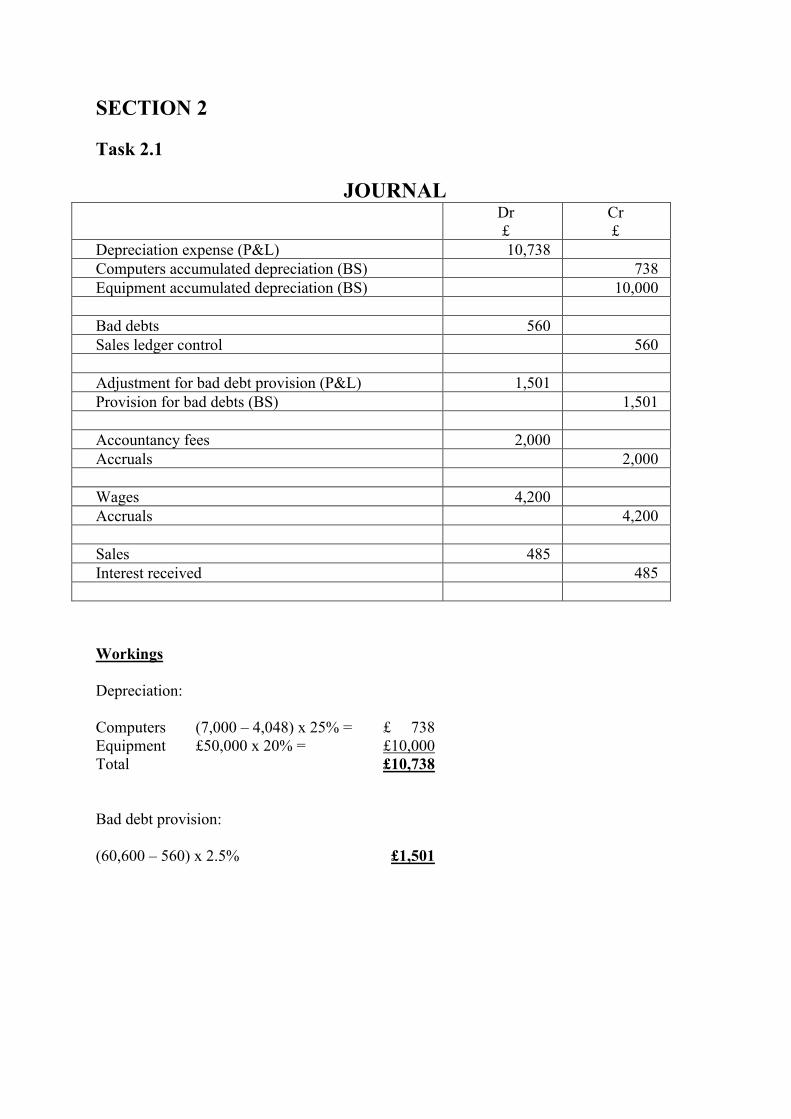

SECTION 2 Task 2.1

JOURNAL

Dr £

Cr £

Depreciation expense (P&L) 10,738 Computers accumulated depreciation (BS) 738 Equipment accumulated depreciation (BS) 10,000 Bad debts 560 Sales ledger control 560 Adjustment for bad debt provision (P&L) 1,501 Provision for bad debts (BS) 1,501 Accountancy fees 2,000 Accruals 2,000 Wages 4,200 Accruals 4,200 Sales 485 Interest received 485

Workings Depreciation: Computers (7,000 – 4,048) x 25% = £ 738 Equipment £50,000 x 20% = £10,000 Total £10,738 Bad debt provision: (60,600 – 560) x 2.5% £1,501

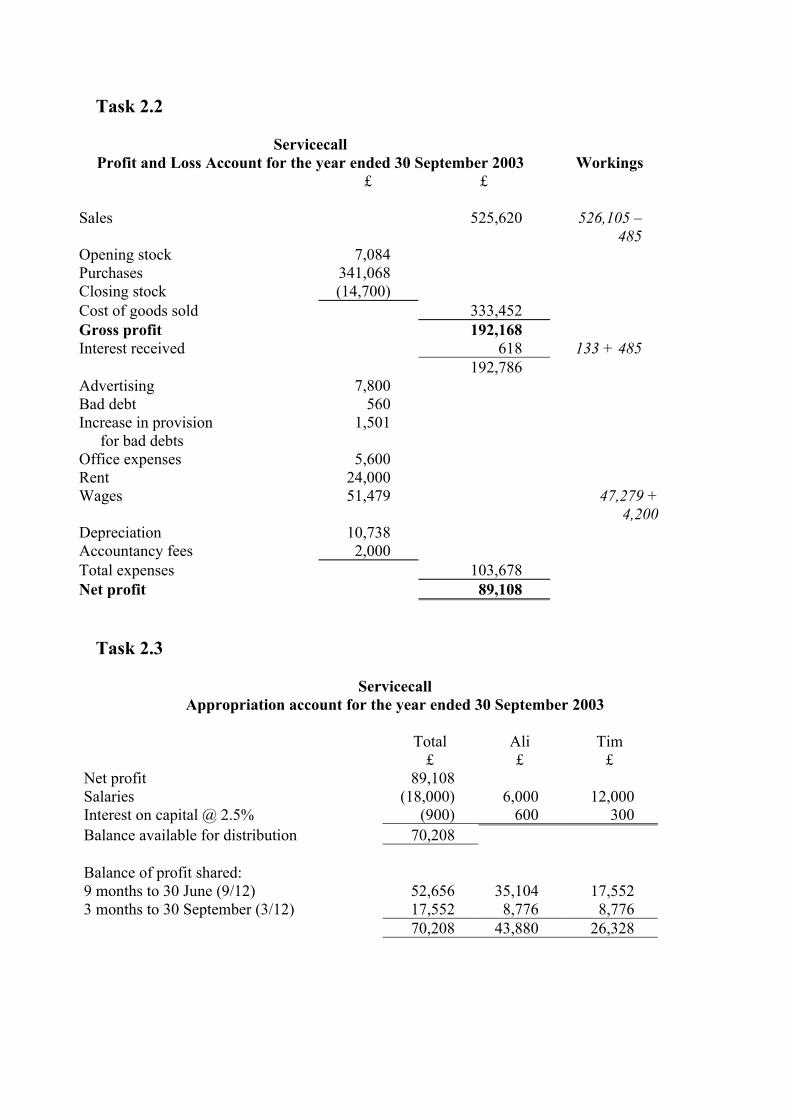

Task 2.2

Servicecall Profit and Loss Account for the year ended 30 September 2003 Workings

£ £ Sales 525,620 526,105 –

485 Opening stock 7,084 Purchases 341,068 Closing stock (14,700) Cost of goods sold 333,452 Gross profit 192,168 Interest received 618 133 + 485 192,786 Advertising 7,800 Bad debt 560 Increase in provision

for bad debts 1,501

Office expenses 5,600 Rent 24,000 Wages 51,479 47,279 +

4,200 Depreciation 10,738 Accountancy fees 2,000 Total expenses 103,678 Net profit 89,108

Task 2.3

Servicecall Appropriation account for the year ended 30 September 2003

Total Ali Tim

£ £ £ Net profit 89,108 Salaries (18,000) 6,000 12,000 Interest on capital @ 2.5% (900) 600 300 Balance available for distribution 70,208 Balance of profit shared: 9 months to 30 June (9/12) 52,656 35,104 17,552 3 months to 30 September (3/12) 17,552 8,776 8,776

70,208 43,880 26,328

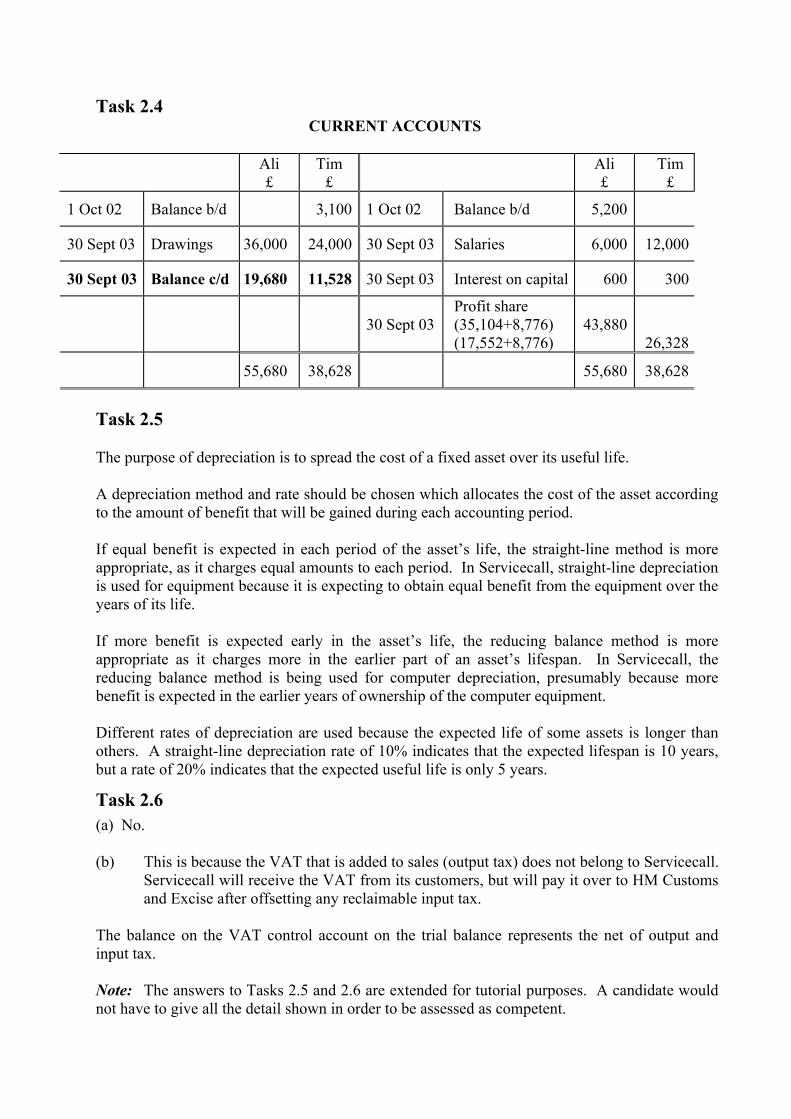

Task 2.4 CURRENT ACCOUNTS

Ali

£ Tim

£ Ali

£ Tim

£

1 Oct 02 Balance b/d 3,100 1 Oct 02 Balance b/d 5,200

30 Sept 03 Drawings 36,000 24,000 30 Sept 03 Salaries 6,000 12,000

30 Sept 03 Balance c/d 19,680 11,528 30 Sept 03 Interest on capital 600 300

30 Sept 03

Profit share (35,104+8,776) (17,552+8,776)

43,880 26,328

55,680 38,628 55,680 38,628

Task 2.5

The purpose of depreciation is to spread the cost of a fixed asset over its useful life.

A depreciation method and rate should be chosen which allocates the cost of the asset according to the amount of benefit that will be gained during each accounting period.

If equal benefit is expected in each period of the asset’s life, the straight-line method is more appropriate, as it charges equal amounts to each period. In Servicecall, straight-line depreciation is used for equipment because it is expecting to obtain equal benefit from the equipment over the years of its life.

If more benefit is expected early in the asset’s life, the reducing balance method is more appropriate as it charges more in the earlier part of an asset’s lifespan. In Servicecall, the reducing balance method is being used for computer depreciation, presumably because more benefit is expected in the earlier years of ownership of the computer equipment.

Different rates of depreciation are used because the expected life of some assets is longer than others. A straight-line depreciation rate of 10% indicates that the expected lifespan is 10 years, but a rate of 20% indicates that the expected useful life is only 5 years.

Task 2.6 (a) No. (b) This is because the VAT that is added to sales (output tax) does not belong to Servicecall.

Servicecall will receive the VAT from its customers, but will pay it over to HM Customs and Excise after offsetting any reclaimable input tax.

The balance on the VAT control account on the trial balance represents the net of output and input tax. Note: The answers to Tasks 2.5 and 2.6 are extended for tutorial purposes. A candidate would not have to give all the detail shown in order to be assessed as competent.