main features of the 2013 state budget - pwc

TRANSCRIPT

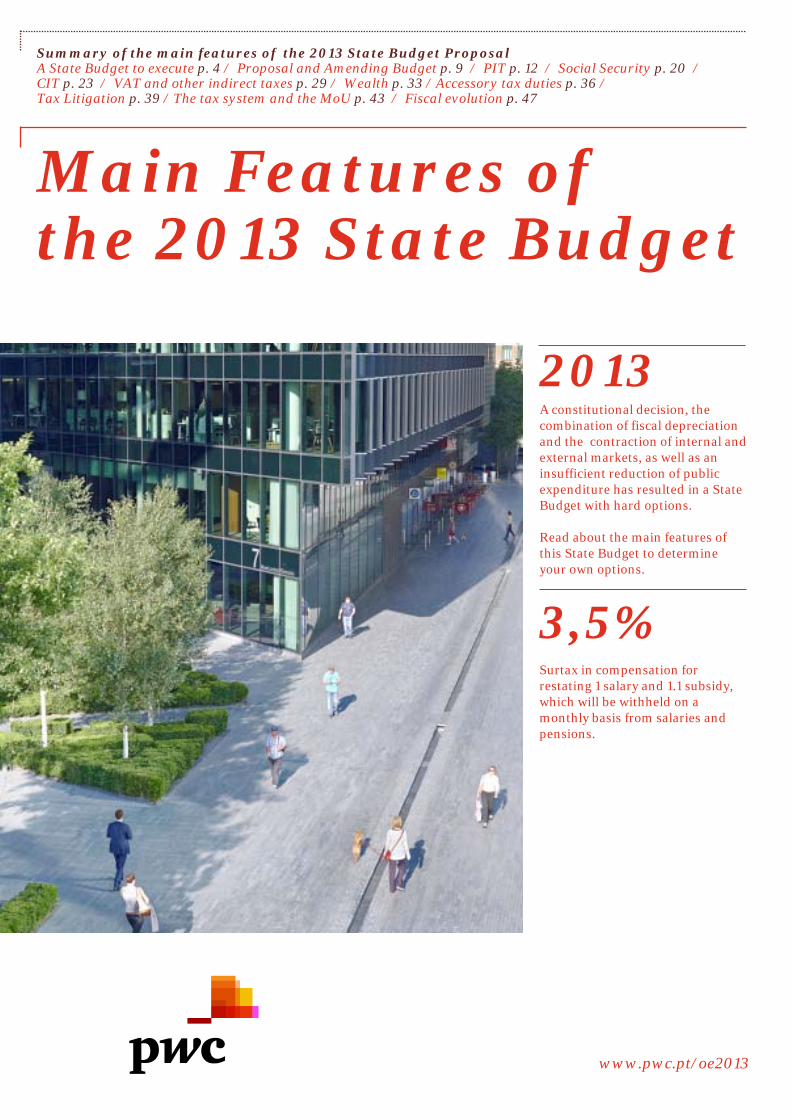

Summary of the main features of the 2013 State Budget Proposal A State Budget to execute p. 4 / Proposal and Amending Budget p. 9 / PIT p. 12 / Social Security p. 20 / CIT p. 23 / VAT and other indirect taxes p. 29 / Wealth p. 33 / Accessory tax duties p. 36 / Tax Litigation p. 39 / The tax system and the MoU p. 43 / Fiscal evolution p. 47

2013 A constitutional decision, the combination of fiscal depreciation and the contraction of internal and external markets, as well as an insufficient reduction of public expenditure has resulted in a State Budget with hard options. Read about the main features of this State Budget to determine your own options.

3,5% Surtax in compensation for restating 1 salary and 1.1 subsidy, which will be withheld on a monthly basis from salaries and pensions.

www.pwc.pt/oe2013

Main Features of the 2013 State Budget

PwC

PwC helps organizations and individuals create the value they’re looking for. We’re a network of firms in 158 countries with more than 180 000 people who are committed to delivering quality in assurance, tax and advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.com. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

A State Budget to execute

4

1. Proposal and Amending Budget 9

2. Personal Income Tax 12

3. Social Security 20

4. Corporate Income Tax 23

5. VAT and other indirect taxes 29

6. Wealth Taxes 33

7. Accessory tax duties 36

8. Tax Litigation 39

The tax system and the MoU 43

Fiscal evolution 47

Contents

3 State Budget 2013

4

A State Budget to execute

4

The 2013 Budget is substantially influenced by the evolution of our economy: anaemic growth over the past decade, uncontrolled public expenditure and unsustainable levels of public debt due to the sovereign debt crisis. Recently, we have seen an unsatisfactory reduction of public expenditure, the unfeasibility of neutral fiscal depreciation by means of VAT, the non-increase of working hours, the decision of the Constitutional Court which will not allow subsidy cuts for civil servants only, the rejection of the cut of labour costs by reducing social security contributions for employers, the fear of social unrest due to the uncontrolled increase of Real Estate Tax, and, finally, the absence of economic growth. In the current context, the budget adjustment was most likely to be on the side of tax revenue, particularly PIT. However, PIT is the tax that during 2013 most increases tax pressure, affecting the expected level of tax revenue according to the increasingly famous Laffer Curve. However, the response to the requirement for equal treatment between public and private employees, families and companies, and the need to find a balance of the contributions based upon income, expense and wealth appears to have been achieved, although within a context of sacrifices at all levels.

Jaime Carvalho Esteves Tax Lead Partner, in charge of the department “Government and Public Sector” www.pwc.pt/oe2013

State Budget 2013 PwC

5

5

A SB to execute

Within this context, concentration on imports destined to Europe might be one of the solutions. Portugal should place itself as platform between Europe and the South Atlantic, beginning with the Portuguese-speaking countries and respective regions of integration, promoting the consolidation of businesses, facilitating exports of goods and services (tourism included), introducing new benefits for companies that reinvest profits, promoting notional interest deduction regimes as well as promoting Portugal as place of residence for high net worth individuals and qualified professionals. If this is not the desired Budget, but simply the one that is possible, economic agents need to adjust their options, starting by understanding the fiscal framework for 2013. We hope that this document contributes to that purpose. Have a nice read.

Nevertheless, the uncertainty level regarding the accomplishment of the targets of the proposal remains high, taking into consideration that the macroeconomic scenario may be too optimistic (see annex), particularly regarding GDP and internal market contraction, unemployment, social support requirements, exports and Foreign Direct Investment (FDI) promotion, as well as the expected increase in tax fraud and tax evasion. Within such context, the Budget should have required a more thorough analysis aiming at the structural reduction of public expense (which, if it exists, has not yet produced the desired results) and the implementation of measures to promote growth which, according to Government’s statements, still need to be agreed with the “troika”. On the other hand, the substantial increase of the taxation of non-residents shall certainly lead to additional difficulties for our companies negotiating with counterparties, to a decrease of FDI, along with increased tax elision and evasion, if not even of tax fraud. The same applies to the proposed taxation of financial transactions. In addition, the limitations to the deductibility of financial costs (even if with a transitional regime) will also lead to additional difficulties for our companies, particularly those with high levels of debt, which will lead to the necessity of immediate adjustments. The same applies to the new rules regarding VAT adjustments in cases of late or missing payments. However, as this is an “emergency” Budget, this fiscal framework may not turn into a new paradigm, as it would almost certainly lead to an unsustainable situation. This being said, one should notice that, along with the expected very difficult execution, a sustained reduction of public expenditure is definitely required as of 2013, as well as the active promotion of economic growth.

“The uncertainty level regarding the accomplishment of the targets of the proposal remains high, taking into consideration that the macroeconomic scenario may be too optimistic (see annex), particularly regarding GDP and internal market contraction, unemployment, social support requirements, exports and Foreign Direct Investment (FDI) promotion, as well as the expected increase in tax fraud and tax evasion.”

State Budget 2013 PwC

6

6

A SB to execute

2009 2010 2011 2012 2013

SB (1st version) Real Execution

Rate SB (1st

version) Real Execution Rate

SB (1st version) Real Execution

Rate SB(1st

version) Execution

Rate SB (1st

version)

1. Tax revenue (2+3+4) 62 981.8 57 664.0 92% 55 625.9 59 473.0 107% 61 790.3 61 272.0 99% 61 480.5 94% 61 323.7

2. Taxes on production and imports

26 445.2 21 487.0 81% 22 369.5 23 154.0 104% 24 631.7 23 327.0 95% 25 653.7 90% 22 823.3

3. Taxes on income and wealth

16 880.8 15 146.0 90% 14 832.6 15 189.0 102% 15 860.5 16 887.0 106% 15 591.5 100% 18 385.9

4. Social contributions 19 655.8 21 031.0 107% 18 423.8 21 130.0 115% 21 298.1 21 058.0 99% 20 235.3 96% 20 114.5

5. Other current revenue 9 487.5 7 797.0 82% 9 222.2 7 379.0 80% 8 042.2 7 580.0 94% 8 231.5 89% 7 924.8

6. Total Current Revenue (1+5) 72 469.3 65 461.0 90% 64 848.1 66 852.0 103% 69 83.5 68 852.0 99% 69 712.0 94% 69 248.5

7. Intermediate consumptions

7 706.7 8 390.0 109% 7 827.7 8 745.0 112% 8 637.6 7 862.0 91% 7 785.5 100% 7 573.1

8. Compensation of employees

18 717.9 21 386.0 114% 18 679.7 21 093.0 113% 19 270.7 19 370.0 101% 16 929.9 98% 17 285.9

9. Social transfers 35 405.3 37 008.0 105% 36 756.9 37 830.0 103% 37 820.2 37 844.0 100% 35 641.3 103% 37 628.9

10.Interest (EDP) 5 776.0 4 775.0 83% 5 334.7 4 936.0 93% 6 326.3 6 622.0 105% 8 823.5 80% 7 164.4

11. Subsidies 2 208.3 1 271.0 58% 2 866.0 1 193.0 42% 799.3 1 183.0 148% 1 666.6 80% 1 325.7

12. Other current expenditure

3 909.6 4 294.0 110% 4 143.9 4 907.0 118% 2 971.4 4 350.0 146% 3 522.0 88% 3 697.3

13. Total Current Expenditure (7+...+12) 73 723.8 77 124.0 105% 75 608.9 78 704.0 104% 75 825.5 77 231.0 102% 74 368.8 98% 74 555.5

14. Gross Saving (6-13) -1 254.5 -11 663.0 930% -10 760.8 -11 852.0 110% -5 993.0 -8 379.0 140% -4 656.8 159% -5 307.0

15. Capital Revenue 3 528.2 1 246.0 35% 2 412.6 4 653.0 193% 2 028.7 7 517.0 371% 2 288.3 94% 1 341.2

16. Total Revenue (6+15) 75 997.5 66 707.0 88% 67 260.7 71 505.0 106% 71 861.2 76 369.0 106% 72 000.3 94% 70 589.7

17. Gross Fixed Capital Formation

4 350.5 5 060.0 116% 4 481.6 6 225.0 139% 3 794.0 4 428.0 117% 3 593.1 95% 2 962.1

18. Other Capital Expenditure

1 773.7 1 626.0 92% 1 124.6 3 528.0 314% 338.6 1 971.0 582% 1 595.3 -22% 566.0

19. Total Capital Expenditure (17+18)

6 124.2 6 687.0 109% 5 606.2 9 753.0 174% 4 132.6 6 400.0 155% 5 188.4 59% 3 528.1

20. Total Expenditure (13+19) 79 848.0 83 811.0 105% 81 215.1 88 457.0 109% 79 958.1 83 631.0 105% 79 557.2 95% 78 083.6

21. Net lending (+)/ Borrowing (-) (EDP) (16-20)

-3 850.5 -17 104.0 444% -13 954.4 -16 952.0 121% -8 096.9 -7 262.0 90% -7 556.9 110% -7 493.9

Sources: GPEARI – Portugal Public Finances Dossier State Budget Reports 2009, 2010, 2011, 2012, 2013 INE

State Budget 2013 PwC

7

7

Sources: State Budget Reports 2009, 2010, 2011, 2012, 2013 GPEARI - Macroeconomic Forecasts for the Portuguese Economy INE Eurostat

State Budget 2013 PwC

2009 2010 2011 2012 2013

SB (1st version) Real SB (1st

version) Real SB (1st version) Real

SB (1st

version)

Forecast Forecast

IMF EC OECD Bank of Portugal

Ministry of Finance

SB 2013 (1st

version)

SB (1st version) IMF EC OECD Bank of

Portugal Growth rate % Real Gross domestic product (GDP)

0.6 -2.9 0.7 1.4 0.2 -1.7 -2.8 -3.0 -3.0 -3.2 -3.0 -1.0 -3.0 -1.0 -1.0 0.2 -0.9 0.0

Gross Public Debt (% GDP) 64.4 83.2 85.4 93.5 86.6 108.1 110.5 /

119.1 119.0 119.1 124.3 123.7

Private Consumption 0.8 -2.3 1.0 2.1 -0.5 -4.0 -4.8 -6.0

(Jul/12) -6.0 -6.8 -5.6 -5.8 -5.9 -2.2 -0.5 (Jul/12) -0.5 -3.2 -1.3

Government consumption 0.2 4.7 -0.9 0.9 -8.8 -3.8 -6.2 -3.2

(Jul/12) -3.4 -2.9 -3.8 -3.5 -3.3 -3.5 -2.6 (Jul/12) -2.7 -2.4 -1.6

Gross Fixed Capital Formation (GFCF)

1.5 -8.6 -1.1 -4.1 -2.7 -11.3 -9.5 -12.2 (Jul/12)

-12.2 -10.1 -12.7 -14.1 -14.1 -4.2 -0.5

(Jul/12) -0.5 -3.2 -2.6

Exports 1.2 -10.9 3.5 8.8 7.3 7.5 4.8 3.5 (Jul/12) 3.5 3.4 3.5 4.3 4.3 3.6 3.5

(Jul/12) 3.5 5.1 5.2

Imports 1.8 -10.0 1.5 5.4 -1.7 -5.3 -4.3 -6.2 (Jul/12) -6.2 -5.7 -6.2 -6.6 -6.6 -1.4 0.9

(Jul/12) 0.9 -0.1 1.5

Unemployment rate (%) 7.6 9.5 9.8 10.8 10.8 12.7 13.4 15.5 15.4 15.4 15.5 15.5 16.4 16.0

(Jul/12) 15.8 16.2

Inflation rate 2.5 -0.83 0.8 1.4 2.2 3.6 3.1 2.8 2.7 3.1 2.6 2.8 2.8 0.7 0.7 (Jul/12) 1.1 0.7 1.0

External Balance (Current and Capital Accounts; %GDP)

-9.4 -9.7 -7.9 -3.9 -1.1 1.0

A SB to execute

8

8

A SB to execute

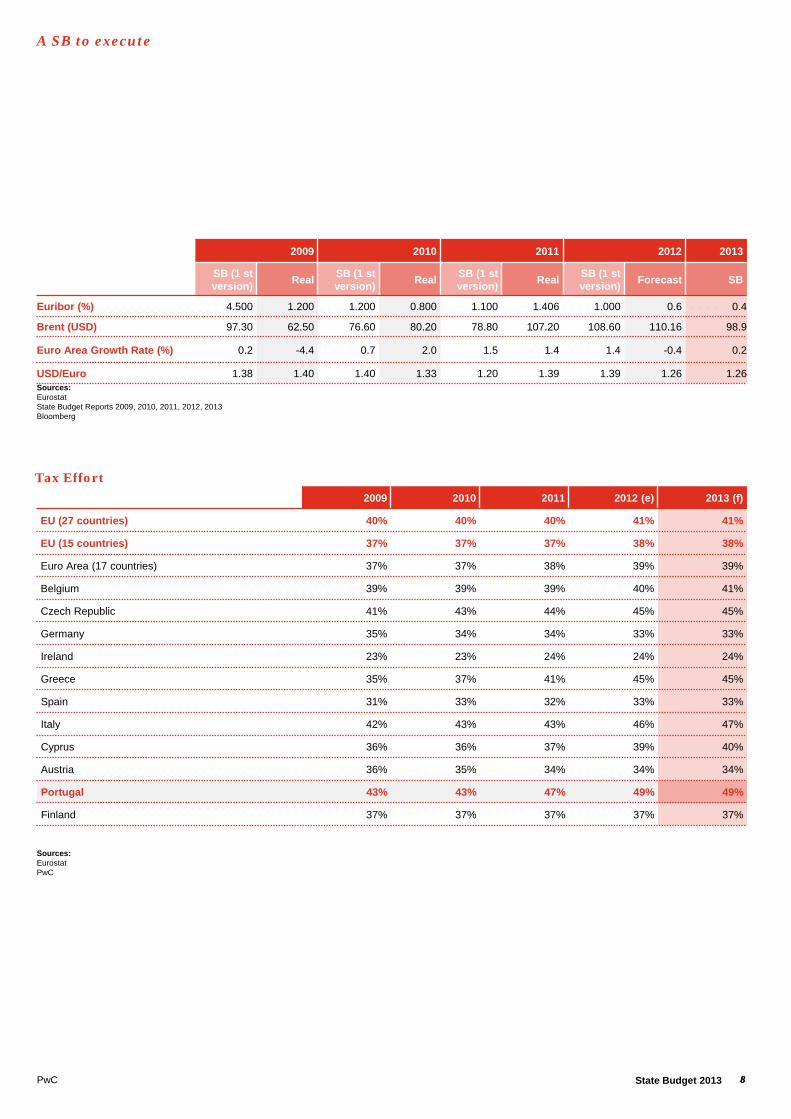

Sources: Eurostat State Budget Reports 2009, 2010, 2011, 2012, 2013 Bloomberg

2009 2010 2011 2012 2013

SB (1 st version) Real SB (1 st

version) Real SB (1 st version) Real SB (1 st

version) Forecast SB

Euribor (%) 4.500 1.200 1.200 0.800 1.100 1.406 1.000 0.6 0.4

Brent (USD) 97.30 62.50 76.60 80.20 78.80 107.20 108.60 110.16 98.9

Euro Area Growth Rate (%) 0.2 -4.4 0.7 2.0 1.5 1.4 1.4 -0.4 0.2

USD/Euro 1.38 1.40 1.40 1.33 1.20 1.39 1.39 1.26 1.26

2009 2010 2011 2012 (e) 2013 (f)

EU (27 countries) 40% 40% 40% 41% 41%

EU (15 countries) 37% 37% 37% 38% 38%

Euro Area (17 countries) 37% 37% 38% 39% 39%

Belgium 39% 39% 39% 40% 41%

Czech Republic 41% 43% 44% 45% 45%

Germany 35% 34% 34% 33% 33%

Ireland 23% 23% 24% 24% 24%

Greece 35% 37% 41% 45% 45%

Spain 31% 33% 32% 33% 33%

Italy 42% 43% 43% 46% 47%

Cyprus 36% 36% 37% 39% 40%

Austria 36% 35% 34% 34% 34%

Portugal 43% 43% 47% 49% 49%

Finland 37% 37% 37% 37% 37%

Sources: Eurostat PwC

Tax Effort

State Budget 2013 PwC

9

1. Proposal and Amending Budget

PwC

“Investment income and capital gains increase to 26.5%, before increasing to 28%.” Adrião Silva, Tax Director

State Budget 2013

10

1. Proposal and Amending Budget

Rates – Income from omnibus accounts Increase from 30% to 35% of the rate applicable to investment income, whenever paid or made available in accounts opened in the name of one or several holders but on behalf of unidentified third-parties, except when the beneficial owner is identified. Capital Gains – Category G The net balance of capital gains and capital losses on the sale of shares, among others, shall be subject to a special rate of 26.5%, instead of 25%, as presently. Non-residents Investment income paid by non-resident entities, which are not subject to withholding tax, is increased from 25% to 26.5% for income earned since 1 January 2012. Investment income which is paid by non-resident entities without a permanent establishment in Portugal and located in territories with a more favourable tax regime, as per list approved by the Ministry of Finance, that are not subject to withholding tax, shall be liable to an special tax rate of 35% (currently 30%).

PIT (Personal Income Tax) Investment income – Category E Investment income subject to a flat tax rate of 25% will be taxed at a flat tax rate of 26.5%. This rate applies to several types of income, as interest on deposits, income from debt securities, dividends, among others. The securities income paid or made available to individuals resident in Portugal, whenever such income is paid by entities that do not have a tax domicile herein (to which it is possible to allocate the payment) and paid by paying agents, will also be subject to a tax rate of 26.5% (currently 25%). Additionally, the income referred to above paid to entities resident in Portugal by non-resident entities without a permanent establishment in Portugal and located in territories with a more favourable tax regime, as per list approved by the Ministry of Finance, will also be subject to a flat tax rate of 35% (currently 30%). Investment income received by entities without a permanent establishment in Portugal and located in territories with a more favourable tax regime, as per list approved by the Ministry of Finance, will be liable to a flat tax rate of 35%.

Rates – Withholding Tax The application for CIT purposes of the PIT withholding tax rates is revoked. The general CIT withholding tax rate is levelled at 25%. However, the 21.5% withholding tax rate, applicable to remunerations obtained by board members of companies and other entities, is maintained.

CIT (Corporate Income Tax) Rates – Income from omnibus accounts Increase from 30% to 35% of the rate applicable to investment income, whenever paid or made available in accounts opened in the name of one or several holders but on behalf of unidentified third-parties, except when the beneficial owner is identified. An identical increase applies to investment income obtained by non-residents in Portugal, who are domiciled in jurisdictions with more favourable tax regimes.

State Budget 2013 PwC

11

Wealth Stamp Tax – Real Estate with a tax registration value equal to or higher than 1 000 000 euros Stamp Tax will be levied on the ownership, usufruct or surface right of urban housing buildings, with a tax registration value equal to or higher than 1 000 000 euros. This tax will be due already in 2012 by the entities owning buildings as of 31 October 2012 and it will assessed based on the buildings' tax registration value at the rate of 0.5% or 0.8%, depending on whether the buildings are already evaluated, or not, according to the rules of the Real Estate Tax (RET) Code. For 2013, it is foreseen an increase of this rate to 1%. The tax rate is 7.5% for buildings, regardless of their use, owned by companies resident in jurisdictions with more favourable tax regimes.

General Tax Law Evidence of wealth The difference between the income declared by the taxpayer and the reference income, as included in the table of wealth evidence, is reduced from 50% to 30%. The total amounts transferred from and to the taxpayer’s bank accounts opened in financial institutions located in jurisdictions with more favourable tax regimes, which have not been reported to the tax authorities, are now regarded as an evidence of wealth.

RET - Safeguard Clause - Leased urban property For buildings that had their rents updated under the specific rules of the New Urban Rental Regime that aim to protect tenants with lower income, RET becomes computed over an amount equivalent to 15 times the updated annual rent. For the remaining buildings, RET becomes computed over an amount equivalent to 15 times the annual rent. The owner of the building must declare, on a yearly basis, by means of the appropriate declaration, the value of the rent pertaining to December, enclosing the corresponding receipt and the fiscal identification of the tenant of the building or fraction benefitting from the RET limitation by application of the safeguard clause. Non-compliance with this obligation leads to the loss of the right to the application of this limitation .

1. Proposal and Amending Budget

State Budget 2013 PwC

12

2. Personal Income Tax

PwC

“In an attempt to stimulate the real estate market, the rental income will be taxed autonomously at a rate of 28%, subject to the option of inclusion in the total reported income.” Leendert Verschoor, Tax Partner

State Budget 2013

13

2. Personal Income Tax

Self-employee Income – Withholding tax The withholding tax rate applicable to income arising from professional activities specifically indicated in the table referred to in Article 151 of the PIT Code is increased to 25% (currently 21.5%). Rental income Rental income is liable to a special tax rate of 28%, but the option for the inclusion of such income in the total aggregated income is possible. Withholding tax is increased to a rate of 25% (presently 16.5%). Stamp duty levied on the value of the buildings or parts of buildings whose rental income has been subject to PIT may be deducted. The specific deduction related with rental income applies to all taxpayers who receive rental income whether taxed at the rate of 28% or who opt for the inclusion of such income in the total aggregated income. Investment Income The new withholding tax rates are presented in the following table. Capital gains The positive balance between capital gains and losses, arising from the disposal of shares is subject to autonomous taxation at a rate of 28%, instead of 25%. Capital gains obtained by small investors From 1 January 2013 onwards, the positive balance between capital gains and capital losses obtained by resident individuals on the transfer of shares, bonds and other debt securities shall become subject to PIT in its total amount. Currently, there is an exemption up to the amount of 500 euros. Intellectual Property Income The maximum annual amount excluded from PIT taxation regarding intellectual property income earned by a resident original author or owner is reduced from 20 000 to 10 000 euros. This rule covers income derived from literary, artistic and scientific property, as well as income derived from the sale of unique art works and from works of educational and scientific nature.

Members of the EU Parliament Following the last decision of the tax authority, income received by EU Parliament members is subject to PIT. Lunch Subsidy The limit of exemption for the lunch subsidy, paid in cash, was reduced to 4.27 euros. Per Diems – Category A PIT exemption related to payment of per diem (travels abroad) are reduced as follows: Additionally, regarding travels in Portugal, the payment of per diem will only be due when the distance from the necessary place of residence exceeds 20 km or when travels occur on successive days further than 50 km of the same place of residence. Specific Deduction – Category A – Employee Income The specific deduction related to the amounts paid in respect of professional training expenses has been revoked. Self-employee income – Simplified system The taxable income of services, when the simplified taxation system applies, is computed using the coefficient of 75%, instead of 70%. Until 30 January 2013 taxpayers that are taxed under the simplified regime may freely opt for the general taxation system.

Amounts in euros 2012 2013

Government members 133.66 100.24

Remuneration higher than level 18 119.13 89.35

Remuneration between level 18 to 9 111.81 85.50

Others 95.10 72.72

State Budget 2013 PwC

14

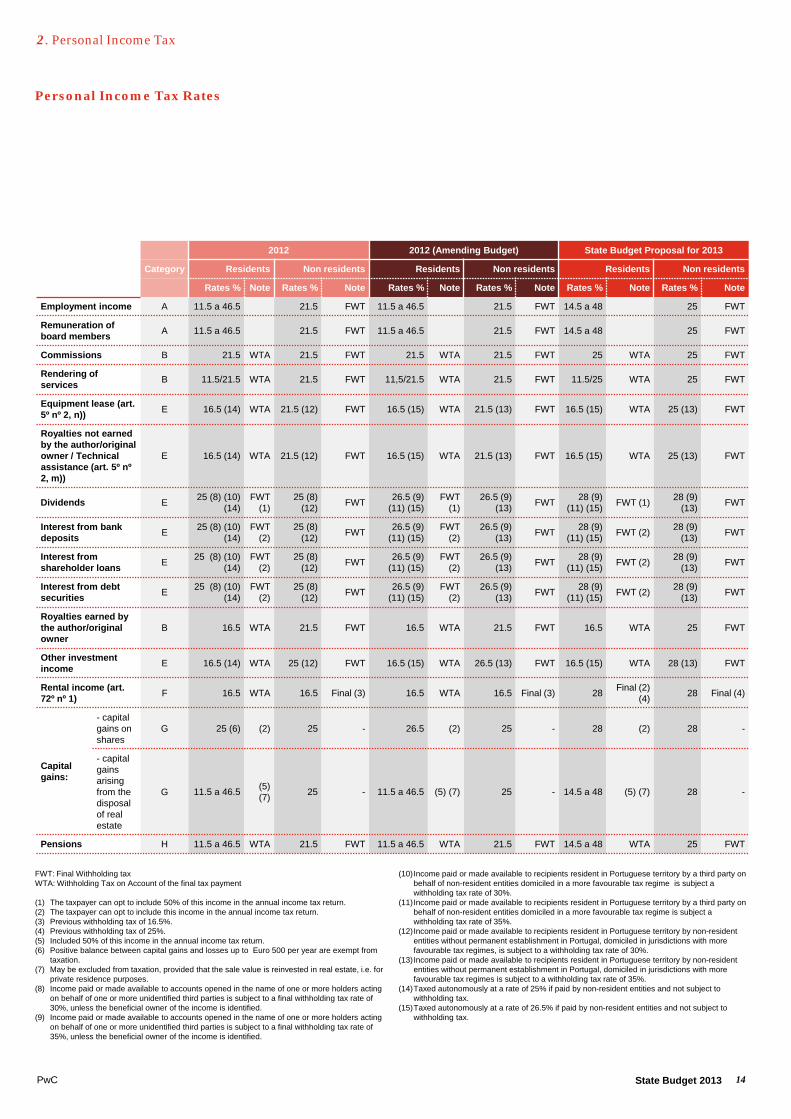

Personal Income Tax Rates

2. Personal Income Tax

State Budget 2013 PwC

2012 2012 (Amending Budget) State Budget Proposal for 2013

Category Residents Non residents Residents Non residents Residents Non residents

Rates % Note Rates % Note Rates % Note Rates % Note Rates % Note Rates % Note

Employment income A 11.5 a 46.5 21.5 FWT 11.5 a 46.5 21.5 FWT 14.5 a 48 25 FWT

Remuneration of board members A 11.5 a 46.5 21.5 FWT 11.5 a 46.5 21.5 FWT 14.5 a 48 25 FWT

Commissions B 21.5 WTA 21.5 FWT 21.5 WTA 21.5 FWT 25 WTA 25 FWT

Rendering of services B 11.5/21.5 WTA 21.5 FWT 11,5/21.5 WTA 21.5 FWT 11.5/25 WTA 25 FWT

Equipment lease (art. 5º nº 2, n)) E 16.5 (14) WTA 21.5 (12) FWT 16.5 (15) WTA 21.5 (13) FWT 16.5 (15) WTA 25 (13) FWT

Royalties not earned by the author/original owner / Technical assistance (art. 5º nº 2, m))

E 16.5 (14) WTA 21.5 (12) FWT 16.5 (15) WTA 21.5 (13) FWT 16.5 (15) WTA 25 (13) FWT

Dividends E 25 (8) (10) (14)

FWT (1)

25 (8) (12) FWT 26.5 (9)

(11) (15) FWT

(1) 26.5 (9)

(13) FWT 28 (9) (11) (15) FWT (1) 28 (9)

(13) FWT

Interest from bank deposits E 25 (8) (10)

(14) FWT

(2) 25 (8)

(12) FWT 26.5 (9) (11) (15)

FWT (2)

26.5 (9) (13) FWT 28 (9)

(11) (15) FWT (2) 28 (9) (13) FWT

Interest from shareholder loans E 25 (8) (10)

(14) FWT

(2) 25 (8)

(12) FWT 26.5 (9) (11) (15)

FWT (2)

26.5 (9) (13) FWT 28 (9)

(11) (15) FWT (2) 28 (9) (13) FWT

Interest from debt securities E 25 (8) (10)

(14) FWT

(2) 25 (8)

(12) FWT 26.5 (9) (11) (15)

FWT (2)

26.5 (9) (13) FWT 28 (9)

(11) (15) FWT (2) 28 (9) (13) FWT

Royalties earned by the author/original owner

B 16.5 WTA 21.5 FWT 16.5 WTA 21.5 FWT 16.5 WTA 25 FWT

Other investment income E 16.5 (14) WTA 25 (12) FWT 16.5 (15) WTA 26.5 (13) FWT 16.5 (15) WTA 28 (13) FWT

Rental income (art. 72º nº 1) F 16.5 WTA 16.5 Final (3) 16.5 WTA 16.5 Final (3) 28 Final (2)

(4) 28 Final (4)

Capital gains:

- capital gains on shares

G 25 (6) (2) 25 - 26.5 (2) 25 - 28 (2) 28 -

- capital gains arising from the disposal of real estate

G 11.5 a 46.5 (5) (7) 25 - 11.5 a 46.5 (5) (7) 25 - 14.5 a 48 (5) (7) 28 -

Pensions H 11.5 a 46.5 WTA 21.5 FWT 11.5 a 46.5 WTA 21.5 FWT 14.5 a 48 WTA 25 FWT

FWT: Final Withholding tax WTA: Withholding Tax on Account of the final tax payment (1) The taxpayer can opt to include 50% of this income in the annual income tax return. (2) The taxpayer can opt to include this income in the annual income tax return. (3) Previous withholding tax of 16.5%. (4) Previous withholding tax of 25%. (5) Included 50% of this income in the annual income tax return. (6) Positive balance between capital gains and losses up to Euro 500 per year are exempt from

taxation. (7) May be excluded from taxation, provided that the sale value is reinvested in real estate, i.e. for

private residence purposes. (8) Income paid or made available to accounts opened in the name of one or more holders acting

on behalf of one or more unidentified third parties is subject to a final withholding tax rate of 30%, unless the beneficial owner of the income is identified.

(9) Income paid or made available to accounts opened in the name of one or more holders acting on behalf of one or more unidentified third parties is subject to a final withholding tax rate of 35%, unless the beneficial owner of the income is identified.

(10)Income paid or made available to recipients resident in Portuguese territory by a third party on behalf of non-resident entities domiciled in a more favourable tax regime is subject a withholding tax rate of 30%.

(11)Income paid or made available to recipients resident in Portuguese territory by a third party on behalf of non-resident entities domiciled in a more favourable tax regime is subject a withholding tax rate of 35%.

(12)Income paid or made available to recipients resident in Portuguese territory by non-resident entities without permanent establishment in Portugal, domiciled in jurisdictions with more favourable tax regimes, is subject to a withholding tax rate of 30%.

(13)Income paid or made available to recipients resident in Portuguese territory by non-resident entities without permanent establishment in Portugal, domiciled in jurisdictions with more favourable tax regimes is subject to a withholding tax rate of 35%.

(14)Taxed autonomously at a rate of 25% if paid by non-resident entities and not subject to withholding tax.

(15)Taxed autonomously at a rate of 26.5% if paid by non-resident entities and not subject to withholding tax.

15 PwC

2013

Taxable Income (Euros) Tax Rate (%) Deductible Amount (Euros)

Up to 7 000.00 14.50% 0

Between 7 000.00 and 20 000.00 28.50% 980

Between 20 000.00 and 40 000.00 37.00% 2 680

Between 40 000.00 and 80 000.00 45.00% 5 880

Above 80 000.00 48.00% 8 280

2012

Taxable Income (Euros) Tax Rate (%) Deductible Amount (Euros)

Up to 4 898.00 11.50% 0.00

Between 4 898.00 and 7 410.00 14.00% 122.45

Between 7 410.00 and 18 375.00 24.50% 900.50

Between 18 375.00 and 42 259.00 35.50% 2 921.75

Between 42 259.00 and 61 244.00 38.00% 3 978.23

Between 61 244.00 and 66 045.00 41.50% 6 121.77

Between 66 045.00 and 153 300.00 43.50% 7 442.67

Above 153 300.00 46.50% 12 041.67

General Rates (additional solidarity rate excluded)

Income brackets - General tax rates The number of PIT brackets was reduced from 8 to 5 and the general tax rates also changed. Additional solidarity rate The additional surcharge is now progressive. The rate of 2.5% is still applicable to taxpayers with a taxable income between 80 000 euros and 250 000 euros. However, a rate of 5% is applicable to taxpayers with a taxable income higher than 250 000 euros. Non habitual tax residents The conditions to eliminate the double taxation on income derived from foreign sources have been clarified. However, this clarification has no interpretative nature. Non-residents – Rates Some types of income received by non-residents subject to a withholding tax at a rate of 21.5% will now be subject to a withholding tax rate of 25%, including employment income, pensions, income derived from the authorisation to use equipment, among others. Capital gains and other income earned by non-residents that are not attributed to a permanent establishment nor subject to withholding tax at flat rates are taxed at a withholding tax rate of 28% (currently 25%). The tax rate on investment income paid by non-resident entities and not subject to withholding tax increases from 25% to 28%.

Rental income obtained by non-residents is taxed at an autonomous rate of 28% (currently 16.5%). Surtax An extraordinary surtax of 3.5% will be applicable to income subject to PIT. This tax rate will apply to all types of income included in the PIT tax return of tax-resident individuals. This surtax will also apply to some types of income that are subject to a special tax rate, such as income received by non-habitual tax-residents. The surtax applies to the net income, per individual taxpayer, exceeding the annual minimum salary (6 790 euros). Taxpayers with Category A and H income will be subject to an extraordinary monthly withholding tax. This withholding tax will be considered as a payment on account of the final surtax which is assessed only with the annual PIT return. If the withholding tax is higher or lower than the surtax due, a reimbursement or an additional payment takes place. Regarding other types of income, the surtax rate will be determined with the submission of the annual PIT return.

2. Personal Income Tax

State Budget 2013

16

Tax credits – Global limits The limit of tax credits is reduced, which includes health, education or professional training expenses, as well as immovable property expenses. Tax credits – Housing loans The limit relating to expenses regarding housing loans (interest) is reduced from 591 to 296 euros. This deduction is not applicable for contracts signed from 1 January 2012 onwards. The limit applicable to rental expenses under the Urban Rental Regime or the New Urban Rental Regime is reduced from 591 to 502 euros. The above mentioned limits may be higher, depending on the taxpayer’s income bracket. Tax credits - Tax benefits The total limit for tax deductions related to tax benefits (retirement plans, donations, premiums for health insurance, etc.) is reduced. Withholding tax The withholding tax limit applicable to employment and pension income cannot exceed 45% of the income paid or made available to each individual in the same year (currently 40%).

Transitional Provisions In 2013, only 90% of Categories A, B and H gross income of taxpayers with disabilities will be computed for PIT assessment purposes. However, such exclusion only applies to income not exceeding 2 500 euros for each category.

“New PIT brackets and the surtax rate contribute decisively to the increase of the average effective tax rate by 3.4 p.p.” Ana Duarte, Tax Director

2. Personal Income Tax

State Budget 2013 PwC

17 PwC

Tax Credits 2012 2013 Amounts in Euros Married Not married Married Not married

Tax credits in respect of taxpayers and their relatives

i) Taxpayer 522.50 261.25 427.50 213.75

ii) Single-parent taxpayers - 380.00 - 332.50

iii) Dependants 190.00 190.00 213.75 213.75

Dependants <= 3 years old on December 31 of the year to which the tax relates 380.00 380.00 427.50 427.50

Households with three or more dependants in their care / for each dependant - - 237.50 237.50

iv) Ancestors actually living in the same household with the taxpayer who do not receive income greater than the minimum pension payable under the general regime 261.25 261.25 261.25 261.25

v) Only one ancestor actually living in the same household with the taxpayer who does not receive income greater than the minimum pension payable under the general regime 403.75 403.75 403.75 403.75

People with disabilities

i) For each taxpayer (1) 3 800.00 1 900.00 (1) 3 800.00 1 900.00

ii) For each dependant with disability 712.50 712.50 712.50 712.50

iii) For each ancestor with disability 712.50 712.50 712.50 712.50

iv) 30% of education and rehabilitation expenditures No limit No limit No limit No limit

v) 25% of life assurance premiums or contributions paid to credit unions 15% of computed tax 15% of computed tax 15% of

computed tax 15% of

computed tax

- Age-related retirement contributions 130.00 65.00 130.00 65.00

Health Expenses

The following expenses are creditable: 10% of deduction 10% of deduction

a) Acquisition of goods and services which are exempt from VAT or that are liable to the reduced VAT rate of 5/6%; (2) 838.44 (2) 838.44 (2) 838.44 (2) 838.44

b) Acquisition of other goods and services duly justified with a medical prescription

65.00 or 2.5% of a),

whichever is higher

65.00 or 2.5% of a),

whichever is higher

65.00 or 2.5% of a),

whichever is higher

65.00 or 2.5% of a),

whichever is higher

c) The health expenses limit shall be increased for households with three or more dependants in their care, for each dependant, in: 125.77 125.77 125.77 125.77

Education and training expenses

i) 30% of amounts spent up to a limit of: 760.00 760.00 760.00 760.00

ii) In households with three or more dependants in their care the limit referred to in i) shall be increased, for each dependant, in: 142.50 142.50 142.50 142.50

Nursing home fees

25% of charges for homes and institutions to support the taxpayer, ancestors and relatives until the third degree who do not have income equal to or above the minimum monthly wage 403.75 403.75 403.75 403.75

Life insurance and personal accident premiums

25% of the amount spent with personal accident insurance and life assurance covering only risks of death, disability and retirement due to age, in the latter case where benefits may be received only after 55 years of age and 5 years of contract

Repealed - Only in place for professions involving rapid wear and

tear and people with disability

Repealed - Only in place for professions involving rapid wear

and tear and people with disability

Alimony

20% of the amount spent 419.22 per month, for beneficiary 419.22 per month, for beneficiary

2. Personal Income Tax

State Budget 2013 PwC

18 PwC

Tax Credits 2012 2013 Amounts in Euros Married Not married Married Not married

Real estate costs

For 2012, a tax credit of 15% of the following expenditures:

a) Debt interest, for contracts concluded until 31 December 2011, incurred on the acquisition, construction or improvement of permanent private residential property used as the taxpayer’s permanent private residence, or rent (paid) in respect of a tenant's duly substantiated permanent residence

591.00 591.00 296.00 296.00

b) Instalments payable as a result of contracts concluded until 31 December 2011 with housing cooperatives or under the group purchasing regime, for the purchase of residential property for use as the (taxpayer’s) personal and permanent residence or rental paid in respect of a tenant's duly substantiated permanent residence, to the extent in which they refer to interest of related debt

591.00 591.00 296.00 296.00

c) Amounts paid by way of rent under a leasing contract concluded until 31 December 2011 in respect of a personal and permanent residence under their regime, to the extent that it does not constitute repayment of capital

591.00 591.00 296.00 296.00

d) Amounts, spent by way of rent , net of subsidies or official contributions, concerning an urban real estate or fraction for permanent housing under the Urban Rental Regime or the New Urban Rental Regime

591.00 591.00 502.00 502.00

For 2012, the limits set out in paragraphs a) to d) are increased as follows:

- Taxable income up to 2nd bracket - 50%, 886.50 886.50 - -

- Taxable income up to 3rd bracket - 20%, 709.20 709.20 - -

- Taxable income up to 4th bracket - 10%. 650.10 650.10 - -

For 2013, the limits set out in paragraphs a), b) and c) are increased as follows:

- Taxable income up to 1nd bracket - 50%, - - 444.00 444.00

- Taxable income up to 2nd bracket - 20%, - - 355.20 355.20

For 2013, the limits set out in paragraph d) are increased as follows:

- Taxable income up to 1nd bracket - 50%, - - 753.00 753.00

- Taxable income up to 2nd bracket - 20%, - - 602.40 602.40

Retirement Savings Funds and Retirement Savings Plans (3)

Tax credit of 20% of the amount invested

i) People under 35 years old 800.00 400.00 800.00 400.00

ii) People between 35 and 50 years old 700.00 350.00 700.00 350.00

iii) People above 50 years old 600.00 300.00 600.00 300.00

Health insurance premiums

Health insurance premiums expenses 10% with a

limit of 100.00

10% with a limit of 50.00

10% with a limit of 100.00

10% with a limit of 50.00

For each dependant accrue 25.00 25.00 25.00 25.00

Donations

Tax credit of 25% :

i) Central, regional or local administration; Foundations (with conditions) No limit No limit No limit No limit

ii) Donations to other entities 15% of computed tax

15% of computed tax

15% of computed tax

15% of computed tax

Capitalisation Public Regime

Tax credit of 20% of the amount invested in individual accounts managed under the capitalisation public regime 700.00 350.00 700.00 350.00

2. Personal Income Tax

State Budget 2013

19 PwC

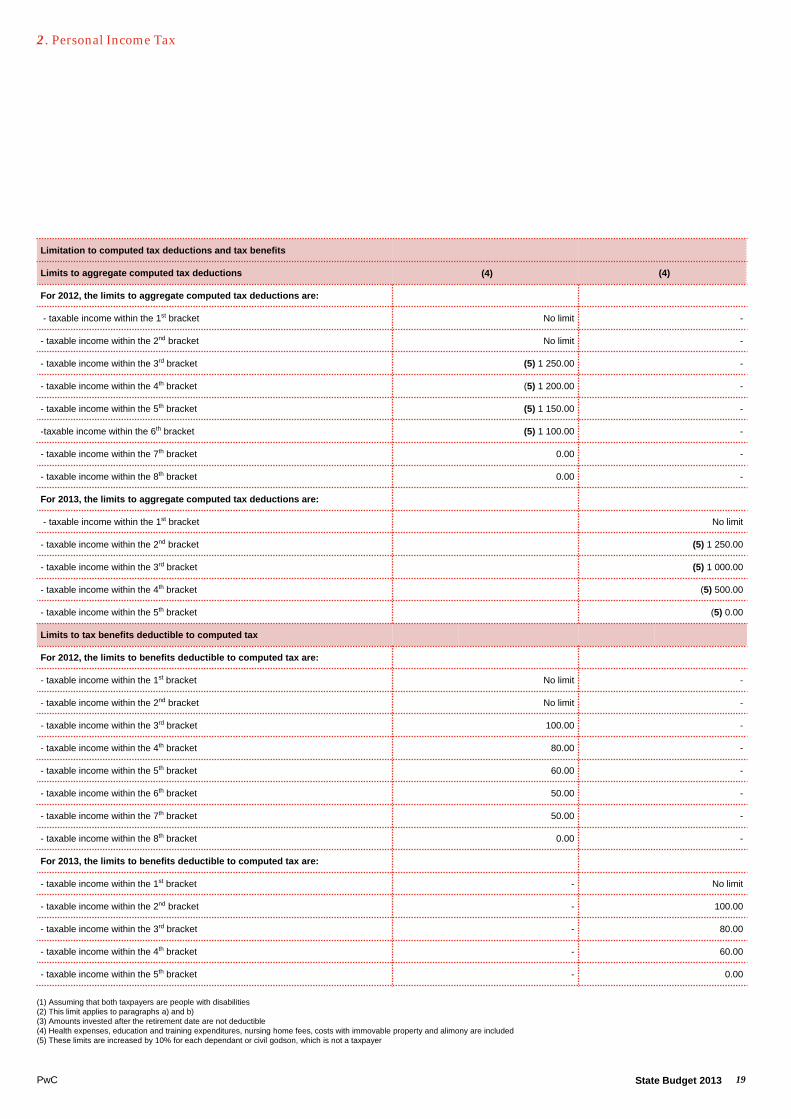

Limitation to computed tax deductions and tax benefits

Limits to aggregate computed tax deductions (4) (4)

For 2012, the limits to aggregate computed tax deductions are:

- taxable income within the 1st bracket No limit -

- taxable income within the 2nd bracket No limit -

- taxable income within the 3rd bracket (5) 1 250.00 -

- taxable income within the 4th bracket (5) 1 200.00 -

- taxable income within the 5th bracket (5) 1 150.00 -

-taxable income within the 6th bracket (5) 1 100.00 -

- taxable income within the 7th bracket 0.00 -

- taxable income within the 8th bracket 0.00 -

For 2013, the limits to aggregate computed tax deductions are:

- taxable income within the 1st bracket No limit

- taxable income within the 2nd bracket (5) 1 250.00

- taxable income within the 3rd bracket (5) 1 000.00

- taxable income within the 4th bracket (5) 500.00

- taxable income within the 5th bracket (5) 0.00

Limits to tax benefits deductible to computed tax

For 2012, the limits to benefits deductible to computed tax are:

- taxable income within the 1st bracket No limit -

- taxable income within the 2nd bracket No limit -

- taxable income within the 3rd bracket 100.00 -

- taxable income within the 4th bracket 80.00 -

- taxable income within the 5th bracket 60.00 -

- taxable income within the 6th bracket 50.00 -

- taxable income within the 7th bracket 50.00 -

- taxable income within the 8th bracket 0.00 -

For 2013, the limits to benefits deductible to computed tax are:

- taxable income within the 1st bracket - No limit

- taxable income within the 2nd bracket - 100.00

- taxable income within the 3rd bracket - 80.00

- taxable income within the 4th bracket - 60.00

- taxable income within the 5th bracket - 0.00

(1) Assuming that both taxpayers are people with disabilities (2) This limit applies to paragraphs a) and b) (3) Amounts invested after the retirement date are not deductible (4) Health expenses, education and training expenditures, nursing home fees, costs with immovable property and alimony are included (5) These limits are increased by 10% for each dependant or civil godson, which is not a taxpayer

2. Personal Income Tax

State Budget 2013

20

3. Social Security

State Budget 2013 PwC

“Sickness and unemployment subsidies become subject to Social Security contributions at a rate of 5% and 6%, safeguarding the minimum amount.” Leendert Verschoor, Tax Partner

21 21

3. Social Security

Suspension of the IAS update For 2013, the update of the Social Security Index (IAS) is suspended, maintaining the value of 419.22 euros. Remuneration decrease The decrease of total gross monthly remuneration of persons holding certain public functions, including public officials, public managers, employees of public companies and military personnel, is maintained. Christmas subsidy During the term of the EU/IMF Assistance Programme (PAEF), the payment of Christmas subsidies to people holding certain public positions (as mentioned above) will be reintroduced, calculated according to the base remuneration after the remuneration decreased mentioned and paid in 12 monthly instalments. Sickness and unemployment subsidies Sickness and unemployment subsidies, granted for a period of more than 30 days, will be liable to Social Security contributions at the rates of 6% and 5%, respectively.

2012 2013

Gross Monthly Pension (Euros): Rate (%) Deductible amount

(Euros) Rate (%) Deductible amount (Euros)

Until 5 030.64 0% 0.00

From 5 030.64 to 7 545.96 25% 1 257.66

Greater than 7 545.96 50% 3 144.15

Greater than 1 350 until 1 800 3,5% 0.00

Greater than1 800 until 3 750 16% 225.00

Greater than 3 750 10% 0.00

In addition:

if greater than 5 030.64 until 7 545.96 15% 754.60

if greater than 7 545.96 40% 2 641.09

Extraordinary Solidarity Contribution (CES) Pensions paid to a sole individual are subject to an extraordinary solidarity contribution, as shown below. The application of this contribution may not result in a monthly pension lower than 1 350 euros. CES is applicable to all pensions paid by Caixa Geral de Aposentações, pension funds and insurance companies, Centro Nacional de Pensões and Caixa de Previdência dos Advogados e Solicitadores. The part related with the reimbursement of capital, in respect to contributions made by the beneficiaries of the annuities paid by the insurance company is excluded for CES purposes. Suspension of the payment of holiday subsidies During PAEF, the payment of holidays subsidies or any other benefits corresponding to the 14th month instalment is suspended for persons holding certain public positions (namely those mentioned above). In certain cases, the same applies to service providers with monthly base remuneration greater than 1 100 euros. The Budget also foresees the suspension of the payment of 90% of this subsidy in case of pensioners with monthly pensions exceeding 1 100 euros. People mentioned above, whose remuneration is equal or greater than 600 euros, but not exceeding 1 100 euros, will be subject to a progressive reduction of the subsidies.

Table – Extraordinary Solidarity Contribution

State Budget 2013 PwC

22 22

3. Social Security

Farmers Contribution rate increased from 28.3% to 33.33% for farmers and respective spouses with income derived solely from agricultural activity. Late-payment interest The obligation of paying late-payment interest becomes mandatory for all entities, irrespective of their nature and in the absence of conflicting provisions. Increase of unemployment subsidies The daily amount of the unemployment subsidy may be increased by 10%, per beneficiary, in the following situations: a) When, in the same household, both spouses or people

in a non-marital cohabitation relationship receive unemployment subsidies and have children or other dependents;

b) When, in a single parent household, the single parent is receiving unemployment subsidy and does not receive any alimony allowance ordered or approved by a Court.

Reimbursement of social security contributions Regarding employees more than 45 years old, a new measure is proposed, of reimbursement of 75% or 100% of the contributions to social security made by employers depending if the employment contract has a fixed or indefinite period, up to a certain value.

Members of governing bodies (MGB) MGB which perform management or administration functions become entitled to protection in the event of unemployment. The contribution rate applicable to members of the board and managers of companies is set at a rate of 34.75%, 23.75% and 11% to employers and MGB, respectively. Entrepreneurs and owners of Individual Establishment of Limited Responsibility (IELR) Entrepreneurs with income arising from any commercial, industrial or forestry activities, as defined in the Personal Income Tax Code, as well as the owners of IELR and their spouses (with whom they develop the activity on a regular and ongoing basis) will be covered by the self-employed regime. Social protection granted by the self-employed regime shall include the right to protection in the event of unemployment. In these cases, the contribution rate is set at 34.75%. Employees holding public functions Employees holding public functions are no longer included in the employees of non-profit entities’ regime, since a new section has been added to the Social Security Code, which applies exclusively to these individuals. This regime remains unchanged, except for the contribution rate for employers which increases from 22.3% to 23.75%, in case of hired employees, and from 17.2% to 18.6%, in case of appointed individuals.

State Budget 2013 PwC

23

4. Corporate Income Tax

State Budget 2013 PwC

“Tax measures with the potential to foster economy are scarce, so additional measures are expected over the next two years.” Maria Torres, Tax Partner

24 State Budget 2013 PwC

4. Corporate Income Tax

Expenses incurred with invoicing equipment and software Expenses with the acquisition or modification of electronic invoicing software and hardware equipment, as a result of the communication obligations foreseen in Decree-Law 198/2012, which are acquired or modified in 2013, may be tax deductible in the fiscal year in which they are incurred. Securities Investment Funds and Real Estate Investment Funds The positive balance between capital gains and capital losses obtained by securities investment funds becomes subject to a 25% tax rate (currently 21.5%). The tax rate applicable to property income obtained by real estate investment funds is increased from 20% to 25%.

Limitation to the deductibility of financial costs Net financial costs may only be deductible up to the higher of the following limits: 3 million euros or 30% of the profit obtained before depreciations, net financing expenses and taxes. Nevertheless, a transitional period is foreseen, under which such limitation shall be gradually increased. The deductible percentage shall then amount to 70% in 2013, 60% in 2014, 50% in 2015, 40% in 2016 and the 30% limit will only apply in 2017. Financial costs, which are not considered as tax deductible, as a result of the application of such limitations may be carried forward for a period of 5 fiscal years, as long as such limits are always complied with. Furthermore, when the amount of financial costs considered as tax deductible is lower than the 30% limit, the immediate and successive carry forward of the unused limit is allowed for the following 5 fiscal years, until the total amount is used. Thin capitalisation This rule is entirely replaced by the limitation to the deductibility of financial costs previously mentioned. Special payments in account The amount of payments in account to be deducted, when computing the special payment in account, in the context of the application of the special fiscal consolidation regime, shall be the one that would be due in the event such regime was not applicable.

25

4. Corporate Income Tax

Rates – Income earned by non-residents Increase of the tax rates, applicable to income earned by non-residents pertaining to royalties, commissions, services and property income from 15% to 25%.

State surcharge The existing progressive rates (3% and 5%) are maintained. However, the State Surcharge is aggravated via the lowering of the minimum taxable income threshold (from 10 million euros to 7.5 million euros), from which the 5% rate begins to apply. This aggravation is applicable to the fiscal year beginning as of or after 1 January 2013. Payments in account The turnover limit for using the lower rate in the calculation of payments in account is updated to 500 000 euros and the applicable rate increases from 70% to 80%, for taxpayers with a turnover in the previous fiscal year equal to or below that amount. The rate applicable to the remaining tax payers increases from 90% to 95%. Whenever the amount of the payment in account already made is equal to or higher than the amount of tax that will be due in the end of the fiscal year, the taxpayer may only cease to make the third payment in account. Additional payments in account The minimum taxable profit threshold for the application of the higher rate, when assessing additional payments in account, is adjusted in conformity with the changes made to the State Surcharge, thereby decreasing from 10 million euros to 7.5 million euros. This aggravation is applicable to the fiscal year beginning as of or after 1 January 2013.

Resident Entities

Income 2012 Amended

2012 Budget

2013

Dividends 25% 25% 25%

Interest on deposits 25% 25% 25%

Interest on shareholders’ loans 25% 25% 25%

Interest on bonds 25% 25% 25%

Capital income paid or made available in accounts opened in the name of one or more holders but on behalf of unidentified third-parties

30% 35% 35%

Royalties 16.5% 25% 25%

Other capital income 16.5% 25% 25%

Property income 16.5% 25% 25%

Non-Resident Entities

Income 2012 Amended

2012 Budget

2013

Commissions 15% 15% 25%

Services 15% 15% 25%

Lease of agricultural, industrial, commercial or scientific equipment 15% 15% 25%

Dividends 25% 25% 25%

Interest on deposits 25% 25% 25%

Interest on shareholder loans 25% 25% 25%

Interest on bonds 25% 25% 25%

Capital income paid or made available to entities resident in low-taxation regions

30% 35% 35%

Capital income paid or made available in accounts opened in the name of one or more holders but on behalf on unidentified third-parties

30% 35% 35%

Royalties 15% 15% 25%

Other capital income 25% 25% 25%

Property income 15% 15% 25%

Wealth increases: Capital gains on shares 25% 25% 25%

Capital gains on real estate 25% 25% 25%

2012 2013

Turnover n-1 (Euros)

Payment in account (rate) Turnover (Euros) Payment in

account (rate)

Equal to or below 498 797.90 70% Equal to or below

500 000 80%

Above 498 797.90 90% Above

500 000 95%

2012 2013

Turnover (Euros) Additional payment in account (rate)

Turnover (Euros) Additional payment in account (rate)

From over 1 500 000 until 10 000 000

2.5% From over 1 500 000 until 7 500 000

2.5%

Above 10 000 000 4.5% Above 7 500 000 4.5%

State Budget 2013 PwC

26

Incentive regime for research and development (SIFIDE II) – Authorisation to introduce changes to the regime A legal authorisation is granted to the Government with the purpose of transferring this tax benefit to the Investment Tax Code, with the following amendments: • The tax benefit shall be granted proportionally to the

assets acquired and allocated to research and development activities;

• Eligible employees' costs shall be capped at the highest additional deduction foreseen in case of costs with employees with higher education;

• Introduction of an additional deduction in case of micro, small and medium companies;

• Change in the additional deduction applicable to micro, small and medium companies which have not yet completed two years of activity and have not benefitted from the incremental rate foreseen under the tax benefit;

• Definition of anti-avoidance rules and control mechanisms available to the tax authorities.

Transfer abroad of a company’s residence The Government is allowed to change the tax regime applicable to the transfer abroad of a company’s residence and to the termination of activity of non-resident entities, in conformity with the decision of the Court of Justice of the European Union, dated 6 September 2012, regarding process C-38/10. This authorization aims to allow the introduction of a new tax regime applicable to the company whose tax residence is altered (or whose permanent establishment is terminated), in which it becomes possible for the company to opt for the deferred payment of the amount of tax computed over the difference between the market value and the amounts relevant for tax purposes of its assets and liabilities at the time of the transfer, in case the move takes place to another EU Member State or state belonging to the European Economic Area. Such deferral can take place until the relevant assets and liabilities are no longer linked to the corporate activity or, alternatively, the payment of the tax amount due can be made in annual instalments. The option for any such form of deferral of taxation shall imply, along with the fulfilment of specific declaratory obligations, the payment of interest and the provision of a suitable guarantee.

Tax Regime for Investment Support – RFAI – Extension The Tax Regime for Investment Support – RFAI is extended until 31 December 2013. Tax Regime for Investment Support (RFAI) - Authorisation to introduce changes to the regime A legal authorisation is granted to the Government with the purpose of introducing the following amendments to the regime: • Extension of its application until 31 December 2017; • Review of the annual cap of the CIT credit - to be set

between 25% and 50% of the assessed CIT (currently 25%);

• Review and broadening of the regime applicable to the CIT credit for eligible investments, in order to include reinvestment of profits made until 2017, introducing rules and caps to the deduction against the assessed CIT in the subsequent five fiscal years of the unused CIT credit, in case the assessed CIT is not sufficient;

• Introduction of an additional tax incentive in case of reinvestment of profits and capital contributions, by means of a CIT credit, of up to 10% of the retained and reinvested profits and capital contributions made until 31 December 2017, whenever used in the acquisition of eligible assets;

• Exclusion from the scope of the regime of certain business activities, in case of entities whose main activity is developed in the energy sector, as well as of investments made within third generation broadband networks;

• Establishment of a set of anti-abuse rules and control mechanisms aiming at allowing the tax authorities to ensure the compliance with the material requirements of the regime.

Capital contributions - newly incorporated companies A legal authorisation is granted to the Government to introduce a tax credit up to the amount of the assessed CIT or PIT, corresponding to a maximum of 20% of the capital contributions made during the first 3 years of activity of newly incorporated companies, capped at 10 000 euros. Result of Assessment The Government is authorised to review the scope of application of article 92 of the CIT Code, in order to exclude the deductions to the assessed tax there foreseen.

4. Corporate Income Tax

State Budget 2013 PwC

27

Incentives for the acquisition of companies in difficult economic situation From 1 January 2013 onwards, the regime of incentives applicable to the acquisition of companies in a difficult economic situation, for cases approved by the Coordination Office for the Recovery of Companies (GACRE), may also apply to cases approved by the Institute for the Support of Small and Medium Enterprises and Innovation (IAPMEI) within the framework of the Incentive System for the Revitalization and Modernization of Companies (SIRME). Generically, the regime foresees the possibility of the deduction of tax losses assessed ,but not yet deduced by the acquired company, in the five fiscal years preceding the application of the regime, against the taxable income of the acquiring company, in proportion of its participation in the share capital of the acquired company, capped at 60% of such taxable income and as long as such tax losses are still within the carry forward period allowed by the CIT Code for tax losses.

4. Corporate Income Tax

“Companies with high financial costs will not be immediately affected, as a result of the introduction of a transition regime until 2017.” Rosa Areias, Tax Partner

Contractual tax benefits for investment A legal authorisation is foreseen, to allow the Government to broaden the scope of application of the contractual investment tax benefits to investments of an amount equal to or higher than 3 million euros (currently, 5 million euros). Madeira International Business Centre The Government shall promote the necessary amendments to the Statute of Tax Benefits in order to transpose the state aid to be granted to the Autonomous Region of Madeira, concerning the tax benefits available for companies licensed and operating in the Madeira International Business Centre.

State Budget 2013 PwC

28

Tax regime applicable to external loans The CIT and PIT exemption, applicable on interest derived from Schuldscheindarlehen loan agreements signed by the Public Treasury Institute (IGCP), on behalf of the Portuguese Republic, provided the creditor is not resident in Portugal and has no permanent establishment herein to which the loan can be allocated to, is extended to 2013. The tax exemption depends on the verification by IGCP of the established requirements. Repo Operations The CIT exemption on gains obtained by non-resident financial institutions on securities’ report operations, undertaken with resident credit institutions, is maintained. The exemption applies provided that such gains are not attributable to Portuguese permanent establishments of non-resident financial institutions.

Special tax regime applicable to debt securities issued by non-resident entities PIT and CIT exemption on income from debt securities representing public and non-public debt issued by non-residents is maintained. The exemption applies provided that the income is considered to be obtained in Portugal, under Portuguese tax rules, and paid by the Portuguese State as a guarantor of the obligations undertaken by the entities in which it owns a participation, together with other EU Member States. This exemption applies to effective beneficiaries that fulfil the requirements stated in the legal diploma of the debt securities regime. Financial sector contribution The financial sector contribution is extended to 2013.

4. Corporate Income Tax

State Budget 2013 PwC

29

5. VAT and other indirect taxes

State Budget 2013 PwC

“There is a new Excise Duty on natural gas and the recovery of VAT on bad and irrecoverable debts has been restructured.” Susana Claro, Tax Partner

30

Recovery of VAT on bad and irrecoverable debts Regarding irrecoverable debts, VAT is now recoverable on debts from companies subject to the special process of revitalization, and also debts from companies under the System for the Extrajudicial Recovery of Business (the reference to the extinct extrajudicial conciliation agreement is eliminated). New rules were introduced for the recovery of VAT on “bad debts” and "irrecoverable debts“ that become due as from 1 January 2013. The recovery of VAT on irrecoverable debts is subject to the certification of the statutory accountant. Regarding bad debts, recovery of VAT will be possible for: a) Credits outstanding for more than 6 months, when

the debtor is a private person or a taxpayer that perform exclusively exempt operations without the right to deduct;

b) Credits outstanding for more than 24 months for which there is a clear evidence of impairment and that efforts have been made to collect such debts, and also that the accounted asset has been written off;

Obligation to submit an authorisation request to the Portuguese Tax and Customs Authorities for the regularization of the bad debts described in b) above. This request for authorisation should be filed within a period of 6 months and is presumed to be tacitly rejected or accepted after 8 months, when the credit value exceeds 150 000 euros or not (VAT included), respectively. The submission of the authorization request triggers the notification of the purchaser to provide its opinion or to adjust the VAT in favour of the State, otherwise an additional assessment may be issued. The present changes are only applicable to the debts that become due from 1 January 2013; the current law is applicable to the debts due before that date. In case of the transfer of credits, the seller loses the right to deduct VAT on bad debts.

Change in the VAT system for operations performed within agricultural holdings Both the VAT exemption foreseen in article 9 (33) of the VAT Code and Annexes A and B are abolished. The supply of goods made under certain agricultural activities and the rendering of services that contribute to performing such agricultural activities will be taxed at the reduced rate. Extension of VAT exemptions The transfer of copyright and the authorisation for the use of intellectual work, as defined in the Portuguese Copyright Code is VAT exempt when the author is a legal person (re-establishing the exemption applicable until the end of 2011). VAT exemption is extended to the offer of goods to the State for subsequent distribution to people in need (thus assimilating these offers to the ones made to Social Security Public Institutions and to non-profit non-governmental organisations) Right to deduct It is clarified that the VAT assessed and paid for by the purchaser of goods and services can be deducted. Extension of the right to deduct of VAT on the use of diesel, LPG (Liquefied petroleum gas), natural gas and biofuels in machines with registration plates attributed by the competent authorities. Waiving of the VAT exemption – immovable property not effectively used for business purposes The period of two years foreseen for the adjustment of the VAT in favour of the State (established in the Regime for the waiving of the VAT exemption related to immovable property transactions), regarding immovable property that is not being effectively used for business purposes, will pass to 3 years.

5. VAT and other indirect taxes

State Budget 2013 PwC

31

Declaration for a single act Abolishment of the obligation to file a declaration in one of the tax offices in case of a single act, becoming obligatory to declare the single act electronically. Unofficial assessment It is clarified that the unofficial assessment issued in the absence of submission of VAT returns does not have effect if an unofficial closing down of the activity, pursuant to article 34 (2), is presented and the referred assessment relates to the period elapsed since the moment when the closing down should have occurred. Legislative authorisations Within the framework of the measures against fraud and tax evasion, the Government is authorised to ask the European Commission for a derogation from the VAT Directive with the purpose of amending article 2 of the VAT Code in order to allow the application of the reverse charge rule to the supply of raw materials in the agricultural, forestry and energy sectors. The Government is also authorised to create a simplified and optional cash accounting VAT scheme applicable to small businesses that do not qualify for tax exemption, according to which the operations carried out become chargeable when the seller gets paid and the right to deduct VAT is exercised at the time of actual payment. Social Security Public Institutions and Lisbon Charity The special VAT refunds scheme is recovered in 2013.

Communication of the information of invoices The limit date to communicate the information of issued invoices to the tax authorities passed to the 25th of the month following the one in which the invoices were issued. Transport documents The entry into force of the changes to the Regime for goods in circulation, established in Decree-Law 198/2012 of 24 August and in the SB, will be postponed to 1 May 2013. If a paper issued invoice serves as a transport document that accompanies goods in circulation, the taxable persons are exempt from the obligation to communicate the transport to the tax authorities. With respect to transports for which the recipient is not known yet, in which the destination of the goods is changed or in case in which the goods are not immediately or totally accepted, the communication is made directly on the site of the tax authorities, up to the 5th working day after the one in which the transport was carried out. With respect to the communication of printing houses to the tax authorities, each request of a taxable person to one of the printing houses will trigger an alert on the website of the tax authorities, implying that the taxable person will not be able to print these documents if he is not registered with the tax authorities. Special scheme for investment gold Reduction of the threshold (from 12 500 to 3 000 euros) as from which the traders in investment gold should keep a record with the identification of each client. Declaration of changes and Declaration for cessation of activity With respect to intra-Community transactions, the declaration of changes and the declaration of cessation of activity take effect on the day of their submission. Unofficial change of elements The Portuguese Tax and Customs Authorities can, on their own initiative, change the elements of the taxpayers in situations of non-activity, false statements or in case where there is evidence of fraud.

5. VAT and other indirect taxes

State Budget 2013 PwC

32

Excise Duty over Natural Gas New Excise Duty on the supply of natural gas to final consumers at the rate of €0.30/gJ. Excise Duty over Electricity A twofold increase of the minimum level of the rates on Electricity: • Minimum level: from €0.5/kw to €1/kw • Maximum level: from €1/kw to €1.1/kw Circulation between the Continent and the Autonomous Regions of products subject to Excise Duty With the exception of certain types of wine and other drinks, the circulation between the Continent and the Autonomous Regions of products subject to Excise Duty at a rate of 0% no longer benefits from the exemption of the application of the general regime of circulation of products subject to Excise Duty. In case of the above referred types of wine and other drinks that keep benefitting from the exemption, a previous authorisation for their circulation is now mandatory.

5. VAT and other indirect taxes

Excise duties on alcohol and alcoholic beverages Increase of 7.5% of the excise duties on spiritual drinks and 1.3% on other drinks subject to excise duties. Excise duties on tobacco Fine-cut tobacco and other forms of tobacco suffer a very significant change in their taxation which results in a substantial increase in the tax, aiming at approximating such taxation to the existing taxation over the more commonly sold tobacco (cigarettes, cigarillos, cigars). Contribution from the Road System Increase of 3.6% on gasoline and diesel oil.

State Budget 2013 PwC

33

6. Wealth Taxes

State Budget 2013 PwC

“Taxation of the financial transactions is now more likely, considering the EU initiative on the reinforced cooperation.“ Jorge Figueiredo, Tax Partner

34 34

6. Wealth

Stamp Tax - Term for the assessment of tax The term for the assessment of tax, which is limited to a 8-year period, currently applicable in case of the Stamp Tax levied on onerous transfers of real estate or other real rights on immovable property, will also apply to acquisitions of real estate by means of donations. Stamp Tax – Repo operations Exemption of Stamp Tax is renewed for 2013 on securities repos or similar rights exchanged in stock markets, as well as the repo and fiduciary sales in guarantee, performed by financial institutions intermediated by central counterparties. Stamp Tax – Company recovery plans An exemption of Stamp Tax is introduced regarding all acts subject to this tax, regarding company recovery plans, under the terms of the Companies Recovery and Insolvency Code. Stamp Tax –Warranties A Stamp Tax exemption is applicable in 2013 on guarantees provided in favour of the State or Social Security institutions, in relation to the payments of debt instalments, which may be collected under administrative procedures, or relating to the recovery of tax and Social Security credits. Stamp Tax – Social games Stamp tax will be levied at 20%, on the prizes received from Euromillion, National Lottery, Lotaria Instantânea, Totobola, Totogolo, Totoloto and Joker, on the amount that exceeds 5 000 euros. In case of prizes paid in instalments, the tax becomes due at the time of each payment, with reference to the proportional part of the tax computed on the total prize.

Real Estate Tax (RET) – Update of the buildings registration value Assuming that the general tax valuation for urban buildings will be concluded by the tax authorities by the end of 2012, it is proposed to revoke the provision foreseeing that the first transmission of urban buildings not yet valuated under the more recent RET rules triggers a new tax valuation under the rules in force. Real Estate Tax (RET) – Payment date For amounts not exceeding 250 euros, it is maintained the payment in one instalment in April. For amounts that exceed that limit, RET will be paid (i) in two instalments in April and November, for amounts between 250 and 500 euros inclusive, and (ii) in three instalments in April, July and November, for amounts exceeding 500 euros. Real estate located in areas of business location Prorogation until 31 December 2013 of the exemptions from property taxes (RET and RETT) on the acquisition or conclusion of real estate located in areas of business location ("ALE - Áreas de localização empresarial"). Investment funds for urban rehabilitation It is kept until 31 December 2013, the possibility of setting up investment funds for urban rehabilitation, that can benefit from the favourable tax regime set in the Statute of Tax Benefits. Real Estate Transfer Tax (RETT) – Close-ended real estate investment funds with private subscription The assignment of buildings to the unit holders at the time of liquidation of closed-ended real estate investment funds with private subscription and the transmission of buildings under a merger between this type of real estate investment funds is subject to RETT.

State Budget 2013 PwC

35 35

6. Wealth

Stamp Tax – Financial Transaction Tax The Government was granted a legislative authorisation to regulate the taxation of financial transactions taking place in a secondary market, with the following scope: • Define the types of transactions covered by this

taxation, namely the purchase and sale of financial instruments, such as shares, bonds, money market instruments, investment funds, structured products and derivatives as well as the conclusion or change of derivative contracts;

• Establish a special regime applicable to highly frequent operations, aiming at the prevention and correction of markets speculative interventions;

• Establish the rules that define the taxable person, tax burden and also territoriality rules;

• Establish the transactions excluded from taxation; • Establish the rules to calculate the amount subject to

taxation, namely in the case of derivative financial instruments and their electable rules;

• Define the tax rates with the following maximum values: i) up to 0.3% for most operations; ii) up to 0.1%, in case of highly frequent operations; iii) up to 0.3%, in the case of derivative instruments;

• Define the procedures, payment deadlines, ancillary obligations and control mechanisms;

• Define a tax liability and penalties regime.

State Budget 2013 PwC

36

7. Accessory Tax Duties

PwC

“The scope of VAT customer and supplier annual reporting (Annexes O and P of Annual Declaration – IES) has been extended to include the billing and documentation of transportation reporting duties” Paulo Ribeiro, TMAS Director

State Budget 2013

37

It becomes mandatory to report in Model 10, some income excluded from taxation, as literary, artistic and scientific prizes. This obligation will also apply to employment income not subject to PIT, in whole or in part, like in the case of payments for the termination of employment agreement. Entities responsible for the payment of income subject to withholding tax at flat rates will be required to deliver to the beneficiaries, resident in Portugal, who will opt for its inclusion in the total aggregate income, a statement proving the amount of such income paid and the amount of withholding tax made in the previous year. Information regarding financial transactions The Budget clarifies that the duty for persons subject to PIT of communicating their bank accounts in non-resident financial institutions applies to all bank accounts in which they are the holders, beneficiaries or are authorised to use. A beneficiary is a person that, directly or indirectly and irrespective of the legal title, controls the rights over the equity elements deposited in such account. Persons subject to PIT are now required to communicate accounts in non-resident branches of resident financial institutions. Presently, such duty only falls on accounts in non-resident financial institutions.

7. Accessory Obligations

PIT Income not subject or partially subject Entities owing income, totally or partially not subject to PIT (e.g. literary prizes, sports’ scholarships, awards for high-performance athletes), are required to fulfil some accessory duties, such as keeping an updated register of the beneficiaries of the income, delivering the taxpayer a document confirming the amounts owed regarding the previous year, amongst others. Income due to non-resident entities The moment of submitting a “Modelo 30” declaration by entities that paid or made available income to non-resident entities has been clarified. This return must be submitted by the end of the second month following that in which the taxable event occurs. Income due to residents The submission of “Modelo 10” related with employment income, is now due until the 10th of the month following the payment date or the date when the income was made available. Surcharge Entities paying employment income and pensions are required to withhold the surcharge and must communicate such amounts by means of the “Modelo 10” declaration, including such amounts to be delivered to the beneficiary of the income. Financial instruments Credit and financial institutions must report the financial instruments’ transactions through “Modelo 13”, by the end of March of the following year, instead of the end of June of the following year. Income and withholding tax obligations The communication of the employment income (currently made through Model 10 on an annual basis) shall be done until the 10th day following the month of its payment or availability notice.

State Budget 2013 PwC

38

Electronic notifications E-mail address Taxpayers who initiate their activity by 31 December 2012 have until the end of January 2013 to communicate their email address to the tax authorities. Persons subject to VAT are required to communicate their e-mail address within 30 days after the beginning of their activity or after being subject to the normal VAT legal framework.

“The international competitiveness of the tax system needs to emphasise the reduction of compliance costs, as well as the expansion of the tax base through simplification and enforcement.” Jaime Esteves, Tax Lead Partner

Tax compliance in Portugal

Facts and numbers • Time necessary to fulfil consumption taxes duties - 96

hours/ year (116th in the global ranking)

• Time necessary to fulfil tax duties – 275 hours/ year (EU & EFTA average – 184 hours)

• Total tax rate – 42.6% (EU & EFTA average – 42.6% | 114th in the global ranking)

PwC | The World Bank / IFC (2013) - Paying Taxes 2013. The Global Picture

7. Accessory Obligations

State Budget 2013 PwC

VAT and other indirect taxes VAT reporting The transaction value for the requirement to report transactions with clients and with suppliers for VAT purposes (annexes O and P of the Annual Declaration - IES) remains at 25 000 euros. Vehicles destruction It will become mandatory to send the tax authorities a certificate of the destruction of a vehicle within 30 days.

Vehicles tax reimbursement The procedures for reimbursement of tax regarding exported vehicles will be simplified, notably in relation to the documents of purchase, sale and shipment.

39

8. Tax Litigation

PwC

“More than substantive changes, the proposed adjustments regarding tax litigation focused mainly on tax procedure regulations.” Jaime Esteves, Tax Lead Partner

State Budget 2013

40 40

8. Tax Litigation

Guarantees In order to suspend the tax collection procedure, the amount of the guarantee being provided, within a term of 30 days as of the notification, is the one included in the notification of the beginning of the tax collection procedure. In cases where the amount in debt is paid in instalments, the waiver of the requirement to present a guarantee covers the entire period established in the instalment payment plan. Payment by instalments The number of instalments through which the tax debt may be paid is increased from 12 to 24, in cases where there is an evident exceptional financial difficulty and expected serious economical consequences. Late-payment interest Within tax collection procedures, the calculation of late-payment interest will not take into consideration the number of days already passed in the month in which the payment is made. Tax collection procedure It has been determined that the tax debt plus the interest payment does not affect the control by the Court of the entity in charge of tax collection, in case the judicial claim remains useful. Pledge of bank deposits The pledge of bank deposits in financial institutions is valid through 1 year, with the possibility of renewal. The depositary (financial institution) may obtain updated information in the tax authorities’ website, on the amount of the tax debt regarding the pledge to be made. In case of any new cash entries, it will also be obliged to proceed with the immediate pledge, up to the amount in debt. Penalty release In case of voluntary payment of the tax amount in debt, the individual taxpayers may be released from the penalty, provided that in the 5 previous years: (i) they have not been sentenced to a penalty in a compulsory procedure or in a tax crime procedure; (ii) they have not benefited from a penalty reduction; (iii) they have not benefited from a penalty release. Irregular consumption introduction The minimum amount of the applicable penalty is increased from 500 to 1 500 euros for individuals, and from 1 000 to 3 000 euros for corporate entities.