macroeconomic policy and economic performance: chile’s recent experience luis f. céspedes...

TRANSCRIPT

Macroeconomic Policy and Economic Performance: Chile’s

Recent Experience

Luis F. Céspedes

Ministry of Finance-Chile

Macroeconomic Policy and Stabilization

• External shocks, such as terms of trade and world interest rate shocks are key driving forces behind business cycle in emerging market economies.

• Economic stabilization depends crucially on the macroeconomic framework: monetary policy, fiscal policy and exchange rate regime.

• Reaction to shocks: countercyclical or pro-cyclical?– Maintain (reduce) interest rates and allow depreciation? – Raise interest rates to avoid depreciation and inflation? – Expansionary fiscal policy?

GDP Accumulated

LossesDuration

Initial fall in GDP

Chile 82 34,5% 7,0 -13,6%Chile 99 10,7% 6,0 -0,8%Mexico 95 10,7% 3,0 -6,2%Korea 98 11,1% 2,0 -6,7%Indonesia 98 22,6% 6,0 -13,1%Colombia 99 9,9% 5,0 -4,2%Ecuador 99 9,6% 3,0 -6,3%Latin America 81-82 24,6% 6,6 -4,2%Average Sample 13,6% 4,6 -2,1%

Latin America 81-82: Brazil, Bolivia, Costa Rica, Ecuador, Uruguay.

Cost and Duration Recessions: Selected Experiences

Chile: Policy Framework

• Flexible Inflation Targeting– Inflation target band: 2-4%.– Medium run horizon.

• Free-floating exchange rate regime.– Foreign exchange interventions under special circumstances.

• Fiscal Rule– Structural fiscal balance

Chile: Policy Framework

• Recent evidence indicates that macroeconomic volatility has been significantly reduced in recent years.

• The implementation of a flexible and credible inflation targeting regime has allowed monetary policy to play a key stabilizing role.

• Fiscal Policy has also been key to reduce the effects of external shocks in activity and in the competitiveness of the economy.

GDP volatility has decreased in recent years

0%

3%

6%

9%

12%

15%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Volatilidad

1990-1996 1997-2002

2003-2007

1980-1989

Sources: Ministry of Finance and Central Bank of Chile.

Central Bank has been able to implement a countercyclical monetary policy

Sources: Ministry of Finance and Central Bank of Chile.

1234567

Dic-01 Jun-02 Dic-02 Jun-03 Dic-03500

550

600

650

700

750

800

Interest Rate Exchange Rate

Fiscal Policy

• A credible fiscal policy is crucial to isolate government expenditure from economic fluctuations.

• During booms, higher fiscal savings reduce pressures on aggregate demand which stabilizes economic activity and the real exchange rate.

• Evidence indicate that in many developing economies, fiscal policy is pro-cyclical. Moreover, it is common that fiscal expenditure increases in a higher proportion than fiscal revenues during good times.

Fiscal Policy in Chile

• Government expenditures are determined by medium and long term fiscal revenues (structural revenues).

• Structural revenues are a function of potential output and the “reference” price of copper.

• During recessions the government borrows and during expansions it saves.

Fiscal Policy in ChileFiscal Surplus

2,2%

4,7%

-0,5%-0,5%

-1,2%

-2%

-1%

0%

1%

2%

3%

4%

5%

2001 2002 2003 2004 2005

External conditions have been favorable for the Chilean economy in recent years.

50100150200250300350400

Ene-0

0

Jul-0

0

Ene-0

1

Jul-0

1

Ene-0

2

Jul-0

2

Ene-0

3

Jul-0

3

Ene-0

4

Jul-0

4

Ene-0

5

Jul-0

5

Ene-0

6

Jul-0

6

Fuente: Cochilco

Fiscal Policy in ChileFiscal Surplus

-4,0%

-3,0%

-2,0%

-1,0%

0,0%

1,0%

2,0%

t-1 t t+1

Chile 1982 Chile 1999 Chile 2001

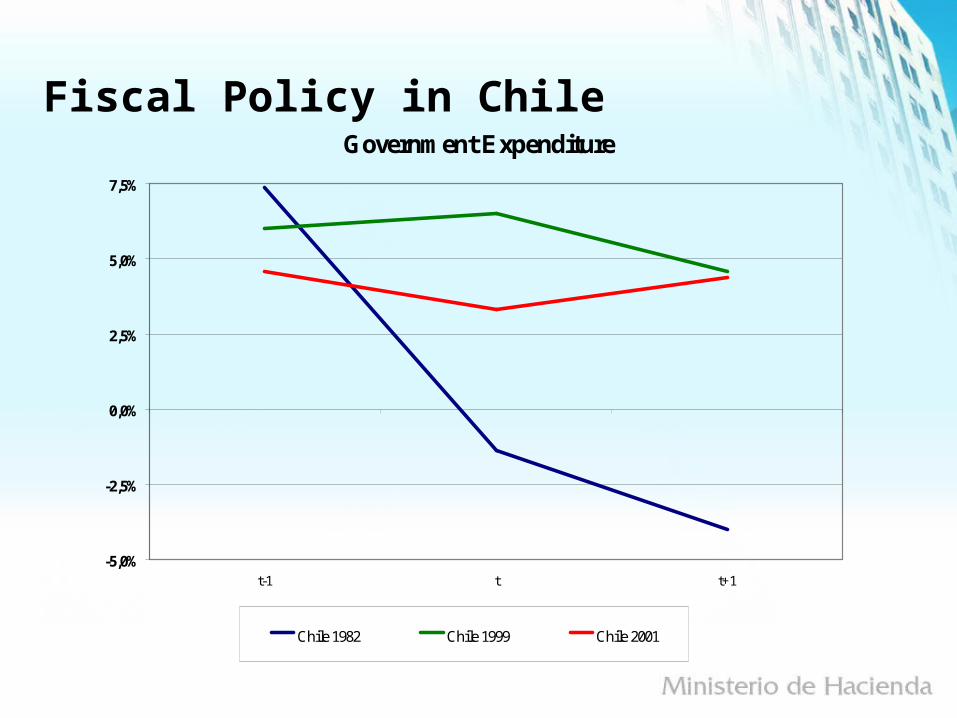

Fiscal Policy in ChileGovernment Expenditure

-5,0%

-2,5%

0,0%

2,5%

5,0%

7,5%

t-1 t t+1

Chile 1982 Chile 1999 Chile 2001

By increasing fiscal saving during good times, fiscal policy has reduced the appreciation of the RER

Sources: Ministry of Finance and Central Bank of Chile.

Average Price of Copper

% RER

Cycle 1994-1997 111,3 -8,4%Cycle 1998-2003 75,3 18,7%Cycle 2004-2006 173,9 -1,8%

Fuente: Banco Central.

Real Exchange Rate

75

80

85

90

95

100

105

110

115

Jun-86 Jun-90 Jun-94 Jun-98 Jun-02 Jun-06

75

80

85

90

95

100

105

110

115

Average 1990-2006 RER RER

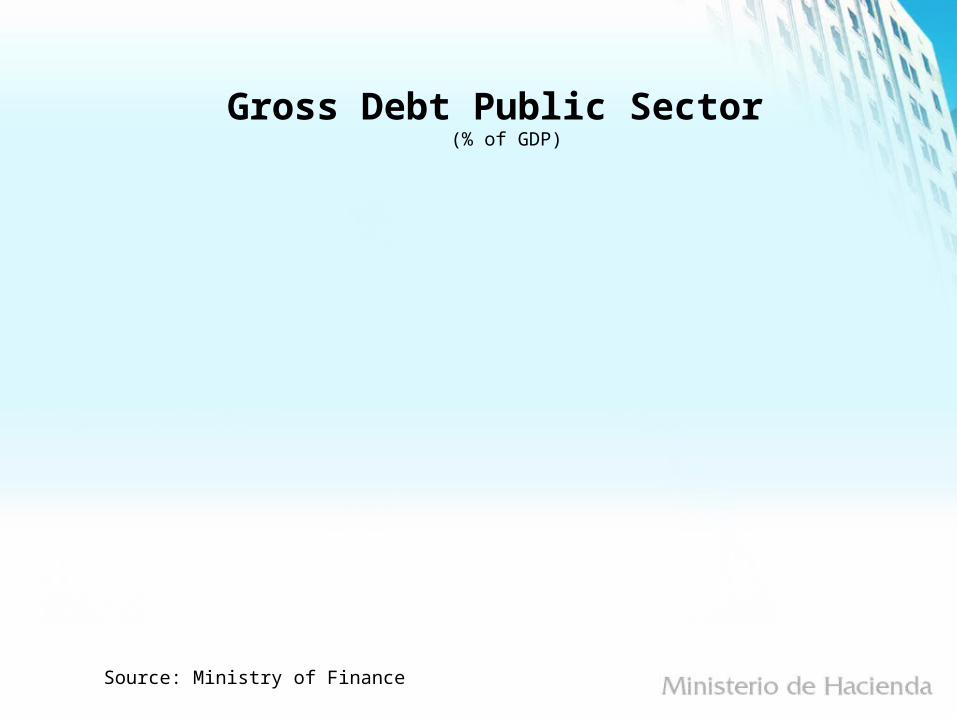

Gross Debt Public Sector (% of GDP)

Source: Ministry of Finance

0%

10%

20%

30%

40%

50%

60%

70%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

(p)

Gross Debt Central Government Gross Debt Central Bank

Portfolio management has also being consistent with keeping “competitiveness” of the economy

Financial Assets of the Treasury

71,3%81,6%

18,4%28,7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

April 2006 June 2006

Foreign Currency

Pesos

• Complements the Structural Balance Rule by focusing on the management of the financial assets generated by the implementation of the rule.

• Includes the creation of two funds: the pension reserve fund and the economic and social stabilization fund.

• Improves transparency of fiscal policy and financial asset management.

• Empowers the Government to capitalize the Central Bank.

The Fiscal Responsibility Law

ECONOMIC AND SOCIAL STABILIZATION FUND

• Accumulates all of the surplus that exceeds 1%of GDP

FISCAL SURPLUS

CAPITALIZATION OF THE CENTRAL BANK

• 0.5% of GDP for 5 years

PENSION RESERVE FUND

• 0.2% of GDP minimum• 0.5% of GDP maximum