macro strategy review jan 2014 - may 2015

TRANSCRIPT

Forward Markets: Macro Strategy ReviewMacro Factors and Their Impact on Monetary Policy,

the Economy and Financial Markets

The following is a recap of the analysis I provided in the monthly Macro Strategy Review (MSR) starting in January 2014 through May 2015. I think you’ll see why it can be a valuable resource as you navigate the current challenging investment environment.

My approach combines fundamental and technical analysis, which is unusual since most economists and financial advisors rely almost exclusively on fundamental analysis, which focuses on economic growth, monetary policy, equity valuations and the outlook for corporate earnings. While fundamental analysis is important, combining it with technical analysis can provide a more complete view since it incorporates market prices. Changes in the technical trend of a market have often led changes in the underlying fundamentals. A perfect example of the interplay between fundamental and technical analysis was provided in 2014.

In March 2014, European Central Bank (ECB) president Mario Draghi expressed concern about the low level of inflation and noted that the 15% increase in the value of the euro since July 2012 had shaved 0.4% off the European Union’s rate of inflation. Since the ECB had already lowered interest rates to 0% and wasn’t close to being able to launch a quantitative easing (QE) program, I concluded that the only stimulus left was for Draghi to lower the value of the euro. A decline in the euro would reverse its deflationary effects, boost growth by making exports cheaper and help make countries like Spain, Italy and France more competitive due to their higher cost of production. During the week of May 9, 2014, the euro experienced a weekly key reversal, which often

signals an important change in a price trend. Since the euro represents 57% of the dollar index, I concluded that the dollar was likely to rally 20%–25% and ultimately reach 100.00–102.00.

I believed a dollar rally of this magnitude would have a negative effect on emerging market (EM) currencies and equity markets and prove a headwind to future growth in those countries that have a current account deficit, a budget deficit and an elevated inflation rate. For advisors with exposure to emerging markets, this proved a valuable insight. I also believed that the rally in the dollar would pressure commodity prices in general, which proved prescient as oil, copper and numerous other commodities subsequently suffered large price declines. In March 2015, the dollar reversed lower after reaching 100.39. This suggested that the dollar was likely to pullback to 92.60–94.70, likely leading to a rally in the euro to 111.00–115.00, oil to $55.00–$59.00 a barrel and EM currencies and equity markets overall.

When prices fall below or rise above critical levels, technical analysis helps me quantify when I’m wrong so I can help advisors and investors do a better job of managing risk. Keeping losses small supports my philosophy that the best way to make money is to limit losses, and technical analysis can do that in real time. In my experience, fundamental analysis too often follows market reversals and by the time the “news” comes out, keeping losses small is more difficult.

Over the years I’ve received great feedback from advisors and investors who have found my analysis to be timely and insightful. Thanks in advance for taking the time to review this summary.

Jim Welsh

Macro Strategy—Portfolio Manager

2014 – 2015

Macro Strategy Review www.forwardinvesting.com2

Table of Contents

Macro Perspective—U.S. Economy _____________________________ 3

Eurozone ____________________________________________________ 9

Emerging Markets ___________________________________________ 16

Japan ________________________________________________________ 19

China ________________________________________________________ 21

U.S. Economy _________________________________________________ 27

Treasury Bonds ______________________________________________ 32

U.S. Stocks ___________________________________________________ 34

Macro Strategy Review www.forwardinvesting.com3

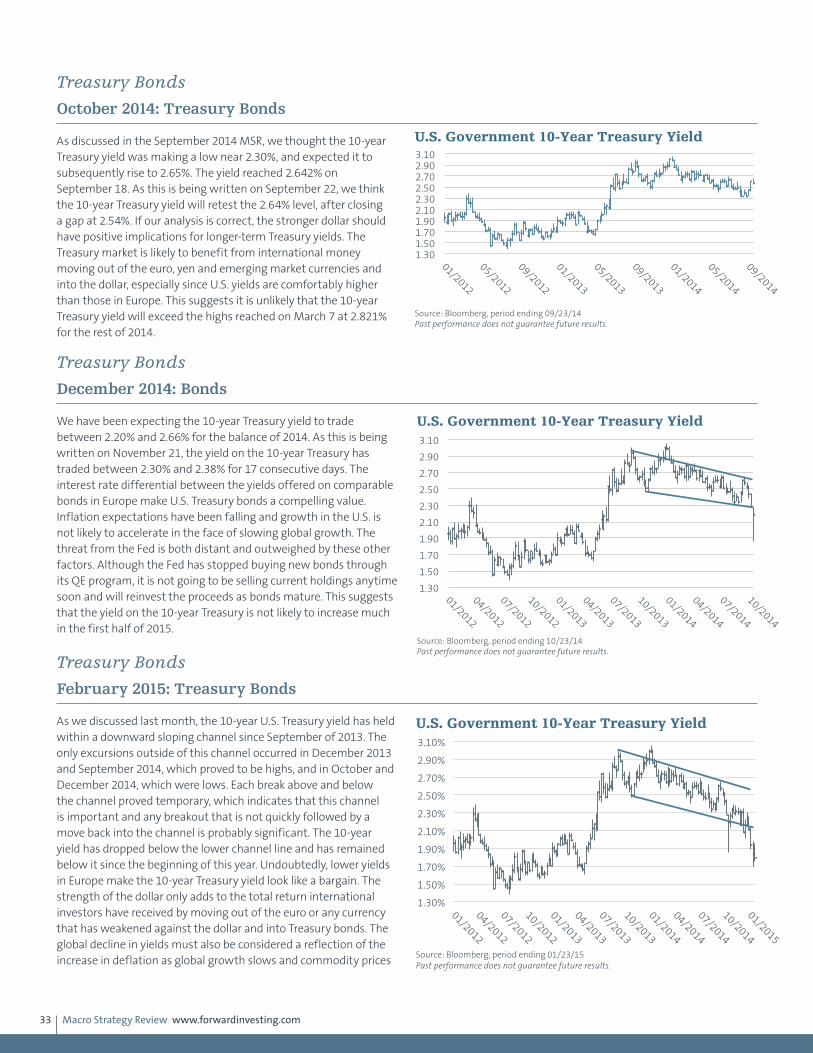

Macro Perspective—U.S. EconomyOctober 2014: Reaching the Limits of Monetary Policy

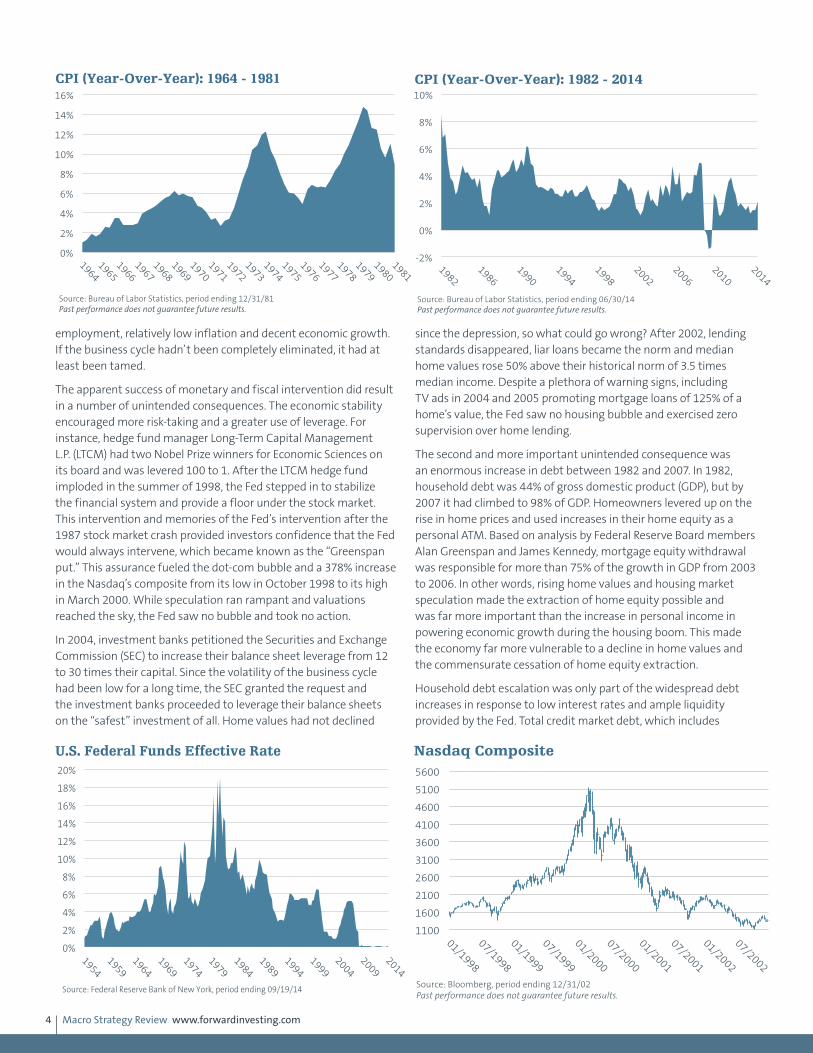

Economics has often been called “the dismal science” for good reason. President Harry Truman became so frustrated with the equivocations of his economists that he said, “Give me a one-handed economist! All my economists say, ‘…on the one hand…on the other.’”1 As the world was mired in the Great Depression in 1936, John Maynard Keynes wrote The General Theory of Employment, Interest and Money, which offered a theory for dealing with recessions. When private demand slackened due to a recession, Keynes advocated for intervention by the government and central bank to rejuvenate demand in the economy. This entailed the central bank lowering interest rates and the government launching infrastructure projects to inject government spending into the economy, which would then increase demand and create jobs. The deficit created by government spending during a recession would be funded by the issuance of government bonds. Once the economy returned to a path of steady growth, government surpluses would be used to pay off the bonds issued during the recession. The logic and common sense of Keynes’ theory made it easy to embrace. Any time a recession developed after World War II, Keynes’ game plan of lower rates and deficit spending was always implemented.

For the most part this economic prescription worked well. In seven of the 15 years after World War II the government actually ran a surplus, and in the 27 years between 1946 and 1972 economic growth averaged 4.15%. There was one problem, however: in the 300 months from 1957 to 1982 there were 64 months of recession. During these recessions, the unemployment rate spiked before the therapeutic effect of lower interest rates and fiscal stimulus turned the economy around. A recession caused the unemployment rate to zoom from 2.6% to 5.8% in 1954 and from 4.0% to 7.4% in 1958. Between 1968 and 1976 it soared from 3.4% to 8.9%. This pattern was unacceptable to the political system since elections could be lost if they occurred during a recession. To address this problem, Congress passed the Full Employment and Balanced Growth Act, which was signed into law by President Jimmy Carter on October

27, 1978. In addition to the Fed’s primary mandate of stable prices, the act would order that the Fed also conduct policy to ensure a low unemployment rate was maintained.

Labor costs make up approximately 65% of the cost of goods sold. Historically, full employment meant there was very little slack in the labor market, which often led to higher wages as companies bid up wages to keep or attract workers. Rising labor costs result in higher prices as companies are forced to raise the prices of their goods and services to cover higher labor costs. Wage inflation is far more intractable than inflation caused by higher food prices due to a drought or a temporary shortage. For the Fed to pursue a policy that would achieve full employment, it risked undermining its mandate for price stability. The contradictory nature of the two mandates wasn’t as important as passing legislation at a time of high unemployment with the words “full employment” in the title. For Congress, the notion of policies that are contradictory is almost perfection, since half the voters will be satisfied and the other half ripe for campaign contributions to fix the new problem.

Normally, people or organizations wouldn’t be given any additional responsibilities unless they had handled their original tasks well. Prior to 1979, the Federal Reserve had one policy mandate, which was to conduct monetary policy so prices remained stable. In 1965, the Consumer Price Index (CPI) rose a scant 1%. By 1975 it exceeded 12%, on its way to 14% in 1980. There were mitigating circumstances: the Organization of Petroleum Export Countries (OPEC) cut back on oil production and oil prices soared from $3.00 to $12.00 a barrel in 1974. Even with this concession, no one considered Fed chairmen Arthur Burns or G. William Miller as maestros of monetary policy. By any standard, the Federal Reserve did not do a good job of accomplishing their stable price mandate. This poor performance, however, did not dissuade Congress from giving the Fed the potentially contradictory second mandate of full employment.

Ironically, the tide of history was about to change after Paul Volker became Fed chairman in August 1979. Volker increased the federal funds rate to 18% in 1981 to break the back of inflation, which resulted in a secular bull market in bonds and stocks. In the 300 months between 1983 and 2007 there were only 16 months that the economy was in recession. By comparison, there were 64 months of recession in the 300 months from 1957 to 1982, as stated previously. The recessions during this 25-year period were more frequent and deeper than the shallow recessions in 1991 and 2001, which each lasted eight months. Between 1983 and 2007, the CPI spent most of its time range bound between 2% and 4%, much more under control than it had been in the 1970s. After peaking at 10.8% in November 1982, the unemployment rate consistently trended lower until it was back under 4% in 2000—returning to levels of the 1950s (see the U.S. Unemployment Rate chart on page 1). On the surface it appeared that manipulating monetary and fiscal policy had achieved the economic holy grail of full

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

1949

1954

1959

1964

1969

1974

1979

1984

1989

1994

1999

2004

2009

2014

U.S. Unemployment Rate

Source: Bureau of Labor Statistics, period ending 08/31/14

Macro Strategy Review www.forwardinvesting.com4

employment, relatively low inflation and decent economic growth. If the business cycle hadn’t been completely eliminated, it had at least been tamed.

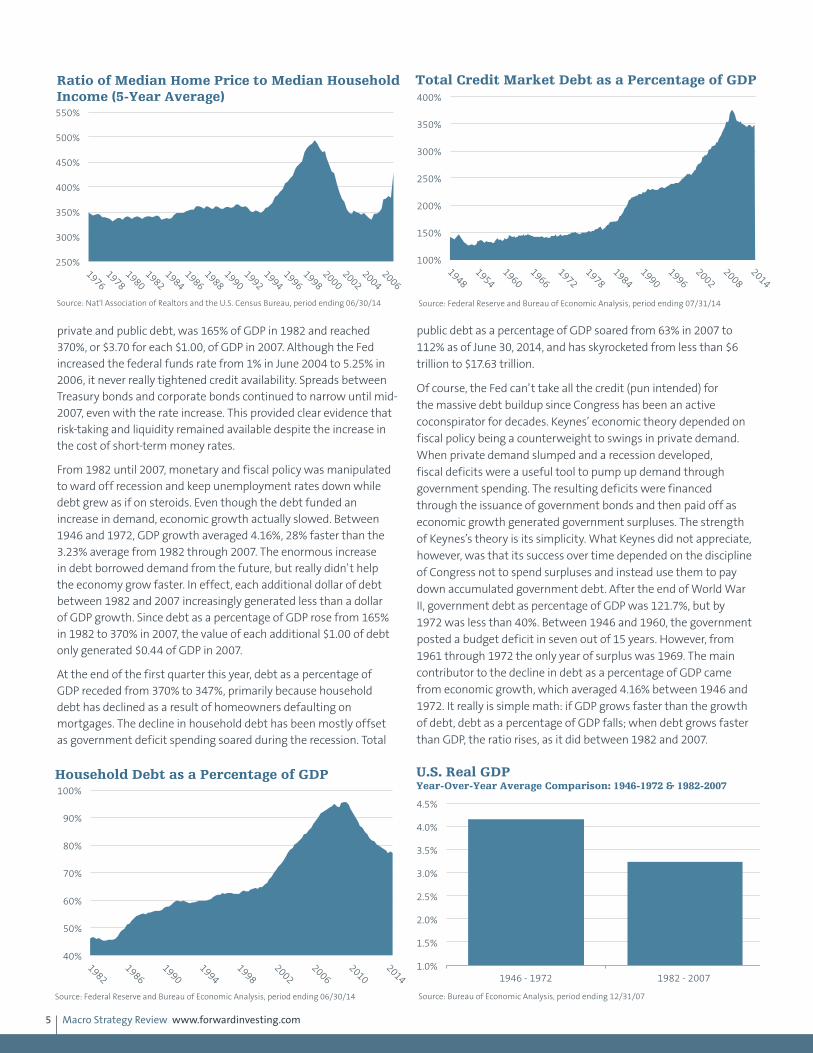

The apparent success of monetary and fiscal intervention did result in a number of unintended consequences. The economic stability encouraged more risk-taking and a greater use of leverage. For instance, hedge fund manager Long-Term Capital Management L.P. (LTCM) had two Nobel Prize winners for Economic Sciences on its board and was levered 100 to 1. After the LTCM hedge fund imploded in the summer of 1998, the Fed stepped in to stabilize the financial system and provide a floor under the stock market. This intervention and memories of the Fed’s intervention after the 1987 stock market crash provided investors confidence that the Fed would always intervene, which became known as the “Greenspan put.” This assurance fueled the dot-com bubble and a 378% increase in the Nasdaq’s composite from its low in October 1998 to its high in March 2000. While speculation ran rampant and valuations reached the sky, the Fed saw no bubble and took no action.

In 2004, investment banks petitioned the Securities and Exchange Commission (SEC) to increase their balance sheet leverage from 12 to 30 times their capital. Since the volatility of the business cycle had been low for a long time, the SEC granted the request and the investment banks proceeded to leverage their balance sheets on the “safest” investment of all. Home values had not declined

since the depression, so what could go wrong? After 2002, lending standards disappeared, liar loans became the norm and median home values rose 50% above their historical norm of 3.5 times median income. Despite a plethora of warning signs, including TV ads in 2004 and 2005 promoting mortgage loans of 125% of a home’s value, the Fed saw no housing bubble and exercised zero supervision over home lending.

The second and more important unintended consequence was an enormous increase in debt between 1982 and 2007. In 1982, household debt was 44% of gross domestic product (GDP), but by 2007 it had climbed to 98% of GDP. Homeowners levered up on the rise in home prices and used increases in their home equity as a personal ATM. Based on analysis by Federal Reserve Board members Alan Greenspan and James Kennedy, mortgage equity withdrawal was responsible for more than 75% of the growth in GDP from 2003 to 2006. In other words, rising home values and housing market speculation made the extraction of home equity possible and was far more important than the increase in personal income in powering economic growth during the housing boom. This made the economy far more vulnerable to a decline in home values and the commensurate cessation of home equity extraction.

Household debt escalation was only part of the widespread debt increases in response to low interest rates and ample liquidity provided by the Fed. Total credit market debt, which includes

-2%

0%

2%

4%

6%

8%

10%

1982

1986

1990

1994

1998

2002

2006

2010

2014

CPI (Year-Over-Year): 1982 - 2014

Source: Bureau of Labor Statistics, period ending 06/30/14 Past performance does not guarantee future results.

0%

2%

4%

6%

8%

10%

12%

14%

16%

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

CPI (Year-Over-Year): 1964 - 1981

Source: Bureau of Labor Statistics, period ending 12/31/81 Past performance does not guarantee future results.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1954

1959

1964

1969

1974

1979

1984

1989

1994

1999

2004

2009

2014

U.S. Federal Funds Effective Rate

Source: Federal Reserve Bank of New York, period ending 09/19/14

1100

1600

2100

2600

3100

3600

4100

4600

5100

5600

01/1998

07/1998

01/1999

07/1999

01/2000

07/2000

01/2001

07/2001

01/2002

07/2002

Nasdaq Composite

Source: Bloomberg, period ending 12/31/02 Past performance does not guarantee future results.

Macro Strategy Review www.forwardinvesting.com5

private and public debt, was 165% of GDP in 1982 and reached 370%, or $3.70 for each $1.00, of GDP in 2007. Although the Fed increased the federal funds rate from 1% in June 2004 to 5.25% in 2006, it never really tightened credit availability. Spreads between Treasury bonds and corporate bonds continued to narrow until mid-2007, even with the rate increase. This provided clear evidence that risk-taking and liquidity remained available despite the increase in the cost of short-term money rates.

From 1982 until 2007, monetary and fiscal policy was manipulated to ward off recession and keep unemployment rates down while debt grew as if on steroids. Even though the debt funded an increase in demand, economic growth actually slowed. Between 1946 and 1972, GDP growth averaged 4.16%, 28% faster than the 3.23% average from 1982 through 2007. The enormous increase in debt borrowed demand from the future, but really didn’t help the economy grow faster. In effect, each additional dollar of debt between 1982 and 2007 increasingly generated less than a dollar of GDP growth. Since debt as a percentage of GDP rose from 165% in 1982 to 370% in 2007, the value of each additional $1.00 of debt only generated $0.44 of GDP in 2007.

At the end of the first quarter this year, debt as a percentage of GDP receded from 370% to 347%, primarily because household debt has declined as a result of homeowners defaulting on mortgages. The decline in household debt has been mostly offset as government deficit spending soared during the recession. Total

public debt as a percentage of GDP soared from 63% in 2007 to

112% as of June 30, 2014, and has skyrocketed from less than $6

trillion to $17.63 trillion.

Of course, the Fed can’t take all the credit (pun intended) for

the massive debt buildup since Congress has been an active

coconspirator for decades. Keynes’ economic theory depended on

fiscal policy being a counterweight to swings in private demand.

When private demand slumped and a recession developed,

fiscal deficits were a useful tool to pump up demand through

government spending. The resulting deficits were financed

through the issuance of government bonds and then paid off as

economic growth generated government surpluses. The strength

of Keynes’s theory is its simplicity. What Keynes did not appreciate,

however, was that its success over time depended on the discipline

of Congress not to spend surpluses and instead use them to pay

down accumulated government debt. After the end of World War

II, government debt as percentage of GDP was 121.7%, but by

1972 was less than 40%. Between 1946 and 1960, the government

posted a budget deficit in seven out of 15 years. However, from

1961 through 1972 the only year of surplus was 1969. The main

contributor to the decline in debt as a percentage of GDP came

from economic growth, which averaged 4.16% between 1946 and

1972. It really is simple math: if GDP grows faster than the growth

of debt, debt as a percentage of GDP falls; when debt grows faster

than GDP, the ratio rises, as it did between 1982 and 2007.

250%

300%

350%

400%

450%

500%

550%

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Ratio of Median Home Price to Median Household Income (5-Year Average)

Source: Nat'l Association of Realtors and the U.S. Census Bureau, period ending 06/30/14

100%

150%

200%

250%

300%

350%

400%

1948

1954

1960

1966

1972

1978

1984

1990

1996

2002

2008

2014

Total Credit Market Debt as a Percentage of GDP

Source: Federal Reserve and Bureau of Economic Analysis, period ending 07/31/14

40%

50%

60%

70%

80%

90%

100%

1982

1986

1990

1994

1998

2002

2006

2010

2014

Household Debt as a Percentage of GDP

Source: Federal Reserve and Bureau of Economic Analysis, period ending 06/30/14

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

1946 - 1972 1982 - 2007

Source: Bureau of Economic Analysis, period ending 12/31/07

U.S. Real GDP Year-Over-Year Average Comparison: 1946-1972 & 1982-2007

Macro Strategy Review www.forwardinvesting.com6

In 2007, federal debt as a percentage of GDP was 64.5%—almost double 1982’s ratio of 32.5%. This increase occurred because the federal government ran a budget deficit in every year except four: 1998, 1999, 2000 and 2001. Capital gains tax revenues from the dot-com bubble were one of the primary reasons for the surplus years. Thus when the stock market declined in 2001 and 2002, those surpluses vanished. When it comes to government deficits, we are agnostic. A deficit is a deficit: whether it is the result of government spending or tax cuts, either way, future generations are on the hook to pay for them. This is one case where the means (liberal or conservative ideology) does not justify the net result. Both parties would, of course, argue this point. Ironically, each party is the opposite side of the same coin, which is currently valued at more than $17 trillion of debt.

A prominent Nobel Prize winning economist has argued that the reason the current recovery is so lackluster is because the government stimulus plan was too small. In other words, if the government had increased outstanding debt since 2009 by $8 trillion or $10 trillion instead of $6 trillion, the country would be better off. This argument totally ignores the fact that since 1982 each additional one dollar of debt has increasingly produced less than one dollar of GDP growth. Hopefully this economist has lots of children, grandchildren and great grandchildren so they can pay for his ideological largesse. A 3% annual budget deficit is commonly accepted as good by the majority of mainstream economists. This is like saying going broke is not a good thing, but if we’re going to go broke, it is better to do it slowly. But, according to the U.S. Office of Management and Budget, the average annual deficit from 1946 through 2013 was 2.09%, which has led to $17.6 trillion in federal debt.

A May 2012 ABC 20/20 news report entitled “Losing it: The Big Fat Trap” reported that Americans spend $20 billion a year on weight loss programs and diets with disappointing results. Losing weight is fairly straightforward—eat smaller portions, eat less fattening food and be more active. Getting our fiscal house in order is also straightforward—no more deficits and use surpluses to pay off prior debt. With each political party pitching their formula of spending or tax cuts to voters who, on balance, spend more time focused on sports, reality TV and social media, the odds of fiscal discipline breaking out anytime soon are slim. As we discussed in

the June MSR section “Economic Enervation,” Congress could also reduce the number of its regulations, which have likely contributed to slower economic growth since 1982. Since both political parties use regulations as a primary fundraising tool, we don’t expect a “let’s roll back regulation” movement to sweep the nation. Nor do we anticipate that Congress and the Federal Reserve will abandon their multidecade unsuccessful attempt to tame the business cycle.

There is a natural ebb and flow for everything on this planet, from ocean tides to seasons of the year. Recessions are a natural part of the business cycle, just as night follows day. In a practical sense, periodic recessions cleanse the economy and financial system of excesses, such as unneeded inventories or overleveraged companies. In this way, a balance is maintained between the supply and demand for raw materials, labor and credit, which ensures the underpinnings of the economy remain sound. The business cycle has been in existence as long as there has been something to sell and willing buyers. The notion the business cycle could be suppressed or eliminated with the ministrations of monetary and fiscal policy should have been deemed preposterous. Instead, hubris trumped common sense. In the pursuit of minimizing increases in unemployment and reelection, politicians embraced fiscal stimulus to ward off recessions but scorned the discipline to pay for the stimulus. The Fed has aided and allowed debt to grow faster than GDP, and in the process printed their way into a blind alley. With $3.47 of debt for every $1.00 of GDP, how much can the Fed raise rates without interest expense becoming a significant headwind for the economy and federal budget? At the September 2014 Federal Open Market Committee (FOMC) meeting, the median forecast for the 2017 federal funds rate was 3.75%. We suspect the Fed will be as correct on the federal funds rate forecast as their projections for 3%+ GDP growth in each of the past four years. The Fed has trained investors to be so dependent on an accommodative monetary policy that markets are fixated on when the Fed will remove the phrase “considerable period” from the FOMC statement. There will come an “uh-oh” moment when the global financial markets realize that central bank monetary policy is tapped out and perception can no longer trump economic reality. In the meantime, global markets can find comfort in the fact that the ECB will probably launch their version of quantitative easing by early 2015, the Bank of Japan will continue to debase its currency and the Fed won’t increase rates for a considerable period.

0

10

20

30

40

50

60

70

80

90

100

1948

1952

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

In T

hou

san

ds

Federal Register Pages Published Annually

Source: Federal Register, period ending 12/31/12

0

2

4

6

8

10

12

14

16

18

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

In T

rilli

ons

($)

U.S. Total Public Debt Outstanding

Source: U.S. Treasury, period ending 08/31/14

Macro Strategy Review www.forwardinvesting.com7

Macro Perspective—U.S. Economy

January 2015: Monetary Policy and Business Investment

The Federal Reserve has kept short-term interest rates barely above 0% for six years and has expanded its balance sheet from $900 billion in 2007 to $4.4 trillion in 2014 through quantitative easing. The suppression of interest rates and bond purchases by the Fed has made it possible for corporations to borrow cheaply. Issuance of investment-grade and junk bonds has soared from $953 billion in 2009 to $1.31 trillion in 2012, $1.41 trillion in 2013 and $1.39 trillion through November 2014. Borrowing at lower interest rates has saved corporate America several hundred billion dollars in interest expense in recent years, which is a good thing. However, an increasing number of companies have used debt to buy back their stock. In the 12 months through the end of November, 374 companies in the S&P 500 Index spent $567.2 billion on share buybacks, up 27% since November 2013. Over the last four years, corporations have spent more than $2.2 trillion on stock buybacks. Between 2003 and 2012, of the 449 companies publicly listed in the S&P 500, 54% of earnings were used to buy back stock and 37% were used to pay dividends. According to Barclays, the proportion of cash flow used for stock buybacks has almost doubled over the last decade. With such a large percentage of earnings being used to buy back stock, the proportion of cash flow used for capital investments has declined. One driver behind the shift toward more stock buybacks has come from the increase in executive compensation derived from stock options and stock awards. In 2012, the 500 highest-paid executives named in proxy statements of U.S. public companies received an average of $30.3 million. Of this total, 42% came from stock options and 41% from stock awards. What’s more astonishing than the level of compensation is the obvious conflict of interest. Some executives recommend to their firm’s board of directors that a better use of the company’s earnings is buying back more stock, or worse, that they should borrow money for the buybacks. The fact that stock buybacks somewhat directly

enrich executives is overlooked by the board, whose focus is supposedly on the long-term interests of the company. A mutual fund portfolio manager who buys a stock for his personal account before purchasing it for the fund runs afoul of security laws. A company, however, can buy its stock all day, every day based on a recommendation from the firm’s executives to the board of directors and the Securities and Exchange Commission sees no conflict of interest.

Cheap money has incentivized companies to increase earnings by using more of their cash flow and borrowed money to reduce their share count through stock buybacks rather than investing in their business and future. In addition to skimming capital investments for buybacks, corporations have kept their hiring and wage increases to a bare minimum. On the surface this looks like a winning business plan since after-tax profits as a percentage of GDP are at an all-time high. But upon further review, there is a less promising message: employee compensation as a percentage of GDP has been trending lower for decades and is at the lowest level since recordkeeping began in 1947.

Earnings juiced by stock buybacks and financial engineering along with the suppression of wages and quality jobs may make the S&P 500’s price-earnings (P/E) ratio appear reasonable. But these earnings are not the same quality of earnings derived from intelligent research and development (R&D) investment, new products and solid revenue growth. Henry Ford became famous for implementing the assembly line, which lowered the amount of time to build one car from 12 hours to just 93 minutes. The increase in the production of cars lowered the cost of each car produced, making them affordable. His real genius though may have been deciding to pay his workers enough so they could buy the cars his assembly lines produced.

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

1947

1953

1959

1965

1971

1977

1983

1989

1995

2001

2007

2013

Profits as a Percentage of GDP

Source: Federal Reserve Bank of St. Louis, period ending 07/01/14

40%

42%

44%

46%

48%

50%

52%

1948

1953

1958

1963

1968

1973

1978

1983

1988

1993

1998

2003

2008

2013

Wages as a Percentage of GDP

Source: Bureau of Economic Analysis, period ending 01/01/13

Macro Strategy Review www.forwardinvesting.com8

Macro Perspective—U.S. Economy

May 2015: Global Debt, Growth and Future Central Bank Policies

The global economic pie is shrinking relative to the growth rates of the past and that’s a problem. According to the International Monetary Fund’s (IMF) World Economic Outlook database, worldwide GDP growth during 2013–2014 averaged 3.10%, compared to 2006–2007, which averaged 5.15%. While GDP growth has declined, the chasm between growth in advanced economies and developing countries has not changed much. GDP growth in advanced economies has slowed -47.37% from 2.85% in 2006–2007 to just 1.50% in 2013–2014 while growth in developing countries has downshifted -45.06% from 8.10% to 4.45%, respectively. As this data indicates, the worldwide slowdown in growth has been evenly distributed and not merely concentrated in either advanced or developing countries.

The widespread impression that the global economy has deleveraged in the wake of the financial crisis is a fallacy—it is more leveraged now than it was prior to the financial crisis, based on the ratio of total global debt to GDP. In February, the McKinsey Global Institute published an extensive review of debt levels in 22 developed and 25 developing countries. The McKinsey analysis found that global debt had increased from $142 trillion in 2007 to $199 trillion in 2014. The $57 trillion increase in global debt represents a surge of 40%, far exceeding the 23% gain in global GDP during the same period. The global debt-to-GDP ratio rose from 269% at the end of 2007 to 286% as of June 30, 2014. The title of the McKinsey study was apt: “Debt and (not much) deleveraging.”

Although total global debt has increased 40% since 2007, the McKinsey Global Institute did find a couple of silver linings. The growth rate in global household debt slowed from 8.5% during the period of 2000–2007 to 2.8% in 2007–2014. Lax mortgage lending standards contributed to the excessive addition of mortgage debt prior to 2007 while tighter standards after the financial crisis curbed growth. The net result is that household debt is now growing in line with global GDP growth as compared to the debt binge prior

to 2007. When household debt grows in line with GDP growth, household incomes are more likely to grow fast enough to prevent a rise in defaults on mortgage, credit card and auto debt. The increase in debt and leverage by banks prior to 2008 was a major contributor to the financial crisis. A number of U.S. investment banks increased their leverage ratio from 12-to-1 in 2004 to almost 30-to-1 in 2007. A number of large European banks had leverage ratios of almost 40-to-1 just prior to the financial crisis. When home values fell in many countries, the excessive leverage decimated bank balance sheets and threatened the global financial system. Financial institutions have significantly lowered the growth rate of debt since 2007 from 9.4% to 2.9%. The deleveraging of bank balance sheets in the wake of the financial crisis is a strong indication that the global financial system is in far better shape than it had been and is capable of handling the next business cycle downturn and any unanticipated economic shock.

The same cannot be said about government debt and leverage. In response to the financial crisis, governments around the world increased spending to offset the decline in private demand as unemployment soared, consumers stopped shopping and businesses slashed spending. Much of the increase in government spending was financed with debt, which grew 60% faster in the seven years following the crisis than the precrisis level (9.3% versus 5.8%). The growth rate in government debt poses a perilous challenge for the global economy in coming years since the current level of government debt is already high enough to impair its capacity to deal with the next economic slowdown. Faced with another recession, we have no doubt that politicians around the world will respond with another round of deficit spending to minimize its impact—as that’s how they have repeatedly responded every time a recession threatened their reelections. Mae West famously said too much of a good thing could be wonderful, but we don’t think debt is one of those things. We don’t know how much debt is too much, but the economic engine of the global economy is certainly more at risk now than it was 30 years ago, even though global interest rates were far higher back then.

Most governments consider a deficit of 3% of GDP to be healthy, but the flaw in this perspective is it ignores the impact of “healthy” deficits over time. Total debt as a percentage of GDP doubles in just 24 years if a country maintains a “healthy” 3% annual deficit, meaning the long-term threat from continually running

Global Stock of Debt Outstanding Compound Annual Growth Rate

2000 – 2007 2007 – 2014

Total 7.3% 5.3%

Household 8.5% 2.8%

Corporate 5.7% 5.9%

Government 5.8% 9.3%

Financial 9.4% 2.9%

*47 nations, including 22 developed and 25 developing countries Source: McKinsey Global Institute, as of 06/30/14

Global Slowdown Compounds the Debt Challenge

Growth Rate 2006 – 2007

Growth Rate 2013 – 2014

Change in Growth Rate

World Average 5.15% 3.10% -39.81%

Advanced Economies 2.85% 1.50% -47.37%

Developing Countries 8.10% 4.45% -45.06%

USA 2.40% 2.05% -14.58%

Eurozone 2.80% 0.20% -92.86%

Source: International Monetary Fund, as of 12/31/14

Economic Growth Hasn’t Kept Pace With Debt

2007 2014

Global Debt* $142 T $199 T

Global Debt/GDP 269% 286%

*47 nations, including 22 developed and 25 developing countries Source: McKinsey Global Institute, as of 06/30/14

Macro Strategy Review www.forwardinvesting.com9

“healthy” annual deficits is that cumulative debt reaches a level that can hardly be described as healthy. However, any slowdown in government deficit spending will dampen growth in the short term unless household and corporate spending picks up the slack. That’s not likely in the short run since the global economy is suffering from a lack of demand due to a combination of high unemployment and underemployment, weak wage growth and excess capacity that has depressed business investment.

The Congressional Budget Office has estimated that a 1.0% increase in Treasury yields across the maturity spectrum would add $150 billion in interest expense to the annual U.S. government budget. Debt-to-GDP ratios in Europe and Japan are far higher than in the U.S., so their budgets and economies are even more vulnerable to higher interest rates. Any meaningful rise in global interest rates in coming years could accelerate budget deficits to well above 3% of GDP as interest expense on the mountain of accumulated sovereign debt soars—one reason central banks, especially in advanced economies, will find it extraordinarily difficult to normalize interest rates in coming years. This situation exposes an inherent conflict of interest between fiscal and monetary policy that has never been so pronounced and has the potential to further compromise central banks’ independence.

The level of GDP growth impacts the amount of cash flow generated in the form of personal income, corporate profits and government tax revenue. As economic growth accelerates, the ability to service debt becomes easier and the risk of defaults on mortgages, auto loans, corporate bonds and bank loans declines. Debt levels are higher now than in 2007 while global economic growth has slowed significantly and is only expected to reach 3.50% in 2015, according to the IMF. Even with that improvement in growth compared to the last two years, it will still be more than

30% slower than in 2007. In this respect the leverage in the global economy is more precarious than in 2007.

In the next few years, the global economy will be vulnerable to either a slowing from current growth levels or an increase in interest rates. Navigating these issues amounts to the economic equivalent of threading the needle since even a modest increase in interest rates is likely to disproportionately weigh on future growth as a larger share of cash flow will be needed to service debt. Any slowdown in the global economy would push central bankers even deeper into the uncharted territory of negative interest rates, unlimited quantitative easing (QE) and currency depreciation. The risk of deflation will continue to lurk in the shadows until the ratio of global debt to GDP actually declines.

Even though interest rates, especially in advanced economies, have spent years at their lowest levels in history, economic growth has fallen far short of historical norms. Big deficits and cheap money have failed to engender sustainable growth. This economic reality provides an insight into just how difficult it will be for the Fed, ECB and Bank of Japan (BoJ) to ever “normalize” short-term interest rates. Any increases are likely to be modest and stretched out over an extended period of time. Beginning in June 2004, the Fed increased the federal funds rate at 17 consecutive meetings. Nothing close to that will happen in this cycle. The pace of central bank rate increases in the next few years is likely to make a tortoise look like the Road Runner. The BoJ may never increase rates in our lifetime and the first increase the ECB effects will be to raise rates from below zero percent to zero percent. Welcome to the brave new world of modern monetary policy that is more effective in distorting market outcomes than generating actual economic growth.

EurozoneFebruary 2014: Eurozone

One of the ongoing challenges of the European Union (EU) is the disparity in productivity among its members. In the wake of the financial crisis, the least productive countries experienced a deeper and more prolonged contraction, resulting in far higher rates of unemployment that persists into 2014. Although the overall unemployment is 12.1% for the EU, it is 11% in France, 12.7% in Italy, 26.7% in Spain and 27.4% in Greece. In contrast, Germany’s unemployment rate is just 5.2%, hence the friction within the EU.

Prior to the formation of the EU in 1999, the productivity gap between countries could be closed through the depreciation of an individual country versus the currency of trading partners. For instance, if Italy wanted to improve its export competitiveness, it would lower the value of the Italian lira by 5%–10% or more. A decline in the lira would lower the cost of Italian exports and make Italian exporters more competitive with exporters around the world. Lowering the cost of exports through the depreciation of its currency, rather than cutting wages, kept Italian domestic demand stable, as a weaker currency lifted exports. However, with the establishment of a common currency for the members of the EU, the only way to improve export competitiveness is

through productivity improvements or lower labor costs, which is far more painful since lower incomes weaken domestic demand and GDP. For those countries whose productivity has lagged Germany over the last decade, the path to increased productivity will primarily be through labor market reforms. In the short run, labor market reforms will be politically unpopular in countries like France and Italy, and if enacted, will likely result in higher unemployment and slower GDP growth.

France’s core problem is that wages have been growing faster than productivity for years. In 2000, the socialists in France instituted the 35-hour workweek, so French workers have been producing less in less time too. Unemployment is 11% and youth unemployment is 26%. The minimum wage is now 62% of median income, versus 38% in the U.S. Anyone who has worked more than 28 months can receive up to 75% of their old salary for 24 months. The employer payroll tax can reach 48%, which means an employee paid $1,000 a month actually costs the employer $1,480 per month. Needless to say, private sector job growth has been almost nonexistent.

Welfare spending, including programs for youth, the unemployed and the elderly is set to reach 31% of GDP, the highest of the 34

Macro Strategy Review www.forwardinvesting.com10

OECD nations. Instead of reducing government spending, France increased spending so that government spending is now 57% of GDP, and debt as a percent of GDP jumped from 60% in 2007 to 92% in 2013.

Whether it was the result of its credit downgrade, Draghi’s comment, or recent polls which show that 74% of the French think France is on the decline and 83% view President Francois Hollande’s reform policies as ineffectual, Hollande appears to have experienced an epiphany. In a speech on January 14 he said, “How can we run a country if entrepreneurs don’t hire? And how can we redistribute if there’s no wealth?”2 Acknowledging that socialist redistribution does not create wealth and relies instead on entrepreneurs must have been an out-of-body experience for Hollande. Proof came when Hollande proposed cutting government spending to fund a $48 billion annual tax cut so companies won’t have to pay for France’s generous family welfare programs by 2017. It’s unlikely that one small program will pull the French economy out of a malaise that took decades to grow.

According to the OEDC, of its 34 participating countries, Italy’s output has grown the least over the last decade. This poor performance is partially due to the lack of currency flexibility, but is also due to government spending, high taxes and inflexible labor market regulations. Government spending is 50.7% of GDP and relies on high payroll taxes to fund its spending. According to the OECD, 33% of Italian salaries support Italy’s pension fund, compared to 13% in the U.S.’s Social Security system. Labor costs are higher than in Spain, but Italian workers have less disposable income after taxes are deducted. This is a bad combination since high labor costs suppress hiring, and low take-home pay mutes economic growth since workers have less money to spend. The lack of growth has resulted in chronic budget deficits, which has increased Italy’s debt to GDP ratio to 130%. Within the EU, only Greece has a higher debt to GDP ratio.

According to PricewaterhouseCoopers (PwC), European banks are sitting on $1.7 trillion in nonperforming loans, which are loans on

which no payments have been made in 90 days. In order to comply with Basel III regulations, European banks will need to increase capital by at least $240 billion to as much as $380 billion, depending on how much each bank restructures its balance sheet assets, according to PwC. A weak economy, bad loans and looming Basel III regulations have led many banks to shrink their balance sheets and lending. The annual change in eurozone loans to nonfinancial corporations has not improved and was still negative in November at -2.3%. In early November, the ECB announced stress tests for 128 systemically important banks that should be completed by the fourth quarter of 2014. The ECB will assume direct supervision over the largest eurozone banks in 2014. With the ECB conducting its stress tests and assuming a more active supervisory role over the largest banks, lending throughout Europe is likely to remain constrained in 2014 and well into 2015. Many banks may choose to write off bad loans before the stress test is completed so they look better, as Deutsche Bank did when it announced a fourth quarter loss of $1.35 billion. As long as credit growth is weak, economic growth is unlikely to exceed 1% in 2014.

There are few instruments left for the ECB to use to spur growth and offset low inflation. The ECB’s refinancing rate was lowered from 0.50% to 0.25% in November. The ECB can lower it further, but another 15 basis points probably won’t make a big difference in spurring bank lending in the EU, or help speed up the structural reforms needed in France or Italy. The ECB can launch another long-term refinancing operation (LTRO) program, but pushing more money into the European banking system is not likely to encourage more lending while banks are undergoing a stress test, economic growth is almost nonexistent and bad loans weigh on bank balance sheets. One step the ECB could take is lowering the value of the euro, which would improve the export competitiveness for every EU member. A cheaper euro would especially help those countries whose productivity has lagged behind Germany. Since a lower value of the euro could increase the cost of imports, like oil, which are priced in dollars, inflation may also rise.

Eurozone

April 2014: Eurozone

In the face of an ongoing contraction in bank lending, weak economic growth and potentially dangerously low inflation, what can the ECB do to boost growth and inflation in coming months when their refinancing rate is already at an all-time low of 0.25%?

In the December 2013 MSR, we suggested the ECB might pursue a lower euro in 2014 to spur growth since their refinancing rate was already low (0.25%) and other policy options were limited. In the February 2014 MSR, we noted that a lower euro would improve the export competiveness of every EU member, especially the southern countries (Italy and Spain) whose productivity has lagged Germany’s over the last decade. A lower euro would increase the cost of imports and contribute to an increase in inflation, which could lessen deflation concerns. After ECB President Mario Draghi stated that the ECB would do “whatever it takes” to stem the sovereign debt crisis on July 24, 2012, the euro has rallied more than 15% versus the dollar.3 The initial rebound in the euro was welcome

and a sign that international confidence in the sustainability of the eurozone was increasing. The strengthening euro was a helpful tailwind, which brought borrowing costs down for the countries most affected by the sovereign debt crisis–Greece, Portugal, Spain and Italy. Lower borrowing costs helped their economies stabilize and narrow budget deficits over the past 18 months. With the eurozone’s economy on the mend, the euro’s strength has shifted from being a tailwind to a headwind. In February, the CPI was up 0.8% versus a 1% increase in core inflation, since the CPI includes energy prices. Both measures of inflation were well below the ECB’s target of 2.0%. The ECB has been concerned that the low rate of inflation makes the eurozone vulnerable to deflation, especially if economic growth faltered. Some of the downward pressure on inflation over the past year has come from a decline in energy prices. However, the strength of the euro has also caused inflation to be lower. At the ECB’s monthly news conference on March 6,

Macro Strategy Review www.forwardinvesting.com11

Mario Draghi said that the strength in the euro since July 2012 had shaved 0.4% off annual inflation. Draghi went on to state, “The strengthening of the euro exchange rate over the past one and a half years has certainly had a significant impact on our low rate of inflation, and, given current levels of inflation, is therefore becoming increasingly relevant in our assessment of price stability.”4 Draghi has consistently argued that the risk of a Japan-style deflation was low. However, on March 6, Draghi acknowledged that the longer inflation in the European monetary block remained low, the higher the risk that deflation would increase. Although the ECB has forecast that inflation will rise to 1.7% in 2016, Draghi’s March 6 comments imply the ECB may not be comfortable with that timetable, since it means that inflation will remain under the ECB’s target of 2% for at least another two years.

Our expectation that the ECB would take steps to lower the euro in 2014 appears on track and seems increasingly likely. We have no idea what actions the ECB might take to reverse the euro’s uptrend or when, but the ECB’s success in bringing down sovereign yields in 2012 may provide a clue. In conjunction with Draghi’s “whatever it takes” statement in July 2012, the ECB announced plans for its Outright Monetary Transactions (OMT) program. Under the OMT program, the ECB would be able to buy sovereign bonds of EU members in the secondary market. There were no limits established on the amount of a country’s outstanding bonds the ECB could buy, as long as that country stuck to the agreed plan for deficit reduction. The ECB didn’t want its OMT program to lessen a country’s commitment to fiscal austerity. Knowing the ECB would step in to backstop any rise in bond yields for EU countries, hedge

funds and international money managers bought sovereign bonds aggressively. Within six months, bond yields had come down dramatically and the ECB didn’t have to spend a dime in achieving their goal. Given this prior success, all the ECB may need is for Draghi to state the desire for a lower euro as well as a willingness from the ECB to sell euros if necessary. Currency traders likely would be happy to accommodate the ECB’s wishes, since they could sell the euro short knowing they were doing so with the blessing of the ECB and with almost zero chance the ECB would intervene. The ECB wouldn’t have to sell a single euro to achieve their goal.

The 50% retracement of the decline from 160.50 in July 2008 to the low in June 2010 at 118.79 is 139.64, and not much above the March 13 high of 137.87.

Eurozone

June 2014: Eurozone

Eurozone GDP grew 0.8% in the first quarter, with Germany and Spain up 3.2% and 1.5%, respectively, while France was flat, Italy was down 0.5%, and GDP in Portugal was off by -2.8%. We do not expect GDP growth in the eurozone to exceed 1% by much in 2014, so the first quarter was in line. Since banks provide 80% of the credit creation in the eurozone, a solid recovery is not likely until lending and credit availability improves. A recent report by the ECB noted that the credit squeeze throughout the eurozone had eased modestly in recent months, but has a long way to go. New bank loans are still only half of their pre-crisis level. Since small- and medium-size businesses represent two-thirds of all jobs, unemployment is not likely to come down quickly in many eurozone countries until credit availability improves materially. The ECB report also noted that 60% of businesses in Greece, 52% in Italy and 43% in Portugal still face a real problem in gaining access to credit. When they can obtain a loan, they are often paying rates two to three times higher than German businesses. The lack of access and cost of credit will make it especially difficult for businesses in Southern Europe to not fall further behind Germany in terms of productivity.

Entering 2014, we expected the ECB to engineer a decline in the value of the euro. As we discussed in the April 2014 MSR, the simplest way for the ECB to lift inflation and further support growth would be to communicate a desire for the euro to decline.

The ECB has estimated that the 15% rise in the euro over the last 18 months has shaved 0.4% off eurozone inflation. Since imported goods will cost more and add to inflation, a weaker euro should alleviate some of the downward pressure on inflation. A weaker euro would also likely make exports from every EU country cheaper for the rest of the world to buy, which would likely lead to an increase in exports and GDP growth. A cheaper euro would especially help Italy, Spain and France, which have higher labor and production costs than Germany. After the ECB’s meeting on May 8, ECB President Mario Draghi stated that the ECB’s governing council is “comfortable with acting next time” and easing policy at their meeting in early June. He also reiterated the connection between the euro and the low rate of inflation. “The strengthening of the exchange rate in the context of low inflation is a cause for serious concern.”5

It appears currency traders have gotten the message since the euro peaked on May 8 at 139.93. As we discussed in April, the 50% retracement of the decline from the July 2008 high of 160.38 to the low in June 2010 at 118.77 was 139.57. The May 8 peak was just 0.46 from a perfect 50% retracement, which technically is significant. During the week of May 9, the euro posted a weekly key reversal when it made a higher high, lower low than the previous week, and closed lower. In fact, the May 9 weekly reversal encompassed the three prior weeks, which adds to its importance.

1.15

1.20

1.25

1.30

1.35

1.40

01/2012

04/2012

07/2012

10/2012

01/2013

04/2013

07/2013

10/2013

01/2014

Euro to U.S. Dollar

Whatever It Takes

Source: Bloomberg, period ending 03/24/14 Past performance does not guarantee future results.

Macro Strategy Review www.forwardinvesting.com12

This is another technical indication that the trend in the euro versus the dollar has turned down. This is one of those times when the fundamentals and the technicals are aligned, which should increase the probabilities that our forecast of a decline in the euro is on

target. As we wrote in the May 2014 MSR, “Shorting the euro has the potential to result in a profitable trade over the next year.” From a risk management point of view, a stop on a short trade should be either just above the May 8 high or pennies below it.

Eurozone

September 2014: Eurozone

After its GDP fell -0.1% in the second quarter, France avoided fulfilling the classic definition of recession (two consecutive quarters of negative GDP) only because GDP was unchanged in the first quarter. The unemployment rate rose to an all-time high of 10.2% in July, and, absent labor market reforms, it is unlikely to improve much in coming quarters. France holds the dubious distinction of having twice as many companies with exactly 49 employees as companies with 50 or more employees. You probably won’t be surprised to learn that the less-than-invisible hand of government regulation is responsible. When a company takes on a 50th employee, it becomes subject to almost three dozen labor laws prescribed by France’s 3,200 page labor code. A 2012 study by the London School of Economics and Political Science showed that the cost of additional rules for companies with 50-plus employees in France added 5% to 10% to labor costs. The study concluded, “There is a strong disincentive to grow.”6

Italy’s GDP fell in the first quarter and the second quarter (by -0.8%), so it is in a recession for the third time in five years. Italy’s debt-to-GDP ratio reached 135.2% in the first quarter and will continue to rise unless GDP growth returns. Like France, Italy has labor market rules that have protected one group of workers over another. In Italy’s case older workers are protected at the expense of younger workers. In an attempt to help young people get jobs in the 1980s and 1990s, Italy encouraged short-term

labor contracts, which made it easier for companies to hire and fire employees. In 1998, 20% of workers younger than 25 were temporary workers, compared to more than 50% now, according to Eurostat. A 2013 Bank of Italy study found that entry level wages for young workers under temporary contracts fell almost 30% between 1990 and 2010. This created a large income gap between older workers, whose jobs and incomes are protected by labor laws, and young workers. The temporary contracts allowed young workers to be let go when the financial crisis struck, so young workers were disproportionately affected. According to Eurostat, since 2007 the employment rate for those under 40 has fallen 9%, while it rose 9% for workers between 55 and 64 years old. In June, the unemployment rate for workers under 25 rose to a record of 43.7%. Unless Italy changes its labor laws, a whole generation of young workers will clearly have a lower standard of living than their parents.

The conundrum facing Mario Draghi and the ECB is that proactive monetary policy can alleviate some of the pressure on countries like France and Italy to make the structural changes needed to improve economic growth over the long term. In the short term, weak economic growth and low inflation will win out over doing nothing, which is why the ECB is likely to implement quantitative easing before year-end.

Eurozone

October 2014: The Return of the Almighty Dollar and Deflation

Since 2010, a vocal chorus has proclaimed that hyperinflation and a crash in the dollar was right around the corner once the Fed became a serial advocate of quantitative easing in the wake of the financial crisis. Since 2008, the Fed has expanded its balance

sheet from $900 billion to more than $4.2 trillion in 2014. Although neither a crash in the dollar or hyperinflation has reared its ugly head, it hasn’t diminished warnings from proponents like Peter Shrill (fictitious name), who in a recent CNBC interview reassured

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

2007

2008

2009

2010

2011

2012

2013

2014

Eurozone Unemployment Rate

Source: Bloomberg, period ending 03/31/14

1.15

1.20

1.25

1.30

1.35

1.40

01/2012

05/2012

09/2012

01/2013

05/2013

09/2013

01/2014

05/2014

Euro to USD

Source: Bloomberg, period ending 05/23/14

Whatever it takes

Key Weekly Reversal

Macro Strategy Review www.forwardinvesting.com13

viewers that the plagues of hyperinflation and the dollar’s demise are still on their way. He’s just been a bit early. As we have discussed previously, there are a number of reasons why hyperinflation and a collapse in the dollar has not happened and likely won’t for some time. A stronger dollar is usually bearish for commodities and increases the deflationary threat from excessive debt.

The classic definition of inflation is too much money chasing too few goods. Although the Fed has greatly expanded its balance sheet since 2008, most of the money has not made its way into the economy. Free reserves held at the Federal Reserve by U.S. banks totaled $2.71 trillion as of September 19, 2014. One of the reasons the current recovery has been mediocre is because there is too little demand, not just in the United States, but globally. Capacity utilization rates around the world are low, which has kept business investment weak and inflation rates low. The U.S. Federal Reserve, ECB and Bank of Japan have been far more concerned about deflation and have strenuously tried to revive inflation with the greatest amount of monetary accommodation ever attempted. Most of the money created by central banks though is not coursing through domestic economies but sitting dormant. Although bank lending has modestly picked up in the U.S., it is still contracting in Europe, with banks more focused on strengthening their balance sheets than lending into a weak economy.

The velocity of money measures how fast each dollar of M2 money supply is turning over. When consumers and businesses are confident, the turnover of M2 rises as consumers spend more and business investment increases. The increase in velocity results in faster GDP growth and fosters a virtuous cycle of better job creation, business investment, wage growth and more bank lending. When they are cautious, consumers spend less, businesses hold back on new investments, banks reduce lending and GDP growth slows. As you can see, the velocity of money is at its lowest rate in more than 50 years and has continued to slow precipitously irrespective of the increase in the Fed’s balance sheet. This is another reason why GDP growth has remained stalled around 2.5% during the last three years despite the efforts of the Fed. Those forecasting hyperinflation and a dollar crash are likely going to need even more patience.

On February 18, 2001, Treasury Secretary Paul O’Neill said, “We are not pursuing, as often said, a policy of a strong dollar. In my opinion, a strong dollar is the result of a strong economy.”7 With

his comments, O’Neill appeared to distance himself and the Bush administration from Robert Rubin’s insistence when he was treasury secretary in the Clinton administration that a strong dollar was in the best interest of the United States. The dollar index topped out five months later in July 2001 at 121.29 and then declined in earnest in 2002. When the Bush administration failed to offer even token support, currency traders shorted the dollar with impunity. The dollar lost 42% of its value between July 2001 and March 2008, when it bottomed at 70.69. As the financial crisis erupted in the fall of 2008, international investors poured money into the dollar as a safe haven, and by March 2009 it had risen 27%. As the stock market recovered and financial market volatility calmed down, the dollar entered a broad trading range during 2009, 2010 and 2011, fluctuating between 73.00 and 89.00.

As discussed in the April 2014 MSR, we thought the dollar was on the cusp of a solid rally after trading in a very narrow range in 2012 and 2013: “The euro represents 57.6% of the dollar index, so a decline of 7.5% to 9.2% in the euro versus the dollar would add 4.3-5.3% to the dollar index. With the dollar index trading near 80.00, the decline in the euro would add 3.4-4.2 points to the dollar index, and easily enable the dollar to trade above near-term resistance at 81.30. Once above 81.30, the next level of resistance is 84.30 to 84.50, the highs in May and July last year.” In the May 2014 MSR, just days before the peak in the euro, we wrote, “Shorting the euro has the potential to result in a profitable trade over the next year.” On September 19, the dollar index traded as high as 84.78 and the euro fell to €128.30. In the September 2014 MSR our downside target for the euro was €128.25-128.75. The dollar and euro have reached our targets, and the dollar is overbought while the euro is quite oversold. This suggests that the potential for a two or three month rebound in the euro is probable, which should usher in a modest decline and consolidation of the recent gains in the dollar. This respite from dollar strength could allow commodities like oil and gold, which have been trending down and are also oversold, to experience oversold technical rallies. Although a bounce in the euro and pullback in the dollar is overdue, the long-term technical trends seem clear.

Between July 2001 and March 2008, the dollar index fell 50.6 points from 121.29 to 70.69. Using a common Fibonacci ratio to measure the rebound from a large decline, a 38.2% retracement of this decline would be 19.33 points, which targets a rally to 90.02. This target is just above the highs of 89.25 in November 2008, 89.71

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

1959

1964

1969

1974

1979

1984

1989

1994

1999

2004

2009

2014

Velocity of M2 Money Stock (Seasonally Adjusted)

Source: Federal Reserve Bank of St. Louis, period ending 04/01/14

65

75

85

95

105

115

125

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

U.S. Dollar Index Spot Rate

Source: Bloomberg, period ending 09/19/14 Past performance does not guarantee future results.

Macro Strategy Review www.forwardinvesting.com14

in March 2009 and 88.80 in June 2010, so we expect the index to hit within the price range of 88.80 to 90.00 in coming months. Should the dollar index reach this range as we expect, the odds of it breaking out above the range are good. The dollar has already tested this zone three times, so a breakout after a fourth attempt is very probable. A 50% retracement of the dollar’s 50.6 point plunge from 2002 to 2008 would create a target of 95.99 while a 61.8% rebound (another common Fibonacci rebound from a large decline) would suggest a possible high of 101.97. We think the higher target more likely as after breaking through serious resistance at 89.00-90.00, a rally to just 95.99 seems too small, whereas a pop to 100.00-101.97 would be a more appropriate follow through. Finally, if we are correct about the eurozone’s extended economic malaise, the euro will decline significantly from current levels.

The euro almost doubled from its low of €82.30 in October 2000 to its high in July 2008 of €160.08, an increase of €77.78. A 50% retracement of this huge rally would have been achieved with a decline to €121.19. The euro bottomed at €118.70 in June 2010 and again at €120.00 in July 2012. The overshoot of the €121.19 target is understandable since Greece was imploding in June 2010 and concerns whether the European Union would hold together were rampant in July 2012, prior to ECB President Mario Draghi’s “whatever it takes” comment. Since the July 2008 top, each euro rally has made a lower high, which is a sign of longer term diminishing strength. The lows in 2010 and 2012 near €120.00 will likely be retested, and probably result in a decent short covering rally. We suspect this short covering rally will not represent “the pause that refreshes,” but rather a failing dead cat bounce, which will set up an unsettling plunge well below €120.00. A decline of 40

points from the high of €139.93 in May would be consistent with the 40 point fall from €160.00 to €120.00, so we see €100.00 as one possible target.

A decline from the September 19 close of €128.52 to €100.00 would represent a 22.2% decline. Since the euro represents 57.6% of the dollar index, the dollar would receive a boost of 12.8% from the euro’s decline, lifting the dollar to 95.58 from its September 19 close of 84.73. Since we expect additional weakness in the Japanese yen and a number of emerging market currencies, it is easy to see how the dollar index could reach 100.00-101.97 over the next nine to 18 months. Although these targets for the euro and dollar indices may seem a bit extreme, the fundamentals and chart analysis are aligned, which raises our confidence.

Eurozone

December 2014: Deflation Battle Becoming Currency War

In the 1930s as the growth of the global economic pie slowed and contracted, trade barriers and tariffs to protect domestic producers and jobs were enacted, unfortunately led by the United States. On June 17, 1930, the Smoot-Hawley Tariff Act was passed and raised tariffs on over 20,000 imported goods to the highest level in more than a century. European countries didn’t appreciate America’s “Beggar-Thy-Neighbor” trade policy and responded with retaliatory tariffs of their own. Between 1929 and 1934, U.S. exports plunged 70% and imports from Europe into the U.S. sank 66%. World trade collapsed 66% between 1929 and 1934. Although trade barriers were a consequence of the Depression and not a cause, they certainly contributed to its depth, longevity and greatness. No doubt the authors of the Smoot-Hawley Tariff Act and their European counterparts felt a degree of pride that their trade protections were so successful back then. However, history has judged their actions far more harshly, and the lesson learned is that protectionism is bad economic policy for everyone involved. Unfortunately, desperate men do desperate things and decades of bad policy has led policymakers in Japan and Europe to engage in a modern day form of protectionism.

As we discussed in the June 2013 MSR section entitled “Japan – Winning in a Zero-Sum Growth World,” there isn’t much difference

between a country that cheapens its currency by 20-25% and a country that slaps import tariffs of 20-25% on products from competing countries. In one way, currency devaluation is worse since it affects every good or service offered by a competing country rather than targeted products like the tariffs of the 1930s. The Keynesian tools of fiscal and monetary policy that policymakers have relied on since World War II to end every recession and foster economic growth have failed in Japan and Europe. This is due in part to problems beyond the scope of monetary or fiscal policy. Political leaders have had many years to address their internal structural problems but have lacked the leadership skills and courage to make necessary changes. Ironically, labor laws erected to “protect” some workers at the expense of other workers within Japan and many EU countries are a form of internal protectionism. Labor market inertia has led to slower economic growth that has persisted despite unprecedented monetary and fiscal stimulus. Given the political realities in these countries, central bankers have opted for currency devaluation in a desperate attempt to rescue their economies at the expense of global trade. While equity markets cheer central bankers, it appears to us that we’re on a slippery road to perdition.

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Euro to U.S. Dollar

Source: Bloomberg, period ending 09/19/14 Past performance does not guarantee future results.

Macro Strategy Review www.forwardinvesting.com15

Eurozone

December 2014: Currency War Beneficiary: The U.S. Dollar

When asked to explain the dollar’s strength, most strategists point to better U.S. growth compared to Europe and Japan as the primary reason. This has led strategists to conclude that the U.S. economy is strong enough to “go it alone.” This analysis, however, overlooks a couple of salient points. In a global economy there is no such thing as one economy decoupling from the rest of the world. Economic growth in the U.S. has been outpacing the recession-plagued European Union and Japan for years. The trigger for the dollar’s rally was not U.S. growth but Draghi’s strong hints that the ECB wanted the euro to decline in March and April. This led to a reversal in the euro’s uptrend in early May and its subsequent fall from 139.93 to below 124.00 on November 21. In the first estimate of third quarter GDP, the Department of Commerce reported that U.S. GDP expanded by 3.5% with trade representing more than 1% of the total. The 12% rally in the dollar is likely to exert downward pressure on exports in coming quarters, which will lower its contribution to GDP growth. This drag will be mostly offset by the decline in energy prices that are causing consumers’ disposable income to increase. As some of this newfound wealth is spent, it will help support the economy, especially in the short run. The dark side

of lower energy prices won’t materialize for some time, unless oil drops to $60 a barrel.

Eurozone

April 2015: Euro – Technical

In the May 2014 MSR we suggested the following: “Shorting the euro has potential to result in a profitable trade over the next year.” At that time, the euro was trading near 1.380 and almost no one was talking about the coming decline in the euro that we expected. As the decline in the euro accelerated after the ECB commenced with its QE program on March 9, 2015, a number of forecasts surfaced projecting a decline in the euro to 0.820 or 0.850. It has been our experience that when extreme forecasts are made after something has either rallied or declined by a large percentage, it is time to expect a counter-trend move. The Fed’s dovish outlook for the U.S. economy initiated a surge of short covering in the euro, which had become a very overcrowded trade. In coming months, the euro has the potential to rally to 1.12–1.14 before the longer-term downtrend resumes. Additional short covering may be spurred by economic reports reflecting improvement in the eurozone. From a money management perspective, we think it reasonable to cover a portion of the short position we suggested last May if the euro drops under 1.065. As we noted in the March 2015 MSR, Germany is likely to benefit disproportionately from any improvement since it is the most productive economy in the eurozone; it generates 50% of its GDP from exports, so the decline

in the euro would prove a boon. Longer term, we expect the euro to decline after any bounce since wealthy Europeans will want to protect their purchasing power by moving assets out of the euro and into other currencies like the dollar.

Eurozone

May 2015: Eurozone

Charles Plosser, president of the Federal Reserve Bank of Philadelphia, said in an interview with the New York Times in early February, “If monetary policy…is distorting what might be normal market outcomes…” In the March 2015 MSR we wrote that

we found this statement to be exceedingly disingenuous as the purpose of the Fed’s monetary policy since the financial crisis has been the intentional manipulation of Treasury yields and inflating the wealth effect of the stock market. It would be fair to say that

65.0

75.0

85.0

95.0

105.0

115.0

125.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

The U.S. Dollar Index Spot Rate

Source: Bloomberg, period ending 11/21/14 Past performance does not guarantee future results.

Euro Reversal

65.0

75.0

85.0

95.0

105.0

115.0

125.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

U.S. Dollar Index Spot Rate

Source: Bloomberg, period ending 03/20/15 Past performance does not guarantee future results.

Euro Reversal

Macro Strategy Review www.forwardinvesting.com16

the ECB has taken the distortion of market outcomes to a new level through its QE program launched on March 9. As of April 22, more than half of eurozone government bonds have negative yields, according to Bank of America Merrill Lynch. In other words, investors that purchase a seven-year German bund will pay the German government 0.07% a year for the privilege, or they will pay the government of Spain 0.116% for owning a one-year Spanish bond.

Negative interest rates are forcing banks throughout Europe to rebuild computer programs, update legal documents and reconstruct spreadsheets to account for negative rates. The Euro Interbank Offered Rate, or Euribor, is the base interest rate used for many banks loans in Spain, Italy and Portugal. More than 90% of the 2.3 million mortgages outstanding in Portugal have variable rates linked to Euribor. Portugal’s central bank recently ruled that banks would have to pay interest on existing loans if Euribor or any additional spread falls below zero percent. Spanish-based Bankinter has been forced to pay some customers interest on mortgages by deducting that amount from the principal the borrower owes.

While the unusual effects of the ECB’s QE program are making headlines for distorting normal market outcomes, the improving health of the banking system in Europe may provide the bigger economic punch. The ECB’s second quarter survey of bank lending showed that the net percentage of banks expecting a rise in loan demand reached 39%, up from 17% in the first quarter. Banks

expect a small net easing of their credit standards to businesses during the second quarter but a further tightening of their credit standards for mortgages. Since banks provide more than 70% of credit creation in the eurozone (compared to 35% in the U.S.), the improvement in lending in coming months will put more money to work in the real economy, which should lift GDP growth to 1.5% or so in 2015. Not great, but certainly better than the 0.9% increase in 2014 and contraction in 2012 and 2013. In our opinion, the coming improvement in bank lending is more important than the ECB’s QE program.

Eurozone

May 2015: Euro – Technical

In the May 2014 MSR, when the euro was trading above 1.380, we suggested shorting the euro. In the April 2015 MSR, we said that from a money management perspective, it seemed reasonable to cover a portion of that short position if the euro dropped under 1.065, and on April 13 and 14 the euro did trade under 1.065. As this is being written on April 24, the euro is trading at 1.086. We expect the euro to rally to 1.110–1.150 in coming months as the timing of the first Fed rate increase is pushed back and better economic news from the eurozone spurs some short covering by the legion of traders expecting the euro and the dollar to reach parity. In recent weeks the euro has been under pressure by another episode in the ongoing Greece drama/comedy. The fact that the euro has not made a new low despite the headlines suggests any “resolution” could ignite a new wave of short covering.

Emerging MarketsFebruary 2014: Emerging Economies

We discussed the economic fundamentals of China, Brazil, India and

Indonesia in detail in the November 2013 MSR, and concluded that

these emerging economies were unlikely to return to prior growth

rates in 2014 and beyond. We noted that China, Brazil, India and