macro china economics - scoopimg.scoop.co.nz/media/pdfs/1412/hsbc_research_china_inside_out... · 2...

TRANSCRIPT

With disinflationary pressure rising, we

lower our GDP and inflation forecasts for 2015 and 2016

Beijing will likely step up policy easing to stabilise the economy

We also expect the pace of key reforms to accelerate

Both economic activity and inflation data have been weaker

than we anticipated in recent months, suggesting rising

disinflationary pressures. We lower our GDP growth forecast to

7.3% for 2015 (from 7.7%) and to 7.4% for 2016 (from 7.6%).

We have also cut our CPI forecasts to 1.8% and 1.9%

(from 2.9% and 2.7%). Despite these revisions, we remain more

constructive than consensus GDP growth of 7% for 2015 and

6.7% for 2016 and consensus CPI of 2.3% and 2.5%. In this

report, we identify five key macro themes for 2015.

Disinflationary pressures are likely to prompt more

aggressive easing. Inflation is likely to stay below 2% in

2015, due to weak demand, spare capacity, and falling

commodity prices. We expect more aggressive monetary and

fiscal easing and forecast another two 25bps of symmetric

rate cuts and three 50bps of reserve ratio cuts in 2015 versus

our previous expectation of no change.

Infrastructure investment should remain strong. A long

project pipeline is likely to sustain infrastructure investment

in 2015, offsetting the slowdown in property investment.

We expect further progress in the New Silk Road plan.

The economic impact of a cooling property market.

The property slowdown will likely continue in 2015,

but recent easing measures provide some support, and the

economic impact remains manageable.

Faster reforms. We expect Beijing to accelerate fiscal,

state-owned enterprise (SOE) and price reforms.

No big devaluation, but further measures to increase

RMB capital account convertibility. We expect further

steps to deregulate cross-border portfolio investment and

promote RMB internationalisation.

Macro China Economics

China Inside Out

Five macro themes for 2015

16 December 2014 Qu Hongbin Chief Economist, Greater China The Hongkong and Shanghai Banking Corporation Limited +852 2822 2025 [email protected]

Julia Wang Economist The Hongkong and Shanghai Banking Corporation Limited +852 3604 3663 [email protected]

Jing Li Economist The Hongkong and Shanghai Banking Corporation Limited +86 10 5999 8240 [email protected]

View HSBC Global Research at: http://www.research.hsbc.com

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

Disclaimer & Disclosures This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

2

Macro China Economics 16 December 2014

abc

Five macro trends 3

Charts 15 GDP 16

Industrial production 18

Private consumption 20

Fixed investment 22

Trade 24

Prices 26

Commodity prices 28

Money and credit growth 30

Interest and exchange rates 32

Employment and income 34

Asset markets 36

Data and forecasts 39

Disclosure appendix 42

Disclaimer 43

Contents

3

Macro China Economics 16 December 2014

abc

1. Disinflationary pressure: expect more aggressive easing

A reflection of weak demand

Inflation has been decelerating sharply since late

2011, with all measures now at a multi-year low

(Chart 1). The Consumer Price Index (CPI) has

fallen from an average of 4% in 2010-11 to 1.4%

in November 2014; the Producer Price Index

(PPI) has been contracting for 33 months; the

deflator is the weakest since quarterly data began

in 2000 (on a year-to-date basis).

We think this disinflation, which is not new, is

mostly a reflection of weak demand. The fall in

inflation is also consistent with weakness in the

labour market, as suggested by the Purchasing

Managers Index (PMI), that also points to low

capacity utilisation (Chart 2), which is widely

corroborated by industry-level data.

Moreover, the trend in inflation has followed the

slowdown in growth fairly steadily (Chart 3).

As the economic cycle typically leads the inflation

cycle, we think the slowdown in inflation since

late 2011 is to a large degree due to the lower

growth rate since mid-2010. Taking core inflation

as a proxy for underlying demand, this points to

weaker headline inflation in 2015.

More disinflation in 2015

On the back of the continued property market

slump (more on this later) and signs of weaker

industrial activity, we lower our 2015 GDP

Five macro trends

With disinflationary pressure rising, we lower our GDP and

inflation forecasts for 2015 and 2016

Beijing will likely step up policy easing to stabilise the economy

We also expect the pace of key reforms to accelerate

Chart 1. Inflation at multi-year low Chart 2. A reflection of weak demand …

Source: CEIC, HSBC Source: Markit, HSBC

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14-10

-5

0

5

10

15

-10

-5

0

5

10

15%%

PPI CPI Official implied deflator

40

45

50

55

60

40

45

50

55

60

04 06 08 10 12 14

HSBC China manufacturing PMI - Capacity UtilizationLong term average

4

Macro China Economics 16 December 2014

abc

growth forecast to 7.3% from 7.7%. We also trim

our 2016 GDP number to 7.4% from 7.6%.

A slower growth trajectory leads us to lower our

inflation forecast to 1.8% and 1.9% for 2015 and

2016, from 2.9% and 2.7%, respectively (Table 1).

While weak demand is likely the primary driver

of disinflation, supply side shocks may have also

exacerbated the downward pressures on prices.

Commodity prices, and the oil in particular, have

fallen quite sharply in 2H 2014. The transmitted

impact to headline CPI is quite small, given that

fuel price is a very small portion of the CPI basket

and the onshore oil price is still regulated and

tends to fluctuate much less than the market price

(Chart 4). However, historical patterns suggest

lower oil prices will put some pressure on the

CPI. Meanwhile, import prices have fallen sharply

and will likely weigh on the PPI.

Apart from oil prices, slower property price

growth is another potential downside risk for the

CPI. As shown in Chart 5, historically the

residence component of the CPI basket (roughly

17%) is significantly less volatile than property

prices. However, given there is a rent component

in the residence index, it does tend to follow

house prices (sometimes with a lag). The

correction in property prices has not been

particularly severe this year. However, given

lacklustre sales, we do not expect much upside

pressures on prices in 2015.

A final factor which has historically been a driver

of the CPI is the price of pork. Food is roughly one

third of the CPI basket, and pork has in the past

been a driver of the food inflation cycle. However,

both pork and food inflation remain relatively

subdued (Chart 6). Barring unanticipated supply

side shocks, the pork price is unlikely to swing

headline CPI.

Selective as well as across-the-board easing

We think intensifying disinflationary pressures will

prompt more aggressive easing by policymakers

(see China: From selective to across-the-board

easing, 21 November 2014). The People’s Bank

of China (PBoC) delivered a bigger than expected

cut to the lending rate (40bp) on 21 November.

Chart 3. …and low capacity utilization Chart 4. Oil prices will weigh somewhat on inflation

Source: CEIC, HSBC Source: CEIC, HSBC

Table 1. Forecast revision

Q1 15 Q2 15 Q3 15 Q4 15 2014 2015 2016

GDP, %, y-o-y 7.4 (7.8) 7.2 (7.8) 7.3 (7.6) 7.3 (7.7) 7.5 7.3 (7.7) 7.4 (7.6) GDP, %, q-o-q 1.6 (1.8) 1.8 (1.8) 1.9 (1.9) 1.7 (1.9) CPI, %, y-o-y 1.5 (2.8) 1.7 (2.9) 1.8 (2.7) 2.1 (3.0) 2.4 1.8 (2.9) 1.9 (2.7)

Source: HSBC estimates

-2

0

2

4

6

-5

0

5

10

15

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

% YoY% YoY

GDP growth CPI core inflation

-100

-50

0

50

100

150

-10

-5

0

5

10

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

% YoY% YoY

PPI (LHS) Oil price (mkt)No.97 Oil import price

5

Macro China Economics 16 December 2014

abc

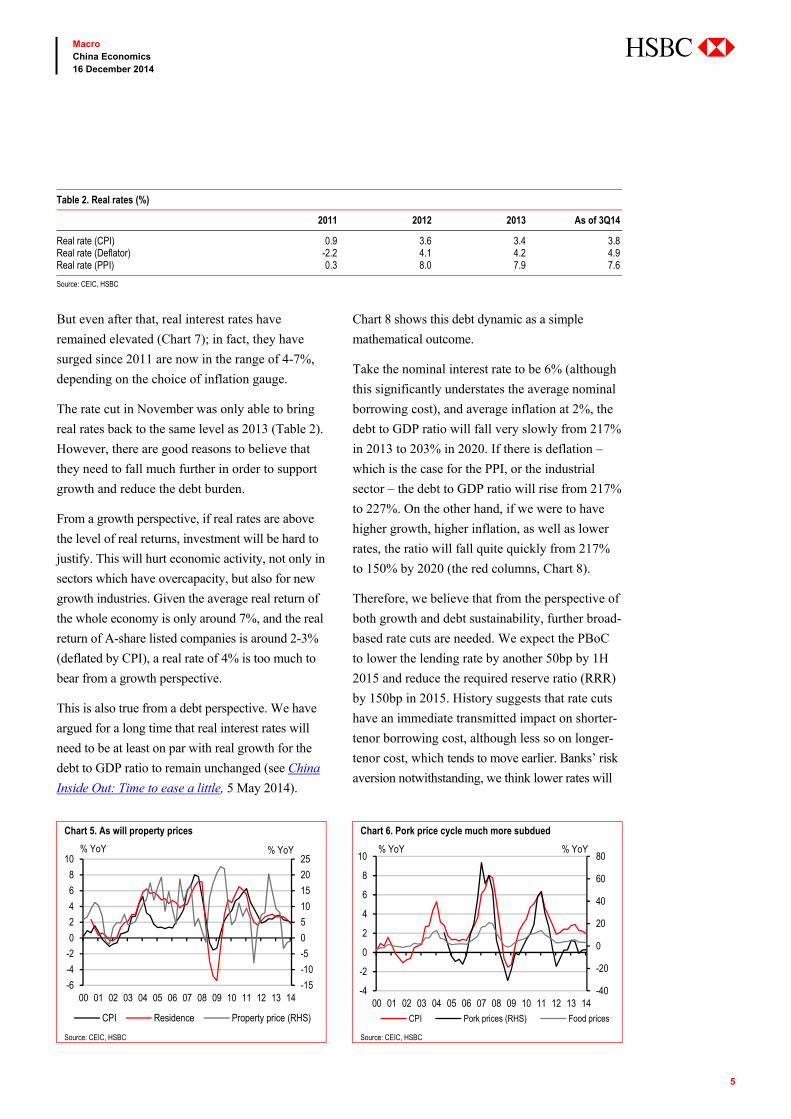

But even after that, real interest rates have

remained elevated (Chart 7); in fact, they have

surged since 2011 are now in the range of 4-7%,

depending on the choice of inflation gauge.

The rate cut in November was only able to bring

real rates back to the same level as 2013 (Table 2).

However, there are good reasons to believe that

they need to fall much further in order to support

growth and reduce the debt burden.

From a growth perspective, if real rates are above

the level of real returns, investment will be hard to

justify. This will hurt economic activity, not only in

sectors which have overcapacity, but also for new

growth industries. Given the average real return of

the whole economy is only around 7%, and the real

return of A-share listed companies is around 2-3%

(deflated by CPI), a real rate of 4% is too much to

bear from a growth perspective.

This is also true from a debt perspective. We have

argued for a long time that real interest rates will

need to be at least on par with real growth for the

debt to GDP ratio to remain unchanged (see China

Inside Out: Time to ease a little, 5 May 2014).

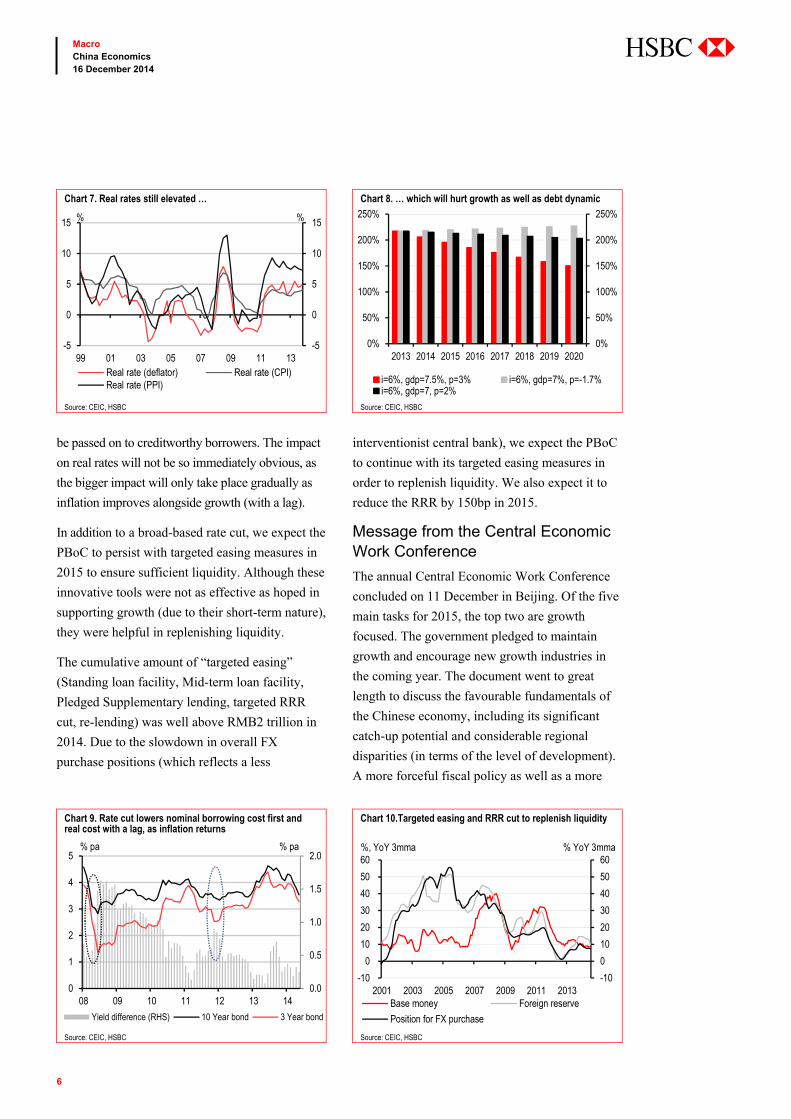

Chart 8 shows this debt dynamic as a simple

mathematical outcome.

Take the nominal interest rate to be 6% (although

this significantly understates the average nominal

borrowing cost), and average inflation at 2%, the

debt to GDP ratio will fall very slowly from 217%

in 2013 to 203% in 2020. If there is deflation –

which is the case for the PPI, or the industrial

sector – the debt to GDP ratio will rise from 217%

to 227%. On the other hand, if we were to have

higher growth, higher inflation, as well as lower

rates, the ratio will fall quite quickly from 217%

to 150% by 2020 (the red columns, Chart 8).

Therefore, we believe that from the perspective of

both growth and debt sustainability, further broad-

based rate cuts are needed. We expect the PBoC

to lower the lending rate by another 50bp by 1H

2015 and reduce the required reserve ratio (RRR)

by 150bp in 2015. History suggests that rate cuts

have an immediate transmitted impact on shorter-

tenor borrowing cost, although less so on longer-

tenor cost, which tends to move earlier. Banks’ risk

aversion notwithstanding, we think lower rates will

Chart 5. As will property prices Chart 6. Pork price cycle much more subdued

Source: CEIC, HSBC Source: CEIC, HSBC

Table 2. Real rates (%)

2011 2012 2013 As of 3Q14

Real rate (CPI) 0.9 3.6 3.4 3.8 Real rate (Deflator) -2.2 4.1 4.2 4.9 Real rate (PPI) 0.3 8.0 7.9 7.6

Source: CEIC, HSBC

-15

-10

-5

0

5

10

15

20

25

-6

-4

-2

0

2

4

6

8

10

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

% YoY% YoY

CPI Residence Property price (RHS)

-40

-20

0

20

40

60

80

-4

-2

0

2

4

6

8

10

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

% YoY% YoY

CPI Pork prices (RHS) Food prices

6

Macro China Economics 16 December 2014

abc

be passed on to creditworthy borrowers. The impact

on real rates will not be so immediately obvious, as

the bigger impact will only take place gradually as

inflation improves alongside growth (with a lag).

In addition to a broad-based rate cut, we expect the

PBoC to persist with targeted easing measures in

2015 to ensure sufficient liquidity. Although these

innovative tools were not as effective as hoped in

supporting growth (due to their short-term nature),

they were helpful in replenishing liquidity.

The cumulative amount of “targeted easing”

(Standing loan facility, Mid-term loan facility,

Pledged Supplementary lending, targeted RRR

cut, re-lending) was well above RMB2 trillion in

2014. Due to the slowdown in overall FX

purchase positions (which reflects a less

interventionist central bank), we expect the PBoC

to continue with its targeted easing measures in

order to replenish liquidity. We also expect it to

reduce the RRR by 150bp in 2015.

Message from the Central Economic Work Conference

The annual Central Economic Work Conference

concluded on 11 December in Beijing. Of the five

main tasks for 2015, the top two are growth

focused. The government pledged to maintain

growth and encourage new growth industries in

the coming year. The document went to great

length to discuss the favourable fundamentals of

the Chinese economy, including its significant

catch-up potential and considerable regional

disparities (in terms of the level of development).

A more forceful fiscal policy as well as a more

Chart 7. Real rates still elevated … Chart 8. … which will hurt growth as well as debt dynamic

Source: CEIC, HSBC Source: CEIC, HSBC

Chart 9. Rate cut lowers nominal borrowing cost first and real cost with a lag, as inflation returns

Chart 10.Targeted easing and RRR cut to replenish liquidity

Source: CEIC, HSBC Source: CEIC, HSBC

-5

0

5

10

15

-5

0

5

10

15

99 01 03 05 07 09 11 13

%%

Real rate (deflator) Real rate (CPI)Real rate (PPI)

0%

50%

100%

150%

200%

250%

0%

50%

100%

150%

200%

250%

2013 2014 2015 2016 2017 2018 2019 2020

i=6%, gdp=7.5%, p=3% i=6%, gdp=7%, p=-1.7%i=6%, gdp=7, p=2%

0.0

0.5

1.0

1.5

2.0

0

1

2

3

4

5

08 09 10 11 12 13 14

% pa% pa

Yield difference (RHS) 10 Year bond 3 Year bond

-10

0

10

20

30

40

50

60

-10

0

10

20

30

40

50

60

2001 2003 2005 2007 2009 2011 2013

% YoY 3mma%, YoY 3mma

Base money Foreign reserve

Position for FX purchase

7

Macro China Economics 16 December 2014

abc

flexible monetary policy will be deployed in

2015. We believe this likely means a bigger fiscal

deficit target (around -2.5% of GDP from -2.1%

GDP in 2014.

Even if the authorities set a more conservative

growth target for 2015, in the range of 7.0% to

7.5%, we believe they will do more to counter the

growth and inflation slowdown (see China:

Central Economic Work Conference: stabilising

growth, accelerating reforms, 11 December).

In addition, the authorities also pledged to

accelerate reforms in 2015. We can expect more

progress on cutting red tape, SOE reforms and

RMB convertibility.

2. Infrastructure investment to stay robust A long project pipeline in 2015

Apart from monetary easing, another key

growth driver in 2015 is likely to be

infrastructure investment.

Chart 11 shows a breakdown of fixed asset

investment (FAI) by type. Traditionally,

manufacturing investment is around 30% of all

FAI, property about 19% and infrastructure 22%.

Overall FAI has slowed from 20% in 2013 to

15%, as of October 2014. The sharpest slowdown

is in property investment, which fell from 19% to

12% over the same period. As the property market

started correcting this year, we calculated that a

10% correction in sales, if sustained for a period of

12 months, could shave 1ppt off GDP. Most of that

negative impact would come from the growth side.

Manufacturing investment also moderated from

18% to 13%. The heavy industrial sector is

struggling with overcapacity and the light

manufacturing sector is experiencing weaker

external demand as well as a tighter credit

environment. Only infrastructure investment

remained robust in 2014, growing 21% y-o-y,

and this will likely remain the case in 2015.

Since early 2014, the National Development and

Reform Commission (NDRC), the main planning

agency, has sped up project approvals and has

already approved nearly RMB1 trillion worth of

infrastructure investment. Although some work

has started in 2014, most will likely commence in

early 2015, supporting infrastructure investment

growth in 2015 and 2016 (see Table 3).

Another are where we can expect to see further

initiatives in 2015 is the New Silk Road plan.

China has pledged USD40bn to improve transport

connections in the New Silk Road economic zone,

which comprises the China-Mongolia-Russia

economic belt, China-South Asia-West Asia

economic belt, Europe China continental bridge

and a maritime route that links China with

counties through the Pacific and Indian Ocean

Chart 11. Infrastructure investment to remain strong Chart 12. Capital stock per worker

Source: CEIC, HSBC Source: Penn World tables, HSBC

-10

0

10

20

30

40

50

60

05 06 07 08 09 10 11 12 13 14-10

0

10

20

30

40

50

60% YoY, 3mma% YoY, 3mma

Total FAI PropertyManufacturing Infrastructure

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

China US Japan Korea Spain Malaysia

Capital stock per worker, USD thousand, 2005 price

1990 2011

8

Macro China Economics 16 December 2014

abc

(see Xi’s New Silk Road Plan: China further

increases funding for overseas infrastructure

investment, 18 November 2014). As a result of

this plan, we expect the nine provinces along the

new Silk Road to benefit from increased

infrastructure investment funding in 2015.

According to the preliminary blueprint,

the economic belt has three elements – the

transport system that links Asia and Europe,

natural gas pipelines connecting central Asia and

China and international highway projects.

As for the familiar question of whether China

needs these projects, let us turn to Chart 12, which

should be familiar to our regular readers. The chart

shows that the capital stock per worker is still only

20% of the level in the US and Japan, and 25% of

the level in Korea. On a fundamental basis,

China’s investment resource per worker is still very

much behind the developed economies. Based on a

national average, China is still in great need of urban

infrastructure, including public transport, 3G and 4G

networks, paved roads and social housing. Although

the east coast is already fairly affluent and built out,

the western part of the country is much less

developed. The west is where most of the approved

infrastructure projects (as well as those for the New

Silk Road) will be rolled out.

Transition to a more sustainable financing method

Despite favourable fundamentals, waste has

occurred, particularly in infrastructure investment.

This is a result of easy access to funding – partly

due to the prioritisation of production over returns –

and the perceived implicit central government

guarantee. Local government debt has expanded to

RMB20 trillion as of end 2013. Most of these

liabilities are short term with relatively higher

borrowing costs, whereas the underlying projects

will not be completed by the time the debt is due,

and profitability is likely to be low too. In addition,

a lot of debt has been raised on the bond market

through Local Government Financing Vehicles

(LGFVs) and this was not fully included in the

initial estimate.

The lack of transparency, the relatively high yield

and the duration mismatch have caused concerns

that this method of financing is unsustainable and

detrimental to financial stability (see China Inside

Out: Local debt: Three options, 1 August 2011).

In 2014, regulators have taken some significant steps

to resolve this issue. Both the NDRC and the State

Council have issued rules which restrict the ability of

highly leveraged local governments to raise

additional debt. More disclosure on fund usage and

payback calculations was also enforced. As a result,

local governments with poorer funding abilities have

had to reduce their borrowing.

In September, the State Council issued a directive

which we believe signals the end of LGFVs as a

source of funding (see China: State Council issues

directive on local debt, 3 October, 2014).

Specifically, although roll-overs are allowed,

LGFV bonds will no longer be recognised as

government liabilities from 2016 onwards.

At the same time, the central government has

ordered a fresh national audit (the last one was at

the end of 2013) which will recalculate and

classify the existing stock of local government

liabilities (including the previously off-balance

sheet LGFV debt) to determine the portion that

the government will be liable for. This has led to

wider credit spreads and greater risk

differentiation. Also, the onshore clearing house

has in recent days tightened the rules on repo

collateral, which effectively rules out most LGFV

bonds. This has led to a wave of unwinding as

banks will move to permanently reduce their

holdings for such bonds in 2015.

9

Macro China Economics 16 December 2014

abc

After the year-end national audit, the government

will move to consolidate the recognised liabilities in

the official fiscal budget. Expenditure is expected

to be tied to income streams according to the terms

of its payback period. From 2015 onwards,

incremental debt issuance will be subject to

stronger monitoring by the central government.

In 2015, we expect infrastructure financing to

come from two main channels, in addition existing

commitments made by banks:

We expect the fiscal deficit to rise from around -

2.1% of GDP to around -2.5%. This will help

accommodate the additional interest payments

as well as provide seed capital for new projects.

Second, we expect the quota for municipal

bonds to rise from RMB400bn this year.

The new figure will be set subject to the

repayment ability of each province after the

end-2014 national audit.

Table 3. Infrastructure investment pipeline in 2015

Date of approval Type of infrastructure Expected investment amount (RMBbn)

Years of construction needed (estimate)

Provinces involved Length, km

4/12/2014 Airport 1.4 Shandong 日照28/11/2014 Railway 12.1 Yunnan, Guizhou, Sichuan (叙永至毕节) 18128/11/2014 Railway 12.1 Heilongjiang (哈尔滨至牡丹江) 3628/11/2014 Railway (tunnel) 1.8 Beijing, Hebei (北京至张家口铁路) 1528/11/2014 Airport 1.5 Gansu (兰州中川机场)25/11/2014 Railway 19.6 3.5 Jilin(长春至白城) 33025/11/2014 Railway 19.1 5 Chongqing (涪陵至梅江) 33925/11/2014 Railway 8.8 3.5 Inner Mongolia, Hebei (正蓝旗至张家口) 19225/11/2014 Railway 18.8 4 Shaanxi(阳平关至安康铁路)20/11/2014 Harbour 12.1 Shanghai (国际航运中心洋山深水港区四期工程)15/11/2014 Railway 19.6 Guangxi, Guangdong (柳州至梧州) 23315/11/2014 Railway 6.5 3.5 Inner Mongolia, Hebei (多伦至丰宁) 14515/11/2014 Railway 45.3 6.5 Sichuan Yunnan (峨嵋至米易) 715/11/2014 Railway 10.5 4.5 Gansu (兰州至合作) 18315/11/2014 Railway 70.9 5 Ningxia, Shaanxi (银川至西安) 59805/11/2014 Railway 6.6 3.5 Shanxi, Hebei (和顺至邢台) 13505/11/2014 Railway 30.5 5 Zhejiang, Fujian(衢州至宁德) 38305/11/2014 Railway 37.6 5 Qinghai, Xinjiang (格尔木至库尔勒) 121505/11/2014 Railway 9.9 2.5 Guangxi (南昆铁路南宁至百色段) 20905/11/2014 Railway 46.5 4.5 Jiangsu (连云港至镇江) 30505/11/2014 Railway 15.5 Yunnan(祥云至临沧) 19905/11/2014 Railway 53.3 5 Jiangxi (南昌至赣州) 42030/10/2014 Railway 193.0 5 Inner Mongolia, Shaanxi, Shanxi, Henan, Hubei,

Hunan, Jiangxi (蒙华铁路,蒙西至华中)1807

30/10/2014 Railway 18.0 Shanxi, Hebei (大同至张家口) 13730/10/2014 Railway 36.6 7 Tibet (拉萨至林芝) 40222/10/2014 Railway 38.4 5.5 Chongqing, Hubei, Hunan (黔江至张家界至常德) 33922/10/2014 Railway bridge 8.6 4 Anuui (商合杭铁路芜湖长江公铁大桥)22/10/2014 Railway 97.4 Henan, Hubei, Chongqing (郑州至万州) 78522/10/2014 Airport 0.8 Jilin (松原)22/10/2014 Airport 1.1 Qinghai,(果洛)22/10/2014 Airport 0.5 Inner Mongolia (扎兰屯)22/10/2014 Airport 1.5 Yunnan(澜沧)22/10/2014 Airport 1.6 Guizhou(仁怀)16/10/2014 Railway 25.6 4 Liaoning, Inner Mongolia (锦州至白音华) 60116/10/2014 Railway 25.7 7 Yunnan(大理至瑞丽) 33016/10/2014 Railway 44.5 Yunnan(玉溪至磨憨) 504

Source: Various media sources, HSBC

10

Macro China Economics 16 December 2014

abc

3. Reforms gaining momentum The Third Plenum, an important policy meeting

held in late 2013, proposed a wide-ranging series

of reforms. We expect the pace of change to

accelerate in 2015. In Table 4 we list the main

reform objectives, progress made in 2014, and our

expectations for 2015.

Fiscal reform: Given the planned budget

consolidation in 2015, we expect fiscal reforms to

pick up pace in the coming months. Apart from

finishing the national audit, we expect progress to

be made on increasing direct transfers from Beijing

and taking stricter control of local government

budgets. At the same time, we expect more changes

to budget management in order to establish a

multi-year, counter-cyclical fiscal budget.

Financial reforms: These moved ahead quickly

in 2014 and we expect the launch of the deposit

insurance scheme to pave the way for greater

financial liberalisation in the next 1-2 years.

For more details see China: Macro implications of

the deposit insurance scheme, 1 December 2014

and China: New blueprint for financial market

reforms 2020, 12 May 2014).

In addition, this year has seen progress made on

outward direct investments, particularly through

the launch of the New Silk Road initiative and the

Asia Infrastructure Investment Bank. Both will

accelerate in 2015, helping China to achieve more

balanced flows and make the RMB a more

internationally used currency (see Xi’s New Silk

Road plan, 18 November 2014; and Building on

China’s overseas investment, 8 August 2014).

4. Property market: cooling, but not collapsing A major risk we flagged in 2014 was the correction

in the property market. As the year progressed,

the fall in property sales indeed deepened, from

around 0% to 10% y-o-y.

Table 4. Reforms are set to accelerate

Third Plenum objective in 2013 Progress in 2014 Expectation for 2015

SOE reform Develop mixed-ownership entities; improve management of state-owned assets; Convert some SOEs into state-owned capital investment firms; Revise senior executive compensation.

Revised senior SOE management compensation; set mandatory requirements to increase mixed-ownership ratio for local SEOs; Asset sales by Sinopec; trial programme for six central SOEs.

Central SOE reform plan; higher private capital share of local SOEs.

Factor price reform Relax government price controls; improve transparency of the pricing process; give market the determinant role in pricing.

Regulated bank service prices; published medical pricing reform draft for consultation; revised railway service prices from fixed price to upper bound (select lines).

Deregulation of utility prices, merge different gas pricing systems, adopt a staggered pricing system for residential gas price; medical pricing reform; railway pricing reform;

Hukou reform Equalise urban and rural hukou rights: increase urbanisation rate to 60% by 2020; remove hukou restrictions in small cities, simplify the process for medium-size cities; increase social benefit coverage for both local residents and migrants

Equal rural and urban status; settlement schemes for migrant workers; expansion of basic social services for all residents.

More cities to implement the hukou conversion and gradually make social services equal for all.

Land reform Build a unified national construction land market; complete the registration of land usage rights nationwide within five years; allow rural collective construction land to be sold in the commercial market (same as urban state-owned land).

Draft proposal submitted to State Council, which includes changes to land acquisition methods and the redevelopment of homestead system.

Final draft either at end-2014 or early 2015, trial programme in certain provinces, and further related legislation in 2015.

Fiscal reform Fiscal budgetary reform and tax reform: Establish multi-year fiscal budget with automatic balances; Increase the share of direct tax; accelerate property tax legislation.

Gave legal premise to the municipal bond market; Tightened rules on local government debts (stock and new issuance); Began a fresh national audit to incorporate all recognised liabilities into the 2015 budget.

Budget consolidation to link liabilities to income streams; Further disable LGFVs, Increase share of direct transfer.

Financial reform A more open financial sector (to foreign and private capital); accelerate equity and bond market reforms; encourage financial innovation; accelerate capital account convertibility and RMB internationalisation; establish deposit insurance system.

Draft regulation for the deposit insurance scheme; re-started the IPO process; raised the upper bound on deposit rates and simplified lending rates; Shanghai-Hongkong Stock Connect; Shanghai Free Trade Zone and negative list; tighter regulations to reduce financial sector risks.

Implement the deposit insurance scheme; establish more RMB offshore settlement centres; build on the New Silk Road initiative; further interest rate liberalisation.

Source: Various media sources, CEIC

11

Macro China Economics 16 December 2014

abc

We estimated in May 2014 that, if property sales

were to contract 10% every month for 12 months,

the cumulative impact on GDP would be roughly

-1ppt (see China’s property slowdown: How

worried should we be?, 29 May 2014).

What’s happened this year is quite close to our

base case. Both local governments as well as the

PBoC became more supportive of the market in

September. After local governments removed

home purchase restrictions in second and third tier

cities, the PBoC relaxed mortgage rules ahead of

the 1 October Golden Week holiday.

In recent months, signs of stabilisation have

emerged, at least on the sales side, but it is still

too early to predict a rebound. Even if the market

starts to improve slowly, the earliest we can expect

to see any positive impact on the economy would

be mid-2015 as sales usually lead investment by

six months. In fact, our base case is that sales will

probably continue to contract but at a more

moderate pace in the coming months. Investment

will likely remain depressed at least for the first

half of 2015. Our base case is that property

investment will stabilise at around 11% in 2015,

down from 12% in 2014 and 20% in 2013.

Continued softness in the property market means

related sectors will likely remain under pressure in

2015. Chart 14, taken from our report of 12 May

2014, China: New blueprint for financial market

reforms 2020, estimates how reliant each sector is

on property demand. Specifically, for every

RMB1 demand in materials, RMB0.25 is down to

the property sector.

Apart from the spill-over effect, both buyers and

sellers will likely increasingly differentiate on a

city basis. The new urbanisation plan will provide

some impetus but the supply and demand

dynamics will vary by region (see Table 4).

5. RMB: no big devaluation Slower inflation

The final theme for 2015 will be the RMB.

The currency’s volatility is rising and will continue

to do so in 2015. In view of expectations for a

stronger USD and further monetary easing, our FX

colleagues have changed their USDCNY forecast to

6.22 from 6.10 (see Asian FX Focus: 2015 Outlook:

The pressure cooker, 8 December 2014).

From a macro perspective, there are two main

implications. First, let’s examine the impact of

structurally slower FX inflows on monetary

conditions. Chart 15 shows the quarterly balance of

payment positions. Apart from a gradually

shrinking current account (due to a smaller trade

balance and increasing services outflow),

the financial account is also seeing more outflows.

As China pursues balanced capital flows, slower

FX inflows look likely to become a structural trend.

Chart 13. The correction in 2014 Chart 14. Closely intertwined

Source: CEIC, HSBC Source: CEIC, HSBC

-20-100102030405060

-40-20

020406080

100120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% YoY% YoY, Ytd

Property sales (LHS) Property price (RHS)0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

2005 2010

12

Macro China Economics 16 December 2014

abc

Meanwhile, a reduction in routine FX intervention

means that the inflows into base money growth will

moderate. As mentioned earlier when discussing

inflation, lower inflows automatically translate into

tighter monetary conditions (Chart 10). We believe

targeted liquidity as well as RRR cuts will be

needed to keep base money growth stable in 2015.

Impact on exports

The second issue to consider is the impact on

exports. Our FX colleagues have trimmed their

RMB forecasts, looking for less than 1%

depreciation in 2015. However, the impact on the

currency’s exchange rate (real or nominal) with its

trade partners less clear. In fact, given

expectations for QE in the Eurozone, and further

monetary easing in Japan, our G10 colleagues

expect the EUR and JPY to depreciate more

versus than USD than the RMB (see Currency

Outlook: Global frailty favours the dollar,

13 November 2014). This means the RMB will

likely appreciate in nominal terms versus its trade

partners, as well as real appreciation (as inflation

will likely still be higher in China than in the

Eurozone or Japan). Although we have factored in

a gradual improvement in external demand, the

lift to exports is likely to be at least partly offset

by appreciation on a REER basis and growth will

remain domestically driven.

But devaluation is not an option

A question frequently asked by clients is whether

China will join the currency war. After all,

if growth is slowing and deflationary risks are

rising, why not pick the seemingly convenient

route of FX devaluation?

Our answer is that policymakers still have

sufficient monetary and fiscal policy ammunition

to boost growth via domestic demand. In fact,

we see them pulling these levers more forcefully

in 2015. As highlighted in the previous sections,

more aggressive monetary easing and a greater

fiscal deficit are ways to support domestic

demand in 2015.

And in view of the still sluggish external demand,

the benefits from depreciation may not be so

obvious. In addition, such a move from the PBoC

might trigger more competitive devaluation from

China’s trade partners. In that case, devaluation

would be counter-productive and might lead to

slower growth in the whole region.

Instead of devaluation, we think policymakers

will do more to increase the RMB’s capital

account convertibility in 2015. Many initiatives

were taken in 2014 to deregulate cross border

portfolio flows (e.g. Shanghai-Hong Kong Stock

Connect, the Shanghai Free Trade Zone) and we

expect more measures in 2015 to further increase

the openness of the onshore capital markets.

Chart 15. Structurally less inflow Chart 16. REER gains will offset some export gains

Source: CEIC, HSBC Source: CEIC, HSBC

-150

-100

-50

0

50

100

150

200

250

-150

-100

-50

0

50

100

150

200

250

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

USDbnUSDbn

Portfolio Inv Others Current Acc Direct Inv

-150

-100

-50

0

50

100

150

200

250

-150

-100

-50

0

50

100

150

200

250

06 07 08 09 10 11 12 13 14

USDbnUSDbn

FX purchase, USDbn FX reserves, USDbn

13

Macro China Economics 16 December 2014

abc

China is also looking for more ways to export its

excess saving, for example, through encouraging

outward direct investment (e.g. Asia Infrastructure

Investment Bank, New Silk Road). We expect

further outward infrastructure investment in 2015

which will lead to increasingly more balanced

investment flows. We believe this is a far more

sustainable way to relieve appreciation pressure

on the currency.

14

Macro China Economics 16 December 2014

abc

This page intentionally left blank.

15

Macro China Economics 16 December 2014

abc

Charts

16

Macro China Economics 16 December 2014

abc

GDP

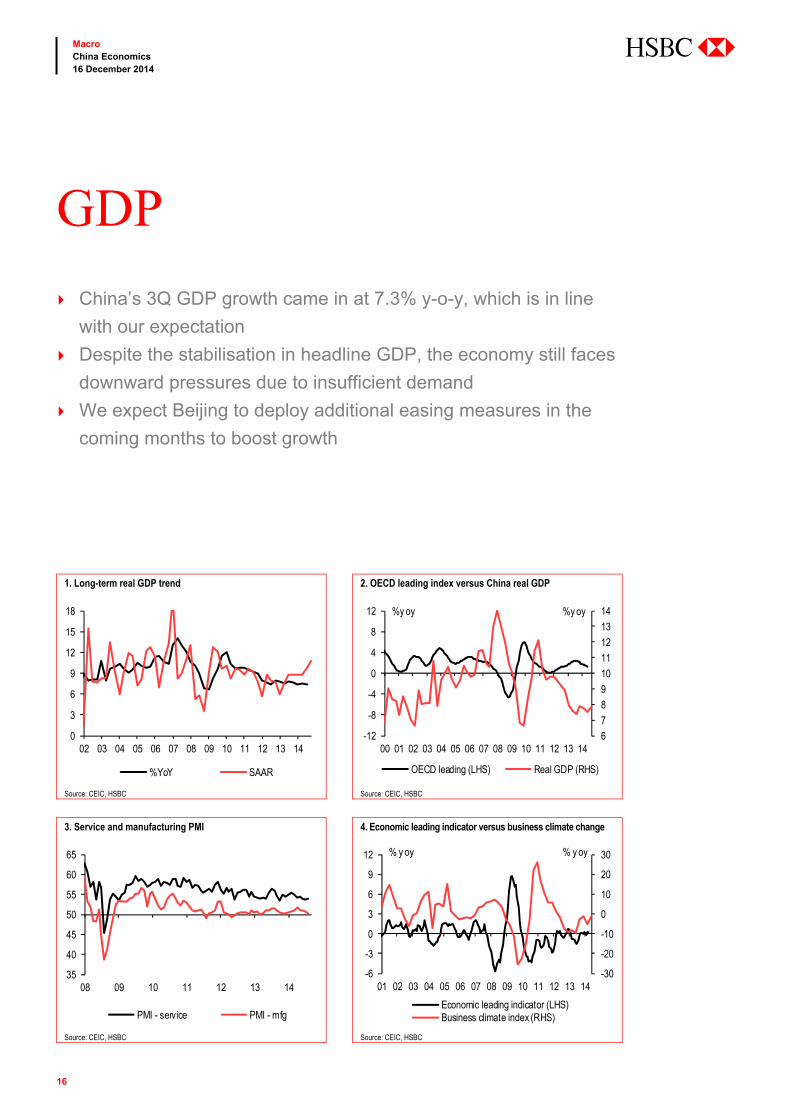

China’s 3Q GDP growth came in at 7.3% y-o-y, which is in line

with our expectation

Despite the stabilisation in headline GDP, the economy still faces

downward pressures due to insufficient demand

We expect Beijing to deploy additional easing measures in the

coming months to boost growth

1. Long-term real GDP trend 2. OECD leading index versus China real GDP

Source: CEIC, HSBC Source: CEIC, HSBC

3. Service and manufacturing PMI 4. Economic leading indicator versus business climate change

Source: CEIC, HSBC Source: CEIC, HSBC

0

3

6

9

12

15

18

02 03 04 05 06 07 08 09 10 11 12 13 14

%YoY SAAR

6

7

8

9

10

11

12

13

14

-12

-8

-4

0

4

8

12

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

OECD leading (LHS) Real GDP (RHS)

%y oy %y oy

35

40

45

50

55

60

65

08 09 10 11 12 13 14

PMI - service PMI - mfg

-30

-20

-10

0

10

20

30

-6

-3

0

3

6

9

12

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Economic leading indicator (LHS)Business climate index (RHS)

% y oy % y oy

17

Macro China Economics 16 December 2014

abc

5. GDP, by region (nominal GDP, weighted) 6. GDP, by industry

Source: CEIC, HSBC Source: CEIC, HSBC

7. Industrial production 8. Commodity production

Source: CEIC, HSBC Source: CEIC, HSBC

9. Construction sector 10. Confidence indices

Source: CEIC, HSBC Source: CEIC, HSBC

5

7

9

11

13

15

17

Jun-

06

Mar

-07

Dec-

07

Sep-

08

Jun-

09

Mar

-10

Dec-

10

Sep-

11

Jun-

12

Mar

-13

Dec-

13

Sep-

14

Bohai YRD PRD

YTD, %y oy

0

3

6

9

12

15

18

21

96 98 00 02 04 06 08 10 12 14

Primary Secondary Tertiary

YTD, %y oy

5

8

11

14

17

20

23

01 02 03 04 05 06 07 08 09 10 11 12 13 14

VAI

% y oy , 3mma

-10-505

101520253035

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Electricity production

% y oy , 3mma

10

15

20

25

30

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

07 08 09 10 11 12 13 14

Construction output value %yoy

RMB bn %y oy

50

55

60

65

85

90

95

100

105

110

02 03 04 05 06 07 08 09 10 11 12 13 14

Consumer confidence (LHS)Future income confidence (RHS)

18

Macro China Economics 16 December 2014

abc

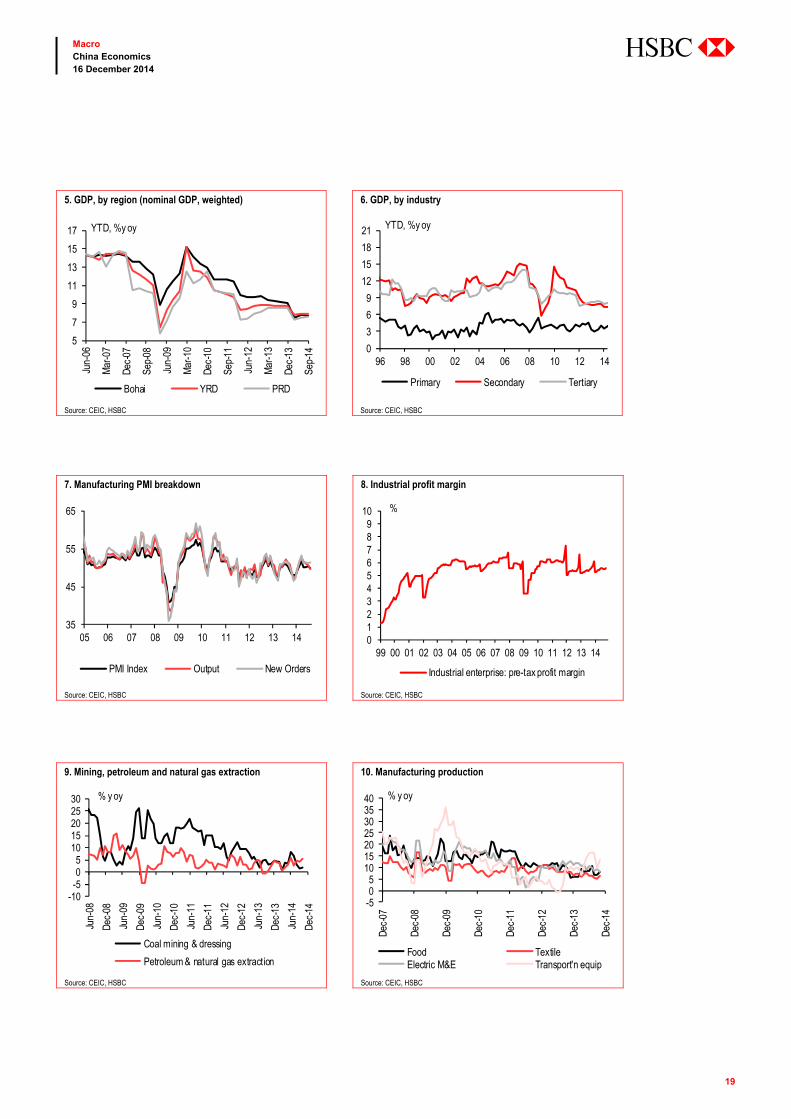

Industrial production

October IP slowed to 7.7% y-o-y as the one-off boost from faster

electronic output in September faded

Slower manufacturing output growth was the main factor behind

the slowdown

The downward pressures on the industrial sector persisted, and

are likely to remain in the coming months

1. Industrial production vs GDP 2. Industrial production growth trend

Source: CEIC, HSBC Source: CEIC, HSBC

3. Industrial production vs manufacturing PMI 4. Electricity production changes together with IP

Source: CEIC, HSBC Source: CEIC, HSBC

6789101112131415

5

7

9

11

13

15

17

19

21

01 02 03 04 05 06 07 08 09 10 11 12 13 14

IP(LHS) GDP (RHS)

%y oy %y oy

-4-3-2-10123456

5

7

9

11

13

15

17

19

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

%YoY SA, %MoM

%y oy, 3mma %mom, 3mma

35

40

45

50

55

60

65

579

11131517192123

05 06 07 08 09 10 11 12 13 14

IP (LHS) Mfg PMI (RHS)

%y oy, 3mma %

-15-10-505101520253035

579

11131517192123

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

IP Electricity production

% y oy , 3mma % y oy , 3mma

19

Macro China Economics 16 December 2014

abc

5. GDP, by region (nominal GDP, weighted) 6. GDP, by industry

Source: CEIC, HSBC Source: CEIC, HSBC

7. Manufacturing PMI breakdown 8. Industrial profit margin

Source: CEIC, HSBC Source: CEIC, HSBC

9. Mining, petroleum and natural gas extraction 10. Manufacturing production

Source: CEIC, HSBC Source: CEIC, HSBC

5

7

9

11

13

15

17

Jun-

06

Mar

-07

Dec-

07

Sep-

08

Jun-

09

Mar

-10

Dec-

10

Sep-

11

Jun-

12

Mar

-13

Dec-

13

Sep-

14

Bohai YRD PRD

YTD, %y oy

0

3

6

9

12

15

18

21

96 98 00 02 04 06 08 10 12 14

Primary Secondary Tertiary

YTD, %y oy

35

45

55

65

05 06 07 08 09 10 11 12 13 14

PMI Index Output New Orders

0123456789

10

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Industrial enterprise: pre-tax profit margin

%

-10-505

1015202530

Jun-

08

Dec-

08

Jun-

09

Dec-

09

Jun-

10

Dec-

10

Jun-

11

Dec-

11

Jun-

12

Dec-

12

Jun-

13

Dec-

13

Jun-

14

Dec-

14

Coal mining & dressing

Petroleum & natural gas extraction

% y oy

-505

10152025303540

Dec-

07

Dec-

08

Dec-

09

Dec-

10

Dec-

11

Dec-

12

Dec-

13

Dec-

14

Food TextileElectric M&E Transport'n equip

% y oy

20

Macro China Economics 16 December 2014

abc

Private consumption

Retail sales grew 11.5% y-o-y in October, in line with

expectations, but slowing from earlier this year

Above-limit spending growth slowed further to 8.3% in October

from 8.5%. Auto sales growth slowed to 4.5% from 6.7%

Private consumption growth remains sluggish as slower growth

weighs on income growth and expectations remain subdued

1. Retail sales trend 2. Consumer confidence

Source: CEIC, HSBC Source: CEIC, HSBC

3. Confidence in income 4. Confidence in prices

Source: CEIC, HSBC Source: CEIC, HSBC

-10

0

10

20

30

40

50

60

5

10

15

20

25

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

%YoY (LHS) SAAR, 3mma (RHS)

80

90

100

110

120

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Consumer confidence Satisfactory indexExpectation index

%

45

50

55

60

65

01 02 03 04 05 06 07 08 09 10 11 12 13

Current income sentimentFuture income confidence

Index

102030405060708090

01 02 03 04 05 06 07 08 09 10 11 12 13

Current price satisfactionFuture price expectation

%

21

Macro China Economics 16 December 2014

abc

5. Retail sales, by sector 6. Retail sales in urban vs rural areas

Source: CEIC, HSBC Source: CEIC, HSBC

7. Per-capita income vs expenditure – Urban households 8. Per-capita income vs expenditure – Rural households

Source: CEIC, HSBC Source: CEIC, HSBC

9. Expenditure, by product – Urban households 10. Expenditure, by product – Rural households

Source: CEIC, HSBC Source: CEIC, HSBC

6

12

18

24

30

06 07 08 09 10 11 12 13 14

Wholesale & Retail TradeAccommodation & Catering Trade

% y oy

9

12

15

18

21

24

27

06 07 08 09 10 11 12 13 14

Urban Rural

% y oy

0

5

10

15

20

25

06 07 08 09 10 11 12 13 14

IncomeDisposable incomeConsumption expenditure

per capita, % y oy

-5

0

5

10

15

20

25

30

02 03 04 05 06 07 08 09 10 11 12 13

Cash Income Cash consumption expenditure

per capita, % y oy

-5

0

5

10

15

20

25

30

03 04 05 06 07 08 09 10 11 12

Food & housing ClothingTransport & telecom Service & others

%y oy

-10

0

10

20

30

40

03 04 05 06 07 08 09 10 11 12

Food & housing ClothingTransport & telecom Service & others

%y oy

22

Macro China Economics 16 December 2014

abc

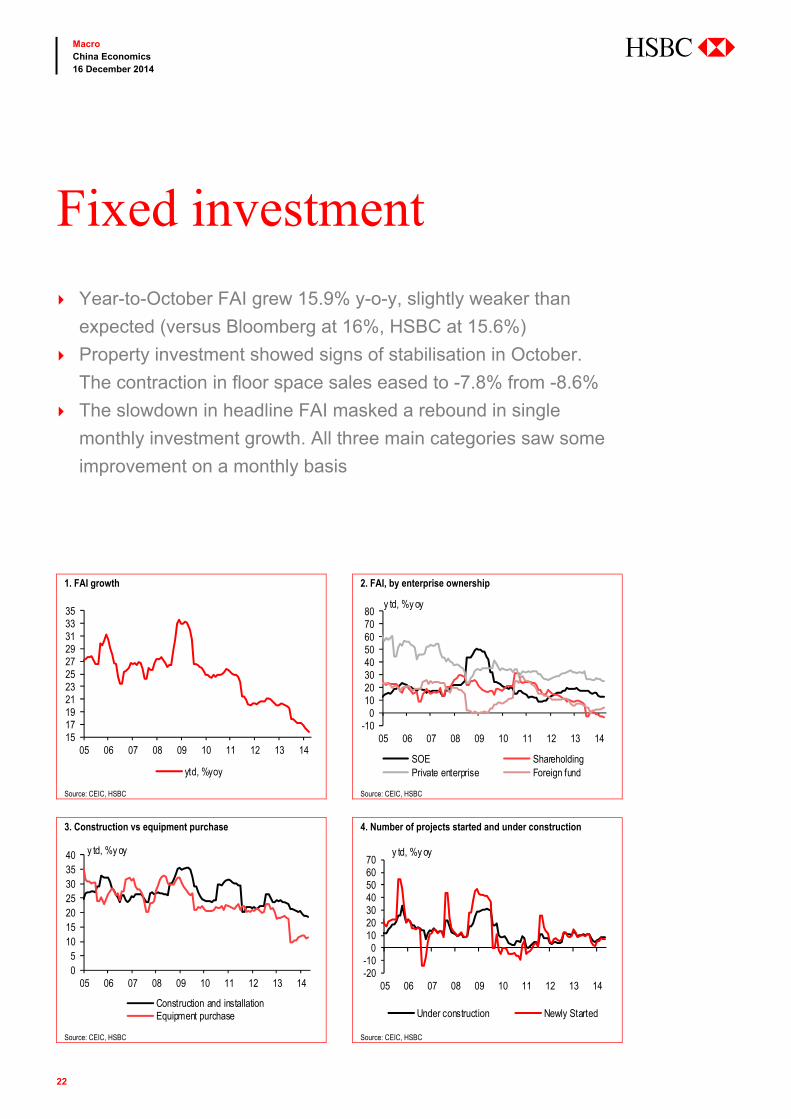

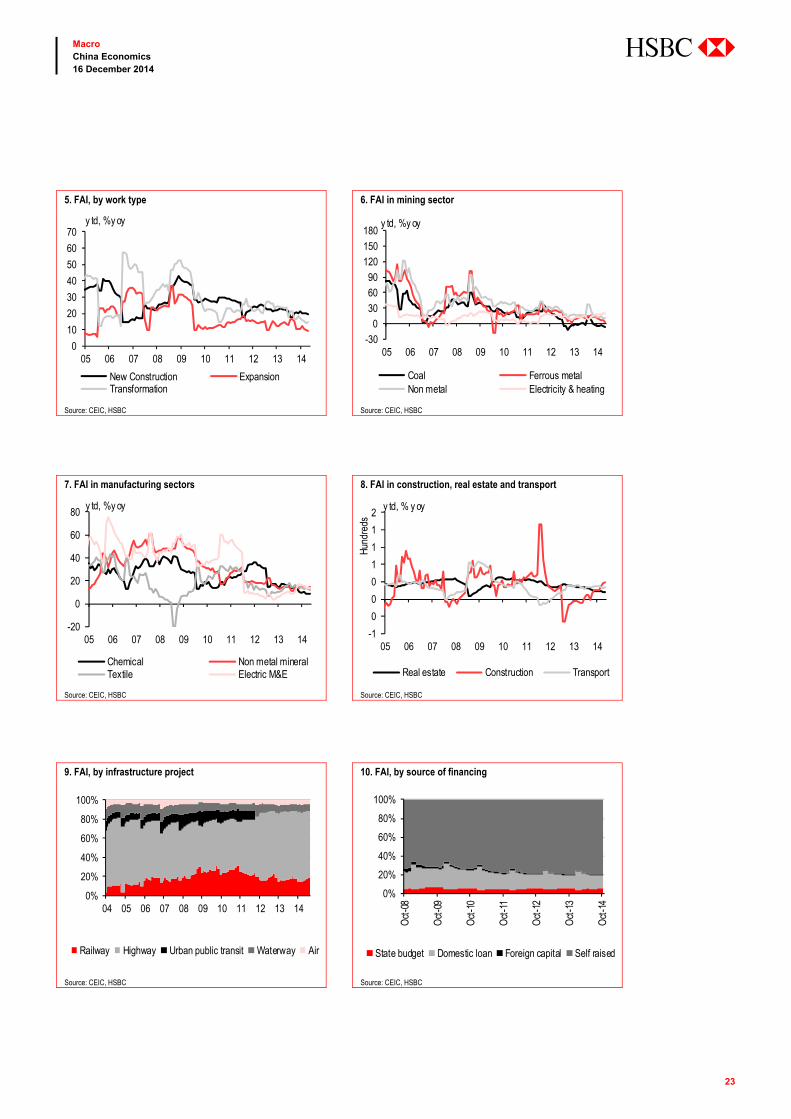

Fixed investment

Year-to-October FAI grew 15.9% y-o-y, slightly weaker than

expected (versus Bloomberg at 16%, HSBC at 15.6%)

Property investment showed signs of stabilisation in October.

The contraction in floor space sales eased to -7.8% from -8.6%

The slowdown in headline FAI masked a rebound in single

monthly investment growth. All three main categories saw some

improvement on a monthly basis

1. FAI growth 2. FAI, by enterprise ownership

Source: CEIC, HSBC Source: CEIC, HSBC

3. Construction vs equipment purchase 4. Number of projects started and under construction

Source: CEIC, HSBC Source: CEIC, HSBC

1517192123252729313335

05 06 07 08 09 10 11 12 13 14

ytd, %yoy

-100

1020304050607080

05 06 07 08 09 10 11 12 13 14

SOE ShareholdingPrivate enterprise Foreign fund

y td, %y oy

05

10152025303540

05 06 07 08 09 10 11 12 13 14

Construction and installationEquipment purchase

y td, %y oy

-20-10

010203040506070

05 06 07 08 09 10 11 12 13 14

Under construction Newly Started

y td, %y oy

23

Macro China Economics 16 December 2014

abc

5. FAI, by work type 6. FAI in mining sector

Source: CEIC, HSBC Source: CEIC, HSBC

7. FAI in manufacturing sectors 8. FAI in construction, real estate and transport

Source: CEIC, HSBC Source: CEIC, HSBC

9. FAI, by infrastructure project 10. FAI, by source of financing

Source: CEIC, HSBC Source: CEIC, HSBC

0

10

20

30

40

50

60

70

05 06 07 08 09 10 11 12 13 14

New Construction ExpansionTransformation

y td, %y oy

-30

030

6090

120150

180

05 06 07 08 09 10 11 12 13 14

Coal Ferrous metalNon metal Electricity & heating

y td, %y oy

-20

0

20

40

60

80

05 06 07 08 09 10 11 12 13 14

Chemical Non metal mineralTextile Electric M&E

y td, %y oy

-1

0

0

0

1

1

1

2

05 06 07 08 09 10 11 12 13 14

Hund

reds

Real estate Construction Transport

y td, % y oy

0%

20%

40%

60%

80%

100%

04 05 06 07 08 09 10 11 12 13 14

Railway Highway Urban public transit Waterway Air

0%

20%

40%

60%

80%

100%

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

State budget Domestic loan Foreign capital Self raised

24

Macro China Economics 16 December 2014

abc

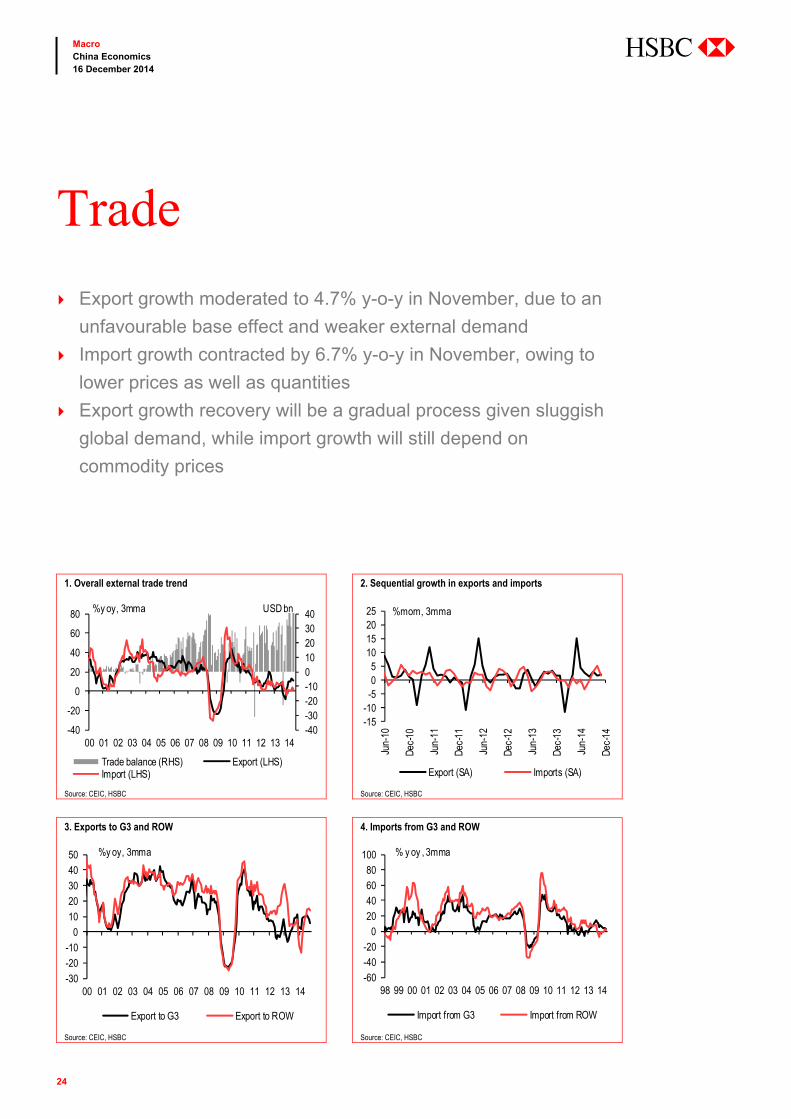

Trade

Export growth moderated to 4.7% y-o-y in November, due to an

unfavourable base effect and weaker external demand

Import growth contracted by 6.7% y-o-y in November, owing to

lower prices as well as quantities

Export growth recovery will be a gradual process given sluggish

global demand, while import growth will still depend on

commodity prices

1. Overall external trade trend 2. Sequential growth in exports and imports

Source: CEIC, HSBC Source: CEIC, HSBC

3. Exports to G3 and ROW 4. Imports from G3 and ROW

Source: CEIC, HSBC Source: CEIC, HSBC

-40-30-20-10010203040

-40

-20

0

20

40

60

80

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Trade balance (RHS) Export (LHS)Import (LHS)

%y oy, 3mma USD bn

-15-10-505

10152025

Jun-

10

Dec-

10

Jun-

11

Dec-

11

Jun-

12

Dec-

12

Jun-

13

Dec-

13

Jun-

14

Dec-

14

Export (SA) Imports (SA)

%mom, 3mma

-30-20-10

01020304050

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Export to G3 Export to ROW

%y oy, 3mma

-60-40-20

020406080

100

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Import from G3 Import from ROW

% y oy , 3mma

25

Macro China Economics 16 December 2014

abc

5. Taiwan’s new export orders as a leading indicator 6. PMI new export orders vs exports

Source: CEIC, HSBC Source: CEIC, HSBC

7. Exports – ordinary vs processing trade 8. Trade price index

Source: CEIC, HSBC Source: CEIC, HSBC

9. Exports, by major commodity 10. Imports, by major commodity

Source: CEIC, HSBC Source: CEIC, HSBC

-40

-20

0

20

40

60

80

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Export Taiwan's new export orders

% y oy , 3mma

44

46

48

50

52

54

56

58

-15

-10

-5

0

5

10

15

20

10 11 12 13 14

Export (SA, LHS) PMI new export orders (RHS)

%mom, 3mma Pts

-40

-20

0

20

40

60

80

100

06 07 08 09 10 11 12 13 14

Export - Ordinary trade Export - Processing

% y oy

-60-40-20

020406080

06 07 08 09 10 11 12 13 14

Export trade index value Import trade index value

% y oy

-60

-30

0

30

60

90

120

06 07 08 09 10 11 12 13 14

Mineral fuel, lubricants & materialManufactured goodsMachiery & transport equipmentMisc. mfg articles

% y oy

-25

0

25

50

75

06 07 08 09 10 11 12 13 14

Iron ore Crude petroleum oil

% y oy , 3mma

26

Macro China Economics 16 December 2014

abc

Prices

November CPI rose 1.4% y-o-y, the lowest reading since Jan

2010, reflecting the fall in oil prices as well as weak demand

Core inflation moderated again in November, suggesting demand

remained weak

Strong disinflationary pressures will likely prompt more monetary

easing in the coming months

1. Consumer price trend 2. CPI, by major segment

Source: CEIC, HSBC Source: CEIC, HSBC

3. Urban vs rural inflation 4. Producer price index

Source: CEIC, HSBC Source: CEIC, HSBC

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-4

-2

0

2

4

6

8

10

01 02 03 04 05 06 07 08 09 10 11 12 13 14

YOY (LHS) MOM (RHS)

% y oy % mom, 3mma

-5

0

5

10

15

20

25

06 07 08 09 10 11 12 13 14

Overall Core Food

% y oy

-4

-2

0

2

4

6

8

10

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Urban Rural

% y oy

-2.5

-1.5

-0.5

0.5

1.5

-10

-5

0

5

10

15

03 04 05 06 07 08 09 10 11 12 13 14

YOY (LHS) MOM (RHS)

% y oy % mom, 3mma

27

Macro China Economics 16 December 2014

abc

5. PPI, by industry (1) 6. PPI, by industry (2)

Source: CEIC, HSBC Source: CEIC, HSBC

7. Purchase and output prices 8. Fixed asset investment price index

Source: CEIC, HSBC Source: CEIC, HSBC

9. Petroleum prices 10. Property prices

Source: CEIC, HSBC Source: CEIC, HSBC

-15

-10

-5

0

5

10

15

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Light industry Heavy industry

% y oy

-10

-5

0

5

10

15

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Producer goods Consumer goods

% y oy

-15

-10

-5

0

5

10

15

20

01 02 03 04 05 06 07 08 09 10 11 12 13 14

PPICorporate goods price indexPurchasing price index - raw materials

% y oy

-10

-5

0

5

10

15

20

05 06 07 08 09 10 11 12 13

Overall index Equip, tool & instrum'tConstruct'n & install'n

% y oy

-60-30

0306090

120150180

05 06 07 08 09 10 11 12 13 14

PPI - petroleum and natural gasImport value index - petroleum

% y oy

-15-10-505

1015202530

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Residential property price

% y oy

28

Macro China Economics 16 December 2014

abc

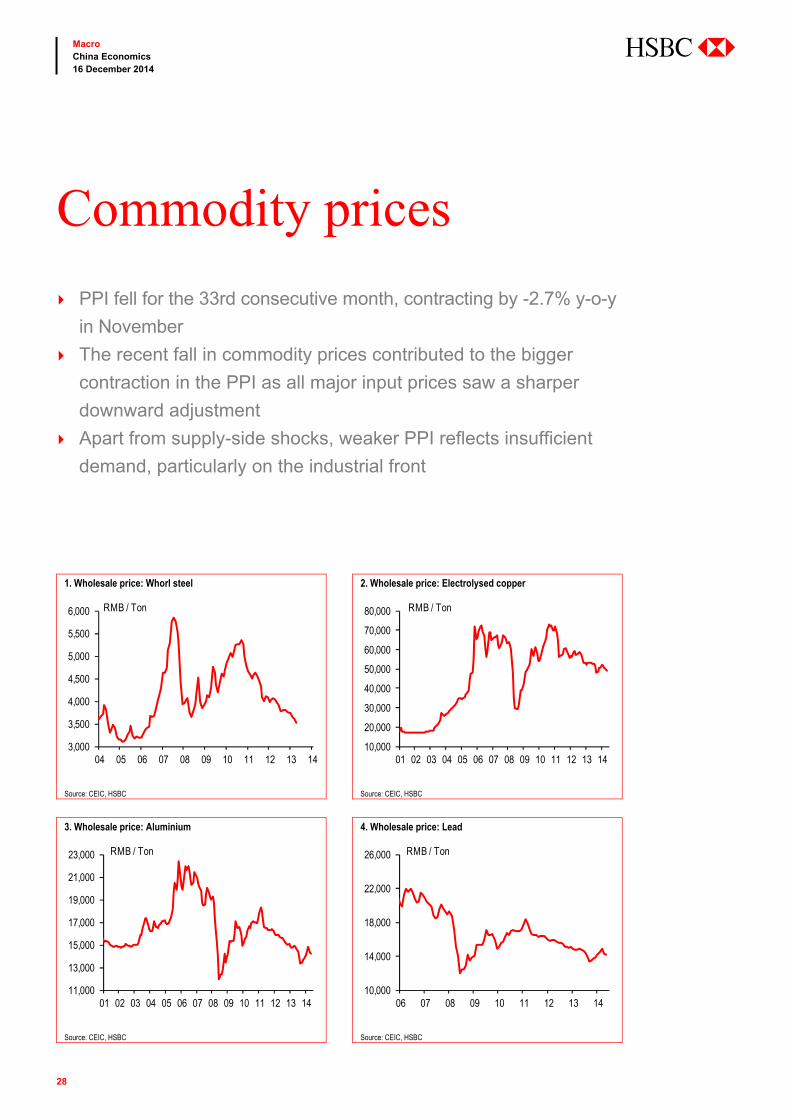

Commodity prices

PPI fell for the 33rd consecutive month, contracting by -2.7% y-o-y

in November

The recent fall in commodity prices contributed to the bigger

contraction in the PPI as all major input prices saw a sharper

downward adjustment

Apart from supply-side shocks, weaker PPI reflects insufficient

demand, particularly on the industrial front

1. Wholesale price: Whorl steel 2. Wholesale price: Electrolysed copper

Source: CEIC, HSBC Source: CEIC, HSBC

3. Wholesale price: Aluminium 4. Wholesale price: Lead

Source: CEIC, HSBC Source: CEIC, HSBC

3,000

3,500

4,000

4,500

5,000

5,500

6,000

04 05 06 07 08 09 10 11 12 13 14

RMB / Ton

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14

RMB / Ton

11,000

13,000

15,000

17,000

19,000

21,000

23,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14

RMB / Ton

10,000

14,000

18,000

22,000

26,000

06 07 08 09 10 11 12 13 14

RMB / Ton

29

Macro China Economics 16 December 2014

abc

5. Wholesale price: Zinc 6. Wholesale price: Nickel

Source: CEIC, HSBC Source: CEIC, HSBC

7. Wholesale price: Diesel oil 8. Wholesale price: Gasoline

Source: CEIC, HSBC Source: CEIC, HSBC

9. Retail price: Rice 10. Retail price: Flour

Source: CEIC, HSBC Source: CEIC, HSBC

8,000

12,000

16,000

20,000

24,000

28,000

32,000

36,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14

RMB / Ton

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14

RMB / Ton

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14

RMB / Ton

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14

RMB / Ton

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

01 02 03 04 05 06 07 08 09 10 11 12 13 14

RMB / Kg

1.752.002.252.502.753.003.253.503.754.004.254.504.755.00

01 02 03 04 05 06 07 08 09 10 11 12 13 14

RMB / Kg

30

Macro China Economics 16 December 2014

abc

Money and credit growth

October new loans came in at RMB548bn, below expectations of

RMB626bn and down from RMB857bn in September

Total Social Financing grew by RMB663bn, lower than

expectation of RMB888bn. Apart from RMB loans, most other

categories contracted

October M2 moderated further 12.6% from 12.9% on the back of

reduced willingness to lend as well as the deposit deviation rule

1. Loans vs money supply 2. Deposits vs loan growth

Source: CEIC, HSBC Source: CEIC, HSBC

3. FAI vs loan growth 4. New renminbi loans

Source: CEIC, HSBC Source: CEIC, HSBC

0

5

10

15

20

25

30

35

40

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

M1 M2 Loan

%y oy

-505

10152025303540

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Deposit Household deposit

%y oy

510152025303540455055

04 05 06 07 08 09 10 11 12 13 14

Loan FAI

%y oy

-3000

300600900

1200150018002100

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Medium & long termShort term and bill financingNew loan

RMB bn

New RMB loan

31

Macro China Economics 16 December 2014

abc

5. PBoC open market operations 6. Consumer credit

Source: Wind, HSBC Source: CEIC, HSBC

7. Loan-to-deposit ratio 8. Money supply vs price level

Source: CEIC, HSBC Source: CEIC, HSBC

9. M1-M2 gap vs CPI 10. Foreign reserves

Source: CEIC, HSBC Source: CEIC, HSBC

-2,000

-1,000

0

1,000

2,000

09 10 11 12 13 14

RMBbn

Liquidity injection Liquidity withdrawalNet position

10

20

30

40

50

60

70

08 09 10 11 12 13 14Consumer loan Loan

%y oy

60

65

70

75

80

85

90

95

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Loan-to-deposit ratio

%

-2

0

2

4

6

8

10

05

1015202530354045

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

M1 (LHS) CPI (Lag by 6 months, RHS)

% y oy % y oy

-2

0

2

4

6

8

10

-15

-10

-5

0

5

10

15

01 02 03 04 05 06 07 08 09 10 11 12 13 14

M1-M2 gap (LHS) CPI (RHS)

% y oy % y oy

0

10

20

30

40

50

60

0500

1,0001,5002,0002,5003,0003,5004,0004,500

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

USD bn (LHS) %YoY (RHS)

32

Macro China Economics 16 December 2014

abc

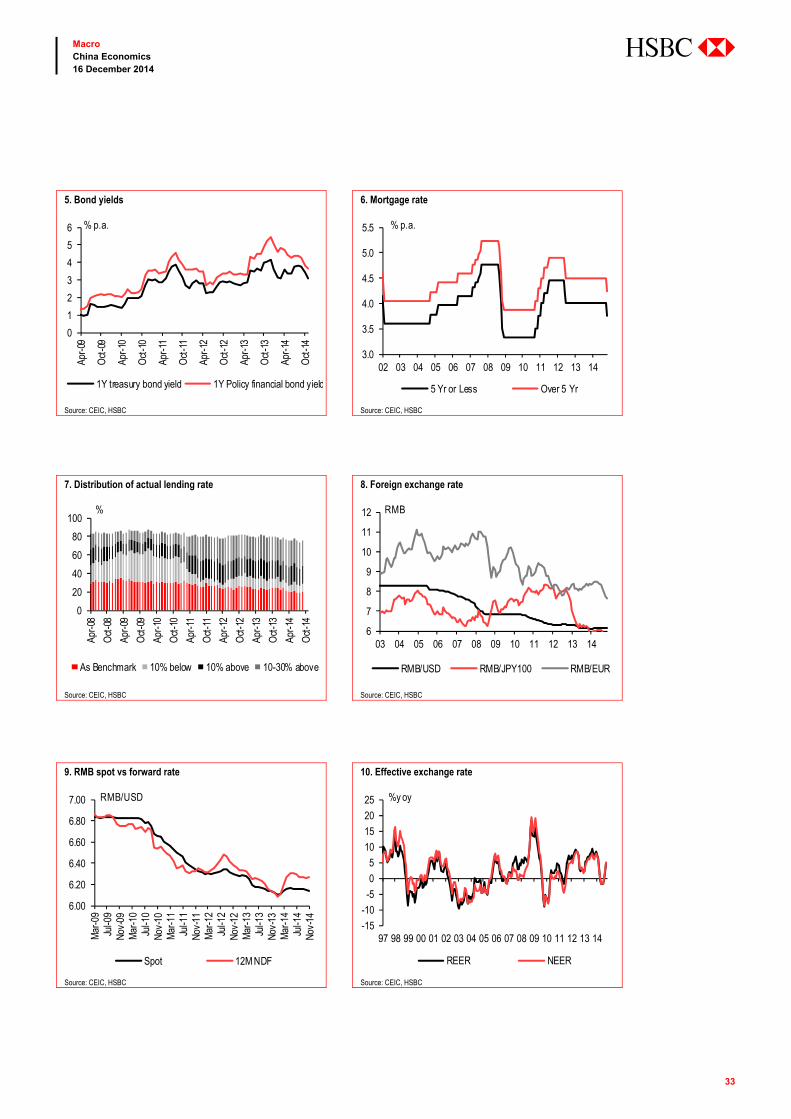

Interest and exchange rates

The PBoC cut policy rates on 21 November 2014. The one-year

deposit rate was lowered by 25bp to 2.75% while the one year

lending rate was lowered by 40bp to 5.6%

The State Council published its deposit insurance scheme draft

regulations in end November

Our HSBC FX Strategist forecasts USD-CNY at 6.22 by end 2015

and 6.30 by end 2016

1. Lending vs savings rates 2. Required reserve ratio

Source: CEIC, HSBC Source: CEIC, HSBC

3. PBoC bill issuance and reference yield 4. Interbank rate

Source: CEIC, HSBC Source: CEIC, HSBC

0

1

2

3

4

5

6

7

8

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

1Y lending rate 1Y deposit rate

% p.a.

79

11131517192123

06 07 08 09 10 11 12 13 14

RRRLarge depository institutionSmall and medium depository institution

%

00.511.522.533.54

0100200300400500600700800900

1,000

05 06 07 08 09 10 11 12 13 14

PBoC total bill issuance (LHS)3M PBoC bill issuance ref. yld

% p.a.RMB bn

0

1

2

3

4

5

6

7

8

06 07 08 09 10 11 12 13 14

3M SHIBOR 3M CHIBOR

% p.a.

33

Macro China Economics 16 December 2014

abc

5. Bond yields 6. Mortgage rate

Source: CEIC, HSBC Source: CEIC, HSBC

7. Distribution of actual lending rate 8. Foreign exchange rate

Source: CEIC, HSBC Source: CEIC, HSBC

9. RMB spot vs forward rate 10. Effective exchange rate

Source: CEIC, HSBC Source: CEIC, HSBC

0

1

2

3

4

5

6

Apr-0

9

Oct

-09

Apr-1

0

Oct

-10

Apr-1

1

Oct

-11

Apr-1

2

Oct

-12

Apr-1

3

Oct

-13

Apr-1

4

Oct

-14

1Y treasury bond yield 1Y Policy financial bond yield

% p.a.

3.0

3.5

4.0

4.5

5.0

5.5

02 03 04 05 06 07 08 09 10 11 12 13 14

5 Yr or Less Over 5 Yr

% p.a.

0

20

40

60

80

100

Apr-0

8

Oct

-08

Apr-0

9

Oct

-09

Apr-1

0

Oct

-10

Apr-1

1

Oct

-11

Apr-1

2

Oct

-12

Apr-1

3

Oct

-13

Apr-1

4

Oct

-14

As Benchmark 10% below 10% above 10-30% above

%

6

7

8

9

10

11

12

03 04 05 06 07 08 09 10 11 12 13 14

RMB/USD RMB/JPY100 RMB/EUR

RMB

6.00

6.20

6.40

6.60

6.80

7.00

Mar

-09

Jul-0

9No

v-09

Mar

-10

Jul-1

0No

v-10

Mar

-11

Jul-1

1No

v-11

Mar

-12

Jul-1

2No

v-12

Mar

-13

Jul-1

3No

v-13

Mar

-14

Jul-1

4No

v-14

Spot 12M NDF

RMB/USD

-15

-10

-5

0

5

10

15

20

25

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

REER NEER

%y oy

34

Macro China Economics 16 December 2014

abc

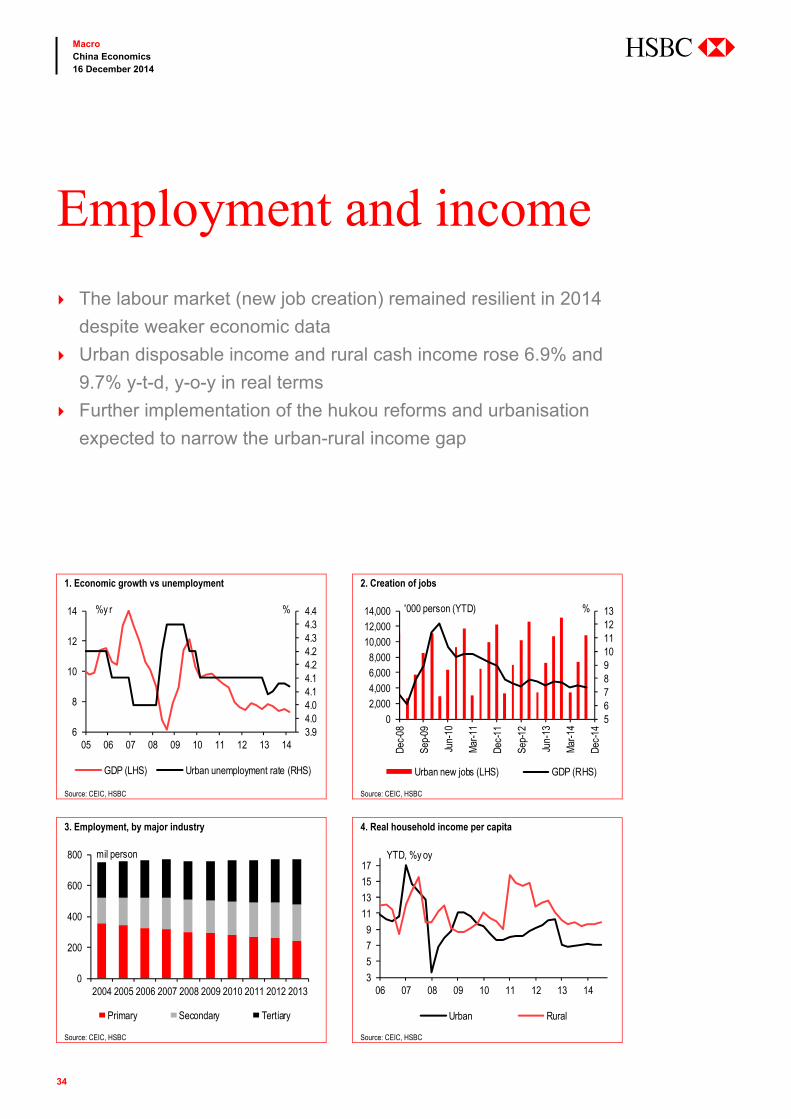

Employment and income

The labour market (new job creation) remained resilient in 2014

despite weaker economic data

Urban disposable income and rural cash income rose 6.9% and

9.7% y-t-d, y-o-y in real terms

Further implementation of the hukou reforms and urbanisation

expected to narrow the urban-rural income gap

1. Economic growth vs unemployment 2. Creation of jobs

Source: CEIC, HSBC Source: CEIC, HSBC

3. Employment, by major industry 4. Real household income per capita

Source: CEIC, HSBC Source: CEIC, HSBC

3.94.04.04.14.14.24.24.34.34.4

6

8

10

12

14

05 06 07 08 09 10 11 12 13 14

GDP (LHS) Urban unemployment rate (RHS)

%y r %

5678910111213

02,0004,0006,0008,000

10,00012,00014,000

Dec-

08

Sep-

09

Jun-

10

Mar

-11

Dec-

11

Sep-

12

Jun-

13

Mar

-14

Dec-

14

Urban new jobs (LHS) GDP (RHS)

'000 person (YTD) %

0

200

400

600

800

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Primary Secondary Tertiary

mil person

3

5

7

9

11

13

15

17

06 07 08 09 10 11 12 13 14

Urban Rural

YTD, %y oy

35

Macro China Economics 16 December 2014

abc

5. Economic growth vs real wage growth 6. Average wage growth

Source: CEIC, HSBC Source: CEIC, HSBC

7. Wage growth, by enterprise 8. Wage growth, by region

Source: CEIC, HSBC Source: CEIC, HSBC

9. Household income distribution – Urban 10. Household income distribution – Rural

Source: CEIC, HSBC Source: CEIC, HSBC

579

111315171921

02 03 04 05 06 07 08 09 10 11 12 13 14

Real average wage growth (YTD) GDP

%y oy

8

12

16

20

02 03 04 05 06 07 08 09 10 11 12 13 14

Nominal Real

YTD, %y oy

5

10

15

20

25

07 08 09 10 11 12 13 14

SOE Collective owned units Others

YTD, %y oy

5

10

15

20

25

30

35

Sep-

02

Sep-

03

Sep-

04

Sep-

05

Sep-

06

Sep-

07

Sep-

08

Sep-

09

Sep-

10

Sep-

11

Sep-

12

Sep-

13

Sep-

14

Eastern Central Central

YTD, %y oy

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 2011

<RMB25k RMB25-55K RMB55-85K >RMB85K

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012

<RMB2K RMB2-10K RMB10-20K >RMB20K

36

Macro China Economics 16 December 2014

abc

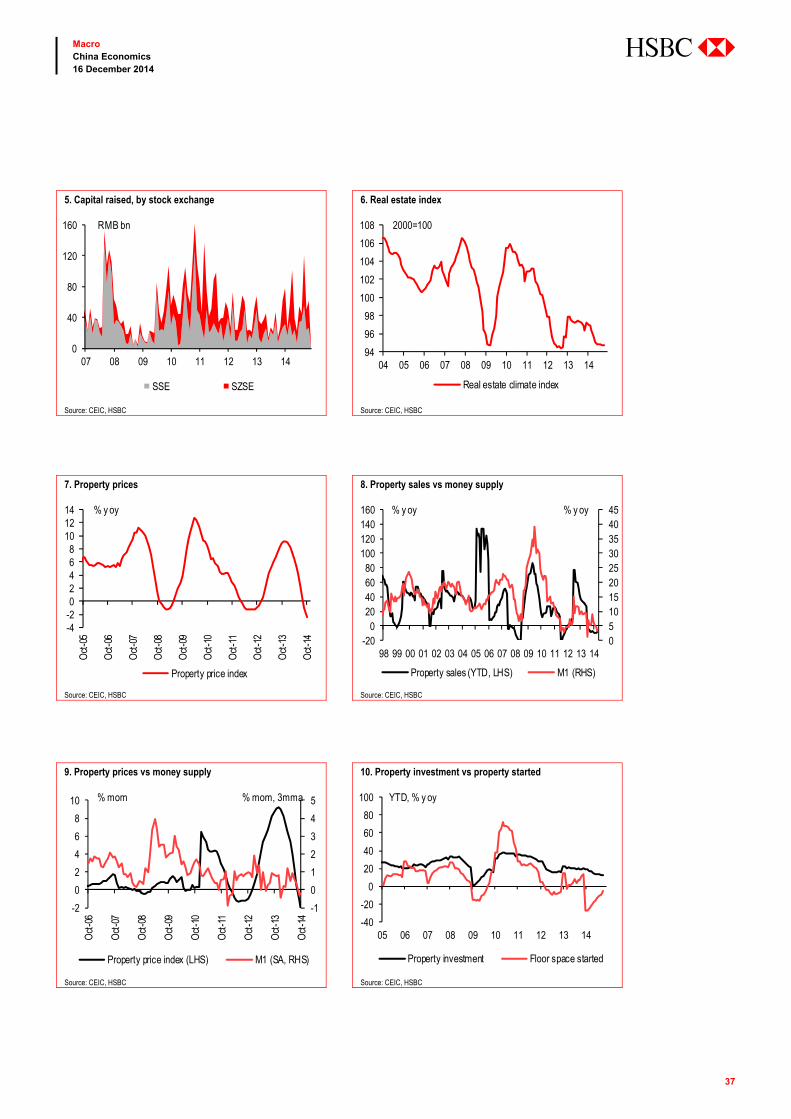

Asset markets

The property market showed initial signs of stabilisation following

the relaxation of mortgage rules, but downside risks persist

The central government has published new land reform

procedures to pave the way for regulated rural land transaction

The stock market staged a sharp rally following the rate cuts from

the PBoC and further easing expectations

1. Stock indices 2. Stock index vs money supply

Source: CEIC, HSBC Source: CEIC, HSBC

3. Price-to-earnings ratio 4. Market capitalisation, by stock exchange

Source: CEIC, HSBC Source: CEIC, HSBC

0

1,000

2,000

3,000

4,000

5,000

6,000

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Shanghai (SSE) Shenzhen (SZSE)

0

510

15

20

2530

35

40

-100

-50

0

50

100

150

200

250

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

SSE index (LHS) M1 (RHS)

%y oy %y oy

10

20

30

40

50

60

70

80

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

SSE SZSE

%

-

10,000

20,000

30,000

40,000

50,000

60,000

06 07 08 09 10 11 12 13 14

SSE SZSE

RMB bn

37

Macro China Economics 16 December 2014

abc

5. Capital raised, by stock exchange 6. Real estate index

Source: CEIC, HSBC Source: CEIC, HSBC

7. Property prices 8. Property sales vs money supply

Source: CEIC, HSBC Source: CEIC, HSBC

9. Property prices vs money supply 10. Property investment vs property started

Source: CEIC, HSBC Source: CEIC, HSBC

0

40

80

120

160

07 08 09 10 11 12 13 14

SSE SZSE

RMB bn

94

96

98

100

102

104

106

108

04 05 06 07 08 09 10 11 12 13 14

Real estate climate index

2000=100

-4-202468

101214

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Property price index

% y oy

051015202530354045

-200

20406080

100120140160

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Property sales (YTD, LHS) M1 (RHS)

% y oy % y oy

-1

0

1

2

3

4

5

-2

0

2

4

6

8

10

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Property price index (LHS) M1 (SA, RHS)

% mom % mom, 3mma

-40

-20

0

20

40

60

80

100

05 06 07 08 09 10 11 12 13 14

Property investment Floor space started

YTD, % y oy

38

Macro China Economics 16 December 2014

abc

This page intentionally left blank.

39

Macro China Economics 16 December 2014

abc

Data and forecasts

40

Macro China Economics 16 December 2014

abc

China Macro framework

2010 2011 2012 2013 2014f 2015f 2016f

Production, demand and employment GDP growth (% y-o-y) 10.4 9.3 7.7 7.7 7.5 7.3 7.4 Nominal GDP (USDbn) 5,938 7,323 8,283 9,265 10,232 11,012 11,901 GDP per capita (USD) 4,367 5,351 6,015 6,686 7,341 7,857 8,447 Nominal retail sales (% y-o-y) 18.5 17.1 14.3 13.1 12.8 13.2 13.2 Fixed asset investment (nominal, % y-o-y) 24.5 23.8 20.6 19.6 19.0 20.0 19.0 Industrial production (excl. small enterprises % y-o-y) -0.2 -0.4 1.0 0.3 0.5 0.6 0.6 Gross domestic saving (% GDP) 15.7 13.9 10.0 9.7 9.1 9.4 9.3 Unemployment rate, average (%) 51.8 50.9 50.5 50.2 49.6 49.0 48.4

Prices & wages CPI, average (% y-o-y) 3.3 5.4 2.7 2.6 2.4 1.8 1.9 CPI, end-year (% y-o-y) 4.6 4.1 2.5 2.9 2.7 2.1 2.2 PPI, end-year (% y-o-y) 5.9 1.7 1.9 -1.4 -1.0 -2.6 -1.8 Manufacturing wages, nominal (% y-o-y) 13.0 13.0 13.0 12.0 12.0 12.6 11.0

Money, FX & interest rates Central bank money M0, average (%) 12.1 16.0 9.6 9.4 6.0 7.0 6.0 Broad money supply M2, average (%) 23.7 16.4 13.4 14.8 13.5 12.0 12.0 Policy rate, end-year (%) 5.64 6.56 6.00 6.00 5.60 5.35 5.10 5yr yield, end-year (%) 6.16 6.90 6.40 6.40 3.58 3.20 4.00 RMB /USD, end-year 6.62 6.30 6.23 6.05 6.12 6.22 6.30 RMB /USD, average 6.76 6.46 6.27 6.14 6.12 6.21 6.29 RMB /EUR, end-year 8.87 8.17 8.22 8.34 7.65 7.15 7.06 RMB /EUR, average 8.92 8.93 8.10 8.12 8.19 7.41 7.12

External sector Merchandise exports (USDbn) 1,578 1,899 2,050 2,211 2,347 2,514 2,703 Merchandise imports (USDbn) 1,394 1,741 1,817 1,949 2,037 2,147 2,272 Trade balance (USDbn) 184.5 157.9 232.8 261.3 310.3 367.0 431.0 Current account balance (USDbn) 305 201 193 188 180 197 251 Current account balance (% GDP) 5.1 2.7 2.3 2.0 1.8 1.8 2.1 Net FDI (USDbn) 105.8 116.2 112.0 117.0 122.9 135.1 148.6 Net FDI (% GDP) 1.8 1.6 1.4 1.3 1.2 1.2 1.2 Current account balance plus FDI (% GDP) 6.9 4.3 3.7 3.3 3.0 3.0 3.4 Exports (% y-o-y) 31.4 20.3 7.9 7.8 6.2 7.1 7.5 Imports (% y-o-y) 38.6 24.9 4.4 7.3 4.5 5.4 5.8 International FX reserves (USDbn) 2,850 3,181 3,312 3,821 3,871 3,971 4,071 Import cover (months) 22.5 20.0 19.7 20.9 19.5 18.9 18.4

Public and external solvency indicators Commercial banks’ FX assets (USDbn) 128.1 147.5 167.3 187.7 N/A N/A N/A Gross external debt (USDbn) 548.9 695.0 737.0 830.9 950.9 1,070.9 1,190.9 Short-term external debt (% of int’l reserves) 13.2 15.7 16.3 16.8 18.9 20.4 21.9 Consolidated government balance (% GDP) -2.5 -1.1 -1.5 -1.9 -2.2 -2.5 -2.5

Source: HSBC

41

Macro China Economics 16 December 2014

abc

Notes

42

Macro China Economics 16 December 2014

abc

Disclosure appendix Analyst Certification The following analyst(s), economist(s), and/or strategist(s) who is(are) primarily responsible for this report, certifies(y) that the opinion(s) on the subject security(ies) or issuer(s) and/or any other views or forecasts expressed herein accurately reflect their personal view(s) and that no part of their compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report: Hongbin Qu, Julia Wang and Jing Li

Important Disclosures This document has been prepared and is being distributed by the Research Department of HSBC and is intended solely for the clients of HSBC and is not for publication to other persons, whether through the press or by other means.

This document is for information purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy the securities or other investment products mentioned in it and/or to participate in any trading strategy. Advice in this document is general and should not be construed as personal advice, given it has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Accordingly, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to their objectives, financial situation and needs. If necessary, seek professional investment and tax advice.

Certain investment products mentioned in this document may not be eligible for sale in some states or countries, and they may not be suitable for all types of investors. Investors should consult with their HSBC representative regarding the suitability of the investment products mentioned in this document and take into account their specific investment objectives, financial situation or particular needs before making a commitment to purchase investment products.

The value of and the income produced by the investment products mentioned in this document may fluctuate, so that an investor may get back less than originally invested. Certain high-volatility investments can be subject to sudden and large falls in value that could equal or exceed the amount invested. Value and income from investment products may be adversely affected by exchange rates, interest rates, or other factors. Past performance of a particular investment product is not indicative of future results.

HSBC and its affiliates will from time to time sell to and buy from customers the securities/instruments (including derivatives) of companies covered in HSBC Research on a principal or agency basis.

Analysts, economists, and strategists are paid in part by reference to the profitability of HSBC which includes investment banking revenues.

Whether, or in what time frame, an update of this analysis will be published is not determined in advance.

For disclosures in respect of any company mentioned in this report, please see the most recently published report on that company available at www.hsbcnet.com/research.

Additional disclosures 1 This report is dated as at 16 December 2014. 2 All market data included in this report are dated as at close 12 December 2014, unless otherwise indicated in the report. 3 HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its

Research business. HSBC’s analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC’s Investment Banking business. Information Barrier procedures are in place between the Investment Banking and Research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

43

Macro China Economics 16 December 2014

abc