macmahon holdings limited for personal use only

TRANSCRIPT

Macmahon Holdings Limited Full Year Results 2013

20 August 2013

For

per

sona

l use

onl

y

Mining focused strategy implemented with sale of construction business

effected in February

Consolidated net loss of $29.5 million greater than anticipated due to

provisions taken for disputed claims, doubtful debts and fixed asset

impairment

Net profit after tax of $43.6 million from continuing operations

Loss after tax of $73.1 million from discontinued construction business

Record mining revenue of ~$1.2 billion, profit before tax of $69.5 million

Strong cash flow from mining operations

Company’s largest ever contract award – 5 year, $1.8 billion Christmas

Creek Mine expansion

Order book of $3.2 billion, quality contracts with long-term blue-chip clients

Healthy balance sheet following $80.7 million equity raise – gearing at 15.4%

Business downsized – offices consolidated, support functions centralised,

cost savings achieved

Board renewal process commenced

2013 - Year in Review

2

645

466

674

880

1,173

2009 2010 2011 2012 2013

Mining revenue

Profit after tax from

continuing operations

528

1,530

1,079

1,968

3,167

2009 2010 2011 2012 2013

Mining order book

(4) 14

26

37

44

2009 2010 2011 2012 2013

For

per

sona

l use

onl

y

Awarded Macmahon’s largest mining contract in January 2013

• 5 year, $1.8 billion Christmas Creek Mine expansion

• Rapid ramp-up complete – 669 people on site, over 100 major items of

equipment commissioned

• Majority of equipment is client-owned – including the Komatsu 930E ultra-class

trucks. Macmahon capex ~$40 million

• Project remains LTI free

10 year, $900 million Tropicana Gold Project fully ramped up with third fleet

• 264 people on site

• Major equipment – 15 x 793 haul trucks, 4 x excavators, 3 x drill rigs

• Project remains LTI free

Record production at Orebody 18/Wheelara – extension discussions in advanced

stages

Operations at Eaglefield extended to Lenton pit following completion of Eaglefield

pit works – recorded six years LTI free

Completed works at Boddington Gold Mine, Orebody 24 and Area C

Operational Update – Surface Mining

3

For

per

sona

l use

onl

y

Operational Update – Underground Mining

Three year contract extension awarded at

Olympic Dam - 6th extension since first

contract award in 2004

Ranger 3 Deeps ramp-up complete, mine

decline progressing well – reaching 1,000

metres in July 2013

Argyle progressing on a reduced scope of

works

CSA Mine – settlement negotiations expected

to occur in early September

Completed development and production

works at Renison Tin Mine and raise drilling

works at Leinster and Ernest Henry

Shotcreting recorded six years LTI free

4

For

per

sona

l use

onl

y

Operational Update – International Ramp-up at Calabar, Nigeria progressing well

10 years of operation in South East Asia – one year extension awarded at Lhok Nga, Indonesia

Expansion opportunities with Lafarge being tendered in both Nigeria and Malaysia

Presence established in Ghana to pursue opportunities in Africa

Operations at Kanthan recorded 3,000 days LTI free, Ewekoro, Lhok Nga and Rawang recorded 1,000 days

LTI free, Calabar recorded one year LTI free

5

For

per

sona

l use

onl

y

Operational Update – Mongolia Mongolian coal industry stagnant due to lower coal prices being received from Chinese customers.

Production not at projected levels

Production at Tavan Tolgoi scaled back to match demand

ROM and border stockpiles full, with approximately 1.2 Mt of coal exposed in pit

Project remains LTI free

6

For

per

sona

l use

onl

y

Map of Operations

7

For

per

sona

l use

onl

y

People

679 employees transferred or made redundant

in sale of construction projects to Leighton

Group

Successful ramp-up for Christmas Creek and

Tropicana Gold Project complete – currently

933 people on site

Focus on right-sizing of organisation structure

– 65 corporate and mining overhead positions

made redundant

Centralised structure for functional services

adopted to increase efficiencies and reduce

duplication

Operator development program introduced at

Christmas Creek

Broad range of training opportunities provided

to staff

3,098 3,021

3,536

4,791

3,495

2009 2010 2011 2012 2013

Group employee numbers

Employee numbers by division

8

For

per

sona

l use

onl

y

• greater accountability at Executive level

• simplifying systems and processes

• bolstering education and training

• reaffirming safety focus

• striving for continuous improvement

Safety

Fatality recorded at CSA Mine Shaft in New South Wales

Kanthan, Malaysia recorded nine years LTI free

Eaglefield/Lenton and underground shotcreting operations recorded six years LTI free

3 day MacStart program launched – incorporates safety into all aspects of induction process

Safety improvement plan launched. Key initiatives include:

9

Safety performance

9

7.4

4.6 3.5

7.7 7.7

0.8 0.4 0.2 1.4 0.9

2009 2010 2011 2012 2013

Freq

uen

cy r

ate

(p

er m

illio

n h

ou

rs w

ork

ed)

TRIFR (Total Recordable Injury Frequency Rate)

LTIFR (Lost Time Injury Frequency Rate)

For

per

sona

l use

onl

y

Financials

For

per

sona

l use

onl

y

Income Statement

11

Note: Numbers in the table may not add due to rounding

$ millions 2013 2012 Change

Total revenue from continuing operations 1,173.4 880.1 33%

Earnings before interest and tax (EBIT) from continuing operations 84.5 62.6 35%

Interest (18.3) (13.3) 38%

Profit before tax from continuing operations 66.3 49.3 34%

Tax expense (22.7) (12.6) 80%

Profit after tax from continuing operations 43.6 36.7 19%

(Loss) / profit from discontinued operations (net of tax) (73.1) 19.3 (479%)

(Loss) / profit for the period attributable to equity holders of the Company (29.5) 56.1 (153%)

Profit after tax margin from continuing operations 3.7% 4.2%

Earnings per share – continuing operations (cents) 4.37 5.04 (13%)

(Loss)/earnings per share – consolidated (cents) (2.96) 7.68 (139%)

Dividends declared per share (cents) nil 4.0

For

per

sona

l use

onl

y

Profit Waterfall

12

$ million

12

56.1 36.7

(19.3) 24.1 19.8

(7.2) (19.7) (10.1)

(73.1)

43.6

(29.5)

-30.0-20.0-10.0

0.010.020.030.040.050.060.070.0

20

12

NP

AT

20

12

NP

AT

fro

md

isco

nti

nu

ed

op

erat

ion

s

20

12

NP

AT

fro

mco

nti

nu

ing

op

era

tio

ns

Min

ing

- V

olu

me

Min

ing

- M

argi

n

Pro

visi

on

s an

dim

pai

rme

nt

Co

rpo

rate

co

sts

Tax

20

13

NP

AT

fro

mco

nti

nu

ing

op

era

tio

ns

20

13

NP

AT

fro

md

isco

nti

nu

ed

op

erat

ion

s

20

13

NP

AT

Note: Numbers may not add due to rounding

For

per

sona

l use

onl

y

Mining Performance

13

Record revenue of $1.2 billion (up 33% on pcp)

following the commencement of mining operations

at Tropicana Gold Project and Christmas Creek

Mine expansion

Profit before tax of $69.5 million (down 4% on pcp)

Profit before tax margin lower due to provisions for

disputed claims recognised in 2013

Record order book of $3.2 billion following award of

$1.8 billion Christmas Creek contract

Capex increased to $197 million including ~$80

million for Tropicana and Christmas Creek

$ millions 2013 2012 Change

Segment revenue 1,173.4 880.1 33%

Profit before tax 69.5 72.3 (4%)

Profit before tax margin % 5.9 8.2

Order book 3,167 1,968 61%

Capex 197 134 47%

Revenue ($ million) and PBT margin

645

466

674

880

1,173

1.8%

7.5%

6.3%

8.2% 5.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

-

200

400

600

800

1,000

1,200

1,400

2009 2010 2011 2012 2013

For

per

sona

l use

onl

y

Full year loss before tax of $126.0 million mainly attributable to Hope Downs 4, Solomon Rail Spur and

Urban Superway

Project completion and closure costs provisioned for in 2013 – no material impacts expected in 2014

Sale of majority of construction projects to Leighton Group approved by shareholders at EGM in

February 2013

Sale of Macmahon Rail assets to McConnell Dowell completed in May 2013

Sale proceeds of $33.6 million received, after tax profit on sale of $15.5 million

Majority of projects completed or novated

Construction fleet – $31.7 million transferred to mining, $22.4 million sold, $6.3 million remains held for

sale (net of impairment provision)

Exit from Construction – Discontinued Operations

$ millions 2013 2012

Segment revenue 581.7 990.7

(Loss) / profit before tax (126.0) 25.9

(Loss) / profit after tax (73.1) 19.3

Order book 63 1,171

14

For

per

sona

l use

onl

y

1. Includes $22.4 million for sale of construction assets and $36.8 million for sale and lease back of equipment

2. Excludes $9.3 million of plant and equipment acquired under finance leases and hire purchase (2012:$1.1 million)

Cash Flow

15

Operating cash flow increased due to approximately $60 million of debtors due in June 2012 paid in

early July 2012

Strong underlying cash flow from continuing mining operations of $117.9 million

Capital expenditure increased to $201.7 million in line with scheduled ramp-up at Tropicana and

Christmas Creek

$ millions 2013 2012 Change

EBITDA 67.5 167.8 (60%)

Net interest paid (18.8) (9.2) 104%

Income tax (paid) / refund (9.6) (4.8) 100%

Working capital and provisions 69.5 (67.0) 204%

Operating cash flow 108.6 86.8 25%

Proceeds from sale of assets 59.11 7.2 721%

Capital expenditure2 201.7 186.4 8%

Equity raising and DRP 83.4 -

Dividend paid (18.3) (10.9)

Cash on hand 153.5 134.9 14%

For

per

sona

l use

onl

y

Balance sheet strengthened following $80.7 million equity raising

Gearing 15.4% - expected to modestly increase in the short-term due mainly to final equipment purchases

for Tropicana

Capital investment programme will be managed tightly in market with ample equipment available

Bank guarantee lines reduced by $40.5 million with further reductions expected as construction projects are

completed or transferred. Syndicated bank facility now $434.5 million

Substantial facilities headroom available

Balance Sheet and Gearing

16

$ millions 2013 2012 Change

Current assets 435.3 528.9 (18%)

Non-current assets 509.2 460.1 11%

Total assets 944.5 989.0 (4%)

Net assets 401.2 356.8 12%

Net debt/(cash) 61.7 82.6 (25%)

Gearing (%) 15.4 23.1

0.6%

-12.9% -12.2%

23.1%

15.4%

Jun-09 Jun-10 Jun-11 Jun-12 Jun-13

Gearing

For

per

sona

l use

onl

y

Outlook F

or p

erso

nal u

se o

nly

Strategy

Refine core competencies

18

Strengthening our position as a leading provider of end-to-end mining services

Mining focused strategy (exit

construction sector)

End-to-end service model

– Surface Mining

– Underground Mining

– Engineering

– Infrastructure Services

– Plant and Maintenance

Diversification through geography,

commodity and service delivery

Focus on business fundamentals

Achieve sustainable growth

Extend existing mining contracts

Maximise asset utilisation

Deliver productivity and efficiency

gains through business

improvement

Strengthen business development

capability

Drive safety improvements

through education and training

Lift Indigenous participation

Maintain strong, long-term

relationships with blue-chip

clients

Pursue offshore opportunities

focusing on West Africa and Asia

Pursue growth in a controlled

and sustainable manner within

gearing limits

Deliver consistent and

sustainable returns for

Shareholders

18

For

per

sona

l use

onl

y

Ross Carroll

Chief Executive Officer and

Managing Director

Theresa Mlikota

Chief Financial Officer

Fraser Ramsay

Chief Operating Officer

Surface Mining and Infrastructure

Nick Cernotta

Chief Operating Officer

Underground Mining International and

Engineering

Robert Barker

Group General Manager

Market Development

David Todd

General Manager

HSEQ

Roger Hughes

Acting General Manager

Human Resources

New Management Team

19 19

Greg Miller Executive General

Manager

Underground Mining

For

per

sona

l use

onl

y

Market Conditions

20

Production of major commodities expected to

increase despite expected reduction in short-term

investment

Declining market conditions and downward

pressure on commodity prices have resulted in a

reduced domestic tendering pipeline and greater

competition for work

Offshore growth opportunities remain – regional

hubs established in Africa, South East Asia and

Central Asia to pursue new work

Increased availability of gear, tyres and people

Tendering pipeline of $3.9 billion (75% domestic,

25% international) Gold Production and Investment, Australia

Iron Ore Production and Investment, Australia

Coal Production and Investment, Australia

Source: BREE, BIS Shrapnel

For

per

sona

l use

onl

y

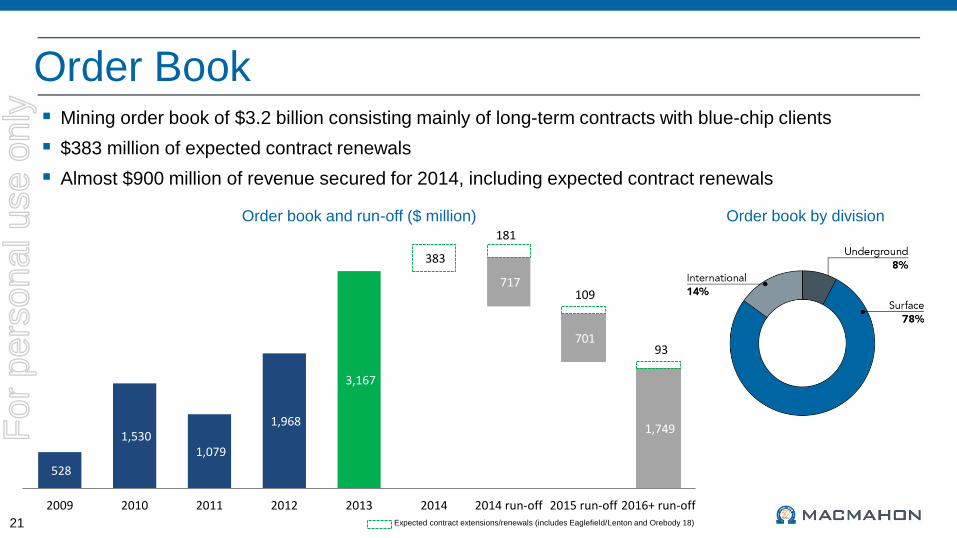

Expected contract extensions/renewals (includes Eaglefield/Lenton and Orebody 18)

Order Book

21

Mining order book of $3.2 billion consisting mainly of long-term contracts with blue-chip clients

$383 million of expected contract renewals

Almost $900 million of revenue secured for 2014, including expected contract renewals

Order book by division Order book and run-off ($ million)

528

1,530 1,079

1,968

3,167 2,683

2,651

1,749 1,749

383

701 93

717 109

181

2009 2010 2011 2012 2013 2014 2014 run-off 2015 run-off 2016+ run-off

For

per

sona

l use

onl

y

Business Outlook

22

Revenue outlook for 2014 expected to be in the range of $0.9 – 1.2 billion,

but remains at risk:

• Fewer new work opportunities

• Scope reductions and contract deferrals by customers

• Significant increase in competition

Margin pressure expected to continue

Focus on business improvement program including:

• Right-sizing the business

• Asset utilisation

• Cost reduction

• Supply contract renewal

Balance sheet and covenant management also a key focus:

• Capex will be managed downwards through utilisation of existing

capacity and low cost rental/lease options to $100 – 150 million

For

per

sona

l use

onl

y

Summary

For

per

sona

l use

onl

y

Summary 50 years of operation

Consolidated net loss of $29.5 million resulting from major construction losses

Record mining revenue and strong historical financial performance

Strong operating cash flow from mining operations - $117.9 million

Solid order book of $3.2 billion, backed by quality contracts with long-term blue-chip clients

Forecast $0.9 – 1.2 billion for 2014 revenue, but remains at risk

Sale of construction effected, removing significant uncertainty, risk and volatility

Healthy balance sheet and gearing (15.4% net debt to equity) following completion of $80.7 million

equity raising. Balance sheet management a priority

Significant cost savings achieved and continued focus on further reductions

Business development and margin improvement a priority to deliver consistent quality earnings and

increased returns to shareholders

24 24

For

per

sona

l use

onl

y

Macmahon Holdings Limited Full Year Results 2013

20 August 2013

For

per

sona

l use

onl

y

Construction Sale

26

$ millions Construction sale Rail assets sale Total

Contract consideration 22.2 - 22.2

Sale of assets 15.6 4.5 20.1

Employee entitlements transferred (4.8) (0.1) (4.9)

Working capital adjustments (4.0) 0.2 (3.8)

Total consideration 29.0 4.6 33.6

For

per

sona

l use

onl

y

Normalisation of 2013 Operating Cash Flow

27

$ millions Discontinued

operations

Continuing

operations Total

Operating cash flow (9.3) 117.9 108.6

Delayed 2012 debtors collected in 2013 (57.0) (7.0) (64.0)

Delayed 2013 debtors - 12.0 12.0

Other (5.4) - (5.4)

Normalised 2013 operating cash flow (71.7) 122.9 51.2

For

per

sona

l use

onl

y

Major Projects

28

Project Value Started

Christmas Creek (WA) $1.8 billion 2012

Orebody 18 / Wheelara (WA) $975 million 2006

Tropicana Project (WA) $900 million 2012

Eaglefield / Lenton (QLD) $550 million 2003

Olympic Dam (SA) $687 million 2004

Argyle Mine (WA) $376 million 2006

Tavan Tolgoi (Mongolia) US$250 million 2012

Calabar Quarry (Nigeria) US$126 million 2012 For

per

sona

l use

onl

y

Revenue and Order Book Diversity

29

2013 revenue by client 2013 revenue by commodity 2013 revenue by location

Order book by location Order book by client Order book by commodity

Note: Revenue and order book information presented on this page relates to mining activities only and excludes construction revenue and order book

For

per

sona

l use

onl

y

Disclaimer and Important Notice

30

This presentation contains forward looking statements that are subject to risk factors associated with the

mining and construction businesses. While Macmahon considers the assumptions on which these statements

are based to be reasonable, whether circumstances actually occur in accordance with these statements may

be affected by a variety of factors. These include, but are not limited to, levels of actual demand, currency

fluctuations, loss of market, industry competition, environmental risks, physical risks, legislative, fiscal and

regulatory developments, economic and financial market conditions in various countries and regions, political

risks, project delay or advancement, approvals and cost estimates. These could cause actual trends or results

to differ from the forward looking statements in this presentation.

All references to dollars, cents or $ in this presentation are to Australian currency, unless otherwise stated.

References to “Macmahon”, “the Company”, “the Group” or “the Macmahon Group” may be references to

Macmahon Holdings Ltd or its subsidiaries.

For

per

sona

l use

onl

y

Macmahon Holdings Limited Full Year Results 2013

20 August 2013

For

per

sona

l use

onl

y