m&a review - bvd · shopping and product recommendation application developer my genius. other...

TRANSCRIPT

M&A Review

France

March 2017

Zephyr Quarterly M&A ReportGlobal, Q3 2015

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 1 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

The following report details completed mergers and acquisitions activity in France in March 2017 using data from the Zephyr database.

It focuses on global deals activity by target company

Click here to access the raw data in an Excel spreadsheet.

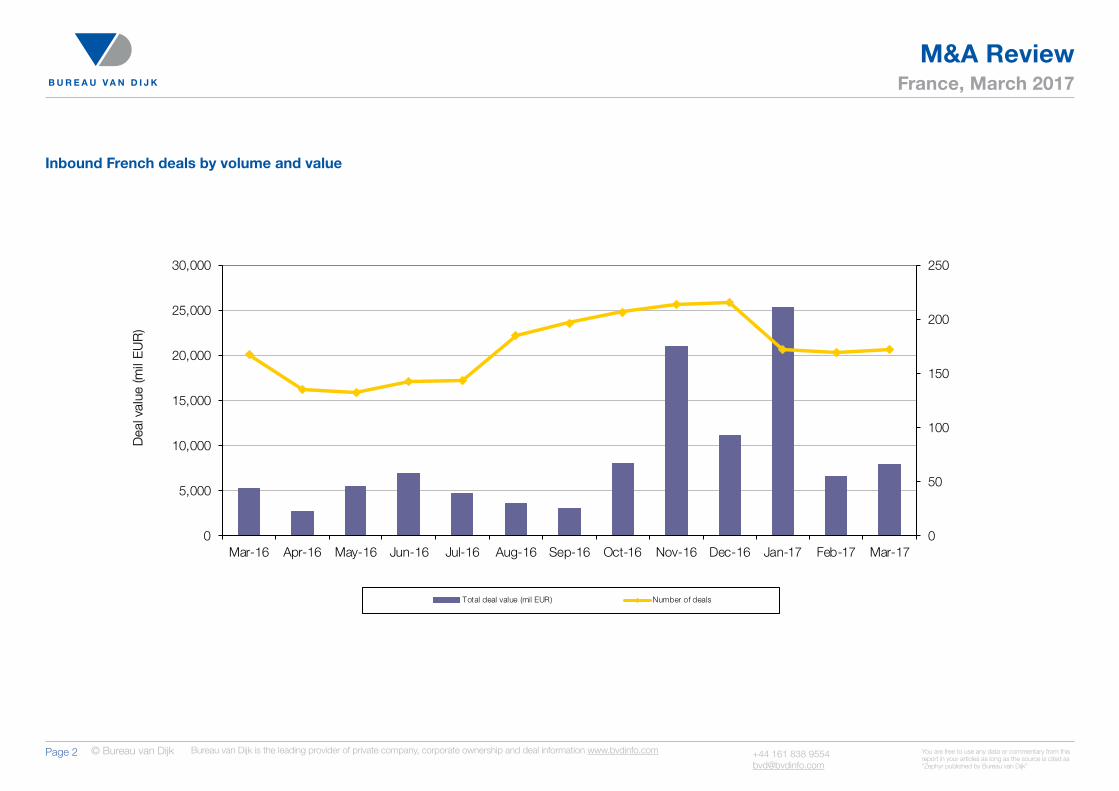

Inbound French M&A volume and value rises month-on-month

Inbound mergers and acquisitions (M&A) targeting French companies increased in March to 173 deals worth a combined EUR 7,986 million, from 170 deals worth EUR 6,635 million in February.

US-based companies were the main acquirors of French companies in March (49 deals totalling EUR 1,314 million). UK acquirors were second by volume (24 deals) but only third by value (EUR 197 million) as Spanish buyers completed one deal worth EUR 450 million.

Electricite de France’s EUR 4,018 million-rights issue was the month’s largest inbound deal, followed by the acquisition of an additional 10 per cent stake in Holding d’Infrastructures de Transport by Abertis Infraestructuras for EUR 450 million.

The gas, water and electricity sector was the most valuable in March with EUR 3,818 million, followed by chemicals, rubber and plastics with EUR 925 million, construction (EUR 451 million) and machinery, equipment, furniture and recycling (EUR 412 million).

Inbound French deals by volume and value

Completed date No of deals Total deal value (mil EUR)

Mar-17 173 7,986

Feb-17 170 6,635

Jan-17 173 25,389

Dec-16 216 11,148

Nov-16 214 21,054

Oct-16 207 8,031

Sep-16 197 3,076

Aug-16 186 3,606

Jul-16 144 4,761

Jun-16 143 6,904

May-16 133 5,520

Apr-16 136 2,674

Mar-16 168 5,305

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

The most comprehensive deal database

The world’s most powerful comparable data resource on private companies

Combining deal and company dataWelcome to the business of certainty.

We capture and treat private company and M&A information for better decision making and increased efficiency.

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 2 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Inbound French deals by volume and value

0

50

100

150

200

250

0

5,000

10,000

15,000

20,000

25,000

30,000

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

Dea

l val

ue (m

il E

UR

)

Total deal value (mil EUR) Number of deals

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 3 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top 20 inbound French deals by value

Deal value (mil EUR) Deal type Target Target

country Acquiror Acquiror country

Completion date

1. 4,018 Capital Increase 23% Electricite de France SA FR 30/03/2017

2. 450 Acquisition increased from 63% to 73% Holding d'Infrastructures de Transport SAS FR Abertis Infraestructuras SA ES 29/03/2017

3. 398 Capital Increase 91% Solocal Group SA FR 13/03/2017

4. 328 Minority stake 10% Spie Operations SA FR 14/03/2017

5 191 Acquisition 100% Bi-Sam Technologies SA FR FactSet Research Systems Inc. US 20/03/2017

6 186 Minority stake 15% Maisons du Monde SAS FR 14/03/2017

7 144 Minority stake increased to 5% Sanofi SA FR BlackRock Inc. US 20/03/2017

8 135 Minority stake Sanofi SA FR 17/03/2017

9 118 Minority stake Total SA FR 15/03/2017

10 116 Minority stake increased to 5% Sanofi SA FR BlackRock Inc. US 14/03/2017

11 113 Minority stake increased to 5% Total SA FR BlackRock Inc. US 21/03/2017

12 110 Minority stake increased from 4% to 5% Accor SA FR Franklin Resources Inc. US 03/03/2017

13 95 Minority stake Sanofi SA FR 24/03/2017

14 82 Minority stake increased to 5% Sanofi SA FR BlackRock Inc. US 27/03/2017

15 78 Minority stake increased to 5% Sanofi SA FR BlackRock Inc. US 08/03/2017

16 69 Minority stake increased to 6% AXA SA FR BlackRock Inc. US 24/03/2017

17 67 Minority stake increased 5% to 6% Societe Generale FR BlackRock Inc. US 09/03/2017

18 61 Minority stake Sanofi SA FR 09/03/2017

19 52 Minority stake Valeo SA FR 14/03/2017

20 50 Minority stake increased to 5% Safran SA FR BlackRock Inc. US 13/03/2017

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 4 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Inbound French target sectors by volume

Target sector Mar-16 Feb-17 Mar-17

Other services 59 52 42

Machinery, equipment, furniture, recycling 36 19 30

Chemicals, rubber, plastics 11 21 27

Metals & metal products 19 30 26

Wholesale & retail trade 15 5 16

Transport 11 14 13

Publishing, printing 0 5 5

Primary sector 1 2 3

Insurance companies 3 6 3

Banks 0 4 2

Hotels & restaurants 2 2 2

Construction 2 2 2

Food, beverages, tobacco 3 5 1

Gas, water, electricity 0 1 1

Education, health 0 0 0

Post and telecommunications 4 1 0

Wood, cork, paper 1 1 0

Textiles, wearing apparel, leather 1 0 0

Public administration and defence 0 0 0

Inbound French target sectors by value

Target sector Mar-16 (mil EUR)

Feb-17 (mil EUR)

Mar-17 (mil EUR)

Gas, water, electricity 0 1 3,818

Other services 1,972 1,275 1,165

Chemicals, rubber, plastics 1,310 1,297 925

Construction 224 133 451

Machinery, equipment, furniture, recycling 502 309 412

Wholesale & retail trade 613 1,125 283

Primary sector 6 626 276

Publishing, printing 0 211 194

Hotels & restaurants 326 33 121

Insurance companies 81 122 109

Metals & metal products 48 96 72

Banks 0 393 67

Transport 41 53 67

Food, beverages, tobacco 139 265 25

Education, health 0 0 0

Post and telecommunications 43 697 0

Textiles, wearing apparel, leather 0 0 0

Wood, cork, paper 0 0 0

Public administration and defence 0 0 0

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 5 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top inbound French acquiror countries by volume

Acquiror country Mar-16 Feb-17 Mar-17

US 19 55 49

UK 27 29 24

Poland 0 0 2

Norway 0 0 2

Germany 0 1 2

Switzerland 0 1 1

Sweden 0 0 1

Gibraltar 0 0 1

Japan 1 1 1

Luxembourg 0 2 1

Spain 0 1 1

Top inbound French acquiror countries by by value

Acquiror country Mar-16 (mil EUR)

Feb-17 (mil EUR)

Mar-17 (mil EUR)

US 1,209 2,753 1,314

Spain 0 0 450

UK 1,741 1,098 197

Norway 0 0 27

Japan 0 0 24

Germany 0 185 17

Sweden 0 0 5

Poland 0 0 4

Gibraltar 0 0 4

Luxembourg 0 29 3

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 6 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Inbound French private equity deals by volume and value

Completed date No of deals Total deal value (mil EUR)

Mar-17 5 2

Feb-17 5 272

Jan-17 6 2,929

Dec-16 9 39

Nov-16 6 787

Oct-16 9 273

Sep-16 9 119

Aug-16 4 19

Jul-16 6 84

Jun-16 9 137

May-16 5 4

Apr-16 0 0

Mar-16 6 1,004

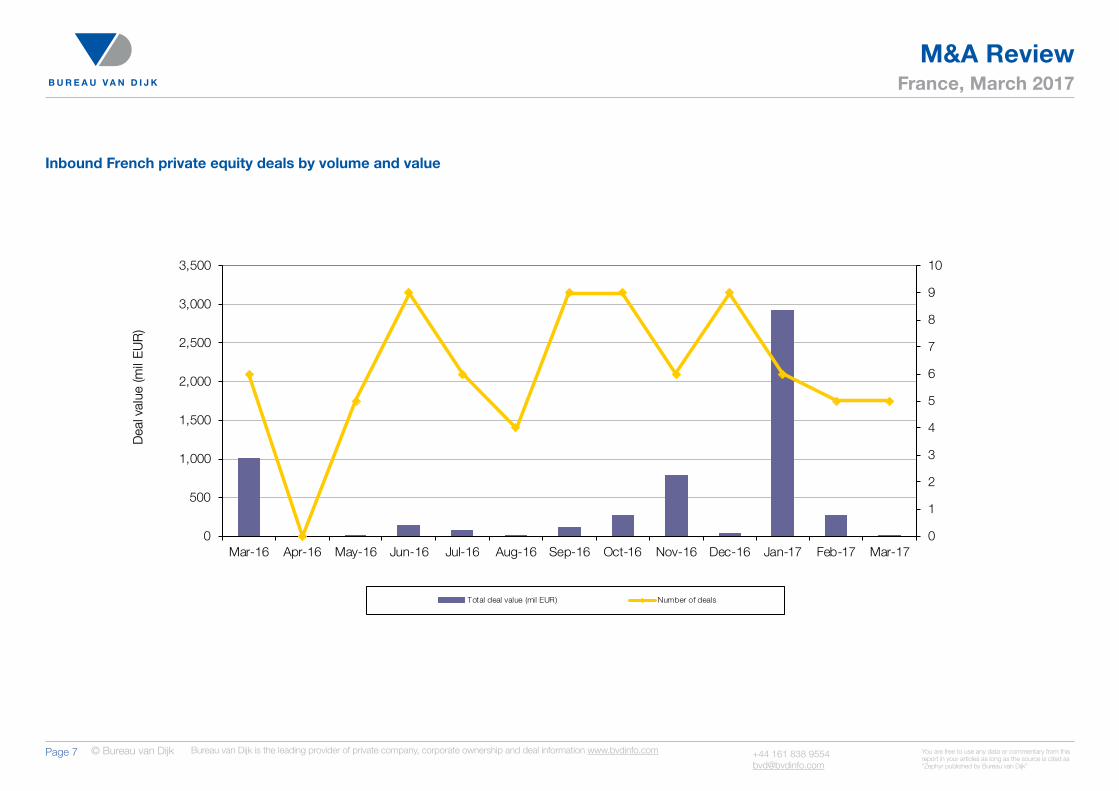

Inbound PE and VC value at 11-month low

The value of inbound private equity and venture capital (PE and VC) investment in French companies reached an 11-month low in March as 5 deals worth a combined EUR 2 million were completed during the four weeks. In terms of volume, results were unchanged month-on-month; however, there was a significant decrease by value from EUR 272 million invested in February.

Year-on-year the decline was more notable as volume fell by 17 per cent, while value was stripped away from EUR 1,004 million recorded in March 2016, which represented the second largest period of the last 12 months under review (January: EUR 2,929 million).

The significant decline can be attributed to the lack of high valued deals in March as only one inbound French PE and VC deal had a disclosed value in the four weeks under review and took the form of a EUR 2 million funding round by mobile collaborative shopping and product recommendation application developer My Genius.

Other targets included GE Money Bank, Primonial Holding, Geomedia and Charvet Groupe.

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 7 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Inbound French private equity deals by volume and value

0

1

2

3

4

5

6

7

8

9

10

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

Dea

l val

ue (m

il E

UR

)

Total deal value (mil EUR) Number of deals

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 8 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top inbound French private equity deals by value

Deal value (mil EUR) Deal type Target Target

country General Partner/Fund Manager Completion date

1. 2 Minority stake My Genius SAS FR 02/03/2017

2. n.a. IBO 100% GE Money Bank SCA; GE Money Bank SCA's French Overseas Territories-based operations FR; FR Cerberus Capital Management LP 28/03/2017

3. n.a. IBO 53% Primonial Holding SAS FR Bridgepoint Advisers Ltd 09/03/2017

4. n.a. IBO majority stake Geomedia SAS FR Atalante SAS 07/03/2017

5. n.a. MBI 100% Charvet Groupe RGF FR Omnes Capital SA 30/03/2017

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 9 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

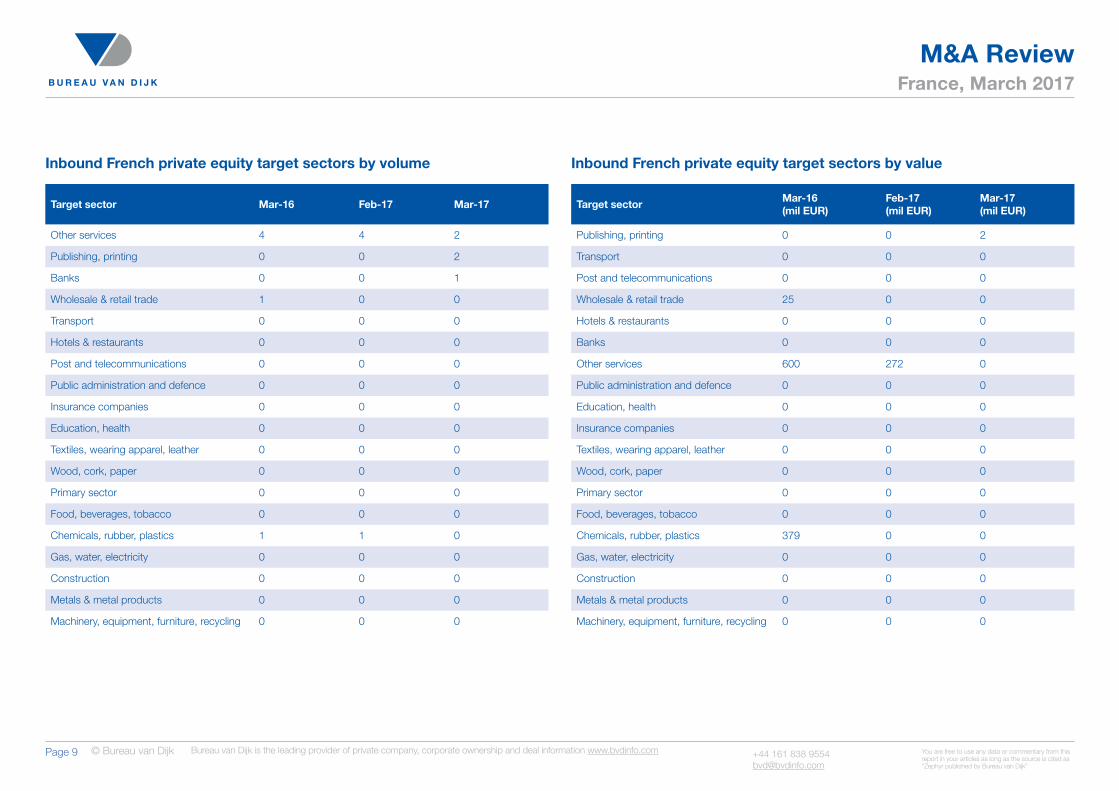

Inbound French private equity target sectors by volume

Target sector Mar-16 Feb-17 Mar-17

Other services 4 4 2

Publishing, printing 0 0 2

Banks 0 0 1

Wholesale & retail trade 1 0 0

Transport 0 0 0

Hotels & restaurants 0 0 0

Post and telecommunications 0 0 0

Public administration and defence 0 0 0

Insurance companies 0 0 0

Education, health 0 0 0

Textiles, wearing apparel, leather 0 0 0

Wood, cork, paper 0 0 0

Primary sector 0 0 0

Food, beverages, tobacco 0 0 0

Chemicals, rubber, plastics 1 1 0

Gas, water, electricity 0 0 0

Construction 0 0 0

Metals & metal products 0 0 0

Machinery, equipment, furniture, recycling 0 0 0

Inbound French private equity target sectors by value

Target sector Mar-16 (mil EUR)

Feb-17 (mil EUR)

Mar-17 (mil EUR)

Publishing, printing 0 0 2

Transport 0 0 0

Post and telecommunications 0 0 0

Wholesale & retail trade 25 0 0

Hotels & restaurants 0 0 0

Banks 0 0 0

Other services 600 272 0

Public administration and defence 0 0 0

Education, health 0 0 0

Insurance companies 0 0 0

Textiles, wearing apparel, leather 0 0 0

Wood, cork, paper 0 0 0

Primary sector 0 0 0

Food, beverages, tobacco 0 0 0

Chemicals, rubber, plastics 379 0 0

Gas, water, electricity 0 0 0

Construction 0 0 0

Metals & metal products 0 0 0

Machinery, equipment, furniture, recycling 0 0 0

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 10 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top inbound French private equity acquiror countries by volume

Acquiror country Mar-16 Feb-17 Mar-17

US 3 1 1

UK 2 0 1

Top inbound French private equity acquiror countries by value

Acquiror country Mar-16 (mil EUR)

Feb-17 (mil EUR)

Mar-17 (mil EUR)

US 979 260 0

UK 600 0 0

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 11 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

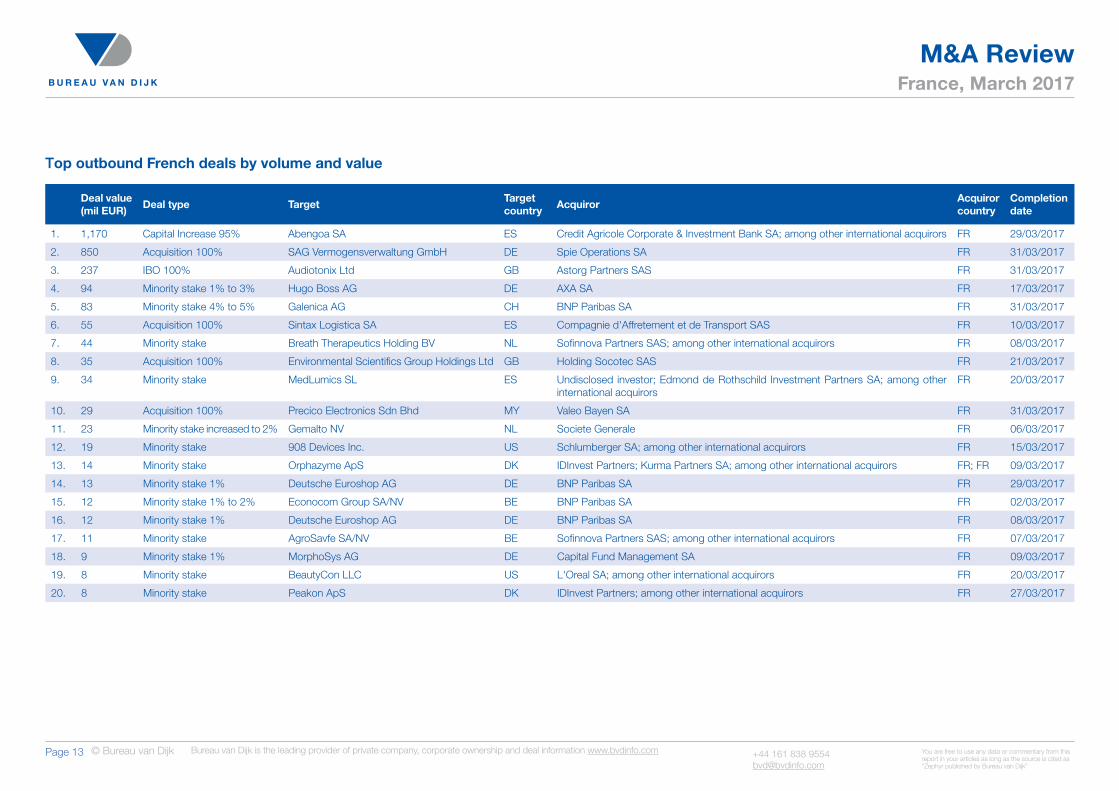

Outbound M&A up in March, due to increased Spanish investment

Outbound M&A by French acquirors reversed declines recorded in January and February as volume improved 16 per cent while value increased 72 per cent over the four weeks. There were 64 deals worth an aggregate EUR 2,791 million in March, compared to 55 deals worth EUR 1,619 million in February (January: 55 deals worth EUR 2,274 million).

On a 12-month comparison volume and value improved 23 per cent and 7 per cent, respectively, from 52 deals worth EUR 2,602 million in March 2016.

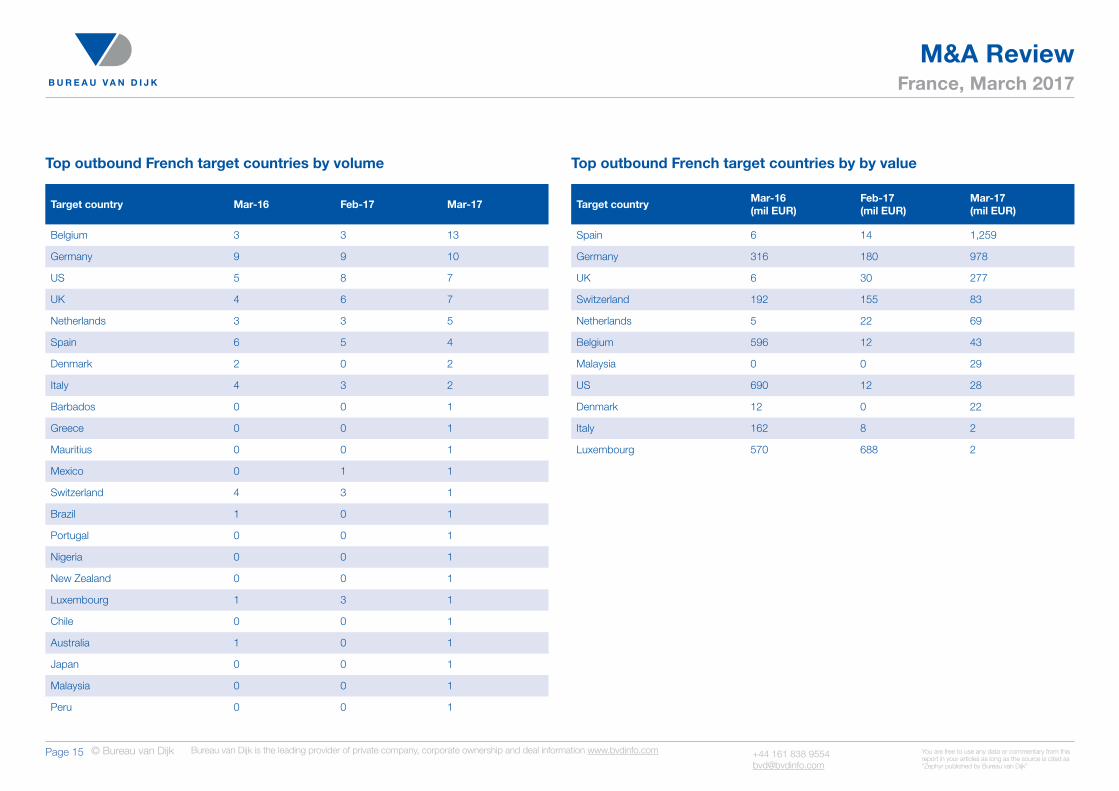

The increase by value over the four weeks can be largely attributed to one deal worth EUR 1,170 million, which was the only deal to exceed EUR 1,000 million during the month under review and represented 42 per cent of total value. The largest outbound M&A transaction by a French acquiror involved Spanish energy and agricultural group Abengoa raising EUR 1,170 million through a debt restructuring process which involved French corporate banking group Credit Agricole Corporate & Investment Bank, as well as other investors such as DE Shaw & Company, HSBC Holdings and Elliott Management.

This deal was followed by French civil engineering and building construction group Spie Operations buying German power infrastructure utility SAG Vermogensverwaltung for EUR 850 million.

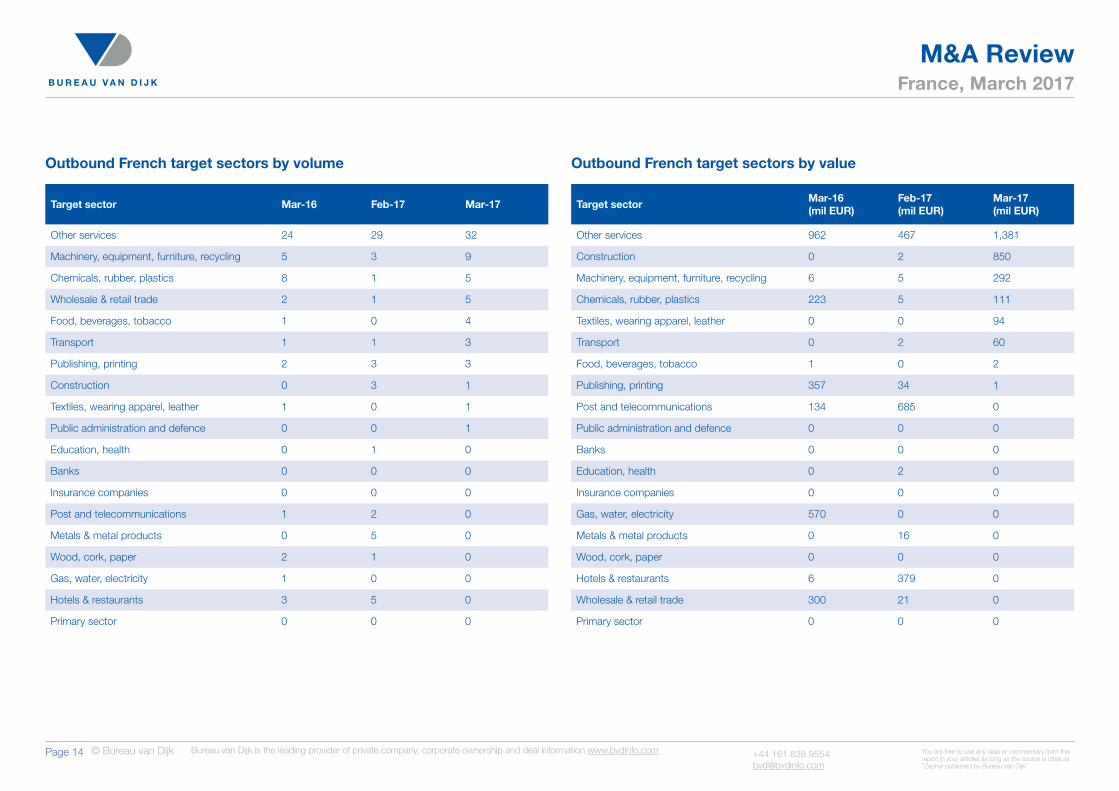

As a result of the top deal by value French outbound M&A favoured companies based in Spain with EUR 1,259 million, the majority of which can be attributed to the Abengoa deal. Germany, the UK, Switzerland and the Netherlands all followed with EUR 978 million, EUR 277 million, EUR 83 million and EUR 69 million, respectively, suggesting buyers favoured companies based in Europe in March.

Outbound French deals by volume and value

Completed date No of deals Total deal value (mil EUR)

Mar-17 64 2,791

Feb-17 55 1,619

Jan-17 55 2,274

Dec-16 68 7,559

Nov-16 54 2,674

Oct-16 52 5,340

Sep-16 66 5,941

Aug-16 37 1,670

Jul-16 106 4,522

Jun-16 76 2,376

May-16 52 12,853

Apr-16 48 1,354

Mar-16 52 2,602

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 12 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Outbound French deals by volume and value

0

20

40

60

80

100

120

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

Dea

l val

ue (m

il E

UR

)

Total deal value (mil EUR) Number of deals

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 13 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top outbound French deals by volume and value

Deal value (mil EUR) Deal type Target Target

country Acquiror Acquiror country

Completion date

1. 1,170 Capital Increase 95% Abengoa SA ES Credit Agricole Corporate & Investment Bank SA; among other international acquirors FR 29/03/2017

2. 850 Acquisition 100% SAG Vermogensverwaltung GmbH DE Spie Operations SA FR 31/03/2017

3. 237 IBO 100% Audiotonix Ltd GB Astorg Partners SAS FR 31/03/2017

4. 94 Minority stake 1% to 3% Hugo Boss AG DE AXA SA FR 17/03/2017

5. 83 Minority stake 4% to 5% Galenica AG CH BNP Paribas SA FR 31/03/2017

6. 55 Acquisition 100% Sintax Logistica SA ES Compagnie d'Affretement et de Transport SAS FR 10/03/2017

7. 44 Minority stake Breath Therapeutics Holding BV NL Sofinnova Partners SAS; among other international acquirors FR 08/03/2017

8. 35 Acquisition 100% Environmental Scientifics Group Holdings Ltd GB Holding Socotec SAS FR 21/03/2017

9. 34 Minority stake MedLumics SL ES Undisclosed investor; Edmond de Rothschild Investment Partners SA; among other international acquirors

FR 20/03/2017

10. 29 Acquisition 100% Precico Electronics Sdn Bhd MY Valeo Bayen SA FR 31/03/2017

11. 23 Minority stake increased to 2% Gemalto NV NL Societe Generale FR 06/03/2017

12. 19 Minority stake 908 Devices Inc. US Schlumberger SA; among other international acquirors FR 15/03/2017

13. 14 Minority stake Orphazyme ApS DK IDInvest Partners; Kurma Partners SA; among other international acquirors FR; FR 09/03/2017

14. 13 Minority stake 1% Deutsche Euroshop AG DE BNP Paribas SA FR 29/03/2017

15. 12 Minority stake 1% to 2% Econocom Group SA/NV BE BNP Paribas SA FR 02/03/2017

16. 12 Minority stake 1% Deutsche Euroshop AG DE BNP Paribas SA FR 08/03/2017

17. 11 Minority stake AgroSavfe SA/NV BE Sofinnova Partners SAS; among other international acquirors FR 07/03/2017

18. 9 Minority stake 1% MorphoSys AG DE Capital Fund Management SA FR 09/03/2017

19. 8 Minority stake BeautyCon LLC US L'Oreal SA; among other international acquirors FR 20/03/2017

20. 8 Minority stake Peakon ApS DK IDInvest Partners; among other international acquirors FR 27/03/2017

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 14 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Outbound French target sectors by volume

Target sector Mar-16 Feb-17 Mar-17

Other services 24 29 32

Machinery, equipment, furniture, recycling 5 3 9

Chemicals, rubber, plastics 8 1 5

Wholesale & retail trade 2 1 5

Food, beverages, tobacco 1 0 4

Transport 1 1 3

Publishing, printing 2 3 3

Construction 0 3 1

Textiles, wearing apparel, leather 1 0 1

Public administration and defence 0 0 1

Education, health 0 1 0

Banks 0 0 0

Insurance companies 0 0 0

Post and telecommunications 1 2 0

Metals & metal products 0 5 0

Wood, cork, paper 2 1 0

Gas, water, electricity 1 0 0

Hotels & restaurants 3 5 0

Primary sector 0 0 0

Outbound French target sectors by value

Target sector Mar-16 (mil EUR)

Feb-17 (mil EUR)

Mar-17 (mil EUR)

Other services 962 467 1,381

Construction 0 2 850

Machinery, equipment, furniture, recycling 6 5 292

Chemicals, rubber, plastics 223 5 111

Textiles, wearing apparel, leather 0 0 94

Transport 0 2 60

Food, beverages, tobacco 1 0 2

Publishing, printing 357 34 1

Post and telecommunications 134 685 0

Public administration and defence 0 0 0

Banks 0 0 0

Education, health 0 2 0

Insurance companies 0 0 0

Gas, water, electricity 570 0 0

Metals & metal products 0 16 0

Wood, cork, paper 0 0 0

Hotels & restaurants 6 379 0

Wholesale & retail trade 300 21 0

Primary sector 0 0 0

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 15 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top outbound French target countries by volume

Target country Mar-16 Feb-17 Mar-17

Belgium 3 3 13

Germany 9 9 10

US 5 8 7

UK 4 6 7

Netherlands 3 3 5

Spain 6 5 4

Denmark 2 0 2

Italy 4 3 2

Barbados 0 0 1

Greece 0 0 1

Mauritius 0 0 1

Mexico 0 1 1

Switzerland 4 3 1

Brazil 1 0 1

Portugal 0 0 1

Nigeria 0 0 1

New Zealand 0 0 1

Luxembourg 1 3 1

Chile 0 0 1

Australia 1 0 1

Japan 0 0 1

Malaysia 0 0 1

Peru 0 0 1

Top outbound French target countries by by value

Target country Mar-16 (mil EUR)

Feb-17 (mil EUR)

Mar-17 (mil EUR)

Spain 6 14 1,259

Germany 316 180 978

UK 6 30 277

Switzerland 192 155 83

Netherlands 5 22 69

Belgium 596 12 43

Malaysia 0 0 29

US 690 12 28

Denmark 12 0 22

Italy 162 8 2

Luxembourg 570 688 2

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 16 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Outbound French private equity deals by volume and value

Completed date No of deals Total deal value (mil EUR)

Mar-17 9 376

Feb-17 14 428

Jan-17 14 80

Dec-16 7 103

Nov-16 6 83

Oct-16 4 711

Sep-16 15 269

Aug-16 9 211

Jul-16 15 481

Jun-16 18 1,298

May-16 17 359

Apr-16 17 282

Mar-16 13 925

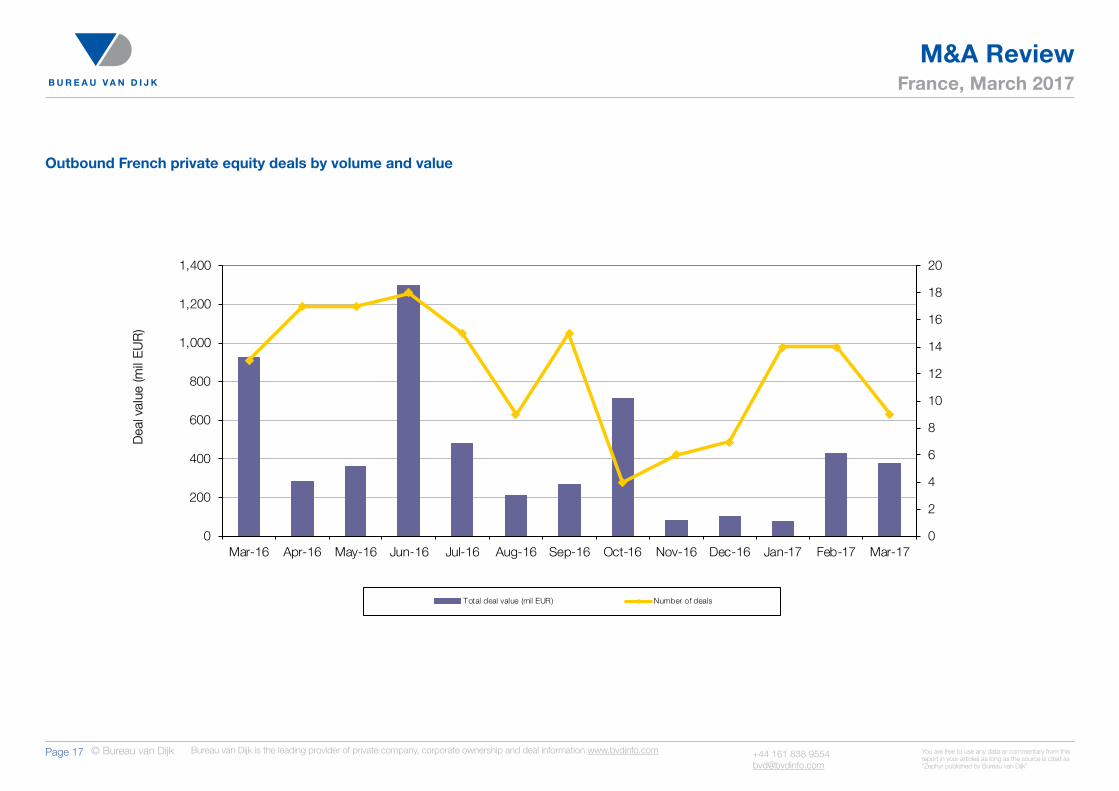

Outbound PE and VC declines in March

The volume and value of outbound PE and VC investment by French companies fell 36 per cent and 12 per cent, respectively, in March to 9 deals worth EUR 376 million from 14 deals worth EUR 428 million in February due to the lack of high valued deals.

Only one deal exceeded EUR 100 million in the four weeks under review, resulting in a 59 per cent decline by value year-on-year, against a 31 per cent decrease by volume from 13 deals worth EUR 925 million in March 2016, which was actually the second highest recorded month in the period under review (June 2016: EUR 1,298 million).

The largest outbound PE and VC deal completed in March involved French private equity firm Astorg Partners acquiring UK-based Audiotonix from Electra Private Equity and Livingbridge for EUR 237 million. This deal was some way ahead of the second largest deal which took the form of a funding round by Dutch respiratory disease therapy maker Breathe Therapeutics, which raised EUR 44 million from Sofinnova Partners, as well as Gimv and Glide Healthcare Partners.

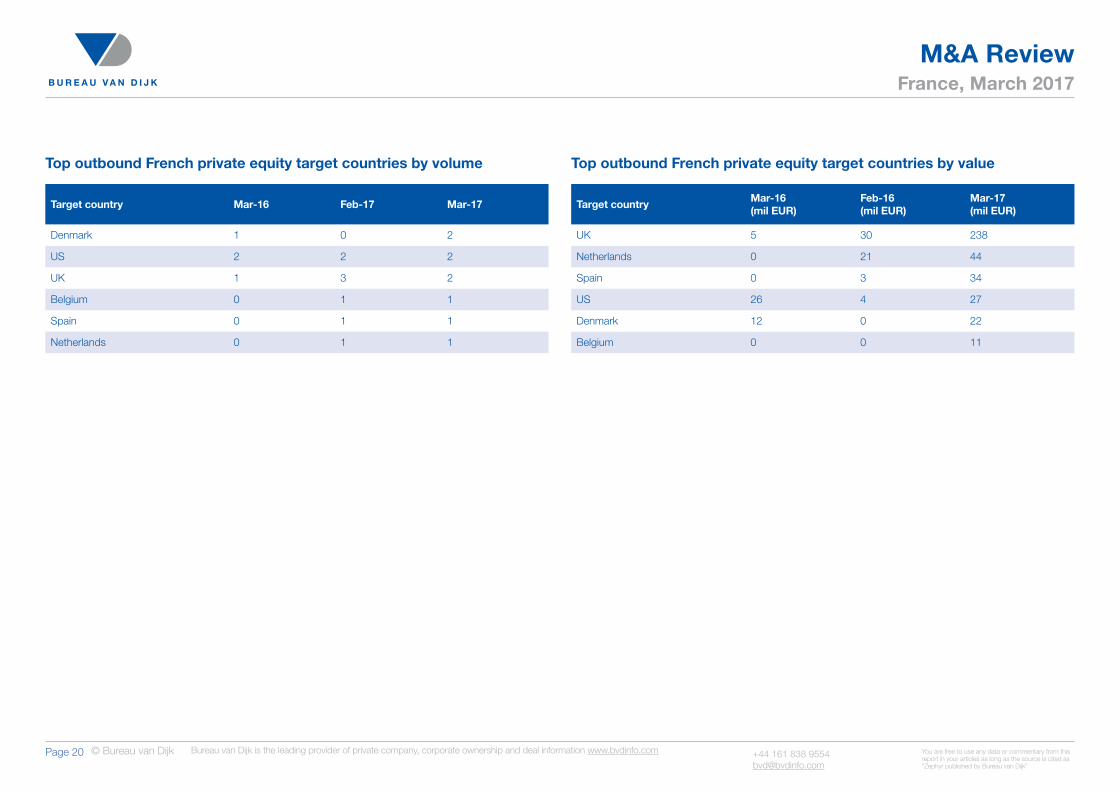

The Audiotonix deal ensured the machinery, equipment, furniture and recycling industry was the most valuable in March (EUR 290 million), and companies based in the UK led the way by value with EUR 238 million. In a similar pattern to M&A, outbound PE and VC investment favoured businesses in Europe as investment in the Netherlands and Spain were the second and third most valuable with EUR 44 million and EUR 34 million, respectively. The US followed with EUR 27 million, while investment of EUR 22 million was recorded for Denmark and EUR 11 million for Belgium.

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 17 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Outbound French private equity deals by volume and value

0

2

4

6

8

10

12

14

16

18

20

0

200

400

600

800

1,000

1,200

1,400

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

Dea

l val

ue (m

il E

UR

)

Total deal value (mil EUR) Number of deals

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 18 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top outbound French private equity deals by value

Deal value (mil EUR) Deal type Target Target

country General Partner/Fund Manager Completion date

1. 237 IBO 100% Audiotonix Ltd GB Astorg Partners SAS 31/03/2017

2. 44 Minority stake Breath Therapeutics Holding BV NL Gimv NV; Sofinnova Partners SAS; Gilde Healthcare Partners BV 08/03/2017

3. 34 Minority stake MedLumics SL ES Edmond de Rothschild Investment Partners SA; Ysios Capital Partners SGECR SA; Innogest SGR SpA; Caixa Capital Risc SGEIC SA; Seroba Life Sciences Ltd

20/03/2017

4. 19 Minority stake 908 Devices Inc. US ARCH Venture Partners LLC; Schlumberger SA; Razor's Edge Ventures LLC; Saudi Aramco Energy Ventures LLC; Casdin Capital LLC; Cormorant Asset Management LLC; Tao Capital Partners LLC

15/03/2017

5. 14 Minority stake Orphazyme ApS DK Novo A/S; Life Sciences Partners BV; Aescap Venture Management BV; Sunstone Capital A/S; IDInvest Partners; Kurma Partners SA; SUNU Ventures BV

09/03/2017

6. 11 Minority stake AgroSavfe SA/NV BE Gimv NV; Sofinnova Partners SAS; ParticipatieMaatschappij Vlaanderen NV; Vlaams Instituut voor Biotechnologie - Flanders Institute for Biotechnology; Agri Investment Fund CVBA; Qbic Venture Partners

07/03/2017

7. 8 Minority stake BeautyCon LLC US L'Oreal SA; Hearst Ventures; A&E Television Networks LLC; CAA Ventures Inc.; BBG Ventures LLC; Main Street Advisors 20/03/2017

8. 8 Minority stake Peakon ApS DK Sunstone Capital A/S; IDInvest Partners; EQT Partners AB 27/03/2017

9. 1 Minority stake Aiden.ai GB Kima Ventures SAS 23/03/2017

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 19 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Outbound French private equity target sectors by volume

Target sector Mar-16 Feb-17 Mar-17

Other services 8 6 5

Machinery, equipment, furniture, recycling 0 0 3

Publishing, printing 0 1 1

Post and telecommunications 0 0 0

Hotels & restaurants 0 2 0

Transport 0 0 0

Insurance companies 0 0 0

Public administration and defence 0 0 0

Banks 0 0 0

Education, health 0 1 0

Wholesale & retail trade 1 1 0

Textiles, wearing apparel, leather 0 0 0

Wood, cork, paper 1 0 0

Primary sector 0 0 0

Food, beverages, tobacco 0 0 0

Gas, water, electricity 1 0 0

Construction 0 2 0

Chemicals, rubber, plastics 2 0 0

Metals & metal products 0 1 0

Outbound French private equity target sectors by value

Target sector Mar-16 (mil EUR)

Feb-17 (mil EUR)

Mar-17 (mil EUR)

Machinery, equipment, furniture, recycling 0 0 290

Other services 24 12 85

Publishing, printing 0 23 1

Post and telecommunications 0 0 0

Hotels & restaurants 0 369 0

Transport 0 0 0

Insurance companies 0 0 0

Public administration and defence 0 0 0

Banks 0 0 0

Education, health 0 2 0

Wholesale & retail trade 300 21 0

Textiles, wearing apparel, leather 0 0 0

Wood, cork, paper 0 0 0

Primary sector 0 0 0

Food, beverages, tobacco 0 0 0

Gas, water, electricity 570 0 0

Construction 0 0 0

Chemicals, rubber, plastics 31 0 0

Metals & metal products 0 0 0

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 20 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top outbound French private equity target countries by volume

Target country Mar-16 Feb-17 Mar-17

Denmark 1 0 2

US 2 2 2

UK 1 3 2

Belgium 0 1 1

Spain 0 1 1

Netherlands 0 1 1

Top outbound French private equity target countries by value

Target country Mar-16 (mil EUR)

Feb-16 (mil EUR)

Mar-17 (mil EUR)

UK 5 30 238

Netherlands 0 21 44

Spain 0 3 34

US 26 4 27

Denmark 12 0 22

Belgium 0 0 11

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 21 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

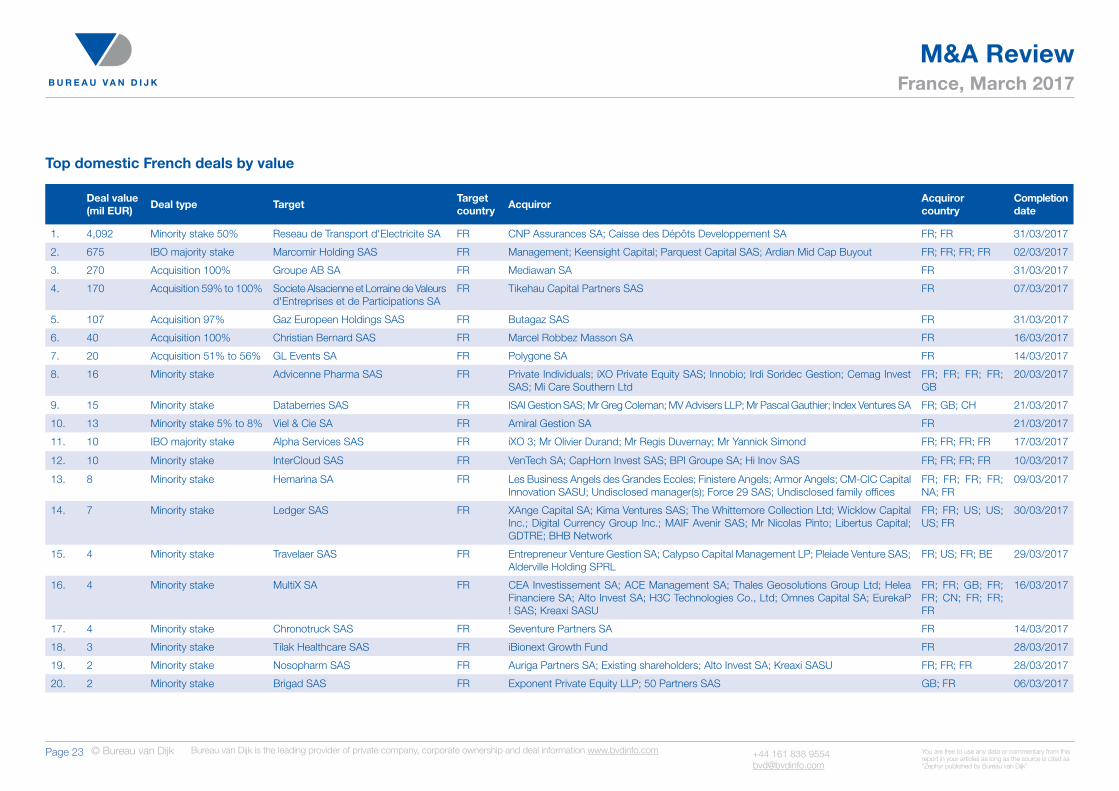

Domestic value at 12-month high against a decline by volume

The value of domestic M&A dealmaking advanced for the second consecutive period to a new 12-month high of USD 5,483 million in March on the back of one USD 4,000 million-plus deal which accounted for three quarters of this total.

Volume was down by more than a third over the four weeks and, at 64 deals (February: 97), was the second lowest recorded for the 12-months after 43 deals completed in August. However, this decline had little impact on value, which was five times higher month-on-month (February: USD 1,037 million) and ten times higher year-on-year (USD 542 million). This indicates acquirors opted for single deals with higher individual valuations rather than prolific dealmaking with lower aggregate valuations.

The two largest domestic deals by value in March were also the two largest PE and VC deals by value for the month: Electricité de France sold just shy of 50 per cent of its high-voltage power grid arm, Réseau de Transport d’Electricité, to state bank Caisse des Dépôts Developpement and CNP Assurances for USD 4,092 million and management, Keensight Capital, Parquest Capital, Ardian Mid Cap Buyout acquired 60 per cent of Marcomir for EUR 675 million.

Unsurprisingly, companies operating in the gas, water and electricity sector were the most valuable targets of M&A in March (USD 4,199 million), followed by chemicals, rubber and plastics (USD 675 million). However, with merely 2 deals and 3 deals, respectively, the volume of dealmaking by these companies were overtaken by those operating in industries such as machinery, equipment, furniture and recycling (9 deals), publishing and printing (4 deals).

Domestic French deals by volume and value

Completed date No of deals Total deal value (mil EUR)

Mar-17 64 5,483

Feb-17 97 1,037

Jan-17 102 911

Dec-16 79 1,621

Nov-16 68 788

Oct-16 85 353

Sep-16 107 1,330

Aug-16 43 2,018

Jul-16 106 3,194

Jun-16 131 2,174

May-16 111 1,977

Apr-16 85 1,522

Mar-16 103 542

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 22 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Domestic French deals by volume and value

0

20

40

60

80

100

120

140

0

1,000

2,000

3,000

4,000

5,000

6,000

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

Dea

l val

ue (m

il E

UR

)

Total deal value (mil EUR) Number of deals

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 23 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top domestic French deals by value

Deal value (mil EUR) Deal type Target Target

country Acquiror Acquiror country

Completion date

1. 4,092 Minority stake 50% Reseau de Transport d'Electricite SA FR CNP Assurances SA; Caisse des Dépôts Developpement SA FR; FR 31/03/2017

2. 675 IBO majority stake Marcomir Holding SAS FR Management; Keensight Capital; Parquest Capital SAS; Ardian Mid Cap Buyout FR; FR; FR; FR 02/03/2017

3. 270 Acquisition 100% Groupe AB SA FR Mediawan SA FR 31/03/2017

4. 170 Acquisition 59% to 100% Societe Alsacienne et Lorraine de Valeurs d'Entreprises et de Participations SA

FR Tikehau Capital Partners SAS FR 07/03/2017

5. 107 Acquisition 97% Gaz Europeen Holdings SAS FR Butagaz SAS FR 31/03/2017

6. 40 Acquisition 100% Christian Bernard SAS FR Marcel Robbez Masson SA FR 16/03/2017

7. 20 Acquisition 51% to 56% GL Events SA FR Polygone SA FR 14/03/2017

8. 16 Minority stake Advicenne Pharma SAS FR Private Individuals; iXO Private Equity SAS; Innobio; Irdi Soridec Gestion; Cemag Invest SAS; Mi Care Southern Ltd

FR; FR; FR; FR; GB

20/03/2017

9. 15 Minority stake Databerries SAS FR ISAI Gestion SAS; Mr Greg Coleman; MV Advisers LLP; Mr Pascal Gauthier; Index Ventures SA FR; GB; CH 21/03/2017

10. 13 Minority stake 5% to 8% Viel & Cie SA FR Amiral Gestion SA FR 21/03/2017

11. 10 IBO majority stake Alpha Services SAS FR iXO 3; Mr Olivier Durand; Mr Regis Duvernay; Mr Yannick Simond FR; FR; FR; FR 17/03/2017

12. 10 Minority stake InterCloud SAS FR VenTech SA; CapHorn Invest SAS; BPI Groupe SA; Hi Inov SAS FR; FR; FR; FR 10/03/2017

13. 8 Minority stake Hemarina SA FR Les Business Angels des Grandes Ecoles; Finistere Angels; Armor Angels; CM-CIC Capital Innovation SASU; Undisclosed manager(s); Force 29 SAS; Undisclosed family offices

FR; FR; FR; FR; NA; FR

09/03/2017

14. 7 Minority stake Ledger SAS FR XAnge Capital SA; Kima Ventures SAS; The Whittemore Collection Ltd; Wicklow Capital Inc.; Digital Currency Group Inc.; MAIF Avenir SAS; Mr Nicolas Pinto; Libertus Capital; GDTRE; BHB Network

FR; FR; US; US; US; FR

30/03/2017

15. 4 Minority stake Travelaer SAS FR Entrepreneur Venture Gestion SA; Calypso Capital Management LP; Pleiade Venture SAS; Alderville Holding SPRL

FR; US; FR; BE 29/03/2017

16. 4 Minority stake MultiX SA FR CEA Investissement SA; ACE Management SA; Thales Geosolutions Group Ltd; Helea Financiere SA; Alto Invest SA; H3C Technologies Co., Ltd; Omnes Capital SA; EurekaP ! SAS; Kreaxi SASU

FR; FR; GB; FR; FR; CN; FR; FR; FR

16/03/2017

17. 4 Minority stake Chronotruck SAS FR Seventure Partners SA FR 14/03/2017

18. 3 Minority stake Tilak Healthcare SAS FR iBionext Growth Fund FR 28/03/2017

19. 2 Minority stake Nosopharm SAS FR Auriga Partners SA; Existing shareholders; Alto Invest SA; Kreaxi SASU FR; FR; FR 28/03/2017

20. 2 Minority stake Brigad SAS FR Exponent Private Equity LLP; 50 Partners SAS GB; FR 06/03/2017

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 24 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Domestic French target sectors by volume

Target sector Mar-16 Feb-17 Mar-17

Other services 56 43 30

Machinery, equipment, furniture, recycling 7 7 9

Publishing, printing 3 15 4

Chemicals, rubber, plastics 1 3 3

Wholesale & retail trade 16 8 3

Food, beverages, tobacco 2 4 3

Metals & metal products 3 0 3

Transport 1 3 2

Gas, water, electricity 0 3 2

Construction 2 2 2

Insurance companies 0 2 1

Wood, cork, paper 2 0 1

Public administration and defence 0 0 0

Education, health 2 1 0

Banks 0 0 0

Primary sector 2 3 0

Textiles, wearing apparel, leather 2 2 0

Post and telecommunications 1 0 0

Hotels & restaurants 1 0 0

Domestic French target sectors by value

Target sector Mar-16 (mil EUR)

Feb-17 (mil EUR)

Mar-17 (mil EUR)

Gas, water, electricity 0 234 4,199

Chemicals, rubber, plastics 2 5 675

Other services 489 689 526

Machinery, equipment, furniture, recycling 3 66 51

Publishing, printing 0 26 20

Construction 0 0 10

Metals & metal products 0 0 2

Banks 0 0 0

Post and telecommunications 9 0 0

Insurance companies 0 0 0

Public administration and defence 0 0 0

Education, health 2 0 0

Transport 0 8 0

Wood, cork, paper 0 0 0

Textiles, wearing apparel, leather 0 0 0

Food, beverages, tobacco 0 1 0

Hotels & restaurants 5 0 0

Wholesale & retail trade 27 8 0

Primary sector 1 0 0

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 25 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

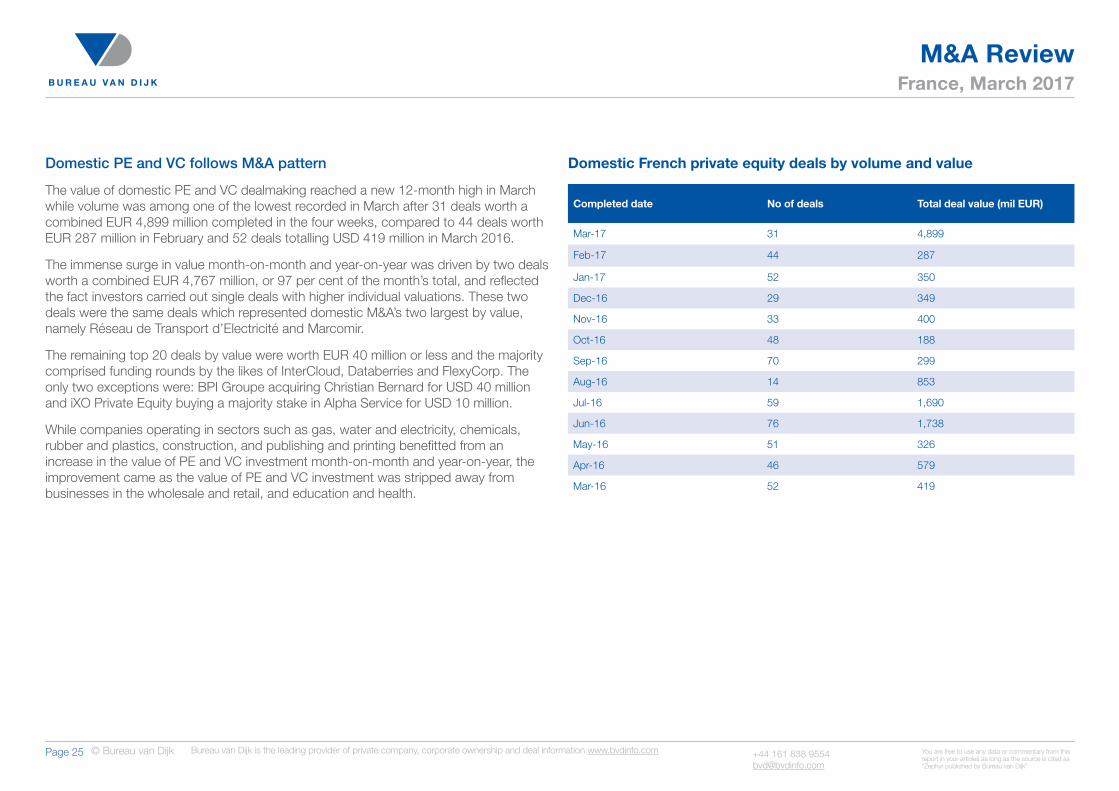

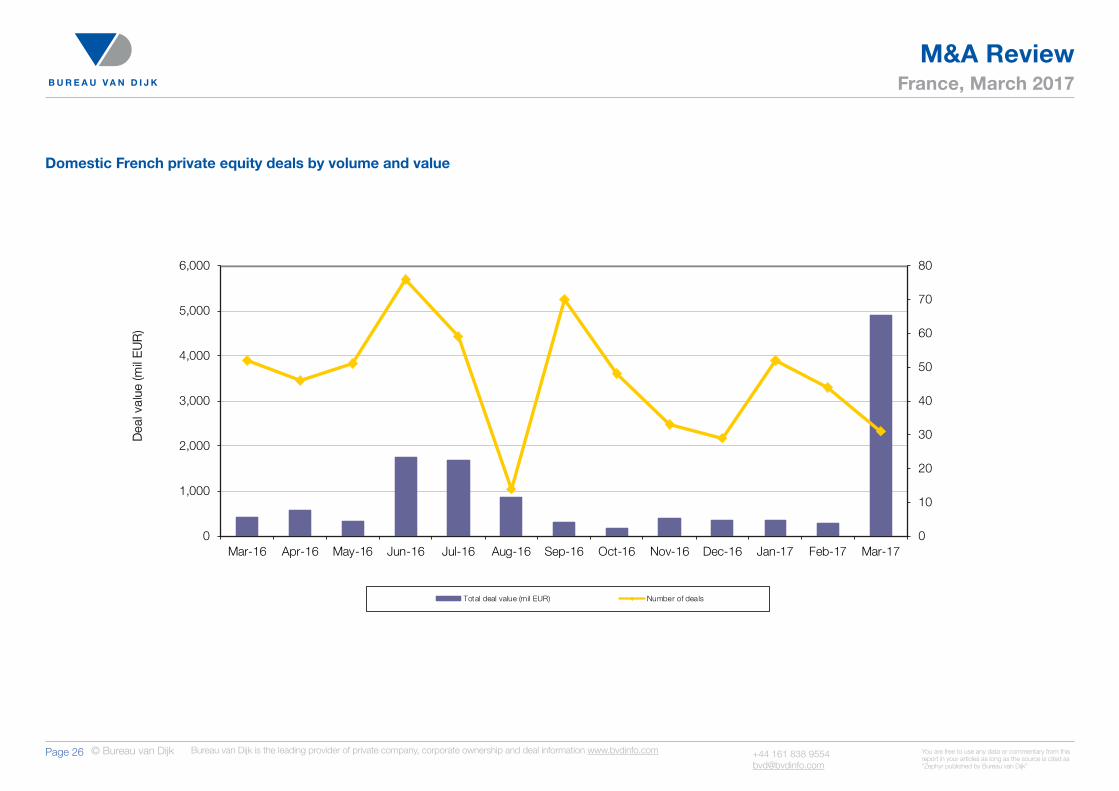

Domestic French private equity deals by volume and value

Completed date No of deals Total deal value (mil EUR)

Mar-17 31 4,899

Feb-17 44 287

Jan-17 52 350

Dec-16 29 349

Nov-16 33 400

Oct-16 48 188

Sep-16 70 299

Aug-16 14 853

Jul-16 59 1,690

Jun-16 76 1,738

May-16 51 326

Apr-16 46 579

Mar-16 52 419

Domestic PE and VC follows M&A pattern

The value of domestic PE and VC dealmaking reached a new 12-month high in March while volume was among one of the lowest recorded in March after 31 deals worth a combined EUR 4,899 million completed in the four weeks, compared to 44 deals worth EUR 287 million in February and 52 deals totalling USD 419 million in March 2016.

The immense surge in value month-on-month and year-on-year was driven by two deals worth a combined EUR 4,767 million, or 97 per cent of the month’s total, and reflected the fact investors carried out single deals with higher individual valuations. These two deals were the same deals which represented domestic M&A’s two largest by value, namely Réseau de Transport d’Electricité and Marcomir.

The remaining top 20 deals by value were worth EUR 40 million or less and the majority comprised funding rounds by the likes of InterCloud, Databerries and FlexyCorp. The only two exceptions were: BPI Groupe acquiring Christian Bernard for USD 40 million and iXO Private Equity buying a majority stake in Alpha Service for USD 10 million.

While companies operating in sectors such as gas, water and electricity, chemicals, rubber and plastics, construction, and publishing and printing benefitted from an increase in the value of PE and VC investment month-on-month and year-on-year, the improvement came as the value of PE and VC investment was stripped away from businesses in the wholesale and retail, and education and health.

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 26 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Domestic French private equity deals by volume and value

0

10

20

30

40

50

60

70

80

0

1,000

2,000

3,000

4,000

5,000

6,000

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

Dea

l val

ue (m

il E

UR

)

Total deal value (mil EUR) Number of deals

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 27 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Top domestic French private equity deals by volume and value

Deal value (mil EUR) Deal type Target Target

country General Partner/Fund Manager Completion date

1. 4,092 Minority stake 50% Reseau de Transport d'Electricite SA FR Caisse des Dépôts Developpement SA 31/03/2017

2. 675 IBO majority stake Marcomir Holding SAS FR Keensight Capital; Parquest Capital SAS; Ardian France SA 02/03/2017

3. 40 Acquisition 100% Christian Bernard SAS FR BPI Groupe SA 16/03/2017

4. 16 Minority stake Advicenne Pharma SAS FR iXO Private Equity SAS; BPI Groupe SA; Irdi Soridec Gestion; Cemag Invest SAS; Mi Care Southern Ltd 20/03/2017

5. 15 Minority stake Databerries SAS FR ISAI Gestion SAS; MV Advisers LLP; Index Ventures SA 21/03/2017

6. 10 IBO majority stake Alpha Services SAS FR iXO Private Equity SAS 17/03/2017

7. 10 Minority stake InterCloud SAS FR VenTech SA; CapHorn Invest SAS; BPI Groupe SA; Hi Inov SAS 10/03/2017

8. 8 Minority stake Hemarina SA FR Les Business Angels des Grandes Ecoles; Finistere Angels; Armor Angels; CM-CIC Capital Innovation SASU; Force 29 SAS 09/03/2017

9. 7 Minority stake Ledger SAS FR XAnge Capital SA; Kima Ventures SAS; The Whittemore Collection Ltd; Wicklow Capital Inc.; Digital Currency Group Inc.; MAIF Avenir SAS; Libertus Capital

30/03/2017

10. 4 Minority stake Travelaer SAS FR Entrepreneur Venture Gestion SA; Calypso Capital Management LP; Pleiade Venture SAS; Alderville Holding SPRL 29/03/2017

11. 4 Minority stake MultiX SA FR CEA Investissement SA; ACE Management SA; Thales Geosolutions Group Ltd; Helea Financiere SA; Alto Invest SA; H3C Technologies Co., Ltd; Omnes Capital SA; EurekaP ! SAS; Kreaxi SASU

16/03/2017

12. 4 Minority stake Chronotruck SAS FR Seventure Partners SA 14/03/2017

13. 3 Minority stake Tilak Healthcare SAS FR iBionext SAS 28/03/2017

14. 2 Minority stake Nosopharm SAS FR Auriga Partners SA; Alto Invest SA; Kreaxi SASU 28/03/2017

15. 2 Minority stake Brigad SAS FR Exponent Private Equity LLP; 50 Partners SAS 06/03/2017

16. 2 Minority stake FlexyCorp SAS FR Newfund Management SA 23/03/2017

17. 2 Minority stake Eqinov Conseil et Financement SAS FR Newfund Management SA 06/03/2017

18. 1 Minority stake Botfuel SAS FR Breega Capital Sarl; Seventure Partners SA 27/03/2017

19. 1 Minority stake PeptiMimesis SAS FR Alsace Capital SAS; Invest PME SA 15/03/2017

20. 1 Minority stake TrustInSoft SA FR IDInvest Partners 09/03/2017

You are free to use any data or commentary from this report in your articles as long as the source is cited as “Zephyr published by Bureau van Dijk”

+44 161 838 9554 [email protected]

M&A ReviewFrance, March 2017

Page 28 © Bureau van Dijk Bureau van Dijk is the leading provider of private company, corporate ownership and deal information www.bvdinfo.com

Domestic French private equity target sectors by volume

Target sector Mar-16 Feb-17 Mar-17

Other services 35 23 13

Machinery, equipment, furniture, recycling 3 2 6

Publishing, printing 1 8 4

Food, beverages, tobacco 1 1 3

Transport 0 0 2

Gas, water, electricity 0 1 1

Construction 0 2 1

Chemicals, rubber, plastics 1 2 1

Post and telecommunications 1 0 0

Education, health 2 0 0

Banks 0 0 0

Public administration and defence 0 0 0

Insurance companies 0 1 0

Metals & metal products 1 0 0

Wood, cork, paper 0 0 0

Textiles, wearing apparel, leather 0 1 0

Hotels & restaurants 1 0 0

Wholesale & retail trade 6 3 0

Primary sector 0 0 0

Domestic French private equity target sectors by value

Target sector Mar-16 (mil EUR)

Feb-17 (mil EUR)

Mar-17 (mil EUR)

Gas, water, electricity 0 0 4,092

Chemicals, rubber, plastics 2 5 675

Other services 383 248 52

Machinery, equipment, furniture, recycling 3 1 51

Publishing, printing 0 23 20

Construction 0 0 10

Banks 0 0 0

Post and telecommunications 9 0 0

Transport 0 0 0

Insurance companies 0 0 0

Public administration and defence 0 0 0

Education, health 2 0 0

Wood, cork, paper 0 0 0

Textiles, wearing apparel, leather 0 0 0

Food, beverages, tobacco 0 1 0

Metals & metal products 0 0 0

Hotels & restaurants 5 0 0

Wholesale & retail trade 14 8 0

Primary sector 0 0 0

Notes to editors

Activity is based on the activity of the target company.

Deal status is completed within the time period.

The sector breakdown uses targets’ activities as defined to be ‘Major Sectors’ by Zephyr.

The date range is 01/03/2017 - 31/03/2017 inclusive