m&a report, hampleton focus area - it service & outsourcing - oct 2013

TRANSCRIPT

M&A Report, October 2013 M&A Report, October 2013

IT Services, Outsourcing and Distribution

• Equity transactions in software and Internet industry``

• Sell-side representation

• M&A advisory and sale of significant stakes to strategic or financial

buyers

• Founded by senior tech industry banker and executives

• Directors with both operational and M&A experience

• Supported by London based research and financial analysts

• Research oriented firm

• Sector Principals – active domain experts

• Industry sector focus

Company Background

Service Focus

Team Strength

Sector Special isation

October 2013

Hampleton is a highly focused firm that concentrates on specific segments of the IT industry. Our international team of experienced sector principals provide in-depth analysis and research into our focus areas.

Focus Areas

October 2013

October 2013

`

IT Services, Outsourcing and Distribution

$35 MMedian value of all disclosed value transactions:Jan 2011-July 2013

$450 MTotal disclosed value of this focus area: Jan 2011-July 2013

“The IT services segment continues to have higher valuations for their companies, up 18% since Jan 2011”

Market Outlook

October 2013

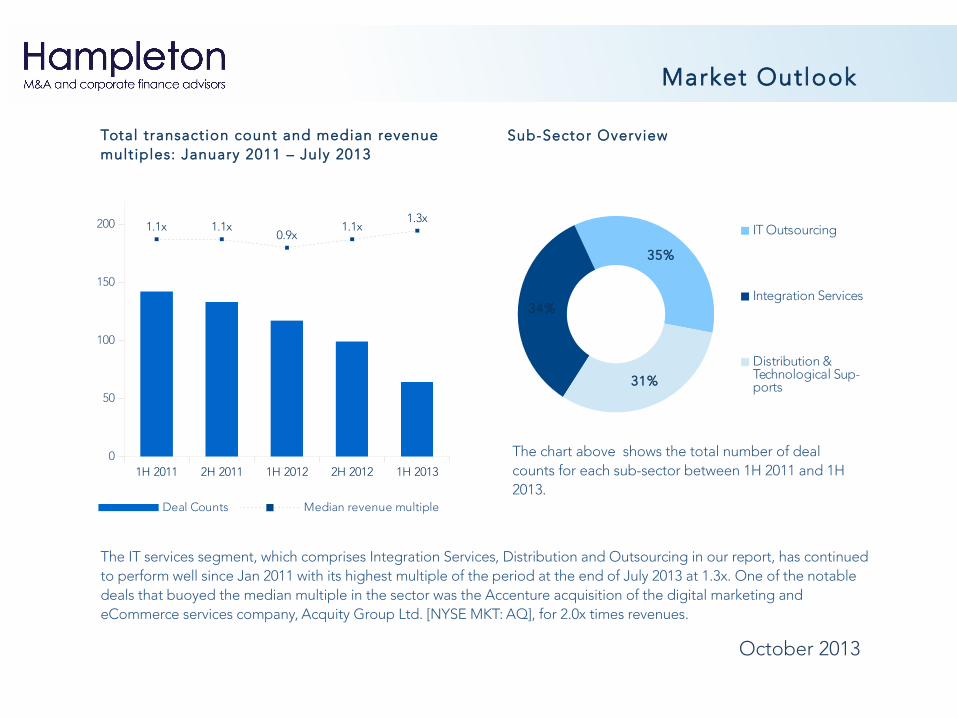

Total transaction count and median revenue mult iples: January 2011 – July 2013

Sub-Sector Overview

1H 2011 2H 2011 1H 2012 2H 2012 1H 20130

50

100

150

200 1.1x 1.1x0.9x

1.1x1.3x

Deal Counts Median revenue multiple

The IT services segment, which comprises Integration Services, Distribution and Outsourcing in our report, has continued to perform well since Jan 2011 with its highest multiple of the period at the end of July 2013 at 1.3x. One of the notable deals that buoyed the median multiple in the sector was the Accenture acquisition of the digital marketing and eCommerce services company, Acquity Group Ltd. [NYSE MKT: AQ], for 2.0x times revenues.

35%

34%

31%

IT Outsourcing

Integration Services

Distribution & Technological Sup-ports

The chart above shows the total number of deal counts for each sub-sector between 1H 2011 and 1H 2013.

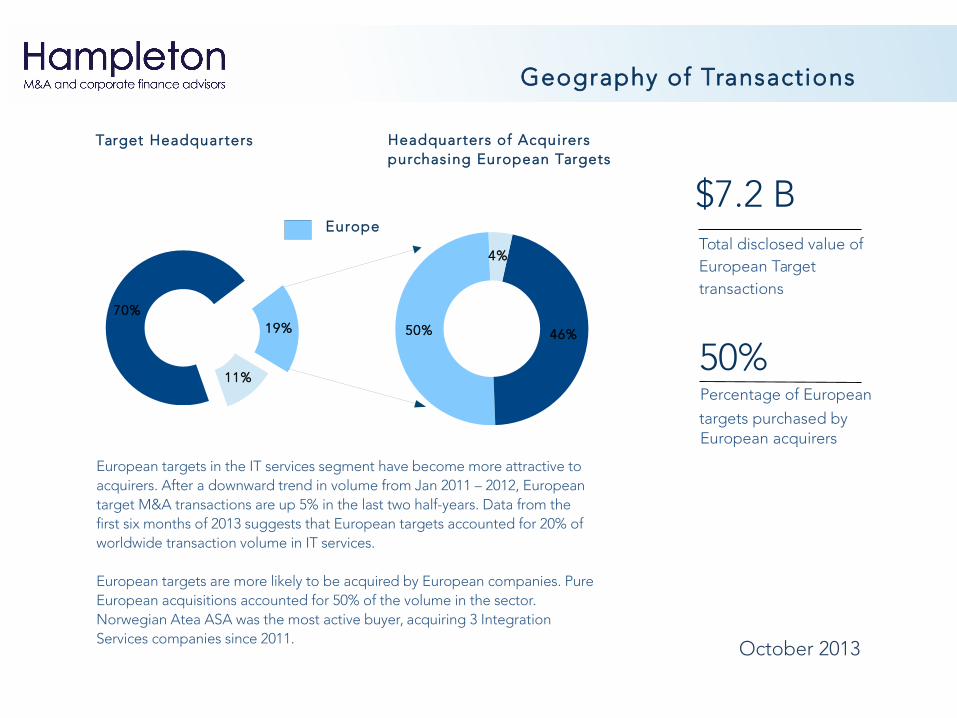

Total disclosed value of European Target transactions

$7.2 B

Percentage of European

targets purchased by European acquirers

50%

Geography of Transactions

October 2013

Target Headquarters Headquarters of Acquirers purchasing European Targets

Europe

19%70%

11%

50% 46%

4%

European targets in the IT services segment have become more attractive to acquirers. After a downward trend in volume from Jan 2011 – 2012, European target M&A transactions are up 5% in the last two half-years. Data from the first six months of 2013 suggests that European targets accounted for 20% of worldwide transaction volume in IT services.

European targets are more likely to be acquired by European companies. Pure European acquisitions accounted for 50% of the volume in the sector. Norwegian Atea ASA was the most active buyer, acquiring 3 Integration Services companies since 2011.

Sub-Sector Breakdown

October 2013

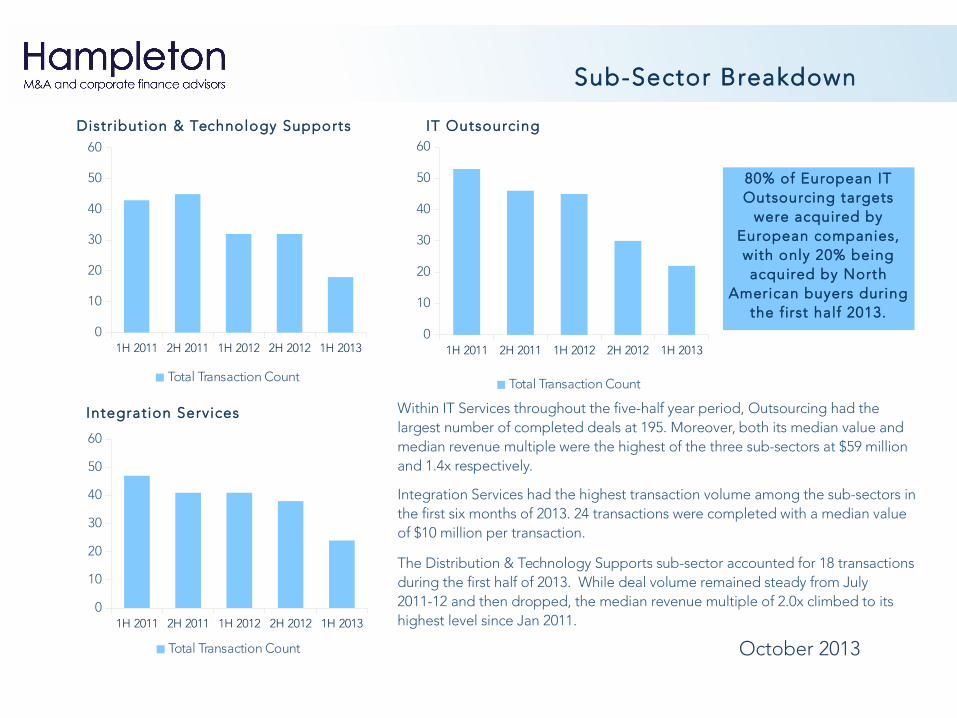

80% of European IT Outsourcing targets

were acquired by European companies, with only 20% being acquired by North

American buyers during the first half 2013.

1H 2011 2H 2011 1H 2012 2H 2012 1H 20130

10

20

30

40

50

60

Total Transaction Count

1H 2011 2H 2011 1H 2012 2H 2012 1H 20130

10

20

30

40

50

60

Total Transaction Count

1H 2011 2H 2011 1H 2012 2H 2012 1H 20130

10

20

30

40

50

60

Total Transaction Count

Within IT Services throughout the five-half year period, Outsourcing had the largest number of completed deals at 195. Moreover, both its median value and median revenue multiple were the highest of the three sub-sectors at $59 million and 1.4x respectively.

Integration Services had the highest transaction volume among the sub-sectors in the first six months of 2013. 24 transactions were completed with a median value of $10 million per transaction.

The Distribution & Technology Supports sub-sector accounted for 18 transactions during the first half of 2013. While deal volume remained steady from July 2011-12 and then dropped, the median revenue multiple of 2.0x climbed to its highest level since Jan 2011.

IT Outsourcing

Integration Services

Distr ibution & Technology Supports

16 Hanover SquareLondonW11 SLTUnited Kingdom

Contact Details

October 2013

Miro Parizek

Principal [email protected]: +44-7551-156-453Skype: miro.parizek

Jo Goodson

Senior [email protected]: +44 7551-156452Skype: jogood1964

Thomas BerglundAssociate Partner

Alexander FrankeSector Principal

Miro ParizekPrincipal Partner

Jo GoodsonSenior Director

Henrik JebergDirector

Neal McCleaveSector Principal

Christian DaherSector Principal

Lynda TrippSenior Editor

Axel BrillDirector

Frank BergerAssociate Partner

Vu NguyenAnalyst

Rachel MuzyczkaAnalyst

Ramakanth DesaiSenior Advisor

Hampleton Professionals

October 2013

October 2013

Hampleton provides independent M&A and corporate finance advice to owners of Internet, IT Services and Software companies. Our research aim to provide our clients with current analysis of the transactions, trends and valuations within our focus areas.

Data Source: We have based our findings on data provided by industry recognised sources. Data and information for this publication was collated from the 451 Research database (www.451research.com), a division of The 451 Group.

Disclaimer: This publication contains general information only and Hampleton Ltd. is not, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. Hampleton Limited shall not be responsible for any loss whatsoever sustained by any person who relies on this publication.

© 2013. For more information, contact Hampleton Ltd.

London San Francisco16 Hanover Square 1 Sutter StW1S1HT CA 94104United Kingdom United States

Email [email protected]