m o r g a n s t a n l e y r e s e a r c h global march 2009 morgan stanley & co. incorporated...

TRANSCRIPT

M O R G A N S T A N L E Y R E S E A R C H

GLOBAL

March 2009

Morgan Stanley & Co. Incorporated

Jason E. [email protected]+1 212 761 7991

Equity Research

U.S. Equity

Strategy

U.S

. S

trat

egy

Morgan Stanley does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Customers of Morgan Stanley in the United States can receive independent, third-party research on the company or companies covered in this report, at no cost to them, where such research is available. Customers can access this independent research at www.morganstanley.com/equityresearch or can call 800-624-2063 to request a copy of this research.

For analyst certification and other important disclosures, refer to the Disclosure Section.

U.S. Equity StrategyBear Market Still Intact

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

2Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Key Global Economic Themes

Critical global issues:

Global growth risks are now more balanced, but around a contracting baseline in 2009. A record global recession and weakness in commodity prices should persist, while the dollar should show renewed weakness later in 2009.

How deep and how long? The answer will hinge on policy actions taken to break the ‘adverse feedback loop’ from credit to the economy and back and whether those policies get traction soon.

Massive stimulus helps China recover first. But China is better positioned than most in the developing world. A severe global downturn and tepid recovery are still likely.

Aggressive (in some cases quantitative) easing, new financing facilities, tools to fix financial systems, and fiscal stimulus are now weapons of choice to fight credit crunch, deep slump and deflation risks.

What’s Next?

Look for others to follow the US with more aggressive monetary ease, fiscal stimulus, and backstops for financial institutions and markets. Look for weaker exports and commodity prices to confirm weaker global growth, especially in EM. Falling inflation could fuel the deflation scare. Look for signs of thawing in funding and credit, and a less-intense rate of decline in output.

Where we differ

Growth: Below consensus in both the industrial and developing economies

Inflation: Deflation scare may intensify, but reflation will ultimately prevail

Rates: Curves rangebound for now, TIPS still attractive, given inflation and policy uncertainty

Equities: More bearish than consensus on growth and margins. Lower inflation unlikely to help stocks; seen as lost pricing power. Overweight EM over developed markets.

Credit: More bullish than consensus on investment grade globally

Currencies: Modestly more bearish on the USD than consensus, and selectively more bearish on EM currencies

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

3Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Key US Equity Recommendations 2009 S&P 500 Outlook

-825 target on $57 dollars of earnings and 14.5x P/E

Key Recommendations

- Buy Corporate Credit – IG (Financials/cash rich Tech over Industrial and Materials)

- Buy Consumers over Producers (Retail, Healthcare, Food & Beverage, Personal Products over Cap Goods, Metals, Energy)

- Buy Brand, Content and Franchise value (CSCO, NKE, MCD, PM, LO, MSFT) over Distribution

Sector Weightings

- Overweight Healthcare, Telecoms

- Neutral Financials, Discretionary, Staples, Energy

- Underweight Materials, Industrials, Tech

Stock & Sector Recommendations:

-Buy healthcare with earnings visibility, yield and strong cash flow - JNJ, ABT, AMGN, BAX

-Buy domestic food and beverage - GIS, CL, K

-Buy custodians (STT, BK) as money markets normalize; WFC and JPM as industry consolidation winners.

-Buy Energy Equipment & Services for long term structural upside – SLB, HAL, BHI, WFT, SII

-Sell - Metals into strength - FCX, X, AKS, CLF

-Sell - Construction machinery, power gen, transportation equipment (FAST, ITW, GWW, EMR, CAT, ROK)

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

4Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

A Slow Path to Global Recovery – Asia/EM’s to Lead Rebound

-6

-5

-4

-3

-2

-1

0

1

2

3

4

2008E 2009E 2010E

Japan

Real GDP (Year-over-Year Percent Change)

US

Europe

-4

-2

0

2

4

6

8

10

12

2008E 2009E 2010E

Real GDP (Year-over-Year Percent Change)

ChinaAsia ex-Japan and China

Latin America

Source: IMF Staff Estimates, Morgan Stanley

Despite aggressive stimulus… … lingering headwinds imply a sub-par global recovery

G-20

Turkey

Italy

Brazil

Mexico

France

Argentina

U.K.

Russia

India

Japan

Indonesia

South Africa

Korea

Canada

Germany

China

Australia

Spain

U.S.

Saudi Arabia

0 1 2 3 4 5 6 7 8 9 10

Discretionary Measures in Percent of GDP, 2008-2010

E = Morgan Stanley Research estimatesSource: Morgan Stanley

3.4%

0.0%

1.3%

0.5%

1.0%

0.3%

1.3%

1.5%

1.7%

1.7%

2.2%

2.4%

2.6%

2.8%

2.8%

3.5%

4.4%

4.5%

5.0%

5.9%

9.2%

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

5Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

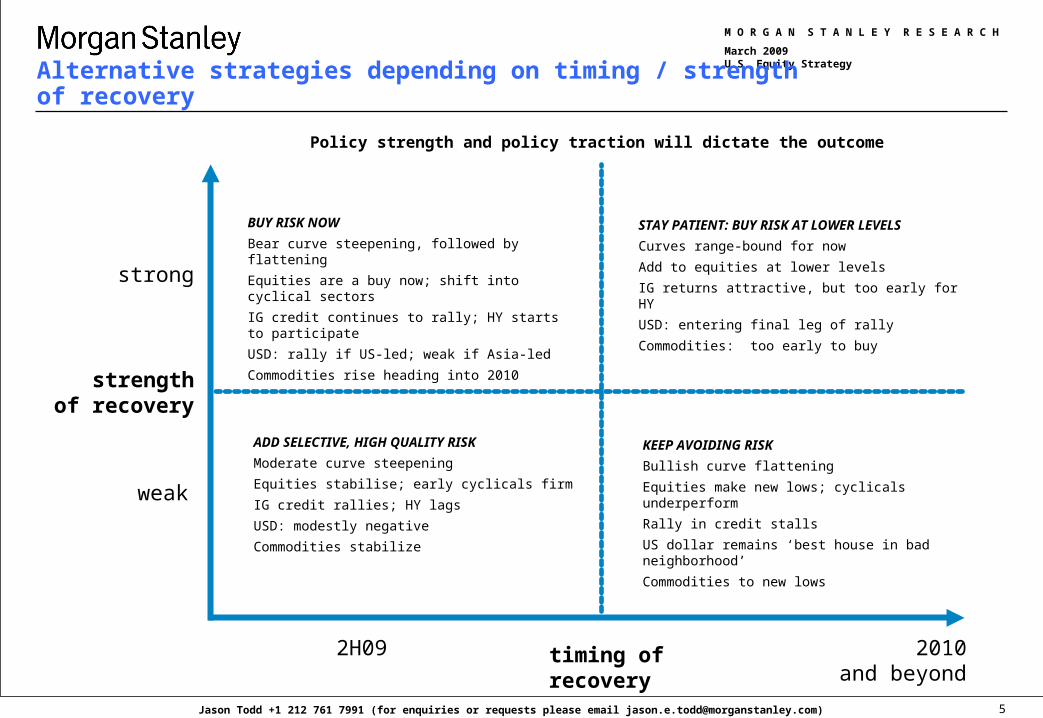

BUY RISK NOW

Bear curve steepening, followed by flattening

Equities are a buy now; shift into cyclical sectors

IG credit continues to rally; HY starts to participate

USD: rally if US-led; weak if Asia-led

Commodities rise heading into 2010

timing ofrecovery

2H09 2010and beyond

weak

strong

strengthof recovery

Alternative strategies depending on timing / strength of recovery

Policy strength and policy traction will dictate the outcome

STAY PATIENT: BUY RISK AT LOWER LEVELS

Curves range-bound for now

Add to equities at lower levels

IG returns attractive, but too early for HY

USD: entering final leg of rally

Commodities: too early to buy

ADD SELECTIVE, HIGH QUALITY RISK

Moderate curve steepening

Equities stabilise; early cyclicals firm

IG credit rallies; HY lags

USD: modestly negative

Commodities stabilize

KEEP AVOIDING RISK

Bullish curve flattening

Equities make new lows; cyclicals underperform

Rally in credit stalls

US dollar remains ‘best house in bad neighborhood’

Commodities to new lows

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

6Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

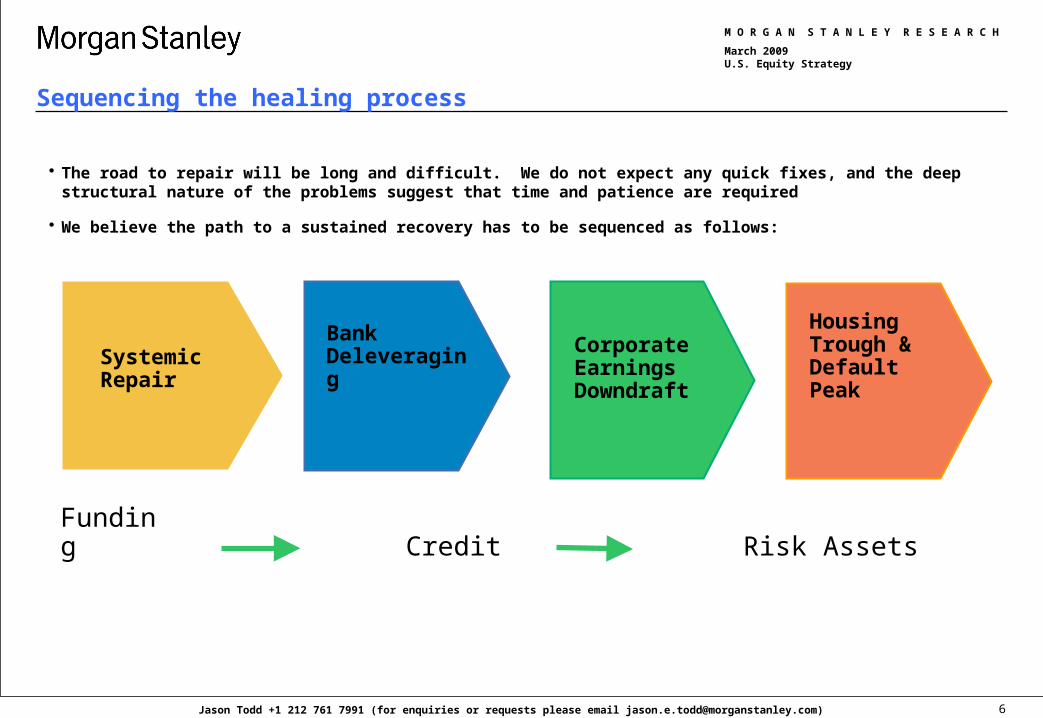

Sequencing the healing process

Housing Trough & Default Peak

Corporate Earnings Downdraft

Bank Deleveraging

Systemic Repair

The road to repair will be long and difficult. We do not expect any quick fixes, and the deep structural nature of the problems suggest that time and patience are required

We believe the path to a sustained recovery has to be sequenced as follows:

Funding Credit Risk Assets

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

7Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Credit Market – Further Healing Still Necessary

LIBOR-OIS spread still hasn’t stabilized

Corporate and HY spreads rose again this month

TED spread still elevated

95

-

50

100

150

200

250

300

350

400

450

500

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

LTCM

10/20/87Post '87 Stock Market

Crash308

364

107

0

50

100

150

200

250

300

350

400

Oct-04 Apr-05 Oct-05 Apr-06 Oct-06 Apr-07 Oct-07 Apr-08 Oct-08 Apr-09

2/25/20091838

50

150

250

350

450

550

2002 2003 2004 2005 2006 2007 2008 2009

200

700

1200

1700

2200

Corporate Bond Option Adjusted Spread - LHS

High Yield Spread to Worst

11/30/2006 34

-

5

10

15

20

25

30

35

Jan

-02

Ma

y-0

2

Se

p-0

2

Jan

-03

Ma

y-0

3

Se

p-0

3

Jan

-04

Ma

y-0

4

Se

p-0

4

Jan

-05

Ma

y-0

5

Se

p-0

5

Jan

-06

Ma

y-0

6

Se

p-0

6

Jan

-07

Ma

y-0

7

Se

p-0

7

Jan

-08

Ma

y-0

8

Se

p-0

8

Jan

-09

HY issuance on a monthly basis ($bn)

HY issuance near all time lows!

Source: Datastream, Robert Schiller, FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

8Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

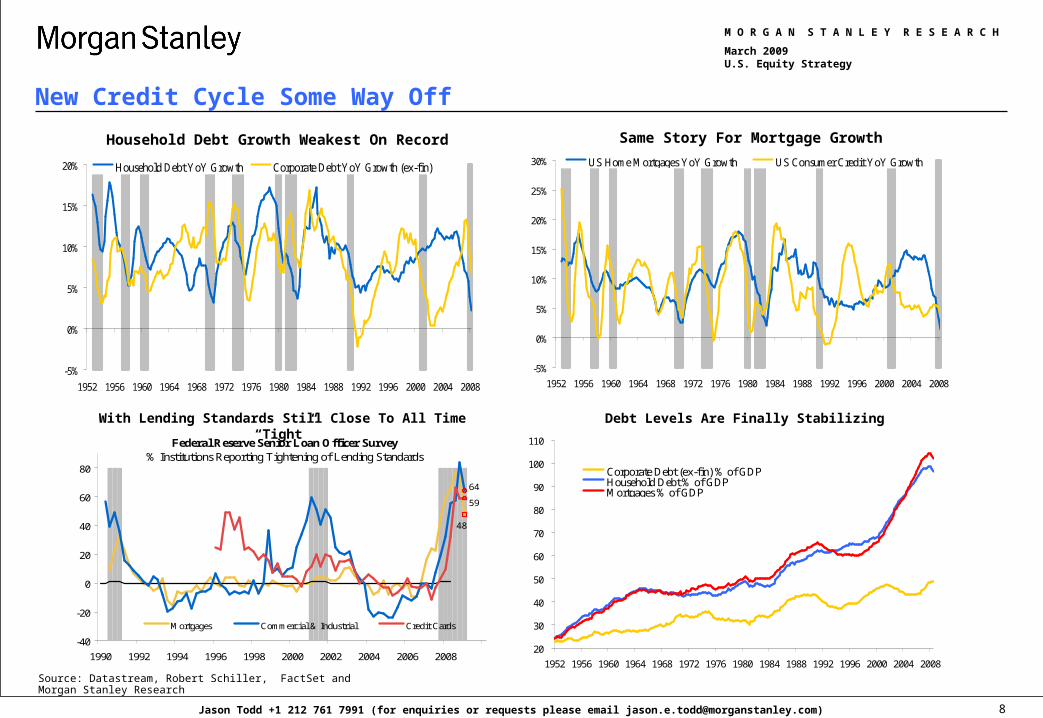

New Credit Cycle Some Way Off

Debt Levels Are Finally Stabilizing

20

30

40

50

60

70

80

90

100

110

1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

Corporate Debt (ex-fin) % of GDPHousehold Debt % of GDPMortgages % of GDP

-5%

0%

5%

10%

15%

20%

1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

Household Debt YoY Growth Corporate Debt YoY Growth (ex-fin)

-5%

0%

5%

10%

15%

20%

25%

30%

1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

US Home Mortgages YoY Growth US Consumer Credit YoY Growth

Household Debt Growth Weakest On Record Same Story For Mortgage Growth

Federal Reserve Senior Loan Officer Survey % Institutions Reporting Tightening of Lending Standards

48

64

59

-40

-20

0

20

40

60

80

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Mortgages Commercial & Industrial Credit Cards

With Lending Standards Still Close To All Time “Tight”

Source: Datastream, Robert Schiller, FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

9Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

US Housing Market – No Sign Of Bottom 3 Years After Peak

House Prices Continue To Fall From Peak…

US Established House Prices

-22

-18

-14

-10

-6

-2

2

6

10

14

18

1988 1992 1996 2000 2004 2008

12M

%

REPEAT SALES*OFHEO PRICES**

* Case-Shiller Index (3MMA) **OFHEO Purchase-Only Index

… With The Futures market pricing in a 30-40% peak to trough decline

100

120

140

160

180

200

220

240

260

280

300

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

US House Prices & Futures Index

Index Levels Implied by Futures Market

36%

* RPX 28 City Composite & Latest Implied Prices From Futures Contracts

Inventory levels remain high in part due to rising foreclosures

0.8

2.8

4.8

6.8

8.8

10.8

12.8

14.8

16.8

18.8

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Months Supply of New Single Family Houses

Months Supply of Existing Homes

Months Supply of Condos and Coops

Delinquencies still rising…

18.5%

22.1%

3.6%

8.4%

0%

5%

10%

15%

20%

25%

98 99 00 01 02 03 04 05 06 07 08

Subprime FRMs

Subprime ARMs

Prime FRMs

Prime ARMs

MBA Mortgage Delinquencies: % Past Due

Adjustable rate mortgages are most at risk

Source: Datastream, Robert Schiller, FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

10Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Breaking the Bear...

3 Ways to Break the Bear Market:

1. Policy Action – QE + Fiscal Policy Support (banks recapitalize and remove toxic assets from balance sheets)

2. Market Trades Lower – Market becomes outright cheap – valuations compensate for poor fundamentals

3. Debt/Deflation Spiral – Japanese Scenario Revisited

Requirements for Sustainable Bottom:

1. Stabilization in House Prices & Inventory Levels (look for lead from Homebuilders)

2. Market moves closer to trough in Earnings – Incl Financials, trough in 3Q09; Excl Financials, Trough in 2Q10

3. Link between Credit and Economy Broken – negative feedback loop from credit markets to economy broken

2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10

S&P500 S&P500Earnings Earnings

Peak Trough

$92 $27S&P500 S&P500

Ex Fin Ex FinEarnings Earnings

Peak Trough

$73 $42

Down 70%

Down 42%

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

11Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

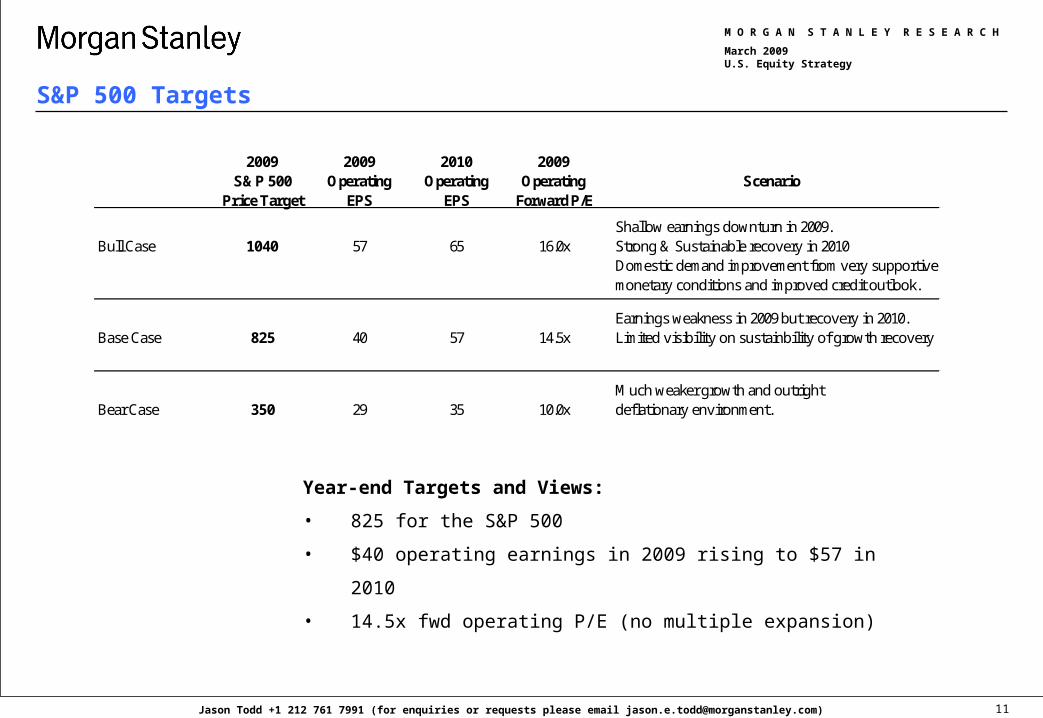

S&P 500 Targets

Year-end Targets and Views:

• 825 for the S&P 500

• $40 operating earnings in 2009 rising to $57 in 2010

• 14.5x fwd operating P/E (no multiple expansion)

2009 2009 2010 2009S&P 500 Operating Operating Operating Scenario

Price Target EPS EPS Forward P/E

Shallow earnings downturn in 2009.Bull Case 1040 57 65 16.0x Strong & Sustainable recovery in 2010

Domestic demand improvement from very supportive monetary conditions and improved credit outlook.

Earnings weakness in 2009 but recovery in 2010.Base Case 825 40 57 14.5x Limited visibility on sustainbility of growth recovery

Much weaker growth and outrightBear Case 350 29 35 10.0x deflationary environment.

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

12Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

S&P 500 Outlook

Bullish Drivers Risk measures on the rise again (VIX nearing 50)

Massive policy intervention

Valuations discounting earnings recession/corporate cash levels building

Yield curve steepening

Stronger USD

Lower energy and commodity prices

Improved inflation readings

Asset deleveraging in financials has made significant progress

Bearish Drivers Still weak housing

Significant earnings disappointments ahead

– Slowdown in revenue growth

– Margins vulnerable

– Provisioning cycle to intensify

Weakening external demand

Substantial deterioration in labor market conditions

Severe credit crunch still unfolding

Rising risk of protectionist policies

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

13Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Earnings – Rising Risk to Optimistic Consensus Estimates

US Trade Weighted Dollar, volatile but Stronger

Source: Haver, Datastream, Factset, Morgan Stanley Research.

4

6

8

10

12

14

16

18

70 73 76 79 82 85 88 91 94 97 00 03 06

After-tax corporate profitsw/ IVA & CCAdj as apercentage of corporate GDP

After-tax corporateprofits as a percentageof corporate GDP

Corporate Profits as a percentage of GDP

10

15

20

25

30

35

40

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008

10

15

20

25

30

35

40% Foreign share of US corporate profits

…A powerful headwind to foreign earnings…

83.1

60

70

80

90

100

110

120

130

140

150

Jan-73 Jan-78 Jan-83 Jan-88 Jan-93 Jan-98 Jan-03 Jan-08

…And profit marginsNegative Earnings Drivers:

Stronger USD

All time high foreign earnings contribution

Slowing non-US growth

Higher funding costs/equity dilution

Rising pension plan requirements

Inventory revaluation drag

Positive Earnings Drivers:

Falling input prices

Limited wage pressures, unit labor costs contained

Steepening yield curve

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

14Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

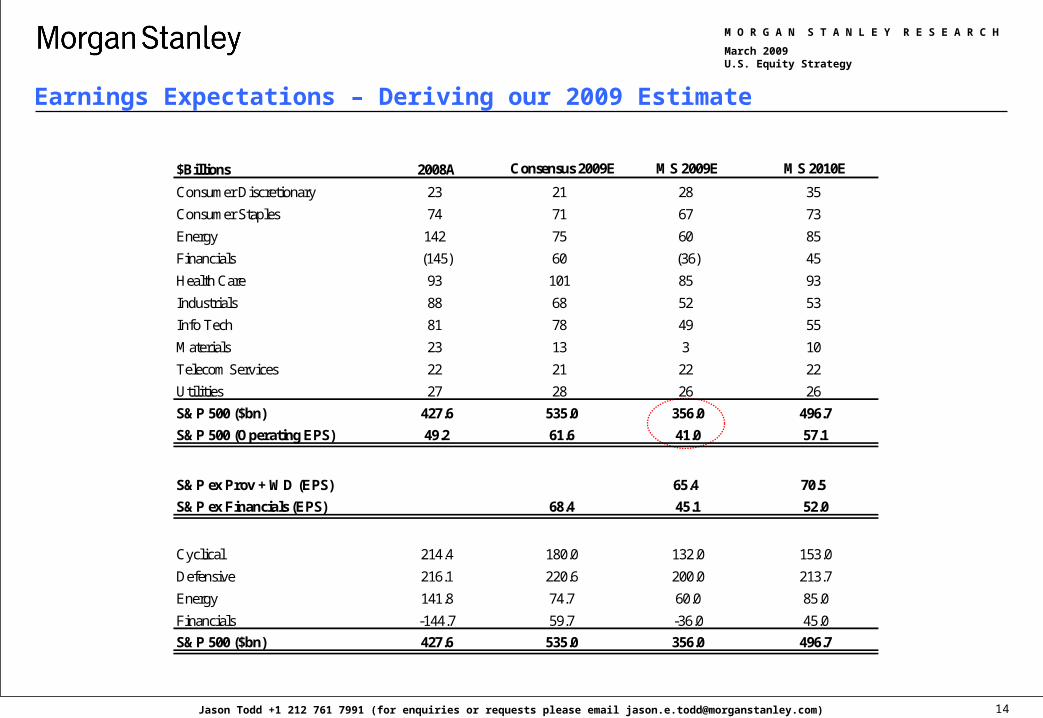

Earnings Expectations – Deriving our 2009 Estimate

$Billions 2008A Consensus 2009E MS 2009E MS 2010E

Consumer Discretionary 23 21 28 35

Consumer Staples 74 71 67 73

Energy 142 75 60 85

Financials (145) 60 (36) 45

Health Care 93 101 85 93

Industrials 88 68 52 53

Info Tech 81 78 49 55

Materials 23 13 3 10

Telecom Services 22 21 22 22

Utilities 27 28 26 26

S&P 500 ($bn) 427.6 535.0 356.0 496.7

S&P 500 (Operating EPS) 49.2 61.6 41.0 57.1

S&P ex Prov + WD (EPS) 65.4 70.5

S&P ex Financials (EPS) 68.4 45.1 52.0

Cyclical 214.4 180.0 132.0 153.0

Defensive 216.1 220.6 200.0 213.7

Energy 141.8 74.7 60.0 85.0

Financials -144.7 59.7 -36.0 45.0

S&P 500 ($bn) 427.6 535.0 356.0 496.7

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

15Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

2009 Earnings – How Much Downside to Bear Case?

$Billions MS Bear MS Base MS Bull

Consumer Discretionary 12 28 38

Consumer Staples 60 67 73

Energy 50 60 90

Financials (90) (52) 0

Health Care 80 85 95

Industrials 45 52 72

Info Tech 43 49 68

Materials (2) 3 15

Telecom Services 20 22 24

Utilities 24 26 28

S&P 500 ($bn) 242.0 340.0 503.0

S&P 500 (Operating EPS) 27.8 39.1 57.9

Probability 20% 65% 15%

Source: Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

16Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

2009-10 Earnings Revisions – A New Record in Progress....

Earnings expectations falling off a cliffRevisions To S&P 500 Consensus Forecasts

10

20

30

40

50

60

70

80

90

100

110

120

130

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

$ Pe

r S

hare

1994

Based On IBES Consensus Estimates

2008

2007

20062005

2004

2003

20022001

2000

19991998

19961995

19931992199119901989

19871988

1985 1986

1997

2009

2010

Rolling 12 mo Forward EPS

Largest Downgrades on Record

2009 non-financials consensus earnings remain elevated Cyclicals’ earnings have fallen the most on YoY basis*…

-65% -62%-57%

-20% -17%-5%

8% 10%

-100%

-75%

-50%

-25%

0%

25%

S&

P 5

00

Con

s D

isc

Mat

eria

ls

Ene

rgy

Tec

h

Indu

stri

als

Tel

ecom

Con

sS

tapl

es

Hea

lth

Car

e

Uti

liti

es

4Q08 Earnmings YoY%

-45

45

131

60

84

-145

2007

2008e

2009e

2010e

MS

Consensus

Financial Earnings $bn

392

451

601

475

552

572

2007

2008e

2009e

2010e

Non Financial Earnings $bn Earnings

Source: Datastream, FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

17Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Earnings vs. Performance – Markets Can Move Ahead of Earnings

Year (t)Earnings Growth

S&P Return(t+1) Earnings

Growth

1908 -12.1 37.4 31.01911 -19.2 0.7 18.61918 -22.7 16.2 -6.11921 -63.8 7.3 137.91927 -10.5 30.9 24.31938 -43.4 25.2 40.61942 -11.2 12.4 -8.71951 -14.1 16.5 -1.61958 -14.2 38.1 17.31970 -10.9 0.1 12.41975 -11.5 31.5 24.71982 -16.2 14.8 12.01991 -14.8 26.3 8.1

Average -20.3 19.8 23.9

…But equity performance leads earnings growth

Instances of >10% EPS decline and Positive S&P Returns

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

S&P 500 %YoY Chg vs %Chg in 12mo Forward Estimates

Grey shading represents US Recession

S&P 500

12mo Forward Estimate

s2/28/09-31.6%

1/31/87, -18.5%

12/31/01-25.2%

12/31/91, -25.0%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

S&P 500 Rolling Earnings Surprise %12mo Forward Estimates vs. Actuals

Grey shading represents US Recession

Under-estimate Earnings

Over-estimate Earnings Growth

Earnings down 32% on estimates made 12 months ago....

Source: Datastream, Robert Schiller, FactSet and Morgan Stanley Research

YearEarnings Growth

S&P Price Return

YearEarnings Growth

S&P Price Return

1956 -5.8 2.6 2007 -2.4 3.51957 -1.2 -14.3 2008E -40.6 -38.51958 -14.2 38.1 2009E -18.5 ?1959 17.3 8.5

Earnings ConsecutiveDecline Yrs of -ve EPS 'g'

1917-1921 -81% 51930-1932 -75% 31956-1958 -20% 32007-2009 -55% ? 3 ?

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

18Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Source: Morgan Stanley Research

Yield Curve Positive for Growth and Financials

Yield Curve: Fed Funds less UST 10 Year Yield

-4

-3

-2

-1

0

1

2

3

4

5

6

7

1960 1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008

NBER-Dated Recessions Fed Funds Rate Target Less 10-Year Treasury Yield average

Inverted Curve Indicates that Fed Policy is Tight

Upward-Sloping Yield Curve Indicates that Fed Policy is Accomodative

LR Average = -0.88

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

19Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

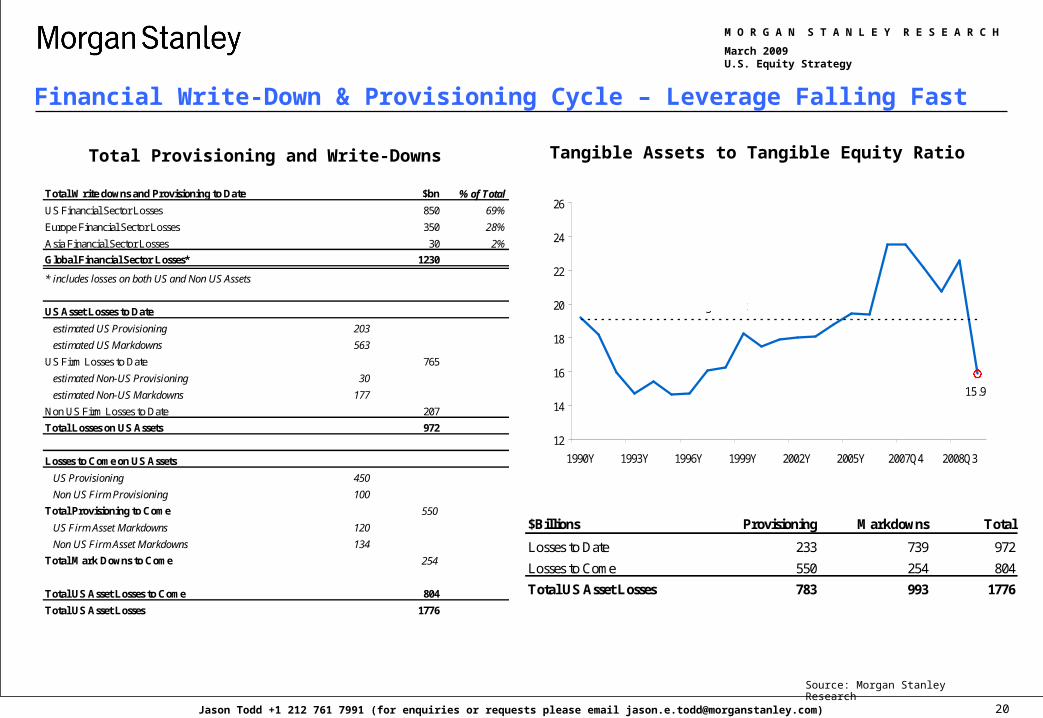

Financial Sector Scorecard

1. Provisioning and markdowns - 60% through the cycle, with listed and unlisted financials globally writing down $1200bn. Final cumulative loss estimate of $1.8tn, split evenly between markdowns and provisioning.

2. Earnings – S&P Financials posted a loss of -$145bn in 2008 and will likely post a further loss of -$36bn in 2009 (peak pre-tax, pre-provisioning earnings were $340bn).

3. Sustainable earnings – Sustainable ROE of 12% (versus 18% historically) on a book value of around $1.2tn. Alternatively, 1% ROA on 15x Tangible Assets/Tangible Equity (TA/TE) ratio ($12tn of assets).

4. Valuation – Using an implied ROE of 12%, S&P 500 Financial sector on a sustainable P/E of 3.9x. Using a 1% sustainable ROA we estimate that our selection of Financial stocks are trading on a P/E of 4.5x.

5. Deleveraging – Progress is slow due to difficult asset markets and poor pricing transparency. TA/TE down from 24x to 16x for the bulk of BKX members, already well below the long-term average of 19x.

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

20Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Financial Write-Down & Provisioning Cycle – Leverage Falling Fast

Total Provisioning and Write-Downs

Source: Morgan Stanley Research

Tangible Assets to Tangible Equity Ratio

15.9

12

14

16

18

20

22

24

26

1990Y 1993Y 1996Y 1999Y 2002Y 2005Y 2007Q4 2008Q3

15 Year Average = 19x

$bn % of Total

US Financial Sector Losses 850 69%

Europe Financial Sector Losses 350 28%

Asia Financial Sector Losses 30 2%

Global Financial Sector Losses* 1230

* includes losses on both US and Non US Assets

US Asset Losses to Date

estimated US Provisioning 203

estimated US Markdowns 563

US Firm Losses to Date 765

estimated Non-US Provisioning 30

estimated Non-US Markdowns 177

Non US Firm Losses to Date 207

Total Losses on US Assets 972

Losses to Come on US Assets

US Provisioning 450

Non US Firm Provisioning 100

Total Provisioning to Come 550

US Firm Asset Markdowns 120

Non US Firm Asset Markdowns 134

Total Mark Downs to Come 254

Total US Asset Losses to Come 804

Total US Asset Losses 1776

Total Write downs and Provisioning to Date

$Billions Provisioning Markdowns Total

Losses to Date 233 739 972

Losses to Come 550 254 804

Total US Asset Losses 783 993 1776

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

21Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Source: Morgan Stanley Research

Drivers of Delinquency Cycle – Claims & Capacity Utilization

Capacity Utilization a Good Indicator of C&I DelinquenciesClaims and Residential Mortgage Delinquencies Closely Correlated

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%Q2 1988 Q2 1990 Q2 1992 Q2 1994 Q2 1996 Q2 1998 Q2 2000 Q2 2002 Q2 2004 Q2 2006 Q2 2008

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%US capacity utilisation - All industry sadj(inverted yoy%) (LH)

US Delinquency Rates - Commercial andIndustrial Loans (yoy%)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Q2 1984 Q2 1987 Q2 1990 Q2 1993 Q2 1996 Q2 1999 Q2 2002 Q2 2005 Q2 2008-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%US Initial claims for unemployment insurance (%yoy, sadj)US residential mortgage delinquencies (% of loans, %yoy, sadj, RHS)

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

22Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Valuation – Equities Not Yet Cheap

Markets Have More Than Halved In The Current Bear Market

Decline from peak*

-60-68

-81

-63

-100

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

1870

1880

1890

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

2010

%

* Decline from inflation-adjusted peak for S&P 500. Calculated from monthly data that may under-state the exact peak

…But Valuations Haven’t Yet Reached “Cheap” Territory

S&P Trough-the-Cycle PE Ratio*

4.9 5.5 6.8

46.1

12.9

0

5

10

15

20

25

30

35

40

45

50

1880

1890

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

2010

PE R

atio

* Graham-Dodd Price-Earnings, based on 10Yr real average earnings

Long Term Average: 16.4

12M Trailing PE

S&P 500 ROE Multiple Expansion to be driven by Declining Inflation

12.6

13.8

18.317.2 17.1

15.4 15.2

9.610.8

8.49.0

8.1

0

2

4

6

8

10

12

14

16

18

20

<0% 0-1% 1-2% 2-3% 3-4% 4-5% 5-6% 6-7% 7-8% 8-9% 9-10% >10%

Level of Y/Y Headline CPI Inflation

Med

ian

S&

P 5

00 L

TM

P/E

S&P 500's Median Trailing P/E Multiple in Different Inflation Environments, Apr '53 to Dec '08

Key Inflection PointsSweet Spot

Source: FactSet and Morgan Stanley Research

11.4%

13.0%

2%

6%

10%

14%

18%

22%

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006

S&P 500 S&P 500 (Ex-Financials)

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

23Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

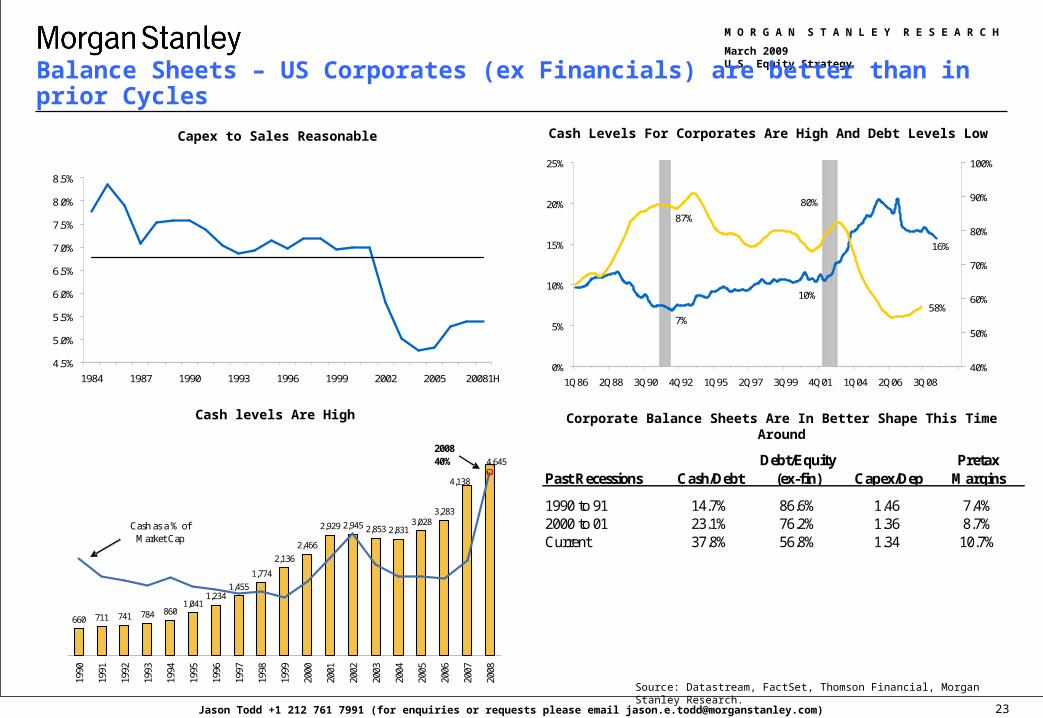

Capex to Sales Reasonable

Balance Sheets – US Corporates (ex Financials) are better than in prior Cycles

Source: Datastream, FactSet, Thomson Financial, Morgan Stanley Research.

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

1984 1987 1990 1993 1996 1999 2002 2005 20081H

Capex to Sales - S&P 500

Average = 6.8

Past Recessions Cash/DebtDebt/Equity

(ex-fin) Capex/DepPretax

Margins

1990 to 91 14.7% 86.6% 1.46 7.4%2000 to 01 23.1% 76.2% 1.36 8.7%Current 37.8% 56.8% 1.34 10.7%

Corporate Balance Sheets Are In Better Shape This Time Around

16%

7%

10%58%

87%

80%

0%

5%

10%

15%

20%

25%

1Q86 2Q88 3Q90 4Q92 1Q95 2Q97 3Q99 4Q01 1Q04 2Q06 3Q08

40%

50%

60%

70%

80%

90%

100%Cash to Total Capital Employed (ex Fin)

Debt to Equity (ex Fin) - rhs

Cash Levels For Corporates Are High And Debt Levels Low

Cash levels Are High

660 711 741 784 8601,041

1,2341,455

1,774

2,136

2,466

2,929 2,945 2,853 2,8313,028

3,283

4,645

4,138

200840%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Cash as a % of Market Cap

US-Based Cash as percentage of Market Cap

Market cap includes total market cap of NYSE, Amex and NASDAQ (World Federation of Exchanges)-updated till Nov 08; Cash in $ bn includes MMF assets, S&P 500, ex fin cash and cash with equity MFs

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

24Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Recession Analysis – How does 2008 Compare?

Acknowledgement Capitulation Full Impact Recovery

S&P 500 Peak

Start of Recession

S&P 500 Trough

End of Recession

Recession Duration (months)

Peak to Start of

Recession (months)

Peak to Start of Recession

(%)

Start of Recession to

Trough (months)

Start of Recession to Trough (%)

Peak to Trough

(months)

Peak to Trough

(%)

Trough to End of

Recession (%)

1/5/53 7/31/53 9/14/53 5/28/54 10 7 -7.1% 2 -8.2% 8 -14.8% 28.5%

7/15/57 8/30/57 10/22/57 4/30/58 8 2 -8.0% 2 -13.8% 3 -20.7% 11.4%

1/5/60 4/29/60 10/25/60 2/28/61 10 4 -10.0% 6 -3.8% 10 -13.4% 21.3%

5/16/69 12/31/69 5/26/70 11/30/70 11 8 -13.1% 5 -24.7% 13 -34.6% 25.8%

1/11/73 10/31/73 10/4/74 3/31/75 17 10 -9.9% 11 -42.4% 21 -48.2% 33.7%

2/13/80 1/31/80 3/27/80 7/31/80 6 -3.6% 2 -14.0% 1 -17.1% 23.9%

11/28/80 7/31/81 8/12/82 11/30/82 16 8 -6.8% 13 -21.8% 21 -27.1% 35.3%

7/17/90 7/31/90 10/11/90 3/28/91 8 0.5 -3.1% 2 -17.0% 3 -19.6% 27.0%

3/27/00 3/30/01 9/21/01 11/30/01 8 12 -23.9% 6 -16.8% 18 -36.6% 18.0%

10/9/07 12/3/07 11/20/08 2 -5.9% 12 -48.9% 14 -51.9%

Average 11 6 -9.1% 6 -21.1% 11 -28.4% 25.0%

Median 10 7 -7.5% 5 -16.9% 11 -23.9% 25.8%

ROE Corporate profits/GDP S&P 500 Peak to Trough

ROE Peak ROE Trough Peak Trough Peak TroughDuration (Months) ROE Decline

Profit Margin Decline

Sep-57 Sep-58 13.2% 9.8% 10.9% 8.8% 12 -3.4% -2.1%Sep-59 Jun-61 11.2% 9.0% 10.6% 9.0% 21 -2.2% -1.6%Sep-69 Dec-70 11.7% 9.8% 9.1% 7.4% 15 -2.0% -1.7%Sep-74 Dec-75 14.6% 11.2% 11.5% 8.9% 15 -3.4% -2.6%Feb-80 Sep-80 16.4% 14.7% 11.5% 9.5% 7 -1.7% -2.0%Jun-81 Mar-83 14.6% 11.0% 8.3% 6.5% 21 -3.7% -1.8%Aug-90 Dec-91 13.4% 10.6% 8.3% 8.1% 16 -2.8% -0.2%Aug-00 Mar-02 19.9% 13.0% 8.8% 7.8% 19 -6.9% -0.9%Apr-07 Dec-08 18.1% 13.6% 17.8% 14.0% 20 -4.4% -3.8%

Average 14.4% 11.1% 9.9% 8.3% 16 -3.3% -1.6%Median 14.0% 10.8% 9.9% 8.5% 16 -3.1% -1.8%

Source: FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

25Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

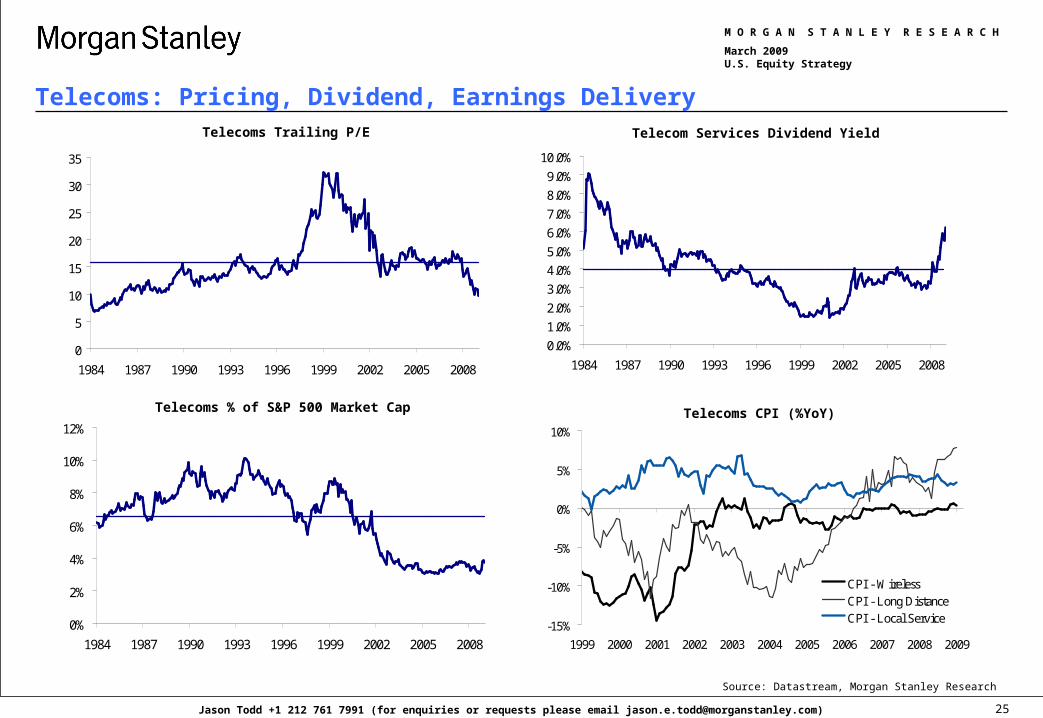

Telecoms: Pricing, Dividend, Earnings Delivery

0

5

10

15

20

25

30

35

1984 1987 1990 1993 1996 1999 2002 2005 2008

-15%

-10%

-5%

0%

5%

10%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

CPI - Wireless

CPI - Long Distance

CPI - Local Service

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

1984 1987 1990 1993 1996 1999 2002 2005 2008

Telecom Services Dividend Yield

0%

2%

4%

6%

8%

10%

12%

1984 1987 1990 1993 1996 1999 2002 2005 2008

Telecoms % of S&P 500 Market Cap

Telecoms Trailing P/E

Telecoms CPI (%YoY)

Source: Datastream, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

26Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Healthcare – Dividend + Earnings Delivery

Healthcare Relative Trailing P/E

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1984 1987 1990 1993 1996 1999 2002 2005 2008

New relative multiple range

(patent, price, pipeline risk)

Ave 1984-2001 = 1.4xAve 2002-2008 = 1.1x

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

Jan-77 Jan-80 Jan-83 Jan-86 Jan-89 Jan-92 Jan-95 Jan-98 Jan-01 Jan-04 Jan-07

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Relative EPS Relative performance (RHS)

US DS Pharamceuticals Relative EPS vs Relative performance

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Jan-73 Jan-77 Jan-81 Jan-85 Jan-89 Jan-93 Jan-97 Jan-01 Jan-05

Rising DY corresponds

with falling LTG

Pharma

S&P 500

Dividend Yield - S&P 500 vs. US Pharma

Source: Morgan Stanley Research

Earnings certainty, attractive and safe dividend/buyback yield and decade low valuations;

Downside risks well recognized and priced (patent cliff) with upside risk (product pipeline expectations, restructuring) underappreciated;

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

27Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Global Construction Activity Rapidly Deteriorating

Global Construction Activity Rapidly Deteriorating(%)

%YoY11 Year Low

(%)11 year High

(%)Current (%)

Australia -5.8 24.7 12.1

Brazil -2.1 23.1 16.3

China 10.2 25.7 12.4

France -2.5 13.8 11.0

Germany -6.3 8.5 7.7

India 8.2 27.9 24.5

Japan -7.3 1.3 -7.3

Spain -0.7 16.6 -0.7

UK 0.0 12.5 0.0

US -8.6 11.1 -8.6

Composite 3.3 11.0 3.3

Global Construction Composite

0%

2%

4%

6%

8%

10%

12%

1996 1998 2000 2002 2004 2006 2008 2010

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Jan-74 Jan-78 Jan-82 Jan-86 Jan-90 Jan-94 Jan-98 Jan-02 Jan-06

%YoY Industrials Earnings

Source: FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

28Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

• The top 15 US industrial companies get 66% of revenues from the US

• Even excluding the rails, the percentage of revenues from the US is around 60%

• Most of the US exposure is concentrated in construction, transportation equipment and industrial equipment, all vulnerable to the unfolding US recession

•Biggest threat is current global financial market conditions and rising cost of funding, causing EM project related spending to slow. Project cancellation has already increased exponentially

Industrial Earnings Trough after Recession, but They Always Decline...

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Jan-74 Jan-78 Jan-82 Jan-86 Jan-90 Jan-94 Jan-98 Jan-02 Jan-06

%YoY Industrials Earnings

-10%

-5%

0%

5%

10%

15%

Oct-95 Oct-97 Oct-99 Oct-01 Oct-03 Oct-05 Oct-07

-10%

-5%

0%

5%

10%

15%

20%

China IP YoY India IP YoY

Brazil IP YoY Russia IP YoY

%YoY Industrial Production Growth (6 mo. avg)

Source: Datastream, FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

29Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

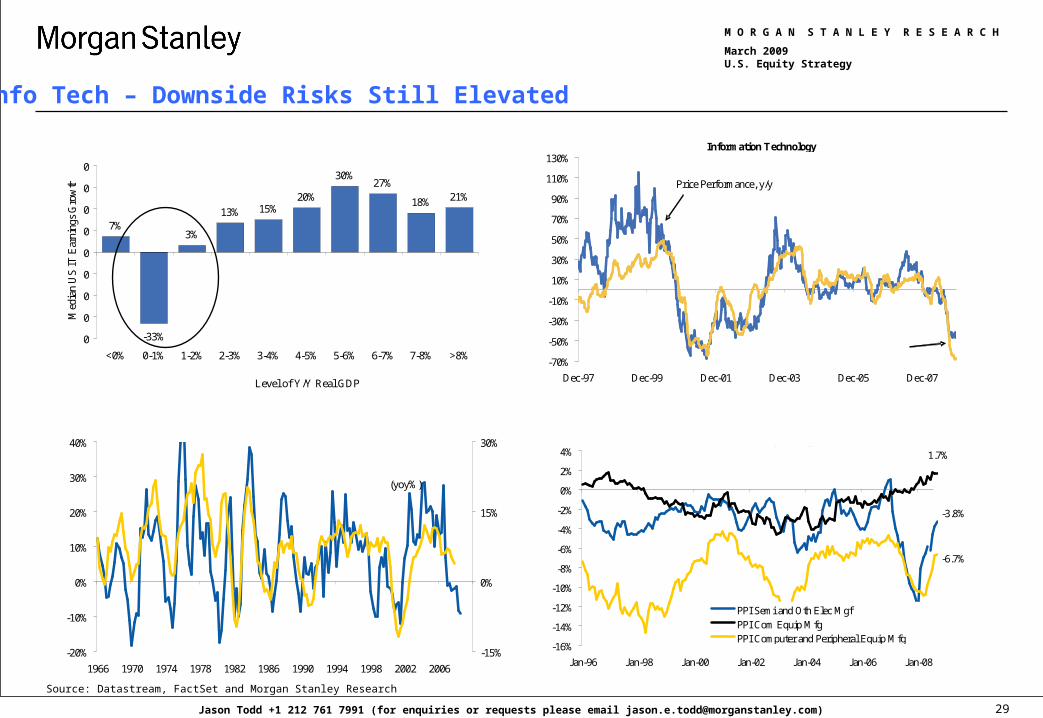

Info Tech – Downside Risks Still Elevated

-70%

-50%

-30%

-10%

10%

30%

50%

70%

90%

110%

130%

Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07

Three Month Earnings Revision Factor

[(#Up - #Down) / Total # Estimates]

Price Performance, y/y

Information Technology

7%

-33%

3%

13% 15%20%

30%27%

18% 21%

0

0

0

0

0

0

0

0

0

<0% 0-1% 1-2% 2-3% 3-4% 4-5% 5-6% 6-7% 7-8% >8%

Level of Y/Y Real GDP

Med

ian

US

IT

Ear

ning

s G

row

th

US IT Earnings Growth During Different GDP Growth Environments

2008/2009 GDP Growth Range

-20%

-10%

0%

10%

20%

30%

40%

1966 1970 1974 1978 1982 1986 1990 1994 1998 2002 2006

-15%

0%

15%

30%US corporate

profits (yoy%)

US nom business fixed investment (yoy% 3qtr lag)

US Profits vs IT Capex Growth

-3.8%

1.7%

-6.7%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

Jan-96 Jan-98 Jan-00 Jan-02 Jan-04 Jan-06 Jan-08

PPI Semi and Oth Elec Mgf PPI Com Equip MfgPPI Computer and Peripheral Equip Mfg

Tech Sector PPI (%YoY)

Source: Datastream, FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

30Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

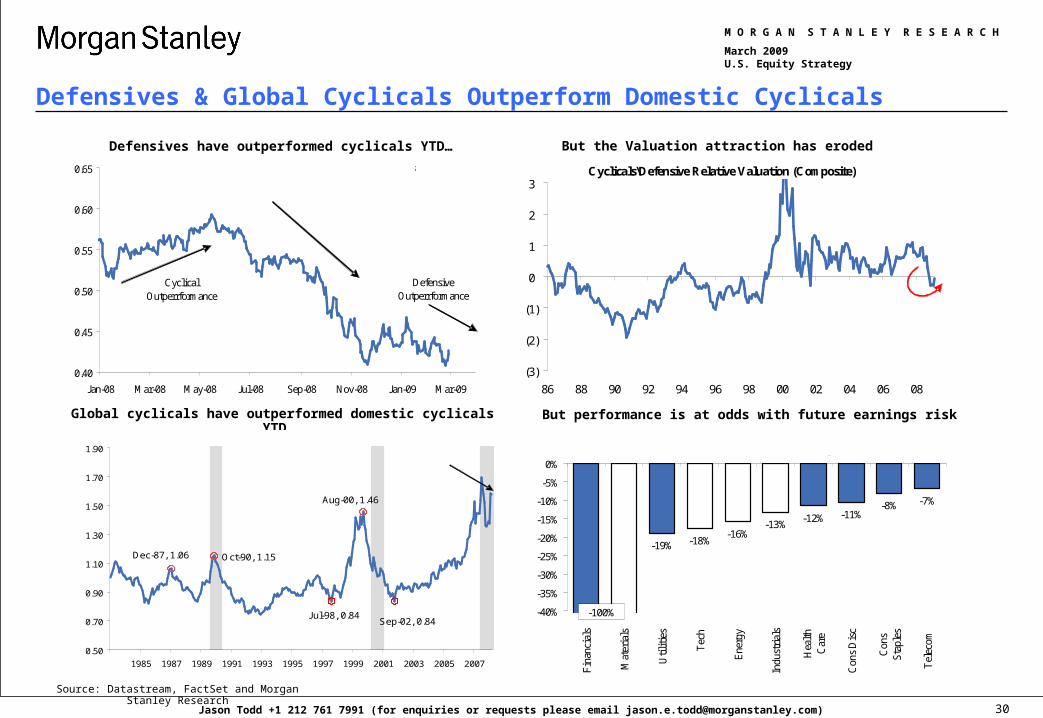

Defensives & Global Cyclicals Outperform Domestic Cyclicals

Defensives have outperformed cyclicals YTD… But the Valuation attraction has eroded

0.40

0.45

0.50

0.55

0.60

0.65

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09

Performance of US Cyclicals relative to US Defensives

Defensive Outperformance

Cyclical Outperrformance

DefensiveOutperrformance

Global cyclicals have outperformed domestic cyclicals YTD..

-19% -18%-16%

-13%-12% -11%

-8% -7%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

Fin

anci

als

Mat

eria

ls

Uti

liti

es

Tec

h

Ene

rgy

Indu

stri

als

Hea

lth

Car

e

Con

s D

isc

Con

sS

tapl

es

Tel

ecom

% Difference MS vs. Consensus 2009 Earnings Estimates

-100%

Aug-00, 1.46

Dec-87, 1.06 Oct-90, 1.15

Sep-02, 0.84Jul-98, 0.84

0.50

0.70

0.90

1.10

1.30

1.50

1.70

1.90

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007

Grey shading represents US recession

Head Fake?

But performance is at odds with future earnings risk

Cyclicals\Defensive Relative Valuation (Composite)

(3)

(2)

(1)

0

1

2

3

86 88 90 92 94 96 98 00 02 04 06 08

Cyclicals Relatively Attractive

Defensives Relatively Attractive

Composite Indicator is an average of relative p/sales, p/e, and p/book z-scores.

Source: Datastream, FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

31Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

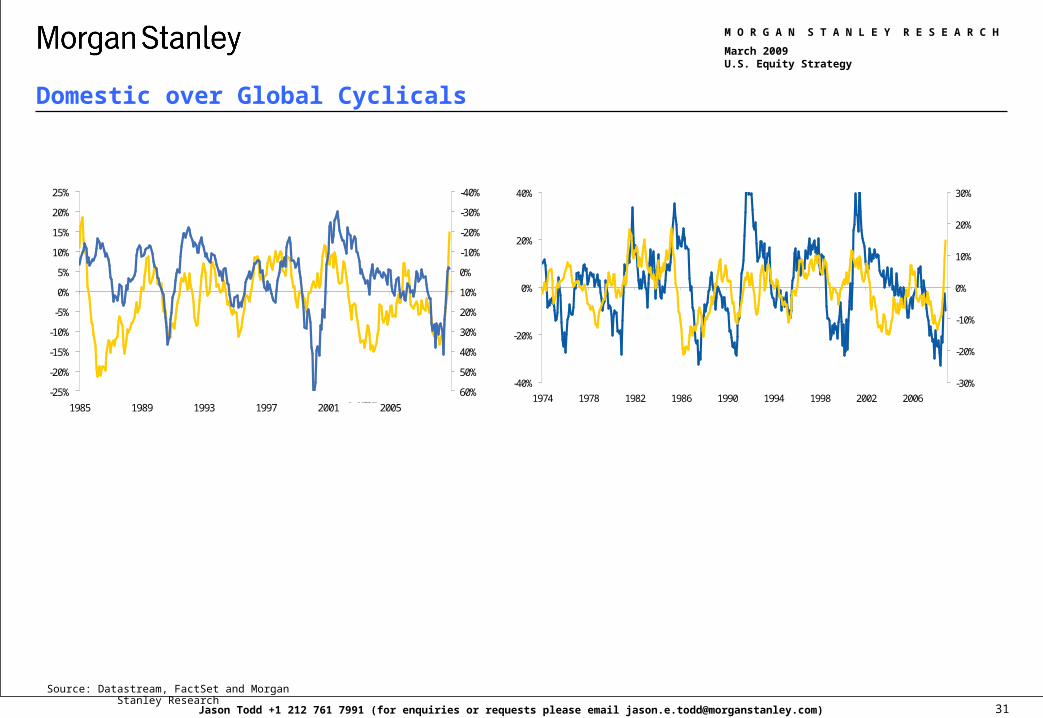

Domestic over Global Cyclicals

-40%

-20%

0%

20%

40%

1974 1978 1982 1986 1990 1994 1998 2002 2006

-30%

-20%

-10%

0%

10%

20%

30%

US Banks vs SPX

TWD %YoY (rhs)

US Bank Relative to SPX vs TWD

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1985 1989 1993 1997 2001 2005

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Global Cyclicals Relative to US Domestic Cyclicals vs TWD

Trade-Weighted Dollar

Source: Datastream, FactSet and Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

32Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

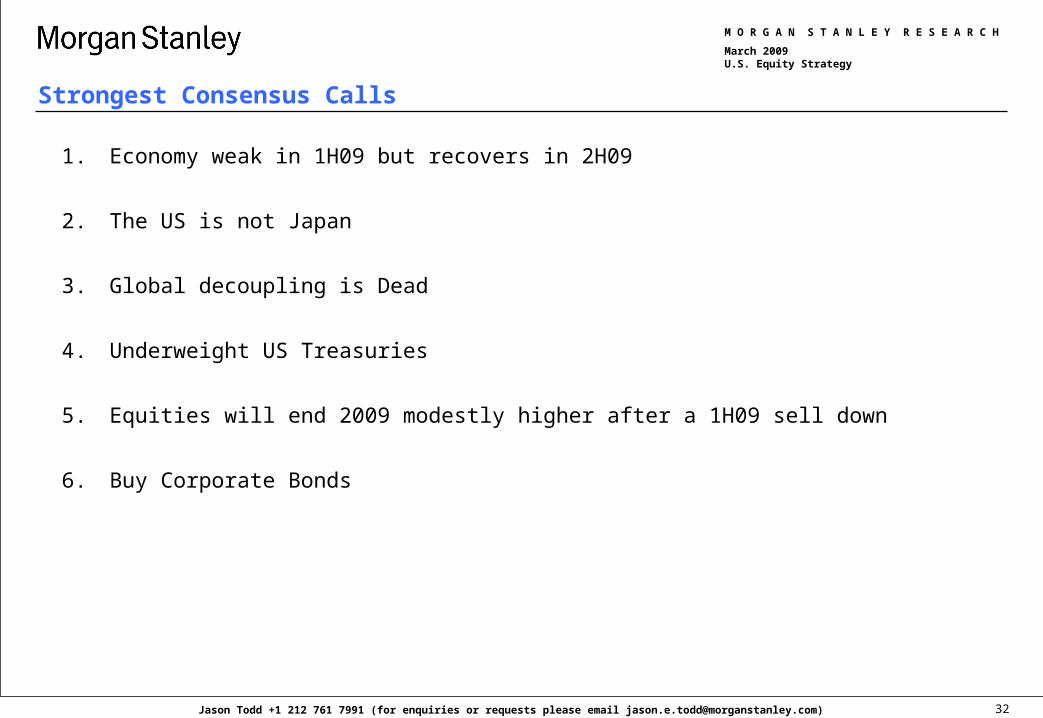

Strongest Consensus Calls

1. Economy weak in 1H09 but recovers in 2H09

2. The US is not Japan

3. Global decoupling is Dead

4. Underweight US Treasuries

5. Equities will end 2009 modestly higher after a 1H09 sell down

6. Buy Corporate Bonds

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

33Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

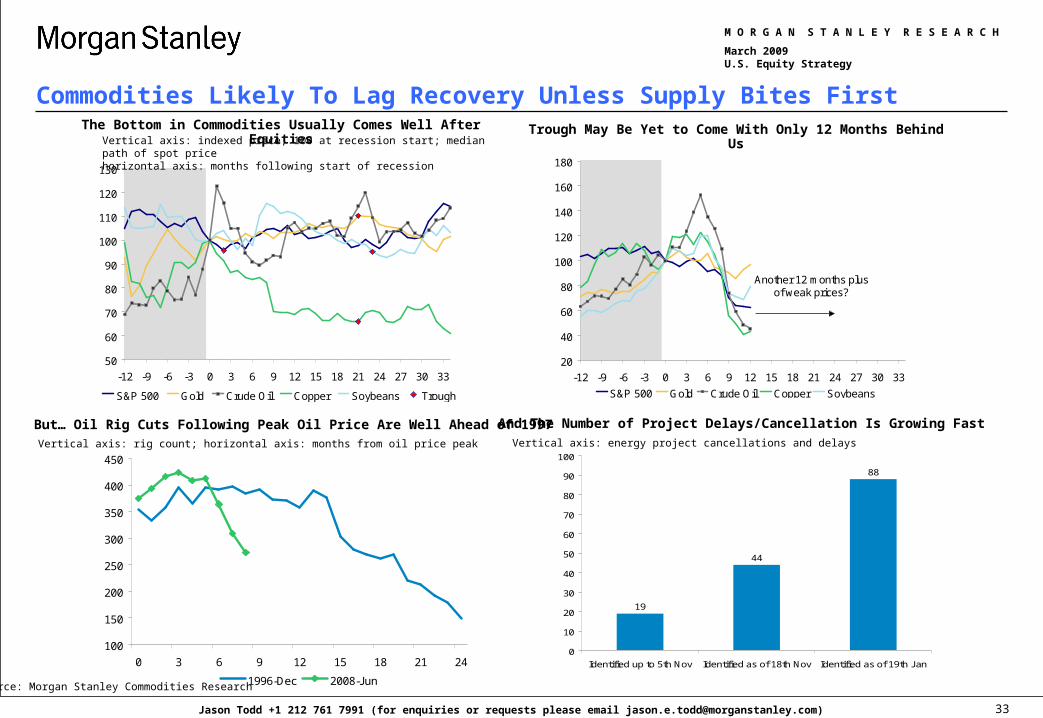

Commodities Likely To Lag Recovery Unless Supply Bites First

50

60

70

80

90

100

110

120

130

-12 -9 -6 -3 0 3 6 9 12 15 18 21 24 27 30 33

S&P 500 Gold Crude Oil Copper Soybeans Trough

20

40

60

80

100

120

140

160

180

-12 -9 -6 -3 0 3 6 9 12 15 18 21 24 27 30 33

S&P 500 Gold Crude Oil Copper Soybeans

Another 12 months plus of weak prices?

The Bottom in Commodities Usually Comes Well After Equities Trough May Be Yet to Come With Only 12 Months Behind Us

100

150

200

250

300

350

400

450

0 3 6 9 12 15 18 21 24

1996-Dec 2008-Jun

But… Oil Rig Cuts Following Peak Oil Price Are Well Ahead of 1997Vertical axis: rig count; horizontal axis: months from oil price peak

And The Number of Project Delays/Cancellation Is Growing Fast

19

44

88

0

10

20

30

40

50

60

70

80

90

100

Identified up to 5th Nov Identified as of 18th Nov Identified as of 19th Jan

Vertical axis: energy project cancellations and delays

Vertical axis: indexed price, 100 at recession start; median path of spot pricehorizontal axis: months following start of recession

Source: Morgan Stanley Commodities Research

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

34Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Core US Equity PortfolioMarket Ann. Weight Performance Price

Price MS Value Div 2009e MS Rec vs from Date atTicker Name Industry Group/ Industry 3/12/2009 Rating ($ Mil) Yield P/E Weight S&P 500 Inclusion % Added Inclusion

S&P 500 Index 750.74 100.0 0.0

Consumer Discretionary 141.53 11.0 2.6 -41.9NKE Nike Inc. (Cl B) Consumer Durables & Apparel 44.59 NC 17,039 2.24 9.08 3.5 -27.8 1/4/08 61.74MCD McDonald's Corp. Consumer Services 52.17 O / I 56,875 3.83 13.35 3.5 -8.6 1/4/08 57.05LOW Lowe's Cos. Retailing 15.61 O / I 22,132 2.18 14.46 2.0 -30.1 12/5/08 22.34COH Coach Inc. Consumer Durables & Apparel 14.46 O / C 4,574 0.00 7.65 2.0 -49.3 9/18/08 28.52

Consumer Staples 209.09 14.5 1.5 -28.6MO Altria Group Inc. Food Beverage & Tobacco 16.30 E / A 33,770 7.85 9.39 3.0 -29.4 1/4/08 23.10PM Philip Morris Int Food Beverage & Tobacco 34.64 O / A 68,075 6.24 11.88 3.5 -32.2 3/28/08 51.06KR Kroger Co. Food & Staples Retailing 21.30 O / A 13,585 1.69 10.30 2.5 -22.3 12/5/08 27.42WMT Wal-Mart Stores Inc. Food & Staples Retailing 48.94 O / I 106,114 1.94 8.15 3.0 -1.4 2/6/09 49.63CL Colgate-Palmolive Household & Personal Products 56.51 NC 28,456 2.83 13.34 2.5 -28.3 1/4/08 78.78

Energy 332.48 11.0 -2.7 -44.0CVX Chevron Corp. Oil Gas & Consumable Fuels 63.40 NC 124,386 4.10 12.52 3.0 -14.8 12/5/08 74.42MRO Marathon Oil Corp. Oil Gas & Consumable Fuels 23.57 NC 15,939 4.07 8.31 2.0 -55.9 5/19/08 53.44COP ConocoPhillips Oil Gas & Consumable Fuels 37.39 NC 56,621 5.03 10.19 3.0 -56.3 1/4/08 85.56VLO Valero Energy Corp. Oil Gas & Consumable Fuels 17.58 NC 8,808 3.41 5.79 3.0 -72.6 1/4/08 64.14

Financials 109.07 9.5 -0.9 -70.4BK Bank of New York Mellon Diversified Financials 24.66 O / I 25,855 3.89 8.17 1.5 -44.4 5/7/08 44.37STT State Street Corp. Diversified Financials 23.85 O / I 9,486 4.03 7.39 1.5 -70.9 1/4/08 81.82JPM JPMorgan Chase & Co. Diversified Financials 23.20 O / I 76,140 6.55 11.27 2.0 -37.5 6/11/08 37.13WFC Wells Fargo & Co. Banks 13.95 O / I 50,133 9.75 12.93 1.5 -48.9 11/12/08 27.30MET MetLife Inc. Insurance 17.30 O / I 12,118 4.28 4.16 1.5 -71.7 5/7/08 61.10CB Chubb Corp. Insurance 37.13 NC 12,684 3.56 6.91 1.5 -28.4 12/5/08 51.85

Health Care 270.89 18.7 3.2 -33.0BDX Becton Dickinson Health Care Equip & Srvs 63.95 O / A 14,969 2.06 12.65 2.5 -27.1 1/4/08 87.76AET Aetna Inc. Health Care Equip & Srvs 23.42 NC 9,881 0.17 5.58 1.5 -58.2 1/4/08 55.97AMGN Amgen Inc. Biotechnology 50.27 O / I 50,084 0.00 10.55 3.0 -16.9 7/26/08 60.48ABT Abbott Laboratories Pharmaceuticals 46.65 O / A 68,999 3.09 12.07 3.0 -16.4 1/4/08 55.79JNJ Johnson & Johnson Pharmaceuticals 49.00 O / A 132,902 3.76 10.78 2.5 -25.6 1/4/08 65.84BMY Bristol-Myers Squibb Co. Pharmaceuticals 20.78 NC 41,124 5.97 10.76 2.5 -6.5 7/18/08 22.23TEVA Teva Pharmaceutical Pharmaceuticals 44.30 E / A 34,465 1.17 15.05 1.7 -7.4 1/4/08 47.83WYE Wyeth Pharmaceuticals 42.78 NC 56,964 2.81 11.82 2.0 25.1 12/8/08 34.20

Industrials 150.89 8.0 -1.7 -55.8DHR Danaher Corp. Capital Goods 54.42 E / C 13,326 0.22 11.30 2.0 -35.8 1/4/08 84.74UTX United Technologies Corp. Capital Goods 41.80 E / C 39,032 3.68 9.61 2.0 -14.7 12/5/08 49.01BA Boeing Co. Capital Goods 33.63 O / C 24,381 5.00 6.46 2.0 -14.9 12/5/08 39.53LMT Lockheed Martin Corp. Capital Goods 61.02 O / C 19,370 3.74 6.71 2.0 -45.4 9/15/08 111.69

Information Technology 224.95 14.5 -3.3 -41.4TXN Texas Instruments Inc. Semis & Semi Equip 15.94 O / I 20,367 2.76 45.81 2.5 9.5 12/5/08 14.56ACN Accenture Ltd. Software & Services 30.05 NC 18,235 1.66 10.48 2.0 -13.9 1/4/08 34.91ORCL Oracle Corp. Software & Services 15.63 O / A 60,093 0.00 8.39 2.5 -23.9 1/31/08 20.55CSCO Cisco Systems Inc. Tech Hardware & Equip 15.51 O / I 90,640 0.00 15.04 2.0 -9.0 2/6/09 17.04NOK Nokia Corp. (ADR) Tech Hardware & Equip 11.04 O / I 47,630 7.56 12.03 3.0 -45.0 9/18/08 20.07IBM IBM Tech Hardware & Equip 90.40 O / I 119,057 2.21 10.52 2.5 -10.6 1/4/08 101.13

Materials 121.97 1.5 -1.7 -52.0DD DuPont Chemicals 19.06 NC 16,558 8.60 9.09 1.5 -21.0 12/5/08 24.12

Telecom Services 97.74 7.3 3.3 -40.5WIN Windstream Corp. Diversified Telecom 7.18 O / A 3,058 13.93 8.22 2.3 -40.0 3/12/09 11.97T AT&T Inc. Diversified Telecom 24.35 O / A 137,602 6.74 11.73 2.5 -40.5 1/4/08 40.89VOD Vodafone Group PLC (ADS) Diversified Telecom 16.44 E / A 87,142 8.23 4.44 2.5 -14.6 12/5/08 19.250.0

Utilities 117.60 4.0 -0.1 -45.2AEP American Electric Power Electric Utilities 25.02 NC 9,972 6.55 7.73 2.0 -45.9 1/4/08 46.29EXC Exelon Corp. Electric Utilities 41.38 NC 26,416 5.07 2.0 -49.6 1/4/08 82.03

Portfolio Performance since Inception -47.26

Average 43,839 4.01 10.76

S&P 500 3.22 11.50 -45.18Relative Return -2.08

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

35Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

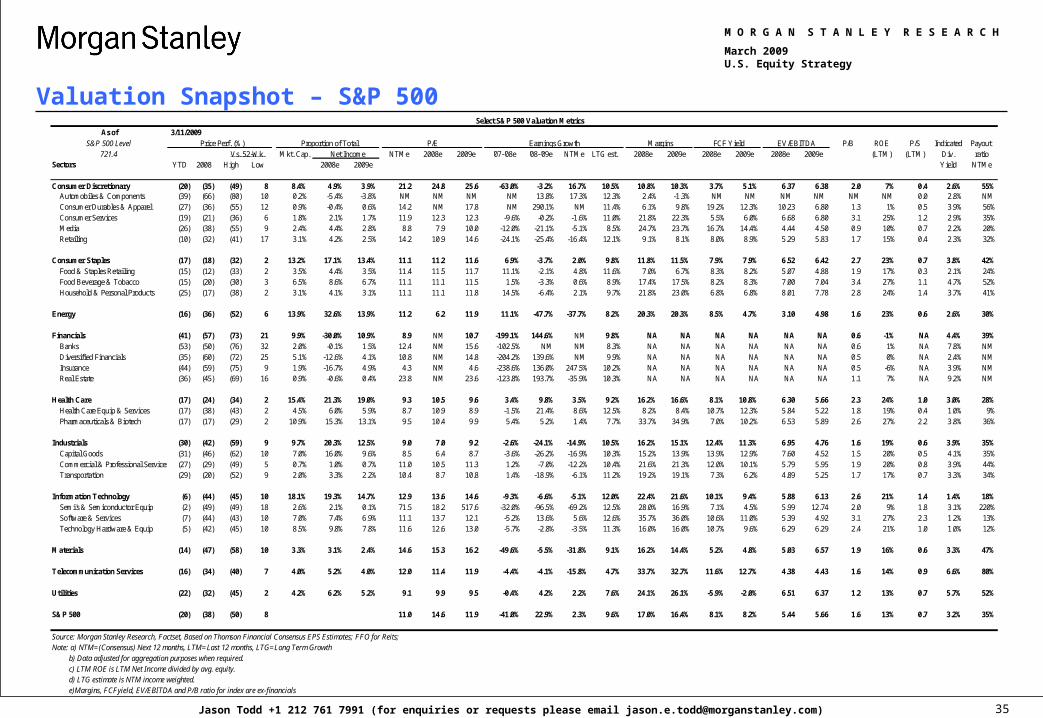

Valuation Snapshot – S&P 500Select S&P 500 Valuation Metrics

As of 3/11/2009S&P 500 Level Price Perf. (%) Proportion of Total P/E Earnings Growth Margins FCF Yield EV/EBITDA P/B ROE P/S Indicated Payout

721.4 Vs. 52-Wk. Mkt. Cap. Net Income NTMe 2008e 2009e '07-'08e '08-'09e NTMe LTG est. 2008e 2009e 2008e 2009e 2008e 2009e (LTM) (LTM) Div. ratioSectors YTD 2008 High Low 2008e 2009e Yield NTMe

Consumer Discretionary (20) (35) (49) 8 8.4% 4.9% 3.9% 21.2 24.8 25.6 -63.0% -3.2% 16.7% 10.5% 10.8% 10.3% 3.7% 5.1% 6.37 6.38 2.0 7% 0.4 2.6% 55%Automobiles & Components (39) (66) (80) 10 0.2% -5.4% -3.8% NM NM NM NM 13.8% 17.3% 12.3% 2.4% -1.3% NM NM NM NM NM NM 0.0 2.8% NMConsumer Durables & Apparel (27) (36) (55) 12 0.9% -0.4% 0.6% 14.2 NM 17.8 NM 290.1% NM 11.4% 6.1% 9.8% 19.2% 12.3% 10.23 6.80 1.3 1% 0.5 3.9% 56%Consumer Services (19) (21) (36) 6 1.8% 2.1% 1.7% 11.9 12.3 12.3 -9.6% -0.2% -1.6% 11.0% 21.8% 22.3% 5.5% 6.0% 6.68 6.80 3.1 25% 1.2 2.9% 35%Media (26) (38) (55) 9 2.4% 4.4% 2.8% 8.8 7.9 10.0 -12.0% -21.1% -5.1% 8.5% 24.7% 23.7% 16.7% 14.4% 4.44 4.50 0.9 10% 0.7 2.2% 20%Retailing (10) (32) (41) 17 3.1% 4.2% 2.5% 14.2 10.9 14.6 -24.1% -25.4% -16.4% 12.1% 9.1% 8.1% 8.0% 8.9% 5.29 5.83 1.7 15% 0.4 2.3% 32%

Consumer Staples (17) (18) (32) 2 13.2% 17.1% 13.4% 11.1 11.2 11.6 6.9% -3.7% 2.0% 9.8% 11.8% 11.5% 7.9% 7.9% 6.52 6.42 2.7 23% 0.7 3.8% 42%Food & Staples Retailing (15) (12) (33) 2 3.5% 4.4% 3.5% 11.4 11.5 11.7 11.1% -2.1% 4.8% 11.6% 7.0% 6.7% 8.3% 8.2% 5.07 4.88 1.9 17% 0.3 2.1% 24%Food Beverage & Tobacco (15) (20) (30) 3 6.5% 8.6% 6.7% 11.1 11.1 11.5 1.5% -3.3% 0.6% 8.9% 17.4% 17.5% 8.2% 8.3% 7.00 7.04 3.4 27% 1.1 4.7% 52%Household & Personal Products (25) (17) (38) 2 3.1% 4.1% 3.1% 11.1 11.1 11.8 14.5% -6.4% 2.1% 9.7% 21.8% 23.0% 6.8% 6.8% 8.01 7.78 2.8 24% 1.4 3.7% 41%

Energy (16) (36) (52) 6 13.9% 32.6% 13.9% 11.2 6.2 11.9 11.1% -47.7% -37.7% 8.2% 20.3% 20.3% 8.5% 4.7% 3.10 4.98 1.6 23% 0.6 2.6% 30%

Financials (41) (57) (73) 21 9.9% -30.0% 10.9% 8.9 NM 10.7 -199.1% 144.6% NM 9.8% NA NA NA NA NA NA 0.6 -1% NA 4.4% 39%Banks (53) (50) (76) 32 2.0% -0.1% 1.5% 12.4 NM 15.6 -102.5% NM NM 8.3% NA NA NA NA NA NA 0.6 1% NA 7.8% NMDiversified Financials (35) (60) (72) 25 5.1% -12.6% 4.1% 10.8 NM 14.8 -204.2% 139.6% NM 9.9% NA NA NA NA NA NA 0.5 0% NA 2.4% NMInsurance (44) (59) (75) 9 1.9% -16.7% 4.9% 4.3 NM 4.6 -238.6% 136.0% 247.5% 10.2% NA NA NA NA NA NA 0.5 -6% NA 3.9% NMReal Estate (36) (45) (69) 16 0.9% -0.6% 0.4% 23.8 NM 23.6 -123.8% 193.7% -35.9% 10.3% NA NA NA NA NA NA 1.1 7% NA 9.2% NM

Health Care (17) (24) (34) 2 15.4% 21.3% 19.0% 9.3 10.5 9.6 3.4% 9.8% 3.5% 9.2% 16.2% 16.6% 8.1% 10.8% 6.30 5.66 2.3 24% 1.0 3.0% 28%Health Care Equip & Services (17) (38) (43) 2 4.5% 6.0% 5.9% 8.7 10.9 8.9 -1.5% 21.4% 8.6% 12.5% 8.2% 8.4% 10.7% 12.3% 5.84 5.22 1.8 19% 0.4 1.0% 9%Pharmaceuticals & Biotech (17) (17) (29) 2 10.9% 15.3% 13.1% 9.5 10.4 9.9 5.4% 5.2% 1.4% 7.7% 33.7% 34.9% 7.0% 10.2% 6.53 5.89 2.6 27% 2.2 3.8% 36%

Industrials (30) (42) (59) 9 9.7% 20.3% 12.5% 9.0 7.0 9.2 -2.6% -24.1% -14.9% 10.5% 16.2% 15.1% 12.4% 11.3% 6.95 4.76 1.6 19% 0.6 3.9% 35%Capital Goods (31) (46) (62) 10 7.0% 16.0% 9.6% 8.5 6.4 8.7 -3.6% -26.2% -16.9% 10.3% 15.2% 13.9% 13.9% 12.9% 7.60 4.52 1.5 20% 0.5 4.1% 35%Commercial & Professional Services (27) (29) (49) 5 0.7% 1.0% 0.7% 11.0 10.5 11.3 1.2% -7.0% -12.2% 10.4% 21.6% 21.3% 12.0% 10.1% 5.79 5.95 1.9 20% 0.8 3.9% 44%Transportation (29) (20) (52) 9 2.0% 3.3% 2.2% 10.4 8.7 10.8 1.4% -18.9% -6.1% 11.2% 19.2% 19.1% 7.3% 6.2% 4.89 5.25 1.7 17% 0.7 3.3% 34%

Information Technology (6) (44) (45) 10 18.1% 19.3% 14.7% 12.9 13.6 14.6 -9.3% -6.6% -5.1% 12.0% 22.4% 21.6% 10.1% 9.4% 5.88 6.13 2.6 21% 1.4 1.4% 18%Semi's & Semiconductor Equip (2) (49) (49) 18 2.6% 2.1% 0.1% 71.5 18.2 517.6 -32.0% -96.5% -69.2% 12.5% 28.0% 16.9% 7.1% 4.5% 5.99 12.74 2.0 9% 1.8 3.1% 220%Software & Services (7) (44) (43) 10 7.0% 7.4% 6.9% 11.1 13.7 12.1 -5.2% 13.6% 5.6% 12.6% 35.7% 36.0% 10.6% 11.0% 5.39 4.92 3.1 27% 2.3 1.2% 13%Technology Hardware & Equip (5) (42) (45) 10 8.5% 9.8% 7.8% 11.6 12.6 13.0 -5.7% -2.8% -3.5% 11.3% 16.0% 16.0% 10.7% 9.6% 6.29 6.29 2.4 21% 1.0 1.0% 12%

Materials (14) (47) (58) 10 3.3% 3.1% 2.4% 14.6 15.3 16.2 -49.6% -5.5% -31.8% 9.1% 16.2% 14.4% 5.2% 4.8% 5.03 6.57 1.9 16% 0.6 3.3% 47%

Telecommunication Services (16) (34) (40) 7 4.0% 5.2% 4.0% 12.0 11.4 11.9 -4.4% -4.1% -15.8% 4.7% 33.7% 32.7% 11.6% 12.7% 4.38 4.43 1.6 14% 0.9 6.6% 80%

Utilities (22) (32) (45) 2 4.2% 6.2% 5.2% 9.1 9.9 9.5 -0.4% 4.2% 2.2% 7.6% 24.1% 26.1% -5.9% -2.0% 6.51 6.37 1.2 13% 0.7 5.7% 52%

S&P 500 (20) (38) (50) 8 11.0 14.6 11.9 -41.0% 22.9% 2.3% 9.6% 17.0% 16.4% 8.1% 8.2% 5.44 5.66 1.6 13% 0.7 3.2% 35%

Source: Morgan Stanley Research, Factset, Based on Thomson Financial Consensus EPS Estimates; FFO for Reits; Note: a) NTM=(Consensus) Next 12 months, LTM=Last 12 months, LTG=Long Term Growth b) Data adjusted for aggregation purposes when required. c) LTM ROE is LTM Net Income divided by avg. equity. d) LTG estimate is NTM income weighted. e)Margins, FCFyield, EV/EBITDA and P/B ratio for index are ex-financials

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

36Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Valuation Snapshot – OthersRussell MidCap Russell 2000

P/E Rel. P/E Earnings Growth ROE Ind. P/E Rel. P/E Earnings Growth ROE Ind.

LTM NTMe 2009e NTMe 2009e NTMe '08-'09e LTG est. (LTM) Div. LTM NTMe 2009e NTMe 2009e NTMe '08-'09e LTG est. (LTM) Div.

Sectors Yield Sectors Yield

Consumer Discretionary 21.0 17.1 16.4 1.5 1.4 NM 242.0% 12.5% -3% 2.0% Consumer Discretionary NM NM NM NM NM 149.7% 166.6% 14.5% -5% 1.4%

Consumer Staples 10.3 10.3 10.1 0.9 0.9 8.8% 10.7% 8.6% 16% 3.2% Consumer Staples 15.3 16.5 15.2 0.9 0.9 13.9% 17.8% 11.5% 10% 1.9%

Energy 5.0 8.5 8.4 0.7 0.7 -37.7% -37.1% 13.1% 21% 1.8% Energy 6.9 12.6 12.3 0.7 0.7 -48.2% -47.2% 12.8% 9% 2.6%

Financials 10.9 9.9 9.9 0.8 0.9 55.9% 58.9% 9.1% 4% 5.2% Financials 16.9 12.6 12.7 0.7 0.7 NM NM 8.2% -1% 5.7%

Health Care 13.3 11.9 11.9 1.0 1.0 5.7% 5.8% 12.8% 16% 0.3% Health Care NM NM NM NM NM 107.9% 114.8% 18.3% -4% 0.3%

Industrials 8.0 10.2 10.2 0.9 0.9 -17.7% -17.5% 12.2% 16% 2.4% Industrials 8.7 15.2 15.0 0.9 0.9 8.5% 11.0% 13.1% 9% 1.5%

Information Technology 12.7 16.8 16.7 1.4 1.4 -37.8% -37.0% 13.8% 13% 0.9% Information Technology 18.3 23.1 22.6 1.3 1.3 -30.9% -26.6% 15.3% 6% 0.3%

Materials 7.5 11.8 11.7 1.0 1.0 -39.1% -38.8% 8.2% 17% 3.0% Materials 8.6 14.2 14.0 0.8 0.8 -27.6% -26.2% 6.5% 6% 2.4%

Telecommunication Services 33.3 20.5 20.1 1.8 1.7 31.8% 17.9% 7.9% 7% 3.7% Telecommunication Services NM NM NM NM NM NM NM 13.0% -37% 2.7%

Utilities 8.9 9.4 9.3 0.8 0.8 -5.2% -3.8% 7.6% 11% 5.4% Utilities 14.5 13.0 13.0 0.7 0.8 19.3% 19.4% 7.2% 8% 5.1%

Index 10.5 11.7 11.6 1.0 1.0 -9.8% -7.2% 10.9% 10% 2.7% Index 16.4 17.8 17.2 1.0 1.0 97.4% 106.5% 12.2% 2% 2.2%

Dow Jones Industrial Average Nasdaq 100

P/E Rel. P/E Earnings Growth ROE Ind. P/E Rel. P/E Earnings Growth ROE Ind.

LTM NTMe 2009e NTMe 2009e NTMe '08-'09e LTG est. (LTM) Div. LTM NTMe 2009e NTMe 2009e NTMe '08-'09e LTG est. (LTM) Div.

Sectors Yield Sectors Yield

Consumer Discretionary NM NM NM NM NM 11.0% 1.0% 9.1% NM 3.6% Consumer Discretionary 13.6 13.6 13.5 1.0 1.0 0.0% 1.4% 10.7% 11% 0.9%

Consumer Staples 12.2 12.6 12.6 1.0 1.0 -3.7% -3.3% 9.9% 21% 3.3% Consumer Staples 15.6 15.4 15.8 1.1 1.1 1.2% -7.4% 12.4% 14% 1.4%

Energy 6.9 13.1 13.8 1.1 1.1 -47.1% -49.9% 7.9% 34% 2.9% Energy

Financials NM NM NM NM NM 152.7% 134.9% 7.4% -4% 1.4% Financials

Health Care 7.3 8.2 8.0 0.7 0.6 -10.9% -8.1% 4.4% 30% 6.4% Health Care 14.9 13.4 13.4 0.9 0.9 10.9% 10.5% 15.1% 20% 0.2%

Industrials 6.0 8.3 8.3 0.7 0.7 -27.1% -26.9% 9.2% 22% 4.6% Industrials 13.7 14.1 13.9 1.0 1.0 -2.8% -1.5% 17.8% 23% 1.4%

Information Technology 9.8 10.7 10.6 0.9 0.9 -8.9% -7.8% 10.4% 32% 2.7% Information Technology 12.1 14.7 14.6 1.0 1.0 -18.1% -17.6% 13.0% 24% 1.3%

Materials 6.1 19.9 17.1 1.6 1.4 -69.1% -64.2% 4.4% 15% 9.6% Materials 7.6 9.4 9.6 0.7 0.7 -18.6% -22.0% 8.3% 25% 2.5%

Telecommunication Services 9.1 11.4 11.0 0.9 0.9 -20.4% -2.1% 4.6% 16% 6.9% Telecommunication Services 7.5 7.0 7.3 0.5 0.5 6.9% 2.7% 11.6% 25% 0.0%

Utilities Utilities

Index 10.3 12.1 12.3 1.0 1.0 -15.3% -14.8% 8.0% 16% 3.9% Index 12.6 14.2 14.2 1.0 1.0 -11.3% -10.9% 13.2% 20% 1.1%

Source: Morgan Stanley Research, Factset, Based on Thomson Financial Consensus EPS Estimates

Note: a) NTM=(Consensus) Next 12 months, LTM=Last 12 months, LTG=Long Term Growth, NM = Not Meaningful

b) Data adjusted for aggregation purposes when required.

c) LTM ROE is LTM Net Income divided by avg. equity.

d) LTG estimate is NTM income weighted.

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

37Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

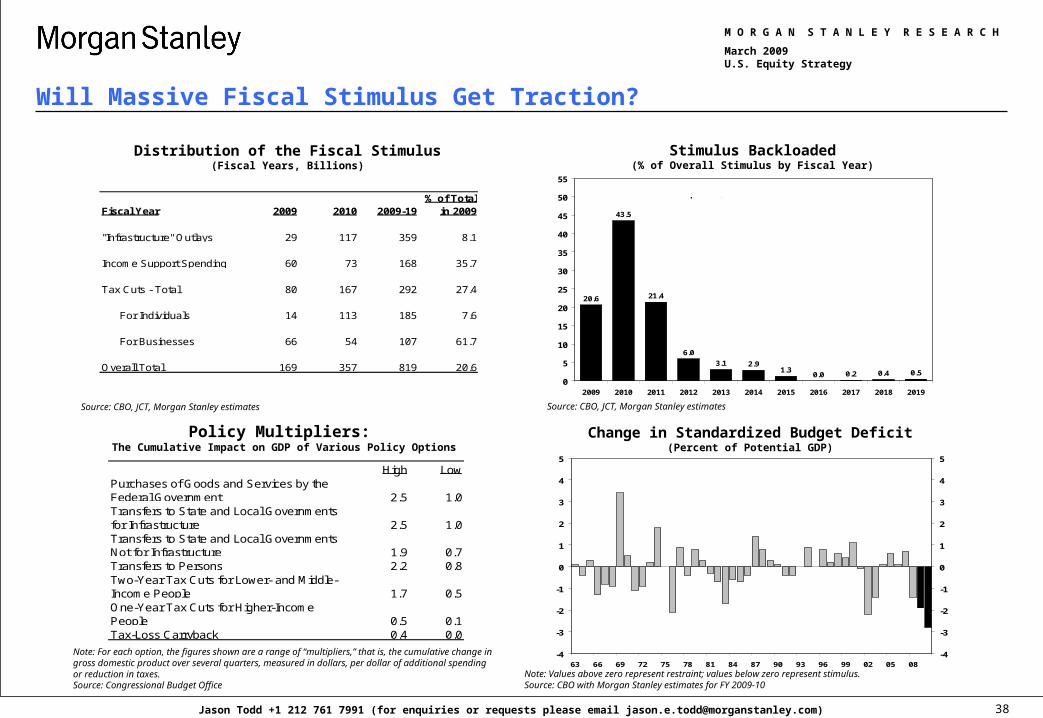

Will Massive Fiscal Stimulus Get Traction?

American Recovery and Reinvestment Act Stimulus “back-loaded” into F2010 Shovel ready? Infrastructure outlays come slowly Assume that consumers save ½ to ¾ of tax cuts “Multiplier” effects muted until credit crunch abates

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

38Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Will Massive Fiscal Stimulus Get Traction?

Source: CBO, JCT, Morgan Stanley estimates Source: CBO, JCT, Morgan Stanley estimates

Note: For each option, the figures shown are a range of “multipliers,” that is, the cumulative change in gross domestic product over several quarters, measured in dollars, per dollar of additional spending or reduction in taxes.Source: Congressional Budget Office

Note: Values above zero represent restraint; values below zero represent stimulus.Source: CBO with Morgan Stanley estimates for FY 2009-10

Stimulus Backloaded(% of Overall Stimulus by Fiscal Year)

Policy Multipliers: The Cumulative Impact on GDP of Various Policy Options

Change in Standardized Budget Deficit(Percent of Potential GDP)

Distribution of the Fiscal Stimulus(Fiscal Years, Billions)

High LowPurchases of Goods and Services by the Federal Government 2.5 1.0Transfers to State and Local Governments for Infrastructure 2.5 1.0Transfers to State and Local Governments Not for Infrastructure 1.9 0.7Transfers to Persons 2.2 0.8Two-Year Tax Cuts for Lower- and Middle-Income People 1.7 0.5One-Year Tax Cuts for Higher-Income People 0.5 0.1Tax-Loss Carryback 0.4 0.0

Fiscal Year 2009 2010 2009-19% of Total

in 2009

"Infrastructure" Outlays 29 117 359 8.1

Income Support Spending 60 73 168 35.7

Tax Cuts - Total 80 167 292 27.4

For Individuals 14 113 185 7.6

For Businesses 66 54 107 61.7

Overall Total 169 357 819 20.6

20.6

43.5

21.4

6.0

3.1 2.91.3

0.0 0.2 0.4 0.50

5

10

15

20

25

30

35

40

45

50

55

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Tax and Spending Stimulus in the House Bill as a % of the Overall 10-Year Impact of $819 bil.

-4

-3

-2

-1

0

1

2

3

4

5

-4

-3

-2

-1

0

1

2

3

4

5

63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08

Actual

Change in standardized budget deficit (percent of potential GDP)

MS estimates

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

39Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Source: Census Bureau, National Association of Realtors

Inventories of Unsold Homes Plunging, But Still High

Construction Employment: More Declines ComingNonfarm Payrolls, Year-over-Year Percent Change

Affordability Soaring but Pent-Up Demand Unfavorable

Equity Extraction Is Collapsing

Source: Census Bureau

Source: Bureau of Labor Statistics

Updated estimates of the mortgage system provided by Jim Kennedy, presented in “Estimates of Home Mortgage Originations, Repayments, and Debt On One-to-Four-Family Residences," Alan Greenspan and James Kennedy, Federal Reserve Board FEDS working paper no. 2005-41.

US Housing Recession at Least Through 2009

0

2

4

6

8

10

12

Active

Passive

Mortgage equity withdrawal,as a % of disposable income,4-quarter moving average

60

80

100

120

140

160

180

200

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

63

64

65

66

67

68

69

70

Composite housingaffordability index(left scale)

US homeownershiprate (right scale)

250

300

350

400

450

500

550

600

96 97 98 99 00 01 02 03 04 05 06 07 08 09

3

5

7

9

11

13

15

New single-family homes for sale,months supply(right scale)

New single-family homes for sale,thousands of units (left scale)

-16

-12

-8

-4

0

4

8

12

86 88 90 92 94 96 98 00 02 04 06 08

-16

-12

-8

-4

0

4

8

12

Specialty trade contractors: residential

Residentialbuilding construction

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

40Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

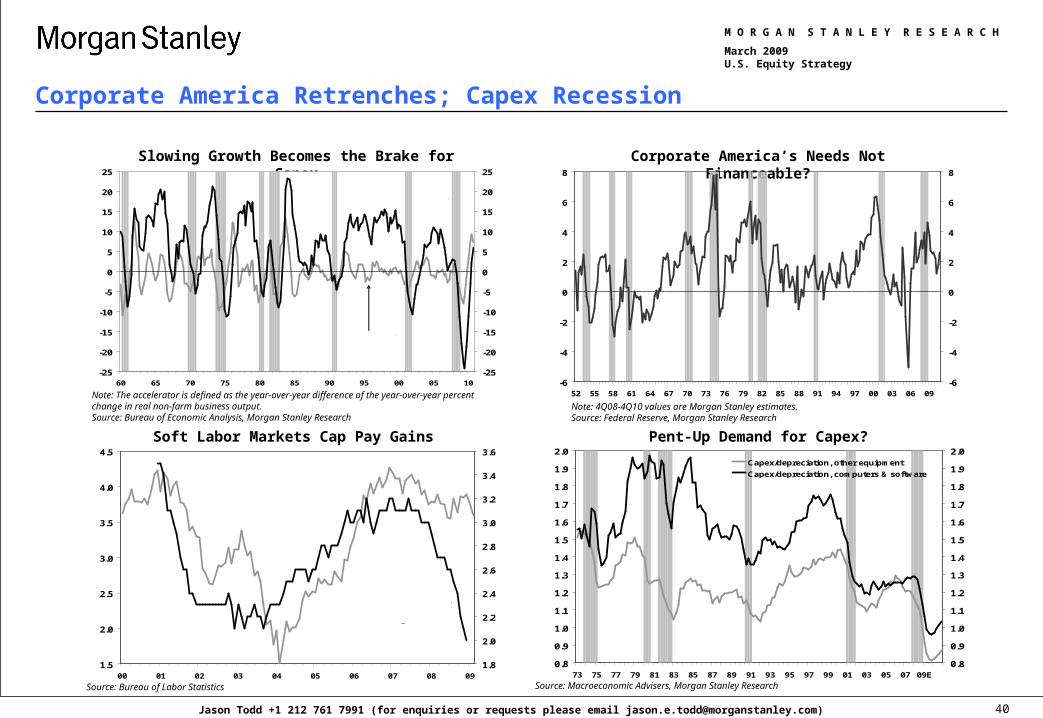

Corporate America Retrenches; Capex Recession

Source: Bureau of Labor Statistics

Note: 4Q08-4Q10 values are Morgan Stanley estimates.Source: Federal Reserve, Morgan Stanley Research

Note: The accelerator is defined as the year-over-year difference of the year-over-year percent change in real non-farm business output. Source: Bureau of Economic Analysis, Morgan Stanley Research

Source: Macroeconomic Advisers, Morgan Stanley Research

Soft Labor Markets Cap Pay Gains

Slowing Growth Becomes the Brake for Capex

Pent-Up Demand for Capex?

Corporate America’s Needs Not Financeable?

-6

-4

-2

0

2

4

6

8

52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 00 03 06 09

-6

-4

-2

0

2

4

6

8Financing gap as a percentage of nonfinancialcorporate GDP

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09E

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0Capex/depreciation, other equipment

Capex/depreciation, computers & software

1.5

2.0

2.5

3.0

3.5

4.0

4.5

00 01 02 03 04 05 06 07 08 09

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

JOLTS jobopenings rate,total private(right scale)

Average hourly earnings,total private industries,year-over-year percentchange (left scale)

-25

-20

-15

-10

-5

0

5

10

15

20

25

60 65 70 75 80 85 90 95 00 05 10

-25

-20

-15

-10

-5

0

5

10

15

20

25

Private nonresidential investment in equipment & software,year-over-year percent change

Accelerator*

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

41Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Global Forecast at a Glance

2008E 2009E 2010E 2008E 2009E 2010E

Global Economy 3.3 -0.5 3.0 6.2 2.0 3.5Industrial World 0.8 -2.5 1.2 3.3 -0.5 1.8Developing World 5.9 1.5 4.6 9.1 4.5 5.0

US 1.1 -3.3 1.8 3.8 -1.4 2.4

Europe 0.8 -1.5 1.2 3.3 0.5 1.7EMU 0.9 -1.6 1.1 3.3 0.5 1.6UK 0.7 -1.3 2.0 3.6 0.7 2.2

CEEMEA 4.2 -1.7 2.5 11.6 8.3 8.2

Japan -0.7 -4.0 -0.3 1.5 -1.2 -0.1Asia ex-Japan 7.0 3.0 6.4 6.4 1.1 2.7China 9.0 5.5 8.0 5.9 -0.8 1.5

Latin America 4.3 -0.4 2.4 8.0 8.3 7.6

Source: Morgan Stanley Research

REAL GDP GROWTH CPI INFLATION

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

42Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Source: Morgan Stanley Research, E = Morgan Stanley Estimates

Winners and Losers in the Global Economy?

Note: 1Q09-4Q10 values are Morgan Stanley estimates.Source: Bureau of Economic Analysis, Macroeconomic Advisers LLC, Morgan Stanley Research

…While Inflation Risks Tilt Higher

Growth Outside the US and China Matters More

Source: Morgan Stanley Research, E = Morgan Stanley Estimates

Source: IMF, E = Morgan Stanley Estimates

Growth Risks Now More Balanced…

Recoupling Risks

-6

-4

-2

0

2

4

6

8

10

12

14

16

2007 2008E 2009E 2010E

World

EuropeJapan US

Other DollarBloc

Latin America

Non-JapanAsia

Annual percentchange in real GDP

China

-1.4

3.3

-0.5

3.0

4.3

0.4

3.3

1.3

3.3

-2

-1

0

1

2

3

4

5

6

2006 2007 2008E 2009E 2010E

Global Economy: Real GDP (%)

BullBaseBear

6.2

2.0

3.5

1.8

6.2

0.0

4.8

3.0

6.2

-1

0

1

2

3

4

5

6

7

2006 2007 2008E 2009E 2010E

Global Economy: CPI Inflation (%)

BullBaseBear

-6

-4

-2

0

2

4

6

8

10

74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

-6

-4

-2

0

2

4

6

8

10

Non-US

US

Real GDP, YoY % chg

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

43Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

US Economic Outlook

US Economic Outlook4th Qtr/4th Qtr Percent Change

Year over Year Percent Change from Prior Quarter*

2008A 2009E 2010E 2008A 2009E 2010E 3Q08A 4Q08A 1Q09E 2Q09E 3Q09E 4Q09E 1Q10E 2Q10E 3Q10E 4Q10E

Real GDP 1.1 -3.3 1.8 -0.8 -2.3 3.1 -0.5 -6.2 -5.5 -4.0 -1.0 1.5 2.5 3.4 3.3 3.4Final Sales+ 1.4 -2.9 1.5 -0.7 -1.9 2.6 -1.3 -6.4 -4.4 -3.2 -1.0 1.0 2.3 2.8 2.6 2.7Personal Consumption Expenditures 0.2 -0.8 2.1 -1.5 1.1 2.3 -3.8 -4.3 0.4 0.0 1.6 2.3 2.5 2.1 2.1 2.4Business Fixed Investment 1.7 -17.7 -2.7 -5.0 -17.9 4.2 -1.7 -21.1 -26.4 -24.9 -12.1 -6.4 0.6 4.1 5.3 6.7 -- Structures 11.5 -11.7 -4.1 7.3 -16.7 1.6 9.7 -5.9 -24.6 -22.0 -10.0 -9.0 -3.0 4.4 2.9 2.4 -- Equipment -3.0 -21.0 -1.8 -11.2 -18.6 5.8 -7.5 -28.8 -27.5 -26.7 -13.4 -4.7 3.0 4.0 7.0 9.6Residential Investment -20.7 -21.4 8.9 -19.3 -16.0 15.7 -16.0 -22.2 -31.7 -27.3 -10.3 11.4 19.7 17.8 14.1 11.4Exports 6.2 -13.4 -0.4 -1.8 -12.3 4.1 3.0 -23.6 -23.3 -12.9 -7.4 -4.3 2.5 4.0 4.9 5.0Imports -3.3 -10.4 2.3 -7.1 -7.1 5.0 -3.5 -16.0 -16.6 -10.6 -1.2 1.2 4.9 4.1 4.6 6.2Federal Government 6.0 5.2 1.8 8.2 2.5 1.4 13.8 6.7 3.5 4.4 0.7 1.5 1.3 4.1 0.5 -0.1State & Local Government 1.2 -0.9 1.9 0.5 -0.8 3.0 1.3 -1.4 -3.7 -0.8 -0.1 1.6 2.4 2.3 3.4 3.8

Business Indicators++Net Exports of Goods & Services -$392.3 -$398.5 -$443.4 -$353.1 -$372.9 -$385.1 -$383.2 -$403.3 -$422.3 -$435.1 -$439.9 -$443.9 -$454.8Current Account as a % of GDP -4.6 -4.1 -4.6 -4.8 -3.7 -3.7 -3.4 -4.3 -5.0 -4.9 -3.9 -4.5 -5.1Change in Real Nonfarm Inventories -32.8 -67.6 -30.7 -33.3 -25.0 -53.7 -75.8 -77.7 -63.2 -56.8 -41.3 -22.1 -2.6

Housing Starts (Thous) 904 476 670 876 661 462 422 474 549 609 654 694 724Light Vehicle Sales (Millions) 13.1 9.8 11.4 12.9 10.3 9.2 9.7 10.1 10.3 10.7 11.2 11.6 12.1Industrial Production (Pct Chg) -1.8 -10.0 1.7 -8.9 -12.1 -17.5 -7.8 -3.0 0.0 3.0 5.0 5.1 5.1Civilian Unemployment Rate (Percent) 5.8 9.2 9.7 6.0 6.9 8.0 9.0 9.6 9.9 9.9 9.8 9.7 9.6

After-Tax "Economic" Profits** $1,098.4 $735.6 $820.6 $1,121.3 $955.2 $862.0 $759.4 $681.5 $639.6 $707.2 $866.0 $865.2 $844.0 -- Percent Change from Prior Year -7.9 -33.0 11.5 -7.9 -18.9 -27.6 -32.6 -39.2 -33.0 -18.0 14.0 27.0 32.0After-Tax "Book" Profits $1,219.4 $923.4 $1,039.2 $1,300.2 $886.3 $1,009.9 $939.6 $887.5 $856.8 $915.7 $1,093.2 $1,085.1 $1,062.9 -- Percent Change from Prior Year -15.1 -24.3 12.5 -10.1 -39.3 -25.1 -30.1 -31.7 -3.3 -9.3 16.4 22.3 24.1Real Disposable Personal Income (Pct Chg) 1.3 2.5 2.3 -8.5 3.4 7.4 3.2 -0.7 0.9 1.0 7.6 2.1 2.3Personal Saving Rate 1.8 5.2 5.6 1.3 3.2 4.9 5.7 5.2 4.9 4.6 5.9 5.9 5.9

Prices and Costs (Percent Change)GDP Chain Price Index 2.2 1.5 1.5 2.0 0.9 1.8 3.9 0.5 2.8 0.4 0.2 0.4 1.2 4.9 0.6 0.7Consumer Price Index 3.8 -1.4 2.4 1.5 -0.3 2.9 6.2 -8.3 -2.4 -3.1 2.0 2.6 2.9 3.0 3.0 2.9CPI ex Food & Energy 2.3 1.2 1.1 2.0 0.9 1.2 2.8 0.6 1.0 1.0 0.8 0.9 1.1 1.1 1.3 1.5PCEPI ex Food & Energy 2.2 1.1 0.9 1.9 0.7 1.1 2.4 0.8 0.9 0.8 0.6 0.7 0.9 1.0 1.2 1.4Market-Based PCEPI ex Food & Energy 1.9 1.0 0.8 1.8 0.7 1.0 2.5 1.0 0.8 0.7 0.5 0.6 0.8 0.9 1.1 1.3Producer Price Index 6.4 -2.7 4.3 1.3 1.3 4.7 9.7 -19.1 -4.5 -2.2 4.5 8.0 7.6 -5.1 8.5 8.4Compensation Per Hour 3.7 3.8 3.1 4.1 3.0 3.5 5.7 5.3 4.4 2.4 2.4 2.8 3.2 3.4 3.6 3.8Productivity 2.8 0.7 1.9 2.2 0.7 2.4 2.1 -0.4 0.5 -0.7 0.8 2.2 1.6 2.7 2.7 2.8Unit Labor Costs 0.9 3.1 1.2 1.8 2.3 1.0 3.5 5.7 3.9 3.1 1.6 0.6 1.6 0.7 0.9 0.9

*Annualized percent change from prior period, unless noted +GDP less inventory change**Including inventory valuation & capital consumption adjustments ++Billions of dollars; real in billions of chain-type 2000 dollarsE = Morgan Stanley estimatesForecast as of March 9, 2009

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

44Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. Customers of Morgan Stanley in the US can receive independent, third-party research on companies covered in Morgan Stanley Research, at no cost to them, where such research is available. Customers can access this independent research at www.morganstanley.com/equityresearch or can call 1-800-624-2063 to request a copy of this research.

Morgan Stanley & Co. International plc, authorized and regulated by Financial Services Authority, disseminates in the UK research that it has prepared, and approves solely for the purposes of section 21 of the Financial Services and Markets Act 2000, research which has been prepared by any of its affiliates. As used in this disclosure section, Morgan Stanley includes RMB Morgan Stanley (Proprietary) Limited, Morgan Stanley & Co International plc and its affiliates.

For important disclosures, stock price charts and rating histories regarding companies that are the subject of this report, please see the Morgan Stanley Research Disclosure Website at www.morganstanley.com/researchdisclosures, or contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Equity Research Management), New York, NY, 10036 USA.

Analyst CertificationThe following analysts hereby certify that their views about the companies and their securities discussed in this report are accurately expressed and that they have not received and will not receive direct or indirect compensation in exchange for expressing specific recommendations or views in this report: Jonathan Garner, Vinicius Silva, Michael Wang.Unless otherwise stated, the individuals listed on the cover page of this report are research analysts.Global Research Conflict Management PolicyMorgan Stanley Research has been published in accordance with our conflict management policy, which is available at www.morganstanley.com/institutional/research/conflictpolicies.Important US Regulatory Disclosures on Subject Companies

As of February 29, 2008, Morgan Stanley beneficially owned 1% or more of a class of common equity securities of the following companies covered in Morgan Stanley Research: Acer Inc., America Movil, Arabtec Holdings, China Steel Corp., Companhia Vale do Rio Doce, Corporacion GEO, Ctrip.com, Garanti Bank, Gazprom, Grupo Financiero Banorte, Grupo Televisa, Hon Hai Precision, Hurriyet, Hyflux Ltd, Hyundai Heavy Industries Co. Ltd., Lonmin Plc, Millicom, NHN Corp, Petrobras, Samsung Electronics, Satyam Computer Services, TSMC, Vimpelcom, Yang Ming Marine, Abbott Laboratories, Amgen, Cisco Systems, Coach Inc, J.P.Morgan Chase & Co., Lowe's Companies, MetLife Inc., Nokia, Philip Morris International Inc, Wells Fargo & Co BRISTOL MYERS SQUIBB... .

As of February 29, 2008, Morgan Stanley held a net long or short position of US$1 million or more of the debt securities of the following issuers covered in Morgan Stanley Research (including where guarantor of the securities): Companhia Vale do Rio Doce, Garanti Bank, Gazprom, Grupo Televisa, Hon Hai Precision, Isbank, Kazkommertsbank, Kookmin Bank, Millicom, Mobile TeleSystems, Petrobras, Samsung Electronics, Telekom Malaysia, Tenaga Nasional Bhd, TIM Participacoes, TPSA, NIKE, INC., CHEVRON CORPORATION, CONOCOPHILLIPS, UNITED TECHNOLOGIES CORPORATION, EXELON CORPORATIONAbbott Laboratories, Altria Group, Inc., Amgen, AT&T, Inc., Boeing Company, Cisco Systems, Coach Inc, Danaher Corp., IBM, J.P.Morgan Chase & Co., Kroger Co., Lockheed Martin Corp., Lowe's Companies, McDonald's Corporation, MetLife Inc., Nokia, Oracle Corporation, Philip Morris International Inc, State Street Corporation, Teva Pharmaceutical Industries Ltd., Texas Instruments, Vodafone Group, Wal-Mart, Wells Fargo & Co.. .

Within the last 12 months, Morgan Stanley managed or co-managed a public offering of securities of BIM, China Mobile Limited Amgen, AT&T, Inc., Cisco Systems, IBM, J.P.Morgan Chase & Co., McDonald's Corporation, MetLife Inc., Oracle Corporation, State Street Corporation, Wal-Mart, Wells Fargo & Co.. .

Within the last 12 months, Morgan Stanley has received compensation for investment banking services from America Movil, Companhia Vale do Rio Doce, Gazprom, Implats Limited, MMK, Norilsk Nickel, Petrobras, Tenaris S.A, TPSA from Abbott Laboratories, Altria Group, Inc., Amgen, AT&T, Inc., Boeing Company, Cisco Systems, Danaher Corp., IBM, J.P.Morgan Chase & Co., Kroger Co., Lockheed Martin Corp., McDonald's Corporation, MetLife Inc., Nokia, Oracle Corporation, State Street Corporation, Texas Instruments, Vodafone Group, Wal-Mart, Wells Fargo & Co.. .

Disclosure SectionMorgan Stanley ModelWare is a proprietary analytic framework that helps clients uncover value, adjusting for distortions and ambiguities created by local accounting regulations. For example, ModelWare EPS adjusts for one-time events, capitalizes operating leases (where their use is significant), and converts inventory from LIFO costing to a FIFO basis. ModelWare also emphasizes the separation of operating performance of a company from its financing for a more complete view of how a company generates earnings.

M O R G A N S T A N L E Y R E S E A R C H

March 2009U.S. Equity Strategy

45Jason Todd +1 212 761 7991 (for enquiries or requests please email [email protected])