m e m o r a n d u m - in.gov€¦ · · 2018-03-05m e m o r a n d u m to: library directors ... a...

TRANSCRIPT

STATE OF INDIANA

M E M O R A N D U M

TO: LIBRARY DIRECTORS

FROM: DEPARTMENT OF LOCAL GOVERNMENT FINANCE

SUBJECT: LIBRARY CAPITAL PROJECTS FUND

(IC 36-12-12)

DATE: April 2009

*** THIS BULLETIN SUPERCEDES ALL PREVIOUS LCPF BULLETINS ***

INTRODUCTION

The purpose of this Bulletin is to outline the policy and procedures of the Department of

Local Government Finance (“Department”) regarding the Library Capital Projects Fund

(“LCPF”). The LCPF is a fund for which a Library District may levy property taxes to be used to

pay for the following:

1) A facility used or to be used by the Library District.

a) Planned construction, repair, replacement or remodeling.

b) Site acquisition.

c) Site development.

d) Repair, replacement or site acquisition that is necessitated by an emergency;

2) The purchase, lease or repair of equipment to be used by the Library Districts.

3) The purchase, lease, upgrading, maintenance or repair of computer hardware or

software.

Before a Library Board may collect property taxes for a LCPF in a particular year, the

Library Board must, after January 1st and before May 15 of the immediately proceeding year

(IC 36-12-12-3):

1) Hold a public hearing on a proposed plan.

INDIANA GOVERNMENT CENTER NORTH

100 NORTH SENATE AVENUE N1058(B)

INDIANAPOLIS, IN 46204

PHONE (317) 232-3777

FAX (317) 232-8779

DEPARTMENT OF LOCAL GOVERNMENT FINANCE

2

2) Pass a resolution to adopt a plan.

3) Submit the plan for approval or rejection by the fiscal body.

TIMELINE FOR ESTABLISHING A LCPF

Steps 1 through 4 must be completed after Jan.1 and before May 15th. (IC 36-12-12-3)

1) The Library Board prepares a proposed LCPF Plan and LCPF Plan Summary in the

year before the taxes are to be collected. This plan must specify anticipated

expenditures along with revenue estimates, tax rates to be charged and estimated

assessed valuation. The plan must apply to at least the three (3) years immediately

following the year the plan is adopted. The format of the LCPF Plan is included in

this memo. The library board may, for each year in which a plan is adopted, impose a

property tax rate that does not exceed $.0167 per $100 of assessed valuation. The

LCPF levy is within the maximum property tax levy limit beginning with taxes

payable in 2009.

2) Senate Bill 1 which was signed December, 2003, added IC 6-1.1-18-12 to define

“maximum rate” for taxes first due and payable after 2003. It requires the maximum

rate of the LCPF to be adjusted each time an annual adjustment to real property takes

place or each time a general reassessment takes place. It establishes a formula for

determining a new maximum rate. The Department will compute the rate adjustment.

3) The Library Board must give at least a ten (10) day notice of Public Hearing on the

proposed LCPF Plan. A sample of the hearing notice form to be used for the

advertising is included in this memo. The publication requirement is for one (1)

insertion in two (2) newspapers. If two (2) newspapers do not exist in the Library

District, the Library Board should refer to IC 5-3-1-4 or the State Board of Accounts

"Guide to Publication of Legal Notices" for the proper publication procedure. The

notice of the public hearing shall be published one (1) time at least ten (10) days

before the date of the hearing. The Notice to Taxpayers must specify planned

expenditures and allocations for future projects for a minimum of three (3) years,

estimates of revenue, proposed tax rates and estimated assessed valuation for the

same years.

4) After considering the comments and contentions presented at the Public Hearing, the

Library Board may pass a resolution to adopt the proposed plan. The Secretary of the

Library Board shall submit a copy of the LCPF Plan to the appropriate fiscal body

along with a certificate that the attached is a complete transcript of the proceedings of

the LCPF Plan Adoption. The following documents should be maintained in the

Library Offices for public inspection:

a) A certified copy of the LCPF Plan adopted by the Library Board.

b) Proper proofs of publication.

c) A copy of the Library Board's resolution adopting the LCPF Plan.

3

5) Within ten (10) days after the Library Board passes a resolution adopting the

Plan, the Library Board shall send a certified copy of the LCPF Plan to the

appropriate fiscal body. The fiscal body shall advertise its public hearing to consider

the plan one (1) time at least 10 days prior to the hearing in accordance with IC 5-3-1-

2. The advertisement should include the date, time, and location of the meeting and

does not need to include the complete plan summary. Sample fiscal body notices are

included in this memo. The appropriate fiscal body, as specified in IC 36-12-12-4, is:

a) The Town Council if the Library District is located entirely within the corporation

boundaries of a town.

b) The City Common Council if the Library District is located entirely within the

Corporation boundaries of a city.

c) The Township Advisory Board if the Library District is not located entirely within

the corporation boundaries of a city or town but is located entirely within the

corporation boundaries of a Township.

d) The Common Council of each county in which the Library District is located if

the Library District is not located entirely within the corporation boundaries of a

city, town or single township.

e) The City-County Council if the Library District is not located entirely within the

corporation boundaries of a city, town or township and is located in a county with

a consolidated city.

5) The appropriate fiscal body shall advertise and hold a public hearing on the LCPF

Plan within thirty (30) days after receiving a certified copy of the LCPF Plan from the

Library Board. The fiscal body will either reject or approve the plan before August 1

of the year the plan is received (IC 36-12-12-4). (See sample FISCAL BODY

RESOLUTION form included in this memo). If the LCPF Plan is approved by the

fiscal body, the Library Board shall submit to the Department on or before

September 20 of the immediate preceding year the plan is to be effective the

following:

a) A certified copy of the LCPF Plan including a plan summary sheet and a

description of the allocation of future projects if applicable.

b) The Library Board’s resolution approving the plan.

c) Certificate of Submission to the Fiscal Body.

d) The Library Fiscal Body’s resolution approving/rejecting the plan.

e) Proofs of publication of the Library Board’s notice of public hearing.

f) Proofs of publication of the Fiscal Body’s notice of public hearing.

g) The Procedure Checklist (included at the end of this memo).

If the Department determines that:

1. The Library Board has properly advertised the plan;

4

2. The plan was timely adopted by the Library Board and timely approved by

the appropriate fiscal body;

3. The plan conforms to the format prescribed by the Department and;

4. The plan was timely filed with the Department;

The Department will require the Library to publish a Notice of Adoption to local

taxpayers of the LCPF plan. If the plan fails to conform to the above requirements the

plan will be returned. Further submissions must conform to the above stated time

requirements.

6) After receiving the plan and other required documentation, the Department will

notify the Library Board to advertise the Notice of Adoption one (1) time. The

Department will prepare the Notice of Adoption. (A sample Notice of Adoption is

included with this memo.) This advertising should be made in accordance with IC 5-

3-1-2. Ten (10) or more taxpayers who will be affected by the adopted plan may file a

petition with the County Auditor of a county in which the library district is located

not later than ten (10) days after publication of the Notice of Adoption, setting forth

their objections to the proposed plan. The County Auditor shall immediately certify

the petition to the Department. (IC 36-12-12-5)

7) The Department will, within a reasonable time, fix a date for a local hearing on the

petition filed. The hearing will be held in a county in which the Library District is

located and the Department will notify:

a) The Library Board, and

b) The first ten (10) taxpayers whose names appear upon the petition, and

c) This notice will be given at leave five (5) days before the date of the hearing.

(IC 36-12-12-6)

8) After a hearing on the petition, the Department will certify its approval, or

disapproval or modification of the LCPF Plan to the Library Board and the County

Auditor. The action of the Department with respect to the plan is final (IC 36-12-12-

7). The Library Board or taxpayers may appeal the Department’s decision to the Tax

Control Court within forty-five (45) days.

9) If no petition objecting to the LCPF Plan is filed with the County Auditor, within

ten (10) days following the objection period, the unit must submit proofs of

publication of the Notice of Adoption and County Auditors Certificate of No

Remonstrance to the Department. Upon receipt, the Department will issue its

order approving or denying the LCPF Plan. Please note that it is the Library’s

responsibility to obtain the Auditor’s Certificate of no remonstrance from the County

Auditor.

BUDGET APPROVAL

In addition to annually adopting a LCPF Plan, the plan must be incorporated into the

5

ensuing years Library Budget, in accordance with IC 6-1.1-17, to receive funding. All budget

forms are to be used in preparing the annual budget for the LCPF. Budget form 4-B is commonly

referred to as the sixteen (16)-line statement. Line one (1) of the form 4-B is the annual budget

appropriation for the ensuing year. Items one (1) through six (6) of the LCPF Plan Summary

Page are to be included on line one (1) of form 4-B. The Allocation For Future Projects - Item

seven (7) of the LCPF Plan Summary Page - is included on line eleven (11) of the form 4-B.

Line eleven (11) is referred to as the operating balance.

The Library Board will advertise and adopt the appropriations and levy for the LCPF

annually using the regular budget calendar. Even though the rate is not advertised with the

annual budget, it must be adopted in the plan and on Budget Form 4B.

The Library Board will supply a copy of the LCPF Plan and Department approval Order

to the Department Hearing Officer for review of the annual budget. The budget order issued by

the Department will approve LCPF appropriations, tax rate and levy where they are consistent

with an approved Plan.

EMERGENCY AMENDMENT OF LCPF PLAN

The Library Board may amend its LCPF Plan for an Emergency (IC 36-12-12-9). As per IC 36-

12-12-1, "emergency" means:

1) when used with respect to repair or replacement, a fire, flood, windstorm, mechanical

failure of any part of a structure, or other unforeseeable circumstance; and

2) when used with respect to site acquisition, the unforeseeable availability of real

property for purchase.

The plan may be amended due to an emergency to:

a) Provide money for the purposes of repair, replacement or site acquisition that is

necessitated by an emergency,

b) To supplement money accumulated in the Emergency Allocation of the LCPF Plan

(IC 36-12-12-9 (a) (2).

The following steps must be completed to amend a capital projects plan:

1) When an emergency arises and the need for funds exceeds the amount accumulated in the

Emergency Allocation, the Library Board must immediately apply to the Department for a

determination that an emergency exists. The Department should be notified by telephone and

in writing (preferably by fax) of the library’s request for amendment of its plan. The request

for a determination should include the name of the location of the problem in the library

system, a description of the emergency, the proposed amendment, and the changes and/or

additions to the expenditures and revenue by plan year necessary to amend the LCPF Plan.

The Library Director may contact the Assistant Director of the Budget Division of the

Department at (317) 232-0651 regarding the amendment. Amendment requests may be faxed

to the Department’s Budget Division at (317) 232-8779.

2) After the Department issues its determination that an emergency exists, the Library Board

will amend its plan at a regular public meeting and forward its resolution to the Department.

The amendment is not subject to the deadlines and procedures for adoption of the original

6

plan. The form of the resolution would be to reduce a designated project(s) and increase the

Emergency Allocation. If the amendment requires use of any part of the Allocation for Future

Projects, the library will also need to process an additional appropriation.

3) The resolution is subject to modification by the Department. An amendment adopted may

require the payment of eligible emergency costs from:

a) Money accumulated in the LCPF for other purposes, or

b) Money to be borrowed from other funds of the Library Board or from a financial

institution.

4) The amendment may also provide for an increase in the property tax rate for the ensuing

budget year for the LCPF to restore money to the fund or to pay principal and interest on a

loan. Before the property tax rate may be increased, the Library Board must submit a plan

containing the increase to the fiscal body and obtain the approval of that fiscal body as

provided in IC 36-12-12-4. The increase in the property tax rate for the LCPF is

effective for property taxes payable for the year next certified by the Department.

However, the rate is not to exceed the maximum rate established under IC 36-12-12-10

and the levy is considered within the maximum levy controls.

COMPUTER REPAIR PERSONNEL

A Library may adopt a LCPF Plan to pay for the services of a full or part-time computer

repair personnel. These items should be incorporated into item six (6) on the LCPF SUMMARY

(Purchase, lease, maintenance, and repair of computer hardware).

ALLOCATION FOR FUTURE PROJECTS

The Allocation for Future Projects allows the library to levy property taxes in a current

year for expenditure in a future year, if the specific use is identified in the LCPF Plan. A

taxpayer or the Department hearing officer should be able to clearly determine the proposed use

and cost of the future project. If the reason for the Allocation for Future Projects is not

disclosed, the property tax levy needed to fund the Future Project will not be approved.

When preparing the ensuing year's LCPF budget, the Allocation for Future Projects should be

included in line 11 of Budget Form 4-B. It should not be appropriated, since its expenditure is

planned for a future year, as documented in the plan.

APPROPRIATION IN A YEAR EARLIER THAN PLANNED

An opportunity also exists to convert the projects planned for second, third or future years

of the plan into a current appropriation during the current budget year of the plan.

The following conditions apply:

1) The Plan must be specific as to the need to be addressed and the manner in which it

will be addressed.

2) The library must proceed with an additional appropriation. The Notice to Taxpayers

of the additional appropriation must state the fund name, a description of the project

and the project cost.

7

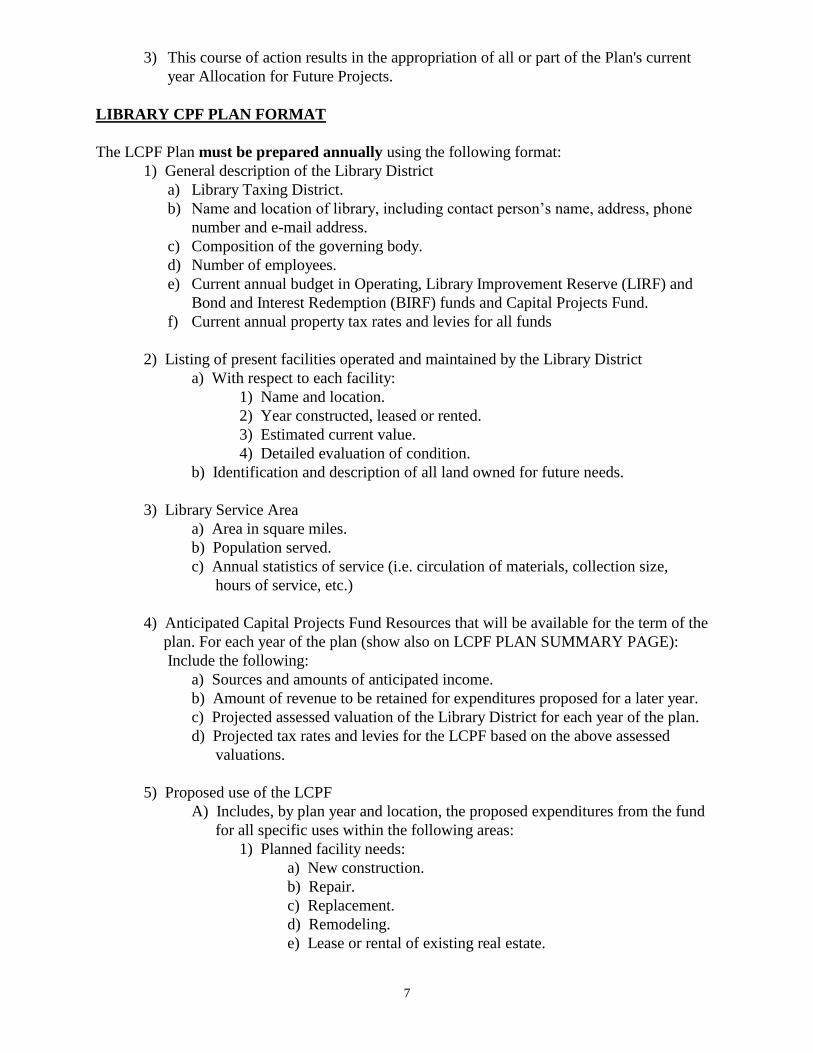

3) This course of action results in the appropriation of all or part of the Plan's current

year Allocation for Future Projects.

LIBRARY CPF PLAN FORMAT

The LCPF Plan must be prepared annually using the following format:

1) General description of the Library District

a) Library Taxing District.

b) Name and location of library, including contact person’s name, address, phone

number and e-mail address.

c) Composition of the governing body.

d) Number of employees.

e) Current annual budget in Operating, Library Improvement Reserve (LIRF) and

Bond and Interest Redemption (BIRF) funds and Capital Projects Fund.

f) Current annual property tax rates and levies for all funds

2) Listing of present facilities operated and maintained by the Library District

a) With respect to each facility:

1) Name and location.

2) Year constructed, leased or rented.

3) Estimated current value.

4) Detailed evaluation of condition.

b) Identification and description of all land owned for future needs.

3) Library Service Area

a) Area in square miles.

b) Population served.

c) Annual statistics of service (i.e. circulation of materials, collection size,

hours of service, etc.)

4) Anticipated Capital Projects Fund Resources that will be available for the term of the

plan. For each year of the plan (show also on LCPF PLAN SUMMARY PAGE):

Include the following:

a) Sources and amounts of anticipated income.

b) Amount of revenue to be retained for expenditures proposed for a later year.

c) Projected assessed valuation of the Library District for each year of the plan.

d) Projected tax rates and levies for the LCPF based on the above assessed

valuations.

5) Proposed use of the LCPF

A) Includes, by plan year and location, the proposed expenditures from the fund

for all specific uses within the following areas:

1) Planned facility needs:

a) New construction.

b) Repair.

c) Replacement.

d) Remodeling.

e) Lease or rental of existing real estate.

8

2) Acquisition of real property

3) Site development

4) Emergency allocation (repair, replacement or site acquisition that is

necessitated by an emergency)

5) Purchase, lease, repair and maintenance of Equipment

a) Administration.

b) Public use.

c) Mechanical.

d) Furniture.

6) Computer hardware and software

a) Purchase or lease.

b) Maintenance and repair.

B) Includes, by plan year, location and project or specific purpose, allocation for

proposed expenditures beyond the upcoming budget year (Allocation for

Future Projects).

Failure to comply with the above format may be cause for disapproval.

9

GLOSSARY OF TERMS

The following definitions apply to LCPF.

1) REPAIR means the restoration of a piece of equipment, a building or land from worn,

damaged or deteriorated condition to or near its original condition.

2) EQUIPMENT means a mobile or fixed unit of furniture or furnishings, an instrument

or set of articles meeting the following conditions:

a) It retains the original shape.

b) It is non-expendable, which means that if the article is damaged or some of its

parts are lost or worn out, it is usually more feasible and economical to repair

it than replace it with an entirely new unit.

c) It represents an investment of money that makes it feasible and advisable to

capitalize the item.

d) It does not lose its identity through incorporation into a different or more

complex unit.

3) EMERGENCY is defined with respect to the LCPF as follows:

a) Repair or replacement of buildings or equipment caused by a fire, flood,

windstorm, mechanical failure, or other unforeseen circumstances, and

b) The unforeseeable availability of real property for purchase when referring

to site acquisition.

COMPLETING THE LIBRARY CAPITAL PROJECTS FUND SUMMARY PAGE:

The purpose of the LCPF Summary Page is to summarize the expenditures, allocations,

transfers, and revenues for your LCPF Plan. The general format is the same as the public notices

for the LCPF Plan.

CURRENT EXPENDITURES is a summary of the planned expenditures noted in each major

classification in your LCPF Plan for each year of the plan for all locations.

SUBTOTAL CURRENT EXPENDITURES is the amount of expenditures that you plan to make

in a given year which require appropriation.

ALLOCATION FOR FUTURE PROJECTS (AFP) is the amount of funds that will accumulate

or continue accumulating for projects to be expended in the second, third, or future year of the

LCPF Plan. Any AFP(s) should be clearly noted on the appropriate location page(s) in your

LCPF Plan. If you plan to expend the AFP in the second or third years, this will increase the

current expenditures and decrease the AFP. If you do not intend to spend the AFP in the second

or third years, the AFP for those years should show the total that you expect will be accumulated

at the end of the year. The AFP budgeted in the third year should include the amount

accumulated in years one and two, plus what will be accumulated during year three. The

summary page of the AFP should be cumulative summation of the AFP from each location.

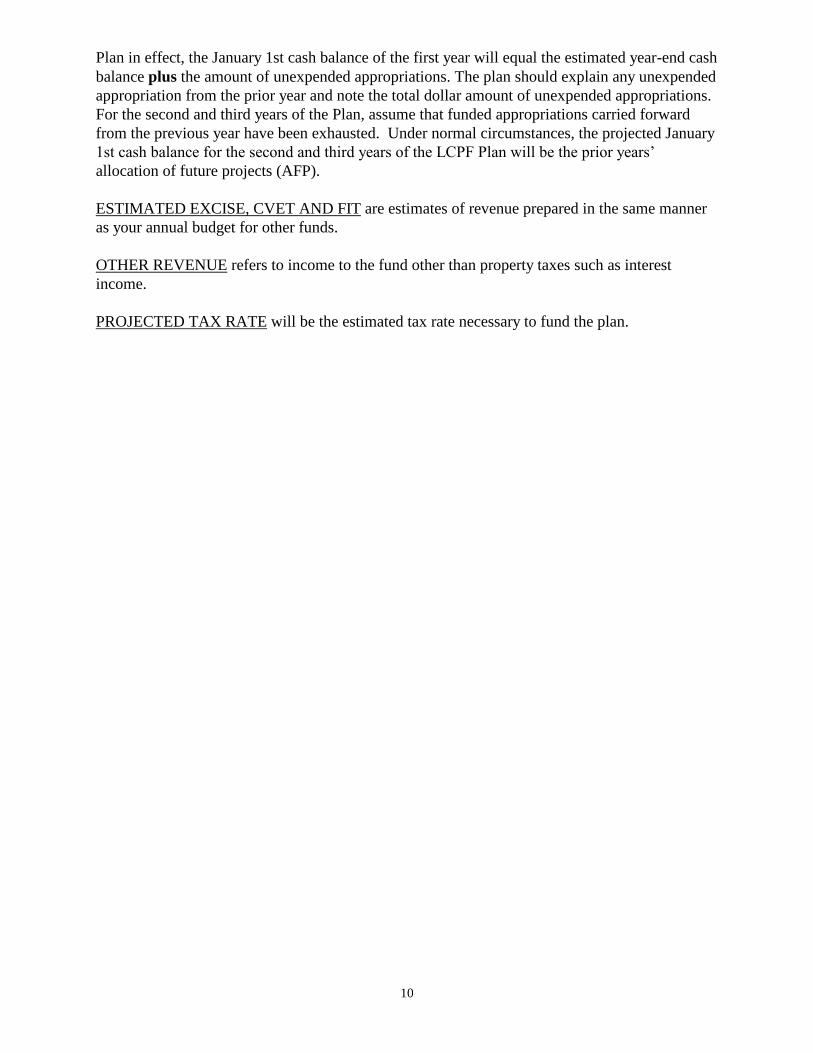

CASH BALANCE AVAILABLE TO FUND THE LCPF PLAN For libraries beginning the first

year of their first plan, the beginning cash balance will be zero (0). For libraries that have a LCPF

10

Plan in effect, the January 1st cash balance of the first year will equal the estimated year-end cash

balance plus the amount of unexpended appropriations. The plan should explain any unexpended

appropriation from the prior year and note the total dollar amount of unexpended appropriations.

For the second and third years of the Plan, assume that funded appropriations carried forward

from the previous year have been exhausted. Under normal circumstances, the projected January

1st cash balance for the second and third years of the LCPF Plan will be the prior years’

allocation of future projects (AFP).

ESTIMATED EXCISE, CVET AND FIT are estimates of revenue prepared in the same manner

as your annual budget for other funds.

OTHER REVENUE refers to income to the fund other than property taxes such as interest

income.

PROJECTED TAX RATE will be the estimated tax rate necessary to fund the plan.

11

QUESTIONS ABOUT LIBRARY CAPITAL PROJECTS FUND

PURCHASES FROM THE LCPF

1. WHAT KIND OF VEHICLES MAY BE PURCHASED FROM LCPF?

Any vehicles for library use including bookmobiles, vans and automobiles may be purchased from

LCPF.

2. MAY LIBRARY MATERIALS AND/OR BOOKS BE PURCHASED FROM LCPF?

NO- the LCPF cannot be used to purchase library materials and/or books, with the exception of

computer software.

3. MAY THE LCPF PLAN INCLUDE FEASIBILITY STUDIES AND ARCHITECT FEES?

YES- the planned expenditures should be included in item one (1) Planned construction, etc. of the

LCPF PLAN SUMMARY. If the architect fees are to be reimbursed, such as in the formation of a

holding corporation, the anticipated reimbursement would be included in the LCPF PLAN

SUMMARY as other revenue.

4. MAY WE PAY FOR ARCHITECT FEES TO DESIGN A BUILDING THAT A HOLDING

CORPORATION WILL PURCHASE AT A LATER DATE?

YES- the LCPF Plan should anticipate the expenditures under Planned Facility Needs (item one

(1)) on the Plan Summary. If the library anticipates reimbursement from the holding corporation,

the reimbursement should be estimated under "other revenue."

5. WHAT ARE SOME EXAMPLES OF “REPLACEMENTS” (ITEM ONE (1) UNDER CURRENT

EXPENDITURES OF THE PLAN)?

Replacements may include carpet, shelving, and computer equipment. For specific questions about

what is a replacement item, contact the Department of Local Government Finance or the State

Board of Accounts.

6. SHOULD WE INCLUDE A NARRATIVE SECTION IN THE PLAN FORMAT FOR SITE

DEVELOPMENT?

Yes.

7. WOULD LANDSCAPING BE CONSIDERED SITE DEVELOPMENT?

It depends on what type of landscaping. Please refer specific questions to the Department of Local

Government Finance or State Board of Accounts.

APPROPRIATIONS

8. IF WE SPEND LESS THAN PLANNED IN ONE PORTION OF THE LCPF PLAN, MAY WE

TRANSFER THE SURPLUS APPROPRIATIONS TO ANOTHER AREA WHERE WE WOULD LIKE

TO SPEND MORE THAN PLANNED?

No- A LCPF Plan cannot be changed once it has been approved by the Department except in the

case of an amendment approved for an emergency or an appropriation of an allocation for a future

project in a year earlier than planned.

9. IF WE DO NOT SPEND ALL OF THE CAPITAL PROJECT FUND APPROPRIATIONS FOR A GIVEN

YEAR OR WE HAVE ENCUMBRANCES, WOULD THOSE AMOUNTS BE INCLUDED IN THE

ENSUING YEAR’S JANUARY 1 CASH BALANCE?

The January 1 cash balance on the Capital Projects plan summary is the estimated or anticipated

cash balance for the ensuing year. If you anticipate unexpended appropriations or encumbrances

for the current year’s plan, then those amounts would be included in the estimated January 1 cash

balance for the ensuing year. The January 1 cash balance may also include allocation for future

projects from the previous year(s).

12

10. IF THE CAPITAL PROJECTS PLAN IS DENIED AND THERE IS A CASH BALANCE, CAN I DO AN

ADDITIONAL APPROPRIATION TO SPEND THAT MONEY?

No, if the plan is denied you may not appropriate funds in the Capital Projects Fund.

THE LIBRARY’S FISCAL BODY

11. MUST THE FISCAL BODY WHO APPROVES THE PLAN ADVERTISE FOR THE REQUIRED

PUBLIC HEARING?

YES – the fiscal officer must give notice of the public hearing to consider the plan. The notice

must be published one (1) time at least ten (10) days before the date of the hearing in accordance

with IC 5-3-1-2. The Library may offer to publish this notice for the fiscal body to ensure that the

advertisement complies with the necessary requirements.

12. HOW DO WE CERTIFY COPIES OF THE LCPF PLAN TO THE LOCAL FISCAL BODY AND THE

DEPARTMENT?

A Certificate of Submission, signed by the Library Board Secretary attesting to the actions of the

Library Board in adopting the LCPF Plan is used for certification. A suggested certification form

is included with the LCPF memo.

13. CAN THE LIBRARY PAY FOR THE ADVERTISEMENT OF THE FISCAL BODY’S PUBLIC

HEARING?

Yes, the Library may submit the Notice to Taxpayers to the newspaper of the fiscal body’s public

hearing and pay for the advertisement.

14. IS THERE A PRESCRIBED FORMAT FOR THE NOTICE TO TAXPAYERS OF THE PUBLIC

HEARING BY THE FISCAL BODY?

A suggested format is included with the LCPF memo.

15. SOME FISCAL BODIES (OF THE LIBRARIES) ADVERTISE THE ENTIRE CAPITAL PROJECTS

PLAN WITH THE NOTICE TO TAXPAYERS. IS THAT PERMISSIBLE?

Yes, but not required. The fiscal body only needs to advertise the date, time and location of the

hearing. The ad should also note that the fiscal body plans to discuss the library capital projects

plan. A suggested format of the notice to taxpayers by the fiscal body is included with the LCPF

memo.

16. IS IT POSSIBLE FOR A FISCAL BODY TO APPROVE APPROPRIATIONS FOR A CAPITAL

PROJECTS PLAN BUT NOT APPROVE A TAX RATE AND LEVY?

Yes.

17. CAN A FISCAL BODY APPROVE A LOWER TAX RATE AND/OR LEVY THAN ADOPTED BY

THE LIBRARY BOARD?

Yes, however it is the responsibility of the Library Board/Director to modify the plan to

accommodate the lower rate and/or levy.

PLAN AMENDMENTS (EMERGENCIES)

18. MAY WE AMEND THE LCPF PLAN FOR NON-EMERGENCY REASONS?

NO- Libraries may only amend the LCPF Plan for emergency reasons as outlined in

IC 36-12-12-9.

19. IF AN EMERGENCY SITUATION OCCURS AND WE NEED TO USE LCPF MONEYS HOW DO WE

CONTACT THE DEPARTMENT?

The Department may be reached by telephone (317-232-0651) and by Faxing (317-232-8779) a

written explanation of the emergency and the proposal for an amendment to the LCPF Plan.

13

20. WHAT IF AN EMERGENCY SITUATION OCCURS AND THE LIBRARY DOES NOT HAVE

APPROPRIATIONS IN THE EMERGENCY ALLOCATION LINE ITEM OR THE LIBRARY DOES

NOT HAVE ENOUGH APPROPRIATIONS IN THAT ALLOCATION TO COVER THE

EMERGENCY?

The Library needs to do an amendment to their Capital Projects plan.

21. HOW QUICKLY CAN AN EMERGENCY AMENDMENT BE APPROVED BY THE DEPARTMENT

OF LOCAL GOVERNMENT FINANCE?

The Department of Local Government Finance will not delay approval on emergency amendments

to the Capital Projects Plan. Please contact the Department of Local Government Finance for

assistance in preparing an amendment to your plan.

ESTABLISHING THE FUND AND THE BUDGET PROCESS

22. IF I RECEIVE AN ORDER APPROVING THE LIBRARY CAPITAL PROJECTS PLAN, MUST I ALSO

GO THROUGH THE NORMAL BUDGET PROCESS?

YES – The submission of the plan to the Department is for approval of the Library Capital

Projects Plan under IC 36-12-12-3. The budget process is subject to IC 6-1.1-17. The Library

Capital Projects Fund must be advertised and adopted as would any other fund for the ensuing

budget year. Failure to do so will result in the appropriations, levy and rate being denied.

23. IS THE LCPF THE SAME AS THE LIBRARY IMPROVEMENT RESERVE FUND (LIRF)?

NO- funds for accumulation in the LIRF come from the Operating Fund Budget as a Transfer to

LIRF and fall within the maximum levy limit set for the Operating Fund. The library may levy a

separate tax rate of not more than one and sixty-seven hundredths cents ($.0167) annually for

accumulation of funds in the LCPF.

24. DOES THE LCPF REPLACE THE LIRF?

NO- both funds are permitted under Indiana Library Law (LCPF: IC 36-12-12 and LIRF: IC 36-12-3-

11).

25. MUST I GO THROUGH THE PLAN AND BUDGET PROCEDURE TO EXPEND FUNDS EVEN IF

OUR LIBRARY DOES NOT WANT A TAX RATE?

YES – IC 36-12-12-8 states that the Department of Local Government Finance may approve

appropriations from the Capital Projects Fund only if the appropriations conform to a plan that has been

advertised and adopted.

26. I ADVERTISED A $.0133 RATE FOR MY CAPITAL PROJECTS FUND IN MY ANNUAL BUDGET.

WHEN I RECEIVED MY BUDGET ORDER, THE RATE WAS REDUCED TO $.005. WHY DIDN’T I

GET THE FULL RATE?

The Library Capital Projects Fund is based upon the need shown in the plan. Need refers to the

total Current Expenditures and Allocation for Future Projects. During the budget process, the rate

approved will be lowered if Current Expenditures and Allocation for Future Projects can be funded

at a lower rate. Also, the rate could be lower because of the adjustment made per IC 6-1.1-18-12.

REVENUES , CASH AND OPERATING BALANCE

27. WHERE DOES THE JANUARY 1 CASH BALANCE COME FROM ON THE PLAN SUMMARY?

A cash balance in the Library Capital Projects Plan can only come from:

(1) Allocation for future projects from the previous year(s)

(2) Unexpended appropriations from previous year(s).

A narrative within the plan must indicate the sources of the anticipated January 1 cash balance for

the ensuing year. Later year cash balances are reflective of the previous year future allocation

amount.

14

28. ISN’T MY OPERATING BALANCE THE SAME AS MY FUTURE ALLOCATIONS?

Yes, the operating balance is the amount of future allocations detailed in your plan. Keep in mind

that the Department of Local Government Finance will not approve a future allocation (line 11)

that is higher than adopted in the plan.

ACCOUNTING FOR CAPITAL PROJECTS FUNDS

29. WHAT IF I HAVE MONEY LEFT OVER IN MY CAPITAL PROJECTS FUND AND IT IS NOT

APPROPRIATED FOR ANYTHING?

The money will remain in the fund and will be accounted for in the operating balance.

30. IF WE USE THE LCPF TO HELP PAY FOR A PROJECT THAT INCLUDES BONDS AS PART OF

THE FINANCING, DO WE DISBURSE THE BOND PROCEEDS THROUGH THE LCPF?

NO- bond proceeds for a project are disbursed through a Construction Fund.

31. WHAT IF MY ENSUING YEAR’S CAPITAL PROJECTS PLAN IS DENIED, AND I HAVE FUNDS

LEFT OVER?

You will have a Capital Projects Fund with a cash balance. This cash balance cannot be

transferred to the Library Operating Fund unless the LCPF is declared dormant.

32. DOES THE INTEREST GENERATED FROM THE CASH IN THE CAPITAL PROJECTS FUND NEED

TO BE RECEIPTED TO THE CAPITAL PROJECTS FUND?

Yes, refer specific questions about this to the Board of Accounts.

33. DO WE NEED TO SET UP A SEPARATE FUND TO ACCOUNT FOR THE CAPITAL PROJECTS

PLAN?

Yes.

34. ARE THERE ANY SPECIAL ACCOUNTING GUIDELINES ASSOCIATED WITH THE CAPITAL

PROJECTS FUND?

Generally, this fund is handled like any other fund. Please refer specific questions on this to the

Board of Accounts.

35. DO WE INCLUDE OUR LOCAL MATCHING FUNDS FOR A LCPF PROJECT IN THE ESTIMATES

OF "OTHER REVENUE" IN THE LCPF PLAN SUMMARY FOR EACH FISCAL YEAR?

NO- local matching funds should be appropriated in the Library Operating Fund, LIRF or other

special fund and should not be included in the LCPF Plan Summary or the LCPF Budget. A

description and explanation of use of the local matching funds should be included as a part of the

narrative describing the LCPF Plan.

OTHER

36. CAN THE PUBLIC HEARING BE HELD ON THE SAME DAY AS A REGULAR LIBRARY BOARD

MEETING? CAN THE PUBLIC HEARING BE HELD ONE HOUR BEFORE THE BOARD

MEETING?

Yes, if advertised correctly beforehand, the public hearing for the Capital Projects Fund may be

held on the same day as the Library Board meeting and can be held an hour before the Board

meeting or at any time specified by the advertisement of the meeting. It is important to note that

the public hearing must be held on the date and time advertised in the Notice to Taxpayers of the

hearing.

37. IF I AM ACCUMULATING MONEY IN MY FUTURE ALLOCATIONS FOR A NEW ROOF (1/3 OF

THE COST EACH YEAR) AND THE FISCAL BODY DENIES MY FUTURE ALLOCATION FOR THE

FINAL (3RD) YEAR, CAN I STILL PURCHASE THE ROOF IF I HAVE SUFFICIENT MONEY IN MY

FUND?

No, but it may be possible to purchase the roof through an emergency amendment. Contact the

15

Department of Local Government Finance.

38. WILL THE AD FROM THE PAPER BE SUFFICIENT TO SUBMIT TO THE DEPARTMENT OF

LOCAL GOVERNMENT FINANCE?

No, a proof of publication from the newspaper is the legal documentation that is required for

advertisements associated with the Capital Projects Plan.

39. IS THE ANNUAL COST FOR TELEPHONE LINES AN ALLOWABLE EXPENSE FROM THE CPF?

No, telephone lines are not considered equipment so the rental charges for this item are not an

allowable expense.

40. CAN THE COST OF INTERNET EXPENSES BE USED AS AN ALLOWABLE EXPENSE FROM THE

LCPF - THIS WOULD INCLUDE EDUCATIONAL SERVICES PROVIDED THROUGH THE

INTERNET?

The initial cost for the installation of the lines could be an allowable expense; however, the

monthly fees for internet service would not qualify.

16

RESOLUTION TO ADOPT LIBRARY CAPITAL PROJECTS FUND PLAN

This resolution is adopted by the Library Board of ____________________________

(Library Name)

of ______________________,County, Indiana.

Whereas, a Library Capital Projects Fund has been established; and

Whereas, the Library Board is required under IC 36-12-12-3 to adopt a plan with respect

to the Library Capital Projects Fund; and

Whereas, the Library Board held a public hearing on the plan on __________________

(Date)

at ____________________________________________________________________

(Location)

THEREFORE BE IT RESOLVED, by the Library Board that the plan entitled

______________________________________________ of ___________________________

(Title) (Date)

is hereby incorporated by reference into this resolution, and is adopted as the Library Board's

plan with respect to the Library Capital Projects Fund.

BE IT FURTHER RESOLVED that the Library Board will submit a certified copy of

this resolution (including the adopted plan) to the appropriate local fiscal body for review and the

Department of Local Government Finance under IC 36-12-12-5.

ADOPTED THIS _________ DAY OF ____________________________, 20____.

AYE NAY

______________________________ ______________________________

______________________________ ______________________________

______________________________ ______________________________

______________________________ ______________________________

______________________________ ______________________________

______________________________ _______________________________

ATTEST:

________________________________

Secretary of Library Board

17

Certificate of Submission to Appropriate Fiscal Body

I, THE UNDERSIGNED OF ______________________________PUBLIC LIBRARY, (Name of Library)

_________________ COUNTY, INDIANA, DO HEREBY CERTIFY TO THE _____________________ (Appropriate Fiscal Body)

________________________________ OF __________________________________, (Unit) _____________________________, INDIANA, (County)

THAT THE ATTACHED IS A COMPLETE TRANSCRIPT OF THE PROCEEDINGS HELD

WITH RESPECT TO THE LIBRARY CAPITAL PROJECTS FUND PLAN ADOPTED BY

THE ABOVE NAMED LIBRARY AT A MEETING HELD ON _______________________. (Date)

NOTICE

PURSUANT TO IC 36-12-12-4 THE APPROPRIATE FISCAL BODY SHALL HOLD A

PUBLIC HEARING ON THIS ISSUE WITHIN THIRTY (30) DAYS OF RECEIPT AND IF

THE PLAN IS APPROVED, PASS SUCH RESOLUTION BEFORE AUGUST 1 OF THE

CURRENT YEAR.

Submitted this ______ day of ________________, 2_____ to the above named fiscal body.

_________________________________ (Signature of Secretary of Library Board)

Instructional Note: The “Submitted” date is the date the LCPF plan was forwarded to the appropriate fiscal body.

18

RESOLUTION OF APPROPRIATE FISCAL BODY OF ACTION ON LIBRARY

CAPITAL PROJECTS PLAN

WHEREAS, the ___________________________ has adopted a Library Capital Projects Plan (Name of Library)

as provided for in IC 36-12-12, be it resolved that the __________________________, being the (Name of Fiscal Body)

appropriate Fiscal Body for the __________________________ as designated in IC 36-12-12-4, (Name of Library)

does hereby _______________________the Plan as received by this body on the _____ day (Approve/Reject)

of _________________, 20___.

ADOPTED THIS _________ DAY OF ______________________, 20____.

AYE NAY

___________________________________ _________________________________

___________________________________ _________________________________

___________________________________ _________________________________

___________________________________ _________________________________

___________________________________ _________________________________

___________________________________ _________________________________

___________________________________ _________________________________

ATTEST:

___________________________________

Secretary of Fiscal Body

Instructional Note: Must be adopted before August 1 of the current year.

19

NOTICE TO TAXPAYERS OF ____________________ PUBLIC LIBRARY

Notice is hereby given to the taxpayers of ______________________, __________________ County, that the Library Board (Library Name) (County Name)

will meet at ____________________, on ________________________ for the purpose of considering a proposal to establish a (Location) (Date and Time)

Library Capital Projects Fund and a proposed plan under IC 36-12-12. The following is a general outline of the proposed plan.

CURRENT EXPENDITURES: 20___ 20 ___ 20 ___

(1) Planned construction, repair, replacement, or remodeling _______ _______ _______

(2) Acquisition of real property _______ _______ _______

(3) Site development _______ _______ _______

(4) Emergency Allocation _______ _______ _______

(5) Purchase, lease, repair, and maintenance of equipment _______ _______ _______

(6) Purchase, lease, repair, and maintenance of computer

hardware and computer software _______ _______ _______

SUBTOTAL CURRENT EXPENDITURES _______ _______ _______

(7) Allocation for future projects (cumulative totals) _______ _______ _______

TOTAL EXPENDITURES AND ALLOCATIONS _______ _______ _______

SOURCES AND ESTIMATES OF REVENUE:

(1) January 1, Cash balance (for each year of plan) _______ _______ _______

(2) Less encumbered appropriations _______ _______ _______

(3) Cash balance available for current plan [ (1) minus (2) ] _______ _______ _______

(4) Plus Property Tax Revenue _______ _______ _______

(5) Plus Auto Excise, CVET and Financial Institutions Tax receipts _______ _______ _______

(6) Plus Other revenue _______ _______ _______

TOTAL FUNDS AVAILABLE FOR PLAN _______ _______ _______

Based upon an anticipated assessed valuation of _______ _______ _______

The Projected Tax Rate for the Library Capital Projects fund will be _______ _______ _______

Taxpayers are invited to attend the meeting for a more detailed explanation of the plan and to exercise their right to be heard on

the proposal.

(Show names and titles (_____________________

of board members) (_____________________

(_____________________

(_____________________

(_____________________

(_____________________

(_____________________

Date:

20

Township: Sample Notice to Taxpayers by Fiscal Body (Library CPF)

NOTICE TO TAXPAYERS

The Township Board of ________________Township, _____________County, Indiana will

hold a public hearing on the _____ day of ___________, 20___, at ____________a.m./p.m. at

the office of the ____________ Township Trustee, ________________________, Indiana, for (address)

the purpose of approving the Library Capital Projects Fund Plan for the year 20___, for the

________________________________________. (Name of Library)

_____________________________

Township Trustee

21

County: Sample Notice to Taxpayers by Fiscal Body (Library CPF)

NOTICE TO TAXPAYERS

The ________________County Council, _____________County, Indiana will hold a public

hearing on the _____ day of ___________, 20___, at ____________a.m./p.m. at the

__________________________________________, ________________________, Indiana, (location of meeting) (address)

for the purpose of approving the Library Capital Projects Fund Plan for the year 20___, for the

________________________________________. (Name of Library)

_____________________________

County Auditor

22

City or Town: Sample Notice to Taxpayers by Fiscal Body (Library CPF)

NOTICE TO TAXPAYERS

The ________________City (or Town) Council, _____________County, Indiana will hold a

public hearing on the _____ day of ___________, 20___, at ____________a.m./p.m. at the

__________________________________________, ________________________, Indiana, (location of meeting) (address)

for the purpose of approving the Library Capital Projects Fund Plan for the year 20___, for the

________________________________________. (Name of Library)

_____________________________

Clerk-Treasurer

23

N O T I C E OF A M E N D M E N T

Notice is hereby given to the taxpayers of _____________________________________________________ Public Library of

______________________________, County, Indiana, that the Library Board has determined that the Library Capital Projects

Plan it adopted for the years 2_____ to 2______ should be amended, did adopt a resolution to amend the said plan at a meeting

held on _____________________, 2______. A brief description of the amendment is as follows:

______________________________________________________________________________________________________

______________________________________________________________________________________________________

______________________________________________________________________________________________________

______________________________________________________________________________________________________

The following is a general outline of the plan with the proposed amendment:

CURRENT EXPENDITURES 2____ 2____ 2____

(1) Planned construction, repair, replacement, or remodeling ______ ______ ______

(2) Acquisition of real property ______ ______ ______

(3) Site development ______ ______ ______

(4) Emergency Allocation ______ ______ ______

(5) Purchase, lease, repair, and maintenance of equipment ______ ______ ______

(6) Purchase, lease, repair, and maintenance of computer

hardware and computer software ______ ______ ______

SUBTOTAL CURRENT EXPENDITURES ______ ______ ______

(7) Allocation for future projects ______ ______ ______

TOTAL EXPENDITURES AND ALLOCATIONS ______ ______ ______

Ten (10) or more taxpayers in the library district who will be affected by the plan, as amended, may file a petition with the

County Auditor of _____________________________ County, not later than ten (10) days after the publication of this notice,

setting forth their objections to the amendment. Upon filing of the petition, the County Auditor shall immediately certify the

same to the Department of Local Government Finance, which Department will fix a date and conduct a public hearing on the

plan before issuing its approval or disapproval thereof.

(______________________________________________

(______________________________________________

(______________________________________________

(______________________________________________

(Show names and titles (______________________________________________

of Board Members) (______________________________________________

(______________________________________________

Attest:

____________________________

Secretary of Library Board

Date:

24

PROOFS OF PUBLICATION AND COUNTY AUDITORS CERTIFICATE OF NO REMONSTRANCE MUST BE FORWARDED TO

THE DEPARTMENT NOT LATER THAN TEN (10) DAYS FOLLOWING THE OBJECTION PERIOD.

* THIS IS A SAMPLE ONLY. THE DEPARTMENT OF LOCAL GOVERNMENT FINANCE WILL PREPARE THE SECOND

NOTICE AND MAIL TO THE LIBRARY FOR ADVERTISING.

NOTICE OF ADOPTION

There has been filed with the Department of Local Government Finance a certified copy of the resolution adopted by the proper legal

officers of (library name) establishing a capital projects fund together with proofs of publication of notice thereof, pursuant to I.C. 36-12-12.

The proper legal officers of (library name) are hereby requested by the Department of Local Government Finance to publish the following notice

in accordance with I.C. 36-12-12-5(a).

PUBLISH THE FOLLOWING ONLY

(Library Name)

CURRENT EXPENDITURES: 2___ 2___ 2___

(1) Planned construction, repair, replacement, or remodeling _______ _______ _______

(2) Acquisition of real property _______ _______ _______

(3) Site development _______ _______ _______

(4) Emergency Allocation _______ _______ _______

(5) Purchase, lease, repair, and maintenance of equipment _______ _______ _______

(6) Purchase, lease, repair, and maintenance of computer

hardware and computer software _______ _______ _______

SUBTOTAL CURRENT EXPENDITURES _______ _______ _______

(7) Allocation for future projects (cumulative totals) _______ _______ _______

TOTAL EXPENDITURES AND ALLOCATIONS _______ _______ _______

SOURCES AND ESTIMATES OF REVENUE:

January 1, Cash balance (of each year of plan) _______ _______ _______

Less encumbered appropriations _______ _______ _______

Equals Cash balance available for current plan _______ _______ _______

Plus Auto Excise, CVET and Financial Institutions Tax receipts _______ _______ _______

Plus Other revenue _______ _______ _______

TOTAL FUNDS AVAILABLE FOR PLAN Based upon an assessed valuation of _______ _______ _______

The Projected Tax Rate for the Library Capital Projects fund will be _______ _______ _______

Ten or more taxpayers in the library district who will be affected by the plan may file a petition with the County Auditor of

_______________________________ County, not later that then (10) days after publication of this notice, setting forth their objections to the

plan. Upon filing of the petition, the County Auditor shall immediately certify the same to the Department of Local Government Finance, which

Department will fix a date and conduct a public hearing on the plan before issuing its approval or disapproval thereof.

DEPARTMENT OF LOCAL GOVERNMENT FINANCE

______________________________________________ Michael C. Dart, General Counsel

Dated this ________ day of _________________, 20____

25

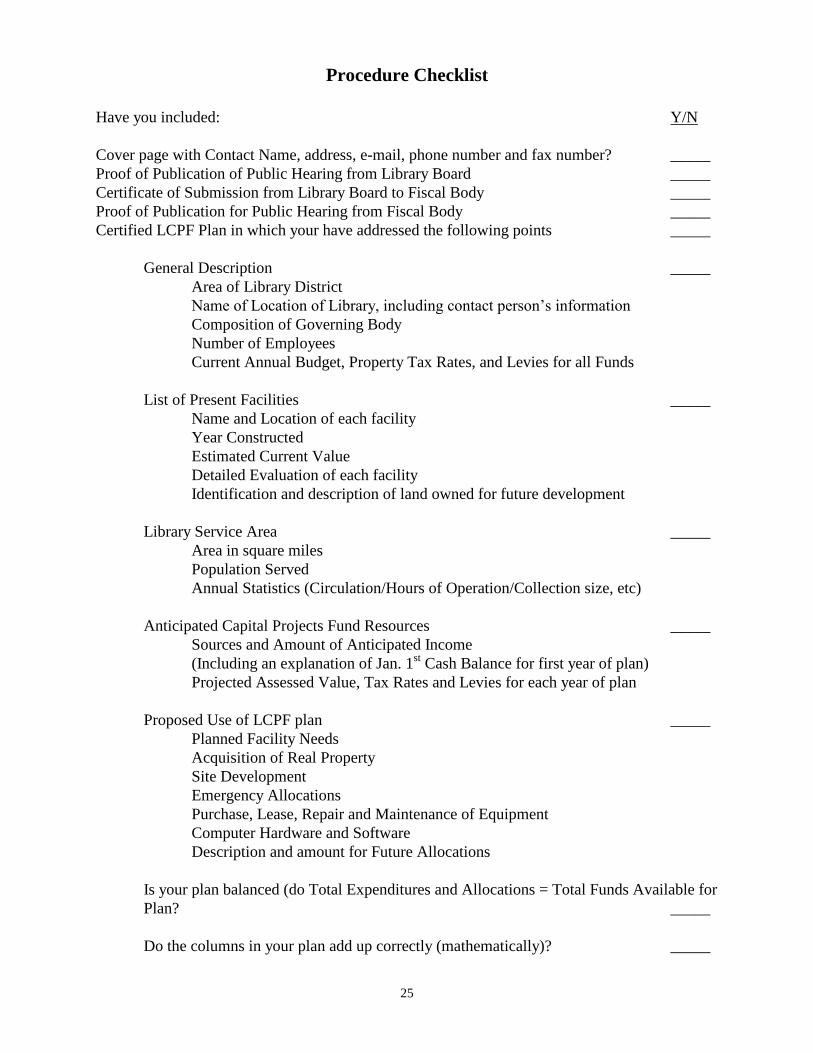

Procedure Checklist

Have you included: Y/N

Cover page with Contact Name, address, e-mail, phone number and fax number? _____

Proof of Publication of Public Hearing from Library Board _____

Certificate of Submission from Library Board to Fiscal Body _____

Proof of Publication for Public Hearing from Fiscal Body _____

Certified LCPF Plan in which your have addressed the following points _____

General Description _____

Area of Library District

Name of Location of Library, including contact person’s information

Composition of Governing Body

Number of Employees

Current Annual Budget, Property Tax Rates, and Levies for all Funds

List of Present Facilities _____

Name and Location of each facility

Year Constructed

Estimated Current Value

Detailed Evaluation of each facility

Identification and description of land owned for future development

Library Service Area _____

Area in square miles

Population Served

Annual Statistics (Circulation/Hours of Operation/Collection size, etc)

Anticipated Capital Projects Fund Resources _____

Sources and Amount of Anticipated Income

(Including an explanation of Jan. 1st Cash Balance for first year of plan)

Projected Assessed Value, Tax Rates and Levies for each year of plan

Proposed Use of LCPF plan _____

Planned Facility Needs

Acquisition of Real Property

Site Development

Emergency Allocations

Purchase, Lease, Repair and Maintenance of Equipment

Computer Hardware and Software

Description and amount for Future Allocations

Is your plan balanced (do Total Expenditures and Allocations = Total Funds Available for

Plan? _____

Do the columns in your plan add up correctly (mathematically)? _____