lxc coin ltd - complete white paper

TRANSCRIPT

LXCCOIN LTDWHITEPAPER

The following pages describe the LXCCoin and its related business. It does not purport to be “all-inclusive” documentation; for further info on any part described herein; please get in touch on [email protected]

Prepared by H Ellefsen[Co-authored by Gravgaard /

Wong /Castberg / Nielsen]Updated 20 August 2014

2

“The government is to explore the role that digital currencies such as Bitcoin could play in

the financial system and whether they need to be regulated. [We have] set out measures

that will make Britain the global centre of such financial innovation".

-Chancellor George Osborne to BBC, 6th August 2014, speaking on the subject of

Cryptocoins (http://www.bbc.com/news/uk-28670414#story_continues_1)

bit.coin.je, an industry body set up to promote and campaign for cryptocurrency,

wanting to make Jersey a "Bitcoin Isle“ comments:

“[Cryptocoins] is a sector that could hold significant opportunities. Our infrastructure of

world-class financial services and digital expertise gives us the tools to be an early leader

in the field. Innovation will be central to Jersey's future prosperity. We are keen to

support local businesses by helping to create a well-regulated and responsive

environment for investment in the sector.“

-Treasury Minister Senator Philip Ozouf

(http://www.bbc.com/news/world-europe-jersey-27921445)

© LXC Coin™ 2014

3

EXECUTIVE SUMMARY

LXCCoin Ltd is a UK company with two main

business areas: P2P investments and

cryptocoin facilitation, which are combined in

one product – the LXC cryptocoin

Our cryptocoin is like no other; targeting a

yield of 15% per year, derived from P2P loan

investments, and strict regulation of demand

and supply by financial measures, governing

trading and use, in a stabile and forecastable

manner

Our seven strong team includes two lawyers

and six specialized experts within finance, IT

and crypto currencies. We have spent more

than a year developing the concept, including

thorough testing, discussions with financial

authorities, self-regulation and funding;

readying for a Q4-14 launch and a 2015

listing target for visibility and transparency

We’re a second generation crypto currency company, with real asset value based + interest

bearing coins, and a framework structure surrounding it to maximize profitability and usability

Big Idea: Aim:

“Real”, safe, stabile cryptocurrency

Solve main problems of cryptocurrency today. A

supplement and not a competitor to all other

cryptocoins. Limited number POS coin

Increased liquidity enhancing value for P2P lenders

Create a P2P second-hand marketplace to ease

P2P investing exits and make P2P more investor

friendly, plus a supporting trading fund to ensure

activity on the platform

Bridge P2P lending and vast cyberspace funding resources

Create a P2P-investing crypto currency,

independent of countries and/or legislations, with

international freedom of movement and

ownership, allowing all the billions in cyberspace

to be used for P2P lending

Use cryptocoins for multinational P2P lending – doubling capacity and profit

Enable P2P lenders to operate worldwide, and

effectively doubling their financial capacity by

using safe cryptocoins as a new lending

instrument, combined with current P2P platforms

© LXC Coin™ 2014

4

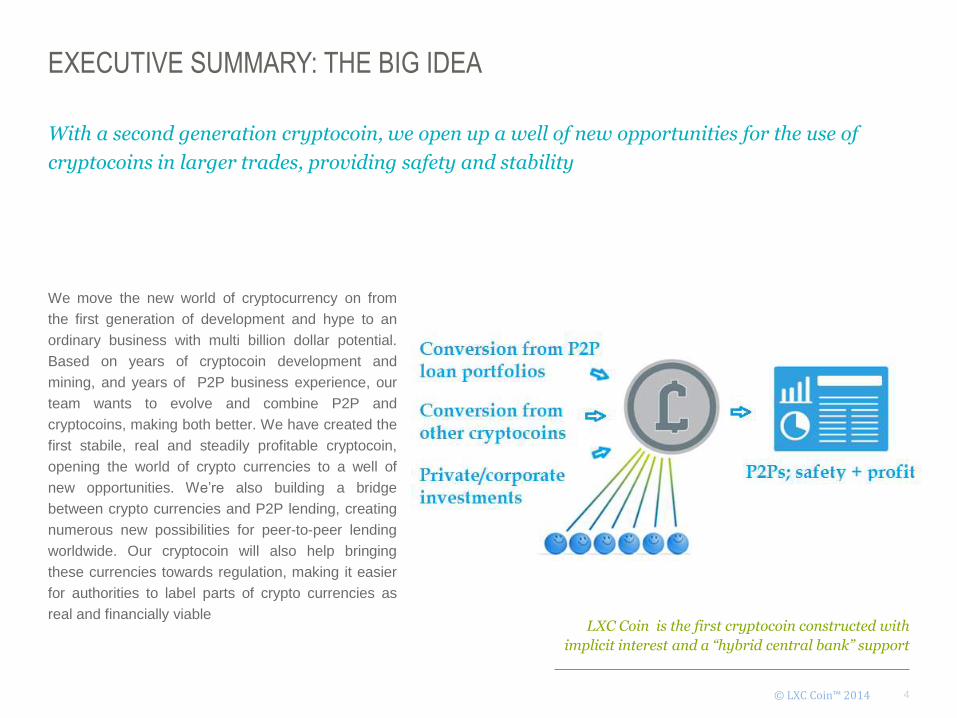

EXECUTIVE SUMMARY: THE BIG IDEA

We move the new world of cryptocurrency on from

the first generation of development and hype to an

ordinary business with multi billion dollar potential.

Based on years of cryptocoin development and

mining, and years of P2P business experience, our

team wants to evolve and combine P2P and

cryptocoins, making both better. We have created the

first stabile, real and steadily profitable cryptocoin,

opening the world of crypto currencies to a well of

new opportunities. We’re also building a bridge

between crypto currencies and P2P lending, creating

numerous new possibilities for peer-to-peer lending

worldwide. Our cryptocoin will also help bringing

these currencies towards regulation, making it easier

for authorities to label parts of crypto currencies as

real and financially viable

With a second generation cryptocoin, we open up a well of new opportunities for the use of

cryptocoins in larger trades, providing safety and stability

LXC Coin is the first cryptocoin constructed with

implicit interest and a “hybrid central bank” support

© LXC Coin™ 2014

5

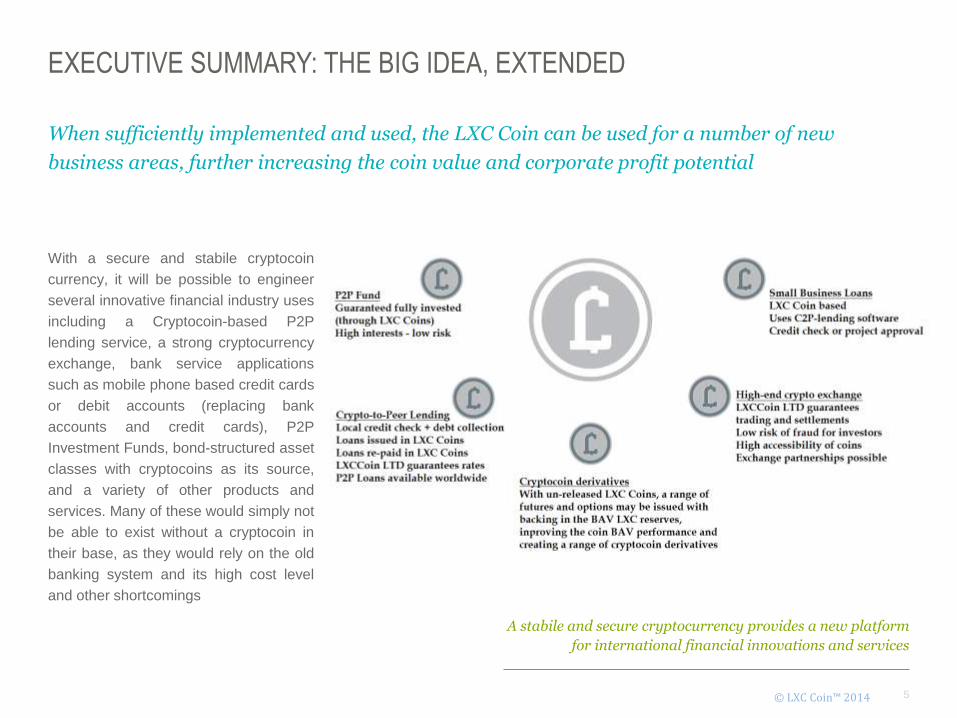

EXECUTIVE SUMMARY: THE BIG IDEA, EXTENDED

With a secure and stabile cryptocoin

currency, it will be possible to engineer

several innovative financial industry uses

including a Cryptocoin-based P2P

lending service, a strong cryptocurrency

exchange, bank service applications

such as mobile phone based credit cards

or debit accounts (replacing bank

accounts and credit cards), P2P

Investment Funds, bond-structured asset

classes with cryptocoins as its source,

and a variety of other products and

services. Many of these would simply not

be able to exist without a cryptocoin in

their base, as they would rely on the old

banking system and its high cost level

and other shortcomings

When sufficiently implemented and used, the LXC Coin can be used for a number of new

business areas, further increasing the coin value and corporate profit potential

© LXC Coin™ 2014

A stabile and secure cryptocurrency provides a new platform

for international financial innovations and services

6

“The massive changes the world has gone through since the invention of the

internet and email has finally caught up with the financial paradigm of the

past century. We’re seeing a lot of financial inventions really moving the

game on; reaching from peer-to-peer operations within lending and funding,

to fantastic production/invention risk-sharing and -supporting through

crowdfunding and crowd equity movements. This is creating more

momentum and higher success rate for entrepreneurs, SMBs and inventors.

With cryptocoins moving the boundaries even further, the financial sector

needs to prepare for a new way of operating in the future.”

Henrik Ellefsen, Founder & CEO, LXCCoin LTD

© LXC Coin™ 2014

7

+ Crypto Exchange business case

+ Exchange features

+ P2P Exchange business case

+ Exchange setup

+ Partners

+ Tehcnology

+ P2P Cryptocoin lending gateway

+ Cryptolending as a P2P service

+ White label services

+ Cryptobanking

+ Debit Cards

+ P2p Fund

+ How P2P changed the world

+ Case study: The Mp3 murder case

+ Case study: The death of Kodak

+ The cryptocoin space explained

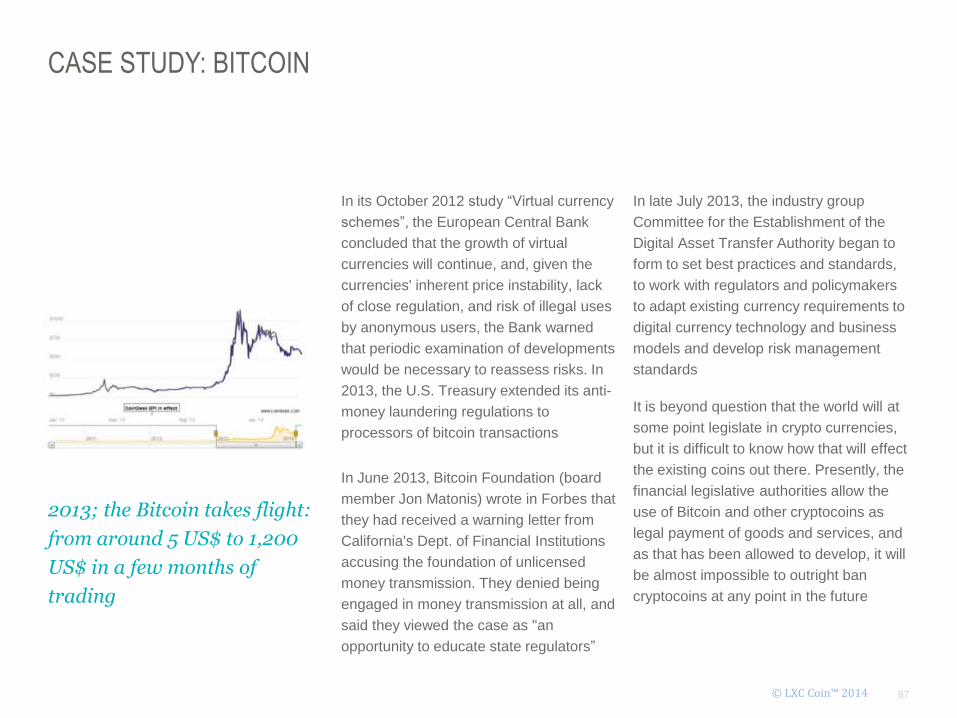

+ Case study: “Bitcoin”

+ Case study: “Dogecoin”

TABLE OF CONTENTS

+ The code

+ Security

+ Network

+ The slow rise

+ Value and launch

+ The “Hybrid Central Bank”

+ Legality

+ Future regulation

LXC Coin cryptocurrency

Exchanges Future business areas

Deeper understanding

01 02 03 04INTRO

Pages 64–94Pages 54–63Pages 45–53Pages 32–44Pages 1–25

LXCCoin Ltd Introduction

P2P EQT (c) 2014© LXC Coin™ 2014

+ The concept

+ The LXC Team

+ Profit model

+ Base Asset Value

+ Valuation and financials

+ Platform/IPR

+ Roadmap

+ Risk factors

8

LXC COIN: THE CONCEPT

LXC Coin is a 100% asset-backed cryptocoin; built on secure official contracts with leading P2Pplatforms – creating a new level of trust for crypto currencies

The world would greatly benefit from a new currency regime, circumventing traditional banks and allowing safe low-cost transactions

without borders and high-cost facilitators. This has led to a lot of positive sentiment revolving the new hybrid currency class named

cryptocoins, which to a certain extent provides a solution to this. Built on open source code the key to making these is widely

available, which has lead to 500+ different coins being created. Sadly, this variety represents more problems than benefits, as there

are too many meaningless “me-too” coins and a lot of scam-attempts or pump-and-dump operations around. And while cryptocoins

are great at transactions, they are a horrible way of storing money. Which is why we’ve created the LXC Coin, which changes that

The LXC Coin is a “standard cryptocurrency”, built on an adapted Bitcoin/Blackcoin code platform, but there the similarity with its

500+ siblings ends. The LXC Coin cannot be mined, it runs mainly on its own dedicated transaction confirmation node network to

secure and protect it, and starts out “fully mined” with all coins owned by the issuing company. Coins will only be released into

circulations in exchange for cash or instantly cashable assets, securing the coin base value. It will increase in base asset value by

roughly 15% annually, making it a value-coin in more than one way. The 15% increase comes from the average profit from the P2P

investment pools the base asset funds are invested in, which has a history of around 15% yearly profits

© LXC Coin™ 2014

9

BEYOND THE COIN

Having our own crypto currency exchange

gives a range of advantages and creates a

lot of opportunities. Securing a fast, safe

and efficient trading floor for our coins,

and giving customers great rates and fees.

A liquid exchange with low fees will also

be instrumental in utilizing the safe crypto

currency for P2P lending, which we aim to

launch once the main structure is in place.

For effectively controlling the price range,

a cryptocoin exchange we control can be

also become an invaluable asset.

LXC Coin is planned with a

dual support – a cryptocoin

exchange creating liquidity for

the coin on one side, and a P2P

Exchange creating liquidity in

the assets the LXC Coins

represent on the other

There are already P2P exchanges active

today, but these are constructed by or for

single key P2P platforms. They have high

activity, and improve the P2P product

dramatically for both the company and the

P2P lending investors. In addition to being

a great business area, it is expected to

become an important tool for maintaining

a steady flow of P2P loan engagements,

and quickly converting LXC Coin funds to

cash if necessary. Currently in discussions

with an initial test customer from the world

of P2P, we hope to become the first multi-

P2P platform in the world.

© LXC Coin™ 2014

Crypto Currency Exchange P2P Loan Exchange

-creates liquidity for the LXC coins -creates liquidity for the LXC assets

Stabile Crypto Currency

-a solid investment, anda great transaction tool

10

LXC COIN: WHAT CAN IT BE USED FOR?

P2P EQT (c) 2014

We expect the second-generation cryptocoins to become the backbone of

merchant business in crypto currencies. The reason for this is simple;

second-generation crypto currencies take out all the cryptocoin risks;

including the obvious volatility and liquidity issues, but also removing fears

of future bans, fraud, restrictions, lack of transparency or accountability,

and risk of “federal-agency-seized” coins being dumped destroying the prices

P2P EQT (c) 2014

Obviously, the LXC Coin can be used for investments and savings. But what about other

uses – such as those currently filled by first-generation cryptocoins? As many first-

generation coins have well developed mainstream usage-constructions, being accepted

as legal tender by giants such as Amazon.com and ebay.com and being accessible

through ATM systems, the framework for implementing any crypto currency into these

systems are open and easily accessible, should the need arise. There is already a

selection of payment gateways catering for first generation coins; connecting cryptocoins

with fiat money and

merchant transactions,

that our coin could

link up to. But with

second-generation

cryptocoins, a lot of

extra opportunities

opens to merchants,

banks, payment gate-

ways and on-line

businesses, and this may become a serious leverage in the payment industry , especially

but not exclusively within the field of micropayments. It also solves the present needs for

business-users of cryptocoins to either continuously exchanging payments for fiat money

or running the volatility risk of having first-generation cryptocoins in stock, awaiting the

next sharp decline in value. As such, we hope the LXC Coin will be used in every way the

Bitcoin and other popular coins are used today.

© LXC Coin™ 2014

11

“A cryptocoin which is stabile is a key to solving the micropayment puzzle.

With no currency volatility risk, and close to zero-cost of transactions, micro

payments can be done virtually free of charge and with maximum security.

We are certain that there’s going to be a lot of top-level industry players

investigating this sector once stabile cryptocoins become mainstream.”

Ragnvald Hoel, CFO, LXCCoin LTD

© LXC Coin™ 2014

12

LXCCOIN LTD MANAGEMENT – OVERVIEW

The management team in LXCCoin Ltd is set up to cover four different areas, with two

specialists in each area, shortening decision time and increasing decision quality. For a

complete overview, please see the separate document on Management

Crypto team

Our technical team consists of a

cryptocoin- and IT-security expert and a

systems architecture specialist, coupled

with an external dev-team with a solid

track record. The team has, amongst

other things, created online stock

exchanges & payment gateway solutions

Management

The management team is the active

core of the company, with full day-to-

day focus on LXCCoin, consisting of

two people from the financial team and

one member from the crypto team. The

team is expected to be increased from

two to five over the forthcoming months

Financial team

The team has four financial specialists; two in the

management team, with backgrounds mostly coming from the

world of corporate finance, and two external parties well

known for creating successfull startups, and a track record of

bringing several companies from seed financing stages to

flotation on international stock excanges

P2P EQT (c) 2014© LXC Coin™ 2014

Legal team

Our team includes two legal advisors, of which one – our

chairman, Allan Nielsen– is a former division leader in the

Danish Financial Authority, and the other – Erik Gravgaard –

has a wide spanning track record from top positions in the

Danish IT/ internet industry, also specializing in tax and

financial law

13

LXC COIN: THE TEAM (CONTINUED)

Allan Nielsen (MSc Law)

Allan Nielsen (Chairman - MSc Law) is the former FCA chief

deputy director in Denmark, and few people have been

instrumental in the close of more risk-exposed banks than him.

Having literally written the book on modern compliance, he is an

expert in banking compliance and financial law. Since starting his

own legal consulting company in 2012, he has taken a keen

interest in financial invention, studying P2P, crowdfunding and

crowd equity funding throughout Europe, publishing a major

report on the subject in August 2014. He is currently also

employed as “of counsel” with award winning Magnusson Law,

one of the best law-firms in the Scandinavian/ Baltic region. He

serves on several boards of directors, and is the key connection

between LXCCoin LTD and the financial authorities. He has

been a major part of the LXCCoin Ltd management since the

team’s original foundation in Denmark in 2013

Erik Gravgaard (MSc Law)

Erik Gravgaard (co-founder, MSc Law) is CEO at Juristhuset

lawfirm and “of counsel” with Magnusson Law, specializing in

corporate and commercial law, Internet law, contracts and

negotiations. He has previously worked in the Danish taxation

authority, has been the CEO of Telepartner A/S (later listed on

NASDAQ in the US) and on the board of 360 Holding AB (listed

on NASDAQ First North) which later became P2P lender

TrustBuddy. He has also been president of the Danish Internet

Industry Organisation, board member of the Danish Internet

Forum, active with the central Danish Internet DNS Registrar

“DK Hostmaster”, and member of SME-Committee of “Danish

Industry”. He has a solid track record within financial inventions,

having been an early adopter of several technologies ranging

from IT solutions through financial hybrids such as the NASDAQ

FN listed Finansbet, and a row of online gaming ventures

P2P EQT (c) 2014© LXC Coin™ 2014

14

LXC COIN: THE TEAM (CONTINUED)

Henrik Ellefsen

(Founder & CEO)

Henrik Ellefsen has been a successful internet entrepreneur

since the mid-1990s, founding the Aker Securities online broker

house (the first real-time online broker house in Norway), an

OTC Stock Exchange which was the first of its kind in

Scandinavia (NorexOTC.com), the environmental processing

company EnPro (later listed at OsloOTC), and a range of other

ventures. Apart from a disastrous transaction in 2003, selling a

trading license to what turned out to be a pyramid scheme

(getting him into all sorts of trouble including a conviction and a

large fine in Norway), he has been instrumental in successful

start-ups and the listing several companies on stock exchanges

and OTC-lists, and his entrepreneur track record includes diverse

ventures like Aker Securities, AMT, A-Viral (OsloOTC), BeWell,

EnPro (OsloOTC) and Xelicity (an online lending project where

two of the group executives moved on to founding TrustBuddy).

The original idea behind LXCCoin was derived following a P2P

funding discussion between Henrik and the CEO of TrustBuddy

Ragnvald “Rags” Hoel

(CFO & fund trader)

During the early 1990s “Rags” was a Financial Information

Systems Executive with a Fortune500 Company, heading banks,

treasuries and commodities. During Deregulation of the Power

Industry, Rags coordinated the first Information system launched

and used today for trading spot electricity. Rags went on to

brokering & trading becoming a Chief Dealer of Derivatives

before CFO of Stocks, Commodities and FX Brokerage. Rags

was part of the first team at the online broker house Aker

Securities alongside LXCCoin’s CEO. A former board member of

the technical analysis foundation in Norway, he has published

news bulletins for two broker houses and as a standalone

venture, before a decade of oil & FX trading, with side interests in

financing and managing start-ups as an ad-hoc CFO. He joined

the LXCCoin team in early 2014, as a part of the relocation to the

UK, and will alongside his work in LXCCoin continue his trading

efforts in the LXC Share/Coin, on behalf of the company and its

shareholders

© LXC Coin™ 2014

15

LXC COIN: THE TEAM (CONTINUED)

Thomas Wong

(IT security- & crypto expert)

Thomas Wong is the father of the LXC Coin code adaptation. He

is a top certified security expert, certified in most current security

standards including is a former Fort Consult white-tie hacker and

security specialist, having written top-priority classified reports for

Scandinavian Ministries of Finance and other government

agencies, lectured in online security, and having been a reference

for the media in relation to web security questions. He is certified

in most top-level on-line security standards, including the latest

ISO certification. Having been a cryptocoin miner since 2009, he

has extensive experience with cryptocoins and cryptocoin code

since their infancy, having co-created several coding projects

before joining the LXCCoin team. Thomas has a full-time position

with an internet tech company, and works with LXCCoin on project

as an advisor, board member and key shareholder.

Wilhelm Castberg

(IT specialist)

Wilhelm is an IT guru with extensive track records within online

security and trading systems. The former Norwegian CTO in

one of the largest IT-companies in Scandinavia, Wilhelm

started out as a system integrator in the 1990s before being

hired by the current LXCCoin CEO to construct the first real-

time online trading system in Norway. Having successfully

completed the system, Wilhelm moved on to creating the most

advanced online trading and funds platform in Norway ever, for

the Fund Manager ACTA (with platform investments of more

than £40 million). He is currently Client Director Manager in

ATEA, an IT company listed on the Oslo Stock Exchange, and

is a part of the LXC team only as an advisor and board

member, following early efforts on software and IT solutions.

P2P EQT (c) 2014© LXC Coin™ 2014

16

LXC COIN: THE TEAM (CONTINUED)

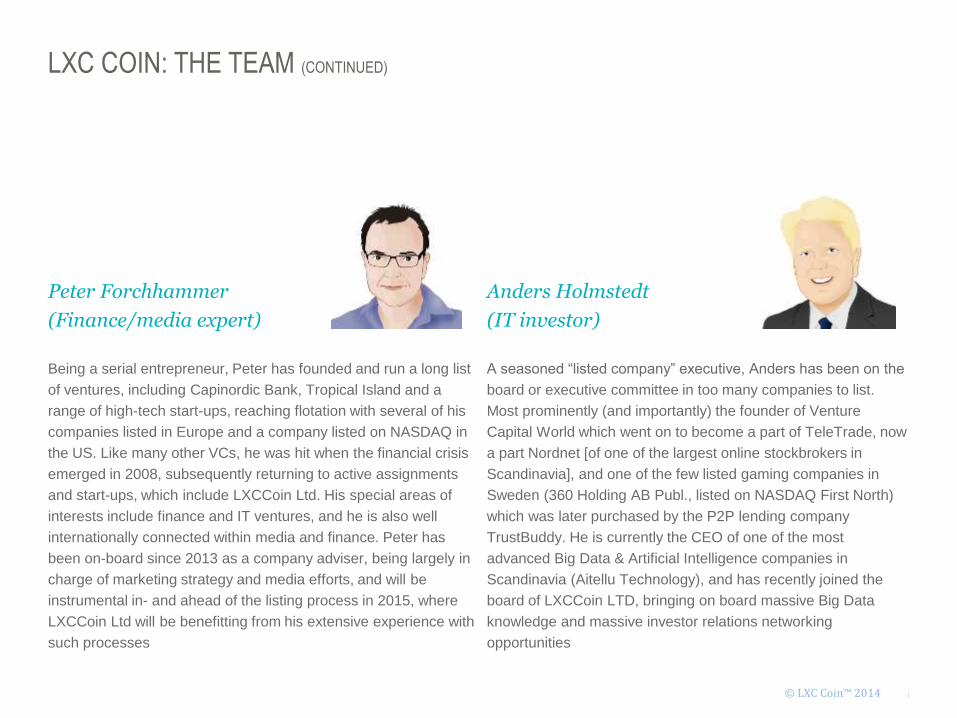

Peter Forchhammer

(Finance/media expert)

Being a serial entrepreneur, Peter has founded and run a long list

of ventures, including Capinordic Bank, Tropical Island and a

range of high-tech start-ups, reaching flotation with several of his

companies listed in Europe and a company listed on NASDAQ in

the US. Like many other VCs, he was hit when the financial crisis

emerged in 2008, subsequently returning to active assignments

and start-ups, which include LXCCoin Ltd. His special areas of

interests include finance and IT ventures, and he is also well

internationally connected within media and finance. Peter has

been on-board since 2013 as a company adviser, being largely in

charge of marketing strategy and media efforts, and will be

instrumental in- and ahead of the listing process in 2015, where

LXCCoin Ltd will be benefitting from his extensive experience with

such processes

Anders Holmstedt

(IT investor)

A seasoned “listed company” executive, Anders has been on the

board or executive committee in too many companies to list.

Most prominently (and importantly) the founder of Venture

Capital World which went on to become a part of TeleTrade, now

a part Nordnet [of one of the largest online stockbrokers in

Scandinavia], and one of the few listed gaming companies in

Sweden (360 Holding AB Publ., listed on NASDAQ First North)

which was later purchased by the P2P lending company

TrustBuddy. He is currently the CEO of one of the most

advanced Big Data & Artificial Intelligence companies in

Scandinavia (Aitellu Technology), and has recently joined the

board of LXCCoin LTD, bringing on board massive Big Data

knowledge and massive investor relations networking

opportunities

P2P EQT (c) 2014© LXC Coin™ 2014

17

LXC COIN: THE TEAM (CONTINUED)

Focus on running costs

LXCCoin has focused on the lowest

possible running costs, protecting the

company from resource draining and

keeping management highly motivated

to perform well over time – only getting

rewarded if the company value ends

up as being high and with a viable exit

strategy. Therefore, the company has

a low spending budget, and a high

percent of shareholders have active

roles in the company. We feel that this

Is a fortunate situation, giving the

maximizing shared goals with a

minimum burn-rate and low spending

of investor funds on personnel

Rigged for utilizing powerful management resource qualities at the lowest possible running

cost, all non-exec directors in LXCCoin Ltd is in on a share-driven no-cure, no-pay basis,

keeping the burn-rate to the absolute minimum

Focus on powerful management resources

Built over a span of 18 months, the founder has had ample time to hand-pick the

necessary resources. Targeting an FCA license in a suitable European country, a

listing, one or two cyberspace exchanges and a banking hybrid, this called for legal

aides, stock-/derivatives/asset-traders, IT/Cloud Computing advisers and a top-of-the-

line security expertise. Obviously, cryptocoins had to be covered by an in-house

expert, and media and strategic decisions needed to be catered for. Since the team

was formed (in three phases), the activity has been intense, taking a final run of 6

months from the team completion to the point where the company wanted to form itself

and surface (spring of 2014). The decision to launch in England and to crowd-equity

fund on Crowd for Angels was the final part of the road towards launch, aimed at

taking place in the fourth quarter of 2014 with the launch of the first product (the LXC

Coin)

The targeted listing process is expected to take 6-12 months from its initiation, and

with 7 of our 8 executives having previous listing experience, this should be a

manageable operation

P2P EQT (c) 2014© LXC Coin™ 2014

18

THE LXCCOIN LTD PROFIT MODEL

Company revenue derives from the following:

o Most LXC Coin investments give a 5% bounty to the LXCCoin company. With coins worth more than 1.1 billion Euro

and rising in value, this accounts for a minimum of around £50 million over a number of years

o Through the LXC Coin trading operations, and the “hybrid central bank” trading efforts, LXCCoin will have a few

additional percent of profits on the yearly turnover of internal LXCs, estimated to give the company an income of £20-

30,000 in the initial phases, rising to several million pounds of yearly activities, target of £10-15m per year fully issued

o With 15% base asset value increase per year, the coin will pay a 1% p.a. commission and 20% of all earnings above

10%, the commissions should amount to around 2% per year on issued LXC Coin BAV. Initially marginal at around

£15-20,000 per year, this will become a massive earnings area with full issue, at more than £20 million per year

o The P2P Exchange is initially a mere necessity for the prevention of “running out of P2P investment targets”, but

should in addition to providing flow, investments and easy exits in the event of needing repurchase-cash quickly,

improve the LXCCoin Ltd margins slightly, both in company revenue and in LXC Coin profitability. It is expected to

add between £100-200,000 in yearly profits for LXCCoin Ltd when fully operational

o The Cryptocoin Exchange will from the LXC trading alone give the company savings of 1% of all LXC trading, in itself

making the exchange a profitable operation. With solid volumes of LXC, near-zero risk of fraud and serious owners,

the exchange may also become a great source of income of trading with other cryptocoins, further increasing the

potential earnings. Once other asset class catch on to the potential of using cryptocoins as an extra layer on their

investment, the Cryptocoin Exchange can in reality become a “stock” exchange for companies and assets alike

o The earnings in the company are highly dependent of the success of the LXC Coin, where a successful coin in full

issue with a BAV of €2-2.5 and a price of €4-6 will give a £50m+ revenue every year for the LXCCoin company, plus

commissions of £20m over a number of years, making it a real cash machine if successful

o With the LXC Coin rising in value more than the BAV, the company will own an implicit increased value in the coins

that are kept in “cold storage”. With 1.1 billion coins, every 10% increase in the premium on coins the vault value will

rise by roughly £ 100 million, thus actually being the major value factor in the company

© LXC Coin™ 2014

19

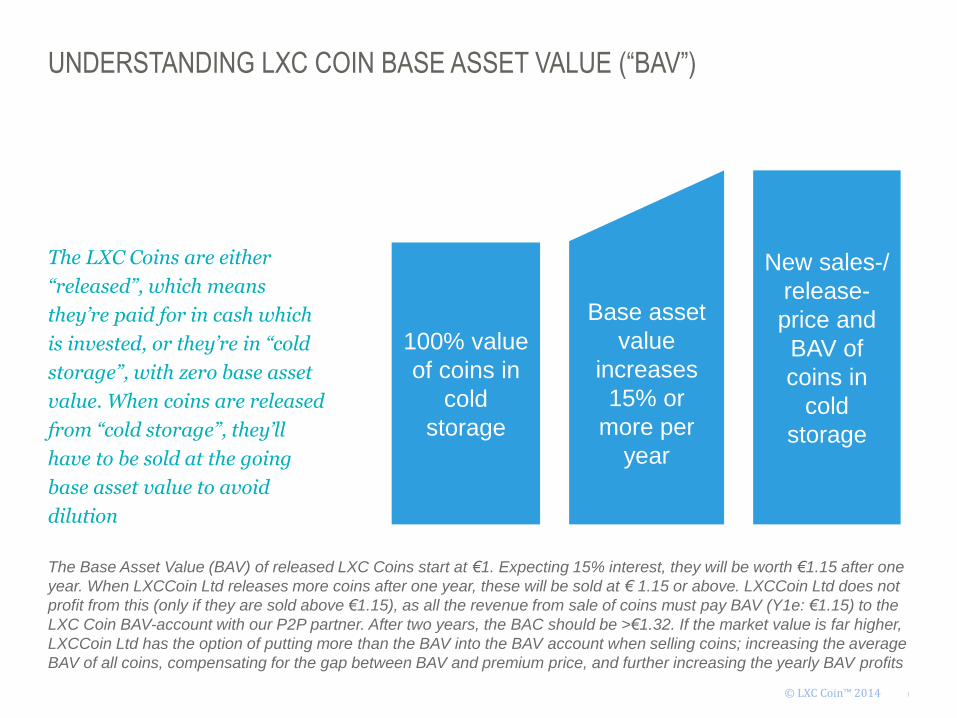

UNDERSTANDING LXC COIN BASE ASSET VALUE (“BAV”)

The LXC Coins are either

“released”, which means

they’re paid for in cash which

is invested, or they’re in “cold

storage”, with zero base asset

value. When coins are released

from “cold storage”, they’ll

have to be sold at the going

base asset value to avoid

dilution

100% value

of coins in

cold

storage

Base asset

value

increases

15% or

more per

year

New sales-/

release-

price and

BAV of

coins in

cold

storage

The Base Asset Value (BAV) of released LXC Coins start at €1. Expecting 15% interest, they will be worth €1.15 after one

year. When LXCCoin Ltd releases more coins after one year, these will be sold at € 1.15 or above. LXCCoin Ltd does not

profit from this (only if they are sold above €1.15), as all the revenue from sale of coins must pay BAV (Y1e: €1.15) to the

LXC Coin BAV-account with our P2P partner. After two years, the BAC should be >€1.32. If the market value is far higher,

LXCCoin Ltd has the option of putting more than the BAV into the BAV account when selling coins; increasing the average

BAV of all coins, compensating for the gap between BAV and premium price, and further increasing the yearly BAV profits

© LXC Coin™ 2014

20

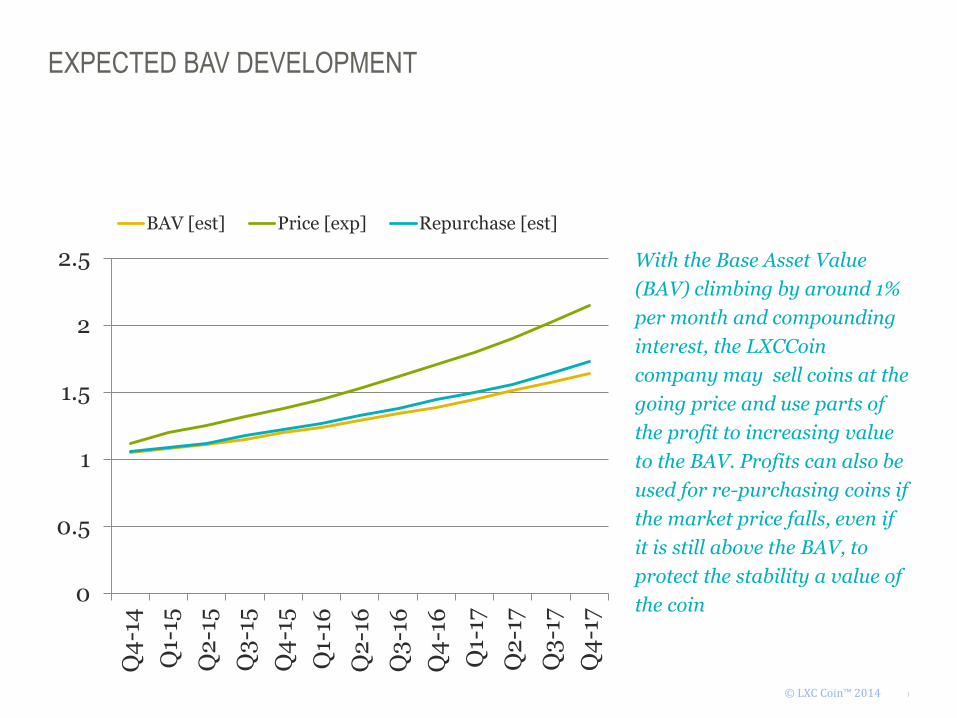

EXPECTED BAV DEVELOPMENT

0

0.5

1

1.5

2

2.5

Q4

-14

Q1-

15

Q2

-15

Q3

-15

Q4

-15

Q1-

16

Q2

-16

Q3

-16

Q4

-16

Q1-

17

Q2

-17

Q3

-17

Q4

-17

BAV [est] Price [exp] Repurchase [est]

With the Base Asset Value

(BAV) climbing by around 1%

per month and compounding

interest, the LXCCoin

company may sell coins at the

going price and use parts of

the profit to increasing value

to the BAV. Profits can also be

used for re-purchasing coins if

the market price falls, even if

it is still above the BAV, to

protect the stability a value of

the coin

© LXC Coin™ 2014

21

ANTICIPATED PREMIUM RANGE

With our base-case scenario, the

LXC Coin should double its BAV

base asset value in a few years

The intrinsic value should secure

that it trades higher, regulated

by supply/demand, usage and

merchant acceptance

As projected here, the coin should be trading

at a premium of 1.5/2 times the actual base

value after a few years, which is in the

extreme-low range in terms of cryptocoins –

there is however no guaranteed premium,

and apart from the BAV price increase

making the minimum performance on the

coin, premium performance will be

depending on supply and demand, other

uses of coins, and external factors

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

2014 2015 2016 2017 2018

BAV (est) Price (exp)

P2P EQT (c) 2014© LXC Coin™ 2014

22

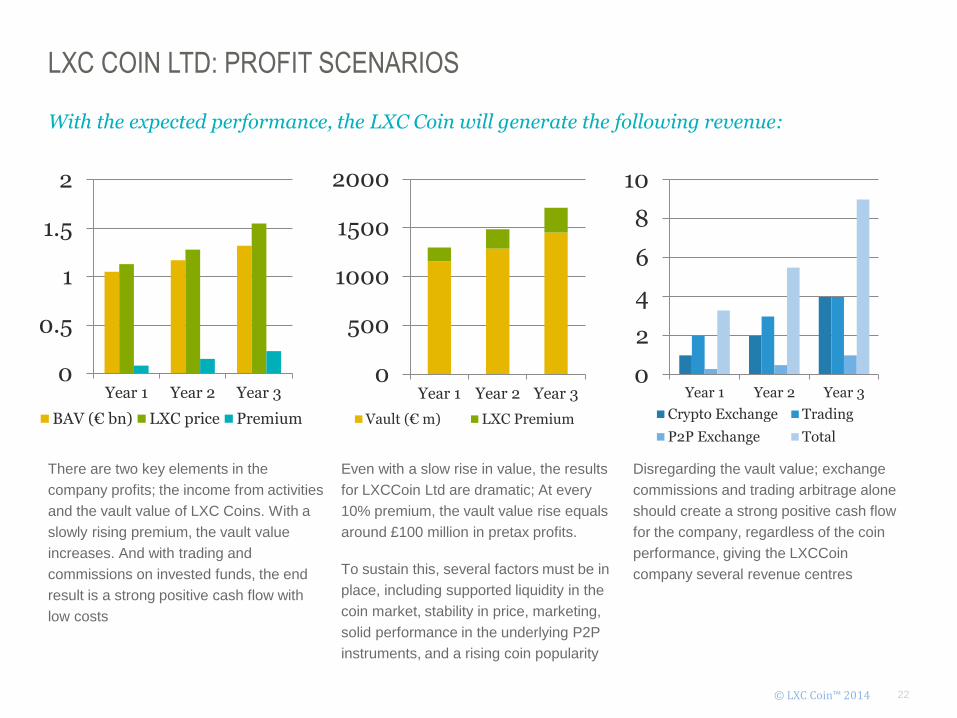

LXC COIN LTD: PROFIT SCENARIOS

0

0.5

1

1.5

2

Year 1 Year 2 Year 3

BAV (€ bn) LXC price Premium

With the expected performance, the LXC Coin will generate the following revenue:

0

500

1000

1500

2000

Year 1 Year 2 Year 3

Vault (€ m) LXC Premium

0

2

4

6

8

10

Year 1 Year 2 Year 3

Crypto Exchange Trading

P2P Exchange Total

There are two key elements in the

company profits; the income from activities

and the vault value of LXC Coins. With a

slowly rising premium, the vault value

increases. And with trading and

commissions on invested funds, the end

result is a strong positive cash flow with

low costs

Even with a slow rise in value, the results

for LXCCoin Ltd are dramatic; At every

10% premium, the vault value rise equals

around £100 million in pretax profits.

To sustain this, several factors must be in

place, including supported liquidity in the

coin market, stability in price, marketing,

solid performance in the underlying P2P

instruments, and a rising coin popularity

Disregarding the vault value; exchange

commissions and trading arbitrage alone

should create a strong positive cash flow

for the company, regardless of the coin

performance, giving the LXCCoin

company several revenue centres

© LXC Coin™ 2014

23

LXC COIN LTD: PROFIT SCENARIOS (CONTINUED)

00.5

11.5

22.5

3 m coins 6 m coins 10 m coins

Commissions Trading

CryptoExc' P2PExc'

Total

Here are three profit scenarios of the running business, based on 10/50/100 million coins sold

0

5

10

Y1: 10mcoins

Y2: 25mcoins

Y3: 50mcoins

Commissions Trading

CryptoExc' P2PExc'

Total

0

5

10

15

Y1: 20mcoins

Y2: 50mcoins

Y3: 100mcoins

Commissions Trading

CryptoExc' P2PExc'

Total

Profits from low sales of coins, low activity

on the exchanges and little trading, mean

the company will make between € 0.4 m

and € 2 m in its first business years –

ignoring the vault value increase. Despite

being a low and unlikely scenario, the

company is still profitable

With a small but rising interest in the

coins, the company is set for a turnover

from €2-5 m, making solid profits, again

without including any vault value increase

At a 10% issued rate of coins, reaching

100m coins in circulation over a three year

duration, internal revenue from activities

should reach £10 million in year 3

The exchanges are constructed to be independent of the success of the coin, and should have success on their own regardless of the coin performance

© LXC Coin™ 2014

24

“To summarize all the opportunities the company has in financial terms

would be somewhat pointless, as the all-important LXC Coin vault value

completely overshadows everything else. Leaving that out of the figures, the

study of numbers become easier and more understandable. A target turnover

of between £2-5 million, with anticipated margins of more than 50%, the

company should be able to get a solid pricing once operational, and

everything else we’re doing will boost the valuation even further.”

Ragnvald “Rags” Hoel, CFO, LXCCoin LTD

© LXC Coin™ 2014

25

LXC COIN: THE PLATFORM

The P2P software platform

can be used for everything

from P2P Exchange functions

to small-business loans, to

offering finance solutions such

as leasing or factoring.

Depending on the range of

partners, LXCCoin Ltd may

enter all booming segments of

P2P, but will start slowly with

pilot projects with strict

control, to create a secure base

for its investors

The LXCCoin software platform is a fully

functional stand-alone software, based on

three main components;

* The Cryptocoin Code

* Our own Exchange software

* Tailored version of Zidisha open-source-

P2P platform for microloans

Our platform covers the coin and the

exchanges, but also contains accounting,

payment transaction systems, ID-control,

registration and verifications, and all other

necessary aspects of P2P finance for

future use. Using the cryptocoin and

exchanges or payment gateways as the

backbone, a well of new features or

products can be created for future use,

which will be once the technology/security

is fully proven and the LXC Coins gain

momentum.

The LXCCoin P2P-platform has to be set

up in complete installations for each new

business segment the company ventures

into, and it is therefore a feasible solution

to go into a few joint ventures instead of

launching our own P2P service which can

not be 100% automated.

The platform is based 100% in the cloud,

in a distributed solution securing 24/7

operations and the lowes cost available.

The platform is open to integration with

most APIs, and is therefore spec’ed for

use in all markets within all target areas

the comany aims to become active in

P2P EQT (c) 2014© LXC Coin™ 2014

26

LXC COIN: PLATFORM OVERVIEW The LXC Coin software platform is based

on our own proprietary systems, with

several extensions for funds, exchange

functionality and cryptocoin asset

management, and external APIs

LXCCoin Ltd proprietary platform

CoinNext CryptoExchange platform

LXCCoin Ltd Platform

-built by LiteBreeze/LXCCoin dev.

P2P Exchange Platform

Crypto Exchange module

API towards P2P Lenders

Bitcoin open source code

Blackcoin open source code

LXC Cryptocoin Platform

-built by LXCCoin dev.

Cryptocoin platform(Coin, block explorer, crawlers etc.)

Crytptocoin

Asset Fund

© LXC Coin™ 2014

27

LXC COIN: INTELLECTUAL PROPERTY RIGHTS

LXCCoin Ltd owns software,

web domains, graphics,

multimedia, trademarks and

licenses. These could be

considered as white-label

opportunities, but we’re more

focused on the use of our own

technology and its

security/protection than of

licensing it to third parties

As a valuation element it has

been summarized here briefly,

but we advise investors to

ignore any high intrinsic value

these may have

Trademarks:

2 different USPTO U.S. Trademark

Applications, assigned serial numbers

86340927 and 86340919, relating to

the name “LXC Coin” and the modified

“£” logo used on the LXC Coin.

Software platform:

The LXC Coin code is based on open

source, and we’ve put our version of

the code up as open source as well in

respect of the open source work done

in all crypto currencies

The P2P Exchange is developed in-

house, and is a fully owned code under

our own license- Our Crypto Exchange

is a partly purchased- and partly

customized software

Our platform also utilizes other open

source systems to a lesser degree

Web domains:

LXCCoin.com

LXCCoins.com

P2PLoan.exchange

Cryp2p.com

P2PUs.com

P2PYou.com

P2PBee.com

P2Bee.com

P2PEqt.com

Graphics:

LXCCoin coin graphics

Website graphics

Movie “Meet the LXC Coin”

Movie “Crowd Equity funding LXC”

Modified currency label “£” with the line

extended from top and bottom of the

symbol, not crossing it

P2P EQT (c) 2014© LXC Coin™ 2014

28

LXCCOIN LTD: ROADMAP

The roadmap for LXCCoin and the P2P Exchange is to start up with the “safe” crypto currency,

its own exchange and later the P2P Exchange, before optioning to moving on to becoming a

broad P2P Fund company based on cryptocoin investments and/or regular fund investments

P2P EQT (c) 2014© LXC Coin™ 2014

Business plan development

2013 2014 2015

Legal framework(s)

Software development

New derivatives

Funding

Cryptocoin launch

Crypto Exchange launch

Software updating

Listing

P2P Exchange launch

Platform design

Compliance updating

29

2013 2014 2015

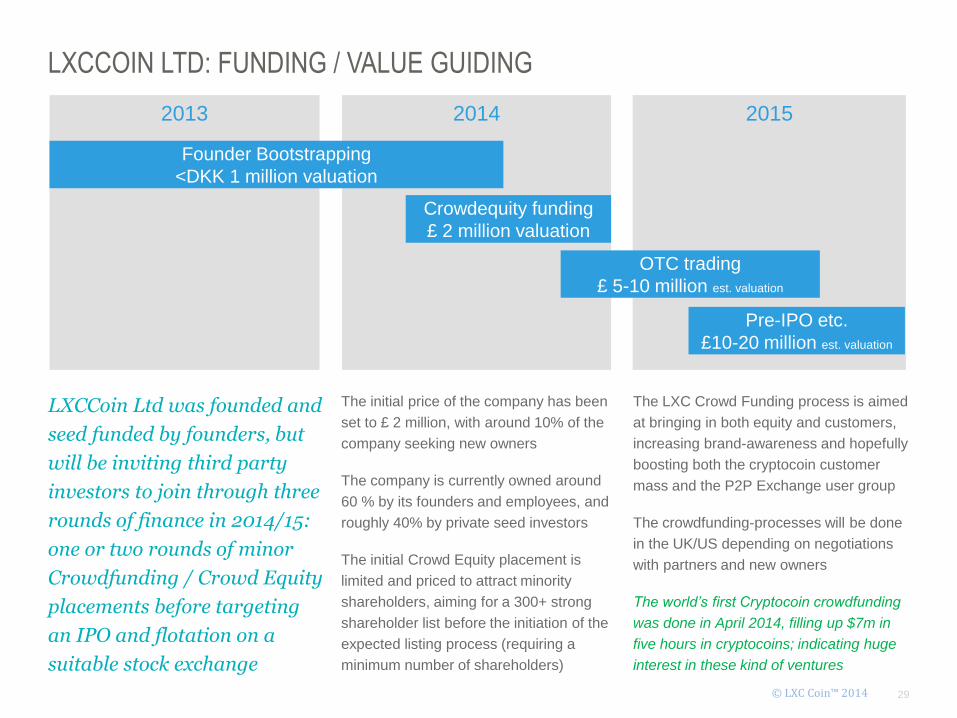

LXCCOIN LTD: FUNDING / VALUE GUIDING

LXCCoin Ltd was founded and

seed funded by founders, but

will be inviting third party

investors to join through three

rounds of finance in 2014/15:

one or two rounds of minor

Crowdfunding / Crowd Equity

placements before targeting

an IPO and flotation on a

suitable stock exchange

The initial price of the company has been

set to £ 2 million, with around 10% of the

company seeking new owners

The company is currently owned around

60 % by its founders and employees, and

roughly 40% by private seed investors

The initial Crowd Equity placement is

limited and priced to attract minority

shareholders, aiming for a 300+ strong

shareholder list before the initiation of the

expected listing process (requiring a

minimum number of shareholders)

The LXC Crowd Funding process is aimed

at bringing in both equity and customers,

increasing brand-awareness and hopefully

boosting both the cryptocoin customer

mass and the P2P Exchange user group

The crowdfunding-processes will be done

in the UK/US depending on negotiations

with partners and new owners

The world’s first Cryptocoin crowdfunding

was done in April 2014, filling up $7m in

five hours in cryptocoins; indicating huge

interest in these kind of ventures

P2P EQT (c) 2014

Founder Bootstrapping

<DKK 1 million valuation

Crowdequity funding

£ 2 million valuation

Pre-IPO etc.

£10-20 million est. valuation

© LXC Coin™ 2014

OTC trading

£ 5-10 million est. valuation

30

SUMMARY

The team

We’re a tight-knit team

of seven experienced

executives and lawyers,

covering all the needed

bases and technologies

involved. We have put

our own money into this

and are determined to

succeed.

We’re in a continuous

dialogue with the

financial authorities, to

make sure our setup is

in compliance with all

legal regulations and

forthcoming laws, with

an ex-financial authority

executive in charge of

the process on our side.

LXCCoin Ltd is a Crypto/P2P conglomerate, aimed at optimizing and evolving cryptocoins,

changing how P2P Lenders are funded, and empowering the massive cryptocoin potential

P2P EQT (c) 2014

Financing

The foundation and

development have been

financed by the team,

and there will be two or

three rounds of further

financing in 2014/15.

Financing includes at

least one round of

crowd-equity funding (in

preparation for an IPO),

aiming at making the

brand and products

marketed towards a

broader audience, and a

crowdfunding sale of

cryptocoins as an early

marketing effort

© LXC Coin™ 2014

SW/Platform

Our software platform is

built by LiteBreeze on

the backbone of several

proven components, as

a proprietary stand-

alone financial platform.

It covers the cryptocoin

services, the fund model

and the exchange

setups, targeting the

P2P lender APIs on one

side and our own

Cryptocoin asset

management system(s)

on the other, working as

a dual transaction

platform and a fund

management platform,

with multiple extension

opportunities

The cryptocoin

Our LXC cryptocoin

(Lending eXchange

Currency coin) is a dual

financial bridge, linking

cryptocoins with real

asset values and giving

cryptocoins a real

profitability. It is also

linking P2P lending

investments to the huge

resources of cryptocoins

and creating a whole

new paradigm for

borderless financial

derivatives. It is a fully

secure coin, based on

the Bitcoin/Blackcoin

fork, with altered mining

functionality and other

customizations

Partners

We have initially chosen

P2P lenders with long

track records and solid

profits, to secure a safe

allocation of LXC funds,

aiming to provide a solid

funding muscle for some

proven and well-known

companies from the

start, and to support the

clear overall impression

of the sincerity and

solidity our company.

We are also in

discussions with other

P2Ps, and important

partners should help to

assure that the cash put

into our products are in

safe hands

31

RISK FACTORS

Risks related to the success of the company range from performance to worldwide legal changes for cryptocoins – investors should inform themselves thoroughly about risks prior to investing. Here are a few, which the company considers the key risk factors:

o Legislation – new or altered legislation may prevent the business from developing or may prohibit the business entirely – this may effect some or all crypto currencies (the Russian Duma is expected to ban the use of virtual currencies shortly, claiming they have no underlying value)

o Partner problems – we are somewhat dependent on our P2P investment partners performing well for our coin to be attractive over time – and even though we target to diversify our portfolios and leverage this risk, we are dependent on our partners to a certain extent

o Competition –other second generation cryptocoin contenders may enter the market with competing products, with better profitability, or faster than our product

o Technology – with the technological development it is difficult to project whether our solutions are current also for a distant future with technologys not presently forseen or anticipated

o Management dependence – like most companies, LXCCoin Ltd is somewhat dependent on its management team, and despite having shares and options, there is a risk involved in the team resources and losing one or more of the team members

o Security – despite the best efforts of the company, there are risks involved with both the crypto currency and the exchanges

o Financial underperformance –in case our business underperforms, the company may run at a loss and require new capital, which may not be readily available at the time and level the company desires/needs

© LXC Coin™ 2014

32

LXC COINCRYPTOCURRENCY

+ The Code

+ Security (On-line/Off-line)

+ The proprietary network

+ The slow-rise paradigm

+ Launch strategy

+ Legality

+ Welcoming regulation

01© LXC Coin™ 2014

33

“Cryptocoins want to take over for regular currencies, but until now they’ve

failed to provide exactly what makes the world trust and depend on existing

currencies. I’m not referring to the governments guaranteeing them, because

we’ve seen that fail numerous times – I’m talking about stability,

exchangeability, dependability, and a guarantee for future use. When crypto

currencies can tick those boxes, they are ready to take on the world. Until

they can do that, or they have a few guiding ones that can [which the others

can exchange into], they will continue to be a curiosity – a footnote in the

history of currencies. But when they make that move, there will be no

stopping them.”

Henrik Ellefsen, CEO/Founder, LXCCoin

© LXC Coin™ 2014

34

LXC COIN: THE CODE

The LXC Coin code is based on Bitcoin and Blackcoin – coins with high activity

and near-immediate error correction. These have never compromised or broken,

are thoroughly proven and are considered completely stabile and secure.

To make the LXC Coin the non-volatile currency we wanted, our design had to

sacrifice mine’ability and bounties that other crypto currencies use to gain quick

popularity. We also had to re-think the way transactions was being done, and

how to charge fees from the transactions that were being done. We wanted to

maintain speed, targeting >10 second worldwide transaction times, and

maintaining a minute dilution for the coin owners through transaction fees

instead of mining. Following our coding and adaptations, we’ve run a six month

testing program, creating and test-mining the coin before transaction-testing it

thoroughly. Then, a new genesis block was created, and the coin fully mined and

locked in “cold storage”.

The result has been a modernized Bitcoin-Blackcoin hybrid, on a network of fully

controlled transaction nodes and through private wallets using “staking”

functionality, giving the wallet owners transaction fee participation without

requiring/consuming the vast resources of most other coins.

© LXC Coin™ 2014

A cryptocurrency can be created in hours using the open source code available; instead, our team has spent a full year, making way for a better product and not just another carbon copy

35

LXC COIN: ON-LINE SECURITY

Implementing the highest level of security available – and then some

To avoid the notorious ”51% attack”, where intruders control more than 50% of the network calculation power and thereby

can manipulate all transactions, our coin is based on ”Proof-of-Stake” which relates to coins and not to power, implicating

owning more than 50% of the coins to manipulate it (minimum €550 million worth of coins), and even then it is unproven

and highly debated whether or not such an attack would be successful

Our code is rife with checkpoints, aimed at preventing any attempt at a ”blockchain roll-back”.

Our sites will randomly be run through the safety checks ordinated by PCI and SANS (http://www.sans.org/ and

https://www.pcisecuritystandards.org ). Our crypto team carries both certifications, including GWAP and GPEN

Our proprietary node network has restricted access an maximum security precautions, and are not password-based.

We’re using a customized version of the NSD harding of Linux, outlined here:

http://www.nsa.gov/ia/mitigation_guidance/security_configuration_guides/operating_systems.shtml#linux2

Within the expected listing of the company, we aim to certify under the ISO27001, yet another standard to which our team

is certified

© LXC Coin™ 2014

36

LXC COIN: OFF-LINE SECURITY

Most other coins are mined and are therefore slowly rising in numbers under

continuous distribution – ours is the complete opposite. As we’ve mined all of the

coins ourselves, the risk of fraud and mishaps can only be deemed as highly

important to contain. Which is why the coins are divided into 100 wallets (large

ones), which are all listed online and kept track of. The wallets are stored offline,

on multiple sets of encrypted hard-drives, encrypted UBS and written media, all

securely stored. The codes have been produced in attendance of our legal team,

and have all been split for separate safekeeping. With two safety deposit boxes

and two lawyer vaults, any intruder would have to procure documents and hard

drives from several different places and know several of our internally kept

encryption passphrases, which would be close to impossible to do undetected.

To add an extra layer of difficulty, the offline stored USBs are purposely

mismatched so intruders would for practical purposes require all discs and

encrypted media just to get the hacking process started – making the task of

intrusion outright impossible. In addition to this, there are other undisclosed

safety measures in place, further increasing security

© LXC Coin™ 2014

With 1.1 billion coins, security is paramount

37

LXC COIN: THE NETWORK

P2P EQT (c) 2014

To protect our own network, guaranteeing transaction security and maintaining a 100% uptime, we’ve created a node network handling 50% of our transaction traffic

One of the most destructive sides of cryptocoins that are rarely addressed, is the energy consumption many cryptocoins have. Bitcoin

in particular, is hugely energy consuming. To give an example: KnC, the Bitcoin mining company based in Stockholm, has energy

bills related to its Bitcoin mining of more than $ 500,000.00 per month. Yes, month. And this is only one of hundreds of mining

companies and mining pools “mining” Bitcoins. There are many coins, our LXC Coin included, that run on different algorithms, which

restrict the difficulty in transaction confirmation to a bare minimum. To continuously decrease the creation of new blocks of coins, the

algorithms used in mining are increasingly raising the difficulty of mining, thereby increasing power consumption as the coin in

question matures over time.

To avoid this, all our coins are pre-mined – and placed in “cold storage” off-line. Thereby, the whole mining-process is effectively

stopped, restricting the power consumption to a bare minimum. The flipside of this is that there is no upside for miners to dedicate

nodes to our coin, so we have solved that by creating our own nodes around the world, on all continents and with 99.97% uptime.

An added benefit is, that with all transactions giving a small transaction fee – around 50% of these fees end up in our node wallets,

increasing company profits. The risk of sabotage where a group owning many nodes can manipulate or take over control of the

transaction flow is also mitigated, and as a POS coin intruders would need to control >50% of the coins to control the network

P2P EQT (c) 2014© LXC Coin™ 2014

38

LXC COIN: THE SLOW RISE PARADIGM

P2P EQT (c) 2014

All cryptocoin creators want

their coin to skyrocket in value.

Except us.

The “normal” currency world is dominated by a few main currencies, which have three main features: they are accepted worldwide,

they are extremely liquid, and they are highly stabile over time. Therefore; they are trustworthy, they can be counted on to provide the

holders with security for their funds, and they won’t leave their holders “stuck” in them at any given time. Also, they can be counted

on for future payments

As the world turns to accepting Bitcoins and other cryptocoins as legal tender to pay for goods and services, the most essential

questions are “how much did I actually just get paid?” and “how do I recollect the value I just got in cryptocoins?”. With Bitcoin, you

don’t know if you got 10% more or less for the goods you just sold, and there are fees from selling or converting. Bitcoin is handling

this well, by providing a highly liquid transaction network. But the coin itself has no real asset value, and can tumble in seconds. Also,

if hit by trouble with legislation or technical issues, holders may lose their complete value in seconds. This is ok if you sold a bottle of

soda in Bitcoins, but if cryptocoins want to become a usable payment for high value assets such as cars, houses or boats, or a tanker

load of oil, they need stability. This doesn’t sell well for miners, short-term profiteers and bounty hunters that plague cryptocoins, but

for all serious contenders it is an absolute requirement. Therefore, we don’t view a huge increase in value and high volatility as a sign

of success. We see it differently. We’d like our coin to rise in value more than its anticipated 15% yearly rise in asset value, but not by

much. Say 15-25% per year in total, in a controlled fashion. That creates a cryptocoin the merchants of the world can trust. An up-to-

date cryptocurrency that opens the doors to future usability and tradability – which is exactly what we have been aiming for

P2P EQT (c) 2014© LXC Coin™ 2014

39

LXC COIN: REGULATING LIKE A HYBRID CENTRAL BANK

P2P EQT (c) 2014

We expect to release the full amount of

LXC Coins over a 5+ year period,

selling when it rises “too much” and

repurchasing if it falls back down or

there is surplus cash, in fact operating

as a “LXC Central Bank”

P2P EQT (c) 2014

With huge un-activated reserves of coins, and with the role of market

maker in its own coin, LXCCoin Ltd is taking on the role that a central bank

has to any regular currency - a function no other cryptocoin enjoys today,

and groundbreaking in the world of cryptocurrency. To the anarchistic part

of the cryptocoin world this may be negative, but it is not that part of

cryptocurrency die-hard’s we are aiming for as primary users. While we

cannot alter interest rates as other central banks, we have more powerful

ways to influence the price movement: restriction on sale of new coins,

steering arbitrage profits into the BAV reserves to increase profitability and

earnings, buyback programs, support purchasing, regulation of conversion

from both P2P loan portfolios and from other cryptocoins, and lockup-

/support agreements with key LXC owners, in a way no other central bank

can or have historically been able to (a few dictatorships not included)

When selling/repurchasing, the “LXC Central Bank” will have the

opportunity to split some of the difference/arbitrage with the asset base,

creating higher-than-average profit, which could easily see yearly interests

climbing towards 20% (BAV increasing)

Using the BAV reserves, the hybrid central bank may also cash out

owners of coins with withdrawals from the asset base, paid out at the

exact BAV at the day of withdrawal, thereby preventing the coin from

falling below the BAV.

© LXC Coin™ 2014

40

LXC COIN: ENOUGH COINS?

P2P EQT (c) 2014

There are 1.1 billion LXC Coins, all

owned by the LXCCoin Ltd company.

We think it is a perfect number – here

is why

P2P EQT (c) 2014

The fully issued LXC Coin amounts to 1.1 billion coins, equal to € 1.1

billion. This is a lot, compared with most other coins (there will for example

«only» be 21 million Bitcoins when/if it is ever fully mined) and with the

amount of money it is possible to invest in P2P with sufficient profits.

However, LXCCoin Ltd plans to carefully release coins worth € 500 million

over a few years, reducing its holding of coins by some 30% (selling at

climbing base asset value), thus giving itself ample time to create bonds

with the world leading P2Ps and investing carefully and securely. With

billions of dollars flowing into P2P, billions of dollars flowing into cryptocoins

and an opportunity for a cryptocoin to leverage the possibilities of both

sectors – 1.1 billion coins may also seem to be too few. Still, with that

amount, the LXC would come to represent 5-6% of the turnover of P2P

lending over a few years, which is a tangible market share that we can both

reach and handle

So why 1.1 billion coins? The order was originally for one billion coins

exactly, but as this is the result of calculations and mining, the extra 100

million coins derives from a management-developer discussion, where one

party was correct and the other was wrong. The result is 1.1 billion coins,

and that may turn out to be a perfect number. At least, we’ve come to think

so, and have in the process learned to leave our developers in peace

© LXC Coin™ 2014

41

LXC COIN: CLOSING THE GAP

P2P EQT (c) 2014

To ensure stability and make the coin a lasting currency, it will be important to avoid huge price drops, which the company will try to enforce

With the premium rising, there will

become a significant gap between the

market price and the BAV, which can

damage the stability of the coin and

make it drop. Thus, while selling off to

prevent too much increase, LXCCoin Ltd

may choose to invest profit into the coin

at higher-than-BAV value, or to use

profits for support-purchases. With much

of the core value of the company relying

on the premium of the coin, the company

recognizes that it is still more important

for long-term business that the coin is

stabile than to have an artificially high

vault value

P2P EQT (c) 2014© LXC Coin™ 2014

0

0.5

1

1.5

2

2.5

Q4

-14

Q1-

15

Q2

-15

Q3

-15

Q4

-15

Q1-

16

Q2

-16

Q3

-16

Q4

-16

Q1-

17

Q2

-17

Q3

-17

Q4

-17

BAV [est] Price [exp]

Repurchase [est] STABILITY SUPPORT

42

LXC COIN: LAUNCH STRATEGY

The LXC Coin is targeted for

launch in Q4 of 2014, with a

one-month pre-trade period

The team will spend a lot of

time promoting the company

products and services,

aiming for a one-year roll-

out period encompassing

two rounds of crowdfunding,

an IPO and several key

partnerships

The LXC Coin will need a through build-up

towards future world-wide attention, and

management is not leaving this to

coincidence. The funding and launch will

provide the initial press coverage plus a

high level of proficiency and security, and

following that up will be a broad long-term

PR/IR strategy and financial results

We have already formed bonds with the

media and with several industry

specialists, ensuring initial launch

coverage

LXCCoin Ltd also aim to do a

crowdfunding sale of coins in the UK (or

on one of the main US sites) to market the

coin and show its presence

The mother company is conducting a

small crowd-equity funding round for itself,

to raise awareness of the company and to

secure sufficient number of shareholders

ahead of its floatation

Over the first months, there will be a

steady flow of news, namely the launch of

the company, the new “kind” of currency

(asset backed), the LXC pre-trade release,

the crowdfunding launch and later its

completion, the company crowd-equity

funding, new partners, new exchanges

trading the coin, hopefully some new P2P

partners coming in on the investment side,

the fund, the IPO plan and all news

leading up to the actual date of floatation

We expect the LXC Coin to be followed by

sub-reddit “writers”, 4chan trolls and a

variety of internet subgroups, which we

aim to encourage through direct presence

The team aims to get the LXC Coin traded

at several cryptocurrency exchanges, and

on its own proprietary exchange

P2P EQT (c) 2014© LXC Coin™ 2014

43

LXC COIN: LEGALITY

Our legal team has special

focus on management of risk

and on new financial sectors,

and are both actively

participating in the legality

process revolving cryptocoins

and the LXC Coin

We’ve registered with the FCA

in the UK to ensure an open

and positive dialogue, and to

be included in any future talks

on the legality of cryptocoins

and our other business areas

In most parts of the world, cryptocoins are

legal to create, trade and own. New

legislation is expected to be introduced

over the forthcoming years, but there is

little doubt that cryptocoins are here to

stay. They are currently non-tax objects in

some countries, but this we expect will

change. Crypto currencies are by nature

unrestricted, which we expect will

continue. Our investment base P2P is

legal, but it is under a lot of focus and

forthcoming legislative restrictions are

expected across all sectors of the industry

The Cryptocoin is already issued, being

fully legal in its jurisdiction

The Crypto Exchange is considered an

asset exchange, and is not (yet) covered

by financial authority legislations

Our P2P Exchange is regulated as a peer-

to-peer asset platform, without issuing

loans and only working as a bulletin board,

and should be viable for P2P transactions

throughout Europe (and should not be

affected by the UK consumer credits law)

With a forthcoming listing in mind, the

mother company in the group has been

incorporated in the UK, With flotation in

mind, we need to stay fully compliant at all

times, and all aspects of the company,

reaching from the cryptocoin to the P2P

platform, is fully compliant legally. Our

legal team will follow up closely for

adaptation to any regulatory changes, and

develop our legal compliance routines

continuously. We’ve registered with the

FCA in the UK to ensure an open dialogue

with the authorities

P2P EQT (c) 2014© LXC Coin™ 2014

44

LXC COIN: WELCOMING REGULATION

LXCCoin LTD is already

taking part in discussions

revolving cryptocoins and

future regulation, which we

expect to see happening

worldwide within a very

foreseeable future. We

welcome this regulation, and

hope to see it widening the

gap between second

generation cryptocoins that

can be fully transparent and

legally compliant, and first

generation coins which will

possibly become left behind

Having spent close to two years in launch

preparation, we’ve been in discussion with

financial authorities since 2013. As of

today, the situation is highly volatile, with

no regulation and a high market share of

amateur operations and more or less

vailed scams. The market has to a large

extent been hype-driven, which is

expected to remain a continuing factor

with first generation cryptocoins. Over

time, we expect that this will create a

divide between the early and first

generation crypto currencies, and the

ones that can make the move on to a

regulated and officially recognized

currency family

Our legal team has since our foundation

been occupied with what could lie ahead

of challenges to move towards a fully

compliant stage for cryptocoins, and the

company is well prepared for this change

which we expect to happen within 2015

and 2016.

The similar sector, P2P finance, has had

the same development, where the first

competitors appeared in 2005 and it took

10 years before they got regulated. Still,

they were not as revolutionary as

cryptocoins are today. When regulation

finally came, it was warmly welcomed by

most P2Ps, recognizing that regulation

would help the serious contenders and

halt the less serious ones

This is the same process we currently see

happening in the world of cryptocoins,

which is why our company develops its

legal compliance routines continuously,

and will try to stay ahead of the legislative

development and attempt to be an active

participant in driving it

P2P EQT (c) 2014© LXC Coin™ 2014

45

EXCHANGES

+ The business case for the P2P Exchange

+ Setup and software platform

+ Partners

+ The business case for the Cryptocurrency Exchange

+ The software platform

+ Potential partners

+ Legality & IPR

02© LXC Coin™ 2014

46

“Creating our own cryptocoin exchange was a “must”. Based on our expected

level of arbitrage trading alone, the cost of using other exchanges would fund

the whole development and operations of a fully owned exchange in itself.

Consequently, we went out and bought a complete exchange – securing a

proven platform and making way for a fully secure and publicly known

crypto exchange, providing much needed structure and safety to cryptocoin

traders. Safe, liquid exchanges will be an important part of the future

stability and usability of cryptocoins. Not just our coin – all coins.”

Thomas Wong, CTO/co-founder, LXCCoin

© LXC Coin™ 2014

47

CRYPTO EXCHANGE: THE BUSINESS CASE

The crypto currency market is in a steady

growth, with around 40 exchanges world

wide handling a reported compiled volume

of more than US$ 20m/day in bitcoins

alone, and several marginal exchanges

for specific coins trading minor amounts

outside the main exchanges. The total

market is estimated at between $ 30-40m

per day and rising. Following the highly

public Bitcoin price collapse in 2013, when

cryptocoin giant Mt.Gox went off-line

reportedly taking more than $100 million in

customer funds with them into the

darkness of anonymity, the crypto

exchange market has been ridden with

distrust and risk of fraud. The result was a

new wave of un-anonymous exchanges,

with varying success but with improved

customer security, which makes room for

new exchanges and improvements

© LXC Coin™ 2014

48

CRYPTO EXCHANGE: COINNEXT BASE

Our cryptocoin exchange is

based on CoinNext; a complete

crypto exchange platform,

thoroughly tested with zero

stability- or safety issues.

Our development team has

improved it further, creating a

great offering for cryptocoin

traders, offering the safety of

a publicly known partner and

the strength of a platform with

a proven track record

With a publicly know company behind our

crypto currency, and with a listing target in

2015, owning our own exchange was an

obvious path to take in relation to our

crypto currency position

Sourcing an existing cryptocurrency

exchange and modifying it to suit our own

needs was decided in 2013, ending up

with the purchase of a proven exchange

which has had a “bounty” on its own

safety, making it the target of mass

hacking activity, of which all have failed.

Our safety measures increases the

already secure platform, making it a safe

and publicly recognized exchange, which

should provide the maximum performance

for cryptocoin customers worldwide

The purchase was concluded in 2014, and

our platform was widened with another

exchange and more functionality, with a

target of a Q4 2014 launch alongside our

cryptocoin

Our aim is to become a maximum-

security, high-quality, low-cost exchange

of all liquid and justified crypto currencies..

With cryptocoin trading fees being high,

the volatility in coins being fierce, our

focus will be on our own LXC Coin,

Bitcoin, LiteCoin and the most exchanged

altcoins. As the crypto currency market

matures, it may be decreased to only

include the second generation coins and

Bitcoins

P2P EQT (c) 2014© LXC Coin™ 2014

49

CRYPTO EXCHANGE: FEATURES

We can provide the safety and

trust that few other exchanges

can today – but we can also

optimize the exchange with a

lot of other features;

* One-stop-shopping

* Mining pool partnering

* Liquidity support

* Low fees

* Strong support

* Later “auto-trade” target

We bring three great features to the

cryptocoin exchange services market.

First and foremost, our company is highly

serious and would not be perceived by

customers as a risky counterpart, taking

out the biggest issue of purchasing coins;

fraudulent intermediaries. Secondly, our

payment solutions and direct-purchase

accounts mean that customers can do all

their transactions in one place, and not

having to buy coins one place and

exchange them another. Thirdly, we’ll try

to maximize the liquidity by linking up with

other exchanges, doing all our LXC Coin

trading through it, and keeping a minimum

content available for the coins we’re

dealing in (only the relatively popular

ones, and not taking huge risks)., primarily

in connection with mining operations with

a constant flow of coins

Our Cryptocoin Exchange is a trading

platform, functioning like any normal

currency exchange, with accounts,

payment solutions, a trading-”floor” with

visible buy-, sell- and last price functions,

plus transaction volume overview and

other extended trading features. There is

no auto-trading module, but this will be

attempted programmed or purchased as a

future functionality

Our business model is to charge a small

transaction fee on both sides, starting at

0.25%. Apart from the risk of fraud, which

is very small and implies having full

access to the targeted account anyway,

the risk involved in running an exchange is

near zero

P2P EQT (c) 2014© LXC Coin™ 2014

50

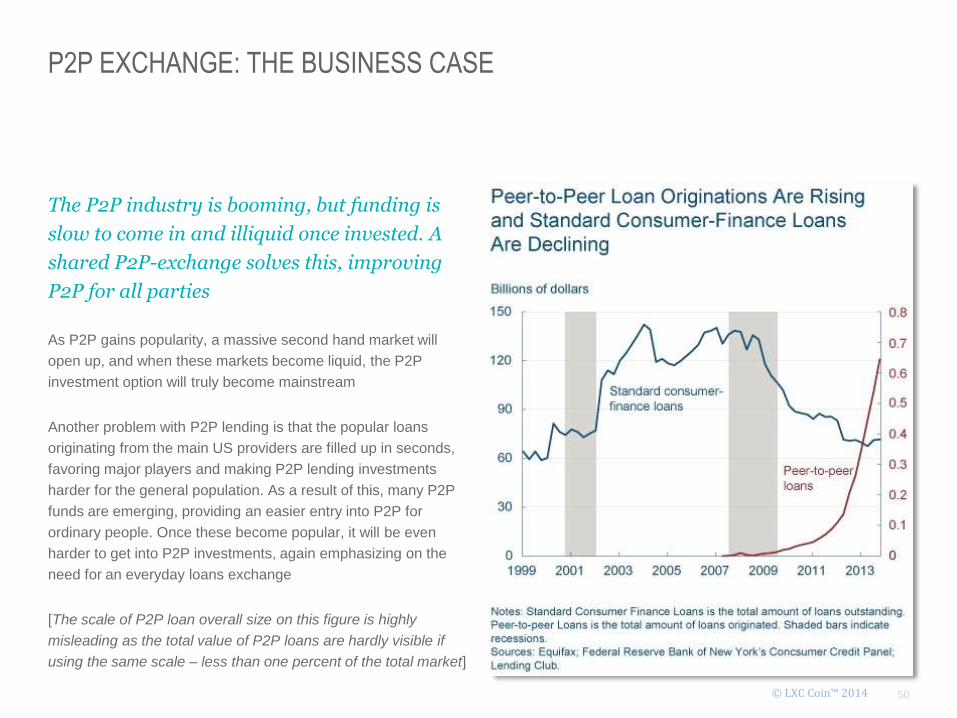

P2P EXCHANGE: THE BUSINESS CASE

The P2P industry is booming, but funding is

slow to come in and illiquid once invested. A

shared P2P-exchange solves this, improving

P2P for all parties

As P2P gains popularity, a massive second hand market will

open up, and when these markets become liquid, the P2P

investment option will truly become mainstream

Another problem with P2P lending is that the popular loans

originating from the main US providers are filled up in seconds,

favoring major players and making P2P lending investments

harder for the general population. As a result of this, many P2P

funds are emerging, providing an easier entry into P2P for

ordinary people. Once these become popular, it will be even

harder to get into P2P investments, again emphasizing on the

need for an everyday loans exchange

[The scale of P2P loan overall size on this figure is highly

misleading as the total value of P2P loans are hardly visible if

using the same scale – less than one percent of the total market]

P2P EQT (c) 2014© LXC Coin™ 2014

51

P2P EXCHANGE: THE SETUP

P2P EQT (c) 2014

To ensure the continuous profitability in the coin, LXCCoin Ltd has created a P2P loan market place, to secure access to P2P loan portfolios once P2P becomes harder to invest in

With LXC Coin revenues directly invested in our dedicated P2P partners, providing top-level profit with low risk, this is in fact a prime

class investment with virtually no loss history. Many international P2P lenders have been maintaining year-long track records of 10-

20% performance and less than 1% losses, but as these are becoming increasingly popular, we need to secure our access to P2P

loans issue. Therefore, we’ve created a P2P loans exchange, like several other P2Ps have or are launching. This way, we secure a

steady flow of P2P loan engagement even when these become harder to acquire. The LXC Coin team will also be partnering with

selected P2P companies with solid track records, loss-reduction guarantees or high average yields justifying any implied risks. Once

P2Ps gain mainstream momentum (which is already present in the US, and is expected to take a few years to reach in Europe), we

have the advantage of utilizing our own P2P Exchange to secure the continued placing power in P2P investments – thereby making it

easier to stay fully invested and maintain profit performance with low risk. In the event of a major sales initiative in the LXC Coin, we

can rapidly liquidate loans on the exchange to meet sales pressure and buy back coins at a profit. We’ve secured two domains for

this: p2pme.com (“P2P Market Exchange”) and P2PLoan.exchange, and have prepared our trading platform for multiple P2P API’s

P2P EQT (c) 2014© LXC Coin™ 2014

52

P2P EXCHANGE: PARTNERS

P2P EQT (c) 2014© LXC Coin™ 2014

We expect both current and new P2Ps to be interested in a liquid second-hand market for their

loans, and LXCCoin Ltd aims to partner up with several P2P lenders to both invest in their

portfolios and to get their loans interfaced with our trading platform – ensuring happy

customers better exit opportunities and increasing growth for both parties

Obviously our key interest in the P2P Exchange is the P2P lenders where there is no

current second-hand loans market, and where customers have been known to be

«stuck» in otherwise brilliantly performing products for years. With a continued LXC Coin

sale, our investments in P2P loans could be done through these companies in new loans

issues, but it may also be done by purchasing existing loan portfolios

External customers interested in loan portfolios may obviously also purchase loans on

our exchange, and by the LXC asset base being able to offer both buy- and sell-side, the

exchange ought to provide a continuous flow of trading, making it an ideal place to come

for new P2Ps in search of lending capital

As the LXC Coin improves its profitability, the company may enter into even more